Embed Size (px)

Citation preview

BroadbandinAmerica2ndEditionWhereItIsandWhereItIsGoing

(AccordingtoBroadbandServiceProviders)

AnUpdateofthe2009ReportOriginallyPreparedfor

theStaffoftheFCC’sOmnibusBroadbandInitiative

By

RobertC.Atkinson,IvyE.SchultzTravisKorte,TimothyKrompinger

May,2011

2

Acknowledgements

TheresearcheffortthatwentintothisreportwasundertakentwoCITIinterns.TheresearchwasstartedinJune,2010by:

TravisKorte(UniversityofCalifornia,BerkleyBA,2010),andTimothyKrompinger(UniversityofConnecticut,BA,2011.

Inaddition,othermembersofCITI’sstaffandanumberofCITIfriendsandaffiliatescontributedtheirexperienceandexpertisebyreviewingandcritiquingdrafts.

Wewouldalsoliketothankthemanyorganizationsthatrespondedtoourrequestsforbroadbanddataandinformationandthoseindividualswhoverifiedtheirorganization’sdatapresentedintheAppendixofthisreport.

CITI,asaninstitution,doesnotauthororpublisharticlesorreports.Therefore,we,astheauthors,areresponsibleforthecontentofthisreport.

Robert C. Atkinson Ivy E. Schultz

RobertC.AtkinsonDirectorofPolicyResearch

IvyE.SchultzManagerofResearchAssistants

3

TableofContentsSection1:ListingofAllPubliclyAnnouncedBroadbandPlans ........................................... 151.1BroadbandByTechnology................................................................................................... 181.2TimelineforBroadbandPlans ............................................................................................. 361.3PenetrationandCoverageFootprint................................................................................... 361.5ExpectedBroadbandPerformance/Quality ........................................................................ 431.6ARPU(AverageRevenueperUser) ..................................................................................... 46PricingAppendix ....................................................................................................................... 49

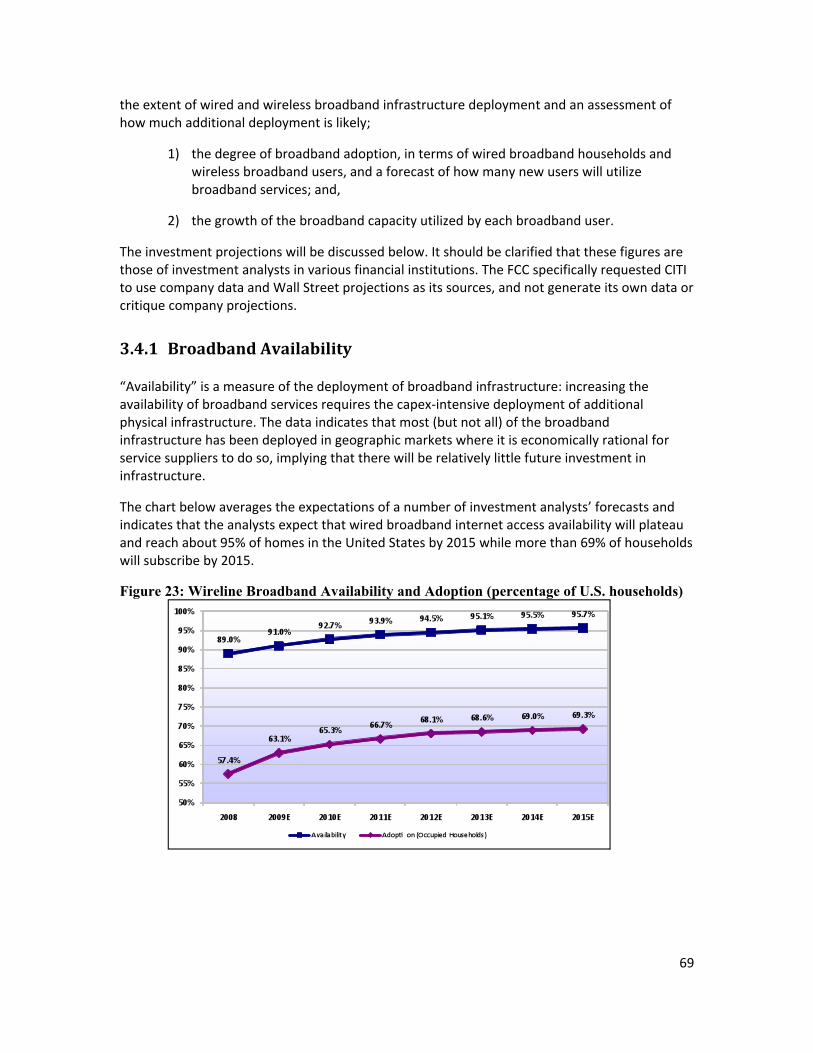

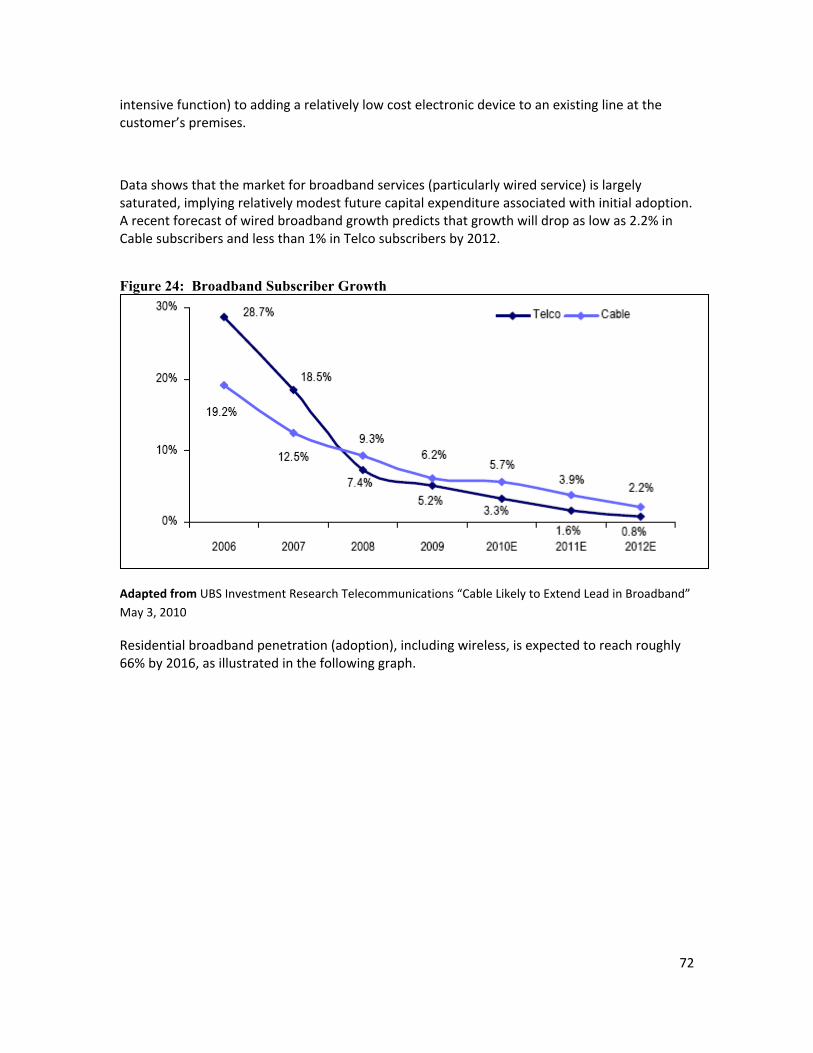

Section2:ComparisonofAllPubliclyAnnouncedPlans ............................................................... 52Section3:FutureProjections ........................................................................................................ 653.1AnnouncedButUncompletedBroadbandPlans................................................................. 653.2BroadbandSatellitePlans ................................................................................................... 683.4.1BroadbandAvailability ..................................................................................................... 693.4.2BroadbandAdoption ........................................................................................................ 713.4.3BroadbandUsagebyCustomers ..................................................................................... 743.4.5ForecastingBroadbandCapitalExpenditures .................................................................. 76

Section4:GuestEssayContributions............................................................................................ 85

Appendix:ListingofAllPubliclyAnnouncedBroadbandPlans .......................................................... A1‐A43

4

ListofFiguresFigure1:TypesofBroadbandServices ......................................................................................... 18Figure2:FTTHConnectionsinmillionsasofMarch30,2010....................................................... 19Figure3:USFTTHSubscribers....................................................................................................... 21Figure4:TelcoFiberHomesPassedandPercentofHouseholds.................................................. 22Figure5:DSLSubscribers .............................................................................................................. 23Figure6:TelecomBroadbandAdds(DSLLoss) ............................................................................. 24Figure7:RuralTelcos:DSLPenetrationofTotalAccessLines(1Q08‐4Q09E)............................. 24Figure8:HomesPassedbyCableCompanies ............................................................................... 26Figure9:MSOsBroadbandSubscriptionPenetrationofHomesPassed ...................................... 26Figure10:CableDOCSIS3.0Roll‐out ............................................................................................ 27Figure11:ExpectedDownstreamSpeedsof3Gand4GWirelessBroadband(Mbps) ................. 28Figure12:MajorInternetBackboneRoutesintheU.S.(>250Gbps) ........................................... 32Figure13:20HighestCapacityU.S.DomesticInternetRoutes.2007–2009(Gbps) ..................... 33Figure14:InternetPenetrationForecast...................................................................................... 37Figure15:GrowthinOnlineHouseholds ...................................................................................... 38Figure16:BroadbandSubscribersandGrowth ............................................................................ 38Figure17:HouseholdswithDial‐UpService ................................................................................ 39Figure18:AT&TandVerizonWirelessCapex,2009‐2010 ............................................................ 40Figure19:BroadbandCapexbytype,3QandYTD2010............................................................... 41Figure20:CapexasaPercentageofSales2008‐2010 .................................................................. 41Figure21:WeightedAverageCableBroadbandARPU ................................................................. 47Figure22:BroadbandPriceGrowth.............................................................................................. 51Figure23:WirelineBroadbandAvailabilityandAdoption(inpercentageofU.S.households).... 69Figure24:BroadbandSubscriberGrowth .................................................................................... 72Figure25:ResidentialHouseholdPenetration.............................................................................. 73Figure26:BroadbandWirelessBuilds........................................................................................... 73Figure27:NorthAmericanConsumerInternetTraffic(Petabits/month)..................................... 74Figure28:EstimatedU.S.ConsumerInternetUse........................................................................ 75Figure29:TypicalSpeeds(inMbps)thatInternetActivitiesandIPTVWillRequirein2013 ........ 76Figure30:IndustrySectors'BroadbandCapex ............................................................................. 80Figure31:TotalCapexandTotalBroadbandCapex ..................................................................... 81Figure32:TotalAverageWirelessARPUComposition ................................................................. 84

ListofTables

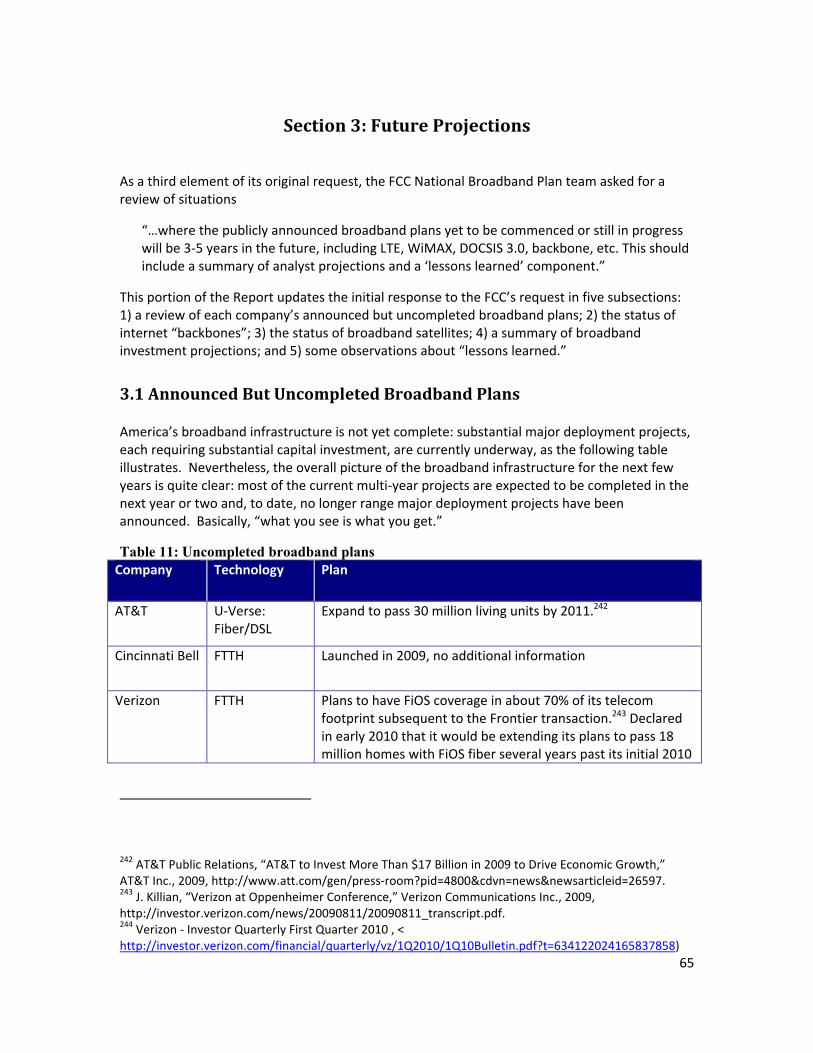

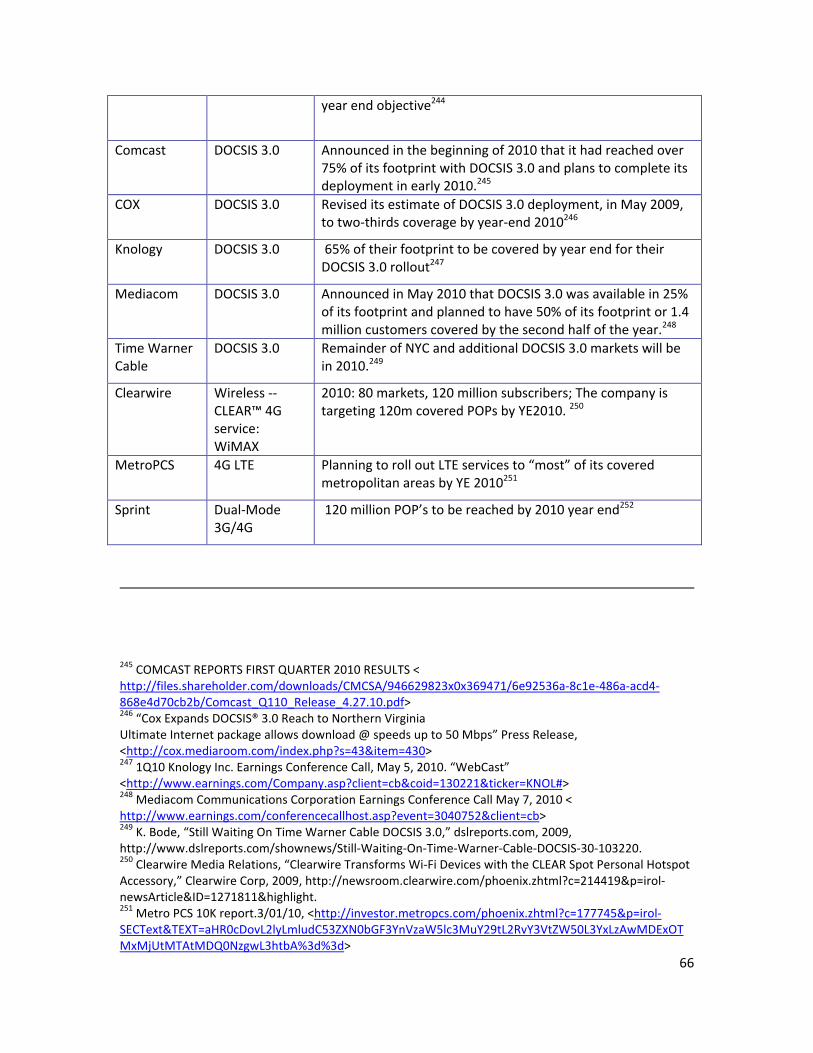

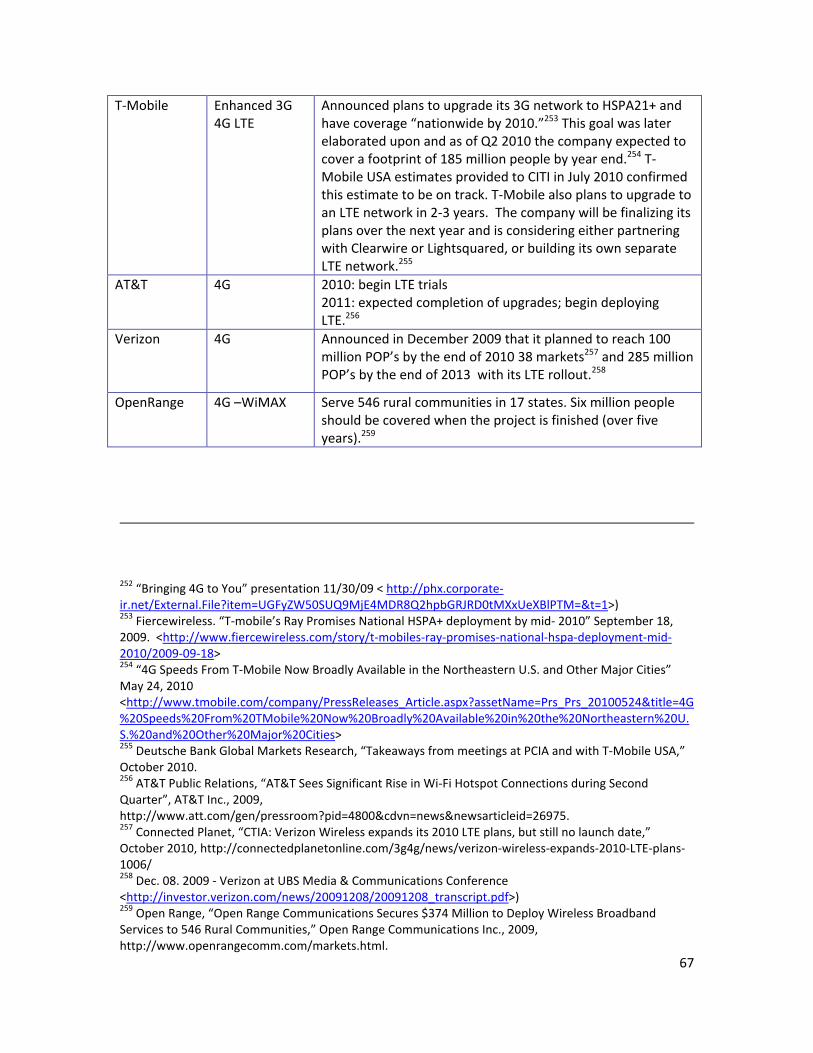

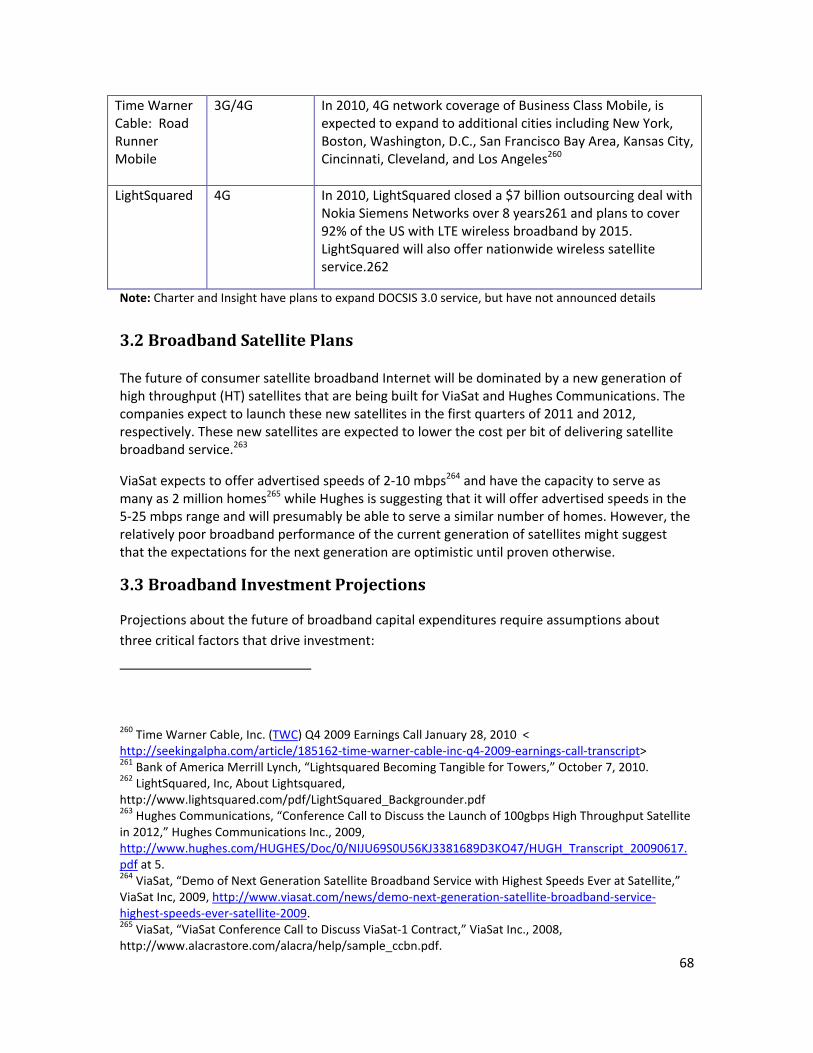

Table1:SpeedsforFTTN/FTTHHouseholds ................................................................................. 21Table2:20HighestCapacityU.S.DomesticInternetRoutes.2007–2009(Gbps) ........................ 32Table3:AggregateCapEx2009‐$56.1B...................................................................................... 39Table4:TotalCapitalExpendituresofLargestCompanies($billions) ......................................... 40Table5:RBOCWiredBroadbandCapex($billion)........................................................................ 42Table6:AverageDownloadSpeedsofISPs(TopTen) .................................................................. 44Table7:AverageUploadSpeedofISPs(TopTen)......................................................................... 44Table8:TypicalWirelessBroadbandPricingplans ....................................................................... 49Table9:BroadbandPricingChanges(DSL).................................................................................... 50Table10:MajorBroadbandDeployments:PerformanceAgainstAnnouncedCompletionDates53Table11:Uncompletedbroadbandplans ..................................................................................... 65Table12:USInternetAccessbyTypeofService........................................................................... 71

5

Table13:TotalCapitalExpendituresforMajorServiceProviders($billion)................................ 76Table14:RBOCWiredBroadbandCapex($billion)...................................................................... 78Table15:TotalCapexandBroadbandCapexbySector................................................................ 79Table16:WirelessBroadbandDataARPU.................................................................................... 83

6

ProjectBackgroundThisisthesecondeditionof“BroadbandinAmerica:WhereItisandWhereItIsGoing”.ItisanupdateandexpansionontheoriginalreportthatwassubmittedtotheFederalCommunicationsCommission(FCC)inNovember2009aspartoftheFCC’sdevelopmentofaNationalBroadbandPlan(NBP).

