Embed Size (px)

Citation preview

ANALYSIS REGULATION COUNTRY SNAPSHOTSWhat long-term damage

did the Visa crash cause to its brand, and the industry?

Australian Royal Commission focuses on credit card decisioning

Need-to-know data on card payments in Portugal,

Finland and Kenya

BOOM OR BUST?

CRYPTO CARDS AIM TO BREAK THROUGH TO THE MAINSTREAM

Issue 556 / june 2018w w w. c a r d s i n t e r n at i o n a l . c o m

CI June 2018 556.indd 1 15/06/2018 14:32:51

2 | June 2018 | Cards International

contents

NEWS

05 / EDITOR’S LETTER06 / DIGEST• Wells Fargo bans credit card

cryptocurrency purchases• Mastercard seeks patent for

blockchain-based verification tech• Chase and Starbucks launch

rewards-based Visa prepaid card• New coalition to enhance US card

payment security• Mastercard to make contactless

standard in five years• Mastercard, Diebold to trial digital

ATM transaction• Mastercard announces solutions for

Open Banking transformation• Visa introduces programme for

European fintech startups• YouGov poll reveals UK consumers

seek better protection and control• Monobank introduces credit card

platform in Norway• Centenary Bank launches new Visa

debit card• Precise Biometrics launches smart

card algorithm

11

this month

Editor:Douglas Blakey

+44 (0)20 7406 [email protected]

Senior Reporter: Patrick Brusnahan

+44 (0)20 7406 [email protected]

Junior Reporter:Briony Richter

+44 (0)20 7406 [email protected]

Group Editorial Director: Ana Gyorkos

+44 (0)20 7406 [email protected]

Sub-editor:Nick Midgley

+44 (0)161 359 [email protected]

Publishing Assistant: Mishelle Thurai

+44 (0)20 7406 6592 [email protected]

Director of Events:Ray Giddings

+44 (0)20 3096 [email protected]

Head of Subscriptions: Alex Aubrey

+44 (0)20 3096 [email protected]

Sales Executive:Jamie Baker

+44 203 096 [email protected]

Financial News Publishing, 2012. Registered in the UK No 6931627. ISSN 0956-5558Unauthorised photocopying is illegal. The contents of this publication, either in whole or part, may not be reproduced, stored in a data retrieval system or transmitted by any form or means, electronic, mechanical,

photocopying, recording or otherwise, without the prior permission of the publishers.

For more information on Verdict, visit our website at www.verdict.co.uk.As a subscriber you are automatically entitled to online access to Cards International.

For more information, please telephone +44 (0)20 7406 6536 or email [email protected].

London office: John Carpenter House, John Carpenter Street, London, EC4Y 0AN

Asia office: 1 Finlayson Green, #09-01, Singapore 049246 Tel: +65 6383 4688, Fax: +65 6383 5433 Email: [email protected]

Customer Services: +44 (0)20 3096 2603 or +44 (0)20 3096 2636, [email protected]

CRYPTO CARDSCOVER STORY

follow CI on twitter@Payments_News

07

CI June 2018 556.indd 2 15/06/2018 14:33:06

www.cardsinternational.com | 3

contents

20

June 2018

14 / AUSTRALIAThe Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry in Australia has attracted publicity for all the wrong reasons, and as Tom Ravlic reports, the cards sector is not immune

s to talk about cracking China, disrupting SWIFT, and leveraging WeChaCOUNTRY SNAPSHOTS16 / PORTUGALThe Portuguese banking sector was deeply affected by the economic crisis, but consumer preference for debt-free payments and prudent spending has resulted in growing debit card transaction volumes and values

18 / FINLANDFrequency of card use is higher in Finland than in other mature European markets such as the UK and Germany. Debit cards are the most popular card type, and are used almost six times more than pay-later cards

20 / KENYAKenya’s payment card market is still very much in a developmental stage. The East African nation recorded a penetration rate of 30 cards per 100 individuals in 2017, and just 16.0 transactions per card per year

16

REGULATION

INDUSTRY INSIGHT22 / CARDTRONICSCommentators have used the 20th anniversary of online banking to declare another banking revolution: one of mobile apps, artificial intelligence and Open Banking, writes Cardtronics director Duncan Faithfull

10 / VISA CRASHOn 1 June 2018, Visa Europe suffered an outage that affected thousands – if not millions – of consumers. While the system was back running by the end of the day, what damage did it do? Patrick Brusnahan writes

ANALYSIS

11 / CRYPTO CARDSA growing number of crypto lenders are looking to disrupt the traditional card sector. Ivan Castano reports on their prospects, and asks whether they really can give Visa and Mastercard a run for their money

FEATURE

22

CI June 2018 556.indd 3 15/06/2018 14:33:14

Page 1

Key Issues :

∤ Economic trends to 2020. Wealth management industry performance

∤ With technology playing an increasingly significant role in service delivery what benefit does institutional size confer?

∤ What are the implications for service, delivery and product distribution in the age of the digital wealth manager?

∤ How is technology enabling faster, more cost effective on-boarding, KYC and compliance reporting among wealth management organisations?

∤ How should Switzerland’s private banking industry define itself in the age of digital technology and intensifying competition?

∤ What channels are working for attracting, retaining and managing an increasingly diverse customer universe?

∤ What’s the connection between distribution and profitability? How are Swiss private banks adapting to the challenge of tight margins and higher costs?

∤ What does the country need to do to stay ahead?

