Embed Size (px)

Citation preview

AALTO University, XBRL Finland

Helsinki, March 25, 2013

Bridging compliance and internal use: XBRL & DPM value for data organisation, sourcing and

analysis for banking and insurance entities

Michal Piechocki

2006 - 2012 © Business Reporting – Advisory Group

Introduction: Michal Piechocki

• Member | XBRL International Member Assembly

• Member | IFRS XBRL Quality Review Team

• Member | Institute of Management Accountants XBRL Committee

• Member | IBM Information Governance Council

• Subject Matter Expert | XBRL International Certification Board

• Co-author | Leveraging XBRL for Value in Organizations (IFAC & ISACA)

• Co-author | XBRL for Interactive Data: Engineering …

• Instructor | XBRL International Taxonomy Development Training

• CEO | Business Reporting – Advisory Group

Past:

• Member At Large | XBRL International Steering Committee

• Chair | XBRL International Certification Committee

• Member | IASCF XBRL Team (IASB)

2006 - 2012 © Business Reporting – Advisory Group

Introduction: BR-AG

2006 - 2012 © Business Reporting – Advisory Group

European Supervision (new architecture)

European Systemic Risk Board (ESRB)

European System of Financial Supervisors (ESFS)

Eu

rop

ea

n B

an

kin

g A

uth

ori

ty (

EB

A)

Eu

rop

ea

n I

nsu

ran

ce

an

d O

ccu

pa

tio

na

l P

en

sio

ns A

uth

ori

ty (

EIO

PA

)

Eu

rop

ea

n S

ecu

riti

es a

nd

Ma

rke

ts

Au

tho

rity

(E

SM

A)

mic

ro l

eve

l m

acro

le

ve

l

Superv

isory

colle

ges

Superv

isory

colle

ges

Superv

isory

colle

ges

until 2011

Chairperson Chairperson Chairperson

until 2011 until 2011

2006 - 2012 © Business Reporting – Advisory Group

Three pillars approach for Basel III

Basel III

Pillar I Minimum capital requirements and

Ratios For example: • Own funds • Credit, market, operational

risk requirements • Minimum capital ratios • Minimum liquidity ratios • Minimum leverage ratio • Regulatory reporting

Pillar II Risk management and

supervision For example: • Stress testing • Prudential supervision • Risk management • Capital buffers • Corporate governance • Supervisory colleges

Pillar III Market discipline

For example: • Public disclosure • Reconciliation of regulatory

capital to accounting framework

2006 - 2012 © Business Reporting – Advisory Group

Basel II

EC 2006/48 & 49 …

Country 1

NBP 1

Report 2 Report 1

------------

------------

------------

Country 3 Country 2 Country 27

NCB 2 FSA 3 NBB 27

Report 3

-----------------------------------------

-----------------------------------------

-----------------------------------------

-------------------------------------

Transition into national legislation

(national options)

European Law 9X,XX% best practices + EU

requirements

National implementation

Challenge! Relations between

information models. Necessity to introduce single rule book based on regulation (not only

directive)

Global best practices

Report 27

-----------------------------

-----------------------------

-----------------------------

-----------------------------

-----------------------------

---------------

Lack of comparability of data for CRD I-III reporting

2006 - 2012 © Business Reporting – Advisory Group

Old way of modelling COREP

at least one base item is necessary • 1 base item - 3 breakdowns (# of members: 6, 4, 4) • 4 base items - 2 breakdowns (# of members: 6, 4) • 6 base items - 2 breakdowns (# of members: 4, 4) • 15 base items - 1 breakdown (# of members: 4) • ? base items – ? breakdowns (# of members: ?) • hidden (implicit) dimensions:

– measurement - carrying amount net or gross? – consolidation scope (CRD/IFRS) – counterparty sector (e.g. debt securities issues by non-retail)

financial liabilities

total

instruments

derivatives

short positions

deposits

debt securities

issued

other

total

portfolio

held for trading

designated at FV through

P&L

measures at amortised

cost

residence (not usable)

domestic

EMU

other EU

other

2006 - 2012 © Business Reporting – Advisory Group

• which is a base item, what is a breakdown?

