Embed Size (px)

Citation preview

BURNS SIMPSONSESSION THREE WORKBOOK

Decisions and Notes for Modules 1 – 6

BSMARTer Business Simulation Management and Relationship Training

Executive Summary

2

Burns Simpson is a $700M wealth management RIA in Oregon with seven partners [Edna, Ken, Ned, Selma, Apu, Ben & Cat]. Below is a brief background of our firm:

1. The firm’s founders, Chuck Burns & Harold Simpson affiliated with a network firm, Destiny Financial Partners in 2012, in order to generate capital to fund their retirement.

Chuck & Harold brought on six partners as part of their succession strategy [Edna, Ken, Selma, Ned, Apu & Ben}. Destiny Financial was the capital source/investor and business partner.

Chuck & Harold were responsible for all of the business development up to their retirement in 2012.

In 2014, the new partners bought out Destiny Financial Partners from their interest in Burns Simpson with the help of Cat Stevens, CFO.

Cat purchased 16% ownership for $3.4M.2. The firm underwent a brand change from Burns Simpson & Associates to Burns Simpson in

2014 to better align with the multi-generational partnership culture while still maintaining the legacy firm credibility.

3. The firm has recently launched initiatives on partner compensation, employee, client and COI engagement.

4. The marketing and business development effort the firm has undertaken has been successful resulting in 17% growth in 2014.

Fundamentals of Equity

MODULE ONE

Changes in Equity

2

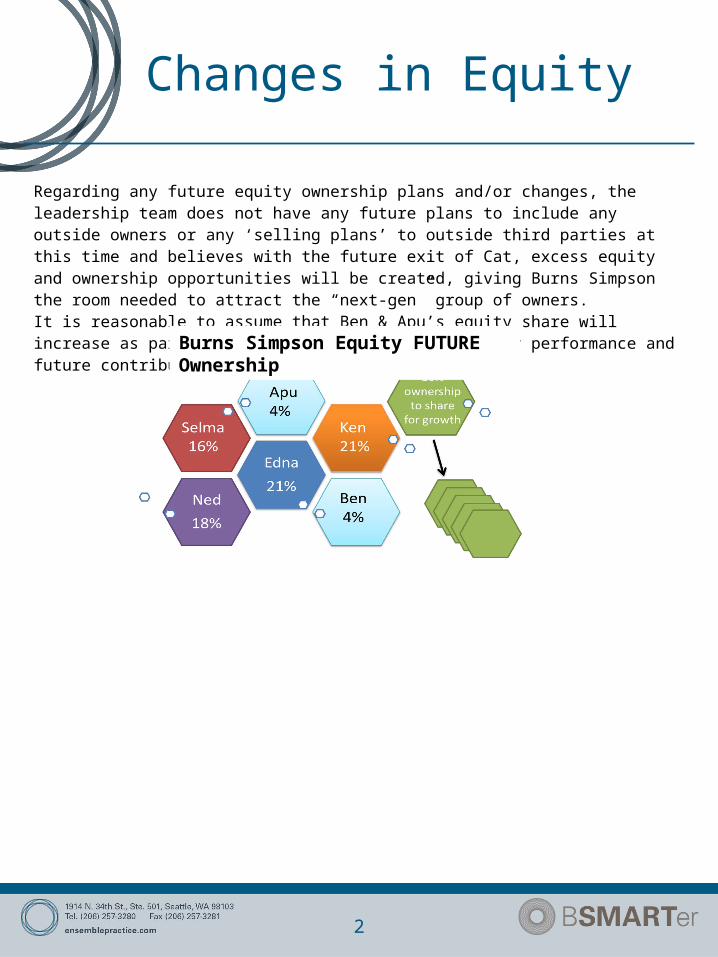

Changes in EquityWe at Burns Simpson have experienced a large amount of change since the original buy-out and hand-off from Chuck and Harold. We believe the firm needs to continue evolving, not only with our current leadership team but also with the addition of new owners and a focus on tomorrow’s next ‘gen’ of clients.