SHAPE THE FUTUREOF PRIVATE BANKING

HEAR ∤ NETWORK ∤ DISCOVER ∤ CELEBRATE

Private Banking & Wealth Management: Switzerland 201812th December 2018 ∤ Marriott, Zurich

Private Banking & Wealth Management: Switzerland 2018 Conference and Awards leverages the expertise across the Verdict research and publishing portfolio, including Private Banker International, Wealth Insight

and Wealth Intelligence Centre. The event is an opportunity to share ideas, discover trends and network with peers across the wealth industry.

For more details please contact:

Vicki Greenwood on [email protected] or call +44 (0) 20 3096 2580

Supported byGold Partner: Silver Partner: Bronze Partners: Exhibitor:

Untitled-2 1 15/06/2018 15:15

www.cardsinternational.com | 5

editor’s letter

RBC gunning for TD

Get in touch with the editor at: [email protected]

Douglas Blakey, Editor

By almost every business metric – mortgages, consumer lending, mutual funds, business lending and deposits – Royal Bank of Canada (RBC) ranks

in first place in its domestic market – but not in the credit cards sector.

RBC, with a 27.3% market share, is now gunning for market leader Toronto Dominion (TD). This will be worth watching: RBC CEO Dave McKay is not in the habit of missing targets.

TD Bank captured the number one spot back in 2013, overtaking long-term credit card market share leader CIBC. At an investor day in Toronto on 13 June, McKay, outlined plans to grow its Canadian customer numbers by 2.5 million in the next five years, with credit card growth very much in his sights. RBC will spend C$3.2bn ($2.5bn) on technology this year, including investment on digital marketing, AI and social media.

RBC, WestJet launch AmpliRBC is also forming a next-generation loyalty platform, dubbed Ampli, with airline Westjet, with the aim of delivering unparalleled value to consumers through amplified earning power on a simple and convenient digital solution.

Open to all Canadians, Ampli will provide members with merchant offers, flexible rewards and exclusive bonuses. In addition, members who spend on RBC cards and fly with WestJet will receive augmented rewards.

McKay said:“The Canadian loyalty landscape is ready for disruption, and Ampli is a fundamental shift in the business model. We are bringing together top Canadian brands to help them reach consumers more efficiently and effectively. We will also provide consumers with opportunities to earn rewards and save money like never before.”

Ampli will go head to head with the Aeroplan rewards programme. Last year, WestJet rival Air Canada announced that it would split with Aeroplan and start its own rewards programme. Visa provides Aeroplan-branded credit cards issued by TD and CIBC; American Express Canada also partners with Air Canada as a credit card partner in the Aeroplan rewards programme. RBC became the first major issuer in Canada to offer both Visa and Mastercard credit cards when it teamed up with WestJet to launch a travel rewards Mastercard co-branded with WestJet.

Almost 90% of Canadian adults hold at least one credit card; the average number of credit cards per Canadian adult is about 2.2 cards, with reward programme benefits a key issue in the cards battleground. Canadians belong to an average of around 11 loyalty programmes, with almost 80% of Canadian adults holding a credit card offering rewards.

McKay said RBC’s decision 20 years ago not to outsource its rewards programme had paid off handsomely. RBC Rewards has five million members; last year RBC Rewards points redemptions grew by 7%, and according to McKay, RBC Rewards will deliver more points than any rival offering by 2019.

RBC Rewards members are 1.7 times more digitally engaged than non-members, hold 1.5 times the average number of RBC products per person and are twice as profitable as non-members.

Digital customers up 8% to 6.5 millionOverall, RBC digital customer numbers grew by 8% last year to 6.5 million, and its digital adoption rate of 49% of all customers is up by six percentage points since 2015.

Digital sales as a percentage of all sales grew also rose by six percentage points in the same period, from 24% to 30%, and McKay has targeted 50% of sales by digital by 2021. Currently, 35% of all credit card sales are digital – a figure RBC is also committed to growing.

A renewed focus on digital marketing is paying off in the credit card sector. The rate of growth of approved new-to-RBC credit card applications is on track to rise threefold in the 12 months to the end of the first half of 2018 compared to the previous 12-month period.

RBC estimates that its current credit card customer acquisition rate is between two and three times the rate of its peers. RBC is also attracting more premium customers. The average FICO score of new customers acquired is a healthy 780, while around 35% of new Visa Infinite RBC Avion credit cardholders are new customers to RBC, up 15 percentage points from 2015.

CIBC held the top slot by market share for around 10 years until 2013; TD has ranked first for the past five years. This one will run and run. <

CI June 2018 556.indd 5 15/06/2018 14:33:16

News | Digest

news digest

6 | June 2018 | Cards International

Mastercard seeks patent for blockchain-based verification tech

The US Patent and Trademark Office has published a patent application from Mastercard for a method and system using blockchain for payment card verification at the point of sale. Mastercard filed for the patent in December 2016.

The new approach is intended to address card skimming, and will involve retrieval of payment credentials from a third-party source via a publicly accessible blockchain. The two-way process will include storage

of an encrypted payment card image on a computing device using private and public keys. When a transaction is carried out using plastic or chip-enabled cards, a private key will be used by the system to decrypt the card image and cross-check the payment information.

Mastercard expects the solution for the sending and retrieval of payment credentials to and at a POS device through a third-party data source will eliminate the need to carry a payment instrument, thereby improving security.

A statement from Mastercard’s application read: “The use of a third-party data source enables an individual to transact safely without concern for their payment credentials being skimmed from their payment instrument, or without having to even carry a payment instrument entirely.

