Embed Size (px)

Citation preview

VOLUME 73 • NUMBER 8 D AUGUST 1987

FEDERAL RESERVE

BULLETIN

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C.

PUBLICATIONS COMMITTEE

Joseph R. Coyne, Chairman • Michael Bradfield • S. David Frost• Griffith L. Garwood • James L. Kichline • Edwin M. Truman

The FEDERAL RESERVE BULLETIN is issued monthly under the direction of the staff publications committee. This committee is responsible foropinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by Mendelle T.Berenson, the Graphic Communications Section under the direction of Peter G, Thomas, and Publications Services supervised by Linda C. Kyles.

Table of Contents

633 MONETARY POLICY REPORT TO THECONGRESS

The economy expanded at a somewhat ac-celerated pace in the first half of 1987, andthe civilian unemployment rate declinedover the period to 6.1 percent in June, thelowest level in this decade.

647 INDUSTRIAL PRODUCTION

Industrial production increased an estimat-ed 0,5 percent in May.

649 STATEMENT TO CONGRESS

Manuel H. Johnson, Vice Chairman, Boardof Governors, offers testimony on the issueof money laundering, including efforts topress for greater international cooperationby bank supervisors in addressing the use ofbanking organizations to launder money,before the Subcommittee on Financial Insti-tutions Supervision, Regulation and Insur-ance of the House Committee on Banking,Finance and Urban Affairs, June 9, 1987.

655 ANNOUNCEMENTS

Statement by Chairman Volcker on thedeath of Arthur F. Burns.

Meeting of Consumer Advisory Council.

Nominations sought for appointments toConsumer Advisory Council.

Direct deposit of social security paymentsin the United Kingdom.

Amendment to Regulation Y.

Comments requested on revised proposal tocharge assessments and fees for certainsupervisory activities.

Changes in Board staff.

Admission of two state banks to member-ship in the Federal Reserve System.

659 LEGAL DEVELOPMENTS

Various bank holding company, bank ser-vice corporation, and bank merger orders;and pending cases.

Ai FINANCIAL AND BUSINESS STATISTICS

A3 Domestic Financial StatisticsA44 Domestic Nonfinancial StatisticsA53 International Statistics

A69 GUIDE TO TABULAR PRESENTATION,STATISTICAL RELEASES, AND SPECIALTABLES

A74 BOARD OF GOVERNORS AND STAFF

A76 FEDERAL OPEN MARKET COMMITTEE

AND STAFF; ADVISORY COUNCILS

A78 FEDERAL RESERVE BOARDPUBLICATIONS

A81 INDEX TO STATISTICAL TABLES

A83 FEDERAL RESERVE BANKS, BRANCHES,AND OFFICES

A84 MAP OF FEDERAL RESERVE SYSTEM

Monetary Policy Report to the Congress

Report submitted to the Congress on July 21,1987, pursuant to the Full Employment and Bal-anced Growth Act of 1978.'

MONETARY POLICY AND THE ECONOMICOUTLOOK I OR 1987 AND 1988

The economy expanded at a somewhat acceler-ated pace in the first half of 1987, and the civilianunemployment rate declined over the period to6.1 percent in June, the lowest level in thisdecade. Moreover, the pattern of activity hasexhibited encouraging signs that a turnaround inthe trade sector is under way. An improvementin net exports in real terms appears to be provid-ing a lift to activity in the industrial sector,offsetting slower growth of domestic spendingand sustaining a moderate rise in overall domes-tic production. However, the process of restor-ing balance to the U.S. external accounts hasinvolved a sizable increase in the prices paid forimported goods. These price increases have oc-curred at the same time that a rebound in worldoil prices has been carrying inflation rates abovelast year's modest pace.

Although some of the elements necessary forsustaining economic growth are now beginning tofall into place, the economic outlook continues tobe clouded by a number of imbalances, risks, anduncertainties. The experience of the first halfunderscored, in particular, the dangers associ-ated with a loss of market confidence in the dollarand the related potential for a rekindling ofinflation expectations. The Federal Reserve, inimplementing monetary policy, was sensitive tothese dangers, while it continued to providesupport for sustainable economic growth. During

1. The charts to the report are available on request fromPublications Services, Board of Governors of the FederalReserve System, Washington, D.C. 20551.

the first part of the year, growth in money andcredit slowed from the rapid pace of 1986, eventhough pressures on the reserve positions ofdepository institutions remained mild. Thosepressures were increased somewhat in late Apriland May, however, as the dollar fell sharplyagainst other key currencies, inflation expecta-tions flared up, and long-term interest ratesjumped to higher levels. In response to thesesteps, and to complementary policy actionstaken abroad, the dollar has stabilized, and inter-est rates have retreated somewhat from theirMay highs.

If the nation is to achieve an orderly transitionto better external balance, one marked by aminimum of financial or inflationary pressures,responsible action by many parties—in additionto the Federal Reserve—will be necessary. Fur-ther progress in reducing our federal budgetdeficit is essential: a failure to achieve this often-stated objective could only damage confidence inour ability to deal with our economic problemsand contribute to imbalances in financial marketsand the economy. In addition, satisfactorygrowth in the other major industrial countries iscrucial, as are efforts on all sides to maintainand improve the openness of the internationalmarketplace. The private sector also mustplay a constructive role by remaining sensitiveto wage and price practices that promote theinternational competitiveness of American busi-ness.

Economic and I'inancial Background

The economic expansion has now progressedwell into its fifth year. Real gross national prod-uct rose at a AVA percent annual rate in the firstquarter. However, much of the increase in pro-duction reflected a rebuilding of business inven-tories that had been drawn down late in 1986, andreal GNP appears to have increased at an appre-ciably more moderate pace in the second quarter.

634 Federal Reserve Bulletin H August 1987

Nonetheless, growth remained strong enough tosustain a downtrend in unemployment.

Beneath these solid gains in aggregate eco-nomic activity have been welcome improve-ments in the fortunes of sectors that have failedto participate in the increasing prosperity of thepast several years. As suggested above, the mostsignificant development has been the emergingimprovement in the nation's trade performance,which has begun to close the gap between thepace of growth in the industrial sector and in therest of the economy; indeed, some segments ofmanufacturing have reached relatively high lev-els of capacity utilization and strong profitability.Economic strains also appear to be casing inother troubled sectors. Oil-well drilling, whilestill at depressed levels, has turned up as aconsequence of the firming of world oil prices.Agricultural income was quite high last year,although it continued to be heavily dependent ongovernment support; farmland values seem tohave stabilized, and the amount of delinquentfarm loans has begun to decline.

While the external sector has been strengthen-ing in real terms in recent quarters, growth indomestic demand has moderated considerably.To some extent, the slower rise in household andbusiness purchases in the early months of thisyear was a reflection of the acceleration that hadoccurred at the end of 1986, motivated by taxconsiderations. However, consumers, in partic-ular, have shown signs of less exuberance in theirexpenditure patterns after a period of severalyears in which their willingness to spend increas-ing proportions of their income provided consid-erable thrust to business activity. A moderationof domestic spending growth is, of course, afundamental ingredient in achieving better exter-nal balance without putting excessive strains onavailable resources.

A key element in the recent trade develop-ments has been the steep drop in the foreignexchange value of the dollar—almost 40 percenton a trade-weighted basis against the currenciesof the other Group of Ten countries—since early1985. That decline, in conjunction with notablerestraint on labor costs, has greatly enhanced thecompetitiveness of U.S. producers in interna-tional markets. At the same time, though, the

depreciation has caused prices of imported goodsto increase—sharply in some cases—and hasexacerbated a bulge in prices coming from higherenergy costs. The rise in consumer prices, aver-aging more than 5 percent at an annual rate overthe first five months of this year, was a disturbingdeparture from recent experience. Moreover, asthe dollar exhibited continued weakness in theearly spring, and with progress toward improve-ment in the U.S. current account slower thanmany had anticipated, concerns mounted aboutinflation prospects. This was reflected for a timein rising prices of precious metals and otheractively traded commodities, an event that onlyserved to reinforce the inflation fears that simul-taneously were unsettling U.S. securities mar-kets.