We have come to the early conclusion and agreement that Cat (current ownership at 16%) will be the first to exit in the next 5-10 years as an owner where her ownership would be transferred to future owners. (Forecast of potential buyers on next page.)The other four large shareholders expect to work for the foreseeable future and are not planning to transition shares at this time; however, the next batch of shares for sale, after Cat is fully liquidated, will come from the four largest shareholders. Any and all changes to equity and ownership structures has to be ‘board approved’ with the board consisting of Edna, Ken, Ned, Selma and Cat. Any and all changes to equity ownership will follow the below process including:1. Board approval of all new owners2. Distribution of equity:3. Existing owners have the right of first refusal when an existing owner sells4. Board defaults to #15. We are under no obligation to provide liquidity to a departing or retiring owner6. Partners who become deceased or disabled will be bought out by the firm at a value

determined by an appraisal of the company (provided by independent firm, approved by board vote)

Changes in Equity

2

Regarding any future equity ownership plans and/or changes, the leadership team does not have any future plans to include any outside owners or any ‘selling plans’ to outside third parties at this time and believes with the future exit of Cat, excess equity and ownership opportunities will be created, giving Burns Simpson the room needed to attract the “next-gen” group of owners. It is reasonable to assume that Ben & Apu’s equity share will increase as part of this transaction based on their performance and future contributions to the firm.

Burns Simpson Equity FUTURE Ownership

Valuation Principles and Experience

MODULE TWO

Firm Value

4

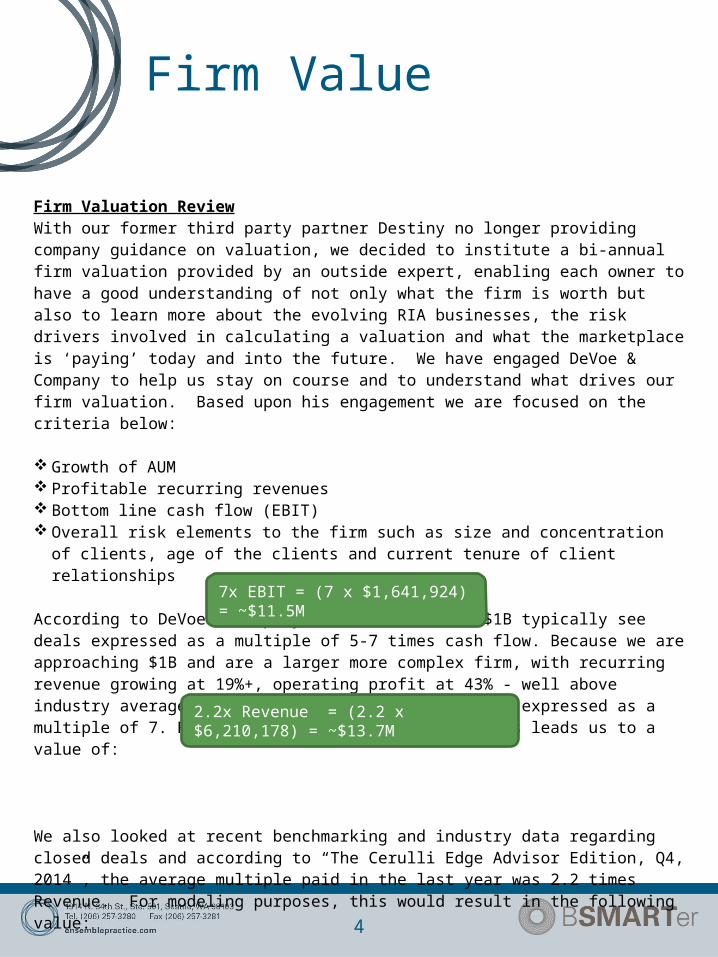

Firm Valuation ReviewWith our former third party partner Destiny no longer providing company guidance on valuation, we decided to institute a bi-annual firm valuation provided by an outside expert, enabling each owner to have a good understanding of not only what the firm is worth but also to learn more about the evolving RIA businesses, the risk drivers involved in calculating a valuation and what the marketplace is ‘paying’ today and into the future. We have engaged DeVoe & Company to help us stay on course and to understand what drives our firm valuation. Based upon his engagement we are focused on the criteria below: Growth of AUM Profitable recurring revenues Bottom line cash flow (EBIT) Overall risk elements to the firm such as size and concentration of clients, age of the clients and

current tenure of client relationships According to DeVoe & Company, firms of $500M - $1B typically see deals expressed as a multiple of 5-7 times cash flow. Because we are approaching $1B and are a larger more complex firm, with recurring revenue growing at 19%+, operating profit at 43% - well above industry averages, we feel our valuation should be expressed as a multiple of 7. For internal modeling purposes, this leads us to a value of: We also looked at recent benchmarking and industry data regarding closed deals and according to “The Cerulli Edge Advisor Edition, Q4, 2014”, the average multiple paid in the last year was 2.2 times Revenue. For modeling purposes, this would result in the following value:

Accordingly, we think the range of valuation for our firm is between $11.5M and $13.7M

7x EBIT = (7 x $1,641,924) = ~$11.5M

2.2x Revenue = (2.2 x $6,210,178) = ~$13.7M

Firm Value

4

As part of the bi-annual valuation exercise we will review the following key drivers as part of our strategic plan to ensure we are maximizing them to increase firm valuation: 1. Review how much revenue is transactional vs. recurring 2. Focus driving growth through a team based approach vs. individuals3. Replace our aging client base with younger clients 4. Review our business and operational processes to ensure they are performing efficiently 5. Ensure we have a disciplined and defined process with compensation plans6. Review current client concentration risk7. Discuss any firm cultural differences to ensure everyone is focused on the same firm goals8. Review current asset retention rates to ensure a sticky client-base9. Benchmark the financials of the firm against other firms of similar size to see how we compare

New Partnership Admission

MODULE THREE

Criteria for New Partners

6

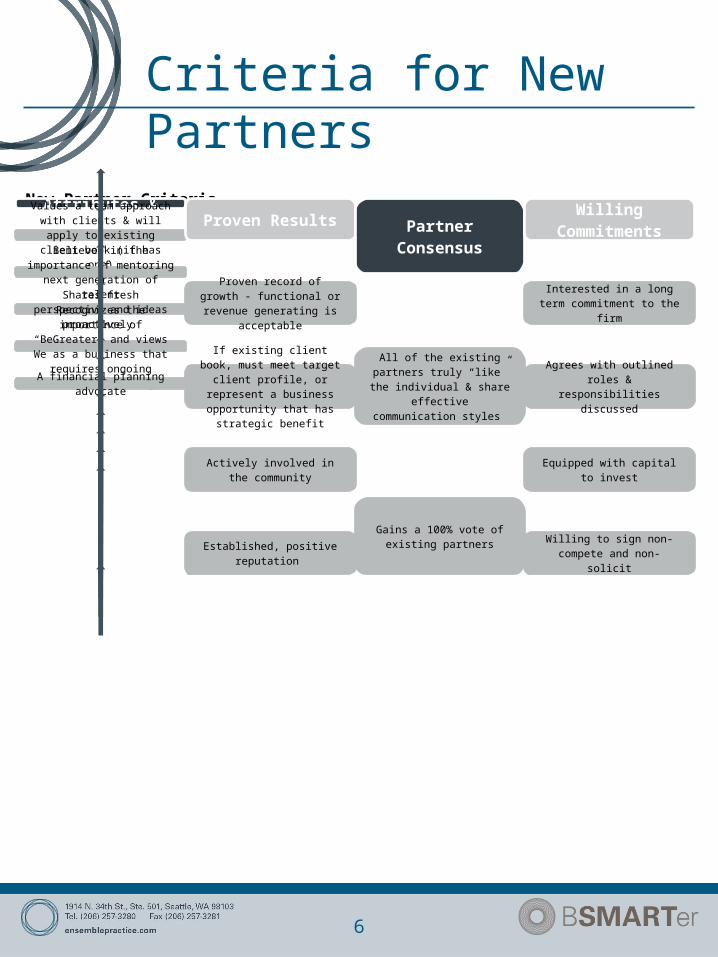

Partner CriteriaOur firm values the opportunity to offer partnership to an internal or external candidate who meets the criteria that the existing partners have carefully discussed and agreed upon. In line with our mission and vision, we believe that it is critical to provide an atmosphere of opportunity at our firm.

The following includes the process for considering new partners, the assessment questions that will be leveraged regarding any candidates, as well as the specific new partner criteria that will be considered.

