Embed Size (px)

Citation preview

BP Amoco:

Policy Statement on the Use of Project Finance

Abhik Tushar Das (20104001)Sitanshu Pathak (20104007)

15 Month Executive MBA ProgramSchool of Petroleum Management, PDPU

Content

• Organization Structure

• Post merger structure

• Assignment

• Discussion on PF and CF – Advantage

– Disadvantage

– Structure

– Sources

– Institutions

• BP Amoco PF and CF Model

6/14/2011 2Comments:

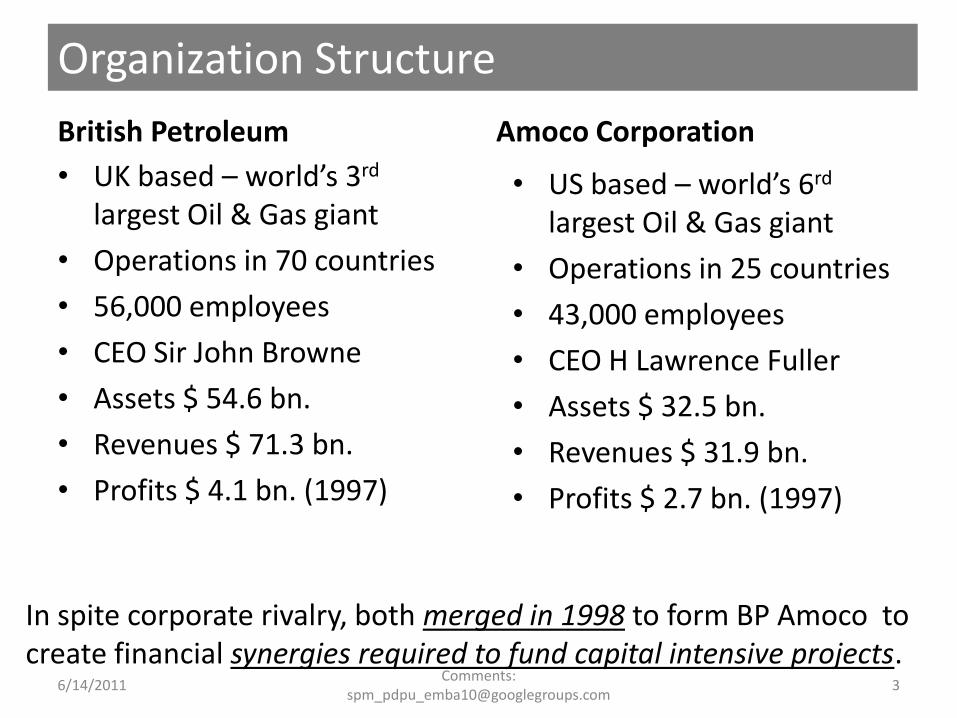

Organization Structure

British Petroleum

• UK based – world’s 3rd

largest Oil & Gas giant

• Operations in 70 countries

• 56,000 employees

• CEO Sir John Browne

• Assets $ 54.6 bn.

• Revenues $ 71.3 bn.

• Profits $ 4.1 bn. (1997)

Amoco Corporation

• US based – world’s 6rd

largest Oil & Gas giant

• Operations in 25 countries

• 43,000 employees

• CEO H Lawrence Fuller

• Assets $ 32.5 bn.

• Revenues $ 31.9 bn.

• Profits $ 2.7 bn. (1997)

In spite corporate rivalry, both merged in 1998 to form BP Amoco to create financial synergies required to fund capital intensive projects.

6/14/2011 3Comments:

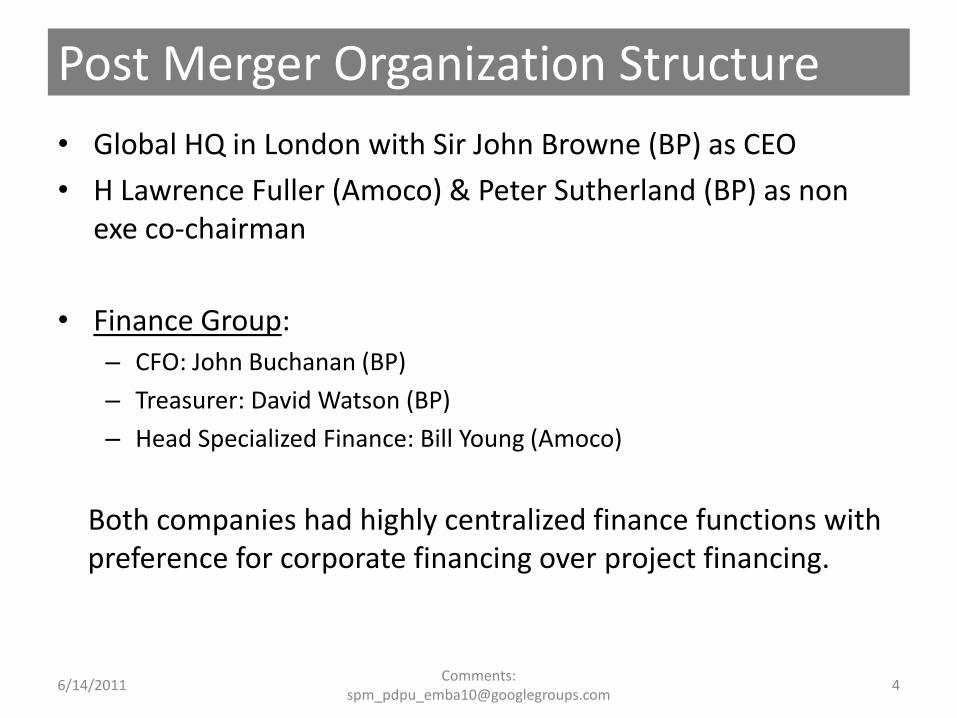

Post Merger Organization Structure

• Global HQ in London with Sir John Browne (BP) as CEO

• H Lawrence Fuller (Amoco) & Peter Sutherland (BP) as non exe co-chairman

• Finance Group:– CFO: John Buchanan (BP)

– Treasurer: David Watson (BP)

– Head Specialized Finance: Bill Young (Amoco)

Both companies had highly centralized finance functions with preference for corporate financing over project financing.

6/14/2011 4Comments:

The Assignment

Goal:

• To work out new financing policy for the merged entity.

Process:

• Watson & Bill sought opinion of finance executives of both the firms regarding their take on project finance vis-a-viscorporate finance.

• BP sparingly used project finance

• Amoco too, believed in corporate finance more. But they sometimes used project finance.

