Embed Size (px)

Citation preview

British Columbia Hydro and Power Authority, 333 Dunsmuir Street, Vancouver BC V6B 5R3 www.bchydro.com

Fred James

Chief Regulatory Officer Phone: 604-623-4046 Fax: 604-623-4407 [email protected]

January 21, 2020 Mr. Patrick Wruck Commission Secretary and Manager Regulatory Support British Columbia Utilities Commission Suite 410, 900 Howe Street Vancouver, BC V6Z 2N3 Dear Mr. Wruck: RE: Project No. 1598990

British Columbia Utilities Commission (BCUC or Commission) British Columbia Hydro and Power Authority (BC Hydro) Fiscal 2020 to Fiscal 2021 Revenue Requirements Application (the Application)

BC Hydro writes to provide, as Exhibit B-11-2, a correction with regards to the financial schedules included as Appendix A of Exhibit B-11. Specifically, BC Hydro is updating the fiscal 2021 current service pension costs that were filed in the Evidentiary Update due to a clerical error.

The impact of this correction is a decrease to the operating cost portion of current service pension costs by $1.0 million in fiscal 2021. Accordingly, BC Hydro is amending its proposed rate decrease in fiscal 2021 from 0.99 per cent to 1.01 per cent. This correction also reduces the Transmission Revenue Requirement by $246,000 in fiscal 2021.

The following documents, showing the changes related to this correction, are attached to this submission:

Evidentiary Update (originally filed as Exhibit B-11);

Appendix A of the Evidentiary Update (for convenience, these changes are shaded in red); and

Appendix E of the Evidentiary Update.

We apologize for the error. If the BCUC or interveners have questions about this error, those questions can be directed to Panel 2.

January 21, 2020 Mr. Patrick Wruck Commission Secretary and Manager Regulatory Support British Columbia Utilities Commission Fiscal 2020 to Fiscal 2021 Revenue Requirements Application (the Application) Page 2 of 2

For further information, please contact Chris Sandve at 604-974-4641 or by email at [email protected].

Yours sincerely,

(for) Fred James Chief Regulatory Officer cs/rh

Enclosure

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Evidentiary Update

August 22, 2019

(Made Public on October 18, 2019)

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page i

Table of Contents

1 Evidentiary Update Has a Favourable Impact on Customers ............................. 1

1.1 Overview of BC Hydro’s Updated Revenue Requirements ....................... 5

1.2 Cost of Energy Has Decreased While Dry Conditions and Lower IPP Purchases Have Increased Market Purchases ......................................... 7

1.3 Operating Costs Have Increased Due to Uncontrollable Factors ............ 12

1.4 Amortization Has Increased Due to the Full Implementation of IFRS 16 ................................................................................................... 14

1.5 Finance Charges Have Increased Due to the Full Implementation of IFRS 16 ................................................................................................... 15

1.6 Actual Fiscal 2019 Powerex Net Income Was Higher Than Planned ...... 15

List of Figures

Figure 1 Five Year Net Bill Increases Forecast ................................................ 1

Figure 2 Volumes of Supply - Fiscal 2020 Plan vs. Fiscal 2020 Update (GWh) ................................................................................................. 8

Figure 3 Volumes of Supply - Fiscal 2021 Plan vs. Fiscal 2021 Update (GWh) ................................................................................................. 9

Figure 4 Cost of Energy - Fiscal 2020 Plan vs. Fiscal 2020 Update – Current View ($ millions) .................................................................. 11

Figure 5 Cost of Energy - Fiscal 2021 Plan vs. Fiscal 2021 Update – Current View ($ millions) .................................................................. 11

Figure 6 Operating Costs - Fiscal 2020 Plan vs. Fiscal 2020 Update – Current View ($ millions) .................................................................. 13

Figure 7 Operating Costs - Fiscal 2021 Plan vs. Fiscal 2021 Update – Current View ($ millions) .................................................................. 14

List of Tables

Table 1 Revenue Requirement - Application vs. Evidentiary Update - Current View ...................................................................................... 5

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page ii

Appendices

Appendix A Financial Schedules Appendix B Draft Order Appendix C Updated Cost of Energy Forecast Appendix D Updated Regulatory Account Balances Appendix E Updated Transmission Revenue Requirement Appendix F Implementation of IFRS 16 Update Appendix G Fiscal 2019 Variance Explanations

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020]

Page 1

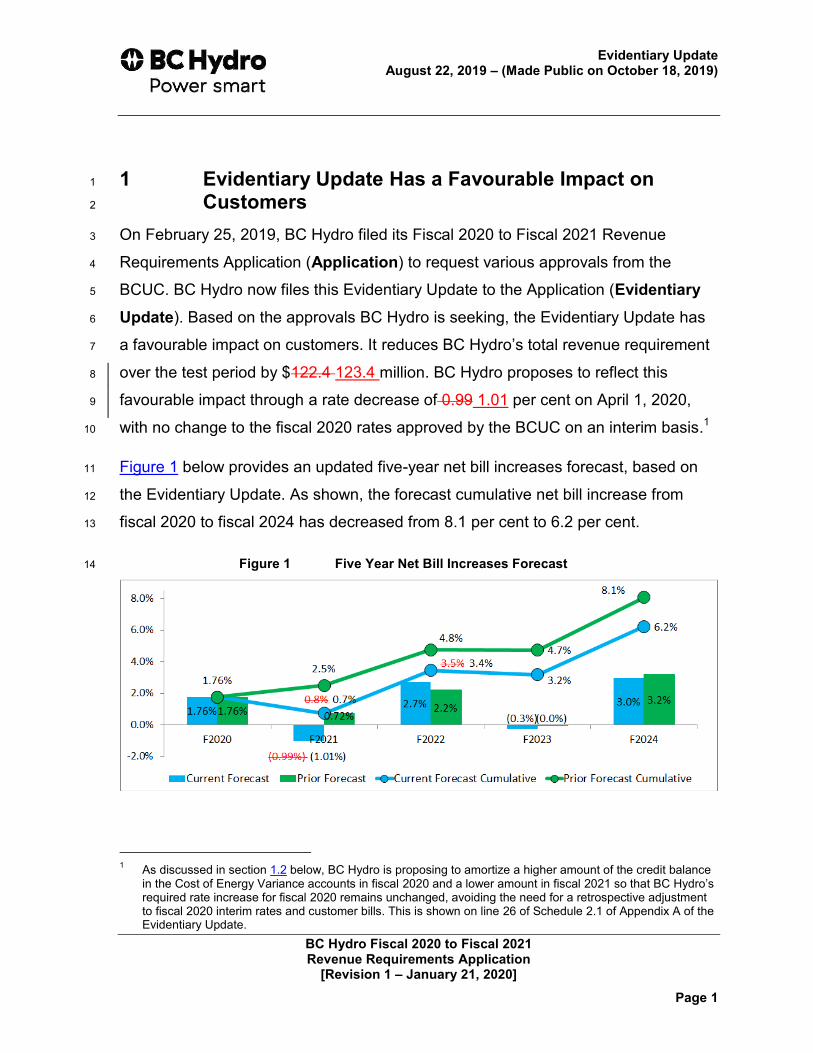

1 Evidentiary Update Has a Favourable Impact on 1

Customers 2

On February 25, 2019, BC Hydro filed its Fiscal 2020 to Fiscal 2021 Revenue 3

Requirements Application (Application) to request various approvals from the 4

BCUC. BC Hydro now files this Evidentiary Update to the Application (Evidentiary 5

Update). Based on the approvals BC Hydro is seeking, the Evidentiary Update has 6

a favourable impact on customers. It reduces BC Hydro’s total revenue requirement 7

over the test period by $122.4 123.4 million. BC Hydro proposes to reflect this 8

favourable impact through a rate decrease of 0.99 1.01 per cent on April 1, 2020, 9

with no change to the fiscal 2020 rates approved by the BCUC on an interim basis.1 10

