Embed Size (px)

Citation preview

Botswana Budget 2016/17Driving Progress

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 D

ETAIL U

NIT

S

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

February 1

Next >>

Budget highlights ......................................................................... 1- General- Fiscal

Income Tax For Individuals ........................................................... 3- Tax rates- Exemption and Tax Free Benefits for Individuals- Benefits Valuation- Motor Vehicle Scale of Values

Capital gains Tax (CGT) ................................................................. 7- Inclusions, Exclusions and Deductions- Tax rates

Withholding Tax ........................................................................... 9- Double Taxation Agreement Withholding Tax rates- Statutory Withholding Tax rates

Corporate Tax Rate .................................................................... 11- Tax rates

Capital Allowances ..................................................................... 11- Tax rates

Capital Transfer Tax .................................................................... 12- Tax rates

Transfer Duty ............................................................................. 12- Tax rates

Value Added Tax ........................................................................ 13- Zero rated Supplies- Exempt Supplies

Self-Assessment Tax (SAT) .......................................................... 14 Filing Deadlines .......................................................................... 15

Interest And Penalties ................................................................ 15

Deloitte Botswana - Tax ............................................................. 16

Key Contacts .............................................................................. 16

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 1

Navigation

<< Previous | Next >>

.......... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS Budget Highlights

Highlights of the budget speech for 2016/2017, presented to the National Assembly on Monday

1 February 2016, by the Minister of Finance and Development Planning, the Honourable O.K. Matambo,

are as follows:

General• The 2016/2017 budget marks the end of the tenth National Development Plan (NDP 10), the

implementation of which was affected by the global financial crisis of 2008/09.• The budget is a transitional one from: NDP 10 to NDP 11; Vision 2016 to Vision 2036; and the United

Nations Millennium Development Goals (MDGs) to Sustainable Development Goals (SDGs).• Government has adopted the Economic Stimulus Programme (ESP) to boost growth, promote economic

diversification and create jobs. • The economy continues to face challenges due to the continued weak recovery of the global economy,

particularly the depressed global demand for and prices of diamonds, lower commodity prices, electricity and water shortages.

Gross Domestic Product • Botswana’s domestic economic growth decreased from 3.2% in 2014 to 1.0% in 2015.• Growth forecast to reach 4.2% in 2016 and 4.3% in 2017.Inflation and Monetary Policy • Botswana’s inflation rate fell from 3.8% in December 2014 to 3.1% in December 2015, in line with the

Bank of Botswana’s objective range of 3 - 6%.• The Bank Rate reduced from 6.5% in January 2015 to 6% in August 2015.Balance of payments and foreign exchange reserves• Overall balance of payments for 2015 is estimated at P3.3 billion as at November 2015, from

P11.4 billion in 2014.• Current account surplus is estimated to fall from P22.9 billion in 2014 to 12.9 billion in 2015.• Foreign exchange reserves at the end of December 2015 amounted to P84.9 billion, which is equivalent

to 19 months import cover for goods and services.

Exchange rates

• The Pula basket weights maintained at 50% Rand and 50% SDR for 2016, while the rate of crawl changed from zero to an upward crawl of 0.38% per annum.

• The Pula depreciated by 11.6% against the Special Drawing Rights, while by December 2015 it appreciated by 13.6% against the South African Rand.

Botswana Budget 2016/17 Driving progress 2

Navigation.......... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

General (cont.)Performance of Public Enterprises• Parastatals which performed satisfactorily included Botswana Development Corporation, Botswana

Telecommunications Corporation, Botswana Communications Regulatory Authority, Botswana Housing Corporation and Botswana Savings Bank.

• Botswana Meat Commission, Air Botswana, National Development Bank and Water Utilities Corporation recorded losses in 2015.

Key thematic areas for 2016/17 financial year• Investing in infrastructural development • Creating employment opportunities• Strengthening human capital• Enhancing national security• Strengthening local governanceBudget for FY 2014/15 & 2015/16• 2014/15 Budget outturn – P5.34 billion overall budget surplus.• 2015/16 Revised budget estimates – P4.2 billion overall budget deficit, compared to original budget

estimated surplus of P1.23 billion.Budget Proposals for FY 2016/17• The Economic Stimulus Programme (ESP) has been introduced to stimulate economic growth and create

job opportunities.• Proposed 2016/17 overall budget is P6.05 billion deficit or 3.8% of GDP. • Total revenues and grants are estimated at P48.4 billion.• Proposed 2016/17 recurrent budget is P36.99 billion. 79.7% of recurrent budget allocated to Ministries

of Education and Skills Development; Health; Local Government and Rural Development, Defence, Justice and Security, Transport and Communications and State President. The Ministry of Education and Skills Development is allocated the largest amount of P10.64 billion or 28.8%.

• Proposed 2016/17 development budget is P14.82 billion. The largest share of the proposed development budget of P3.59 billion or 24.2%, is allocated to the Ministry of Defence, Justice and Security, followed by the Ministry of Minerals, Energy and Water Resources (23.1%) and Ministry of Transport and

Communications (9.5%).

Public Service Salaries• Government remains fully committed to the Bargaining Council in the process of negotiating public

service salaries and will continue to consult with Trade Unions.

