Embed Size (px)

Citation preview

Welcome to the team! We at Beacon Payments strive to provide the best service in the industry to our agents as well as our merchants. We’ve been recognized as the number one organization in the electronic transaction industry. It is extremely important to our management team to hold ourselves to a higher standard than our competitors through continued training and support of everyone from our newest agent to our most seasoned executive. Our goal is to help our agents achieve their goals by providing them with a complete bag of tools necessary to become successful. In the following pages you will find explanations of wholesale cost, our rate structure, equipment setup procedures, the entire sales process, and even some basic sales training for those of you who need it. Do not be afraid to ask questions, in fact, we encourage you to do so. Your mentor has experience selling merchant services in the field and will be an incredible source of information for you. We will never ask you to do something we’ve never done, and we are all success stories. You have the opportunity to work your way into management through diligence, willingness to learn, and hard work. Some of you are coming to us with years of industry experience, while some of you have never been in sales before. The following training material will have something for everyone. The hardest part of this business is training. Pay attention to what you are about to read, write down ALL of your questions, and don’t forget that training will never end! Be humble and approach each day with an eagerness to learn. The sales will take care of themselves! Good luck, work hard & remember: Your attitude dictates your production!

David Selenow Executive Vice President

1

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

TABLE OF CONTENTS

HOW OUR AGENTS MAKE MONEY & FAQ 3

“WHAT’S YOUR RATE?” 7

EXPLANATION OF WHOLESALE COST 7

UNDERSTANDING THE RATE STRUCTURES 9

INTERCHANGE PASS-‐THRU PRICING 9

TIERED PRICING 10

THE DURBIN AMENDMENT 11

SALES PROCESS 13

SALES PITCH & SAMPLE SCRIPT 14

COMMON OBJECTIONS & REBUTTALS 20

UNDERWRITING POLICIES & PROCEDURES 22

SAMPLE APPLICATION (MPA) 26

MERCHANT PROCESSING APPLICATION & AGREEMENT 33

TERMS & DEFINITIONS 33

EQUIPMENT/TERMINAL OPTIONS 35

$99 DEPOSIT TERMINAL PROGRAM 35

REPROGRAMMING EXISTING EQUIPMENT 35

EQUIPMENT SALES/PRICING 36

REPROGRAMMING PROCEDURE 37

VALUE-‐ADDED SERVICES 39

SALES 101 42

2

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

HOW OUR AGENTS MAKE MONEY Agents earn commission on the array of products and services Beacon Payments offers. The end goal is to generate a large residual income which will be paid to you for as long as your accounts continue to process with us.

Our mutual, primary goal is to build your portfolio of clients as fast and efficiently as possible. The most successful agents in this industry are cold calling new businesses at first, then working their portfolio of clients for referrals. It is also a good idea to find alternate methods of marketing, such as social media, business networking groups, internet leads or referral partners like book keeping companies or banks.

In addition to credit card processing services, our agents earn commission on check processing services cash advance programs, gift and loyalty services, as well as POS (point of sale) sales.

FREQUENTLY ASKED QUESTIONS

• How do I get my leads?

The most successful Beacon Payments agents are calling on merchants face to face. You are not restricted to face to face cold calling. Phone and internet leads, networking events and social media are also a great way to generate additional business.

• What materials do I need?

All you need is a folder, a pen, a few applications, and some fliers. The Beacon Payments Merchant Letter is usually the best marketing piece to start with because it explains how we price our accounts, and how it benefits the merchant. You’ll have a few options of fliers to choose from. Use what works best for you.

• How willing are clients to give their merchant statement?

It all depends on your approach, if you treat the information as guarded and sacred, they will do the same. If you treat it as simply a utility bill that has the info we need for a quote, they will have no reservations volunteering the statement. Don’t make it a big deal and neither will they. 1 out of every 100 merchants will refuse to give you a statement. Some suggestions of what to say are

• How do I track my accounts?

Once you sign your first deal we will set you up with an online tool called Portfolio Manager. You will be able to see all of your account’s daily activity, monthly statements, when the merchant last closed a batch, and some other vital information. You’ll also have data on your total portfolio, such as total volume of the aggregate of your accounts.

3

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

• When do I get paid?

All new account bonuses APPROVED by Wednesday night at 11:59 pm will be released by Beacon Payments on Thursday afternoon. Most banks post the funds to your account on Friday. Anything approved beginning Thursday morning will roll over to the following week’s pay. Monthly bonuses and residual payments are made the first full week of each month – again, payments are initiated each Thursday.

• Do you provide business cards?

Beacon Payments will provide all of your business cards after your first deal is approved and setup. Once your first merchant has processed a transaction, just email your manager the information you would like to appear on your business card. Generally it includes phone, fax, email, and sometimes address. We normally call our agents ‘Regional Account Executive’, but if you want something else just run it by us. It takes at least 2 weeks for the first order to be delivered. We will provide you with a blank template if you want to print a few hundred just to get you by.

• Where do I find marketing materials?

All marketing materials are available on the Beacon Payments website. Login to the agent portal and you’ll be able to download everything you need. There will be a place to put your name and phone number on our marketing materials, which most new agents take advantage of while they’re waiting for their business cards.

• Who reprograms the equipment? You are responsible for making sure your merchants are setup. It is ok to have your merchants setup their own equipment, but there are at least three good reasons to do this yourself.

1.) You earn a commission on each transaction. The sooner you set up the account, the sooner you are making money. Sometimes it takes merchants weeks to find time to perform the simplest tasks.

2.) Showing up to do the reprogram gives you the opportunity to show you are providing great service and build a stronger relationship with your merchants. The more often they see you, the more comfortable they will be with you, and the less likely they will be to switch away from you without giving you a chance to keep their business.

3.) You can pump your merchants for referrals after each time you do something for them.

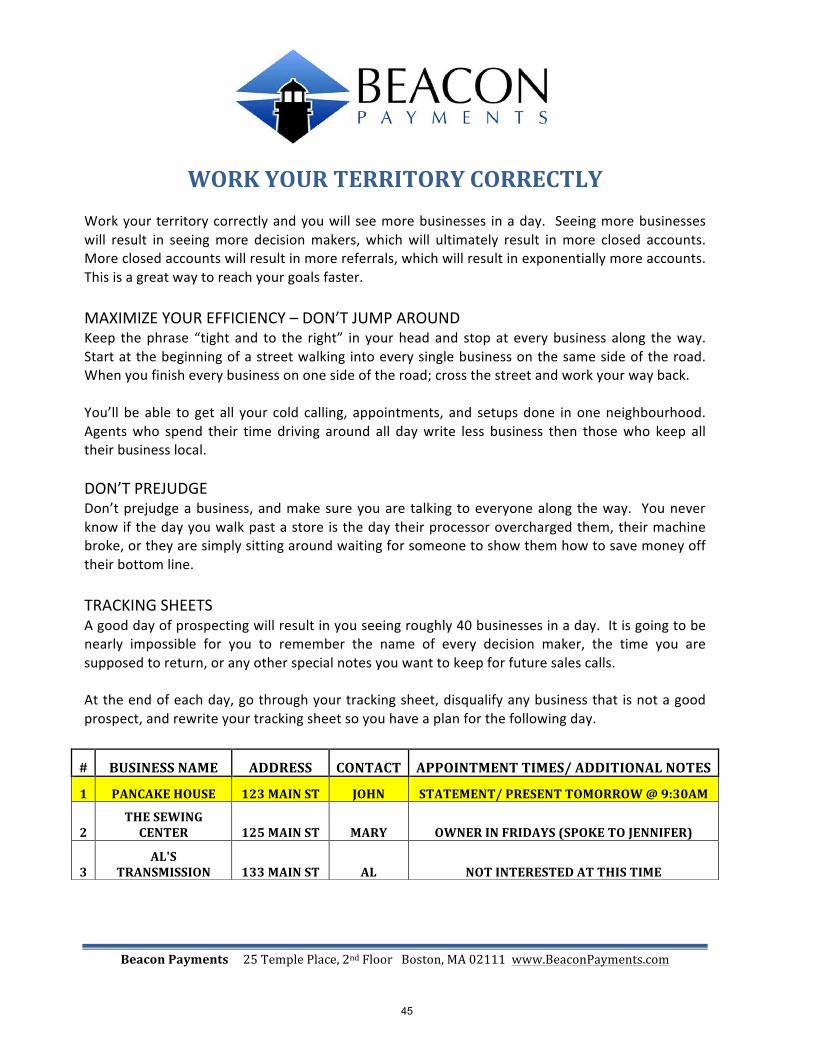

• How many businesses should I see each day? 40 a day to start. You’re going to make mistakes. It takes a little while to get good at signing up new merchant accounts. As you learn and grow, you’ll be able to see 30 a day; within 6 months you’ll only need to see 20 a day, and then strictly work referrals so you don’t need to cold call anymore. It may sound like a lot of businesses in one day, but if a business owner isn’t present it will only take you a minute or two to get in and out.

4

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

• Can I bring on sub agents?

Definitely. Part of the career path with Beacon Payments includes hiring sub agents. In order to be able to properly manage a team you must first build a book of business so you know the basics of the industry. Agents are required to write at least 25 new accounts before we will provide the tools to become a manager. We prefer our agents write 50 deals with us before they actively begin recruiting. When you bring on subagents you will be responsible for teaching and training them, as well as supporting them. You will be the first line of defence when they have a question, so it is a good idea to learn the industry inside and out before bringing people on. Agents can be referred to Beacon Payments for a referral bonus of up to $1,000.

