Embed Size (px)

DESCRIPTION

Analysis of Bangladesh stockmarket crash and recommended capital markets reforms

Citation preview

BRIEFING NOTE ON STOCK MARKET REFORMS FOR BAPLC SUBMISSION TO IBRAHIM STOCKMARKET ENQUIRY

(Ifty Islam, AT Capital and Ahsan Mansur, Policy Research Institute)

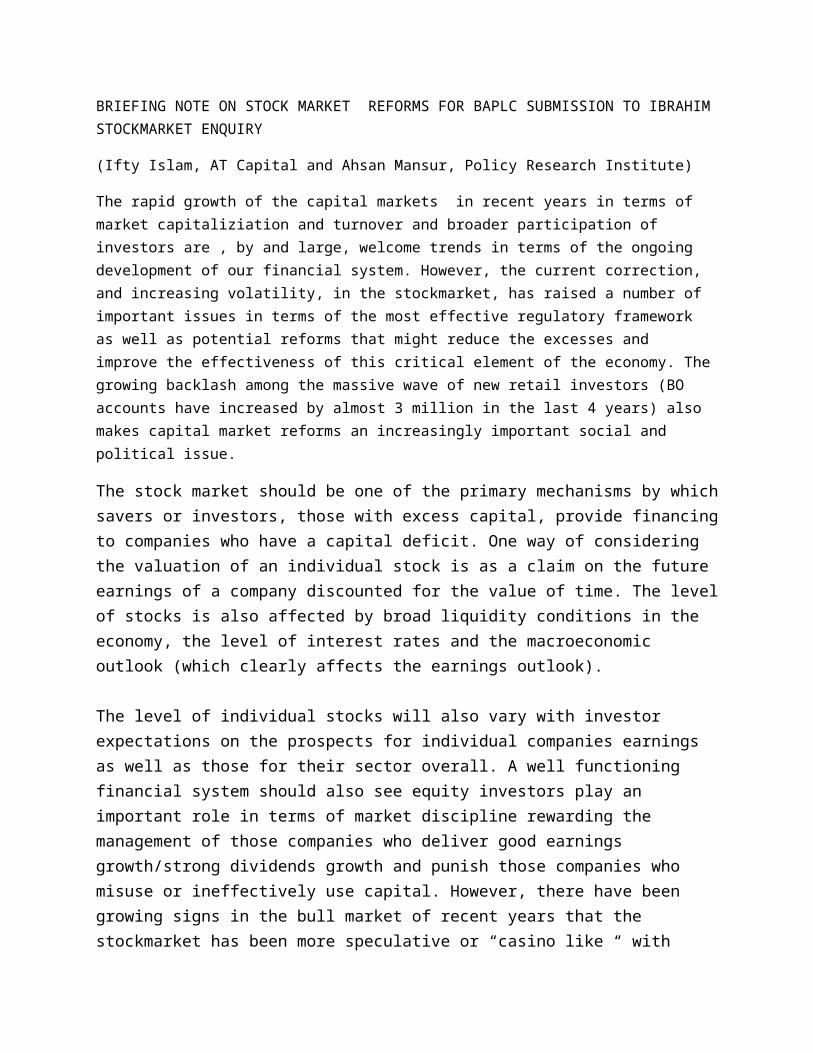

The rapid growth of the capital markets in recent years in terms of market capitaliziation and turnover and broader participation of investors are , by and large, welcome trends in terms of the ongoing development of our financial system. However, the current correction, and increasing volatility, in the stockmarket, has raised a number of important issues in terms of the most effective regulatory framework as well as potential reforms that might reduce the excesses and improve the effectiveness of this critical element of the economy. The growing backlash among the massive wave of new retail investors (BO accounts have increased by almost 3 million in the last 4 years) also makes capital market reforms an increasingly important social and political issue.

The stock market should be one of the primary mechanisms by which savers or investors, those with excess capital, provide financing to companies who have a capital deficit. One way of considering the valuation of an individual stock is as a claim on the future earnings of a company discounted for the value of time. The level of stocks is also affected by broad liquidity conditions in the economy, the level of interest rates and the macroeconomic outlook (which clearly affects the earnings outlook).

