Embed Size (px)

Citation preview

Campbelltown Shop U012, Macarthur Square Shopping Centre, Gilchrist Drive, Ambarvale NSW 2560

Fairfield Shop G50, Neeta City Shopping Centre, Smart Street, Fairfield NSW 2165

Greenacre 138 Waterloo Rd, Greenacre NSW 2190

Katoomba 63 Pioneer Place, Katoomba NSW 2780

Leichhardt 7–15 Wetherill Street, Leichhardt NSW 2040

Lidcombe 27–29 Church Street, Lidcombe NSW 2141

Marrickville Shop 7-8, 34 Victoria Road Marrickville NSW 2204

Mascot 1197 Botany Road, Mascot NSW 2020

Parkes 189 Clarinda Street, Parkes NSW 2870

Parramatta 207 Church Street, Parramatta NSW 2150

Penrith 16–20 Riley Street, Penrith NSW 2750

Rockdale Shop 5, Rockdale Plaza, Rockdale NSW 2216

Rouse Hill Shop GR092A, Civic Way, Rouse Hill Town Centre, Rouse Hill NSW 2155

Springwood 268 Macquarie Road, Springwood NSW 2777

Sutherland 20 Eton Street, Sutherland NSW 2232

Sydney City 210 Clarence Street, Sydney NSW 2000

Windsor Shop 7–8, 251 George Street, Windsor NSW 2756

Registered Office: 19 Second Ave, Blacktown NSW 2148

Branches

scu.net.auCall 13 61 91

Sydney Credit Union Ltd ABN 93 087 650 726 AFSL 236476 Australian Credit Licence No 236476. Please address all mail to PO Box 444 Blacktown NSW [email protected]

2017 annual report

Sydney Credit Union Ltd | ABN 93 087 650 726 1

scu.net.au 2017 Annual Report

Chair and CEO’s Report

It is a pleasure to present SCU’s 2016 /17 Annual Report and reflect on what has been a year of stronggrowth and performance where we have delivered on the initiatives to which we committed to remainrelevant to our members.

Highlights

There are many areas that stand out:

• the Board’s approval of our Strategy, our roadmap for building-on our 50 year old foundations andcreating first class technologies to meet the needs of our members and people

• continuing to simplify and standardise the things we do, achieving better outcomes for our membersand our people

• deepening our experience in financial and risk management and operational stability

• delivering on our promise to enhance the member experience through improvements to web basedtechnology, online banking for mobile, loan processing, customer relationship management and dataanalytics

• our financial performance

Financial Performance

I’m pleased to report that SCU continues to be in a strong position financially with an increase in assets to$867m, loans increased to $624m and deposits up 3.2% to $777m.

We hold over $76m in net assets and our capital adequacy ratio sits at 17%.

Our performance reinforces our position as a strong and stable competitor in the financial sector.

Throughout the year, we endeavoured to invest in productivity and technology to secure the organisation’srelevance whilst ensuring we remain financially strong. To this extent we continued our focus on renewaland innovation whilst achieving a Net Profit after Tax (NPAT) of $2.158m.

What are the key actions for 2017/18?

In broad terms our focus is on delivering on our Strategy by continuing to grow, reforming our systems,developing our people, strengthening our engagement with members and achieving our financial targets.

What this means specifically is:

• Review of priorities of current strategic initiatives to allow fast-tracking of member focused projects

• Initiation of a “Fintech” strategy with the first steps involving stakeholder input on key areas forexploration

• Scoping of a cultural change programme

• Review of change management processes

• Structured programs to connect with members so as to increase product penetration and retainbusiness portfolios

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 1

2017 Annual Report scu.net.au

2 Sydney Credit Union Ltd | ABN 93 087 650 726

• On-boarding experience developed for new and existing members

• Investing in our people, learning and leadership programs

• Uniform Channel experience embracing “know me”, “remind me”, and “they’ve got it together”;mobile applications that are simpler, faster and easier; and a highly effective website

• Improvement in branch look, functionality and digital capability

• Implement the New Payment Platform as a product available to SCU members

The regulatory landscape remains challenging

One of the things that the recent Senate inquiry into the banking sector highlighted was how important it isfor us to build knowledge and understanding of the mutual sector.

We need to ensure our members’ needs are taken into consideration when government develops policy.SCU needs to do more to educate the decision makers about the impact their decisions are having oncompetition.

SCU will continue to work in this space, being an advocate for competition in the banking sector.

Our People

Our people are essential to our success and are the key driver of member satisfaction and SCU’sperformance.

We thank all our people for their continued achievements during the year.

They are engaged and operate in an environment that promotes ethical behaviour and is member-focused.

It is ultimately our people that set us apart from our peers and we are proud to be an employer of choicefor gender equality, with women in 52.5% of management roles.

We wish to thank the Board of Directors for their wisdom and commitment. Our Board consists of eightdirectors who offer a diversity of specialist skills and who are united in their dedication to our underlyingvalues.

After seven years, Dir. Greg Hayes decided to resign from the SCU Board. Greg filled many Board Executiveroles at SCU, having previously being Chair of Sutherland Shire Council Employees Credit Union.

We thank Greg for his contribution and commitment to SCU.

In May 2017, we welcomed Anton Usher as a SCU Director. Anton brings a breadth of experience andexpertise to the Board and is a member of Board Risk Committee.

We would also like to thank the Members for their continuing support and helping us deliver anothersuccessful year.

Hans Kludass Ashley JenningsChair Chief Executive Officer

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 2

Sydney Credit Union Ltd | ABN 93 087 650 726 3

scu.net.au 2017 Annual Report

Directors’ Report

Your Directors present their report on Sydney Credit Union Ltd (SCU) for the financial year ended 30 June 2017.SCU is a company registered under the Corporations Act 2001.

Information on Directors

The names of the Directors in office at any time during or since the end of the year are:-

Mr H R Kludass (Chair)Mr M E Sawyer (Deputy Chair)Mr R W ThornMr G M VarcoeMs V M BourkeMs K DaynesMr J M ParsonsMr A W Usher (Board appointed May 2017)Mr G J Hayes (retired January 2017)Mr P Stewart (retired November 2016)Mr J W Bourke (retired August 2016)Mr B T Nevin (retired August 2016)

Mr H R Kludass – Director

Qualifications – Bachelor of Commerce (Accounting)Associate Diploma in Business (Accounting)Member of Instil

Experience – Director, June 2009–CurrentChair, Nov 2014–CurrentRemunerations Committee, 2010–CurrentExecutive Committee, 2010–CurrentCorporate Governance Committee, 2010–CurrentBoard Risk Committee, Aug 2016–CurrentDeputy Chair, 2010–Nov 2014Board Audit Committee, Nov 2009–Nov 2014Manager, Sutherland Shire Council Executive Officer, Sutherland Shire Council Employees Credit Union (SSCECU) 2000–2009

Chairman, SSCECU, 1999–2000Director, SSCECU, 1997–2000Business Consultant, 1997–2008

Interest in Shares – 1 Member Share in SCU

Mr M E Sawyer – Director

Qualifications – Diploma of Financial ServicesFellow of the Australasian Mutuals InstituteMember of the Australian Institute of ManagementMember of InstilSupervision Certificate Train the Trainer CertificateElectrical Trades Certificate

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 3

Experience – Deputy Chair, Nov 2014–CurrentDirector, Oct 2005–CurrentChair, Corporate Governance Committee, Dec 2011–CurrentExecutive Committee, Dec 2011–CurrentRemuneration Committee, Dec 2011–CurrentBoard Audit Committee, Dec 2005–Nov 2008Board Risk Committee, Nov 2008–Nov 2011 and Aug 2016Director, Karpaty Foundation Pty Ltd, 2011–CurrentDirector, Pinnacle Credit Union, 2003–2005Director of Licensed/Registered Club, 1993–1994Total Quality Management (Energy Australia 1992–1994)Managing Director of a travel company, 2008–Current

Interest in Shares – 1 Member Share in SCU

Ms V M Bourke – Director

Qualifications – Master of Human Resource ManagementBachelor of Business (HR)Graduate Certificate in Human Resource ManagementGraduate Certificate in Local Government Management Member of Instil

Experience – Director, Nov 2014–CurrentBoard Audit Committee, Nov 2014–Current17 years’ experience in senior HR roles in Local Government

Interest in Shares – 1 Member Share in SCU

Ms K A Daynes – Director

Qualifications – Graduate Certificate of BusinessGraduate Certificate in ManagementMember of Instil

Experience – Director, Dec 2014–CurrentBoard Risk Committee, Dec 2014–Current16 years’ experience in senior roles at Department of Human ServicesDirector, AMCU, 2004–Nov 2014Vice Chairman, AMCU, 2012–Nov 2014Interest Rate Committee, AMCU, 2012–Nov 2014

Interest in Shares – 1 Member Share in SCU

Mr J M Parsons – Director

Qualifications – Certificate in AccountingMember of Instil

Experience – Director, Dec 2014–CurrentBoard Risk Committee, Dec 2014–CurrentExecutive Committee, July 2016–CurrentCorporate Governance Committee, July 2016–CurrentRemuneration Committee, July 2016–CurrentChair, Board Risk Committee, July 2016–Current37 years in senior roles at the Australian Tax OfficeDirector, AMCU, 1988–Nov 2014Chairman, AMCU, 1994–Nov 2014