ThefirstthreesectionsofthissecondeditionaregeneralupdatesofthefactualdatasubmittedtotheFCCapproximatelyinlate2009.Thefourthsectionisentirelynew:itcomprisesanalysisandcommentarybyafewleadingbroadbandexpertswhoprovidetheirinsightsintosomeoftheissuesassociatedwithBroadbandinAmerica.

• TheFirstEdition

Inmid‐2009,thestaffoftheFCC’sOmnibusBroadbandInitiative(alsoknownastheNationalBroadbandPlanTaskForce)askedtheColumbiaInstituteforTele‐Information(CITI)toconductanindependentanalysisofpubliclyannouncedbroadbandnetworkdeployments(bothnewandupgradednetworks)ofcompaniesintheUnitedStates,forthepurposeofinformingtheFCC’seffortsindevelopingitsNationalBroadbandPlan.OnAugust6,theFCCannouncedthatCITIhad

agreedtoundertaketheanalysisproject.1

TwomembersofCITI’smanagementstaff,BobAtkinsonandIvySchultz,undertookthe2009project.TheyworkedindependentlyoftheFCCandconductedtheprojectwithCITI’sresearchresourcesandwithoutanyprojectfundingfromtheFCCoranyotherorganization.Asaresult,theseprojectarrangementsensuredtheindependenceandintegrityoftheworkproduct.

AsrequestedbytheFCC,theprojectencompassedacomprehensiveexaminationandanalysisofcompanies’announcementsandsimilarpublicinformation,industryanalysts’reports,andotherrelevantdatasourcedtothebroadbandserviceproviderstomeasureandassessbroadbandplans.AlsoattheFCC’srequest,thereportincludedanassessmentofwherebroadbanddeploymentswillbein3–5yearsandacomparisonofresultswithpreviouslyreleasedplansthatareinprogressorcomplete.Toavoidduplicationandtofocustheresultingreportonwhatbroadbandserviceprovidersweredoingandplanning,theprojectpurposefullydidnotincludedataandotherinformationalreadygatheredandpublishedbytheFCC.

TheresearchforthisprojectfocusedonthethreespecificareasrequestedbytheFCC,eachofwhichisaddressedasasectionintheFirstandSecondReports:

1FCCPressRelease,http://hraunfoss.fcc.gov/edocs_public/attachmatch/DOC‐292598A1.pdf.

7

Section1:ListingofAllPubliclyAnnouncedBroadbandPlans,sortedboth(1)bycompanyand(2)bytechnology(e.g.DSL,cable,fiber(FTTx),fixedwireless,wireless,satellite),withadescriptionofrelevantdetailssuchas(1)generaldetailsoftheplan,includingcompany,technology,andtimeline,(2)expectedcapitaloutlaysandoperatingexpenditures,(3)expecteddeployment/coveragefootprint,(4)expectedbroadbandperformanceandquality,and(5)expectedARPUs(AverageRevenuePerUser).

Section2:ComparisonofAllPubliclyAnnouncedBroadbandPlans,basedupontheListingofAllPubliclyAvailableBroadbandPlans.Thislooksbackwardstowhatwasannouncedatthetimetheplanwasestablishedandthencomparestheannouncementwiththeoutcomesofcompletedplansandthecurrentstatusforthoseplansstillinprogress.

Section3:FutureProjection:Thisisananalysisofwherethepubliclyannouncedbroadbandplansthatareyettobecommencedorstillinprogresswillbein3‐5years,includingLTE,WiMAX,DOCSIS3.0,backbone,etc.Thisincludesasummaryofanalystcapitalexpenditureforecastsanda“lessonslearned”component.

Section4:Essays&Analyses(onlyinSecondReport)byfiveleadingbroadbandexpertsbasedontheirpresentationsataMarch18conferenceorganizedbyCITIandGeorgetownUniversity’sCommunicationCultureandTechnologyProgramtocommemoratethefirstanniversaryoftheNationalBroadbandPlan.2

AfterreceivingtheFirstReport,theFCCreleaseditforpubliccommentandreceivedanumberofcommentsfromvariouscompaniesandtradeassociationsinvolvedintheNationalBroadbandProceeding.MostofthecommentsendorsedtheReportandnonetookissuewiththemethodologyoranalysis.TheCITIauthorspresentedtheReportatapublicmeetingheldattheFCConDecember10,2009.ThepresentationwasrecordedandisavailableontheFCCwebsiteathttp://www.broadband.gov/ws_deployment_research.htmlandtheCITIwebsiteathttp://www4.gsb.columbia.edu/citi/research/current.

GeneralResearchMethodology

ThisSecondReportfollowsthesamegeneralmethodologyusedintheFirstReport.CITIresearchersworkedindependentlyoftheFCCandconductedtheprojectwithCITI’sresearchresourcesandwithoutanyprojectfundingfromtheFCCoranyotherorganization.Asaresult,theprojectarrangementscontinuetoensuretheindependenceandintegrityoftheworkproduct.

2See:http://www4.gsb.columbia.edu/citi/events/NBP2011fortheconferencepresentationsandvideo.

8

SincetheFCC’soriginalrequestwasforareviewofthestateofbroadbandinAmericabasedonwhatthebroadbandserviceprovidershavepubliclyannounced,researchersassignedtothisprojectagaincollecteddataprimarilyfrom:1)serviceproviders’publicreportsandstatements;2)reportsbyinvestmentanalystsandresearchfirms(whicharegenerallybasedoninformationobtaineddirectlyfromtheserviceprovidersthemselves);3)newsreportsdirectlyquotingtheserviceproviders;and,4)informationcompiledbyindustrytradeassociationsdirectlyfromtheirmembercompanies.Consequently,wedidnotdevelopindependentdataorevaluatethevalidityofthedatareportedbytheserviceprovidersand,toavoidrepetitionandduplication,wedidnotuseacademic,governmentorotherstudiesregardingthestateofbroadbandthatareavailabletotheFCCandtheCommission’sstaff.

Relyingoninformationprovidedasdirectlyaspossiblebytheserviceprovidershasitsownlimitations.Eachserviceproviderhasanaturalinclinationandincentivetopresentinformationaboutitselfinawaythatitregardsasmostbeneficialtoitsinterests.Forcompetitiveandotherbusinessreasonsandtocomplywithsecuritieslawsregardingdisclosureofmaterialinformation,publiclytradedbroadbandserviceprovidersarecarefulaboutreleasingdetailedinformationabouttheircurrentperformanceandfutureplansregardingbroadbanddeploymentsandfinancialresults.Smallprivatecompaniesaresimilarlyreticenttoprovidedetailedinformationabouttheirfutureplans,eventotheirtradeassociations.

Thepublicandanyonewithrelevantinformationareinvitedtosubmitadditionalinformationanddatatoadedicatedemailaddress:CITI‐[email protected].

9

ExecutiveSummary

OneprincipalconclusiondrawnfromtheFirstReportwasthatby2013‐4,broadbandservice

providersexpectedtobeabletoserveabout95%3ofU.S.homeswithatleastalowspeedof

wiredbroadbandserviceandtheyexpectedtooffertoabout90%ofhomesadvertisedspeeds

of50mbpsdownstream.4Serviceprovidersexpectedtoprovidemanyhomeswithaccessto

thesehigherspeedsby2011‐2012.5Anotherconclusionwasthatwirelessbroadbandservice

providersexpectedtoofferwirelessinternetaccessatadvertisedspeedsrangingupto12mbpsdownstream(butmorelikely5mbpsorlessduetocapacitysharing)toabout94%ofthepopulationby2013.TheFirstReportalsoconcludedthat,inadditiontoseveralwirelessbroadbandchoices,themajorityofAmericanhomeswillhavethechoiceoftwowiredbroadbandservices.Upstreamspeedsforwiredandwirelessserviceswillgenerallybesignificantlylowerthandownstream.TheupdatedinformationincludedinthisSecondReportcontinuestosupportalloftheseexpectations.

AnotherprincipalconclusiondrawnintheFirstReportwasthatasignificantnumberofU.S.

homes,perhapsfivetotenmillion(whichrepresent4.5to9percentofhouseholds)6,willhave

significantlyinferiorchoicesinbroadband:mostofthesehomeswillhavewirelessorwiredservicebroadbandavailableonlyatspeedssubstantiallylowerthanthespeedsavailabletotherestofthecountry.Someofthesehomeswillhavenochoiceexceptsatellitebroadband,whichhassomeperformanceattributesthatmakeitlesssatisfactoryformanyapplicationsthanaterrestrialbroadbandservice.Onceagain,theseconclusionsremainvalid.

TheFirstReportalsoconcludedthatadoptionofbroadbandservicewillcontinuetolagsubstantiallybehindtheavailabilityofbroadbandfortheforeseeablefuture.Lastyear,investmentanalystsforecastthatabout69%ofhouseholdswillsubscribetowiredbroadband

by2015,andthat53%ofthepopulationwillsubscribetowirelessbroadbandservicesby2013.7TheupdatedforecastincludedinthisSecondReporthasnotsignificantlychanged,althoughmanyanalystsnotethatcurrentbroadbandgrowthhasbeenslowerthaninrecentyears.

Withrespecttoadoptionrates,analystforecastsandserviceproviderexpectationsincludedintheFirstReportdidnottakeintoaccounttheeffectofvariousbroadbandstimulusprogramsoranychangesingovernmentpoliciesthatmayaffectdeploymentoradoption.Ayearlater,thisis

3SeeSection3,p.65.4SeeSection3,p.65.5SeeSection3,p.65.6SeeSection3,p.65.7SeeSection3,p.65.

10

stillthecasesincethevariousbroadbandstimulusprogramsarestillintheirinfancy.Forecastsalsodonotexpectsubstantialpricereductionsthatmightstimulategreateradoptionofbroadbandbyprice‐sensitivecustomers.

Broadbandcoverage

WirelineCoverage:Ifjustthetwolargesttelephonecompanies(AT&TandVerizon)achievetheirstatedgoalsforwirelinebroadbanddeployment,atleast50millionhomeswillbeabletoreceiveadvertisedspeedsof10megabitspersecondormoredownstreamwithinthenexttwoyears.Othertelephonecompanieswillbeprovidingsimilarofferingsintheirserviceareas.Specifically,industryresearchersestimatedthatfibertothehome(FTTH)wasavailabletoabout15.2millionhomes(homespassed)inMarch2009,18.2millioninMarch2010(anincreaseof20percent),and21millioninMarch2011(anincreaseof14.6percent).8In2009,thelargestproviderofFTTHservice,Verizon,announcedthatitwouldcompleteitsFTTHdeploymentandbecapableofserving17millionlocationsby2010.9Anumberofothersmallercompanies,includingsmallruraltelephonecompanies,willbecoveringadditionalhomeswithFTTH.Inmid2010,VerizonannouncedthatthedownloadspeedofitsDSLbroadbandservicewoulddouble.10Theotherlargetelephonecompany,AT&T,announceditwouldofferDSLfromfiber‐fedcabinets(fibertotheneighborhood:FTTN‐DSL)to30millionhomesby2011.11AT&Tcurrentlyoffersadvertisedspeedsofupto18megabitsperseconddownstream12(althoughtheactualspeedcanbemuchlower),withincreasespossiblewithpairbonding.

Thecableindustryistheothermajorproviderofwirelinebroadbandservice.Cablebroadbandiscurrentlyavailableto92%ofhouseholdsaccordingtoaresearchfirmthattracksthecableindustry.13Thispercentagehasnotchangedfrom2009to2010.CablebroadbandisbeingupgradedtotheDOCSIS3.0standard14andisbecomingwidelyavailableatadvertisedspeedsashighas50mbpsdownstream(withonefirmadvertising101megabitspeeds).15Sincecablebroadbandcapacityissharedamonggroupsofcustomers,theactualspeedutilizedbyanyonecustomermaybesubstantiallylowerthantheadvertised“upto”speed.Comcast,thelargestcablecompanyaddressingnearlyhalftheUnitedStates,expectedin2009tocovernearlyallits

8RVAMarketResearchandConsulting,“NorthAmericanFTTHStatus–March31,2011”http://s.ftthcouncil.org/files/rva_ftth_status_april_2011_final_final_0.pdf9SeeSection3:UncompletedBroadbandPlans,p.65.10Verizon,“NewCopper‐BasedBroadbandTierMoreThanDoublesExistingMaximumDownloadSpeedsforConsumersandSmallBusinesses”August,2010.11SeeSection3:UncompletedBroadbandPlans,p.65.12SeeSection1:1.1Technology,p.21.13SeeSection1:1.3ExpectedDeployment/CoverageFootprint,p.36.14DOCSISisastandarddevelopedbyCableLabsandstandsfor“DataOverCableServiceInterfaceSpecification”15SeeSection1:1.1Technology,p.18.

11

50.6millionhomespassed16by2010anditislikelytoachievethisgoal,basedonrecentstatements.OneanalystbelievesDOCSIS3.0willbeavailableby2013to“nearlyall”17thehomescoveredtodaybycablemodemservices.18Thatwouldbeabout92%of112millionhouseholds,or103millionhomes.

WirelessCoverage:AnumberofwirelessbroadbandserviceprovidersexpecttodeployLongTermEvolution(LTE)andWiMAXtechnologies(so‐calledfourthgenerationor“4G”wirelessservices)between2010and2013and,ifsuccessful,bringmulti‐megabitsspeedstoamajorityofU.S.homesandpopulation.19Thewirelessservicesoffersharedbandwidth,sothespeedsobtainedbyuserswillbedependentonactualtrafficloadsateachcell‐site,andinparticularonhowmanyusersaresimultaneouslyusingbandwidth‐intensiveapplications,suchaswatchingvideoonwirelessInternetconnections.Asoneexample,by2013VerizonexpectsthatLTEwillprovidesubscriberswith5to12mbpsdownloadsinadeploymentplannedtoreachallofitscoveredpopulation(attheendof2008,Verizon’snetworkcovered288millionpeople20or94%oftheU.S.population).21Otherwirelesscompaniescoverasmallershareofthepopulation.EntrepreneurialandindependentWirelessInternetServiceProviders(WISPs)provideWiMAX‐typeservicestoatleast2millioncustomers22inruralareas,includingmanyareasnotcoveredbythenationalwirelesscompanies.

SatelliteCoverage:Satellitebroadbandisavailableatalmostanylocationinthecountrythathasanunimpededline‐of‐sighttothesouthernskyandthereforecanprovidebroadbandservicetothemostremoteanddifficult‐to‐servelocations.However,thecurrentsatelliteserviceshaverelativelylowspeedsandlatencyproblems,andcostmorethanterrestrialbroadbandservices.Twonewsatelliteswithgreatercapacityareexpectedtobecomeoperationalbeginningin2011,withtheoperatorsannouncingthateachsatellitewillbecapableofproviding2‐10mbps23service.Transmissionratesmayaverage5megabitsperseconddownstreamby2011,24butthebandwidthavailabletoeachuserwillvaryinverselywiththeactualtrafficloadasoverallbandwidthissharedamongallusers.

16SeeAppendixA.17SeeSection1:1.3ExpectedDeployment/CoverageFootprint,p.36.18SeeSection1:1.3ExpectedDeployment/CoverageFootprint,p.36.19SeeSection3,p.66.20VerizonCommunications,“2008AnnualReport,”VerizonCommunicationsInc.,2009,at9.21SeeSection1:1.1Technology,p.18.22SeeSection1:1.1Technology,p.29.23SeeSection3:3.3StatusofBroadbandSatellitePlans,p.68.24SeeSection3:3.3StatusofBroadbandSatellitePlans,p.68.

12

BroadbandTransmissionRates

FasterWirelineTransmissionRates:MostU.S.homeswillbeservedbyadvertised“upto50megabitpersecond”speedoptionswithinthenextfewyearsfromatleastonesupplier,ascableisexpectedtocovernearlyitsentirefootprint(92%ofhouseholds)withDOCSIS3.025andtelcosexpandFTTHserviceswhichhavevirtuallyunlimitedspeedcapabilityalthoughcurrentlyofferedspeedsareinthe“upto”50mbpsrange.SlowerDSL‐fiberhybrids,called“fibertothenode,”currentlyareadvertisedasproviding“upto24mbps26”downstreambyAT&T.DSLbonding,nowincommercialdeployment,isintendedtodoubleDSLspeeds.Includinghybridfiber‐DSL(FTTN‐DSL)andbondedDSL,sixtytoseventymillionhomeswillhaveachoiceofprovidersforadvertisedspeedsof10megabitsdownstreamorhigher.“Phantompair”technologyandotherdevelopmentsmayfurtherextendthelifeofDSL‐typetechnology.27

FasterWirelessSpeeds:VerizonindicatesthatitsLTEdeploymentwillbecapableofdeliveringpracticalspeedsof4to12mbps.However,wirelessbandwidthisshared,anduntilthenetworksaretestedundersubstantialloaditisnotclearwhetherspeedsabove5mbpscanbeobtainedregularlybymorethanafewsubscribersatthesametime.28Thedemandforwireless

broadbandbandwidthhasbeengrowingrapidly29andgrowthisexpectedtocontinue,

especiallyifwirelessbroadbandisusedforvideoovertheInternet.Futurepricingarrangementsforwirelessbroadbandarelikelytogreatlyaffecthowmuchvideotrafficandotherbandwidth‐intensiveapplicationsarecarriedonthewirelessbroadbandnetworks.

Improvedsatellitebroadbanddatarates:Satellites,liketerrestrialwirelesssystems,sharetheavailablebandwidthcoveredbyeachspotbeamsothespeedobtainedbyauserwilldependonthesimultaneoususageofotherusers.ViaSatexpectstooffersharedspeedsof2to10megabitsstartingin2011.30

Upstreamspeeds:Mostconsumerbroadbandservicesareasymmetrical,withdownstream

speedssignificantlyfasterthanupstreamspeeds.31FTTHofferingscurrentlyprovideadvertised

upstreamspeedsofaround20mbps,32althoughfiberhasthecapacityformuchhigherspeeds.

25SeeSection1:1.3ExpectedDeployment/CoverageFootprint,p.36.26SeeSection1:1.1Technology,p.21.27SeeSection1:1.1Technology,andAlcatelLucent,p.22.28SeeSection1:1.1Technology,p.29.29AT&T’smobiledatatraffichasincreasednearly50timesinthepastthreeyears,presumablylargelyduetotheiPhone.M.Meekeretal.,“Economy+InternetTrends,”MorganStanley,2009,at57,http://www.morganstanley.com/institutional/techresearch/pdfs/MS_Economy_Internet_Trends_102009_FINAL.pdf.30SeeSection2:ComparisonofAllPubliclyAnnouncedBroadbandPlans,p.52.31SeeAppendixA.32SeeAppendixA:Verizon.

13

DOCSIS3.0upstreamisonlyincommercialtrialsintheUnitedStates.UntilupstreamDOCSIS3.0

isfullydeployed,upstreamcablespeedswillbeintherangeof768Kbpsto5mbps.33

Broadbandadoption

In2009,approximately63%ofU.S.homesutilizedawirelinebroadbandserviceandin2010thefigurewasapproximately65%.Thisfigureisexpectedtoincreaseslowlytoabout69%by2014,

implyingmarketsaturation,atleastatcurrentpricinglevels.34In2009,investmentanalysts

estimatedthat31%ofAmericansovertheageof14currentlyusedwirelessbroadband(broadbanddoesnotincludeShortMessageService“texting”).In2010,thisfigureincreasedto38%anditisexpectedtoincreasesteadilywithanalystsexpectingwirelessbroadbandadoptiontopass50%by2013.

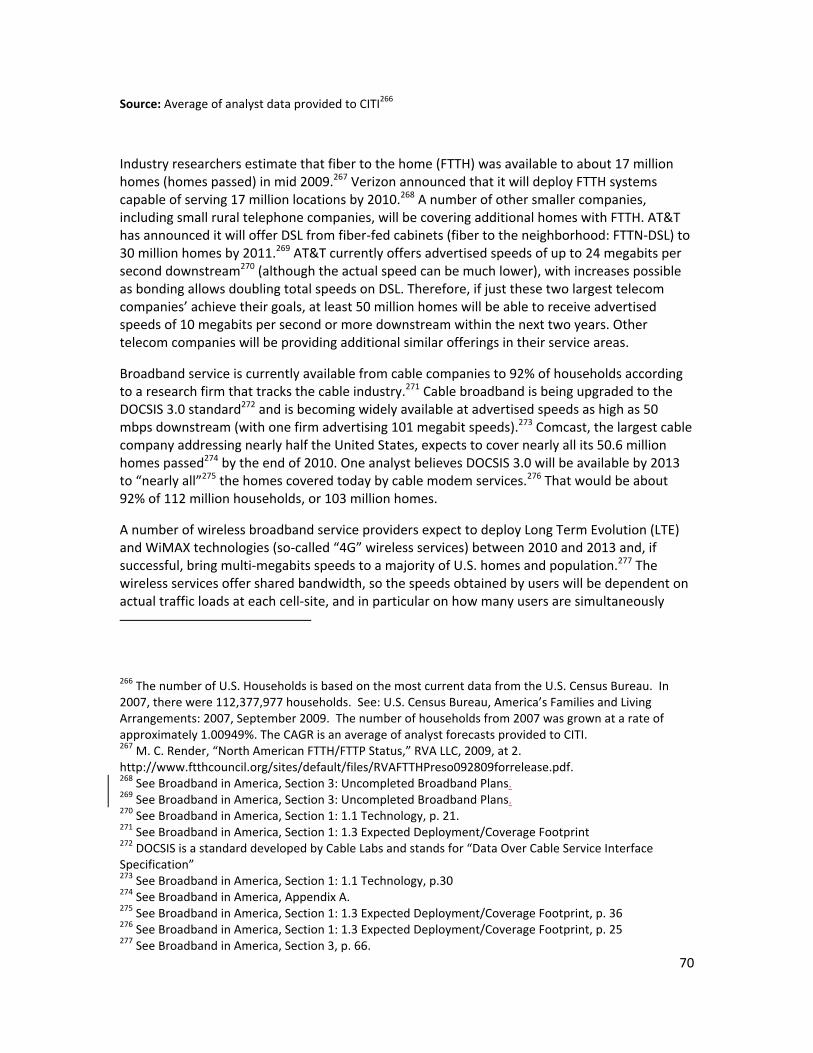

Manyhouseholdsandindividualswillsubscribetobothwirelineandwirelessbroadbandservices,justastheysubscribetofixedandmobilevoicetelephoneservices.Andjustassomeindividualshave“cutthecord”andrelyexclusivelyonamobiletelephoneforvoiceservices,somefamiliesandindividualsmaychoosetogowireless‐onlyforbroadband,35particularlyiftheyarenotusingbroadbandforvideoorvideo‐intensiveapplicationsthatrequirethehigherspeedsgenerallyobtainableonlyfromwiredservices.

