Embed Size (px)

DESCRIPTION

BRANCHLESS BANKING: WWB GHANA’S EXPERIENCE. OUR DEFINITION OF BRANCHLESS BANKING. Use of information technology to deliver financial services to low income people beyond traditional banking channels and using field staff and retail agents. i.e., Leveraging People (Field Staff & Agents) - PowerPoint PPT Presentation

Citation preview

BRANCHLESS BANKING: WWB GHANA’S

EXPERIENCE

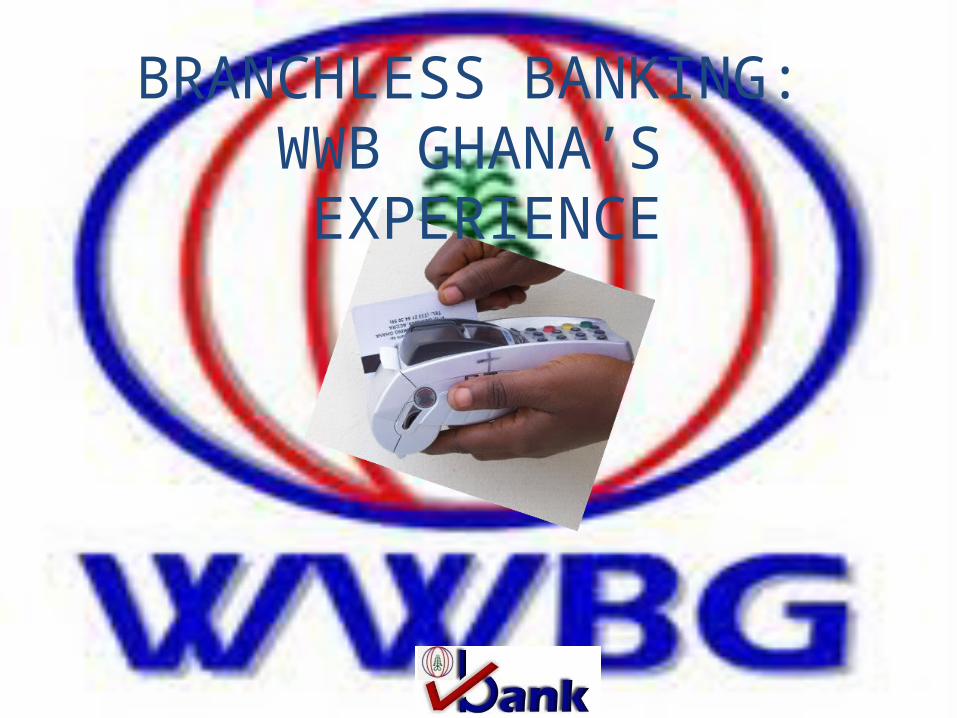

OUR DEFINITION OF BRANCHLESS BANKING

• Use of information technology to deliver financial services to low income people beyond traditional banking channels and using field staff and retail agents.

i.e.,• Leveraging– People (Field Staff & Agents)– Processes (Complete transactions

at client locations)– Technology (POS, Swipe

Card, Mobile Phones, etc.)

to deliver financial services to the unbanked and underbanked (2M Accounts for Population of 22M, with 6M mobile phone holders).