Interest in Shares – 1 Member Share in SCU

2017 Annual Report scu.net.au

4 Sydney Credit Union Ltd | ABN 93 087 650 726

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 4

Mr R W Thorn – Director

Qualifications – Bachelor of BusinessCertificate in Electrical EngineeringMember of Instil

Experience – Director, Dec 2005–CurrentExecutive Committee, 2008–CurrentRemuneration Committee, 2010–CurrentCorporate Governance Committee, 2010–CurrentChair, Board Audit Committee, Nov 2008–CurrentBoard Audit Committee, Dec 2005–CurrentDirector, Prospect Credit Union, 2001–2006

Interest in Shares – 1 Member Share in SCU

Mr A Usher – Director

Qualifications – Bachelor of LawsBachelor of Arts (Economics)Graduate Diploma of Applied Corporate GovernanceCertificate, Human Resource PracticeSolicitor Member, Law Society of NSWFellow, Governance Institute of AustraliaMember, Institute of Chartered Secretaries & AdministratorsAssociate Fellow, Risk Management Institution of AustralasiaMember of Instil

Experience – Director, May 2017–CurrentMember, Board Risk Committee, May 2017–Current Manager, Sutherland Shire Council

Interest in Shares – 1 Member Share in SCU

Mr G M Varcoe – Director

Qualifications – Bachelor of Engineering (Civil)Master of Business Administration (Technology Management)Graduate Diploma of Management (Technology Management)Builders’ Licence Member of Instil

Experience – Director, Apr 2008–CurrentBoard Risk Committee, Dec 2015–CurrentBoard Audit Committee, May 2008–Nov 2015Director, Blue Mountains & Riverlands Community Credit Union (BM&RCCU),

1997–Mar 2008 Chair, Corporate Governance Committee, BM&RCCU, 2006–Mar 2008Licensed Builder and Consultant Engineer

Interest in Shares – 3 Member Shares in SCU

Mr J W Bourke – Director

Qualifications – Associate, Local Government Administration Member of Instil

Experience – Director, 2008–10 Aug 2016Board Audit Committee, 2008–Aug 2016General Manager, South Sydney Council, 1989–2001

Interest in Shares – 1 Member Share in SCU

Sydney Credit Union Ltd | ABN 93 087 650 726 5

scu.net.au 2017 Annual Report

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 5

Mr B T Nevin – Director

Qualifications – Certified Practising AccountantMember of Instil

Experience – Director, 1972–10 Aug 2016Chair, 1997–2008, 2010–Nov 2014Deputy Chair, 1986–1997, 2008–2010Executive Committee, 1986–Nov 2014Corporate Governance Committee, 2010–Nov 2014Remunerations Committee, 2010–Nov 2014Board Risk Committee, Jul 2014–Nov 2015Board Audit Committee, Dec 2015–Aug 2016

Interest in Shares – 1 Member Share in SCU

Mr P Stewart – Director

Qualifications – Diploma of Corporate ManagementAssociate Member of the Institute of Chartered SecretariesAssociate Member of the Institute of Banking & FinanceMember of Instil

Experience – Director, 2010–9 Nov 2016Chair, Board Risk Committee, Nov 2014–Aug 2016Member, Board Risk Committee, 2010–Nov 2016Executive Committee, Nov 2014–Aug 2016Remuneration Committee, Nov 2014–Aug 2016

Interest in Shares – 1 Member Share in SCU

Mr G Hayes – Director

Qualifications – Bachelor of CommerceLocal Government Managers AssociationMember of Instil

Experience – Director, 2010–22 Jan 2017Member, Board Audit Committee, Dec 2016Member, Board Risk Committee, 2010–Oct 2016Chair, Board Risk Committee, Dec 2013–Nov 2014Executive Committee, Dec 2013–Nov 2014Corporate Governance Committee, Dec 2013–Nov 2014Remuneration Committee, Nov 2013–Nov 2014C.F.O. SSCECU, 1992–2009Director, SSCECU, 1985–1991Chairman, SSCECU, 1989–1991Deputy Chair, SSCECU, 1987–1989

Interest in Shares – 1 Member Share in SCU

2017 Annual Report scu.net.au

6 Sydney Credit Union Ltd | ABN 93 087 650 726

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 6

Mr A J Jennings - Chief Executive Officer and Company Secretary

Qualifications - Advanced Diploma in AccountingCertificate III in Investment and Personal Financial PlanningDiploma of ManagementMember of InstilJustice of the Peace

Experience - 36 years in the Financial Services IndustrySydney Credit Union CEO & Company Secretary since 1998

Other Directorships - TransAction Solutions Pty LtdAustralasian Mutuals Institute (AMI)Karpaty Foundation Pty Ltd Shared Services Pty LtdShared Services Partners Pty Ltd

Interest - 1 Member Share in SCU

Sydney Credit Union Ltd | ABN 93 087 650 726 7

scu.net.au 2017 Annual Report

Executive & Audit & Risk CorporateDirector Board Remuneration Compliance Management Governance Period of Appointment

H A H A H A H A H A

Hans Kludass 11 10 4 4 2 2 - - 3 3 1/7/2016 to 30/6/2017

Mark Sawyer 11 10 4 4 - - 1 1 3 3 1/7/2016 to 30/6/2017

Ray Thorn 11 11 4 4 4 4 1 1 3 3 1/7/2016 to 30/6/2017

Gary Varcoe 11 10 - - - - 4 3 - - 1/7/2016 to 30/6/2017

Vanessa Bourke 11 8 - - 4 1 - - - - 1/7/2016 to 30/6/2017

Kerrie Daynes 11 10 - - - - 4 2 - - 1/7/2016 to 30/6/2017

John Parsons 11 10 3 3 2 2 4 4 3 3 1/7/2016 to 30/6/2017

Anton Usher 2 2 - - - - - - - - 1/7/2016 to 30/6/2017

Greg Hayes 5 1 - - - - 2 0 - - 1/7/2016 to 30/6/2017

Peter Stewart 4 3 1 1 - - 2 1 - - 1/7/2016 to 30/6/2017

Brian Nevin 1 1 - - - - - - - - 1/7/2016 to 30/6/2017

John Bourke 1 0 - - - - - - - - 1/7/2016 to 30/6/2017

H = Meetings Held

A = Meetings Attended

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 7

8 Sydney Credit Union Ltd | ABN 93 087 650 726

2017 Annual Report scu.net.au

Directors’ Benefits

No Director has received or become entitled toreceive during, or since the financial year, a benefitbecause of a contract made by SCU, controlledentity, or a related body corporate with a Director, afirm of which a Director is a Member or an entity inwhich a Director has a substantial financial interest,other than that disclosed in Note 31 of the financialreport.

Indemnifying Officer Or Auditor

Insurance premiums have been paid to insure eachof the Directors and officers of SCU, against anycosts and expenses incurred by them in defendingany legal proceeding arising out of their conductwhile acting in their capacity as an officer of SCU. Inaccordance with normal commercial practicedisclosure of the premium amount and the natureof the insured liabilities is prohibited by aconfidentiality clause in the contract.

No insurance cover has been provided for thebenefit of the auditors of SCU.

Financial Performance Disclosures

Principal Activities

The principal activities of SCU during the year werethe provision of retail financial services to Membersin the form of taking deposits and giving financialaccommodation as prescribed by the Constitution.

No significant changes in the nature of theseactivities occurred during the year.

Operating Results

The net profit of SCU for the year after providingfor income tax was $2,158,154 (2016 $2,344,533).

There were no significant events during the yearthat impacted upon the current year’s result.

Dividends

Since the end of the financial year, no dividendshave been paid or declared by the Directors ofSCU from the profits earned during the year ended30 June 2017 or prior.

Review Of Operations

The results of SCU’s operations from its activities ofproviding financial services to its Members did notchange significantly from those of the previous year.

Significant Changes In State Of Affairs

There were no significant changes in the state ofthe affairs of SCU during the year.

Events Occurring After Balance Date

No matters or circumstances have arisen since theend of the financial year which significantly affectedor may significantly affect the operations, or state ofaffairs of SCU in subsequent financial years, otherthan:On 30 August 2017 SCU sold its property at 27-29Church Street Lidcombe for a gross sale price of$3,000,000. The estimated profit from the sale ofthis property is $2,046,254. SCU has entered into anagreement with the purchaser to lease back theproperty and will continue to operate its LidcombeBranch operations from the premises.

Likely Developments And Results

No other matter, circumstance or likely developmentin the operations has arisen since the end of thefinancial year that has significantly affected or maysignificantly affect:

(i) The operations of SCU;(ii) The results of those operations; or(iii) The state of affairs of SCU

in the financial years subsequent to this financialyear.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 8

Auditors’ Independence

The auditors have provided the declaration ofindependence to the Board as prescribed by theCorporations Act 2001 as set on page 10 of thisreport.

Rounding

The amounts contained in the financial statementshave been rounded to the nearest one thousanddollars in accordance with ASIC Corporations(Rounding in Financial/Directors’ Reports) Instrument2016/191. SCU is permitted to round to the nearestone thousand ($’000) for all amounts exceptprescribed disclosures which are shown in wholedollars.