Thegovernment’svariousbroadbandstimulusplansmayinfluencetheseadoptionforecaststhroughincreaseddeploymentofbroadbandtounservedareasandencouragingincreasedadoptionofbroadbandservices.However,theresultsoftheseprogramsarenotyetobservable.

Backbones

Backbonebandwidthtrafficvolumeandcapacitywillgrowroughlyatthesamepace,withaleadingnetworkequipmentfirmforecastinggrowthinNorthAmericanIPtrafficof39%(CAGR)from2009to2013.36Forthesameperiod,capacityisforecasttoincreasebyapproximately44%onmajorroutessothatmajorroutebackbonecapacityshouldkeepupwithdemandand

33Seefootnote42.34Sinceacomputerisaprerequisitetoutilizingawiredbroadbandservice,itmightbemoreaccuratetomeasureadoptionasapercentageofcomputer‐equippedhouseholdsratherthanallhouseholds.Asoneinvestmentanalystnoted,“Weestimatethereare67MbroadbandsubscribersintheU.S.,representing60%ofoccupiedhouseholdsand~70%ofPChomes.Givenbroadbandavailabilityinroughly90%ofhomes,normallydistributingPChomesacrossbroadbandavailablehomesputsrealpenetrationatalmost80%.”UBSInvestmentResearch,“SortingThroughtheDigitalTransition,”UBSAG,2009,at5.35SeeSection3:CuttingtheCord,p.65.36SeeSection1:StatusofInternetBackbone,p.13.

14

significantproblemsofbackbonecongestiononmajorroutesarenotexpected.However,localizedcongestionmayoccuronlowercapacityroutesincludingconnectionstocelltowersthatexperiencerapidwirelessbroadbandgrowth.

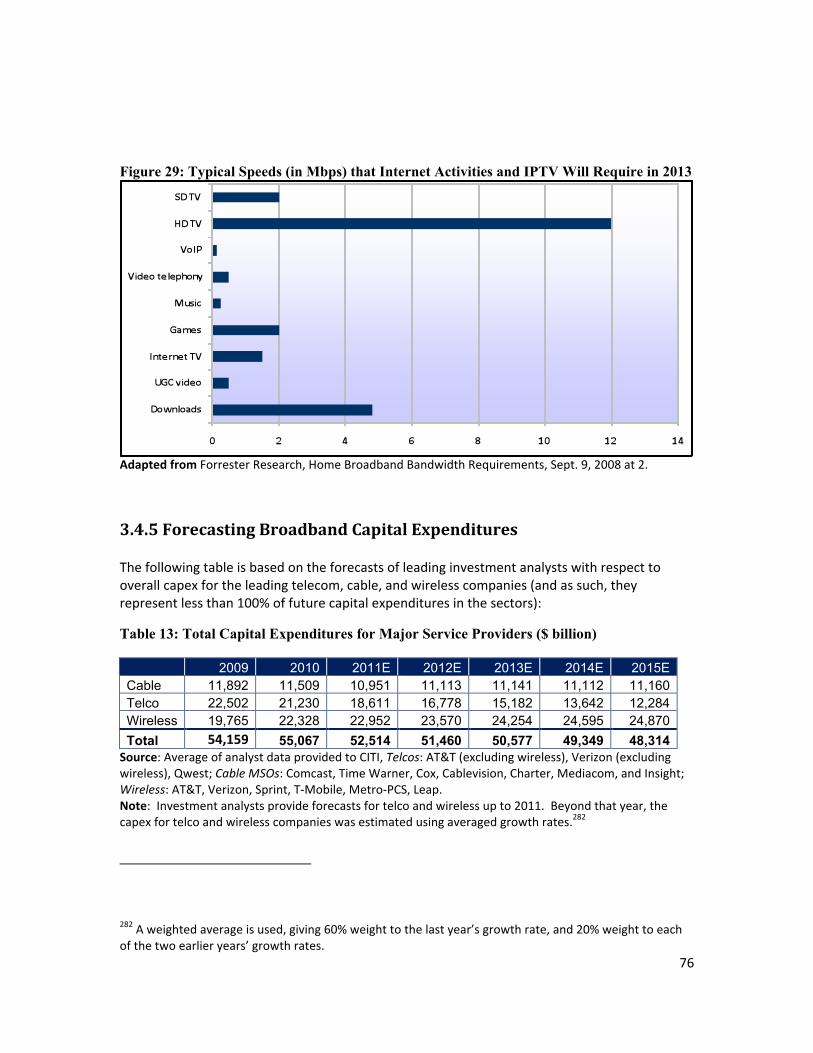

Capitalspending

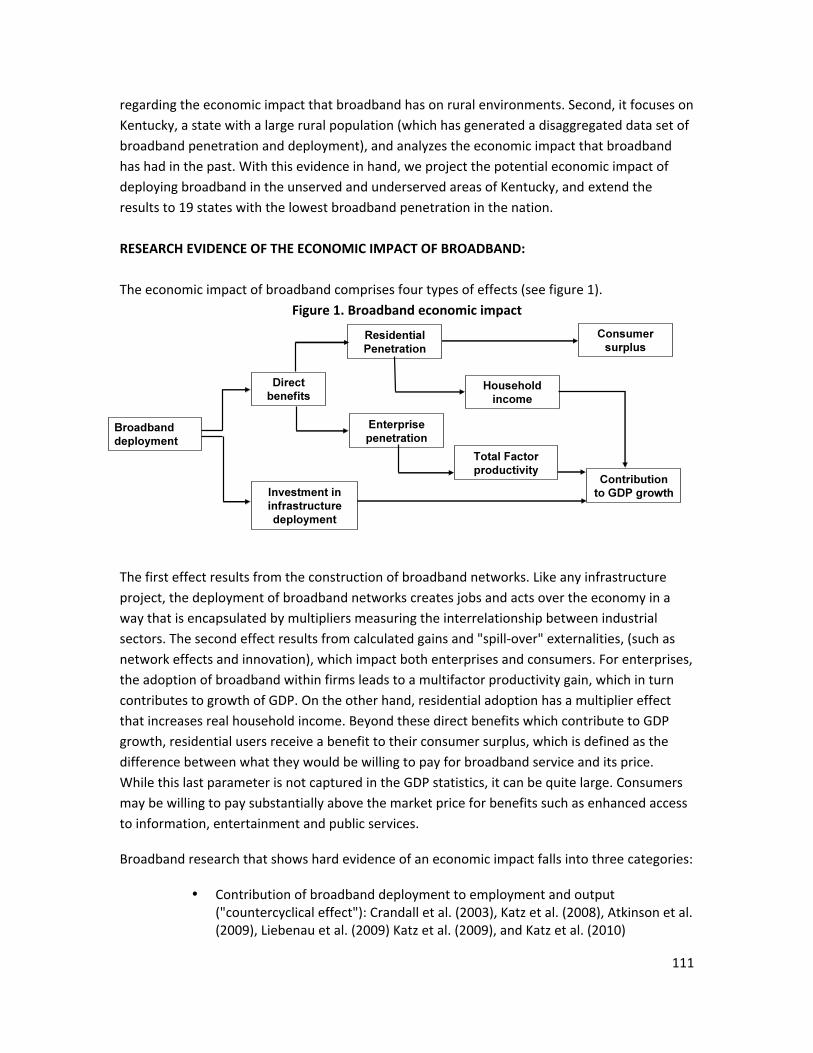

Serviceprovidersrarelybreakbroadbandoutoftheiroverallcapitalspendingfiguresforalltheirserviceofferingssoitisdifficulttoisolatebroadband‐specificcapitalexpenditures.37Indeed,muchoftheserviceproviders’capitalisinvestedinmulti‐purpose(or“converged”)digitalnetworksthatcarryvoice,data(includingbroadband)andtelevisionservicessimultaneously.Therefore,determiningwhatconstitutes“broadband”capitaloftenrequiresanallocation,whichisinherentlysubjectivetosomedegree.

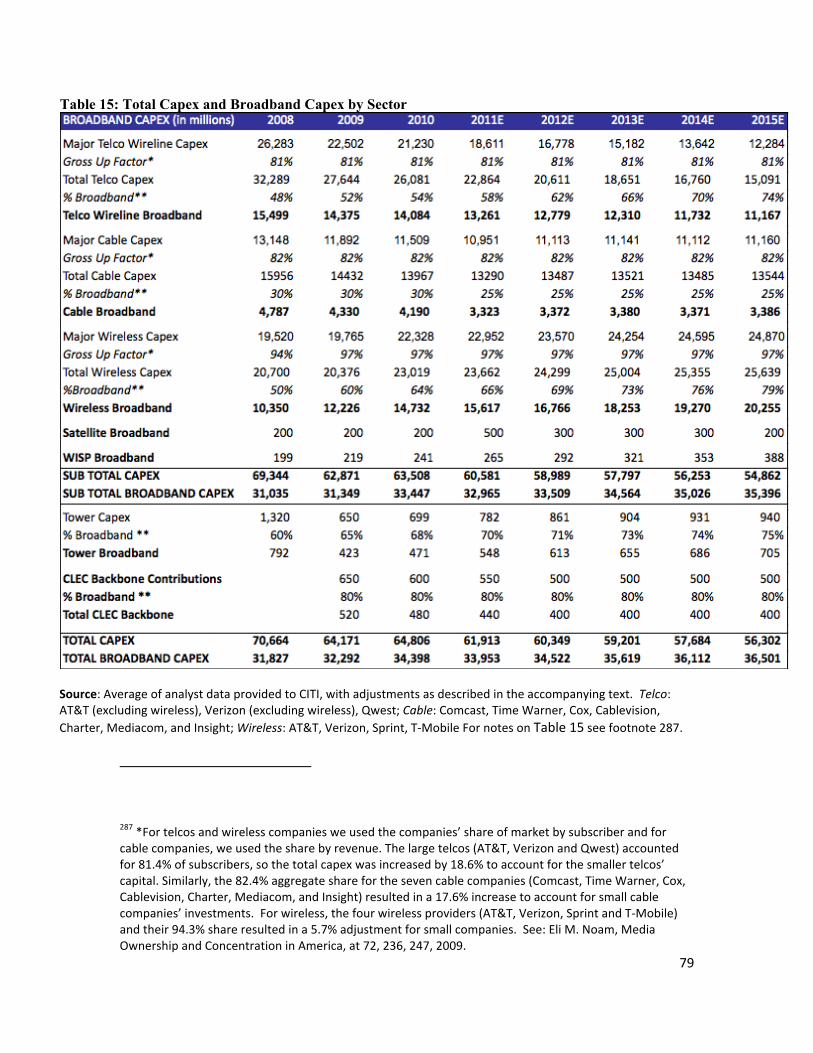

In2009,marketresearchersandinvestmentanalystsestimatedthatasmuchastwo‐thirdsofcurrentinvestmentsarebeingmadetoprovideandexpandwiredandwirelessbroadband,38andtheproportionallocatedtobroadbandhasbeengrowingoverthepastfewyears.Thistrendisexpectedtocontinueoverthenextfiveyears.

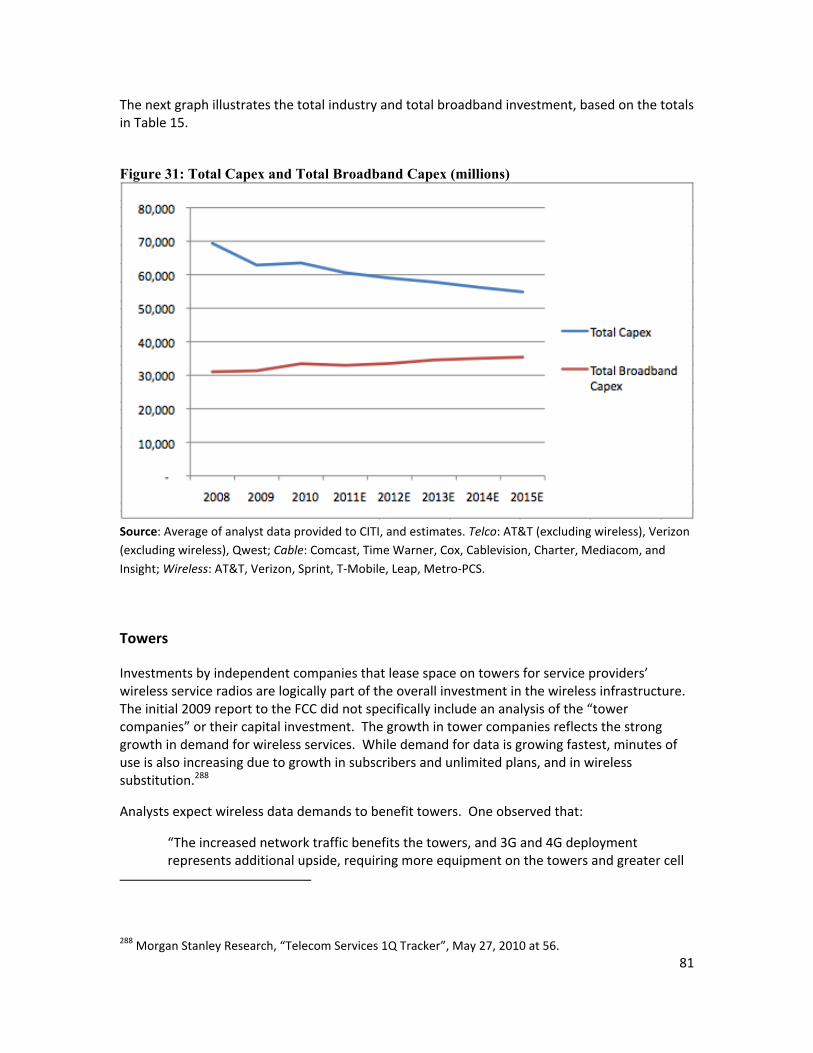

Overall,totalindustrycapitalexpendituresforallserviceswereabout$64billionfor2009(thepredictionintheFirstReportwasabout$60billion)andanalystsexpectthatnumbertobedownslightlyat$62billionfor2010andtothendecreaseinthenextfewyearsintothemid‐$50billionrangeannuallyasthemajornewbasicinfrastructuredeploymentscometoanendandcapitalisdevotedmoretoupgradesandexpandingthecapacityofthedeployedsystemsratherthanentirelynewdeployments.39

Withrespecttobroadband,theFirstReportforecastthattotalbroadbandcapexwouldbe$30billionin2009.ThisSecondReportestimatesthattheactualcapexin2009was$31.3billion,adeclineof$3billionfrom2008.Lookingforward,thisupdateforecaststhatthecapitalinvestmentsinbroadbandinfrastructurewillremainflatatapproximately$33billionperyearforthenextfewyears.Atthesametime,asnotedabove,totalcapexinallthesectors(Telco,Cable,Wireless,Satellite,TowersandWISP)isexpectedtodeclinefrom$64billionin2010to$56billionin2012.

37Suchabreakoutwouldalsobesubjecttoallocationofcapitalamongtypesofservicesforjointlyusedfacilities,suchasbackofficesystemsandbackbonetransportfacilitiesthatcarryconventionaltelephone,wireless,broadbandandvideotraffic.38SeeSection1:1.4ExpectedCapitalOutlays/OperatingExpenditures,p.3939SeeSection3:TotalCapitalExpendituresfor3LargestTelcosand7MajorCableCompanies.

15

Section1:ListingofAllPubliclyAnnouncedBroadbandPlans

Asafirststep,theFCCaskedforalistofallpubliclyannouncedbroadbandplans,

“…sortedboth(1)bycompanyandby(2)technology(e.g.DSL,cable,fiber(FTTx),fixedwireless,wireless,satellite),withadescriptionofrelevantdetails,suchas(1)generaldetailsoftheplan,includingcompany,technology,andtimeline,(2)expectedcapitaloutlaysandoperatingexpenditures,(3)expecteddeployment/coveragefootprint,(4)expectedbroadbandperformanceandquality,and(5)expectedARPUs.”

Tofindthedetailsofbroadbandplansforpubliclytradedcompanies,ourresearchersexaminedcompanies’investorrelationswebsites,includingtheirAnnualReportsfrom2004‐2010,lookedatquarterlyreportsandearningscalltranscriptsforthefirsttwoquartersof2010,searchedforinvestmentanalysts’reportsusingtheThomsonOnedatabase,andfinally,usedgeneralwebsearchestoobtainadditionalinformation.

Obtaininginformationaboutprivatelyheldcompanieswasmoredifficult.Sincemanyofthenon‐publiccompaniesaresmallcable,telephoneandwirelessInternetserviceprovider(WISP)companiesthattendtoservethemoreruralpartsofthecountry,informationwasscarcestforthe“unserved”and“underserved”populations.Toobtaininformationaboutprivatecompaniesordivisionsofpubliccompanies,ourresearchersreviewedcompanywebsites,contactedrelevanttradeassociations,andperformedgeneralwebsearches.Aggregatedinformationaboutsmallercompanieswasobtainedfromreportsandsurveysbycable,wireless,andtelephonecompanytradeassociations.

Oncethepreliminaryinformationwascompiled,company‐specificinformationwassenttothesubjectcompanyaskingforverificationoftheinformationgatheredtothatpoint.Responseswerereceivedfromsomecompaniesandadjustmentsweremadebasedonacompany’ssuggestionafterconfirmingtheaccuracyoftheadditionalinformation.

Thecompletedatabaseisavailableonline.40TheAppendixtothisSecondReportcontainscompany‐by‐companyinformationextractedfromtheonlinedatabasefor33companies(therewere29companyprofilesintheFirstReport)withpubliclyannouncedbroadbandplans.Theinformationwassortedbycompanyandbytechnology,wherepossible.Asalways,wewelcomefurtherupdatesandadditionalinformationfromanycompanyinvolvedintheprovisionofbroadbandservicesandwillupdatethedatabaseaccordingly.41

40Seehttp://www4.gsb.columbia.edu/citi/research/current41Updatedandadditionalinformationshouldbesentto:CITI‐[email protected].

16

ThedetailsofthedatabasecanbeseenintheAppendix,whichlistsinformation,includingdetailsofcurrentbroadbanddeployments,forthefollowing:

Company Page Company PageAT&T A‐2 MediaCom A‐23CableOne A‐6 MetroPCS A‐24Cablevision A‐7 OpenRange A‐25CenturyLink A‐8 Qwest A‐26Charter A‐9 RCN A‐27CincinnatiBell A‐10 SprintNextel A‐28Clearwire A‐11 T‐Mobile A‐31Comcast A‐13 TimeWarnerCable A‐32Cox A‐14 Verizon A‐33EchoStarCorp A‐15 ViaSat A‐37Fairpoint A‐16 WildBlue A‐38Frontier A‐17 Windstream A‐39Gilat A‐18 WISPIndustry A‐40Hughes A‐19 OPATSCO A‐41Insight A‐20 AmericanCableAssoc. A‐42Knology A‐21 NTCA A‐43LeapWireless A‐22

Toreiterate,theFCCaskedustofocusourresearchontheinformationprovidedbythebroadbandserviceproviders.ThefollowingnarrativebroadlysummarizestheinformationinthedatabasewithrespecttosixcategoriesspecifiedbytheFCC:

1)Technology,

2)TimelineforDeployment,ExpectedDeployments,

3)CoverageFootprintandPenetration,

4)ExpectedCapitalOutlays/Operatingexpenditures,

5)ExpectedBroadbandPerformanceandQuality,

6)ExpectedARPUs.

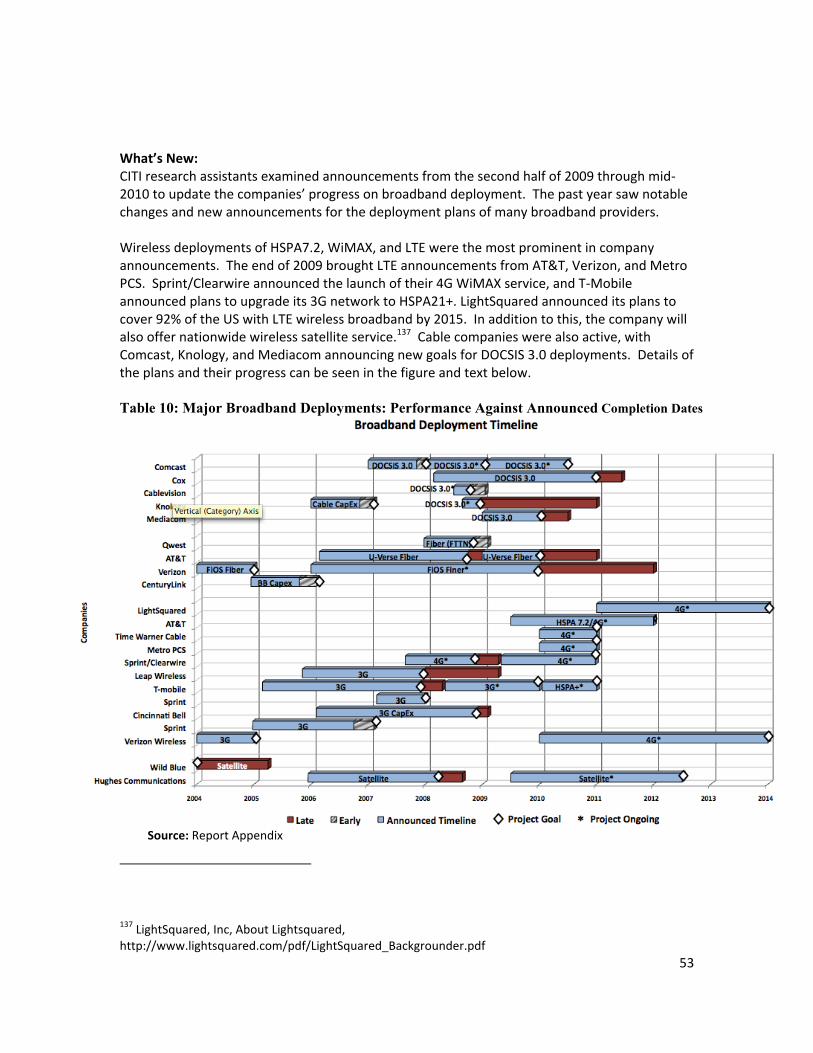

What’sNew:

ToupdatetheFirstReport,CITIresearchassistantsfollowedthesamemethodology(describedabove)usedtopreparetheoriginalReportaddingupdatesformergedcompaniesand,forthe

17

firsttime,includingplansfortowercompaniessincesuchcompaniesclearlyprovideacrucialpartofthewirelessinfrastructure.