Figure 1 below provides an updated five-year net bill increases forecast, based on 11

the Evidentiary Update. As shown, the forecast cumulative net bill increase from 12

fiscal 2020 to fiscal 2024 has decreased from 8.1 per cent to 6.2 per cent. 13

Figure 1 Five Year Net Bill Increases Forecast 14

1 As discussed in section 1.2 below, BC Hydro is proposing to amortize a higher amount of the credit balance

in the Cost of Energy Variance accounts in fiscal 2020 and a lower amount in fiscal 2021 so that BC Hydro’s required rate increase for fiscal 2020 remains unchanged, avoiding the need for a retrospective adjustment to fiscal 2020 interim rates and customer bills. This is shown on line 26 of Schedule 2.1 of Appendix A of the Evidentiary Update.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 2

The reduction in BC Hydro’s revenue requirements over the test period is the 1

product of updated information. Specifically, the Evidentiary Update: 2

Reflects Actual Financial Results from Fiscal 2019: The Evidentiary Update 3

replaces the fiscal 2019 forecast with actual fiscal 2019 results. Fiscal 2019 4

actual results impact the test period because they impact the amortization of 5

BC Hydro’s regulatory accounts in fiscal 2020 and fiscal 2021. Among other 6

things, this includes actual Powerex Net Income for fiscal 2019 which was 7

$230.4 million higher than forecast in the Application, increasing the credit 8

balance in the Cost of Energy Variance Accounts, which BC Hydro has 9

proposed to refund to ratepayers over the test period. Further information is 10

provided in section 1.6 below; 11

Updates the Cost of Energy Forecast: The Evidentiary Update replaces the 12

October 2018 Energy Study forecast in the Application with the June 2019 13

Energy Study forecast, which includes actual costs for April and May 2019. Dry 14

conditions and lower water inflows have decreased planned hydroelectric 15

generation (water rentals) and purchases from IPPs and Long-Term 16

Commitments, resulting in lower planned surplus sales and higher planned 17

market electricity purchases. Further information is provided in section 1.2 18

below; 19

Updates the Discount Rate for Pension Costs: The Evidentiary Update 20

replaces the forecast discount rate of 3.83 per cent used to forecast BC Hydro’s 21

pension costs in the Application with the actual discount rate of 3.33 per cent as 22

of April 1, 2019. The lower discount rate has an unfavourable impact on 23

operating costs, as discussed in section 1.3 below; 24

Updates Interest and Foreign Exchange Rates: The Evidentiary Update 25

replaces the October 2018 Government of B.C. interest and foreign exchange 26

rates forecast in the Application with the January 2019 Government of B.C. 27

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 3

forecasts. It also replaces the September 30, 2018 forward interest rates used 1

for future debt hedges in the Application with interest rates as of May 31, 2019. 2

This has a favourable impact on Finance Charges, as discussed in section 1.5 3

below; 4

Reflects the Full Implementation of the new Leasing Standard (IFRS 16): 5

In the Application, BC Hydro estimated the impact of IFRS 16 on Electricity 6

Purchase Agreements based on its preliminary assessment. We noted that the 7

actual impacts from the implementation of the standard may vary from these 8

estimates. The Evidentiary Update reflects BC Hydro’s completed assessment. 9

The difference between the estimates in the Application and those of the 10

completed assessment in the Evidentiary Update result in: 11

An increase of $82.8 million to the Non-Heritage Deferral Account; and 12

A decrease to Cost of Energy and an increase to Amortization and to 13

Finance Charges, resulting in a net increase to BC Hydro’s revenue 14

requirement of $16.6 million in fiscal 2020 and $15.5 million in fiscal 2021. 15

The impact to the test period revenue requirements is not net neutral because if 16

an Electricity Purchase Agreement is determined to be a lease under IFRS 16, 17

more costs are recognized in the earlier years of the agreement and fewer 18

costs are recognized in the later years of the agreement. Further information is 19

provided in Appendix F of the Evidentiary Update; 20

Updates for April and May Actuals: The Evidentiary Update replaces 21

BC Hydro’s forecasts in the Application for April and May 2019 with the actual 22

financial results for those months. This includes an update to domestic sales 23

revenue. Domestic sales revenue for the remainder of fiscal 2020 and all of 24

fiscal 2021 remains based on the October 2018 Load Forecast. In accordance 25

with the regulatory timetable for this proceeding, BC Hydro will file a 20-year 26

load forecast on October 3, 2019. This forecast was completed after the 27

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 4

financial inputs into the Evidentiary Update were finalized and is not reflected in 1

the Evidentiary Update. As BC Hydro will explain further in its October 3, 2019 2

filing, the difference in the test period between the October 2018 Load Forecast 3

volumes and the Load Forecast BC Hydro will file in October 2019 is less than 4

0.5 per cent. Therefore, BC Hydro has not updated its financial schedules 5

based on the updated Load Forecast.2 6

Overall, actual domestic sales revenue in April and May 2019 was lower than 7

forecast due to warm weather, reduced use per account and lower consumption 8

at the step two rate, which resulted in lower residential revenue. Large industrial 9

revenue was also lower due to delayed commercial operation dates for new 10

cryptocurrency customers and lower production in the oil and gas sector 11

because of poor market conditions. 12

As discussed in section 1.2, BC Hydro’s planned market electricity purchases 13

have increased for fiscal 2020 and fiscal 2021. As actual sales in April and 14

May 2019 were lower than forecast, BC Hydro’s market electricity purchases 15

were also lower than they otherwise would have been; and 16

Updates the Demand-Side Management Expenditure Schedule: In the 17

Application, BC Hydro requested BCUC approval of a Demand-Side 18

Management (DSM) expenditure schedule of $90.8 million in fiscal 2020 and 19

$116.3 million in fiscal 2021. The Evidentiary Update reduces BC Hydro’s DSM 20

expenditure request by $27.2 million in fiscal 2021 from $116.3 million to 21

$89.1 million because two projects that BC Hydro expected to proceed under 22

the Thermo-Mechanical Pulp (TMP) Program did not submit applications by the 23

required deadline. As this update is limited to expenditures in fiscal 2021 which 24

2 In the June 24, 2019 Procedural Conference, BC Hydro stated that the impetus for filing the 20-year load

forecast in this proceeding was for information purposes only, in response to certain Round 1 information requests. The 20-year load forecast was not expected to update the test period itself. For further information, refer to page 209 to 210 of Transcript Volume 2.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020]

Page 5

are amortized into rates starting in fiscal 2022, it does not impact BC Hydro’s 1