6/14/2011 5Comments:

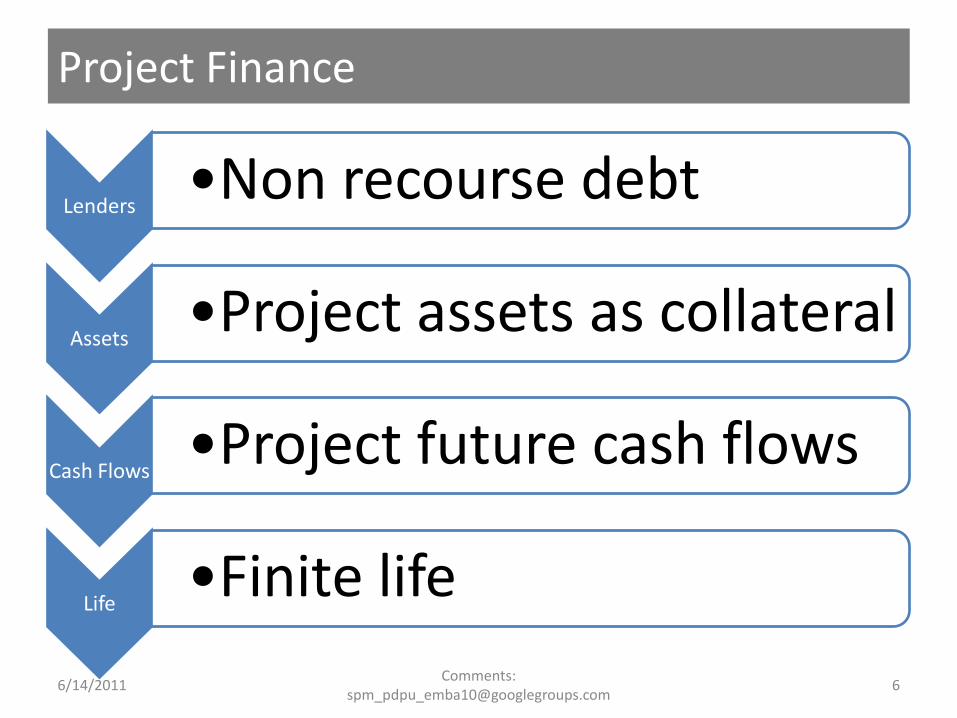

Project Finance

Lenders•Non recourse debt

Assets•Project assets as collateral

Cash Flows•Project future cash flows

Life•Finite life

6/14/2011 6Comments:

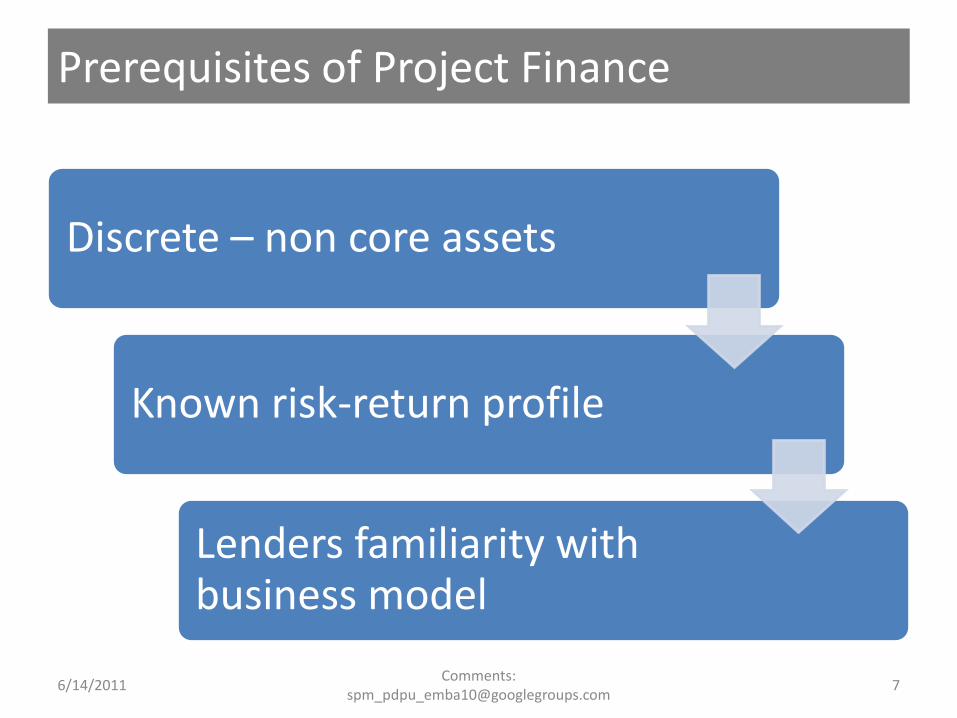

Prerequisites of Project Finance

Discrete – non core assets

Known risk-return profile

Lenders familiarity with business model

6/14/2011 7Comments:

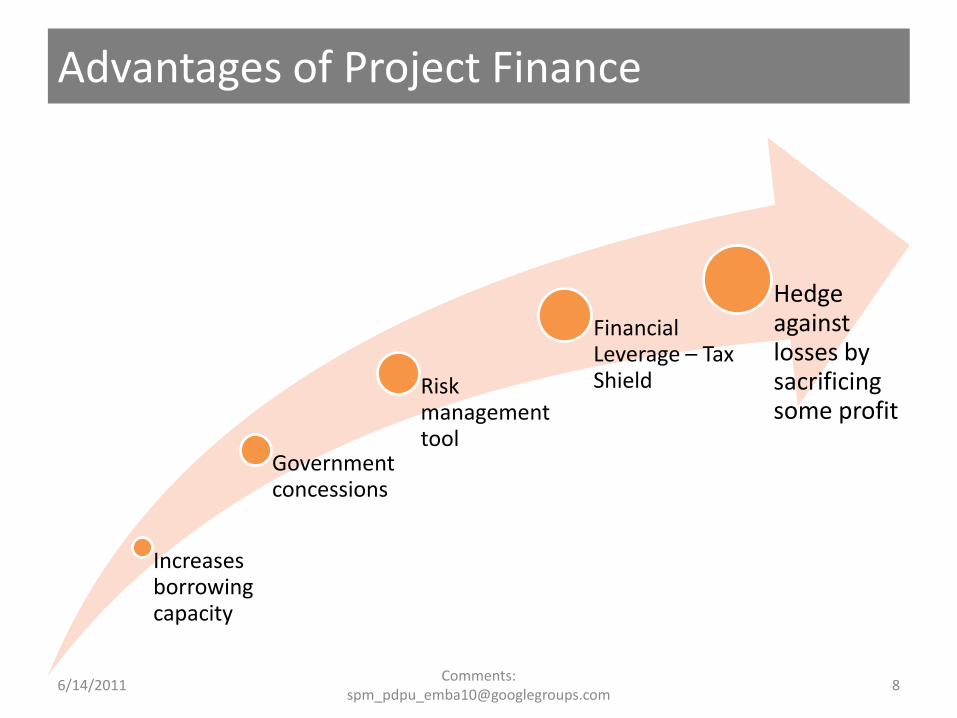

Advantages of Project Finance

Increases borrowing capacity

Government concessions

Risk management tool

Financial Leverage – Tax Shield

Hedge against losses by sacrificing some profit

6/14/2011 8Comments:

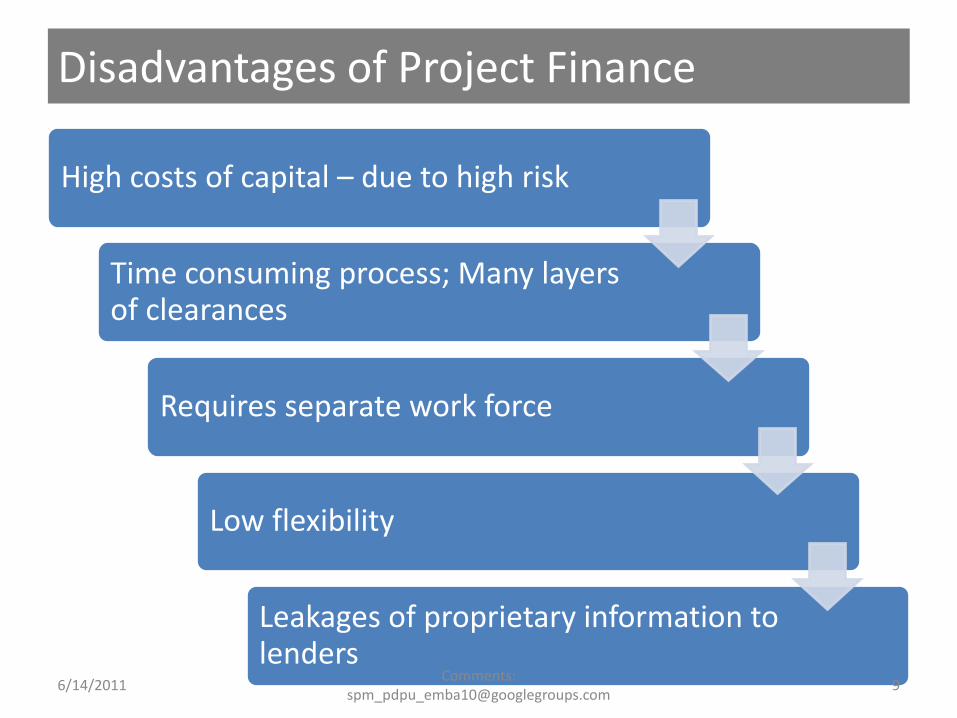

Disadvantages of Project Finance

High costs of capital – due to high risk

Time consuming process; Many layers of clearances

Requires separate work force

Low flexibility

Leakages of proprietary information to lenders

6/14/2011 9Comments:

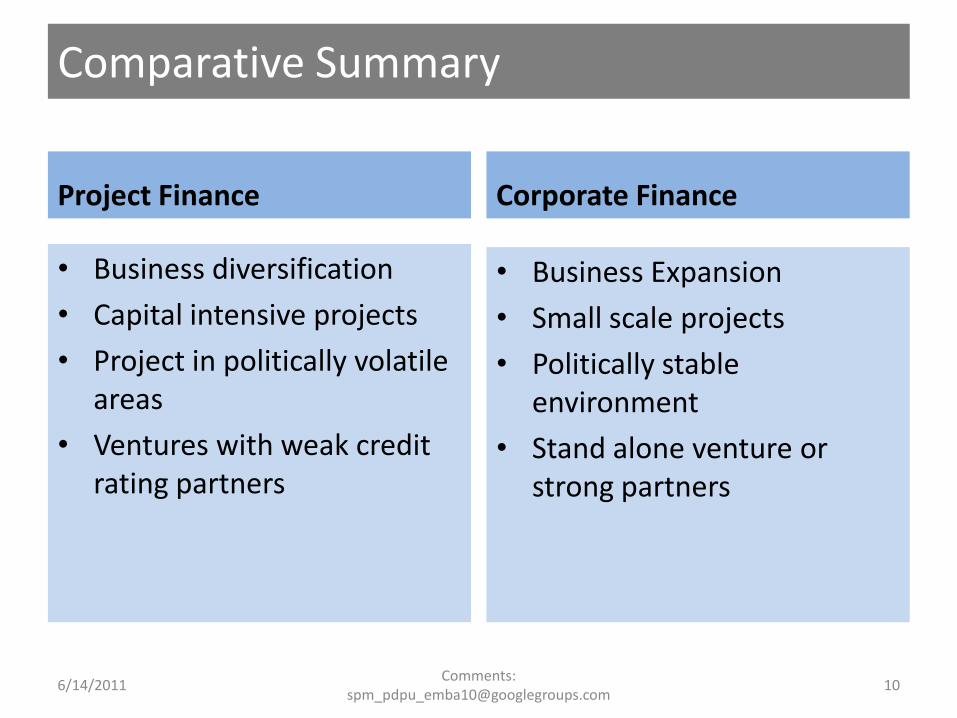

Comparative Summary

Project Finance

• Business diversification

• Capital intensive projects

• Project in politically volatile areas

• Ventures with weak credit rating partners

Corporate Finance

• Business Expansion

• Small scale projects

• Politically stable environment

• Stand alone venture or strong partners

6/14/2011 10Comments:

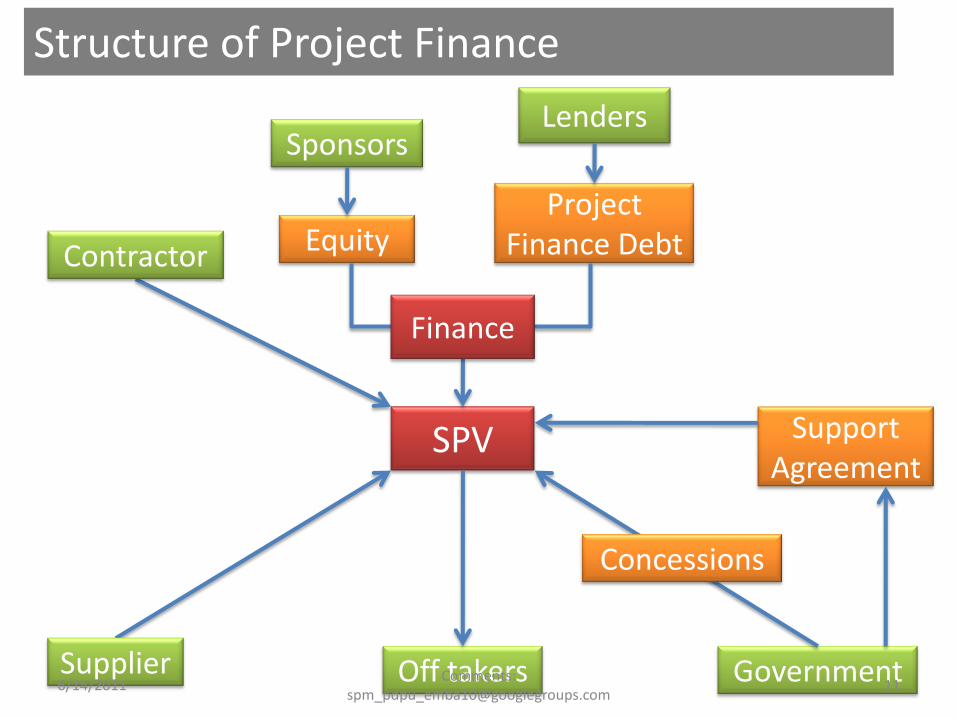

SponsorsLenders

EquityProject

Finance Debt

Off takers Government

Support Agreement

SPV

Concessions

Finance

Supplier

Contractor

Structure of Project Finance

6/14/2011 11Comments:

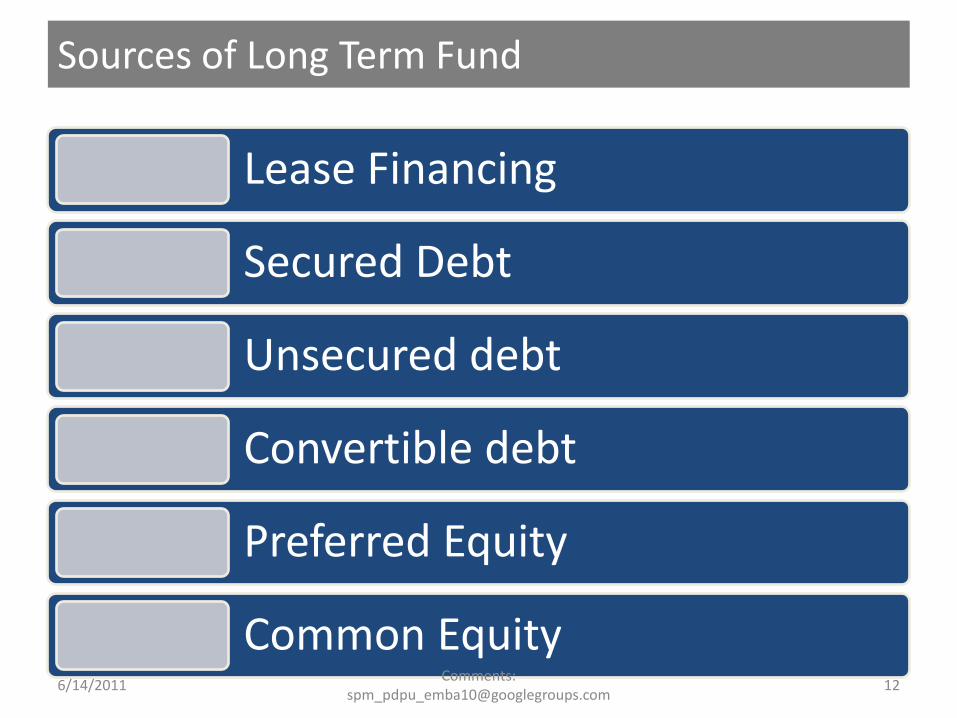

Sources of Long Term Fund

Lease Financing

Secured Debt

Unsecured debt

Convertible debt

Preferred Equity

Common Equity6/14/2011 12

Comments: [email protected]

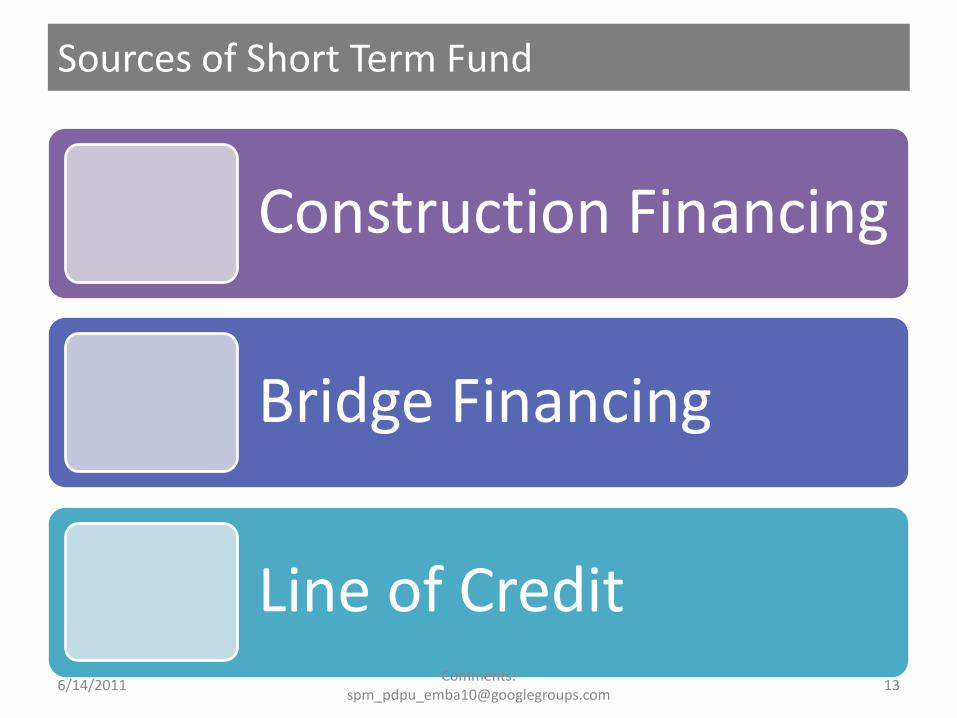

Sources of Short Term Fund

Construction Financing

Bridge Financing

Line of Credit6/14/2011 13

Comments: [email protected]