• Where do I start? Who do I start with? The best place to start prospecting is with people you know or frequently do business with. These people often know who you are, and value your business. Try your dentist, auto repair shop, dry cleaner, restaurants, and salon/barber shop. Let them know you appreciate what they offer and want to help them out by lowering their overhead. Whether they sign with you or not, be sure to ask them who they know that may also benefit from saving money on their processing fees. Once you’ve signed one business, work the entire neighbourhood telling everyone you are currently working with a respected business owner on their street. Use your existing merchants as leverage to get others to follow.

• What do I do next? Read this manual in its entirety organizing all of your questions as you go. Contact your manager for a follow up training call and get all of your questions answered. After you’re out of questions it’s time to start prospecting for your first account. Remember your career cannot start indoors. Give yourself a kick in the butt and get out there. Make sure you have plenty of Merchant Letters and applications. You might feel like you’re not ready, but after reading this manual, and chatting with your manager you will likely know more than almost everyone you talk to. If you get a question from a merchant, and you don’t know the answer you should contact us. Your merchants will appreciate you taking the time for find out the correct answer rather than making one up. If your manager doesn’t answer, call the office and dial extension 3 for agent support. Anyone who answers the phone can help you.

5

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

“WHAT IS YOUR RATE?” The most frequently asked question we get is “what is your rate?” The answer is not as simple as it may seem. All credit card processing companies purchase a wholesale rate, mark it up, and sell it to merchants at a higher rate to earn profit on each transaction. The wholesale rate is the same for all processors. Wholesale rates start as low as 0.05%, and go as high as 3.25%. With that information in mind, it is impossible for any processor to offer a single rate. Commonly we’ll hear merchants tell us “I am paying 1.70%.” To which we would respond, “Some transactions cost us 2.20% at wholesale, some 3.00%. There is no way your company is charging 1.70% for something that costs 2.20%. There are other rates and fees you are paying somewhere on your statement.” Every time a credit or debit card is swiped in the US there are fees charged by three different entities; WHOLESALE INTERCHANGE, CARD ASSOCIATION & PROCESSOR FEES

WHOLESALE INTERCHANGE Credit card issuers (mostly banks) charge a fee each time a merchant accepts one of their cards for payment. The term “Interchange” can be simply interpreted as the cost an issuing bank charges when a merchant accepts one of the cards they’ve issued. All Interchange fees are paid to the issuing bank, and not shared with the major Card Associations (Visa, MasterCard, Discover), nor are they shared with the ISO/sales office servicing the account (Beacon Payments). Interchange fees will generally cost a merchant between 0.05% -‐ 3.25% plus a flat transaction fee. As of October 2011, some common Interchange fees are as follows: Visa Check Card 0.05% + $0.22 MasterCard Check Card 0.05% + $0.22 Visa Credit Card 1.54% + $0.10 MasterCard Credit Card 1.58% + $0.10 Visa Rewards Card 1.65% + $0.10 – 1.95% + $0.10 MasterCard Rewards Card 1.73% + $0.10 – 2.05% + $0.10 Visa CPS Key Entered Credit Card 1.80% + $0.10 MasterCard Key Entered Credit Card 1.89% + $0.10 Visa Corporate Cards 2.10% + $0.10 – 2.95% + $0.10 MasterCard Corporate Cards 2.05% + $0.10 – 2.95% + $0.10 You’ll notice each type of card carries a different interchange cost. An easy way to explain why different cards carry different interchange costs is through RISK & REWARD.

6

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

RISK A merchant can process the same exact credit card two different ways and the Interchange cost will be different. A swiped Visa CPS Retail card has an Interchange cost of 1.54% + $0.10. CPS retail is a regular credit card that does not earn rewards points. The same exact Visa CPS Retail Card will cost 1.80% + $0.10 when it is Key-‐Entered (manual) rather than swiped. The reason for the difference in cost is how the transaction is captured (swiped vs. manual entry). Years of data and research have shown Key-‐Entered transactions are more often fraudulent or stolen, resulting in a higher rate of charge backs than swiped transactions. Merchants pay a higher fee to accept a keyed transaction because there is a higher risk the issuing bank will take a loss on a fraudulent transaction. REWARD Banks issue credit cards which earn points every time a cardholder makes a purchase. An example of a rewards card is a major airline sponsored card where the card holder earns one air mile for each dollar spent on that card. Once the customer accrues enough miles they are rewarded with a free flight to the destination of their choice. This is a win-‐win for the card issuer and for the card holder. The card issuer is encouraging their cardholders to make purchases on a credit card rather than spending cash. The cardholder earns “free stuff” for paying for their day to day goods and services on a credit card rather than using cash. However, this isn’t the best scenario for the merchant because they pay a higher Interchange fee when accepting a rewards card, rather than a standard retail card. As mentioned above, a Visa Rewards 2 card carries an Interchange cost of 1.95% + $0.10. The only difference between a rewards 1 card and a CPS Retail card (1.54% + $0.10) is simply the rewards. In other words, the merchant is paying for those airline miles or rewards points the cardholder is accruing. Business cards cost the most (starting at 2.05% + $0.10) because there is a mix of risk and reward. There is inherent risk in issuing a card to a business because of the high rate of failure and bankruptcy. Most issuers offer high rewards on business or corporate cards because businesses generally charge more on their cards than a consumer, and issuers want to earn this kind of business.

7

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

CARD ASSOCIATION FEES Each Card Association (Visa, MasterCard, and Discover) charge fees in order operate their networks. Some of the operating costs include infrastructure (the lines and switches required to route each transaction between acquiring and issuing banks), research and development to prevent fraud, setting the rules and guidelines of acceptance, and marketing to promote the card brand. As of October 1st, 2011: Visa/MasterCard Dues & Assessments 0.11% Discover Dues & Assessments 0.10% Visa Acquirer Processing (APF) Fee $0.0195 MasterCard Name Assoc. & Brand Usage (NABU) Fee $0.0185 *Dues and Assessments are charged on the total sales volume. APF & NABU fees are charged on each settled transaction.

PROCESSOR FEES (HOW WE MAKE MONEY) Interchange Fees, Dues and Assessments, NABU and APF fees are charged to Beacon Payments by the Card Associations, and in turn passed through to the client at cost with no markup. If we were to sell to merchants at these wholesale costs we would not make any money; we would actually lose money because we have overhead and other costs in addition to wholesale. Some examples of additional costs are; printing and mailing statements, the 24/7/365 Help Desk based in Omaha, the cost of each phone call/authorization, paying our support staff. Processing Fees are paid to the ISO (Independent Sales Office) supporting the account. This means every time a merchant swipes a card there is a profit made. Every month that merchant works with Beacon Payments this profit is shared with the agent who signed the account. This is where Beacon Payments and its agents generate their residuals!

Agents earn commission(s) based on an array of products and services in this business. The end goal is to generate a large residual income which will be paid to you whether you continue to work, or take a few months/years off.

Our mutual, primary goal is to build your portfolio of clients as fast and efficiently as possible. The most successful agents in this industry are cold calling new businesses at first, then working their existing portfolio of clients for referrals.

In addition to credit card processing services, our agents earn commissions on check processing/conversion services, cash advance programs, gift and loyalty card printing and processing services, as well as POS (point of sale) sales.

8

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

UNDERSTANDING THE RATE STRUCTURES There are two rate structures commonly offered to merchants; INTERCHANGE PASS-‐THRU PRICING & TIERED PRICING INTERCHANGE PASS-‐THRU PRICING 99.99% of the accounts we write at Beacon Payments are on a pricing structure called Interchange Pass-‐Through. It is the most cost effective and efficient way to process credit cards. In addition to the wholesale costs (Interchange, Dues and Assessments, NABU and APF) we add a markup to make a profit on each transaction, generating a residual stream. In the following example we are marking up the wholesale rate 0.20% and $0.10 per transaction. We pass through wholesale and add 0.20% plus $0.10 regardless of the wholesale cost. *The 0.20% markup is commonly referred to as the Discount Fee If a merchant accepts a Visa Rewards 1 card, they will pay:

1.65% + $0.10 Interchange Fee +0.11% + $0.0195 Dues and Assessments + APF fee +0.20% + $0.10 Discount fee + Transaction fee 1.96% + $0.2195 Total

The same formula would be used if the merchant key entered a CPS retail card. The only difference would be substituting the 1.80% + $0.10 interchange fee associated with a key entered CPS card. After adding Interchange, Dues and Assessments, APF Fees, the Discount fee of 0.20% and the transaction fee of $0.10 the total fee paid by the merchant would be 2.11% + $0.2195.

1.80% + $0.10 Interchange Fee +0.11% + $0.0195 Dues and Assessments + APF fee +0.20% + $0.10 Discount fee + Transaction fee 2.11% + $0.2195 Total

*Ask your Agent Development Leader to further clarify this for you if you need further explanation. The variable in this pricing structure is the Interchange Fee. It will change with the type of card the merchant accepts. Dues and Assessments, APF, the discount fee and the authorization fee will remain constant when calculating the cost of accepting each type of card. The average Beacon Payments merchant is marked up 0.35% and $0.10 over cost. Once you have mastered the sales, we will teach you how to price your own accounts to make sure you are saving your merchants money, while still making enough to put in your pocket. It is a good idea to try to write all your accounts at 0.50% + $0.10 above cost, and negotiate down if you need to.

