Embed Size (px)

Citation preview

Fri, 22 May 2015

Equi ty Research EGL Holdings (6882 HK) Tour ism/ China

Fly me to the moon

EGL Holdings (6882 HK, “EGL”) is a leading travel company in Hong Kong

providing package tours and FIT products to more than 250 cities in over 60

countries. With experienced management and direct land operations in Japan,

EGL has built up unique competitive advantages to ride on the massive growth in

Japan tours and Chinese outbound travel market.

Everything Good and Long-lasting: EGL, in other words, has the

customers’ best interests at heart; winning trust and creating a strong,

indelible image at the same time. Unlike other travel agents, EGL carved out

its leading position through solid ground work – handling operations on the

ground in Japan’s travel tour business with down-to-earth management. By

setting up JVs with local land operators in other countries, EGL will replicate

its successful model to drive sustainable growth.

Strong outlook for FY15E results: Depreciation of the Japanese Yen plus

drop in fuel costs have led to drop in air ticket prices, giving Japan 44%

growth in the number of visitors in 1Q15. By long term relationships with

suppliers, EGL has strong capability to secure hotel rooms, flight bookings

and local bus transportations in peak seasons. We believe the recent robust

demand growth in Japan-bound package tours will give high visibility for the

strong results of EGL in FY15E.

Making a quantum leap in China market: Under CEPA, EGL is expected to

set up branches in China as restrictions have been removed for HKSS. In

addition, EGL will co-operate with other qualified travel agencies in China to

extend their award-winning travel products distribution network into China.

We believe EGL will have a re-rating in valuation by capturing the explosive

Chinese outbound travel market through this two-prong development.

Value play in a hot sector. Initiate BUY: Thanks to the robust demand

growth and favorable policies, Chinese listed travel companies are trading at

high valuation of average 59x forward PE by strong market sentiment in

tourism. As EGL is trading at a deep discount of 86% or 8.0x FY15E PE, we

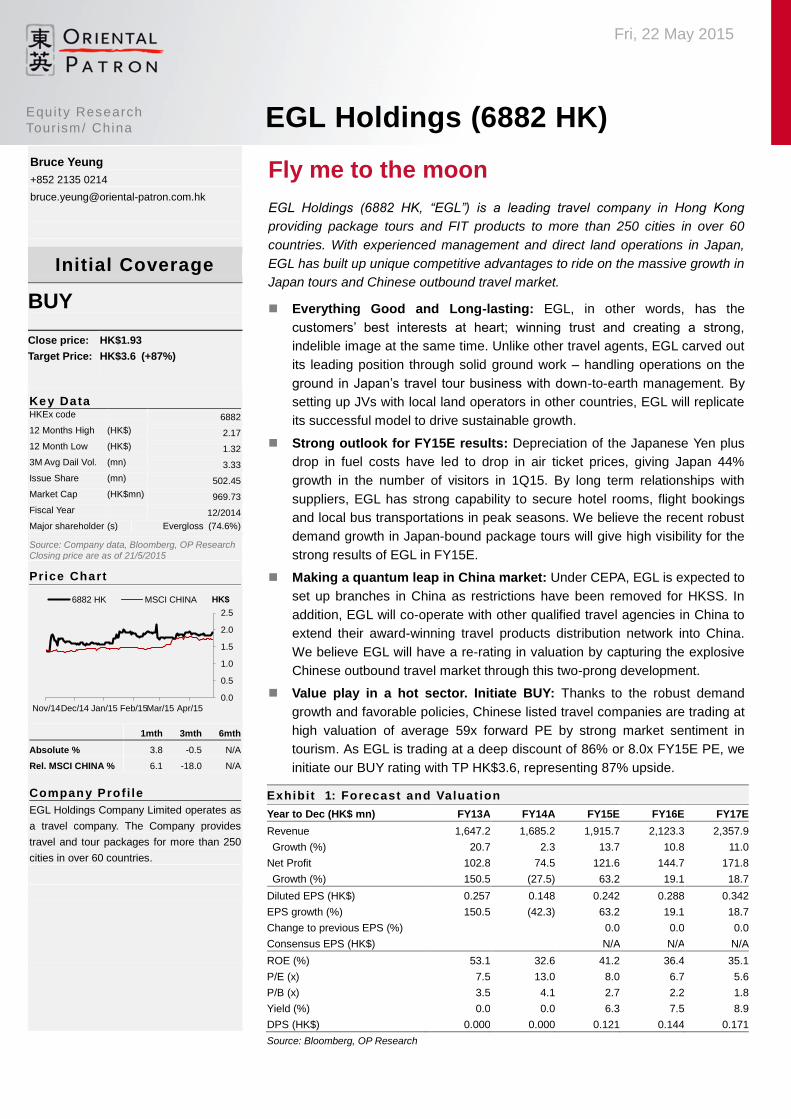

initiate our BUY rating with TP HK$3.6, representing 87% upside.

Bruce Yeung

+852 2135 0214

Initial Coverage

BUY

Close price: HK$1.93

Target Price: HK$3.6 (+87%)

Key Data

HKEx code 6882

12 Months High (HK$) 2.17

12 Month Low (HK$) 1.32

3M Avg Dail Vol. (mn) 3.33

Issue Share (mn) 502.45

Market Cap (HK$mn) 969.73

Fiscal Year 12/2014

Major shareholder (s) Evergloss (74.6%)

Source: Company data, Bloomberg, OP Research

Closing price are as of 21/5/2015

Price Chart

1mth 3mth 6mth

Absolute % 3.8 -0.5 N/A

Rel. MSCI CHINA % 6.1 -18.0 N/A

Company Profi le

EGL Holdings Company Limited operates as

a travel company. The Company provides

travel and tour packages for more than 250

cities in over 60 countries.

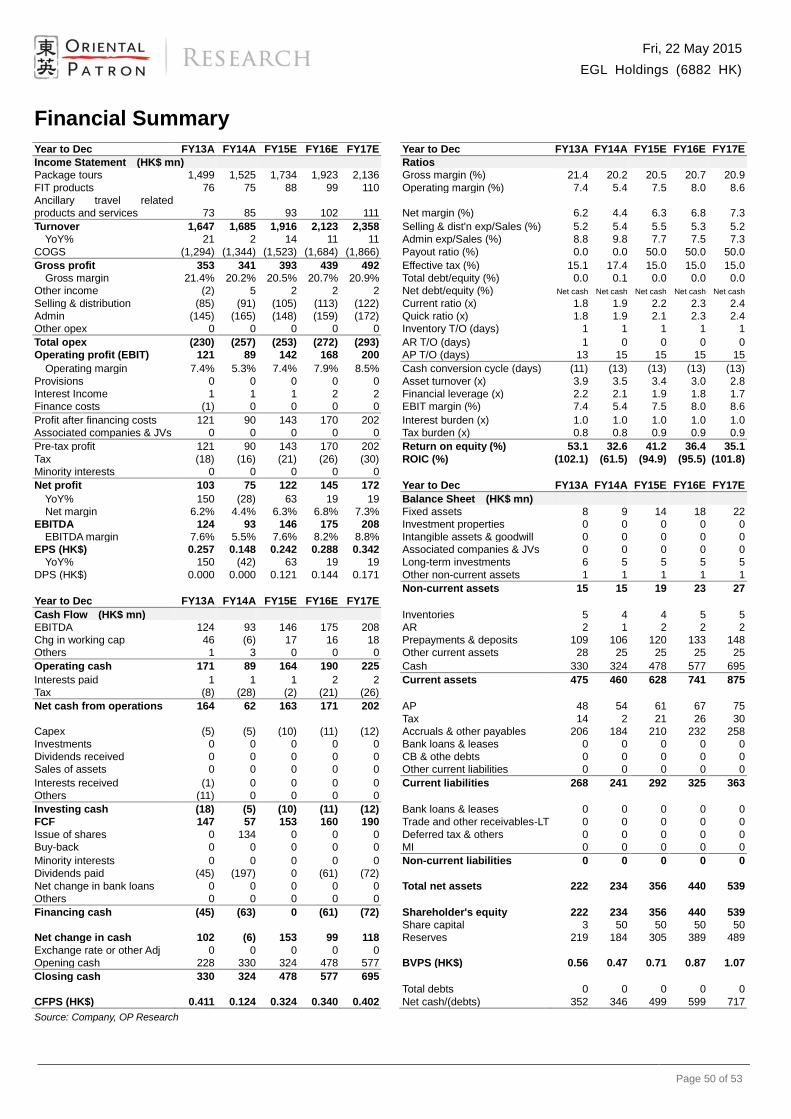

Exhibit 1: Forecast and Valuation Year to Dec (HK$ mn) FY13A FY14A FY15E FY16E FY17E

Revenue 1,647.2 1,685.2 1,915.7 2,123.3 2,357.9

Growth (%) 20.7 2.3 13.7 10.8 11.0

Net Profit 102.8 74.5 121.6 144.7 171.8

Growth (%) 150.5 (27.5) 63.2 19.1 18.7

Diluted EPS (HK$) 0.257 0.148 0.242 0.288 0.342

EPS growth (%) 150.5 (42.3) 63.2 19.1 18.7

Change to previous EPS (%) 0.0 0.0 0.0

Consensus EPS (HK$) N/A N/A N/A

ROE (%) 53.1 32.6 41.2 36.4 35.1

P/E (x) 7.5 13.0 8.0 6.7 5.6

P/B (x) 3.5 4.1 2.7 2.2 1.8

Yield (%) 0.0 0.0 6.3 7.5 8.9

DPS (HK$) 0.000 0.000 0.121 0.144 0.171

Source: Bloomberg, OP Research

0.0

0.5

1.0

1.5

2.0

2.5

Nov/14Dec/14 Jan/15 Feb/15Mar/15 Apr/15

HK$6882 HK MSCI CHINA

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 2 of 53

Table of Contents

Table of Contents ......................................................................................................................................... 2

Investment Summary ................................................................................................................................... 3

Industry overview ......................................................................................................................................... 4

Everything Good and Long-lasting ..............................................................................................................10

Strong outlook for FY15E results ................................................................................................................21

Making a quantum leap in China market .....................................................................................................26

Value play in a hot sector. Initiate BUY ........................................................................................................32

Investment risks ..........................................................................................................................................35

Management background ...........................................................................................................................37

Company history .........................................................................................................................................39

Corporate structure .....................................................................................................................................41

Appendix I: Travel industry market data details ...........................................................................................42

Appendix II: Awards ....................................................................................................................................45

Appendix III: Employee structure ................................................................................................................46

Appendix IV: Properties and branches details .............................................................................................47

Appendix V: Regulations on the industries ..................................................................................................48

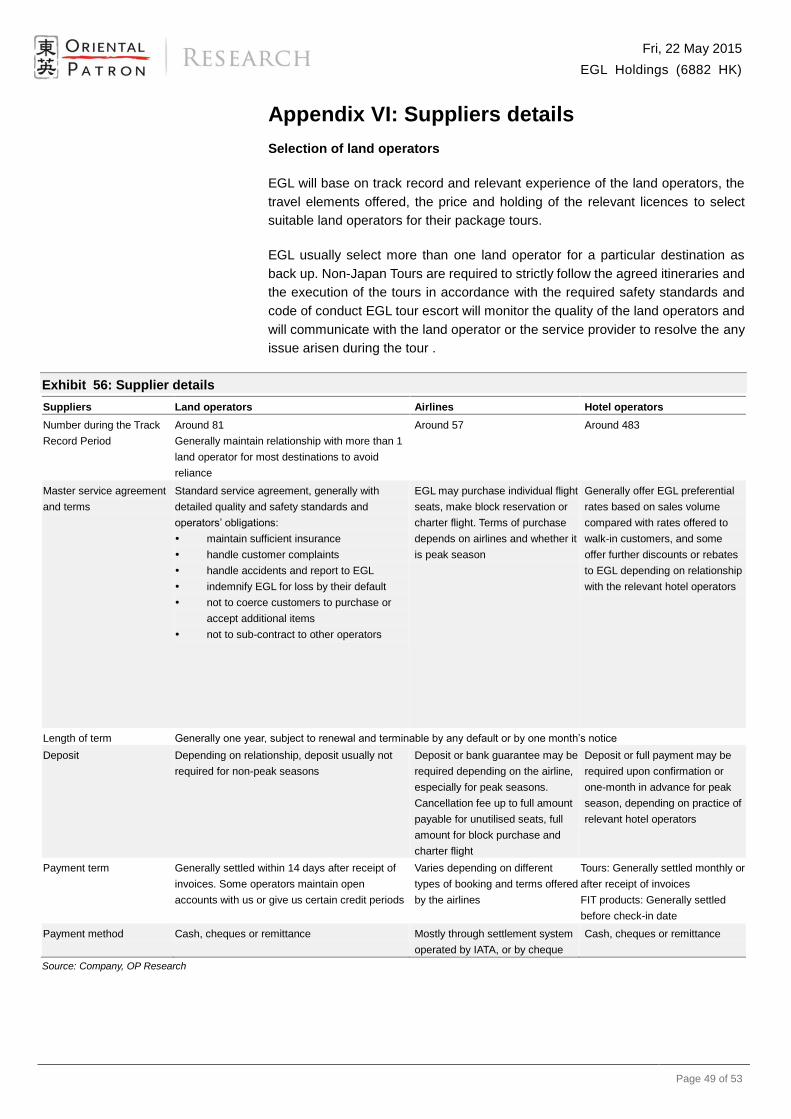

Appendix VI: Suppliers details .....................................................................................................................49

Financial Summary .....................................................................................................................................50

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 3 of 53

Investment Summary

The earth has music for those who listen

EGL is one of the largest travel agencies in Hong Kong providing package tours

and free and independent travelers (“FIT”) products to more than 250 cities in

over 60 countries. Although the current price of EGL is 39% higher than the IPO

listing price in November 2014, we still believe the company has strong upside

potential given (1) unique direct land operations to give strong competitive edge

to Japan-bound travel products (2) a strong earnings growth in FY15E from

Japanese Yen (“JPY”) depreciation (3) capturing the robust outbound travel in

China market (4) undemanding valuation of 8.0x FY15E with 6.3% dividend yield

representing a massive discount of 86% to peers average.

Apart from outsourcing the land operations to third party local travel companies in

the destinations, EGL directly arranges hotel accommodation, bus transportations,

meals and sightseeing activities for Japan-bound package tours. The direct land

operations give EGL strong competitive edge in cost control, quality control,

relations with suppliers, flexibility in product design and development plus wider

products range in FIT products. Although EGL only ranked third with 9.3% of total

market share in Hong Kong, EGL achieved top market share of 31.6% for Japan

tours in 2013 and 18.5% gross margin or 8.3 ppt higher than Non-Japan tours in

FY14.

With JPY depreciating more than 12% and crude oil price dropping over 35%

since 4Q14, stronger real spending power in Japan and lower air ticket costs

triggered strong growth in Japan travel in early 2015. Japan recorded 44% growth

in total number of visitors in 1Q15, with tourists from Hong Kong and China

leading the growth by 60% and 93% respectively. We expect EGL will record

strong FY15E results as high operating leverage with asset-light business nature.

Under the new CEPA Agreement signed on December 2014, 5 travel agency

companies by Hong Kong Service Supplier (“HKSS”) are allowed to operate

Chinese outbound travel in Guangdong province on a pilot basis. Besides, by

teaming up with other local agencies in the cities of Guangdong Province, such

as Shenzhen, Zhongshan and Zhuhai, EGL is switching on their twin engines to

capture the robust demand in Chinese outbound travel in 2H15. As Chinese

mainland travelers have been drifting from low-end Hong Kong & Macau into

mid-high end Japan & Korea, we believe EGL has strong edge to expand in

China market.

We expect EGL will have 63% net profit growth to HK$122 mn or 8.0x FY15E PE,

representing 86% discount to peers average and a 3-year CAGR of 32%. Since

the company plans at least 50% payout ratio on strong cash flow, the forward

dividend yield of 6.3% offers a huge safety margin of best risk-reward ratio. As

travel industry is one of the hottest investment sectors based on tailwind in

Chinese outbound travel and favorable policies, we believe EGL will have a

strong re-rating after the market realizes the treasure inside and our target price

of HK$3.6 implies an attractive 87% upside on target 15x FY15E PE.

