Embed Size (px)

Citation preview

Brazilian Banking Conference 2019 27 de Junho de 2019 São Paulo

Visão Geral Sobre o Rating Soberano Rafael Guedes, Diretor-executivo, Fitch Ratings

Agenda

1. Global Macro Outlook

2. Brazil’s Sovereign Ratings: Economic and Fiscal Profile

3. Ambitious Reform Agenda

4. What Will Fitch Monitor for Future Rating Decisions?

8

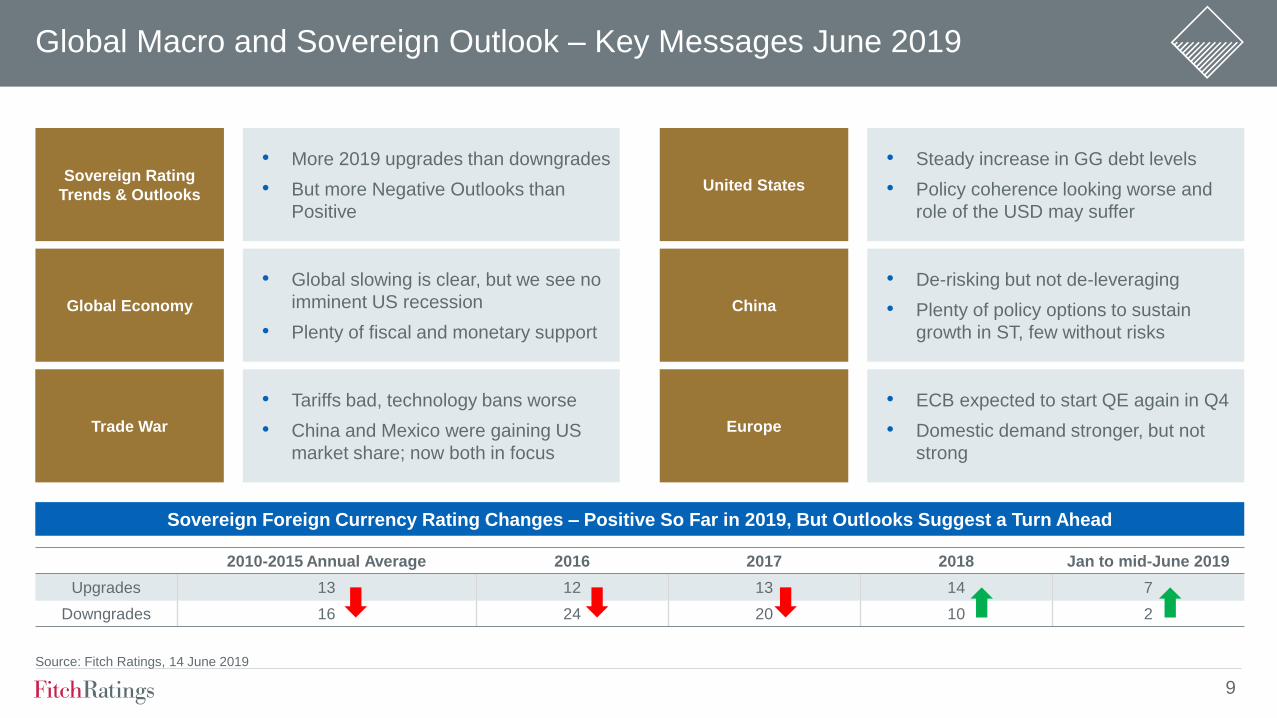

Global Macro and Sovereign Outlook – Key Messages June 2019

Sovereign Rating

Trends & Outlooks

Global Economy

Trade War

United States

China

Europe

• More 2019 upgrades than downgrades

• But more Negative Outlooks than

Positive

2010-2015 Annual Average 2016 2017 2018 Jan to mid-June 2019

Upgrades 13 12 13 14 7

Downgrades 16 24 20 10 2

Sovereign Foreign Currency Rating Changes – Positive So Far in 2019, But Outlooks Suggest a Turn Ahead

• ECB expected to start QE again in Q4

• Domestic demand stronger, but not

strong

• Tariffs bad, technology bans worse

• China and Mexico were gaining US

market share; now both in focus

• Global slowing is clear, but we see no

imminent US recession

• Plenty of fiscal and monetary support

• De-risking but not de-leveraging

• Plenty of policy options to sustain

growth in ST, few without risks

• Steady increase in GG debt levels

• Policy coherence looking worse and

role of the USD may suffer

Source: Fitch Ratings, 14 June 2019

9

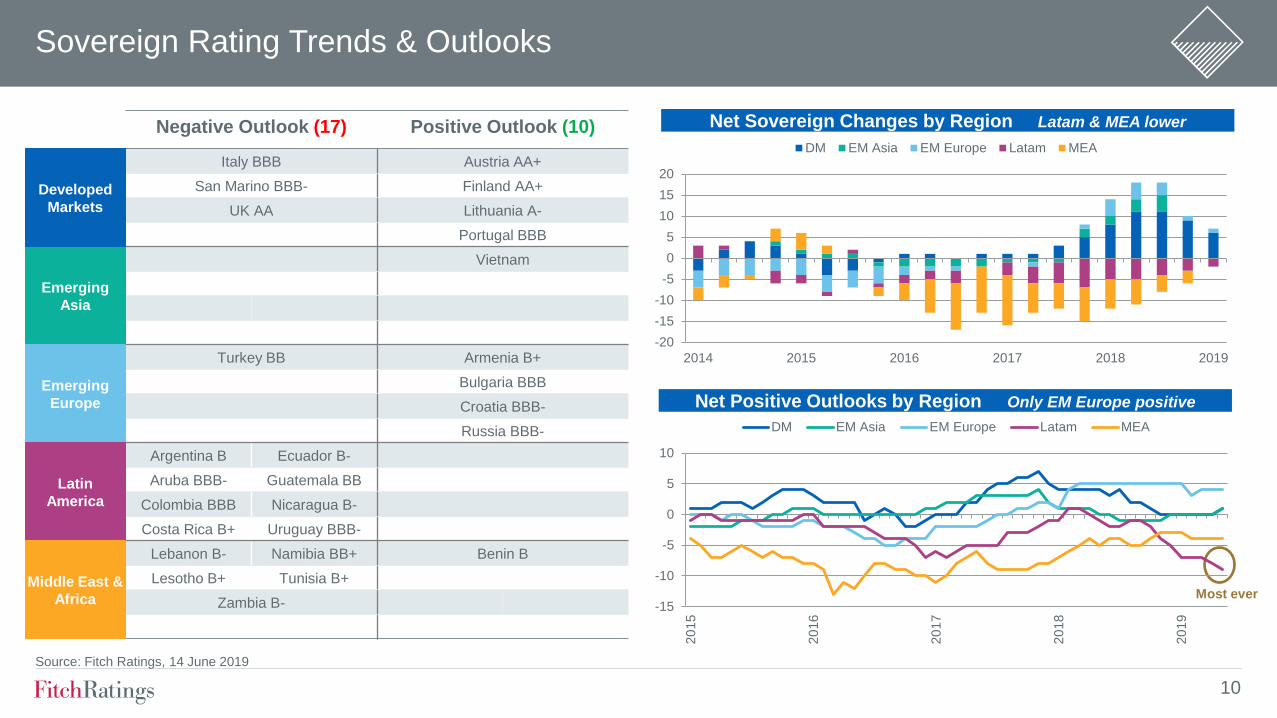

Sovereign Rating Trends & Outlooks

Negative Outlook (17) Positive Outlook (10)