This report is made in accordance with a resolutionof the Board of Directors and is signed for and onbehalf of the Directors by:

Signed and dated this 28 September 2017

Sydney Credit Union Ltd | ABN 93 087 650 726 9

scu.net.au 2017 Annual Report

H Kludass R ThornChair Chair, Board Audit Committee

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 9

64

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited. Liability limited by a scheme approved under Professional Standards Legislation.

Level 17, 383 Kent Street Sydney NSW 2000 Correspondence to: Locked Bag Q800 QVB Post Office Sydney NSW 1230 T +61 2 8297 2400 F +61 2 9299 4445 E [email protected] W www.grantthornton.com.au

Auditor’s Independence Declaration To the Directors of Sydney Credit Union Ltd In accordance with the requirements of section 307C of the Corporations Act 2001, as lead auditor for the audit of Sydney Credit Union Ltd for the year ended 30 June 2017, I declare that, to the best of my knowledge and belief, there have been:

a no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and

b no contraventions of any applicable code of professional conduct in relation to the audit.

GRANT THORNTON AUDIT PTY LTD Chartered Accountants

C L Gilmartin Partner - Audit & Assurance Sydney, 28 September 2017

2017 Annual Report scu.net.au

10 Sydney Credit Union Ltd | ABN 93 087 650 726

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 10

9

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited. Liability limited by a scheme approved under Professional Standards Legislation.

Level 17, 383 Kent Street Sydney NSW 2000 Correspondence to: Locked Bag Q800 QVB Post Office Sydney NSW 1230 T +61 2 8297 2400 F +61 2 9299 4445 E [email protected] W www.grantthornton.com.au

Independent Auditor’s Report To the members of Sydney Credit Union Ltd Auditor’s Opinion We have audited the financial report of Sydney Credit Union Ltd (the Company), which comprises the statement of financial position as at 30 June 2017, the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies, and the directors’ declaration. In our opinion, the accompanying financial report of Sydney Credit Union Ltd is in accordance with the Corporations Act 2001, including: a giving a true and fair view of the Company’s financial position as at 30 June 2017 and of its

performance for the year ended on that date; and

b complying with Australian Accounting Standards and the Corporations Regulations 2001. Basis for Opinion We conducted our audit in accordance with Australian Auditing Standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Report section of our report. We are independent of the Company in accordance with the Corporations Act 2001 and the ethical requirements of the Accounting Professional and Ethical Standards Board’s APES 110 Code of Ethics for Professional Accountants (the Code) that are relevant to our audit of the financial report in Australia. We have also fulfilled our other ethical responsibilities in accordance with the Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Information other than the Financial Report and Auditor's Report The Directors are responsible for the other information. The other information comprises the information included in the Company’s report for the year ended 30 June 2017, but does not include the financial report and our auditor’s report thereon.

Sydney Credit Union Ltd | ABN 93 087 650 726 11

scu.net.au 2017 Annual Report

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 11

10

Our opinion on the financial report does not cover the other information and accordingly we do not express any form of assurance conclusion thereon. In connection with our audit of the financial report, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial report or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard. Responsibilities of the Directors for the Financial Report The Directors of the Company are responsible for the preparation of the financial report that gives a true and fair view in accordance with Australian Accounting Standards and the Corporations Act 2001. The Directors responsibility also includes such internal control as the Directors determine is necessary to enable the preparation of the financial report that gives a true and fair view and is free from material misstatement, whether due to fraud or error. In preparing the financial report, the Directors are responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so. Auditor’s Responsibilities for the Audit of the Financial Report Our objectives are to obtain reasonable assurance about whether the financial report as a whole is free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with the Australian Auditing Standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of this financial report. A further description of our responsibilities for the audit of the financial report is located at the Auditing and Assurance Standards Board website at: http://www.auasb.gov.au/auditors_files/ar3.pdf . This description forms part of our auditor’s report.

GRANT THORNTON AUDIT PTY LTD Chartered Accountants

Claire Gilmartin Partner - Audit & Assurance Sydney, 28 September 2017

2017 Annual Report scu.net.au

12 Sydney Credit Union Ltd | ABN 93 087 650 726

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 12

Sydney Credit Union Ltd | ABN 93 087 650 726 13

scu.net.au 2017 Annual Report

Directors’ Declaration

1. In the opinion of the Directors of the SydneyCredit Union Limited:(a) the financial statements and notes of

Sydney Credit Union Limited are inaccordance with the Corporations Act2001, including (i) complying with Australian

Accounting Standards (includingthe Australian AccountingInterpretations) and theCorporations Regulations 2001;and

(ii) giving a true and fair view of theCompany’s financial position asat 30 June 2017 and of its perform ance for the year endedon that date.

(b) there are reasonable grounds tobelieve that Sydney Credit UnionLimited will be able to pay its debts asand when they become due andpayable.

2. The financial statements comply withInternational Financial Reporting Standards.

This declaration is made in accordance with aresolution of the Board of Directors and is signed forand on behalf of the Directors by:

H KludassChair

Dated this 28 September 2017

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 13

14 Sydney Credit Union Ltd | ABN 93 087 650 726

2017 Annual Report scu.net.au

Statement of Profit and Loss and OtherComprehensive Incomefor the year ended 30 June 2017

Note 2017 2016$’000 $’000

Interest revenue 2.a 31,821 33,696Less: Interest expense 2.c 11,888 13,558Net Interest income 19,933 20,138

Add: Fees, Commission and Other Income 2.b 3,987 3,599Sub Total 23,920 23,737

Less: Non-Interest Expenses Impairment Losses on loans receivable from Members 2.d 348 31Fee and Commission expenses 4,435 4,116

4,783 4,147General Administration — Employees compensation and benefits 11,036 10,614— Depreciation and Amortisation 2.e 651 765— Information Technology 182 395— Office Occupancy 1,954 1,915— Other Administration 1,418 2,022Total General Administration 15,241 15,711

Other Operating Expenses 2.f 984 840

Total Non-Interest Expenses 21,008 20,698

Profit before Income Tax 2,912 3,039

Income Tax Expense 3 754 694

Profit after Income Tax 2,158 2,345

Add: Other Comprehensive IncomeOther Increases in Members equity - -

Total comprehensive income 2,158 2,345

The above Statement of Profit and Loss and OtherComprehensive Income should be read in conjunctionwith the accompanying notes.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 14

Sydney Credit Union Ltd | ABN 93 087 650 726 15

scu.net.au 2017 Annual Report

Statement of Changes in Member Equityfor the year ended 30 June 2017

Opening Profit Redemption Transfers ClosingBalance for the of Share to/(from) Dividends Balance1/7/2016 Year Capital Reserves Paid 30/6/2017

$’000 $’000 $’000 $’000 $’000 $’000

Preference Share Capital 1,753 - (1,753) - - -

Capital Reserve Account 683 - - 36 - 719

Asset Revaluation Reserve 2,458 - - - - 2,458

General Reserve 12,829 - - - - 12,829

General Reserve for Credit Losses 2,040 - - 260 - 2,300

Retained Earnings 56,636 2,158 - (296) (21) 58,477

TOTAL 76,399 2,158 (1,753) - (21) 76,783

Statement of Changes in Member Equityfor the year ended 30 June 2016

Opening Profit Gain on Transfers ClosingBalance for the Business to/(from) Dividends Balance1/7/2015 Year Transfer Reserves Paid 30/6/2016

$’000 $’000 $’000 $’000 $’000 $’000

Preference Share Capital 1,753 - - - - 1,753

Capital Reserve Account 672 - - 11 - 683

Asset Revaluation Reserve 2,458 - - - - 2,458

General Reserve 12,829 - - - - 12,829

General Reserve for Credit Losses 2,040 - - - - 2,040

Retained Earnings 54,376 2,345 - (11) (74) 56,636

TOTAL 74,128 2,345 - - (74) 76,399

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 15

16 Sydney Credit Union Ltd | ABN 93 087 650 726

2017 Annual Report scu.net.au

Note 2017 2016$’000 $’000

ASSETSCash and Cash Equivalents 4 13,359 27,748Liquid Investments at Amortised Cost 5 216,007 210,904Receivables 6 2,209 2,067Prepayments 378 330Loans to Members 7 & 8 621,808 591,089Society One Loans 7 & 8 1,698 -Available for Sale Equity Investments 9 1,899 1,899Property, Plant and Equipment 10 7,296 7,767Taxation Assets 11 & 15 2,169 2,076Intangible Assets 12 220 215

TOTAL ASSETS 867,043 844,095

LIABILITIESDeposits from Members 13 777,372 753,627Creditor Accruals and Settlement Accounts 14 6,994 8,382Borrowings – Subordinated Deposit 17 1,997 1,989Taxation Liabilities 15 134 64Provisions 16 3,763 3,634

TOTAL LIABILITIES 790,260 767,696

NET ASSETS 76,783 76,399

MEMBERS EQUITYPreference Share Capital 18 - 1,753Capital Reserve Account 19 719 683Asset Revaluation Reserve 20 (i) 2,458 2,458General Reserves 20 (ii) 12,829 12,829General Reserve for Credit Losses 21 2,300 2,040Retained Earnings 58,477 56,636TOTAL MEMBERS EQUITY 76,783 76,399

The above Statement of Financial Position should beread in conjunction with the accompanying notes.