revenue requirements in the test period. 2

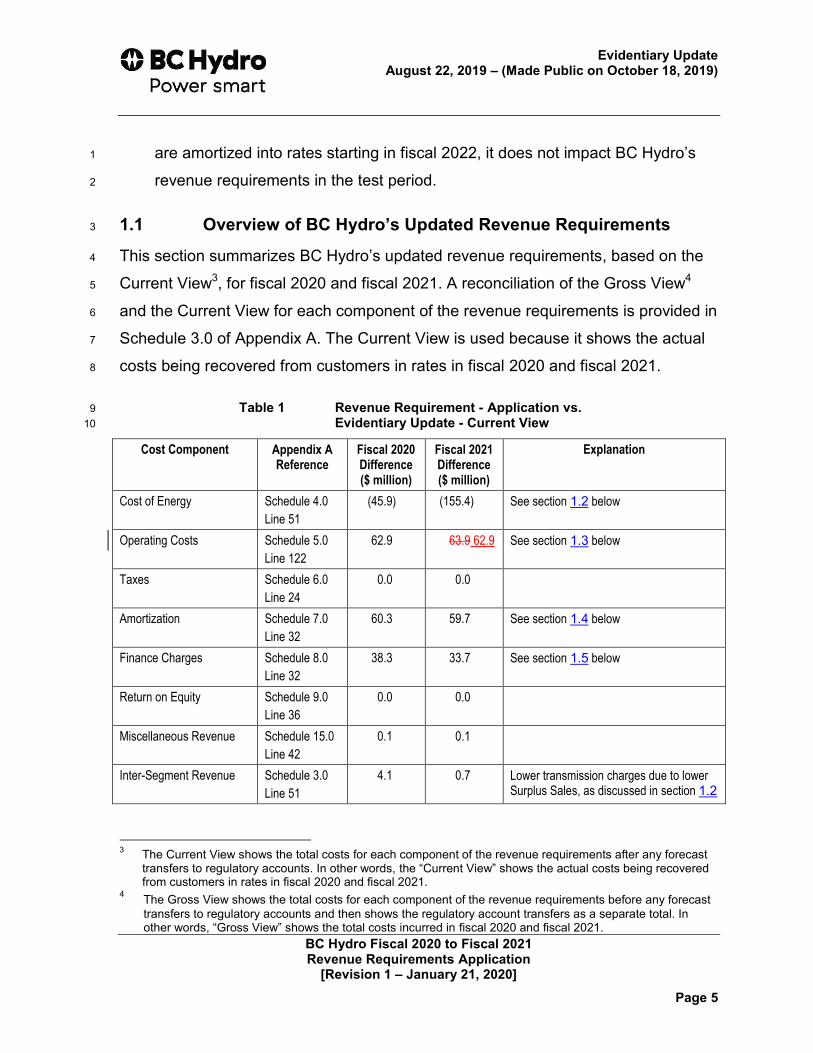

1.1 Overview of BC Hydro’s Updated Revenue Requirements 3

This section summarizes BC Hydro’s updated revenue requirements, based on the 4

Current View3, for fiscal 2020 and fiscal 2021. A reconciliation of the Gross View4 5

and the Current View for each component of the revenue requirements is provided in 6

Schedule 3.0 of Appendix A. The Current View is used because it shows the actual 7

costs being recovered from customers in rates in fiscal 2020 and fiscal 2021. 8

Table 1 Revenue Requirement - Application vs. 9 Evidentiary Update - Current View 10

Cost Component Appendix A Reference

Fiscal 2020 Difference ($ million)

Fiscal 2021 Difference ($ million)

Explanation

Cost of Energy Schedule 4.0

Line 51

(45.9) (155.4) See section 1.2 below

Operating Costs Schedule 5.0

Line 122

62.9 63.9 62.9 See section 1.3 below

Taxes Schedule 6.0

Line 24

0.0 0.0

Amortization Schedule 7.0

Line 32

60.3 59.7 See section 1.4 below

Finance Charges Schedule 8.0

Line 32

38.3 33.7 See section 1.5 below

Return on Equity Schedule 9.0

Line 36

0.0 0.0

Miscellaneous Revenue Schedule 15.0

Line 42

0.1 0.1

Inter-Segment Revenue Schedule 3.0

Line 51

4.1 0.7 Lower transmission charges due to lower Surplus Sales, as discussed in section 1.2

3 The Current View shows the total costs for each component of the revenue requirements after any forecast

transfers to regulatory accounts. In other words, the “Current View” shows the actual costs being recovered from customers in rates in fiscal 2020 and fiscal 2021.

4 The Gross View shows the total costs for each component of the revenue requirements before any forecast transfers to regulatory accounts and then shows the regulatory account transfers as a separate total. In other words, “Gross View” shows the total costs incurred in fiscal 2020 and fiscal 2021.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020]

Page 6

Cost Component Appendix A Reference

Fiscal 2020 Difference ($ million)

Fiscal 2021 Difference ($ million)

Explanation

Subsidiary Net Income Schedule 3.0

Lines 55/56

(151.6) (92.6) As discussed further in section 1.6 below, Subsidiary Net Income is higher in fiscal 2020 and fiscal 2021 because, in the Current View, the favourable difference between forecast and actual Powerex Net Income in fiscal 2019 is recovered in fiscal 2020 and fiscal 2021.

Other Utilities Revenue Schedule 14.0

Line 18

(0.2) 0.0

Liquefied Natural Gas Revenue

Schedule 14.0

Line 19

(0.6) 0.0

Deferral Account Rate Rider Revenue

Schedule 14.0

Line 21

0.0 0.0

Total Schedule 1.0 Line 35

(32.5) (89.9) (90.9) Numbers may not add due to rounding

122.4 123.4

The sub-sections below provide further details on the differences shown in the table 1

above. 2

Appendix A contains the detailed financial schedules reflecting our updated revenue 3

requirements. The working revenue requirements model that produces these 4

schedules is also provided in electronic form as part of the Evidentiary Update. 5

Appendix B contains a Draft Order that sets out our requests, as updated by the 6

Evidentiary Update. The following updates are reflected in this Draft Order: 7

A rate decrease of 0.99 1.01 per cent, effective April 1, 2020; 8

Updated Open Access Transmission Tariff Rates (OATT) for fiscal 2020 and 9

fiscal 2021; 10

Amortizing into rates, over the fiscal 2020 to fiscal 2021 test period, the 11

fiscal 2019 net closing balance and the forecast fiscal 2020 and fiscal 2021 net 12

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 7

additions and net interest applied to the Cost of Energy Variance Accounts, 1

such that fiscal 2020 rates remain the same.5 2

An updated Demand Side Management (DSM) expenditure schedule of 3

$90.8 million in fiscal 2020 and $89.1 million in fiscal 2021;6 and 4

Closure of the Arrow Water Systems Provision Regulatory Account and the 5

Arrow Water Systems Regulatory Account in fiscal 2020.7 6

Appendix C provides detailed information on BC Hydro’s updated Cost of Energy 7

forecast. 8

Appendix D provides BC Hydro’s updated regulatory account balances. 9

Appendix E provides BC Hydro’s updated Transmission Revenue Requirement and 10

OATT rates. 11

Appendix F provides a more detailed explanation of the difference between the 12

estimated impacts from the implementation of IFRS 16 in the Application and the 13

actual impacts shown in the Evidentiary Update. 14

Appendix G provides explanations for variances between fiscal 2019 RRA plan and 15

fiscal 2019 actual amounts. 16

1.2 Cost of Energy Has Decreased While Dry Conditions and 17

Lower IPP Purchases Have Increased Market Purchases 18

The Cost of Energy forecast in the Application was based on BC Hydro’s 19

October 2018 energy study. The Cost of Energy forecast in the Evidentiary Update 20

is based on the June 2019 energy study. 21

5 Refer to section 1.2 for further discussion. 6 Refer to BC Hydro’s response to BCUC IR 1.182.1. 7 Refer to BC Hydro’s response to BCUC IR 1.40.3.1.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 8

