Embed Size (px)

Citation preview

Broad guidelines on ‘Refunds’

1. Introduction

Under Section 11B of the Central Excise Act, 1944, any person claiming refund of any duty of excise may make an application in prescribed form for refund of such duty before expiry of one year from the relevant date (as defined in the explanation under Section 11B (5) of Central Excise Act, 1994) and the application shall be accompanied by such documentary or other evidence as the applicant may furnish to establish that the amount of duty of excise in relation to which such refund is claimed was collected from, or paid by him and the incidence of such duty had not been passed on by him to any other person. Refunds include rebates of duty of excise on excisable goods exported out of India or on excisable materials used in the manufacture of goods which are exported out of India. Under Section 11BB of Central Excise Act, 1944, interest is payable to the applicant if any duty ordered to be refunded is not refunded within three months from the date of receipt of application.

As per the figures furnished by the Ministry, the amount of refunds (other than rebate) made during the years 2002-03, 2003-04 and 2004-05 was Rs.999.77 crore, Rs.965.75 crore and Rs.1128.83 crore the numbers of cases being 31574, 33965 and 16541 respectively. While there was sharp increase in amount of refunds during the year 2004-05 as compared to year 2003-04, the number of cases declined from 33965 in 2003-04 to 16541 in 2004-05. This is indicative of the large amount of refunds being involved per case.

Interest on refunds has risen from Rs.1.22 crore during the year 2002-03 to Rs.25.11 crore during the year 2003-04 and to Rs.61.02 crore during the year 2004-05. This is indicative of the fact that the finalization of refunds cases are being delayed beyond three months. The amount of rebate under Rule 18 of the Central Excise Rules was Rs.1491.75 crore, 2423.13 crore and 2616.53 crore during the years 2002-03, 2003-04 and 2004-05 respectively.

The Commissionerate-wise details of refunds and rebate as also copies of important circulars/instructions issued by the Department in this regard are given in Annexure A.

2. Audit objectives

The review may be conducted to assess: -

(i) The adequacy of statutory provisions and instructions/notifications issued from time to time to guard against any irregular refund and erroneous refund causing revenue loss;

(ii) Performance of the department in disposal of refund cases and payment of only that amount of refund which was due within the stipulated timeframe so as to avoid payment of interest; and

1

(iii) Effectiveness of monitoring and control mechanism devised for refunds.

3. Statistical information

Statistical information may be collected Commissionerate-wise and Chief Commissionerate-wise as per Annexure B-I, B-II and B-III.

4. Sample of review

The selection of sample size is crucial for in-depth analysis of the refund cases. Audit coverage may be decided by Accountants General/Pr. Directors of Audit at their discretion based on number of refunds, amount of the refunds and payment of interest in each Division/Commissionerate. However for the purpose of conducting pilot study, the sample may be selected as under: -

(i) One Division each from a Commissionerate with minimum number not less than five Divisions in field offices where 10 or more Commissionerates are located;

(ii) Minimum three Divisions, one from each Commissionerate where between five and nine Commissionerates are located; and

(iii) The remaining field offices may select two divisions each.

The Commissionerate-wise details of rebate/refunds as enclosed (Annexure A) could be of help in selection of Commissionerates.

The findings of pilot study may be sent to headquarters by 31 August 2006. The findings would be discussed in the three regional seminars to be held in September 2006, in which selected field offices would participate. In the light of discussions in these seminars, additional guidelines on the required sample size, formats devised for collection of information and other emerging issues to be focused upon in the review would be issued.

The details of the sample size and the basis for selection should be outlined in the pilot study report.

5. Broad Issues

5.1 Refunds (other than rebate under section 11B)

Chapter 9 of Central Board of Excise and Custom’s Manual of Supplementary Instructions dealing with refunds as also instructions of the Board issued from time to time on this subject may be gone through.

It may be seen in audit: -

(i) The reasons for the assessee applying for a refund and department’s action which occasioned the arising of refund may be examined.

2

(ii) Whether the refund claim has been filed within one year from the relevant date in the specified form (refund can be claimed by the assessee within one year from the relevant date). The relevant date for this purpose is as defined in the explanation under Section 11B (5) of Central Excise Act, 1944.

(iii) Whether the assessee has filed the claim in proper form with all supporting documents/records to establish that he has not passed on the duty incidence to others.