Detailsdescribingthe2009‐2010changesarenotedineachsubsectionofthisreport.Insummary:

• SincethereleaseoftheoriginalReportinNovember2009,therehasbeenevolutionarygrowthinthenewerbroadbandtechnologies,includingFTTH,DOCSIS3.0,and4Gwirelessservices.Boththetelcosandcablecompanieshavebeengainingsubscriberswiththeirhigherspeedofferingsandwirelessbroadbandisgrowingbrisklywiththeintroductionof4Gwirelessclearlyonthehorizon.Bycontrast,thenumberofsubscribersutilizingthemorematureandsomewhatobsolescentDSLtechnologyhasbeendeclining.

• In2010,cableandwirelessbroadbandprovidersincreasedtheircapexspending,whilewirelinetelcobroadbandprovidersdecreasedtheircapexspending.Thenetresultisthattotalbroadbandcapitalexpenditureshavebeendecreasingandthedownwardtrendisexpectedtocontinue.

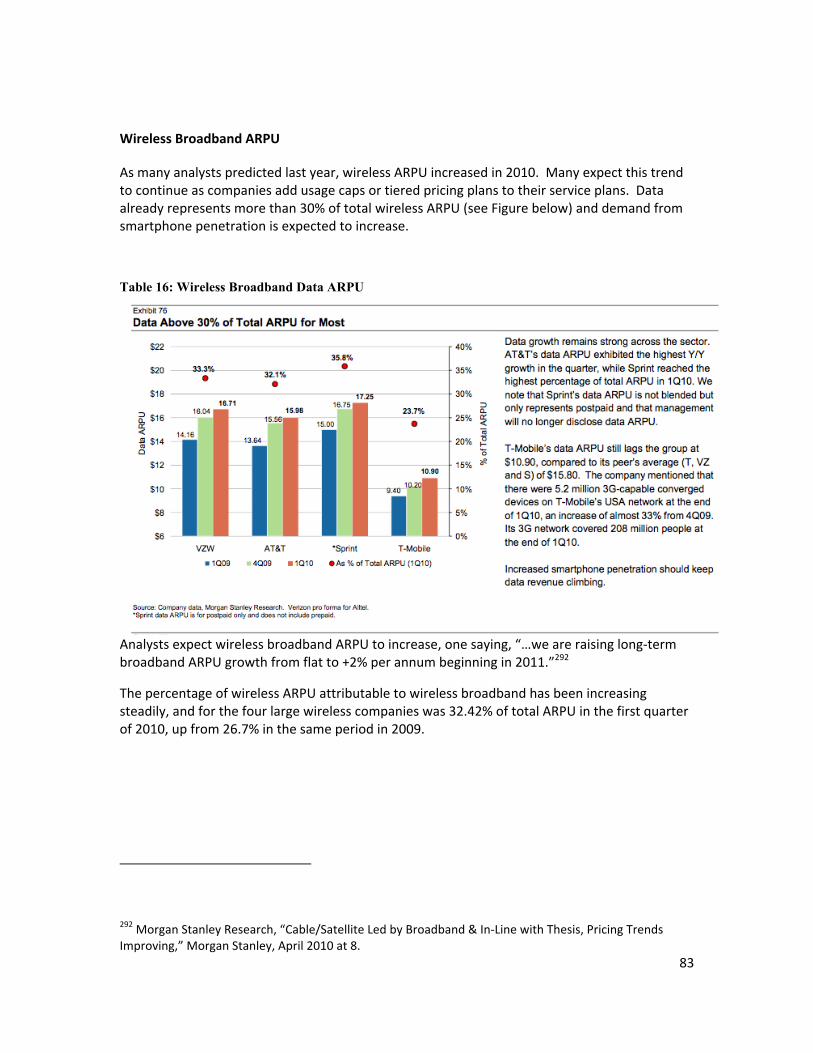

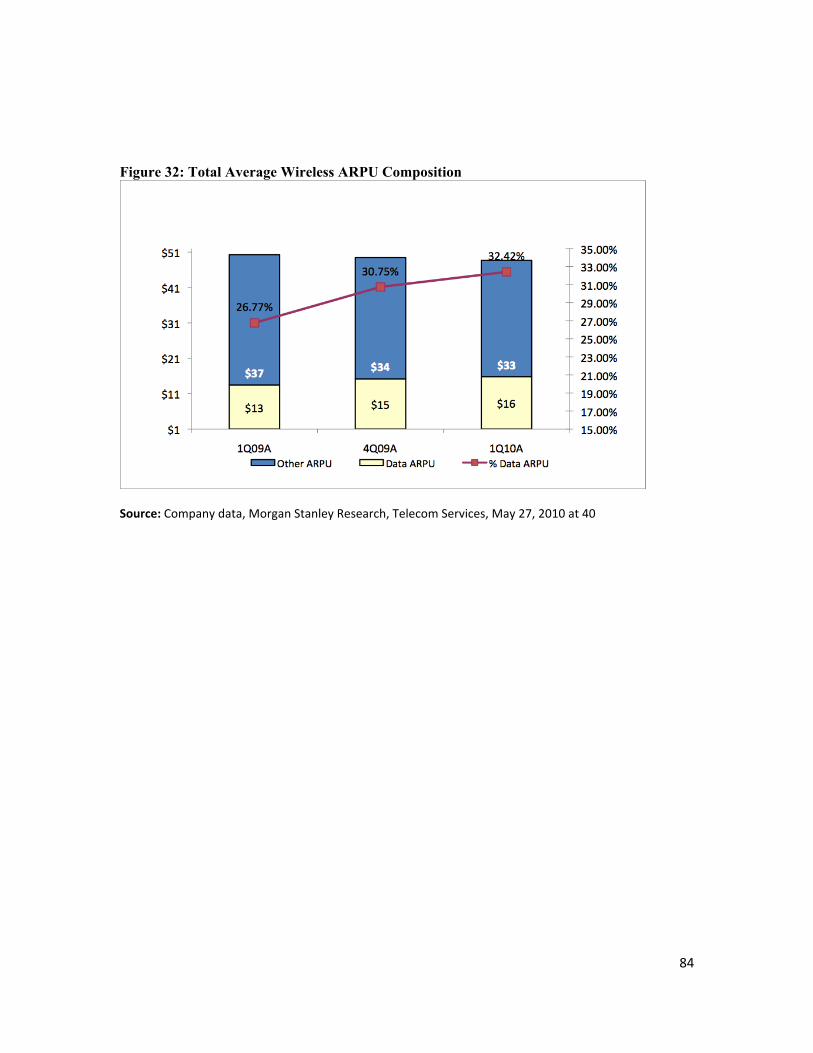

• Averagerevenueperuser(ARPU)forbroadbandservicesisincreasinglydifficulttocalculatesincemanybroadbandservicesarepurchasedaspartofadiscountedbundleofvoice,video,andevenwirelessservice.ForthebroadbandARPUsthatareavailable,thetrendhasbeenslightlyupward,astheresultofpriceincreasesofabout2%annually.

18

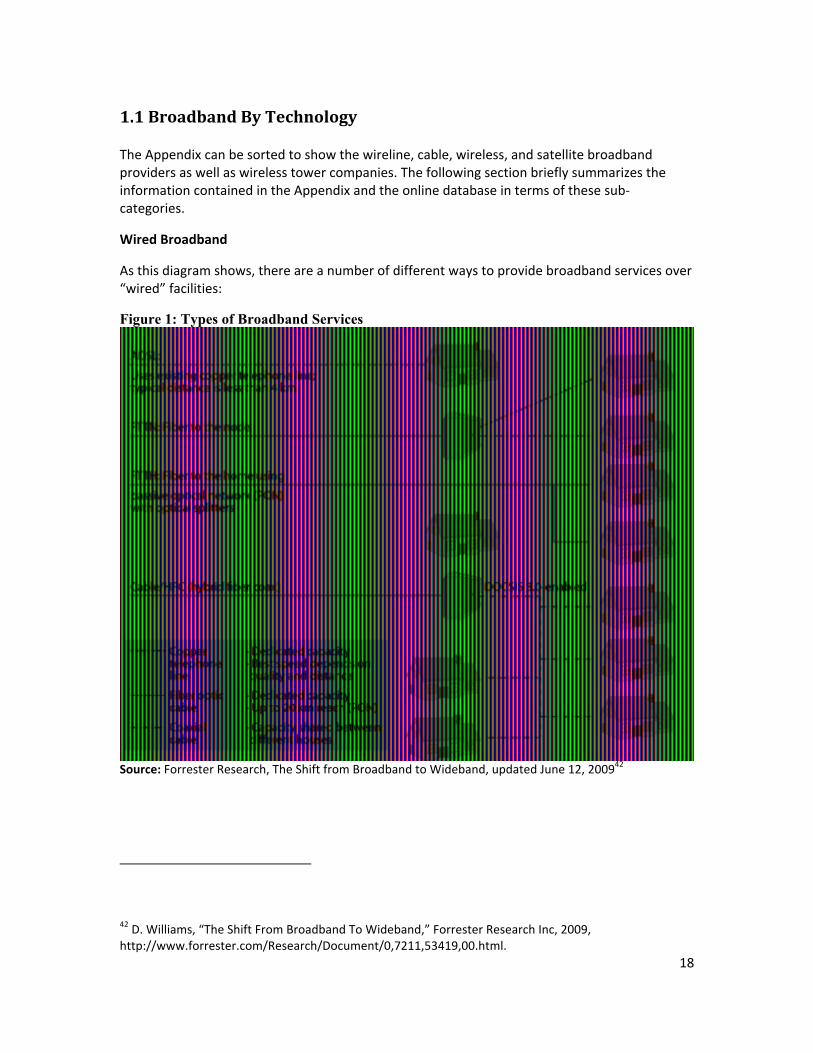

1.1BroadbandByTechnology

TheAppendixcanbesortedtoshowthewireline,cable,wireless,andsatellitebroadbandprovidersaswellaswirelesstowercompanies.ThefollowingsectionbrieflysummarizestheinformationcontainedintheAppendixandtheonlinedatabaseintermsofthesesub‐categories.

WiredBroadband

Asthisdiagramshows,thereareanumberofdifferentwaystoprovidebroadbandservicesover“wired”facilities:

Figure 1: Types of Broadband Services

Source:ForresterResearch,TheShiftfromBroadbandtoWideband,updatedJune12,200942

42D.Williams,“TheShiftFromBroadbandToWideband,”ForresterResearchInc,2009,http://www.forrester.com/Research/Document/0,7211,53419,00.html.

19

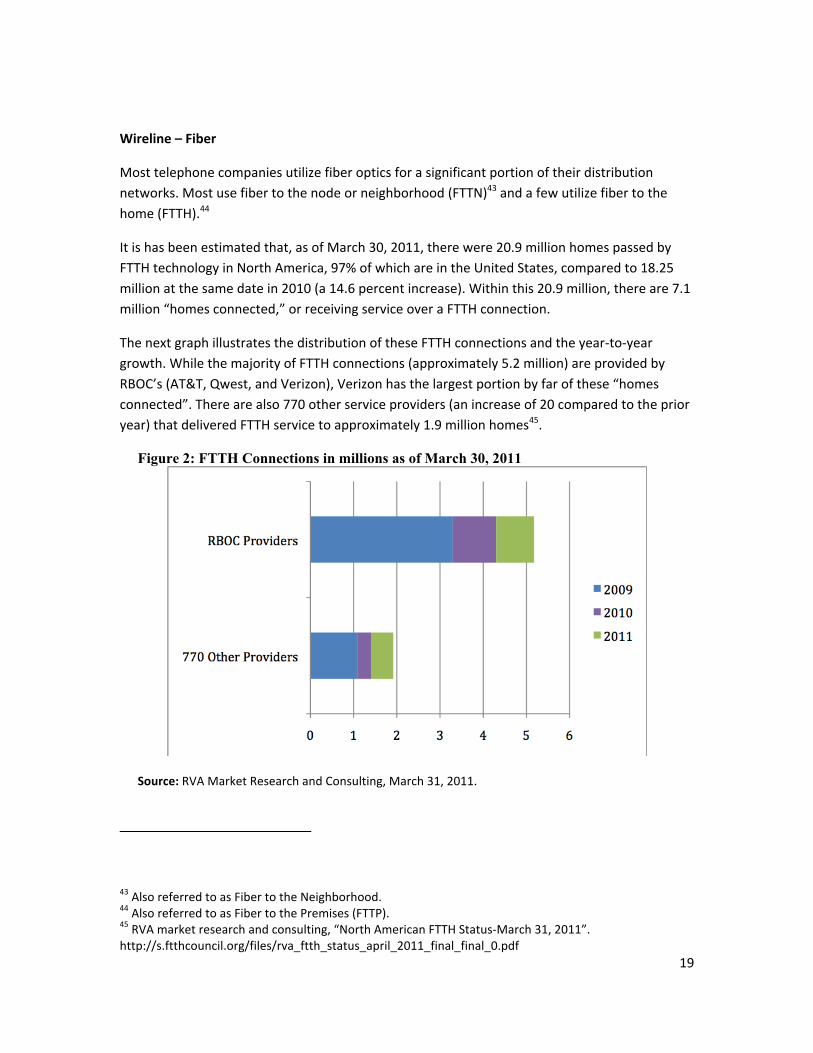

Wireline–Fiber

Mosttelephonecompaniesutilizefiberopticsforasignificantportionoftheirdistributionnetworks.Mostusefibertothenodeorneighborhood(FTTN)43andafewutilizefibertothehome(FTTH).44

Itishasbeenestimatedthat,asofMarch30,2011,therewere20.9millionhomespassedbyFTTHtechnologyinNorthAmerica,97%ofwhichareintheUnitedStates,comparedto18.25millionatthesamedatein2010(a14.6percentincrease).Withinthis20.9million,thereare7.1million“homesconnected,”orreceivingserviceoveraFTTHconnection.

ThenextgraphillustratesthedistributionoftheseFTTHconnectionsandtheyear‐to‐yeargrowth.WhilethemajorityofFTTHconnections(approximately5.2million)areprovidedbyRBOC’s(AT&T,Qwest,andVerizon),Verizonhasthelargestportionbyfarofthese“homesconnected”.Therearealso770otherserviceproviders(anincreaseof20comparedtotheprioryear)thatdeliveredFTTHservicetoapproximately1.9millionhomes45.

Figure 2: FTTH Connections in millions as of March 30, 2011

Source:RVAMarketResearchandConsulting,March31,2011.

43AlsoreferredtoasFibertotheNeighborhood.44AlsoreferredtoasFibertothePremises(FTTP).45RVAmarketresearchandconsulting,“NorthAmericanFTTHStatus‐March31,2011”.http://s.ftthcouncil.org/files/rva_ftth_status_april_2011_final_final_0.pdf

20

Whilethemajorityofnon‐RBOCFTTHserviceisprovidedbyotherlocalexchangetelephonecompanies(ILECs),FTTHisalsoprovidedbyfacilities‐basedCLECs,realestatedevelopers,andmunicipalities.Astheresearchfirmnoted,

“VerizonandTier3ILECs(generallysmall,singleindependentlocalexchangecarriers)haveactuallypenetratedarelativelyhighpercentoftheircustomerbase.Theseproviders–whowemaycallaggressiveILECs‐coverroughlyonethirdoftheUSpopulation”46

Perhapsmostsurprisingisthecommitmentofsomesmall,usuallyrural,telephonecompaniestofiberdeployment.Theresearchfirmexplainedthat

“Driversfortheruralindependenttelcos[todeployFTTH]includeagingcopperlinesinneedofreplacement,theopportunitytodelivervideogivenamorerobustplatform,andapioneeringtradition.Insomecases,theseprovidershavealsobeenaidedbyloansandsubsidiessuchasruralbroadbandloanprogramsanduniversalservicefunds.”47

Inadditiontothe“Tier3”telephonecompanies,municipalities(particularlythoseinruralareas)havedeployedFTTHsystems,whichare“…usuallyundertakenafterprivateserviceprovidershavedeclinedtoupgradetheirnetworksorbuildsuchsystems.”48TheFirstReportreported57publicFTTHsystemsintheU.S.,mostlyinsmallruraltowns.Thereisno2010updateforthistotal.49DistributionoffibersubscribersamongRBOCsandnon‐RBOCprovidersaregiveninthefollowinggraph.

46RVAmarketresearchandconsulting,“NorthAmericanFTTHStatus‐March31,2011”.http://s.ftthcouncil.org/files/rva_ftth_status_april_2011_final_final_0.pdf47Ibid.48D.St.John,“MunicipalFibertotheHomeDeployments:NextGenerationBroadbandasaMunicipalUtility,”FTTHCouncil,2009,at1,http://www.baller.com/pdfs/MuniFiberNetsOct09.pdf.49Forthelistofthe57municipalities,seeibidat5.

21

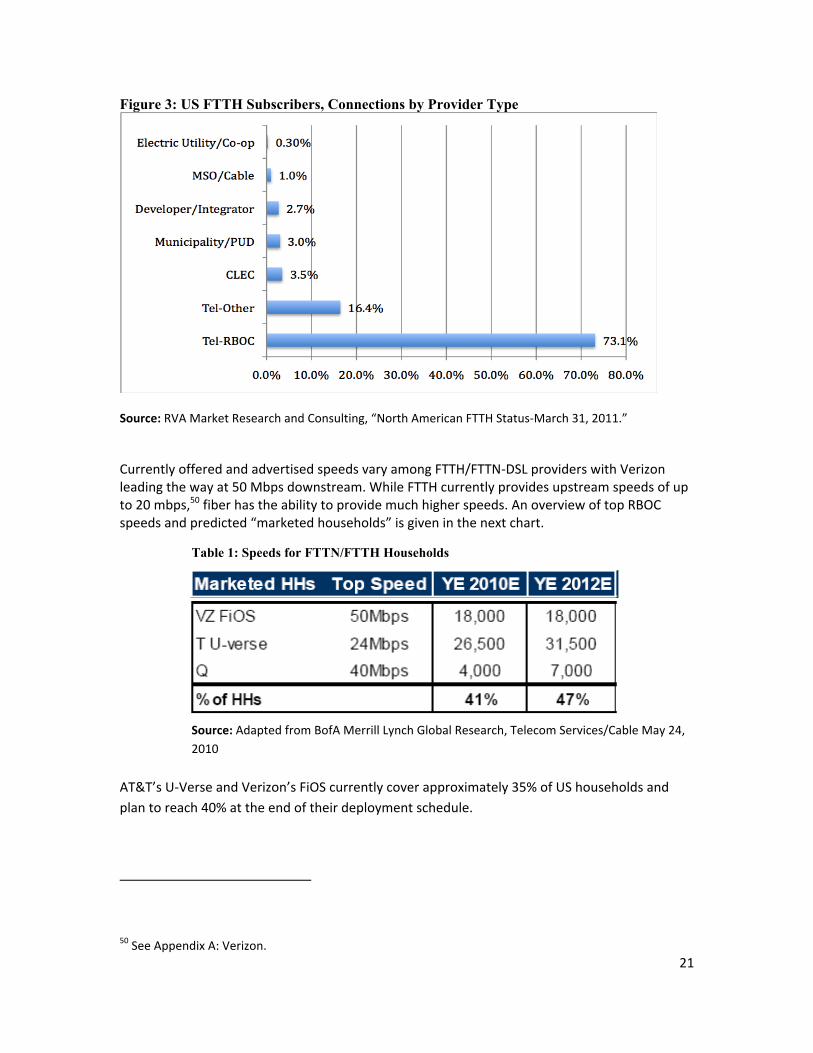

Figure 3: US FTTH Subscribers, Connections by Provider Type

Source:RVAMarketResearchandConsulting,“NorthAmericanFTTHStatus‐March31,2011.”

CurrentlyofferedandadvertisedspeedsvaryamongFTTH/FTTN‐DSLproviderswithVerizonleadingthewayat50Mbpsdownstream.WhileFTTHcurrentlyprovidesupstreamspeedsofupto20mbps,50fiberhastheabilitytoprovidemuchhigherspeeds.AnoverviewoftopRBOCspeedsandpredicted“marketedhouseholds”isgiveninthenextchart.

Table 1: Speeds for FTTN/FTTH Households

Source:AdaptedfromBofAMerrillLynchGlobalResearch,TelecomServices/CableMay24,2010

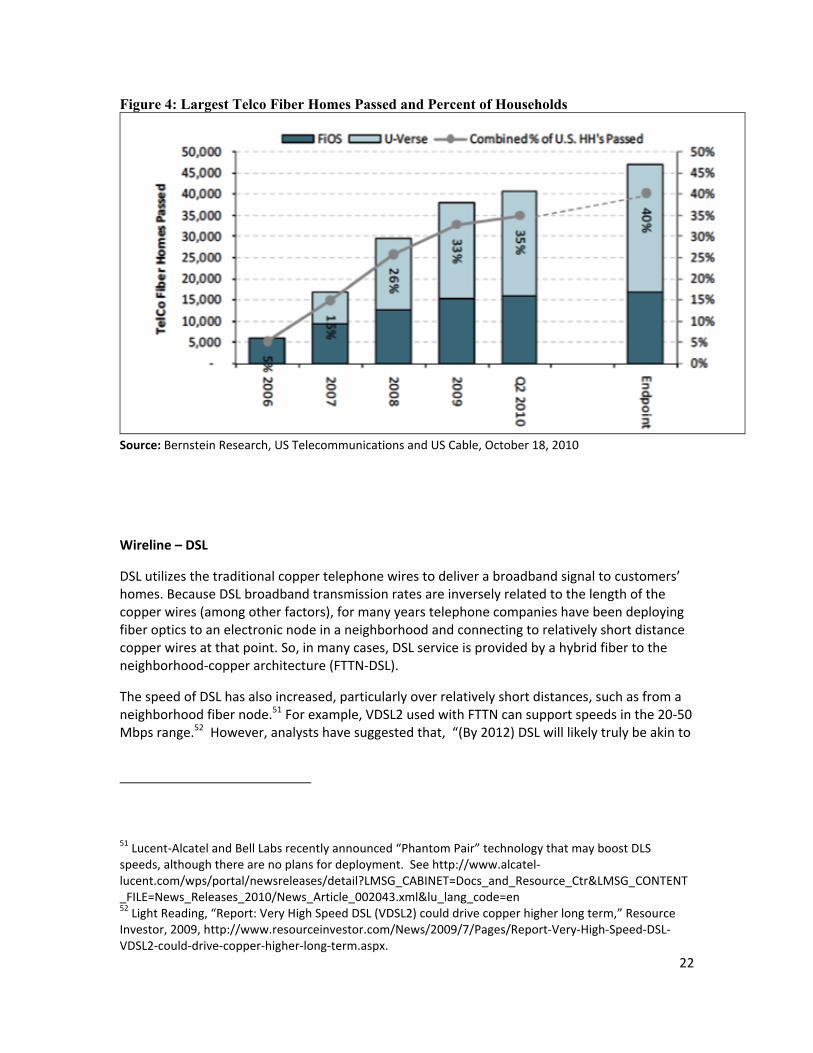

AT&T’sU‐VerseandVerizon’sFiOScurrentlycoverapproximately35%ofUShouseholdsandplantoreach40%attheendoftheirdeploymentschedule.