The level of individual stocks will also vary with investor expectations on the prospects for individual companies earnings as well as those for their sector overall. A well functioning financial system should also see equity investors play an important role in terms of market discipline rewarding the management of those companies who deliver good earnings growth/strong dividends growth and punish those companies who misuse or ineffectively use capital. However, there have been growing signs in the bull market of recent years that the stockmarket has been more speculative or “casino like “ with insufficient attention paid to both its primary function as a means of raising capital and

We break this report into three major sections in terms of an analysis of

1)The main drivers of the 4 year bull market in stock prices;

2) A summary of the regulatory interventions in the past 12 months, and

3) Recommended regulatory and structural reforms

WHAT DROVE THE BULL MARKET IN STOCKS?

The rally was primarily driven by four major factors:

1) Excess Liquidity Growth

2) Structural Increase in Retail Investors

3) Lack of Supply/IPOs

4) Excessive Bank Exposure to the Capital Markets

5) Regulatory Interventions Increasing Moral Hazard

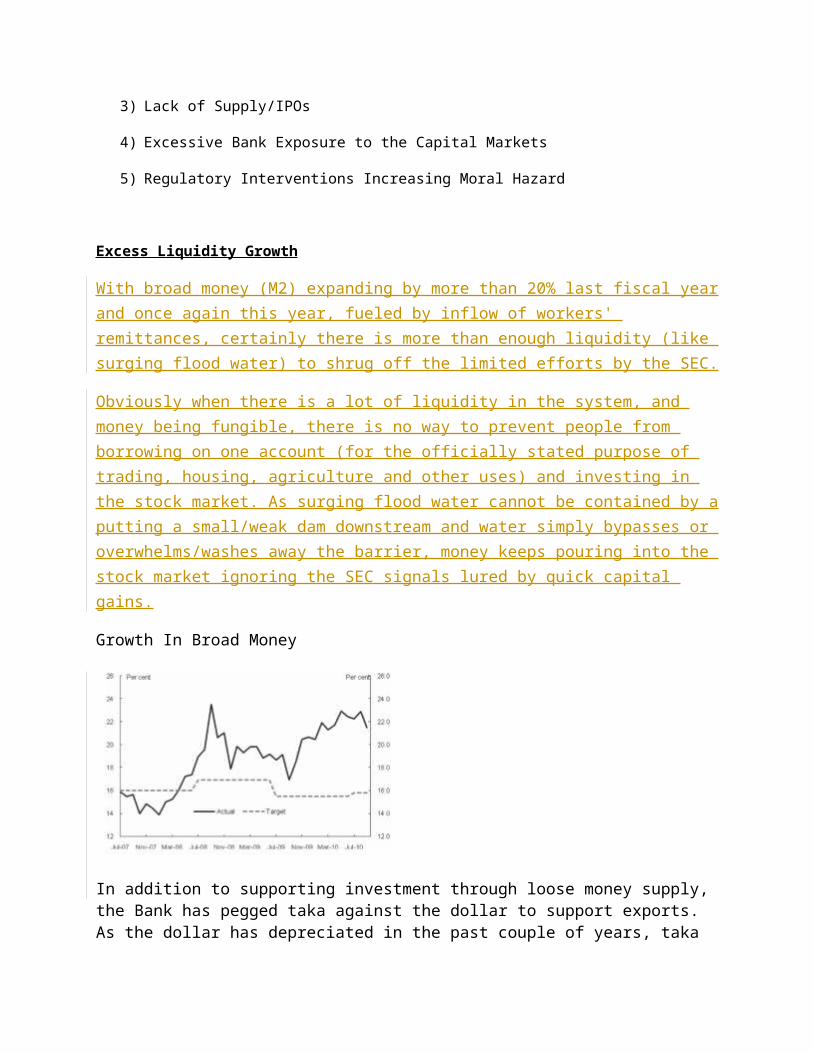

Excess Liquidity Growth

With broad money (M2) expanding by more than 20% last fiscal year and once again this year, fueled by inflow of workers' remittances, certainly there is more than enough liquidity (like surging flood water) to shrug off the limited efforts by the SEC.

Obviously when there is a lot of liquidity in the system, and money being fungible, there is no way to prevent people from borrowing on one account (for the officially stated purpose of trading, housing, agriculture and other uses) and investing in the stock market. As surging flood water cannot be contained by a putting a small/weak dam downstream and water simply bypasses or overwhelms/washes away the barrier, money keeps pouring into the stock market ignoring the SEC signals lured by quick capital gains.

