Embed Size (px)

Citation preview

11/24/2011

1

BUILDING BUSINESS VALUE –

WHAT IS YOUR BUSINESS WORTH AND WHY YOU SHOULD CARE!

Presentation to Members of the Oshawa Chamber of Commerce

November 24, 2011

Presented by:

Jason Kwiatkowski, CA, CBV, ASA, CEPA

Partner and President, Valuation Support Partners Ltd.

Information About the Speaker

11/24/2011

2

Jason Kwiatkowski, CA, CBV, ASA, CEPA

Jason is a Chartered Accountant and Chartered Business Valuator with 16 years of

experience in professional services, 13 years of which in the valuation area.

Jason supports the business and legal communities with independent expert

valuation and litigation support services. Services include rendering of conclusions

on the value of businesses and intangible assets as well as the quantification of

economic damages. He has completed numerous valuation and expert reports for

various purposes, including: tax planning, mergers, acquisitions and divestitures,

insurance coverage, financial reporting, commercial, shareholder and matrimonial

disputes, breach of contract, securities law, and personal injury matters.

Jason also assists private business owners with exit planning and transaction

advisory services, including preparing comprehensive exit plans, benchmark

business valuations, pricing analyses, value enhancement, pre-sale planning and

financial due diligence.

Jason has testified before the Ontario Superior Court of Justice as an expert

witness in business valuation and damages quantification and has participated as

an expert in business valuation at mediation and arbitration for shareholder

disputes. Jason has also testified before the Ontario Securities Commission as an

expert in matters involving business valuation.

Jason has written articles and lectured at various conferences and professional

development sessions on topics related to valuations, litigation support and

corporate finance.

Agenda

I. Business Valuation

• When Are Business Valuations Needed?

• Benefits of Obtaining a Business Valuation

• Business Valuation Approaches

II. Value Enhancement & Key Value Drivers

• Factors that Determine the Value of a Business

• Key Value Drivers

III. Effective Exit Planning

• What is Exit Planning?

• The Exit Options

• Benefits of Having an Exit Plan

• 6 Steps to an Effective Exit Plan

IV. Group Exercise

11/24/2011

3

I. Business Valuation

Agenda

Business Valuation

• When Are Business Valuations Needed?

• Benefits of Obtaining A Business Valuation

• Business Valuation Approaches

11/24/2011

4

When are Business Valuations

Needed?

When Are Business Valuations Needed?