50SeeAppendixA:Verizon.

22

Figure 4: Largest Telco Fiber Homes Passed and Percent of Households

Source:BernsteinResearch,USTelecommunicationsandUSCable,October18,2010

Wireline–DSL

DSLutilizesthetraditionalcoppertelephonewirestodeliverabroadbandsignaltocustomers’homes.BecauseDSLbroadbandtransmissionratesareinverselyrelatedtothelengthofthecopperwires(amongotherfactors),formanyyearstelephonecompanieshavebeendeployingfiberopticstoanelectronicnodeinaneighborhoodandconnectingtorelativelyshortdistancecopperwiresatthatpoint.So,inmanycases,DSLserviceisprovidedbyahybridfibertotheneighborhood‐copperarchitecture(FTTN‐DSL).

ThespeedofDSLhasalsoincreased,particularlyoverrelativelyshortdistances,suchasfromaneighborhoodfibernode.51Forexample,VDSL2usedwithFTTNcansupportspeedsinthe20‐50Mbpsrange.52However,analystshavesuggestedthat,“(By2012)DSLwilllikelytrulybeakinto

51Lucent‐AlcatelandBellLabsrecentlyannounced“PhantomPair”technologythatmayboostDLSspeeds,althoughtherearenoplansfordeployment.Seehttp://www.alcatel‐lucent.com/wps/portal/newsreleases/detail?LMSG_CABINET=Docs_and_Resource_Ctr&LMSG_CONTENT_FILE=News_Releases_2010/News_Article_002043.xml&lu_lang_code=en52LightReading,“Report:VeryHighSpeedDSL(VDSL2)coulddrivecopperhigherlongterm,”ResourceInvestor,2009,http://www.resourceinvestor.com/News/2009/7/Pages/Report‐Very‐High‐Speed‐DSL‐VDSL2‐could‐drive‐copper‐higher‐long‐term.aspx.

23

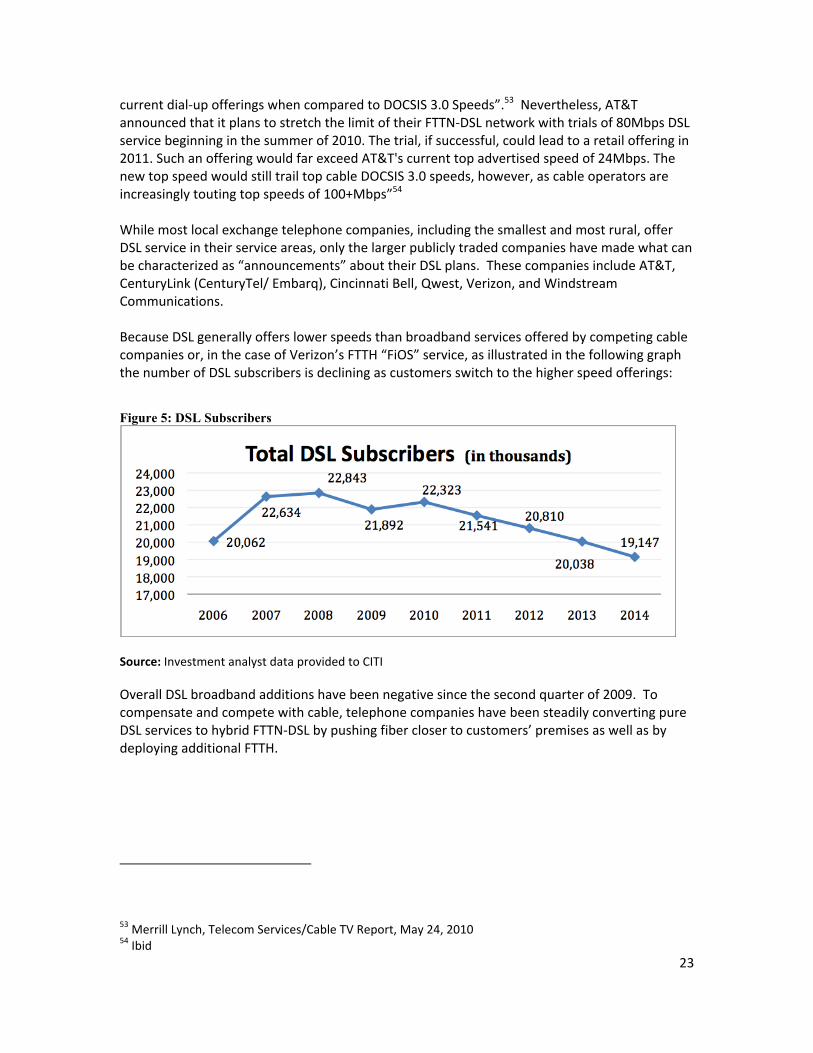

currentdial‐upofferingswhencomparedtoDOCSIS3.0Speeds”.53Nevertheless,AT&TannouncedthatitplanstostretchthelimitoftheirFTTN‐DSLnetworkwithtrialsof80MbpsDSLservicebeginninginthesummerof2010.Thetrial,ifsuccessful,couldleadtoaretailofferingin2011.SuchanofferingwouldfarexceedAT&T'scurrenttopadvertisedspeedof24Mbps.ThenewtopspeedwouldstilltrailtopcableDOCSIS3.0speeds,however,ascableoperatorsareincreasinglytoutingtopspeedsof100+Mbps”54Whilemostlocalexchangetelephonecompanies,includingthesmallestandmostrural,offerDSLserviceintheirserviceareas,onlythelargerpubliclytradedcompanieshavemadewhatcanbecharacterizedas“announcements”abouttheirDSLplans.ThesecompaniesincludeAT&T,CenturyLink(CenturyTel/Embarq),CincinnatiBell,Qwest,Verizon,andWindstreamCommunications.BecauseDSLgenerallyofferslowerspeedsthanbroadbandservicesofferedbycompetingcablecompaniesor,inthecaseofVerizon’sFTTH“FiOS”service,asillustratedinthefollowinggraphthenumberofDSLsubscribersisdecliningascustomersswitchtothehigherspeedofferings:

Figure 5: DSL Subscribers

Source:InvestmentanalystdataprovidedtoCITI

OverallDSLbroadbandadditionshavebeennegativesincethesecondquarterof2009.Tocompensateandcompetewithcable,telephonecompanieshavebeensteadilyconvertingpureDSLservicestohybridFTTN‐DSLbypushingfiberclosertocustomers’premisesaswellasbydeployingadditionalFTTH.

53MerrillLynch,TelecomServices/CableTVReport,May24,201054Ibid

24

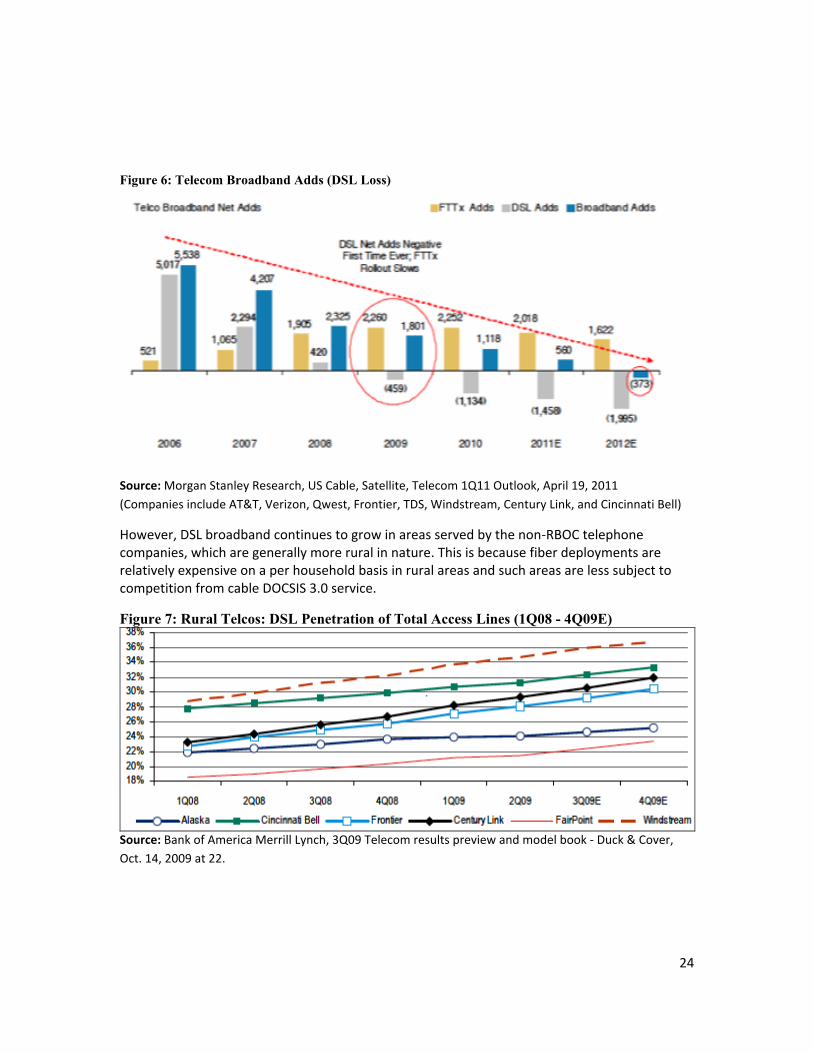

Figure 6: Telecom Broadband Adds (DSL Loss)

Source:MorganStanleyResearch,USCable,Satellite,Telecom1Q11Outlook,April19,2011(CompaniesincludeAT&T,Verizon,Qwest,Frontier,TDS,Windstream,CenturyLink,andCincinnatiBell)

However,DSLbroadbandcontinuestogrowinareasservedbythenon‐RBOCtelephonecompanies,whicharegenerallymoreruralinnature.ThisisbecausefiberdeploymentsarerelativelyexpensiveonaperhouseholdbasisinruralareasandsuchareasarelesssubjecttocompetitionfromcableDOCSIS3.0service.

Figure 7: Rural Telcos: DSL Penetration of Total Access Lines (1Q08 - 4Q09E)

Source:BankofAmericaMerrillLynch,3Q09Telecomresultspreviewandmodelbook‐Duck&Cover,Oct.14,2009at22.

25

In2009,oneinvestmentanalystsuggestedthatbroadbandpenetrationasapercentageoftotalsubscriberswashigher(30.5%)forruraltelephonecompaniescomparedtotheRBOCs(27.7%forVerizon,AT&TandQwest55)becauseruralcarriersgenerallyfacelowercablepenetrationandalesscompetitiveenvironmentthanthemajortelephonecompanies.Theanalystalsopointedout,however,thattheruralcarriersmayhavelessgrowthpotentialthanthemoreurbancarriersbecauseoflowerpersonalcomputerpenetrationinruralhomes.

ThesmallesttelephonecompaniesrepresentedbytheNationalTelephoneCooperativeAssociation(NTCA)alsohaveahighpenetrationofbroadbandlinesintheirruralareas.LastyearNCTAreportedthat:

“...oursurveyresultsshowedthatrespondentswereofferingbroadbandserviceinexcessof768kbpsto83%oftheircustomers.Applyingthatnumbertoourestimateof3.5millionaccesslinesgive2.9millionbroadbandlinesservedbyNTCAmembercompanies.”56

NTCAhasnotprovidedupdatednumbersforaccesslinesorbroadbandlinesfor2010.

Wireline‐Cable:Cabletelevisioncompanieshavebeensignificantprovidersofbroadbandinternetaccessservicesformanyyearsandcurrentlyprovideinternetaccesstoanestimated39%ofhouseholds(versus31%fortelcobroadband).57Cablepenetrationnumbershaveincreasedbytwopercentfrom2009to2010.

Cablebroadbandgenerallyusesahybridfiber‐coaxarchitecture:fiberopticsbringscableservicestoaneighborhoodnodeatwhichpointconnectionsaremadetocoaxialcablesthatservethecustomers’premises.Incontrasttotelephonecompanies’FTTHandFTTN,clustersofhybridfiber‐coaxuserssharethecapacityofeachnodesoactualspeedsvarydependingonthesimultaneoususebyothersservedbythesamenode.58Mostcablebroadbandsystemsarecurrentlycapableofprovidingdownloadspeedsofatleast10mbps.59

ThefivelargestcableMultipleSystemOperators(MSOs)accountforasubstantialnumberofhomespassedandcansupplybroadbandservicetonearlyallofthesehomes,asexpressedinthefollowinggraph:

55MorganStanleyResearch,“TelecomServices,”MorganStanley,2009,at42.56DataprovidedfromNTCAtoCITI,2009.NTCAalsonotedthat“themarginoferrorcouldpotentiallybefairlylarge.”57J.Armstrongetal.,“Americas:CommunicationsServices,”TheGoldmanSachsGroupInc,2009at15.;GoldmanSachsResearch,USServicesReview(1Q10),May2010at17.58D.Williams,“TheShiftfromBroadbandtoWideband,”ForresterResearchInc,2009,http://www.forrester.com/Research/Document/0,7211,53419,00.html.59Ibid.

26

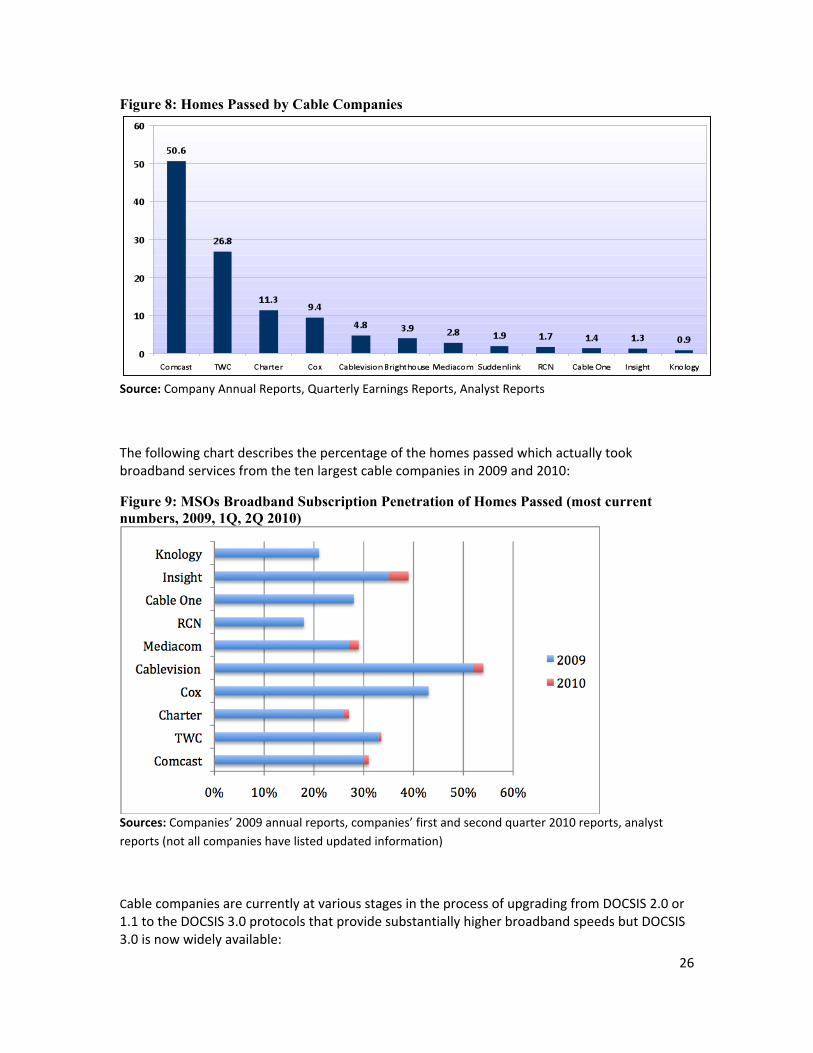

Figure 8: Homes Passed by Cable Companies

Source:CompanyAnnualReports,QuarterlyEarningsReports,AnalystReports

Thefollowingchartdescribesthepercentageofthehomespassedwhichactuallytookbroadbandservicesfromthetenlargestcablecompaniesin2009and2010:

Figure 9: MSOs Broadband Subscription Penetration of Homes Passed (most current numbers, 2009, 1Q, 2Q 2010)

Sources:Companies’2009annualreports,companies’firstandsecondquarter2010reports,analystreports(notallcompanieshavelistedupdatedinformation)

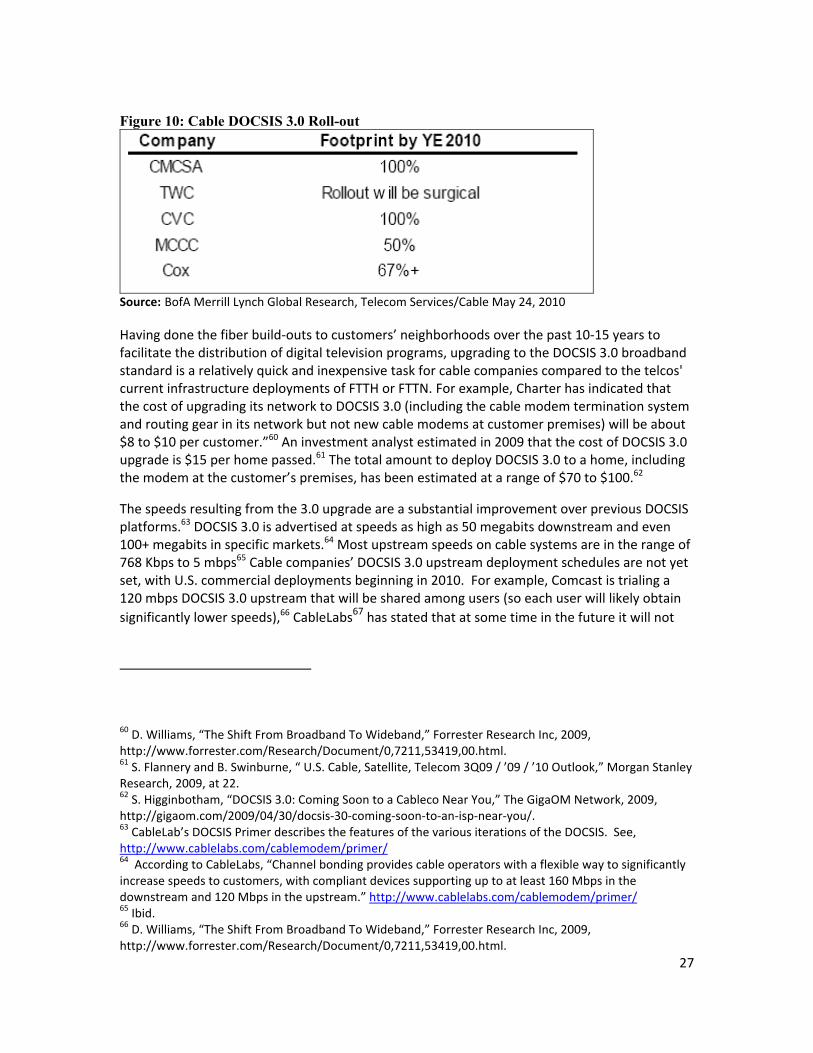

CablecompaniesarecurrentlyatvariousstagesintheprocessofupgradingfromDOCSIS2.0or1.1totheDOCSIS3.0protocolsthatprovidesubstantiallyhigherbroadbandspeedsbutDOCSIS3.0isnowwidelyavailable:

27

Figure 10: Cable DOCSIS 3.0 Roll-out

Source:BofAMerrillLynchGlobalResearch,TelecomServices/CableMay24,2010

Havingdonethefiberbuild‐outstocustomers’neighborhoodsoverthepast10‐15yearstofacilitatethedistributionofdigitaltelevisionprograms,upgradingtotheDOCSIS3.0broadbandstandardisarelativelyquickandinexpensivetaskforcablecompaniescomparedtothetelcos'currentinfrastructuredeploymentsofFTTHorFTTN.Forexample,CharterhasindicatedthatthecostofupgradingitsnetworktoDOCSIS3.0(includingthecablemodemterminationsystemandroutinggearinitsnetworkbutnotnewcablemodemsatcustomerpremises)willbeabout$8to$10percustomer.”60Aninvestmentanalystestimatedin2009thatthecostofDOCSIS3.0upgradeis$15perhomepassed.61ThetotalamounttodeployDOCSIS3.0toahome,includingthemodematthecustomer’spremises,hasbeenestimatedatarangeof$70to$100.62

Thespeedsresultingfromthe3.0upgradeareasubstantialimprovementoverpreviousDOCSISplatforms.63DOCSIS3.0isadvertisedatspeedsashighas50megabitsdownstreamandeven100+megabitsinspecificmarkets.64Mostupstreamspeedsoncablesystemsareintherangeof768Kbpsto5mbps65Cablecompanies’DOCSIS3.0upstreamdeploymentschedulesarenotyetset,withU.S.commercialdeploymentsbeginningin2010.Forexample,Comcastistrialinga120mbpsDOCSIS3.0upstreamthatwillbesharedamongusers(soeachuserwilllikelyobtainsignificantlylowerspeeds),66CableLabs67hasstatedthatatsometimeinthefutureitwillnot

60D.Williams,“TheShiftFromBroadbandToWideband,”ForresterResearchInc,2009,http://www.forrester.com/Research/Document/0,7211,53419,00.html.61S.FlanneryandB.Swinburne,“U.S.Cable,Satellite,Telecom3Q09/’09/’10Outlook,”MorganStanleyResearch,2009,at22.62S.Higginbotham,“DOCSIS3.0:ComingSoontoaCablecoNearYou,”TheGigaOMNetwork,2009,http://gigaom.com/2009/04/30/docsis‐30‐coming‐soon‐to‐an‐isp‐near‐you/.63CableLab’sDOCSISPrimerdescribesthefeaturesofthevariousiterationsoftheDOCSIS.See,http://www.cablelabs.com/cablemodem/primer/64AccordingtoCableLabs,“Channelbondingprovidescableoperatorswithaflexiblewaytosignificantlyincreasespeedstocustomers,withcompliantdevicessupportinguptoatleast160Mbpsinthedownstreamand120Mbpsintheupstream.”http://www.cablelabs.com/cablemodem/primer/65Ibid.66D.Williams,“TheShiftFromBroadbandToWideband,”ForresterResearchInc,2009,http://www.forrester.com/Research/Document/0,7211,53419,00.html.