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 3

Navigation........... Budget Highlights

.......... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

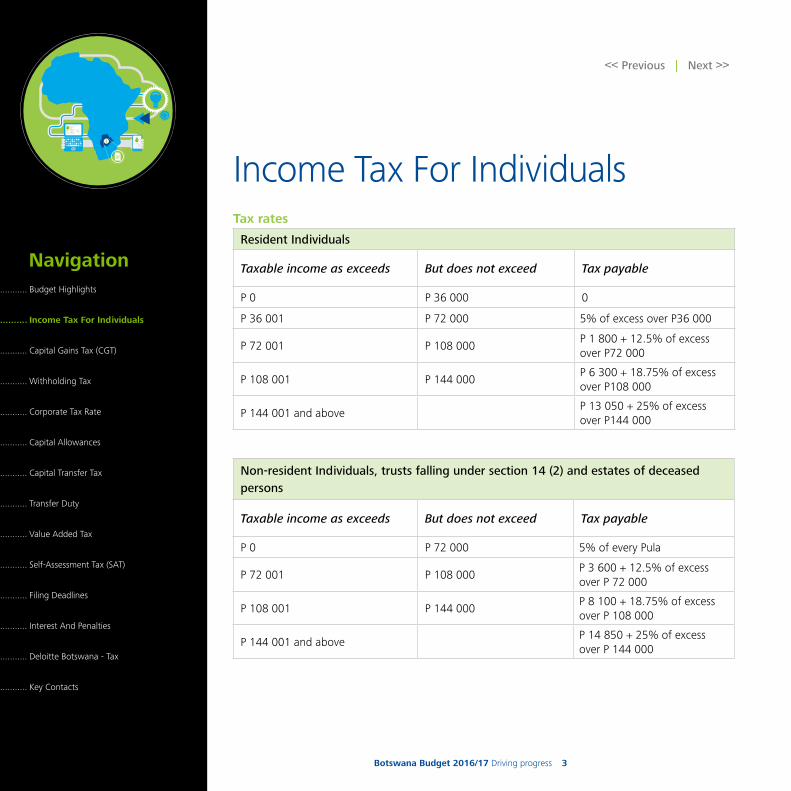

Income Tax For IndividualsTax rates

Resident Individuals

Taxable income as exceeds But does not exceed Tax payable

P 0 P 36 000 0

P 36 001 P 72 000 5% of excess over P36 000

P 72 001 P 108 000P 1 800 + 12.5% of excess over P72 000

P 108 001 P 144 000 P 6 300 + 18.75% of excess over P108 000

P 144 001 and above P 13 050 + 25% of excess over P144 000

Non-resident Individuals, trusts falling under section 14 (2) and estates of deceased persons

Taxable income as exceeds But does not exceed Tax payable

P 0 P 72 000 5% of every Pula

P 72 001 P 108 000P 3 600 + 12.5% of excess over P 72 000

P 108 001 P 144 000 P 8 100 + 18.75% of excess over P 108 000

P 144 001 and above P 14 850 + 25% of excess over P 144 000

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 4

Navigation........... Budget Highlights

.......... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

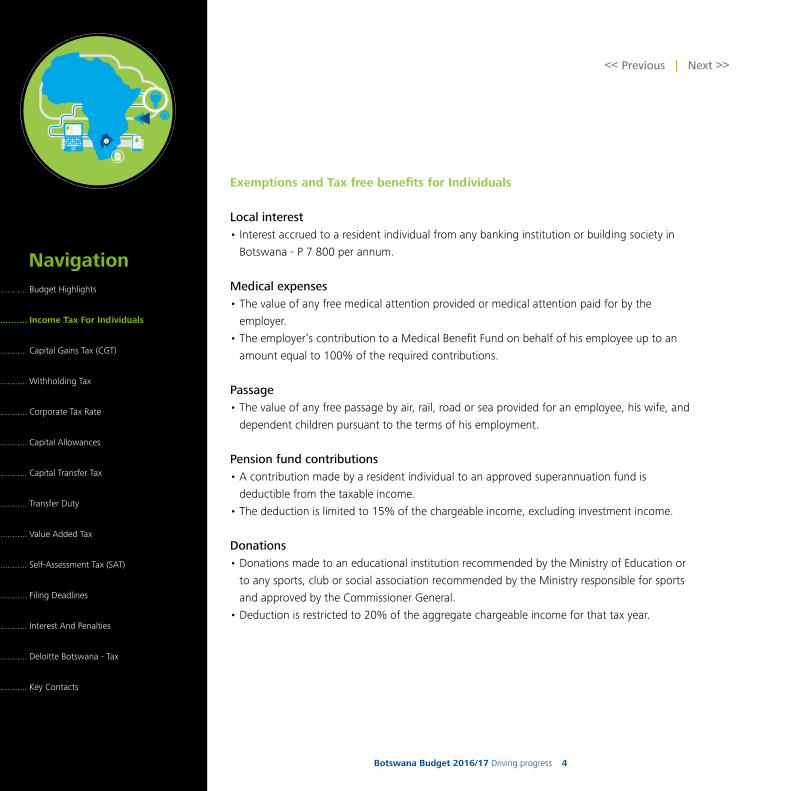

Exemptions and Tax free benefits for Individuals

Local interest• Interest accrued to a resident individual from any banking institution or building society in

Botswana - P 7 800 per annum.

Medical expenses• The value of any free medical attention provided or medical attention paid for by the

employer.

• The employer’s contribution to a Medical Benefit Fund on behalf of his employee up to an

amount equal to 100% of the required contributions.

Passage• The value of any free passage by air, rail, road or sea provided for an employee, his wife, and

dependent children pursuant to the terms of his employment.

Pension fund contributions• A contribution made by a resident individual to an approved superannuation fund is

deductible from the taxable income.

• The deduction is limited to 15% of the chargeable income, excluding investment income.

Donations• Donations made to an educational institution recommended by the Ministry of Education or

to any sports, club or social association recommended by the Ministry responsible for sports

and approved by the Commissioner General.

• Deduction is restricted to 20% of the aggregate chargeable income for that tax year.