In these circumstances, and with the economicadvance evidencing reasonable momentum, theFederal Reserve in late April and May adjustedits open market operations to impose a somewhatgreater, but still quite limited, degree of pressureon the reserve positions of depository institu-tions. This step was reassuring to the markets.Coupled with complementary actions by mone-tary authorities abroad and more favorable newson prices and U.S. merchandise trade flows, thefirming of money market conditions contributednot only to a turnaround in the dollar on ex-change markets but also to a rally in bond prices.On balance, however, short-term interest ratescurrently are about Vi percentage point abovetheir levels at the time of the Board's Februarymonetary policy report to the Congress, andlong-term rates are up about a full percentagepoint.

The rate of growth of the money stock mea-sures M2 and M3 has been well below that of lastyear and close to, or below, the lower end of thetarget ranges adopted in February. This has beenviewed as acceptable by the Federal Open Mar-ket Committee (FOMC), given the inflation andexchange rate developments described above, aswell as indications of grcater-than-anticipatedstrength in the velocity of money (that is, theratio of nominal GNP to money). M2 rose at anannual rate of only 4 percent between the fourthquarter and June, appreciably below the growthrange of 5'/2 to 8'/2 percent for the year, while M3

Monetary Policy Report to the Congress 635

grew at a 5lA percent rate, a shade below thelower bound of its identical range.

The marked deceleration of monetary growth,and the accompanying rise in M2 and M3 veloc-ity after two years of decline, reflected a varietyof influences. Some unwinding of the buildup inbalances that occurred late last year in connec-tion with a huge volume of tax-related transac-tions may have been involved; tax reform alsomay have damped growth in money as individu-als reduced their additions to deposit holdingsrather than using consumer credit, on whichinterest is no longer fully tax-deductible. Capitalconstraints on the growth of bank and thriftinstitution assets may have limited the deposito-ries' efforts to seek funds, an effect likely toexpress itself most fully at the level of M3, whichencompasses a broad range of depository-insti-tution liabilities.

But it is another factor that appeared mostimportant, particularly in the case of M2.Changes in deposit rates have lagged changes inmarket rates—behavior exhibited quite consis-tently in the period since most restrictions ondeposit rates were removed. With market ratesrising, financial assets other than those includedin M2 have become relatively more attractive tothe public, the opposite of developments in 1985and 1986. This same phenomenon, reinforced bythe normal downward adjustment of compensat-ing-balance requirements as rising interest ratesenable banks to earn more on business demanddeposits, has had a marked effect on Ml growthas well, which slowed to a 10 percent annual ratebetween the fourth and second quarters (and to a7V4 percent rate between the fourth quarter andJune); M1 velocity appears to have changed littlein the second quarter, after more than two yearsof steep decline.

Reflecting in large part the diminution of thefederal deficit and a slowing in state and localgovernment borrowing, influenced by the TaxReform Act, aggregate credit expansion in theeconomy has slowed noticeably this year. Thedebt of domestic nonfinancial sectors is esti-mated to have expanded at an annual rate ofabout 93/4 percent through June, still high relativeto the growth of nominal GNP but less rapid thanin the past several years and within the monitor-

ing range of 8 to 11 percent specified by theFederal Open Market Committee.

Ranges for Monex and Credit Growth in1987 and 1988

At its meeting earlier this month, the FOMC didnot change the 1987 ranges for money and creditgrowth that it had established in February. Asindicated at that time, operating decisions willcontinue to be made not only with due regard tothe behavior of these aggregates, but also in lightof evidence on emerging trends in economicactivity and inflation and developments in do-mestic and international financial markets. Atthis juncture, given the actual growth achieved inthe first half, it seems likely that, absent majormovements in interest rates that alter the incen-tives to hold monetary assets, expansion in M2and M3 around the lower ends of their 5Vi to 81/?percent annual ranges may well be appropriate.Indeed, should the recent tendency toward astrengthening in velocity, which has been partic-ularly noticeable in the case of M2, persist, or ifinflationary pressures appear to be mounting,some shortfall from the annual ranges might wellbe appropriate. With regard to the domestic debtaggregate, the FOMC anticipated that the slowerpace of debt growth in the first half wouldcontinue and that the aggregate would end theyear well within the monitoring range of 8 to IIpercent.

Consistent with the objective of maintainingprogress over time toward general price stabilitywhile supporting sustainable growth in economicactivity, the FOMC decided to adopt on a tenta-tive basis lower growth ranges for money andcredit in 1988. The target growth ranges for M2and M3 were reduced Vi percentage point, to 5 to8 percent, measured from the fourth quarter of1987 to the fourth quarter of 1988. At the same

Ranges of growth for monetary and credit aggregatesPercent change, fourth quarter to fourth quarter

Monetary or credit aggregate

M2M3 .Credit .

1987 1988,tentative

SVi to 8I/2 5 to 851/2 to 8'/2 5 to 8

8 to II 7'/2to lOH

636 Federal Reserve Bulletin LI August 1987

time, the monitoring range for growth of nonfi-nancial sector debt also was tentatively reducedby '/: percentage point, to IV2 to IO'/J percent.

The Committee noted that M1 has continued toexhibit considerable sensitivity to changes ininterest rates, among other factors, as illustratedby its sharp deceleration in the first half of thisyear. In view of this, and the still-limited expe-rience with the behavior of deregulated transac-tions accounts, the Committee decided not to seta specific target range for M1 for the second halfof 1987, and no tentative range was adopted for1988. In its policy deliberations over the remain-der of the year, the FOMC will take account ofMl growth in light of the behavior of its velocity,incoming information about the economy andfinancial markets, and the degree of emergingprice pressures.

/Economic Projections

As noted above, the Committee believes that themonetary objectives that it has set are consistentwith restraint on inflation in the context of con-tinued moderate growth in economic activity andprogress toward a sustainable external position.As is indicated in the following table, the centraltendency of the forecasts of Committee membersand other Reserve Hank presidents is for growthin real GNP of 2Vi to 3 percent in 1987 and 1988.Between now and the end of next year, this paceof activity is expected to generate jobs in aboutsufficient number to match the expansion of thework force. Consequently, the civilian unem-ployment rate is not expected to change appre-ciably from the 6 'A percent average of the secondquarter, although recent experience suggests thatthe projected growth of real GNP might lead tosomewhat lower unemployment.

Real net exports of goods and services arcexpected to strengthen further while the growthof domestic demand remains relatively subdued.The improved competitive position of U.S. pro-ducers resulting in large part from the dollardepreciation of the past two years has only begunto be reflected in trade flows, and further im-provement in the nation's external positionshould be realized in coming quarters. House-hold spending is expected to grow slowly, butstronger increases in business investment, espc-

Heonoinie projections for IW7 andPercent

GNP or unemployment

GNP, change from fourth quarter tofourth quarter

NominalRealImplicit deflator

Civilian unemployment rate, averagelevel in the fourth quarter

GNP, change from fourth quarter tofourth quarter

NominalRealImplicit deflator

Civilian unemployment rate, averagelevel in the fourth quarter

FOMC members andother FRB Presidents

Range Centraltendency

1987

2 to VA3 to 4'/4

6'/4 to 7VA to 31<A to 4

6,1 to 6.5 6.2 to 6.4

1988

5 to 81 to 3

2'A to 5

5.9 to 6.8

5% to 7Vh to 3VA to 4'/«

6 to 6.5

1. The administration has yet to publish its midscssion budgetreview but spokesmen have indicated that earlier forecasts will berevised. As a consequence, the customary comparison of l'OMCforecasts and administration economic goals has not been included inthis report.

cially in equipment, are anticipated as industrialfirms respond to more favorable sales trends.

Prices, as measured by the implicit deflator forGNP, are expected to rise V/i to 4 percent overthe four quarters of 1987—slightly more than thecentral-tendency range reported to the Congressin February. For 1988, projections of the in-crease in the GNP deflator center on 4 percent.Assuming world oil prices are more stable, thereshould be no repetition of the rebound in domes-tic energy prices that raised the general rate ofinflation earlier this year. However, the acceler-ation in prices of non-oil imported goods that isoccurring in the wake of the decline in the foreignexchange value of the dollar likely will continuefor a time to provide some impetus to inflation,even if the dollar is more stable over the periodahead, as assumed. The size of further increasesin import prices resulting from the depreciationto date will depend on the aggressiveness withwhich foreign exporters and U.S. distributorsseek to restore profit margins that have beensqueezed in the past two years. The view thatinflation next year will not rise significantly fromthe pace projected for 1987 is grounded in a beliefthat recognition of the potential for losses of

Monetary Policy Report to the Congress 637

market share and job opportunities will continueto influence wage- and price-setting behavior.