EGL has strong upside potential

given direct land operations,

strong growth in FY15E,

expanding into China market and

deep discount to peers

Direct land operations give EGL

strong competitive edge and

result 8.6 ppt higher in gross

margin and top market shares of

31.6%

Japanese Yen depreciation and

drop in air ticket prices triggered

a strong growth in Japan travel in

1Q15.

New CEPA Agreement and

cooperation with local travel

agents open up opportunities for

EGL to capture strong growth in

China market

EGL is trading at 8.0x FY15E PE

with 6.3% dividend yield,

representing 86% discount to

peers average. Our TP implies a

best risk-reward ratio of 87%

upside.

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 4 of 53

Industry overview

The time to relax is when you don’t have time for it

Travel spending is high income elasticity

Demand for vacation, recreation and leisure travel has been generally increasing

with the rising levels of household disposal income. Since travelling and holidays

are superior goods with high income elasticity, the growth of travel spending will

be higher and accelerate than that of disposal income as people have more

desire for recreation and pleasure when they get wealthier.

In Hong Kong and Macau, the average nominal annual household disposal

income increased at CAGR of 4.1% and 11% to HK$615,000 and MOP466,600 in

2013 respectively. Average annual household spending on outbound travel

increased at a higher CAGR of 7.7% and 17.9% to HK$71,066 and MOP90,773

in 2013, as the proportion of disposal income to spend on outbound travel

increased by 1.5ppt and 4.2ppt to 11.6% and 19.5% from 2009 to 2013 in Hong

Kong and Macau respectively.

With higher disposal income and higher proportion to spend on outbound travel, it

is expected average annual household spending on outbound travel will increase

at CAGR of 5.2% and 6.5% from 2014E to 2018E in Hong Kong and Macau

respectively. We think EGL will have higher than market average growth thanks to

the leading position by well-established brand and competitive strength in land

operations in Japan.

Exhibit 2: Hong Kong average annual household spending on outbound

travel

Source: Ipsos Report, OP Research

52,847 58,320

62,985 65,676 71,066

74,949 78,996

83,183 87,508

91,554 10.1%10.8% 10.9% 11.1%

11.6% 11.8% 12.0% 12.3% 12.4% 12.6%

0%

2%

4%

6%

8%

10%

12%

14%

0

20,000

40,000

60,000

80,000

100,000

120,000

2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E

Average annual household spending on outbound travel

% of average annual household disposable income

(HK$)

Spending on outbound travel has

a higher growth than that of

disposal income

10%-20% of disposal income will

be spent on outbound travel in

developed markets

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 5 of 53

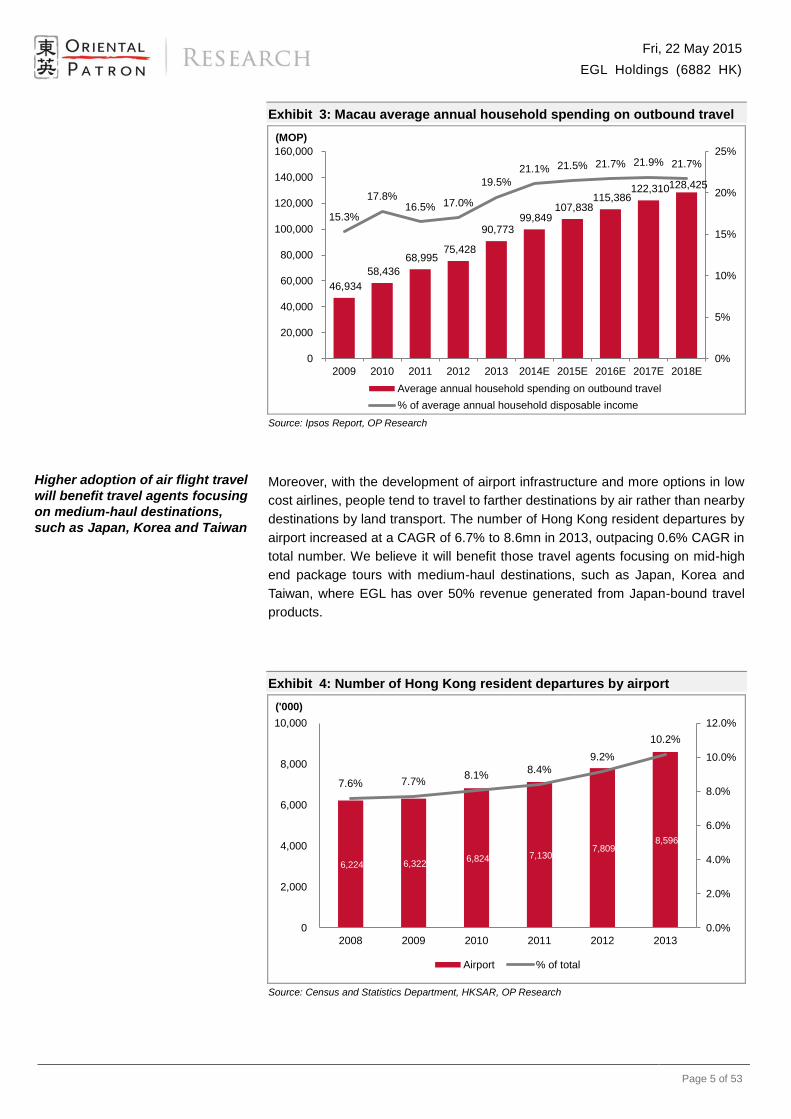

Exhibit 3: Macau average annual household spending on outbound travel

Source: Ipsos Report, OP Research

Moreover, with the development of airport infrastructure and more options in low

cost airlines, people tend to travel to farther destinations by air rather than nearby

destinations by land transport. The number of Hong Kong resident departures by

airport increased at a CAGR of 6.7% to 8.6mn in 2013, outpacing 0.6% CAGR in

total number. We believe it will benefit those travel agents focusing on mid-high

end package tours with medium-haul destinations, such as Japan, Korea and

Taiwan, where EGL has over 50% revenue generated from Japan-bound travel

products.

Exhibit 4: Number of Hong Kong resident departures by airport

Source: Census and Statistics Department, HKSAR, OP Research

46,934

58,436

68,995 75,428

90,773 99,849

107,838 115,386

122,310 128,425

15.3%

17.8%16.5% 17.0%

19.5%

21.1% 21.5% 21.7% 21.9% 21.7%

0%

5%

10%

15%

20%

25%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E

Average annual household spending on outbound travel

% of average annual household disposable income

(MOP)

6,224 6,322 6,824 7,130

7,809 8,596

7.6% 7.7%8.1%

8.4%

9.2%

10.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

2,000

4,000

6,000

8,000

10,000

2008 2009 2010 2011 2012 2013

Airport % of total

('000)

Higher adoption of air flight travel

will benefit travel agents focusing

on medium-haul destinations,

such as Japan, Korea and Taiwan

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 6 of 53

Travel companies maintain a core role for travel products and service

In addition to selling tour products, arranging transportation, accommodation and

catering, travel companies also provide advisory services to customers for

suitable places to visit and design theme tours with special travel elements, such

as overseas wedding, photo shooting, gourmet restaurants and sport events.

Because of difference in languages and time zones, customers still prefer to buy

package tours from travel companies to avoid the difficulties in planning and

arranging travel itinerary in other countries. Besides, with tour escorts to take

care of details during the trips, such as safety and cultural difference, travel

companies maintain a core role in the industry by providing a one-stop travel

solution.

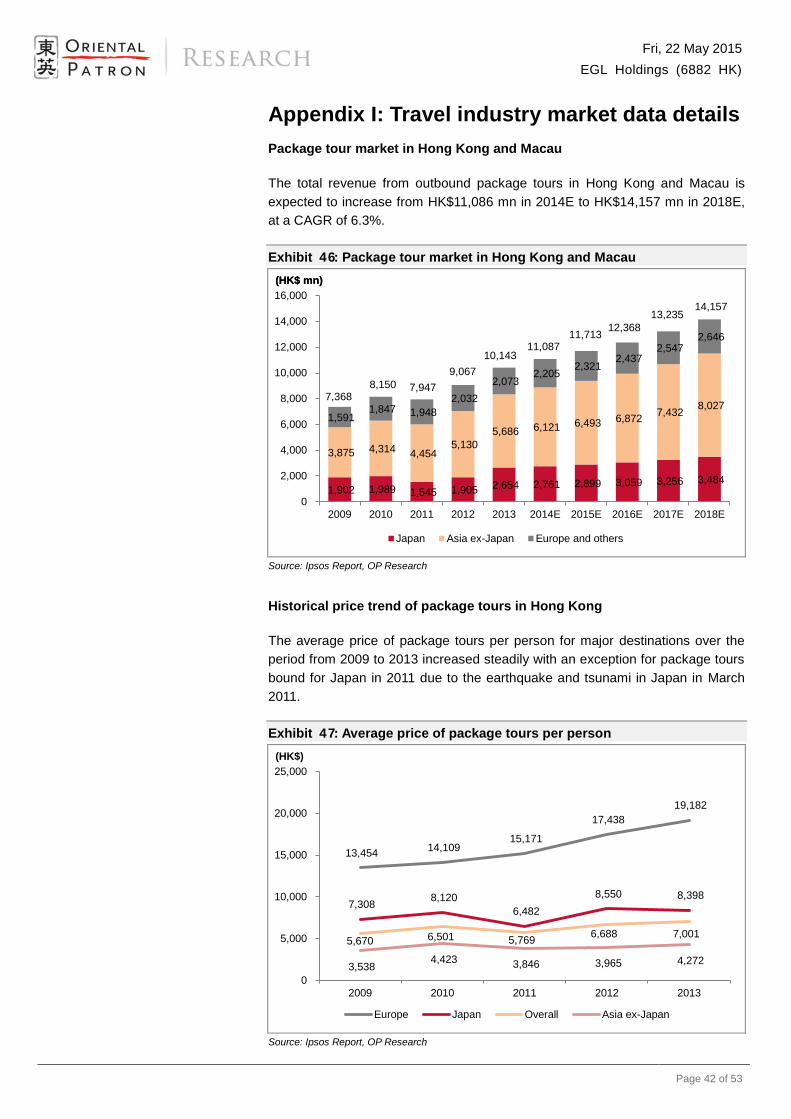

The aggregate revenue for the travel service industry in Hong Kong and Macau

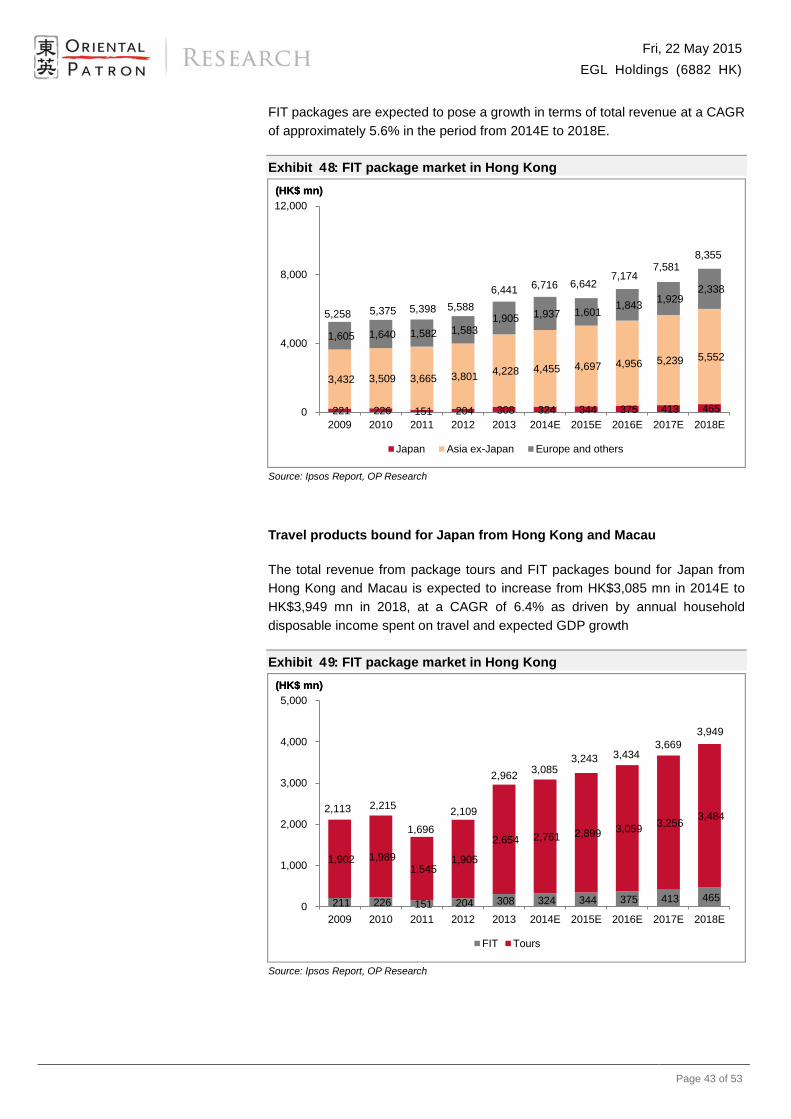

increased at a CAGR of 7.5% to HK$16,855 million in 2013. It is expected to grow

at a CAGR of 6.0% to HK$22,512 million in 2018E. Within this aggregate, 61.8%

was generated by package tours and 38.2% by FIT products in 2013. The growth

of package tours and FIT products is expected to remain stable from 2014E to

2018E at CAGR of 6.3% and 5.6% respectively.

The major costs of package tours are mainly for air tickets and hotel

accommodation, which have generally accounted for 50% and 25% of total cost

of sales and fluctuate with international oil prices as well as demand for hotel

rooms in destinations. Although the selling prices of package tours and FIT

products are normally determined on a cost-plus basis of the travel elements,

customers are willing to pay premium for products and services offered by travel

companies with strong brand recognition and track records of service quality as

there have been smaller travel agents going bankrupt or having serious safety

incidents, such as the Manila hostage crisis, in the past. Since EGL management

has down-to-earth working style as tour guide, their products are designed to

customer needs, such as flexible package tour itinerary, car rental services with

FIT products and custom-made travel insurance. We believe EGL will enjoy a

greater growth than the market average in the long run.