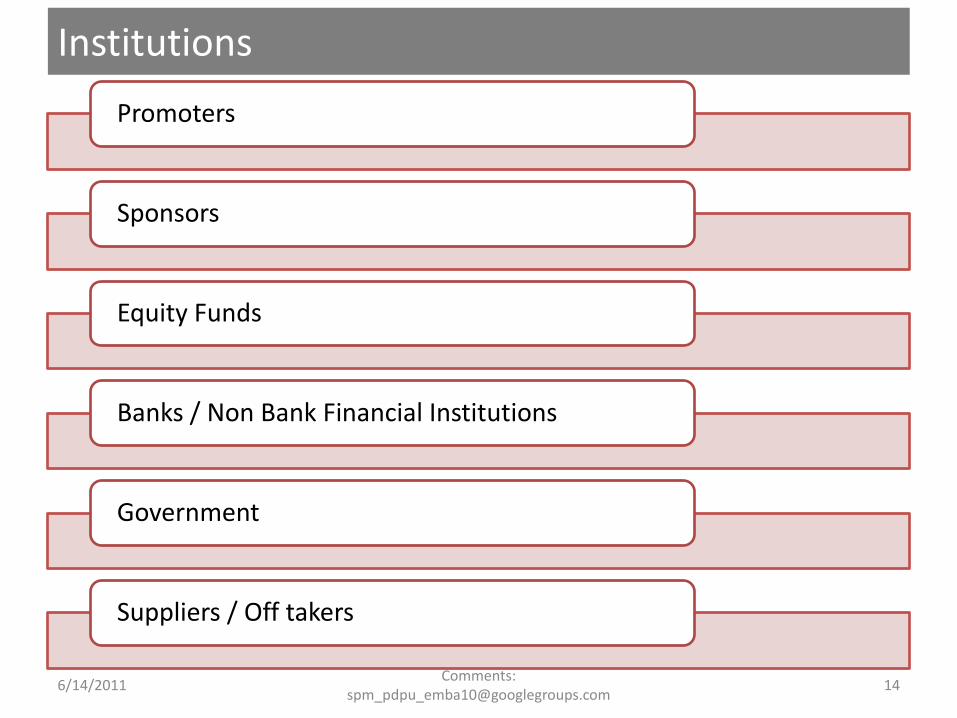

Institutions

Promoters

Sponsors

Equity Funds

Banks / Non Bank Financial Institutions

Government

Suppliers / Off takers

6/14/2011 14Comments:

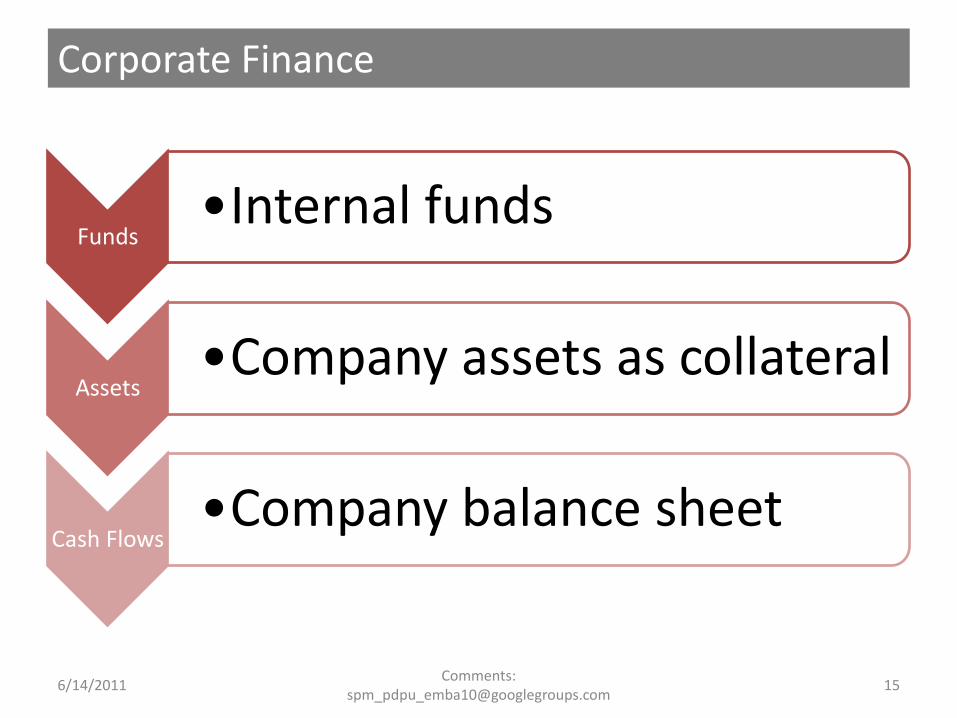

Corporate Finance

Funds•Internal funds

Assets•Company assets as collateral

Cash Flows•Company balance sheet

6/14/2011 15Comments:

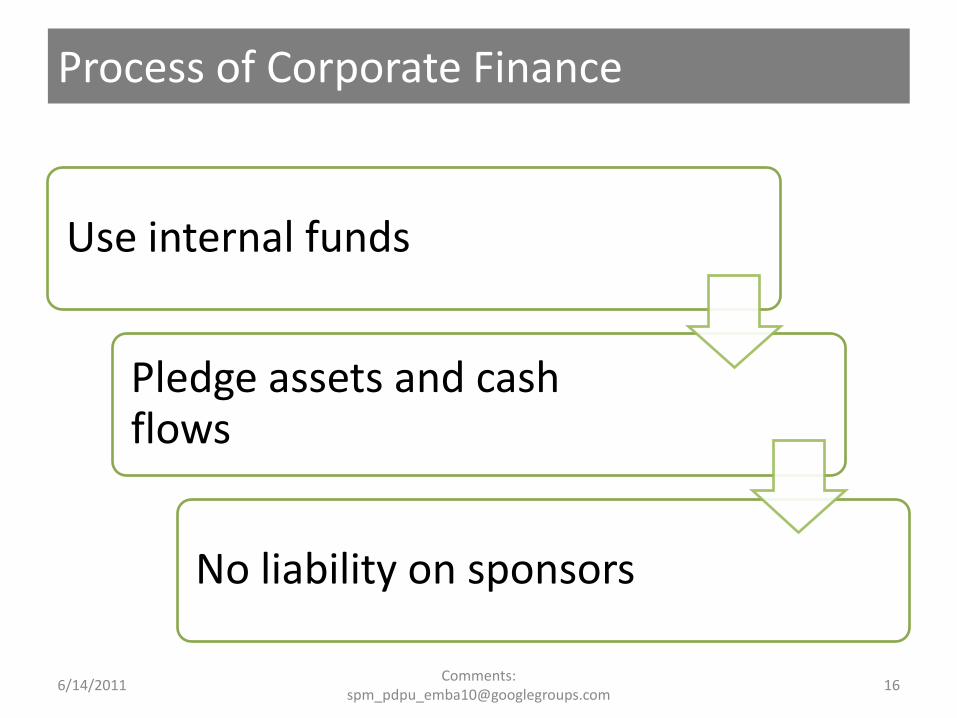

Process of Corporate Finance

Use internal funds

Pledge assets and cash flows

No liability on sponsors

6/14/2011 16Comments:

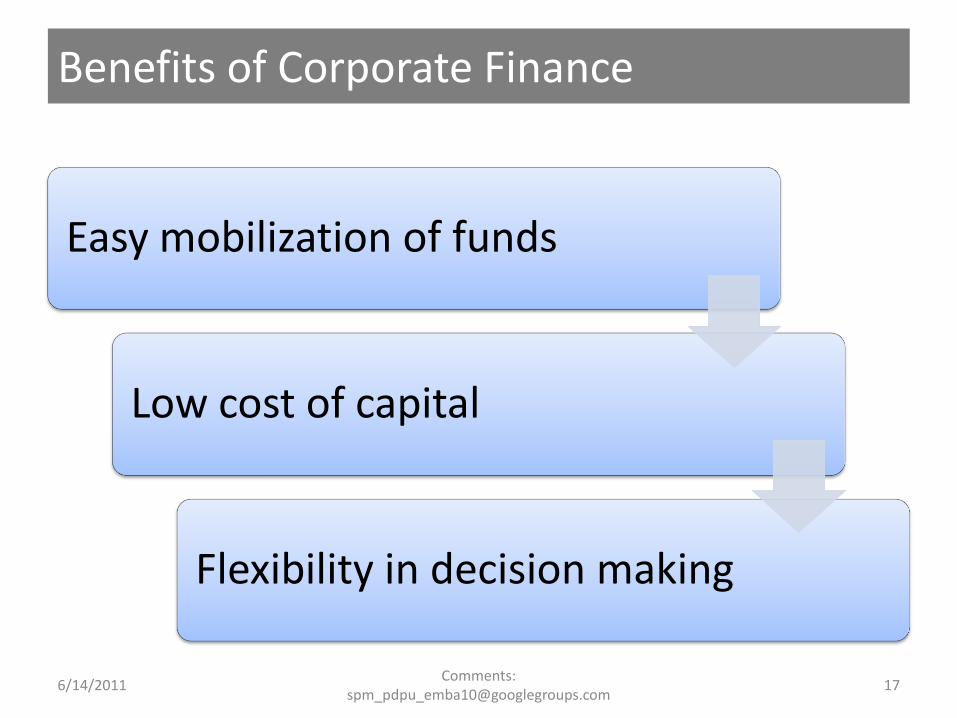

Benefits of Corporate Finance

Easy mobilization of funds

Low cost of capital

Flexibility in decision making

6/14/2011 17Comments:

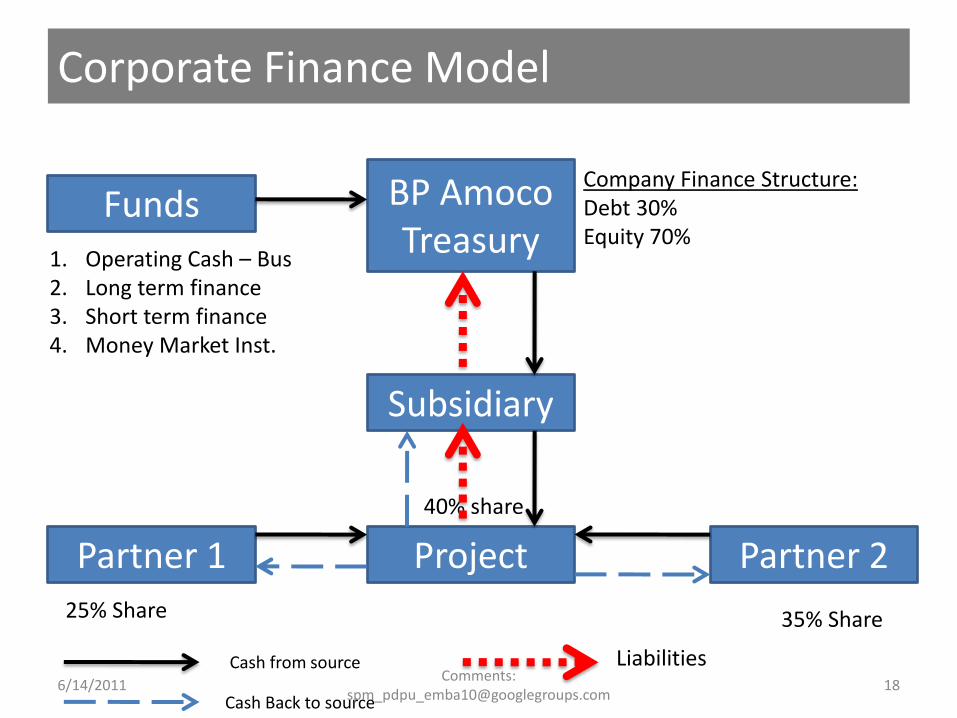

Corporate Finance Model

Project Partner 2Partner 125% Share 35% Share

Subsidiary

40% share

Cash Back to source

Cash from source

BP AmocoTreasury

Company Finance Structure:Debt 30%Equity 70%

Funds1. Operating Cash – Bus2. Long term finance3. Short term finance4. Money Market Inst.

Liabilities6/14/2011 18

Comments: [email protected]

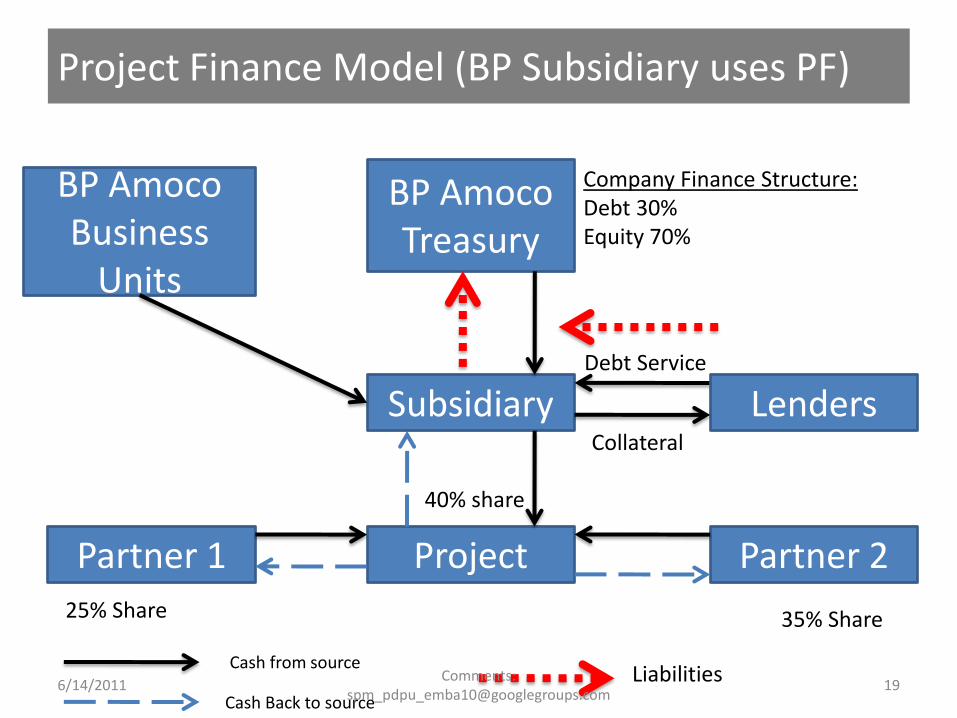

Project Finance Model (BP Subsidiary uses PF)