While restraint on inflation is crucial in achiev-ing an orderly adjustment as our massive exter-nal imbalance is corrected, so too is continuedprogress in reducing the federal budget deficit.Inflows of foreign capital will shrink in step withthe reduction in our current account deficit, andin that context excessive federal borrowing re-quirements, as they put pressure on financialmarkets, pose a threat to the ability of oureconomy to fund necessary private capital for-mation.

Finally, the members of the Committee andother Reserve Bank presidents also view theprospects for a healthy U.S., and world, econ-omy as depending significantly on the avoidanceof further protectionist measures here andabroad and on satisfactory economic growth inother major industrial countries.

Tin-: PERFORMANCE OE THE ECONOMY

DURING THE /'/RSI HALF OE 1987

The economy continued to expand in the firsthalf of 1987, and, in contrast to the pattern of thepreceding four years, the composition of activityappeared to be moving toward a better balancebetween domestic spending and domestic pro-duction. The overall growth in output during thefirst six months of the year led to a net gain injobs of around 1 lA million, a faster pace of hiringthan during 1986. Moreover, the civilian unem-ployment rate, which had hovered close to 7percent throughout most of last year, moveddown to 6.1 percent by June.

Inflation picked up early this year, with mostbroad indexes of prices posting increases sub-stantially above those of the past several years.In large part, the acceleration reflected develop-ments in oil markets, where prices have retracedpart of last year's decline. But rising prices forother imported goods also began to surface at theretail level, and, at the producer level, pricespaid for raw materials and other supplies clearlyturned up. Wage trends, however, have re-mained both stable and restrained.

Higher inflation rates have been, in part, aconsequence of the ongoing adjustment of theU.S. economy to a lower foreign exchange value

of the dollar. Prices of non-oil imports, particu-larly for finished consumer goods and capitalequipment, have been rising at rates in excess ofdomestic prices in recent quarters, damping thedemand for imported goods. At the same time,goods produced in the United States have be-come more competitive in world markets. Thevolume of exports, which began to pick upnoticeably in the second half of 1986, continuedto expand in early 1987, although the reboundlikely has been limited by slow economic growthabroad.

Toward the end of 1986, some manufacturingindustries—notably those producing textiles, ap-parel, steel, chemicals, and paper—began toexperience a firming in demand apparently asso-ciated with improved trade conditions. In thefirst six months of 1987, production of officeequipment and some other high-tech capitalgoods as well as several categories of industrialmachinery also picked up. Moreover, domesticenergy output stabilized, after having been aserious drag on industrial production last year.On the whole, the pace of activity in the goods-producing sector moved back into line with theoverall rise in GNP. The index of industrialproduction increased at a 3 percent annual ratebetween the third quarter of 1986 and the secondquarter of 1987, after little change during thepreceding year.

The External Sector

The dollar depreciated further against other ma-jor currencies in the first half of 1987, with mostof the adjustment concentrated in one episodeearly in January and in another during a period ofunsettled markets in the early spring. Since mid-May, the dollar has retraced part of its recentdecline, but, on a trade-weighted basis againstother G-10 currencies, it remains about 6 percentbelow its average level in December 1986 andalmost 40 percent below its peak in February1985. The underlying downward pressure on thedollar during the first half was fueled by percep-tions that progress in reducing the U.S. currentaccount deficit had been slow and by disappoint-ment concerning prospects for policy adjust-ments, here and abroad, aimed at restoring betterbalance in the world economy. An offsetting

638 Federal Reserve Bulletin LI August 1987

factor until recently was the widening of interestrate differentials between the United States andthe other major industrial countries, as rates rosein the United States while declining abroad.

The U.S. current account deficit stood at justunder $150 billion in the first quarter of 1987,little changed, in nominal terms, from the deficitin the second half of 1986. The volume of mer-chandise imports ofgoods other than oil has beenabout flat in recent quarters, after rising steadilyfor three and one-half years. Demand has leveledoff for a wide range of imported industrial mate-rials, consumer goods, and capital equipment.This adjustment occurred, however, as dollarprices for these goods began to pick up, and thusthe value of non-oil imports has continued toedge higher. Demand for imported petroleumproducts dropped back early this year, but withworld oil prices higher, the U.S. oil import billstayed at about its 1986 level.

At the same time, the expansion in the volumeof merchandise exports that began in mid-1986extended into early 1987. The improvement inforeign sales has been broadly based; in particu-lar, shipments abroad of industrial materials andcapital goods, which account for the bulk of U.S.merchandise exports, both were up about 10percent in real terms in the first quarter from theaverage in the first half of 1986. The volume ofagricultural exports also firmed somewhat re-cently, as sharply reduced support prices appearto be combining with the lower dollar to boostforeign demand for some U.S. farm products.

The adjustment in the U.S. trade position todate has occurred without much impetus fromeconomic expansion abroad. Growth of realCiNP in other industrial countries averaged lessthan 2Vi percent last year; moreover, economicactivity began to slow in the second half of theyear, and, at least in Kurope, the weaknesscontinued into early 1987. Hxport and importvolumes in Hurope and Japan have begun toadjust to the exchange rate movements of thepast two years, cutting into the growth generatedby their external sectors. While growth in domes-tic demand has been maintained above the ratefor domestic production, it, too, has slowed andhas not taken up the slack from a weak externalsector.

Outside of the industrial countries, average

growth last year was quite uneven and, on bal-ance, provided only a limited offset to slowereconomic activity in Europe and Japan. Weak-ness in oil markets held down OPIiC growthwhile the newly industrialized countries in Asiacontinued to expand strongly. In Latin America,which is an important market for U.S exports,output rose close to 4 percent for a third year, amarked turnaround from the 1982-83 period,when the onset of external financing difficultiesseriously disrupted trade. Internal pressures tomaintain reasonably strong growth persist inthese countries; such growth could be facilitatedby an improved performance of the industrialeconomics as a group.

I he Household Sector

Consumer spending weakened considerably inthe first half of 1987, after three years in whichreal gains averaged 3V4 percent per year. Inparticular, households cut back sharply theirpurchases of durable goods and outlays for non-durables flattened out; spending for services,however, continued to trend up. Slower sales ofnew automobiles contributed importantly to theoverall deceleration in consumer spending. Dur-ing the first half, sales of new cars averaged 10million units at an annual rate, down from arecord 11 '/> million units in 1986. The slackeningin demand was most noticeable for domesticmakes and persisted despite the continuation ofspecial incentive programs on a wide range ofmodels.

The deceleration in consumer outlays, espe-cially for durables such as motor vehicles, furni-ture, and home appliances, followed a period ofseveral years during which a variety of factorswere working to encourage households to in-crease their holdings of big-ticket items: rela-tively moderate increases, or even decreases, inthe prices of many home goods; declines ininterest rates; and pent-up demands from theperiod of economic weakness in the early 1980s.As those influences dissipated, and with thepersonal saving rate reaching an historically lowlevel by late 1986, consumers apparently becamemore cautious in their buying patterns. Nonethe-less, survey evidence still suggested that house-

Monetary Policy Report to the Congress 639

holds' evaluations of market conditions for majorpurchases and of their personal finances re-mained generally positive.

During the first five months of 1987, growth innominal disposable income picked up from its1986 pace; but, with consumer prices rising morerapidly, income growth in real terms was littledifferent from the 2 percent pace of the precedingtwo years. However, the aggregate balance sheetof the household sector showed further improve-ment early this year. Asset holdings were bol-stered especially by gains in stock prices, whiledebt accumulation slowed. Growth of mortgagedebt dropped back from the extraordinary paceof late 1986 despite the popularity of home equityloans, and growth of consumer credit droppedsharply. To some extent, the deceleration inconsumer debt, as well as the slowdown inspending on durable goods, may be a conse-quence of the rapid rise in household debt bur-dens during the past several years. In addition,the new tax law diminished the incentive tofinance expenditures with installment credit. De-spite the slower growth of consumer and mort-gage debt, some indicators suggest that a consid-erable number of households still are havingproblems servicing existing liabilities. Althoughsome loan delinquency rates dropped a bit,others rose in the first quarter, as did personalbankruptcies.