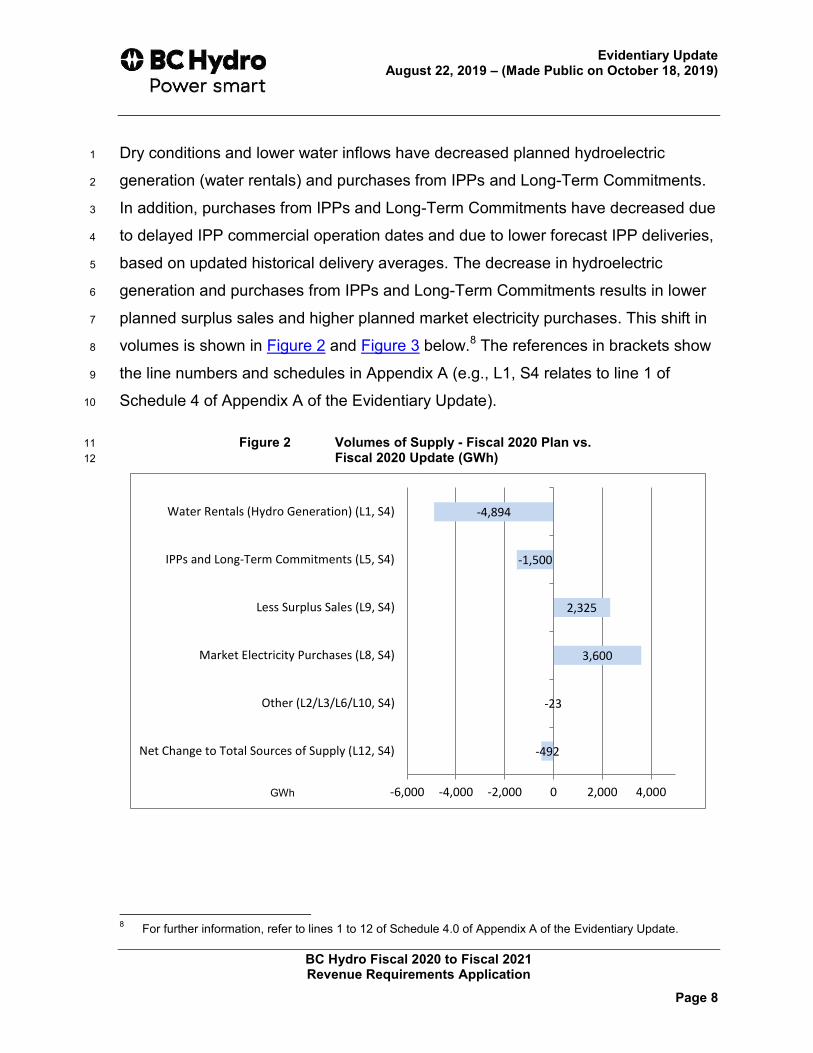

Dry conditions and lower water inflows have decreased planned hydroelectric 1

generation (water rentals) and purchases from IPPs and Long-Term Commitments. 2

In addition, purchases from IPPs and Long-Term Commitments have decreased due 3

to delayed IPP commercial operation dates and due to lower forecast IPP deliveries, 4

based on updated historical delivery averages. The decrease in hydroelectric 5

generation and purchases from IPPs and Long-Term Commitments results in lower 6

planned surplus sales and higher planned market electricity purchases. This shift in 7

volumes is shown in Figure 2 and Figure 3 below.8 The references in brackets show 8

the line numbers and schedules in Appendix A (e.g., L1, S4 relates to line 1 of 9

Schedule 4 of Appendix A of the Evidentiary Update). 10

Figure 2 Volumes of Supply - Fiscal 2020 Plan vs. 11 Fiscal 2020 Update (GWh) 12

8 For further information, refer to lines 1 to 12 of Schedule 4.0 of Appendix A of the Evidentiary Update.

-492

-23

3,600

2,325

-1,500

-4,894

Net Change to Total Sources of Supply (L12, S4)

Other (L2/L3/L6/L10, S4)

Market Electricity Purchases (L8, S4)

Less Surplus Sales (L9, S4)

IPPs and Long-Term Commitments (L5, S4)

Water Rentals (Hydro Generation) (L1, S4)

-6,000 -4,000 -2,000 0 2,000 4,000GWh

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 9

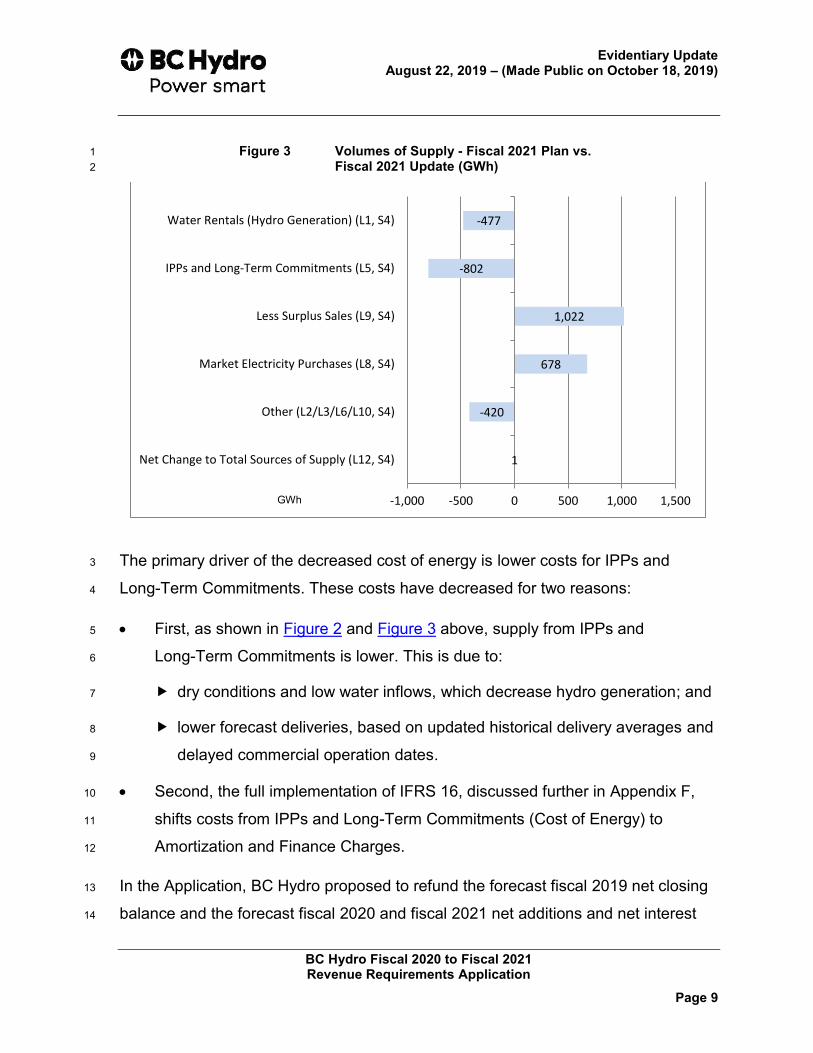

Figure 3 Volumes of Supply - Fiscal 2021 Plan vs. 1 Fiscal 2021 Update (GWh) 2

The primary driver of the decreased cost of energy is lower costs for IPPs and 3

Long-Term Commitments. These costs have decreased for two reasons: 4

First, as shown in Figure 2 and Figure 3 above, supply from IPPs and 5

Long-Term Commitments is lower. This is due to: 6

dry conditions and low water inflows, which decrease hydro generation; and 7

lower forecast deliveries, based on updated historical delivery averages and 8

delayed commercial operation dates. 9

Second, the full implementation of IFRS 16, discussed further in Appendix F, 10

shifts costs from IPPs and Long-Term Commitments (Cost of Energy) to 11

Amortization and Finance Charges. 12

In the Application, BC Hydro proposed to refund the forecast fiscal 2019 net closing 13

balance and the forecast fiscal 2020 and fiscal 2021 net additions and net interest 14

1

-420

678

1,022

-802

-477

-1,000 -500 0 500 1,000 1,500

Net Change to Total Sources of Supply (L12, S4)

Other (L2/L3/L6/L10, S4)

Market Electricity Purchases (L8, S4)

Less Surplus Sales (L9, S4)

IPPs and Long-Term Commitments (L5, S4)

Water Rentals (Hydro Generation) (L1, S4)

GWh

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 10

applied to the Cost of Energy Variance Accounts, over the fiscal 2020 to fiscal 2021 1

test period with equal amounts being amortized in fiscal 2020 and fiscal 2021. In the 2

Evidentiary Update, BC Hydro is proposing to amortize a higher amount of the credit 3

balance in the Cost of Energy Variance accounts in fiscal 2020 and a lower amount 4

in fiscal 2021. The result is that BC Hydro’s requested rate increase for fiscal 2020 5

remains unchanged, avoiding the need for a retrospective adjustment to fiscal 2020 6

interim rates and customer bills. 7

As a result of this proposal and the difference between forecast and actual fiscal 8