9

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

TIERED PRICING The most common rate structure we see is not Interchange Pass-‐through. It is called tiered pricing. From the explanation of wholesale above, we already know there are hundreds of Interchange categories. On the Interchange pass through rate structure the merchant will pay hundreds of rates. On a 4-‐tier rate structure the merchant will pay four rates. This rate structure drops hundreds of Interchange categories into one of the four tiers listed below. Also included is an example of the average rates we are seeing on our competitor’s statements: CHECKCARD RATE* 1.49% + $0.25 (Includes any card linked to a checking account) QUALIFIED RATE 1.69% + $0.25 (Includes non rewards credit cards) MID-‐QUALIFIED RATE 2.50% + $0.25 (Includes all rewards cards and keyed transactions) NON-‐QUALIFIED RATE 3.25% + $0.25 (Includes all business cards and foreign bank cards) * 3-‐tier rate structures combine the Checkcard and Qualified tiers under a single Qualified rate Again, we’ve noted above that the cost of wholesale is the same to the processor regardless of what rate structure the merchant has. CHECKCARD The two most common wholesale Interchange categories that fall into the Checkcard rate are Visa CPS Retail Debit -‐ 0.05% + $0.22 and MasterCard Merit III – 0.05% + $0.22. A merchant paying 1.49% + $0.25 is paying 1.44% + $0.03 over cost. This means HUGE profits for their processor and not a good deal for the merchant. QUALIFIED The Qualified rate is a teaser rate. Most consumer cards used in the United States are either Check Cards or Rewards cards. There are not many card holders carrying non-‐rewards credit cards. The Interchange rates for cards that fall into this category are 1.54% + $0.10 for Visa CPS Retail, and 1.58% + $0.10 MasterCard Merit III. At a Qualified Rate of 1.69% there are only a few basis points in profit here for Visa and no profit at all on MasterCard when you add 0.11% for dues and assessments. Many processors pitch 1.69% to new merchants. They do not teach their agents about any other rates or fees, so the agent and the merchant think they are going to get 1.69% on all transactions. They are not disclosing there are Mid-‐Qualified and nonqualified rates or surcharges.

10

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

MID-‐QUALIFIED The Mid-‐Qualified rate includes transactions costing between 1.65%+ $0.10 and 2.05% + $0.10. Swiped rewards cards between 1.65% + $0.10 and 1.95% + $0.10, and Key-‐entered transactions carrying an Interchange cost between 1.80% + $0.10 and 2.05% + $0.10. In the example above, our competitor’s Mid-‐Qualified rate of 2.50% + $0.25 remains constant whether the merchant accepts a card with an Interchange cost of 1.65% + $0.10 or a card with an Interchange cost of 2.05% + $0.10. A merchant paying 2.50% on a Visa Rewards I card with a cost of 1.65% is paying a markup of 0.85%. The same merchant paying 2.50% on a Key-‐Entered MasterCard Enhanced card with an Interchange cost of 2.05% is paying a markup of 0.45%. The markup of 0.85% is not a good deal for the merchant. The markup of 0.45% is fair. This means the merchant is paying between 0.45% and 0.85% on cards in this category. NON-‐QUALIFIED The Interchange rates in the Non Qualified category will range from 2.10% to 3.25%, with most cards falling between 2.20% and 2.65%. At a Non-‐Qualified rate of 3.50%, the merchant is paying a markup between 0.25% and 1.40%. The reason an interchange pass through pricing structure is better for the merchant is because the markup is low and fixed regardless of the type of card they swipe. On a tiered rate structure, the markup varies, and almost always costs more.

11

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

THE DURBIN AMENDMENT WHAT IS THE DURBIN AMENDMENT? In July 2011, the Federal Reserve was required by Congress to rule on a reduced Interchange fee banks are allowed to charge when a merchant accepts one of their debit cards. Prior to October 1st, 2011 the average Interchange cost banks were charging was $0.44 per transaction. The Federal Reserve ruled that the banks can only charge 0.05% + $0.22 per transaction. This brings the average down to $0.24 per transaction. This is nearly a 50% reduction in the average fee.

HOW THIS NEW RULE AFFECTS SMALL & MEDIUM-‐SIZED MERCHANTS: Merchants processing on an Interchange Plus rate structure will automatically see a reduction in their fees associated with debit cards. Almost all of Beacon Payments’ clients are currently on the Interchange Plus pricing structure. Businesses on a tiered pricing structure will not automatically receive this price reduction. The wholesale cost incurred by the processor goes down does not mean they will automatically lower your fees.

EXAMPLE: BEACON PAYMENTS vs. 3-‐TIERED PRICING (1.59% and $0.25) TIERED RATE EXAMPLE TICKET SIZE: $100.00

COST 1.59% + $0.25 D&A 0.00% + $0.00 FEES 0.00% + $0.00 TOTAL 1.59% + $0.25

COST $1.84

I/C PLUS RATE EXAMPLE TICKET SIZE: $100.00

COST 0.05% + $0.22 D&A 0.11% + $0.0195 FEES 0.40% + $0.10 TOTAL 0.51% + $0.3395

COST $0.85 DIFFERENCE -‐$0.99

A merchant processing at wholesale plus 0.40% and $0.10 per transaction will save $0.99 PER TRANSACTION over a merchant on a tiered rate. In order to benefit from this government mandated fee reduction the merchant MUST be on an Interchange plus Pricing structure. This creates a HUGE selling point vs. Tiered processors.

12

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

SALES PROCESS The sales process in this business is as follows:

1.) Build a relationship with the prospective merchant 2.) Let the merchant know you have been able to save their neighbours 10%-‐30% off their

processing fees. 3.) Get a copy of their most recent processing statement. Fax or email it to the office so we

can prepare a cost analysis and send it back to you. 4.) Present the benefits of switching to Beacon Payments including the cost savings. 5.) Close the account, and fill out the Merchant Processing Application and Agreement. 6.) Fax or email the application to the office to be reviewed by underwriting. Underwriting

will approve, pend or decline every account within 48 hours of submission. 99% of accounts get approved.

7.) Once approved: reprogram or install new equipment. 8.) Ask for referrals.

It is our long term goal to teach each one of you how to analyze a statement, and prepare a cost comparison. However, it is helpful for most agents to submit statements for analysis while they are learning the industry. Some of our most seasoned agents, with years of experience, still send statements to us for analysis so they can focus on selling. Closing a deal on the first visit will happen from time to time, but, often the sale is a multi-‐visit process. Below is a fairly typical sales cycle, and what you should expect with most of your merchants. STOP 1 Introduction, Questioning, Presentation, Close for the statement – Let the merchant know who you are and what you intend to accomplish. Ask good questions, present the company, and close for the statement. Once you acquire the merchant’s processing statement let them know you are extremely confident you can help them get better service -‐ we’ve been recognized as the number one service organization in this industry, and lower pricing -‐ we can match or beat any rate every time. Tell the merchant you will run numbers for them and return with a nice, neat, easy to understand proposal. At this point you should schedule a second appointment where you will return their statement and a proposal, as well as show them how wholesale pricing will help them save money. Keep in mind your intention will be to close the deal on the second visit. In order to accomplish this, you’ll want to make sure you understand all of their needs and write down any questions to which you don’t know the answers. It’s also a good idea to ask if anyone else will need to be present to make a decision.

13

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

If the merchant does not have a statement to give you, schedule a time to go back and pick it up – make sure you show up when you say you will. Some merchants will tell you to come back just to see if you show up, but more importantly – to see if you show up on time. If the merchant does not have a statement to give you when you show up for your scheduled follow up visit, offer to contact their current processor and have them fax over a copy of their most recent statement. Simply call the processor and ask them to fax it over to you the merchant or to you directly. STOP 2 After receiving the prepared analysis we must present the savings and close the deal -‐ During the presentation briefly explain what you did for them -‐ prepared a cost analysis based on the current rates on their statement. After reading the presentation training material below, you will know exactly how to do this. Close the deal. Two stop closes are ideal for efficiency, but many times the merchant needs to check with someone else or wants to think about it. Stay on top of your merchants without annoying them. Suggest a day when you will follow up, and make sure the merchant agrees. The biggest compliment someone can pay you is calling you persistent.

SALES PITCH AND SAMPLE SCRIPT

INTRODUCTION A strong introduction is vital to every step of the pitch, including overturning objections and the close. The introduction can make or break your chances of signing a new account. The first step to the introduction is breaking the ice. If you can make a client laugh, you have already built their trust. Tell them a joke, or find another way to help them see you as a human being rather than a sales person/robot saying the same thing to the 50 sales people who tried to sell them something before you. Here are a few examples of ice breakers:

• Hey there! How are you today? Unbelievable game last night, huh? Should’ve put my money elsewhere!

• Hello, how is everything going today? Crazy weather out there, huh? Didn’t know I’d need a raft this morning.

• Hey! How’s it going? Looks great in here. You have an amazing spot! • Happy Monday, Valentine’s day, Halloween, Martin Luther King Day, Presidents’ day, etc!

(HUGE smile – wait for prospect to smile back)

14

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

Next, tell them your name and why you are there. Keep it short and simple. Anyway, my name is ________ and I am the new account executive for Beacon Payments here in _________ (name of city/town/neighbourhood).

• The reason I’m here is Visa and MasterCard have had some significant rate reductions over the past few months. My company sent me out here today to find out what kind of rates you’re being charged to see what we can do to help you out.

• I handle the credit card processing for a lot of merchants in the area. While I was out

visiting with them, my company asked me to stop here and introduce myself to whoever handles that for your company. That’s you, right? Great! What’s your name? It is important you remember the merchant’s name. Call the merchant by their name a few times throughout your visit so they know you have listened to them.