• alignment with design of analytical models

Old way - consequences

• each data point defined as a base item

• high total number of items

• easy to define, difficult to maintain

• significant consequences of little changes to

data model

only base items few base items, many breakdowns

• each data point defined as a base item in a combination of members of breakdowns

• lower number of items in total (Cartesian product is multiplication)

• distinguishing between base items and breakdowns not always easy

• supports maintenance: relation concept-breakdown is stable but components of breakdowns tend to change

2006 - 2012 © Business Reporting – Advisory Group

"form centric” • based on presentation that

conveys semantics (interpretation in certain contexts)

• identification of data based on location in table (i.e. Table XYZ, Row 010, Column 200)

"data centric” • explicit definition irrespective of

presentation (every term fully understood by its own with all properties included in its definition)

• identification of data based on its attributes (i.e. Type of instrument, Counterparty, Currency)

2006 - 2012 © Business Reporting – Advisory Group

information requirements (legal acts, templates and

guidelines)

definitions of business terms and their classification

valid combinatinos

$v1 = $v2 + $v3

$v1 = abs($v2 div $v3)

...

business rules and error messages

data model

§

Need for a data model

§ Business Domain Experts

IT Experts

analysis (query, comparisons, manipulation) and supervision

Processes

1 2 3

2006 - 2012 © Business Reporting – Advisory Group

held-for-trading

assets liabilities income/expense

loans

derivatives

natures

instruments

debt securities

designated at fair value

available-for-sale

portfolios Portfolio breakdown (purpose and measurement) • e.g. held for trading -

„acquired or incurred principally for the purpose of selling or repurchasing it in the near term”; includes different instruments: Derivatives, Loans, Debt securities, Equity instruments, …

Instruments breakdown: • e.g. debt instrument -

„contractual or written assurance to repay a debt”; can fall into different portfolios: Held-for-trading, Designated at fair value, Available for sale, …

assets: property, resources, goods, etc that a company possesses and controls, e.g.

financial instruments owned by a reporting entity that shall generate economic benefits

in the future

liabilities: sources of funding for company’s assets and operations, e.g. financial

instruments that have been issued by a reporting entity, thus represents an obligation

that needs to be settled in the future by a transfer of some assets (such as cash) from

the entity

income/gains or expenses/losses:

economic benefits that occurred during the period and originated

from increase/decrease in value or result on sales/purchase of a given

financial instrument

Everything is a perspective

2006 - 2012 © Business Reporting – Advisory Group

Net carrying amount of not yet unimpaired but already past due (over 180 days) debt securities held, issued in EUR by MFIs located in EMU with original maturity under one year, measured at amortised cost and relating only to business activities conduced in Spain (local business).

Categories:

Total (…)

Cash

Loans

Debt securities

Equity instruments

Tangible and intangible

Other than (…)

Counterparty sectors:

All / Not-applicable

MFIs

MMFs

MFIs other than MMFs

Central Administration

Other general government

Non-MFIs other than government

Original maturity:

All

< 1 year

≥ 1 year < 2 year

≥ 2 years

Counterparty residences:

All / Not-applicable

EMU

Other than EMU (…)

Original currencies:

All / Not-applicable

EUR

Other than EUR Locations of activities:

All / Not-applicable

EU

Other than EU (…)

Amount types:

Carrying amount

Gross carrying amount

(Specific allowances)

(Collective allowances)

Base terms:

Assets

Liabilities

Equity

Off-balance sheet

Exposures

Portfolios:

Total (…)

Fair value through profit or loss

Amortised cost

Impairment status:

All / Not-applicable

Impaired

Unimpaired

Past due periods:

All

0 days

< 180 days

≥ 180 days

Base term: Assets

Category: Debt securities

Portfolio: Amortised cost

Amount type: Carrying amount

Impairment status: Unimpaired

Past due period: ≥ 180 days

Original currency: EUR

Original maturity: < 1 year

Counterparty sector: MFIs

Counterparty residence: EMU

Location of activity: EU

Measure (metric):

Monetary

Text

Date

Time reference:

Current period end

Previous period end

Current period

Measure (metric): Monetary

Time reference: Current period end

Data point

2006 - 2012 © Business Reporting – Advisory Group

Queries based on DPM

by counterparty residence assets

SELECT SUM(factValue)

FROM allFacts

WHERE

item=″assets″ AND

portfolio=″held-for-trading″ AND

category=″derivatives″ AND

amount=″notional″ AND

ctResidence=″uk″ AND

ctSector=″credit institutions″ AND

originalCurrency=″eur″ AND

riskType=″commodity″ AND

market=″OTC″ AND

…

24.320.223,54

2006 - 2012 © Business Reporting – Advisory Group

2006 - 2012 © Business Reporting – Advisory Group

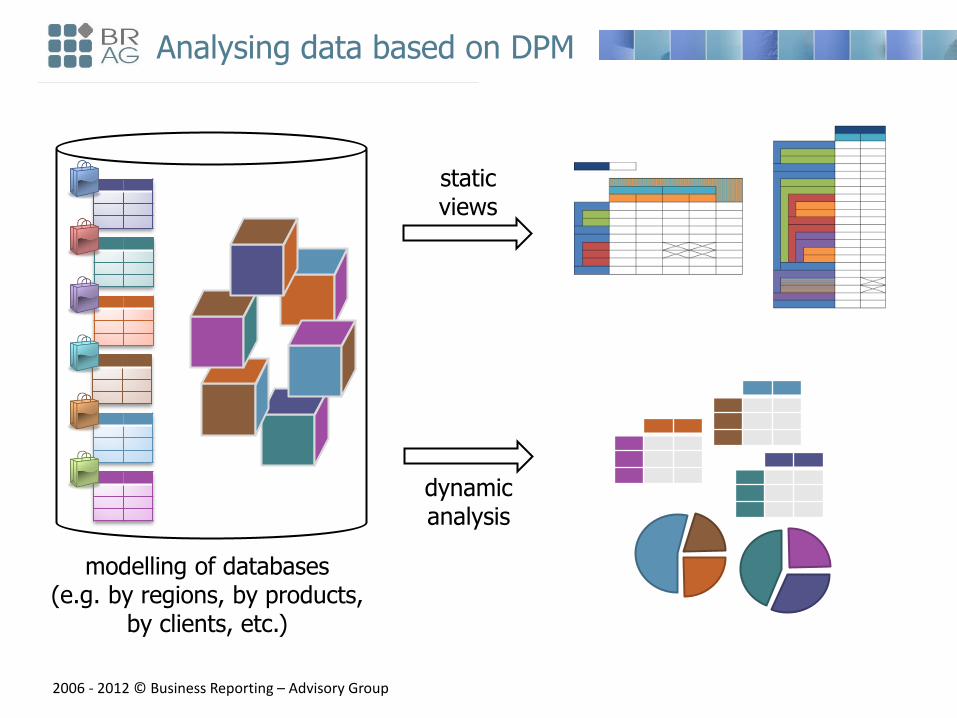

Analysing data based on DPM

static views

dynamic analysis

modelling of databases (e.g. by regions, by products,

by clients, etc.)

