Embed Size (px)

DESCRIPTION

Briefing on the Procurement Leverage Program. AGENDA. Context for the supplier development program Progress on the supplier development program New Initiatives Locomotive Fleet Procurement. 2. Infrastructure investment at around 5% of GDP between 1994-2004 has created a significant backlog. - PowerPoint PPT Presentation

Citation preview

Briefing on the Procurement Leverage Program

Strictly confidential 2

Context for the supplier development program

Progress on the supplier development program

New Initiatives

Locomotive Fleet Procurement

AGENDA

Strictly confidential 3

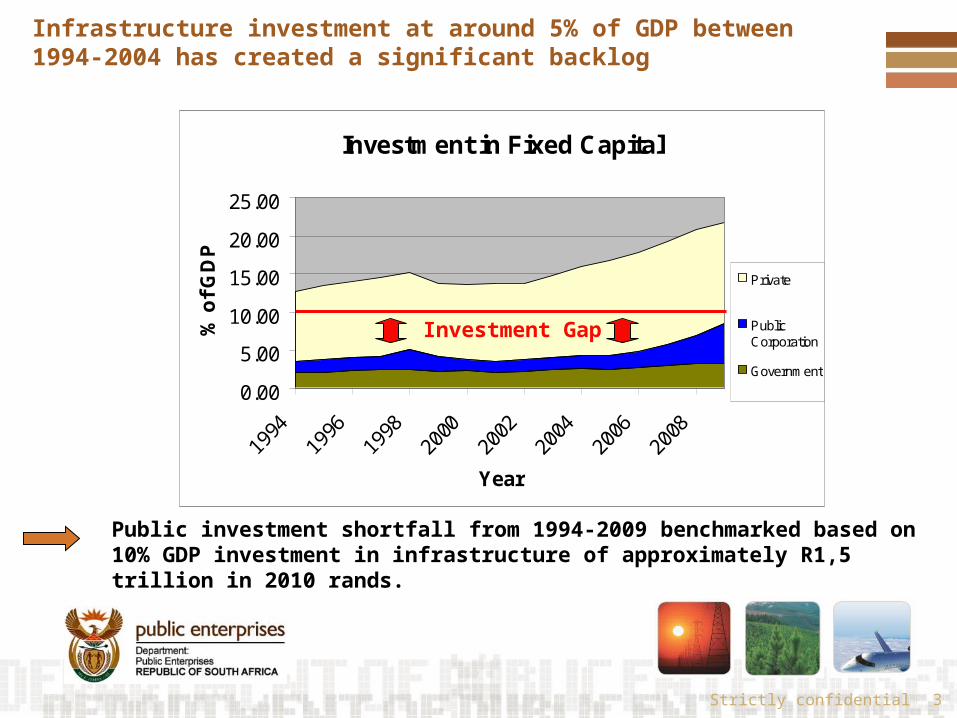

Infrastructure investment at around 5% of GDP between 1994-2004 has created a significant backlog

Public investment shortfall from 1994-2009 benchmarked based on 10% GDP investment in infrastructure of approximately R1,5 trillion in 2010 rands.

Investment in Fixed Capital

0.00

5.00

10.00

15.00

20.00

25.00

Year

% o

f G

DP

Private

PublicCorporation

Government

Investment Gap

Strictly confidential 4

A key strategic insight is that there is an industrial complex associated with infrastructure provision – this complex declined with infrastructure spend

Strictly confidential 5

Similarly, the development of related skills have also tended to track the investment cycle.

2000=100

0

100

200

300

400

500

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Year

Num

ber

of

gra

duate

s

5

10

15

20

25

30

35

40

Civ

il s

pendin

g (

R-b

illion)

Civil engineeringgraduations Spending in civilconstruction

Strictly confidential 6

The impact on supplier industries was also seriously exacerbated by the lumpy nature of the procurement

0

50

100

150

200

250

300

Series1

Number of Locomotives Procured

Average of approximately 80 locomotives a year over 40 years

Strictly confidential 7

The role of SOE in industrial policy is to drive and leverage investment in infrastructure, enabling an infrastructure driven growth and industrialisation process

Increase investment in infrastructure channeled through a procurement leverage programme

Unlock investment in “customer” industries through providing additional capacity

Improve productivity of operations in the infrastructure service provider

Unlock investment in supplier industries through increased demand

Realise externalities associated with network industries

Increased GDP, jobs and associated

tax collection

Sustained Growth Requires Continuous Investment!!!