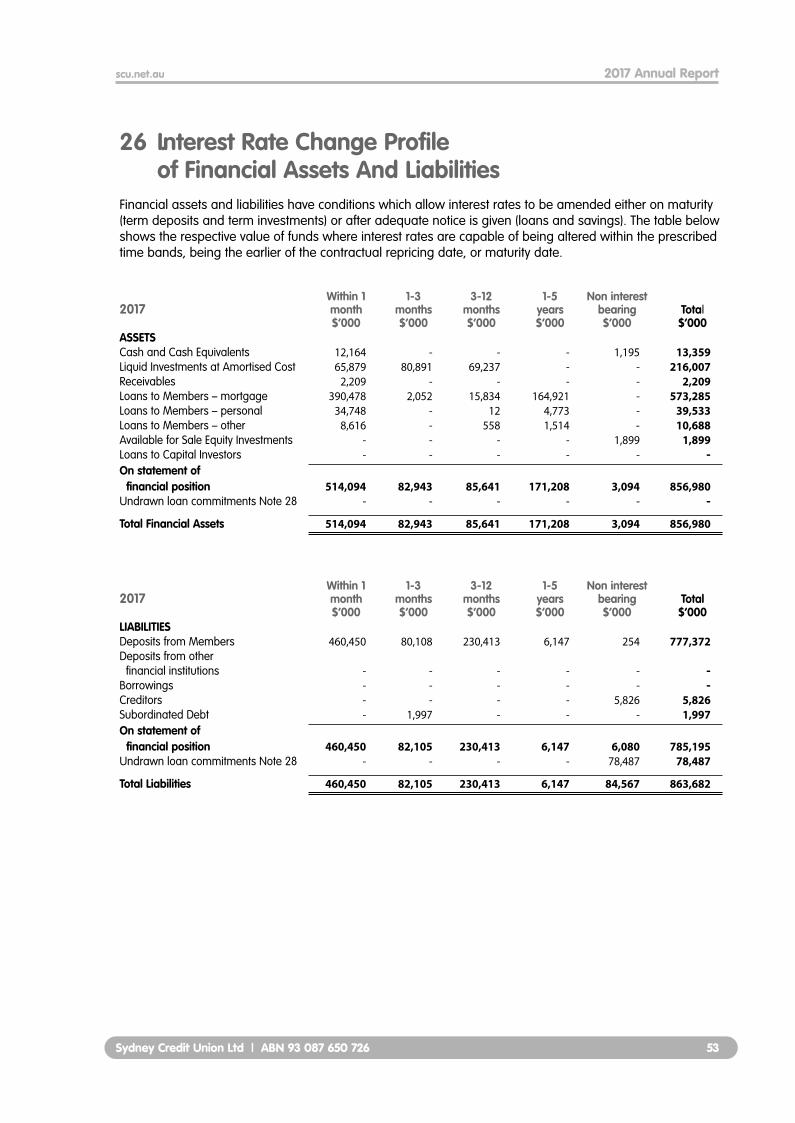

Note Description Note Description22 Financial Risk Management Objectives and Policies 30 Contingent liabilities23 Categories of financial instruments 31 Disclosures on Directors and other Key 24 Maturity profile of Financial Assets and Liabilities Management Personnel25 Non-Current Profile of Financial Assets and Liabilities 32 Economic dependency26 Interest rate change profile of Financial Assets and 33 Superannuation liabilities

Liabilities 34 Securitisation27 Net fair value of Financial Assets and Liabilities 35 Notes to statement of cash flows28 Financial commitments 36 Corporate information29 Standby borrowing facilities 37 Subsequent events

Statement of Financial Positionas at 30 June 2017

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 16

Sydney Credit Union Ltd | ABN 93 087 650 726 17

scu.net.au 2017 Annual Report

Note 2017 2016$’000 $’000

REVENUE ACTIVITIES

Revenue InflowsInterest received 31,752 34,622Fees and commissions 3,174 2,989Dividends 538 405Other income 182 185

35,646 38,201Revenue OutflowsInterest paid (12,310) (14,187)Suppliers and employees (19,948) (19,804)Income taxes paid (772) (406)Dividends Paid (21) (74)

(33,051) (34,471)Net Cash from Revenue Activities 35(c) 2,595 3,730

INFLOWS FROM OTHER OPERATING ACTIVITIESDecrease in Member loans (net movement) (32,724) (1,125)Increase in Member deposits and shares (net movement) 22,753 30,827Decrease in receivables from other financial institutions (net movement) (5,103) (19,712)

Net Cash from Operating Activities (15,074) 9,990

INVESTING ACTIVITIES

InflowsProceeds on sale of property, plant and equipment 49 28Less: Outflows Purchase of intangible assets (102) (77)Purchase of Investment Shares - -Purchase of property plant and equipment (104) (84)Net Cash from Investing Activities (157) (133)

FINANCING ACTIVITIES

Inflows (Outflows)Decrease in preference shares (1,753) -Increase in preference shares - -Net Cash from Financing Activities (1,753) -

Total Net Cash increase/(decrease) (14,389) 13,587Cash at Beginning of Year 27,748 14,161Cash at End of Year 35(a) 13,359 27,748

The above Statement of Cash Flows should be read in conjunction with the accompanying notes.

Statement of Cash Flowsfor the year ended 30 June 2017

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 17

2017 Annual Report scu.net.au

18 Sydney Credit Union Ltd | ABN 93 087 650 726

1. Statement of Significant Accounting PoliciesThis financial report is prepared for SCU as a single entity, for the year ended the 30 June 2017. The reportwas authorised for issue on 28 September 2017 in accordance with a resolution of the Board of Directors. The financial report is presented in Australian dollars.

The financial report is a general purpose financial report which has been prepared in accordance with therequirements of the Corporations Act 2001, Australian Accounting Standards and other authoritativepronouncements of the Australian Accounting Standards Board. Compliance with Australian AccountingStandards ensures compliance with the International Financial Reporting Standards (IFRSs) as issued by theInternational Accounting Standards Board (IASB). SCU is a for-profit entity for the purpose of preparing thefinancial statements.

a. Basis of Measurement

The financial statements have been prepared on an accruals basis, and are based on historicalcosts, which do not take into account changing money values or current values of non-currentassets. The accounting policies are consistent with the prior year unless otherwise stated.

b. Classification and subsequent measurement of financial assets and financial liabilities

Financial assets and financial liabilities are recognised when SCU becomes a party to the contractualprovisions of the financial instrument, and are measured initially at fair value adjusted by transac -tions costs, except for those carried at fair value through profit or loss, which are measured initially atfair value. Subsequent measurement of financial assets and financial liabilities are described below.

Financial assets are derecognised when the contractual rights to the cash flows from the financialasset expire, or when the financial asset and all substantial risks and rewards are transferred.A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.

(i) Classification and subsequent measurement of financial assets

For the purpose of subsequent measurement, financial assets other than those designatedand effective as hedging instruments are classified into the following categories upon initialrecognition: • loans and receivables• financial assets at fair value through profit or loss (FVTPL) • held-to-maturity (HTM) investments • available-for-sale (AFS) financial assets.

The category determines subsequent measurement and whether any resulting income andexpense is recognised in profit or loss or in other comprehensive income.

All financial assets except for those at FVTPL are subject to review for impairment at least ateach reporting date to identify whether there is any objective evidence that a financial asset ora group of financial assets is impaired. Different criteria to determine impairment are appliedfor each category of financial assets, which are described below. As at 30 June 2017, SCU didnot hold any financial assets at FVTPL.

All income and expenses relating to financial assets that are recognised in profit or loss, arepresented within interest revenue and interest expense, except for impairment of loans andreceivables which is presented within other expenses.

(ii) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinablepayments that are not quoted in an active market. After initial recognition, these aremeasured at amortised cost using the effective interest method, less provision for impairment.SCU's Liquid Investments (Term Deposits), trade and most other receivables fall into thiscategory of financial instruments.

Individually significant receivables are considered for impairment when they are past due orwhen other objective evidence is received that a specific counterparty will default. Receivables

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 18

Sydney Credit Union Ltd | ABN 93 087 650 726 19

scu.net.au 2017 Annual Report

that are not considered to be individually impaired are reviewed for impairment, which aredetermined by reference to the industry and region of a counterparty and other shared creditrisk characteristics. The impairment loss estimate is then based on recent historical counter -party default rates for each identified Credit Union.

(iii) HTM investments

HTM investments are non-derivative financial assets with fixed or determinable payments andfixed maturity other than loans and receivables. Investments are classified as HTM if SCU hasthe intention and ability to hold them until maturity. SCU currently holds Negotiable Certificatesof Deposit (NCD), Bonds, and Bank accepted Bills Of Exchange in this category. If more thanan insignificant portion of these assets are sold or redeemed early then the asset class will bereclassified as Available For Sale financial assets.

HTM investments are measured subsequently at amortised cost using the effective interestmethod. If there is objective evidence that the investment is impaired, determined by referenceto external credit ratings, the financial asset is measured at the present value of estimatedfuture cash flows. Any changes to the carrying amount of the investment, includingimpairment losses, are recognised in profit and loss.

(iv) Available For Sale (AFS) financial assets

AFS financial assets are non-derivative financial assets that are either designated to thiscategory or do not qualify for inclusion in any of the other categories of financial assets. SCU'sAFS financial assets, include the equity investment in Cuscal Limited, Shared Service PartnersPty Ltd (SSP) and TransAction Solutions Pty Limited (TAS).