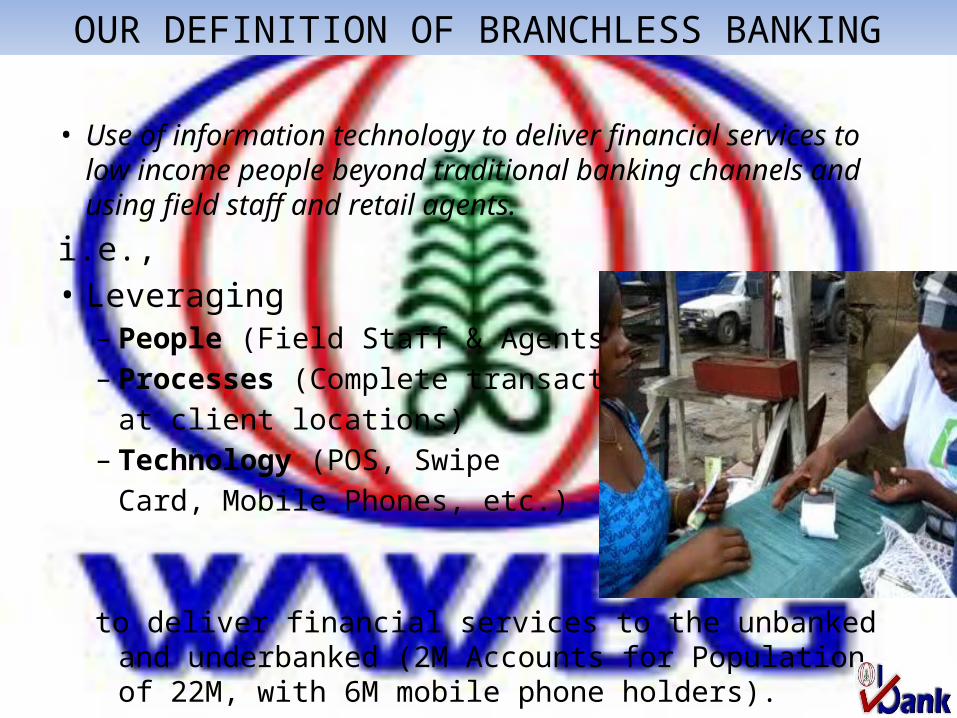

PERSPECTIVES DRIVING THE WWBG MODEL

1. Regulatory Environment

[WWBG Branchless Banking Model – Virtual Bank (Vbank)]

2. Customer Perspective

(Customer Value Proposition)

3. Technological Environment

4. Institutional Perspective

(The Business Case)

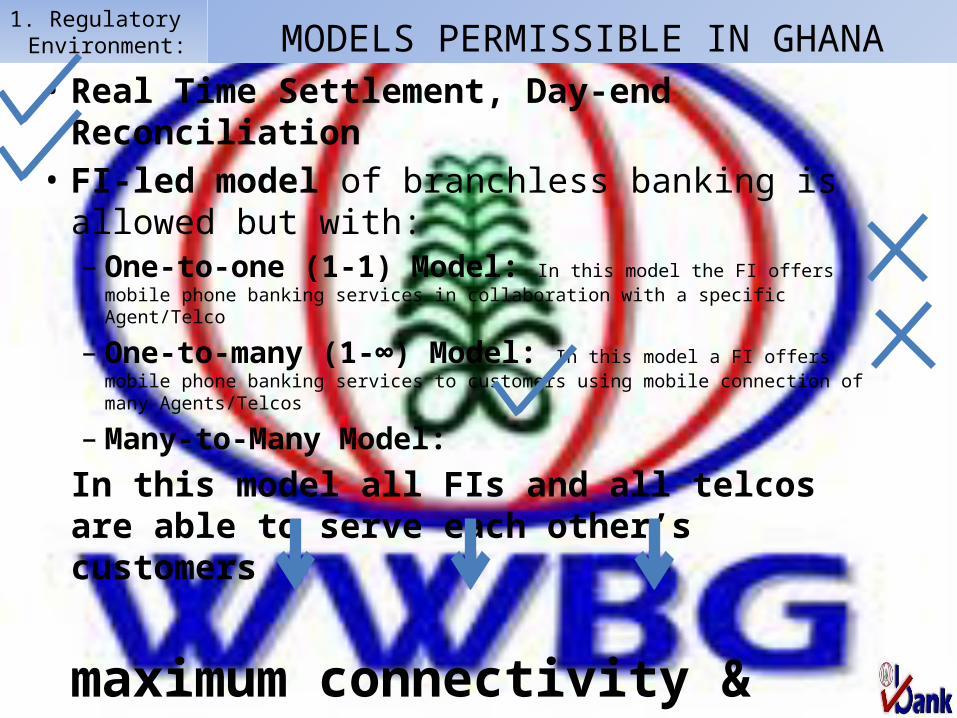

• Real Time Settlement, Day-end Reconciliation• FI-led model of branchless banking is allowed

but with: – One-to-one (1-1) Model: In this model the FI offers mobile phone

banking services in collaboration with a specific Agent/Telco

– One-to-many (1-∞) Model: In this model a FI offers mobile phone banking services to customers using mobile connection of many Agents/Telcos

