Embed Size (px)

Citation preview

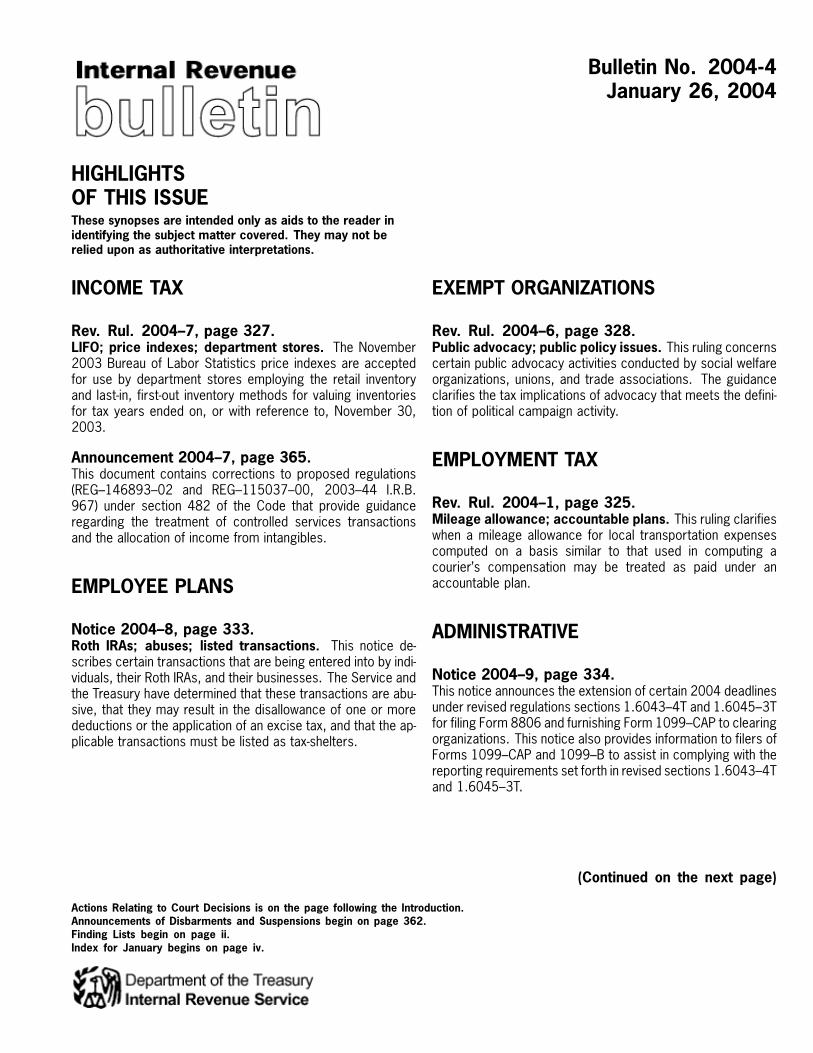

Bulletin No. 2004-4January 26, 2004

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Rev. Rul. 2004–7, page 327.LIFO; price indexes; department stores. The November2003 Bureau of Labor Statistics price indexes are acceptedfor use by department stores employing the retail inventoryand last-in, first-out inventory methods for valuing inventoriesfor tax years ended on, or with reference to, November 30,2003.

Announcement 2004–7, page 365.This document contains corrections to proposed regulations(REG–146893–02 and REG–115037–00, 2003–44 I.R.B.967) under section 482 of the Code that provide guidanceregarding the treatment of controlled services transactionsand the allocation of income from intangibles.

EMPLOYEE PLANS

Notice 2004–8, page 333.Roth IRAs; abuses; listed transactions. This notice de-scribes certain transactions that are being entered into by indi-viduals, their Roth IRAs, and their businesses. The Service andthe Treasury have determined that these transactions are abu-sive, that they may result in the disallowance of one or moredeductions or the application of an excise tax, and that the ap-plicable transactions must be listed as tax-shelters.

EXEMPT ORGANIZATIONS

Rev. Rul. 2004–6, page 328.Public advocacy; public policy issues. This ruling concernscertain public advocacy activities conducted by social welfareorganizations, unions, and trade associations. The guidanceclarifies the tax implications of advocacy that meets the defini-tion of political campaign activity.

EMPLOYMENT TAX

Rev. Rul. 2004–1, page 325.Mileage allowance; accountable plans. This ruling clarifieswhen a mileage allowance for local transportation expensescomputed on a basis similar to that used in computing acourier’s compensation may be treated as paid under anaccountable plan.

ADMINISTRATIVE

Notice 2004–9, page 334.This notice announces the extension of certain 2004 deadlinesunder revised regulations sections 1.6043–4T and 1.6045–3Tfor filing Form 8806 and furnishing Form 1099–CAP to clearingorganizations. This notice also provides information to filers ofForms 1099–CAP and 1099–B to assist in complying with thereporting requirements set forth in revised sections 1.6043–4Tand 1.6045–3T.

(Continued on the next page)

Actions Relating to Court Decisions is on the page following the Introduction.Announcements of Disbarments and Suspensions begin on page 362.Finding Lists begin on page ii.Index for January begins on page iv.