Exhibit 5: Total travel service industry revenue in Hong Kong and Macau

for outbound travel

Source: Ipsos Report, OP Research

11,641 12,371 12,276 13,167 14,966 15,712 16,085 17,063 18,120

19,810

975 1,154 1,068

1,490

1,899 2,090 2,291

2,489 2,695

2,902

12,616 13,525 13,344

14,657

16,865 17,802 18,376

19,552 20,815

22,712

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E

Macau

Hong Kong

Total travel service industry revenue in HK and Macau (outbound)

(HK$ mn)

Travel companies provide

one-stop solutions to travel in

other countries

Travel service industry revenue

will have a CAGR of 6% during

2014E-2018E

Air tickets and hotel room

charges accounted for 50% and

25% of the total cost of sales

Brand recognition and service

quality are the key to gaining

customers in competitive travel

market

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 7 of 53

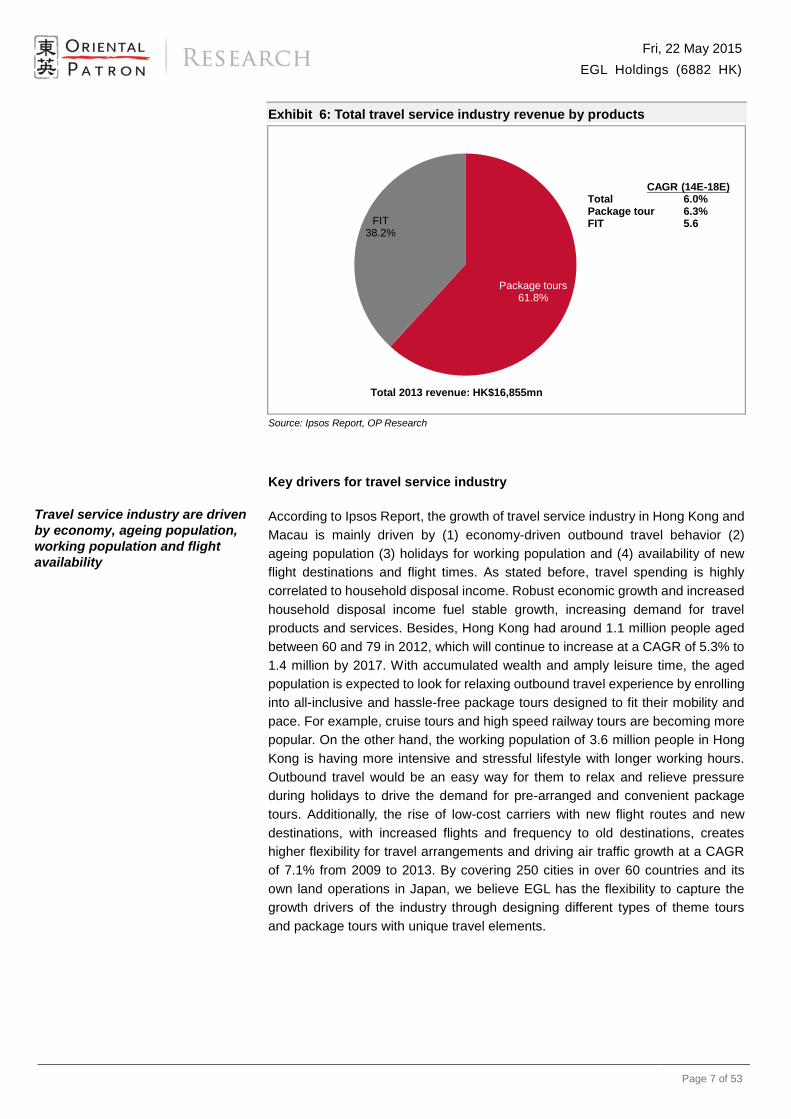

Exhibit 6: Total travel service industry revenue by products

Source: Ipsos Report, OP Research

Key drivers for travel service industry

According to Ipsos Report, the growth of travel service industry in Hong Kong and

Macau is mainly driven by (1) economy-driven outbound travel behavior (2)

ageing population (3) holidays for working population and (4) availability of new

flight destinations and flight times. As stated before, travel spending is highly

correlated to household disposal income. Robust economic growth and increased

household disposal income fuel stable growth, increasing demand for travel

products and services. Besides, Hong Kong had around 1.1 million people aged

between 60 and 79 in 2012, which will continue to increase at a CAGR of 5.3% to

1.4 million by 2017. With accumulated wealth and amply leisure time, the aged

population is expected to look for relaxing outbound travel experience by enrolling

into all-inclusive and hassle-free package tours designed to fit their mobility and

pace. For example, cruise tours and high speed railway tours are becoming more

popular. On the other hand, the working population of 3.6 million people in Hong

Kong is having more intensive and stressful lifestyle with longer working hours.

Outbound travel would be an easy way for them to relax and relieve pressure

during holidays to drive the demand for pre-arranged and convenient package

tours. Additionally, the rise of low-cost carriers with new flight routes and new

destinations, with increased flights and frequency to old destinations, creates

higher flexibility for travel arrangements and driving air traffic growth at a CAGR

of 7.1% from 2009 to 2013. By covering 250 cities in over 60 countries and its

own land operations in Japan, we believe EGL has the flexibility to capture the

growth drivers of the industry through designing different types of theme tours

and package tours with unique travel elements.

Package tours61.8%

FIT 38.2%

Total 2013 revenue: HK$16,855mn

CAGR (14E-18E)Total 6.0%Package tour 6.3%FIT 5.6

Travel service industry are driven

by economy, ageing population,

working population and flight

availability

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 8 of 53

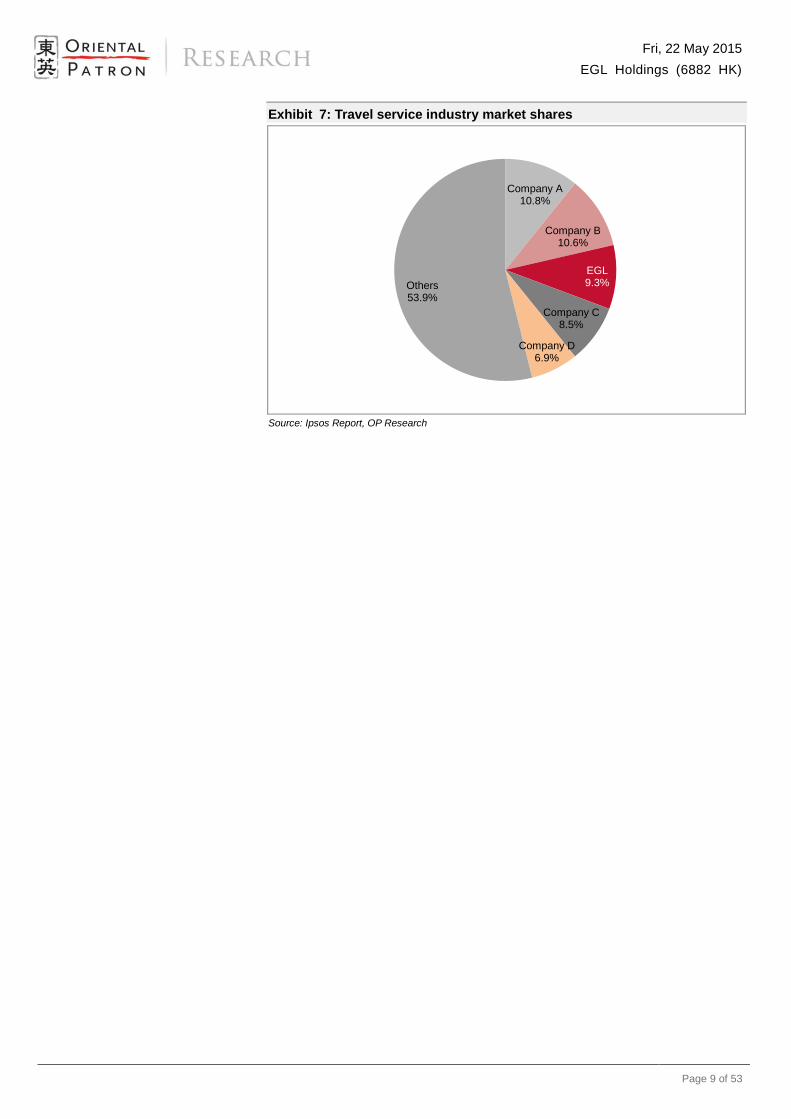

Competitive landscape: A consolidated market with few leaders

In 2013, the top five licensed travel companies in Hong Kong and Macau

accounted for almost 50% of the total industry revenue in 2013 largely due to (1)

scale of establishment (2) industry recognition and (3) abilities to explore new

travel options. With economy of scale, larger travel agents can secure air flights

at peak season by chartered flights. For the HK$16,855 million aggregated

revenue of travel service industry in 2013, EGL ranked the third and had 8.9%,

8.9% and 9.3% of the total market share in 2011, 2012 and 2013 respectively.

Local land operations in Japan and long term direct relations with suppliers

enable EGL to design unique tour itinerary and to secure hotel rooms as well as

bus transportation in peak seasons. EGL shows their competitive strength and

has been the top travel company in the Japan-bound package tour market in

Hong Kong with 32.5%, 29.6% and 31.6% market share in 2011, 2012 and 2013

respectively.

With unique featured items, such as car rental services, theme part tickets,

railway passes and custom-made insurance, EGL can differentiate their FIT

products in the competitive and homogeneous market. EGL was the top travel

company in the Japan-bound FIT market in Hong Kong with 16.2%, 15.2% and

14.3% market share in 2011, 2012 and 2013 respectively.

EGL has direct access to travel elements supply

In 2013, there were 1,466 of 1,698 licensed travel companies in Hong Kong

providing outbound travel products and services according to Ipsos Report.

Because of smaller market, there were 207 licensed travel companies providing

inbound and outbound travel products and services in Macau. The large number

of participants in the market is due to relatively low entry barrier for travel agent

licences. However, most of the travel companies act somehow like third party

agent without direct access to the travel elements supply as it involves much

more investment and operating history to secure the necessary ties with

suppliers.

IATA Passenger Agency Programme is a global program designed to facilitate the

secure distribution and sale of airline tickets. Only IATA accredited agents are

allowed to represent the member airlines of IATA to sell international air

passenger tickets. In July 2014, there were only 322 and 18 IATA accredited

travel companies in Hong Kong and Macau respectively. With their long operating

history and dedicated involvement in the industry, EGL Tours and EGL Macau

have been IATA accredited agents since 1991 and 2008, respectively.

Top five companies accounting

for almost 50% market shares

EGL ranked the third and had

9.3% market shares in 2013

EGL ranked first and had 31.6% of

Japan-bound package tour

market share in 2013

EGL also ranked first and had

14.3% of Japan-bound FIT market

share in 2013

1,698 and 207 licensed travel

companies in Hong Kong and

Macau in 2013

Only IATA accredited agents are

allowed to sell air tickets for its

members

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 9 of 53

Exhibit 7: Travel service industry market shares

Source: Ipsos Report, OP Research

Company A10.8%

Company B10.6%

EGL9.3%

Company C8.5%

Company D6.9%

Others53.9%

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 10 of 53

Everything Good and Long-lasting

Success comes from Within not Without

Founded in 1987, EGL strives to deliver consistent quality tours, travel products

and services that leave a pleasant impression with customers by having

customers’ best interests at heart as epitomised by “EGL – Everything Good and

Long-lasting”. Under the award-winning “東瀛遊 EGL Tours” brand, EGL

became a leading travel company, ranking third with 9.3% market share, with

354,434 customers purchasing their travel products to over 250 cities in more

than 60 countries in 2013. We believe EGL, as a leading travel company with a

reputable brand of safe and carefree travelling, can utilize their market-leader

status and established business model to capture the industry growth trend to

increase market share under multiple expansion opportunities.

Unlike other travel agents, that are driven by down-to-earth management, EGL

created its leading position by its own travel tour ground handling operations in

Japan and they were at the top in Japan-bound package tour market and

Japan-bound FIT products market with 31.6% and 14.3% shares in 2013

respectively. EGL management possesses over 30 years of experience in the

travel industry and has been working as the same team in the last 28 years. In

order to control products and services quality, rather than outsourcing to third

party local land operators with less costs in investment and staff training, EGL has

its own land operations in the destinations for Japan-bound package tours to

achieve higher customer satisfaction and repeat customers (28.6%, 29.5% and

29.0% in 2011, 2012 and 2013 respectively).

Special business model derives special value

In order to lower the investment costs and human resources involvement, travel

agents will only arrange flights and sometimes hotel accommodations to run a

package tour. They will normally outsource land operations in the destinations to

third party travel service providers. Tour escorts will be assigned to accompany

the tour group throughout the tour to serve customers and ensure satisfactory

performance of the land operators. Like industry peers, EGL adopts the

outsourcing model for Non-Japan Tours as their expertise is on Japan tours as

illustrated by the brand name.

EGL secure their competitive advantages in Japan Tours by directly carrying out

the tour operation, which includes the arrangements for hotels accommodation,

local transportation, meals, guides and sightseeing activities in the destinations.

EGL tour escorts for Japan Tours are provided with up-to-date training to meet

the service standard to have good understanding in Japanese culture, its

customs and information of scenic spots and tourist attractions.

EGL’s motto: “Strive for

consistent improvement of

high-quality service, with

customer in our heart and

sincerity”

High customer satisfactory

proved by high percentage of

repeat customers

Like its industry peers, EGL

adopts outsourcing model for

Non-Japan Tours

EGL has expertise in Japan Tours

by its direct land operations

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 11 of 53

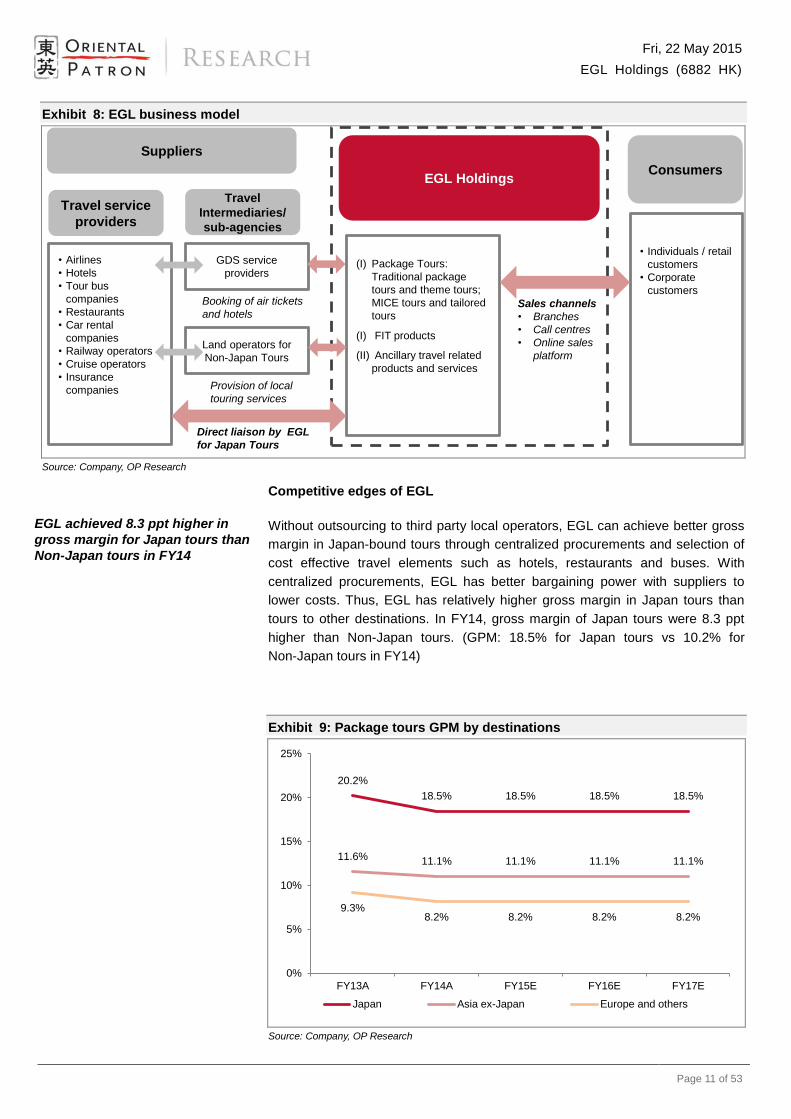

Exhibit 8: EGL business model

Source: Company, OP Research

Competitive edges of EGL

Without outsourcing to third party local operators, EGL can achieve better gross

margin in Japan-bound tours through centralized procurements and selection of

cost effective travel elements such as hotels, restaurants and buses. With

centralized procurements, EGL has better bargaining power with suppliers to

lower costs. Thus, EGL has relatively higher gross margin in Japan tours than

tours to other destinations. In FY14, gross margin of Japan tours were 8.3 ppt

higher than Non-Japan tours. (GPM: 18.5% for Japan tours vs 10.2% for

Non-Japan tours in FY14)

Exhibit 9: Package tours GPM by destinations

Source: Company, OP Research

Suppliers

Travel service

providers

Travel

Intermediaries/

sub-agencies

EGL HoldingsConsumers

• Airlines

• Hotels

• Tour bus

companies

• Restaurants

• Car rental

companies

• Railway operators

• Cruise operators

• Insurance

companies

GDS service

providers

Land operators for

Non-Japan Tours

Booking of air tickets

and hotels

Provision of local

touring services

Direct liaison by EGL

for Japan Tours

(I) Package Tours:

Traditional package

tours and theme tours;