– Many-to-Many Model:

In this model all FIs and all telcos are able to serve each other’s customers

maximum connectivity & maximum outreach

MODELS PERMISSIBLE IN GHANA1. Regulatory

Environment:

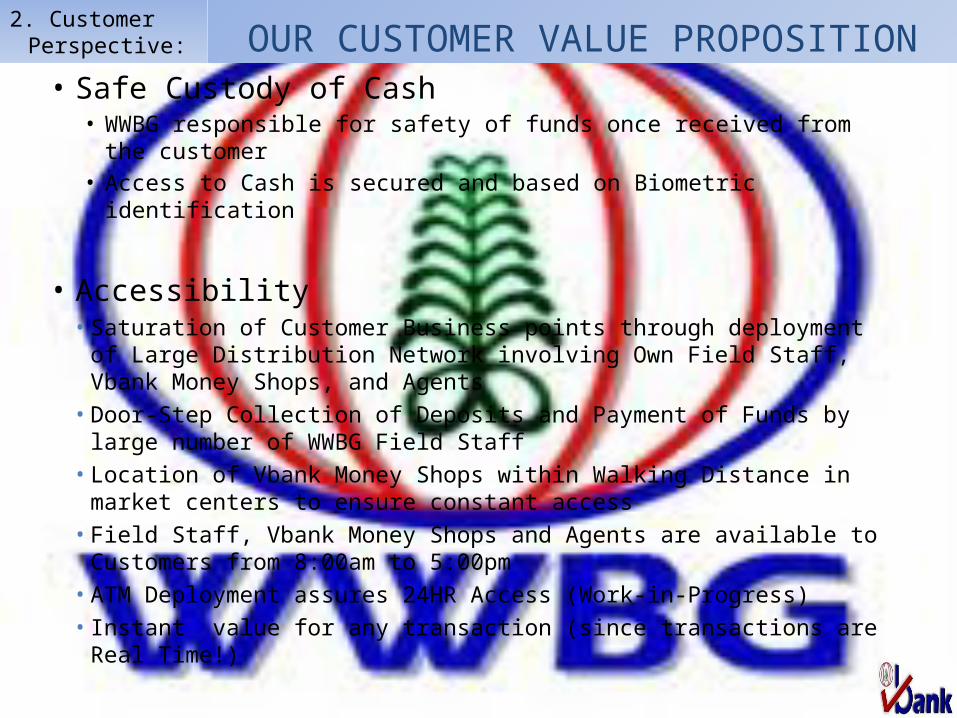

• Safe Custody of Cash• WWBG responsible for safety of funds once received from the customer• Access to Cash is secured and based on Biometric identification

• Accessibility• Saturation of Customer Business points through deployment of Large

Distribution Network involving Own Field Staff, Vbank Money Shops, and Agents

• Door-Step Collection of Deposits and Payment of Funds by large number of WWBG Field Staff

• Location of Vbank Money Shops within Walking Distance in market centers to ensure constant access

• Field Staff, Vbank Money Shops and Agents are available to Customers from 8:00am to 5:00pm

• ATM Deployment assures 24HR Access (Work-in-Progress)• Instant value for any transaction (since transactions are Real Time!)