Spurred by a decline in mortgage interestrates, which reached a nine-year low at the endof March, starts of new single-family homesaveraged 1 'A million units at an annual rate fromJanuary through April, the highest level since thelate 1970s. Sales of single-family homes, whichhad been boosted by tax considerations at theend of 1986, also remained brisk through April.Subsequently, the backup in mortgage rates toearly-1986 levels resulted in some reduction insingle-family homebuilding, to around the pacethat prevailed last fall. In the multifamily market,the downtrend in activity that began in early 1986continued through the first half of 1987. In thesecond quarter, multifamily starts were one-thirdbelow last year's peak. Despite the adjustmentthus far to overbuilding and the reduced after-taxprofitability of multifamily housing investment,rental vacancy rates nationwide are still close torecord highs.

The Business Sector

Business spending on plant and equipment fellsharply in the first quarter of 1987. For equip-ment, the weakness was concentrated in Januaryand followed a tax-induced bunching of pur-chases in late 1986. In subsequent months, ship-ments of nondefense capital goods recovered,leaving the average level for April and May, innominal terms, IV4 percent above the third quar-ter of last year. New orders for nondefensecapital goods also dipped at the beginning of theyear, but then strengthened noticeably as book-ings for aircraft and for office and computingequipment rose sharply. The recent level oforders appears consistent with a continuation inthe near term of the moderate uptrend in spend-ing on equipment that has prevailed over the pasttwo years. According to responses to privatesurveys concerning business capital spendingplans for the year as a whole, firms still intend todirect the bulk of these purchases toward mod-ernization and cost-saving improvements in theirproduction lines.

In contrast, the environment for expansion ofplant facilities and office space is still generallyunfavorable. Large amounts of vacant and under-used space in both office buildings and factoriesbegan to take a toll of nonresidential constructionlast year; and less favorable treatment of com-mercial structures under the new tax code rein-forced the tendencies toward a lower level ofactivity in this sector. As a result, spending forcommercial and industrial buildings dropped fur-ther in the first quarter of 1987, to a level about 20percent below that of a year earlier. The declinein spending for these types of buildings ac-counted for the overall weakness in nonresiden-tial structures early this year, in the face of anupturn in oil drilling and some increases in othercategories.

A sizable swing in business inventories aroundthe turn of this year was associated with sharp,tax-induced fluctuations in sales. The surge inconsumer and business spending at the end of1986 was met to a considerable extent by drawingdown stocks, which were then rebuilt at thebeginning of this year. This spring, inventory-sales ratios generally were not indicating seriousimbalances, with the notable exception of the

640 Federal Reserve Bulletin I J August 1987

auto industry. Domestic car makers boosted pro-duction in early 1987 in excess of slackeningsales, leading to a substantial backlog of unsoldcars on dealer lots. My June, a scaling back ofassemblies had stemmed further accumulation,but the industry entered the summer with stocksthat were quite large by historical standards.

Hcfore-tax profits of nonfinancial corpora-tions, which had slipped a bit relative to GNPsince 1984, rose in the first quarter. After-taxprofits relative to GNI' were up as well, althoughthe rise was damped by increases in corporatetax liabilities associated with the new tax law.Corporations paid out a slightly larger share ofearnings as dividends in the first quarter; none-theless, internally generated funds remained siz-able relative to investment outlays.

The (iovcninwnl Sector

A substantial reduction in the federal budgetdeficit for fiscal year 1987 appears in train, withthe most recent estimate from the CongressionalBudget Office at $161 billion, compared with $221billion in fiscal 1986. Growth in receipts has beenextremely rapid; this reflects, in large part, aone-time surge in tax payments this April fromindividuals who realized capital gains last De-cember, taking advantage of lower tax ratesunder the old tax code. But more fundamentalprogress in reducing spending growth also ap-pears to have been made in the wake of theGramm-Rudman-Hollings legislation. Total out-lays have been rising al a rate of around 2 percentin the current fiscal year, a marked slowing from8 percent per year during the preceding fiveyears. Although entitlements spending is stillincreasing steadily, agricultural support pay-ments and interest outlays have leveled off.Moreover, military spending has begun to re-spond to reductions in defense authorizationsand has slowed to about half its 1986 rate ofincrease. In addition, there has been continuedbudgetary restraint on discretionary domesticprograms. On balance, these developments haveheld down the growth of federal purchases,which account for about a third of total federalexpenditures; excluding changes in farm inven-tories held by the Commodity Credit Corpora-

tion, real federal purchases were little changedbetween the second quarter of 1986 and the firstquarter of this year.

Real purchases of goods and services by stateand local governments rose at a 4 percent annualrate in the first quarter of 1987, close to the briskpace of the past several years. The growth inoutlays continues to be boosted by efforts toupgrade basic infrastructures. This rise in spend-ing has outpaced growth in receipts, however,and the sector's combined operating and capitalaccounts (that is, excluding social insurancefunds) moved into deficit in the first quarter ofthis year. In many instances, a current deficitdocs not signal any fundamental financial prob-lem, as capital expenditures are financed throughbond issues. Nonetheless, a good many units areexperiencing a degree of difficulty, with oil-pro-ducing states under the most stress. Many statesare responding with plans to trim their generalfunds budgets; some arc considering tax in-creases or are planning to retain the extra re-ceipts generated by changes in federal tax laws.

Labor Markets

Employment accelerated early in 1987, and, de-spite a slowing in recent months, the averagemonthly increase in nonfarm payroll employmentof just over 200,000 so far this year exceeds thepace of hiring in 1986. The improvement in labordemand has been fairly broadly based. In manu-facturing, a two-year string of cutbacks in dura-ble goods industries ended late last year, andhiring picked up a bit in the nondurable goodssector. As a result, factory employment, overall,edged higher over the first six months of 1987. Inaddition, the number of jobs in oil and gasextraction stabilized after the sharp retrench-ment in 1986. At the same time, the expansion ofjobs in the trade, services, and finance industries,despite some recent slowing, remained sizable.

The combination of strong gains in employ-ment and declining numbers of unemployedworkers over the first half lowered the civilianjobless rate to 6'/4 percent on average in thesecond quarter from just under 7 percent at theend of last year. The rate for adult men (aged 25years and over), which had been stuck at around

Monetary Policy Report to the Congress 641

5'/> percent from mid-1984 to late 1986, movedbelow 5 percent this spring; further improvementalso occurred for adult women, whose unem-ployment rate in the past year has moved belowthat of their male counterparts.

Despite falling unemployment, available mea-sures of labor compensation showed little sign ofacceleration early this year. Hourly compensa-tion, as measured by the employment cost index,rose 3.1 percent in the 12 months ending inMarch, the same as the year-ovcr-year changesin the second half of 1986 and down nearlythree-quarters of a percentage point from a yearearlier. A wide gap persisted between the size ofpay increases for white-collar workers and forthose in blue-collar occupations. Nonetheless,the slowing in wage inflation compared with ayear earlier was relatively widespread by indus-try and occupational group. An exception is theNortheast region, where wages showed no decel-eration in the year ending in March and increaseswere still outpacing those in other parts of thecountry by a sizable margin.

The moderation in hourly compensation in-creases has been the principal factor holdingdown labor costs, as productivity continues to bequite sluggish. After declining in the second halfof 1986, output per hour in the nonfarm businesssector rebounded in the first quarter of 1987, butremained little different from its year-earlierlevel. Since 1984, productivity gains in the non-farm business sector have averaged less than Ipercent per year. The trend has been much morefavorable in the manufacturing sector, wherefirms apparently have had some success in theirefforts to boost the efficiency of their productionprocesses; indeed, productivity gains in U.S.manufacturing between 1985 and 1986 out-stripped those recorded by other major industrialcountries.

Price De veto pin ents

As expected, inflation rates have been higher sofar this year, largely reflecting a rebound inenergy prices. The GNP fixed-weight price in-dex, a broad measure of inflation for goods andservices produced by the United States, in-creased at an annual rate of about 4 percent in the

first quarter; it had risen 21/? percent during 1986.Sharper accelerations occurred in the consumerprice index, which was up at a 5'/» percent rateover the first five months of the year, and in theproducer price index for finished goods, whichrose at a 4'/2 percent annual rate over the sixmonths ended in June.