Growth In Broad Money

In addition to supporting investment through loose money supply, the Bank has pegged taka against the dollar to support exports. As the dollar has depreciated in the past couple of years, taka has seen appreciation pressures. According to one analyst, had it not been for the Bank’s intervention, taka would have appreciated to 60 per dollar.4 The cost of keeping the taka undervalued has been the excess growth in money supply. As the appreciation pressure mounted on taka, money growth exceeded the target rate by ever-faster pace since late 2009. A large proportion of that extra money found its way to the stock market. With no commensurate rise in the supply of shares, increased turnover meant rapidly increased share prices.

The budgetary provision in 2009 to allow whitening of undisclosed money into the stock market also played an important role in flooding the market with liquidity.

Structural Increase in Retail Investors

According to Centre for Policy Dialogue's (CPD) analysis, the total number of beneficiary owners' (BO) account holders was 3.21 million on December 20 last year. This compares with less than 500,000 less than 3 years ago. The opening of brokerage houses at the district level (238 brokerage houses of DSE opened 590 branches at 32 districts), arranging a countrywide

'share mela (fair)' and introducing interest-based trading operation, easy access to market information, were some of the factors identified by the CPD that accelerated the flow of investors.

Lack of Supply

Some estimates have suggested that more than 80 % of corporate Bangladesh has yet to be listed. Moreover, even for those companies that are listed, many have a relatively limited free float. As a result, excess liquidity finding itself into to the stockmarket has had an exaggerated impact on stimulating asset prices and exacerbating the bubble due to a supply/demand imbalance. In 2010 there were only 6 IPOS and two direct listings. Expectations for additional IPOs from State-Owned Companies (SOEs) failed to materialize as did further listings from other Telecoms companies.

Excessive Bank exposures to the Capital Markets

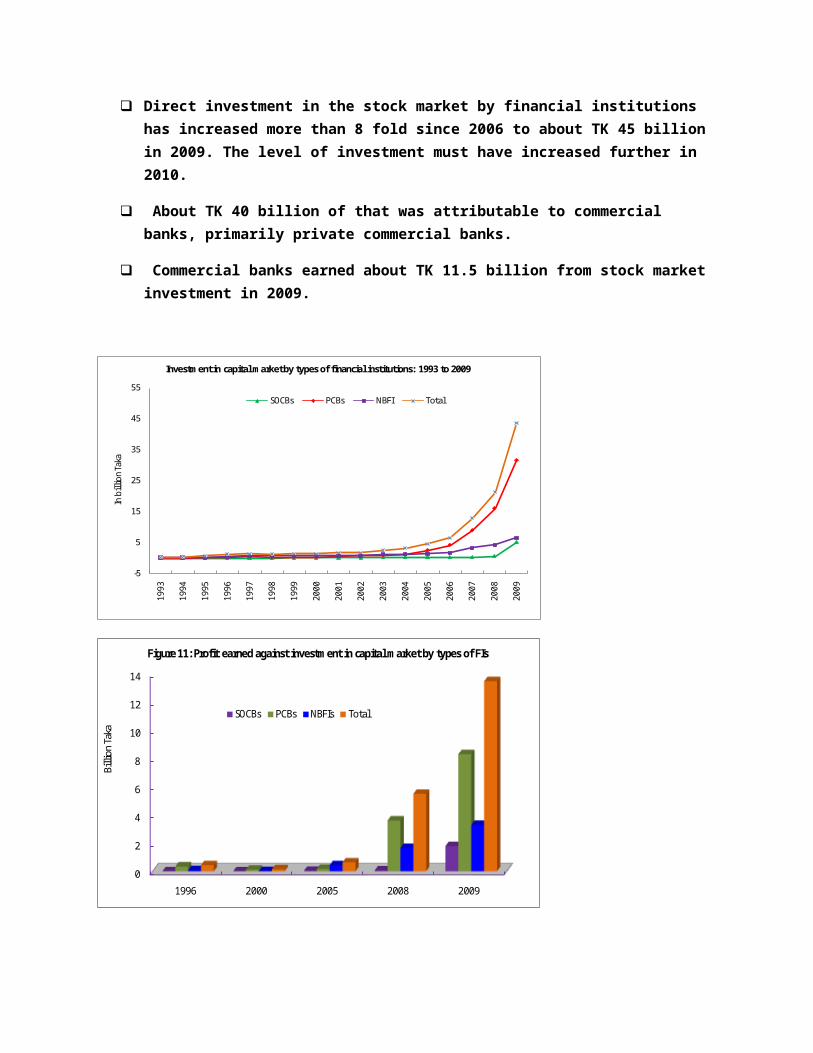

Direct investment in the stock market by financial institutions has increased more than 8 fold since 2006 to about TK 45 billion in 2009. The level of investment must have increased further in 2010.