• Businesses generally do not require a valuation every year

• However, most businesses will require a valuation at some point in

time

• There are many different reasons or triggers for a business valuation

1. Notional valuations

2. Actual transactions

3. Financial reporting

11/24/2011

5

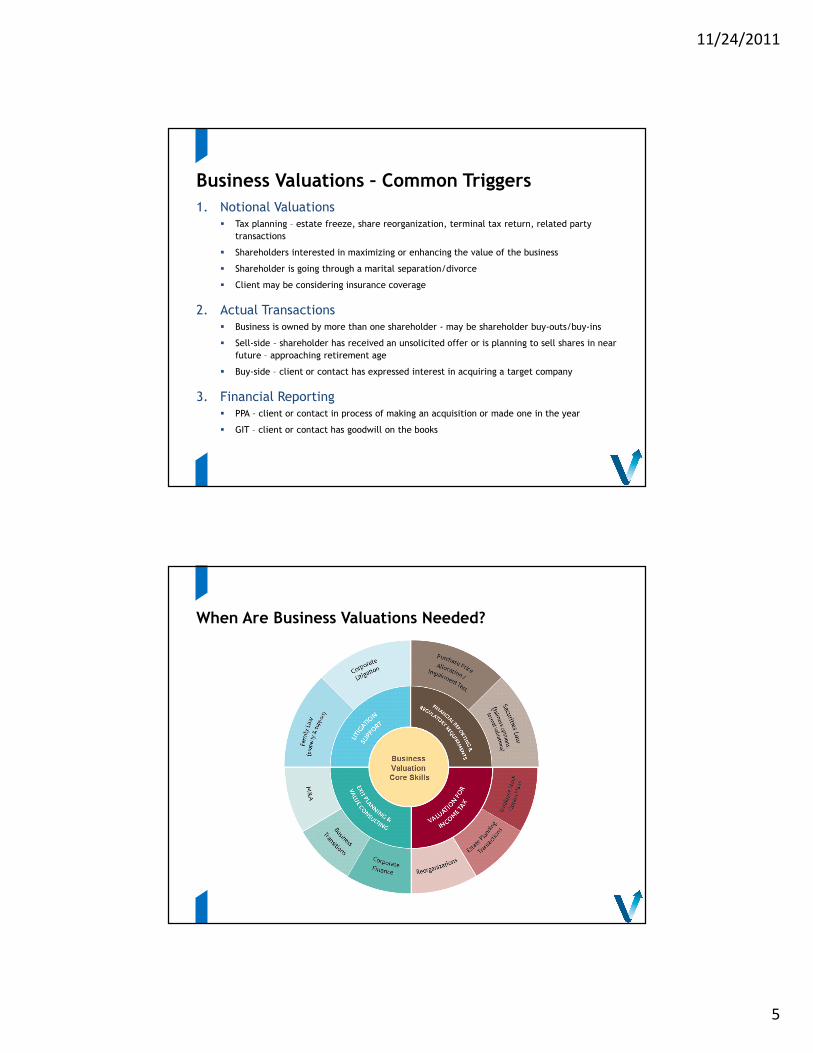

Business Valuations – Common Triggers

1. Notional Valuations� Tax planning – estate freeze, share reorganization, terminal tax return, related party

transactions

� Shareholders interested in maximizing or enhancing the value of the business

� Shareholder is going through a marital separation/divorce

� Client may be considering insurance coverage

2. Actual Transactions� Business is owned by more than one shareholder - may be shareholder buy-outs/buy-ins

� Sell-side – shareholder has received an unsolicited offer or is planning to sell shares in near

future – approaching retirement age

� Buy-side – client or contact has expressed interest in acquiring a target company

3. Financial Reporting � PPA – client or contact in process of making an acquisition or made one in the year

� GIT – client or contact has goodwill on the books

When Are Business Valuations Needed?

11/24/2011

6

Benefits of Obtaining a

Business Valuation

Benefits of Obtaining a Business Valuation

1. Provides a value to be used for tax planning purposes

2. Provides a benchmark value for value enhancement

3. Provides a value for shareholder buy-out or buy-in (shareholder

agreement)

4. Help to assess offers by potential purchasers

5. Provides a value to help determine insurance coverage

Some of the benefits of obtaining a business valuation include:

11/24/2011

7

Business Valuation Approaches

Business Valuation Approaches

• There are many different ways to value a company or an asset.

• Certain techniques are more appropriate than others for a

particular business.

• All companies have their own unique valuation issues.

• It is important for management of a company to have a basic

understanding of valuation methods in order to understand and

properly use a valuation report.

Overview

11/24/2011

8

Business Valuation Approaches

• The fundamental premise on which all investment decisions are

made is that value to a potential investor is equal to the present

worth of the future benefits.

• There are two bases on which to determine the value of a company

or asset:

i. Going Concern; or

ii. Liquidation

General Principles

Business Valuation Approaches

Going Concern

This approach assumes that a company or asset will be expected to

continue to operate well into the future, and the prospective investor

will evaluate the risks and expected returns of the company or asset.

Liquidation

An investor is only interested in individual assets as collateral should

the company choose to liquidate.

* We will only focus on Going Concern for this seminar*

General Principles

11/24/2011

9

Business Valuation Approaches

• All methodologies applied to the valuation of an asset or business

may be broadly classified into:

i. Asset (Adjusted Book Value) approach

ii. Income approach

iii. Market approach

Methods

Business Valuation Approaches

• There are several methodologies used in the income approach,

including:

~ Discounted Cash Flow approach (“DCF”)

~ Capitalization of Earnings/Cash Flow approach

Income Approach

11/24/2011

10

Business Valuation Approaches

• Using the DCF, the present value of projected future cash flows to

be generated from the business and theoretically available (though

not necessarily paid) to the capital providers of the company is

estimated.