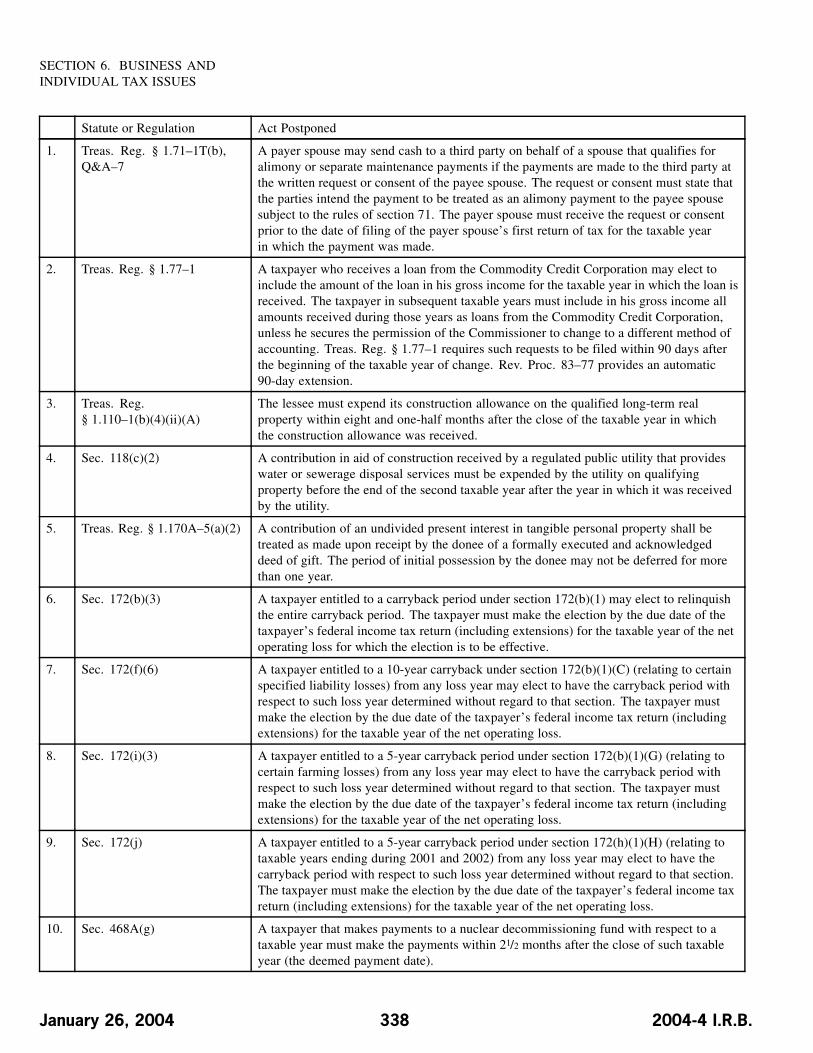

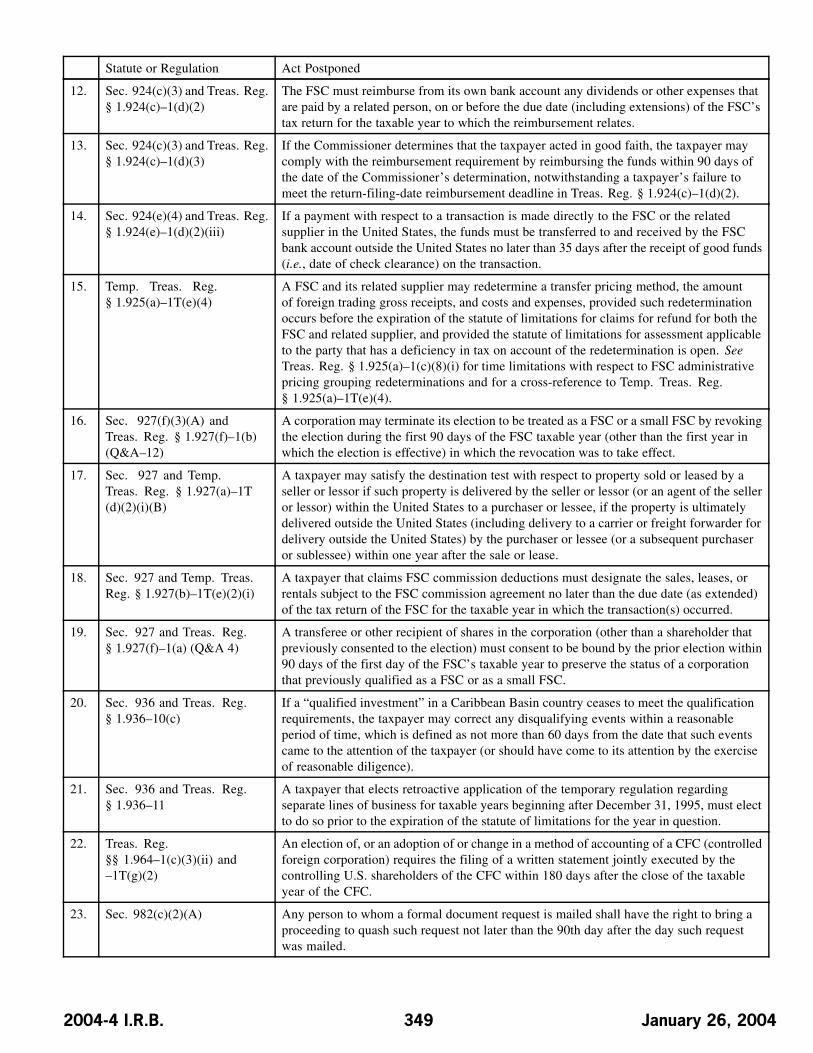

Rev. Proc. 2004–13, page 335.This procedure provides an updated list of time-sensitive acts,the performance of which may be postponed under sections7508 and 7508A of the Code. Section 7508 postpones spec-ified acts for individuals serving in the Armed Forces of theUnited States or serving in support of such Armed Forces ina combat zone. Section 7508A permits a postponement ofspecified acts for taxpayers affected by a Presidentially de-clared disaster or a terroristic or military action. The list ofacts in this procedure supplements the list of postponed actsin section 7508(a)(1) and regulations section 301.7508A–1(b).Rev. Proc. 2002–71 superseded.

Announcement 2004–4, page 357.The Service and the Treasury Department announce that theyare requesting comments from the public on proposed newForm 8858, Information Return of U.S. Persons With Respectto Foreign Disregarded Entities. The form will be required to befiled by U.S. persons that own a foreign disregarded entity di-rectly or, in certain circumstances, indirectly or constructively.The reporting of information on Form 8858 will be required un-der sections 6011, 6012, 6031, and 6038 of the Code andthe related regulations, for annual accounting periods of taxowners of foreign disregarded entities beginning on or afterJanuary 1, 2004.

Announcement 2004–5, page 362.The Service announces the availability of new Form 8806, Infor-mation Return for Acquisition of Control or Substantial Changein Capital Structure. This form is used by a reporting corpora-tion to report an acquisition of control or a substantial changein the capital structure of a domestic corporation.

January 26, 2004 2004-4 I.R.B.

The IRS MissionProvide America’s taxpayers top quality service by helpingthem understand and meet their tax responsibilities and by

applying the tax law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bul-letin contents are consolidated semiannually into CumulativeBulletins, which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscella-neous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Sec-retary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.*

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

* Beginning with Internal Revenue Bulletin 2003–43, we are publishing the index at the end of the month, rather than at the beginning.

2004-4 I.R.B. January 26, 2004

Actions Relating to Decisions of the Tax CourtIt is the policy of the Internal Rev-

enue Service to announce at an early datewhether it will follow the holdings in cer-tain cases. An Action on Decision is thedocument making such an announcement.An Action on Decision will be issued atthe discretion of the Service only on unap-pealed issues decided adverse to the gov-ernment. Generally, an Action on Decisionis issued where its guidance would be help-ful to Service personnel working with thesame or similar issues. Unlike a TreasuryRegulation or a Revenue Ruling, an Actionon Decision is not an affirmative statementof Service position. It is not intended toserve as public guidance and may not becited as precedent.

Actions on Decisions shall be reliedupon within the Service only as conclu-sions applying the law to the facts in theparticular case at the time the Action onDecision was issued. Caution should beexercised in extending the recommenda-tion of the Action on Decision to similarcases where the facts are different. More-over, the recommendation in the Action onDecision may be superseded by new legis-lation, regulations, rulings, cases, or Ac-tions on Decisions.

Prior to 1991, the Service publishedacquiescence or nonacquiescence only in

certain regular Tax Court opinions. TheService has expanded its acquiescenceprogram to include other civil tax caseswhere guidance is determined to be help-ful. Accordingly, the Service now mayacquiesce or nonacquiesce in the holdingsof memorandum Tax Court opinions, aswell as those of the United States DistrictCourts, Claims Court, and Circuit Courtsof Appeal. Regardless of the court decid-ing the case, the recommendation of anyAction on Decision will be published inthe Internal Revenue Bulletin.

The recommendation in every Actionon Decision will be summarized as ac-quiescence, acquiescence in result only,or nonacquiescence. Both “acquiescence”and “acquiescence in result only” meanthat the Service accepts the holding ofthe court in a case and that the Servicewill follow it in disposing of cases withthe same controlling facts. However, “ac-quiescence” indicates neither approvalnor disapproval of the reasons assignedby the court for its conclusions; whereas,“acquiescence in result only” indicatesdisagreement or concern with some or allof those reasons. “Nonacquiescence” sig-nifies that, although no further review wassought, the Service does not agree withthe holding of the court and, generally,

will not follow the decision in disposingof cases involving other taxpayers. Inreference to an opinion of a circuit courtof appeals, a “nonacquiescence” indicatesthat the Service will not follow the hold-ing on a nationwide basis. However, theService will recognize the precedentialimpact of the opinion on cases arisingwithin the venue of the deciding circuit.

The Actions on Decisions published inthe weekly Internal Revenue Bulletin areconsolidated semiannually and appear inthe first Bulletin for July and the Cumula-tive Bulletin for the first half of the year. Asemiannual consolidation also appears inthe first Bulletin for the following Januaryand in the Cumulative Bulletin for the lasthalf of the year.

The Commissioner withdraws ACQUI-ESCENCE in the following decision:

Sidney L. Olson and Miriam K.Olson v. Commissioner,1

48 T.C. 855 supplemented,49 T.C. 84 (1967), acq., 1968–2 C.B. 2Docket Numbers: 1713–65, 1714–65,

1715–65, 1716–65, 3328–65

1 Withdrawal of the Service’s acquiescence relating to whether the distribution of the stock of a controlled corporation by a distributing corporation to the shareholders of the distributingcorporation to prevent the potential union of the distributing corporation from claiming that the distributing and controlled corporations constitute a single employer for labor law purposesqualifies as a valid corporate business purpose under section 1.355–2(b) of the Income Tax Regulations.

January 26, 2004 2004-4 I.R.B.

Part I. Rulings and Decisions Under the Internal Revenue Codeof 1986Section 62.—AdjustedGross Income Defined

Mileage allowance; accountableplans. This ruling clarifies when amileage allowance for local transporta-tion expenses computed on a basis similarto that used in computing a courier’s com-pensation may be treated as paid under anaccountable plan.

Rev. Rul. 2004–1

ISSUE

Whether a mileage allowance for lo-cal transportation expenses computed on abasis similar to that used in computing acourier’s compensation may be treated aspaid under an accountable plan so that itwill be excluded from the courier’s grossincome and exempt from the withholdingand payment of employment taxes.

FACTS

1. Situation OneEmployer, a courier company, hires em-

ployee drivers to deliver packages locally.Drivers must own or lease an automobile(including vans, pickups, or panel trucks)for use in connection with the performanceof services as couriers. When deliveringpackages, drivers incur the ordinary andnecessary expenses of operating an auto-mobile.

Employer charges customers for de-liveries based on location, time of day,expedited service (if requested), mileagebetween pickup and delivery, size andweight of a package, and other factors.This per package charge is referred to asthe “tag rate.” The mileage componentof the tag rate is computed as thougheach package were delivered separately.However, drivers often pick up multiplepackages from one location, deliver mul-tiple packages to another location, andtravel overlapping routes between andamong customers. Consequently, the tagrate may not accurately reflect the trans-portation expenses incurred with respectto a particular package.

Employer pays drivers a commissionequal to X percent of the tag rate as com-

pensation for services. Additionally, em-ployer pays drivers a mileage allowanceequal to Y percent of the tag rate to coverthe expenses of operating their automo-biles. Because the mileage allowance iscomputed based on a percentage of thetag rate, the mileage rate (cents per mile)paid with respect to any particular packagevaries depending on the number of milestraveled.

Employer determines the percentage ofthe tag rate paid as a mileage allowanceannually and the percentage remains fixedthroughout the calendar year. The percent-age paid as a mileage allowance is basedon employer’s review of a sample of doc-uments submitted by drivers (including re-ceipts, logbooks, and invoices) reflectingthe drivers’ operating and fixed costs. Em-ployer pays the mileage allowance onlywith respect to miles traveled while deliv-ering packages.