About TK 40 billion of that was attributable to commercial banks, primarily private commercial banks.

Commercial banks earned about TK 11.5 billion from stock market investment in 2009.

-5

5

15

25

35

45

55

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

In b

illio

n Ta

ka

Investment in capital market by types of financial institutions: 1993 to 2009

SOCBs PCBs NBFI Total

0

2

4

6

8

10

12

14

1996 2000 2005 2008 2009

Billi

on T

aka

Figure 11: Profit earned against investment in capital market by types of FIs

SOCBs PCBs NBFIs Total

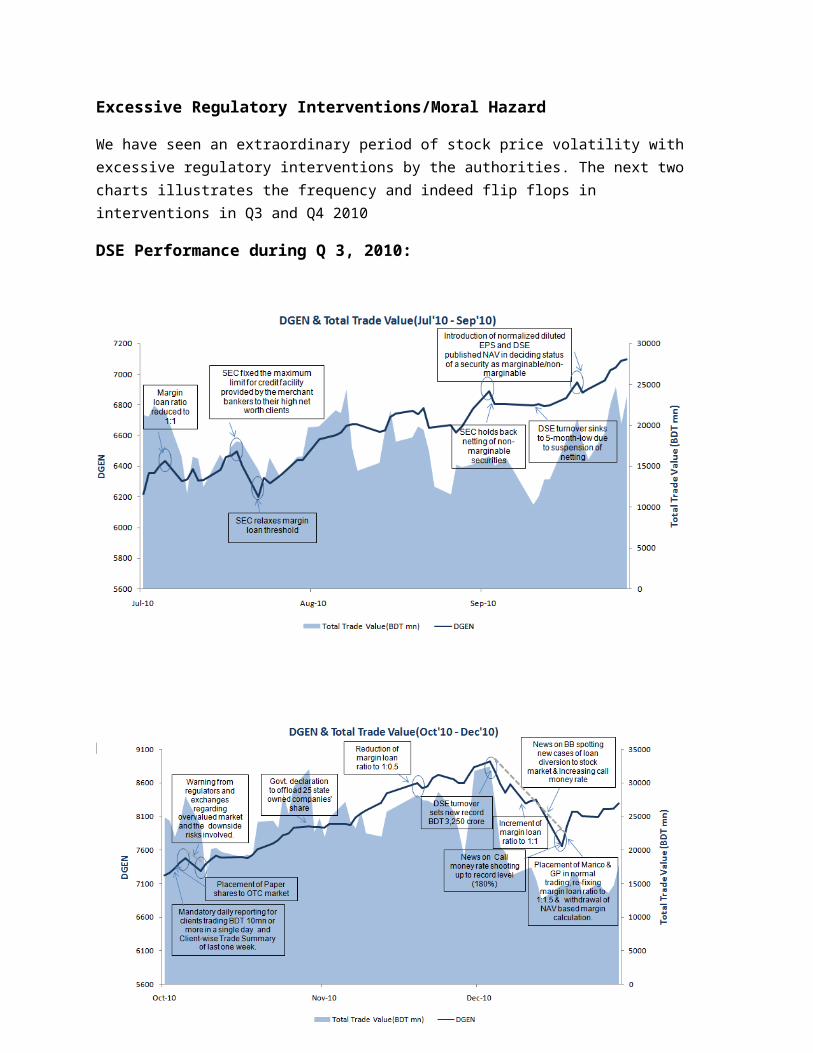

Excessive Regulatory Interventions/Moral Hazard

We have seen an extraordinary period of stock price volatility with excessive regulatory interventions by the authorities. The next two charts illustrates the frequency and indeed flip flops in interventions in Q3 and Q4 2010

DSE Performance during Q 3, 2010:

DSE Performance during Q 4, 2010:

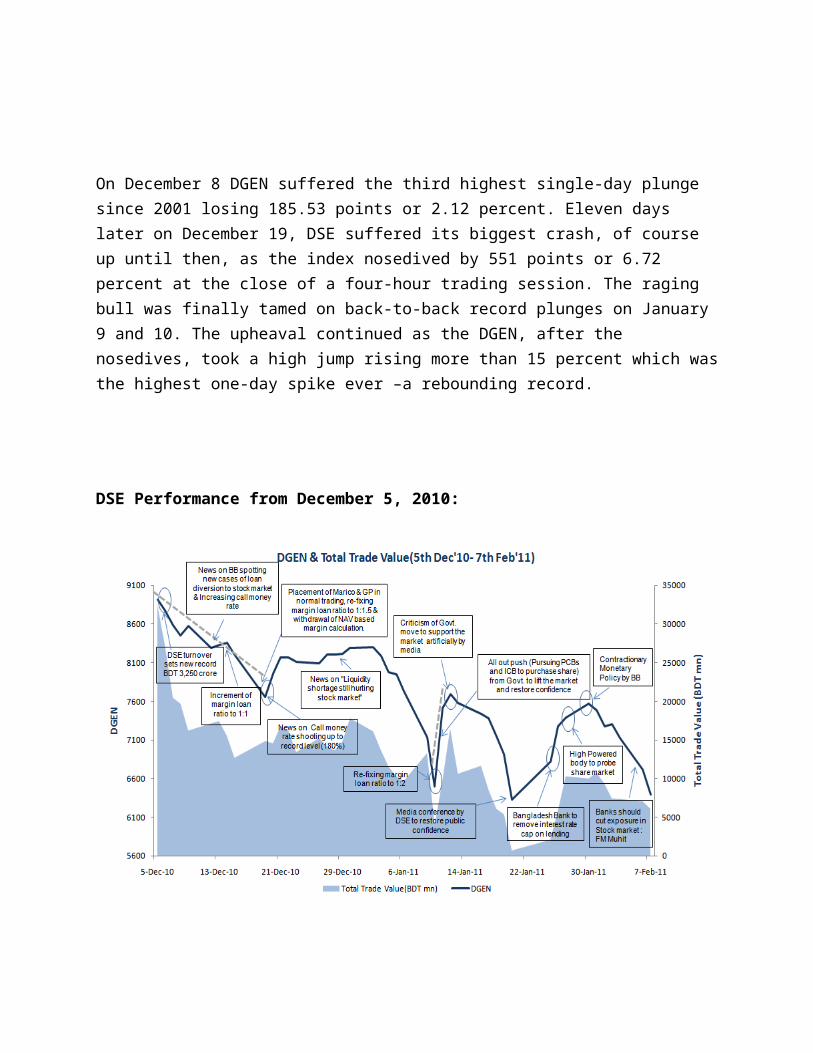

On December 8 DGEN suffered the third highest single-day plunge since 2001 losing 185.53 points or 2.12 percent. Eleven days later on December 19, DSE suffered its biggest crash, of course up until then, as the index nosedived by 551 points or 6.72 percent at the close of a four-hour trading session. The raging bull was finally tamed on back-to-back record plunges on January 9 and 10. The upheaval continued as the DGEN, after the nosedives, took a high jump rising more than 15 percent which was the highest one-day spike ever –a rebounding record.

DSE Performance from December 5, 2010:

; Bangladesh Bank initiated the withdrawal of illegally invested industrial loans from the market by December 31, 2010 and raised the Cash Reserve Requirement (CRR) and statutory liquidity requirement (SLR) both to 6 percent and 19 percent respectively. The central bank circular issued on November 28, 2010 asked banks to adjust all loans, amounting Tk 10 million and above, that have been diverted to areas other than the purposes mentioned in the loan applications by December 15

However, as the market sold off in January, the SEC and Bangladesh Bank responded with a number of market supportive measures. The securities regulator increased the margin loan ratio from 1:1 to 1:1.5 and then to 1:2. SEC also restored normal trading of Grameenphone (GP) and Marico,

suspended the Net Asset Value (NAV) based margin loan calculation and execution of order relating to increased margin deposit by members of the bourses.