“The transaction may be conducted via the display of a machine-readable code to the point-of-sale device, which may further prevent skimming as the reading of such a code can be more easily controlled via control of the underlying display; the display can be easily shielded, and is often obscured when in a pocket or purse.” <

Wells Fargo bans credit card cryptocurrency purchasesUS banking major Wells Fargo has decided to ban the use of credits cards to buy digital currencies such as Bitcoin.

A statement from Wells Fargo read: “Cus-tomers can no longer use their Wells Fargo credit cards to purchase cryptocurrency.

“We’re doing this in order to be consistent across the Wells Fargo enterprise due to the multiple risks associated with this volatile investment. This decision is in line with the overall industry.”

The bank plans to start declining trans-actions with bank-issued credit cards on

known cryptocurrency exchanges and brokerage platforms.

A recent study by LendEDU revealed that 18% of people who bought cryptocurrency used a credit card, and 22% of then could not pay off their balance.

Wells Fargo’s move increases the number of banks that have implemented similar pol-icies this year. In February, major banks such as Lloyds Bank, JP Morgan Chase, Bank of America, Commonwealth Bank of Australia, CitiGroup, Canada’s TD Bank and Virgin Money introduced similar bans. <

Chase and Starbucks launch rewards-based Visa prepaid card

Starbucks has partnered with Chase to launch its new general-purpose reloadable prepaid product, the Starbucks Rewards Visa prepaid card.

The new card is part of the Starbucks Rewards loyalty programme, and allows users to earn Star reward points even on transactions outside Starbucks, wherever Visa is accepted. It comes with zero monthly, annual and reload fees, and cardholders will automatically receive Gold status along with other existing benefits and rewards.

Chase digital products head Jennifer Roberts said: “We want to offer Starbucks customers a flexible card that delivers more Star-earning potential in the fastest way possible. The new Starbucks Rewards Visa Prepaid Card is perfect for Starbucks fans who want a simple way to pay and get rewarded for everyday purchases.”

The new Starbucks Rewards Visa Prepaid Card is the second co-branded product by Chase and Starbucks this year, with the Starbucks Rewards Visa Card introduced in February.

Starbucks chief marketing officer Matt Ryan said: “As we continue to expand and strengthen our digital relationships with customers, we want to make sure we’re providing choices that are both rewarding and meet their preferences in how they engage with us.”

Ryan added: “This reloadable Visa Prepaid card is a unique and modern option that gives customers one more way to earn more Stars and rewards through everyday spend, in a way they haven’t been able to before.” <

CI June 2018 556.indd 6 15/06/2018 14:33:22

News | digest

www.cardsinternational.com | 7

Mastercard to make contactless standard in five years

Mastercard has revealed plans to make contactless payments standard by 2023 in Europe, the Middle East, Asia-Pacific, Latin America and Africa, to ensure greater payment consistency.

The initiative is expected to enable card users to benefit from digital advances that offer improved security and convenience.

The company said it will begin multiple card and terminal upgrades in global regions from this year in order to deliver

contactless card payment technology to more consumers.

Use of contactless payments, which use dynamic EMV-grade authentication to prevent fraud, is gradually increasing worldwide. The standard is currently active in more than eight million locations in 111 countries.

Mastercard’s plans mean all new acceptance terminals in Europe, Latin America, the Middle East, Africa and Asia-Pacific will have EMV chip and contactless technology enabled from October this year. All new cards issued in these regions from April 2019 will carry the corresponding functionality.

Mastercard aims to make all merchant terminals EMV chip and contactless-enabled by April 2023.

Mastercard chief security solutions officer Ajay Bhalla said: “Our vision is a world where everyone can simply and safely tap their card or device when paying in a store, and quickly be on their way.

“This marks a significant step towards greater consistency, security and speed for everyday payments while laying the groundwork for future innovation.” <

Mastercard, Diebold to trial digital ATM transactions

Mastercard has partnered with financial services provider Diebold Nixdorf to trial two new ATM products to enable digital cash transactions.

Integration of the new Mastercard Cash Pick-Up and Cardless ATM, which combines Mastercard services with Diebold’s ATMs and middleware, will be assessed during the projects.

The Mastercard Cash Pick-Up service aims to allow quick and secure delivery of cash by banks even to customers who do not have an account or card. The solution is designed to serve underbanked consumers, and enable financial institutions and ATM deployers to increase transaction volumes and revenues.

The Cardless ATM service uses a mobile banking app to enable cash withdrawals from the nearest available ATM, with users authenticating the transactions.

Mastercard’s senior vice-president of ATM product management, Daniel Goodman, said: “As a technology company, we are always considering what the future can bring, and today we have a great opportunity with Diebold Nixdorf to define the next wave of digital products to the ATM channel. By bringing together the Mastercard network and Diebold Nixdorf’s large global scale, we can help move the ATM industry towards a globally scalable standard for driving digital innovation in the ATM channel.”

Diebold Nixdorf’s senior vice-president of software, Alan Kerr, added: “This partnership with Mastercard is another way we are continuing to securely bridge the digital and physical worlds of cash by innovating the ATM experience for consumers through our Vynamic suite of software solutions.

“Many of our customers are looking to retain consumers and drive incremental transactions to their self-service channels, and this partnership with Mastercard delivers on both of these fronts.” <

New coalition to enhance US card payment securityRetail groups and ATM networks have formed a new coalition aimed at improving electronic payments security in the US.

The Secure Payments Partnership (SPP) will promote card and technology payment security, address fraud, and work on devising improvements.