• A discount rate reflecting the risks of ownership and risk of realizing

the stream of projected future cash flows is applied to the

projected future cash flow to arrive at the present value.

• The DCF approach is generally appropriate where the business has a

finite life and/or the business is forecast to experience change for a

number of years before achieving a sustainable operating level.

Income Approach - DCF

Business Valuation Approaches

• Consider capital expenditures and working capital needs.

• Cash flows interdependent with selected discount rate:

Income Approach – DCF – Valuation Issues

Cash Flows Discount Rate

Pretax → Pretax

Debt-free → WACC

Inflationary growth included → Real rate of return

Optimistic → Higher risk

11/24/2011

11

Business Valuation Approaches

• Selecting appropriate discount rate given risks of investment.

• Deduct debt where appropriate:

~ If pre-debt cash flows, then result is Enterprise Value – so deduct debt

• Proper treatment of redundant assets / liabilities and real estate

Income Approach – DCF – Valuation Issues (continued)

Business Valuation Approaches

• This approach is based on capitalizing some measure of financial

performance such as earnings or cash flows, using a capitalization

rate that reflects both the risk and long-term growth prospects of

the subject company.

• It is generally appropriate where the business is mature with

relatively consistent earnings/cash flow, or where it can be

estimated through a business cycle and where forecasts for a

business are not available or are unreliable.

Income Approach – Capitalization of Earnings/Cash Flow

11/24/2011

12

Business Valuation Approaches

• Same as for DCF.

• Normalize historical earnings if used as a basis for calculation.

• Consider future growth in multiple.

Capitalization of Earnings/Cash Flow – Valuation Issues

Business Valuation Approaches

• This approach involves comparing the subject company to similar

businesses or “guideline” companies whose securities are actively

traded in public markets or which have recently been sold in a

private transaction.

Market Approach

11/24/2011

13

Business Valuation Approaches

• Selecting and properly applying the appropriate valuation metric:

~ EV to EBITDA

~ EV to Revenue

~ Price or EV/Book Value

~ EV to EBIT

~ Price to Earnings

• Deducting debt where appropriate from the conclusion:

~ Enterprise Value (EV) – Debt = Equity Value

Market Approach – Valuation Issues

Business Valuation Approaches

• Proper treatment of redundant assets / liabilities and real estate:

~ Redundant assets / liabilities to add (deduct) from market approach

value

~ Real estate may skew result if guideline companies own but subject

company rents (or vice-versa)

• May be appropriate and necessary to discount multiples in the

public market when applying it to your business.

Market Approach – Valuation Issues (continued)

11/24/2011

14

II. VALUE ENHANCEMENT & KEY VALUE DRIVERS

Agenda

Value Enhancement & Key Value Drivers

• Factors that Determine the Value of a Business

• Key Value Drivers

11/24/2011

15

Factors that Determine

the Value of a Business

Introduction

• Value Drivers vary according to the business, the industry, potential

buyers and the reason for the acquisition.

• There are a number of common categories of drivers that can add

value to your business.

• Identifying and optimizing the appropriate drivers for your business

can help strengthen the attributes of your company that will be

highly valued by prospective purchasers.

• We will discuss examples of common value drivers – but, every

business is unique. Seek advice for drivers specific to your

business.

11/24/2011

16

Factors that Determine the Value of a Business

• Value and price are different – price is what you pay, value is what

you receive.

• Value for many operating businesses is a function of two primary

components:

i. The quantum of expected future earnings and/or cash flows; and

ii. The quality of (or risk associated with) those earnings and/or cash flow

Value and Price

Factors that Determine the Value of a Business

• Reflects the revenues generated by the business, minus the costs

associated with generating those revenues (i.e. profits).

• Generally, prospective buyers will place more value on cash flow

that is expected to increase in the future (i.e. growth).