The rebound in energy prices began in Janu-ary, when spot prices of crude oil jumped about$3 per barrel in response to the reductions inoutput to which OPEC had agreed late in Decem-ber. Higher crude oil costs were quickly passedon to end-users, and by May consumer prices forgasoline and fuel oil had risen about 15 percent,retracing half of last year's decline. Spot pricesof petroleum products moved up a bit furtherearly in the summer as inventories tightened, andthese increases were supported subsequently bythe renewal of OPEC's agreement to controlproduction.

In addition to the developments in energymarkets, the influence of a lower value of thedollar, as well as trade restrictions, on the pricesof imported goods became increasingly evidentat the retail level in the first part of this year. Thedockside prices of non-oil imports turned up in1986 after several years in which stable or declin-ing import prices had helped to restrain domesticinflation. Although price changes have variedconsiderably among different categories of im-ported goods, some of the largest increases havebeen reported for consumer commodities, in-cluding autos. Retail prices for a number of itemswith higher-than-average import proportions—such as apparel, footwear, and some other homegoods—have shown markedly faster increasesthan they did during the past several years.These increases contributed to a sharp accelera-tion in the consumer price index for goods otherthan food and energy between December andMay compared with 1986, while the rise in pricesof nonenergy services over the same period wasslightly less rapid than last year.

At the domestic producer level, prices of fin-ished consumer goods and capital equipmentother than food and energy rose at an annual rateof less than 2 percent over the first six months ofthe year. At earlier stages of processing, how-ever, prices of domestically produced intermedi-ate materials other than food and energy rose at

642 Federal Reserve Bulletin U August 1987

a 4 percent annual rate, after two years ofessentially no change. This acceleration reflecteda sharp rise in the prices of industrial chemicalsand some other petroleum-related materials aswell as increases in a number of other categories.

Prices of primary commodities other than pe-troleum also have increased so far in 1987. In theagricultural sector, crop prices have retracedpart of last year's decline, which occurred whenfarmers sold large amounts of the grain they hadreceived from the government in lieu of cashpayments. Prices of cattle and hogs also were upmarkedly into the spring, but, with suppliesimproving, cattle prices have retraced much oftheir advance, and hog futures prices point todeclines later this year. Prices of industrial ma-terials, with the exception of a brief period earlythis year, have been rising fairly steadily sincethe early autumn of 1986. Spot prices for pre-cious metals have been particularly sensitive todevelopments in foreign exchange markets andrenewed market concerns about inflation; afterclimbing sharply into May, they fell back a bitwith the subsequent firming of the dollar.

M ONE LAKY POLICY AND I-'INANCIM.MARKETS IN THE FIRST HALE OE I9H7

The Federal Open Market Committee at its meet-ing in February established 1987 target ranges,measured from the fourth quarter of 1986 to thefourth quarter of 1987, of 51/: to Wi percent forboth M2 and M3. It also set a 1987 monitoringrange for domestic nonfinancial debt of 8 to 11percent. The M2 and M3 ranges represented areduction of Vz percentage point from last year'starget ranges, and the Committee expectedgrowth to be well within the ranges, especially inthe absence of dramatic movements in interestrates. The range for debt was unchanged from1986 but below the actual outcome in that yearand other recent years; thus, the Committeeanticipated that debt growth also would slow thisyear.

The Committee viewed a substantial slowing inmoney and credit growth from the rapid pace of1986 as likely to be consistent with continuationof sustainable economic expansion and condu-cive to further progress over time toward reason-

able price stability. Growth of Ml also wasexpected to moderate considerably this year.However, the Committee in February elected notto set a target range for Ml for 1987 because ofthe continuing uncertainties about the relation-ship of this aggregate to the economy. Theseuncertainties partly reflected the substantial sen-sitivity of its velocity to changes in financialconditions that had been evident in recent years,capped by a record postwar decline in the veloc-ity of Ml over 1986. Instead, the FOMC decidedto continue evaluating movements in this aggre-gate in light of the behavior of its velocity, therate of economic expansion, inflationary pres-sures, and developments in financial markets.

Over the first half of 1987, monetary policywas conducted against a backdrop of heightenedconcerns about inflation, stimulated in part bysubstantial downward pressure on the dollar inforeign exchange markets. At the same time,growth of money and credit aggregates moder-ated considerably and the velocities of thebroader monetary aggregates turned upward af-ter several years of rapid money growth andfalling velocities. Measured from the fourth quar-ter of 1986, M2 in June was below the lower endof its target growth range, while M3 was aroundthe lower end of its range. Meanwhile, growth inM1 slowed to a VA percent pace and debt expan-sion moderated to a 914 percent rate. As pres-sures on the dollar and inflation worries intensi-fied in April and May, interest rates began to risesubstantially, especially in long-term markets. Inlate April and May, the Federal Reserve adopteda somewhat less accommodative stance withrespect to the provision of reserves through openmarket operations. These actions, together withmonetary easing moves by key industrial tradingpartners, helped to stabilize the dollar and calminflation fears, contributing to some decline inlong-term interest rates and strengthening of thedollar.

Money, Credit, and Monetary Policy

In its conduct of policy thus far this year, theFederal Reserve has given a good deal of weightto a number of considerations in addition to themonetary aggregates—principally recurrent epi-

Monetary Policy Report to the Congress 643

Growth of money and creditPercentage changes at annual rates

Period

Fourth quarter to fourth quarter197919801981198219831984 . '.19851986

Fourth quarter 1986 to June 1987

Quarterly average1986:1

234

1987:12

Ml

7.97.35.1(2.4)'8.6

10.25.4

12.115.3

9.9

7.7

8.815.516.517.013.16.4

M2

8.28.99.39.1

12.17.98.88.9

4.5

4.0

5.39,4

10.69.26.32.5

M3

10.49.6

12.39.99.8

10.77.78.8

5.3

5.3

7.7879.78.06.34.1

Domesticnonfinancialsector debt

12.29.69.98.9

11.513.913.413.2

9.8'

9.8'

15.510 212.512.110.49.0'

1. Ml figure in parentheses is adjusted for shifts to NOW accountsin 1981.

sodes of heavy downward pressure on the dollar,indications from long-term securities and com-modity markets of heightened inflation expecta-tions, and evidence that the economy continuedto advance at a pace sufficient to produce risinglevels of resource utilization, Under these cir-cumstances, interest rates tended to movehigher, and the patterns of rapid money growthand declining velocities of the last several years,when inflation and interest rates were movingdown, began to be reversed. Growth of the broadaggregates remained around the lower bounds oftheir growth cones through most of the first halfof the year, although M2 dropped well below itslong-run range later in the period. Growth of bothM2 and M3 was considerably below the pace ofrecent years, and their velocities increased. Ex-pansion of Ml also slowed markedly, whilegrowth of domestic nonfinancial sector debtmoderated.

Through the early spring of this year, Systemopen market operations were conducted to keeppressures on the reserve positions of depositoryinstitutions unchanged from last year. In Janu-ary, the strong credit and money demands asso-ciated with a burst of tax-related financial activ-ity in late 1986 began to abate, and short-terminterest rates eased; however, these rates re-mained above levels prevailing in the fall of lastyear.

e estimated

In foreign exchange markets, the dollar hadbegun to decline in late December, after a periodof some stability. The drop continued throughJanuary, amid market concerns about the pros-pects for correcting U.S. and foreign externalimbalances. In late February, the statement inParis by the ministers of finance and central bankgovernors of six major industrial countries thatthey "agreed to cooperate closely to foster sta-bility of exchange rates around current levels,"along with a cut in the discount rate by the Bankof Japan, seemed to stabilize the dollar for atime.

The spread between private short-term ratesand Treasury bill rates widened after Brazil an-nounced a suspension of interest payments tobanks in February, and subsequently widenedfurther as the Treasury's paydown of bills, whichbegan early in the year, picked up and foreignofficial institutions purchased bills with the pro-ceeds of dollars acquired in exchange marketintervention. Reflecting the somewhat higher pri-vate short-term interest rates and concomitantincreases in funding costs, commercial banksraised the prime rate by VA percentage point onApril 1.

Long-term rates, which had not been muchaffected by the transitory credit demands of late1986, continued to drift down in the early monthsof 1987, displaying little short-term volatility.