(iv) Whether the range superintendent has completed the scrutiny of the refund claim within two weeks from the date of its receipt in the range and sent his report to the Deputy/Assistant Commissioner of Central Excise.

(v) Whether final processing has been completed and the order of Deputy/Assistant Commissioner of Central Excise obtained in the Divisional Office within three months. In case of any deficiency in the application, whether assessee has been informed within 15 days with a copy to range office.

(vi) Whether all refund/rebate claims, involving an amount of Rs.5 lakh or above have been subjected to pre-audit at the level of Jurisdictional Commissioner. In such cases, a suitable Order-In-Original, has to be passed by the Deputy/Assistant Commissioner of Central Excise. Since the claim is pre-audited with the concurrence of Commissioner, the usual review proceedings under Section 35E of Central Excise Act, 1944, may not be necessary in such cases.

(vii) Whether the refund claim has been deliberately kept below Rs.5 lakh so as to avoid pre audit. If so in how many cases? Is this done by all the officers who held the charge or by some specific persons? For this assessee wise refunds in a year and their periodicity may be looked out.

A gist of the complaint case received in this office in this connection is placed in Annexure A.

(viii) Whether refund/rebate claims involving an amount above Rs.50,000/- but below Rs.5 lakh, Order-In-Original have been passed by Deputy/Assistant Commissioner and subjected to compulsory post-audit at the level of Additional/Joint Commissioner (Audit). Such Orders-In–Original are subjected to review under Section 35E.

(ix) Whether order-in-original has been issued involving refund/rebate claims of an amount up to Rs.50,000/-, where the sanctioned amount was less than the claimed amount.

3

(x) Whether claims of an amount upto Rs.50,000/- have been post-audited on the basis of the random selection by the Deputy/Assistant Commissioner (Audit), in such a way that at least 25 per cent of the claims were post-audited.

(xi) Whether jurisdictional Commissionerate has devised a suitable monitoring mechanism to assure timely disposal of refund/rebate claims so as to avoid payment of interest. If a mechanism exists then it may be examined for its adequacy and effectiveness.

(xii) Whether there is propensity to keep the refund cases pending and dispose of the same in April of each year after the close of financial year with a view to show achievements of targets. To substantiate this point duty paid in March but quickly refunded in April need to be probed. Also to examine specifically if duty was paid in excess than was due and claimed back by way of refunds.

(xiii) Whether a register of refunds in the prescribed form has been maintained and all the applications entered therein.

(xiv) Whether Deputy/Assistant Commissioner has sent a statement in the prescribed proforma to the Chief Accounts Officer in duplicate on 8th, 15th, 22nd and the last date of each month.

(xv) Whether there is proper monitoring to ensure that one copy of proforma is returned by Chief Accounts Officer after post audit.

(xvi) If the refund process is automated using any software then details regarding the software used such as who developed it, when and since when it is being put to use may be provided. Also run some sample checks of the software in doing the needful as envisaged in law.

5.2 Theory of unjust enrichment

Section 11B was inserted with effect from 11 July 1980. The most important amendment took place on 20 September 1991, wherein the theory of unjust enrichment was built into the statute. This concept of the unjust enrichment postulates paying once and getting twice (that is once from the customer and again from the Government). This theory postulates that only the person who had not passed on the incidence of duty will be eligible to claim the refund. This concept was upheld in M/s. Mafatlal Ind. Ltd. Vs Union of India by a nine members Bench of the Supreme Court. The implication of the judgement was as under: -

(i) Section 11B and Section 27 (Customs Act) are self-contained codes for refunds and resorting to civil suits or writs is not permissible unless the taxing provision is struck down as unconstitutional.

(ii) Unless the levy is struck down as un-constitutional, all Courts must exercise jurisdiction in terms of Section 11B and refuse to grant relief if the incidence of tax has been passed on.

4

(iii) Whatever amount is collected as duty, will have to be paid to the Government. If any excess is collected (than payable), it would be credited into consumer’s welfare fund or given as refund to the person who had borne the incidence of duty.