The process to consider a potential partner: Nomination during our annual evaluation period for internal candidates Open consideration during the hiring process for executive level talent Nomination is required by an existing partner Analysis and collaboration done by the managing partners by leveraging the

questions within the IWS Talent Assessment guide, as well as carefully considering the outlined new partner criteria

Partnership approval requires a positive vote from all of the managing partners

IWS assessment questions: Ability to grow the business: Is the individual able to generate ongoing revenue for

the firm? Management acumen: Can this individual prioritize work and make good

management decisions? Leadership and people skills: How well does the individual lead team members? Self-knowledge: Does the individual know his or her strengths and weaknesses

and is he or she able to fill any gaps? Trust: Does this individual have the integrity to work with you in an effective

transition? Willingness to take responsibility: Is the individual willing to accept the risks and

accountabilities of ownership?

Criteria for New Partners

6

New Partner CriteriaPersonal Attributes & Experience

Values a team approach with clients & will apply to existing

client book (if has one)Believes in the importance of mentoring next generation of

talent

Shares fresh perspective and ideas proactively

Recognizes the importance of “BeGreater” and views We as a business that requires ongoing

strategic planning

A financial planning advocate

Proven Results

Proven record of growth - functional or revenue generating

is acceptable

If existing client book, must meet target client profile, or represent a business opportunity that has

strategic benefit

Actively involved in the community

Established, positive reputation

Partner Consensus

All of the existing partners truly “like” the individual & share

effective communication styles

Gains a 100% vote of existing partners

Willing Commitments

Interested in a long term commitment to the firm

Agrees with outlined roles & responsibilities discussed

Equipped with capital to invest

Willing to sign non-compete and non-solicit

Partnership Agreements

MODULE FOUR

Partnership Agreements

8

Partnership Agreement ChangesGiven the significant ownership changes in the last five years (founders leaving and restructure after outside equity partner payoff), we feel that it is time to revisit our Partnership Agreement. The original agreement was written when there were two partners. An updated agreement is needed to provide the framework for future ownership changes, AUM growth, and role clarity. A – Entity and BusinessBurns Simpson is an LLC.

We decided to make a slight, though meaningful, change to our name, from Burns Simpson & Associates to Burns Simpson. We feel the name better aligns with our mission to build a business with a multigenerational approach towards our talent and our clients that will be here for long into the future.

B – Board of DirectorsGiven the lack of role clarity previously in the firm, we decided to commit to an active CEO that will manage the business. The Board will manage the CEO and strategic decisions.1. The Board of Directors will oversee the management. The CEO will have ultimate decision

making authority with regard to managing the firm’s day to day operations and will report to the Board. The Board can remove the CEO. The CEO will have a seat on the Board.

2. The Board will consist of the managing partners. Board changes will be made by a super-majority, greater than 60% vote of the current board. Currently the managing partners are Edna, Ken, Ned, Cat, and Selma. The Chairman of the Board will be elected by the managing partners.

3. The Board will make decisions on most matters by simple majority, except for removing managing partners, which requires a super majority. In the case of a tied vote, the matter will be submitted for vote to all partners.

4. Each member of the Board will have one vote.5. The Board will meet quarterly or as needed to make decisions. 6. Every three years, a board members term comes up for renewal. The member can resign the

seat or is eligible to be re-nominated.

Partnership Agreements

8

TERMINATION OF PARTNERSHIP - It is hereby agreed by all parties that at the termination of the partnership or a partner, the said partners shall within a period of thirty (30) days, give a true and final account of all things relating to their business including money, goods, wares, fixtures, and all other properties, which after payment of the partnerships liabilities, shall be divided between them in the same percentages as were profits and losses and within a period of ninety (90) days, truly adjust all matters with the departing partner. At no point can the partner or partners sell their contribution to outside entities. Buy outs will only be made to the departing partner and/or partners; and should said partners be unable to ascertain the value of any of the assets belonging to the partnership, said assets shall then be sold either at private or public sale to be agreed upon by the parties hereto and a division of the proceeds of said sale shall be divided as herein provided. C - Ownership Interest1. The current ownership interest is:

2. The owners agree not to compete with the firm for a period of 2 years after leaving the firm and will not solicit clients away from the firm for a period of 2 years following their departure.