Project Partner 2Partner 125% Share 35% Share

Subsidiary

40% share

Cash Back to source

Cash from source

BP AmocoTreasury

Company Finance Structure:Debt 30%Equity 70%

BP Amoco Business

Units

LendersCollateral

Debt Service

Liabilities6/14/2011 19

Comments: [email protected]

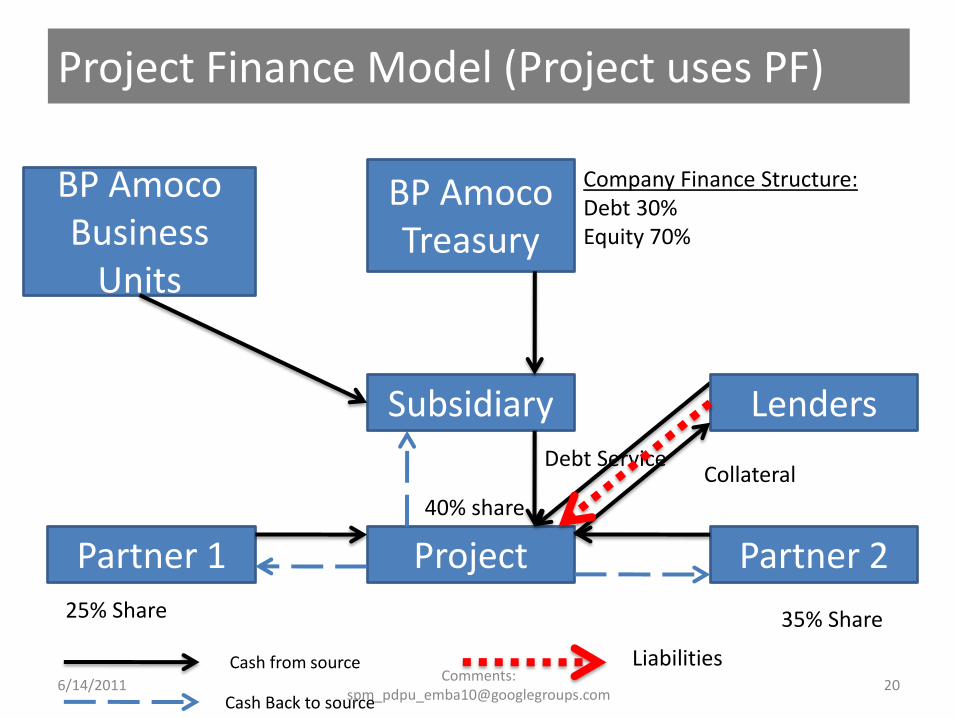

Project Partner 2Partner 125% Share 35% Share

Subsidiary

40% share

Cash Back to source

Cash from source

BP AmocoTreasury

Company Finance Structure:Debt 30%Equity 70%

BP Amoco Business

Units

Lenders

CollateralDebt Service

Project Finance Model (Project uses PF)

Liabilities6/14/2011 20

Comments: [email protected]

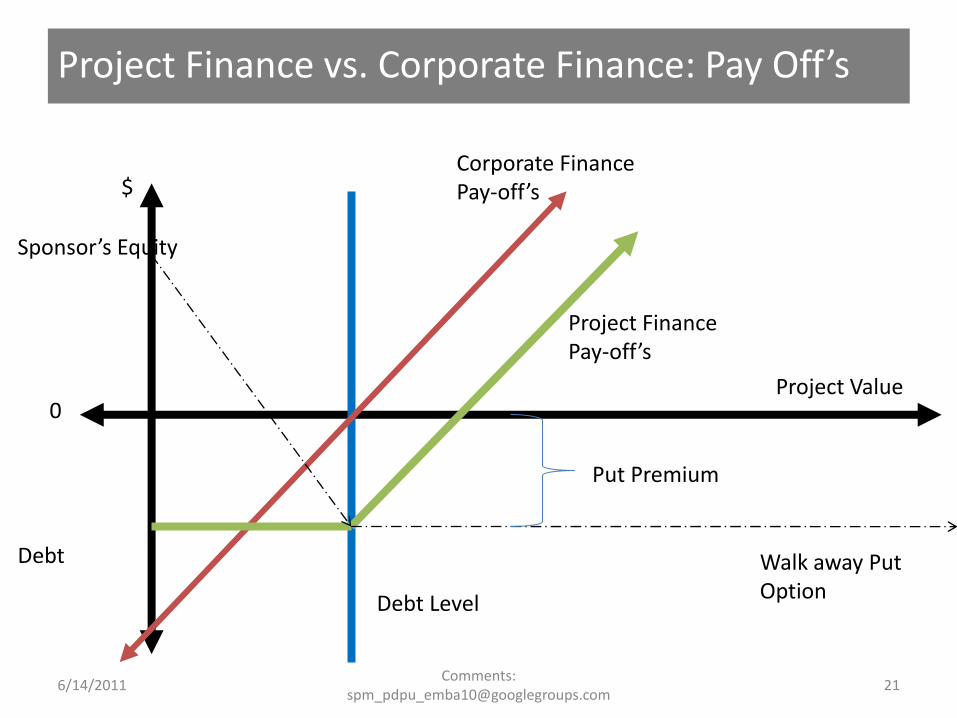

Project Finance vs. Corporate Finance: Pay Off’s

Put Premium

Walk away Put Option

Project Value

Project Finance Pay-off’s

Corporate Finance Pay-off’s

Debt Level

Sponsor’s Equity

0

$

Debt

6/14/2011 21Comments:

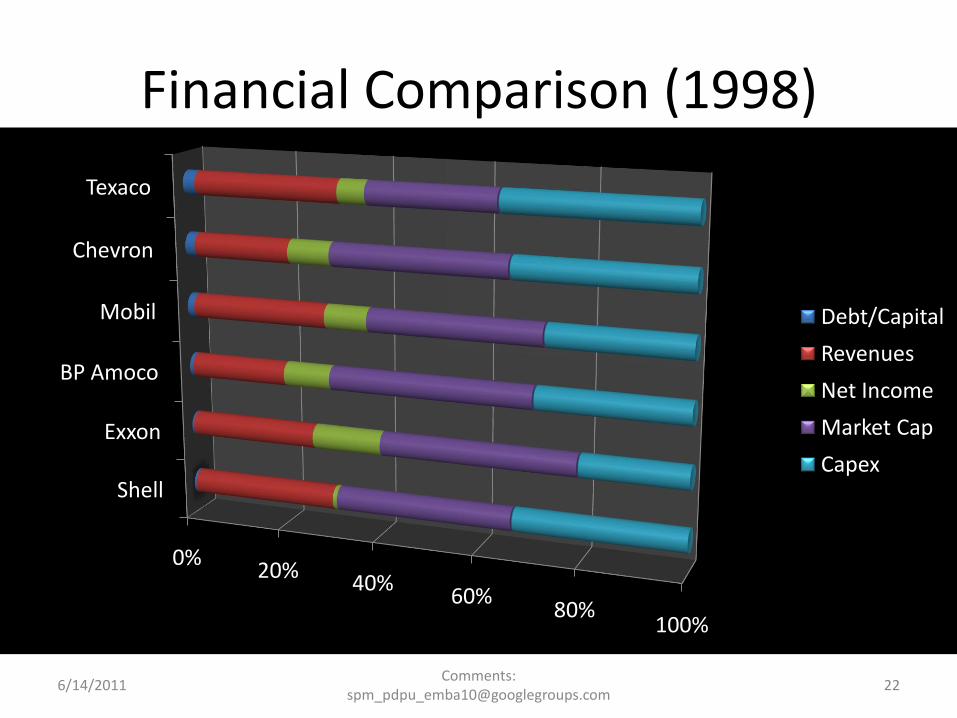

Financial Comparison (1998)

0%20%

40%60%

80%100%

Shell

Exxon

BP Amoco

Mobil

Chevron

Texaco

Debt/Capital

Revenues

Net Income

Market Cap

Capex

6/14/2011 22Comments:

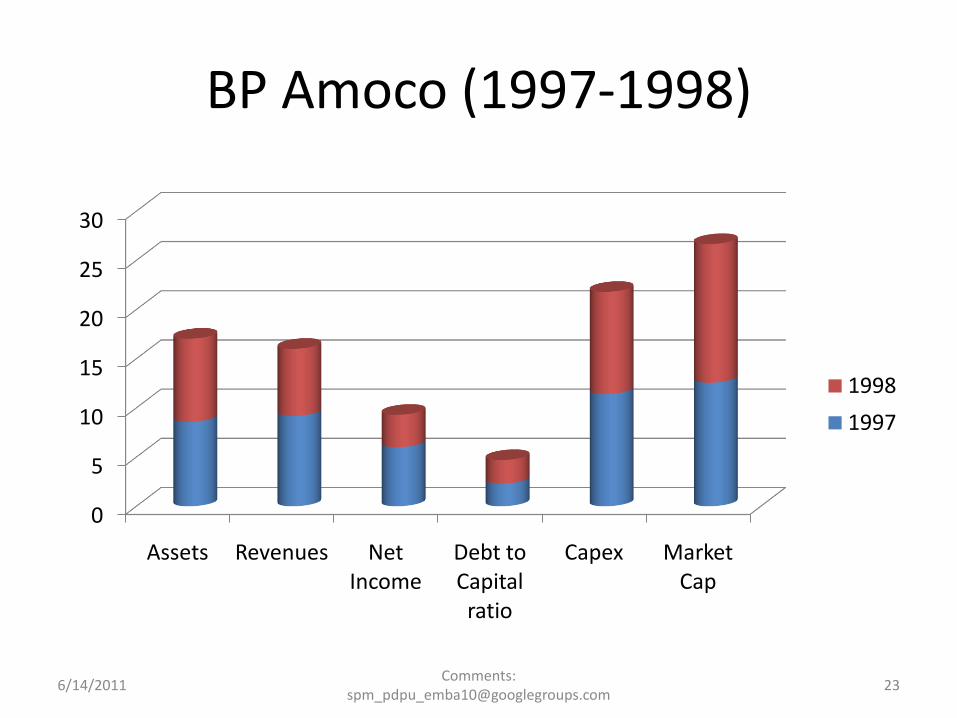

BP Amoco (1997-1998)

0

5

10

15

20

25

30

Assets Revenues Net Income

Debt to Capital

ratio

Capex Market Cap

1998

1997

6/14/2011 23Comments:

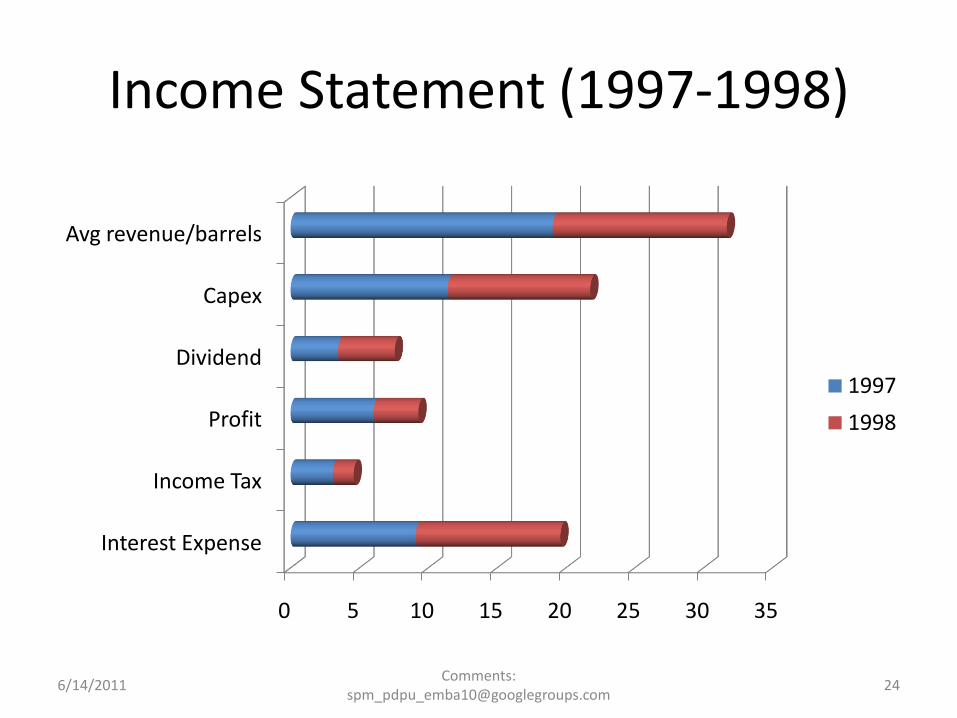

Income Statement (1997-1998)

0 5 10 15 20 25 30 35

Interest Expense

Income Tax

Profit

Dividend

Capex

Avg revenue/barrels

1997

1998

6/14/2011 24Comments: