Embed Size (px)

Citation preview

BUILDING BLOCKS FOR SUCCESS

Successful Compliance Strategies for

High Tech Growth

an Executive Panel Session

Tuesday, April 26 * 10:45 - 11:45 PM * Room 209-210

Guy ClarkeSenior Manager, Business Advisory ServicesGrant Thornton

Robert O’Connor, Jr.President & CEOSoftrax Corporation

Today’s Panel

John WallesExecutive Vice President Acquisitions & Integration

SSA Global

Agenda

• Introduction• Technology Solutions – critical business need and

opportunityBob O’Connor, Softrax Corporation

• Industry Barometer – what’s really happening in the marketplace, and what you can do about itGuy Clarke, Grant Thornton

• From the Trenches - Insights from inside one of the industry’s leading corporations John Walles, SSA Global

• Questions & Answers

Technology Solutions

Critical business need and opportunity

Robert O’Connor, Jr.President & CEOSoftrax Corporation

Hot compliance issues –costs and controls

• Companies can’t take any risks with financial reporting

• M&A preparedness – Buyer/Seller• Changing role of the auditor• No more spreadsheets• With spiraling compliance cost,

companies are looking for ROI

Key Challenges

• Revenue Recognition• Management of long term

multi-element contracts• Documentation• Audit trail• Renewable business• Forecasting

Source: www.RevenueRecognition.com and IDC, 2004n=118, does not add to 100% due to rounding

In your opinion, for which area is it mostdifficult to establish internal controls?

Contract Administration and Management, 29%

Revenue Recognition Accounting, 36%

General Ledger, 0%Treasury, 1%Payroll and Equity, 2%Other, 3%Billing and Accounts Receivable, 3%Order Processing, 4%Fixed Assets, 5%Inventory, 8%Purchasing and Payables. 8%

Internal Controls –Revenue Recognition Most Difficult

“Revenue accuracy is the singlemost contested issue in any M&A activity.”

Revenue in M&A

SOP 98-9

SOP 97-2

SAB 101

SOP 81-1

FASB

SEC

AICPA

Sarbanes-Oxley

EITF 00-21

Licenses

Subscriptions

Transactions

Services

Maintenance

Royalties

Utilization

Contracts

Renewals

Revenue

• Key reporting requirement

• Highly regulated

• Greatly scrutinized

• Heavily audited

• Hard to manage

Often insufficient internal controls

Revenue under Pressure

• Integrity of key transactions

• Documentation of transactional changes

• Revenue recognition compliance

• Real time disclosure and reporting

• Visibility and forecasting

M&A due diligence

IPO preparation

Not only for public companies:

Sarbanes-Oxley Increases Urgency

SOP 98-9

SOP 97-2

SAB 101

SOP 81-1

FASB

SEC

AICPA

Sarbanes-Oxley

EITF 00-21

Licenses

Subscriptions

Transactions

Services

Maintenance

Royalties

Utilization

Contracts

Renewals

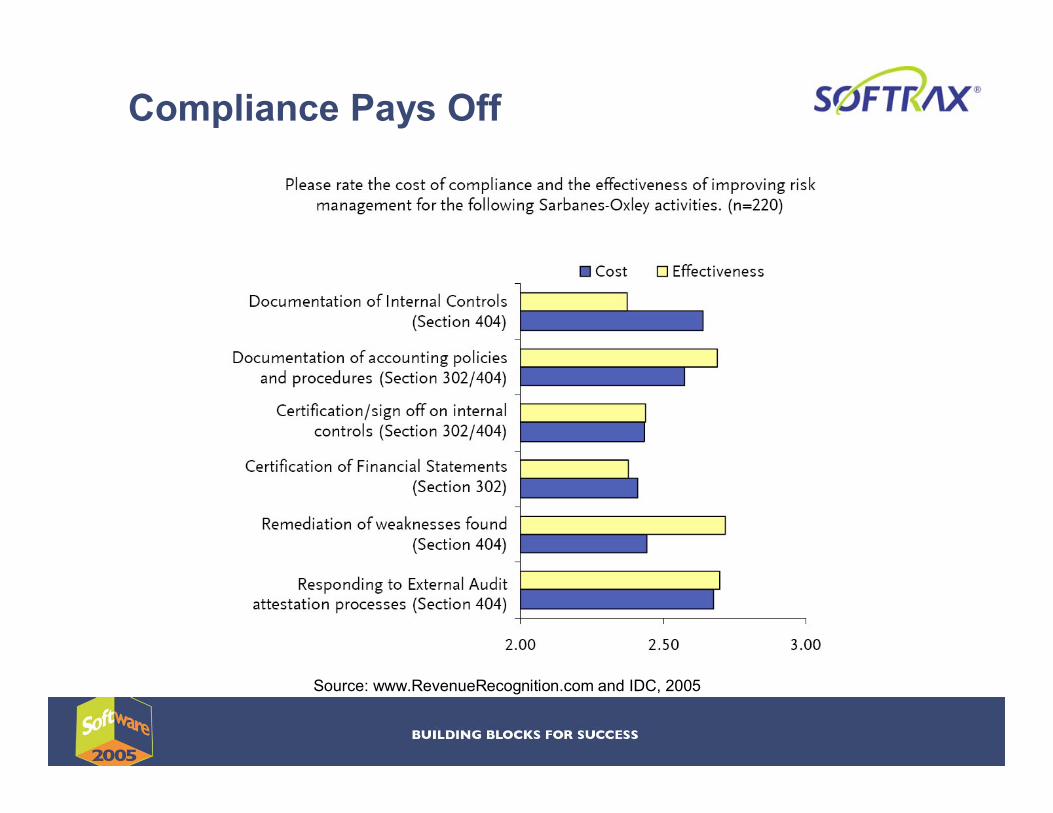

Compliance Pays Off

• Provide – Transparent revenue history– Proper revenue recognition and deferred revenue processes– Complete customer, contract, and order database

• Results in …– Greater buyer confidence– Simpler Due Diligence– Higher valuation/multiples– No last minute surprises– Reduce write-down of deferred revenue

When you’re being acquired …

Compliance Pays Off

• Looking for …– Complete visibility into acquisitions true financial health– Verifiable, auditable history– Solid evidence of revenue performance and expectations

• Results in …– Minimized risk– Faster, smoother M&A process– More efficient integration– No last minute surprises

When you’re acquiring …

Source: www.RevenueRecognition.com and IDC, 2005

Compliance Pays Off

Source: www.RevenueRecognition.com and IDC, 2005

Compliance Pays Off

Documenting Internal Controls is more costly than effective

Source: www.RevenueRecognition.com and IDC, 2005

Benefits of fixing Internal Control weaknesses outweigh cost

Compliance Pays Off

The bottom-line - the cost of compliance: Is there an ROI?

• Crossing the “Compliance Chasm”• Taking advantage of

better processes• ROI

Softrax Revenue Management

Revenue

Cost

Compliance

Industry Barometer

What’s really happening in the marketplace, and what you can do about it

Guy ClarkeSenior Manager, Business Advisory ServicesGrant Thornton

Agenda

• Overview of Sarbanes-Oxley

• The Marketplace – what's happening??

• Making the connection – Lessons Learned

• Questions & Answers

The catalyst - SOX– In the wake of mounting corporate scandals and accounting

misdeeds, the Sarbanes-Oxley Act was passed into law in 2002 with the purpose of restoring investor confidence in the U.S.

– The passage of the Act, coupled with related rules adopted by the SEC are designed to make it harder for publicly held companies to commit and conceal corporate fraud.

– Now, corporate governance and internal controls are no longer a luxury – they are required by law.

SOX Section 404 –Management's responsibility• Section 404 – Management’s annual internal

control assertion must state:

– Management's responsibility for internal control over financial reporting

– The framework used by management to conduct the evaluation (e.g., COSO / CobiT, )

– Management's assessment of control effectiveness, including disclosure of any "material weaknesses"

– The auditor has issued an attestation report on management's assessment

– Section 302 – Management's quarterly certifications of financial statements / internal controls (continuous)

Understanding the components– Financial and Operational Process Controls– Inventory of relevant information technology– General IT controls

• Governance• Security• Change management• Operations

– Spreadsheets (data)• Minimize reliance and implement change control

– Third-Party Service Providers (SAS70's)• Outsource key business processes, but must

maintain ownership

It's happening right now in the marketplace…• SOX does not scale easily

– Large vs. Small companies

• Requires expertise to apply / fit to a company's environment– Consulting assistance

• Private Companies– Compliance 12 mos. after initial SEC filing (Debt or

Equity)

• Investment (Time & Money) vs. ROI – Benefits?– Increased controls should yield efficiencies in financial

reporting and auditing from Year Two forward

GAO restatement Study Analysis of restatement causes (Jan '97 – Jun '02)

Source: October 2002 GAO study, Financial Statement Restatements.

FEI Survey findings – March 2005

3890

2018

964

Average External hours

76.4%$544,000$679,0006995$100 – 499 M

73.8%$250,000$336,0004300$25 – 99 M

76.4%$132,000$494,0004757Less than $25 M

What percentages of your processes

are you documenting

to comply with Section 404?

Average additional audit fee

(attestation report)

Average consultant, software, vendor

cost* necessary for compliance

Average Internal hours

Annual sales revenues

* excluding auditors fee

There is hope…

– SEC postpones 404 filing date for non-accelerated filers and foreign private issuers (July 2006)

– SECs two new initiatives:

• Committee established to help evaluate the impact of related regulations on smaller public companies

• Task force assembled by COSO to develop new internal control guidance to be published this summer for smaller companies

The end-game:Who are the stakeholders here and what do they need?

Investor protection and reliable financial informationRegulators

Reliable financial information and litigation protectionAuditors

Job and morale protectionEmployees

Investment protection and reliable financial informationInvestors

Job/litigation protection (i.e., piece of mind) and reliable financial information

Management

Lessons learned from our 404 fieldwork (100+ companies)

– Prior external audit management comments may come back to haunt you – deficiencies no longer can be overlooked by substantive audit work and many CPA firms spend little time on IT controls

– Little attention paid to records retention and management, (often assumed to be IT's responsibility) –SEC seeks documentation evidence to support management's position and the solution must extend across organization

– Many significant remediation issues fall within the IT domain are quite visible – weak IT general controls undermine automated applications that enable financial processes and external audit firms may insist on manual "stopgap" measures to compensate

More lessons learned– Education is a critical component often overlooked

– understanding what controls are and the impact they have

– Creating a stable IT environment is a must –continual changes to or implementation of new controls will require excessive testing

– Planning is Key – Be proactive and start early!

Guy ClarkeSenior Manager, Business Advisory ServicesGrant Thornton LLPGreater Bay Area, CAp: 408.346.4312e: [email protected]

John WallesExecutive Vice President Acquisitions & Integration

SSA Global

From the Trenches

Insights from inside one of the industry’s leading corporations

Questions !

www.revenuerecognition.com

www.softrax.com