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 5

Navigation........... Budget Highlights

.......... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

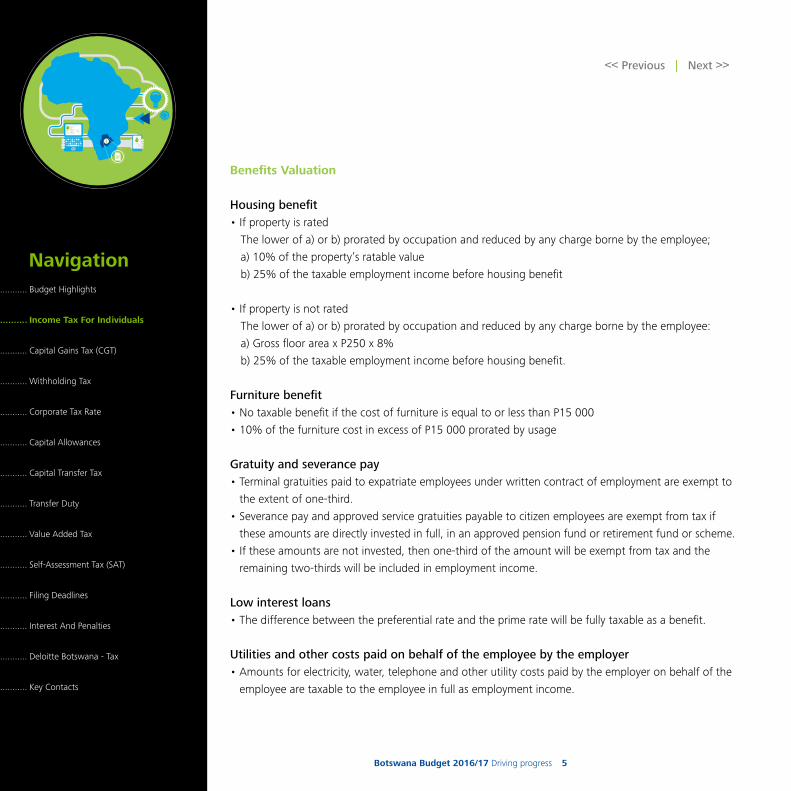

Benefits Valuation

Housing benefit• If property is rated

The lower of a) or b) prorated by occupation and reduced by any charge borne by the employee;

a) 10% of the property’s ratable value

b) 25% of the taxable employment income before housing benefit

• If property is not rated

The lower of a) or b) prorated by occupation and reduced by any charge borne by the employee:

a) Gross floor area x P250 x 8%

b) 25% of the taxable employment income before housing benefit.

Furniture benefit• No taxable benefit if the cost of furniture is equal to or less than P15 000

• 10% of the furniture cost in excess of P15 000 prorated by usage

Gratuity and severance pay• Terminal gratuities paid to expatriate employees under written contract of employment are exempt to

the extent of one-third.

• Severance pay and approved service gratuities payable to citizen employees are exempt from tax if

these amounts are directly invested in full, in an approved pension fund or retirement fund or scheme.

• If these amounts are not invested, then one-third of the amount will be exempt from tax and the

remaining two-thirds will be included in employment income.

Low interest loans• The difference between the preferential rate and the prime rate will be fully taxable as a benefit.

Utilities and other costs paid on behalf of the employee by the employer• Amounts for electricity, water, telephone and other utility costs paid by the employer on behalf of the

employee are taxable to the employee in full as employment income.

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 6

Navigation........... Budget Highlights

.......... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

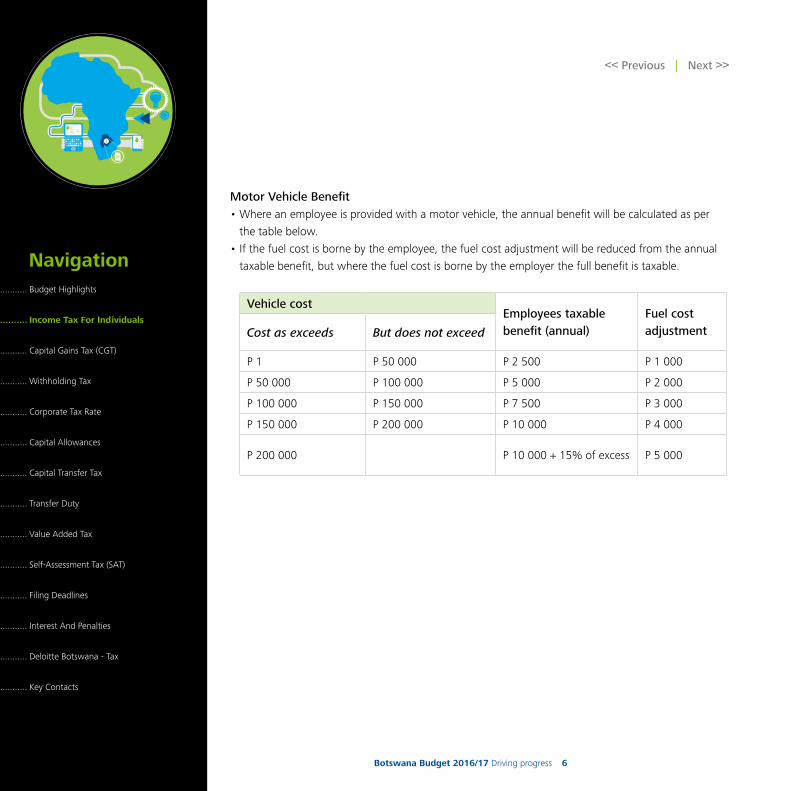

Motor Vehicle Benefit• Where an employee is provided with a motor vehicle, the annual benefit will be calculated as per

the table below.

• If the fuel cost is borne by the employee, the fuel cost adjustment will be reduced from the annual

taxable benefit, but where the fuel cost is borne by the employer the full benefit is taxable.

Vehicle costEmployees taxable benefit (annual)