MICE tours and tailored

tours

(I) FIT products

(II) Ancillary travel related

products and services

Sales channels

• Branches

• Call centres

• Online sales

platform

• Individuals / retail

customers

• Corporate

customers

20.2%

18.5% 18.5% 18.5% 18.5%

11.6% 11.1% 11.1% 11.1% 11.1%

9.3%8.2% 8.2% 8.2% 8.2%

0%

5%

10%

15%

20%

25%

FY13A FY14A FY15E FY16E FY17E

Japan Asia ex-Japan Europe and others

EGL achieved 8.3 ppt higher in

gross margin for Japan tours than

Non-Japan tours in FY14

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 12 of 53

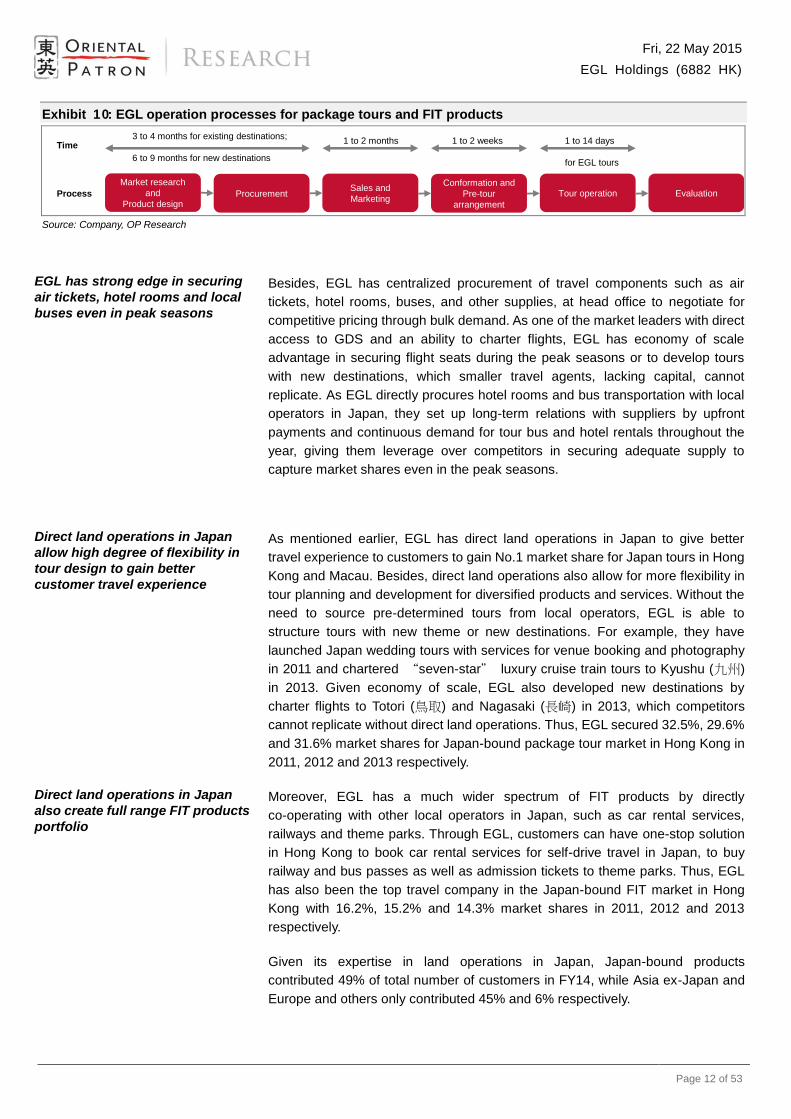

Exhibit 10: EGL operation processes for package tours and FIT products

Source: Company, OP Research

Besides, EGL has centralized procurement of travel components such as air

tickets, hotel rooms, buses, and other supplies, at head office to negotiate for

competitive pricing through bulk demand. As one of the market leaders with direct

access to GDS and an ability to charter flights, EGL has economy of scale

advantage in securing flight seats during the peak seasons or to develop tours

with new destinations, which smaller travel agents, lacking capital, cannot

replicate. As EGL directly procures hotel rooms and bus transportation with local

operators in Japan, they set up long-term relations with suppliers by upfront

payments and continuous demand for tour bus and hotel rentals throughout the

year, giving them leverage over competitors in securing adequate supply to

capture market shares even in the peak seasons.

As mentioned earlier, EGL has direct land operations in Japan to give better

travel experience to customers to gain No.1 market share for Japan tours in Hong

Kong and Macau. Besides, direct land operations also allow for more flexibility in

tour planning and development for diversified products and services. Without the

need to source pre-determined tours from local operators, EGL is able to

structure tours with new theme or new destinations. For example, they have

launched Japan wedding tours with services for venue booking and photography

in 2011 and chartered “seven-star” luxury cruise train tours to Kyushu (九州)

in 2013. Given economy of scale, EGL also developed new destinations by

charter flights to Totori (鳥取) and Nagasaki (長崎) in 2013, which competitors

cannot replicate without direct land operations. Thus, EGL secured 32.5%, 29.6%

and 31.6% market shares for Japan-bound package tour market in Hong Kong in

2011, 2012 and 2013 respectively.

Moreover, EGL has a much wider spectrum of FIT products by directly

co-operating with other local operators in Japan, such as car rental services,

railways and theme parks. Through EGL, customers can have one-stop solution

in Hong Kong to book car rental services for self-drive travel in Japan, to buy

railway and bus passes as well as admission tickets to theme parks. Thus, EGL

has also been the top travel company in the Japan-bound FIT market in Hong

Kong with 16.2%, 15.2% and 14.3% market shares in 2011, 2012 and 2013

respectively.

Given its expertise in land operations in Japan, Japan-bound products

contributed 49% of total number of customers in FY14, while Asia ex-Japan and

Europe and others only contributed 45% and 6% respectively.

Time

Market research

and

Product designProcurement

Sales and

Marketing

Conformation and

Pre-tour

arrangement

Tour operation Evaluation

3 to 4 months for existing destinations;

6 to 9 months for new destinations

1 to 2 months 1 to 2 weeks 1 to 14 days

for EGL tours

Process

EGL has strong edge in securing

air tickets, hotel rooms and local

buses even in peak seasons

Direct land operations in Japan

allow high degree of flexibility in

tour design to gain better

customer travel experience

Direct land operations in Japan

also create full range FIT products

portfolio

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 13 of 53

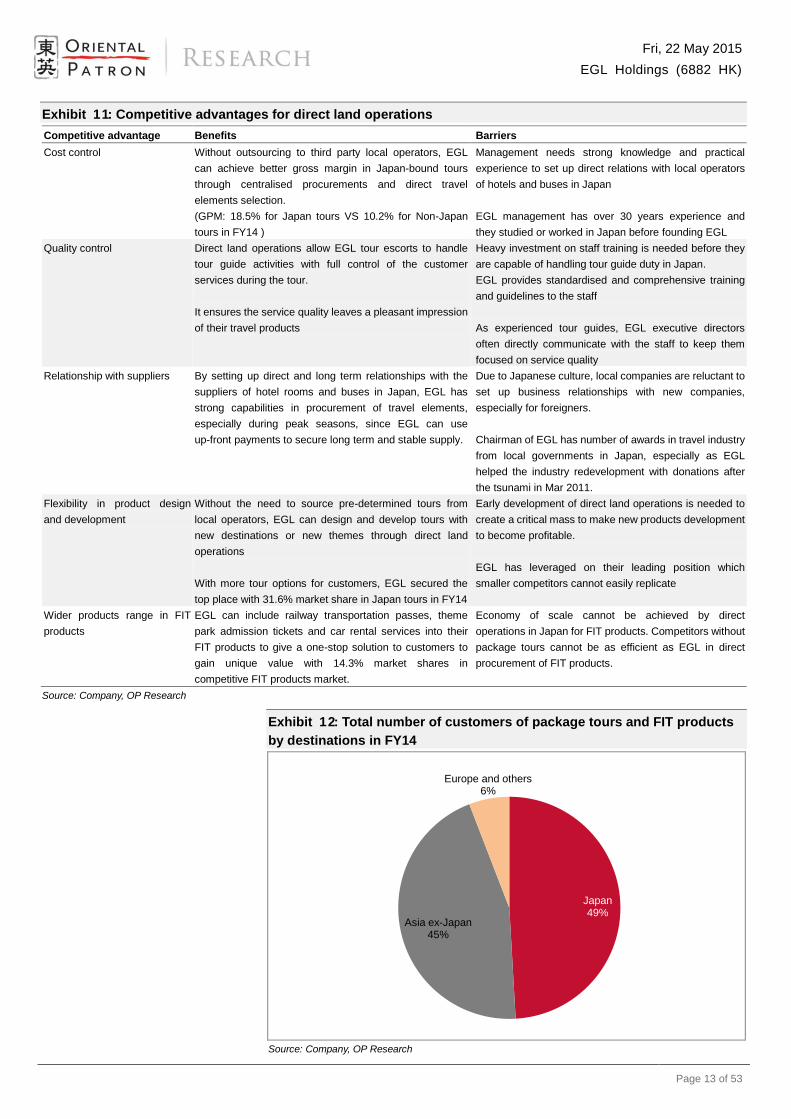

Exhibit 11: Competitive advantages for direct land operations

Competitive advantage Benefits Barriers

Cost control Without outsourcing to third party local operators, EGL

can achieve better gross margin in Japan-bound tours

through centralised procurements and direct travel

elements selection.

(GPM: 18.5% for Japan tours VS 10.2% for Non-Japan

tours in FY14 )

Management needs strong knowledge and practical

experience to set up direct relations with local operators

of hotels and buses in Japan

EGL management has over 30 years experience and

they studied or worked in Japan before founding EGL

Quality control Direct land operations allow EGL tour escorts to handle

tour guide activities with full control of the customer

services during the tour.

It ensures the service quality leaves a pleasant impression

of their travel products

Heavy investment on staff training is needed before they

are capable of handling tour guide duty in Japan.

EGL provides standardised and comprehensive training

and guidelines to the staff

As experienced tour guides, EGL executive directors

often directly communicate with the staff to keep them

focused on service quality

Relationship with suppliers By setting up direct and long term relationships with the

suppliers of hotel rooms and buses in Japan, EGL has

strong capabilities in procurement of travel elements,

especially during peak seasons, since EGL can use

up-front payments to secure long term and stable supply.

Due to Japanese culture, local companies are reluctant to

set up business relationships with new companies,

especially for foreigners.

Chairman of EGL has number of awards in travel industry

from local governments in Japan, especially as EGL

helped the industry redevelopment with donations after

the tsunami in Mar 2011.

Flexibility in product design

and development

Without the need to source pre-determined tours from

local operators, EGL can design and develop tours with

new destinations or new themes through direct land

operations

With more tour options for customers, EGL secured the

top place with 31.6% market share in Japan tours in FY14

Early development of direct land operations is needed to

create a critical mass to make new products development

to become profitable.

EGL has leveraged on their leading position which

smaller competitors cannot easily replicate

Wider products range in FIT

products

EGL can include railway transportation passes, theme

park admission tickets and car rental services into their

FIT products to give a one-stop solution to customers to

gain unique value with 14.3% market shares in

competitive FIT products market.

Economy of scale cannot be achieved by direct

operations in Japan for FIT products. Competitors without

package tours cannot be as efficient as EGL in direct

procurement of FIT products.

Source: Company, OP Research

Exhibit 12: Total number of customers of package tours and FIT products

by destinations in FY14

Source: Company, OP Research

Japan49%

Asia ex-Japan45%

Europe and others6%

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 14 of 53

Apart from higher margin yield and enhancing service quality from direct land

operations, EGL also has a strong competitive edge throughout the whole

operation process. Because of in-depth knowledge of Japan and tour operations,

EGL executive directors will also escort tours and conduct site visits to new and

existing tour destinations from time to time to seek new tour destinations, new

attractions and travel elements, such as new hotels to include in package tours or

FIT products. By considering market trends, customers’ feedback and availability

of flights, land operators and hotels, EGL aims to introduce new package tours

every few months with new destinations, new themes of local festivities or new

activities.

EGL has strong physical sales presence with seven branches in Hong Kong and

one in Macau. Sales representatives in the branches can provide visual

merchandise tour marketing brochures and promote the latest special offers. By

centralizing its booking system, tour availability enquiries, tour selections and tour

reservations, bookings can be efficiently made in these branches to facilitate the

sales process. With relatively high rental expenses for expanding the number of

outlets, EGL has developed cost effective sales channels of call centers and

online platform. Customers can make enquiries and bookings through sales

representatives on the hotlines, which is almost the same as the way it is done in

the branches.

Given the faster pace of life and higher mobile network adaptation, EGL has a

website (www.egltours.com) to work as a sales and marketing platform for online

payment as well as product promotions and information around the clock without

limitation of branch opening and closing hours. Purchase through online platform

increased at a CAGR of 15.1% from 2009 to 2012, which was higher than

traditional channel like online travel platforms in China, such as Ctrip.com and

Tiniu.com.

Exhibit 13: Revenue by sales channel in FY13

Source: Ipsos Report, OP Research

Note: Others include direct sale of MICE products to corporate customers, sale of FIT products to other travel agents, and commission rebate from suppliers.

Branches64.3%

Call centres and online sales

platform26.2%

Others9.5%

EGL management has dedicated

involvement in product

development

EGL has sales channels of eight

branches, call centers and online

platform

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 15 of 53

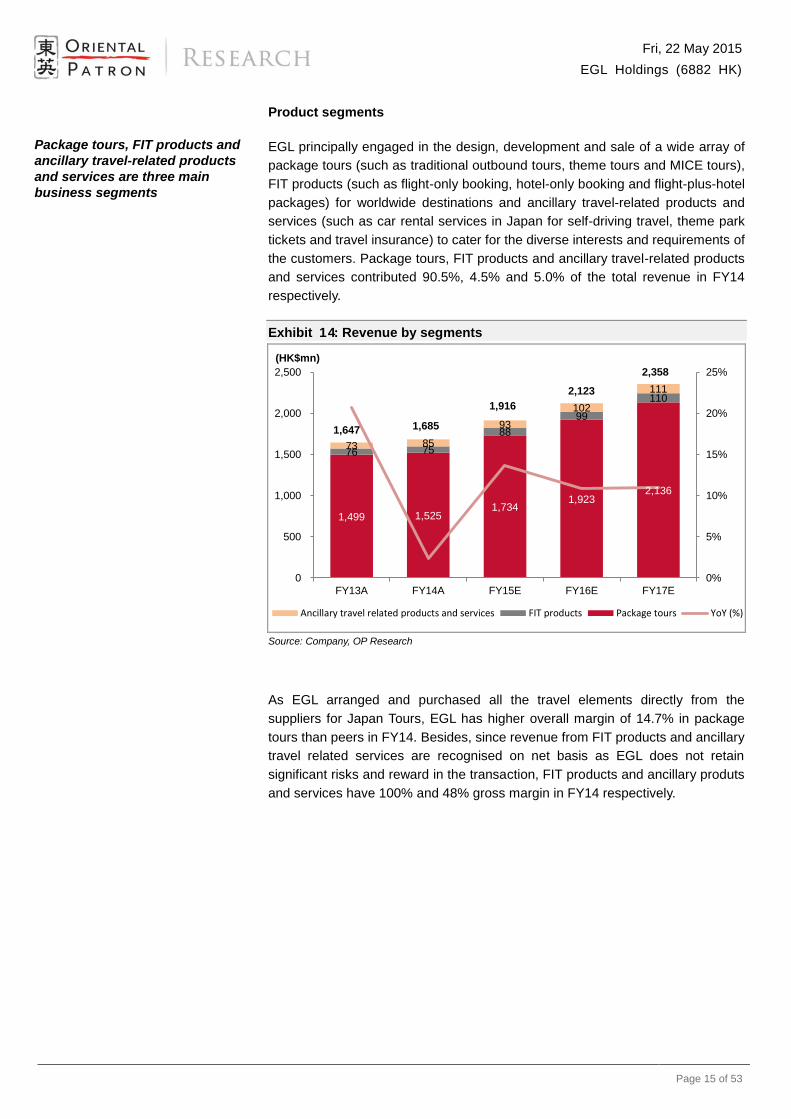

Product segments

EGL principally engaged in the design, development and sale of a wide array of

package tours (such as traditional outbound tours, theme tours and MICE tours),

FIT products (such as flight-only booking, hotel-only booking and flight-plus-hotel

packages) for worldwide destinations and ancillary travel-related products and

services (such as car rental services in Japan for self-driving travel, theme park

tickets and travel insurance) to cater for the diverse interests and requirements of

the customers. Package tours, FIT products and ancillary travel-related products

and services contributed 90.5%, 4.5% and 5.0% of the total revenue in FY14

respectively.