2. Customer Perspective: OUR CUSTOMER VALUE PROPOSITION

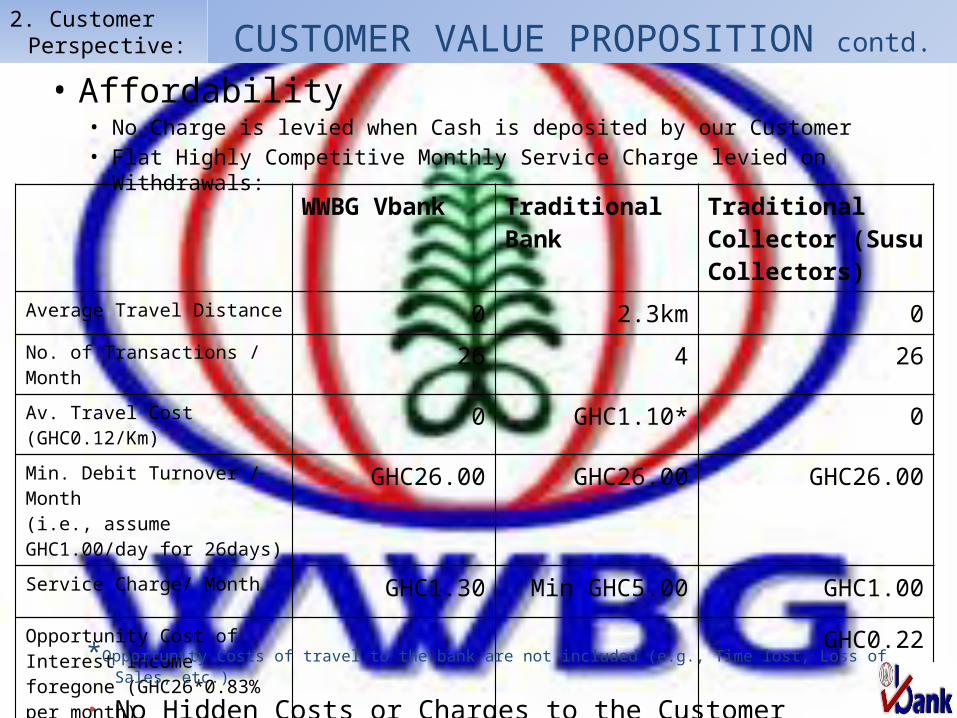

• Affordability• No Charge is levied when Cash is deposited by our Customer• Flat Highly Competitive Monthly Service Charge levied on Withdrawals:

2. Customer Perspective: CUSTOMER VALUE PROPOSITION contd.

WWBG Vbank Traditional Bank Traditional Collector (Susu Collectors)

Average Travel Distance 0 2.3km 0No. of Transactions / Month 26 4 26Av. Travel Cost (GHC0.12/Km) 0 GHC1.10* 0Min. Debit Turnover / Month(i.e., assume GHC1.00/day for 26days)

GHC26.00 GHC26.00 GHC26.00

Service Charge/ Month GHC1.30 Min GHC5.00 GHC1.00

Opportunity Cost of Interest Income foregone (GHC26*0.83% per month)

GHC0.22

Total Transaction Cost to Customer

GHC1.30 GHC6.10 GHC1.22

*Opportunity Costs of travel to the bank are not included (e.g., Time lost, Loss of Sales, etc.)