Employer requires that, on a monthlybasis, each driver provide information suf-ficient to substantiate the number of busi-ness miles traveled. Employer multipliesthe number of miles traveled times thebusiness standard mileage rate (as pub-lished by the Commissioner) to calculatethe amount of travel expenses deemed sub-stantiated. Employer subtracts the amountdeemed substantiated from the mileage al-lowance paid and reports the excess aswages on the driver’s Form W–2.

2. Situation TwoThe facts are the same as in Situation

One except employer pays drivers a com-mission equal to Z percent of the tag ratereduced by a mileage allowance equal tothe number of miles traveled multiplied bythe business standard mileage rate. Thus,drivers always receive Z percent of the tagrate, but the amount treated as a mileageallowance varies based on the number ofbusiness miles traveled and subsequentlysubstantiated by drivers.

LAW

Section 61 of the Internal RevenueCode provides that gross income meansall income from whatever source derived,including compensation for services, fees,

commissions, fringe benefits, and similaritems.

Section 62(a)(2)(A) provides that, forpurposes of determining adjusted gross in-come, an employee may deduct certainbusiness expenses paid by the employeein connection with the performance of ser-vices as an employee of the employer un-der a reimbursement or other expense al-lowance arrangement.

Section 62(c) provides that, for pur-poses of section 62(a)(2)(A), an arrange-ment will in no event be treated as a re-imbursement or other expense allowancearrangement if (1) the arrangement doesnot require the employee to substantiatethe expenses covered by the arrangementto the person providing the reimbursement,and (2) the arrangement provides the em-ployee the right to retain any amount in ex-cess of the substantiated expenses coveredunder the arrangement.

Section 1.62–2(c)(1) of the Income TaxRegulations provides that a reimbursementor other expense allowance arrangementsatisfies the requirements of section 62(c)if it meets the requirements of businessconnection, substantiation, and return-ing amounts in excess of expenses. If anarrangement meets these requirements,all amounts paid under the arrangementare treated as paid under an accountableplan. Amounts treated as paid under anaccountable plan are excluded from theemployee’s gross income, are not reportedas wages or other compensation on theemployee’s Form W–2, and are exemptfrom the withholding and payment of em-ployment taxes. See section 1.62–2(c)(4).Conversely, amounts treated as paid un-der a nonaccountable plan are included inthe employee’s gross income, must be re-ported as wages or other compensation onthe employee’s Form W–2, and are subjectto withholding and payment of employ-ment taxes. See section 1.62–2(c)(5).

Section 1.62–2(d)(1) provides that anarrangement meets the business connec-tion requirements if it provides advances,allowances, or reimbursements only forbusiness expenses that are allowable as de-ductions and that are paid or incurred bythe employee in connection with the per-formance of services as an employee of the

2004-4 I.R.B. 325 January 26, 2004

employer. If, however, a payor arrangesto pay an amount to an employee regard-less of whether the employee incurs (or isreasonably expected to incur) deductibleemployee business expenses, the arrange-ment does not satisfy the business connec-tion requirements and all amounts paid un-der the arrangement are treated as paid un-der a nonaccountable plan. See section1.62–2(d)(3)(i); see also section 1.62–2(j),example (1) which describes the paymentof a fixed amount as either compensationor travel allowance and concludes that thearrangement does not satisfy the businessconnection requirements.

Section 1.62–2(e)(2) provides that anarrangement reimbursing use of a passen-ger automobile meets the substantiationrequirements if information sufficient tosatisfy the substantiation requirements ofsection 274(d) is submitted to the payor.Section 274(d) provides that no deduc-tion shall be allowed under section 162with respect to any listed property (includ-ing passenger automobiles and any otherproperty used as a means of transporta-tion) unless the taxpayer complies withcertain substantiation requirements. Sec-tion 1.274–5(g) grants the Commissionerthe authority to prescribe rules relating tomileage allowances for ordinary and nec-essary expenses of using a vehicle for lo-cal transportation. Pursuant to this grant ofauthority the Commissioner may prescriberules under which such allowances, if inaccordance with reasonable business prac-tice, will be regarded as (1) equivalent tosubstantiation of the amount of such trans-portation expenses, and (2) satisfying therequirements of an adequate accounting tothe employer of the amount of such ex-penses. The Commissioner annually pub-lishes a revenue procedure establishing abusiness standard mileage rate taxpayersmay use to substantiate the amount of thedeductible costs of operating an automo-bile for business purposes. See, for exam-ple, Rev. Proc. 2003–76, 2003–43 I.R.B.924 (or any successor.) A taxpayer mustnonetheless actually substantiate the ele-ments of time, use, and business purposerelating to the expenses.

Section 1.62–2(f) provides that anarrangement meets the return require-ments if it requires the employee to returnto the payor within a reasonable periodof time any amount paid under the ar-

rangement in excess of substantiated ex-penses. However, section 1.62–2(f)(2)provides that a reimbursement or otherexpense allowance arrangement that pro-vides mileage allowances for ordinary andnecessary expenses of local travel will betreated as satisfying the return of excessrequirements even though the arrangementdoes not require the employee to return theportion of such an allowance that relatesto the miles of travel substantiated andthat exceeds the amount of the employee’sexpenses deemed substantiated. This ex-ception applies only if the allowance ispaid at a rate for each mile of travel thatis reasonably calculated not to exceed theamount of the employee’s expenses oranticipated expenses and the employee isrequired to return to the payor within areasonable period of time any portion ofsuch allowance which relates to miles oftravel not substantiated.

In Shotgun Delivery, Inc. v. UnitedStates, 269 F.3d 969 (9th Cir. 2001), acourier company paid its drivers a com-mission equal to 40 percent of the tag rate.The commission was allocated betweencompensation paid at the minimum wageand a variable mileage reimbursement.The district court found that “becauseShotgun’s tag rates were not based solelyon distance traveled, and since Shotgundrivers could double up on deliveries,Shotgun’s reimbursement arrangement,was in fact, reimbursing its drivers in amanner not correlated to expenses Shot-gun’s employees incurred or were reason-ably likely to incur.” Shotgun Delivery,Inc. v. United States, 85 F.Supp. 2d 962,965 (N.D. Cal. 2000.) Consequently, thedistrict court concluded that Shotgun’sreimbursement arrangement failed to meetthe business connection requirements andheld that the mileage reimbursementswere paid under a nonaccountable plan. Inaffirming the district court’s holding, theNinth Circuit observed that such arrange-ments blur “the fundamental distinctionbetween taxable compensation and tax-ex-empt reimbursement which underpins thisentire aspect of the tax system” and con-cluded that “requiring a demonstrableconnection to actual business expensesprevents companies from improperly shel-tering otherwise taxable compensationunder the guise of reimbursement.” Shot-gun Delivery, 269 F.3d at 974.

ANALYSIS

1. Situation OneIn Situation One, the mileage al-

lowance meets the business connectionrequirements of section 1.62–2(d). Themileage allowance is paid with respect todeductible employee business expensesreasonably expected to be incurred by thedrivers. Employer reviews a sample ofreceipts, logbooks, and invoices annu-ally to estimate the drivers’ operating andfixed costs and, correspondingly, to setthe percentage of the tag rate paid as amileage allowance. Although the mileageallowance is computed on a basis simi-lar to that used in computing the driver’scompensation and, consequently, is paidat a variable mileage rate, the percentageof the tag rate paid as a mileage allowanceremains fixed throughout the calendaryear. Unlike the reimbursements at issuein Shotgun Delivery, Inc. v. United States,269 F.3d 969 (9th Cir. 2001), the mileageallowance in Situation One is paid withrespect to expenses reasonably expectedto be incurred and does not vary inverselywith the commission based on the numberof hours worked.

Similarly, in Situation One the mileageallowance meets the substantiation re-quirements of section 1.62–2(e). Specifi-cally, the drivers are required to substan-tiate monthly the time, use, and businesspurpose, i.e., the number of business milestraveled, relating to their use of an au-tomobile while delivering packages. Inlieu of substantiating the actual amount ofthe driver’s deductible transportation ex-penses, an amount is deemed substantiatedequal to the number of miles traveled mul-tiplied by the business standard mileagerate. An allowance paid with respect toordinary and necessary transportation ex-penses that is reasonably calculated not toexceed the amount of anticipated expensesand is paid at a flat rate or stated scheduleconstitutes a mileage allowance pursuantto section 1.274–5(g) and the rules pro-mulgated thereunder. See Rev. Proc.2003–76. While the mileage allowance inSituation One is paid at a variable mileagerate, it is nonetheless computed based ona fixed percentage of the tag rate and isconsidered paid at a flat rate or statedschedule. Thus, drivers are deemed tohave substantiated expenses at the busi-

January 26, 2004 326 2004-4 I.R.B.

ness standard mileage rate with respect toeach mile of travel actually substantiated.

Finally, in Situation One the mileageallowance meets the return of excess re-quirements of section 1.62–2(f). Employerintends to pay the mileage allowance onlywith respect to miles of travel substanti-ated by the drivers. Consequently, driversare not required to return the portion of themileage allowance exceeding the amountof expenses deemed substantiated. Seesection 1.62–2(f)(2).