Fuel cost adjustmentCost as exceeds But does not exceed

P 1 P 50 000 P 2 500 P 1 000

P 50 000 P 100 000 P 5 000 P 2 000

P 100 000 P 150 000 P 7 500 P 3 000

P 150 000 P 200 000 P 10 000 P 4 000

P 200 000 P 10 000 + 15% of excess P 5 000

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 7

Navigation........... Budget Highlights

........... Income Tax For Individuals

.......... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

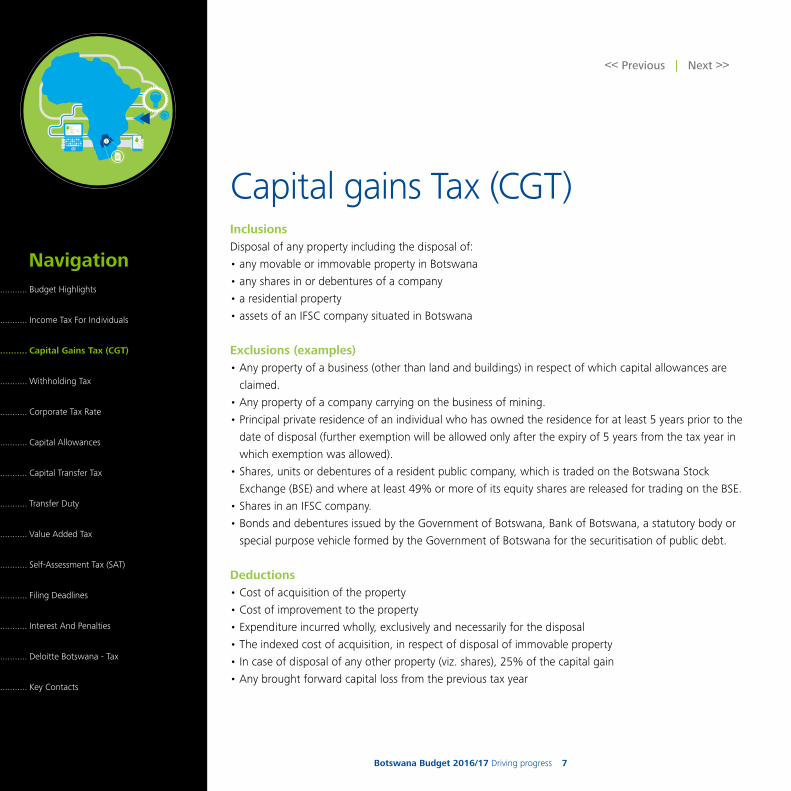

Capital gains Tax (CGT)InclusionsDisposal of any property including the disposal of:

• any movable or immovable property in Botswana

• any shares in or debentures of a company

• a residential property

• assets of an IFSC company situated in Botswana

Exclusions (examples)• Any property of a business (other than land and buildings) in respect of which capital allowances are

claimed.

• Any property of a company carrying on the business of mining.

• Principal private residence of an individual who has owned the residence for at least 5 years prior to the

date of disposal (further exemption will be allowed only after the expiry of 5 years from the tax year in

which exemption was allowed).

• Shares, units or debentures of a resident public company, which is traded on the Botswana Stock

Exchange (BSE) and where at least 49% or more of its equity shares are released for trading on the BSE.

• Shares in an IFSC company.

• Bonds and debentures issued by the Government of Botswana, Bank of Botswana, a statutory body or

special purpose vehicle formed by the Government of Botswana for the securitisation of public debt.

Deductions• Cost of acquisition of the property

• Cost of improvement to the property

• Expenditure incurred wholly, exclusively and necessarily for the disposal

• The indexed cost of acquisition, in respect of disposal of immovable property

• In case of disposal of any other property (viz. shares), 25% of the capital gain

• Any brought forward capital loss from the previous tax year

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 8

Navigation........... Budget Highlights

........... Income Tax For Individuals

.......... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

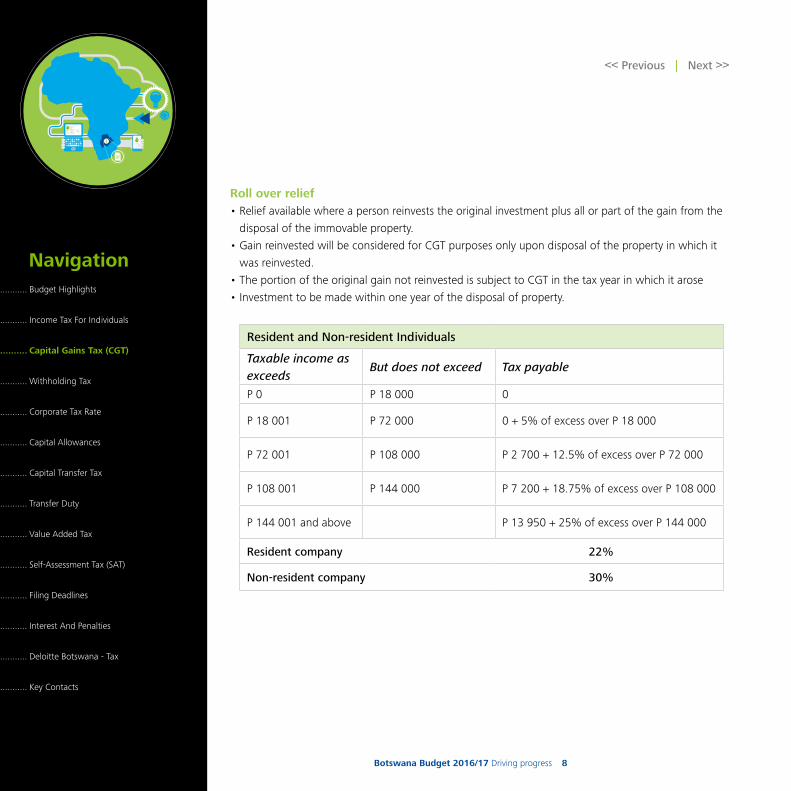

Roll over relief• Relief available where a person reinvests the original investment plus all or part of the gain from the

disposal of the immovable property.

• Gain reinvested will be considered for CGT purposes only upon disposal of the property in which it

was reinvested.

• The portion of the original gain not reinvested is subject to CGT in the tax year in which it arose

• Investment to be made within one year of the disposal of property.