Circumstances where unjust enrichment is not applicable

In the following cases, refund is to be given and the bar of unjust enrichment is not applicable: -

(i) In respect of rebate of duty of excise on excisable goods exported out of India or on excisable materials used in the manufacture of goods which are exported out of India, it was clarified by the Board that, the duty paid through the actual credit, or deemed credit account on the goods exported must be refunded in cash and that there was no discretion with the sanctioning authority to give the refund through credit accounts (Circular No.687/3/02-CX dated 3 January 2003). However, it should be checked in audit, whether excess duty (higher rates) was paid from Cenvat account, to encash excess credit in Cenvat account, by way of rebate in cash. In this connection a gist of complaint case as per Annexure A may also be perused.

(ii) Unspent advance deposits lying in balance in the applicant’s account current, maintained with the Commissioner of Central Excise.

(iii) Refund of credit of duty paid on excisable goods used as inputs in accordance with the rules made, or any notification used, under this Act.

(iv) The duty of excise paid by the manufacturer if he had not passed on the incidence of such duty to any other person.

(v) Duty of excise borne by the buyer if he has not passed on the incidence of such duty to any other person.

It may be seen in audit: -

(i) Whether the refund has not resulted into unjust enrichment of the assessee in terms of the theory of unjust enrichment as interpreted by Supreme Court.

(ii) Duty collected in excess of what was payable has been credited into consumer welfare fund or given as refund after re-determination of the excess duty being payable.

5.3 Refund cases where appeal was filed

(i) Whether speedy action has been taken by Commissioner to submit all the relevant papers to the Board for obtaining Law Ministry’s advice and if agreed filing Special Leave Petitions and Stay Petition against the orders of the High Court in cases where it is considered advisable to contest an adverse High Court judgement involving substantial refund.

5

(ii) Whether Commissionerate have filed simultaneously an application before High Court for extension of time in case where a High Court has stipulated any time for implementation of its orders.

(iii) The delays in such cases both at Commissionerate level and Board’s level and resultant payment of refunds may be highlighted. Cases where there was delay on the part of the board may also be referred to Headquarter for further examination.

(iv) Whether prompt action for filing an appeal/obtaining stay orders taken in cases where it is intended to file an appeal against orders of Central Excise Officer sub-ordinate to Commissioner/Commissioner (Appeals)/ Commissioner/CEGAT involving high refund.

5.4 Refund of pre-deposit

As per circular Nos.275/37/2000-CX 8A dated 2 January 2002 and 82/35/2004-CX, dated 8 December 2004, pre-deposits are required to be returned within a period of three months of the disposal of the appeal in the assessee’s favour.

It may be seen in audit: -

(i) Whether the pre-deposits have been refunded within three months.

(ii) Whether any interest had to be paid due to delay beyond three months

(iii) The stage at which the refund was delayed.

5.5 Refund of excise duty to Diplomatic Mission

Refund is governed by the conditions mentioned in Notification No.3/2001-CE dated 1 March 2001. As per Board’s instruction F. No.156/14/2000-CX 4 dated 11 April 2001, refunds would be entertained by the Commissionerate within whose territorial jurisdiction, the missions/consular office is located.

It may be seen in audit: -

(i) That the time limit for making the refund claim viz. one year from the date of purchase of the goods by the diplomatic mission or consular office has been adhered to.

(ii) That no extension beyond one year from the date of purchase, has been granted.

5.6 Refund of Cenvat credit

Under Rule 5 of Cenvat Credit Rules, 2004, Cenvat credit on inputs used in the final products which is cleared for export under bond and which could not be

6

utilised for payment of duty of excise on final product cleared for home consumption or for export on payment of duty is allowed to be refunded.

In this connection notification No.11/2002-CE (NT), dated 1 March 2002 as amended by Notification No.49/2003-CE (NT), dated 17 May 2003 may be gone through.

It may be seen in audit: -

(i) Whether refund claims have been submitted only once in any quarter in a calendar year if the average export clearances in value terms is less than 70 per cent.

(ii) Whether application has been submitted in prescribed form.

(iii) Whether refund of only that portion of credit has been made which could not be utilised.

(iv) Whether relevant documents have been submitted before the expiry of the period specified in Section 11B of the Central Excise Act, 1944.

5.7 Refund towards motor vehicle

Motor Vehicles falling under Sub-Heading No.8702.10 or 8703.90, which after clearance have been registered for use solely as ambulance or (ii) Sub-Heading No.8703.90 which, after clearance have been registered for use solely as taxi are exempted from the payment of special excise duty vide notification No.6/2002 dated 1 March 2002 as amended. However while clearing the goods the manufacturer has to pay 24 per cent (16 per cent BED + 8 per cent SED) and is eligible for refund of 8 per cent SED after registration of vehicles under the above category.

