Embed Size (px)

DESCRIPTION

Chris Easingwood, Steven Moxey, and Henry Capleton

Citation preview

Bringing High Technology to Market:

Successful Strategies Employed in the

Worldwide Software Industry

Chris Easingwood, Steven Moxey, and Henry Capleton

The launch stage can be critical for many new products, but particularly so for

technology-intensive ones. This study examines this key stage in a high-tech sector:

the worldwide computer software industry. Using a research instrument developed

across a number of high-tech sectors, but adapted to the targeted sector, it describes

a worldwide telephone-based survey of 300 organizations, resulting in 190 inter-

views, a response rate of 63%. It shows that five distinct and interpretable strategies

are employed: (1) alliance strategy involves forming early strategic alliances as

well as tactical alliances at the execution stage together with the development of

unique distribution channels; (2) targeted low risk attempts to reduce the risk of

adoption among identified segments by producing versions of the product specifi-

cally customized to the segments; (3) low-price original equipment manufacturer

(OEM) is the only price-driven strategy and combines low price with channel

building to OEMs who are looking for attractive price-to-performance ratios; (4)

broadly based market preparation is an early-stage strategy that concentrates on

educating the market vis-a-vis the technology and developing channels; and (5)

niche-based technological superiority uses a technologically superior product to

dominate a niche and corresponds closely to the chasm-crossing strategy expounded

by Moore and others. Regarding superior product performance, successful software

companies first of all engage in a broadly based preparation of the market but

switch to a targeted strategy at the following stages of positioning and execution,

built around superior technological performance and reduced risk. A somewhat dif-

ferent mix of strategies is adopted when the objective is superior market develop-

ment, namely opening up new markets, reaching new customers, and developing new

product platforms. Again the mix includes broadly based market preparation, this

time along with alliances. This strategy is very much about working with partners.

The broadly based market preparation strategy is key for both objectives, is long

term in nature, and avoids narrowly defined niches. It seems that starting broad

based and narrowing down, perhaps to a niche, only at a later stage when this is

clearly the appropriate thing to do, pays dividends.

Introduction

Innovation is an important determinant of wealth

creation and economic growth. Yet innovation

in the form of new products and services is for

naught unless the new products can be brought to

Address correspondence to: Chris Easingwood, Manchester Schoolof Business, Manchester M15 6PB, England. Tel.: þ 44 (0) (161) 275-6482. E-mail: [email protected].

J PROD INNOV MANAG 2006;23:498–511r 2006 Product Development & Management Association

market and successfully overcome the inevitable

hurdles to change and adoption that exist (Kim and

Mauborgne, 2000; McDonald, Corkindale, and

Sharp, 2003). That being so, the launch stage is a

critical step in this wealth creation process that begins

with the generation of an idea for a new product

and ends with commercial success. This article looks

at the launch of technology-intensive products and

identifies some successful launch strategies.

Literature

The subject of product launch probably has its origins in

the work of Cooper (1975, 1979, 1980), Cooper and

Kleinschmidt (1986), and Cooper and de Brentani

(1991) on the new product development process, in

which launch sometimes featured as one of many var-

iables, from idea generation to concept development to

firm synergy, that were included in increasingly compre-

hensive and detailed surveys to uncover the drivers of

new product success (see Montoya-Weiss and Calan-

tone, 1994 for a meta-analysis). In fact, launch was

identified early on as one of the most important drivers,

probably contributing to it becoming a separate subject

for study. Although a few years ago the literature on

new product launch might have been said to be relatively

sparse (Green et al., 1997), that is not the case now, with

the subject currently growing apace with some influen-

tial contributions (see particularly Debruyne et al., 2002;

Hultink and Hart, 1998; Hultink et al., 1997, 2000;

Langerak, Hultink, and Robben, 2004).

However, though this general increase in activity is

clear, this is not the case for the launch of technology-

intensive products (Easingwood and Harrington,

2002). Yet the launch stage for high-tech products is

likely to be especially critical. Many high-tech markets

are characterized by a winner take most mode, and the

eventual winner may not necessarily be the best prod-

uct but the one that establishes an early lead (Arthur,

1996; Schilling, 1998). Furthermore, the window of

opportunity in technology-intensive markets is likely to

be narrow as newer technology may be waiting in the

wings even as the new technology gets its one chance to

establish itself (Mohr, 2000). Fluff that chance, and

there may not be another (Easingwood and Koustelos,

2000). Rewards accrue to those who are first to see the

shape of the next emerging technological play (Arthur,

1996), such as eBay, the Internet auction site. The

present article looks at the launch of technology-inten-

sive products, choosing the computer software envi-

ronment for its empirical testing.

Few attempts have been made to take an overview

of the subject of the new product launch, partly be-

cause research into launch is scattered and partly

because it may be just one of many factors examined.

An exception is Hultink et al.’s (2000) comprehensive

examination of strategic and tactical launch variables

in both consumer and industrial markets.

Sometimes the launch event is examined more from

the perspective of the incumbent attempting to ward off

the new product than from that of the company intro-

ducing the new product (see Cespedes, 1994; Kuester,

Homburg, and Robertson, 1999). Defending companies

take actions in an attempt to protect their own position

and to reduce the new product’s impact. A few articles

manage to look at both innovator actions and incum-

bent responses (e.g., Debruyne et al., 2002; Schilling,

2003). For instance, the incumbent’s reaction to the

changed situation is dependent on the characteristics of

the new product launch (Debruyne et al., 2002).

Opinions have not been consistent regarding which

variables belong in the launch stage (Hultink and

Hart, 1998), but a common approach is to examine

the strategies a company employs using a framework

based on the marketing mix. Thus, advertising spend

may be increased, price may be reduced, or a product

may be modified (Hauser and Shugan, 1984). For in-

stance, in fast-moving consumer markets, incumbents

with nondominant share should on average reduce

BIOGRAPHICAL SKETCHES

Dr. Chris Easingwood is professor of marketing at Manchester

Business School and head of marketing and strategy. He has a

Ph.D. from the Wharton Business School and is an active researcher

in a number of areas including services marketing, financial services

marketing, marketing of technology, new product development and

product marketing. He has published more than 80 articles appear-

ing in leading international journals such as Marketing Science, In-

ternational Journal of Research in Marketing, Journal of Business

Research, Journal of Product Innovation Management, and Business

Horizons.

Dr. Steven Moxey has a Ph.D. from Oxford University and has held

senior marketing positions in technology companies including Ca-

ble & Wireless and IBM Software, where he was responsible for the

marketing management profession. Dr. Moxey has extensive expe-

rience of product development and marketing launch strategies for

global software products. He is currently managing director of Se-

rrula Ltd., a technology research and consultancy company with

research specialization in technology marketing for the telecommu-

nications and information technology industries.

Henry Capleton is an experienced marketing manager from the

software industry with international experience in Europe and the

United States. He was formerly a marketing planning manager for

IBM Software and is now a consultant with research interests in

market planning, software product development, and channels.

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

499

price and advertising support, whereas those with

dominant shares should also reduce price but should

increase advertising support (Gruca, Kumar, and

Sudharshan, 1992).

Marketing mix-based approaches can be helpful, and

managers do at one level make adjustments to the com-

ponents of the marketing mix, but ‘‘in the case of a

highly innovative new product, an analysis of the mar-

keting mix adaptations may provide too narrow a per-

spective’’ (Debruyne et al., 2002, p. 168). Some studies

examine the effect of variables that represent the com-

bined effect of a number of factors in summarized form,

such as the magnitude of marketing investment or com-

petitive advantage (e.g., Green and Ryans, 1990). Use-

ful as these studies undoubtedly are, it is also useful to

take the level of analysis down to consideration of the

actions and tactics that managers actually use.