Italy BBB Austria AA+

San Marino BBB- Finland AA+

UK AA Lithuania A-

Portugal BBB

Vietnam

Turkey BB Armenia B+

Bulgaria BBB

Croatia BBB-

Russia BBB-

Argentina B Ecuador B-

Aruba BBB- Guatemala BB

Colombia BBB Nicaragua B-

Costa Rica B+ Uruguay BBB-

Lebanon B- Namibia BB+ Benin B

Lesotho B+ Tunisia B+

Zambia B-

Emerging

Asia

Developed

Markets

Emerging

Europe

Latin

America

Middle East &

Africa

Source: Fitch Ratings, 14 June 2019

Net Positive Outlooks by Region Only EM Europe positive

Most ever

6.5 15.8

17.14

3.42

6.5 15.8

17.14

10.82

-15

-10

-5

0

5

10

20

15

20

16

20

17

20

18

20

19

DM EM Asia EM Europe Latam MEA

-20

-15

-10

-5

0

5

10

15

20

2014 2015 2016 2017 2018 2019

DM EM Asia EM Europe Latam MEA

Net Sovereign Changes by Region Latam & MEA lower

10

Sovereign Rating Trends & Outlooks

6.5 15.8

17.14

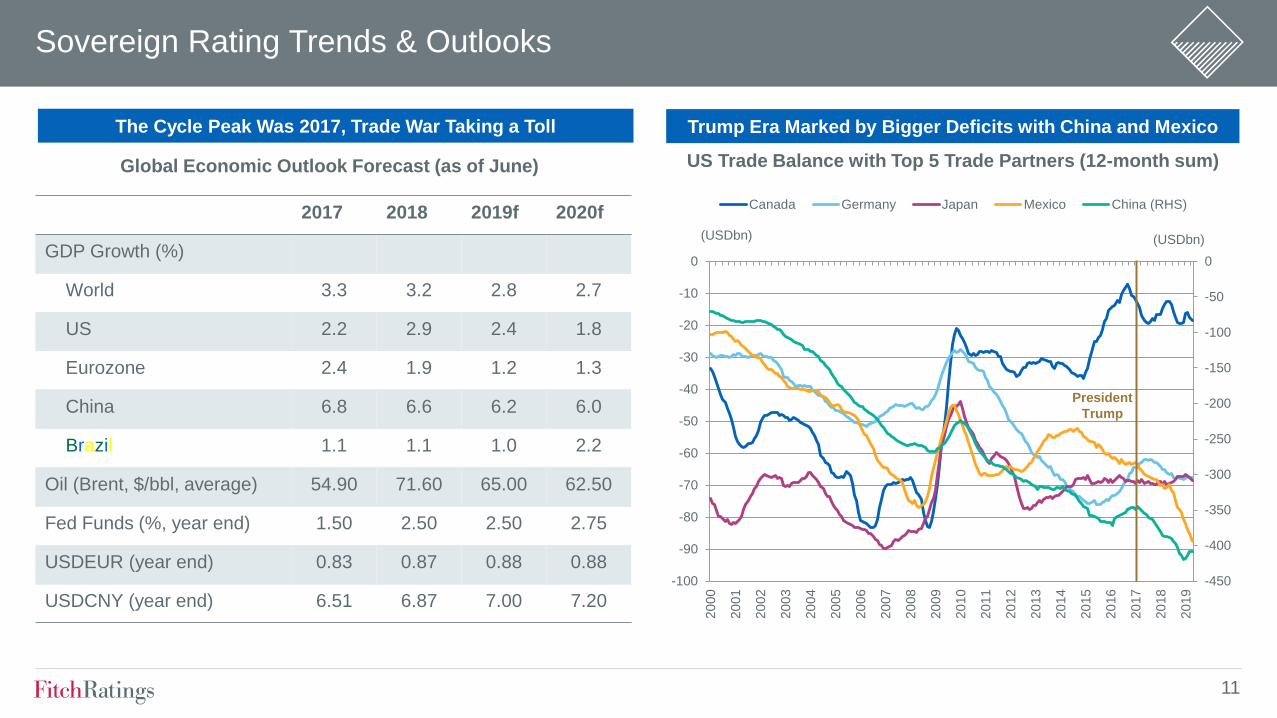

3.42 2017 2018 2019f 2020f

GDP Growth (%)

World 3.3 3.2 2.8 2.7

US 2.2 2.9 2.4 1.8

Eurozone 2.4 1.9 1.2 1.3

China 6.8 6.6 6.2 6.0

Brazil 1.1 1.1 1.0 2.2

Oil (Brent, $/bbl, average) 54.90 71.60 65.00 62.50

Fed Funds (%, year end) 1.50 2.50 2.50 2.75

USDEUR (year end) 0.83 0.87 0.88 0.88

USDCNY (year end) 6.51 6.87 7.00 7.20

Global Economic Outlook Forecast (as of June)

The Cycle Peak Was 2017, Trade War Taking a Toll

-450

-400

-350

-300

-250

-200

-150

-100

-50

0

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

(USDbn) (USDbn)

Canada Germany Japan Mexico China (RHS)

Trump Era Marked by Bigger Deficits with China and Mexico

US Trade Balance with Top 5 Trade Partners (12-month sum)

President

Trump

11

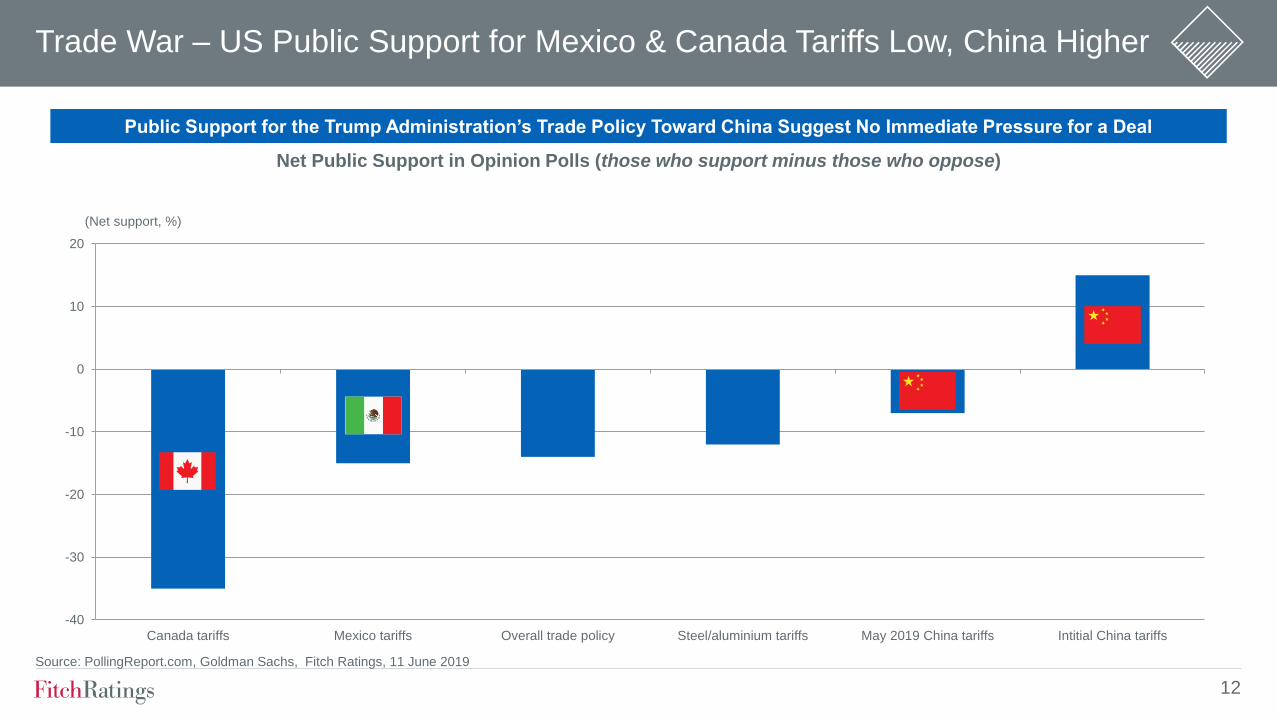

Trade War – US Public Support for Mexico & Canada Tariffs Low, China Higher

-40

-30

-20

-10

0

10

20

Canada tariffs Mexico tariffs Overall trade policy Steel/aluminium tariffs May 2019 China tariffs Intitial China tariffs

(Net support, %)

Public Support for the Trump Administration’s Trade Policy Toward China Suggest No Immediate Pressure for a Deal

Net Public Support in Opinion Polls (those who support minus those who oppose)

Source: PollingReport.com, Goldman Sachs, Fitch Ratings, 11 June 2019

12

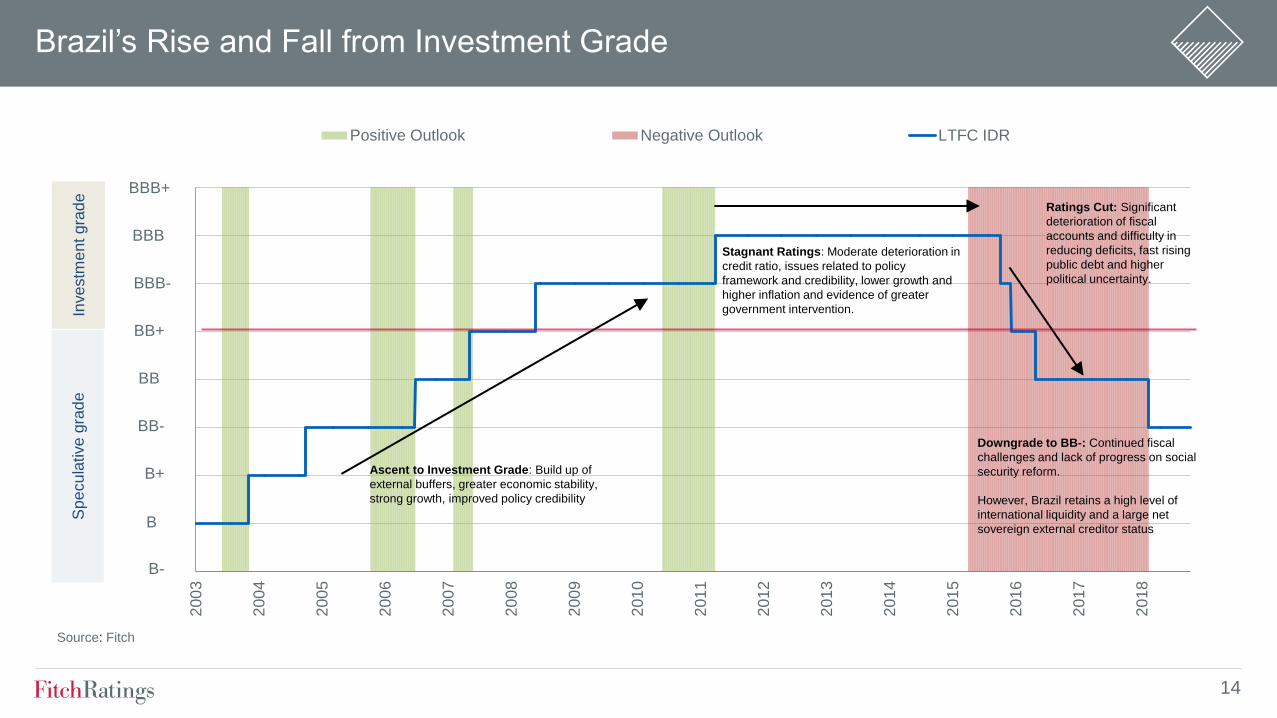

Brazil was downgraded to ‘BB-’ from ‘BB’ in 2018, with Stable Outlook.