Having met the business connection,substantiation, and return of excess re-quirements of section 1.62–2(c)(1), theportion of the mileage allowance that isnot in excess of the expenses deemed sub-stantiated may be treated as paid underan accountable plan in accordance withsection 62(c). Such amounts are excludedfrom the drivers’ gross income and areexempt from the withholding and pay-ment of employment taxes. The portionof the mileage allowance that is in excessof the expenses deemed substantiated istreated as paid under a nonaccountableplan. These amounts must be included inthe drivers’ gross income and are subjectto the withholding and payment of em-ployment taxes.

2. Situation TwoIn Situation Two, the reimbursement ar-

rangement does not meet the business con-nection requirements of section 1.62–2(d).A variable allocation between commissionand mileage allowance ensures that eachdriver receives Z percent of the tag rate re-gardless of the amount of deductible em-ployee business expenses incurred by thedriver. A bona fide reimbursement ar-rangement must preclude the recharacter-ization as a mileage allowance of amountsotherwise payable as a commission. Seesection 1.62–2(j), example (1); see alsoH.R. Conf. Rep. No. 998, 100th Cong.,2d Sess. 202–206 (1988). Consequently,the reimbursement arrangement in Situa-tion Two is treated as a nonaccountableplan, and all amounts paid under the planmust be included in the drivers’ gross in-come and are subject to the withholdingand payment of employment taxes.

HOLDING

Under the circumstances set forth inSituation One, a mileage allowance for lo-cal transportation expenses computed ona basis similar to that used in computinga courier’s compensation may be treatedas paid under an accountable plan. Theportion of the mileage allowance that isnot in excess of the expenses deemed sub-stantiated is excluded from the courier’sgross income and is exempt from thewithholding and payment of employmenttaxes. However, the portion of the mileageallowance that is in excess of the expensesdeemed substantiated is treated as paidunder a nonaccountable plan, must beincluded in the courier’s gross income,and is subject to the withholding and pay-ment of employment taxes. Under thecircumstances set forth in Situation Two,a variable allocation between commissionand mileage allowance does not meet thebusiness connection requirements. Conse-quently, the reimbursement arrangementis treated as a nonaccountable plan, andall amounts paid under the plan must beincluded in the drivers’ gross income andare subject to the withholding and pay-ment of employment taxes.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is Neil D. Shepherd of the Office of Di-vision Counsel/Associate Chief Counsel(Tax Exempt and Government Entities).For further information regarding this rev-enue ruling, contact Neil D. Shepherd at(202) 622-6040 (not a toll-free call).

Section 274.—Disallowanceof Certain Entertainment,etc., Expenses

26 CFR 1.274-5: Substantiation requirements.

Whether a mileage allowance for local transporta-tion expenses computed on a basis similar to thatused in computing a courier’s compensation may betreated as paid under an accountable plan so that itwill be excluded from the courier’s gross income and

exempt from the withholding and payment of em-ployment taxes. See Rev. Rul. 2004-1, page 325.

Section 472.—Last-in,First-out Inventories26 CFR 1.472–1: Last-in, first-out inventories.

LIFO; price indexes; departmentstores. The November 2003 Bureau ofLabor Statistics price indexes are acceptedfor use by department stores employingthe retail inventory and last-in, first-outinventory methods for valuing inventoriesfor tax years ended on, or with referenceto, November 30, 2003.

Rev. Rul. 2004–7

The following Department Store In-ventory Price Indexes for November 2003were issued by the Bureau of Labor Statis-tics. The indexes are accepted by the Inter-nal Revenue Service, under § 1.472–1(k)of the Income Tax Regulations and Rev.Proc. 86–46, 1986–2 C.B. 739, for ap-propriate application to inventories ofdepartment stores employing the retailinventory and last-in, first-out inventorymethods for tax years ended on, or withreference to, November 30, 2003.

The Department Store Inventory PriceIndexes are prepared on a national basisand include (a) 23 major groups of depart-ments, (b) three special combinations ofthe major groups — soft goods, durablegoods, and miscellaneous goods, and (c) astore total, which covers all departments,including some not listed separately, ex-cept for the following: candy, food, liquor,tobacco, and contract departments.

2004-4 I.R.B. 327 January 26, 2004

BUREAU OF LABOR STATISTICS, DEPARTMENT STOREINVENTORY PRICE INDEXES BY DEPARTMENT GROUPS

(January 1941 = 100, unless otherwise noted)

GroupsNov.2002

Nov.2003

Percent Changefrom Nov. 2002to Nov. 2003¹

1. Piece Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 473.3 480.5 1.52. Domestics and Draperies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 571.3 548.6 -4.03. Women’s and Children’s Shoes . . . . . . . . . . . . . . . . . . . . . . . . . . . . 652.4 649.8 -0.44. Men’s Shoes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 899.2 845.3 -6.05. Infants’ Wear . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 622.7 598.3 -3.96. Women’s Underwear. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 551.8 514.2 -6.87. Women’s Hosiery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345.3 343.3 -0.68. Women’s and Girls’ Accessories . . . . . . . . . . . . . . . . . . . . . . . . . . . 559.1 555.8 -0.69. Women’s Outerwear and Girls’ Wear . . . . . . . . . . . . . . . . . . . . . . . 373.5 375.7 0.610. Men’s Clothing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 572.1 549.5 -4.011. Men’s Furnishings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 603.6 598.3 -0.912. Boys’ Clothing and Furnishings . . . . . . . . . . . . . . . . . . . . . . . . . . . . 461.3 451.0 -2.213. Jewelry. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 871.7 866.8 -0.614. Notions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 793.1 797.2 0.515. Toilet Articles and Drugs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 972.5 976.2 0.416. Furniture and Bedding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 622.2 612.9 -1.517. Floor Coverings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 600.6 594.5 -1.018. Housewares. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 738.6 712.6 -3.519. Major Appliances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 221.6 210.0 -5.220. Radio and Television. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47.5 44.3 -6.721. Recreation and Education2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84.6 82.2 -2.822. Home Improvements2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125.2 124.9 -0.223. Automotive Accessories2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111.7 112.0 0.3

Groups 1–15: Soft Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 575.9 567.7 -1.4Groups 16–20: Durable Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 404.5 388.9 -3.9Groups 21–23: Misc. Goods2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95.4 93.9 -1.6

Store Total3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 513.0 503.1 -1.9

1Absence of a minus sign before the percentage change in this column signifies a price increase.2Indexes on a January 1986 = 100 base.3The store total index covers all departments, including some not listed separately, except for the following: candy, food, liquor,tobacco and contract departments.

DRAFTING INFORMATION

The principal author of this revenueruling is Michael Burkom of the Officeof Associate Chief Counsel (Income Taxand Accounting). For further informa-tion regarding this revenue ruling, contactMr. Burkom at (202) 622–7924 (not atoll-free call).

Section 527.—PoliticalOrganizations26 CFR 1.527–2: Definitions.(Also § 501.)

Public advocacy; public policy issues.This ruling concerns certain public advo-cacy activities conducted by social wel-fare organizations, unions and trade asso-ciations. The guidance clarifies the tax im-plications of advocacy that meets the defi-nition of political campaign activity.

Rev. Rul. 2004–6

Organizations that are exempt from fed-eral income tax under § 501(a) as organiza-

tions described in § 501(c)(4), § 501(c)(5),or § 501(c)(6) may, consistent with theirexempt purpose, publicly advocate posi-tions on public policy issues. This advo-cacy may include lobbying for legislationconsistent with these positions. Becausepublic policy advocacy may involve dis-cussion of the positions of public officialswho are also candidates for public office,a public policy advocacy communicationmay constitute an exempt function withinthe meaning of § 527(e)(2). If so, the or-ganization would be subject to tax under§ 527(f).

January 26, 2004 328 2004-4 I.R.B.

ISSUE

In each of the six situations describedbelow, has the organization exempt fromfederal income tax under § 501(a) as anorganization described in § 501(c)(4),§ 501(c)(5), or § 501(c)(6) that engagesin public policy advocacy expended fundsfor an exempt function as described in§ 527(e)(2)?

LAW

Section 501(c)(4) provides exemptionfrom taxation for civic leagues or organi-zations not organized for profit, but oper-ated exclusively for the promotion of so-cial welfare.

Section 1.501(c)(4)–1 of the IncomeTax Regulations states an organization isoperated exclusively for the promotion ofsocial welfare if it is primarily engaged inpromoting in some way the common goodand general welfare of the people of thecommunity.

Section 501(c)(5) provides exemptionfrom taxation for labor, agricultural, orhorticultural organizations.

Section 1.501(c)(5)–1 requires that la-bor, agricultural, or horticultural organiza-tions have as their objects the bettermentof the conditions of those engaged in suchpursuits, the improvement of the grade oftheir products, and the development of ahigher degree of efficiency in their respec-tive occupations.

Section 501(c)(6) provides exemptionfrom taxation for business leagues, not or-ganized for profit and no part of the netearnings of which inures to the benefit ofany private shareholder or individual.

Section 1.501(c)(6)–1 provides that abusiness league is an association of per-sons having some common business inter-est, the purpose of which is to promotesuch common interest and not to engage ina regular business of a kind ordinarily car-ried on for profit. A business league’s ac-tivities should be directed to the improve-ment of business conditions of one or morelines of business as distinguished from theperformance of particular services for in-dividual persons.

Section 527 generally provides that po-litical organizations that collect and ex-pend monies for exempt function purposesas described in § 527(e)(2) are exempt

from Federal income tax except on their in-vestment income.