644 Federal Reserve Bulletin LI August 1987

The placid conditions in long-term markets wereabruptly changed in late March, primarily bydevelopments in the international sphere. An-nouncements of trade sanctions by the UnitedStates, persisting weakness of the dollar, anddisappointing trade figures all raised questionsabout continuing private demands for dollar as-sets, prospects for inflation, and the response ofmonetary policy. The dollar dropped sharply inthe last three weeks of March, and between lateMarch and late April, yields on 30-year govern-ment bonds rose about I percentage point onbalance. The exchange and bond markets be-came highly volatile during this period, as thedollar continued to drop and inflation fears ap-peared to be intensified by the publication ofadverse price data. Mortgage rates and yields onmortgage pass-through securities reacted verypromptly to the deterioration in the bond marketsand, indeed, rose more than most other long-term rates as many investors shied away fromthese instruments subject to substantial prepay-ment risk.

The effects of these developments also wereevident in short-term credit markets, where ratesrose in April partly in anticipation that monetarypolicy would have to firm to contain pressures onprices and the dollar. In late April and again inMay, the Federal Reserve did move to tightenthe availability of nonborrowed reserves throughopen market operations. Short-term interestrates rose about Vz to V* percentage point duringApril and May, and the prime rate was raisedtwice more, on May 1 and May 15, in quarter-point increments. The System's firming actions,along with complementary moves abroad, helpedto stabilize the dollar and ameliorate the con-cerns about the inflation outlook.

Along with some better price news and evi-dence of improvement in our trade deficit, thispolicy appeared to impart an improved tone toshort-term and, especially, long-term credit mar-kets over the latter part of May and June. SinceMay, most short-term rates have posted declinesof VA percentage point or more. Longer-term mar-kets generally have registered greater gains, andin early July long rates were off Vi to VA percentagepoint from their May highs. The dollar, mean-while, has shown more dramatic improvement,regaining the ground it lost in April and May.

As interest rate incentives favoring market

instruments over monetary assets became morepronounced in the first half of the year, growth ofthe monetary aggregates slowed. M2 deceleratedin both quarters, expanding at an annual rate ofonly 2'/2 percent in the March-to-Junc period. Inaddition to the influence of rising interest rates,tax reform may have weakened the public'sdemand for M2 assets, particularly household-type deposits, to the extent that it induced indi-viduals to pay down consumer debt or to financeexpenditures out of liquid assets rather than withcredit. The velocity of M2 is estimated to haverisen in the first and second quarters, after de-clining in 1985 and 1986.

The slowing of M2 growth was accompaniedby a marked change in the composition of depositinflows away from transactions and other highlyliquid instruments and toward longer-term retaildeposits. This reversal of the pattern of portfolioshifts in 1985 and 1986 occurred as rates on timedeposits adjusted more promptly to rising marketrales than did yields on more liquid monetarycomponents, and the deposit rate curve steep-ened.

Growth in transactions instruments fell in thefirst half to a pace not seen since 1984, the lasttime interest rates rose on a sustained basis.Demand deposits, along with other checkabledeposits (OCDs), were boosted smartly in Aprilas individuals prepared to pay tax liabilities,which were swollen by capital gains taken in 1986to avoid higher rates under tax reform. On bal-ance, however, demand deposits have exhibitedno sustained strength since late last summer.Among other factors, the rise in interest ratesreduced the volume of demand deposits thatbusinesses need to hold as compensating bal-ances for bank services. As rates on time depos-its and market instruments rose, OCDs became aless attractive savings vehicle. The progressiveslowing this year of OCD growth, which hadaveraged close to 30 percent during most of1986, was interrupted only by the April surge.With demand deposits and OCDs both runningoff in June, growth in Ml for the second quarterwas down to a 6V2 percent rate. The velocity ofM1 in the second quarter is estimated to havechanged little, after declining in each quartersince 1984.

Growth in other liquid balances also has beenfalling. Savings deposits, after expanding at a

Monetary Policy Report to the Congress 645

rate of around 30 percent since the late summerof last year, slowed in the second quarter andadvanced at a rate of only 10 percent in June, andmoney market deposit accounts have been par-ticularly weak this year. By contrast, small timedeposits, which had run off over much of lastyear in an environment of falling short-termrates, expanded significantly in June for the firsttime since April 1986. Growth in small timedeposits this year has been especially strong atthrift institutions, reflecting elevated offeringrates and, in certain cases, a shift to deposits indenominations of under $100,000, as some ofthese institutions have encountered difficulties inissuing large time deposits.

Even with weak inflows to core deposits, theneed among commercial banks to tap wholesalemanaged liabilities was limited by a moderationin demands for credit. M3 growth was furtherdamped in the first half as banks obtained fundsfrom sources not encompassed by the monetaryaggregates, including borrowing from their for-eign branches and a sharp rise in Treasury de-posits. Federal Home Loan Bank advances tothrifts also were strong, although below the paceof last year. Growth of M3 fell below that ofincome in the first half, and M3 velocity appar-ently rose in both quarters, the first sustainedincrease in three years.

Credit flows were reduced in the first half of1987, with total domestic nonfinancial sectordebt expanding at an annual rate of around 9-V4percent, compared with rates in excess of 13percent in each of the preceding three years.Even so, expansion of both the private andpublic components of the debt aggregate contin-ued to outstrip the growth of income, as gener-ally has been the case in the 1980s.

Overall business credit demands continued tobe buoyed in the first half by heavy net retire-ments of shares associated with mergers, buy-outs, and other corporate restructurings. Withlong-term rates subdued in the first three monthsof the year, firms concentrated their borrowingsin bond markets and short-term business creditcontracted. However, as long-term markets de-teriorated in April, bond issuance abated andbusiness credit demands focused on the commer-cial paper market. By June, with some improve-ment in long-term markets, these financing pat-terns reversed again as bond issuance picked up

and growth of short-term business credit came toa halt.

Growth of consumer installment credit wasconsiderably diminished during the first half. Thereduced deductibility of consumer interest pay-ments under the new tax code encouraged thisdevelopment. The tax law change made the useof mortgage credit relatively more attractive, andthe active promotion by lenders of home equitylines of credit reinforced tendencies toward sub-stitution. In addition to credit taken down underhome equity lines, mortgage growth in the firsthalf was maintained by heavy volumes of newand existing home sales.

Federal government credit needs in the firsthalf were held down by unusually strong taxpayments stemming from the retroactive repealof the investment tax credit and, principally,from the capital gains realized late last year. Thebudget showed a small surplus in the April-to-June period, after a $59 billion deficit in the firstquarter. Net borrowing from the public neverthe-less rose in the second quarter on a seasonallyadjusted basis as the Treasury replenished itscash balances, which had been drawn downsharply in the initial months of the year. TheTreasury ran off bills in both quarters but contin-ued to issue coupon securities in volume. Federaldebt expanded at a 93/t percent annual rate inthe first half of the year, down from the pace of1986.

Borrowing by state and local governments hasfallen off this year. Issuance of municipal debt fornew capital has been slowed considerably byprovisions of tax reform that narrowed the defi-nition of public-purpose debt and constrainedprivate-purpose offerings. In addition, issuanceof refunding bonds, which was strong in the firstquarter, slackened after April because of higherinterest rates.

The financial system has continued to evidencestrains in 1987. Indications that the agriculturalsector is beginning to stabilize have emerged,with loan delinquencies declining, land pricesbottoming out, and export volume firming; thefailure rate among agricultural banks seemslikely to have peaked. However, the Farm CreditSystem, the nation's largest farm lender, lostconsiderable sums in 1985 and 1986, and many ofits units continue to struggle with troubled loanportfolios.

646 Federal Reserve Bulletin D August 1987

In addition to difficulties with agriculturalloans, commercial banks have been saddled withpersisting problems in their energy and dcvclop-ing-country loan portfolios. Although somebanks remain highly profitable, 19 percent lostmoney last year, compared with about 3 percentas the decade began; loan-loss provisions werethe main cause of the earnings problems. Thebanking system is likely to post record losses thisyear owing to huge reserve provisions taken bylarge banks primarily as a consequence of devel-opments in the international debt area. Despitethe shrinkage in the book value of shareholderequity recognized by these actions, share pricesrose at many banks that announced large in-creases in loan-loss reserves.