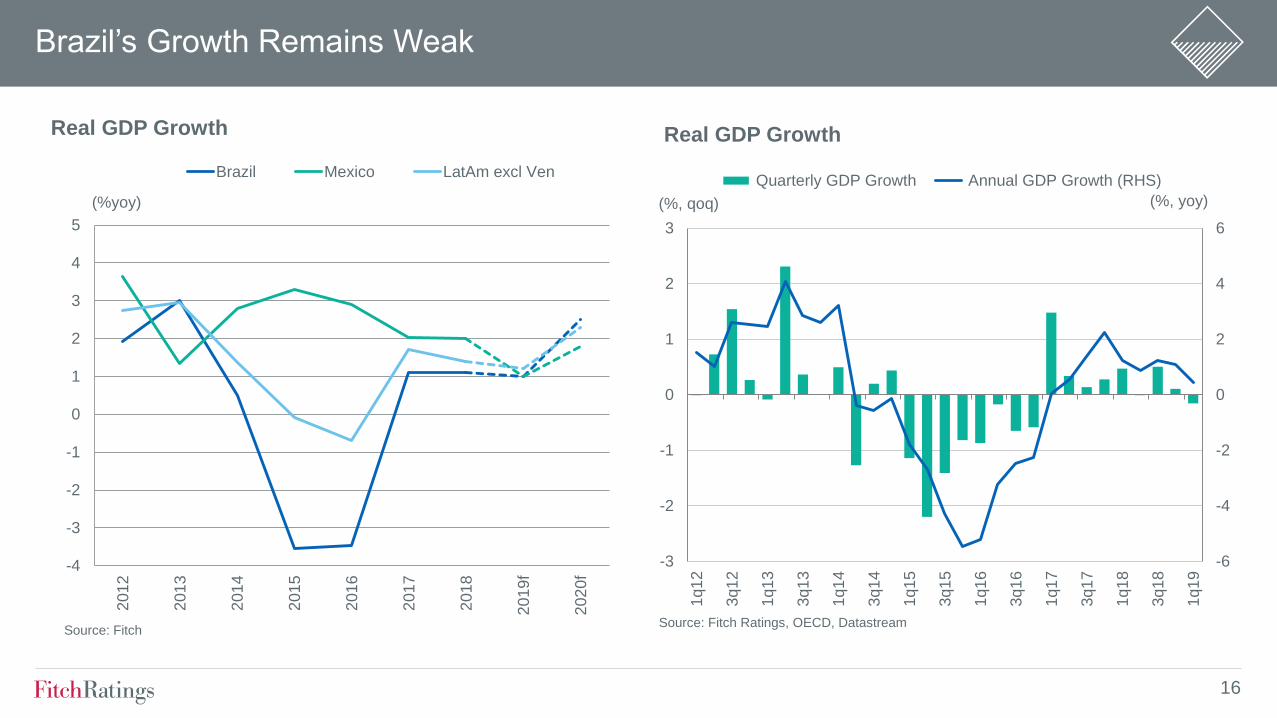

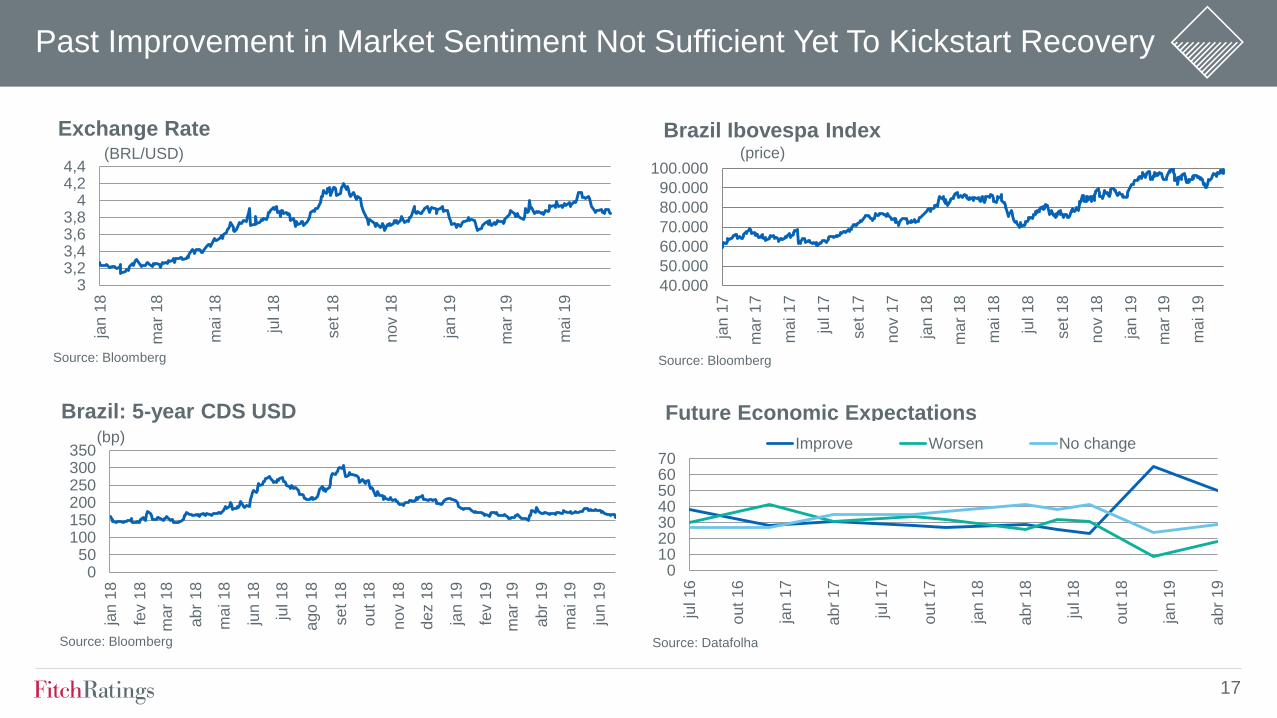

Brazil’s growth is still being challenged with Fitch forecasting growth of only 1% in 2019. Market sentiment

turned positive and confidence indicators improved after the elections. But this has not resulted in improvement

in economic activity so far. Growth performance is weak following the nation’s worst recession and fiscal

challenges persist and potential growth has been revised down.