Section 527(e)(1) defines a political or-ganization as a party, committee, associa-tion, fund or other organization (whetheror not incorporated), organized and oper-ated primarily for the purpose of accept-ing contributions or making expenditures,or both, for an exempt function.

Section 527(e)(2) provides that the term“exempt function” for purposes of § 527means the function of influencing or at-tempting to influence the selection, nom-ination, election, or appointment of anyindividual to any Federal, State, or localpublic office or office in a political organ-ization, or the election of Presidential orVice-Presidential electors, whether or notsuch individual or electors are selected,nominated, elected, or appointed. By itsterms, § 527(e)(2) includes all attempts toinfluence the selection, nomination, elec-tion, or appointment of the described offi-cials.

Section 527(f)(1) provides that an or-ganization described in § 501(c) and ex-empt from tax under § 501(a) is subjectto tax on any amount expended for an ex-empt function described in § 527(e)(2) atthe highest tax rate specified in § 11(b).The tax is imposed on the lesser of the netinvestment income of the organization forthe taxable year or the amount expendedon an exempt function during the taxableyear. A § 501(c) organization is taxed un-der § 527(f)(1) only if the expenditure isfrom its general treasury rather than froma separate segregated fund described in§ 527(f)(3).

Section 527(f)(3) provides that if an or-ganization described in § 501(c) and ex-empt from tax under § 501(a) sets up a sep-arate segregated fund (which segregatesmonies for § 527(e)(2) exempt functionpurposes) that fund will be treated as aseparate political organization described in§ 527 and, therefore, be subject to tax as apolitical organization under § 527.

Section 527(i) provides that, in order tobe tax-exempt, a political organization isrequired to give notice that it is a polit-ical organization described in § 527, un-less excepted. An organization describedin § 501(c) that does not set up a sepa-rate segregated fund, but makes exemptfunction expenditures subject to tax under§ 527(f) is not subject to this requirement.§ 527(i)(5)(A).

Section 527(j) provides that, unless ex-cepted, a tax-exempt political organiza-tion that has given notice under § 527(i)and does not timely make periodic reportsof contributions and expenditures, or thatfails to include the information required,must pay an amount calculated by mul-tiplying the amount of contributions andexpenditures that are not disclosed by thehighest corporate tax rate. An organizationdescribed in § 501(c) that does not set upa separate segregated fund, but makes ex-empt function expenditures subject to taxunder § 527(f), is not subject to the report-ing requirements under § 527(j).

Section 1.527–2(c)(1) provides that theterm “exempt function” includes all activ-ities that are directly related to and supportthe process of influencing or attempting toinfluence the selection, nomination, elec-tion, or appointment of any individual topublic office or office in a political organ-ization. Whether an expenditure is for anexempt function depends on all the factsand circumstances.

Section 1.527–6(f) provides that an or-ganization described in § 501(c) that is ex-empt under § 501(a) may, if it is consistentwith its exempt status, establish and main-tain a separate segregated fund to receivecontributions and make expenditures in apolitical campaign.

Rev. Rul. 2003–49, 2003–20 I.R.B.903 (May 19, 2003), discusses the re-porting and disclosure requirements forpolitical organizations in question andanswer format. In Q&A–6, the rulingholds that while a § 501(c) organizationthat makes an expenditure for an exemptfunction under § 527(e)(2) is not requiredto file the notice required under § 527(i), ifthe § 501(c) organization establishes a sep-arate segregated fund under § 527(f)(3),that fund is required to file the notice inorder to be tax-exempt unless it meets oneof the other exceptions to filing.

Certain broadcast, cable, or satellitecommunications that meet the definitionof “electioneering communications” areregulated by the Bipartisan CampaignReform Act of 2002 (BCRA), 116 Stat.81. An exempt organization that violatesthe regulatory requirements of BCRA maywell jeopardize its exemption or be subjectto other tax consequences.

2004-4 I.R.B. 329 January 26, 2004

ANALYSIS OF FACTUALSITUATIONS

An organization exempt from federalincome tax under § 501(a) as an organi-zation described in § 501(c) that, consis-tent with its tax-exempt status, wishes toengage in an exempt function within themeaning of § 527(e)(2) may do so withits own funds or by setting up a separatesegregated fund under § 527(f)(3). If theorganization chooses to establish a sepa-rate segregated fund, that fund, unless ex-cepted, must give notice under § 527(i) inorder to be tax-exempt. A separate seg-regated fund that has given notice under§ 527(i) is then subject to the reporting re-quirements under § 527(j). See Rev. Rul.2003–49. If the organization chooses touse its own funds, the organization is notsubject to the notice requirements under§ 527(i) and the reporting requirements un-der § 527(j), but is subject to tax under§ 527(f)(1) on the lesser of its investmentincome or the amount of the exempt func-tion expenditure.

All the facts and circumstances must beconsidered to determine whether an expen-diture for an advocacy communication re-lating to a public policy issue is for an ex-empt function under § 527(e)(2). When anadvocacy communication explicitly advo-cates the election or defeat of an individualto public office, the expenditure clearly isfor an exempt function under § 527(e)(2).However, when an advocacy communica-tion relating to a public policy issue doesnot explicitly advocate the election or de-feat of a candidate, all the facts and circum-stances need to be considered to determinewhether the expenditure is for an exemptfunction under § 527(e)(2).

In facts and circumstances such as thosedescribed in the six situations, factors thattend to show that an advocacy communi-cation on a public policy issue is for an ex-empt function under § 527(e)(2) include,but are not limited to, the following:

a) The communication identifies a can-didate for public office;

b) The timing of the communication co-incides with an electoral campaign;

c) The communication targets voters ina particular election;

d) The communication identifies thatcandidate’s position on the public policyissue that is the subject of the communi-cation;

e) The position of the candidate on thepublic policy issue has been raised as dis-tinguishing the candidate from others inthe campaign, either in the communicationitself or in other public communications;and

f) The communication is not part of anongoing series of substantially similar ad-vocacy communications by the organiza-tion on the same issue.

In facts and circumstances such as thosedescribed in the six situations, factors thattend to show that an advocacy communi-cation on a public policy issue is not for anexempt function under § 527(e)(2) include,but are not limited to, the following:

a) The absence of any one or more ofthe factors listed in a) through f) above;

b) The communication identifies spe-cific legislation, or a specific event outsidethe control of the organization, that the or-ganization hopes to influence;

c) The timing of the communication co-incides with a specific event outside thecontrol of the organization that the organ-ization hopes to influence, such as a leg-islative vote or other major legislative ac-tion (for example, a hearing before a leg-islative committee on the issue that is thesubject of the communication);

d) The communication identifies thecandidate solely as a government officialwho is in a position to act on the publicpolicy issue in connection with the spe-cific event (such as a legislator who iseligible to vote on the legislation); and

e) The communication identifies thecandidate solely in the list of key or prin-cipal sponsors of the legislation that is thesubject of the communication.

In all of the situations, the advocacycommunication identifies a candidate in anelection, appears shortly before that elec-tion, and targets the voters in that election.Even though these factors are present, theremaining facts and circumstances mustbe analyzed in each situation to determinewhether the advocacy communication isfor an exempt function under § 527(e)(2).

Each of the situations assumes that:1. All payments for the described activ-

ity are from the general treasury of the or-ganization rather than from a separate seg-regated fund under § 527(f)(3);

2. The organization would continueto be exempt under § 501(a), even if thedescribed activity is not a § 501(c) ex-empt activity, because the organization’s

primary activities are described in the ap-propriate subparagraph of § 501(c); and

3. All advocacy communications de-scribed also include a solicitation of con-tributions to the organization.

Situation 1. N, a labor organization rec-ognized as tax exempt under § 501(c)(5),advocates for the betterment of conditionsof law enforcement personnel. SenatorA and Senator B represent State U in theUnited States Senate. In year 200x, Nprepares and finances full-page newspa-per advertisements supporting increasedspending on law enforcement, whichwould require a legislative appropriation.These advertisements are published in sev-eral large circulation newspapers in StateU on a regular basis during year 200x.One of these full-page advertisements ispublished shortly before an election inwhich Senator A (but not Senator B) is acandidate for re-election. The advertise-ment published shortly before the electionstresses the importance of increased fed-eral funding of local law enforcementand refers to numerous statistics indicat-ing the high crime rate in State U. Theadvertisement does not mention SenatorA’s or Senator B’s position on law en-forcement issues. The advertisement endswith the statement “Call or write SenatorA and Senator B to ask them to supportincreased federal funding for local lawenforcement.” Law enforcement has notbeen raised as an issue distinguishing Sen-ator A from any opponent. At the time thisadvertisement is published, no legislativevote or other major legislative activity isscheduled in the United States Senate onincreased federal funding for local lawenforcement.