• No Hidden Costs or Charges to the Customer

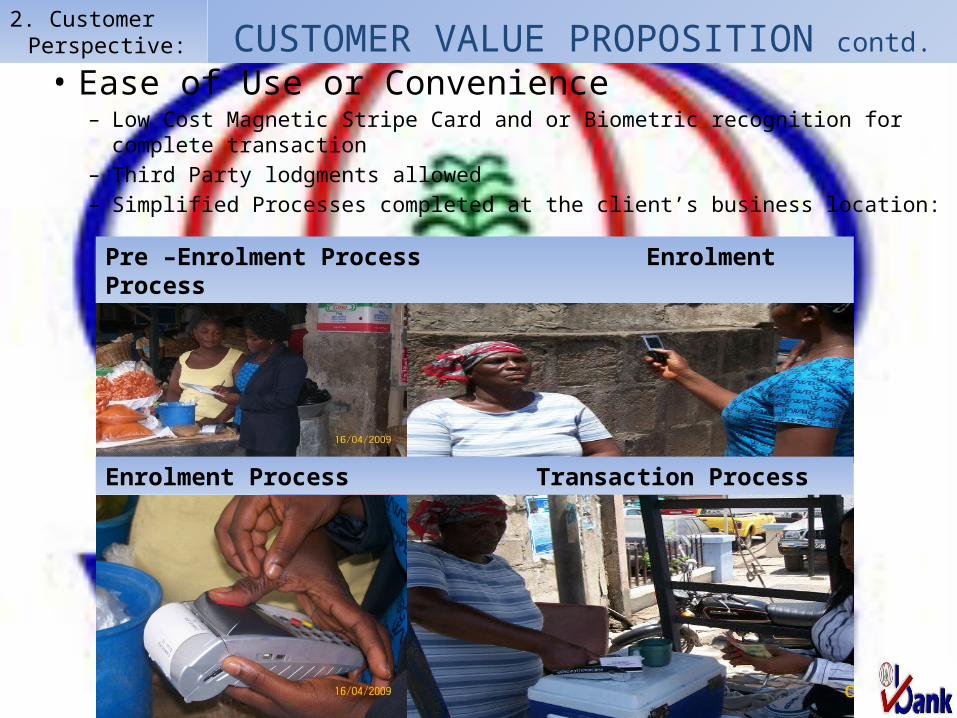

• Ease of Use or Convenience– Low Cost Magnetic Stripe Card and or Biometric recognition for complete

transaction– Third Party lodgments allowed– Simplified Processes completed at the client’s business location:

2. Customer Perspective: CUSTOMER VALUE PROPOSITION contd.

Enrolment Process Transaction Process

Pre –Enrolment Process Enrolment Process

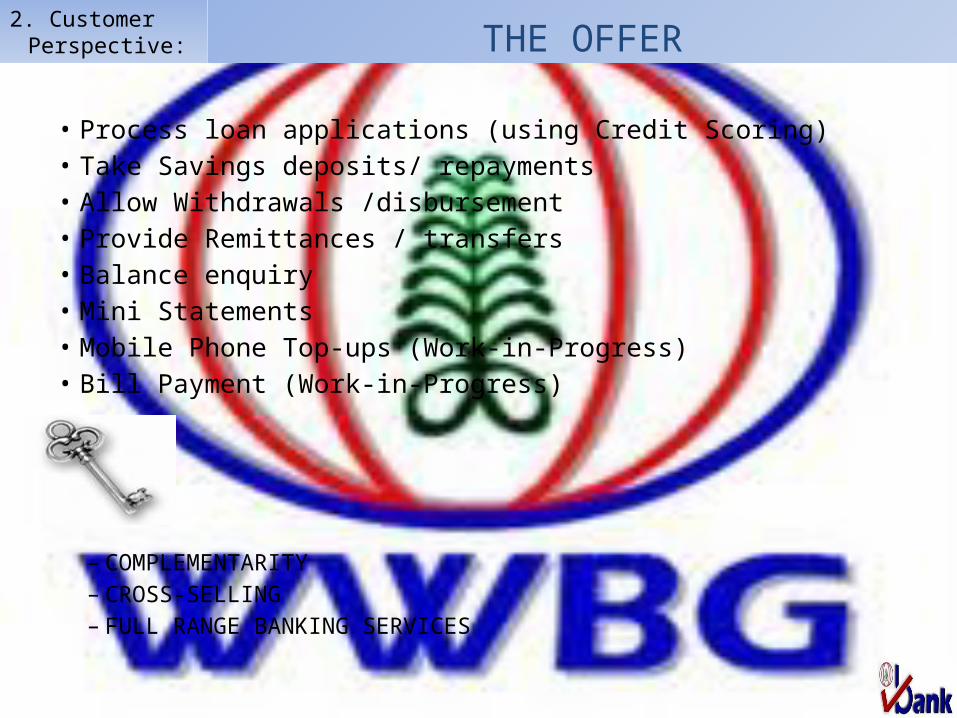

• Process loan applications (using Credit Scoring)• Take Savings deposits/ repayments• Allow Withdrawals /disbursement• Provide Remittances / transfers• Balance enquiry• Mini Statements• Mobile Phone Top-ups (Work-in-Progress)• Bill Payment (Work-in-Progress)