3. Owners are required to sign a non-compete, non-solicitation, and confidentiality agreements.

OWNER % SHAREEdna 21%

Ken 21%

Ned 18%

Selma 16%

Apu 4%

Ben 4%

Cat 16%

Partnership Agreements

8

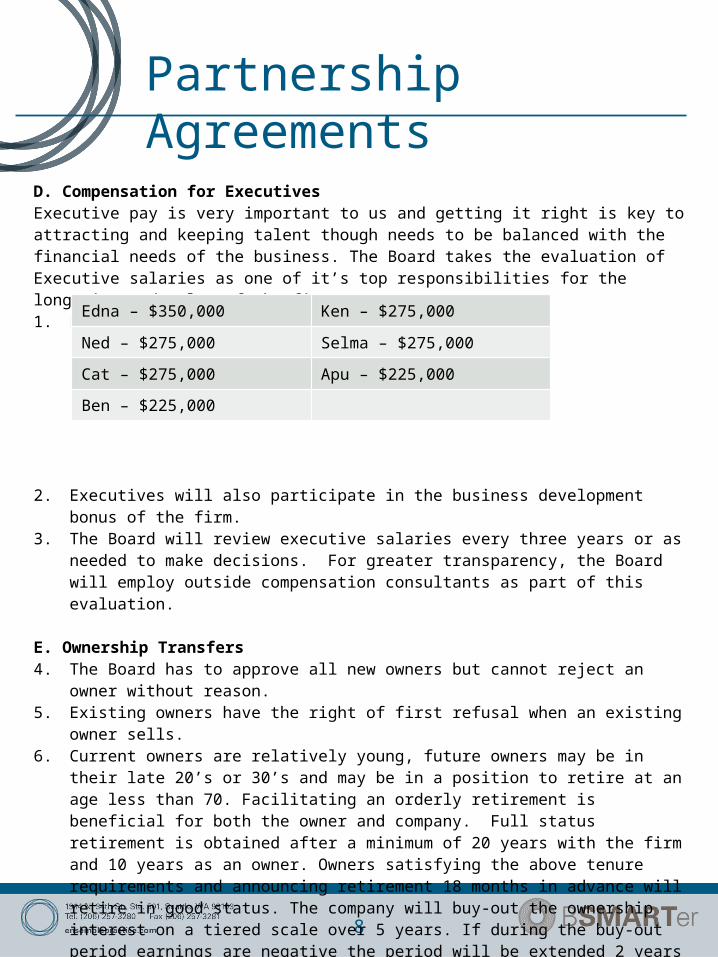

D. Compensation for ExecutivesExecutive pay is very important to us and getting it right is key to attracting and keeping talent though needs to be balanced with the financial needs of the business. The Board takes the evaluation of Executive salaries as one of it’s top responsibilities for the longevity and value of the firm. 1. Executives will receive compensation as follows:

2. Executives will also participate in the business development bonus of the firm.3. The Board will review executive salaries every three years or as needed to make decisions. For

greater transparency, the Board will employ outside compensation consultants as part of this evaluation.

E. Ownership Transfers4. The Board has to approve all new owners but cannot reject an owner without reason.5. Existing owners have the right of first refusal when an existing owner sells.6. Current owners are relatively young, future owners may be in their late 20’s or 30’s and may

be in a position to retire at an age less than 70. Facilitating an orderly retirement is beneficial for both the owner and company. Full status retirement is obtained after a minimum of 20 years with the firm and 10 years as an owner. Owners satisfying the above tenure requirements and announcing retirement 18 months in advance will retire in good status. The company will buy-out the ownership interest on a tiered scale over 5 years. If during the buy-out period earnings are negative the period will be extended 2 years for each negative year to a maximum of 10 years. If not in Good status when leaving the firm then firm has the option to purchase at a 50% discount.

7. Owners who become deceased or disabled will be bought out by the firm at a 20% discount to facilitate timely payments.

8. Add ‘key-man’ insurance for all Executives and owners with greater than a 5% ownership interest for all death and disability scenarios.

9. Mandatory ownership divesting at age 70, using a five year divesting schedule.

Edna – $350,000 Ken – $275,000

Ned – $275,000 Selma – $275,000

Cat – $275,000 Apu – $225,000

Ben – $225,000

Partnership Agreements

8

F. Management of the Firm1. The CEO has ultimate decision making authority in managing the firm. The CEO reports to the

Board of Directors. The CEO will retain a seat on the Board of Directors. 2. Day to day management is provided by the Management Committee, consisting of the

functional leaders.3. The Management Committee can sign on behalf of the firm. G. Distributions and Capital 4. The firm will distribute at least as much of its profits as necessary to meet the resulting tax

liability to the owner.5. Each owner is responsible for filing their own tax return and making estimated payments.6. The firm cannot force owners to contribute more cash or other assets to the firm.