If the customer says they are not the person who handles that/the decision maker, follow up with Oh, what’s the name of the person who takes care of that stuff for you guys? What day is s/he usually in? Is it better to catch her/him during the morning or the afternoon? You’ll want to build a bit of a relationship. Some small talk is ok, but it is better to find some way to relate to your prospect. You can read more about building relationships in the “Sales 101” section of this training manual. Some agents find it useful to not even mention the reason they are visiting. They build and build and build a relationship until the merchant finally asks what they do for work. It is a technique that can work and a good exercise for those you who are really working on your relationship building skills. QUESTIONING/SHORT STORY Now that you have made a positive impression on your prospect you may begin to build your product into the conversation. Your ultimate goal is to present your product, close for the statement and then the application. Gathering information on the needs of your prospect will give you ammunition to fire at them during your presentation. By the time they get to their buying decision it will be easy for them to say ‘yes’ if you have addressed all of their concerns.

15

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

The best way to learn about their needs is to ask GREAT questions. Open ended questions are always better than questions eliciting a yes or no response. Get them talking, and make sure you listen to their responses while making mental notes. All sales people were created with two ears and one mouth for a reason. Make sure you listen twice as much as you talk. You build trust by listening to their concerns and responding properly. Less is more. Great sales people are able to decipher what a merchant wants to hear, rather than telling them what they think the merchant needs to hear. The only way to figure out what a merchant wants to hear is by truly listening to what is important to them. Now’s the time to get the merchant talking about the product. Identify the business owner’s hot spots. Keep everything topical and you will be able give your prospects solutions to any problem they have. Here are some examples of good questions to ask:

• Who are you currently working with? • When was the last time you had a full rate review? • What are the rates your current company is charging? (If a merchant says 1.69%, you’ll

need to follow up with – that’s a great rate for qualified cards, but what is the total effective rate you are being charged when you divide total fees by total sales? –or-‐ what are your mid and non qualified surcharges?)

• How many points above Interchange are you processing at? (confusion tactic – most merchants don’t know about Interchange)

• What type of terminal are you using? Does it ever give you any trouble? Do you like it or want a new one?

• Is there anything you wish your company would do for you? • What are some things about your company you really like? • Do you have a local rep? When was the last time you saw your representative? • Are there any other services you can use? Perhaps a gift card program or Check Guarantee

services? • When was the last time you had a rate review? Rates change every April and October, so

it is really important you stay on top of it if you’re not on Interchange Plus pricing. • There have been a lot of changes with visa/mc in the last year, are you sure they are

getting you the best rates out there? • Are you aware the rules have changed so you can set a minimum amount a customer can

use their card for (i.e. accepting cards for $10 or more only)?

16

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

• Visa and MasterCard recently made some special pricing available to your industry, and

only merchants on Interchange Plus pricing are getting these special rates. Have you seen this discount on your statement?

• Do you understand how to read your statement? They can be pretty confusing. Use strong, concise questioning to gather information. Create needs with your questions. You can also use good questions to create doubt or confusion regarding that the merchant has the best possible rate and service. Remember to listen! CLOSING FOR THE STATEMENT Once you have asked the proper questions, you need to respond by firing the ammunition you have been collecting as you listened. The “close” for each merchant will be a little different but, as long as you have listened twice as much as you have spoken you should have no problem addressing each issue the merchant discussed. After addressing all of the merchants needs, you will want to close for a recent processing statement. A good statement closing line is:

• Grab a copy of your statement and let’s take a look at it together. I’ll show you how wholesale pricing can help you.

• Visa and MasterCard have made some discounts available specifically for your type of business (auto repair, restaurants, etc.). Let’s take a look at your statement and make sure your current company is passing these discounts on to you.

• Some of your neighbours have been grossly overpaying for processing fees. Let’s take a look to make sure you’re not in the same boat.

• The next step is for me to prepare an analysis based on your current fees. Grab a cop y of your most recent statement and we’ll put some numbers together for you.

It is important to take control during the entire conversation, but especially during the close. Notice we did not ask the merchant to retrieve the statement, rather told them to go get it. This is a powerful statement to make, and might feel uncomfortable at first. You will achieve better results by taking control and telling the merchant how this process works, rather than asking them to comply. WHAT IF THE MERCHANT WON’T GIVE ME THEIR STATEMENT? Good question. This comes up all the time. Some merchants will tell you they won’t give you their statement, but want to know your rate. We’ve already covered the answer to the question “what is your rate?” in the opening of this manual -‐ it’s just not quite that simple. There are hundreds of rates and hundreds of ways a competing processor could be overcharging the merchant.

17

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

• If your car is sputtering, and you take it to the mechanic to get a price on the repair, the

mechanic is going to need to take a look at the car. He could give you a blind quote, but it likely wouldn’t be accurate. The same is true for your merchant services. There are hundreds of card types that carry different costs. I don’t know what kind of cards you’re taking without seeing a statement, so I could tell you the price is 1.54%, but it likely won’t be accurate.

• Your statement has all of the categories we need to properly assess a quote. Believe me,

there are a lot of companies that will quote off the cuff, or come in here and tell you what you want to hear and that the rate is 1.50%. We’re not one of those companies. I want to give you an accurate assessment of what you’re going to pay before you come over to us.

Pulling statements is 80% of the sale. Your manager will work with you to put together a competitive cost analysis to present to the merchant. PRESENTATION OF COST ANALYSIS At this point we are going to start the presentation process and close all over again. Only now we have even more ammunition with a statement and a proposal detailing the rate the merchant will pay with us and the amount of savings offered. AFTER RECEIVING A QUOTE FROM YOUR MANAGER The Presentation of a quote should be a concise, quick statement giving the prospect information regarding the savings. KEEP IT SIMPLE, and be direct. Show the merchant the amount and percentage of savings. Answer any questions the merchant has, and transition into a closing line statement. A few examples would be:

• Okay Mr./Mrs. Customer, what we did was run an exact cost comparison against your current company. As you can see, you are paying X with them, and it would have been Y with us. We are saving you money in almost every category. Bottom line is you would have saved Z if you processed the exact same month with us as you did with them.

• As you know we did an analysis on your statement, and as you can see the savings is significant. This is a company we need to get you away from to put you on the right processing system.

• We ran an analysis on your account, and these are the savings we’ve come up with. I’ve learned from talking to hundreds of successful business owners that every little bit counts. If we can knock off a few dollars here, and you can save in a few other areas, that’s just more money you can plug right back into your business or put in your pocket.

18

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

There may be a few categories or rates where we charge more than their company. It is important to address this rather than brushing it under the table. Do it by letting the merchant know we might be higher in a category or two, but we are saving them money in most categories for an overall lower cost. Then point them to the bottom of the proposal and show them how much money they’ll save. CLOSE FOR THE APPLICATION

• All we have to do to get this started is fill out some paperwork and we’ll get you up and running. (Put your pen on the application; write your name at the top) What is the legal name of your company?

If the merchant does not stop you, continue to fill out the application. If they stop you, and have more questions, stop what you are doing (put your pen down), fully address the question or questions, and go back to filling out the paperwork. Remember: S.A.C. – STOP what you are doing. ANSWER their question. CLOSE again! Here are some alternate closing phrases that will assist you in closing the account:

• Okay, let’s quickly go through some paperwork and wrap this up. • All we need to do now is fill out some paperwork and we’ll get you up and running by

Tuesday or Wednesday. • Here is what happens next: we fill out some paperwork together, underwriting will

review your account, and once it is approved I’ll give you a call to setup a time to come back and take care of your machine for you.

Putting the pen on the paper and starting to write will give the merchant the opportunity to object to what you are doing, or allow you to continue the sales process. Do not ask, “So do you want to do this?” You are allowing the merchant to say “no, or not yet.” Closing a deal can and should be the easiest part of the process. After building a GREAT relationship during the introduction, asking GREAT questions, and addressing all the merchant’s issues during the presentation the deal should be closed. Always assume the close. A doctor will examine a patient, diagnose the illness and prescribe a cure. You should be doing the same. Examine the merchant, diagnose their problems and prescribe a cure. Many sales people think the close is the hardest part of the sale. In actuality this is the easiest part of the sale if you have examined and diagnosed properly.

19

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

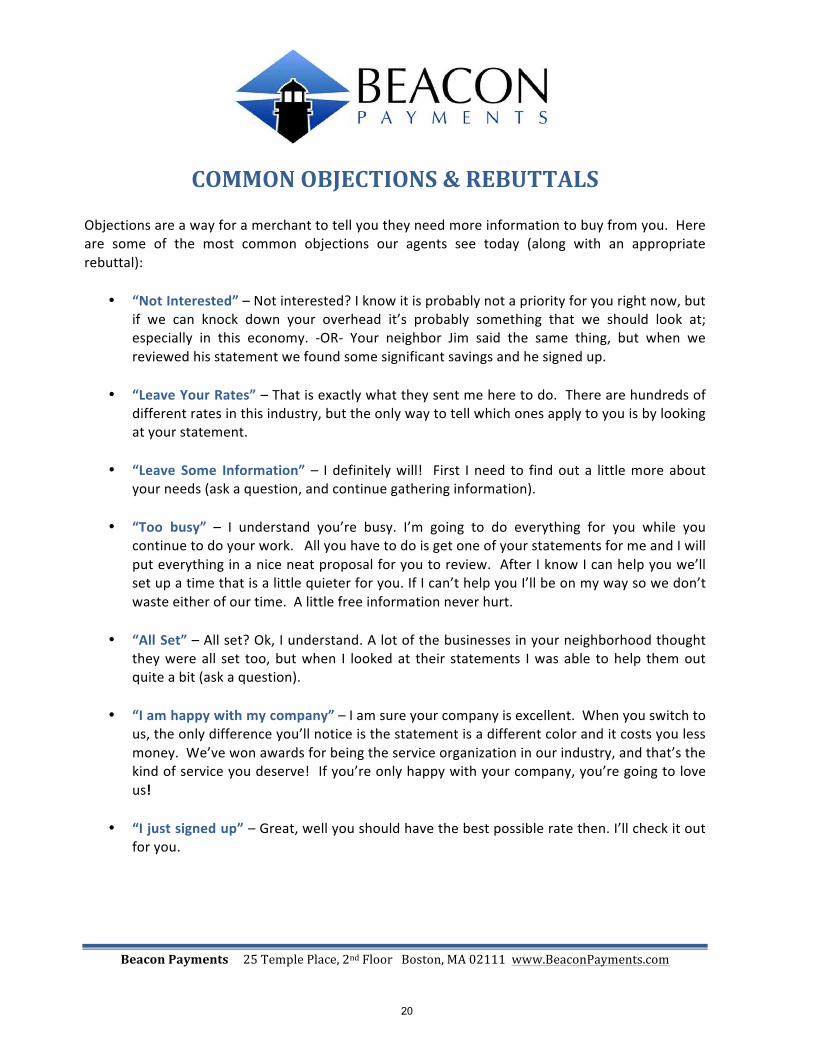

COMMON OBJECTIONS & REBUTTALS Objections are a way for a merchant to tell you they need more information to buy from you. Here are some of the most common objections our agents see today (along with an appropriate rebuttal):