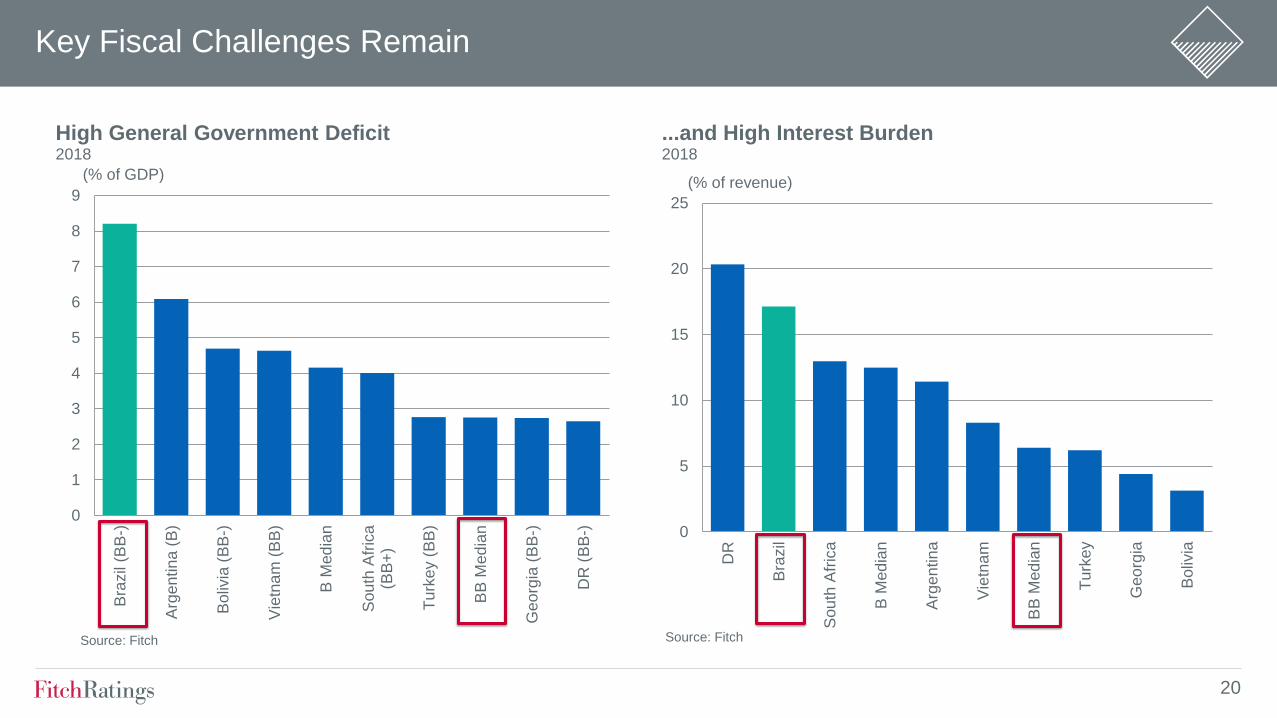

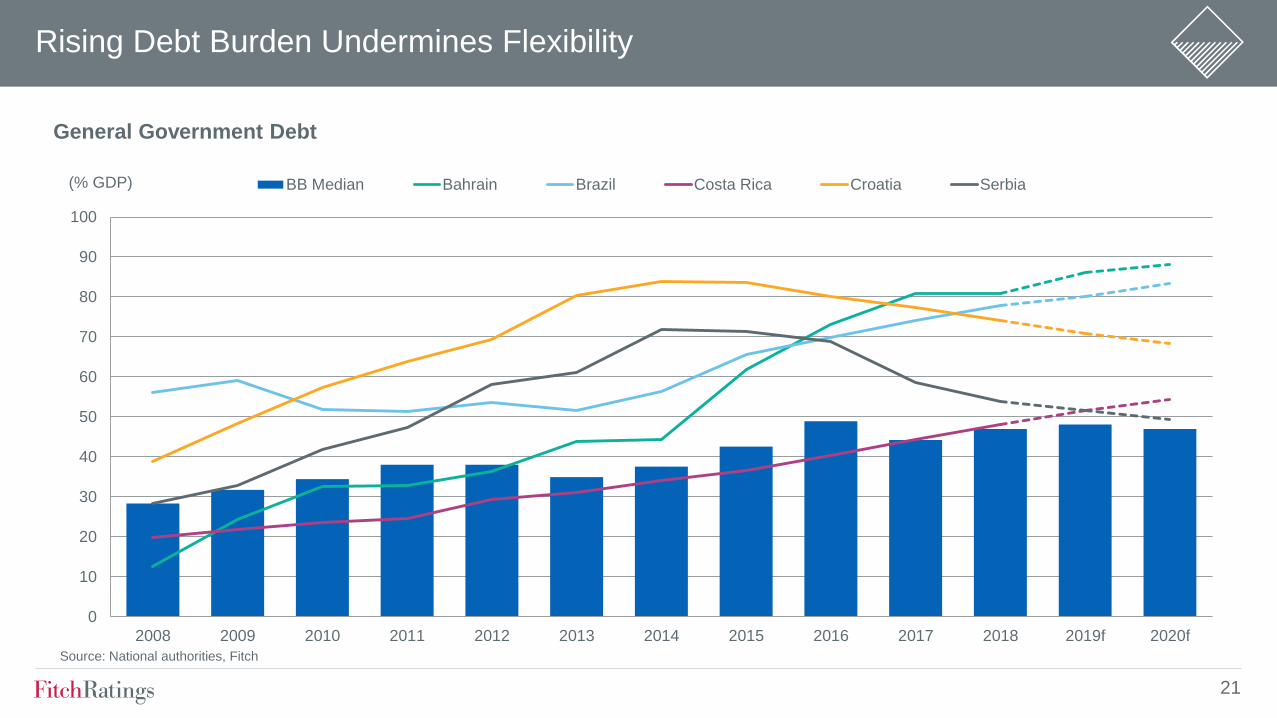

The general government deficit – at 8.2% in 2018 – is well above peers and has led to a rapidly rising debt

burden, forecast at around 80% in 2019 up from 51% in 2013.

The new government’s reform agenda, if implemented well, could be positive for growth (by addressing

structural challenges) and reducing fiscal pressures.

Progress on the implementation of the economic agenda is key, beginning with pension reform this year.

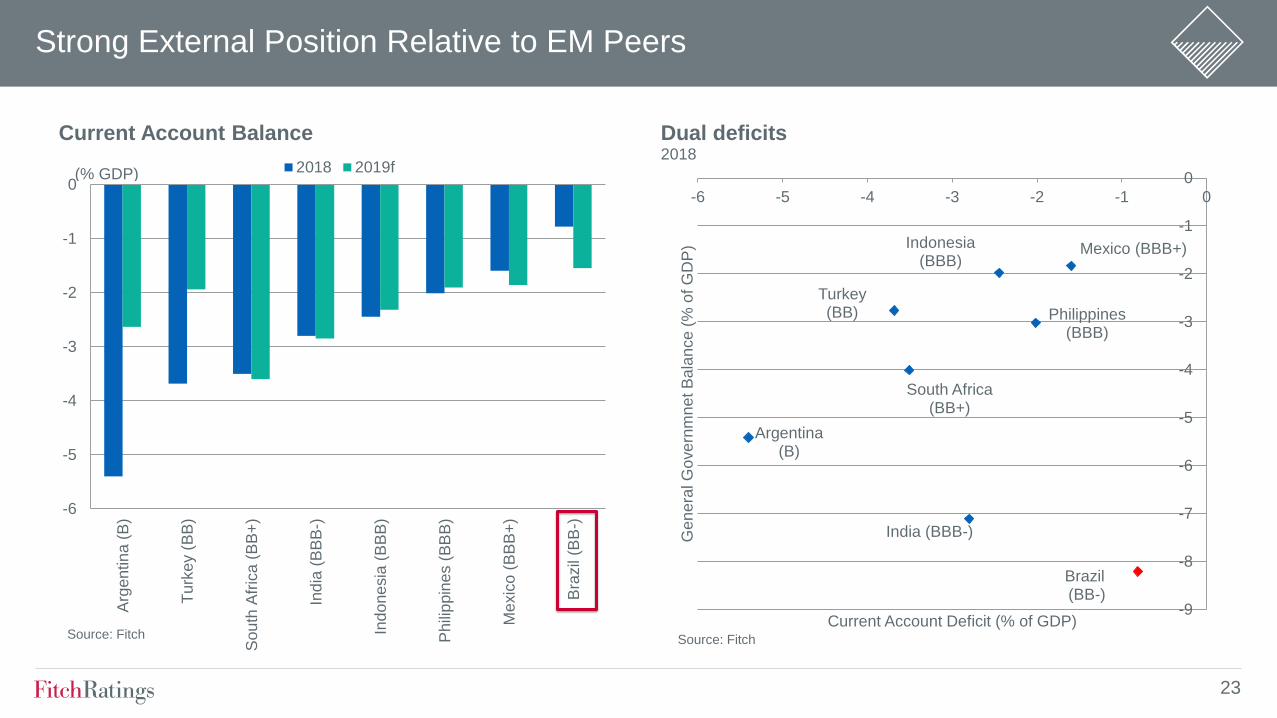

Furthermore, Brazil maintains a strong external position relative to other EM peers

Key Messages

13

Brazil’s Rise and Fall from Investment Grade

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

Positive Outlook Negative Outlook LTFC IDR

Source: Fitch

BB-

B+

B

B-

BBB+

BBB

BBB-

BB+

BB

Inve

stm

en

t gra

de

S

pe

cu

lative

gra

de

Ascent to Investment Grade: Build up of

external buffers, greater economic stability,

strong growth, improved policy credibility

Stagnant Ratings: Moderate deterioration in

credit ratio, issues related to policy

framework and credibility, lower growth and

higher inflation and evidence of greater

government intervention.

Downgrade to BB-: Continued fiscal

challenges and lack of progress on social

security reform.

However, Brazil retains a high level of

international liquidity and a large net

sovereign external creditor status

Ratings Cut: Significant

deterioration of fiscal

accounts and difficulty in

reducing deficits, fast rising

public debt and higher

political uncertainty.

14

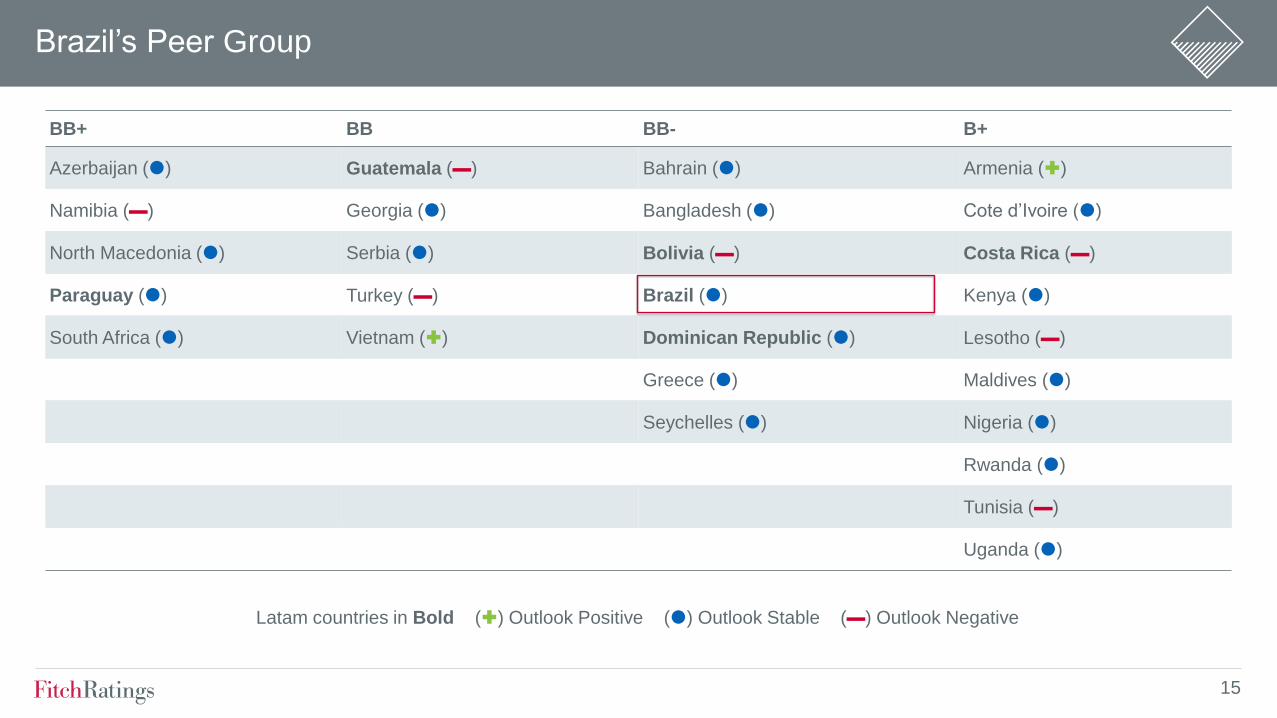

BB+ BB BB- B+

Azerbaijan () Guatemala (▬) Bahrain () Armenia ()

Namibia (▬) Georgia () Bangladesh () Cote d’Ivoire ()

North Macedonia () Serbia () Bolivia (▬) Costa Rica (▬)

Paraguay () Turkey (▬) Brazil () Kenya ()