• Strive for strong cash flow generation with good expectations for

future growth:

~ Seek opportunities to grow and diversify revenue sources

~ Increase gross margins

~ Control costs

Quantum of Cash Flow (maintainable earnings or cash flow)

11/24/2011

17

Factors that Determine the Value of a Business

• Refers to: Sustainability, Variability, and Sensitivity to Risks

• The risk associated with cash flow is generally reflected in value by

the multiple or capitalization rate applied.

• The multiple or capitalization rate applied to the selected cash flow

to convert it to the value of the business, reflects an expected rate

of return for an investment and is, therefore, a key component of

value.

• The rate of return is a function of:

~ Market conditions and rates of return in the marketplace; and

~ Risk factors specific to a business (internal and external)

Quality of Cash Flow

Factors that Determine the Value of a Business

• Prospective buyers will place more value on a predictable stream of

cash flow than on one that is less predictable, or more volatile

• Strive for improved quality of cash flow:

~ Increase the proportion of total revenues that are recurring in nature

(e.g. repeat customers)

~ Seek opportunities to diversify revenue sources and reduce customer

concentration

~ Seek opportunities to improve consistency of gross margins

~ Reduce supplier dependence

Quality of Cash Flow

11/24/2011

18

Top 4 Key Value Drivers

1. Customer Base

2. Management Team

3. Growth

4. Income and/or Cash Flows

Top 4 Key Value Drivers

• Customer Base is the most important source of recurring revenue.

• Prospective buyers look for a growing base of loyal (i.e. repeat), long-term customers and the existence of long-term contracts.

• Quality of customers can be determined by looking at:

~ Historical sales trends

~ Size of customer base

~ Number or percentage of new customers acquired each year

~ Average number or percentage of customers that leave each year

• It’s important to minimize customer concentration and attrition and to strengthen relationships, repeat business and locking in contracts.

1. Customer Base

11/24/2011

19

Top 4 Key Value Drivers

• Depth and breadth of a company’s management team are important

considerations when valuing a business.

• The strengths and weaknesses, such as experience and knowledge,

of the existing management team are relevant in coming to a view

as to its capability of managing the business going forward.

• Value enhancers include a team that:

~ Shares a clear focus and strong commitment to the company

~ Follows a business plan that demonstrates the enterprise is prepared to deal

with economic, competitive, and other influences

• It’s important to groom an excellent management team.

2. Management Team

Top 4 Key Value Drivers

• Investors are attracted to potential growth / opportunity for increased cash flows.

• A sound and viable growth plan will enhance the company’s value (new products/services, new markets/customers, increased prices and margins, decreased costs, etc.)

• The strategic plan for your business must detail your plan to growth the business.

• It’s important to show a recent and proven track record of growth to demonstrate management’s ability to achieve growth (i.e. convince potential purchasers that the planned growth can and will be achieved).

3. Growth

11/24/2011

20

Top 4 Key Value Drivers

• Cash is King!

• Value is prospective

• Potential purchasers/investors are interested in cash flows that are

HIGH, INCREASING and WILL CONTINUE TO INCREASE

4. Income and/or Cash Flows

Other Key Value Drivers

• Sound business / strategic plan

• Workforce

• Market position

• Strategic advantages

• Information systems

• Financial leverage

• Condition of capital assets

• Labour force – skilled, shortage

• Supplier dependence

• Market conditions

• Competition

• Marketing ability, experience,

depth, approach

• R&D requirements/efforts

• Management continuity and

dependence

• Geographical focus for sales

• Impact of foreign exchange

• Vulnerability to cycles, recessions

• Product/service life style

• Significant contracts

11/24/2011

21

III. EFFECTIVE EXIT PLANNING

• Recent studies show that 40% of boomers will exit their

businesses within 5 years, 80% within 10 years.

• Studies have also shown that the majority of business

owners do not have an exit plan.

• A recent survey of SME’s* found that:

– 92% of entrepreneurs believe that it is important to have an exit strategy but only 44% actually have an exit strategy

– 71% intend to sell their businesses within the decade.

*SME = small and medium size enterprises, 99 employees or less.