Under the facts and circumstances inSituation 1, the advertisement is not for anexempt function under § 527(e)(2). Al-though N’s advertisement identifies Sena-tor A, appears shortly before an election inwhich Senator A is a candidate, and targetsvoters in that election, it is part of an ongo-ing series of substantially similar advocacycommunications by N on the same issueduring year 200x. The advertisement iden-tifies both Senator A and Senator B, who isnot a candidate for re-election, as the rep-resentatives who would vote on this issue.Furthermore, N’s advertisement does notidentify Senator A’s position on the issue,and law enforcement has not been raised asan issue distinguishing Senator A from any

January 26, 2004 330 2004-4 I.R.B.

opponent. Therefore, there is nothing toindicate that Senator A’s candidacy shouldbe supported or opposed based on this is-sue. Based on these facts and circum-stances, the amount expended by N on theadvertisement is not an exempt functionexpenditure under § 527(e)(2) and, there-fore, is not subject to tax under § 527(f)(1).

Situation 2. O, a trade association rec-ognized as tax exempt under § 501(c)(6),advocates for increased international trade.Senator C represents State V in the UnitedStates Senate. O prepares and financesa full-page newspaper advertisement thatis published in several large circulationnewspapers in State V shortly before anelection in which Senator C is a candidatefor nomination in a party primary. Theadvertisement states that increased inter-national trade is important to a major in-dustry in State V. The advertisement statesthat S. 24, a pending bill in the UnitedStates Senate, would provide manufactur-ing subsidies to certain industries to en-courage export of their products. The ad-vertisement also states that several manu-facturers in State V would benefit from thesubsidies, but Senator C has opposed simi-lar measures supporting increased interna-tional trade in the past. The advertisementends with the statement “Call or write Sen-ator C to tell him to vote for S. 24.” Interna-tional trade concerns have not been raisedas an issue distinguishing Senator C fromany opponent. S. 24 is scheduled for a votein the United States Senate before the elec-tion, soon after the date that the advertise-ment is published in the newspapers.

Under the facts and circumstances inSituation 2, the advertisement is not for anexempt function under § 527(e)(2). O’sadvertisement identifies Senator C, ap-pears shortly before an election in whichSenator C is a candidate, and targetsvoters in that election. Although interna-tional trade issues have not been raisedas an issue distinguishing Senator C fromany opponent, the advertisement identi-fies Senator C’s position on the issue ascontrary to O’s position. However, theadvertisement specifically identifies thelegislation O is supporting and appearsimmediately before the United States Sen-ate is scheduled to vote on that particularlegislation. The candidate identified, Sen-ator C, is a government official who isin a position to take action on the pub-lic policy issue in connection with the

specific event. Based on these facts andcircumstances, the amount expended byO on the advertisement is not an exemptfunction expenditure under § 527(e)(2)and, therefore, is not subject to tax under§ 527(f)(1).

Situation 3. P, an entity recognized astax exempt under § 501(c)(4), advocatesfor better health care. Senator D representsState W in the United States Senate. P pre-pares and finances a full-page newspaperadvertisement that is published repeatedlyin several large circulation newspapers inState W beginning shortly before an elec-tion in which Senator D is a candidate forre-election. The advertisement is not partof an ongoing series of substantially simi-lar advocacy communications by P on thesame issue. The advertisement states thata public hospital is needed in a major cityin State W but that the public hospital can-not be built without federal assistance. Theadvertisement further states that SenatorD has voted in the past year for two billsthat would have provided the federal fund-ing necessary for the hospital. The adver-tisement then ends with the statement “LetSenator D know you agree about the needfor federal funding for hospitals.” Federalfunding for hospitals has not been raisedas an issue distinguishing Senator D fromany opponent. At the time the advertise-ment is published, a bill providing federalfunding for hospitals has been introducedin the United States Senate, but no legisla-tive vote or other major legislative activityon that bill is scheduled in the Senate.

Under the facts and circumstances inSituation 3, the advertisement is for an ex-empt function under § 527(e)(2). P’s ad-vertisement identifies Senator D, appearsshortly before an election in which Sena-tor D is a candidate, and targets voters inthat election. Although federal funding ofhospitals has not been raised as an issuedistinguishing Senator D from any oppo-nent, the advertisement identifies SenatorD’s position on the hospital funding issueas agreeing with P’s position, and is notpart of an ongoing series of substantiallysimilar advocacy communications by P onthe same issue. Moreover, the advertise-ment does not identify any specific leg-islation and is not timed to coincide witha legislative vote or other major legisla-tive action on the hospital funding issue.Based on these facts and circumstances,the amount expended by P on the adver-

tisement is an exempt function expenditureunder § 527(e)(2) and, therefore, is subjectto tax under § 527(f)(1).

Situation 4. R, an entity recognized astax exempt under § 501(c)(4), advocatesfor improved public education. GovernorE is the governor of State X. R preparesand finances a radio advertisement urgingan increase in state funding for public ed-ucation in State X, which requires a leg-islative appropriation. The radio adver-tisement is first broadcast on several radiostations in State X beginning shortly be-fore an election in which Governor E is acandidate for re-election. The advertise-ment is not part of an ongoing series ofsubstantially similar advocacy communi-cations by R on the same issue. The adver-tisement cites numerous statistics indicat-ing that public education in State X is un-der-funded. While the advertisement doesnot say anything about Governor E’s po-sition on funding for public education, itends with “Tell Governor E what you thinkabout our under-funded schools.” In publicappearances and campaign literature, Gov-ernor E’s opponent has made funding ofpublic education an issue in the campaignby focusing on Governor E’s veto of anincome tax increase the previous year toincrease funding of public education. Atthe time the advertisement is broadcast, nolegislative vote or other major legislativeactivity is scheduled in the State X legisla-ture on state funding of public education.

Under the facts and circumstances inSituation 4, the advertisement is for anexempt function under § 527(e)(2). R’sadvertisement identifies Governor E, ap-pears shortly before an election in whichGovernor E is a candidate, and targetsvoters in that election. Although the ad-vertisement does not explicitly identifyGovernor E’s position on the funding ofpublic schools issue, that issue has beenraised as an issue in the campaign by Gov-ernor E’s opponent. The advertisementdoes not identify any specific legisla-tion, is not part of an ongoing series ofsubstantially similar advocacy communi-cations by R on the same issue, and is nottimed to coincide with a legislative voteor other major legislative action on thatissue. Based on these facts and circum-stances, the amount expended by R on theadvertisement is an exempt function ex-penditure under § 527(e)(2) and, therefore,is subject to tax under § 527(f)(1).

2004-4 I.R.B. 331 January 26, 2004

Situation 5. S, an entity recognized astax exempt under § 501(c)(4), advocatesto abolish the death penalty in State Y.Governor F is the governor of State Y.S regularly prepares and finances televi-sion advertisements opposing the deathpenalty. These advertisements appearon several television stations in State Yshortly before each scheduled execution inState Y. One such advertisement opposingthe death penalty appears on State Y televi-sion stations shortly before the scheduledexecution of G and shortly before an elec-tion in which Governor F is a candidatefor re-election. The advertisement broad-cast shortly before the election providesstatistics regarding developed countriesthat have abolished the death penalty andrefers to studies indicating inequities re-lated to the types of persons executed inthe United States. Like the advertisementsappearing shortly before other scheduledexecutions in State Y, the advertisementnotes that Governor F has supported thedeath penalty in the past and ends with thestatement “Call or write Governor F to de-mand that he stop the upcoming executionof G.”

Under the facts and circumstances inSituation 5, the advertisement is not for anexempt function under § 527(e)(2). S’s ad-vertisement identifies Governor F, appearsshortly before an election in which Gover-nor F is a candidate, targets voters in thatelection, and identifies Governor F’s posi-tion as contrary to S’s position. However,the advertisement is part of an ongoing se-ries of substantially similar advocacy com-munications by S on the same issue and theadvertisement identifies an event outsidethe control of the organization (the sched-uled execution) that the organization hopes

to influence. Further, the timing of theadvertisement coincides with this specificevent that the organization hopes to influ-ence. The candidate identified is a govern-ment official who is in a position to takeaction on the public policy issue in con-nection with the specific event. Based onthese facts and circumstances, the amountexpended by S on the advertisements isnot an exempt function expenditure under§ 527(e)(2) and, therefore, is not subject totax under § 527(f)(1).

Situation 6. T, an entity recognizedas tax exempt under § 501(c)(4), advo-cates to abolish the death penalty in StateZ. Governor H is the governor of StateZ. Beginning shortly before an electionin which Governor H is a candidate forre-election, T prepares and finances a tele-vision advertisement broadcast on severaltelevision stations in State Z. The adver-tisement is not part of an ongoing seriesof substantially similar advocacy commu-nications by T on the same issue. Theadvertisement provides statistics regard-ing developed countries that have abol-ished the death penalty, and refers to stud-ies indicating inequities related to the typesof persons executed in the United States.The advertisement calls for the abolish-ment of the death penalty. The advertise-ment notes that Governor H has supportedthe death penalty in the past. The adver-tisement identifies several individuals pre-viously executed in State Z, stating thatGovernor H could have saved their livesby stopping their executions. No execu-tions are scheduled in State Z in the nearfuture. The advertisement concludes withthe statement “Call or write Governor H todemand a moratorium on the death penaltyin State Z.”