Founding members of the SPP include the Food Marketing Institute, the National Retail Federation, the National Association of Convenience Stores, the National Grocers Association, First Data’s Star Network and Shazam. The coalition’s primary goal is to ensure fast and secure payments with new and advanced technology.

According to the SPP, Visa and Master-card currently control security standards in the US without consideration of expertise from competing card networks, merchants, consumers and financial institutions. The coalition members believe all involved

organisations need to work jointly to achieve successful payment security, enhance trans-parency and reduce fraud.

The National Retail Federation’s senior vice-president and general counsel, Steph-anie Martz, said: “The payments system has to keep pace with rapidly evolving technology and the needs of consumers and commerce. The US payments infrastructure should be the strongest, most innovative and most secure in the world, but we won’t get there unless we change the way we make security decisions.”

The alliance will mainly work towards meeting consumer expectations in terms of security, convenience and flexibility for payment options.

In addition, the SPP will prioritise user authentication, open standards setting, innovation of payment security and network routing competition. <

CI June 2018 556.indd 7 15/06/2018 14:33:25

News | Digest

8 | June 2018 | Cards International

Visa introduces fast-track programme for European fintech startupsVisa has announced plans for two new support programmes for European fintechs engaged in the creation of new digital payment solutions.

The new fintech fast-track programme will provide early-stage startups access to Visa’s capabilities across its global network, to enable them to build their own ideas.

Set to begin in July 2018, the fast-track initiative allows onboarding onto Visa’s global network within four weeks, including reduced charges.

Visa said it will work with providers to fund startups to join the programme, with an aim of delivering “new and innovative digital commerce experiences to both consumers and merchants”.

Visa CEO for Europe Charlotte Hogg commented: “At Visa we are open for all players to take advantage of the reach, capabilities and security of our global

network to grow their businesses.“Our commitment is to be the most

responsive and supportive network for both emerging payment players, and our existing clients and partners.”

Initially, the company plans to collaborate with payments and processing platform provider Contis, and will focus on UK-based start-up businesses. The programme will later be extended to other European and international markets.

Visa has also launched a $100m venture fund to support startups working on innovations in Open Banking, and using technology to develop new security and commerce experiences.

Visa has already invested in Klarna, solarisBank and Payworks in Europe. Platforms and fintechs such as Contis, Evry, Jaja, Revolut and Wirecard have said that they intend to work with Visa. <

Mastercard announces solutions to underpin Open Banking transformationMastercard is to develop a new suite of services designed to build trust in the new Open Banking ecosystem among consumers, banks, retailers and third parties, as well as simplifying and streamlining their interac-tions with each other.

With the opening up of financial data, trusted third parties have access to infor-mation held by banks. This not only enables third parties and banking incumbents to offer enhanced and individualised products and services, but it will also allow them to initiate payments on behalf of the business or consumer in some cases.

Mastercard’s new services will include:• A pan-European directory of third-par-

ty providers to help banks ensure that parties seeking access to a customer’s account are legitimate;

• A fraud-monitoring service based on Mastercard’s safety and security solutions, to enable banks to better assess the risk associated with a given third party;

• A dispute-resolution mechanism with a clear set of rules and a communications platform, leveraging Mastercard’s exper-tise of handling disputes, and

• A connectivity hub that will help third parties to establish and maintain commu-nication with banks.

“We believe that these services address sig-nificant obstacles to the creation of a vibrant and successful open banking ecosystem,” said Jason Lane, Mastercard’s executive vice-president, market development Europe.

“We recognise that trust challenges exist on both sides – third parties need to be able to access the data and infrastructure controlled by banks, and at the same time banks need confidence that the third parties requesting account access are legitimate.”

Lane continued: “We want our solutions to give banks and third parties peace of mind, so that they can focus their time and efforts

on where they add most value – creating innovative user experiences.”

“The challenge to create trust is not the only one – we are already working on improving end-user experiences in the Open Banking environment, relating to both payments and information access, and look forward to rolling those out as the services and ecosystem, evolves,” he added

Mastercard’s new services will be launched first during a pilot phase in early 2019, with the UK and Poland being priority markets, before being rolled out across Europe later in the year. <

CI June 2018 556.indd 8 15/06/2018 14:33:30

www.cardsinternational.com | 9

News | Digest

YouGov poll reveals UK consumers seek better protection and controlUK consumers want to see more efficient, secure and real-time interaction with banks, according to a study from YouGov on behalf of Ondot.

The results revealed that online security is the major concern among UK consumers, with 60% wanting ‘peace of mind’ when using cards online.

The survey also indicated that consumers want much more proactive roles in manag-ing their money.

Key findings from the survey included:• 50% complained about talking to banks’

call centres;• 50% objected to transactions being

stopped without notification of the reason, and

• 30% resented having to wait for blocked cards to be replaced.

Consumers also indicated a widespread desire for greater control over their debit and credit cards, and 30% of those surveyed wanted a mobile app that could control loca-tion parameters, such as limiting card use at a holiday destination.

Location control can also allow the user to decide a card’s activity range within a city, a larger geographical area, or a specified radius around the phone’s location. By enabling these features, transactions made will only be approved if the card is being used in a location that the user has chosen. If the card is used elsewhere, the transaction will be declined.

More than a quarter (27%) wanted trans-action alerts to be displayed in real time,

while 22% wanted the ability to set their own transaction limits.

Rachna Ahlawat, founder and EVP of Ondot Systems, stated: “The essence of the problem is the desire for personalised service. Banks respond with digital compro-mises, like automated phone services that are time-consuming and frustrating to navigate. Over half of those surveyed complained about this.”