11/24/2011

22

Agenda

Effective Exit Planning

• What is Exit Planning?

• The Exit Options

• Benefits of Having an Exit Plan

• 6 Steps to An Effective Exit Plan

What is Exit Planning?

11/24/2011

23

What is Exit Planning?

How will it feel to have built it?

PRESENT THE TRANSITION FUTUREWhat does your house look like?

What is Exit Planning?

• Involves working with business owners to develop a formalized action plan to prepare for the eventual exit of their business.

• Is a comprehensive road map to successfully exit a privately held business.

• Addresses the business, personal, legal, financial, and tax issues relating to the ultimate sale/transfer.

• Allows you to get the maximum value out of the business at the right time and on your terms:

~ Maximize underlying value of the business

~ Use the best sale process (exit option) to maximize what the market will pay while accomplishing goals

~ Minimize taxes paid on sale of business

An Exit Plan:

11/24/2011

24

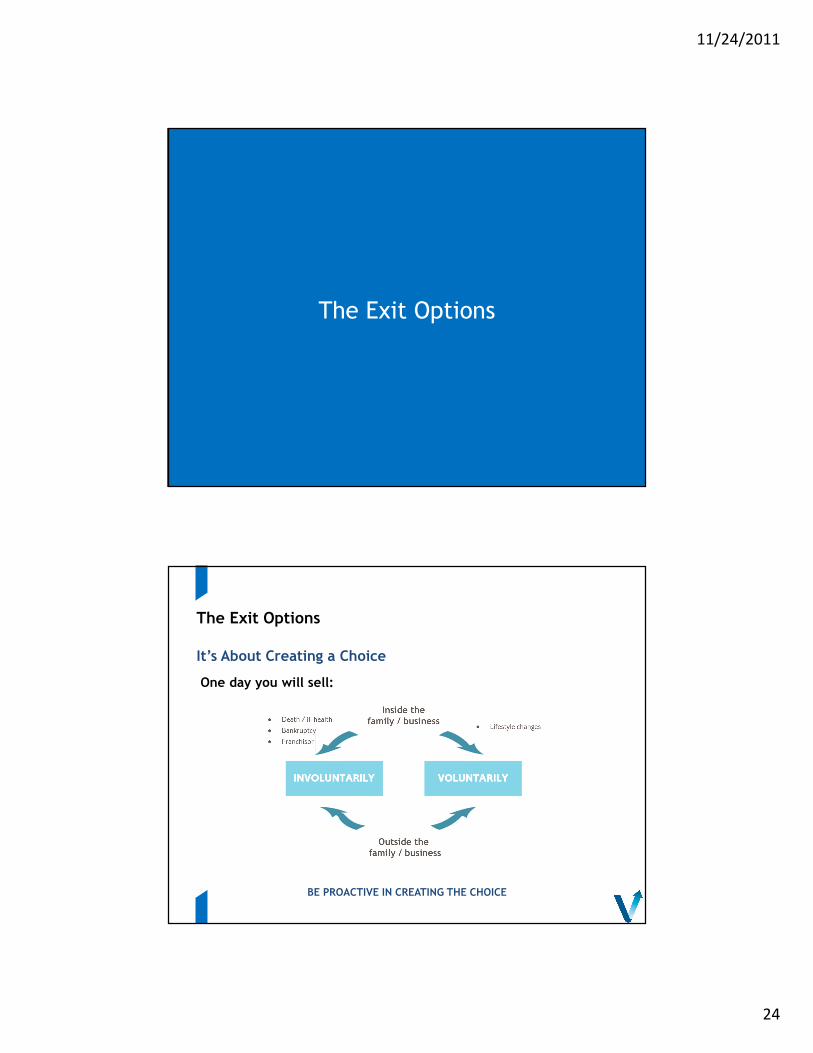

The Exit Options

The Exit Options

BE PROACTIVE IN CREATING THE CHOICE

One day you will sell:

It’s About Creating a Choice

11/24/2011

25

Exit Options – Voluntary Exit

• Shareholders: Shareholder Buy-Sell Agreement

• Family: Intergenerational Transfer

• Management: Management Buyout

• Employees: ESOP

Internal Exit Options involve a transfer or sale to:

Exit Options – Voluntary Exit

• Third Party Sale: Stay

• Third Party Sale: Retire

• Public Offering

• Refinance or Recapitalize

• Liquidate

External Exit Options involve a transfer or sale to:

11/24/2011

26

Benefits of Having an Exit Plan

Benefits of Having an Exit Plan

• Regain control over how and when you exit the business – choose

the appropriate exit option to achieve your goals.