South Africa () Vietnam () Dominican Republic () Lesotho (▬)

Greece () Maldives ()

Seychelles () Nigeria ()

Rwanda ()

Tunisia (▬)

Uganda ()

Latam countries in Bold () Outlook Positive () Outlook Stable (▬) Outlook Negative

Brazil’s Peer Group

15

Brazil’s Growth Remains Weak

-4

-3

-2

-1

0

1

2

3

4

5

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9f

202

0f

Real GDP Growth

Brazil Mexico LatAm excl Ven

(%yoy)

Source: Fitch

-6

-4

-2

0

2

4

6

-3

-2

-1

0

1

2

3

1q1

2

3q1

2

1q1

3

3q1

3

1q1

4

3q1

4

1q1

5

3q1

5

1q1

6

3q1

6

1q1

7

3q1

7

1q1

8

3q1

8

1q1

9

(%, yoy) (%, qoq)

Real GDP Growth

Quarterly GDP Growth Annual GDP Growth (RHS)

Source: Fitch Ratings, OECD, Datastream

16

Past Improvement in Market Sentiment Not Sufficient Yet To Kickstart Recovery

050

100150200250300350

jan 1

8

fev 1

8

ma

r 18

abr

18

ma

i 1

8

jun 1

8

jul 18

ago

18

se

t 1

8

out

18

nov 1

8

dez 1

8

jan 1

9

fev 1

9

ma

r 19

abr

19

ma

i 1

9

jun 1

9

Brazil: 5-year CDS USD (bp)

Source: Bloomberg

010203040506070

jul 16

out

16

jan 1

7

abr

17

jul 17

out

17

jan 1

8

abr

18

jul 18

out

18

jan 1

9

abr

19

Improve Worsen No change

Future Economic Expectations

Source: Datafolha

33,23,43,63,8

44,24,4

jan 1

8

ma

r 18

ma

i 1

8

jul 18

se

t 1

8

nov 1

8

jan 1

9

ma

r 19

ma

i 1

9

Exchange Rate (BRL/USD)

Source: Bloomberg

40.000

50.000

60.000

70.000

80.000

90.000

100.000

jan 1

7

ma

r 17

ma

i 1

7

jul 17

se

t 1

7

nov 1

7

jan 1

8

ma

r 18

ma

i 1

8

jul 18

se

t 1

8

nov 1

8

jan 1

9

ma

r 19

ma

i 1

9

Brazil Ibovespa Index (price)

Source: Bloomberg

17

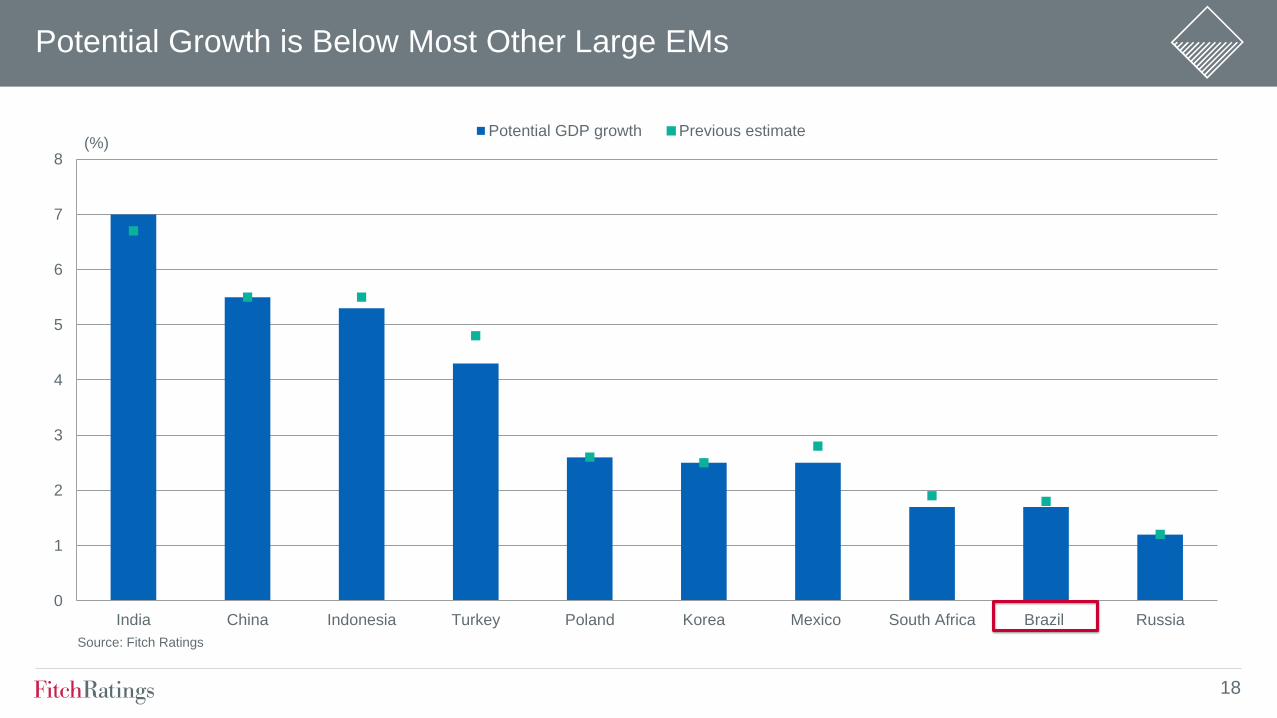

Potential Growth is Below Most Other Large EMs

0

1

2

3

4

5

6

7

8

India China Indonesia Turkey Poland Korea Mexico South Africa Brazil Russia

Potential GDP growth Previous estimate

Source: Fitch Ratings

(%)

18

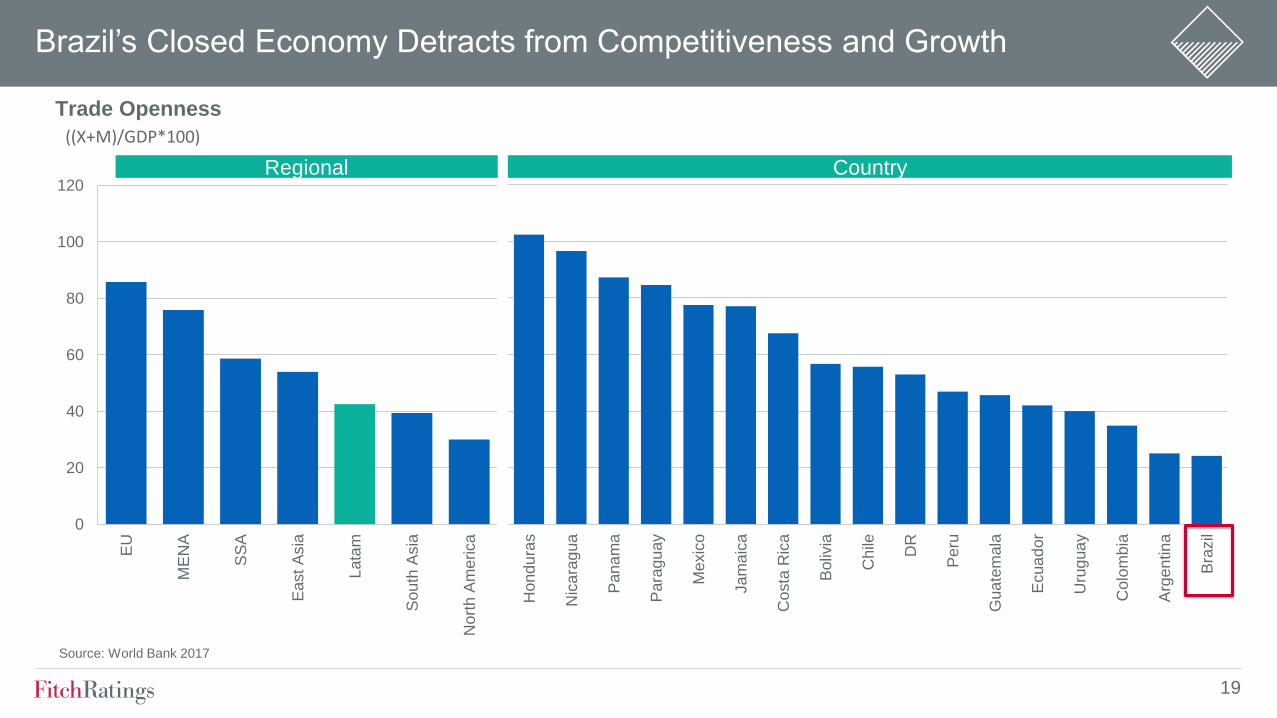

Brazil’s Closed Economy Detracts from Competitiveness and Growth

0

20

40

60

80

100

120

EU

ME

NA

SS

A

East

Asia

Lata

m

Sou

th A

sia

Nort

h A

me

rica

Source: World Bank 2017

Trade Openness

((X+M)/GDP*100)

Hond

ura

s

Nic

ara

gua

Pan

am

a

Para

gu

ay

Me

xic

o

Ja

ma

ica

Costa

Ric

a

Boliv

ia

Chile DR

Peru

Gua

tem

ala

Ecua

dor

Uru

gua

y

Colo

mb

ia

Arg

en

tin

a

Bra

zil

Regional Country

19

0

5

10

15

20

25

DR

Bra

zil

Sou

th A

fric

a

B M

ed

ian

Arg

en

tin

a

Vie

tna

m

BB

Med

ian

Turk

ey

Geo

rgia

Boliv

ia

...and High Interest Burden 2018

(% of revenue)

Source: Fitch

Key Fiscal Challenges Remain

0

1

2

3

4

5

6

7

8

9

Bra

zil

(BB

-)

Arg

en

tin

a (

B)