She continued: “Customers are looking for better card controls that allow them to better personalise, manage and control how payments are made in today’s world of always-on digital commerce.

“The survey validates the need for UK consumers to benefit from what, globally, more than 3,000 banks are already offering to millions of cardholders: a mobile-based payment card control app.” <

Monobank introduces credit card platform in NorwayMonobank, a digital bank based in Norway, has introduced a new credit card platform comprising a physical card and mobile payment application.

Through the combination of the Monocard and Mono Pay app, the company aims to simplify banking and shopping for customers, and enable tracking of purchases. Monobank plans to work with partners to distribute the new credit card and app solution to customers.

The digital bank also announced plans to partner with Scandinavian airline Widerøe to launch the Widerøe credit card in September 2018. The card will utilise the bank’s new platform.

Monobank CEO Bent Gjendem said: “People want safe and easy-to-use banking and shopping solutions to improve their digital experiences. Our credit card platform with the Monocard and Mono Pay app provides that by combining the traditional credit card with a mobile payment app.

“It also makes it easier for users to keep track of their purchases and private economy. We can already see that our customers appreciate the solution.”

Established in 2015, Monobank focuses on providing new fintech solutions for loans, deposits and credit cards in order to enhance the customer experience. <

Precise Biometrics launches smart card algorithmFingerprint technology provider Precise Biometrics has launched a new algorithm solution, Precise BioMatch Card, to match fingerprints in smart cards.

The BioMatch Card can identify fingerprints in ‘constrained’ computing settings, including Secure Elements (SEs).

SEs are processor chips embedded into biometric smart cards to offer protection against fraud. The Precise BioMatch solution can support fingerprint sensors with an area down to 30mm square.

Previously, the card was a part of Precise BioMatch Embedded and has now been released as a stand-alone solution into the smart card market.

Torgny Hellström, executive chair of Precise Biometrics’s, board said: “Smart cards are the next growth area for fingerprint technology. In payment cards alone, there are over three billion cards issued globally every year.

“As a frontrunner in the development of biometric payment cards, it´s important for us to provide Precise BioMatch Card that specifically addresses this market.” <

Centenary Bank launches new Visa debit cardUganda-based Centenary Bank has introduced the new CenteVisa debit card featuring chip-and-PIN technology.

The CenteVisa card can be used globally at all merchants enabled to accept Visa transactions. Customers can exchange old ATM cards for new ones at any of the bank’s 69 branches. The bank said members need to take the new Visa cards within the next six months, after which old magnetic stripe cards will be disabled from the system.

Centenary Bank MD Fabian Kasi said: “Our electronic banking story started in 2003 when we acquired the first ATM and we have been growing since then.

“Currently we have 176 ATMs, 64 point-of-sale machines, phone banking through our CenteMobile platform and internet banking.

“Your cards are ready: simply walk into any of the 69 branches with the old ATM card and either a national ID, passport or driving permit and walk out with your new Visa card at no cost.” <

CI June 2018 556.indd 9 15/06/2018 14:33:36

10 | June 2018 | Cards International

ANALYSIS | visa crash

The full extent of the issue is not yet clear, but Visa is still investigating the cause of the problems.

Visa Europe said in a statement at the time: “Visa is currently experiencing a service disruption. This incident is preventing some Visa transactions in Europe from being

processed. We are investigating the cause and working as quickly as possible to resolve the situation.”

Other card payment facilitators, such as banks, were also impacted. Lloyds Bank released a statement saying: “We are aware of an industry-wide issue effecting Visa payments

which is under investigation. ATM and Mastercard transactions are not impacted. We are working to resolve the issue as quickly as possible.”

Following the outage and with Visa Europe back to full capacity, Visa CEO Al Kelly said: “Our goal is to ensure all Visa payments work reliably 24 hours a day, 365 days a year. We fell well short of this goal today, and we apologise to all of our partners and Visa account holders for any inconvenience this may have caused.”

This could cause a huge reputational damage for Visa, given its market share. Visa accounted for 96.8% of the overall debit card transaction value in 2017; Mastercard only had 3% of the debit cards in the UK in 2017.

While Visa will be trying to recover from the outage, Mastercard could take advantage. In July 2017, Mastercard signed a seven-year contract with TSB – a bank that has had its own outage problems. This would make TSB the biggest issuer of Mastercard-branded debit cards in the UK.

If Mastercard proves reliable in the wake of TSB’s architecture issues, and if Visa makes another mistake, we are likely to see a shift in market share in the UK. <

visa network goes down across europeOn 1 June 2018, Visa Europe suffered an outage that affected thousands – if not millions – of consumers. People were unable to make transactions or even withdraw cash. While the system was back running by the end of the day, what damage did it do? Patrick Brusnahan writes

back to Cash after Network Crash?How many of us carry enough cash in our wallets to pay for our daily lunches, lattes and train fares? Last year, card payments overtook cash in the UK for the first time, and it was announced in May that you can even tip buskers in London without handing over cash.

It is estimated that contactless payments now make up a third of all card purchases. Coupled with instances such as the recent Visa outage, payment providers are facing growing pressure to ensure downtime is kept to a minimum. Consumers will favour the most convenient payment options on offer, and if these instances become more regular, they could potentially revert to relying on cash again.

Organisations will need to plan to ensure the chance of transaction failures is mitigated in the first instance, or ensure downtime is minimised when it does go wrong. The industry needs to ensure that, in the case of failure, technology can either be identified at a central location, through data centres, or switched out in-store as soon as the problem arises.