• Maximize company value in good times and bad – won’t leave

money on the table.

• Minimize, defer, or eliminate capital gains taxes.

• Ensure you achieve your business and personal goals.

• Reduce stress and tension among the business owner, employees

and family.

• Ensure continuity of the business.

11/24/2011

27

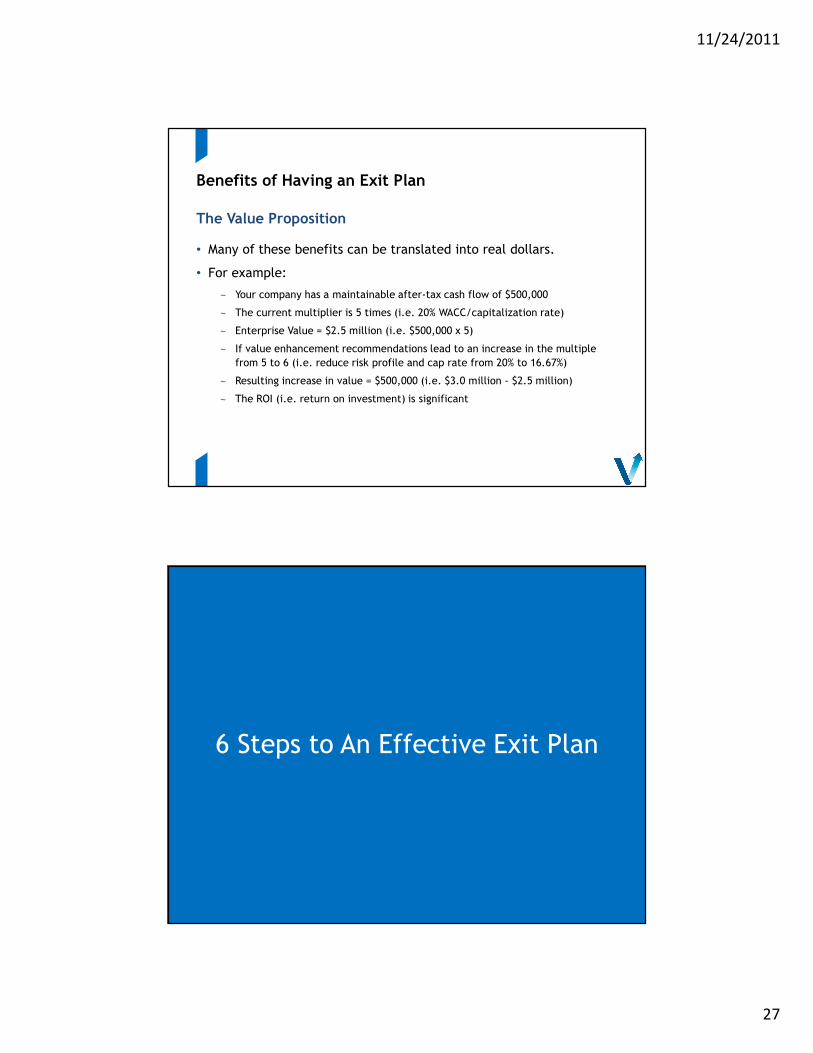

Benefits of Having an Exit Plan

• Many of these benefits can be translated into real dollars.