Boliv

ia (

BB

-)

Vie

tna

m (

BB

)

B M

ed

ian

Sou

th A

fric

a(B

B+

)

Turk

ey (

BB

)

BB

Med

ian

Geo

rgia

(B

B-)

DR

(B

B-)

High General Government Deficit 2018

(% of GDP)

Source: Fitch

20

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019f 2020f

General Government Debt

BB Median Bahrain Brazil Costa Rica Croatia Serbia

Rising Debt Burden Undermines Flexibility

(% GDP)

Source: National authorities, Fitch

21

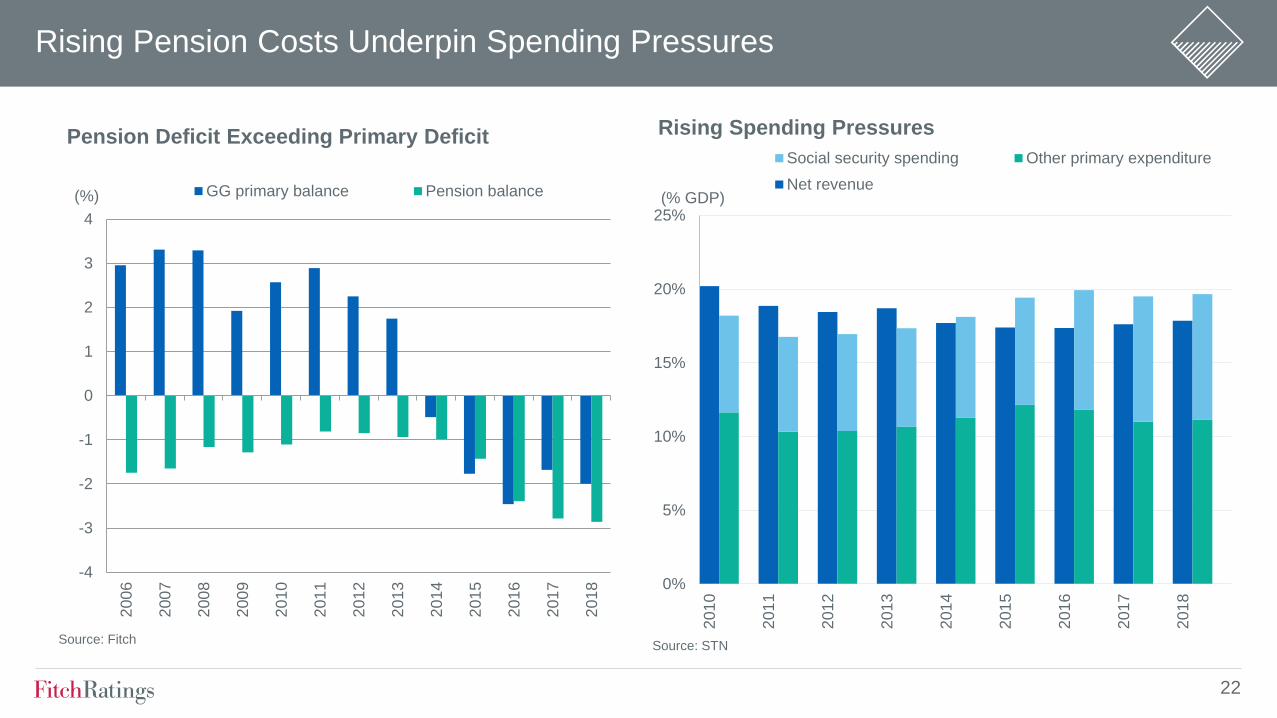

Rising Pension Costs Underpin Spending Pressures

-4

-3

-2

-1

0

1

2

3

4

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

GG primary balance Pension balance

Source: Fitch

(%)

Pension Deficit Exceeding Primary Deficit

0%

5%

10%

15%

20%

25%

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

Social security spending Other primary expenditure

Net revenue

Source: STN

Rising Spending Pressures

(% GDP)

22

-6

-5

-4

-3

-2

-1

0

Arg

en

tin

a (

B)

Turk

ey (

BB

)

Sou

th A

fric

a (

BB

+)

Ind

ia (

BB

B-)

Ind

one

sia

(B

BB

)

Phili

ppin

es (

BB

B)

Me

xic

o (

BB

B+

)

Bra

zil

(BB

-)

Current Account Balance

2018 2019f(% GDP)

Source: Fitch

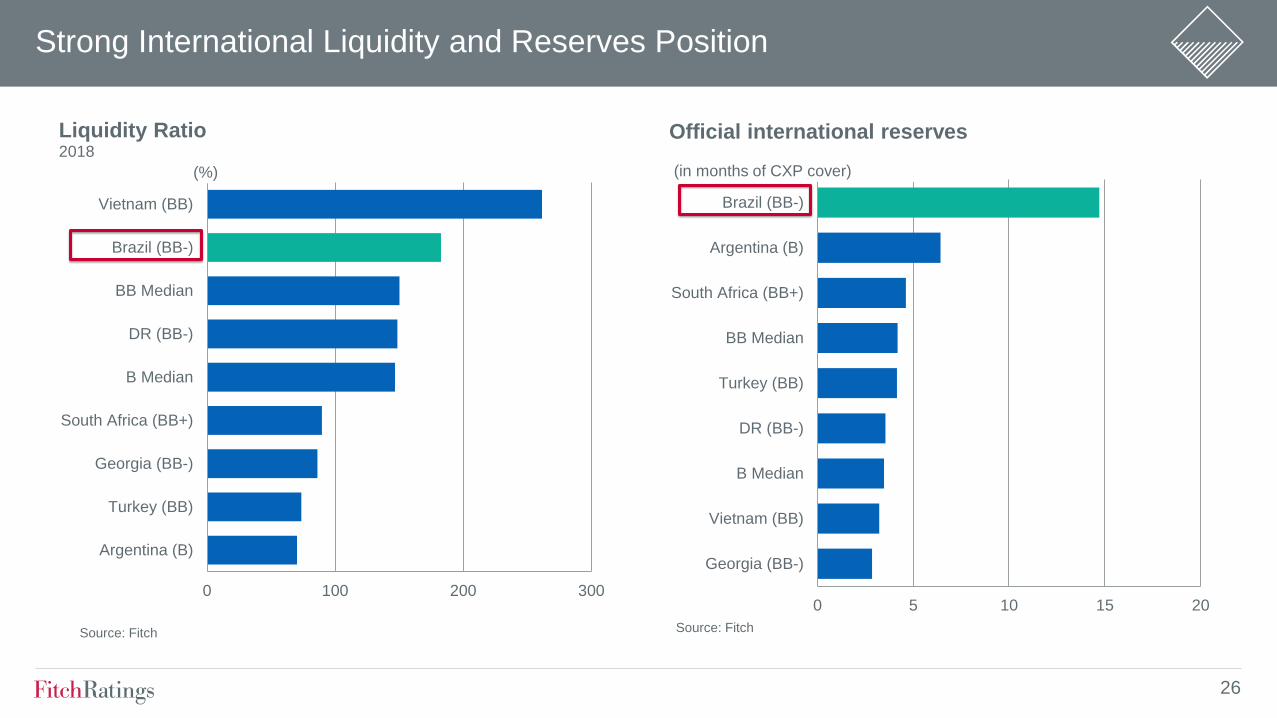

Strong External Position Relative to EM Peers

Argentina (B)

Turkey (BB)

South Africa (BB+)

India (BBB-)

Indonesia (BBB)

Philippines (BBB)

Mexico (BBB+)

Brazil (BB-)

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

-6 -5 -4 -3 -2 -1 0

Ge

ne

ral G

ove

rnm

ne

t B

ala

nce

(%

of G

DP

)

Current Account Deficit (% of GDP)

Dual deficits 2018

Source: Fitch

23

Despite High Debt, Strong Risk Mitigating Factors

0

10

20

30

40

50

60

70

80

90

Bra

zil

(BB

-)

Sou

th A

fric

a(B

B+

)

Vie

tna

m (

BB

)

Turk

ey (

BB

)

BB

Med

ian

Boliv

ia (

BB

-)

DR

(B

B-)

Geo

rgia

(B

B-)

Arg

en

tin

a (

B)

Share of GG Debt in FX 2018

(% of total)

Source: Fitch

0

5

10

15

20

25

30

35

40

45

Sou

th A

fric

a(B

B+

)

Peru

(B

BB

+)

Ind

one

sia

(BB

B)

Me

xic

o(B

BB

+)

Colo

mb

ia(B

BB

)

Turk

ey (

BB

)

Thaila

nd

(BB

B+

)

Bra

zil

(BB

-)

2009Q4 2018Q2

Foreign Ownership of Local Currency Government

Securities

(% of outstanding)

Source: Arslanalp and Tsuda, IMF Working Paper

24

Inflation Under Control With Expectations Well-Anchored

0

2

4

6

8

10

12

14

16

ma

i 1

5

nov 1

5

ma

i 1

6

nov 1

6

ma

i 1

7

nov 1

7

ma

i 1

8

nov 1

8

ma

i 1

9

(%)

Inflation Exepctations and Target

Target Range Policy Rate Inflation 12 month Expectation

Source: BCB

0

2

4

6

8

10

12

ma

i 1

5

nov 1

5

ma

i 1

6

nov 1

6

ma

i 1

7

nov 1

7

ma

i 1

8

nov 1

8

ma

i 1

9

IPCA IPCA Services IPCA Core

Inflation

(% yoy)

Source: BCB

25

0 5 10 15 20

Georgia (BB-)

Vietnam (BB)

B Median

DR (BB-)

Turkey (BB)

BB Median

South Africa (BB+)

Argentina (B)

Brazil (BB-)

Official international reserves

Source: Fitch

0 100 200 300

Argentina (B)