Net operating income before taxes for solventthrift institutions rose last year as interest mar-gins widened with falling market rates, and thriftsoverall have raised their ratio of net worth tototal assets by taking advantage of strong stockprices to issue large volumes of equity. Nonethe-less, at a significant minority of thrifts, alreadynegative net worth positions have been aggra-

vated by continued losses. Moreover, the prob-lems of some troubled institutions intensified thisyear as the real estate market in certain areas ofthe country remained depressed and interestrates backed up.

The difficulties of the thrift industry are mir-rored in the situation of the Federal Savings andLoan Insurance Corporation. Fstimatcs indicatethat current and potential claims against theFSLIC exceed its reserves by significantamounts. With premiums levied on member in-stitutions already at a statutory maximum, someaction clearly is called for to strengthen theFSLIC and bolster its ability to deal with prob-lem institutions. Plans currently under study bythe Congress would involve using retained earn-ings from the Federal Home Loan Banks tocapitalize a financing corporation that, in turn,would issue obligations and invest the proceedsin FSLIC capital stock. At this stage, these planscall for a maximum capacity to issue debt of $8'/2billion. This would be repaid over an extendedperiod of time through FSLIC assessments onmember institutions.

Industrial Production

647

Released for publication June 16

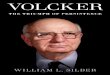

Industrial production increased an estimated 0.5percent in May, while the level of output in eachof the preceding three months was revised up-ward. In May, gains in output were widespreadamong products and materials. At 127.8 percentof the 1977 average, the total index for May was2.9 percent higher than that of a year earlier.

In market groups, output of consumer goodsincreased 0.6 percent in May following a declineof 0.8 percent in April. Auto production was offslightly in May, but output of lightweight trucksas well as that of home goods and nondurableconsumer goods increased during the month.Auto assemblies were trimmed further in May toan annual rate of 7.1 million units, but stillexceeded sales for May; industry schedules for

140

120

100

80

60

TOTAL INDEX

1 1

MANUFACTURING

"~ CONSUMER GOODS

1

MOTOR VEHICLES

—

A A/1 (

r—' "

I i

Durable ^ _ ^ ^ _

Nondurable

1 1

Nondurable^_ >~~r-*

• / - . ^ ^ _ - . ~ - •ry~

Durable

AND PARTS

-

1

-

1

-

•

-

-

-

Ratio scale, 1977 = 100

140

120

- 100

80

140

120

- 100

1981 1983 1985 1987

All data are seasonally adjusted. Latest figures: May.

- 160

- 140

120

100

- 80

Products

MATERIALS Durable

Nondurable -^^r • -

Energy

INTERMEDIATE PRODUCTS

Business supplies

— Construction supplies

J_

FINAL PRODUCTS

Defense and space

Consumer goods

240

200

160

140

20

100

1981 1983 1985 1987

648

Group

Total industrial production

Products, totalFinal products

Consumer goodsDurableNondurable

Business equipmentDefense and space

Intermediate productsConstruction supplies

Materials

Manufacturing.DurableNondurable .

MiningUtilities

1977 = 100

1987

Apr. May

127.2

135.6134.4126.6118.4129.6140.4186.5140.0127.9115.6

132.0129.8135.196.5

110.4

127.8

136.5135.2127.4119.4130.3141.2187.4140.7128.6116.0

132.7130.4135.996.3

111.9

Jan.

-.1.0

- . 4- 1 . 2- . 1

.7- . 3- . 4

3.0

.1- . 1

.35

-1.0

Percentage change from preceding month

1987

Feb. Mar.

Major market groups

.91.0.6

2.0.2

1.9.7.4.1.0

.0

.1

.0

.0- . 6

.3- . 1

.0

.3.1

- . 1

Major industry groups

.71.1.1

-1 .0.1

.1

.1

.2

.2- . 3

Apr.

- . 1

- . 4- . 5- . 8

- 2.6

- ! l- . 1- . 1- . 5

.4

- . 2- . 6

.4

.11.1

May

.6

.6

.6

.8

.6

.5

.5

.5.5.4

.5

.5

.6- . 21.4

Percentagechange,

May 1986to May

1987

2.9

3.12.82.54.91.72.45.34.24.22.7

3.5274.6

-3.53.1

Noli;. Indexes are seasonally adjusted.

June production show a further small decline.Production of business equipment was up inMay, continuing the overall improvement thatbegan in January, particularly in the output ofmanufacturing and commercial equipment.

After almost no change in both March andApril, output of defense equipment increased inMay, bringing production to a level about 5percent higher than that of a year earlier. Output

Total industrial production—RevisionsEstimates as shown last month and current estimates

Month

FebruaryMarch

May

Index (1977-1(1(1)

Previous

127.1126.8126.3ii.a.

Current

127.2127.3127.2127.8

Percentage changefrom previous

months

Previous Current

.4 .5-.2 .0-.4 -.1

n.a. .5

n.a.—Not applicable.

of both construction and business supplies in-creased half a percent in May but has shown, onbalance, only small gains since the beginning ofthe year. Total materials production rose 0.4percent following a similar gain (upward revised)in April. Among durable materials, output ofmetals and equipment parts increased in May;nondurable materials, such as chemicals andpaper, also rose. Output of energy materials,although relatively strong in May due largely toincreased electricity generation, remained belowyear-earlier levels.

In industry groups, total manufacturing outputincreased 0.5 percent in May following a declineof 0.2 percent in April, which occurred mainly indurables. In May, the durable manufacturingsector almost regained March levels; nondurablemanufacturing, with a gain of 0.6 percent in Mayfollowing a revised rise of 0.4 percent in April,surpassed the March level considerably. Miningoutput edged down in May, but production byutilities was up sharply.

649

Statement to Congress

Statement by Manuel H. Johnson, Vice Chair-man, Board of Governors of the Federal ReserveSystem, before the Subcommittee on FinancialInstitutions Supervision, Regulation and Insur-ance of the Committee on Banking, Finance andUrban Affairs, U.S. House of Representatives,June 9, 1987.

I am pleased to appear on behalf of the FederalReserve Board to offer additional testimony onthe issue of money laundering. The FederalReserve has a strong commitment to implement-ing appropriate policies to ensure compliancewith laws enacted to eliminate money launder-ing.

My goal today is to more fully inform thecommittee of efforts by myself and by the staff topress for greater international cooperation bybank supervisors in addressing the use of bank-ing organizations to launder money. In addition,the committee has asked that I give a statusreport on the studies required under the Anti-Drug Abuse Act of 1986 and that I address thesubject of bank fraud and insider dealing. Final-ly, I will provide further information on theFederal Reserve's supervisory efforts to ensurecompliance with the Bank Secrecy Act and otherlaws to discourage the use of banks and thepayments system generally for laundering mon-ey.

INTERNATIONAL COOPERATION

The Federal Reserve shares the concerns of thiscommittee and believes that the effectiveness ofefforts to discourage money laundering could befurther enhanced by initiatives on an internation-al level. For the past year, the Federal Reserve,together with the other federal banking agencies,has worked to secure the cooperation of banksupervisory authorities in other countries of theworld. Discussions have been held among mem-bers of the Basle Committee on Bank Regulation

and Supervisory Practices with the goal of ob-taining a consensus on how best to proceed withefforts to discourage criminal elements from us-ing the international payments system for thepurpose of laundering money.1 The subject wasfirst raised with the Basle Committee in a meet-ing in Washington last June. Although all mem-bers of the committee were clear in their viewthat abuse of the banking system in the form ofcurrency laundering was a serious matter, manymembers felt that the primary responsibility formonitoring and detecting this activity restedlargely with law enforcement authorities. None-theless, the committee agreed that the subjectshould be reviewed, and at the December 1986meeting the U.S. delegation agreed to draft apaper outlining the issue and making recommen-dations.