2019 closing account balances, net recoveries from the Heritage Deferral Account 9

and Non-Heritage Deferral Account are higher than planned in fiscal 2020 and lower 10

than planned in fiscal 2021. 11

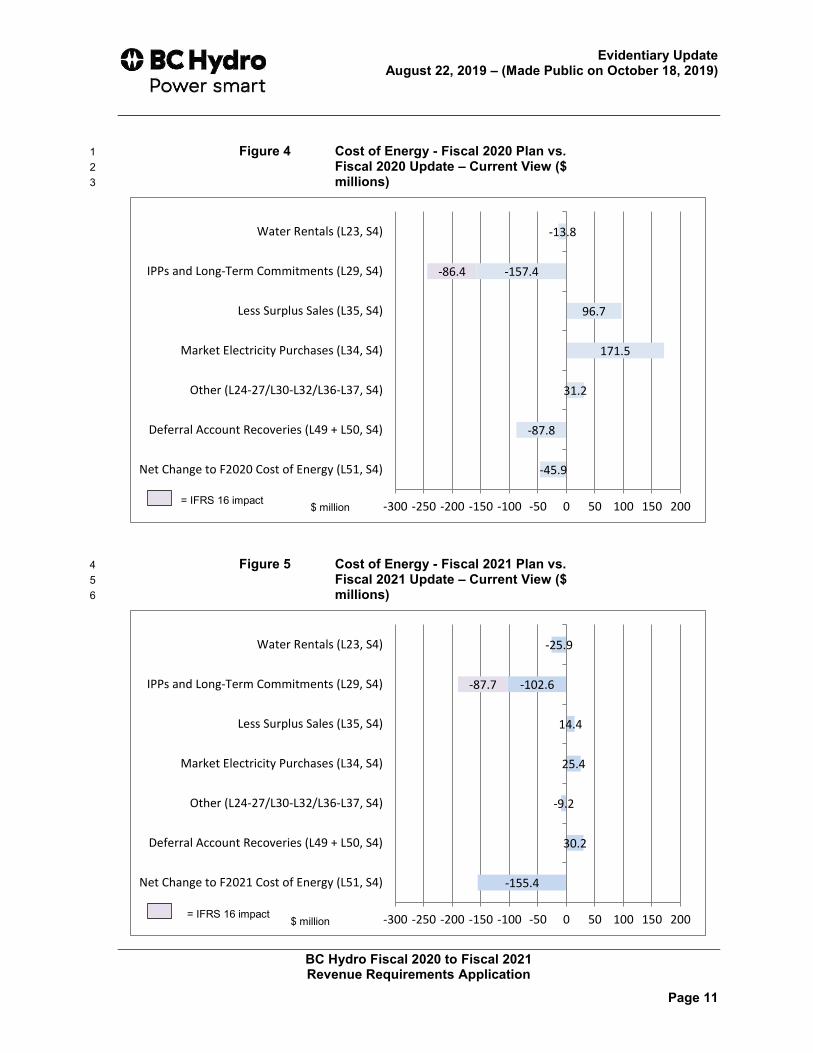

The increases and decreases to the components of the Cost of Energy in fiscal 2020 12

and fiscal 2021 are shown in Figure 4 and Figure 5 below.9 13

9 For further information, refer to lines 23 to 39 of Schedule 4.0 of Appendix A of the Evidentiary Update.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 11

Figure 4 Cost of Energy - Fiscal 2020 Plan vs. 1 Fiscal 2020 Update – Current View ($ 2 millions) 3

Figure 5 Cost of Energy - Fiscal 2021 Plan vs. 4 Fiscal 2021 Update – Current View ($ 5 millions) 6

-45.9

-87.8

31.2

171.5

96.7

-157.4

-13.8

-86.4

-300 -250 -200 -150 -100 -50 0 50 100 150 200

Net Change to F2020 Cost of Energy (L51, S4)

Deferral Account Recoveries (L49 + L50, S4)

Other (L24-27/L30-L32/L36-L37, S4)

Market Electricity Purchases (L34, S4)

Less Surplus Sales (L35, S4)

IPPs and Long-Term Commitments (L29, S4)

Water Rentals (L23, S4)

-155.4

30.2

-9.2

25.4

14.4

-102.6

-25.9

-87.7

-300 -250 -200 -150 -100 -50 0 50 100 150 200

Net Change to F2021 Cost of Energy (L51, S4)

Deferral Account Recoveries (L49 + L50, S4)

Other (L24-27/L30-L32/L36-L37, S4)

Market Electricity Purchases (L34, S4)

Less Surplus Sales (L35, S4)

IPPs and Long-Term Commitments (L29, S4)

Water Rentals (L23, S4)

= IFRS 16 impact $ million

= IFRS 16 impact $ million

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020]