An example is the market preparation/targeting/

positioning/execution framework of Easingwood and

Koustelos (2000), which is based on interpretation of

qualitative work carried out with high-tech marketing

and product managers. The launch program is divided

into stages: (1) market preparation, in which markets

are readied for the product’s arrival; (2) targeting, in

which promising sectors are identified; (3) positioning

to achieve competitive advantage; and (4) execution,

in which the market is attacked and includes direct

actions to build sales.

Activities undertaken in the first three stages are

mostly strategic, in the sense that they involve high

commitments of resources, take some time to work

through, and are difficult to reverse (Debruyne et al.,

2002). They are also strategic in the sense that they

largely occur prior to launch (Hultink et al., 2000).

Activities undertaken in the final execution stage are

mostly tactical in that they belong to the product’s

commercialization stage and can be modified at a later

stage in the product’s launch (Hultink et al., 1997).

High technology is no longer confined to the tra-

ditional sectors of computer hardware and software,

telecommunications, and consumer electronics but

has invaded many other sectors that rely on technol-

ogy to enable them to deliver improved customer so-

lutions, for instance service industries (Mohr and

Shooshtari, 2003).

Purpose

The present article examines the launch event in a

high-tech environment from the perspective of the

company introducing the new product and attempting

to secure good performance. It studies the use and

effect of a number of tactics employed to launch the

new product. It attempts to understand which tactics

are natural bedfellows. In other words, which tactics,

when used together, can be expected to complement

and support one another? In addition, this article

looks at the relationship, if any, between the mix of

tactics employed and the resulting performance.

In summary there are three main objectives: (1) to

investigate whether any particular combinations of

launch tactics are frequently employed; (2) to examine

the launch tactics to see if they reinforce one another,

forming strategies with coherent aims—in other

words, to identify clearly definable combinations of

tactics, called strategies; and (3) to identify strategies

associated with enhanced performance.

Implicit in this is an examination of the extent to

which the stages build or do not build on one another.

Thus, a secondary objective is to examine the strate-

gies that emerge to see whether they are formed from

tactics from all stages or whether the stages them-

selves form the strategies. In the present authors’ ex-

perience, mangers think in terms of the stages, so it is

useful to see if the strategies actually employed con-

form to this perspective.

Companies in the process of bringing new techno-

logy to market may have invested considerable re-

sources and time in doing so (Urban and Hauser,

1993); in addition, more just than the financial returns

from that single product may be riding on the out-

come. Every new product launch by a high-tech

company has the potential to consolidate or under-

mine its reputation for leading-edge work depending

on the success enjoyed. For instance, high-tech

companies need the ongoing support of their chan-

nels of distribution to support their products and

services and to present them effectively to end users.

Successful launches can increase the levels of support

from the channels, and unsuccessful launches can

do the opposite. In such cases getting the launch

stage right can assume major importance. Deriving

a better understanding of the launch strategies that

work best would thus seem to be a worthwhile

objective.

Methodology

Development of the Research Instrument

Based on many discussions with practitioners in

technology-based markets, it was concluded that

500 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

managers in technology-based markets think in terms

of actions taken (e.g., circulating information in ad-

vance, supplying original equipment manufacturers

[OEMs], communicating technological advantages,

reducing the risk of adoption, running trial programs,

working effectively with channel partners). These and

others form the bricks of high-tech product launches

from which the strategies are constructed. It is there-

fore sensible to examine the consequences of the ac-

tual actions employed. Thus, although others have

adopted the marketing mix with success when re-

searching the marketing of new products, a frame-

work that has been customized to the high-tech

marketplace would provide a useful perspective.

Such a framework already exists composed of a

number of launch tactics derived from grounded work

with marketing and product managers working in

several different high-technology sectors (see Easing-

wood and Koustelos, 2000) and has been successfully

employed across several high-tech sectors—eight

different sectors that include pharmaceuticals, com-

puters, automation, and telecommunications. This

framework was adopted, although it had first to be

adapted to the particular high-tech sector to be re-

searched—the worldwide computer software indus-

try—for a number of reasons: The framework had not

been subjected to a second scrutiny by high-tech man-

agers, needed to be updated given the speed with

which high-tech sectors evolve, and possibly needed

adapting from its general high-tech origins to the spe-

cific software sector to which it would be applied.

Eight managers from the sponsoring high-technol-

ogy company agreed to examine the research instru-

ment in detail, five face to face and three over the

telephone, which resulting in the following changes:

� Expansion/clarification: The precision of the ter-

minology used was improved in some statements.

For instance, the market preparation option ‘‘ed-

ucate the market’’ was rephrased as ‘‘educate the

market to understand new uses’’; the execution

option ‘‘concentrate on a particular application’’

was made clearer as ‘‘concentrate on a niche,’’

which also has the advantage of better expressing

the important ‘‘kingpin’’ strategy (Moore, 1998,

1999).

� Restatement: Some options were thought to be too

specific and were reexpressed more generally. For

instance, the market preparation option ‘‘coopera-

tion/licensing/alliances’’ was restated as ‘‘form stra-

tegic alliances.’’ Some phrasing lacked clarity, so,

for instance, the positioning option ‘‘emphasize a

safe bet’’ was reexpressed as ‘‘emphasize low risk.’’

� Combine stages: It was thought that the second

and third stages, targeting and positioning, be-

longed together. Planning the target segment and

the claimed position in that targeted segment are

normally thought through in one step. Thus, the

second and third stages were combined.

� Removal: Some statements, such as the targeting

options ‘‘target competitors,’’ ‘‘customers,’’ and

‘‘target conservatives,’’ were considered to be too

specialized for the targeted market and so were

dropped.

� Addition: Three new tactics were added. An often

used execution tactic in the software industry

known as versioning is to modify the product to

suit different segments, expressed as ‘‘offer differ-

ent versions targeted at different buyers,’’ and this

was included. Another option, ‘‘focus on channel

partners,’’ was added to the execution options to

capture the later stage efforts to motivate the

channel partners. Also added to the execution

stage was ‘‘use reference sites,’’ as this is a fre-

quently used option in the surveyed market.

The outcome was a clearer and more relevant re-

search instrument (Table 1). This modified framework

provides the list of measurement items used to identify

the launch strategies.

Telephone Survey

The high-technology sector chosen for the study was

computer software. Software has the characteristics

expected of a high-tech sector (Mohr, 2001): a high

degree of scientific and technical uncertainty; new

technology with the potential to make old technolo-

gy obsolete and to do so rapidly; high or very high

demand for new technologies often from new players;

customer uncertainty over the potential value of the

innovation; and a high percentage of sales invested in

research and development (R&D). Leading players

such as Microsoft, IBM, Oracle, and SAP are ac-

knowledged high-tech companies.

The research was targeted at software companies

throughout the world with the requirement that they

develop, produce, and market their own software

products. A database, ‘‘Software 500,’’ of the top

500 software companies in the world produced by

Software Magazine was obtained. The plan was to

produce 200 completed questionnaires.

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

501

The use of face-to-face interviews was ruled out

on the grounds of expense, since the targeted software

companies were located throughout the world.

Also ruled out was a mailed survey, as it would

most likely result in a low level of response. It was

therefore decided to use telephone interviews

because the research instrument was straightforward

enough to be explained over the phone, the cost

would be acceptable, and the response rate likely to

be high. Telephone interviews would be conducted

with senior product, brand, or marketing managers

responsible for the marketing of one or more software

products.

The questionnaire was successfully telephone pre-

tested for clarity, nonambiguity, and completeness

with 10 software product managers from the support-

ing high-tech company. Contact was then made with

the software companies by e-mail and telephone to

screen the companies as well as seeking cooperation.