Turkey (BB)

Georgia (BB-)

South Africa (BB+)

B Median

DR (BB-)

BB Median

Brazil (BB-)

Vietnam (BB)

Liquidity Ratio 2018

Source: Fitch

Strong International Liquidity and Reserves Position

(in months of CXP cover) (%)

26

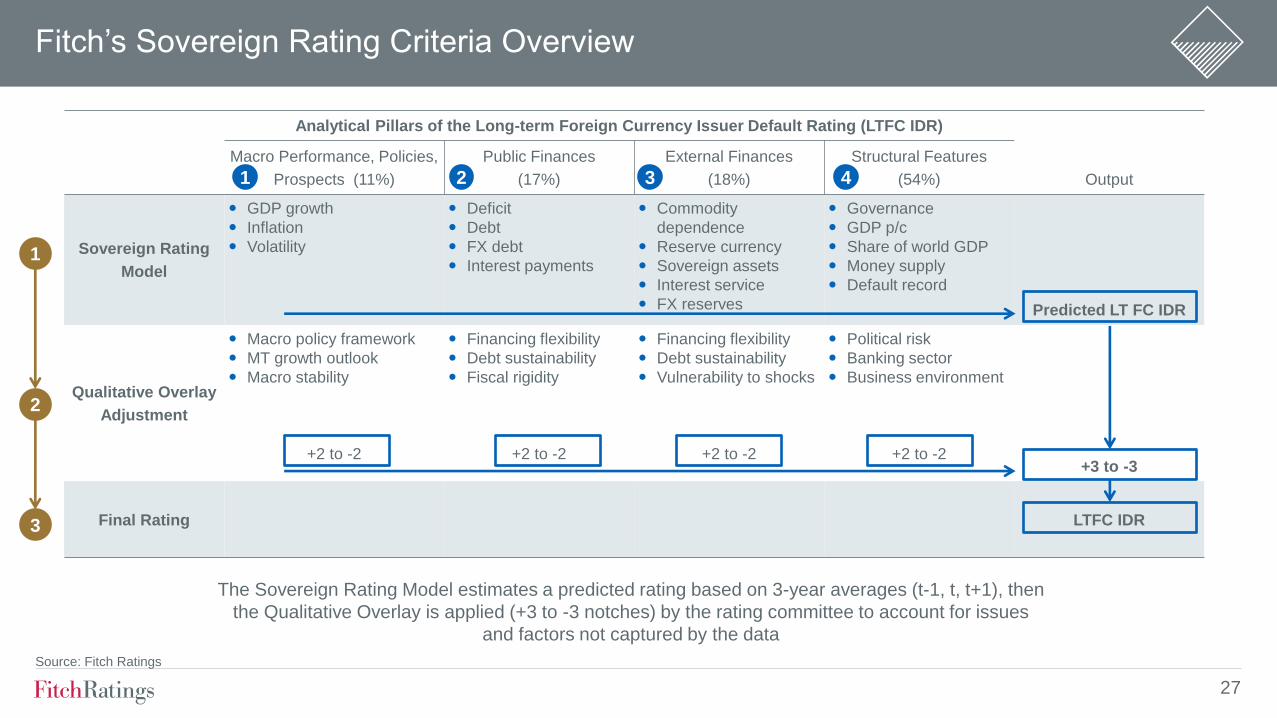

Fitch’s Sovereign Rating Criteria Overview

Analytical Pillars of the Long-term Foreign Currency Issuer Default Rating (LTFC IDR)

Macro Performance, Policies,

Prospects (11%)

Public Finances

(17%)

External Finances

(18%)

Structural Features

(54%) Output

Sovereign Rating

Model

GDP growth

Inflation

Volatility

Deficit

Debt

FX debt

Interest payments

Commodity

dependence

Reserve currency

Sovereign assets

Interest service

FX reserves

Governance

GDP p/c

Share of world GDP

Money supply

Default record

Predicted LT FC IDR

Qualitative Overlay

Adjustment

Macro policy framework

MT growth outlook

Macro stability

+2 to -2

Financing flexibility

Debt sustainability

Fiscal rigidity

+2 to -2

Financing flexibility

Debt sustainability

Vulnerability to shocks

+2 to -2

Political risk

Banking sector

Business environment

+2 to -2

+3 to -3

Final Rating

LTFC IDR

1

2

3

The Sovereign Rating Model estimates a predicted rating based on 3-year averages (t-1, t, t+1), then

the Qualitative Overlay is applied (+3 to -3 notches) by the rating committee to account for issues

and factors not captured by the data

1 4 3 2

Source: Fitch Ratings

27

SRM and Qualitative Overlay

Macro

Status

Public Finance External Structural

Weakness

Stable Stable Negative

Weakness Strength Neutral

Trend Stable

SRM output Qualitative overlay FC IDR

BBB-

Factor Notch adjustment

BB-

Macro 0

Public finances

- Rapidly worsened general government debt burden, which is expected to

continue increasing during the forecast period.

- Highly rigid spending profile and a heavy tax burden make adjustment to

shocks difficult.

-1

External finances 0

Structural features

- Challenging political environment and corruption-related issues that have

hampered timely progress on reforms to improve confidence in the medium-

term trajectory of public finances.

- Ease of Doing Business indicators are weaker than the 'BB' median

-2

Total -3

28

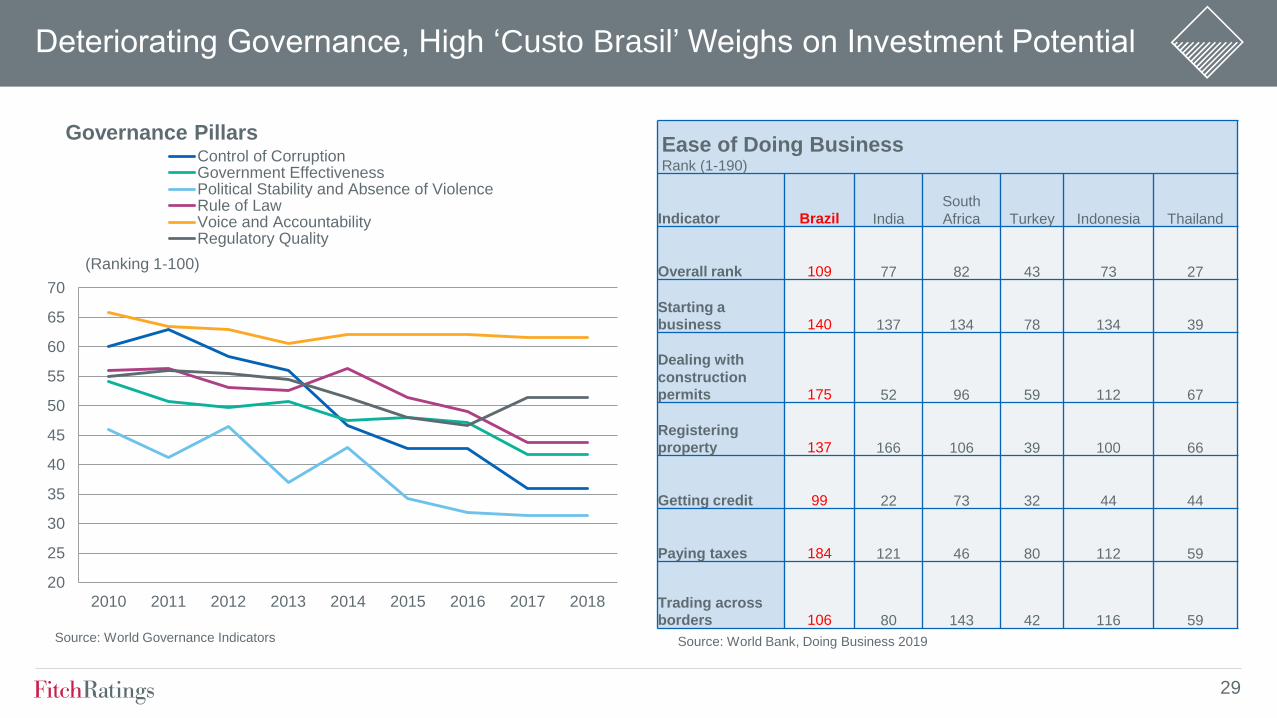

Deteriorating Governance, High ‘Custo Brasil’ Weighs on Investment Potential

Ease of Doing Business Rank (1-190)

Indicator Brazil India

South

Africa Turkey Indonesia Thailand

Overall rank 109 77 82 43 73 27

Starting a business 140 137 134 78 134 39

Dealing with

construction

permits 175 52 96 59 112 67

Registering

property 137 166 106 39 100 66

Getting credit 99 22 73 32 44 44

Paying taxes 184 121 46 80 112 59

Trading across borders 106 80 143 42 116 59

20

25

30

35

40

45

50

55

60

65

70

2010 2011 2012 2013 2014 2015 2016 2017 2018

Control of CorruptionGovernment EffectivenessPolitical Stability and Absence of ViolenceRule of LawVoice and AccountabilityRegulatory Quality

Governance Pillars

(Ranking 1-100)