Resident and Non-resident Individuals

Taxable income as exceeds

But does not exceed Tax payable

P 0 P 18 000 0

P 18 001 P 72 000 0 + 5% of excess over P 18 000

P 72 001 P 108 000 P 2 700 + 12.5% of excess over P 72 000

P 108 001 P 144 000 P 7 200 + 18.75% of excess over P 108 000

P 144 001 and above P 13 950 + 25% of excess over P 144 000

Resident company 22%

Non-resident company 30%

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 9

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

.......... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

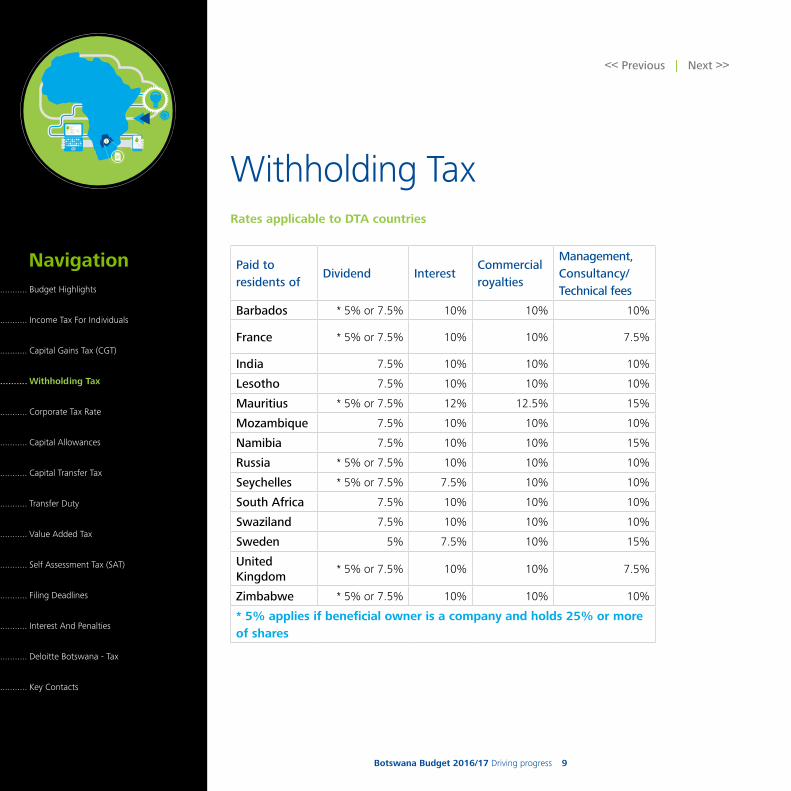

Withholding TaxRates applicable to DTA countries

Paid to residents of

Dividend InterestCommercial royalties

Management,Consultancy/ Technical fees

Barbados * 5% or 7.5% 10% 10% 10%

France * 5% or 7.5% 10% 10% 7.5%

India 7.5% 10% 10% 10%

Lesotho 7.5% 10% 10% 10%

Mauritius * 5% or 7.5% 12% 12.5% 15%

Mozambique 7.5% 10% 10% 10%

Namibia 7.5% 10% 10% 15%

Russia * 5% or 7.5% 10% 10% 10%

Seychelles * 5% or 7.5% 7.5% 10% 10%

South Africa 7.5% 10% 10% 10%

Swaziland 7.5% 10% 10% 10%

Sweden 5% 7.5% 10% 15%

United Kingdom

* 5% or 7.5% 10% 10% 7.5%

Zimbabwe * 5% or 7.5% 10% 10% 10%

* 5% applies if beneficial owner is a company and holds 25% or more of shares

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 10

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

.......... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

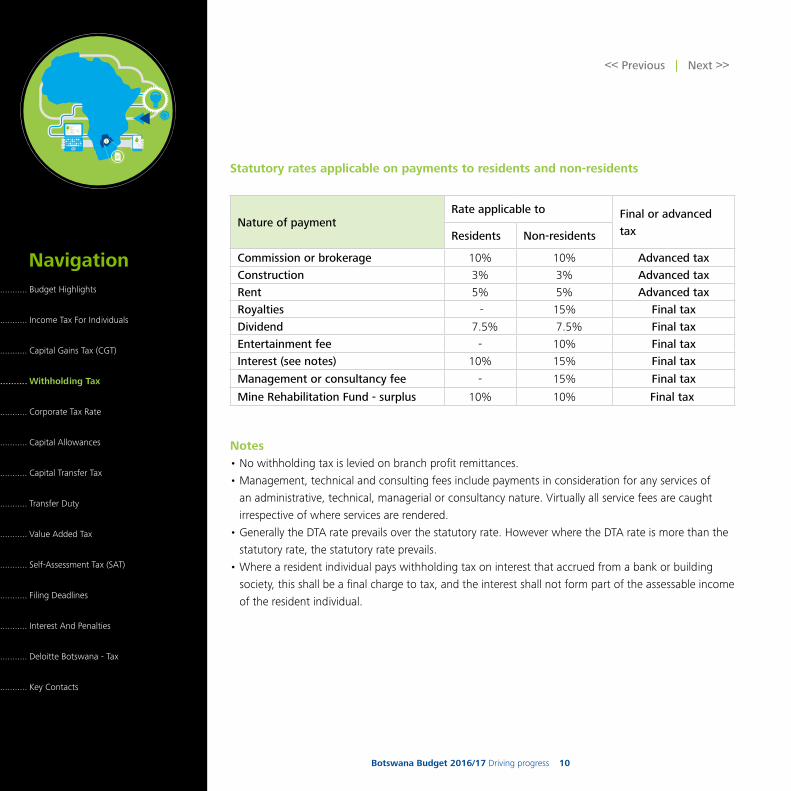

Statutory rates applicable on payments to residents and non-residents

Nature of paymentRate applicable to Final or advanced

taxResidents Non-residents

Commission or brokerage 10% 10% Advanced tax

Construction 3% 3% Advanced tax

Rent 5% 5% Advanced tax

Royalties - 15% Final tax

Dividend 7.5% 7.5% Final tax

Entertainment fee - 10% Final tax

Interest (see notes) 10% 15% Final tax

Management or consultancy fee - 15% Final tax

Mine Rehabilitation Fund - surplus 10% 10% Final tax

Notes• No withholding tax is levied on branch profit remittances.

• Management, technical and consulting fees include payments in consideration for any services of

an administrative, technical, managerial or consultancy nature. Virtually all service fees are caught

irrespective of where services are rendered.

• Generally the DTA rate prevails over the statutory rate. However where the DTA rate is more than the

statutory rate, the statutory rate prevails.

• Where a resident individual pays withholding tax on interest that accrued from a bank or building

society, this shall be a final charge to tax, and the interest shall not form part of the assessable income

of the resident individual.