Founder Succession

MODULE FIVE

Succession Plan

10

Succession PlanBased on the overall ‘negative’ experience of the ineffective transition of the two founders to the existing partners at Burns Simpson, the firm now wants to set up a formal process to ensure a smooth succession plan for the future of the firm.

The board and overall leadership of the firm is over 10 years younger than Cat and is focused on the longer term picture of running the firm without Cat on board. For this reason, our initial goal of the firm will be the succession of Cat, her leadership position and 16% ownership of the firm.

Her job function as CFO will be gradually moved to Selma, current COO at the firm Selma will also move into a larger, leadership role taking the place of Cat

Cat will mentor Selma and transfer responsibilities over the transition period Selma’s background, experience, education and aptitude are aligned with the

skills needed for these responsibilities Cat’s ownership would begin to be sold and distributed to partners and owners

identified over the next ten year period: We are pursing advice from our attorney on whether puts/calls for Cat’s

ownership stake is needed 10% of her shares sold internally to Ben & Apu – seller financed Cat retains 6%, maintains her board seat until board agrees / votes on remaining

6% to be sold / divested – she will maintain at least 5% ownership until her last day

No outside shareholders will own these shares (i.e. in a divorce situation)

Succession Plan

10

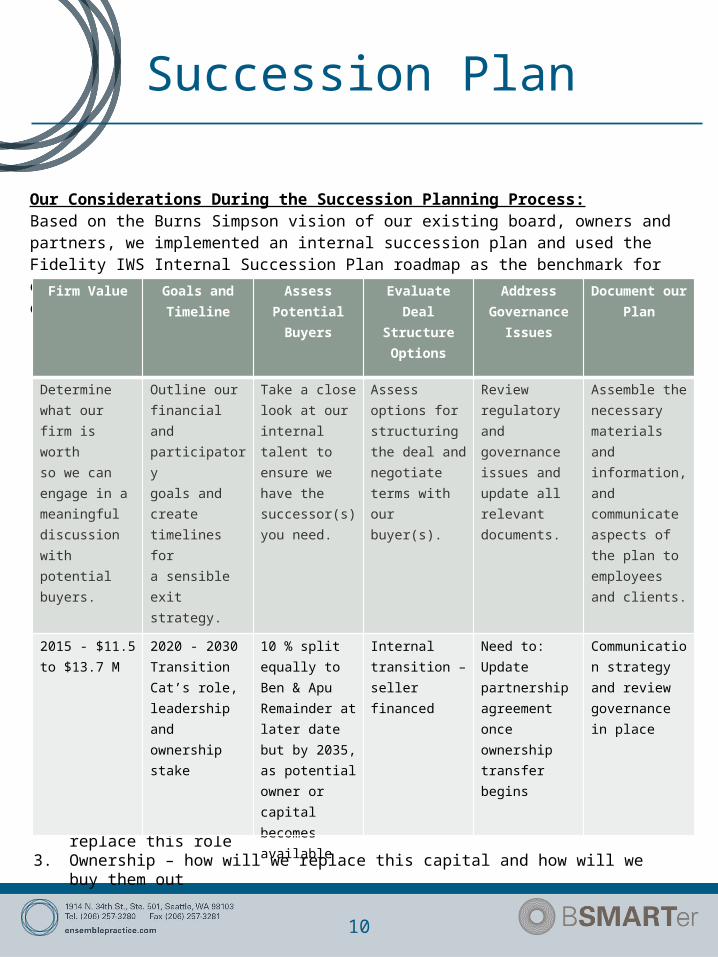

Our Considerations During the Succession Planning Process:Based on the Burns Simpson vision of our existing board, owners and partners, we implemented an internal succession plan and used the Fidelity IWS Internal Succession Plan roadmap as the benchmark for our plan and how we institutionalize the process for all future owners of the firm.