Page 12

For more detailed information on BC Hydro’s updated Cost of Energy forecast, 1

please refer to Appendix C. 2

1.3 Operating Costs Have Increased Due to Uncontrollable 3

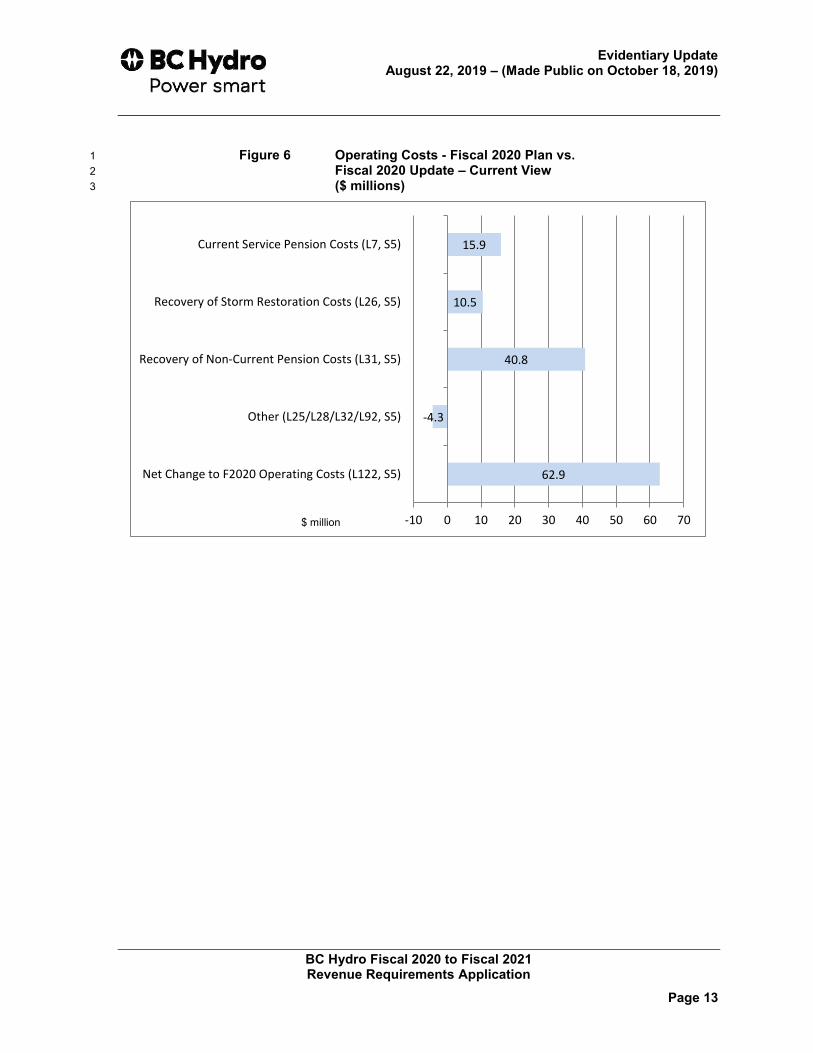

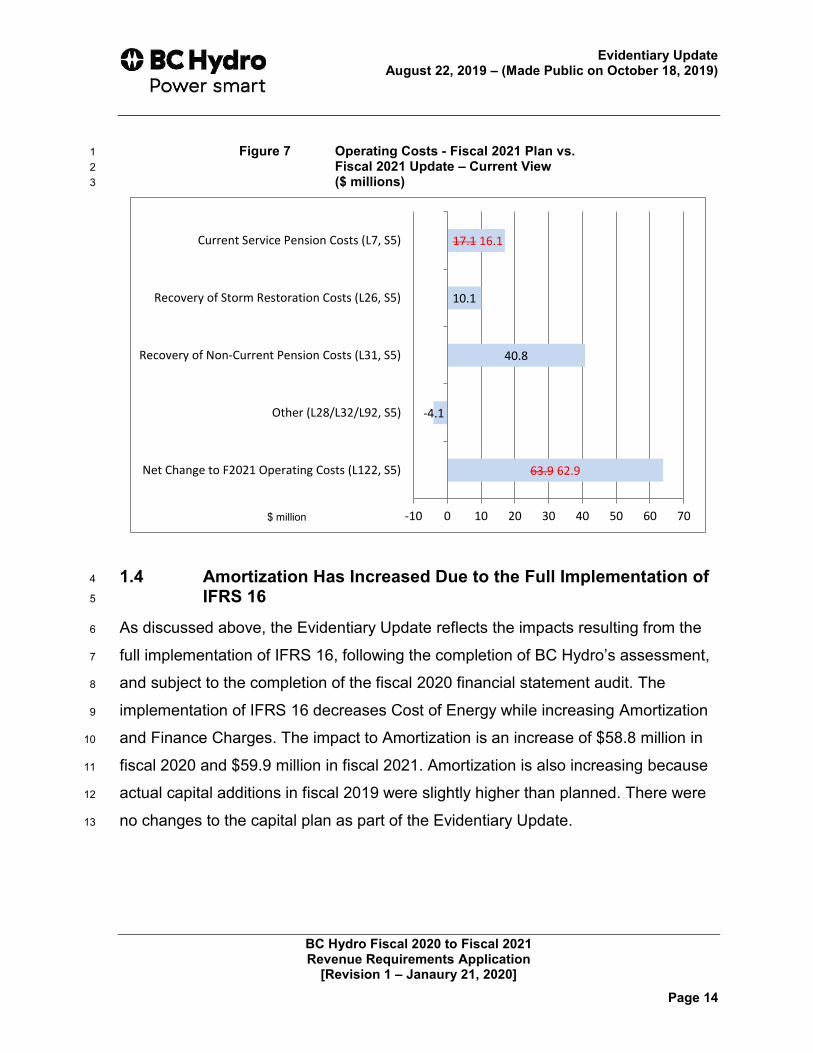

Factors 4

Operating costs have increased due to two factors that are outside of BC Hydro’s 5

control: 6

First, the discount rate used to value BC Hydro’s pension liability has 7

decreased from 3.83 per cent as of September 30, 2018 to 3.33 per cent as of 8

April 1, 2019. The discount rate is driven by market conditions and is 9

determined by BC Hydro’s external actuary. It is not controllable by BC Hydro 10

as it is based on ‘AA’ Canadian Corporate bonds. A decrease in the discount 11

rate results in a higher present value of BC Hydro’s pension liability. This 12

increases BC Hydro’s current service pension costs by $15.9 million in 13

fiscal 2020 and $17.1 16.1 million in fiscal 2021. 14

The lower discount rate also increased BC Hydro’s fiscal 2019 non-current 15

pension costs. This increase is deferred to the Non-Current Pension Cost 16

Regulatory Account and amortized into rates over a 13-year period, which 17

increases the required recovery by $40.8 million in both fiscal 2020 and 18

fiscal 2021. 19

Second, storm restoration costs were higher than planned in fiscal 2019 due to 20

more severe storms, including the December 2019 storm. These costs were 21

deferred to the Storm Restoration Costs Regulatory Account and are amortized 22

over the test period, which increases the required recovery in fiscal 2020 and 23

fiscal 2021. 24

These cost increases are summarized in Figure 6 and Figure 7 below.1025

10 For further information, refer to lines 1 to 122 of Schedule 5.0 of Appendix A of the Evidentiary Update.

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 13

Figure 6 Operating Costs - Fiscal 2020 Plan vs. 1 Fiscal 2020 Update – Current View 2 ($ millions) 3

62.9

-4.3

40.8

10.5

15.9

-10 0 10 20 30 40 50 60 70

Net Change to F2020 Operating Costs (L122, S5)

Other (L25/L28/L32/L92, S5)

Recovery of Non-Current Pension Costs (L31, S5)

Recovery of Storm Restoration Costs (L26, S5)

Current Service Pension Costs (L7, S5)

$ million

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – Janaury 21, 2020]

Page 14

Figure 7 Operating Costs - Fiscal 2021 Plan vs. 1 Fiscal 2021 Update – Current View 2 ($ millions) 3

1.4 Amortization Has Increased Due to the Full Implementation of 4

IFRS 16 5

As discussed above, the Evidentiary Update reflects the impacts resulting from the 6

full implementation of IFRS 16, following the completion of BC Hydro’s assessment, 7

and subject to the completion of the fiscal 2020 financial statement audit. The 8

implementation of IFRS 16 decreases Cost of Energy while increasing Amortization 9

and Finance Charges. The impact to Amortization is an increase of $58.8 million in 10

fiscal 2020 and $59.9 million in fiscal 2021. Amortization is also increasing because 11

actual capital additions in fiscal 2019 were slightly higher than planned. There were 12

no changes to the capital plan as part of the Evidentiary Update. 13

63.9 62.9

-4.1

40.8

10.1

17.1 16.1

-10 0 10 20 30 40 50 60 70

Net Change to F2021 Operating Costs (L122, S5)

Other (L28/L32/L92, S5)

Recovery of Non-Current Pension Costs (L31, S5)

Recovery of Storm Restoration Costs (L26, S5)

Current Service Pension Costs (L7, S5)

$ million

Evidentiary Update August 22, 2019 – (Made Public on October 18, 2019)

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Page 15

1.5 Finance Charges Have Increased Due to the Full 1

Implementation of IFRS 16 2

Finance Charges are also increasing due to the impacts resulting from the full 3

implementation of IFRS 16. The resulting impact to Finance Charges is an increase 4

of $44.3 million in fiscal 2020 and $43.3 million in fiscal 2021. This increase is 5

partially offset by lower finance charges on debt that was hedged subsequent to the 6

filing of the Application, at interest rates that were lower than forecast in the 7

Application. 8

1.6 Actual Fiscal 2019 Powerex Net Income Was Higher Than 9

Planned 10

In the Application, Powerex Net Income was forecast to be $205.3 million in 11

fiscal 2019. Actual Powerex Net Income in fiscal 2019 was $435.7 million or 12

$230.4 million higher than the forecast. This difference increases the credit balance 13

in the Cost of Energy Variance Accounts, which BC Hydro has proposed to refund to 14

ratepayers over the test period. In the Current View, this refund is reflected in 15

BC Hydro’s revenue requirements as Subsidiary Net Income. As a result, Subsidiary 16

Net Income is $151.6 million higher in fiscal 2020 and $92.6 million higher in 17

fiscal 2021, which decreases BC Hydro’s revenue requirements.11 18

11 The total increase in refunds in fiscal 2020 and fiscal 2021 is greater than the difference between forecast

and actual Powerex Net Income in fiscal 2019, primarily due to variances in interest accrual amounts on the balance in the Trade Income Deferral Account. The refund amount is higher in fiscal 2020 than fiscal 2021 so that BC Hydro’s requested rate increase in fiscal 2020 remains unchanged. For further information, refer to section 1.2 above.