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 11

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

.......... Corporate Tax Rate

.......... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

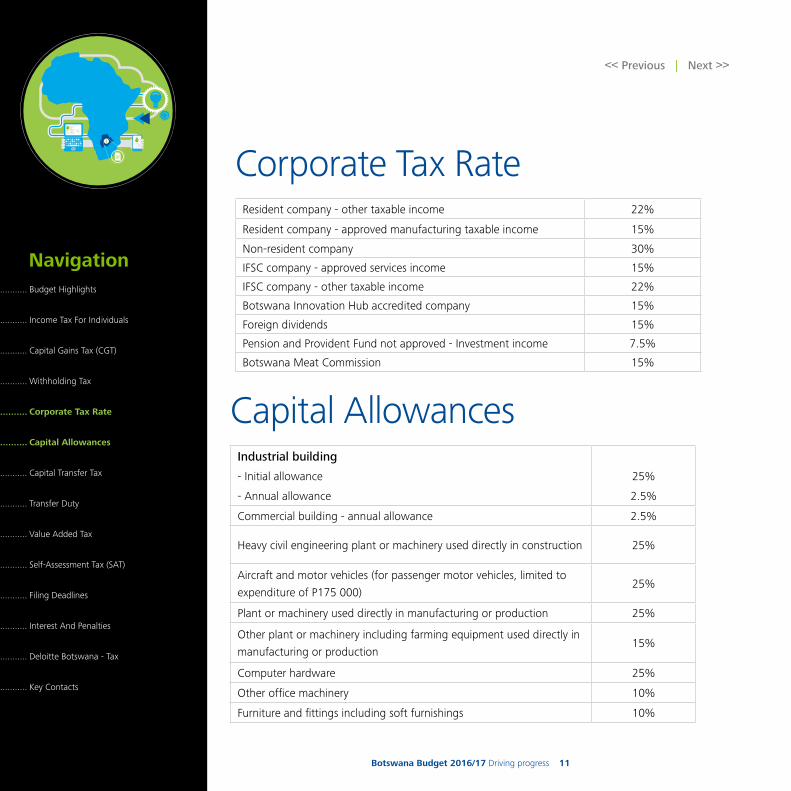

Corporate Tax RateResident company - other taxable income 22%

Resident company - approved manufacturing taxable income 15%

Non-resident company 30%

IFSC company - approved services income 15%

IFSC company - other taxable income 22%

Botswana Innovation Hub accredited company 15%

Foreign dividends 15%

Pension and Provident Fund not approved - Investment income 7.5%

Botswana Meat Commission 15%

Capital AllowancesIndustrial building

- Initial allowance 25%

- Annual allowance 2.5%

Commercial building - annual allowance 2.5%

Heavy civil engineering plant or machinery used directly in construction 25%

Aircraft and motor vehicles (for passenger motor vehicles, limited to

expenditure of P175 000)25%

Plant or machinery used directly in manufacturing or production 25%

Other plant or machinery including farming equipment used directly in

manufacturing or production15%

Computer hardware 25%

Other office machinery 10%

Furniture and fittings including soft furnishings 10%

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 12

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

.......... Capital Transfer Tax

.......... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

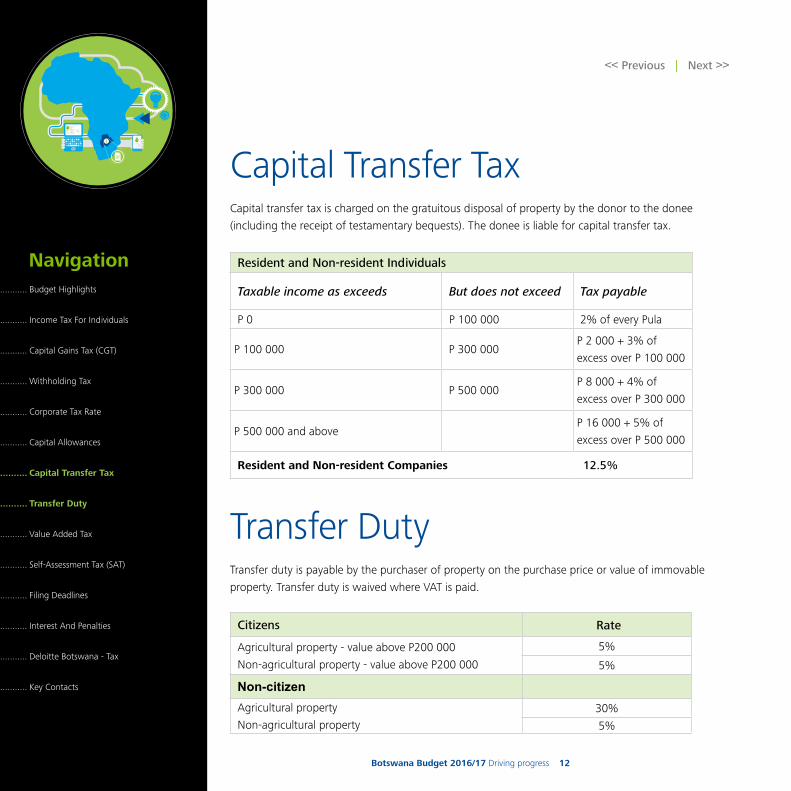

Capital Transfer TaxCapital transfer tax is charged on the gratuitous disposal of property by the donor to the donee

(including the receipt of testamentary bequests). The donee is liable for capital transfer tax.

Resident and Non-resident Individuals

Taxable income as exceeds But does not exceed Tax payable

P 0 P 100 000 2% of every Pula

P 100 000 P 300 000P 2 000 + 3% of

excess over P 100 000

P 300 000 P 500 000P 8 000 + 4% of

excess over P 300 000

P 500 000 and above P 16 000 + 5% of

excess over P 500 000

Resident and Non-resident Companies 12.5%

Transfer DutyTransfer duty is payable by the purchaser of property on the purchase price or value of immovable

property. Transfer duty is waived where VAT is paid.