In addition, this paper will propose rules ofconduct that could be utilized by banks in anycountry to discourage the use of the paymentssystem for illegal transactions. In constructingthis proposal, we have consulted with othercountries for the purpose of incorporating theirideas as well as seeking their support of a moreactive role for bank supervisors. We expect thatin the next few weeks a draft of an initialproposal will be ready for review by the BasleCommittee, and we are attempting to put theitem on the committee agenda for the regularmeeting later this month. We recognize thatencouraging foreign supervisors to endorse theconcept that international banks should adopt acode of conduct falls short of the extensivecurrency reporting requirements in place in theUnited States; however, we are hopeful that this

1. The Basle Committee was established at the end of 1974by the central bank governors of the Group of Ten industra-lized countries with the objective of strengthening collabora-tion among national authorities in their prudential supervisionof international banking. The committee, whose members areofficials of the central banks and supervisory agencies, meetsthree times a year at the Bank for International Settlements inBasle, Switzerland.

650 Federal Reserve Bulletin • August 1987

effort, in combination with the activities of ourfederal law enforcement authorities, will make ameaningful contribution toward inhibiting theuse of the banking system for illicit money laun-dering.

Attempts to eliminate money launderingthrough legislation are, of course, not confined tothe United States. Recently, Switzerland, forexample, has proposed laws designed to makemoney laundering a crime. It is our hope thatother countries will follow suit. The proposedrules of conduct to which I have just referredendorse the concept that bank supervisory au-thorities should support legislation that wouldmake money laundering a crime.

Federal Reserve efforts to encourage interna-tional cooperation in this area will not be limitedto the Basle Committee. We intend to discussthis issue when appropriate at formal and infor-mal meetings with foreign bank supervisory au-thorities. It is our hope, however, that the workgoing on in the Basle Supervisors' Committeewill serve as the principal vehicle for advancingeffective constraints on the involvement of inter-national banking institutions in money launder-ing activities.

INTERNATIONAL STUDIES

The Anti-Drug Abuse Act of 1986 requires thattwo studies be conducted and furnished to thiscommittee. Both of these studies are being pre-pared under the auspices of the Department ofthe Treasury in consultation with the Board ofGovernors. The Justice Department is also tocontribute to one of the studies.

The first study deals with the results of discus-sions with central banks and other appropriategovernmental authorities concerning the estab-lishment of arrangements to facilitate the flow ofinformation among supervisory authoritiesthroughout the world. The flow of informationamong international supervisors is particularlyimportant, and the Federal Reserve is discussingwith international authorities the need to im-prove communications and information-sharingprocedures to strengthen supervisory activitiesvis-a-vis international banking organizations. Weexpect to be able to provide the Treasury withthe results of our discussions in sufficient time toensure a timely response to this committee.

The other study requires that information befurnished to this committee on the following: (1)the extent to which foreign branches of domesticinstitutions are used to facilitate illicit transfersof currency and other monetary instruments orto evade reporting requirements; (2) the extent towhich U.S. law is applicable to the activities ofsuch foreign branches; and (3) methods for ob-taining the cooperation of foreign countries forthe purpose of enforcing money laundering lawsand currency reporting requirements. The Feder-al Reserve and the Comptroller of the Currencywere asked to assist the Treasury on sections 2and 3 of the study. While we arc still in theprocess of developing materials to provide to theTreasury, we expect that the study will be com-pleted within the committee's requested timeframe.

BANK FRAUD AND INSIDER DEAEING

I would now like to turn to the subject of bankfraud and insider dealings. Experience has dem-onstrated that insider abuse and misconduct, aswell as criminal activities, arc among the factorscontributing to bank failures. Data provided tothe Department of Justice and the Federal Bu-reau of Investigation (FBI) confirm that criminalmisconduct, such as fraud and embezzlement, isa serious problem. For example, the FBI recent-ly reported that in 1985 it worked on 6,373 bankfraud and embezzlement cases—one-third ofwhich involved amounts exceeding $100,000. In1986, this number rose to 7,286—with a corre-sponding increase in the number of cases involv-ing more than $100,000. The FBI reports that in1985 the amount of reported dollar losses be-cause of bank fraud and embezzlement totaledabout $850 million; in 1986, this total increased tomore than $1.1 billion.

Over the past several years, the Federal Re-serve by itself, and in conjunction with the otherfederal banking and law enforcement agencies,has taken a number of steps to address bankfraud and insider abuse. A major part of thiseffort relates to our involvement in the Interagen-cy Bank Fraud Enforcement Working Group (the"Working Group") that was formed in April1985. The Working Group is comprised of offi-cials from all of the federal financial institution

Statement to Congress 651

regulator agencies, the Justice Department, andthe FBI. The principal results of the WorkingGroup's efforts over the past two years includethe following:

• The Working Group developed and imple-mented a uniform criminal referral form to beused by all banks, bank holding companies,savings and loan institutions, and credit unions.

• The Department of Justice developed andimplemented a "significant referral" trackingsystem. For this purpose, a criminal referral isconsidered "significant" if the dollar amount ofthe suspected violation exceeds $200,000, thesuspected offense involves insider abuse by sen-ior officials, or the violation involves, in theopinion of Board staff, activities or practices thataffect the integrity of the supervisory process orotherwise have nationwide implications. Eachsignificant referral received by the Federal Re-serve System is forwarded to the Fraud Sectionof the Department of Justice for tracking andspecial attention.

• As a complement to these efforts, the En-forcement Section of the Board's Division ofBanking Supervision and Regulation developedand implemented an automated system to moni-tor and track all of the Federal Reserve criminalreferrals. Complete access to the Board's crimi-nal referral recordkeeping system is available toall the agencies comprising the Working Group.

• The members of the Working Group devel-oped and distributed lists of key persons to becontacted at the local FBI offices, U.S. Attor-ney's offices, Federal Reserve Banks, and alldistrict offices of the Comptroller of the Curren-cy, the Federal Deposit Insurance Corporation,and the Federal Home Loan Bank Board onmatters relating to criminal referrals and bank-related insider abuse and fraud. These lists pro-vide important information for the staffs of theagencies that are reponsible for criminal referraland follow-up.

• The examiner training programs sponsoredby the Federal Financial Institutions Examina-tion Council have been expanded to includeextensive instruction in the detection and investi-gation of insider abuse and misconduct withinfinancial institutions. In addition, the membersof the Working Group jointly sponsor white-collar crime seminars with the FBI.

• At the urging of the Working Group, the

Attorney General called upon each U.S. attorneyto intensify his or her efforts in bank fraudenforcement. In a memorandum distributed inFebruary 1987, the Attorney General asked allU.S. attorneys to prepare inventories of bankfraud cases involving more than $100,000 that arepending prosecutive decision or action, to makeprompt prosecutive determinations in those cas-es ready for decision, and to assign the neededpersonnel to complete the investigation of opencases with the goal of indictment or declinationwithin nine months.

As part of this overall effort, the FederalReserve Board has attempted to improve itscommunication and coordination with the en-forcement agencies in this all-important area. Ibelieve that we have made considerable progressin strengthening our working relationships withthe Department of Justice and the FBI at boththe federal and the local levels. There is alsonow, I believe, a better mutual understanding ofthe procedures and responsibilities of the federalfinancial institution supervisory agencies and thefederal law enforcement agencies.

Besides these interagency efforts, the Boardhas sought to enhance its supervisory and en-forcement activities regarding insider abuse andmisconduct. This effort is reflected in an increasein the number of formal enforcement actionstaken by the Board. In the period 1981-82, theFederal Reserve System averaged 42 enforce-ment actions per year; from 1984-86, the averagenumber of enforcement actions had increased to177. These figures include actions against statemember banks, bank holding companies, andEdge act corporations. Moreover, during thisperiod, there has been a significant increase inthe number of enforcement orders addressingimproper or abusive actions of bank officials.This increase in enforcement actions has oc-curred across the Board—involving civil moneypenalties and fines, cease and desist orders, andsuspension and removal proceedings against offi-cers and directors.

Board staff members are also working withtheir counterparts at the other federal financialinstitution regulatory agencies to develop a jointlegislative proposal for amending the agencies'enforcement statutes. The purpose of the pro-posal would be to clarify the agencies' authorityto obtain reimbursement from individuals who

652 Federal Reserve Bulletin • August 1987

violate applicable banking laws; broaden theagencies' powers to issue cease and desist or-ders; strengthen removal procedures; and codifyexisting interpretations of the Right to FinancialPrivacy Act. We believe that these changeswould strengthen the agencies' ability to addressbank fraud and insider dealings, and it is ourhope that a proposal will be ready soon forreferral to the Congress.

DOMESTIC REGULATORY ACTIVITIES