It may be seen in audit that the manufacturer has filed a claim for refund of the said amount of duty before expiry of six months from the date of payment of duty on the said motor vehicle.

The possibility of misuse of these vehicles by selling the same and getting it reregistered as normal vehicles may be looked into in coordination with State Receipt Audit wing.

Since the normal time limit of one year is not applicable in this case, Cases of belated filing of claims and incorrect sanctions of refund may be probed into and commented upon.

The information about the buyers of the motor cars registered as Taxis may be exchanged with the persons conducting audit on service tax. This information should be obtained from the Regional Transport Offices through audit parties of SRA.

7

Irregularities noticed may be tabulated in Annexure C-I to C-XI.

Individual cases involving substantial amount may be highlighted separately.

5.8 Rebate of duty on export of goods

The Government by notification issued under Rule 18 of Central Excise Rules have granted rebate of the whole duty paid on excisable goods, exported out of India or on excisable materials used in the manufacture of goods which are exported out of India. The conditions and procedures relating to export under claim of rebate are contained in Notification No.19/2004-CE (NT), dated 6 September 2004 and No.20/2004-CE (NT), dated 6 September 2004. Process, not amounting to manufacture such as packing and blending, is also eligible for benefit.

(a) Important points to be seen in checking rebate of duty on exported goods

It may be seen in audit: -

(i) Whether all the required documents have been filed for claiming rebate.

(ii) Whether deficiencies in the claim have been pointed out within 15 days.

(iii) Whether the claim of rebate has been disposed of within a period of two months.

(iv) Whether supplementary rebate claim has been filed within the stipulated period under Section 11B.

(v) Whether individual rebate claim exceeding Rs.5 lakh has been pre-audited.

(vi) Whether there is a marked trend to present rebate claim not exceeding Rs.5 lakh so as to avoid pre-audit.

(vii) Whether excess duty at higher rates have been paid from Cenvat to encash excess unused credit by way of rebated in cash.

(viii) Whether goods have been exported directly from a factory or warehouse. Goods can be exported for a place other than the factory or the warehouse if there are specific instructions from the Board in this regard.

(ix) Whether the excisable goods have been exported within six months from the date on which they were cleared for export for factory or warehouse. However, Commissioner of Central Excise has powers to extend this period for reasons to be recorded in writing.

(x) Whether the market price of excisable goods at the time of exportation is not less than the amount of rebate of duty claimed for export.

8

(xi) Whether the rebate of duty paid is on these excisable goods export of which are not prohibited under any law

(b) Important points to be seen in checking of rebate of duty on excisable material

Input stage rebate cannot be claimed in any of the following situations: -

(i) Where the finished goods are exported under claim for duty Drawback.

(ii) Where finished goods are exported in discharge of export obligation, under a Value based Advance Licence or Quantity Based Advance License issued before 31 March 1995.

(iii) Where a facility of input stage credit is availed under CENVAT Credit Rules 2002.

(iv) The market price is less than rebate amount.

(v) The amount of rebate admissible is less then Rs.500/-

It may be seen in audit: -

(i) Whether the manufacturer or processor has filed a declaration with Deputy/Assistant Commissioner of Central Excise having jurisdiction over the factory of manufacturer describing the finished goods proposed to be manufactured or processed along with their rates of duty leviable and manufacturing/processing formula with particular reference to quantity or proportion in which the materials are actually used as well as quality.

(ii) Whether separate, statement of input, output ratio have been furnished for each export/product where there are more than one export products.

(iii) Whether the consumption is net of recycled materials. Where recoverable wastage are generated and not recycled, but sold on account of its unsuitability, the same was clearly reflected in the declaration.

(iv) Whether in case of a new product or in case where manufacturer is not regularly manufacturing the export goods and clearing for home consumption or export, a write up of manufacturing process has been furnished alongwith declaration.

The information may be collected as per Annexure D-I to D-VII.

The individual cases involving substantial amount may be highlighted separately.