The reliance on this tech has obvious benefits to both merchants, who receive funds into their accounts faster, and also consumers, who benefit from a more convenient retail experience.

The recent Visa outage was accredited to “hardware failure”, affecting thousands of consumers across Europe. The company said its goal is to “ensure [the network] operates 24 hours a day, 365 days a year”, something that all of us – consumers and merchants alike – take for granted these days.

We predict that, regardless of this recent issue, retailers will face increasing pressure to provide more cashless options as consumer demand for tech grows. Consumers have become accustomed to one-click payments online, expecting the same easy transactions when in store. Their shopping experience must be seamless, and as such, data centres and merchant providers need to offer same-day fixes to keep shoppers shopping.

Our recent research finds that retail technology downtime is leaving one in

three UK shoppers unable to complete purchases. Although outages such as Visa’s are rare, the survey also found that two-thirds of consumers had experienced wider payment technology hardware failing on at least one occasion. Despite this, customers still want innovation: findings show that three-quarters of consumers support in-store technology that makes their experience as seamless as possible.

Payment providers will have to work closely with merchants to minimise downtime, making sure they experience fewer faulty contactless machines or unresponsive touchscreens. Technological advances will be essential in making sure high-street retail remains an engaging experience for shoppers. If this is to happen, the payment industry and merchants alike will need to work closely to ensure reliable, same-day fixes to failing tech, avoiding lost sales and making sure we continue our love affair with contactless. <

Claudine Mosseri, general manager – field support, ByBox

CI June 2018 556.indd 10 15/06/2018 14:33:38

www.cardsinternational.com | 11

feature | crypto cards

Last October, Julian Hosp, co-founder of cryptocurrency debit card TenX, posted a YouTube video

boasting of the business’s growth after garnering $80m in its initial coin offering (ICO) or crowdfunding – a blowout sale oversubscribed by 45,000.

“We have been growing massively and have had so many people…we are totally packed here,” Hosp brimmed as he toured the fledgling company’s Singapore offices, engaging with a bunch of glowing marketing, customer service and HR executives.

“We don’t have any more seats, so we have people sitting on the floor,” he joked.

Fast-forward three months and that enthusiasm had soured. In January, Visa cut ties with TenX distributor Wavecrest, forcing it to cancel all its cards and angering around 100,000 customers, many of whom requested refunds or cut their ties with the nascent issuer.

Hosp and TenX representatives rushed to soothe irate customers, offering refunds and reminding them that its partner’s collapse was outwith their control. Despite those spirited efforts, the ordeal cost the startup $2m-4m in customer adjustments and reputational damage. As CI went to press, most customers

were still holding dead cards, waiting for TenX to issue additional ones through new partners.

‘IN A 1,000 YEARS’“I paid for a pre-order card, but TenX’s email was ‘after the integration is complete we will perform a gradual roll-out of cards by geographical region,’” a customer using the name Stefanescu.octavian complained on the firm’s support chat. “Hmmm, in 1,000 years. I want my money back…”

To be fair, Wavecrest’s collapse – reportedly stemming from Visa’s know-your-customer (KYC) and anti-money-laundering (AML) rule violations – hit the entire sector, including main rivals Cryptopay, Xapo, Bitwala and Wirex, which had a bigger, 500,000-card stack in circulation when Wavecrest collapsed. Other high-flying issuer Monaco (MCO) was spared, however, as it uses German-based network Wirecard. Bitcoin card Cointed also survived.

“It delayed everything for everyone else, so we were not in the worst spot,” Hosp tells CI, adding that since January, the 60-strong TenX has significantly streamlined customer service for its maiden debit card, which enables people to convert Bitcoin, Ethereum

and other top digital coins into fiat to meet its “making cryptocurrencies spendable anytime, anywhere” operating mantra.

Still, its woes are symptomatic of the embryonic, $350bn cryptocurrency Wild West, with rollercoaster price swings and widespread scams prompting many to brand the sector a “bubble” or “rat poison”, to quote Warren Buffet.

In late May, the US Justice Department launched an investigation into traders’ alleged Bitcoin manipulation, sending the world’s first digital currency into a tailspin and dragging other cryptos with it.

The possibility that regulators will curtail its skyrocketing growth is burdening the new “decentralised, token economy”. So far, the US, Europe and other developed economies have limited regulatory oversight to tackle fraud in ICOs – digital currency funding events similar to initial public offerings – while China has fully banned cryptocurrencies. Informally, however, over-the-counter crypto purchases remain brisk.

That said, blockchain, the encrypted, hyperledger technology underpinning cryptos, is booming as businesses – including American Express – and governments see its scaling benefits, facing fewer setbacks.

crypto cards hit the market, but can they build visibility?

A growing number of crypto-lenders are looking to disrupt the traditional card sector. Ivan Castano reports on their prospects, and asks whether they really can give Visa and Mastercard a run for their money

CI June 2018 556.indd 11 15/06/2018 14:33:43

12 | June 2018 | Cards International

feature | crypto cards

TENX TARGETS 1 MILLION Hosp says Ten X is on the brink of obtaining a European banking licence to issue its own plastic, and has already struck deals with an unnamed US partner to issue “a high, five-digit” number of cards.

It has signed another European partner, and Hosp said the identity of the firm would be revealed in the next two months.

If all goes well, the business aims to have one million customers this year, up from around 300,000 now, mostly in Europe and Asia. By 2023, it is targeting several million users in 50 countries, from 25 currently.