Exhibit 14: Revenue by segments

Source: Company, OP Research

As EGL arranged and purchased all the travel elements directly from the

suppliers for Japan Tours, EGL has higher overall margin of 14.7% in package

tours than peers in FY14. Besides, since revenue from FIT products and ancillary

travel related services are recognised on net basis as EGL does not retain

significant risks and reward in the transaction, FIT products and ancillary produts

and services have 100% and 48% gross margin in FY14 respectively.

1,499 1,525 1,734

1,923 2,136

76 75

88

99

110

73 85

93

102

111

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

FY13A FY14A FY15E FY16E FY17E

Ancillary travel related products and services FIT products Package tours YoY (%)

1,647 1,685

1,916

2,123

2,358

(HK$mn)

Package tours, FIT products and

ancillary travel-related products

and services are three main

business segments

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 16 of 53

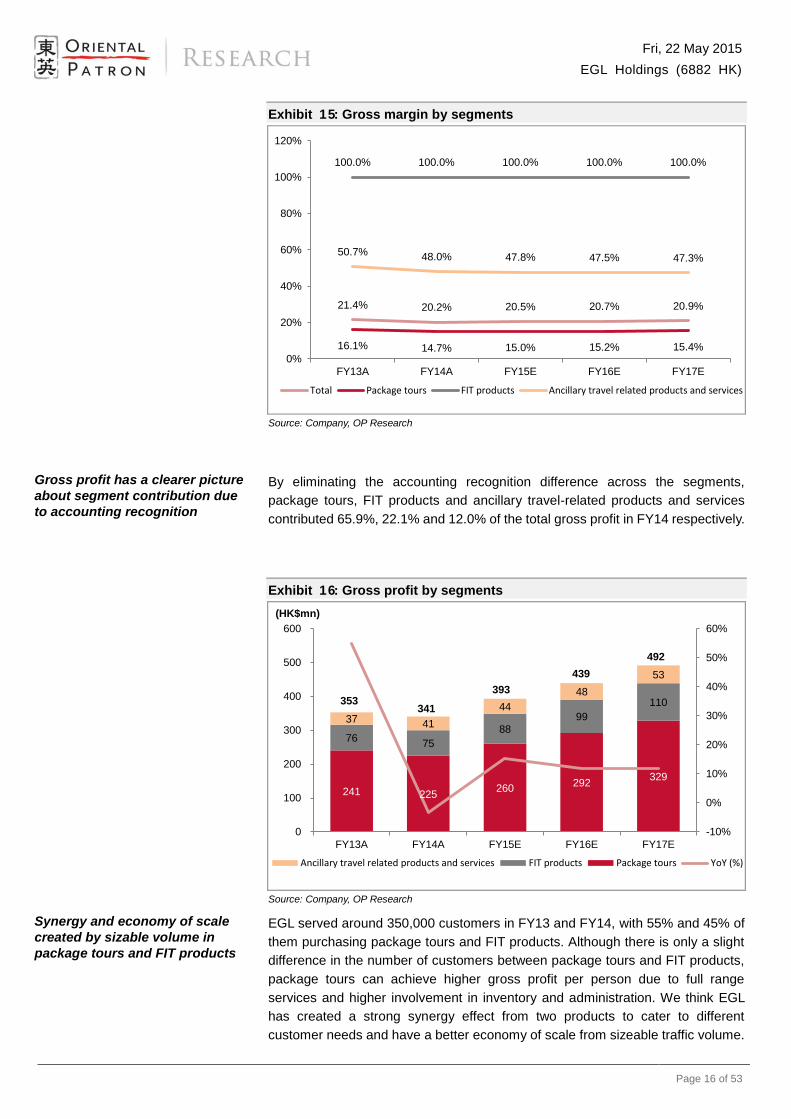

Exhibit 15: Gross margin by segments

Source: Company, OP Research

By eliminating the accounting recognition difference across the segments,

package tours, FIT products and ancillary travel-related products and services

contributed 65.9%, 22.1% and 12.0% of the total gross profit in FY14 respectively.

Exhibit 16: Gross profit by segments

Source: Company, OP Research

EGL served around 350,000 customers in FY13 and FY14, with 55% and 45% of

them purchasing package tours and FIT products. Although there is only a slight

difference in the number of customers between package tours and FIT products,

package tours can achieve higher gross profit per person due to full range

services and higher involvement in inventory and administration. We think EGL

has created a strong synergy effect from two products to cater to different

customer needs and have a better economy of scale from sizeable traffic volume.

21.4% 20.2% 20.5% 20.7% 20.9%

16.1% 14.7% 15.0% 15.2% 15.4%

100.0% 100.0% 100.0% 100.0% 100.0%

50.7% 48.0% 47.8% 47.5% 47.3%

0%

20%

40%

60%

80%

100%

120%

FY13A FY14A FY15E FY16E FY17E

Total Package tours FIT products Ancillary travel related products and services

241 225 260

292 329

76 75

88

99

110

37 41

44

48

53

-10%

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

FY13A FY14A FY15E FY16E FY17E

Ancillary travel related products and services FIT products Package tours YoY (%)

353341

393

439

492

(HK$mn)

Gross profit has a clearer picture

about segment contribution due

to accounting recognition

Synergy and economy of scale

created by sizable volume in

package tours and FIT products

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 17 of 53

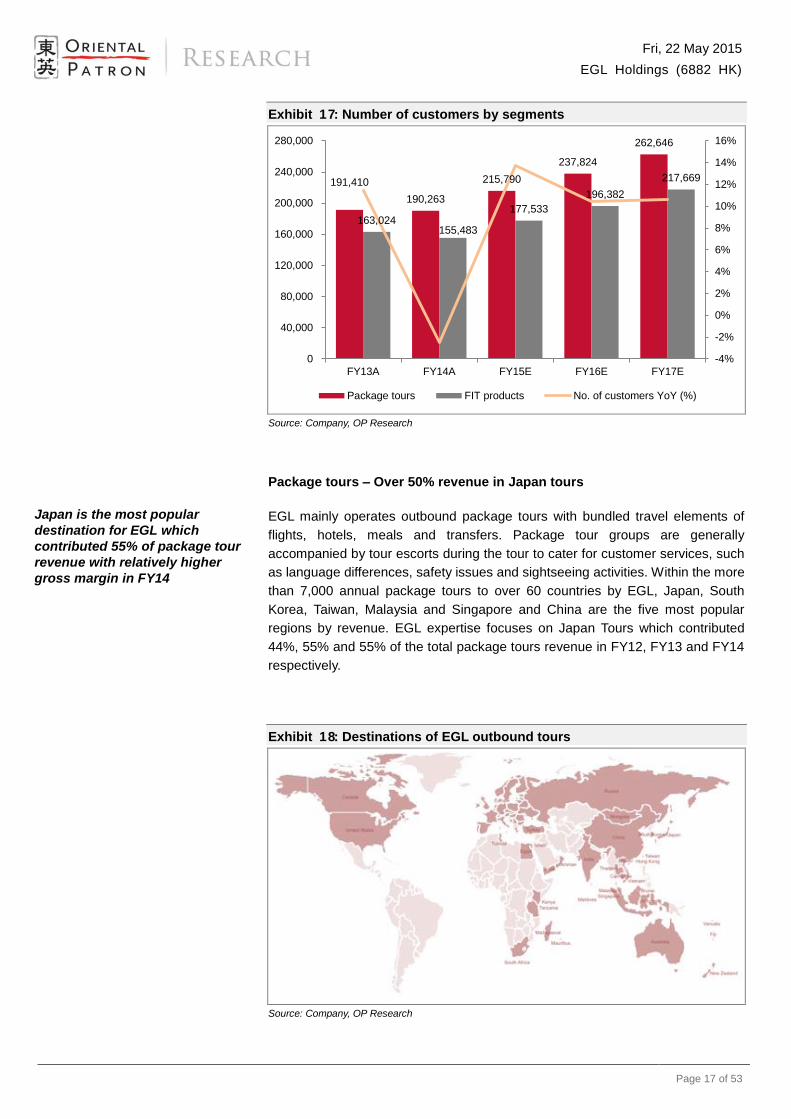

Exhibit 17: Number of customers by segments

Source: Company, OP Research

Package tours – Over 50% revenue in Japan tours

EGL mainly operates outbound package tours with bundled travel elements of

flights, hotels, meals and transfers. Package tour groups are generally

accompanied by tour escorts during the tour to cater for customer services, such

as language differences, safety issues and sightseeing activities. Within the more

than 7,000 annual package tours to over 60 countries by EGL, Japan, South

Korea, Taiwan, Malaysia and Singapore and China are the five most popular

regions by revenue. EGL expertise focuses on Japan Tours which contributed

44%, 55% and 55% of the total package tours revenue in FY12, FY13 and FY14

respectively.

Exhibit 18: Destinations of EGL outbound tours

Source: Company, OP Research

191,410

190,263

215,790

237,824

262,646

163,024 155,483

177,533

196,382

217,669

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

40,000

80,000

120,000

160,000

200,000

240,000

280,000

FY13A FY14A FY15E FY16E FY17E

Package tours FIT products No. of customers YoY (%)

Japan is the most popular

destination for EGL which

contributed 55% of package tour

revenue with relatively higher

gross margin in FY14

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 18 of 53

Exhibit 19: Package tours revenue by destinations

Source: Company, OP Research

FIT products and packages – one-stop travel solutions service provider

To cater to the needs of flexibility, independence and freedom of non-escorted

travel, EGL developed FIT products and packages, such as flight-only booking,

hotel-only booking and flight-plus-hotel bundled packages on their brand image,

experience and well-established relationship with suppliers. Because of direct

operation experience and well-established relationship with hotels in Japan, EGL

is able to provide more accommodation options from quality hotels at more

competitive prices than other competitors in the market, where over 50% of FIT

products are bound for Japan.

Exhibit 20: FIT products revenue by destinations

Source: Company, OP Research

823 839

1,017

1,170

1,345

493 465 474 498 523

183 221 243 255 268

0%

20%

40%

0

400

800

1,200

1,600

FY13A FY14A FY15E FY16E FY17E

Japan Asia ex-Japan Europe and others Package tours YoY (%)

(HK$mn)

49 48

60

69

79

25 25 25 26 28

2 3 3 3 4

-20%

0%

20%

40%

0

20

40

60

80

100

FY13A FY14A FY15E FY16E FY17E

Japan Asia ex-Japan Europe and others FIT products (%)

(HK$mn)

EGL leveraged on their network

strength in Japan for FIT products

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 19 of 53

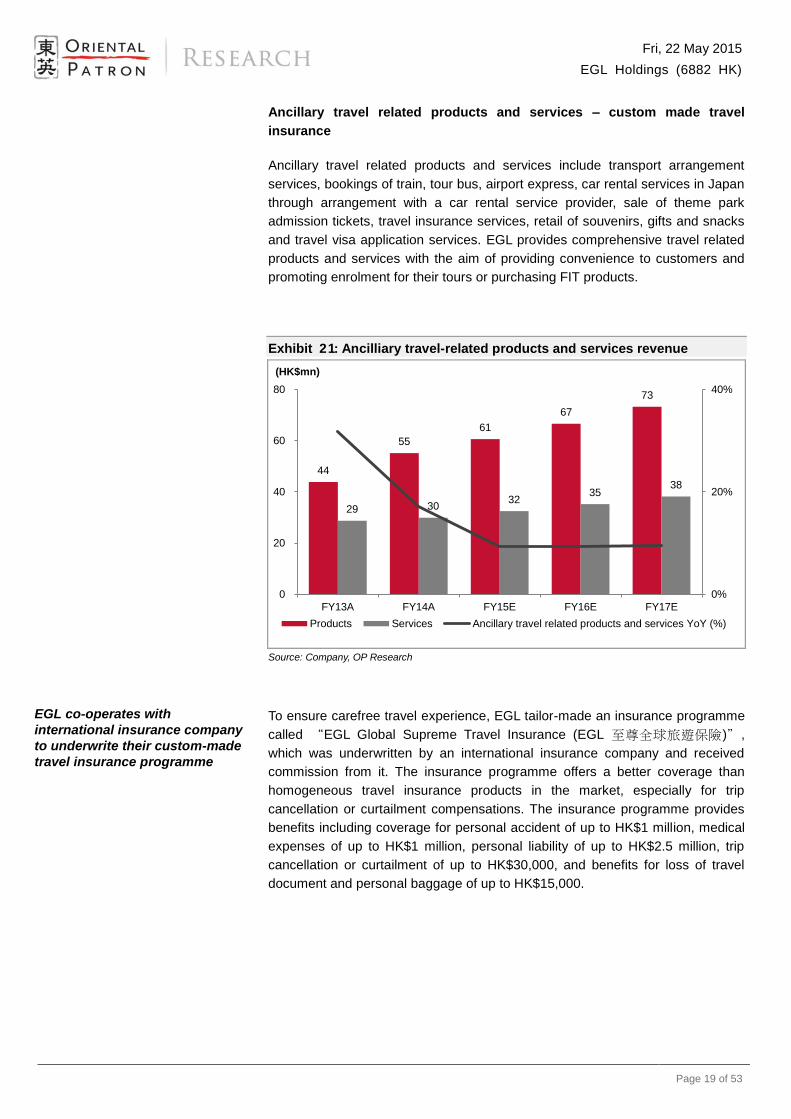

Ancillary travel related products and services – custom made travel

insurance

Ancillary travel related products and services include transport arrangement

services, bookings of train, tour bus, airport express, car rental services in Japan

through arrangement with a car rental service provider, sale of theme park

admission tickets, travel insurance services, retail of souvenirs, gifts and snacks

and travel visa application services. EGL provides comprehensive travel related

products and services with the aim of providing convenience to customers and

promoting enrolment for their tours or purchasing FIT products.

Exhibit 21: Ancilliary travel-related products and services revenue

Source: Company, OP Research

To ensure carefree travel experience, EGL tailor-made an insurance programme

called “EGL Global Supreme Travel Insurance (EGL 至尊全球旅遊保險)”,

which was underwritten by an international insurance company and received

commission from it. The insurance programme offers a better coverage than

homogeneous travel insurance products in the market, especially for trip

cancellation or curtailment compensations. The insurance programme provides

benefits including coverage for personal accident of up to HK$1 million, medical

expenses of up to HK$1 million, personal liability of up to HK$2.5 million, trip

cancellation or curtailment of up to HK$30,000, and benefits for loss of travel

document and personal baggage of up to HK$15,000.

44

55

61

67

73

29 30 32

35 38

0%

20%

40%

0

20

40

60

80

FY13A FY14A FY15E FY16E FY17E

Products Services Ancillary travel related products and services YoY (%)

(HK$mn)

EGL co-operates with

international insurance company

to underwrite their custom-made

travel insurance programme

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 20 of 53

Exhibit 22: EGL Global Supreme Travel Insurance

Source: Company, OP Research

Expanding successful model from Japan into other regions

With the success of the direct land operations in Japan, EGL made two

investment plans in local land operators in Japan and Korea in FY14 to expand

the network coverage. EGL holds 38% interest in Kabushiki Kaisha EGL

OKINAWA, which was established on Okinawa Island in February 2015 to

engage in serving package tours for destinations on Okinawa Island. EGL will

also establish a 38% owned travel agency JV in South Korea to engage in

serving package tours for destinations in Korea.

As the investments in these two JVs are expected to officially put into operation in

2Q15E, it will enable EGL to effectively improve service quality control and take

dominant role on cost monitoring to increase profit margin. In the long run, we

believe EGL will increase its stake in the JVs to a controlling level after ramping

up the business scale in the future.

Besides, we think EGL will also consider further expansion of the travel tour

ground handling operation by setting up JVs in other popular destinations, such

as Taiwan, in near future. By replicating the successful model, we believe EGL

will be able to deliver sustainable growth even in relative mature markets in Hong

Kong and Macau.