9

10

5.9 Export of goods to Nepal

Under notification No.20/2004-CE (NT), dated 6 September 2004 as amended by notification No.30/2004-CE (NT) dated 21 October 2004 and No.15/2005-CE (NT) dated 1 March 2005 rebate of the whole of the duty paid on the excisable goods exported to Nepal shall be granted to His Majesty’s Government of Nepal subject to the conditions, limitation and procedures specified therein.

Director General of Audit Central Revenues may see that the procedure as prescribed in the notifications has been followed by Director General of Inspection Customs and Central Excise (Nepal Refund Wing), New Delhi and the amount of rebate to be granted to Nepal Government has been correctly worked out.

Annexure B-I

Statement showing details of the amount of refunds (other than rebate) made under Section 11B of Central Excise Act, 1944 (From all Commissionerates)

(Position as on 30 September 2006)

Name of the Divisions ____________________

Name of the Commissionerate ____________________ (Amount in lakh of rupees)

Commissionerate Year Opening balance Additions Clearance Balance Interest paid under Section 11BB

No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

2003-04

2004-05

2005-06

11

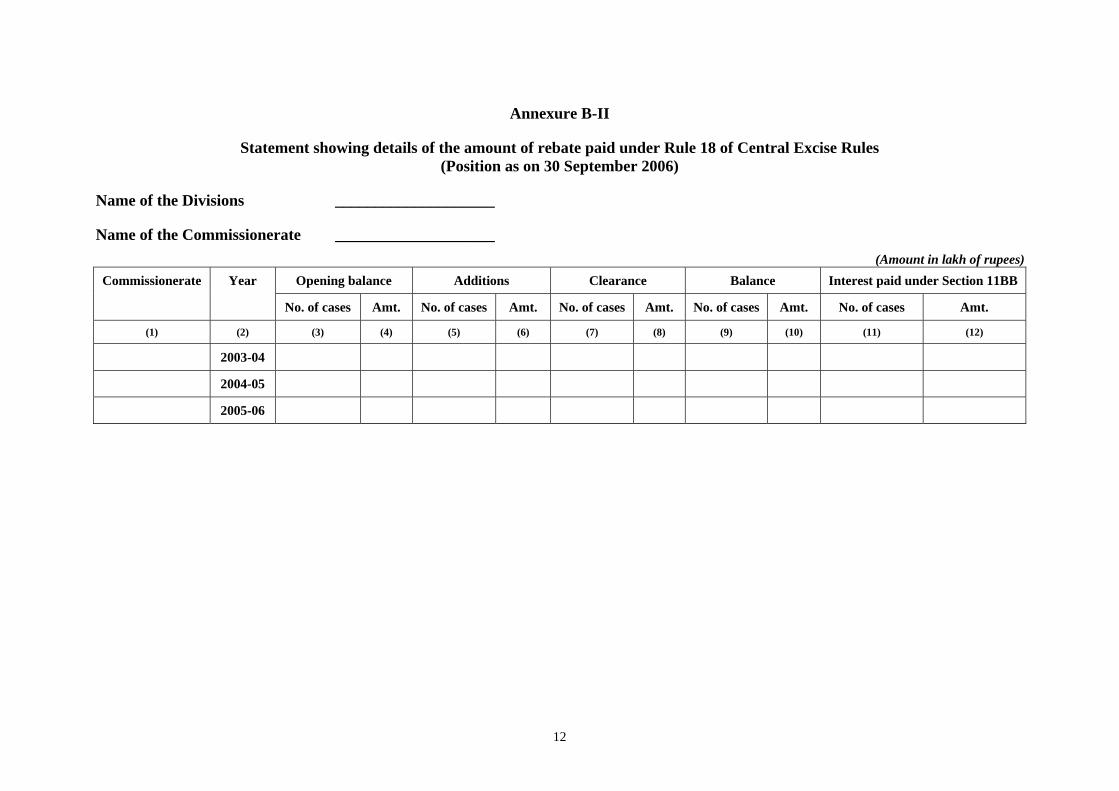

Annexure B-II

Statement showing details of the amount of rebate paid under Rule 18 of Central Excise Rules (Position as on 30 September 2006)

Name of the Divisions ____________________

Name of the Commissionerate ____________________ (Amount in lakh of rupees)

Commissionerate Year Opening balance Additions Clearance Balance Interest paid under Section 11BB