28

certifycablemodemterminationsystems(CMTS)ascompliantwithDOCSIS3.0withoutupstreambonding.However,itiscertifyingdownstream‐onlysystemsatthistime.68

InadditiontothelargeMSOcablecompanies,manysmaller,usuallyrural,cablecompaniesaredeployingbroadband.TheAmericanCableAssociation(ACA),whichrepresentsover900small,independentcablecompanies,reportedthat803ofitsmembershavedeployed“someformofhigh‐speedinternetservice.”69TheACAdidnotreportontypesorspeedsofservicesornumbersofhomespassedorcustomerssubscribingtobroadband.A2009ACAsurveyfoundthatfouradditionalcompanieshadplanstodeployhigh‐speedInternetservicewithinayearand36companieshadnoplanstodeployhigh‐speedInternetservice.Duringatelephoneinterview,anexpertonthecableindustry’sbroadbandcoverageestimatedthatthesmallruraltelephonecompaniesarecapableofprovidingbroadbandserviceto75%ofthehomestheycollectivelypass.70

Wireless:Arangeofwirelessbroadbandtechnologiesiscurrentlyinusebythevariouscellulartelephonecompanies.Secondgeneration(2Gand2.5G)digitaltechnologywasthefirsttosupportInternetaccessandthatsecondgenerationisbeingrapidlysupplantedbythirdgeneration(3G)wirelessevenasdeploymentof4Ghasbegun.

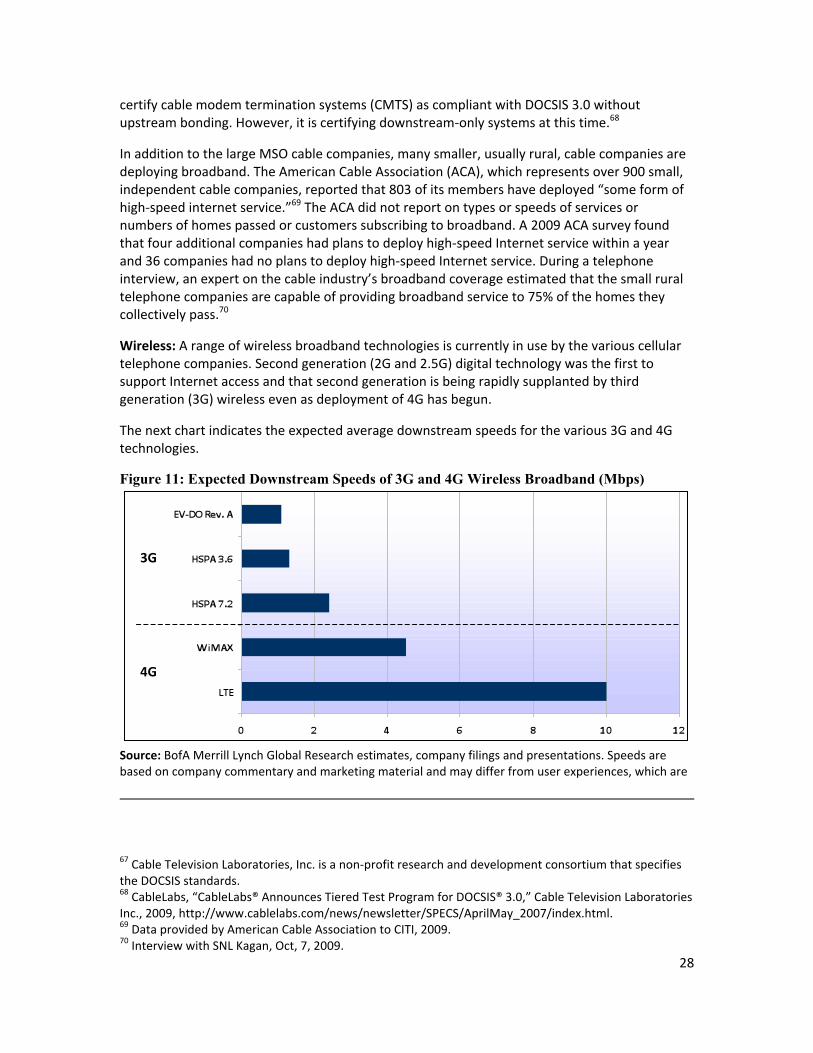

Thenextchartindicatestheexpectedaveragedownstreamspeedsforthevarious3Gand4Gtechnologies.

Figure 11: Expected Downstream Speeds of 3G and 4G Wireless Broadband (Mbps)

Source:BofAMerrillLynchGlobalResearchestimates,companyfilingsandpresentations.Speedsarebasedoncompanycommentaryandmarketingmaterialandmaydifferfromuserexperiences,whichare

67CableTelevisionLaboratories,Inc.isanon‐profitresearchanddevelopmentconsortiumthatspecifiestheDOCSISstandards.68CableLabs,“CableLabs®AnnouncesTieredTestProgramforDOCSIS®3.0,”CableTelevisionLaboratoriesInc.,2009,http://www.cablelabs.com/news/newsletter/SPECS/AprilMay_2007/index.html.69DataprovidedbyAmericanCableAssociationtoCITI,2009.70InterviewwithSNLKagan,Oct,7,2009.

3G

4G

29

impactedbynumberofusers,distancefromcellsite,andtopographyamongotherfactors.Theoreticalspeedsarehigher.AdaptedFrom:BankofAmericaMerrillLynch,4GFootrace–Carriersrefinedeploymentplans,Sept.30,2009at6.

Anumberoffourthgenerationwirelessbroadbandtechnologiesareinvariousstagesofdeployment,planningandtesting.MajorwirelesscompaniesthathavemadebroadbandannouncementsincludeAT&TWireless,Cablevision,CenturyLink(themergedCenturyTel/Embarq),CincinnatiBell,Clearwire,Comcast,CoxCommunications,FrontierCommunications,LightSquared,MetroPCS,Sprint,T‐MobileandVerizon.

Asexplainedinthesourcenoteforthegraphabove,wirelessbandwidthisshared,anduntilthenetworksaretestedundersubstantialloaditisnotclearwhetherspeedsabove5megabitscanbeobtainedconsistentlybymorethanafewsubscribersatthesametime.Asoneanalystobserved,“4Gwirelessnetworksofferamajorstep‐functioninwirelessbroadbandcapabilities–3Gtodaytypically0.5‐1.5mbps–WiMAXtoinitiallydeliver2‐4mbps–LTElikelytodeliver3‐6mbps”.71Othersaremoreoptimistic,suggestingthat4Gwirelesssystemswillprovidedownloadspeedsinthe4–12mbpsrange,aslongassystemsaren’toverloadedwithtoomanysubscribersusingbandwidth‐intensiveapplications.72

WiMAX4Giscurrentlybeingdeployed,includingbySprint,ClearwireandOpenRange.HundredsofsmallerWirelessInternetServiceProviders(WISPs)havedeployedwireless(mostlyWiMAX)Internetserviceinruralareasanditisexpectedthattheywillcontinuethedeployments.However,manyoftheseWISPcompaniesaresmallprivateventuresandtendtobesecretiveabouttheirdeploymentplans.73The350membersoftheWISPAssociation—farfromthetotalnumberofWISPs—providefixedbroadbandwirelessservicestoover2millionlocations.74

NotallWISPsaresmall,independent,localbusinesses.OpenRangeiseffectivelyanationalWISPfundedinpartbya$267millionBroadbandAccessLoanfromtheDepartmentofAgricultureand$100millionofprivateinvestment.ItplanstouseWiMAXtoinitiallyserve6millionpeople

71S.FlanneryandB.Swinburne,“U.S.Cable,Satellite,Telecom3Q09/’09/’10Outlook,”MorganStanleyResearch,2009at1772Verizonreportsarangeofdownloadspeedsfrom8‐12mbps,andClearwire’sWiMaxwillofferupto6mbps.See:K.Brown,“Verizon:LTEspeedwillbe8–12mbps,”OneTouchIntelligenceLLC,2009,http://www.onetrak.com/Uploads/scott/WIRELESSTRAK%20‐%20July%202009.pdf.Seealso,MorganStanley,TelecomServices,April19,2011,at7:“Verizonhasnotedthatitisseeing4G/LTEspeedsconsistentlyaround10Mbps…”73AnassociationofWISPshaspublishedamapanddirectorywhichindicateswheresomeWISPsarecurrentlyofferingservices.See:WISP,“WelcometoWISPDirectory,”wispdirectory.com,http://www.wispdirectory.com/index.php?option=com_mtree&task=viewlink&link_id=300&Itemid=53.74FilingofWISPAinFCCGNDocket09‐51,2009,at1‐2.

30

in546communitiesin17states75andisofferingitsfirstserviceswitha$38.95permonthbroadbandservice.76

LongTermEvolutionor“LTE”isthe4GtechnologyadoptedbyVerizonandAT&T,whichtogetherserve56.3%ofthemarket.77Verizoniscurrentlyontargettocover200millionPOPsbytheendof2011andprovidefullnationalcoverageby201378andAT&TreportedthatitisontrackwithupdatingtheirnetworktoLTE.OthercompaniesincludingCoxandMetroPCSarealsoplanningtouseLTEtechnologyfortheir4Gservices.

HSPA+isa3Gupgradewiththepotentialtodeliver“4Glikespeeds.”T‐MobileismarketingHSPA+asa4Gnetworkandplanedtocover100majormetropolitanareas‐‐185millionpeople‐‐withHSPA+byyear‐end2010.79AT&ThasalsobegundeployingHSPA+asa“steppingstone”fortheirfullupgradetoLTEin2011.80Thetechnologyhasbeenusedtohelpmaketheconversionfromoriginal3Gnetworksto4Gnetworksasmootherprocess.

Satellite‐BroadbandservicestoresidencesandsmallbusinessesviacommunicationssatellitesareofferedbyEchoStar,Gilat,Hughes,LightSquared,ViaSat,andWildBlue.81ThemostattractiveattributeofsatellitebroadbandisthatitisavailableinalmostanylocationintheUnitedStatesthathaselectricalpowerandaline‐of‐sighttothesouthernskywheresatellitesare“parked”ingeostationaryorbitsovertheequator.However,thelatencycausedbythetimerequiredsendingasignaltothesatellitesandbackmeansthatsatellitesarelesssatisfactorythanterrestrialbroadbandservicesforlatency‐sensitiveapplicationssuchasvoicetelephony,interactivegaming,andonlinevideoapplications.

Satellitebroadbandisalsomoreexpensivethanterrestrialbroadbandservices:inadditiontopayingamonthlysubscriptionchargethatcanbetwicethecostoftypicalterrestrialservices,theusermustalsopurchaseasatellite“dish”atpricesthatrangefrom$149.95to$299.99.

75OpenRangeCommunications,“OpenRangeCommunicationsSecures$374MilliontoDeployWirelessBroadbandServicesto546RuralCommunities,”OpenRangeCommunications,2009,http://www.openrangecomm.com/pr/pr_022009.html.76OpenRangeCommunications,“PerfectPackage–HighSpeedInternet,DigitalPhone,andE‐Mail,”OpenRangeCommunications,2009,http://www.openrangecomm.com/packages.html.77“ComScoreReportsMarch2010U.S.MobileSubscriberMarketShare”,May6,2010<http://comscore.com/Press_Events/Press_Releases/2010/5/comScore_Reports_March_2010_U.S._Mobile_Subscriber_Market_Share>78DeutscheBank,CTIAWireless2011:Day1MeetingsSummary,March23,2011at2.79Fiecewirless,June15,2020“T‐mobileexpandsHSPA+to25markets,willcallit‘4G’”<http://www.fiercewireless.com/story/t‐mobile‐expands‐hspa‐25‐markets‐will‐call‐it‐4g/2010‐06‐15>80Ibid.81WildBluehasbeenacquiredbyViaSat.

31

Anewgenerationoftwo‐wayHighThroughput(HT)satellitesisbeingbuiltforlaunchbeginninginearly2012.Thesenewspotbeamsatelliteswillhave100gbpsofcapacity,whichis18‐25timesthecapacityofsatellitesthatwerelaunchedafewyearsago.82

Backbone:Anessentialcomponentofbroadbandservices,whetherwiredorwireless,aretheso‐calledbackbonenetworksthatareeffectivelythecore“superhighways”oftheInternet.Backbonesaretypicallymultipleopticalfibersbundledintocableswiththecapacityofeachfibermeasuredbyopticalcarrieror“OC”.AnOC‐3lineiscapableoftransmitting155mbpswhileanOC‐48cantransmit2.48gbps.StateofthearttechnologytodayisOC‐768or40gbpsperfiberwith100gpbsonthevergeofgeneraldeployment.

MajorbackbonecapacityprovidersintheU.S.includeAT&T,Cogent,GlobalCrossing,Level3,Sprint,andVerizon.83XOHoldings,ZayoGroup,andTWtelecomshouldalsobeconsideredaslargecontributorsofbackbonecapacity.

CiscoSystems84andTeleGeography85estimatethattheU.S.Internetbackbonewillgrowatabout40%peryear.TheUniversityofMinnesota’sMINTSestimatesahighergrowthrateof50%‐60%.86Inadditiontogrowingvolumesfromwirelinebroadbandcustomers,wirelesstrafficisalsogrowingrapidlyandisexpectedtodramaticallyincreasewhen4Gnetworksaredeployed.

Asthefollowingchartillustrates,backboneconnectionswithhugecapacitiesareneededbetweenmajorcitieswherethepopulationdensityishighandbusinessactivityisstrong.

82F.Valle,“SatelliteBroadbandRevolution:HowTheLatestKa‐BandSystemsWillChangeTheRulesOfTheIndustry.AnInterpretationoftheTechnologicalTrajectory,”SpringerScience+BusinessMedia,2009,http://www.springerlink.com/content/x0x51281h3520202/fulltext.pdf.

83TeleGeographyResearch,“GlobalInternetGeographyUnitedStates,“PriMetricaInc.,2009,http://www.telegeography.com/ee/dm/gig2010/42148.php.84CiscoSystems,“CiscoVisualNetworkingIndex:ForecastandMethodology2008‐2013,”CiscoSystemsInc,2009,http://www.cisco.com/en/US/solutions/collateral/ns341/ns525/ns537/ns705/ns827/white_paper_c11‐481360_ns827_Networking_Solutions_White_Paper.html.85TeleGeographyResearch,“GlobalInternetGeographyUnitedStates,“PriMetricaInc.,2009,http://www.telegeography.com/ee/dm/gig2010/42148.php.86AndrewOdlyzko,“MinnesotaInternetTrafficStudies(MINTS),”UniversityofMinnesota,2007,http://www.dtc.umn.edu/mints/home.php.

32

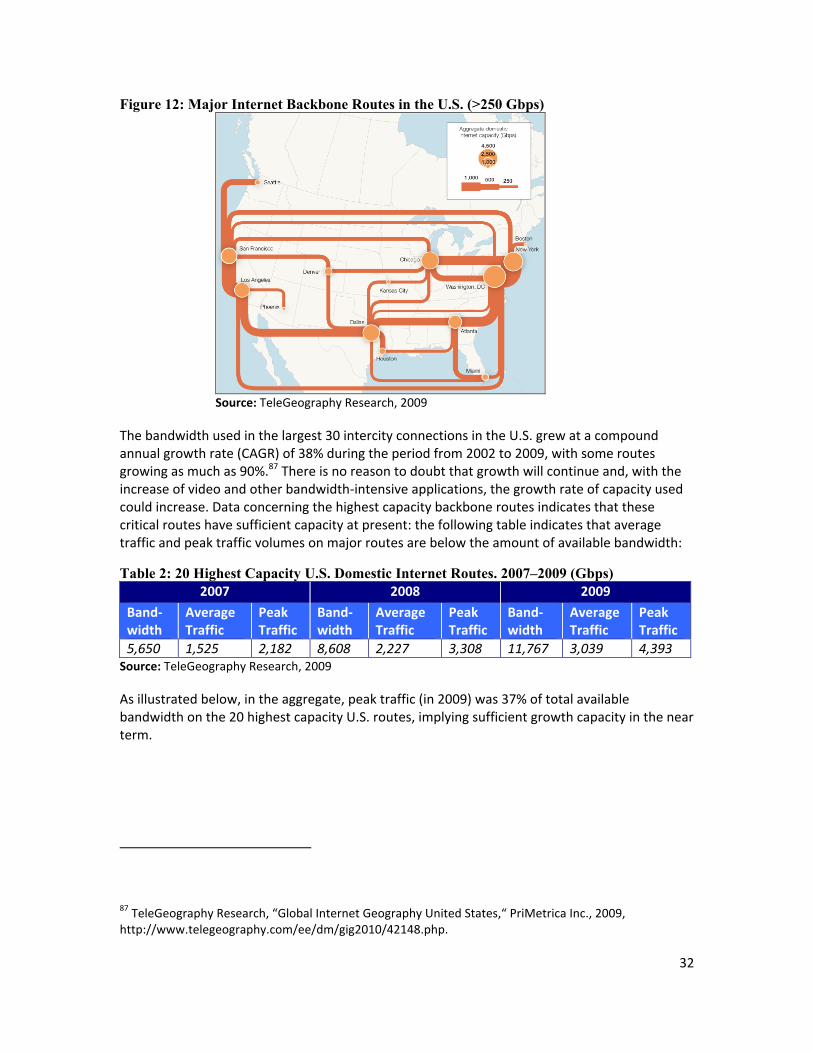

Figure 12: Major Internet Backbone Routes in the U.S. (>250 Gbps)

Source:TeleGeographyResearch,2009

Thebandwidthusedinthelargest30intercityconnectionsintheU.S.grewatacompoundannualgrowthrate(CAGR)of38%duringtheperiodfrom2002to2009,withsomeroutesgrowingasmuchas90%.87Thereisnoreasontodoubtthatgrowthwillcontinueand,withtheincreaseofvideoandotherbandwidth‐intensiveapplications,thegrowthrateofcapacityusedcouldincrease.Dataconcerningthehighestcapacitybackboneroutesindicatesthatthesecriticalrouteshavesufficientcapacityatpresent:thefollowingtableindicatesthataveragetrafficandpeaktrafficvolumesonmajorroutesarebelowtheamountofavailablebandwidth:

Table 2: 20 Highest Capacity U.S. Domestic Internet Routes. 2007–2009 (Gbps) 2007 2008 2009

Band‐width

AverageTraffic

PeakTraffic

Band‐width

AverageTraffic

PeakTraffic

Band‐width

AverageTraffic

PeakTraffic

5,650 1,525 2,182 8,608 2,227 3,308 11,767 3,039 4,393Source:TeleGeographyResearch,2009

Asillustratedbelow,intheaggregate,peaktraffic(in2009)was37%oftotalavailablebandwidthonthe20highestcapacityU.S.routes,implyingsufficientgrowthcapacityinthenearterm.

87TeleGeographyResearch,“GlobalInternetGeographyUnitedStates,“PriMetricaInc.,2009,http://www.telegeography.com/ee/dm/gig2010/42148.php.

33

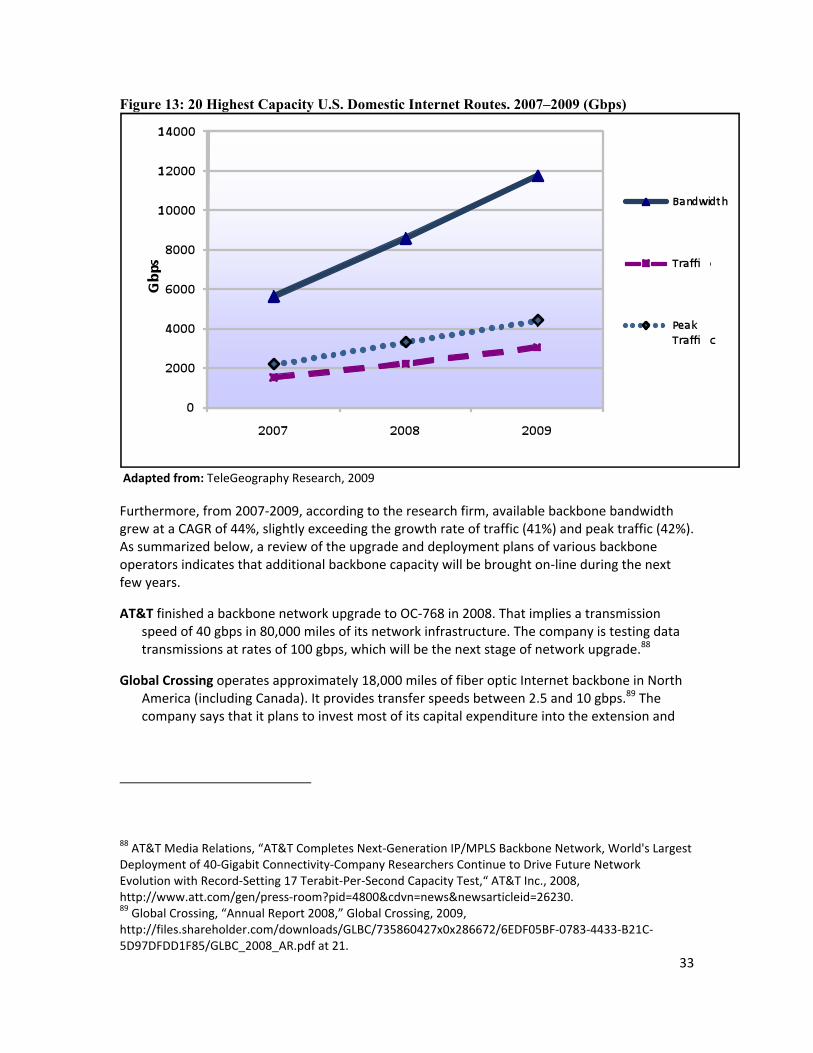

Figure 13: 20 Highest Capacity U.S. Domestic Internet Routes. 2007–2009 (Gbps)

Adaptedfrom:TeleGeographyResearch,2009

Furthermore,from2007‐2009,accordingtotheresearchfirm,availablebackbonebandwidthgrewataCAGRof44%,slightlyexceedingthegrowthrateoftraffic(41%)andpeaktraffic(42%).Assummarizedbelow,areviewoftheupgradeanddeploymentplansofvariousbackboneoperatorsindicatesthatadditionalbackbonecapacitywillbebroughton‐lineduringthenextfewyears.