Citizens Rate

Agricultural property - value above P200 000

Non-agricultural property - value above P200 000

5%

5%

Non-citizen Agricultural property

Non-agricultural property30%

5%

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 13

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

.......... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

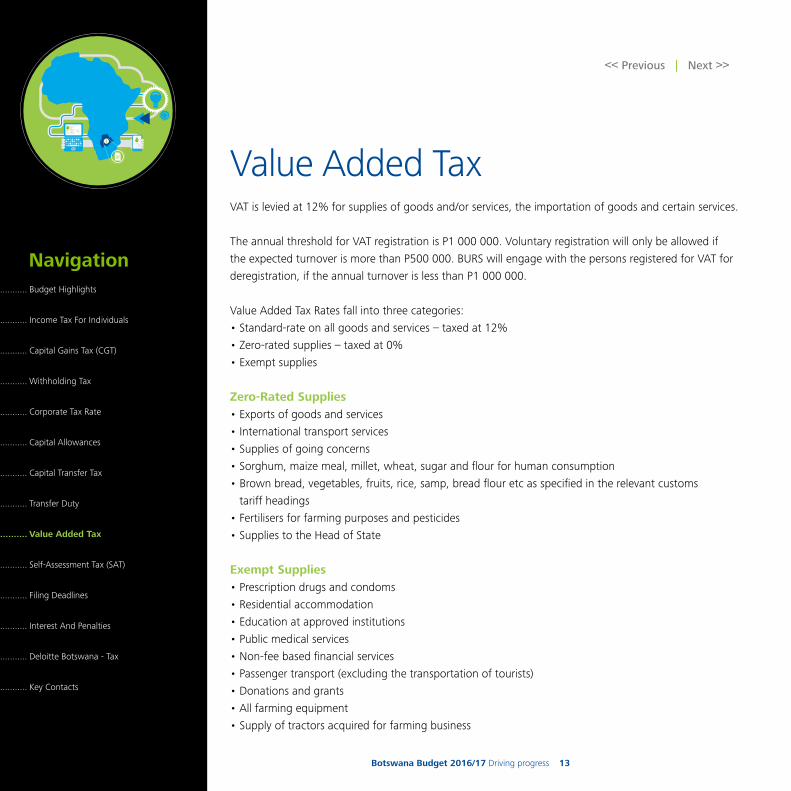

Value Added TaxVAT is levied at 12% for supplies of goods and/or services, the importation of goods and certain services.

The annual threshold for VAT registration is P1 000 000. Voluntary registration will only be allowed if

the expected turnover is more than P500 000. BURS will engage with the persons registered for VAT for

deregistration, if the annual turnover is less than P1 000 000.

Value Added Tax Rates fall into three categories:

• Standard-rate on all goods and services – taxed at 12%

• Zero-rated supplies – taxed at 0%

• Exempt supplies

Zero-Rated Supplies• Exports of goods and services

• International transport services

• Supplies of going concerns

• Sorghum, maize meal, millet, wheat, sugar and flour for human consumption

• Brown bread, vegetables, fruits, rice, samp, bread flour etc as specified in the relevant customs

tariff headings

• Fertilisers for farming purposes and pesticides

• Supplies to the Head of State

Exempt Supplies• Prescription drugs and condoms

• Residential accommodation

• Education at approved institutions

• Public medical services

• Non-fee based financial services

• Passenger transport (excluding the transportation of tourists)

• Donations and grants

• All farming equipment

• Supply of tractors acquired for farming business

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 14

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

.......... Self-Assessment Tax (SAT)

.......... Filing Deadlines

........... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

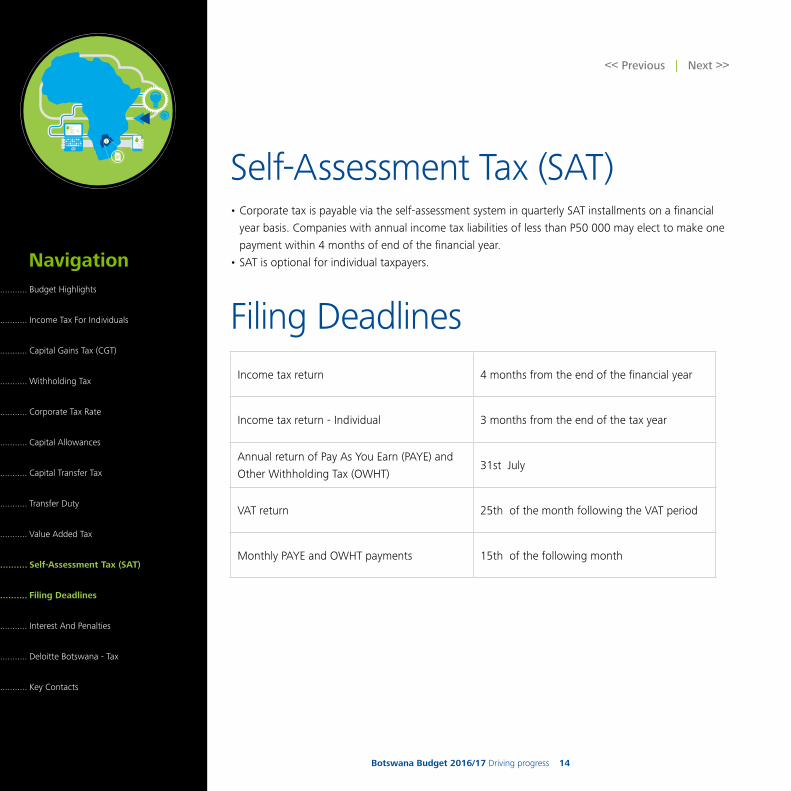

Self-Assessment Tax (SAT) • Corporate tax is payable via the self-assessment system in quarterly SAT installments on a financial

year basis. Companies with annual income tax liabilities of less than P50 000 may elect to make one

payment within 4 months of end of the financial year.

• SAT is optional for individual taxpayers.