No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

2003-04

2004-05

2005-06

12

Annexure B-III

Statement showing details of refunds made under Section 11C of Central Excise Act, 1944 (From all Commissionerates)

(Position as on 30 September 2006)

Name of the Divisions ____________________

Name of the Commissionerate ____________________ (Amount in lakh of rupees)

Commissionerate Year Opening balance Additions Clearance Balance Interest paid under Section 11BB

No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt. No. of cases Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

2003-04

2004-05

2005-06

13

Annexure C-I

Statement showing details of irregular refunds (Amount in lakh of rupees)

Commissionerate Division Assessee Period Nature of irregularity Amount of refund made Amount of refund required to be made Excess refund made Remarks

(1) (2) (3) (4) (5) (6) (7) (8) (9)

14

Annexure C-II

Statement showing details of cases where refund was made beyond 3 months necessitating payment of interest (Amount in lakh of rupees)

Commissionerate No. of divisions Period Total No. of refund cases Cases where refund made after 3 months Cases where interest was paid Remarks

No. Amt. No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

2003-04

2004-05

2005-06

Note: Full details of cases may be furnished separately alongwith this information.

15

Annexure C-III

Details of cases involving an amount of more than Rs.50000/- but less than Rs.5 lakh where post audit was not done (Selected Divisions/Commissionerates)

(Amount in lakh of rupees) Commissionerate Divisions Period Total No. of cases above Rs.50000/- but less than Rs.5 lakh Cases where post audit not done Remarks

No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

Details of cases not reviewed under Section 35E (Amount in lakh of rupees)

Commissionerate Divisions Period Total No. of cases above Rs.50000/- but less than Rs.5 lakh

Cases not reviewed under Section 35E

Cases where adverse orders issued after review

No. Amt. No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9)

2003-04

2004-05

2005-06

16

Annexure C-IV

Details of cases where 25 per cent of the claims upto Rs.50000/- not post audited

Commissionerate No. of Divisions Period Percentage of claims post audited Percentage of claims less post audited Remarks

(1) (2) (3) (4) (5) (6)

2003-04

2004-05

2005-06

17

Annexure C-V

Statement showing the details of cases where amount of refund was kept just below Rs.5 lakh (Amount in lakh of rupees)

Sl. No. Commissionerate Division Period Name of assessee Refund amount Remarks

(1) (2) (3) (4) (5) (6) (7)

ABSTRACT

Sl. No.

Commissionerate Division Period Total No. of cases Cases of refunds involving Rs.5 lakh or above

Involving less than Rs.5 lakh but more than Rs.50000/-

Involving less than Rs.50000

No. Amt. No. Amt. No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

2003-04

2004-05

2005-06

18

Annexure C-VI

Statement showing the details of cases where scrutiny of refund claim not completed within two weeks (Selected ranges)

(Amount in lakh of rupees) Commissionerate No. of ranges Period Total No. of refund cases Cases where scrutiny not completed within two weeks Remarks

No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

Note: Details of cases may be furnished separately alongwith this information.

19

Annexure C-VII

Statement showing details refunds of pre-deposits made beyond 3 months (Amount in lakh of rupees)

Commissionerate Divisions Period Total No. of refund cases Cases where refund made after 3 months Cases where interest was paid Remarks

No. Amt. No. of cases Amt. No. of cases Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

2003-04

2004-05

2005-06

Note: Full details of cases may be furnished separately alongwith this information.

20

Annexure C-VIII

Statement showing details of refunds made to Diplomatic mission beyond one year (Amount in lakh of rupees)

Commissionerate Divisions Period Details of cases of refund beyond one year

Details of diplomatic missions No. of cases Amt.

(1) (2) (3) (4) (5) (6)

2003-04

2004-05

2005-06

21

Annexure C-IX

Statement showing the details of irregular refunds of Cenvat credit under Rule 5 of Cenvat Credit Rules, 2004 (Amount in lakh of rupees)

Commissionerate Divisions Period Nature of irregularity

No. of cases Amount of Cenvat credit refunded

Amount of Cenvat irregularly refunded (Out of 6)

Remarks

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

22

Annexure C-X

Statement showing details of irregular refund towards Motor Vehicles (Amount in lakh of rupees)

Commissionerate Divisions Period Nature of irregularity No. of cases Amount of refund Amount of irregular refund (Out of 6)