Excluded from the sample were companies producing

software products that are so closely related to pro-

prietary hardware that the marketing and sales of the

software is inextricably linked to that of the hardware,

for example, proprietary operating systems or disk

storage management software. Also excluded from

the sample were companies producing software that is

individually developed and charged for as part of a

service contract—in other words, bespoke software or

software that is not packaged and marketed inde-

pendently.

A total of 190 interviews were completed out of 300

organizations contacted, which gave a response rate

of 63%. The high response rate figure was credited to

three factors: the high reputation in the sector of the

research company employed to do the interviews; the

efforts made to secure full participation; and the high

interest in the topic under investigation. The majority

of cooperating companies was based in the United

States, followed by the United Kingdom (Table 2a).

Some European and American firms were contacted

at the U.K. office; all interviews were conducted in

English. Checks on the types of company, on size, on

geographic distribution, and on standard industry

classification (SIC) categories indicated that the sam-

ple could be considered representative of the top 500

companies in the software industry. Most respondents

held a worldwide responsibility for the marketing of

their products (Table 2b).

Information was sought on the number of products

marketed by the business unit in question. Then the

interviewees were asked if they managed more than

one product. If so, they were asked to declare which

recently launched product or product family is the

most important to their organization in terms of

current and potential sales and profits. The remain-

der of the questionnaire was then focused on that one

product. Thus, only one product, or product family,

was investigated per interview even if the interviewee

had broader responsibility. The respondents were

Table 1. Launch Tactics

Market PreparationMP1: Form strategic alliancesMP2: Supply to OEMs to incorporate in other productsMP3: Provide clear product information to the marketMP3: Educate the market to understand new usesMP4: Create unique distribution channels

Targeting and PositioningTP1: Target high-value usersTP2: Emphasize low priceTP3: Emphasize technology superiorityTP4: Emphasize low riskTP5: Offer different versions targeted at different buyers

ExecutionE1: Use opinion leadersE2: Have trial programs (e.g., demonstrations, ‘‘try and buy’’)E3: Concentrate on nichesE4: Cultivate a winner image (i.e., winning mindset)E5: Focus on channel partnersE6: Exploit tactical alliancesE7: Use reference sites

Table 2a. Country Location of Respondent

Distrbution of Respondents by Country

Frequency Percent Cumulative Percent

United States 130 68.4 68.4United Kingdom 48 25.3 93.7Canada 4 2.1 95.8France 3 1.6 97.4Germany 2 1.1 98.4Israel 2 1.1 99.5Sweden 1 0.5 100.0

Total 190 100.0

Table 2b. Scope of Responsibility of Interviewee

Frequency Percent

Worldwide 113 59.5Region 36 18.9Country 41 21.6

Total 190 100.0

502 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

asked to indicate the importance of each tactic in the

launch of the selected software product on a 1 to 5

scale, with 1 being of no importance and 5 being very

important.

Also collected was information on the success of

the product using five measures of financial and sales

success. However, the knowledge and experience

gathered during the new product development proc-

ess can be as important as the project itself (Bowen et

al., 1994), including the platform created for subse-

quent new products, perhaps even families of prod-

ucts (Meyer and Utterback, 1993). Companies that do

not develop new products and reinforce their core

competencies soon fall behind the technology frontier

(Schilling, 1998). Therefore, in addition to the five fi-

nancial measures, four measures of success were add-

ed to capture the follow-on benefits of the new

product project: (1) platform for further new prod-

ucts; (2) opening up access to new markets; (3) impact

on image; and (4) attracting new customers (see Grif-

fin and Page, 1993, for a review of success and failure

product development measures). In addition, some

background information was collected.

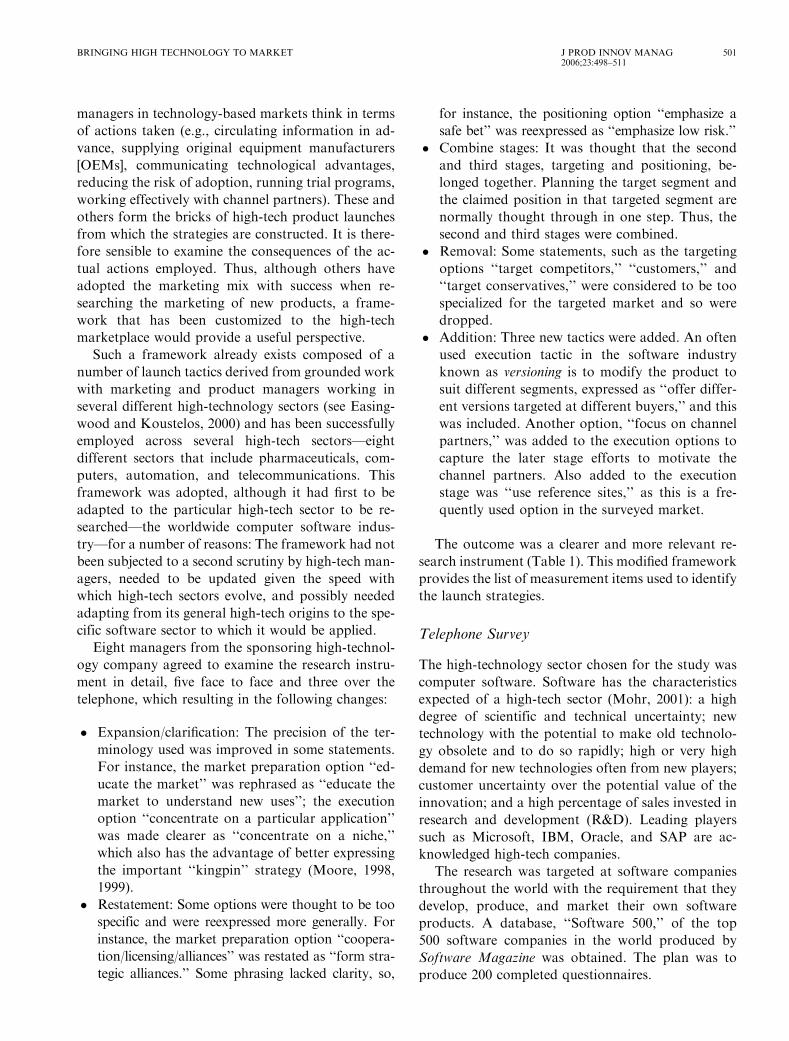

Results

Launch Strategies

The data on the importance of each tactic in the mar-

keting of the software products were then subjected to

principal components factor analysis: varimax rota-

tion and Kaiser normalization (Table 3). The scree

plot for the eigenvalues has a longish tail; accordingly

a cut-off level of 1.1 was set for the eigenvalues to

prevent the inclusion of too many factors.

This resulted in five factors explaining 52% of the

original variance, each one a particular combination

of launch tactics.

The first factor has high loadings on those tactics

that involve working closely with other players in-

volved in bringing technology-based products to mar-

ket. Particularly important are creating formal

alliances, both strategic at the market preparation

stage and tactical at the execution stage; creating

unique distribution channels at the preparation

stage and then focusing efforts on the channel

partners at the execution stage; and developing

Table 3. Marketing Tactics and Factor Loadings

Rotated FactorLoadingsa

Percent VarianceExplained Eigenvalues

Factor 1: Alliances 13.977 2.376MP1: Form strategic alliances .730MP5: Create unique distribution channels .483E5: Focus on channel partners .724E6: Exploit tactical alliances .831E7: Use reference sites .409

Factor 2: Targeted Low Risk 9.984 1.697TP4: Emphasize Low Risk .492TP5: Offer different versions targeted at different buyers .633E1: Use opinion leaders .536E2: Have trial programs (e.g., demonstrations, ‘‘try and buy’’) .575E4: Cultivate a winner image (winning mindset) .448

Factor 3: Low-Price OEM 9.970 1.695MP2: Supply to OEMs to incorporate in other products .419MP5: Create unique distribution channels .519TP1: Target high-value users � .548TP2: Emphasize low price .704

Factor 4: Broadly Based Market Preparation 9.789 1.664MP2: Supply to OEMs to incorporate in other products .549MP3: Provide clear product information to the market .676MP4: Educate the market to understand new uses .723

Factor 5: Niche-Based Technological Superiority 7.924 1.347TP3: Emphasize technology superiority .774E3: Concentrate on niches .565

aCut-offs: 0.4.