– COMPLEMENTARITY– CROSS-SELLING– FULL RANGE BANKING SERVICES

2. Customer Perspective: THE OFFER

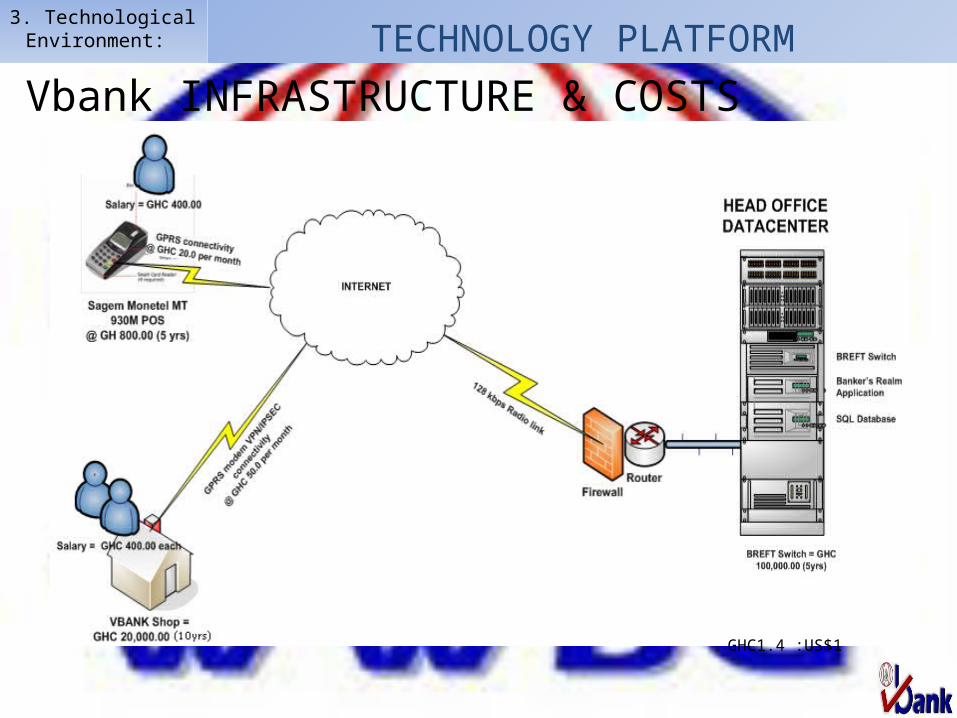

3. Technological Environment: TECHNOLOGY PLATFORM

Vbank INFRASTRUCTURE & COSTS

GHC1.4 :US$1

Branch Banking

Branch Banking

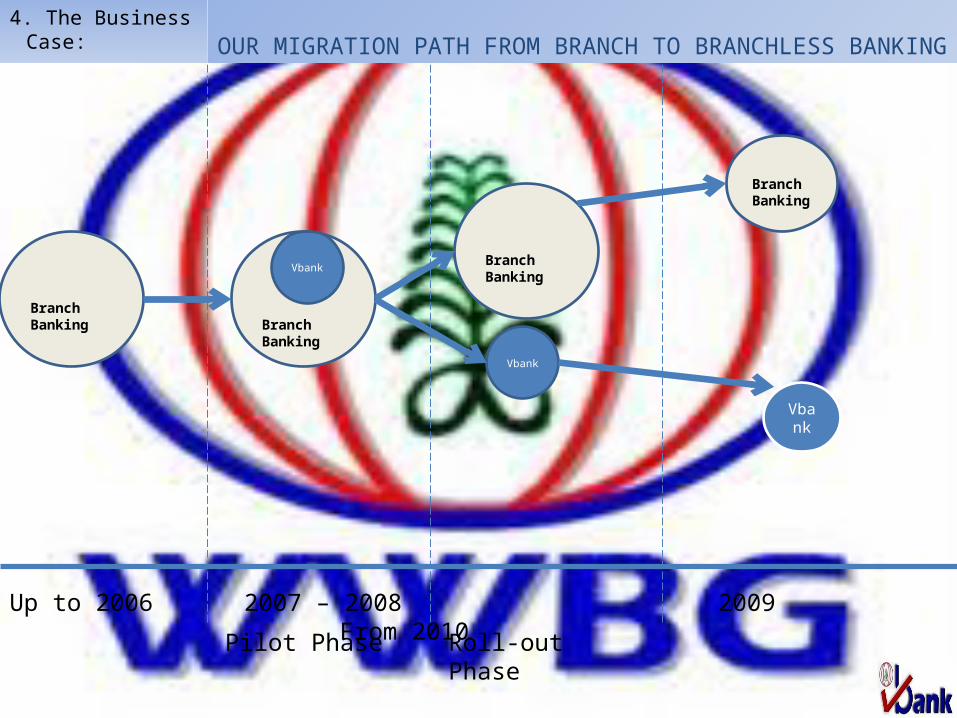

4. The Business Case:

OUR MIGRATION PATH FROM BRANCH TO BRANCHLESS BANKING