It also intends to hold 200 cryptos in its mobile wallet – from which users can load up its card – compared to 10 now. It recently added Litecoin and forged a partnership to launch co-branded cards with the sixth-largest crypto, reinvigorating its failed plan to seduce merchants through its now-defunct Lite Pay card.

With an eye to the future, Hosp says crypto cards will give way to more efficient payment systems like digital currency wallets, offering so-called ‘atomic swaps’ or the ability to exchange diverse cryptos instantly to pay at various merchants.

COMIT ROLL OUTTo profit from that era, assuming enough people use digital money in five years, TenX is rolling out a wallet system called Comit that works by linking up different blockchains through “interoperability” protocols.

Hovering at $2.20 in late May, down from a $5.33 high last July, TenX faces cut-throat competition from a string of emerging coins, including Hold, which recently garnered $11.3m in its ICO; FuzeX, which secured $43m in February; and Crypto Credit Card (CCC), a Russian venture targeting $3m in its crowdsale ending in late May.

Hold stands out by allowing customers to collateralise their crypto to obtain a loan that they can then unload through its card.

Hold aims to solve a big problem with crypto cards so far: customers’ reluctance to directly spend their crypto because its price may rise overnight.

“Instead of selling, we allow members to leverage their crypto assets as collateral to obtain fiat whenever they need it,” the company says on its website.

“Cash advances are instant and can be used globally through the Hold prepaid card and mobile app.”

Hold hopes to sign a distribution deal with an undisclosed European partner to launch its products in the third quarter, says adviser Robin Ebers. Eventually, the debit card will be available for use with 45 million merchants and for cash withdrawals from three million ATMs. It will also offer 1% cashback on purchases.

To stand out in the increasingly crowded field, Hold will offer more competitive fees than TenX or other crypto lenders such as Salt and PIVX, and ensure its distribution partnerships are successful to avoid shipping delays that he claims have hobbled Monaco.

“Our projections look really good; lending will be big,” Ebers boasts, without sharing specific figures.

Size – in terms of the liquidity and lending pools the fledgling payment concerns will carry – will become increasingly crucial as, and if, the world continues to migrate into decentralised payments systems.

“We are going to offer bigger withdrawal and conversion – Bitcoin to euro, for instance – limits, will have loan aggregators and a bigger liquidity pool,” boasts Sergey Salynin, CEO of CCC.

ONE-STOP SHOPCCC is building a cryptocurrency exchange and mobile wallet enabling people to hold multiple fiat currencies, swap coins and obtain crypto-backed loans to spend fiat with its debit and credit cards. Uniquely, the business claims it will offer customers the ability to invest in a curated list of promising ICOs.

By striking partnerships with leading but as-yet-unnamed banks in Switzerland, CCC hopes to build an unrivaled “ecosystem” – crypto lingo for a blockchain platform that

will enable it to deploy its card in the autumn, mainly in Europe, but eventually everywhere.

By using its CCR token, customers will be able to pay transaction fees in the card which will hold 20 cryptos. CCR will also offer cashback for merchant purchases, a spokeswoman says, although she declines to give further details.

Cashback and diverse rewards – as well as fancy VIP cards – should help Monaco beat rivals, the company’s senior vice-president Eric Anziani said during Consensus 2018, the annual cryptocurrency conference.

The business, which raised $26m last summer, has rolled out a stylish, obsidian black-metal card offering 2% cashback in its Monaco (MCO) coin, free airport lounge accesses, no monthly fees and up to $1,000 in free ATM withdrawals.

Monaco will only issue 999 of the platinum cards, which will force users to purchase 50,000 MCOs and hold them for six months to obtain the perks, according to marketing literature.

At the time of writing, Monaco was about to launch its mobile wallet and Visa-labeled cards enabling customers to convert four cryptos into seven fiat currencies to make international merchant purchases. To enable such transactions, the company charges real-time interbank rates it claims are 5-8% lower than those of high-street banks.

Anziani says Monaco is also moving to deploy a card that will allow users to hedge their crypto to borrow 40-60% of their assets, based on whether they use MCOs or Bitcoin. If, for example, a customer deposits $10,000 MCO, the customer can borrow up to $6,000.

Marketing aside, however, Anziani concedes that the crypto space faces huge challenges.

The TenX card and mobile wallet

CI June 2018 556.indd 12 15/06/2018 14:33:44

www.cardsinternational.com | 13

feature | crypto cards

“Only 20 million to 30 million people are using crypto today. Globally, this is less than 1% of the population so we are facing a very nascent industry and we all have to collectively work to democratise blockchain technology and its use cases with the public,” Anziani told Consensus, which drew 8,000 crypto enthusiasts to discuss the state of the industry – flashy Lamborghinis in tow.

“It is still very difficult to buy and exchange cryptocurrency. It is a long on-boarding process with limited customer support,” Anziani noted, referring to the long identity checks and KYC queues required to buy digital cash in exchanges like Coinbase for the first time.

This “lack of independence” to buy and sell cryptos – and their notorious price volatility – is hindering the industry’s growth, Salynin says. However, he notes that institutional investors’ widely anticipated jump into the space – a move not expected until a large and trusted custodian investment firm emerges, with Coinbase and Goldman Sachs’ Circle vying for top spot – should level the field.

Most global merchants are shunning cryptocurrencies because their volatility can eat into sales margins. However, Salynin says 150 Japanese retailers already accept cryptocurrencies, showing that the feat is possible, especially in the crypto-loving Asian county.