2006 - 2012 © Business Reporting – Advisory Group

Impact of DPM

Entity

Period

Unit

Fact

Risk type

Exposure type

Cunterparty

Data point = new point of view on fact

2006 - 2012 © Business Reporting – Advisory Group

DPM oriented data model (databases)

2006 - 2012 © Business Reporting – Advisory Group

DPM and cross-sector reporting

ECB Statistics

Percentage Intervals

Amount interval

Minimum reserve

COREP

Exposure type

Securitization type

…

FINREP

Collateral

Sector

Risk type

Impairment

Currency

Time intervals

Geographical areas

Amount type

Entity code

Main categories

Loan type

Transfer

Comprehensive income

Controling/ Non-controlling

Fair value level

Portfolio

…

FINREP rev 2

Market

Approach/Model used

Approach/Model used

SOLVENCY II

Line of business

Type of business

Diversification

Type of contract

Change in basic own funds

Type of claim

…

2006 - 2012 © Business Reporting – Advisory Group

COREP XBRL (EBA) Architecture

Conceptual level (Dictionary) + Dimensional relationships

(coherent with definitions in legal format)

Presentation relationships layer

(flexible views)

National extension

Dimensional relations Complete model

of data requirements

Presentation relations Current data requirements

Dictionary Concepts declarations, labels and

references

Data warehouse User interface

design and stability of mapping flexible views

• aim: coherency, stability, flexibility (+ simplicity and efficiency)

• aspects: implementation and maintenance (both at filer and supervisor sides)

2006 - 2012 © Business Reporting – Advisory Group

EBA development process

conv information requirements

(legal regulations)

analysis matrix (information from

annotated templates)

metadata database conversion tool

(XBRL properties)

XBRL taxonomy

XBRL taxonomy

macro

analysis and

publication

mapping and storage

exchange and

validation

DPM Architect

2006 - 2012 © Business Reporting – Advisory Group

Implementation scenarios

ERP REPORT WRITER

Portal

ERP

1. Receiver provides XBRL enabled excel, word, PDF templates

2. Outsourcing (printer, consultant, vendor to prepare reports )

3. Bolt-on (tools to transform your reports into XBRL at the last stage )

4. Integrate (build XBRL into company’s business reporting supply chain)

Portal

Portal

Portal

Benefits Challenges

• no implementation costs • need for manual work (rekeying data)

• error prone • no benefit outside of this

particular reporting context

• comprehensive support • low risk • no knowledge required

• lack of control • possibly high cost • lack of internal capabilities

• simplified approach • potential cost-saving • control over result

• comprehensive approach • cost-saving (mid-long) • control over result • automated processing • enhanced reporting • high data quality

• upfront investment • level of complication

• knowledge required • time risk • significant effort for change

update

2006 - 2012 © Business Reporting – Advisory Group

Compliance

REPORTING GATE

Webservice & validation

Data input interface & validation

REPORTING ENTITY (BANK)

RELATED ENTITY (e.g. SUBSIDIARY)

XBRL Taxonomies

XBRL

SUPERVISOR (analysis, publication)

REGULATORY AGENCIES (sharing, registry)

INVESTOR, LENDER (analysis)

FOREIGN REGULATORY AGENCY (analysis, publication)

XBRL Taxonomies

XBRL file upload & validation

Other (authentication, security, prefill, notifications)

XBRL

XBRL

XBRL

XBRL

2006 - 2012 © Business Reporting – Advisory Group

Conclusions

In internal scenarios:

• DPM can be used as a bridge allowing precise communication

• XBRL can be used as electronic information exchange standards

In external (compliance) scenarios:

• DPM allows to map internal data sources

• XBRL allows to create the final report

XBRL software:

• Disclosure management systems enabled with XBRL and DPM

• ETL mechanisms understanding DPM and using XBRL

• Validators, mappers to XBRL

Michal Piechocki, CEO

m: +48 505 558628 | o: +48 618 522277 | f: +48 618 522277

Business Reporting – Advisory Group spółka z ograniczoną odpowiedzialnością spółka komandytowa

Sniadeckich 28/5 | 60-774 Poznan | Poland

http://www.br-ag.eu | [email protected]

Contact