AT&TfinishedabackbonenetworkupgradetoOC‐768in2008.Thatimpliesatransmissionspeedof40gbpsin80,000milesofitsnetworkinfrastructure.Thecompanyistestingdatatransmissionsatratesof100gbps,whichwillbethenextstageofnetworkupgrade.88

GlobalCrossingoperatesapproximately18,000milesoffiberopticInternetbackboneinNorthAmerica(includingCanada).Itprovidestransferspeedsbetween2.5and10gbps.89Thecompanysaysthatitplanstoinvestmostofitscapitalexpenditureintotheextensionand

88AT&TMediaRelations,“AT&TCompletesNext‐GenerationIP/MPLSBackboneNetwork,World'sLargestDeploymentof40‐GigabitConnectivity‐CompanyResearchersContinuetoDriveFutureNetworkEvolutionwithRecord‐Setting17Terabit‐Per‐SecondCapacityTest,“AT&TInc.,2008,http://www.att.com/gen/press‐room?pid=4800&cdvn=news&newsarticleid=26230.89GlobalCrossing,“AnnualReport2008,”GlobalCrossing,2009,http://files.shareholder.com/downloads/GLBC/735860427x0x286672/6EDF05BF‐0783‐4433‐B21C‐5D97DFDD1F85/GLBC_2008_AR.pdfat21.

34

upgradeofitsexistingnetwork.90Thecapitalexpendituresin2008weremainlydrivenbyacquisitionsofothercompanies($192million).91

Level3invested$155millionintonetworkupgradesinthefirsthalfof2009.92Thecompanyplanstofocusitscapitalexpenditureonnewequipmentinthefuture.RecentupgradesanddeploymentsweremadeinNewYork,Seattle,andTennessee.93Thecompanyoperates27,000routemilesofcablewithitsnewestdeploymentsoperatingat40gbps.94

QwestisoneofthelargestbackboneoperatorsaswellasoneofthelargestregionaltelephonecompaniesprovidingtelephoneserviceinmuchoftheWestotherthanCalifornia.ItsbackbonereachesacrosstheU.S.andisavailableinalmosteverystate.Currentlyitsbackboneoperatesattransmissionratesof40gbpsbutthespeedwillbeupgradedto100gbpsduring2009and2010.95

Verizoncurrentlyoperatesitsbackboneat40gbpsandisplanningtoupgradeto100gbpsbeginningin2009.96

XOiscurrentlyoperatingabackbonenetworkof18,000milesoperatingat10gbps.97Itiscurrentlyundertakingmanyenhancementprojectsincludingadeploymentof1.6terabits‐capablesystemsonselectedinter‐cityroutes.98Recentinvestmentinnetworkupgradesandnewdeploymentstotaled$450million.99

Fromthebackbonedevelopmentsdescribedabove,itwouldbereasonabletoconcludethattheinternetbackboneintheU.S.isexpandingatapacethatshouldkeepupwithexpecteddemandoverthenextfewyears,providedthatthereisnohugeandunexpectedincreaseinusage

90GlobalCrossing,“AnnualReport2008,”GlobalCrossing,2009,http://files.shareholder.com/downloads/GLBC/735860427x0x286672/6EDF05BF‐0783‐4433‐B21C‐5D97DFDD1F85/GLBC_2008_AR.pdfat.24.91Ibid.92Level3CommunicationsPublicRelations,“QuarterlyReport,”Level3CommunicationsLLC.,2009,http://files.shareholder.com/downloads/LVLT/740502237x0xS1104659‐09‐48275/794323/filing.pdfat26.93Level3CommunicationsPublicRelations,“Level3ExpandsOperationsinUpstateNewYork,”Level3CommunicationsLLC.,2009,http://www.level3.com/index.cfm?pageID=491&PR=772.94Level3CommunicationsPublicRelations,“OurNetwork,”Level3CommunicationsLLC.,2009,http://www.level3.com/index.cfm?pageID=242.95C.A.Tyler,“QwestPositionsitsNationalNetworkforFastest‐AvailableEthernetTechnology,”QwestCommunicationsInternationalInc.,2009,http://news.qwest.com/QwestNetworkEnhancements.96VerizonInvestorRelations,“GlobalNetwork,”VerizonCommunicationsInc.,2009,http://www.verizonbusiness.com/about/network.97XOCommunications,“NetworkDetails,”XOCommunications,2009http://www.xo.com/about/network/Pages/details.aspx.98XOCommunications,“AnnualReport(2008),”XOCommunications,2009,http://www.xo.com/SiteCollectionDocuments/about‐xo/investor‐relations/Annual_Reports/XO_2008_10K.pdfat3.99XOCommunications,“AboutXOOverview,”XOCommunications,2009http://www.xo.com/about/Pages/overview.aspx.

35

patterns.With78%ofbackbonetrafficconsistingofpeer‐to‐peerconnectionsandvideostreaming,100increasingvideotrafficshouldnotbeanunanticipateddevelopment.

Wirelesstrafficisalsolikelytoplaceincreaseddemandonthebackbones.Forexample,AT&Thasreportedexplosivegrowth(nearly5,000%inthepast3years)initswirelessdatatraffic,presumablyduetotheiPhone,101andwirelesscarriershaveaskedforbidstoprovidefiberopticconnectionsto7,500of17,000cellsitesinQwest’soperatingarea.102Ontheotherhand,wirelesstrafficwillbeatleastpartlyasubstituteforwiredtrafficratherthanbeingcompletelyadditive.

Asupgradingbackbonefacilitiesrequires6‐18months,103thebackboneprovidersshouldbeabletoreactreasonablyquicklytoaccommodateunexpecteddemand.

Towers:Adiscussionof“towers”wasnotincludedintheoriginalFirstReportbut,becausetowersareanessentialpartofthetelecommunicationsinfrastructure,thatoversightisbeingcorrectedinthisSecondReport.

TowercompaniesprovideessentialelementsofinfrastructureneededtodeliverwirelessbroadbandsignalsthroughouttheUnitedStates:towersanddistributedantennasystems(DAS).Towersarethelargestructures(includingroof‐tops)uponwhichwirelessserviceprovidersinstalltheirtransmitter/receiverequipment.DASarecollectionsofsmallantennasspreadoveralimitedgeographicareaandareconnected,usuallybyfiber,toacentrallocation,usuallyabasestation”104

Accordingtoananalyst,“[DAS]isusedtofillingapswherethebigcellsmaynotreach,butgoingforwarditwillprobablyreplacealotofbigcellsinalotofsituationswheretheyneedhighcapacity.”105Therefore,althoughdistributedantennasystemshaveusuallybeenusedtosolvespecificcoverageproblems,DASarebecomingmorecentralto4Gnetworkdeploymentplans.

TowercompaniessuchasAmericanTower,CrownCastleInternational,andSBACommunicationCo.haveestablishedbothtowerandDASinfrastructurelinesofbusiness.However,thereare

100SeethefirstchartinthisSection3.Seealso,G.Kim,“WirelessisKeyforBroadbandAccessDemandandSupply,”TechnologyMarketingCorporation,2009,http://4g‐wirelessevolution.tmcnet.com/wimax/topics/wimax/articles/55281‐wireless‐key‐broadband‐access‐demand‐supply.htm.101MorganStanleyResearch,“Economy+InternetTrends,”MorganStanley,2009,http://www.morganstanley.com/institutional/techresearch/pdfs/MS_Economy_Internet_Trends_102009_FINAL.pdfat57.102S.Carew,“Rpt‐Update2‐Interview:Qwest2010capexflat,fiberasbiggerpa,”Reuters,2009,http://www.reuters.com/article/technology‐media‐telco‐SP/idUSN2046085120091021?pageNumber=2&virtualBrandChannel=11604.103K.Papagiannaki,N.Taftetal.,“Long‐TermForecastingofInternetBackboneTraffic,”IEEETransactionsonneuralnetworks,2005,http://ieeexplore.ieee.org/stamp/stamp.jsp?arnumber=01510713.104“Distributedantennasystems:Fromnichetonecessity”March4th2010,FierceWirelesshttp://www.fiercewireless.com/story/distributed‐antenna‐systems‐niche‐necessity/2010‐03‐04#ixzz0vm5VUXSL105IbidAllenNogee,analystatIn‐Stat

36

alsocompanieswhoconstructonlyDASsystemssuchasExteNetSystemsInc.,NextGNetworksandNewPathNetworks.106

1.2TimelineforBroadbandPlans

Forcompetitivereasonsandtoavoidcomplicationswithsecuritieslawsdealingwithdisclosuresofmaterialinformation,mostbroadbandservicecompaniesarereticentaboutreleasingdetailsofthetimingoftheirfuturebroadbanddeploymentplans.Whereinvestmentanalystshavemadeforecastsforthemajorcompanies’deploymentplans(sincethisisamatterofgreatinteresttoinvestors),thecompaniesthemselveshavenotverifiedtheanalysts’forecasts.Totheextentcompaniesdomakeannouncements,theplanstypicallydonotextendpast2012,andmostlyonlycoverthenextyear.

Knowndetailsofpublicplans,timelines,andexpectedcoveragearesummarizedinthefollowingdiscussionon“ExpectedDeployment,”whichhasbeenupdatedfor2010inSection2ofthisReport.TheAppendixandthediscussionofanalystprojectionsinSection3ofthisReportalsoprovideinsightsintodeploymenttimelines.

1.3PenetrationandCoverageFootprint

Investmentanalystsandotherresearchfirmsestimatecurrent(year‐end2010)wirelinebroadbandpenetrationatapproximately70%ofallU.S.households,with31%bytelephonecompaniesand39%bycablecompanies.107Asthefollowingchartillustrates,anestimated19%ofU.S.householdsdonotaccesstheInternetatalland12%accesstheInternetwithdial‐uptelephoneservice.(ItisworthnotingthatsomeofthehouseholdsthatarenotaccessingtheInternetdonothavetheessentialprerequisiteforusingtheInternet:apersonalcomputer.Accordingtoanalysts,“PenetrationofconsumerInternetaccessintotal(includingdial‐up)isestimatedat~87%ofPCHouseholds”108).

106Ford,Tracy,“DASNetworksgaintractionamongcarriers,”RCRWirelessNews,October2009,http://www.rcrwireless.com/ARTICLE/20091028/WIRELESS_NETWORKS/910289999/das‐networks‐gain‐traction‐among‐carriers107LeichtmanResearchGroup,“Under650,000addbroadbandinthesecondquarterof2009,”LeichtmanResearchGroupInc,2009,at2,http://www.leichtmanresearch.com/press/081709release.pdf.Leichtmanestimates69,902,289totalbroadbandsubscribersatendof2Q2009,whichisroughly60%ofU.S.households.

108BofAMerrillLynchGlobalResearch,TelecomServices/Cable,May24,2010

37

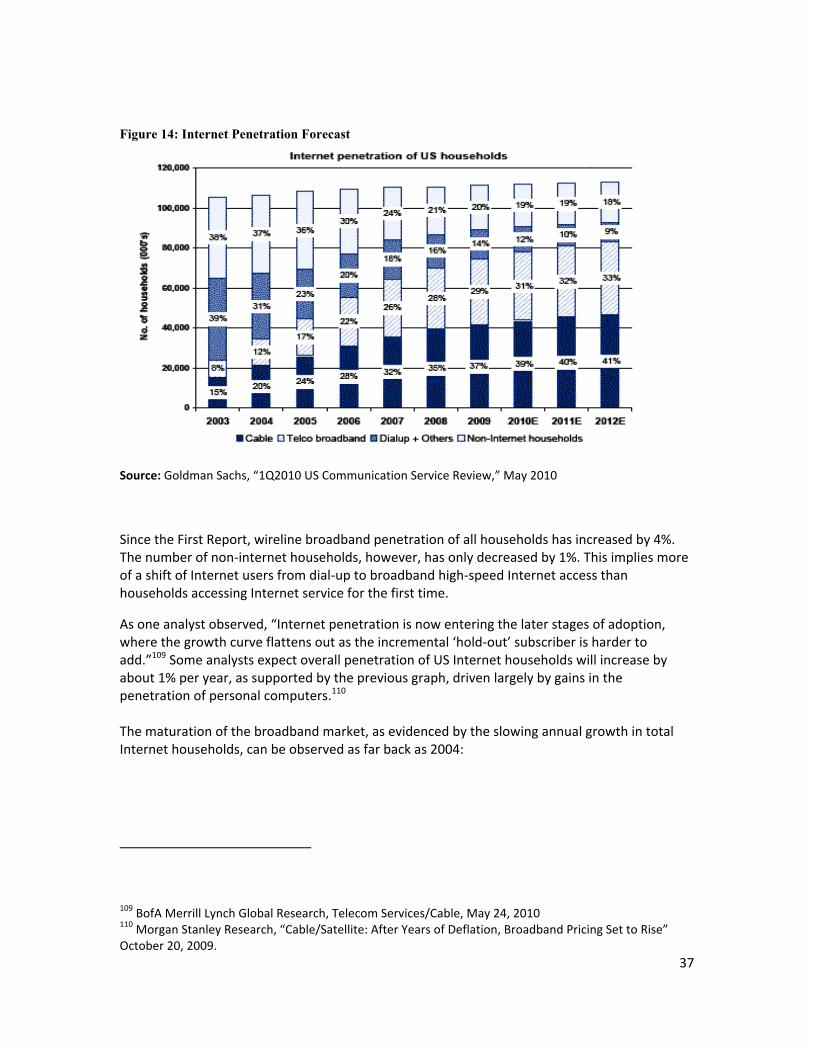

Figure 14: Internet Penetration Forecast

Source:GoldmanSachs,“1Q2010USCommunicationServiceReview,”May2010

SincetheFirstReport,wirelinebroadbandpenetrationofallhouseholdshasincreasedby4%.Thenumberofnon‐internethouseholds,however,hasonlydecreasedby1%.ThisimpliesmoreofashiftofInternetusersfromdial‐uptobroadbandhigh‐speedInternetaccessthanhouseholdsaccessingInternetserviceforthefirsttime.

Asoneanalystobserved,“Internetpenetrationisnowenteringthelaterstagesofadoption,wherethegrowthcurveflattensoutastheincremental‘hold‐out’subscriberishardertoadd.”109SomeanalystsexpectoverallpenetrationofUSInternethouseholdswillincreasebyabout1%peryear,assupportedbythepreviousgraph,drivenlargelybygainsinthepenetrationofpersonalcomputers.110Thematurationofthebroadbandmarket,asevidencedbytheslowingannualgrowthintotalInternethouseholds,canbeobservedasfarbackas2004:

109BofAMerrillLynchGlobalResearch,TelecomServices/Cable,May24,2010110MorganStanleyResearch,“Cable/Satellite:AfterYearsofDeflation,BroadbandPricingSettoRise”October20,2009.

38

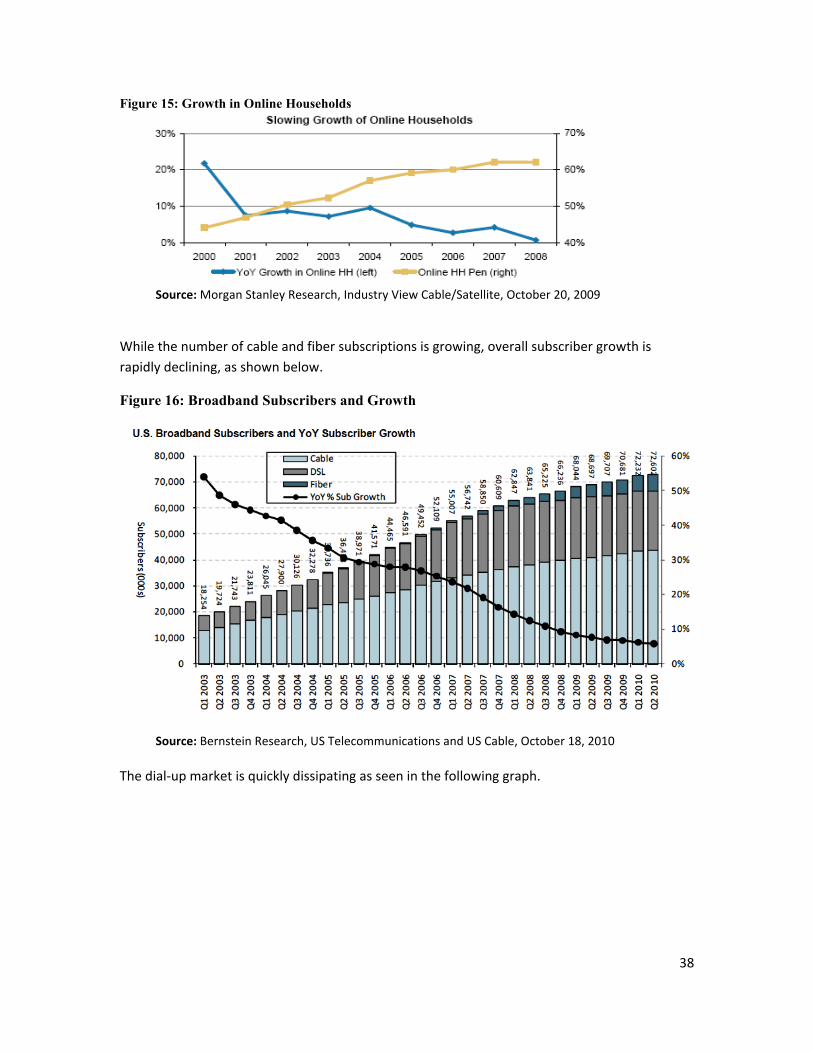

Figure 15: Growth in Online Households

Source:MorganStanleyResearch,IndustryViewCable/Satellite,October20,2009

Whilethenumberofcableandfibersubscriptionsisgrowing,overallsubscribergrowthisrapidlydeclining,asshownbelow.

Figure 16: Broadband Subscribers and Growth

Source:BernsteinResearch,USTelecommunicationsandUSCable,October18,2010Thedial‐upmarketisquicklydissipatingasseeninthefollowinggraph.

39

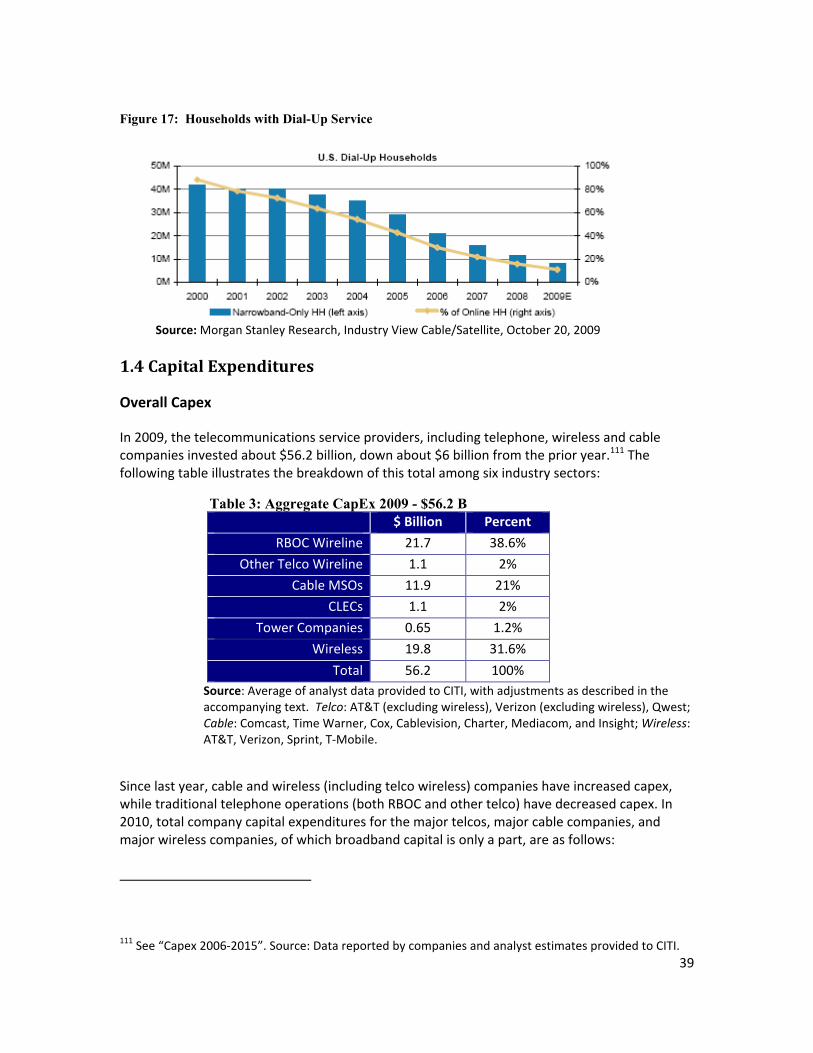

Figure 17: Households with Dial-Up Service

Source:MorganStanleyResearch,IndustryViewCable/Satellite,October20,2009

1.4CapitalExpenditures

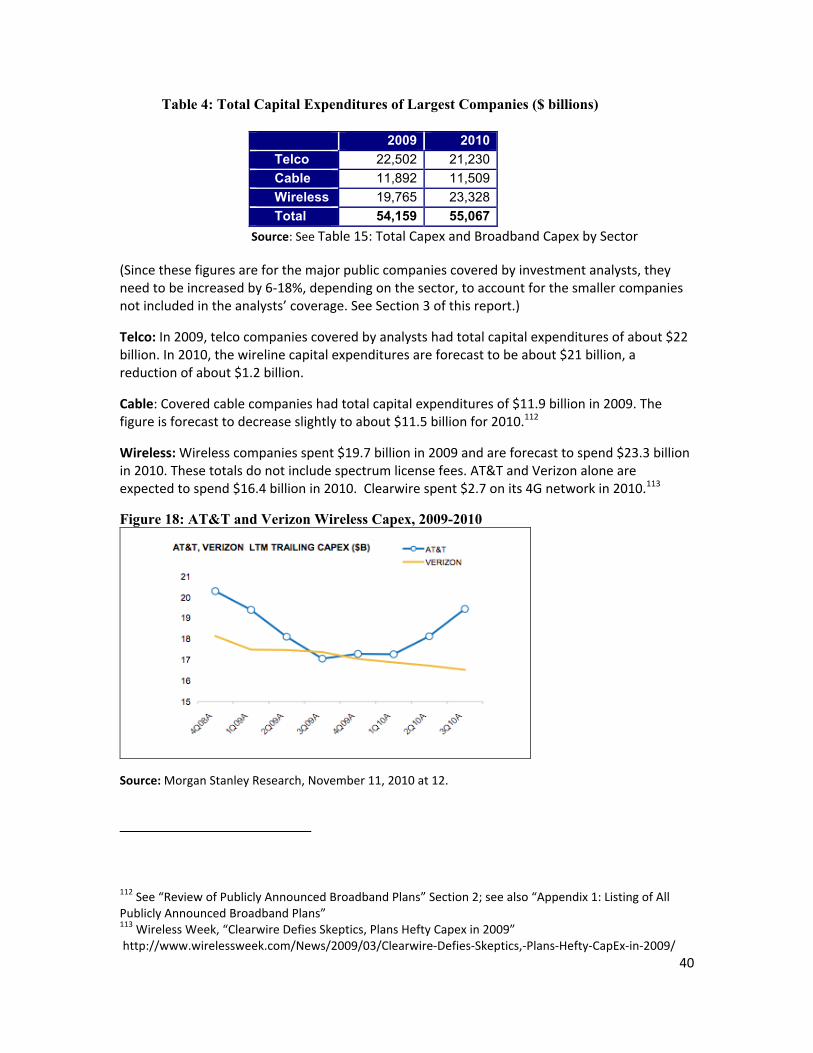

OverallCapex

In2009,thetelecommunicationsserviceproviders,includingtelephone,wirelessandcablecompaniesinvestedabout$56.2billion,downabout$6billionfromtheprioryear.111Thefollowingtableillustratesthebreakdownofthistotalamongsixindustrysectors:

Table 3: Aggregate CapEx 2009 - $56.2 B $Billion Percent

RBOCWireline 21.7 38.6%

OtherTelcoWireline 1.1 2%

CableMSOs 11.9 21%

CLECs 1.1 2%

TowerCompanies 0.65 1.2%

Wireless 19.8 31.6%

Total 56.2 100%Source:AverageofanalystdataprovidedtoCITI,withadjustmentsasdescribedintheaccompanyingtext.Telco:AT&T(excludingwireless),Verizon(excludingwireless),Qwest;Cable:Comcast,TimeWarner,Cox,Cablevision,Charter,Mediacom,andInsight;Wireless:AT&T,Verizon,Sprint,T‐Mobile.