Strictly confidential

The objective of the intervention is to develop a procurement tool-kit and supporting measures to promote investment and the development of internationally competitive capabilities in supplier sectors to the SOE’s capital and relevant operational spend, with the aim of:

– Reducing costs through increasing efficiencies

– Reducing dependency on imports and foreign exchange exposure

– Developing niche export areas.

The Competitive Supplier Development Program has the objective of laying a platform for investment and learning by suppliers in the SOE supply chain

The key first step to the process was the design of a strategic supplier development plan by the SOE which was done in 2008.

Strictly confidential

This reflects the need to make qualitatively new investments to decrease the imported component. . .

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

05 06 07 08 09 10 11 12 13 14

Real GDP level (Normal sourcing)Real GDP level (Increased domestic sourcing)

.00

.04

.08

.12

.16

.20

.00

.04

.08

.12

.16

.20

05 06 07 08 09 10 11 12 13 14

Real GDP growth (Normal sourcing)Real GDP growth (Increased domestic sourcing)

The growth impact of local supplier development is extremely significant as the imported component drops

A 25% drop in imports will have a disproportional impact on growth and output

Strictly confidential

The development of local suppliers is a competitiveness initiative – un-thought through price premiums paid to increase local content could be self-defeating

Price premiums could simply crowd-out investment amongst SOE’s customers while encouraging unsustainable investment amongst SOE suppliers.

The objective is to build the competitiveness of supplier industries, not local content at all costs.

Price premiums paid to suppliers for local content

Increase in price charged by SOEs for services

Crowding out of investment in customer industries

Multiplier

Increased costs

% change in level of Real GDP

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36

% difference w hen compared to baseline

Quarters

% change in level of Real GDP

1% increase in Customs Duty

Strictly confidential

Achieving global competitiveness in manufacture will require high levels of supplier effort and investments in learning

11

Strictly confidential 12

As there is no simple text-book methodology, the first phase of the competitive supplier development program was designed to enable a “learning by doing” process by the SOE.

Developing an effective operational approach and associated management capability to accumulate experience and learning so as to find out what works within constraints and opportunities of the environment

Bottom up execution:

Delivery organisation

driven planning, implementation

and learning (e.g. clear definition of

projects, focus areas and targets.)

Show care from the top: Hands-

on top down accountability and dialogue (e.g. regular, substantive report-back meetings on progress and

obstacles)

Provide Support: Put in place

resources and enabling initiatives

that enhance delivery (e.g.

specialised skills development)

Output of phase one: Learning about what works in practice!

Strictly confidential 13

There are three phases to the supplier development program

Phase One: Transactional Capabilities

• Optimisation of what is to be procured (to optimise capital, lifecycle cost, industrial impact)

• Methodology to define, contract and manage localisation requirements.• Develop methodology for defining procurement process (how to procure).• Strong contract management skills

Phase Two: Manufacturing Partnership Capabilities

• Abililty to identify key fleets and define long term fleet requirement. • Standardisation methodology to ensure economies of scale. • Across government – enterprise coordination capability including long term

funding strategy, definition of procurement vision and comprehensive government support for advanced manufacturing capabilities.

Phase Three: Innovation Capabilities

• Identificaqtion of design capability vision.• Structuring of design partnership• Management of design technology transfers.

• We are presently moving from phase one to phase two, although enterprise capability remains weak and very uneven.