The equity investment in Cuscal Limited, SSP and TAS are measured at cost less anyimpairment charges, as its fair value cannot currently be estimated reliably. Impairmentcharges are recognised in profit or loss.

All other AFS financial assets are measured at fair value. Gains and losses on these assets arerecognised in other comprehensive income and reported within the AFS reserve within equity,except for impairment losses, which are recognised in profit or loss. When the asset isdisposed of or is determined to be impaired, the cumulative gain or loss is recognised as areclassification adjustment within the comprehensive income. Interest is calculated using theeffective interest method and dividends are recognised in profit or loss within 'other income'.

Reversals of impairment losses are recognised in other comprehensive income, except forfinancial assets that are debt securities which are recognised in profit or loss only if the reversalcan be objectively related to an event occurring after the impairment loss was recognised.

(v) Classification and subsequent measurement of financial liabilities

SCU’s financial liabilities include borrowings and trade and other payables.

Financial liabilities are measured subsequently at amortised cost using the effective interestmethod.

c. Loans to Members

(i) Basis of recognition

All loans are initially recognised at fair value, net of loan origination fees and inclusive oftransaction costs incurred. Loans are subsequently measured at amortised cost. Anydifference between the proceeds and the redemption amount is recognised in the incomestatement over the period of the loans using the effective interest method.

Loans to Members are reported at their recoverable amount representing the aggregateamount of principal and unpaid interest owing to SCU at balance date, less any allowance orprovision against impairment for debts considered doubtful. A loan is classified as impairedwhere recovery of the debt is considered unlikely as determined by the Board of Directors.

(ii) Interest earned

Term loans – The loan interest is calculated on the basis of daily balance outstanding and ischarged in arrears to a Member’s account on the last day of each month.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 19

2017 Annual Report scu.net.au

20 Sydney Credit Union Ltd | ABN 93 087 650 726

Overdraft – The loan interest is calculated initially on the basis of the daily balanceoutstanding and is charged in arrears to a Member’s account on the last day of each month.

Credit cards – The interest is calculated initially on the basis of the daily balance outstandingand is charged in arrears to a Member’s account on the 28th day of each month, on cashadvances and purchases in excess of the payment due date. Purchases are granted up to 55days interest free until the due date for payment.

Non-accrual loan interest – While still legally recoverable, interest is not brought to account asincome where SCU is informed that the Member has deceased, or, where a loan is impaired.

(iii) Loan origination fees and discounts

Loan establishment fees and discounts are initially deferred as part of the loan balance, andare brought to account as income over the expected life of the loan as interest revenue.

(iv) Transaction costs

Transaction Costs are expenses which are direct and incremental to the establishment of theloan. These costs are initially deferred as part of the loan balance, and are brought to accountas a reduction to income over the expected life of the loan. The amounts brought to accountare included as part of Interest revenue.

(v) Fees on loans

The fees charged on loans after origination of the loan are recognised as income when theservice is provided or costs are incurred.

(vi) Net gains and losses

Net gains and losses on loans to Members to the extent that they arise from the partialtransfer of business or on securitisation, do not include impairment write downs or reversalsof impairment write downs.

d. Loan Impairment

(i) Specific and Collective Provision for Impairment

A provision for losses on impaired loans is recognised when there is objective evidence thatthe impairment of a loan has occurred. Estimated impairment losses are calculated on eithera portfolio basis for loans of similar characteristics, or on an individual basis. The amountprovided is determined by management and the board to recognise the probability of loanamounts not being collected in accordance with terms of the loan agreement. The criticalassumptions used in the calculation are as set out in Note 8. Note 22 details the credit riskmanagement approach for loans

The APRA Prudential Standards require a minimum provision to be maintained, based onspecific percentages on the loan balance which are contingent upon the length of time therepayments are in arrears. This approach is used to assess the collective provisions forimpairment.

An assessment is made at each statement of financial position date to determine whetherthere is objective evidence that a specific financial asset or a group of financial assets isimpaired. Evidence of impairment may include indications that the borrower has defaulted, isexperiencing significant financial difficulty, or where the debt has been restructured to reducethe burden to the borrower.

(ii) General Reserve for Credit Losses

In addition to the above specific provision, the Board has recognised the need to make anallocation from retained earnings to ensure there is adequate protection for Members againstthe prospect that some Members will experience loan repayment difficulties in the future. Thereserve is based on estimation of potential risk in the loan portfolio based upon:

– the level of security taken as collateral; and– the concentration of loans taken by employment type.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 20

Sydney Credit Union Ltd | ABN 93 087 650 726 21

scu.net.au 2017 Annual Report

(iii) Renegotiated loans

Loans which are subject to renegotiated terms which would have otherwise been impaired donot have the repayment arrears diminished and interest continues to accrue to income. Eachrenegotiated loan is retained at the full arrears position until the normal repayments arereinstated and brought up to date and maintained for a period of 6 months.

e. Bad debts written off (direct reduction in loan balance)

Bad debts are written off from time to time as determined by management and the Board of Directorswhen it is reasonable to expect that the recovery of the debt is unlikely. Bad debts are written offagainst the provisions for impairment, if a provision for impairment had previously been recognised. Ifno provision had been recognised, the write offs are recognised as expenses in the income statement.

f. Property, Plant and Equipment

Land and buildings are measured at acquisition cost less accumulated depreciation. Valuations areobtained where the Directors believe there has potentially been a diminution in the value of land andBuildings owned by SCU and used to determine the need to recognise in the accounts any impair -ment to the acquisition cost. Any revaluation increments are credited to the asset revaluation reserve,unless it reverses a previous decrease in value in the same asset previously debited to the profit orloss. Revaluation decreases are debited to the profit and loss unless it directly offsets a previousrevaluation increase in the same asset in the asset revaluation reserve.

Property, plant and equipment with the exception of freehold land, are depreciated on a straight linebasis so as to write off the net cost of each asset over its expected useful life to SCU. The useful lives areadjusted as appropriate at each reporting date. Estimated useful lives at the balance date are as follows:

– Buildings – 40 years.– Leasehold Improvements – lesser of the lease term or 10 years.– Plant and Equipment – 3 to 7 years.– Assets less than $300 are not capitalised.

g. Receivables from Other Financial Institutions

Term deposits, Bonds and Negotiable Certificates of Deposit with other financial institutions areunsecured and have a carrying amount equal to their principal amount. Interest is paid on the dailybalance at maturity. All deposits are in Australian currency.

The accrual for interest receivable is calculated on a proportional basis of the expired period of theterm of the investment. Interest receivable is included in the amount of receivables in the statementof financial position.

h. Equity Investments and Other Securities

Investments in shares are classified as available for sale financial assets where they do not qualifyfor classification as loans and receivables, or investments held for trading.

Investments in shares listed on the stock exchanges are re-valued to fair value based on the marketbid price at the close of business on statement of financial position date. The gains and losses in fairvalue are reflected in equity through the asset revaluation reserve.

Investments in shares which do not have a ready market and are not capable of being reliablyvalued are recorded at the lower of cost or recoverable amount.

Realised net gains and losses on available for sale financial assets taken to the profit and lossaccount comprises only gains and losses on disposal.

All investments are in Australian currency.

i. Member Deposits

(i) Basis for Measurement

Member savings and term investments are quoted at the aggregate amount of money owingto depositors.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 21

2017 Annual Report scu.net.au

22 Sydney Credit Union Ltd | ABN 93 087 650 726

(ii) Interest Payable

Interest on savings is calculated on the daily balance and posted to the accounts periodically,or on maturity of the term deposit. Interest on savings is brought to account on amount ofmoney owing to depositors on an accrual basis in accordance with the interest rate terms andconditions of each savings and term deposit account as varied from time to time. The amountof the accrual is shown as part of amounts payable.

j. Borrowings

All loans and borrowings are initially recognised at fair value, net of transaction costs incurred.Borrowings are subsequently measured at amortised cost. Any difference between the proceeds (netof transaction costs) and the redemption amount is recognised in the profit and loss over the periodof the loans and borrowings using the effective interest method.

k. Provision for Employee Benefits

Provision is made for SCU’s liability for employee benefits, including annual leave and personal leavearising from services rendered by employees to balance date. Employee benefits expected to besettled within one year, have been measured at their nominal amount.

Other employee benefits payable later than one year have been measured at the present value ofthe estimated future cash outflows to be made for those benefits discounted using nationalgovernment bond rates.

Provision for long service leave is on a pro-rata basis from commencement of employment with SCUbased on the present value of its estimated future cash flows.

Annual leave is accrued in respect of all employees on pro-rata entitlement for part years of serviceand leave entitlement due but not taken at balance date. Annual leave is reflected as part of thesundry creditors and accruals.

Contributions are made by SCU to an employee’s superannuation fund and are charged to theincome statement as incurred.

l. Leasehold on Premises

Leases where the lessor retains substantially all the risks and rewards of ownership of the net assetare classified as operating leases. Payments made under operating leases (net of incentivesreceived from the lessor) are charged to the income statement on a straight-line basis over theperiod of the lease.

A provision is recognised for the estimated make good costs on the operating leases, based on theNet Present Value of the future expenditure at the conclusion of the lease term discounted at 5%.