Sincelastyear,cableandwireless(includingtelcowireless)companieshaveincreasedcapex,whiletraditionaltelephoneoperations(bothRBOCandothertelco)havedecreasedcapex.In2010,totalcompanycapitalexpendituresforthemajortelcos,majorcablecompanies,andmajorwirelesscompanies,ofwhichbroadbandcapitalisonlyapart,areasfollows:

111See“Capex2006‐2015”.Source:DatareportedbycompaniesandanalystestimatesprovidedtoCITI.

40

Table 4: Total Capital Expenditures of Largest Companies ($ billions)

Source:SeeTable15:TotalCapexandBroadbandCapexbySector

(Sincethesefiguresareforthemajorpubliccompaniescoveredbyinvestmentanalysts,theyneedtobeincreasedby6‐18%,dependingonthesector,toaccountforthesmallercompaniesnotincludedintheanalysts’coverage.SeeSection3ofthisreport.)

Telco:In2009,telcocompaniescoveredbyanalystshadtotalcapitalexpendituresofabout$22billion.In2010,thewirelinecapitalexpendituresareforecasttobeabout$21billion,areductionofabout$1.2billion.

Cable:Coveredcablecompanieshadtotalcapitalexpendituresof$11.9billionin2009.Thefigureisforecasttodecreaseslightlytoabout$11.5billionfor2010.112

Wireless:Wirelesscompaniesspent$19.7billionin2009andareforecasttospend$23.3billionin2010.Thesetotalsdonotincludespectrumlicensefees.AT&TandVerizonaloneareexpectedtospend$16.4billionin2010.Clearwirespent$2.7onits4Gnetworkin2010.113

Figure 18: AT&T and Verizon Wireless Capex, 2009-2010

Source:MorganStanleyResearch,November11,2010at12.

112See“ReviewofPubliclyAnnouncedBroadbandPlans”Section2;seealso“Appendix1:ListingofAllPubliclyAnnouncedBroadbandPlans”113WirelessWeek,“ClearwireDefiesSkeptics,PlansHeftyCapexin2009”http://www.wirelessweek.com/News/2009/03/Clearwire‐Defies‐Skeptics,‐Plans‐Hefty‐CapEx‐in‐2009/

2009 2010 Telco 22,502 21,230 Cable 11,892 11,509 Wireless 19,765 23,328 Total 54,159 55,067

41

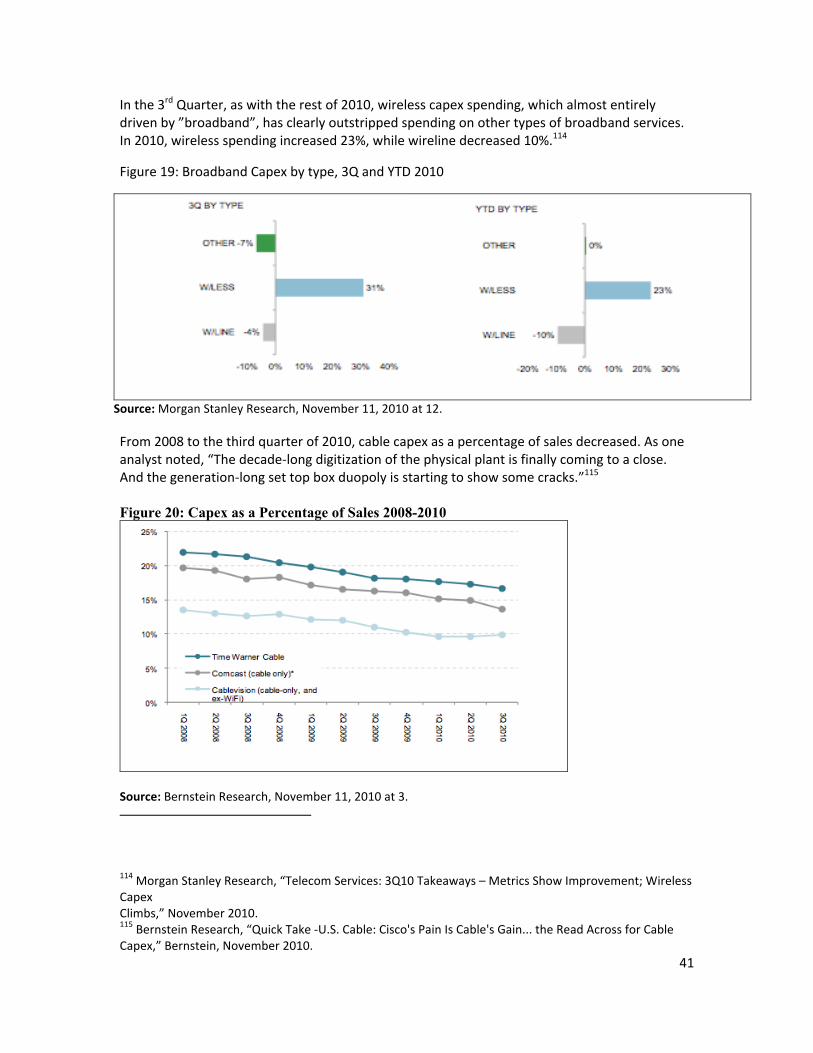

Inthe3rdQuarter,aswiththerestof2010,wirelesscapexspending,whichalmostentirelydrivenby”broadband”,hasclearlyoutstrippedspendingonothertypesofbroadbandservices.In2010,wirelessspendingincreased23%,whilewirelinedecreased10%.114

Figure19:BroadbandCapexbytype,3QandYTD2010

Source:MorganStanleyResearch,November11,2010at12.

From2008tothethirdquarterof2010,cablecapexasapercentageofsalesdecreased.Asoneanalystnoted,“Thedecade‐longdigitizationofthephysicalplantisfinallycomingtoaclose.Andthegeneration‐longsettopboxduopolyisstartingtoshowsomecracks.”115Figure 20: Capex as a Percentage of Sales 2008-2010

Source:BernsteinResearch,November11,2010at3.

114MorganStanleyResearch,“TelecomServices:3Q10Takeaways–MetricsShowImprovement;WirelessCapexClimbs,”November2010.115BernsteinResearch,“QuickTake‐U.S.Cable:Cisco'sPainIsCable'sGain...theReadAcrossforCableCapex,”Bernstein,November2010.

42

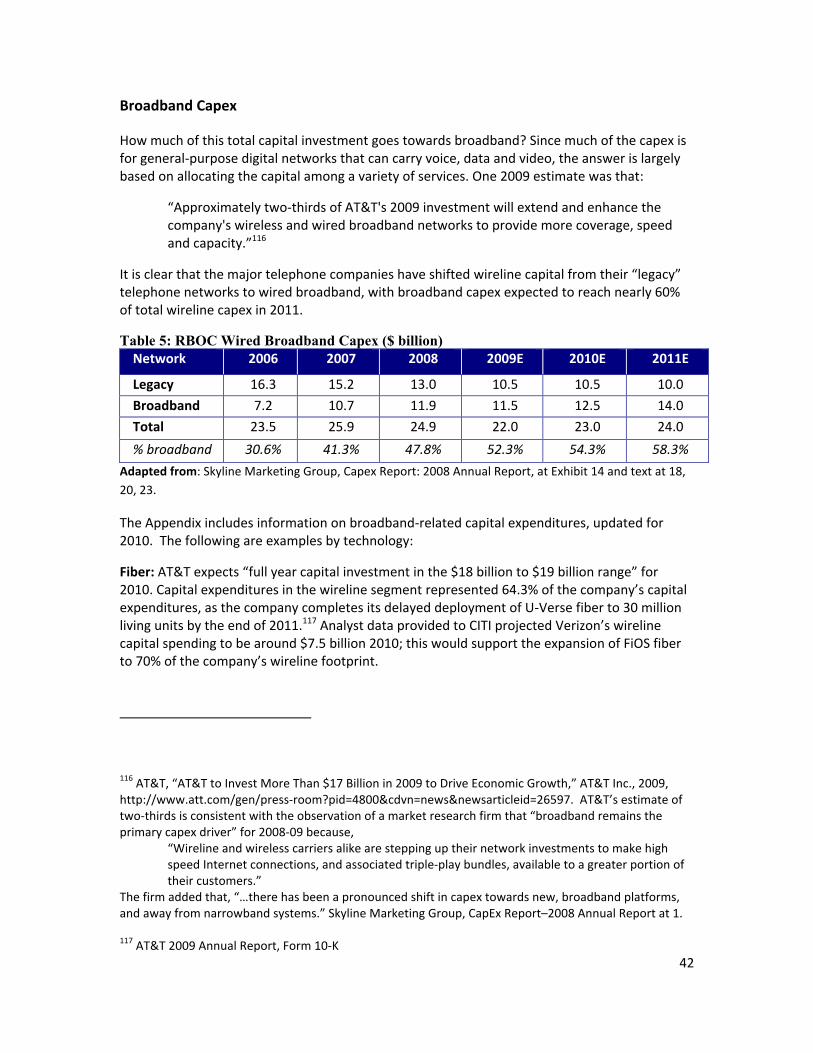

BroadbandCapex

Howmuchofthistotalcapitalinvestmentgoestowardsbroadband?Sincemuchofthecapexisforgeneral‐purposedigitalnetworksthatcancarryvoice,dataandvideo,theanswerislargelybasedonallocatingthecapitalamongavarietyofservices.One2009estimatewasthat:

“Approximatelytwo‐thirdsofAT&T's2009investmentwillextendandenhancethecompany'swirelessandwiredbroadbandnetworkstoprovidemorecoverage,speedandcapacity.”116

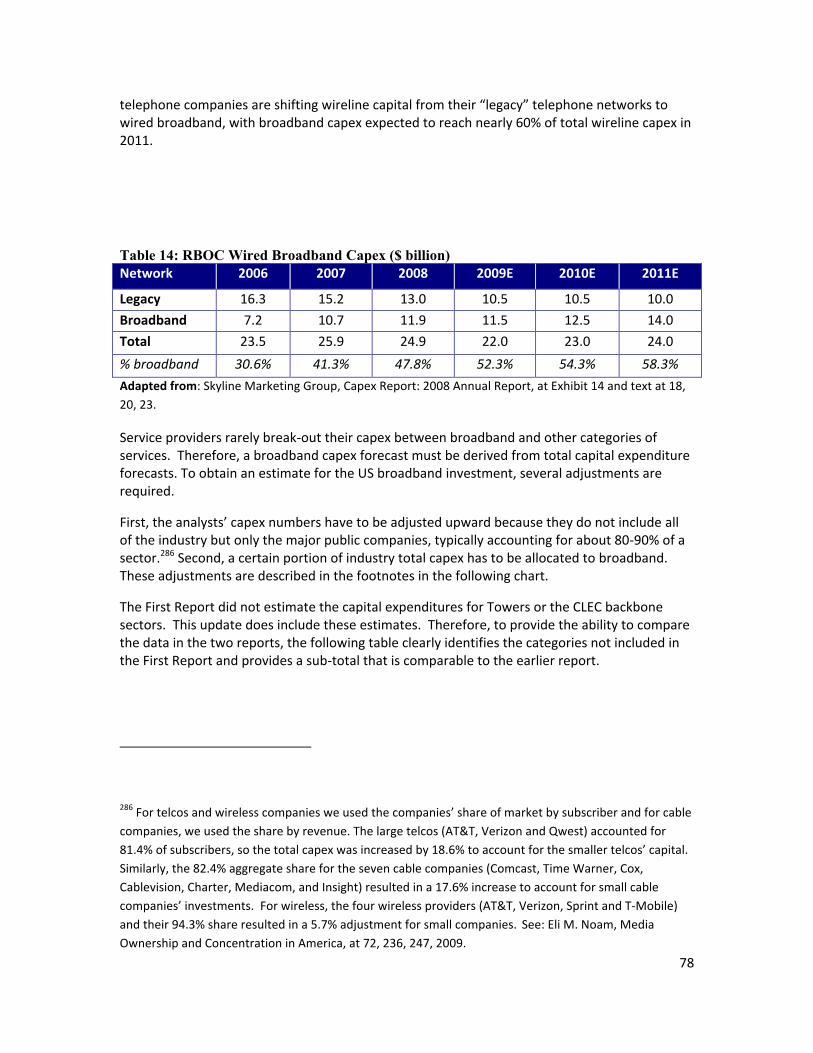

Itisclearthatthemajortelephonecompanieshaveshiftedwirelinecapitalfromtheir“legacy”telephonenetworkstowiredbroadband,withbroadbandcapexexpectedtoreachnearly60%oftotalwirelinecapexin2011.

Table 5: RBOC Wired Broadband Capex ($ billion) Network 2006 2007 2008 2009E 2010E 2011E

Legacy 16.3 15.2 13.0 10.5 10.5 10.0

Broadband 7.2 10.7 11.9 11.5 12.5 14.0

Total 23.5 25.9 24.9 22.0 23.0 24.0

%broadband 30.6% 41.3% 47.8% 52.3% 54.3% 58.3%

Adaptedfrom:SkylineMarketingGroup,CapexReport:2008AnnualReport,atExhibit14andtextat18,20,23.

TheAppendixincludesinformationonbroadband‐relatedcapitalexpenditures,updatedfor2010.Thefollowingareexamplesbytechnology:

Fiber:AT&Texpects“fullyearcapitalinvestmentinthe$18billionto$19billionrange”for2010.Capitalexpendituresinthewirelinesegmentrepresented64.3%ofthecompany’scapitalexpenditures,asthecompanycompletesitsdelayeddeploymentofU‐Versefiberto30millionlivingunitsbytheendof2011.117AnalystdataprovidedtoCITIprojectedVerizon’swirelinecapitalspendingtobearound$7.5billion2010;thiswouldsupporttheexpansionofFiOSfiberto70%ofthecompany’swirelinefootprint.

116AT&T,“AT&TtoInvestMoreThan$17Billionin2009toDriveEconomicGrowth,”AT&TInc.,2009,http://www.att.com/gen/press‐room?pid=4800&cdvn=news&newsarticleid=26597.AT&T’sestimateoftwo‐thirdsisconsistentwiththeobservationofamarketresearchfirmthat“broadbandremainstheprimarycapexdriver”for2008‐09because,

“WirelineandwirelesscarriersalikearesteppinguptheirnetworkinvestmentstomakehighspeedInternetconnections,andassociatedtriple‐playbundles,availabletoagreaterportionoftheircustomers.”

Thefirmaddedthat,“…therehasbeenapronouncedshiftincapextowardsnew,broadbandplatforms,andawayfromnarrowbandsystems.”SkylineMarketingGroup,CapExReport–2008AnnualReportat1.117AT&T2009AnnualReport,Form10‐K

43

Cable:Comcast’s2010totalcapitalexpenditureswerelowerin“bothabsolutedollarsandasapercentageofrevenue”comparedwith2009’s$5.1billionexpenditures.118TimeWarnerCable’stotalcapitalexpendituresfor2009were$3.2billion,supportingthecompany’sexpansionofDOCSIS3.0cable.119

Wireless:Verizonspent$8billionin2010toexpandandmaintainitswirelessnetwork.120Clearwire,initseffortstocover120millionPOPsbytheendof2010,expectstospendbetween$2.8billionand$3.2billion“intotalcash”.121Two‐thirdsofAT&T’saforementioned“$18to$19billion”ofcapitalspendingwillgotobroadbandandwireless,withanalystsestimatingatotalof7.7to8billioninwirelesscapexforthefullyear.122

Satellite:SatellitecommunicationcompaniessuchasViaSatInc.(ViaSat‐1)andHughesCommunications,Inc.(Jupiter)areplanningtolaunchnewsatellitesin2011(ViaSat‐1)and2012(Jupiter),respectively.Satelliteconstruction,launchandinsurancecancostupwardsof$400millionpersatellite.123

Tower:AmericanTowerexpectstospend$515to$605milliononcapitalexpendituresin2010.124SBACommunicationsexpectstoincurdiscretionarycashcapitalexpendituresof$190millionto$210million.125

1.5ExpectedBroadbandPerformance/Quality

Mostbroadbandserviceprovidersdescribetheirbroadbandperformanceintermsofupstreamanddownstreamspeed.Speedclaims,however,aredifficulttoverifyandcompanieshavedifferentnumbersintermsofadvertised,actual,throughput,andaveragespeeds.Generally,aconsumer’s“actualspeed”islikelytovary,particularlyoncableandwirelesssystemswherecapacityisshared,andinmostcasesissubstantiallylessthantheadvertised“upto”speed.Theadvertisedandtheoreticalspeedcapabilitiesofthevarioustechnologieshavebeenbroadlydescribedinthepreviousdiscussionofeachtechnology.CompletecompanyspeedinformationmaybefoundintheAppendix.

118ComcastQ22010EarningsCallTranscript,http://seekingalpha.com/article/217044‐comcast‐corporation‐q2‐2010‐earnings‐call‐transcript?source=thestreet119http://www.timewarnercable.com/MediaLibrary/1/1/about/pressrelease/twc_4Q09_earnings_announcement.pdf120GoldmanSachs.“TheQuarterinpictures,1Q2010USCommunicationServicesReview”121ClearwireQ12010EarningsCall,http://seekingalpha.com/article/203243‐clearwire‐q1‐2010‐earnings‐call‐transcript122BankofAmerica,“1Q10telecomandcablescorecards”123P.B.Selding,“ViaSattoBuyWildBluefor$568Million,”SpaceNews,2009,http://www.spacenews.com/archive/archive08/kabandside_0114.html.124AmericanTower,Form10‐Q,Q12010,http://phx.corporate‐ir.net/phoenix.zhtml?c=98586&p=irol‐SECText&TEXT=aHR0cDovL2lyLmludC53ZXN0bGF3YnVzaW5lc3MuY29tL2RvY3VtZW50L3YxLzAwMDExOTMxMjUtMTAtMTExMDUyL3htbA%3d%3d125SBACommunicationsCorporationForm10‐Q,Q12010,http://www.sec.gov/Archives/edgar/data/1034054/000119312510112092/d10q.htm

44

Overall,downstreambroadbandspeedsonaverageintheUSareat9.98Mbpswithupstreamspeedsatanaverageof2.18Mbps.126ThetopaveragebroadbandspeedsactuallyexperiencedintheresidentialU.S.arelistedasfollows:

AverageUSDownloadSpeeds:

Table 6: Average Download Speeds of ISPs (Top Ten) TopISP’s Average

SpeedtestsTotalIP

Addresses

1 Westnet 25.62Mbps 12,016

2 Psinet 22.52Mbps 13,214

3 IowaNetworkServices 16.76Mbps 33,206

4 ComcastCable 16.10Mbps 6,919,468

5 MidcontinentCommunications

14.99Mbps 48,636

6 CharterCommunications 14.86Mbps 1,748,148

7 InsightCommunicationsCompany

14.14Mbps 219,955

8 CoxCommunications 13.96Mbps 1,727,342

9 TimeWarnerRoadRunner 13.57Mbps 4,337,530

10 OptimumOnline 13.36Mbps 193,786

Table 7: Average Upload Speed of ISPs (Top Ten) TopISP’s Average

SpeedtestsTotalIP

Addresses

1 Westnet 19.73Mbps 12,016

2 Psinet 13.98Mbps 13,214

3 IowaNetworkServices 11.43Mbps 33,206

4 SurewestBroadband 8.65Mbps 25,555

5 AT&TServices 6.53Mbps 23,930

6 VerizonInternetServices 6.19Mbps 4,118,703

126NetIndex,July28,2010<http://www.netindex.com/upload/2,1/United‐States/>

45

7 TWTelecomHoldings 5.98Mbps 14,749

8 ApogeeTelecom 4.39Mbps 13,831

9 CoxCommunications 3.57Mbps 1,727,342

10 CbeyondCommunications 3.55Mbps 32,213

Source:Adaptedfrom,Ookla.http://www.netindex.com/download/2,1/United‐States/

Cable:SpeedsbeingdeliveredbyDOCSIS3.0arecurrentlyreachingashighas100+Mbpsandeven200Mbpsbysomecompanies.127Speedsvary,however,throughoutthecablemarketwithsomeprovidersdeliveringtopspeedsaslowas20Mbpsandmanydeliveringaround50Mbps.Upstreamspeedsarestillsignificantlylowerwithmostpeakingaround10‐12Mbps.SeetheAppendixformoredetail.

Telco:FTTHandFTTN‐DSLprovidersaredeliveringspeedstokeepupwithcable’sDOCSIS3.0rollout.AT&TU‐verseisplanningtocoverits120U‐versemarketswith24Mbpsdownstreamand3Mbpsupstream,128whileVerizonifoffering50Mbpsdownstream/20MbpsupstreamwithFiOS.129Smallertelephonecompaniesofferawiderangeofspeeds,fromverylowtospeedsthatmatchorexceedthoseofthelargetelcosandcablecompanies.Forinstance,RuralTelephone/Nex‐Tech,inKansas,willuseacombinationoffiberandWiMAXtechnologyto23,000householdsthatiscapableofdelivering100Mbpsspeeds.130NITCO,asmallIndianaTelephonecompany,saidit"willbeworkingdiligentlytoutilizethelatestversionsofDSL,fiber,andWiMaxtechnologiestoachieveandexceedtheseuploadanddownloadspeedstandards."131

Satellite:Downloadspeedsaretypicallyfivetosixtimesfasterthansatelliteuploadspeedsandcurrentlyrangefrom512kbpsto1.5mbpsdownstreamand100kbps–300kbpsupstream.132Overcominglatencyandsignallossduetoprecipitationhavebeenmajorperformanceandqualityobstaclesforsatelliteproviders.Geostationarysatellitecommunicationsexperience