Thought process and basis for succession plan:1. What is the functional job of the individual(s) before they move on and how we will replace2. Does the individual(s) play a leadership role; how will we replace this role3. Ownership – how will we replace this capital and how will we buy them out

Firm Value

Goals and Timeline

AssessPotential

Buyers

EvaluateDeal

StructureOptions

AddressGovernance

Issues

Document our Plan

Determinewhat ourfirm is worthso we canengage in ameaningfuldiscussionwithpotentialbuyers.

Outline ourfinancial andparticipatorygoals andcreate timelines fora sensible exitstrategy.

Take a closelook at ourinternaltalent toensure wehave thesuccessor(s)you need.

Assessoptions forstructuringthe deal andnegotiateterms withour buyer(s).

Reviewregulatoryandgovernanceissues andupdate allrelevantdocuments.

Assemble thenecessarymaterials andinformation,andcommunicateaspects ofthe plan toemployeesand clients.

2015 - $11.5 to $13.7 M

2020 - 2030Transition Cat’s role, leadership and ownership stake

10 % split equally to Ben & ApuRemainder at later date but by 2035, as potential owner or capital becomes available

Internal transition – seller financed

Need to:Update partnership agreement once ownership transfer begins

Communication strategy and review governance in place

Other Initiatives

MODULE SIX

Other Initiatives

12

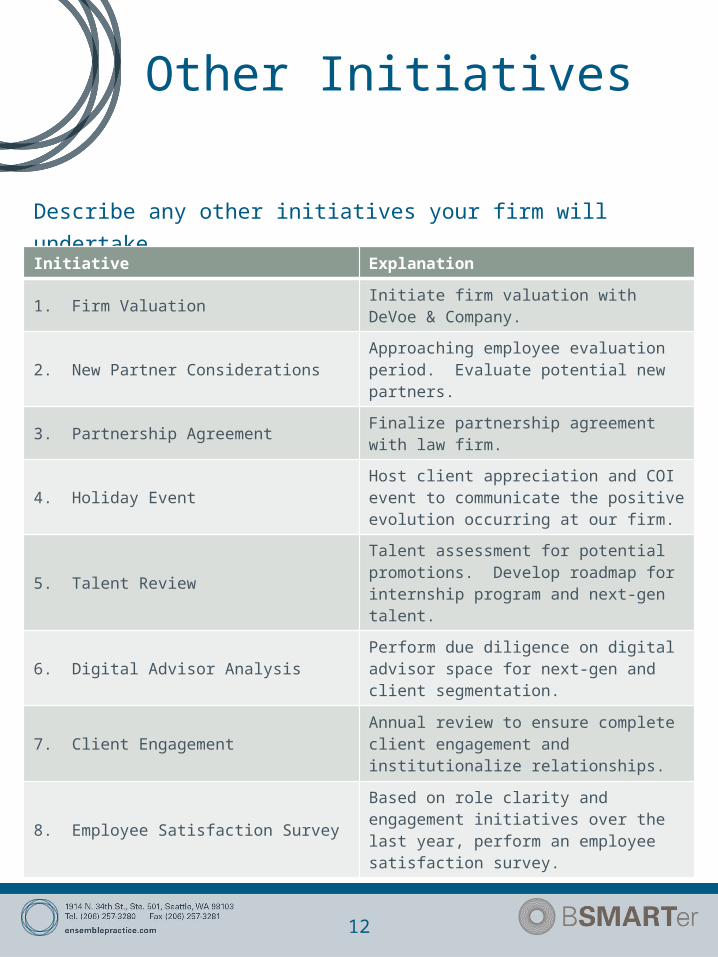

Describe any other initiatives your firm will undertake.

Notes

Initiative Explanation

1. Firm Valuation Initiate firm valuation with DeVoe & Company.

2. New Partner Considerations Approaching employee evaluation period. Evaluate potential new partners.

3. Partnership Agreement Finalize partnership agreement with law firm.

4. Holiday EventHost client appreciation and COI event to communicate the positive evolution occurring at our firm.

5. Talent ReviewTalent assessment for potential promotions. Develop roadmap for internship program and next-gen talent.

6. Digital Advisor Analysis Perform due diligence on digital advisor space for next-gen and client segmentation.

7. Client Engagement Annual review to ensure complete client engagement and institutionalize relationships.

8. Employee Satisfaction SurveyBased on role clarity and engagement initiatives over the last year, perform an employee satisfaction survey.