Are we In a Stockmarket Bubble and Lessons from 1996/7 crash

Generally a strong stock market performance is associated with strong economic fundamentals, and one should be pleased with the outcome. However, the surge in the price index and the associated increased market volatility, somehow reminds us about the boom and bust of 1996. A sudden influx of funds and a surge in retail investors are pushing the DSE index forward without regard to economic fundamentals; the unfolding scenario is virtually a reenactment of the first part (constituting/representing the bull run) of the 1996 stock market episode. We are drawing on the 1996 episode, since lessons of 1996 is very much relevant today.

During the second half of 1996, the DSE all share index increased by 139 per cent, a robust growth by any measure, fueled by the herd mentality of the non-professional retail investors and a huge influx of funds. Participants in the overheated market were aggressively chasing a few available stocks. The hike in market capitalization and market turnover were also aberrant as the number of listed companies and available shares of good companies remained almost unchanged during this period. During June to November 1996, the DSE all share price index increased more than three folds from 959 to 3065 or by 220%!

The newly elected government of that time, initially misinterpreted this formation of the stock market bubble as fundamental strength of the economy and a manifestation of people's confidence in the new government. However, policymakers' enthusiasm was short-lived and was soon replaced by concerns about the demise of the bubble and the impending market crash. When the market index more than doubled in one month to 3000 in October 1996, efforts were made to stabilize the market, but it was too little and too late. As the bubble busted in November 1996, the DSE general index collapsed to its post-peak lowest level of 957 in April 1997, stabilizing at about the same level where it was some 10 months back (See Fig 1). By the end of April 1997, the stock market price index plunged by almost 70% from its peak of November 1996.

During this bubble period only few traders and market manipulators who had knowledge and inside information gained, while general investors paid heavily. The bear market that started with the busting of the bubble lasted for seven years, the DSE general index rarely crossing the 1000-point mark during this period. The market started a recovery from April 2004, when it was fairly underpriced with the average price-earnings ratio at about 10, and thereafter the DSE index steadily gained through July 2009.

No two bubble episodes are exactly the same across countries or across time. A sharp rise in stock prices does not necessarily mean formation of a bubble. Stock prices may also rise across the board when something change fundamentally in the economy or in the economic outlook, such as the developments in the Spanish and Irish stock markets on the eve of their joining the European Union (EU). Such price surges cannot be characterized as bubbles since the indices may stabilize at their new high levels with earning potentials realized over time. However, generally most stock market bubble episodes have some common characteristics. Some of these characteristics include: exuberant demand manifested through weak correlation between price and economic value; high price volatility; acceleration in money and

margin lending; narrow market leadership; structural weaknesses like lack of institutional investors and weak regulatory regime.

Political Economy and Moral Hazard

The current government appears determined to avoid a repetition of 1996 and the damaging political consequences and hence have tried to prop up the market.

We would agree with Jyoti Rahman’s sentiment in a recent article in the Daily Star Weekend Magazine where he noted that one might have thought that the best way of avoiding the repetition of 1996 would have been to prevent the rapid run up in stock prices that were witnessed in the monsoon and autumn of 2010. Had the SEC or the Bangladesh Bank stood firm then, perhaps a ’soft landing’ – a moderate fall in stock prices followed by a period of market stability – could have been achieved.”

But any fall in prices would have left some people worse off. And the government, it appears, was not ready to accept that. Jyoti notes that “ Every session of fall in share price was followed by thuggish behaviour in Motijheel, and caving in by the SEC. But without the expressed support of the top econocrats, it’s not surprising that the micro regulators of the SEC lacked the stomach to allow market correction."

Recommended Stockmarket Reforms

Greater Resources for the SEC in Market Monitoring/More Fundamental Research

An important role for stock market regulators is to ensure that there is transparency and a level playing field in the market, and that either companies or large investors do not trade on inside information. In increasingly complex markets, this requires substantial investment in market-monitoring technology.

As there is greater fundamental research in the marketplace, Bangladesh also needs to develop a framework to avoid analyst conflicts of interest. A lack of fundamental analysis is a recipe for a speculative capital market that is news-driven and an inefficient allocator of capital to the corporate sector. But one needs to recognise the need for effective regulations to avoid market manipulation and insider trading.

Transparent Balance Sheets/Lessons from Sarbannes Oxley

They also need to ensure that companies that raise capital in the market for the first time in an Initial Public Offering (IPO) do so on the basis of honest and accurate information about the state of the company's finances/balance sheet as well as the current and future prospects for the basis. A key role for market regulators should also be to ensure that companies ongoing reporting of their financial results is honest.