• “Not Interested” – Not interested? I know it is probably not a priority for you right now, but if we can knock down your overhead it’s probably something that we should look at; especially in this economy. -‐OR-‐ Your neighbor Jim said the same thing, but when we reviewed his statement we found some significant savings and he signed up.

• “Leave Your Rates” – That is exactly what they sent me here to do. There are hundreds of

different rates in this industry, but the only way to tell which ones apply to you is by looking at your statement.

• “Leave Some Information” – I definitely will! First I need to find out a little more about

your needs (ask a question, and continue gathering information). • “Too busy” – I understand you’re busy. I’m going to do everything for you while you

continue to do your work. All you have to do is get one of your statements for me and I will put everything in a nice neat proposal for you to review. After I know I can help you we’ll set up a time that is a little quieter for you. If I can’t help you I’ll be on my way so we don’t waste either of our time. A little free information never hurt.

• “All Set” – All set? Ok, I understand. A lot of the businesses in your neighborhood thought

they were all set too, but when I looked at their statements I was able to help them out quite a bit (ask a question).

• “I am happy with my company” – I am sure your company is excellent. When you switch to

us, the only difference you’ll notice is the statement is a different color and it costs you less money. We’ve won awards for being the service organization in our industry, and that’s the kind of service you deserve! If you’re only happy with your company, you’re going to love us!

• “I just signed up” – Great, well you should have the best possible rate then. I’ll check it out

for you.

20

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

• “I am with my bank” – A lot of my clients were with their banks before I met them. Banks

are outsourcing to companies like us, so you are paying two companies for a service one can provide. Furthermore, bankers are good at banking, and we are good at credit card processing. If you called your banker and asked him how to close a batch, he would tell you to call tech support. If you called me and asked the same question I would give you the answer on the spot.

• “I’m in a contract” – That’s no problem; we have a contract buyout program most

merchants qualify for. Grab your statement and I’ll be able to tell you if you qualify!

• “I don’t want to change” – nothing really is going to change, except Jane at customer service is going to become Mary, your red statement is going to become blue, and you’re going to pay less money. I am going to take care of the whole thing for you, including the setup. Your machine will work exactly the same; your money will be deposited into your bank account within 24-‐48 hours; you will have 24/7/365 tech support in Omaha, Nebraska, where they speak 60 different languages; Think of it more of a rate reduction than a “change.”

• “Lots of reps come through here” – We are not like most companies. We’ve been able to

save a lot of your neighbor’s money by switching them to a wholesale plus rate structure. This is the same rate structure McDonald’s and Wal-‐Mart’s are using to process their cards.

A great way to overturn an objection you don’t have a prepared answer for is to Repeat, Reassure and Resume. The business owner needs to know you understand why they’re objecting to what you’re saying. Tell them you hear what they are saying, understand the problem and have a solution. Then continue pitching. Example 1: “I’m not interested” -‐ You’re not interested? I understand. Joe next door told me the same thing. I was able to help him save tons of dough, and I assure you I’m going to do the same for you! So you how do you like that terminal you’re using? Example 2: “My terminal is locked down and I can’t change” – OK, your terminal is locked down. I assure you we’ve had this same situation come up in the past and we’re able to overcome it with a little creative thinking. What is the name of the company that locked your terminal? Example: “You merchant services guys are all crooks!” – I certainly understand how you feel, and have come across many business owners who feel the same way. However, I’ve found that merchants doing business with us have a different outlook once they experience our service. When I tell you I am going to do something for you, I do it. That’s the reason we’ve been recognized as the number one credit card ISO in the entire industry!

21

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

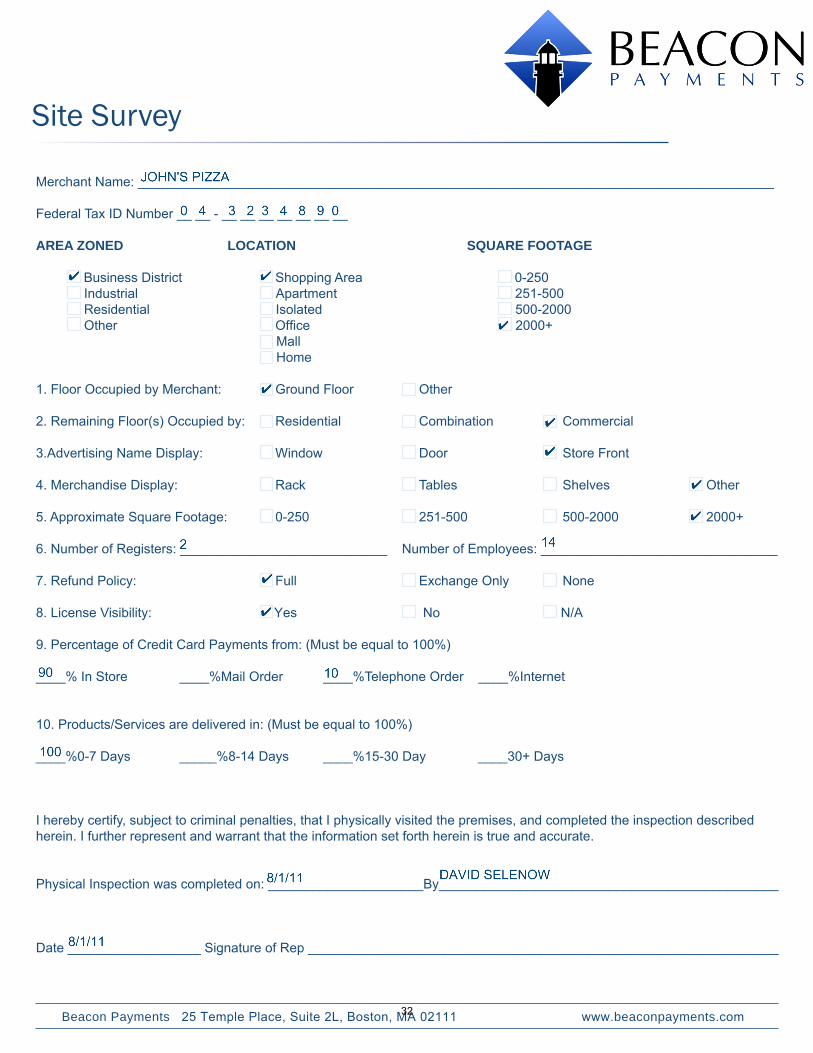

UNDERWRITING POLICIES & PROCEDURES We seek relationships that produce a fair return without incurring more than an acceptable level of risk. Our activities will be directed toward the development of qualified sub-‐merchants and merchants who are expected to provide long-‐term profitable relationships. As such the following pages list the procedures to be followed in underwriting those relationships. APPROACH TO UNDERWRITING The purpose of underwriting is to determine that the merchant’s financial condition is basically sound, that the business and its principals have satisfactory credit and/or bank card processing histories, and that there is nothing in the merchant’s background or method of doing business that would preclude the business from being a customer. It is recognized that there are varying degrees of risks associated with different types of merchants and different processing limits. Because of that, it is appropriate to apply varying levels of scrutiny to different merchants, ranging from basic due diligence for the merchant with an established low risk profile, through a thorough and detailed review for merchants deemed to present greater risks. PROHIBITED MERCHANTS Certain types of merchants carry more risk than others, or require specialized expertise to monitor merchant activity and control risk. For these reasons, certain merchant types are excluded. This list, PROHIBITED MERCHANT (DO NOT SOLICIT) LIST, is not meant to be all-‐inclusive. Other types of products may be declined due to the type of business on a case-‐by-‐case basis. RESTRICTED MERCHANTS BP recognizes that many merchant types, while posing increased risks through higher chargebacks and refunds due to the nature of the product or service provided (i.e. future service, items that are easily sold on the black market, digital content items that are easily disputed, etc) present business opportunities. The risk presented by this classification of business opportunities can be closely monitored and controlled, and therefore mitigated to present an acceptable level of risk for processing. Those on this list should be reviewed with greater scrutiny. When reviewed the required documents will be those of the next level and the chargebacks and refunds must be lower and the financial statements must be stronger. This list, see RESTRICTED MERCHANT (HIGH RISK) LIST, is not meant to be all-‐inclusive. Other types of products may be restricted due to the type of business on a case-‐by-‐case basis. These merchants will be required to be set up with a 1-‐day ACH delay and will be put on daily discount. These business types will also be required to have the Personal Guarantee signed on each application.

