Embed Size (px)

Citation preview

Building Your Financial Houseusing

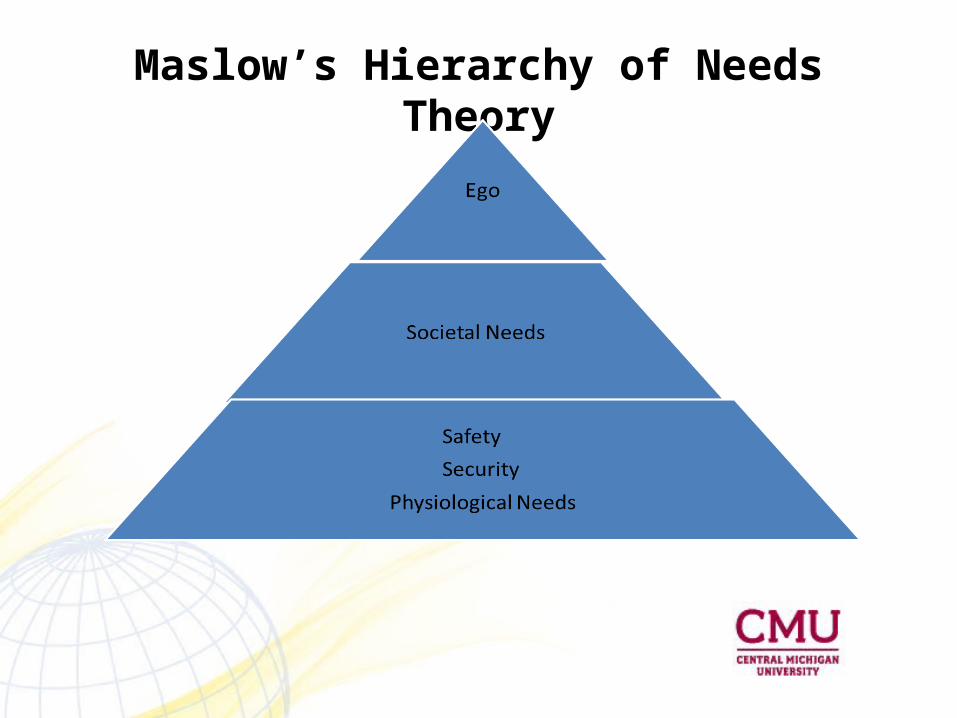

Maslow’s Hierarchy of Needs Theory

Diana Webb, Ph.D.Associate Professor of Finance

Maslow’s Hierarchy of Needs Theory

Building Your Financial House

Get Rich Quick Futures Options Individual Stocks Accounts

Savings Emergency

Checking Money

Market Retirement 401K , IRA

Insurances = Protection Health Disability Income

Life Long Term Care

Auto & Home Retirement

Retirement Planning for the 21st Century

• 50 years ago Social Security was strong More people were paying in than taking out of the system People worked until they were age 65

• Today the Social Security System is weakLiving longer due to advances in the medicineMore add-ons to Social Security (widows, orphaned children, disabled workers)More people retiring earlier than age 65

What do we do now that we understand the Federal Government cannot support our retirement?

• Plan ahead for our retirement and stop depending on Government

• Take charge of our lifestyle

• Begin saving today

• How do we do this saving for retirement?– Raises at work– Income tax refund– Bonuses– Inheritance

Ideas on How to Invest, What to Invest, and Where

Mutual Funds Individual Stocks

Government Bonds Money Market Accounts

Municipal Bonds Corporate Bonds

Growth Stocks Income Stocks

International Stocks International Bonds

EE Savings Bonds Utilities

Real Estate Investment Trusts (REITs)

Ideas on How to Open a Retirement Account

• Employer Plans– 401 K plans– 403 B plans– 457 plans

• Individual Retirement Accounts– Roth Individual Retirement Accounts– Traditional Retirement Accounts

• Brokerage Accounts– Online Accounts without using a broker or

registered representative – Internet education on investing– Personal Finance class via CMU

What to know before you begin investing

• Your risk analysisWhere are you on a scale of 1-10?

1 = Not willing to take any risk

Conservative

5 = Willing to take some risk Moderate

10 = Willing to take a lot of risk Aggressive

• How willing are you to take on risk?– Interest Rate Risk– Stock Market Risk– Economic Risk

Funding Your Child’s Future Education 529 College Savings Plans

• 529 Plans and how they work

• Setting up a 529 Plan

• Funding the 529 Plan

• Advantages

• Disadvantages

• Information on 529 Plans

Finding Your Financial Direction Using Your Compass

• Where are you today?

• Where do you want to be tomorrow?

• How do you assess where you are today? Hint: take a personal finance class and learn about building your financial house

• Setting goals

• Getting rid of debt

• Starting fresh

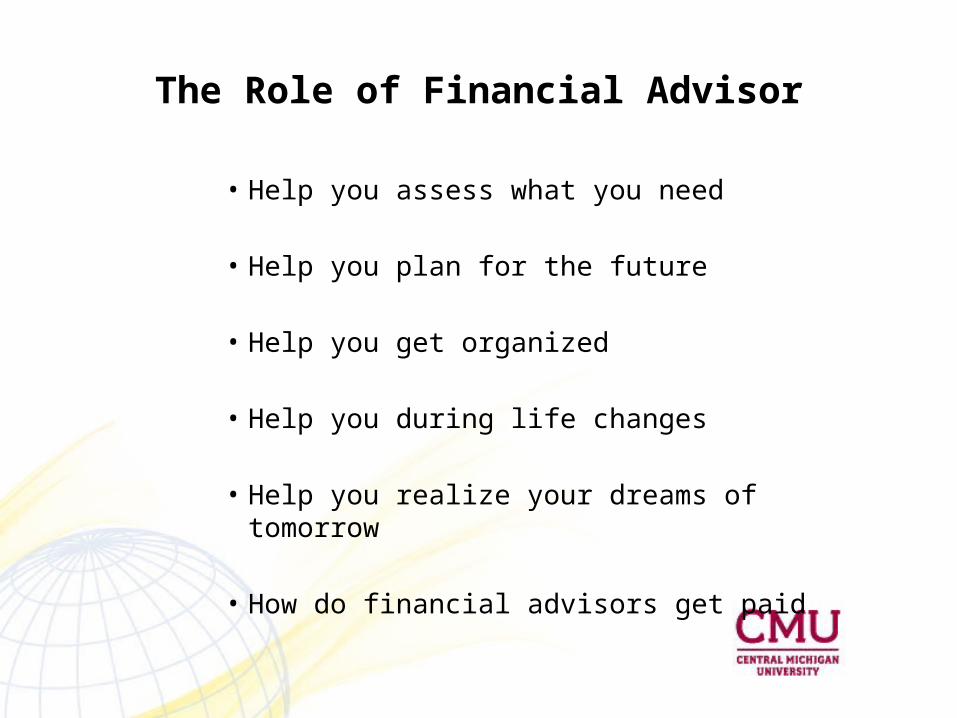

The Role of Financial Advisor

• Help you assess what you need

• Help you plan for the future

• Help you get organized

• Help you during life changes

• Help you realize your dreams of tomorrow

• How do financial advisors get paid

Why & When to Rebalance your Investment Accounts• As we get older our investment objectives change

Accumulation Stage (ages 25-65)– Your working years– You can be more investment aggressive up to about age 60-65

• Stocks • Bonds

– Prior to retirement, rebalance for more moderate investing

• Distribution Stage (ages 65-85)– Your retirement years– More moderate investments due to retirement– Keeping up with inflation and taxes, but more moderate– Rebalance more money in moderate to conservative

investments

• Estate Planning Stage (65-?)

• Where do you want your investments and money to go?

Getting Started• Where are you today?• Take your pulse • What debt do you have?• Does your debt include Needs or Wants?• Track every single cent you spend for 4 months• Is more going out for senseless things?• Do you see patterns of spending?• Can you change those patterns of spending?• After the 4 months of record keeping you will know your

pulse• Now you can begin to build a healthy financial house &

remember its all about the money, honey!Sincerely,Dr. Webb

![Improving Maslow’s Hierarchy of Needs: New Approach to ...€¦ · Maslow’s Hierarchy of Needs – 1970 Expression [41] Level in Hierarchy Maslow Need Description 7 Aesthetic](https://img.pdfslide.us/doc/110x75/5f4b71e1c352b64dde2f3478/improving-maslowas-hierarchy-of-needs-new-approach-to-maslowas-hierarchy.jpg)