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Appendix A

Financial Schedules

REFER TO LIVE SPREADSHEET MODEL

Provided in electronic format only

(Accessible by opening the Attachments Tab in Adobe)

CONFIDENTIAL - FOR BCUC ONLY Appendix A

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

Appendix E

Updated Transmission Revenue Requirement

Evidentiary Update August 22, 2019 - (Made Public on October 18, 2019)

Appendix E Updated Transmission Revenue Requirement

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020] Page 1

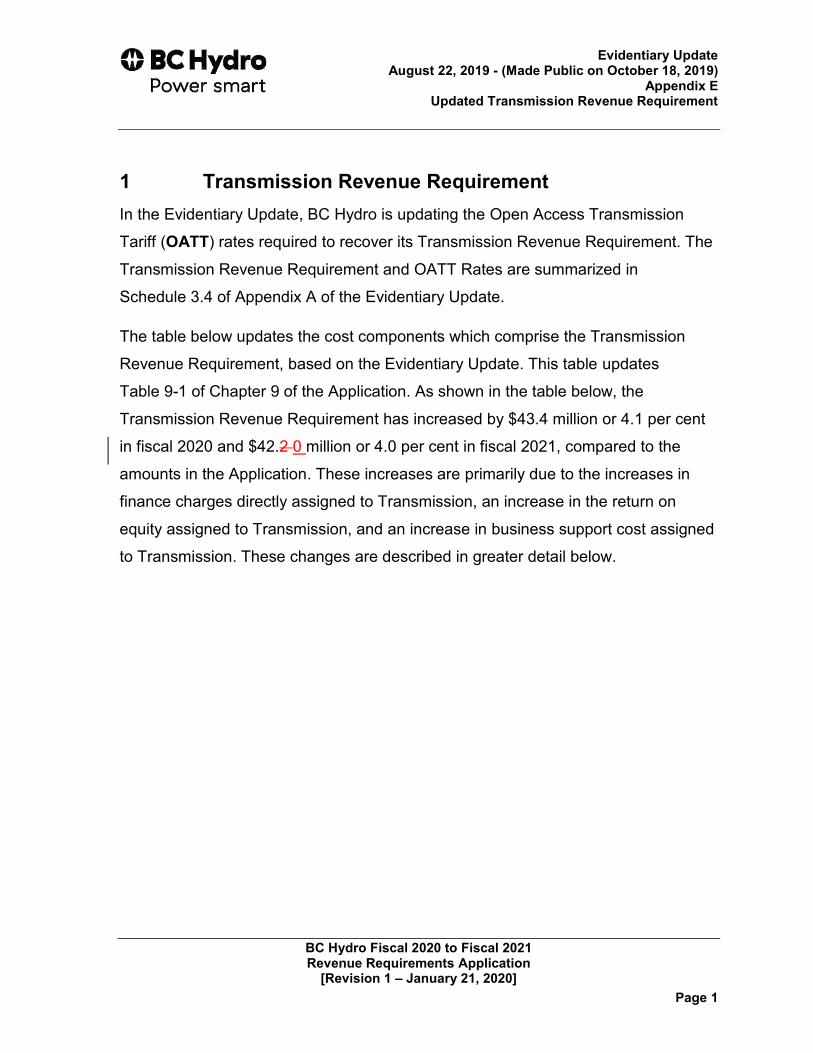

1 Transmission Revenue Requirement In the Evidentiary Update, BC Hydro is updating the Open Access Transmission

Tariff (OATT) rates required to recover its Transmission Revenue Requirement. The

Transmission Revenue Requirement and OATT Rates are summarized in

Schedule 3.4 of Appendix A of the Evidentiary Update.

The table below updates the cost components which comprise the Transmission

Revenue Requirement, based on the Evidentiary Update. This table updates

Table 9-1 of Chapter 9 of the Application. As shown in the table below, the

Transmission Revenue Requirement has increased by $43.4 million or 4.1 per cent

in fiscal 2020 and $42.2 0 million or 4.0 per cent in fiscal 2021, compared to the

amounts in the Application. These increases are primarily due to the increases in

finance charges directly assigned to Transmission, an increase in the return on

equity assigned to Transmission, and an increase in business support cost assigned

to Transmission. These changes are described in greater detail below.

Evidentiary Update August 22, 2019 - (Made Public on October 18, 2019)

Appendix E Updated Transmission Revenue Requirement

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020] Page 2

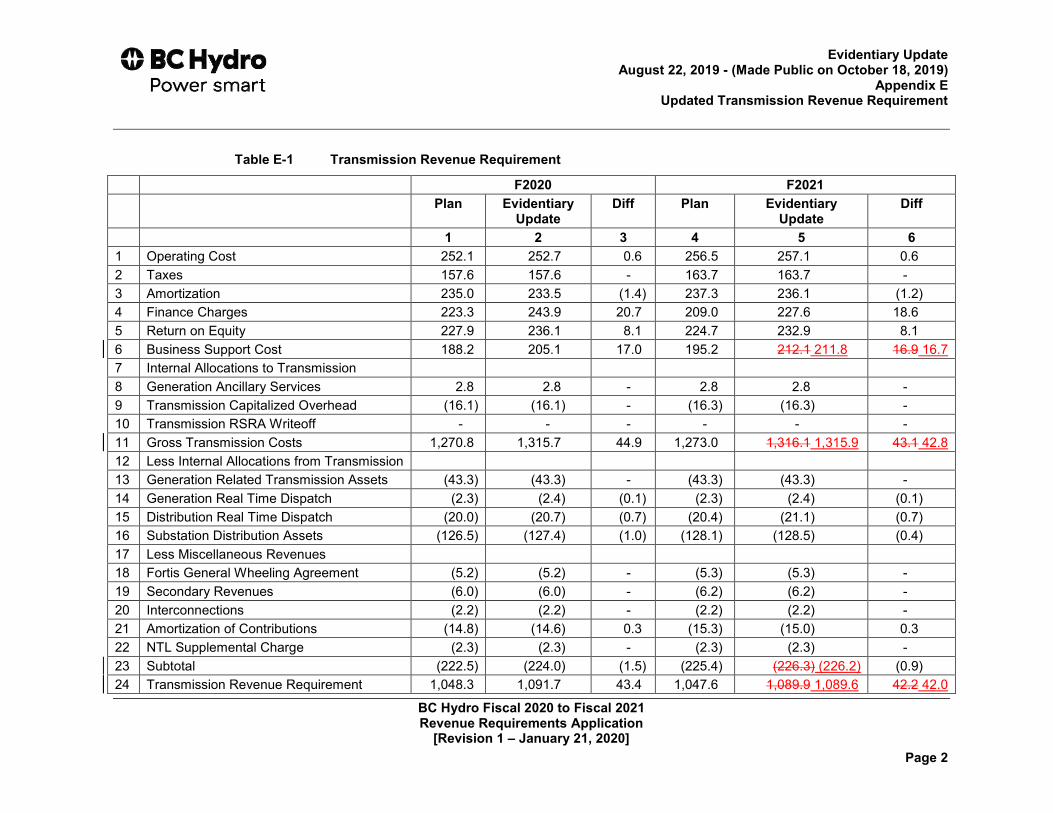

Table E-1 Transmission Revenue Requirement

F2020 F2021 Plan Evidentiary

Update Diff Plan Evidentiary

Update Diff

1 2 3 4 5 6 1 Operating Cost 252.1 252.7 0.6 256.5 257.1 0.6 2 Taxes 157.6 157.6 - 163.7 163.7 - 3 Amortization 235.0 233.5 (1.4) 237.3 236.1 (1.2) 4 Finance Charges 223.3 243.9 20.7 209.0 227.6 18.6 5 Return on Equity 227.9 236.1 8.1 224.7 232.9 8.1 6 Business Support Cost 188.2 205.1 17.0 195.2 212.1 211.8 16.9 16.7 7 Internal Allocations to Transmission 8 Generation Ancillary Services 2.8 2.8 - 2.8 2.8 - 9 Transmission Capitalized Overhead (16.1) (16.1) - (16.3) (16.3) - 10 Transmission RSRA Writeoff - - - - - - 11 Gross Transmission Costs 1,270.8 1,315.7 44.9 1,273.0 1,316.1 1,315.9 43.1 42.8 12 Less Internal Allocations from Transmission 13 Generation Related Transmission Assets (43.3) (43.3) - (43.3) (43.3) - 14 Generation Real Time Dispatch (2.3) (2.4) (0.1) (2.3) (2.4) (0.1) 15 Distribution Real Time Dispatch (20.0) (20.7) (0.7) (20.4) (21.1) (0.7) 16 Substation Distribution Assets (126.5) (127.4) (1.0) (128.1) (128.5) (0.4) 17 Less Miscellaneous Revenues 18 Fortis General Wheeling Agreement (5.2) (5.2) - (5.3) (5.3) - 19 Secondary Revenues (6.0) (6.0) - (6.2) (6.2) - 20 Interconnections (2.2) (2.2) - (2.2) (2.2) - 21 Amortization of Contributions (14.8) (14.6) 0.3 (15.3) (15.0) 0.3 22 NTL Supplemental Charge (2.3) (2.3) - (2.3) (2.3) - 23 Subtotal (222.5) (224.0) (1.5) (225.4) (226.3) (226.2) (0.9) 24 Transmission Revenue Requirement 1,048.3 1,091.7 43.4 1,047.6 1,089.9 1,089.6 42.2 42.0