22

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

APPROACH TO UNDERWRITING

LEVEL 1 PROCESSING VOLUME INTERNET UP TO $50K/ MONTHLY

MOTO, KEYED, HOTEL or FUTURE DELIVERY UP TO $100K/ MONTHLY RETAIL, WIRELESS or RESTAURANT UP TO $200K/ MONTHLY

*NO ADDITIONAL DOCUMENTATION IS NEEDED UPON SUBMISSION OF THESE ACCOUNTS

LEVEL 2 PROCESSING VOLUME

INTERNET $50,001 -‐ $100,000/MONTHLY MOTO, KEYED, HOTEL or FUTURE DELIVERY $100,001 -‐ $249,999/MONTHLY

RETAIL & WIRELESS $200,001 -‐ $999,999/MONTHLY

ACCOUNTS WITH AN AVERAGE TICKET OF $1,000 -‐ 7,999 BUSINESSES THAT WOULD NORMALLY BE LEVEL 1 BUT ARE ON THE RESTRICTED LIST REQUIRED ADDITIONAL INFORMATION: * 3 MONTHS PREVIOUS PROCESSING STATEMENTS * 3 MONTHS PREVIOUS BANK STATEMENTS (IF NO BUSINESS BANK STATEMENTS, MUST PROVIDE 3 MONTHS

PERSONAL BANK STATEMENTS

LEVEL 3 PROCESSING VOLUME

INTERNET > $100,000/MONTHLY MOTO, KEYED, HOTEL or FUTURE DELIVERY > $250,000/MONTHLY

RETAIL & WIRELESS > $1,000,000/MONTHLY ACCOUNTS WITH AN AVERAGE TICKET OF $8,000 OR MORE BUSINESSES THAT WOULD NORMALLY BE LEVEL 2 BUT ARE ON THE RESTRICTED LIST REQUIRED ADDITIONAL INFORMATION: * 3 MONTHS PREVIOUS PROCESSING STATEMENTS * 3 MONTHS PREVIOUS BANK STATEMENTS (IF NO BUSINESS BANK STATEMENTS, MUST PROVIDE 3 MONTHS PERSONAL BANK STATEMENTS * 2 YEARS' BUSINESS FINANCIALS, AUDITED OR 2 YEARS' BUSINESS FINANCIALS UNAUDITED AND TAX RETURNS TO SUBSTANTIATE NUMBERS * WE WILL HAVE A SITE SURVEY CONDUCTED OF WAREHOUSE OR LOCATION WITH INVENTORY

23

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

PROHIBITED MERCHANT (DO NOT SOLICIT) LIST Age Verification Aggregators Airlines Any Product/Service/Activity Considered Illegal &/or Prohibited by MasterCard and/or Visa Auctions of any type Automobile Clubs Bailbonds Benefit Programs Buyers’ clubs/Membership clubs Check Cashing and Payment Facilitating Services Collection Agencies Currency / Commodity Exchange / Money Transfer businesses Credit Card Protection Credit Counseling, Restoration, Repair Agencies Cruise Lines Direct Marketing – Subscription Merchants – IPSP Prohibited only Discount and Other Membership Clubs Drug Paraphernalia E-‐Cash Extended Warranty Companies Foreclosure protection/guarantee/assistance Fortune Tellers Freight Forwarders Furniture – All types -‐ New Future delivery – greater than 90 days Gambling – including but not limited to:

• Lotteries • Internet Gaming • Contests • Sweepstakes • Gamers

“Get Rich Quick” schemes and seminars Golf Clubs and accessories – Online Gun Dealers -‐ online Herbal smoking blends and herbal incense Inbound Telemarketing with an Up Sell Infomercial – IPSP Prohibited only Investment Programs or Opportunities International Matchmaking or Dating

Lifetime memberships or subscriptions Loan Modifications Long Distance and Teleservices Magazines Mail order brides Marijuana Dispensaries Merchants Offering Free Gifts, Incentives or Enticements Merchants Offering Prizes, Sweepstakes or Contests as an Inducement to Purchase a Product and/or Service Mortgage Reduction Services Multilevel Marketing – New Nutraceuticals-‐ Internet w/out retail storefront location On line and/or Non-‐face-‐to-‐face Pharmacy or Pharmacy Referral and Direct Merchant Prohibited On line and/or Non-‐face-‐to-‐face Tobacco Sales Outbound Telemarketing Penny Auctions Prepaid Phone Cards, Phone Services and Cell Phones Programs on How to Apply for Low Interest Credit Cards Pseudo-‐Pharmaceuticals – including but not limited to Anti-‐aging Pills Sex Nutrients Diet Pills Quasi-‐Cash Rebate Based Business Replica goods and/or products Sexually Oriented or Pornographic Products and Services – including but not limited to:

• Audio/Videotext • Adult book/video stores • Modeling Agencies • Massage Parlors • Topless Bars/Clubs • Companion/Escort Services Dating Services

Sports Forecasting / Odds Making Ticket Agencies -‐ New Timeshare Programs Travel Agencies Travel Clubs “Up-‐Sell” Merchants Vacation Rentals Warranty Companies and Extended warranty companies

24

Beacon Payments 25 Temple Place, 2nd Floor Boston, MA 02111 www.BeaconPayments.com

RESTRICTED MERCHANT (HIGH RISK) LIST Antique / Collectible / Memorabilia Apartment Rentals Books / Periodicals / Newspapers (subscription) Cable and Other Pay TV Programs Cablegrams / Telegrams Cameras / Photographic Supplies Carpet / Rugs / Floor Coverings Charitable / Civic / Political / Religious and Other Organizations Coin Dealers, Stamp Dealers or Those Who Sell Precious Metals and or Precious Stones Computer / Computer Equipment / Peripherals / Software Computer Maintenance / Repair Services Computer Network / Information Services / Internet Service Providers / Electronic Bulletin Boards Computer Programming / Data Processing / Integrated System Design Digital Goods Direct Marketing Electrical Equipment / Parts Electronic Stores Employment Agencies Equipment Hospital / Medical / Dental Financial Services such as Investment Consulting and Stock Broker Flight Training Furniture – All types -‐ Established Future delivery – up to 90 days Gift Certificates Golf Clubs/accessories Gun Dealers (must have site survey) Hardware Equipment / Supplies Health / Beauty Spas Health Clubs / Gyms / Sports Clubs / Golf Courses / Other Sports Membership Health Insurance Providers

Heating Equipment / Supplies Home-‐based businesses -‐ New Hydroponics Import/Export of any type Information Retrieval Services Infomercial Merchants Insurance Sales / Underwriting / Premiums Internet Accounts -‐ New Internet Malls Keyed Accounts – New Merchants deemed to have poor credit Metal Service Centers and Offices Miami-‐based businesses/signers Motion Picture and Video Tape Production / Distribution MOTO Accounts -‐ New Motor Vehicle Supplies / Parts Multilevel Marketing – Established Nutraceuticals-‐ Retail Store Front Pawn Shops Petroleum and Related Products Postal Services Prepaid Legal Services Printing / Publishing Services Real Estate Agents and Brokers Sanitation / Polishing / and Specialty Cleaning Preparations Seminars – Get rich quick seminars are prohibited Subscription and/or Recurring Billing Merchant Telecommunication Equipment and Telephone Sales / Beepers / Pagers / Paging Equipment / Cell Phones Testing Labs Ticket Agencies – Established Tours Used Car and Truck Dealers Vehicle Consulting, Rental or Leasing Water Purification Systems Window Tinting

25

New Account Cover Page BUSINESS NAME:

AGENT'S NAME:

AGENT'S SIGNATURE:

EQUIPMENT OPTIONS (CIRCLE ONE): REPROGRAM -‐ $99 DEPOSIT -‐ TERMINAL PURCHASE

EQUIPMENT TYPE #1: # OF TERMINALS

EQUIPMENT TYPE #2: # OF TERMINALS

EQUIPMENT TYPE #1: # OF TERMINALS

PRICE PER TERMINAL $

EQUIPMENT TYPE #2: # OF TERMINALS

PRICE PER TERMINAL $

PIN PAD PURCHASE: VERIFONE HYPERCOM PRICE $

SHIP TO (CIRCLE ONE): MERCHANT LOCATION -‐ AGENT LOCATION -‐ OTHERIF OTHER, PROVIDE:

FILE TYPE RETAIL (NO TIPS) RESTAURANT (WITH TIPS)AMEX YES NO YES NOPIN PAD YES NO YES NOAVS/CVV2 YES NO YES NOTIP ADJUST N/A N/A YES NOSERVER ID # N/A N/A YES NO

AUTO CLOSE YES NO YES NOIF YES, TIME: IF YES, TIME:

OTHER NOTES:

PROGRAMMING INFORMATION -‐ MUST CIRCLE SOMETHING ON EVERY LINE

EQUIPMENT PURCHASE OR EQUIPMENT DEPOSIT

REPROGRAM INFORMATION

26

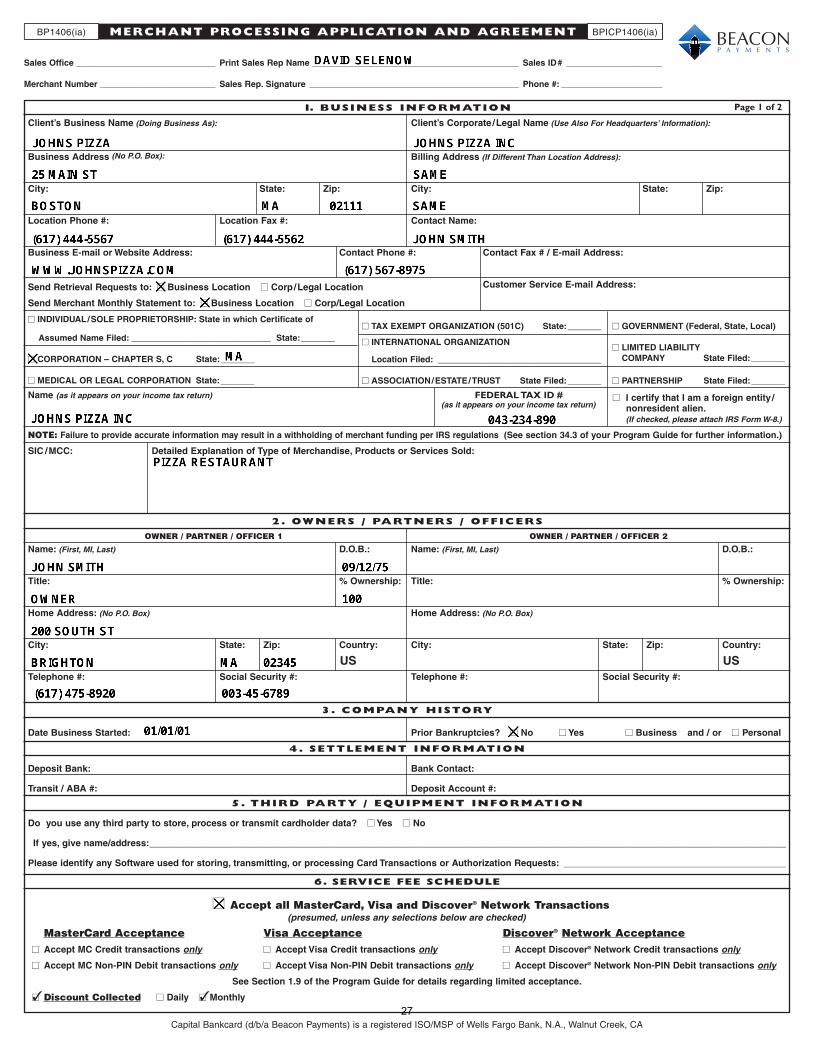

1. BUSINESS INFORMATION

Client’s Business Name (Doing Business As): Client’s Corporate/Legal Name (Use Also For Headquarters’ Information):

Business Address (No P.O. Box): Billing Address (If Different Than Location Address):

City: State: Zip: City: State: Zip:

Location Phone #: Location Fax #: Contact Name:

Business E-mail or Website Address: Contact Phone #: Contact Fax # / E-mail Address:

Send Retrieval Requests to: ■■ Business Location ■■ Corp/Legal Location Customer Service E-mail Address:

Send Merchant Monthly Statement to: ■■ Business Location ■■ Corp/Legal Location

■■ INDIVIDUAL/SOLE PROPRIETORSHIP: State in which Certificate of

Assumed Name Filed: _____________________________ State:_______

■■ CORPORATION – CHAPTER S, C State:_______

■■ MEDICAL OR LEGAL CORPORATION State:_______

2. OWNERS / PARTNERS / OFFICERS

OWNER / PARTNER / OFFICER 1 OWNER / PARTNER / OFFICER 2

Name: (First, MI, Last) D.O.B.: Name: (First, MI, Last) D.O.B.:

Title: % Ownership: Title: % Ownership:

Home Address: (No P.O. Box) Home Address: (No P.O. Box)

City: State: Zip: Country: City: State: Zip: Country:

Telephone #: Social Security #: Telephone #: Social Security #:

Name (as it appears on your income tax return) FEDERAL TAX ID # ■■ I certify that I am a foreign entity /(as it appears on your income tax return) nonresident alien.

(If checked, please attach IRS Form W-8.)

NOTE: Failure to provide accurate information may result in a withholding of merchant funding per IRS regulations (See section 34.3 of your Program Guide for further information.)

SIC /MCC: Detailed Explanation of Type of Merchan dise, Products or Services Sold:

3. COMPANY HISTORY

Date Business Started: Prior Bankruptcies? ■■ No ■■ Yes ■■ Business and / or ■■ Personal

■■ TAX EXEMPT ORGANIZATION (501C) State:_______

■■ INTERNATIONAL ORGANIZATION

Location Filed: __________________________________

■■ ASSOCIATION/ESTATE/TRUST State Filed:_______

■■ GOVERNMENT (Federal, State, Local)

■■ LIMITED LIABILITY COMPANY State Filed:_______

■■ PARTNERSHIP State Filed:_______

Page 1 of 2

4. SETTLEMENT INFORMATION

Deposit Bank: Bank Contact:

Transit / ABA #: Deposit Account #:

5. THIRD PARTY / EQUIPMENT INFORMATION

Do you use any third party to store, process or transmit cardholder data? ■■ Yes ■■ No

If yes, give name/address:___________________________________________________________________________________________________________________________

Please identify any Software used for storing, transmitting, or processing Card Transactions or Authorization Requests: ___________________________________________

Capital Bankcard (d/b/a Beacon Payments) is a registered ISO/MSP of Wells Fargo Bank, N.A., Walnut Creek, CA

6. SERVICE FEE SCHEDULE

■■ Accept all MasterCard, Visa and Discover® Network Transactions(presumed, unless any selections below are checked)

MasterCard Acceptance Visa Acceptance Discover® Network Acceptance■■ Accept MC Credit transactions only ■■ Accept Visa Credit transactions only ■■ Accept Discover® Network Credit transactions only

■■ Accept MC Non-PIN Debit transactions only ■■ Accept Visa Non-PIN Debit transactions only ■■ Accept Discover® Network Non-PIN Debit transactions only

See Section 1.9 of the Program Guide for details regarding limited acceptance.

■■✓Discount Collected ■■ Daily ■■✓Monthly

US US

MERCHANT PROCESSING APPLICATION AND AGREEMENT

Sales Office _____________________________ Print Sales Rep Name ___________________________________________ Sales ID# ____________________

Merchant Number ________________________ Sales Rep. Signature ____________________________________________ Phone #: _____________________

BPICP1406(ia)BP1406(ia)

27

8. S IGNATURE(S)

Client certifies that all information set forth in this completed Merchant Processing Application is true and correct and that Client has received a copy of the Program Guide [versionBP1406(ia)] and Confirmation Page, which is part of this Merchant Processing Application (consisting of Sections 1-8), and by this reference incorporated herein. Client further agreesthat Client will not accept more than 20% of its card transactions via mail, telephone or Internet order. However, if your Application is approved based upon contrary information stated inSection 7, Transaction Information section above, you are authorized to accept transactions in accordance with the percentages indicated in that section. Client authorizes Capital Bankcardand Wells Fargo Bank, N.A. (“Bank”) and their Affiliates to investigate the references, statements and other data contained herein and to obtain additional information from credit bureausand other lawful sources, including persons and companies names in this Merchant Processing Application. Client authorizes Capital Bankcard and BANK and their Affiliates (a) to procureinformation from any consumer reporting agency bearing his/her personal credit worthiness, credit standing, credit capacity, character, general reputation, personal characteristics, ormode of living, and (b) to contact all previous employers, personal references and educational institutions. Each of the undersigned authorizes us and our Affiliates to provide amongsteach other the information contained in this Merchant Processing Application and Agreement and any information received from all references, including banks and consumer reportingagencies. It is our policy to obtain certain information in order to verify your identity while processing your account application. If Capital Bankcard does not approve Client for a MerchantProcessing Agreement in connection with this Merchant Processing Application, Client hereby consents to the forwarding of all information contained in this Merchant Processing Appli -ca tion, as well as all other information disclosed by Client in connection with this Merchant Processing Application to Capital Bankcard, for the purpose of considering Client for a merchantprocessing account subject to the same terms, conditions and pricing contained in the Agreement. By signing below, I represent that I have read and am authorized to sign and submit this application for the above entity which agrees to be bound by the American Express® Card Accep -tance Agreement (“Agreement”), and that all information provided herein is true, complete and accurate. I authorize Capital Bankcard and American Express Travel Related ServicesCompany, Inc. (“AXP”) and AXP’s agents and Affiliates to verify the information in this application and receive and exchange information about me personally, including by requestingreports from consumer reporting agencies, and disclose such information to their agent, subcontractors, Affiliates and other parties for any purpose permitted by law. I authorize and directCapital Bankcard and AXP and AXP agents and Affiliates to inform me directly, or through the entity above, of reports about me that they have requested from consumer reporting agencies.Such information will include the name and address of the agency furnishing the report. I also authorize AXP to use the reports from consumer reporting agencies for marketing andadministrative purposes. I understand that upon AXP’s approval of the Application, the entity will be the Agreement and materials welcoming it, either to AXP’s program for Capital Bankcardto perform services for AXP or in AXP’s standard Card acceptance program, which has different servicing terms (e.g., different speeds of pay). I understand that if the entity does notqualify for the Capital Bankcard servicing program, the entity may be enrolled in AXP’s standard Card acceptance program, and the entity may terminate the Agreement. By accepting theAmerican Express Card for the purchase of goods and/or services, or otherwise indicating its intention to be bound, the entity agrees to be bound by the Agreement. You further acknowledge and agree that you will not use your merchant account and/or the Services for illegal transactions, for example, those prohibited by the Unlawful Internet GamblingEnforcement Act, 31 U.S.C. Section 5361 et seq, as may be amended from time to time. Client agrees to all the terms of this Merchant Processing Application and Agreement. This Merchant Processing Application and Agreement shall not take effectuntil Client has been approved and this Agreement has been accepted by Capital Bankcard and Bank. Client’s Business Principal/Officer:Client’s Business Principal /Officer:

Signature X_____________________________________________________________ Signature X ___________________________________________________________________

Print Name of Signer _____________________________________________________ Print Name of Signer _____________________________________________________(must match name in Section 2) (must match name in Section 2)

Title___________________________________________________ Date____________ Title___________________________________________________ Date____________

Personal Guarantee: The undersigned guarantees to Capital Bankcard and Bank the performance of this Agreement and any addendum thereto by Client, and in the event of default,hereby waives Notice of Default and agrees to indemnify the other parties, including payment of all sums due and owing and costs associated with enforcement of the terms thereof. CapitalBankcard and Bank shall not be required to first proceed against Client or enforce any other remedy before proceeding against the under signed individual. This is a continuing guaranteeand shall not be discharged or affected by the death of the under signed and shall bind the heirs, administrators, representatives and assigns and been enforced by or for the benefit ofany successor of Capital Bankcard and Bank. The term of this guarantee shall be for the duration of the Merchant Processing Application and Agreement and any addendum thereto andshall guarantee all obligations which may arise or occur in connection with my activities during the term thereof through enforcement shall be sought subsequent to any termination.