Increases in the provision in future years due to the unwinding of the interest charge, is recognisedas part of the interest expense.

m. Income Tax

The income tax expense shown in the Profit and Loss is based on the operating profit before incometax adjusted for any non tax deductible, or non-assessable items between accounting profit andtaxable income. Deferred Tax Assets and Liabilities are recognised using the statement of financialposition liability method in respect of temporary differences arising between the tax bases of assetsor liabilities and their carrying amounts in the financial statements. Current and deferred taxbalances relating to amounts recognised directly in equity are also recognised directly in equity.

Deferred tax assets and liabilities are recognised for all temporary differences between carryingamounts of assets and liabilities for financial reporting purposes and their respective tax bases at therate of income tax applicable to the period in which the benefit will be received or the liability willbecome payable. These differences are presently assessed at 30%.

Deferred tax assets are only brought to account if it is probable that future taxable amounts will beavailable to utilise those temporary differences. The recognition of these benefits is based on theassumption that no adverse change will occur in income tax legislation; and the anticipation that

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 22

Sydney Credit Union Ltd | ABN 93 087 650 726 23

scu.net.au 2017 Annual Report

SCU will derive sufficient future assessable income and comply with the conditions of deductibilityimposed by the law to permit a future income tax benefit to be obtained.

n. Cash and cash Equivalents

Cash comprises cash on hand and demand deposits. Cash equivalents are short-term, highly liquidinvestments that are readily convertible to known amounts of cash and which are subject to aninsignificant risk of changes in value.

o. Intangible Assets

Items of computer software which are not integral to the computer hardware owned by SCU areclassified as intangible assets.

Computer software held as intangible assets is amortised over the expected useful life of thesoftware. These lives range from 2 to 5 years.

p. Goods and Services Tax (GST)

As a financial institution SCU is input taxed on all income except other income from commissionsand some fees. An input taxed supply is not subject to GST collection, and similarly the GST paid onrelated or apportioned purchases cannot be recovered. As some income is charged GST, the GST onpurchases are generally recovered on a proportionate basis. In addition certain prescribedpurchases are subject to reduced input tax credits (RITC), of which 75% of the GST paid isrecoverable.

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST). Tothe extent that the full amount of GST incurred is not recoverable from the Australian Tax Office (ATO),the GST is recognised as part of the cost of acquisition of the asset or as part of an item of the expense.

Receivables and payables are stated with the amount of GST included where applicable GST iscollected. The net amount of GST recoverable from, or payable to, the ATO is included as a currentasset or current liability in the statement of financial position. Cash flows are included in the cashflow statement on a gross basis. The GST components of cash flows arising from investing andfinancing activities which are recoverable from, or payable to, the Australian Taxation Office areclassified as operating cash flows.

q. Business Combinations

The Group applies the acquisition method in accounting for business combinations.

Under Financial Sector (Transfers of Business) Act 1999 all the assets and liabilities of the transferringbody, wherever those assets and liabilities are located, become (respectively) assets and liabilities ofthe receiving body without any transfer, conveyance or assignment.

The consideration transferred by SCU to obtain control of the net assets is calculated as the sum ofthe acquisition-date fair values of assets transferred, liabilities incurred and the equity interestsissued by SCU, which includes the fair value of any asset or liability arising from a contingentconsideration arrangement. Acquisition costs are expensed as incurred.

SCU recognises identifiable assets acquired and liabilities assumed in a business combinationregardless of whether they have been previously recognised in the acquired entity's financialstatements prior to the acquisition. Assets acquired and liabilities assumed are generally measuredat their acquisition-date fair values.

Goodwill (if applicable) is stated after separate recognition of any identifiable intangible assets. It iscalculated as the excess of the sum of (a) fair value of consideration transferred, (b) the recognisedamount of any non-controlling interest in the acquired entity and (c) acquisition-date fair value of anyexisting equity interest in the acquired entity, over the acquisition-date fair values of identifiable netassets.

Where the fair values of identifiable net assets exceed the sum calculated above, the excess amountis recognised directly in equity for a mutual organisation [as prescribed by AASB 3 Guidance B47].Acquisition costs are expensed as incurred.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 23

2017 Annual Report scu.net.au

24 Sydney Credit Union Ltd | ABN 93 087 650 726

r . Impairment of Assets

At each reporting date SCU assesses whether there is any indication that individual assets areimpaired. Where impairment indicators exist, recoverable amount is determined and impairmentlosses are recognised in the profit and loss where the asset's carrying value exceeds its recoverableamount. Recoverable amount is the higher of an asset's fair value less costs to sell and value in use.For the purpose of assessing value in use, the estimated future cash flows are discounted to theirpresent value using a pre-tax discount rate that reflects current market assessments of the timevalue of money and the risks specific to the asset. Where it is not possible to estimate recoverableamount for an individual asset, recoverable amount is determined for the cash-generating unit towhich the asset belongs.

s. Accounting Estimates and Judgements

Management have made judgements when applying SCU’s accounting policies with respect to

i. De-Recognition of loans assigned to a special purpose vehicle used for securitisationpurposes – refer Note 34.

ii. The classification of preference shares as equity instruments – refer Note 18.

Management have made critical accounting estimates when applying SCU’s accounting policies withrespect to the impairment provisions for loans – refer Note 8.

t. Rounding

The amounts contained in the financial statements have been rounded to the nearest one thousanddollars in accordance with ASIC Corporations (Rounding in Financial/Directors’ Reports) Instrument2016/191. SCU is permitted to round to the nearest one thousand ($’000) for all amounts exceptprescribed disclosures which are shown in whole dollars.

u. New standards applicable for the current year

There were no new or revised accounting standards applicable for financial years commencing from1 July 2016 that had any significant impact on the financial statements of SCU.

v. New or emerging standards not yet mandatory

Certain Accounting standards and interpretations have been published that are not mandatory for30 June 2017 reporting periods. SCU’s assessment of the impact of these new standards andinterpretations is set out below.

AASBReference

AASB 9 FinancialInstruments(Issued December2015)

Nature of Change

The new standard replaces AASB 139 and supersedesAASB 9 versions previously issued in December 2009 andDecember 2010. It amends the requirements forclassification and measurement of financial assets.AASB 9 requirements regarding hedge accounting

represent a substantial overhaul of hedge accounting thatenable entities to better reflect their risk managementactivities in the financial statements. Furthermore, AASB 9 introduces a new impairment model

based on expected credit losses. Recognition of creditlosses are to no longer be dependent on SCU firstidentifying a credit loss event. SCU will consider a broaderrange of information when assessing credit risk andmeasuring expected credit losses including past experienceof historical losses for similar financial instruments.

ApplicationDate

Periodsbeginning onor after 1January 2018

Impact on Initial Application

Due to the recent release of theseamendments and that adoption is onlymandatory for the 30 June 2019 year end,SCU has not yet made a detailedassessment of the impact of theseamendments.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 24

Sydney Credit Union Ltd | ABN 93 087 650 726 25

scu.net.au 2017 Annual Report

AASBReference

AASB 15Revenue fromContracts withCustomers

AASB 16 Leases Replaces AASB 117

AASB 2016-1Amendments toAustralianAccountingStandards -Disclosure Initiative:Amendments toAASB 112.

AASB 2016-2Amendments toAustralianAccountingStandards –Disclosure Initiative:Amendments toAASB 107.

Transfers ofInvestment Property(Amendments to IAS40).

Nature of Change

Revenue from financial instruments is not covered by thisnew Standard, but AASB 15 establishes a new revenuerecognition model for other types of revenue.AASB 15 is based on the principle that revenue is

recognised when control of a good or service transfers to acustomer. The standard replaces AASB 118 Revenue, AASB111 Construction Contracts and related revenueinterpretations.

AASB 16: replaces AASB 117 Leases and some lease-relatedInterpretations • requires all leases to be accounted for ‘on-balance sheet’

by lessees, other than short-term and low value assetleases

• provides new guidance on the application of thedefinition of lease and on sale and lease backaccounting

• requires new and different disclosures about leases

AASB 2016-1 amends AASB 112 Income Taxes to clarify howto account for deferred tax assets related to debtinstruments measured at fair value, particularly wherechanges in the market interest rate decrease the fair valueof a debt instrument below cost.

AASB 2016-2 amends AASB 107 Statement of Cash Flows torequire entities preparing financial statements inaccordance with Tier 1 reporting requirements to providedisclosures that enable users of financial statements toevaluate changes in liabilities arising from financingactivities, including both changes arising from cash flowsand non-cash changes.

The amendments clarify that transfers to, or from,investment property are required when, and only when,there is a change in use of property supported by evidence.The amendments also re-characterise the list ofcircumstances appearing in IAS 40,57 (a) – (d) as a non-exhaustive list of examples of evidence that a change inuse has occurred. In addition, the IASB has clarified that achange in management’s intent, by itself, does not providesufficient evidence that a change in use has occurred.Evidence of a change in use must be observable.

ApplicationDate

Periodsbeginning onor after 1January 2018.

Periodsbeginning onor after 1January 2019

1 January2017

1 January2017

1 January2018

Impact on Initial Application

Based upon a preliminary assessment,the Standard is not expected to have amaterial impact upon the transactionsand balances recognised when it is firstadopted, as most of the Bank’s revenuearises from the provision of financialservices which are governed by AASB 9Financial Instruments. Few revenuetransactions of SCU are impacted by thenew standard.