Source: World Governance Indicators Source: World Bank, Doing Business 2019

29

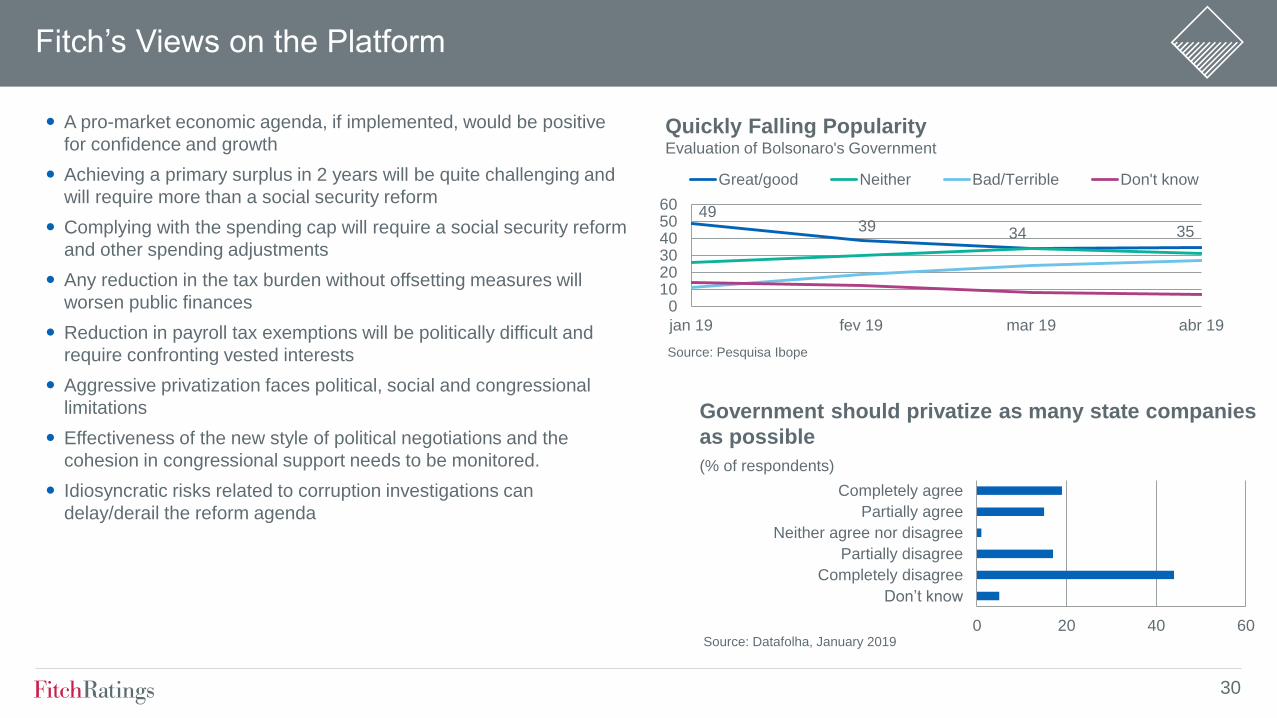

Fitch’s Views on the Platform

A pro-market economic agenda, if implemented, would be positive

for confidence and growth

Achieving a primary surplus in 2 years will be quite challenging and

will require more than a social security reform

Complying with the spending cap will require a social security reform

and other spending adjustments

Any reduction in the tax burden without offsetting measures will

worsen public finances

Reduction in payroll tax exemptions will be politically difficult and

require confronting vested interests

Aggressive privatization faces political, social and congressional

limitations

Effectiveness of the new style of political negotiations and the

cohesion in congressional support needs to be monitored.

Idiosyncratic risks related to corruption investigations can

delay/derail the reform agenda

0 20 40 60

Don’t know

Completely disagree

Partially disagree

Neither agree nor disagree

Partially agree

Completely agree

Source: Datafolha, January 2019

Government should privatize as many state companies

as possible

(% of respondents)

49 39 34 35

0102030405060

jan 19 fev 19 mar 19 abr 19

Great/good Neither Bad/Terrible Don't know

Source: Pesquisa Ibope

Quickly Falling Popularity Evaluation of Bolsonaro's Government

30

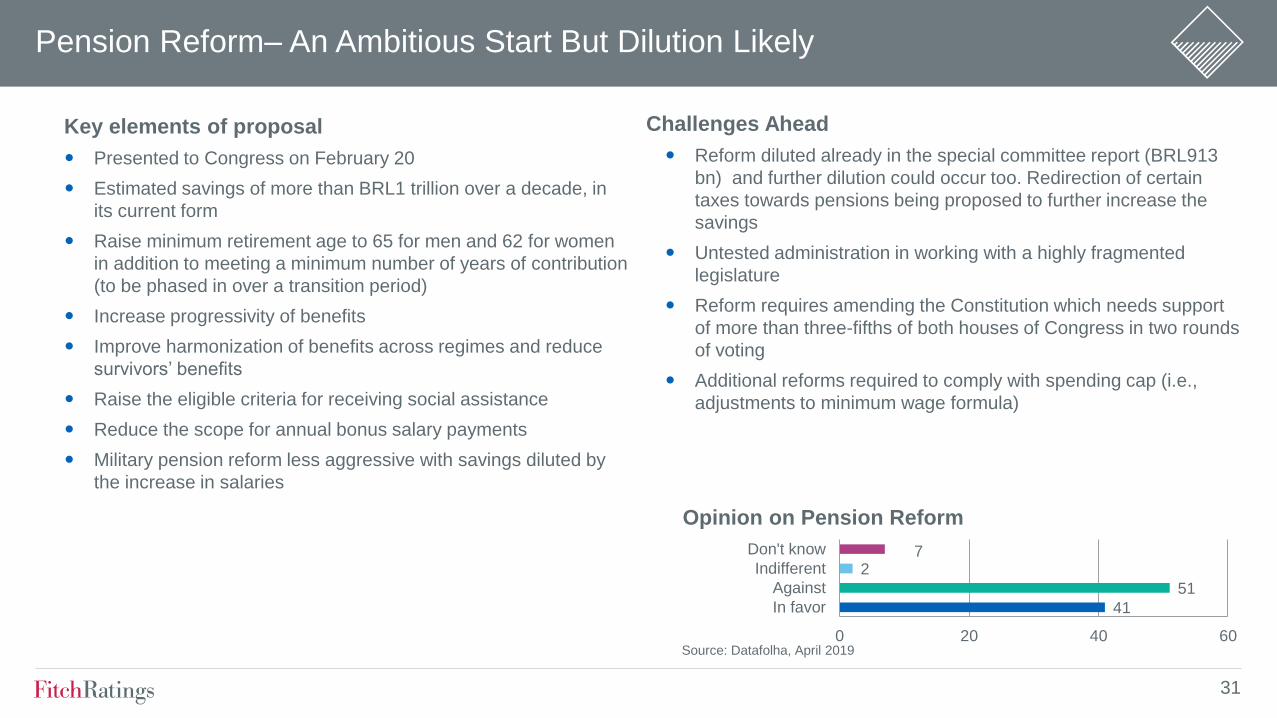

Pension Reform– An Ambitious Start But Dilution Likely

Key elements of proposal

Presented to Congress on February 20

Estimated savings of more than BRL1 trillion over a decade, in

its current form

Raise minimum retirement age to 65 for men and 62 for women

in addition to meeting a minimum number of years of contribution

(to be phased in over a transition period)

Increase progressivity of benefits

Improve harmonization of benefits across regimes and reduce

survivors’ benefits

Raise the eligible criteria for receiving social assistance

Reduce the scope for annual bonus salary payments

Military pension reform less aggressive with savings diluted by

the increase in salaries

Challenges Ahead

Reform diluted already in the special committee report (BRL913

bn) and further dilution could occur too. Redirection of certain

taxes towards pensions being proposed to further increase the

savings

Untested administration in working with a highly fragmented

legislature

Reform requires amending the Constitution which needs support

of more than three-fifths of both houses of Congress in two rounds

of voting

Additional reforms required to comply with spending cap (i.e.,

adjustments to minimum wage formula)

41

51

2 7

In favor

Against

Indifferent

Don't know

0 20 40 60

Opinion on Pension Reform

Source: Datafolha, April 2019

31

What Will Fitch Monitor in Future Rating Decisions

Political willingness and capacity for economic reforms

Cohesiveness of the economic team to implement the policy

agenda

Operational and formal independence of the BCB

Political strategy of the administration to negotiate in congress to

pursue and approve reforms

Assessment of fiscal proposals and the degree to which those

reduce fiscal deficits and stabilize the rising debt burden

Broader micro economic reform agenda to boost growth and

reduce unemployment

Positive Rating Sensitivities

Improvement in the political environment that facilitates the

implementation of credible policy initiatives to address medium term

public debt sustainability

Fiscal consolidation and improved prospects for debt stabilization

Improved growth outlook amid continued macroeconomic stability

Negative Rating Sensitivities

Lack of fiscal reform that is sufficient to support an improvement in

the fiscal and growth prospects, leading to a rapid growth in the

government debt burden that threatens medium term public debt

sustainability

Deterioration in the sovereign's domestic and/or external borrowing

conditions

Erosion of international reserves buffer and the broader external

balance sheet

32

Fitch Ratings’ credit ratings rely on factual information received from issuers and

other sources.

Fitch Ratings cannot ensure that all such information will be accurate and complete.

Further, ratings are inherently forward-looking, embody assumptions and predictions

that by their nature cannot be verified as facts, and can be affected by future events

or conditions that were not anticipated at the time a rating was issued or affirmed.

The information in this presentation is provided “as is” without any representation or

warranty. A Fitch Ratings credit rating is an opinion as to the creditworthiness of a

security and does not address the risk of loss due to risks other than credit risk,

unless such risk is specifically mentioned. A Fitch Ratings report is not a substitute

for information provided to investors by the issuer and its agents in connection with a

sale of securities.

Ratings may be changed or withdrawn at any time for any reason in the sole

discretion of Fitch Ratings. The agency does not provide investment advice of any

sort. Ratings are not a recommendation to buy, sell, or hold any security.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND

DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS AND

THE TERMS OF USE OF SUCH RATINGS AT WWW.FITCHRATINGS.COM.

@fitchratings

fitchratings.com

New York London 33 Whitehall Street

New York, NY 10004

30 North Colonnade

Canary Wharf

London, E14 5GN