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

503

mutually beneficial relationships with customers who

then provide reference sites for the new products. This

combination of tactics is thus named the alliance

strategy.

The second factor represents a later stage strategy,

with no market preparation activities. It has two com-

ponents. The first is an attempt at lowering the cus-

tomer’s perceived risk of adoption using a number of

tactics: emphasizing low risk; attempting to be seen as

the winner, which, if it is successful, convinces cus-

tomers that the software is safe to adopt; offering tri-

als so customers can test the product for themselves;

offering guarantees; and gaining the support of influ-

ential opinion leaders whose recommendations are

seen as proof the product is adoptable. The second

component of the strategy involves targeting, partic-

ularly by producing versions of the product that have

been prepared specifically for the targeted sectors.

This strategy is thus summarized simply as targeted

low risk.

The third strategy has a clear, narrowly defined

profile. It is built around low price and places more

emphasis on this tactic than any of the other strate-

gies. There is an emphasis on supplying OEMs and on

creating unique distribution strategies. Consistent

with its low price stance, it is very much not about

serving high-value users. This is a low-price OEM

strategy.

The fourth strategy is very much based on an em-

phasis on the early-stage tactics of market prepara-

tion. It concentrates on providing the market with

information and indeed on educating the market,

which can be a long-term task. It seeks to develop

unique channels particularly to OEMs and is broad

based in the sense that it avoids narrowly defined

niches. This strategy is thus dubbed broadly based

market preparation.

The fifth strategy is tightly built around a superior

technological advantage aimed at well-defined niches

and is thus called a niche-based technological superi-

ority strategy.

Five distinct launch strategies have been identified.

The first two objectives of this work are accomplished

namely demonstrating that software companies use

distinct combinations of launch tactics that are clearly

defined and highly interpretable and hence are

deserving to be called strategies.

The frequency of use of each strategy was estimated

by counting the number of times each strategy en-

joyed the highest score among all strategies for each

firm (Table 4). The strategies were fairly uniformly

popular, with the low-price OEM strategy heading the

list, followed by niche-based technology superiority.

Performance

To address the final objective it was necessary to

introduce one or more measures of success. As

explained, respondents were asked to estimate the

chosen product’s performance on nine measures us-

ing a 1–5 scale. The data were subjected to a principal

components factor analysis, yielding a two-factor

solution, explaining 28% and 21%, respectively, of

the variance (Table 5).

As can be seen, two distinct factors emerge: product

performance, composed of sales, share, and profita-

bility measures; and market development, which em-

phasizes longer-term development variables such as

new markets, image, and new product platforms.

Product performance. To investigate how the five

factors influence product performance, the cases were

divided into three equal groups based on the product

performance measure of success. The high scoring

group was then contrasted with the low scoring

group, a commonly used practice (e.g., Hultink and

Hart, 1998), using discriminant analysis, or stepwise

variable selection using Wilks’s Lambda.

The discriminant function is

�0:047þ 0:519 � targeted low risk

þ0:397 � broadly based market prep

þ0:418 � niche-based technological superiority:Table 6 shows the percentage of cases correctly

classified using this function and also using the cross-

validation approach; each case is classified by the

function derived from all cases other than that case. A

total of 66.9% of the original grouped cases and

65.4% of cross-validated grouped cases were correct-

ly classified. Lehmann’s one-tailed test statistic z is

significant at the 1% level, confirming this is not a

random assignment.

Table 4. Launch Strategy Frequency

Highest Scoring Launch Strategy Count Percent

Alliances 35 18.42Targeted Low Risk 38 20.00Low-Price/OEM 47 24.74Broad-Based Market Preparation 30 15.79Niche Technological Superiority 40 21.05

190 100.00

504 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

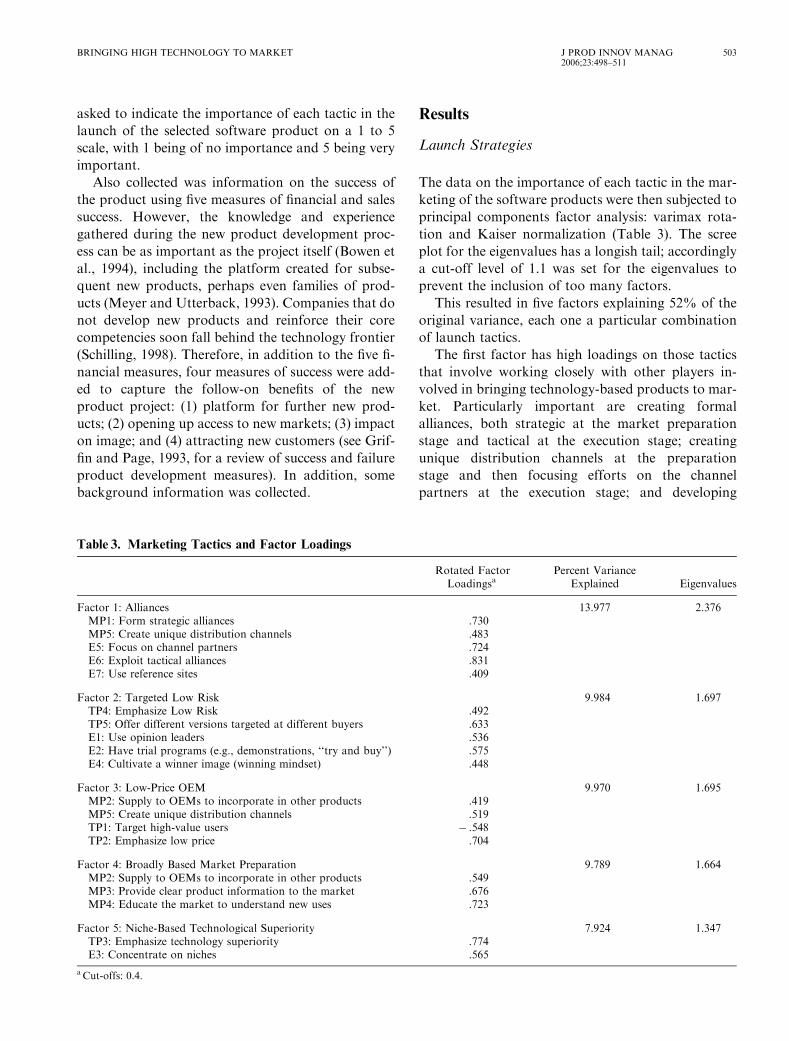

The third objective was to see if particular combi-

nations of strategies deliver enhanced performance.

For product performance it seems that this is the case.

To secure product performance—that is, product

sales, growth, share, and profitability—it seems that

successful software companies first of all engage in a

broadly based preparation of the market but switch to

a targeted strategy at the following stages of position-

ing and execution built around superior technological

performance and risk reduction.

Market development. In the same way as product

performance, the sample was divided into three

equal groups based on the market development per-

formance scores, and the high and low groups were

compared.