Vbank Branch Banking

Vbank

Branch Banking

Vbank

Up to 2006 2007 – 2008 2009 From 2010

Pilot Phase Roll-out Phase

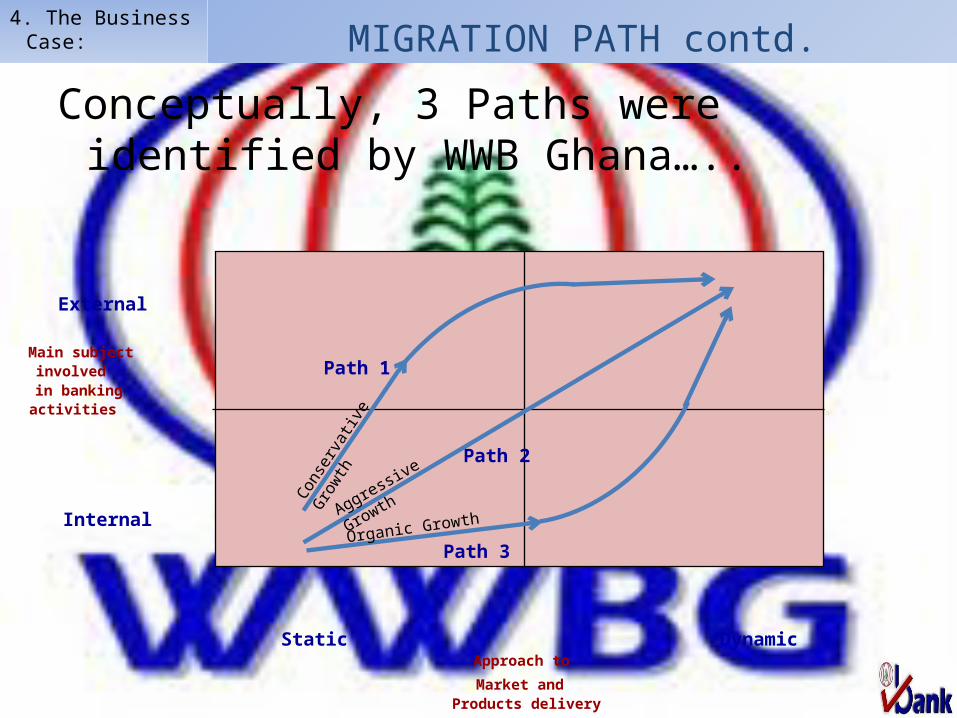

4. The Business Case: MIGRATION PATH contd.

Internal

External

Main subjectinvolvedin bankingactivities

Static DynamicApproach to

Market andProducts delivery

Path 1

Conceptually, 3 Paths were identified by WWB Ghana…..