Remarks

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

23

Annexure C-XI

Details of refund cases where there was delay in filing appeal/stay orders (Amount in lakh of rupees)

Commissionerate Divisions Period Details of cases Level at which delayed/stay order not obtained

Period of delay and other such information

Remarks

Name of assessee Amt. refunded

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

24

Annexure D-I

Statement showing details of irregular rebates (Amount in lakh of rupees)

Commissionerate Division Assessee Period Nature of irregularity Amount of rebate paid Amount of rebate required to be paid Excess rebate paid Remarks

(1) (2) (3) (4) (5) (6) (7) (8) (9)

25

Annexure D-II

Statement showing details of cases where rebate was paid beyond three months necessitating payment of interest (Amount in lakh of rupees)

Commissionerate No. of divisions Period Total rebate cases Cases where rebate paid beyond 3 months Cases where interest was paid Remarks

No. Amt. No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

2003-04

2004-05

2005-06

Note: Full details of cases may be furnished separately alongwith this information.

26

Annexure D-III

Statement showing details of rebate cases where rebate was made beyond two months (Amount in lakh of rupees)

Commissionerate No. of divisions Period Total No. of rebate cases Cases where rebate made beyond 2 months Remarks

No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

27

Annexure D-IV

Statement showing details of cases where individual rebate claim exceeding Rs.5 lakh has not been pre-audited (Amount in lakh of rupees)

Commissionerate No. of divisions Period Total rebate claim involving more than Rs.5 lakh Cases not pre-audited Remarks

No. Amt. No. Amt.

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

28

Annexure D-V

Statement showing the details of cases where amount of rebate was kept just below Rs.5 lakh (Amount in lakh of rupees)

Sl. No. Commissionerate Division Period Name of assessee Rebate amount

(1) (2) (3) (4) (5) (6)

29

Annexure D-VI

Statement showing details of cases where goods exported beyond six months (Amount in lakh of rupees)

Commissionerate Divisions Period No. of cases Amount Whether period extended by Commissioner Remarks

(1) (2) (3) (4) (5) (6) (7)

2003-04

2004-05

2005-06

30

Annexure D-VII

Statement showing details of cases where market price is less than rebate amount (Amount in lakh of rupees)

Commissionerate Divisions Period No. of rebate cases Amount of rebate Market Price Amount of irregular rebate Remarks

(1) (2) (3) (4) (5) (6) (7) (8)

2003-04

2004-05

2005-06

31

Annexure A

(i) A gist of the complaint case

The assessee was exporting goods and claiming rebate under Rule 18 of Central

Excise Rules. The applicable rate of duty on rear tractor tyres as declared in monthly

return (E.R.I) falling under TSH No.4011.20 of Central Excise Tariff during the relevant

period was 16 per cent only, whereas the assessee had paid duty at rate of 24 per cent to

encash the Modvat credit illegally with connivance of officers during the relevant period

and get refund.

The 83 claims, most of the claims were hurriedly processed/sanctioned in the

month of June/July and August 2004. As per the instructions the refund claims of Rupees

more than 5 lakhs are required to be sent to the audit for pre audit and the cheque is

issued only after it is pre audited. But the Deputy Commissioner disposed off the same

by individual order, so as to make the payment promptly to the party in cash of the refund

amount below Rs.5 lakhs, without sending for pre audit.

The goods were physically examined and verified by the concerned

Superintendent Range/Sector officer before the same were stuffed into the container and

sealed and the fact that the rear tractor tyre are being exported after debiting duty from

the Modvat illegally. The intention to encash by claiming refund was in the knowledge

of all the officers from inspectors to Deputy Commissioners involved in exporting and

processing the refund claims during the period from 25 November 2002 to 30 December

2004. But they all worked as a chain, connived with the assessee and damaged the

government revenue of Rs.10 crore.

![422 Worldspan Refunds Course July 2007 boek 6[1]de.travelportservices.com/.../files/403_Worldspan_Refunds_Manual.pdfREFUNDS MANUAL Jul 07 Refunds Manual The World’s Leading provider](https://img.pdfslide.us/doc/110x75/5ae44dd67f8b9ae74a8eed2a/422-worldspan-refunds-course-july-2007-boek-61de-manual-jul-07-refunds-manual.jpg)