The discriminant function is

1:573þ 0:713�allianceþ 0:623�broadly based market preparation:

Table 7 shows the percentage of cases correctly

classified. The discriminant function correctly classi-

fies 73.5% of the cases, with 72.1% of cross-validated

grouped cases correctly classified. Lehmann’s one-

tailed test statistic z is significant at the 1% level.

The question posed by the third objective is whether

particular combinations of launch strategies deliver

superior performance. The answer, as for product

performance, appears also to be in the affirmative

for market development. Market development with its

focus on opening up new markets, reaching new cus-

tomers, improving image, and managing one new

product launch so as to increase the likelihood of fur-

ther launches is long term in its orientation. It seems

that the potential for market development is driven by

alliances and broadly based market preparation,

which is also significant for product performance.

This strategy is very much about working with

Table 5. Measuring Product Success and Factor Loadings

Rotated FactorLoadingsb

Percent VarianceExplained

CumulativePercent Variance

Explained

Factor 1: Product Performance 28.2 28.2Your products’ growth rate exceeds objectives. .741Your product’s growth rate exceeds the market growth. .680Total sales of the product are very high. .760The product has large market share. .601The profitability of the product exceeds objectives. .699

Factor 2: Market Development 21.1 49.3The product has helped open up new markets. .740The product has attracted significant new customers to the company. .734The product and its performance has positive impact on the image ofthe company.

.706

The product gives the company a platform on which to introduce newproducts.

.416

aCronbach’s alpha: factor 15 0.76; factor 25 0.64.bCut-offs: 0.4.

Table 6. Discriminant Analysis for Product Performance

PredictedGroup

Membership

TotalLow High

Original Count Low 42 26 68High 19 49 68

Percent Low 61.8 38.2 100.0High 27.9 72.1 100.0

Cross-Validated Count Low 42 26 68High 21 47 68

Percent Low 61.8 38.2 100.0High 30.9 69.1 100.0

Table 7. Discriminant Analysis for Market Development

PredictedGroup

Membership

TotalLow High

Original Count Low 50 18 68High 18 50 68

Percent Low 73.5 26.5 100.0High 26.5 73.5 100.0

Cross-Validated Count Low 48 20 68High 18 50 68

Percent Low 70.6 29.4 100.0High 26.5 73.5 100.0

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

505

partners: strategic alliances, OEMs, unique distribu-

tion channels, channel partners, and tactical partners

at the execution stage. And a key part of working with

these partners is that of informing and educating

them. It was considered possible that some other var-

iables might affect the employment of the launch

strategies. Therefore the effects of three independent

variables were investigated: newness of market served,

innovativeness of technology, and level of competition.

The procedure used was to classify the sample into

low and high groups according to the independent

variable and then to use an independent samples t-test

to look for significant differences in the mean launch

factor score for each group.

Discussion

Strategies

The current research identified five distinct strategies

consistently employed by companies in this high-tech

sector.

The first strategy, alliances, is hardly a surprise

given that it is widely practiced in many sectors (Vyas,

Shelburn, and Rogers, 1995), with the top 500 global

businesses averaging 60 major strategic alliances each

(Dale, Kale, and Singh, 2001). Strategic alliances are

not relationships at arms’ length but instead involve a

‘‘commitment to cooperation along some important

competitive dimension’’ (Hill, 1997, p. 12). They are

particularly prevalent among technology-led compa-

nies looking for complementary technologies as well

as leveraging marketing resources and attempting to

establish industry standards. Alliances help compa-

nies reduce the technological uncertainty that is char-

acteristic of high-tech markets and may reduce

potential confusion in the market place (Moriarty

and Kosnik, 1989), are particularly appropriate

when faced by highly capable competitors (Hill,

1997), and are extensively used in spite of the associ-

ated risks (Doz and Hamel, 1998). They are some-

times formed when a competitor is also at a fairly

advanced stage in developing a competing technology

(Hill, 1997). Companies try to establish industry

standards by licensing technology to try to create

the platform around which product categories can

be built (Cusumano and Gawer, 2004). Famously this

is what Microsoft did with Windows. Sony made it

relatively easy for developers to produce games for

Playstation, leading to a primary position in the video

game console market (Schilling, 2003). A platform

enables others to add value to the product category

and to create network effects so that nonadopters are

distinctly disadvantaged. Nearly a quarter of Ama-

zon’s sales are now generated on behalf of third-party

sellers (Nuttal and Waters, 2004, p. 17). High-tech

products rarely stand alone but instead exist in mini-

ecologies that ‘‘support and enhance them’’ (Arthur,

1996, p. 105). Companies should offer attractive li-

censing and distribution policies to attract third-party

developers and distributors and also should ensure

that all partners receive a fair reward for their partic-

ipation (Schilling, 2003).

As the strategy indicates, alliances are also forged

with the channels of distribution, who, given a stake

in the future of the technology, may support the tech-

nology more actively than otherwise they would.

The second strategy, targeted low risk, attempts to

reduce the risk of adoption in several ways for a tar-

geted segment. It is the strategy that places most em-

phasis on versioning and is likely to be attractive to

large companies that have made a significant invest-

ment in an existing product platform and need to lev-

erage that investment. They have the resources and

expertise that allows them to tune the product

through a series of new versions; good examples are

Microsoft Windows products, Oracle database soft-

ware, and IBM WebSphere. The rationale also is that

larger companies have established market positions

and customer bases that are susceptible to this kind of

incremental marketing strategy.

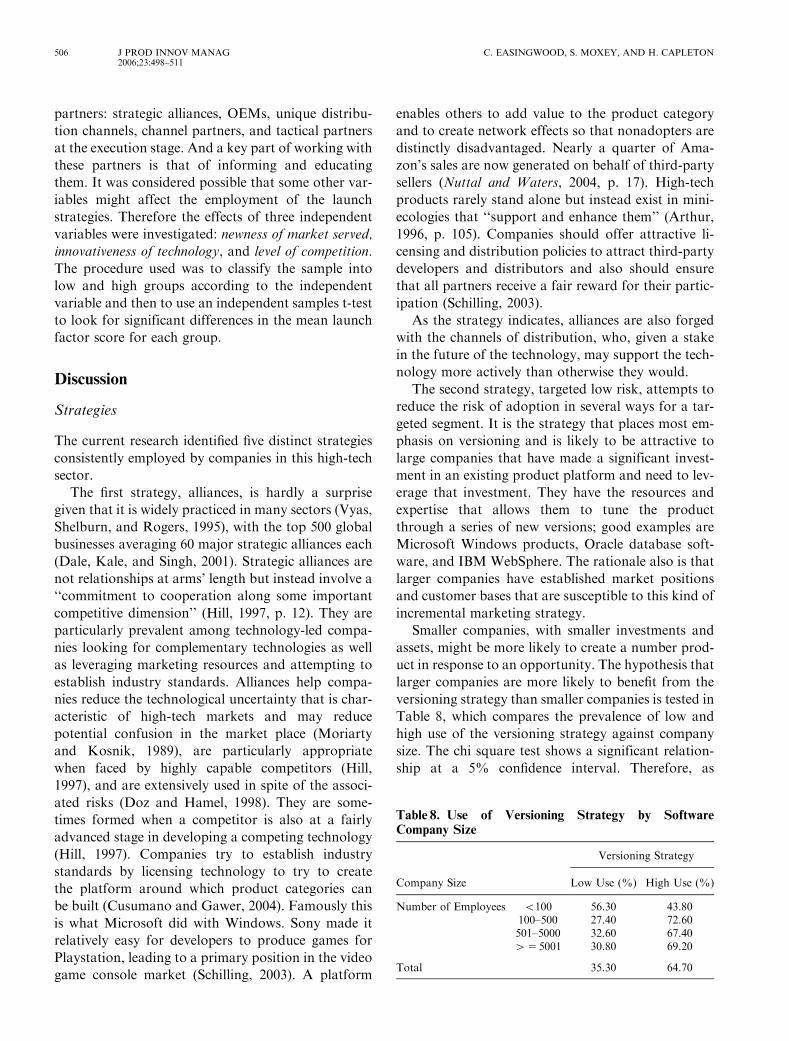

Smaller companies, with smaller investments and

assets, might be more likely to create a number prod-

uct in response to an opportunity. The hypothesis that

larger companies are more likely to benefit from the

versioning strategy than smaller companies is tested in

Table 8, which compares the prevalence of low and

high use of the versioning strategy against company

size. The chi square test shows a significant relation-

ship at a 5% confidence interval. Therefore, as

Table 8. Use of Versioning Strategy by SoftwareCompany Size

Company Size

Versioning Strategy

Low Use (%) High Use (%)

Number of Employees o100 56.30 43.80100–500 27.40 72.60501–5000 32.60 67.4045 5001 30.80 69.20

Total 35.30 64.70

506 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

hypothesized, larger companies (i.e., more than 100

employees) are more likely than smaller companies

(i.e., less than 100 employees) to favor the versioning

strategy.

Products that have been modified to meet the needs

of the served market are expected to win higher mar-

ket share (Langerak, Hultink, and Robben, 2004;

Ryans, 1988). Creating an early winner image through

the use of heavy initial support and advertising is one

way to help create the perception of a high-installed

base leading to a rapid growth in sales and high actual

installed base (Schilling, 2003). Purchasers seek the

reassurance of buying the accepted product. Bundling

a new high-technology product with existing technol-

ogy may reduce perceived risk (Sarin, Sego, and

Chanvarasuth, 2003).

The third strategy, low-price OEM, has a clear

profile. It is the only price-driven strategy and com-

bines price with channel building to OEMs, who care-

fully manage the quality and price of all components.

Essentially OEMs are looking for attractive price-to-

performance ratios; hence, the high emphasis is on

low price. This is a specialized OEM strategy and is

most often number one among the sample companies

(Table 4). This may not be a typical finding for some

other technology markets. For instance for successful

products in industrial markets, often with a techno-

logically based product advantage, a skimming price

is more typical (Hultink et al., 2000), as it is also for

products with high advantage (Hultink and Hart,

1998). However, discounting is also used (Arthur,

1996, p. 105): For instance, it may sometimes pay

firms to offer products at or even below cost at the

time of launch to accelerate adoption in the expecta-

tion that there will be compensating increased sales of

either the core technology or of complementary goods

once the technology is established, as in the video

game market (Schilling, 2003, p. 22).

The fourth strategy, broadly based market prepa-

ration, is longer term in nature. It attempts to educate

the market, which can take time and is expensive. In

addition, it seeks to develop unique channels, which is

not normally accomplished rapidly. By adopting a

broad-based outlook, in the sense that it avoids nar-

rowly defined niches, this also fits in with a longer-

term orientation: Start broad based, and narrow

down only when this is clearly the appropriate thing

to do. Niche orientation comes later (Millier, 1999).

Long-term market preparation is normally seen as

the preserve of companies that have dominant posi-

tions and market share. They may then be in a posi-

tion to benefit from patient nurturing of the market. A

company facing an erosion of its dominant position is

likely to find that the time available for market prep-

aration between product announcement and product

availability will have to shorten or demand will tend

to be filled by competition.

Finally, the fifth strategy, niche-based technologi-

cal superiority, uses a technologically superior prod-

uct to dominate a niche. This strategy places the most

emphasis on technological superiority. Competition

at the early stages of high-growth markets is more

likely to be technologically based than marketing

based (Kuester, Homberg, and Robertson, 1999).

This is the route to the creation of new products

that are technologically differentiated, that have no

direct customers, and that stake out fundamentally

new market space (Kim and Mauborgne, 1999). Rad-

ical technological innovation is the recommended

route to break into an industry dominated by an en-

trenched standard (Schilling, 2003). Niche strategies

are more likely to be used where the levels of product

advantage are high (Hultink and Hart, 1998). It has

also been noted that technologies that ultimately be-

came widely diffused were first incubated in a rela-

tively isolated niche (Adner and Levinthal, 2002).

This strategy can be compared to the strategy pro-

posed by Moore (1998, 1999) for new technology in-

troduction. He argued that initial sales might

be promising as some visionaries adopt, but this can

be deceptive as sales then start to languish. They hit

the chasm. The situation is rescued by developing a

complete product for a key segment or niche, resulting

in sales lift-off and domination of the chosen niche.

The fifth strategy, with its emphasis on the develop-

ment of a product with superior benefits for a targeted

niche, exactly represents the chasm strategy—possibly

the first time it has been identified empirically in a

large sample of companies. (Moore’s books are said

to be required reading in high-tech companies

[Dhebar, 2001]). Neither is the fifth strategy incom-

patible with strategies used for disruptive techno-

logies, namely ones that offer a different and

initially less-attractive mix of attributes than those

of prevailing technologies (Bower and Christensen,

1995; Christensen, 1997). Disruptive technologies are

likely to be rejected by mainstream customers, and so

companies must turn to selected niche segments that

are prepared to respond to the new mix of attributes

(Dhebar, 2001).

The chasm strategy to escape the chasm, or saddle,

results in a strong position in the first segment, which

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

507

provides the platform—resources, experience, invest-

ment in R&D—to attack a related segment in exactly

the same way so that a strong position is also

achieved in that segment. This provides a stronger

platform for further success (Easingwood and Har-

rington, 2002; Goldenberg, Libai, and Muller, 2002).

This is also what happens with disruptive strategies.

Domination of the outsider segment provides the

platform from which to base a return to attack, the

mainstream markets that initially so readily rejected

the disruptive technology (Bower and Christensen,

1995), this time with improved or lower-priced tech-

nology.

It has been shown that new industrial products are

more likely to be targeted at niches than are new con-

sumer products (Hultink et al., 2000) and that indus-

trial niche innovators enjoy above-average success

(Hultink et al., 1997). In addition, a niche strategy

for a new industrial product is less likely to elicit a

competitive reaction than a more broadly based strat-

egy (Debruyne et al., 2002).

Notice that two of the strategies—targeted low

risk and niche-based technological superiority—are

focused or targeted strategies supporting one of the

core ideas of the high-tech literature (Adner and

Levinthal, 2002; Moore, 1998; Moriarty and Kosnik,

1989); only one strategy is broadly based—strategy

four—broadly based market preparation—but this is

at the initial market preparation stage when many

companies will try to retain as wide a range of options

as is possible.

Performance: Product Performance

The combinations of strategies associated with supe-

rior product performance are targeted low risk,

broadly based market preparation, and niche-based

technological superiority. This can be summarized

as a strategy for a technologically superior product

that begins with preparation of the market followed

by targeting one or more niches, customizing the

product to those niches, and making adoption easy

by reducing the risk of adoption. Moore (1998)

advocates a similar change from a broad marketing

strategy to a niche strategy to successfully cross the

chasm. Firms must target specific niche segments

and focus effort to deliver the complete solutions to

make sales.

This strategy deemphasizes the creation of new dis-

tribution channels, which is associated with the

alliance and targeted low risk strategies. This is a

low-risk, sound strategy, not adventurous or even

conservative. It is not inconsistent with the strategic

launch strategy found by Hultink et al. (2000) to in-

crease the chances of a successful introduction of a

new industrial product. They found that industrial

firms actually achieve more success when they use in-

novation to increase penetration of existing markets

rather than by adopting more adventurous strategies

that try to use innovation to open up new markets, as

companies are sometimes prone to do.

Neither is this strategy short term only, because the

intention is to use the success in the targeted segments

to achieve success across wider swathes of the market

(Adner and Levinthal, 2002). The sales, share, and

profitability achieved in a relatively narrowly defined

part of the entire market provide the basis for more

broadly defined success over the longer term.

Performance: Market Development

The strategies associated with the market develop-

ment of new opportunities are alliances and broadly

based market preparation. It seems that the way to

develop new opportunities (e.g. new markets, new

customers) is to form alliances—early and strategic,

late and tactical—and to focus on all market devel-

opment activities.

This strategy is very much about working with and

informing and educating partners (e.g. strategic alli-

ances, OEMs, channel partners). It is a powerful ex-

ample of what has been called the third-party model

of business, in which business is driven by the com-

pany’s channels and its partners (High, 2005). Win the

channels, and inform and educate them; the like-

lihood is that opportunities will materialize. This is

the long-term view of market opportunities. The com-

pany with a good position in the channel will be

strongly positioned to participate in the longer-term

development of the market.

Notice that the strategy low-price OEM is not as-

sociated with either product performance or market

development success. It seems that, for software, this

kind of low-price strategy does not normally lead to

success, which must be disappointing, given it is the

most popular strategy.

Conclusions

The exploratory work reported here has identified five

launch strategies used in a high-tech environment.

508 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

These strategies are defined, uniquely for the launch

literature, in terms of the actual actions employed.

Yet this is what high-tech companies do. Further-

more, the identified strategies are, to varying extents,

mixtures of both tactical and strategic actions. This

seems to offer empirical support for treating strategies

in this way. Launch strategies do have both tactical

and strategic components. Certainly when tactical and

strategic launch actions were treated separately in one

study, the effects they had on performance were less

clear cut. Launch tactics were found to be associated

with performance but launch strategies were not

(Langerak, Hultink, and Robben, 2004).

An important question is to what extent do launch

stages build on one another? Four of the five strate-

gies identified combine tactics from more than one

stage. Only one strategy, broadly based market prep-

aration, is composed of tactics from one stage: the

preparation stage. Thus, although managers think in

terms of stages, they actually seem to put together se-

lections of tactics from different stages to produce ef-

fective strategies. Logic suggests that tactics selected

from the different stages will be employed sequenti-

ally, though this theory has not been explicitly tested.

The software industry is well known for its occa-

sional use of vaporware strategies—notorious strate-

gies in which a company announces a product that

does not currently exist and that sometimes does not

even have any product development plans. The pur-

pose of the vaporware strategy is to hold off compe-

tition until real products can be readied for market.

Where, if anywhere, do vaporware strategies fit

among the five proposed strategies? This strategy is

surely an extreme example of market preparation by

early announcement. It is an attempt to mold market

opinion. Most commentators would not regard

vaporware strategies as legitimate. They should per-

haps be labeled as market deception strategies rather

than market preparation strategies.

The approach used has been at the product level in

one sector: the worldwide software market. The

study sample represents nearly 40% of the total

population of firms in the Software 500. Given the

concentrated nature of the software industry this is an

even larger proportion by revenue. The factor analysis

described here is exploratory, but given the large sam-

ple size it is reasonable to assume that the results and

conclusions are confirmed for the Software industry.

It would clearly be useful to repeat this study

across other industries such as life sciences, telecom-

munications, and information technology hard-

ware to test the wider validity of the theory across

the entire high-technology sector. As a result, find-

ings are not likely to be skewed by cross-industry

factors.

However, there are limitations. First, the work uses

a telephone survey methodology with one key re-

spondent and is thus subject to problems such as

post-hoc rationalization, social desirability answering,

and common method variance problems, since both

the dependent and independent variables are being

measured from the same respondent. The fact that

telephone interviews were used, not a mailed survey,

carried out by experienced researchers in technology-

based markets did in part help reduce the impact of

these potential biases. The problem of common meth-

od variance, which is ubiquitous, can be only partially

addressed by statistical methods; it is far better to

look for procedural or design remedies (Podsakoff

and Organ, 1986). However, collection of information

on the dependent variables from another source

would have significantly increased the cost or reduced

the sample size and would not necessarily have been

effective, as the second source would have been drawn

from the same management group as the first.

In addition, the research did not attempt to incor-

porate the intricacies of action and counteraction. In-

stead it focused on building up strategies formed from

the basic building blocks of management action,

showing how these strategies correspond to consist-

ent programs of action and are correlated with meas-

ures of performance. Future work should attempt to

retain this level of detail and also should address some

of the competitive issues, for although the intention

may be to create entirely new market space (Kim and

Mauborgne, 1999) many new products do not. Two

thirds of new industrial products can expect to face a

response by existing companies (Debruyne et al.,

2002). Thus, most new products will come up against

incumbents and can expect them to act to protect

market share and profits. Kuester, Homburg, and

Robertson (1999) found that 93% of companies re-

acted in some way to the entry of a new competitor;

Gatignon, Robertson, and Fein (1997) found that

90% reacted, although it is encouraging to note that

the more innovative the new entry, the longer it takes

for an incumbent to retaliate (Kuester, Homburg, and

Robertson, 1999). The implication of this latter ob-

servation is that innovative companies must create a

culture of product innovation so that competitors are

constantly trying to catch up (Chandy and Tellis,

2000; Chandy, Prabhu, and Kersi, 2003).

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

509

References

Adner, Ron and Levinthal, Daniel A. (2002). The Emergence ofEmerging Technologies. California Management Review 45(1):50–66 (Fall).

Arthur, W. Brian (1996). Increasing Returns and the New World ofBusiness. Harvard Business Review 74(4):100–9 (July–August).

Bowen, H.K., Clark, K.B., Holloway, C.A. and Wheelwright, S.C.(1994). Development Projects: The Engine of Renewal. HarvardBusiness Review 72(5):110–20.

Bower, Joseph L. and Christensen, Clayton M. (1995). DisruptiveTechnologies: Catching the Wave. Harvard Business Review73(3):43–53 (January–February).

Cespedes, F.V. (1994). Industrial Marketing—Managing New Re-quirements. Sloan Management Review 35(3):45–60.

Chandy, Rajesh K., Prabhu, Jaideep C. and Kersi, Anita D. (2003).What Will the Future Bring? Dominance, Technology Expecta-tions, and Radical Innovation. Journal of Marketing 67(3):1–18(July).

Chandy, Rajesh K. and Tellis, Gerard J. (2000). The Incumbent’sCurse? Incumbency, Size, and Radical Product Innovation. Journalof Marketing 64(3):1–17 (July).

Christensen, Clayton M. (1997). The Innovator’s Dilemma: When NewTechnologies Cause Great Firms to Fail. Boston: Harvard BusinessSchool Press.

Cooper, Robert G. (1975). Why New Industrial Products Fail. Indus-trial Marketing Management 4(6):315–26.

Cooper, Robert G. (1979). The Dimensions of Industrial New ProductSuccess and Failure. Journal of Marketing 43(3):93–103.

Cooper, Robert G. (1980). Project NewProd: Factors in New ProductSuccess. European Journal of Marketing 14(5–6):277–91.

Cooper, Robert G. and de Brentani, Ulrike (1991). New IndustrialFinancial Services: What Distinguishes the Winners. Journal ofProduct Innovation Management 8(3):75–90.

Cooper, Robert G. and Kleinschmidt, Elko J. (1986). An Investigationinto the New Product Process: Steps, Deficiencies, and Impact.Journal of Product Innovation Management 3(2):71–85.

Cusumano, Michael and Gawer, Annabelle (2004). Platform Leader-ship: How Intel, Microsoft and Cisco Drive Industry Innovation.Boston: Harvard Business School Press.