Local land operator JV has been

set up in Okinawa and will be set

up in South Korea to improve cost

control and profit margin

EGL is expected to increase stake

in the JVs after ramping in the

future

More local land operator JVs are

expected to be setup in other

destinations to replicate

successful business model in

Japan

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 21 of 53

Strong outlook for FY15E results

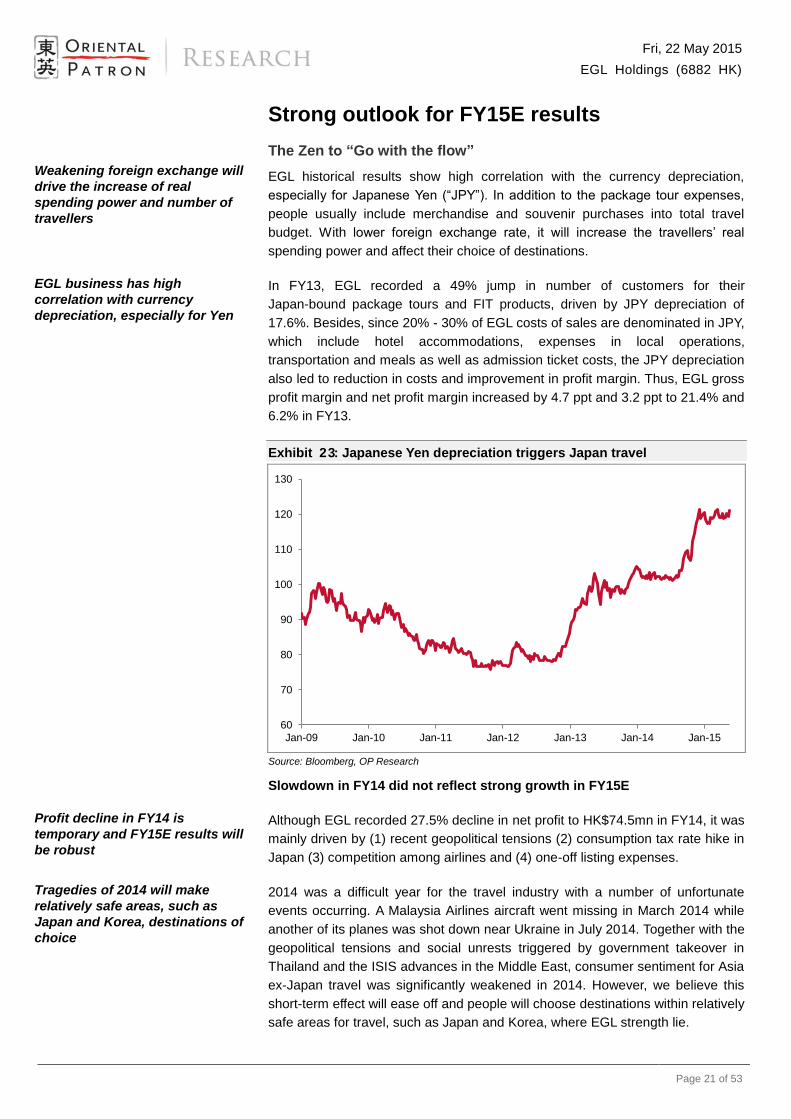

The Zen to “Go with the flow”

EGL historical results show high correlation with the currency depreciation,

especially for Japanese Yen (“JPY”). In addition to the package tour expenses,

people usually include merchandise and souvenir purchases into total travel

budget. With lower foreign exchange rate, it will increase the travellers’ real

spending power and affect their choice of destinations.

In FY13, EGL recorded a 49% jump in number of customers for their

Japan-bound package tours and FIT products, driven by JPY depreciation of

17.6%. Besides, since 20% - 30% of EGL costs of sales are denominated in JPY,

which include hotel accommodations, expenses in local operations,

transportation and meals as well as admission ticket costs, the JPY depreciation

also led to reduction in costs and improvement in profit margin. Thus, EGL gross

profit margin and net profit margin increased by 4.7 ppt and 3.2 ppt to 21.4% and

6.2% in FY13.

Exhibit 23: Japanese Yen depreciation triggers Japan travel

Source: Bloomberg, OP Research

Slowdown in FY14 did not reflect strong growth in FY15E

Although EGL recorded 27.5% decline in net profit to HK$74.5mn in FY14, it was

mainly driven by (1) recent geopolitical tensions (2) consumption tax rate hike in

Japan (3) competition among airlines and (4) one-off listing expenses.

2014 was a difficult year for the travel industry with a number of unfortunate

events occurring. A Malaysia Airlines aircraft went missing in March 2014 while

another of its planes was shot down near Ukraine in July 2014. Together with the

geopolitical tensions and social unrests triggered by government takeover in

Thailand and the ISIS advances in the Middle East, consumer sentiment for Asia

ex-Japan travel was significantly weakened in 2014. However, we believe this

short-term effect will ease off and people will choose destinations within relatively

safe areas for travel, such as Japan and Korea, where EGL strength lie.

60

70

80

90

100

110

120

130

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Weakening foreign exchange will

drive the increase of real

spending power and number of

travellers

EGL business has high

correlation with currency

depreciation, especially for Yen

Profit decline in FY14 is

temporary and FY15E results will

be robust

Tragedies of 2014 will make

relatively safe areas, such as

Japan and Korea, destinations of

choice

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 22 of 53

Exhibit 24: Number of customers for Asia ex-Japan travel

Source: Company, OP Research

Negative impacts from consumption tax rate hike in Japan will ease off

Based on the high base of growth in FY13, the number of customers of

Japan-bound travel of EGL dropped 3% in FY14. The slowdown was partly driven

by the increase in the consumption tax rate of Japan from 5% to 8% in April 2014.

Although the costs of certain travel elements in Japan, such as hotel

accommodation, meals and transportation, increased on higher consumption tax

rate, EGL did not raise the price level of the tour products to maintain

competitiveness during the summer holiday season in FY14. Thus, the gross

margin of Japan-bound package tours dropped by 1.7 ppt to 18.5% in FY14.

Despite JPY depreciating 12.1% in FY14, JPY mainly went down from September

2014. As customers usually plan their trips a few months in advance, we believe

the strong demand for Japan tours will be factored in the FY15E results. Besides,

under higher demand, EGL can pass on the increased costs from consumption

tax to customers more easily to maintain a stable margin going forward.

Exhibit 25: EGL number of customers for Japan travel

Source: Company, OP Research

92,712 87,404 89,152

93,610 98,290

69,027 68,323

69,689 73,174

76,833

-12%

-8%

-4%

0%

4%

8%

0

30,000

60,000

90,000

120,000

FY13A FY14A FY15E FY16E FY17E

Package tours FIT products Asia ex-Japan travel YoY (%)

87,228 89,954

112,443

129,309

148,705

87,843

79,781

99,726

114,685

131,888

-10%

0%

10%

20%

30%

40%

50%

60%

0

40,000

80,000

120,000

160,000

FY13A FY14A FY15E FY16E FY17E

Package tours FIT products Japan travel YoY (%)

Hike in consumption tax rate in

Japan hit consumer demand and

gross margin in FY14, but strong

growth in FY15E will be driven by

JPY depreciation and passing

through costs to customers

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 23 of 53

Strong growth in number of visitors to Japan in 1Q15

As JPY dropped 12% in 4Q14, the weak level of 120 JPY to 1 USD has been

creating a strong demand in Japan tours in 2015. Moreover, with amusement

theme parks, such as Harry Porter section in Universal Studio Osaka, have been

opened in 2014, it is expected to see more tourists picking Japan as their

destination in 2015.

According to Japan National Tourism Organization (“JNTO”), the total number of

visitors to Japan surged 29.4% and 43.7% to 13.41 million and 4.13 million in

2014 and 1Q15 respectively due to lower foreign exchange rate and boom of

outbound travel in China. Noticeably, the number of visitors from China and Hong

Kong leads other regions and record 93.2% yoy and 63.0% yoy growth

respectively. We believe EGL will have a strong FY15E results given their strong

edge in Japan-bound travel products and expanding network in China in 2H15.

Exhibit 26: Total number of visitors to Japan

Source: JNTO, OP Research

Exhibit 27: Number of visitors to Japan from Hong Kong

Source: JNTO, OP Research

-0.5%

17.8%

9.6% 9.0%13.8%

0.0%

-18.7%

26.8%

-27.8%

34.4%

24.0%29.4%

43.7%

-40%

-20%

0%

20%

40%

60%

0

4,000,000

8,000,000

12,000,000

16,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15

Total YoY

-10.5%

15.4%

-0.5%

17.9%22.6%

27.3%

-18.3%

13.2%

-28.3%

32.0%

54.9%

24.1%

63.0%

-40%

-20%

0%

20%

40%

60%

80%

0

200,000

400,000

600,000

800,000

1,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15

Hong Kong YoY

Japan recorded a strong growth

of 44% yoy in number of visitors

in 1Q15 (+63% yoy from Hong

Kong and +93% yoy from China)

EGL will ride the tide for Japan

travel from Hong Kong and China

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 24 of 53

Exhibit 28: Number of visitors to Japan

Country/Area Mar, 2014 Mar, 2015 (%) Jan-Mar, 2014 Jan-Mar, 2015 (%)

South Korea 192,078 268,200 39.6 679,097 947,900 39.6

China 184,064 338,200 83.7 477,905 923,500 93.2

Taiwan 208,610 277,900 33.2 596,768 772,500 29.4

Hong Kong 64,482 117,200 81.8 192,794 314,300 63.0

Thailand 71,122 92,400 29.9 132,617 181,200 36.6

Singapore 16,378 23,100 41.0 37,636 51,200 36.0

Malaysia 23,372 28,200 20.7 51,442 59,800 16.2

Indonesia 14,302 19,500 36.3 27,958 37,300 33.4

Philippines 12,709 26,800 110.9 29,364 55,400 88.7

Vietnam 11,145 18,700 67.8 25,271 40,500 60.3

Inida 6,892 8,200 19.0 18,761 22,000 17.3

Australia 21,334 29,200 36.9 85,290 108,100 26.7

U.S.A. 80,929 95,600 18.1 192,712 216,900 12.6

Canada 16,079 21,600 34.3 40,351 52,200 29.4

United Kingdom 20,029 25,200 25.8 48,836 58,000 18.8

France 15,788 18,100 14.6 33,802 40,100 18.6

Germany 13,752 18,400 33.8 30,071 36,500 21.4

Italy 6,541 8,900 36.1 13,621 17,800 30.7

Russia 6,426 5,500 -14.4 14,134 12,300 -13.0

Spain 3,636 6,300 73.3 7,752 11,600 49.6

Other 60,891 78,800 29.4 138,406 172,300 24.5

Grand total 1,050,559 1,526,000 45.3 2,874,588 4,131,400 43.7

Source: JNTO, OP Research

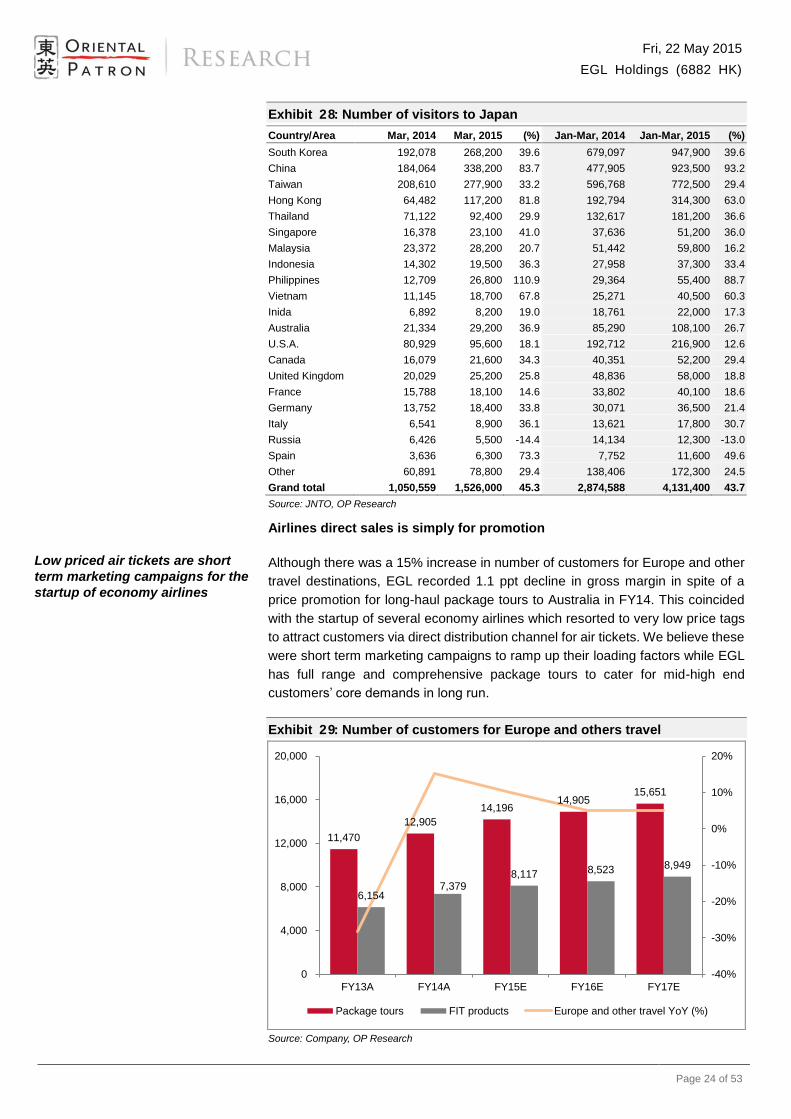

Airlines direct sales is simply for promotion

Although there was a 15% increase in number of customers for Europe and other

travel destinations, EGL recorded 1.1 ppt decline in gross margin in spite of a

price promotion for long-haul package tours to Australia in FY14. This coincided

with the startup of several economy airlines which resorted to very low price tags

to attract customers via direct distribution channel for air tickets. We believe these

were short term marketing campaigns to ramp up their loading factors while EGL

has full range and comprehensive package tours to cater for mid-high end

customers’ core demands in long run.

Exhibit 29: Number of customers for Europe and others travel

Source: Company, OP Research

11,470

12,905

14,196 14,905

15,651

6,154 7,379

8,117 8,523 8,949

-40%

-30%

-20%

-10%

0%

10%

20%

0

4,000

8,000

12,000

16,000

20,000

FY13A FY14A FY15E FY16E FY17E

Package tours FIT products Europe and other travel YoY (%)

Low priced air tickets are short

term marketing campaigns for the

startup of economy airlines

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 25 of 53

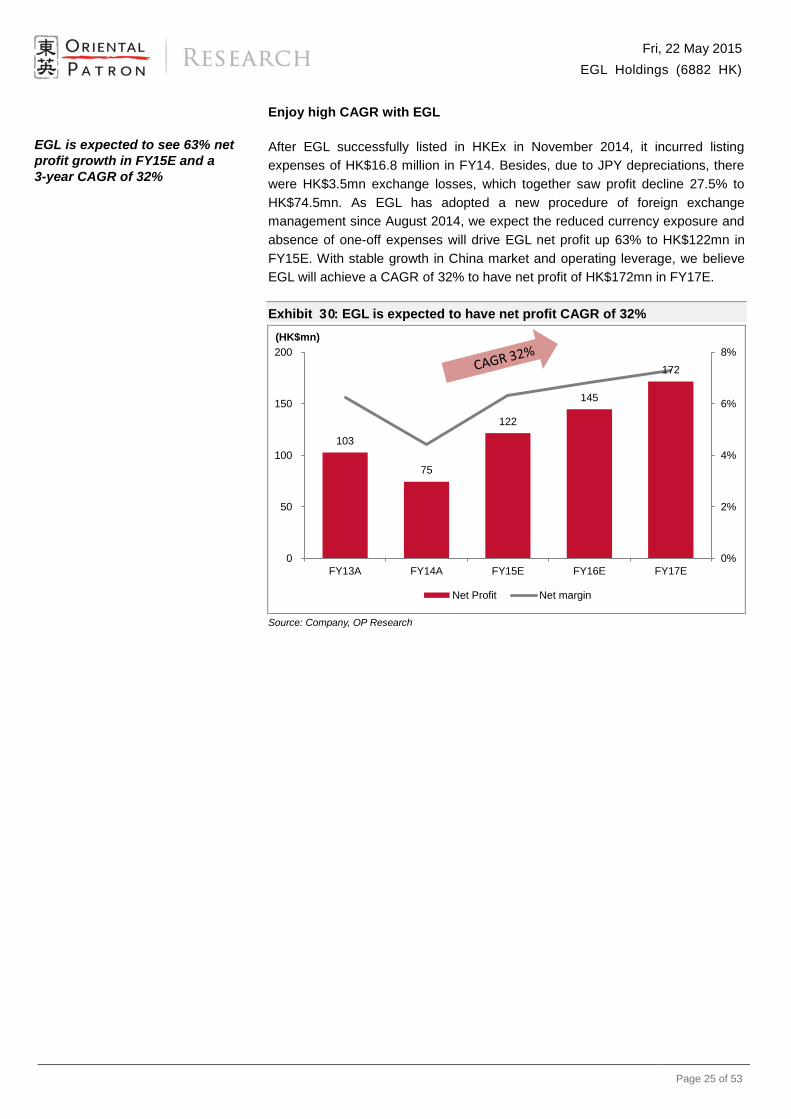

Enjoy high CAGR with EGL

After EGL successfully listed in HKEx in November 2014, it incurred listing

expenses of HK$16.8 million in FY14. Besides, due to JPY depreciations, there

were HK$3.5mn exchange losses, which together saw profit decline 27.5% to

HK$74.5mn. As EGL has adopted a new procedure of foreign exchange

management since August 2014, we expect the reduced currency exposure and

absence of one-off expenses will drive EGL net profit up 63% to HK$122mn in

FY15E. With stable growth in China market and operating leverage, we believe

EGL will achieve a CAGR of 32% to have net profit of HK$172mn in FY17E.