Under the facts and circumstances inSituation 6, the advertisement is for anexempt function under § 527(e)(2). T’sadvertisement identifies Governor H, ap-pears shortly before an election in whichGovernor H is a candidate, targets the vot-ers in that election, and identifies Gover-nor H’s position as contrary to T’s posi-tion. The advertisement is not part of anongoing series of substantially similar ad-vocacy communications by T on the sameissue. In addition, the advertisement doesnot identify and is not timed to coincidewith a specific event outside the control ofthe organization that it hopes to influence.Based on these facts and circumstances,the amount expended by T on the adver-tisement is an exempt function expenditureunder § 527(e)(2) and, therefore, is subjectto tax under § 527(f)(1).

HOLDINGS

In Situations 1, 2, and 5, the amountsexpended by N, O, and S are not exemptfunction expenditures under § 527(e)(2)and, therefore, are not subject to tax un-der § 527(f)(1). In Situations 3, 4, and6, the amounts expended by P, R and Tare exempt function expenditures under§ 527(e)(2) and, therefore, are subject totax under § 527(f)(1).

DRAFTING INFORMATION

The principal author of this revenue rul-ing is Judith E. Kindell of Exempt Or-ganizations, Tax Exempt and GovernmentEntities Division. For further informa-tion regarding this revenue ruling, contactJudith E. Kindell at (202) 283–8964 (not atoll-free call).

January 26, 2004 332 2004-4 I.R.B.

Part III. Administrative, Procedural, and MiscellaneousAbusive Roth IRA Transactions

Notice 2004–8

The Internal Revenue Service and theTreasury Department are aware of a typeof transaction, described below, that tax-payers are using to avoid the limitations oncontributions to Roth IRAs. This noticealerts taxpayers and their representativesthat these transactions are tax avoidancetransactions and identifies these trans-actions, as well as substantially similartransactions, as listed transactions for pur-poses of § 1.6011–4(b)(2) of the IncomeTax Regulations and §§ 301.6111–2(b)(2)and 301.6112–1(b)(2) of the Procedureand Administration Regulations. This no-tice also alerts parties involved with thesetransactions of certain responsibilities thatmay arise from their involvement withthese transactions.

Background

Section 408A was added to the InternalRevenue Code by section 302 of the Tax-payer Relief Act of 1997, Pub. L. 105–34,105th Cong., 1st Sess. 40 (1997). Thissection created Roth IRAs as a new typeof nondeductible individual retirementarrangement (IRA). The maximum an-nual contribution to Roth IRAs is the samemaximum amount that would be allowableas a deduction under § 219 with respectto the individual for the taxable year overthe aggregate amount of contributions forthat taxable year to all other IRAs. Neitherthe contributions to a Roth IRA nor theearnings on those contributions are sub-ject to tax on distribution, if distributedas a qualified distribution described in§ 408A(d)(2).

A contribution to a Roth IRA above thestatutory limits generates a 6-percent ex-cise tax described in § 4973. The excisetax is imposed each year until the excesscontribution is eliminated.

Facts

In general, these transactions involvethe following parties: (1) an individual(the Taxpayer) who owns a pre-existingbusiness such as a corporation or a sole

proprietorship (the Business), (2) a RothIRA within the meaning of § 408A that ismaintained for the Taxpayer, and (3) a cor-poration (the Roth IRA Corporation), sub-stantially all the shares of which are ownedor acquired by the Roth IRA. The Businessand the Roth IRA Corporation enter intotransactions as described below. The ac-quisition of shares, the transactions or bothare not fairly valued and thus have the ef-fect of shifting value into the Roth IRA.

Examples include transactions in whichthe Roth IRA Corporation acquires prop-erty, such as accounts receivable, from theBusiness for less than fair market value,contributions of property, including intan-gible property, by a person other than theRoth IRA, without a commensurate receiptof stock ownership, or any other arrange-ment between the Roth IRA Corporationand the Taxpayer, a related party describedin § 267(b) or 707(b), or the Business thathas the effect of transferring value to theRoth IRA Corporation comparable to acontribution to the Roth IRA.

Analysis

The transactions described in this noticehave been designed to avoid the statutorylimits on contributions to a Roth IRA con-tained in § 408A. Because the Taxpayercontrols the Business and is the beneficialowner of substantially all of the Roth IRACorporation, the Taxpayer is in the posi-tion to shift value from the Business to theRoth IRA Corporation. The Service in-tends to challenge the purported tax ben-efits claimed for these arrangements on anumber of grounds.

In challenging the purported tax bene-fits, the Service will, in appropriate cases,assert that the substance of the transac-tion is that the amount of the value shiftedfrom the Business to the Roth IRA Corpo-ration is a payment to the Taxpayer, fol-lowed by a contribution by the Taxpayerto the Roth IRA and a contribution by theRoth IRA to the Roth IRA Corporation.In such cases, the Service will deny or re-duce the deduction to the Business; mayrequire the Business, if the Business is acorporation, to recognize gain on the trans-fer under § 311(b); and may require inclu-

sion of the payment in the income of theTaxpayer (for example, as a taxable divi-dend if the Business is a C corporation).See Sammons v. United States, 433 F.2d728 (5th Cir. 1970); Worcester v. Com-missioner, 370 F.2d 713 (1st Cir. 1966).

Depending on the facts of the specificcase, the Service may apply § 482 to al-locate income from the Roth IRA Corpo-ration to the Taxpayer, Business, or otherentities under the control of the Taxpayer.Section 482 provides the Secretary withauthority to allocate gross income, deduc-tions, credits or allowances among personsowned or controlled directly or indirectlyby the same interests, if such allocation isnecessary to prevent evasion of taxes orclearly to reflect income. The § 482 reg-ulations provide that the standard to be ap-plied is that of a person dealing at arm’slength with an uncontrolled person. Seegenerally § 1.482–1(b) of the Income TaxRegulations. To the extent that the con-sideration paid or received in transactionsbetween the Business and the Roth IRACorporation is not in accordance with thearm’s length standard, the Service may ap-ply § 482 as necessary to prevent evasionof taxes or clearly to reflect income. Inthe event of a § 482 allocation between theRoth IRA Corporation and the Businessor other parties, correlative allocations andother conforming adjustments would bemade pursuant to § 1.482–1(g). Also see,Rev. Rul. 78–83, 1978–1 C.B. 79.

In addition to any other tax conse-quences that may be present, the amounttreated as a contribution as describedabove is subject to the excise tax de-scribed in § 4973 to the extent that it isan excess contribution within the meaningof § 4973(f). This is an annual tax that isimposed until the excess amount is elim-inated.

Moreover, under § 408(e)(2)(A), theService may take the position in appro-priate cases that the transaction gives riseto one or more prohibited transactionsbetween a Roth IRA and a disqualifiedperson described in § 4975(e)(2). Forexample, the Department of Labor1 hasadvised the Service that, to the extent thatthe Roth IRA Corporation constitutes aplan asset under the Department of La-

1 Under section 102 of Reorganization Plan No. 4 of 1978 (43 FR 47713), the Secretary of Labor has interpretive jurisdiction over § 4975 of the Internal Revenue Code.

2004-4 I.R.B. 333 January 26, 2004

bor’s plan asset regulation (29 C.F.R.§ 2510.3–101), the provision of servicesby the Roth IRA Corporation to the Tax-payer’s Business (which is a disqualifiedperson with respect to the Roth IRA under§ 4975(e)(2)) would constitute a prohib-ited transaction under § 4975(c)(1)(C).2

Further, the Department of Labor has ad-vised the Service that, if a transactionbetween a disqualified person and theRoth IRA would be a prohibited trans-action, then a transaction between thatdisqualified person and the Roth IRA Cor-poration would be a prohibited transactionif the Roth IRA may, by itself, require theRoth IRA Corporation to enter into thetransaction.3

Listed Transactions

The following transactions are identi-fied as “listed transactions” for purposes of§§ 1.6011–4(b)(2), 301.6111–2(b)(2) and301.6112–1(b)(2) effective December 31,2003, the date this document is releasedto the public: arrangements in whichan individual, related persons described in§ 267(b) or 707(b), or a business controlledby such individual or related persons, en-gage in one or more transactions with acorporation, including contributions ofproperty to such corporation, substantiallyall the shares of which are owned by oneor more Roth IRAs maintained for thebenefit of the individual, related personsdescribed in § 267(b)(1), or both. Thetransactions are listed transactions withrespect to the individuals for whom theRoth IRAs are maintained, the business(if not a sole proprietorship) that is a partyto the transaction, and the corporationsubstantially all the shares of which areowned by the Roth IRAs. Independent oftheir classification as “listed transactions,”these transactions may already be subjectto the disclosure requirements of § 6011(§ 1.6011–4), the tax shelter registrationrequirements of § 6111 (§§ 301.6111–1Tand 301.6111–2), or the list maintenancerequirements of § 6112 (§ 301.6112–1).

Substantially similar transactions in-clude transactions that attempt to use asingle structure with the intent of achiev-

ing the same or substantially same tax ef-fect for multiple taxpayers. For example,if the Roth IRA Corporation is owned bymultiple taxpayers’ Roth IRAs, a substan-tially similar transaction occurs wheneverthat Roth IRA Corporation enters into atransaction with a business of any of thetaxpayers if distributions from the RothIRA Corporation are made to that tax-payer’s Roth IRA based on the purportedbusiness transactions done with that tax-payer’s business or otherwise based on thevalue shifted from that taxpayer’s businessto the Roth IRA Corporation.