Dale, Jeffrey H., Kale, Prashant and Singh, Harbir (2001). How toMake Strategic Alliances‘Work. Sloan Management Review42(4):37–43 (Summer).

Debruyne, Marion, Moenaert, Rudy, Griffin, Abbie, Hart, Susan,Hultink, Erik Jan and Robben, Henry (2002). The Impact ofNew Product Launch Strategies on Competitive Reaction in In-dustrial Markets. Journal of Product Innovation Management19(2):159–70.

Dhebar, Anirudh (2001). Six Chasms in Need of Crossing. Sloan Man-agement Review 42(3):95–99 (Spring).

Doz, Y. and Hamel, G. (1998). The Alliance Advantage: The Art ofCreating Value through Partnering. Boston: Harvard BusinessSchool Press.

Easingwood, C.J. and Harrington, S. (2002). Launching and Re-launching High Technology Products. Technovation 22(11):657–66.

Easingwood, Chris and Koustelos, Anthony (2000). Marketing HighTechnology: Preparation, Targeting, Positioning, Execution. Busi-ness Horizons 43(3):27–34 (May–June).

Gatignon, Hubert, Robertson, Thomas and Fein, Adam J. (1997).Incumbent Defense Strategies against New Product Entry.International Journal of Research in Marketing 14(2):163–76 (May).

Goldenberg, Jacob, Libai, Barek and Muller, Eitan (2002). Riding theSaddle: How Cross-Market Communications Can Create a MajorSlump in Sales. Journal of Marketing 66(2):1–16 (April).

Green, Paul E., Krieger, Abba M. and Vavra, Terry G. (1997).Evaluating New Products. Marketing Research 9(4):12.

Green, Donna H. and Ryans, Adrian B. (1990). Entry Strategies andMarket Performance: Causal Modeling of a Business Simulation.Journal of Product Innovation Management 7(1):45–58.

Griffin, Abbie and Page, Albert L. (1993). An Interim Report onMeasuring Product Development Success and Failure. Journal ofProduct Innovation Management 10(4):291–308.

Gruca, Thomas S., Kumar, K. Ravi and Sudharshan, D. (1992). AnEquilibrium Analysis of Defensive Response to Entry Using aCouples Response Function Model. Marketing Science 11(4):348–58 (Fall).

Hauser, John R. and Shugan, Steven M. (1984). Application of the DE-FENDER Consumer Model. Marketing Science 3(4):327–51 (Fall).

High, K. (2005). Financial Times, A Digital Distribution RevolutionGathers Pace. June 21, p. 14.

Hill, Charles W.L. (1997). Establishing a Standard: Competitive Strat-egy and Technological Standards in Winner-Take-All Industries.Academy of Management Executive 2:7–25 (May).

Hultink, Erik Jan and Hart, Susan (1998). The World’s Path to theBetter Mousetrap: Myth or Reality? An Empirical Investigationinto the Launch Strategies of High and Low Advantage New Prod-ucts. European Journal of Innovation Management 1(3):106–22.

Hultink, Erik Jan, Hart, Susan, Robben, Henry S.J. and Griffin, Abbie(1997). Industrial New Product Launch Strategies and ProductDevelopment Performance. Journal of Product Innovation Manage-ment 14(3):243–57.

Hultink, Erik Jan, Hart, Susan, Robben, Henry S.J. and Griffin, Abbie(2000). Launch Decisions and New Product Success: An EmpiricalComparison of Consumer and Industrial Products. Journal ofProduct Innovation Management 17(1):5–23.

Kim, W. Chan and Mauborgne, Renee (1999). Creating New MarketSpace. Harvard Business Review 77(1):83–93 (January–February).

Kim, W. Chan and Mauborgne, Renee (2000). Knowing a WinningBusiness Idea When You See One. Harvard Business Review78(5):129–38 (September–October).

Kuester, Sabine, Homburg, Christine and Robertson, Thomas S.(1999). Retaliatory Behaviour to New Product Entry. Journal ofMarketing 63(4):90–106 (October).

Langerak, Fred, Hultink, Erik Jan and Robben, Henry S.J. (2004). TheImpact of Market Orientation, Product Advantage, and LaunchProficiency on New Product Performance and OrganizationalPerformance. Journal of Product Innovation Management 21(2):79–94.

McDonald, Heath, Corkindale, David and Sharp, Byron (2003).Behavioral Versus Demographic Predictors of Early Adopters:A Critical Analysis and Comparative Test. Journal of MarketingTheory and Practice 11(3) (Summer).

Meyer, M.H. and Utterback, J.M. (1993). The Product Family andthe Dynamics of Core Capability. Sloan Management Review 3(3):29–47.

Millier, P. (1999).Marketing the Unknown. New York: John Wiley andSons.

Mohr, Jakki (2000). The Marketing of High-Technology Products andServices: Implications for Curriculum Content and Design. Journalof Marketing Education 22(3):246–59 (December).

Mohr, J. (2001). Marketing of High-Technology Products and Innova-tions. Upper Saddle River, NJ: Prentice-Hall.

Mohr, Jakki J. and Shooshtari, Nader H. (2003). Introduction to theSpecial Issue: Marketing of High-Technology Products and Innova-tions. Journal of Marketing Theory and Practice 11(3):1–13 (Summer).

Montoya-Weiss, M. and Calantone, R. (1994). Determinants of NewProduct Performance: A Review and Meta-Analysis. Journal ofProduct Innovation Management 11(5):397.

Moore, G.A. (1998). Crossing the Chasm. Oxford: Capstone PublishingLtd.

510 J PROD INNOV MANAG2006;23:498–511

C. EASINGWOOD, S. MOXEY, AND H. CAPLETON

Moore, G.A. (1999). Inside the Tornado: Marketing Strategiesfrom Silicon Valley’s Cutting Edge. Oxford: Capstone PublishingLtd.

Moriarty, Roland T. and Kosnik, Thomas J. (1989). High-Tech Mar-keting: Concepts, Continuity and Change. Sloan ManagementReview 7(4):7–17 (Summer).

Nuttall, C. and Waters, R. (2004). Financial Times, The Biggest U.S.Internet Companies Enjoy Huge Economies of Scale. June 10,p. 17.

Podsakoff, Philip and Organ, Dennis W. (1986). Self-Reports in Or-ganizational Research: Problems and Prospects. Journal of Man-agement 12(4):531–44.

Ryans, Adrian B. (1988). Strategic Market Entry Factors and MarketShare Achievement in Japan. Journal of International BusinessStudies 19(3):389–409 (Fall).

Sarin, Shikar, Sego, Trina and Chanvarasuth, Nataporn (2003).Strategic Use of Bundling for Reducing Consumers’ PerceivedRisk Associated with the Purchase of New High-Tech Products.Journal of Marketing Theory and Practice 11(3):71–84 (Summer).

Schilling, Melissa A. (1998). Technological Lockout: An IntegrativeModel of the Economic and Strategic Factors Driving TechnologySuccess and Failure. Academy of Management Review 23(2):267–84.

Schilling, Melissa A. (2003). Technological Leapfrogging: Lessonsfrom the USA Video Game Console Industry. California Manage-ment Review 23(2):6–32 (Spring).

Urban, G.L. and Hauser, J.R. (1993). Design and Marketing of NewProducts. Englewood Cliffs, NJ: Prentice-Hall.

Vyas, N.M., Shelburn, W.L. and Rogers, D.C. (1995). An Analysis ofStrategic Alliances: Forms, Functions and Framework. Journal ofBusiness and Industrial Marketing 10(3):47–60.

BRINGING HIGH TECHNOLOGY TO MARKET J PROD INNOV MANAG2006;23:498–511

511