The United States, the largest and most sophisticated economy and capital market in the world, suffered accounting scandals as recently as 2002. Worldcom overstated its results by $ 3.9 billion resulting in bankruptcy. Energy trading giant Enron suffered a similar fate. This followed the bursting of the Tech bubble in 2000 when many internet stocks were artificially boosted by analysts publishing glowing reports that exaggerated the positive fundamentals to get more investment banking/IPO business for their capital markets decisions.

As a result, the US Congress passed a bill, Sarbannes-Oxley (popularly known as “SOX”). Among other things, it established the Public Company Accounting Oversight Board, to provide independent oversight of public accounting firms providing audit services ("auditors"). It forced company CEOs and auditors to personally sign and imposed substantial penalties for false reporting or manipulation of accounts. It also legally mandated substantially greater resources to the SEC to ensure they had the capacity to enforce the more complex rules.

Measures to stimulate increased equity issuance in Bangladesh

Prior to the Grameenphone (GP) IPO last year, it was estimated that around 90% of corporate Bangladesh was not yet listed on the stockmarket and this was reflected in Bangladesh having a relatively low market capitalization/GDP ratio relative to India and a majority of other bourses in the region. However, there are a number of measures already underway and some others that we believe are worth considering in motivating more companies to come to market. Among others, we would highlight:

1) Fairer IPO pricing with the adoption of the bookbuilding method: One ongoing concern preventing a number of companies from listing has been what they have perceived as an inequitable IPO pricing mechanism, with the substantial premium new issues traded on listing reflecting a low valuation assigned by the regulator. In a simplified sense, companies did not have an incentive beyond the tax we highlight below to sell themselves “cheaply” on the stockmarket. However, with the adoption of bookbuilding, companies are likely to be incentivized to come to market (we summarize some of the key highlights of the bookbuilding process in Appendix 1)

2) Regulations and Tax incentives for Increased Free Float: The SEC and Ministry of Finance have come up with a series of minimum direct listing requirements. However, we would recommend that they consider amending the existing tax incentive of 10% corporate tax differential for non-financial listed companies to a differentiated tax incentive that increases the benefits for those companies over a certain size with a greater free float in the market place.

3) Accounting Irregularities as a Constraint on Listing: A more challenging and controversial issue is that some companies that understate their earnings and assets to minimize their tax liability might be dissuaded from listing given that the valuation they would receive for their company would be significantly less than a “fair” value based on a true representation of their company accounts. While one might argue there should be no exemptions that would cause moral hazard on mis-reporting of accounts, it might be worth considering a tax amnesty where those companies that chose to restate their accounts as part of a listing process would avoid fines to restate their accounts. If the tax incentives for listing were significant enough then perhaps more companies would choose to restate.

4) Development of a Mechanism whereby Companies can raise the capital they need and meet Free Float requirements: The current IPO (i.e. capital raising) listing rules and mechanism are distinct from the direct listing rules and mechanism (i.e. offloading of shares). In order to achieve benchmark free float requirements and raise the desired amount of capital, we would recommend that the mechanisms are combined whereby a company listing can both raise capital and sell shares at the same time and pricing. This would ensure that companies can raise the amount of capital they need and use the capital raised productively thus enhancing shareholder value, but also fulfill free float and stock liquidity requirements by selling shares into the market.

5) Increased Listing of State Owned Enterprises: There has been growing enthusiasm for accelerated listing of SOEs as a means of increasing supply on the stockmarket. While we believe there are merits in terms of economic efficiency as well as redressing the supply/demand imbalance in the capital markets, this is unlikely to be a short-term fix. The State Banks are likely immediate candidates for listing, but the authorities need to be careful that the companies they wish to privatize have been restructured and are financially viable before coming to market. The listings of Titas Gas, PGCB and DESCO have been received with much enthusiasm; as such, this can be extended to state-owned power plants, utilities, airports, hotels, transportation companies, jute mills, paper mills, fertilizer factories, etc.

6) Private Equity Investment: Again not a short-term solution, but private equity investors are primarily interested in exiting their non-market investments, and the favoured method in a developing economy like Bangladesh would be an IPO. So the authorities should look to encourage both the growth of the domestic PE industry as well as attract international PE investors to take stakes in BD companies.