• For example:

~ Your company has a maintainable after-tax cash flow of $500,000

~ The current multiplier is 5 times (i.e. 20% WACC/capitalization rate)

~ Enterprise Value = $2.5 million (i.e. $500,000 x 5)

~ If value enhancement recommendations lead to an increase in the multiple

from 5 to 6 (i.e. reduce risk profile and cap rate from 20% to 16.67%)

~ Resulting increase in value = $500,000 (i.e. $3.0 million - $2.5 million)

~ The ROI (i.e. return on investment) is significant

The Value Proposition

6 Steps to An Effective Exit Plan

11/24/2011

28

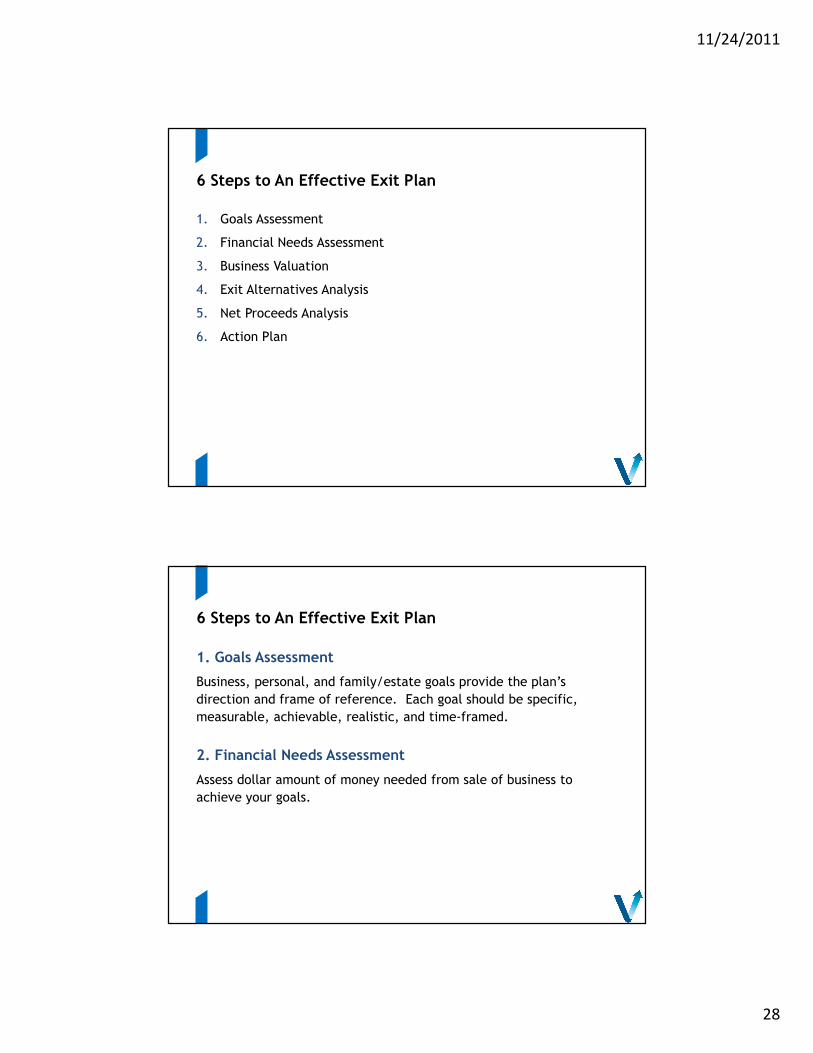

6 Steps to An Effective Exit Plan

1. Goals Assessment

2. Financial Needs Assessment

3. Business Valuation

4. Exit Alternatives Analysis

5. Net Proceeds Analysis

6. Action Plan

6 Steps to An Effective Exit Plan

1. Goals Assessment

Business, personal, and family/estate goals provide the plan’s

direction and frame of reference. Each goal should be specific,

measurable, achievable, realistic, and time-framed.

2. Financial Needs Assessment

Assess dollar amount of money needed from sale of business to

achieve your goals.