Persons required to register these taxshelters under § 6111 who have failed todo so may be subject to the penalty un-der § 6707(a). Persons required to main-tain lists of investors under § 6112 whohave fail to do so (or who fail to pro-vide such lists when requested by the Ser-vice) may be subject to the penalty under§ 6708(a). In addition, the Service may im-pose penalties on participants in this trans-action or substantially similar transactions,including the accuracy-related penalty un-der § 6662, and as applicable, persons whoparticipate in the reporting of this transac-tion or substantially similar transactions,including the return preparer penalty under§ 6694, the promoter penalty under § 6700,and the aiding and abetting penalty under§ 6701.

The Service and the Treasury recognizethat some taxpayers may have filed tax re-turns taking the position that they were en-titled to the purported tax benefits of thetype of transaction described in this notice.These taxpayers should consult with a taxadvisor to ensure that their transactions aredisclosed properly and to take appropriatecorrective action.

Drafting Information

The principal author of this notice isMichael Rubin of the Employee Plans,Tax Exempt and Government Entities Di-vision. However, other personnel from theService and Treasury participated in itsdevelopment. Mr. Rubin may be reachedat (202) 283–9888 (not a toll-free call).

Information ReportingRelating to CorporateInversions

Notice 2004–9

SECTION 1. Purpose

This notice announces the extensionof certain 2004 deadlines under revised§§ 1.6043–4T and 1.6045–3T of the In-come Tax Regulations for filing Form8806 and furnishing Form 1099–CAP toclearing organizations. This notice alsoprovides information to filers of Forms1099–CAP and 1099–B to assist in com-plying with the reporting requirementsset forth in revised §§ 1.6043–4T and1.6045–3T. The 2003 Forms 1099–CAPand 1099–B, and their instructions, donot reflect the provisions of the revisedtemporary regulations.

SECTION 2. Background

On December 30, 2003, the InternalRevenue Service (Service) issued tempo-rary regulations under sections 6043(c)and 6045 of the Internal Revenue Code(T.D. 9101, 2004–5 I.R.B. [68 FR75119]). These regulations, which revisetemporary regulations issued on Novem-ber 18, 2002 (T.D. 9022, 2002–2 C.B.909 [67 FR 69468]), require informa-tion reporting if a domestic corporationundergoes an acquisition of control or asubstantial change in capital structure af-ter December 31, 2002, if the reportingcorporation or any shareholder is requiredto recognize gain (if any) as a result ofthe application of section 367(a) of theInternal Revenue Code (Code). Pursuantto the revised regulations, a corporationmust file Form 8806, “Information Returnfor Acquisition of Control or SubstantialChange in Capital Structure,” reportingand describing the acquisition of controlor substantial change in capital structure.In addition, the revised regulations requirethe corporation to file Form 1099–CAP,“Changes in Corporate Control and Cap-ital Structure,” with the Service withrespect to each of its shareholders that

2 For the Roth IRA Corporation to be considered as holding plan assets under the Department of Labor’s plan asset regulation, the Roth IRA’s investment in the Roth IRA Corporation mustbe an equity interest, the Roth IRA Corporation’s securities must not be publicly-offered securities, and the Roth IRA’s investment in the Roth IRA Corporation must be significant. 29 C.F.R.§§ 2510.3–101(a)(2), 2510.3–101(b)(1), 2510.3–101(b)(2), and 2510.3–101(f). Although the Roth IRA Corporation would not be treated as holding plan assets if the Roth IRA Corporationconstituted an operating company within the meaning of 29 C.F.R. § 2510.3–101(c), given the context of the examples described in this notice, it is unlikely that the Roth IRA Corporationwould qualify as an operating company.

3 See 29 C.F.R. § 2509.75–2(c).

January 26, 2004 334 2004-4 I.R.B.

is not an exempt recipient, and to furnishForm 1099–CAP to each such shareholder.The regulations also require a broker thatholds stock on behalf of a customer in thecorporation that the broker knows or hasreason to know has engaged in a transac-tion described in these regulations to fileForm 1099–B, “Proceeds From Brokerand Barter Exchange Transactions,” withthe Service with respect to its customer,and to furnish a copy of the Form 1099–Bto the customer.

SECTION 3. Extension of Deadlines

Section 6081 of the Code providesthat the Secretary may grant a reasonableextension of time for filing any return,declaration, statement, or other documentrequired by the Code or by regulationsthereunder. Under the authority of section6081, the Service is extending the dead-lines set forth in revised §§ 1.6043–4Tand 1.6045–3T for filing Forms 8806with the Service and furnishing Forms1099–CAP to clearing organizations fortransactions occurring in calendar year2003. Forms 8806 otherwise required tobe filed with the Service by January 5,2004, must be filed by January 12, 2004.Forms 1099–CAP otherwise required tobe furnished to clearing organizations byJanuary 5, 2004, must be furnished byJanuary 12, 2004. This extension does notapply to any other deadline.

SECTION 4. Information for Filers ofForm 1099–CAP

Under revised § 1.6043–4T(b), areporting corporation must file Form1099–CAP with respect to its sharehold-ers who are not exempt recipients. Thelist of exempt recipients is set forth in§ 1.6043–4T(b)(5), and includes brokers.Clearing organizations are not exemptrecipients under the revised regulations.Therefore, corporations must file Form1099–CAP with respect to shares heldby a clearing organization, and furnish acopy of the form to the clearing organiza-tion. Pursuant to § 1.6043–4T(b)(4), Form1099–CAP must be furnished to clearingorganizations by January 5th of the yearfollowing the calendar year in which thetransaction took place. Pursuant to Sec-tion 3 of this notice, Forms 1099–CAPotherwise due on January 5, 2004, mustbe furnished to clearing organizations no

later than January 12, 2004. Taxpayers,however, are encouraged to comply assoon as possible prior to January 12, 2004.

The Depository Trust Company (DTC)is a clearing organization which holds alarge percentage of publicly issued se-curities, and is likely to receive Forms1099–CAP pursuant to the provisions of§ 1.6043–4T(b). In anticipation of receiv-ing such forms, DTC has established aspecific mailing address. DTC requeststhat Forms 1099–CAP be delivered viaexpress mail or other overnight service to:

Tax Information Reporting ServicesDepository Trust & Clearing Corporation55 Water Street — 25th FloorNew York, NY 10041(212) 855–4703

The envelope should be marked withthe words:

TIME CRITICAL TAXINFORMATION FORM 1099–CAP

DTC will also accept Form 1099–CAPelectronically. Forms should be emailedto:

[email protected] in Adobe AcrobatPDF file format

Furnishing Forms 1099 to payees elec-tronically is permitted pursuant to section401 of the Job Creation and Worker Assis-tance Act of 2002, if the rules set forth in§ 31.6051–1T(j) are followed.

SECTION 5. Information for Filers ofForm 1099–B

Pursuant to revised § 1.6045–3T(a), abroker that holds shares on behalf of acustomer in a corporation that the brokerknows or has reason to know has engagedin a transaction under § 1.6043–4T(c) or(d) must file an information return with re-spect to the customer, unless the customeris an exempt recipient, and furnish a copyof the information return to the customer.Revised § 1.6045–3T(c) provides that thebroker must use Form 1099–B, along withtransmittal Form 1096, for this informa-tion reporting requirement. With respect totransactions in 2003, the broker may electto use Form 1099–CAP in lieu of Form1099–B.

In completing Form 1099–B, brokersshould aggregate all proceeds (cash, stock,

and other property) provided to the cus-tomer in Box 2 (Stocks, bonds, etc.). Bro-kers should use Box 5 (Description) to re-port the name and address of the corpo-ration which engaged in the transactionand the number and class of shares ex-changed by the customers (as required by§ 1.6045–3T(d)(2) and (3)).

SECTION 6. DRAFTINGINFORMATION

For further information regarding thisnotice, contact Nancy Rose of the Officeof the Associate Chief Counsel (Procedure& Administration), Administrative Pro-visions and Judicial Practice Division, at(202) 622–4910 (not a toll-free call).

26 CFR 301.7508–1: Time for performing certainacts postponed by reason of service in a combat zoneor a Presidentially declared disaster.(Also Part I, § 7508A; § 301.7508A–1.)

Rev. Proc. 2004–13

SECTION 1. PURPOSE

.01 This revenue procedure provides anupdated list of time-sensitive acts, the per-formance of which may be postponed un-der sections 7508 and 7508A of the Inter-nal Revenue Code (Code). Section 7508of the Code postpones specified acts forindividuals serving in the Armed Forcesof the United States or serving in sup-port of such Armed Forces in a combatzone. Section 7508A of the Code permits apostponement of specified acts for taxpay-ers affected by a Presidentially declareddisaster or a terroristic or military action.The list of acts in this revenue proceduresupplements the list of postponed acts insection 7508(a)(1) of the Code and sec-tion 301.7508A–1(b) of the Regulations onProcedure and Administration.

.02 This revenue procedure does not,by itself, provide any postponements un-der sections 7508 or 7508A. In order fortaxpayers to be entitled to a postponementof any act listed in this revenue proce-dure, the IRS generally will publish a No-tice or issue other guidance (including anIRS News Release) providing relief withrespect to a specific combat zone, Presi-dentially declared disaster, or a terroristicor military action.

2004-4 I.R.B. 335 January 26, 2004