SCU is yet to under take a detailedassessment of the impact of AASB 16. Whilst SCU owns a number of the

buildings used for its business, it alsoleases a number of its branch offices andwill therefore be impacted by this change.

When these amendments are firstadopted for the year ending 30 June 2018there will be no material impact on thefinancial statements.

When these amendments are firstadopted for the year ending 30 June 2018there will be no material impact on thefinancial statements.

When these amendments are firstadopted for the year ending 30 June 2019there will be no material impact on thefinancial statements.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 25

2017 Annual Report scu.net.au

26 Sydney Credit Union Ltd | ABN 93 087 650 726

2. Statement of Profit and Loss and Other Comprehensive Income

Note 2017 2016$’000 $’000

a. Analysis of interest revenue

Interest revenue on assets carried at amortised costCash – deposits at call 392 274Receivables from financial institutions 5,591 5,522Loans to Members 25,838 27,896Loans to capital investors - 4TOTAL INCOME FROM RECEIVABLES 31,821 33,696

b. Fee, commission and other income

Fee and commission revenueFee income on loans – other than loan origination fees 395 532Fee Income from Member deposits 875 1,025Other fee income 496 96Insurance commissions 595 467Other commissions 874 893TOTAL FEE AND COMMISSION REVENUE 3,235 3,013

Other income Available for sale assetsDividends received on available for sale assets 538 405Bad debts recovered 88 122Income from property (rental income) 97 42Gain on disposal of assets– Property, plant and equipment 29 17TOTAL FEE COMMISSION AND OTHER INCOME 3,987 3,599

c. Interest expenses

Interest expense on liabilities carried at amortised cost Deposits from Members 11,653 13,367Overdraft 21 19Interest – Subordinated Debt 214 172TOTAL INTEREST EXPENSE 11,888 13,558

d. Impairment losses Available for Sale Assets - -

Loans and advances Increase in provision for impairment 348 31

TOTAL IMPAIRMENT LOSSES 348 31

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 26

Sydney Credit Union Ltd | ABN 93 087 650 726 27

scu.net.au 2017 Annual Report

Note 2017 2016$’000 $’000

e. Other prescribed disclosures

General administration – employees costs include:– net movement in provisions for employee

annual leave 44 16– net movement in provisions for employee

long service leave 118 152

General Administration – Depreciation & Amortisation expense comprisesBuildings 212 212Plant and equipment 168 177Leasehold improvements (includes lease make-good prov.) 174 255Intangibles 97 121

651 765General Administration – Office Occupancy costs include –Property operating lease payments– minimum lease payments 1,350 1,334

f. Other Operating expenses include

Audit and review of financial statements (GST Exclusive)– Audit fees – current year – Grant Thornton 106 111

Other Services (GST Exclusive)

– Taxation Services – Grant Thornton 6 11– Compliance Services – Grant Thornton 7 3

119 125

Defined contribution superannuation expenses 16 13

Loss on disposal of assets– Property, plant, equipment - -

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 27

2017 Annual Report scu.net.au

28 Sydney Credit Union Ltd | ABN 93 087 650 726

Note 2017 2016$’000 $’000

3. Income Tax Expensea. The income tax expense comprises amounts

set aside as:-

Current tax expense 851 867Adjustments for previous years (10) (64)Deferred tax expense (87) (109)Total current income tax expense 754 694

b. The prima facie tax payable on profit is reconciled to the income tax expense in the accounts as follows:

Profit 2,912 3,039Prima facie tax payable on profit before income tax at 30% 874 911

Add tax effect of expenses not deductible– Other non-deductible expenses 162 67– Dividend Imputation adjustment 69 56Subtotal 1,105 1,034

Less– Deductions Allowed not in Accounting Expenses (22) (22)– Franking rebate (232) (186)– Deferred tax asset not previously brought to account (87) (68)– Adjustments for previous years (10) (64)Income tax expense attributableto current year profit 754 694

c. Franking CreditsFranking credits held by SCU after adjusting forfranking credits that will arise from the payment ofincome tax payable as at the end of the financial year is: 14,700 12,862

4. Cash and Cash EquivalentsCash on hand 1,195 1,323Deposits at call 12,164 26,425

13,359 27,748

5. Liquid Investments at Amortised Costa. Hold to Maturity

Negotiable Certificates of Deposits 131,965 119,786Bonds 32,040 31,358ReceivablesTerm Deposits 52,002 59,760

216,007 210,904b. Dissection of Receivables

Deposits with Industry Bodies – Cuscal 34,557 16,401Deposits with other Societies 41,390 40,957Deposits with banks 140,060 153,546

216,007 210,904

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 28

Sydney Credit Union Ltd | ABN 93 087 650 726 29

scu.net.au 2017 Annual Report

Note 2017 2016$’000 $’000

6. ReceivablesInterest receivable on deposits with other financial institutions 1,043 974

Sundry debtors and settlement accounts 1,166 1,0932,209 2,067

7. Loans To Membersa. Amount due comprises:

Overdrafts and revolving credit 16,646 17,588Term loans 607,582 574,091Subtotal 624,228 591,679Less:Unamortised loan origination fees (15) (53)Unearned Income (123) (126)Subtotal 624,090 591,500Less:Provision for impaired loans Note 8 (8) (584) (411)

623,506 591,089b. Credit Quality – Security held against loans

Secured by mortgage over business assets 5,375 4,372Secured by mortgage over real estate 581,409 544,876Partly secured by goods mortgage 9,850 10,856Wholly unsecured 27,594 31,575 Total 624,228 591,679

It is not practicable to value all collateral as at thebalance date due to the variety of assets andcondition. A breakdown of the quality of theresidential mortgage security on a portfolio basisis as follows:

Security held as mortgage against real estate is on the basis of

– loan to valuation ratio of less than 80% 518,956 469,826

– loan to valuation ratio of more than 80% but mortgage insured 55,423 61,998

– loan to valuation ratio of more than 80% and not mortgage insured 7,370 13,052

Total 581,749 544,876

The Board decided not to require disclosure of the fair value of collateral held, but to requiredisclosure of only a description of collateral held as security and other credit enhancements. TheBoard noted that such disclosure does not require an entity to establish fair values for all its collateral(in particular when the entity has determined that the fair value of some collateral exceeds thecarrying amount of the loan) and, thus, would be less onerous for entities to provide than fair values.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 29

2017 Annual Report scu.net.au

30 Sydney Credit Union Ltd | ABN 93 087 650 726

Note 2017 2016$’000 $’000

c. Concentration of Loans

The values discussed below include on statement of financial position values and off statement of financial position undrawn facilities as described in Note 29. (29)

(i) Loans to individual or related groups of Members which exceed 10% of Member’s equity in aggregate - -

(ii) There are no loans to Members concentrated to individuals employed in any individual industry

(iii) Loans to Members are concentrated in the following Geographical locations:

New South Wales 587,104 557,148ACT 6,932 6,043Victoria 7,643 4,510Queensland 16,840 18,092South Australia 1,200 1,756Western Australia 2,824 2,465Northern Territory 767 387Tasmania 918 1,278TOTAL 624,228 591,679

(iv) Loans by Customer type were:

Loans to Natural persons– Residential loans and facilities 574,007 538,691– Personal loans and facilities 36,644 39,623– Society One loans 1,751 -– Business loans and facilities - -

612,402 578,314 Loans to corporations 11,826 13,365TOTAL 624,228 591,679

8. Provision on Impaired Loans

a. Total provision comprises

Individual Specific provisions 531 394Society One provision 53 -General provision - 17Total Provision 584 411

b. Movement in the provision for impairment

Balance at the beginning of year 411 719Add (deduct):– Transfers from (to) Income Statement 348 31– Bad debts written off provision (175) (339)Specific Provision Balance at end of year 584 411

Details of credit risk management is set out in Note 22. (22)