Exhibit 30: EGL is expected to have net profit CAGR of 32%

Source: Company, OP Research

103

75

122

145

172

0%

2%

4%

6%

8%

0

50

100

150

200

FY13A FY14A FY15E FY16E FY17E

Net Profit Net margin

(HK$mn)

EGL is expected to see 63% net

profit growth in FY15E and a

3-year CAGR of 32%

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 26 of 53

Making a quantum leap in China market

Twin engines taking off China market expansion

EGL plans to expand into the China market by engaging with local travel

agencies to promote and sell their products, especially for Japan tours. Since

EGL has direct land operations in Japan, it allows them to design different

itineraries to cater to different demands from Chinese customers. Besides, EGL

can also develop Japan-bound package tours with Mandarin-speaking tour

escorts, which depart from Hong Kong or China, to increase their product

attractiveness.

According to China National Tourism Administration (“CNTA”), the China travel

agency market is very fragmented and there were 2,151 and 251 travel agents

providing outbound travel products and services in China and Guangdong

Province in 2013 respectively. As many smaller local travel agencies do not have

their own outbound travel products, it creates a strong incentive for them to

distribute EGL travel products. Thus, EGL can leverage on their powerful brand

and well-established platform to capture the massive travel market in China

through this win-win co-operation.

EGL has received questionnaire replies from six travel companies in Shenzhen,

Zhongshan and Zhuhai about the views on tour destinations in Japan and the

forecast sales of the tour products. It is expected the cooperation will commence

and start to contribute in 2H15.

Luck is what happens when preparation meets opportunity - Seneca

On 18 December 2014, a new agreement was signed under CEPA to adopt a

brand new approach for further liberalization of service industry between the

Mainland and Hong Kong. The Mainland has opened up 153 services trade

sub-sectors in Guangdong to Hong Kong services industry, accounting for 95.6%

of all services trade sub-sectors. Under a total of 27 new liberalization measures

and investment facilitation, tourism and travel related services is one of the

sectors to benefit from liberalization. The Agreement came into effect on the day

of signing and implemented from 1 March 2015, opening up an explosive growth

opportunity for EGL to develop China market by leveraging their strong business

model and operations in Hong Kong.

Under CEPA, 5 travel agents are allowed to set up wholly-owned companies to

run outbound group tours for Mainland residents to destinations beyond Hong

Kong and Macau (excluding Taiwan). We expect EGL will set up subsidiary in

China and try to get the outbound travel agency licence in near future to directly

sell their award-winning products to Mainland customers. As EGL will launch their

mobile platform to sell their package tours and FIT products in 4Q15, we expect

they can ramp up China business at an explosive speed without heavy

investment on opening branches once the qualification is granted under CEPA.

Thus, we expect the China market to contribute 30% of EGL’s revenue in 3 years

under the twin engines of growth in China market.

EGL plans to capture the travel

services market in China by

cooperating with local travel

agencies in Guangdong Province

for distribution of their Japan

tours travel products

The cooperation is expected to

commerce in 2H15

“The Agreement between the

Mainland and Hong Kong on

Achieving Basic Liberalization of

Trade in Services in Guangdong”

was signed on 18 Dec, 2014

5 wholly-owned travel agents are

allowed to setup in China by

HKSS to operate outbound group

tours for Mainland residents

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 27 of 53

Exhibit 31: Liberalization for travel services industry under CEPA Agreements

Sub-sector Reserved restrictive measures for Commercial Presence

Hotels and restaurants Apply national treatment

Travel agencies and tour operators services The number of travel agents set up on a wholly-owned basis operating outbound group tours for

Mainland residents on a pilot basis to destinations beyond Hong Kong and Macau (excluding Taiwan)

is restricted to 5.

No restriction is imposed with regard to the number of Mainland-Hong Kong joint venture travel

agents operating outbound group tours for Mainland residents to destinations beyond Hong Kong and

Macao (excluding Taiwan).

Tourist guides services Apply national treatment

Other Apply national treatment

Source: Trade and Industry Department of HKSAR, OP Research

Exhibit 32: New CEPA Agreement singed on December 2014

Source: Financial Secretary Office of HKSAR, OP Research

Booming Chinese outbound travel

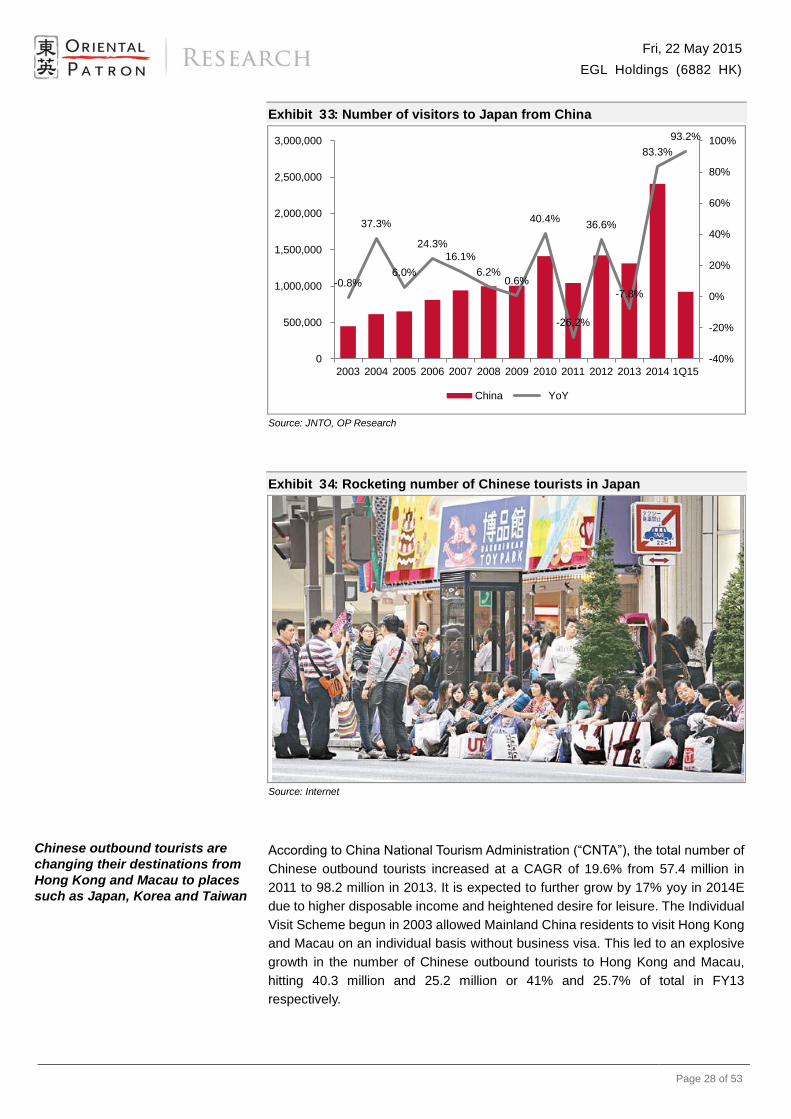

According to JNTO, China replaced Taiwan as the second largest source of

visitors in 2014 after anti-Japan emotions eased during 2013. The number for

visitors from China to Japan increased sharply by 83% yoy and 93% yoy in 2014

and 1Q15 respectively. We believe Japan is one of the favorite destinations of

Chinese tourists due to (1) geographic proximity (2) abundant shopping options

(3) restaurants providing high quality foods and drinks and (4) refined culture and

attractive sightseeing spots. We believe travel agencies, such as EGL, with

expertise in Japan tours have a strong competitive edge in capturing this Chinese

outbound travel boom.

Number of visitors from China to

Japan increased 83% yoy and

93% yoy in 2014 and 1Q15

respectively

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 28 of 53

Exhibit 33: Number of visitors to Japan from China

Source: JNTO, OP Research

Exhibit 34: Rocketing number of Chinese tourists in Japan

Source: Internet

According to China National Tourism Administration (“CNTA”), the total number of

Chinese outbound tourists increased at a CAGR of 19.6% from 57.4 million in

2011 to 98.2 million in 2013. It is expected to further grow by 17% yoy in 2014E

due to higher disposable income and heightened desire for leisure. The Individual

Visit Scheme begun in 2003 allowed Mainland China residents to visit Hong Kong

and Macau on an individual basis without business visa. This led to an explosive

growth in the number of Chinese outbound tourists to Hong Kong and Macau,

hitting 40.3 million and 25.2 million or 41% and 25.7% of total in FY13

respectively.

-0.8%

37.3%

6.0%

24.3%

16.1%

6.2%0.6%

40.4%

-26.2%

36.6%

-7.8%

83.3%

93.2%

-40%

-20%

0%

20%

40%

60%

80%

100%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15

China YoY

Chinese outbound tourists are

changing their destinations from

Hong Kong and Macau to places

such as Japan, Korea and Taiwan

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 29 of 53

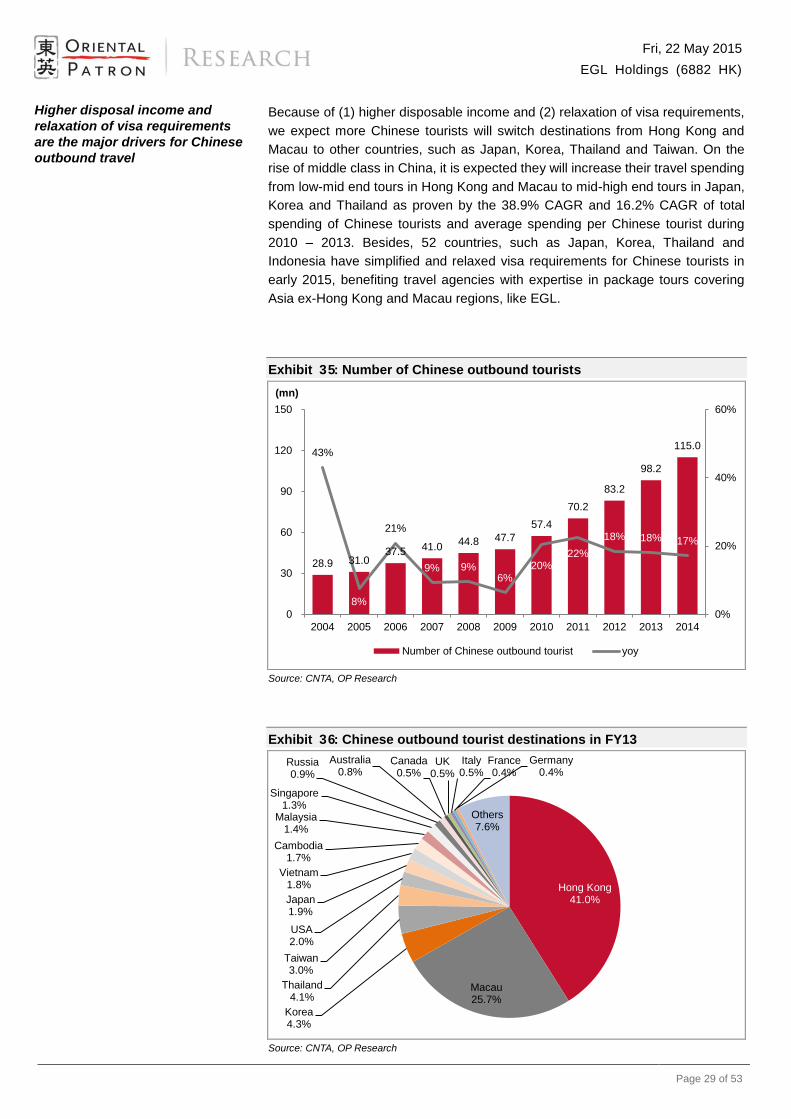

Because of (1) higher disposable income and (2) relaxation of visa requirements,

we expect more Chinese tourists will switch destinations from Hong Kong and

Macau to other countries, such as Japan, Korea, Thailand and Taiwan. On the

rise of middle class in China, it is expected they will increase their travel spending

from low-mid end tours in Hong Kong and Macau to mid-high end tours in Japan,

Korea and Thailand as proven by the 38.9% CAGR and 16.2% CAGR of total

spending of Chinese tourists and average spending per Chinese tourist during

2010 – 2013. Besides, 52 countries, such as Japan, Korea, Thailand and

Indonesia have simplified and relaxed visa requirements for Chinese tourists in

early 2015, benefiting travel agencies with expertise in package tours covering

Asia ex-Hong Kong and Macau regions, like EGL.