Path 2

Path 3

Aggressive Growth

Cons

erva

tive G

rowth

Organic Growth

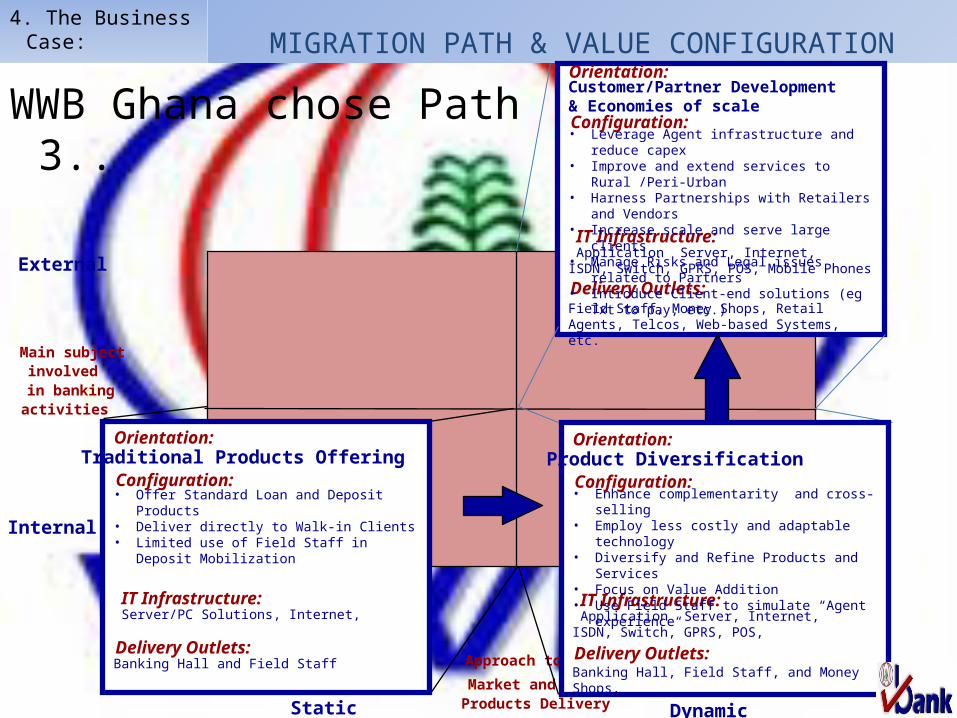

4. The Business Case: MIGRATION PATH & VALUE CONFIGURATION

Internal

External

Main subjectinvolvedin bankingactivities

Static Dynamic

Approach to

Market andProducts Delivery

Orientation:Customer/Partner Development& Economies of scale

IT Infrastructure:

Configuration:

Delivery Outlets:

WWB Ghana chose Path 3..• Leverage Agent infrastructure and reduce capex• Improve and extend services to Rural /Peri-Urban• Harness Partnerships with Retailers and Vendors • Increase scale and serve large clients• Manage Risks and Legal issues related to Partners• Introduce Client-end solutions (eg Txt to pay, etc.)

Application Server, Internet, ISDN, Switch, GPRS, POS, Mobile Phones

Field Staff, Money Shops, Retail Agents, Telcos, Web-based Systems, etc.

Orientation:Traditional Products Offering

IT Infrastructure:

Configuration:

Delivery Outlets:

• Offer Standard Loan and Deposit Products• Deliver directly to Walk-in Clients• Limited use of Field Staff in Deposit Mobilization

Server/PC Solutions, Internet,

Banking Hall and Field Staff

Orientation:Product Diversification

IT Infrastructure:

Configuration:

Delivery Outlets:

• Enhance complementarity and cross-selling• Employ less costly and adaptable technology• Diversify and Refine Products and Services• Focus on Value Addition• Use Field Staff to simulate “Agent experience“

Application Server, Internet, ISDN, Switch, GPRS, POS,

Banking Hall, Field Staff, and Money Shops,

PLATFORM INTEGRATION4. The Business

Case:

BENEFITS TO CUSTOMERS

• FAST: a palm top operated account at your doorstep so clients do not have to queue for banking services.

• ACCESSIBLE: our Field Staff and Retail Agents are a phone call and walking distance away. They will come or you can walk to at your own convenience anytime.

• SECURED: clients fingerprint safe guards their account. No one can access their account without their input. Every transaction hits clients account immediately.

• SIMPLIFIED: it is very easy to operate. Your balance is available to you immediately.

BENEFITS TO WWBG

• Rapid expansion of deposit mobilization services.

• Low cost deployment of banking services to the unbanked.

• Cost efficient mobilization of deposit.• Growth in deposit mobilization• Low cost of funds for lending Positive impact

on our returns

KEY SUCCESS DRIVERS• Thorough Research-Backed Pilot Testing (allowing for

refinement-products/services, channels, systems )• On-going Process Mapping and Refinement (front- and

back-end)• Suitability of Branchless Banking Application and

Timeliness of Support• Cross-selling of products and full range of products• Favorable legal and technological environment• Less costly dynamic technology with scalability• Effective Risk Management• Cost recovery• Well thought through Migration Path & Value

Configuration