Evidentiary Update August 22, 2019 - (Made Public on October 18, 2019)

Appendix E Updated Transmission Revenue Requirement

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020] Page 3

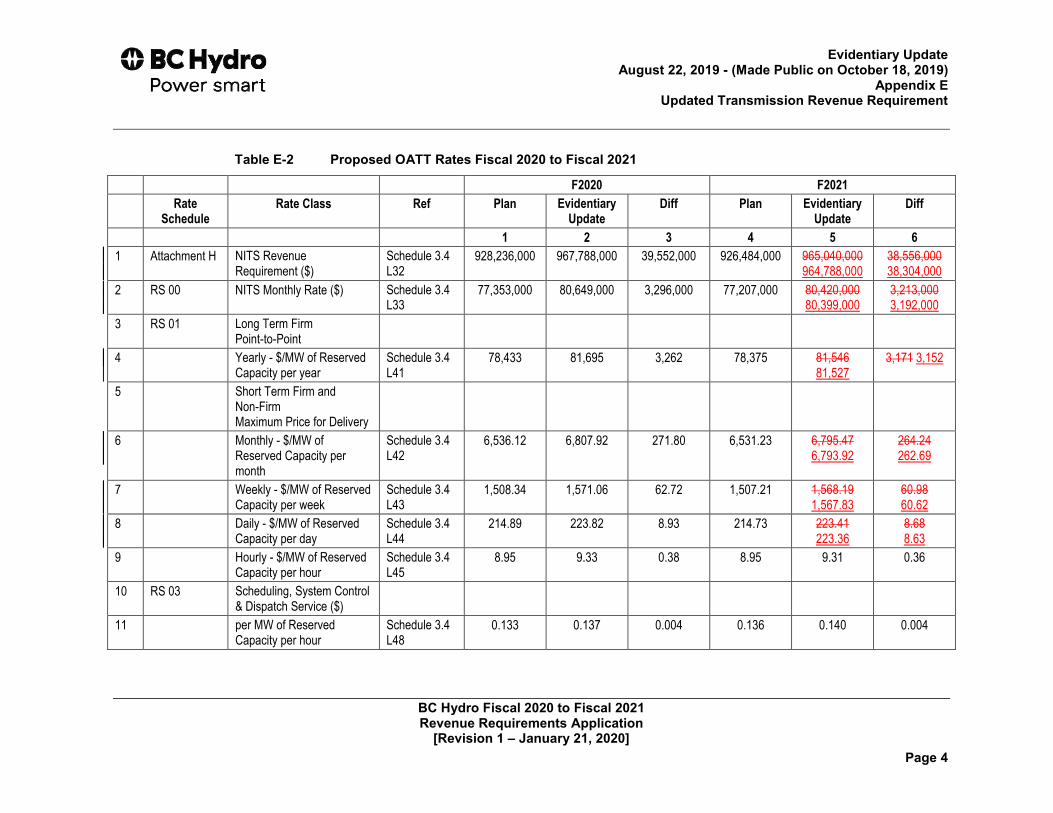

As shown on line 38 of Schedule 8.0 of Appendix A, the finance charges allocated to

Transmission increased by $20.7 million in fiscal 2020 and $18.6 million in

fiscal 2021. This increase is due to an overall increase in finance charges (see

section 1.5 of the Evidentiary Update) as well as an increase to the proportion of

finance charges assigned to Transmission. Finance charges are allocated based on

a rate base. As shown on line 34 of Schedule 8.0 of Appendix A, the proportion of

Rate Base allocated to Transmission increased by 1.1 per cent in both fiscal 2020

and fiscal 2021. This increase results from a reclassification of the Altagas

contribution to the Northwest Transmission Line due to transition to IFRS.

Contributions to aid in the construction of the Transmission system have been

reclassified from Transmission contribution in aid of construction to other non-current

liabilities and accounts payable for the current portion.

As shown on line 42 of Schedule 9.0 of Appendix A of the Evidentiary Update, the

increase to the proportion of Rate Base allocated to Transmission also results in an

increase to return on equity allocated to Transmission of $8.1 million in both

fiscal 2020 and fiscal 2021.

As shown on line 45 of Schedule 3.1 of Appendix A, Business Support costs

allocated to transmission have increased by $17.0 million in fiscal 2020 and

$16.9 7 million in fiscal 2021. This is primarily due to increases in current pension

service costs (see section 1.3 of the Evidentiary Update) and higher recoveries from

the Non-Current Pension Costs Regulatory Account (see Appendix D).

The table below provides BC Hydro’s updated proposed OATT Rates, based on the

updated Transmission Revenue Requirement. This table updates Table 9-8 of

Chapter 9 of the Application.

Evidentiary Update August 22, 2019 - (Made Public on October 18, 2019)

Appendix E Updated Transmission Revenue Requirement

BC Hydro Fiscal 2020 to Fiscal 2021 Revenue Requirements Application

[Revision 1 – January 21, 2020] Page 4

Table E-2 Proposed OATT Rates Fiscal 2020 to Fiscal 2021

F2020 F2021

Rate Schedule

Rate Class Ref Plan Evidentiary Update

Diff Plan Evidentiary Update

Diff

1 2 3 4 5 6

1 Attachment H NITS Revenue Requirement ($)

Schedule 3.4 L32

928,236,000 967,788,000 39,552,000 926,484,000 965,040,000 964,788,000

38,556,000 38,304,000

2 RS 00 NITS Monthly Rate ($) Schedule 3.4 L33

77,353,000 80,649,000 3,296,000 77,207,000 80,420,000 80,399,000

3,213,000 3,192,000

3 RS 01 Long Term Firm Point-to-Point

4 Yearly - $/MW of Reserved Capacity per year

Schedule 3.4 L41

78,433 81,695 3,262 78,375 81,546 81,527

3,171 3,152

5 Short Term Firm and Non-Firm Maximum Price for Delivery

6 Monthly - $/MW of Reserved Capacity per month

Schedule 3.4 L42

6,536.12 6,807.92 271.80 6,531.23 6,795.47 6,793.92

264.24 262.69

7 Weekly - $/MW of Reserved Capacity per week

Schedule 3.4 L43

1,508.34 1,571.06 62.72 1,507.21 1,568.19 1,567.83

60.98 60.62

8 Daily - $/MW of Reserved Capacity per day

Schedule 3.4 L44

214.89 223.82 8.93 214.73 223.41 223.36

8.68 8.63

9 Hourly - $/MW of Reserved Capacity per hour

Schedule 3.4 L45

8.95 9.33 0.38 8.95 9.31 0.36

10 RS 03 Scheduling, System Control & Dispatch Service ($)

11 per MW of Reserved Capacity per hour

Schedule 3.4 L48

0.133 0.137 0.004 0.136 0.140 0.004