Exhibit 35: Number of Chinese outbound tourists

Source: CNTA, OP Research

Exhibit 36: Chinese outbound tourist destinations in FY13

Source: CNTA, OP Research

28.9 31.0 37.5 41.0

44.8 47.7

57.4

70.2

83.2

98.2

115.0 43%

8%

21%

9% 9%6%

20%22%

18% 18% 17%

0%

20%

40%

60%

0

30

60

90

120

150

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Number of Chinese outbound tourist yoy

(mn)

Hong Kong41.0%

Macau25.7%

Korea4.3%

Thailand4.1%

Taiwan3.0%

USA2.0%

Japan1.9%

Vietnam1.8%

Cambodia1.7%

Malaysia1.4%

Singapore1.3%

Russia0.9%

Australia0.8%

Canada0.5%

UK0.5%

Italy0.5%

France0.4%

Germany0.4%

Others7.6%

Higher disposal income and

relaxation of visa requirements

are the major drivers for Chinese

outbound travel

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 30 of 53

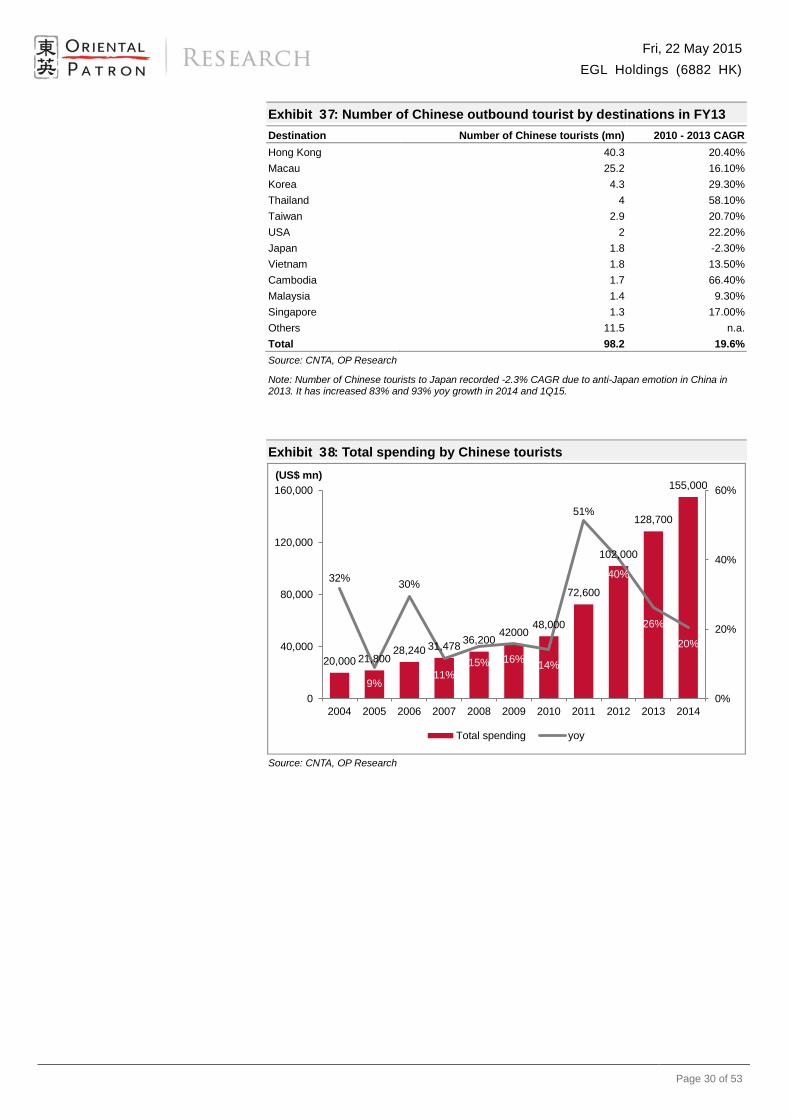

Exhibit 37: Number of Chinese outbound tourist by destinations in FY13

Destination Number of Chinese tourists (mn) 2010 - 2013 CAGR

Hong Kong 40.3 20.40%

Macau 25.2 16.10%

Korea 4.3 29.30%

Thailand 4 58.10%

Taiwan 2.9 20.70%

USA 2 22.20%

Japan 1.8 -2.30%

Vietnam 1.8 13.50%

Cambodia 1.7 66.40%

Malaysia 1.4 9.30%

Singapore 1.3 17.00%

Others 11.5 n.a.

Total 98.2 19.6%

Source: CNTA, OP Research

Note: Number of Chinese tourists to Japan recorded -2.3% CAGR due to anti-Japan emotion in China in 2013. It has increased 83% and 93% yoy growth in 2014 and 1Q15.

Exhibit 38: Total spending by Chinese tourists

Source: CNTA, OP Research

20,000 21,80028,240 31,478

36,20042000

48,000

72,600

102,000

128,700

155,000

32%

9%

30%

11%15% 16%

14%

51%

40%

26%

20%

0%

20%

40%

60%

0

40,000

80,000

120,000

160,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total spending yoy

(US$ mn)

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 31 of 53

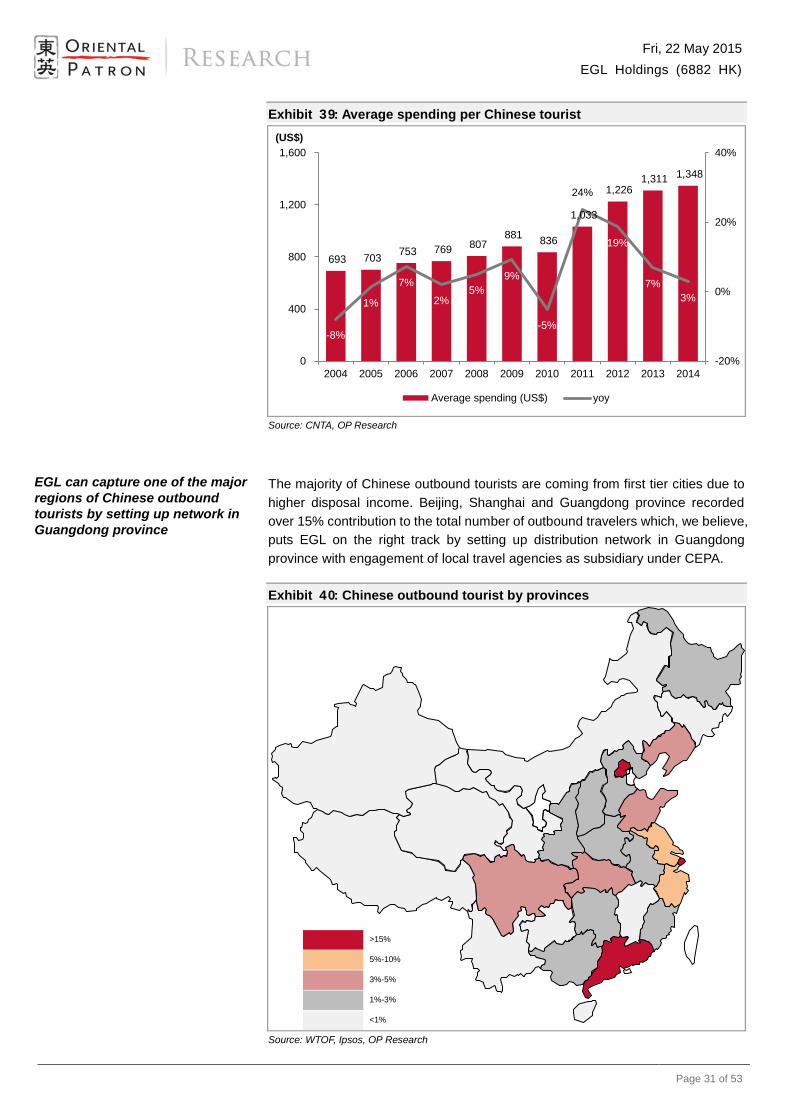

Exhibit 39: Average spending per Chinese tourist

Source: CNTA, OP Research

The majority of Chinese outbound tourists are coming from first tier cities due to

higher disposal income. Beijing, Shanghai and Guangdong province recorded

over 15% contribution to the total number of outbound travelers which, we believe,

puts EGL on the right track by setting up distribution network in Guangdong

province with engagement of local travel agencies as subsidiary under CEPA.

Exhibit 40: Chinese outbound tourist by provinces

Source: WTOF, Ipsos, OP Research

693 703 753 769

807 881

836

1,033

1,226 1,311 1,348

-8%

1%

7%

2%5%

9%

-5%

24%

19%

7%

3%

-20%

0%

20%

40%

0

400

800

1,200

1,600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Average spending (US$) yoy

(US$)

>15%

5%-10%

3%-5%

1%-3%

<1%

EGL can capture one of the major

regions of Chinese outbound

tourists by setting up network in

Guangdong province

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 32 of 53

Value play in a hot sector. Initiate BUY

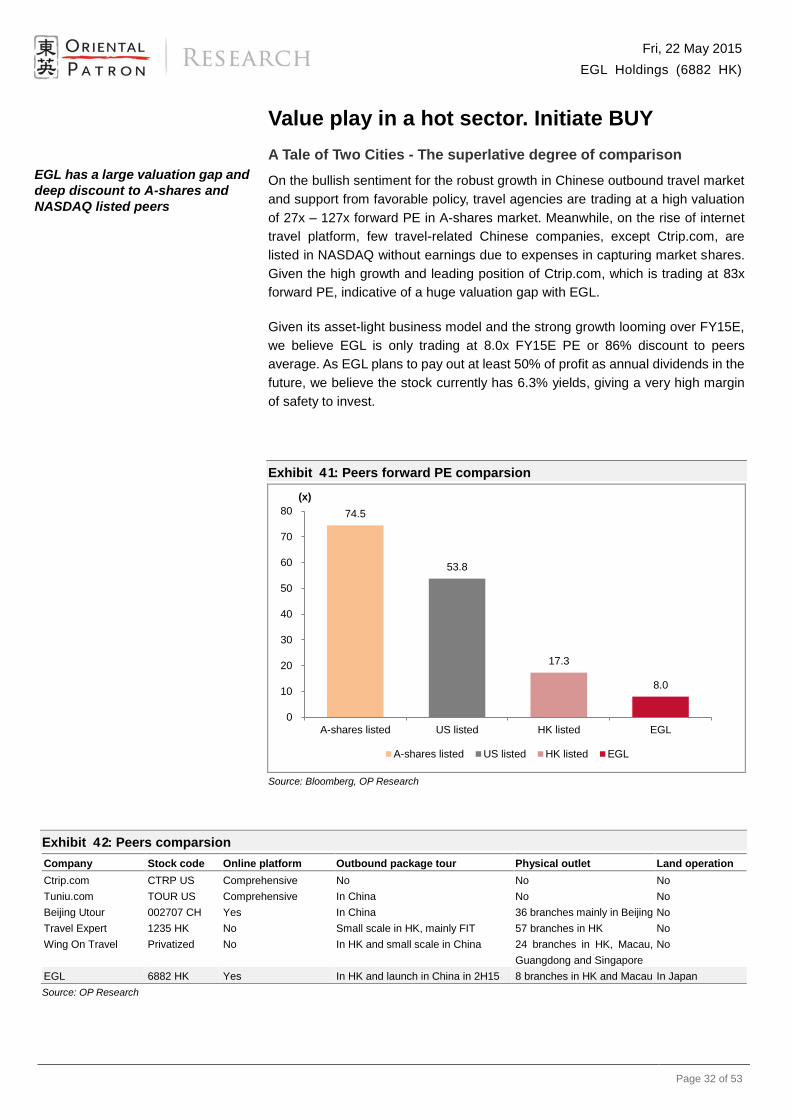

A Tale of Two Cities - The superlative degree of comparison

On the bullish sentiment for the robust growth in Chinese outbound travel market

and support from favorable policy, travel agencies are trading at a high valuation

of 27x – 127x forward PE in A-shares market. Meanwhile, on the rise of internet

travel platform, few travel-related Chinese companies, except Ctrip.com, are

listed in NASDAQ without earnings due to expenses in capturing market shares.

Given the high growth and leading position of Ctrip.com, which is trading at 83x

forward PE, indicative of a huge valuation gap with EGL.

Given its asset-light business model and the strong growth looming over FY15E,

we believe EGL is only trading at 8.0x FY15E PE or 86% discount to peers

average. As EGL plans to pay out at least 50% of profit as annual dividends in the

future, we believe the stock currently has 6.3% yields, giving a very high margin

of safety to invest.

Exhibit 41: Peers forward PE comparsion

Source: Bloomberg, OP Research

Exhibit 42: Peers comparsion

Company Stock code Online platform Outbound package tour Physical outlet Land operation

Ctrip.com CTRP US Comprehensive No No No

Tuniu.com TOUR US Comprehensive In China No No

Beijing Utour 002707 CH Yes In China 36 branches mainly in Beijing No

Travel Expert 1235 HK No Small scale in HK, mainly FIT 57 branches in HK No

Wing On Travel Privatized No In HK and small scale in China 24 branches in HK, Macau,

Guangdong and Singapore

No

EGL 6882 HK Yes In HK and launch in China in 2H15 8 branches in HK and Macau In Japan

Source: OP Research

74.5

53.8

17.3

8.0

0

10

20

30

40

50

60

70

80

A-shares listed US listed HK listed EGL

A-shares listed US listed HK listed EGL

(x)

EGL has a large valuation gap and

deep discount to A-shares and

NASDAQ listed peers

Fri, 22 May 2015

EGL Holdings (6882 HK)

Page 33 of 53

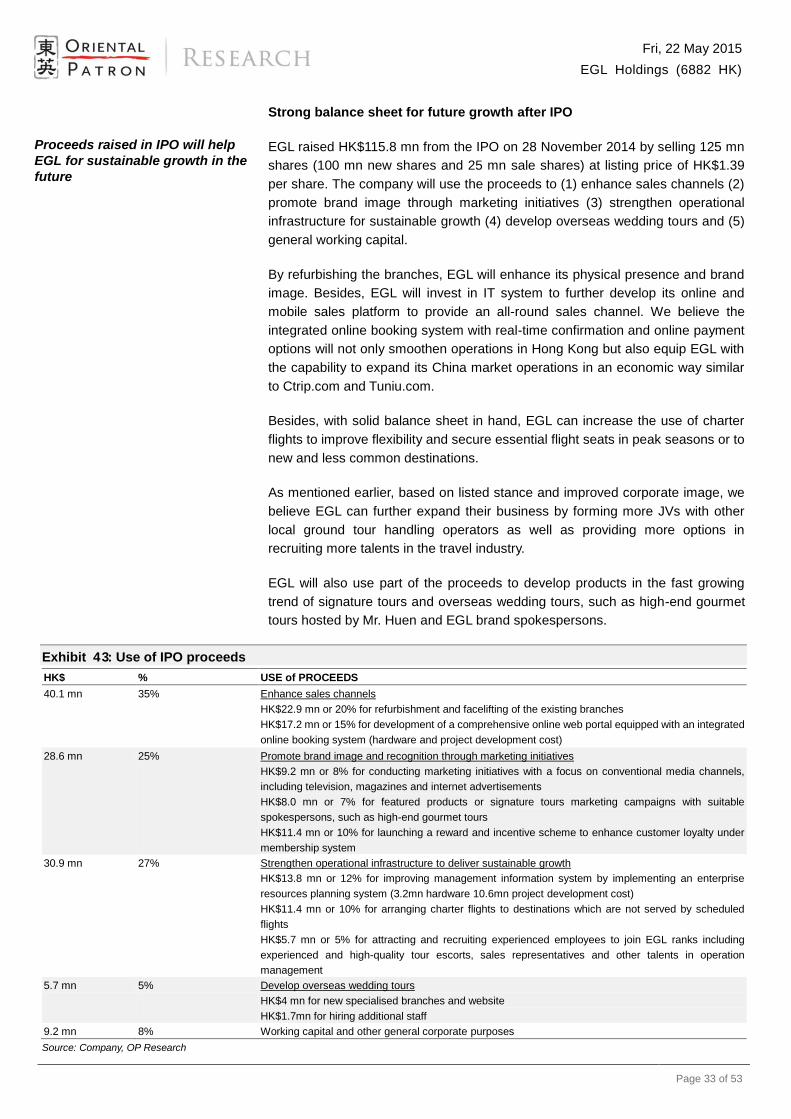

Strong balance sheet for future growth after IPO

EGL raised HK$115.8 mn from the IPO on 28 November 2014 by selling 125 mn

shares (100 mn new shares and 25 mn sale shares) at listing price of HK$1.39

per share. The company will use the proceeds to (1) enhance sales channels (2)

promote brand image through marketing initiatives (3) strengthen operational

infrastructure for sustainable growth (4) develop overseas wedding tours and (5)

general working capital.

By refurbishing the branches, EGL will enhance its physical presence and brand

image. Besides, EGL will invest in IT system to further develop its online and

mobile sales platform to provide an all-round sales channel. We believe the

integrated online booking system with real-time confirmation and online payment

options will not only smoothen operations in Hong Kong but also equip EGL with

the capability to expand its China market operations in an economic way similar

to Ctrip.com and Tuniu.com.

Besides, with solid balance sheet in hand, EGL can increase the use of charter

flights to improve flexibility and secure essential flight seats in peak seasons or to

new and less common destinations.

As mentioned earlier, based on listed stance and improved corporate image, we

believe EGL can further expand their business by forming more JVs with other

local ground tour handling operators as well as providing more options in

recruiting more talents in the travel industry.

EGL will also use part of the proceeds to develop products in the fast growing

trend of signature tours and overseas wedding tours, such as high-end gourmet

tours hosted by Mr. Huen and EGL brand spokespersons.

Exhibit 43: Use of IPO proceeds

HK$ % USE of PROCEEDS

40.1 mn 35% Enhance sales channels

HK$22.9 mn or 20% for refurbishment and facelifting of the existing branches

HK$17.2 mn or 15% for development of a comprehensive online web portal equipped with an integrated

online booking system (hardware and project development cost)

28.6 mn 25% Promote brand image and recognition through marketing initiatives

HK$9.2 mn or 8% for conducting marketing initiatives with a focus on conventional media channels,