• Continued focus on entrenching supplier development at a transactional level

Strictly confidential

Segmentation Examples

Required government interventions increase with degree of industrial complexity

Ultra heavy forging

Pipe milling

Government driven investments for strategic economic purposes – not commercially viable in short-medium term

ASME III production facility

High voltage switchgear

Commercially viable but high complexity - government investment required in plant, specialised skills and technologies to enable investment

Pipe prefabrication

Gas cycle system

Investment requirements within capability of company balance sheets, but clear medium term procurement commitment required

Construction

Structural steel

Within current industry capability

Proper planning and communication required to optimise use of industry capacity and encourage investment

Globallyleading

Advanced

Inter-mediate

Shallow

Intervention requirements

Strictly confidential

To illustrate, the Eskom CSDP will focus on intermediate manufacturing

5 year CSDP targets, % local spendPriority components for CSDP 2008-2013

Not a focus of CSDP 2008-2013

Selected red components, e.g., Large power transformers C&I transmitters and transducers Electrical actuators Boiler feed pumps

All yellow components, e.g., Small and medium power transformers Fan shafts Bag filters

All green components, e.g., Air-cooled condensors Boiler fuel cycle Cables and conductors

09 11 2013 2008 10 12

9099

59

16

3628

13

Strictly confidential

Eskom has leveraged over a billion rand of investment in manufacture from the present build programme – although interventions have been largely ad-hoc

▪ 11,000m2 boiler pressure part workshop built in Nigel– Boiler Membrane Wall

Workshop– Two new CNC Benders

commissioned– New welding training centre– CNC header drilling machine

▪ Training facilities in Gauteng– 1400 artisans, 60 engineers,

36 operators, 24 maintenance workers

▪ Sulzer South Africa subcontracted for the production of 96 pumps (36 BFP, 24 CEP, 36 boosters) for Medupi and Kusile

▪ 45% of contract has local content commitments, including manufacture of castings and rotating components

▪ Manufacturing capacity investments by Sulzer expected to be ~R60m

▪ Sulzer revenues increased significantly since 2007

Sulzer SA, a local manufacturer of feed pumps, has invested R60mn

Hitachi is investing ~R900m in facilities and training in South Africa

▪ Expansion of existing facilities to manufacture MV switchgear locally

▪ R21m invested to date

Actom committed to an investment of R84m in local facilities

▪ Plant that saw global manufacture of 275kV insulators move to South Africa▪ Previously manufactured in

Switzerland▪ Investment complete and first

production units rolled off production line

Pfisterer investment of R25m in plant in KZN

Strictly confidential 17

Eskom has also leveraged the training of 6130 people by suppliers.

Area Committed numbers In Training Training Completed

Medupi 2178 1299 284

Kusile 2234 792 626

Ingula 137 16 5

Power Delivery 1382 1002

Plant and Equipment

199 38 1137

Total 6130 2145 3054

Majority of training takes place in the following disciplines: Coded Welders, Boilermakers, Riggers, Fitters, Technicians, Laboratory

technicians and Quantity Surveyors.

Strictly confidential 18

Eskom has also established component hubs to enable the identification of supplier development opportunities for specific components.

• Transformer and motor:• CTC • Tanks• Radiators

• Boiler plant:• Filter bags• Pressure vessels• Boiler steel

• Turbine plant• Valves • Blades• Motors & pumps

• Foundry

• Castings for various components

• Nuclear

• Industry awareness for future programme

CustomersChair

• Independent chair

• Industry Associations representing suppliers

• Development of business cases for funding of R&D, skills development and shared technical infrastructure

• Independent chair

• Industry Associations representing suppliers

• Development of business cases for funding of R&D, skills development and shared technical infrastructure

FundingSkills Accreditation

Pre-qualified suppliers Competitive assurance

Benchmarking

Industry association

These hubs will see the South African Industry aligning itself to the future demand

from SOE’s prior to the commercial transaction

Strictly confidential 19

Transnet has secured three major CSDP transactions

• The current CSDP plan with EMD was finalised in November 2009.• The EMD CSDP plan aims for (1) TRE to become part of their Global Supply Chain for rebuilt

traction motors and diesel engines, (2) to accredit TRE’s maintenance facilities for EMD locomotive maintenance and (3) to localise the supply of at least 10% of the value and/or quantity of the parts listed per the Spare Parts Agreement.