Filing Deadlines

Income tax return 4 months from the end of the financial year

Income tax return - Individual 3 months from the end of the tax year

Annual return of Pay As You Earn (PAYE) and

Other Withholding Tax (OWHT)31st July

VAT return 25th of the month following the VAT period

Monthly PAYE and OWHT payments 15th of the following month

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 15

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

.......... Interest And Penalties

........... Deloitte Botswana - Tax

........... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

SPENDSTATS

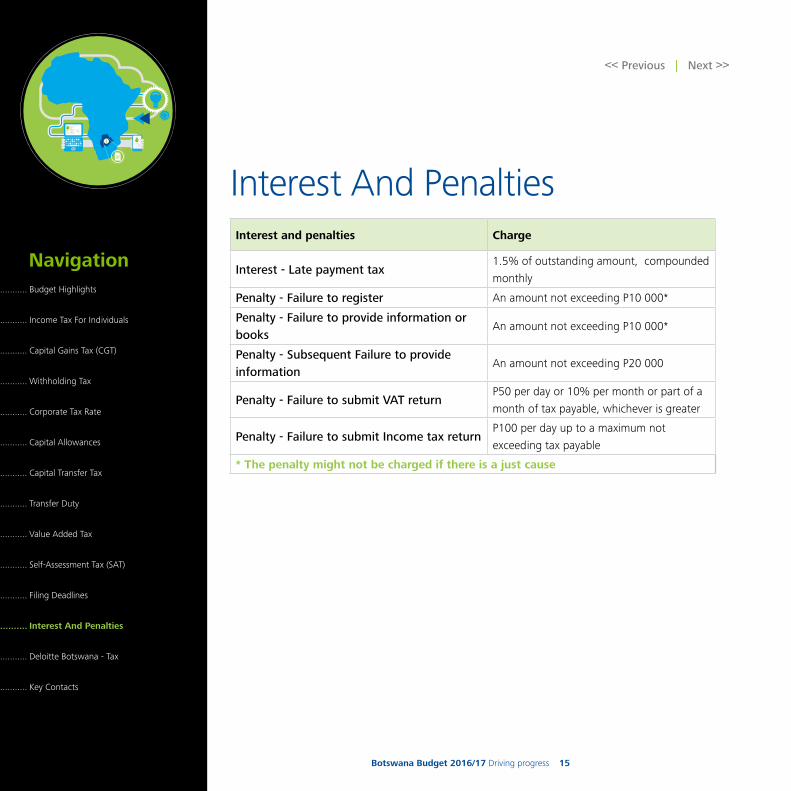

Interest And PenaltiesInterest and penalties Charge

Interest - Late payment tax 1.5% of outstanding amount, compounded

monthly

Penalty - Failure to register An amount not exceeding P10 000*

Penalty - Failure to provide information or books

An amount not exceeding P10 000*

Penalty - Subsequent Failure to provide information

An amount not exceeding P20 000

Penalty - Failure to submit VAT returnP50 per day or 10% per month or part of a

month of tax payable, whichever is greater

Penalty - Failure to submit Income tax returnP100 per day up to a maximum not

exceeding tax payable

* The penalty might not be charged if there is a just cause

<< Previous | Next >>

Botswana Budget 2016/17 Driving progress 16

Navigation........... Budget Highlights

........... Income Tax For Individuals

........... Capital Gains Tax (CGT)

........... Withholding Tax

........... Corporate Tax Rate

........... Capital Allowances

........... Capital Transfer Tax

........... Transfer Duty

........... Value Added Tax

........... Self-Assessment Tax (SAT)

........... Filing Deadlines

........... Interest And Penalties

.......... Deloitte Botswana - Tax

.......... Key Contacts

Detai l One

CONTEXT - 2014/2015

A short descriptio nwith additiona ldetail

Detai l OneA short descriptio nwith additiona ldetail

Detai l OneA short descriptio n

Detai l OneA short descriptio n

301511

8

64 DETAIL UNITS

477 DETAIL UNITS

19 DETAIL UNITS

568UNITS

6 DETAIL UNITS

50bn2015

70bn2016

25bn2014

39%26%

57%68%75%

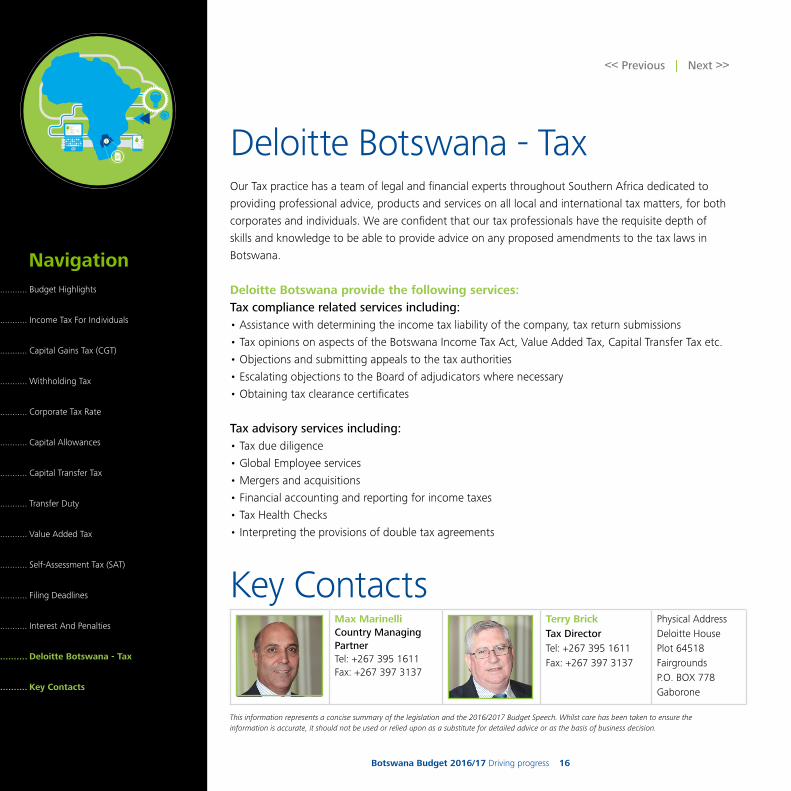

SPENDSTATS Deloitte Botswana - Tax

Our Tax practice has a team of legal and financial experts throughout Southern Africa dedicated to

providing professional advice, products and services on all local and international tax matters, for both

corporates and individuals. We are confident that our tax professionals have the requisite depth of

skills and knowledge to be able to provide advice on any proposed amendments to the tax laws in

Botswana.

Deloitte Botswana provide the following services:Tax compliance related services including:• Assistance with determining the income tax liability of the company, tax return submissions

• Tax opinions on aspects of the Botswana Income Tax Act, Value Added Tax, Capital Transfer Tax etc.

• Objections and submitting appeals to the tax authorities

• Escalating objections to the Board of adjudicators where necessary

• Obtaining tax clearance certificates

Tax advisory services including:• Tax due diligence

• Global Employee services

• Mergers and acquisitions

• Financial accounting and reporting for income taxes

• Tax Health Checks

• Interpreting the provisions of double tax agreements

Max MarinelliCountry Managing PartnerTel: +267 395 1611Fax: +267 397 3137

Terry BrickTax DirectorTel: +267 395 1611Fax: +267 397 3137

Physical AddressDeloitte HousePlot 64518FairgroundsP.O. BOX 778Gaborone

This information represents a concise summary of the legislation and the 2016/2017 Budget Speech. Whilst care has been taken to ensure the information is accurate, it should not be used or relied upon as a substitute for detailed advice or as the basis of business decision.

<< Previous | Next >>

Key Contacts

Botswana Budget 2016/17 Driving progress 17

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (DTTL), its network of member firms and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms, and their related entities (collectively, the “Deloitte network”). None of the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2016 Deloitte & Touche. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Designed and produced by Creative Services at Deloitte, Johannesburg. (811079/vee)

<< Previous