11/24/2011

29

6 Steps to An Effective Exit Plan

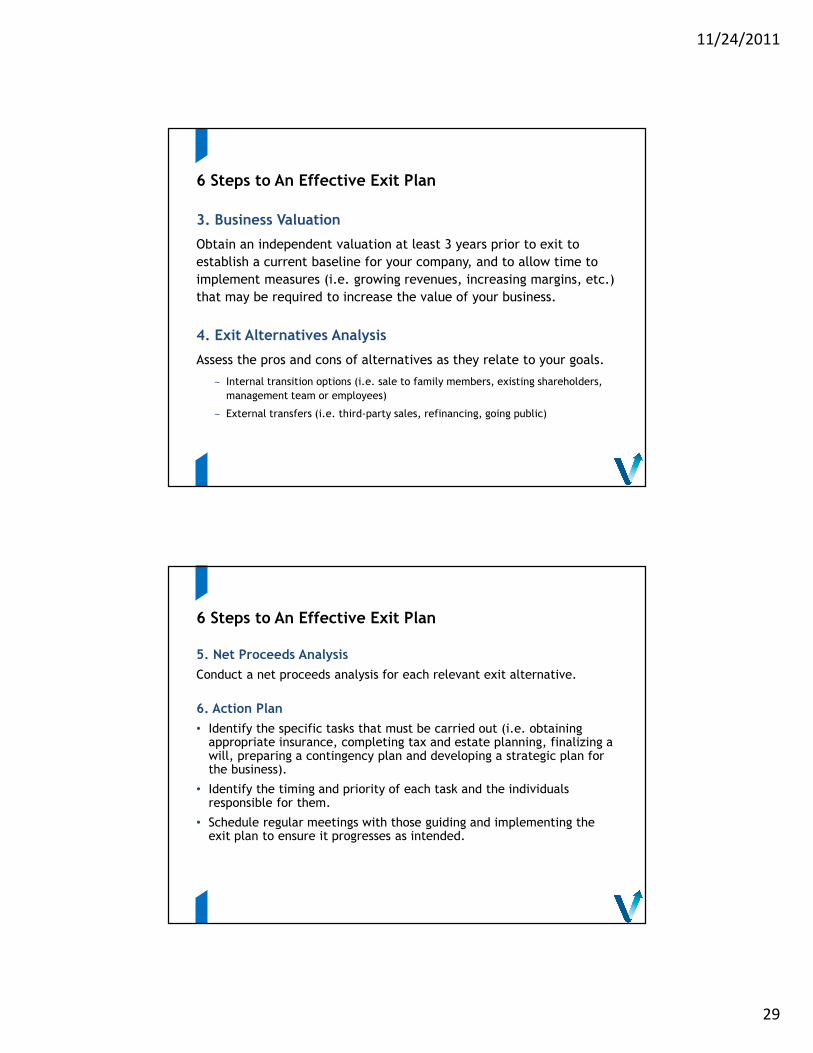

3. Business Valuation

Obtain an independent valuation at least 3 years prior to exit to

establish a current baseline for your company, and to allow time to

implement measures (i.e. growing revenues, increasing margins, etc.)

that may be required to increase the value of your business.

4. Exit Alternatives Analysis

Assess the pros and cons of alternatives as they relate to your goals.

~ Internal transition options (i.e. sale to family members, existing shareholders,

management team or employees)

~ External transfers (i.e. third-party sales, refinancing, going public)

6 Steps to An Effective Exit Plan

5. Net Proceeds Analysis

Conduct a net proceeds analysis for each relevant exit alternative.

6. Action Plan

• Identify the specific tasks that must be carried out (i.e. obtaining appropriate insurance, completing tax and estate planning, finalizing a will, preparing a contingency plan and developing a strategic plan for the business).

• Identify the timing and priority of each task and the individuals responsible for them.

• Schedule regular meetings with those guiding and implementing the exit plan to ensure it progresses as intended.

11/24/2011

30

Group Exercise

Group Exercise

• What is the nature of your business?

• What are the goals of your business?

• What are the 3 key value drivers for your business and why?

• How would you rank/prioritize those value drivers in terms of

impact and relevance?

One volunteer from each group to present.

In groups, please discuss the following:

11/24/2011

31

Questions