• These CSDP goals will be achieved through the transfer of skills and relevant intellectual property required to carry out the activities mentioned.

• EMD is already actively supporting TRE in acquiring new work in Africa..• Execution of the EMD CSDP plan is well underway

• The contract for the building of the 100 Locomotives was awarded to GE and signed on 17 December 2009.

• GE developed a CSDP plan consisting of 3 main initiatives – training for maintenance development, Lean, Six Sigma and Candidate Engineers; localisation of various components and parts as well as a licence agreement with TRE for the overhaul and modernisation of GE locomotives.

• The signing of the CSDP Plan was concluded on 30 June 2010• The Licence Agreement would allow for TRE and GE to enter into a technology partnership

for locomotive overhauls and modernizations, with GE being the prime contractor and TRE the sub-contractor.

EMD:Spare partsContract Value:R550 million

GE: 100 Loco dealContract Value:R2.6 billion

50 “Like new” locomotives

• 50 “Like-new” programme now complete under the equivalent of the CSDP Framework using Transnet Rail Engineering

Strictly confidential 20

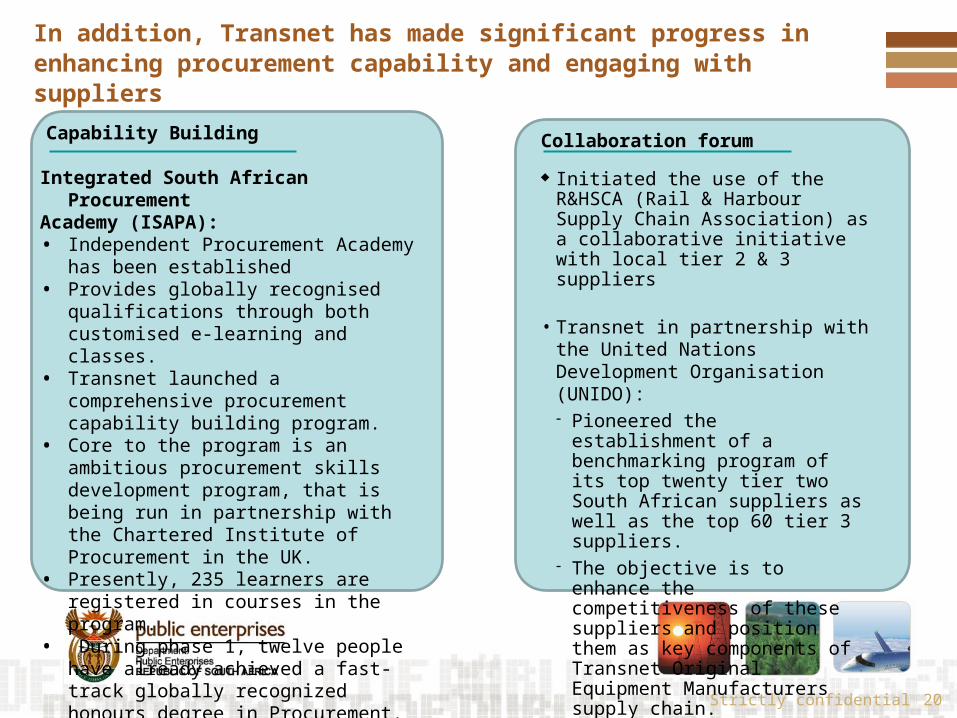

In addition, Transnet has made significant progress in enhancing procurement capability and engaging with suppliers

Integrated South African Procurement

Academy (ISAPA): • Independent Procurement Academy

has been established• Provides globally recognised

qualifications through both customised e-learning and classes.

• Transnet launched a comprehensive procurement capability building program.

• Core to the program is an ambitious procurement skills development program, that is being run in partnership with the Chartered Institute of Procurement in the UK.

• Presently, 235 learners are registered in courses in the program.

• During phase 1, twelve people have already achieved a fast-track globally recognized honours degree in Procurement.

Capability Building Collaboration forum

Initiated the use of the R&HSCA (Rail & Harbour Supply Chain Association) as a collaborative initiative with local tier 2 & 3 suppliers

• Transnet in partnership with the United Nations Development Organisation (UNIDO): Pioneered the establishment of

a benchmarking program of its top twenty tier two South African suppliers as well as the top 60 tier 3 suppliers.

The objective is to enhance the competitiveness of these suppliers and position them as key components of Transnet Original Equipment Manufacturers supply chain.

Strictly confidential

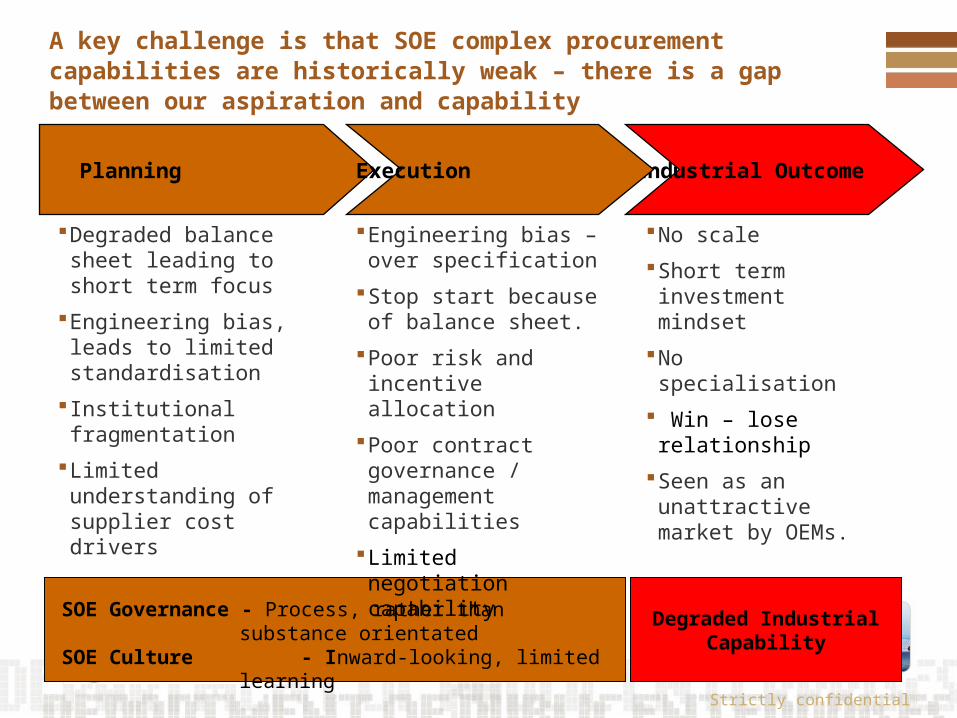

A key challenge is that SOE complex procurement capabilities are historically weak – there is a gap between our aspiration and capability

Planning

Degraded balance sheet leading to short term focus

Engineering bias, leads to limited standardisation

Institutional fragmentation

Limited understanding of supplier cost drivers

No scale

Short term investment mindset

No specialisation

Win – lose relationship

Seen as an unattractive market by OEMs.

Industrial OutcomeExecution

Engineering bias – over specification

Stop start because of balance sheet.

Poor risk and incentive allocation

Poor contract governance / management capabilities

Limited negotiation capability

SOE Governance - Process, rather than substance orientatedSOE Culture - Inward-looking, limited learning

Degraded IndustrialCapability

Strictly confidential

The fleet or programmatic procurement process was developed to ensure that the impact of key strategic procurements are optimised.

• Development and disclosure of long term fleet plans Fleet refers to any long term equipment of a similar function

that is essential to maintain an operation or service.

• A standardisation strategy needs to accompany the fleet plans.

• A credible funding mechanism needs to be in place to support the procurement plan giving suppliers a reasonable degree of certainty that the program will be sustained.

• Supplier industry consolidation, often associated with the selection (or establishment) of a national capability champion to lead investment in a capability.

• The ability to structure and manage the procurement of complex systems that include technology transfers and investment in industrial capability.

This should align policy, planning and execution in targeted fleets

Presently, none of these fundamentals are in place

Imperative to have an institutional mechanism to quality control the process!!!!

Strictly confidential

A draft policy has been developed based on managing the quality of the procurement process

• The policy was formulated based on the gateway review system to ensure quality control.

• Three policies were developed a programmatic policy ,a transactional policy and an innovation policy

• The policy focuses on the crucial elements that need to be addressed but allows for flexibility to reach these decisions

• The policy is supplemented by guidelines to guide implementation

Step 3: Formulate policy• The policy provides a definition of the information required by decision

makers, who will be organised in review panels, at key milestones or moments in the relevant process

• The review panels will have the responsibility of evaluating the rigour and coherence of the commercial and developmental case presented before giving a mandate for the procurement to continue

• Depending on the nature of the transaction there are 3 key processes that can be followed each with different milestones:

1

2

3

Programmatic Process

Transactional Process

Testing for Innovation

Strictly confidential

The objective of the programmatic / fleet policy is to enable long-term fleet procurement with significant developmental impacts

The comprehensive and rigorous identification of developmental impacts that justifies the funding support and risks associated with undertaking the procurement

The management of the quality of the procurement process through an external review panel.

The provision of financial support for the procurement by government or related institutions so as to go beyond the funding abilities of the balance sheet of the buying institution

The identification and containment of risks that go beyond the normal planning horizon of the commercial entity such as those related to the length and scale of the procurement and the industrialisation process

The systematic provision of required support by government to ensure the achievement of the vision

1

Strictly confidential

The objective of the transactional policy is to integrate supplier development concerns into all procurements where there is value leverage

The transactional process addressed both strategic procurement and ‘catch-all’ transactions

Strategic procurement refers to transactions which have a shorter duration than programmatic procurements (short to medium term) but can still address investment in in plant and/or technology to develop supply chain around a particular industry

These transactions are generally constrained by the funding ability of the buying institution but targeted government support can still be obtained for the development of advanced industrial capabilities

Catch-all are transactions that by virtue of their scale can be used to encourage supplier development. Therefore the focus is generally on investment in technology or skills that enhance existing capability but will not lead to development of the supply chain around a particular industry

Source: Team Analysis

2

Strictly confidential

• Various initiatives such as CSDP and Enterprise Development currently exist where SOEs are involved in supplier development via their procurement spend.

• This type of involvement takes place through formalised procurement processes.

• Many local suppliers may not have opportunities to compete because their products may not have been formally tested or are still in the conceptual design

• Therefore in order to support these local suppliers the SOE could assist by providing them with an operational testing platform for their products.

• This will require support from the dti and DST allow suppliers to develop their product as an enterprise development project, enabling them to participate in the procurement processes of SOEs in the future.

26

The objective of the innovation policy is to allow for testing of a local product within an operational environment

Source: Team Analysis

3

Strictly confidential 27

A centre of excellence will be established to support organisations undertaking complex procurement

The centre of excellence will be responsible for:

Supporting the selection an external review panel

Provide focused support for fleet procurements – particularly in understanding of the relevant global and national supplier community.

Creating a mechanisms for knowledge accumulation and sharing across transactions

Conducting benchmarking of procurement capability

To provide support and facilitate training on complex procurement

Strictly confidential

Transnet need to replace its aging locomotive fleet through a long term fleet procurement which will provide a platform of stable demand to re-establish a viable local industry

28

Benefits to Transnet• Improved availability and

reliability• Lower maintenance costs and

faster turnaround through standardisation

• Facilitate movement from road to rail

• Transnet’s primary (diesel) and secondary (electrical) carbon footprint will be reduced

Loco Fleet Age

0

50

100

150

200

250

300

350

0 10 20 30 40 50

Age - Years

Nu

mb

er

by T

yp

e

Avg age 33

years

Desired Age

Need to procure 120+ locomotives a year to provide a critical mass for industrialisation

Strictly confidential

To sustain the current locomotive fleet requires an additional 70 locomotives per annum

29

Major runouts are expected between 2014/15 – 2018/19 and 2019/20 – 2027/28

Based on 30 year life approximately 70 locomotives are required per annum to sustain current fleet

From 2014/15 the runout increases to around 700 locomotives in five years which equates to approximately 140 locomotives per year.

This accords with the historical procurement pattern

High runout rate predicates extending locomotive life to 45 years

2 400

2025

2024

2023

2022

2021

2020

2019

2018

200

2017

2016

2015

600

2014

2008

2012

1 200

2011

2010

2 200

1 400

400

800

1 800

1 600

2007

2009

0

2 000

1 000

2013

No. of locos required To sustain fleet (2007-2025)No. per year

Source: TFR loco fleet plan

Strictly confidential

Government also needs to consider the positive externalities of goods going by rail, rather than road.

30

• Total road externalities of around R34bn per annum• Road costs 5x the ton per km than rail

Road Externality Costs

Strictly confidential31

Lifecycle Cost

Industrial-isation

Opportunity Cost

Standardisation•Higher standardisation leading to larger demand and lower LCCs through inter-operability, lower maintenance costs, less specialised skills..

Capital Cost•The initial cost of the locomotive

Lifecycle cost•The total cost of the locomotive over its lifecycle including energy, maintenance and operating costs.•The speed of absorbing a technology into the system.

Industrialisation•The capability and capacity of the domestic locomotive manufacturing & service industry to “absorb” a technology.•The ability to use capabilities for manufacture in different applications•The ability to compete in global supply chains

Source: Team Analysis

Opportunity Cost

•The cost to the company in lost revenue due to the non-availability, delay or cancellation of trains

•The cost of customers moving from rail to other forms of transport due to poo rperception of rails reliability

The decision on what models to buy for the fleet is extremely complex and strategic!!!

Strictly confidential

Standardisation •Low standardisation due to small purchases linked to donor aid

32

• Low Cost Locomotives• Link to Donor AidCapital

Cost

Lifecycle Cost

Industrial-isation

Opportun-ity Cost

• Small purchase numbers make localisation unfeasible

• Low technology parts which are easy to localise

• No export potential as parts are build using existing industrial capability

• Limited benefits to other industrial sectors as capabilities already exist

• High LCC driven by low availability

• Low cost spare parts required frequently

• Locomotives are fuel inefficient and have very high emissions

• Lack of standardisation drives up cost of training, operations, maintenance

• Low OC due to low utilisation of rail network

• E.g. delay or cancellation of trains has little impact on company or its reputation

Source: Team Analysis

High life cycle costs may make sense is certain contexts…

Strictly confidential

33

Through the programmatic fleet procurement, the supplier industry can be significantly developed

Current Localisation Breakdown for LocomotivesPercentage of Loco Value (%)

Total

100,00

Not Feasibl

e to Localis

e

15,00

Future Potenti

al to Localise

43,39

Localisable

8,18

Local Conten

t

33,43

ILLUSTRATIVE

Strictly confidential

SOE procurement leverage and the locomotive fleet procurement are cornerstones of the IPAP strategy – a more robust governance mechanism is required to enhance impact.

34

• Joint DPE – dti - ED Ministerial oversight of the over-arching roll-out of the supplier development process required to enhance accountability and support – quarterly meetings with the CEO of Eskom and Transnet.

• Collaborative operational committee put in place with SOE Supplier Development Champions (nominated by CEOs) which will meet to:

– Assess progress– Assist in the removals of obstacles.– Develop support program

• By the end of September, both Transnet and Eskom will have prepared their next generation supplier development plans

• It is proposed that the Oversight Committee calls for a presentation of these plans