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 30

Sydney Credit Union Ltd | ABN 93 087 650 726 31

scu.net.au 2017 Annual Report

2017 2016$’000 $’000

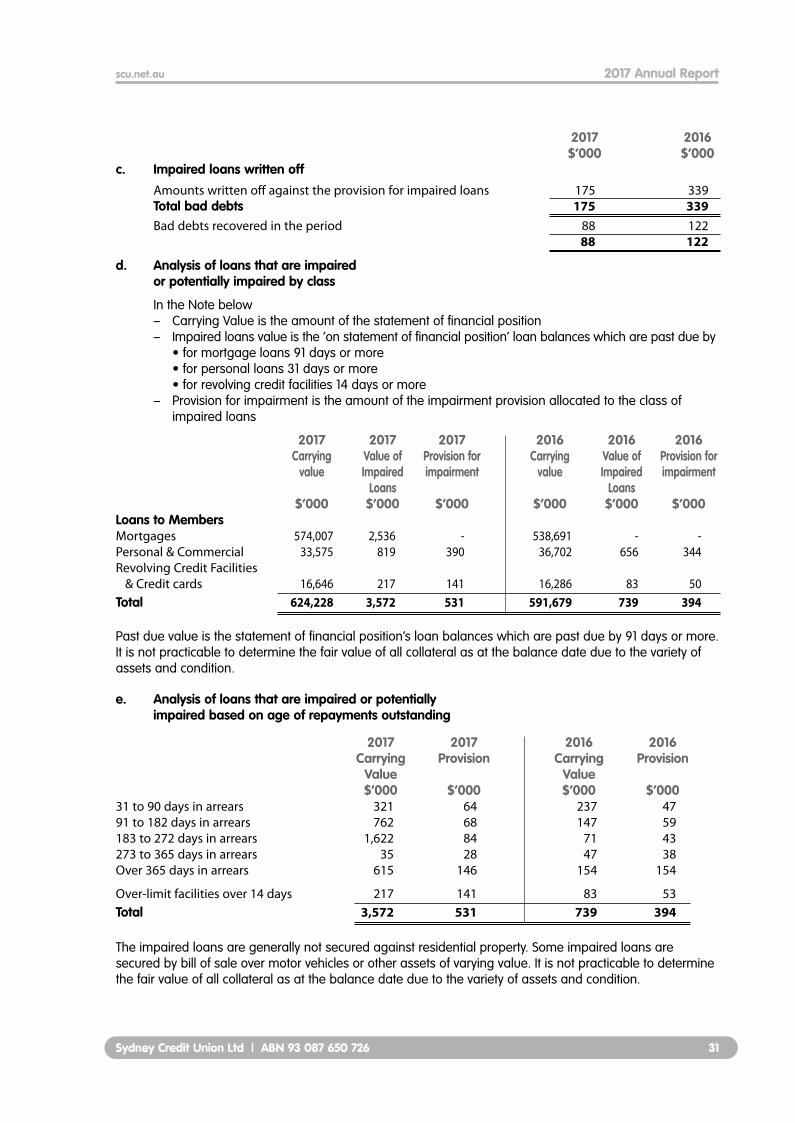

c. Impaired loans written off

Amounts written off against the provision for impaired loans 175 339Total bad debts 175 339Bad debts recovered in the period 88 122

88 122

d. Analysis of loans that are impaired or potentially impaired by class

In the Note below – Carrying Value is the amount of the statement of financial position– Impaired loans value is the ‘on statement of financial position’ loan balances which are past due by

• for mortgage loans 91 days or more • for personal loans 31 days or more• for revolving credit facilities 14 days or more

– Provision for impairment is the amount of the impairment provision allocated to the class ofimpaired loans

2017 2017 2017 2016 2016 2016Carrying Value of Provision for Carrying Value of Provision for

value Impaired impairment value Impaired impairmentLoans Loans

$’000 $’000 $’000 $’000 $’000 $’000Loans to Members Mortgages 574,007 2,536 - 538,691 - -Personal & Commercial 33,575 819 390 36,702 656 344Revolving Credit Facilities& Credit cards 16,646 217 141 16,286 83 50

Total 624,228 3,572 531 591,679 739 394

Past due value is the statement of financial position’s loan balances which are past due by 91 days or more.It is not practicable to determine the fair value of all collateral as at the balance date due to the variety ofassets and condition.

e. Analysis of loans that are impaired or potentially impaired based on age of repayments outstanding

2017 2017 2016 2016Carrying Provision Carrying Provision

Value Value$’000 $’000 $’000 $’000

31 to 90 days in arrears 321 64 237 4791 to 182 days in arrears 762 68 147 59183 to 272 days in arrears 1,622 84 71 43273 to 365 days in arrears 35 28 47 38Over 365 days in arrears 615 146 154 154

Over-limit facilities over 14 days 217 141 83 53Total 3,572 531 739 394

The impaired loans are generally not secured against residential property. Some impaired loans aresecured by bill of sale over motor vehicles or other assets of varying value. It is not practicable to determinethe fair value of all collateral as at the balance date due to the variety of assets and condition.

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 31

2017 Annual Report scu.net.au

32 Sydney Credit Union Ltd | ABN 93 087 650 726

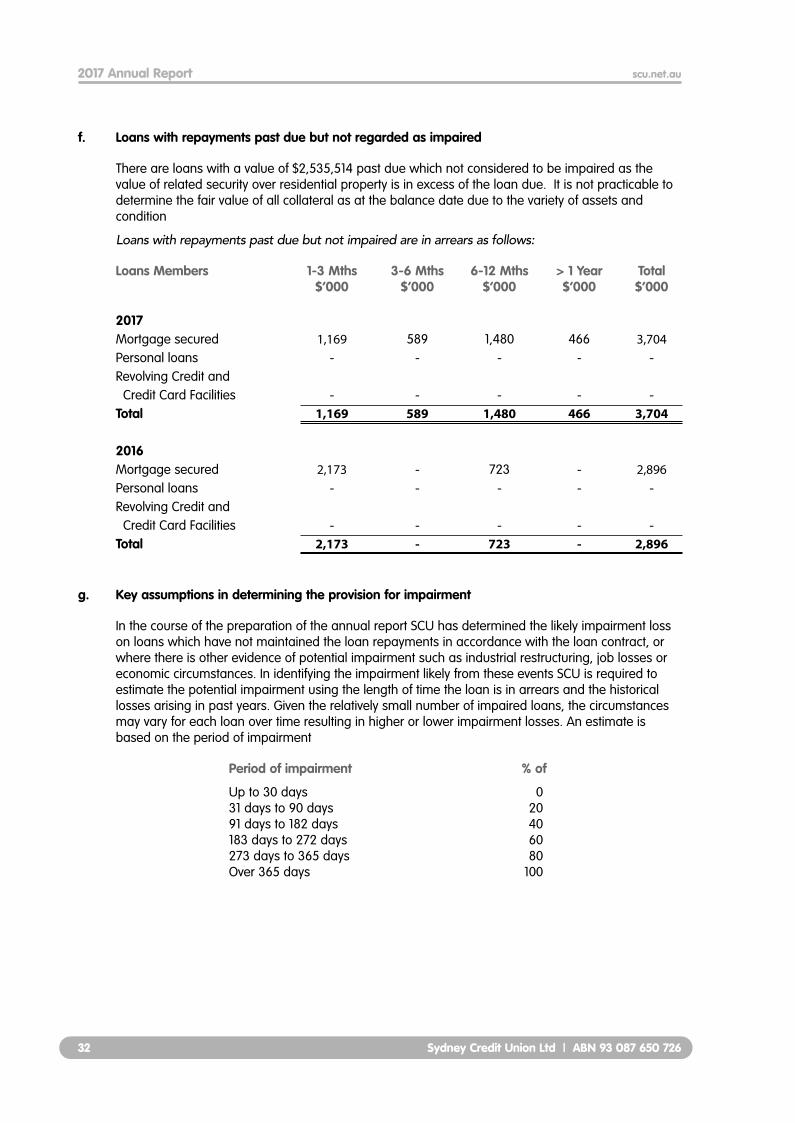

f. Loans with repayments past due but not regarded as impaired

There are loans with a value of $2,535,514 past due which not considered to be impaired as thevalue of related security over residential property is in excess of the loan due. It is not practicable todetermine the fair value of all collateral as at the balance date due to the variety of assets andcondition

Loans with repayments past due but not impaired are in arrears as follows:

Loans Members 1-3 Mths 3-6 Mths 6-12 Mths > 1 Year Total$’000 $’000 $’000 $’000 $’000

2017Mortgage secured 1,169 589 1,480 466 3,704Personal loans - - - - -Revolving Credit andCredit Card Facilities - - - - -

Total 1,169 589 1,480 466 3,704

2016Mortgage secured 2,173 - 723 - 2,896Personal loans - - - - -Revolving Credit andCredit Card Facilities - - - - -

Total 2,173 - 723 - 2,896

g. Key assumptions in determining the provision for impairment

In the course of the preparation of the annual report SCU has determined the likely impairment losson loans which have not maintained the loan repayments in accordance with the loan contract, orwhere there is other evidence of potential impairment such as industrial restructuring, job losses oreconomic circumstances. In identifying the impairment likely from these events SCU is required toestimate the potential impairment using the length of time the loan is in arrears and the historicallosses arising in past years. Given the relatively small number of impaired loans, the circumstancesmay vary for each loan over time resulting in higher or lower impairment losses. An estimate isbased on the period of impairment

Period of impairment % of

Up to 30 days 031 days to 90 days 2091 days to 182 days 40183 days to 272 days 60273 days to 365 days 80Over 365 days 100

SCU 2017 AR inners FFA.qxp_A4 15/10/17 4:27 pm Page 32

Sydney Credit Union Ltd | ABN 93 087 650 726 33

scu.net.au 2017 Annual Report

2017 2016$’000 $’000

9. Available for Sale InvestmentsShares in Unlisted companies – at cost– Cuscal Limited (a) 1,875 1,875– Shared Service Partners Pty Ltd 20 20– TransAction Solutions Pty Limited (b) 258 258Total Value of investments 2,153 2,153

Less Provisions for impairment– TransAction Solutions Pty Limited (b) (254) (254)TOTAL INVESTMENTS net of provision 1,899 1,899

Disclosures on Shares held at cost

a. Cuscal Limited

The shareholding in Cuscal is measured at cost as its fair value could not be measured reliably. Thiscompany supplies services to SCU organisations. These shares are held to enable SCU to receiveessential banking services – refer to Note 32. The shares are able to be traded.