Signature X ____________________________________________________________ Print Name_____________________________________________ Date ____________

Signature X ____________________________________________________________ Print Name_____________________________________________ Date ____________(must match name in Section 2)

DBA Name: _________________________________________________________________________ Merchant #: ___________________________________________________

Page 2 of 2

7. TRANSACTION INFORMATION

FINANCIAL DATA WHERE IS SALE TRANSACTED? (Must = 100%)

Store Front / Swiped ________%

Internet ________%

Mail Order / Telephone Order ________%

Face to Face Keyed ________%

Total ________%

Average Monthly Sales Volume (Cash + Credit + Debit + Check) $___________

Average MONTHLY MC/Visa/Discover Network/American Express Volume $___________

Average MC/Visa/Discover Network/American Express Ticket $___________

Seasonal? ■■ No ■■ Yes High Volume Months Open:___________________________________________ 100

Capital Bankcard (d/b/a Beacon Payments) is a registered ISO/MSP of Wells Fargo Bank, N.A., Walnut Creek, CA

BP1406(ia) BPICP1406(ia)

MonthlyService Fee $_________

Application Fee $_________

Voice Auth Fee $_________

Annual Fee $_________

Min. Monthly Discount Fee $_________

Retrieval Fee $_________

Chargeback Fee $_________

AVS (per transaction) $_________

Per Batch $_________

Debit Network Access $_________

Wireless Fee $_________

Early Termination Fee $_________

Other: $_________

_________________________

DISCOUNT RATES: Visa/MC/Discover Network: Discount Rate Per Item

Check /Debit Cards __________% $__________

Credit Cards __________% $__________Visa/MC/Discover Network IC Pass Thru You will be charged the applicable interchange rate and assessment fee from MasterCard, Visa and Discover Network, plus any other fees indicated in this Service Fee Schedule.

TRANSACTIONS: Per Trans/ American Express PIN DebitCommunication Per Trans /Communication (plus the applicable network fees)

$__________ $__________ $__________

AMERICAN EXPRESS: New Service Requested? ■■ Yes ■■ No■■ One Point / Full Service (EDC) or ■■ ESA/Pass Through

Per Item Rate $__________ SE #:______________________________________

American Express OnePoint Rate __________% Per Item $__________

0.30% downgrade will be charged for transactions whenever a CNP (Card Not Present) charge occurs. CNP means acharge for which the card is not presented at the point of purchase (e.g., charges by mail, telephone or Internet), isused at unattended establishments (e.g., customer activated terminals), or for which the transaction is key entered.

(For Internal Use Only)

Accepted By Capital Bankcard Wells Fargo Bank, N.A., 1200 Montego Way, Walnut Creek, CA 94598

Signature X ____________________________________________________________ Signature X ___________________________________________________________

Title _________________________________________________ Date____________ Title __________________________________________________ Date __________

The following fees will be passed through: VISA – Misuse of Authorization, Zero Floor Limit, International Acquirer, ACQ ISA, APF;MASTERCARD – Acquirer Support, Cross Border, NABU; DISCOVER – International Processing; Data Usage

6. SERVICE FEE SCHEDULE (cont’d)

28

BP1406(ia) 32

BP1406(ia) CONFIRMATION PAGE

Print Client’s Business Legal Name: _________________________________________________________________________________________________

By its signature below, Client acknowledges that it received (either in person, by facsimile, or by electronic transmission) the completeProgram Guide [Version BP1406(ia)] consisting of 32 pages (including this confirmation).

Client further acknowledges reading and agreeing to all terms in the Program Guide, which shall be incorporated into Client’s Agreement.Upon receipt of a signed facsimile or original of this Confirmation Page by us, Client’s Application will be processed.

Client understands that a copy of the Program Guide is also available for downloading from the Internet at:

www.beaconpayments.com/mpa

NO ALTERATIONS OR STRIKE-OUTS TO THE PROGRAM GUIDE WILL BE ACCEPTED AND, IF MADE, ANY SUCH ALTER A TIONSOR STRIKE-OUTS SHALL NOT APPLY.

Client’s Business Principal: Signature (Please sign below):

X___________________________________________________________________________ ____________________________________________________ __________________________Title Date

________________________________________________________________________Please Print Name of Signer

Please read the Program Guide in its entirety. It describes the terms under which we will provide merchant pro cessing services to you.

From time to time you may have questions regarding the contents of your Agreement with Bank and/or Processor. The following informationsummarizes portions of your Agreement in order to assist you in answering some of the questions we are most commonly asked.

9. Card Organization DisclosureVisa and MasterCard Member Bank Information: Wells Fargo Bank, N.A. The Bank’s mailing address is 1200 Montego Way, Walnut Creek, CA 94598, and its phone number is (925) 746-4143.

Important Member Bank Responsibilities:

a) The Bank is the only entity approved to extend acceptance of Visa and MasterCard products directly to a Merchant.

b) The Bank must be a principal (signer) to the Merchant Agreement.

c) The Bank is responsible for educating Merchants on pertinent Visa and MasterCard rules with which Merchants must comply;but this information may be provided to you by Processor.

d) The Bank is responsible for and must provide settlement funds tothe Merchant.

e) The Bank is responsible for all funds held in reserve that arederived from settlement.

Important Merchant Responsibilities:

a) Ensure compliance with cardholder data security and storagerequirements.

b) Maintain fraud and chargebacks below Card Organizationthresholds.

c) Review and understand the terms of the Merchant Agreement.

d) Comply with Card Organization rules.

1. Your discount rates are assessed on transactions that qualify for cer -tain reduced interchange rates imposed by MasterCard, Visa and DiscoverNetwork. Any transactions that fail to qualify for these reduced rates willbe charged an additional fee (see Sec tion 18 of the Program Guide).

2. We may debit your bank account from time to time for amounts owedto us under the Agreement.

3. There are many reasons why a Chargeback may occur. When they occurwe will debit your settlement funds or settlement account. For a more de -tailed discussion regarding Chargebacks, see Section 10.

4. If you dispute any charge or funding, you must notify us within 60days of the date of the statement where the charge or funding appears orshould have appeared.

5. The Agreement limits our liability to you. For a detailed des criptionof the limitation of liability see Section 20.

6. We have assumed certain risks by agreeing to provide you with Cardprocessing. Accordingly, we may take certain actions to mitigate our risk,in cluding termination of the Agree ment, and/or hold monies otherwisepayable to you (see Section 23, Term; Events of Default and Section 24,Reserve Account; Security Interest).

7. By executing this Agreement with us you are authorizing us and ourAffiliate to obtain financial and credit information regarding your businessand the signer and guarantors of the Agreement until all your obligationsto us and our Affiliate are satisfied.

8. The Agreement contains a provision that in the event you terminatethe Agreement early, you may be responsible for the payment of earlytermination fees as set forth in Section 34, Additional Fee Information.

29

Merchant agrees to pay refundable $99.00 deposit on each terminal placement. The

$99.00 deposit will be refunded to the merchant, when the equipment has been

returned to Beacon Payments in good working condition, within ten (10) business

days.

This agreement is a contract between the Merchant below and Beacon Payments.

The Merchant agrees the equipment is the property of Beacon Payments; the

equipment is being licensed to the merchant, and must be returned in good working

condition within ten (10) days of the termination or expiration of the merchant

processing agreement with Beacon Payments. If the equipment is not returned

within ten (10) days, merchant agrees to pay the equipment value of $599.00. In

addition, Merchant agrees to be responsible for any damage to the Equipment as a

result of misuse or negligence.

Merchant agrees to hold Beacon Payments harmless from any and all liabilities,

losses, damages, disputes, claims, offsets, or counterclaims of any kind related to

the use of the equipment.

The merchant understands that Beacon Payments will warranty the equipment as

long as the merchant has an active merchant processing contract in place.

Merchants are limited to one free replacement terminal; any additional replacements

will incur a charge of $199.00.

By signing below, merchant acknowledges that this agreement constitutes a legal

contract; which binds the merchant.

___________________________________ ______________________________________ _____________

Print Name Signature Date

The undersigned, who will derive a benefit by entering into the above agreement

between the Merchant and Beacon Payments hereby guarantees to Beacon

Payments and to its successors and assigns, the full, prompt and complete

performance of merchant and all of the merchant’s obligations under this agreement.

The undersigned, by signing below, agrees to be bound by the agreement and this

guaranty.

Company Name: __________________________________________________________________________

Address: _________________________________________________________________________________

Signature: ________________________________________ Date: _____________________________

Personal Guarantor (Print Name): ______________________________________________________

30