Meanwhile, many online merchants, such as OpenBazaar, are also improving the user experience, betting that an eventual crypto shopping boom will boost their fortunes.

Yaniv Feldman, an Israeli economist specialising in crypto, says the ideal Bitcoin card customers are those who hold huge amounts of it and are keen to spend.

“If you have 200 Bitcoins you bought for $10 a few years ago, you have lots of money and you want to do stuff with it because otherwise the tax man could see it,” Feldman explains, adding that many global banks continue to ban crypto-related deposits, making these crypto cards attractive options to more easily spend vast wealth.

SITTING PRETTY?As the TenXs of the world take the market by storm, should Visa and Mastercard be worried? Not in the short term, says Feldman, echoing other experts.

He says: “Besides KYC or AML compliance issues, I don’t see a reason where legacy credit cards would suffer. They are benefitting with every transaction. The more [crypto] cards

come out, the more Visa makes.”In the event that crypto adoption

strengthens, a separate, decentralised payments network could emerge to challenge the incumbents, Feldman says. In that case, they could roll out their own cards or acquire their crypto competitors to rein in the market, he adds.

However, “creating a network like Visa or Mastercard would be a monumental task,” says Jerry Straessle, owner of boutique US payments consultancy JLS Associates. “They have created this over 40 years, and to replace it with another network would be difficult.”

Straessle adds that all financial institutions and retailers are tracking crypto, but none are yet taking it too seriously – except those focusing on e-commerce. This is mainly because the SEC and other regulators have yet to issue clear regulation on the space, something he expects will continue to hinder its development.

BEATING HACKERS Security is also a big challenge at a time when crypto exchange hackings continue unabated, says Mike Ryan, a consultant specialising on Bluetooth and Internet of Things devices working in the space.

“Every card should start with security as its foundation, then user experience,” he notes.

“My experience with electronic cards has been that most are focused on marketing and tech, and spend very little on security and user experience, which should go hand in hand.”

FuzeX, which allows users to store up to 15 cryptocurrency accounts, as well as 10 debit and credit cards, does those two things very well, Ryan notes. The e-card looking to make physical wallets obsolete features an electronic crypto balance display, letting users know their coin balance before and after making a purchase, as illustrated by a McDonald’s demo-transaction video on its site. FuzeX also comes with a lock-up feature in case its user forgets it.

PIVX, a so-called privacy coin, has also introduced a debit card with partner Uquist, featuring security and privacy as a prime

differentiator. It can be used on Amazon, Uber, Deliveroo and other merchants, according to Uquist, which claims to operate up to 90 debit cards, including ones for Bitcoin, Ethereum, EOS, Bitcoin Cash and Litecoin.

PIVX would be “an excellent addition” for any crypto card, says an anonymous executive using the pseudonym Turtleflax to respect the business’s privacy philosophy. This is because the company’s success hinges on rapid merchant adoption or point-of-sale applications for which it has designed its apps. PIVX also makes deposits and withdrawals much faster and more private than rivals, boasts Turtleflax, speaking through the Discord chatting app.

“Crypto cards will be a good solution if they can navigate regulation…while the aversion to spending with them will decrease as volatility does.”

$5TRN IN 12 MONTHS?Turtleflax expects adoption to increase rapidly, adding: “People will want crypto because they want to control their money and privacy. Facebook, Amazon and others can offer ‘blockchain’, but they can’t offer a decentralised system.

“They will always control it, which means they would control your money, see your

information, and limit how you can spend your coins.”

Turtleflax continues: “Crypto is here to disrupt the current system, and the cracks are already starting to show. Paypal continues to lock people’s funds and Western Union continues to price-gouge people for remittance payments.”

Feldman agrees, adding that crypto could soar parabolically to $3trn-5trn in 12-18 months, and then melt down.

“It will probably crash like the dot.com boom or 1929 [stock market crash] which is how this market cycles go,” he says.

“Once that happens, all the speculators will be driven out and the economy will be able to grow and really get value from this the new blockchain era.” <

It is still very difficult to buy and exchange cryptocurrency. It is a long on-boarding process with limited support

CI June 2018 556.indd 13 15/06/2018 14:33:44

14 | June 2018 | Cards International

regulation | australia

The Commonwealth Bank of Australia (CBA) has been under fire during evidence at the Financial

Services Royal Commission (FSRC) for increasing credit card limits on accounts held by a customer who told the bank of gambling problems.

A case study presented to the FSRC, which was called on 30 November 2017 by Prime Minister Malcolm Turnbull, featured details about the ease with which a bank customer, David James Harris, obtained credit from the CBA despite self-identifying as a problem gambler.

Harris, 30, is one of a number of bank customers that have been called to provide evidence to the Royal Commission, which was called in part to expose the underbelly of the sales culture, compliance failures and poor governance practices of the financial services sector in Australia.

CONSUMER PRESSURETurnbull was forced to call the full-blown inquiry into bad banking behaviours as a result of increasing pressures placed on him by consumer groups, members of Commonwealth parliamentary committees, and financial services institutions.

“Those institutions are the bedrock of the economy. There would be very few Australians who are not a customer or shareholder of the banks. Many of us are both, with almost every worker holding bank shares through their

superannuation fund. The banks employ more than 200,000 people alone,” the besieged Turnbull told the assembled Canberra press corps on 30 November 2017.

“Now, the speculation about an inquiry cannot go on. It is moving into dangerous territory where some of the proposals being put forward have the potential seriously to damage some of our most important institutions.”

Turnbull announced the appointment of Royal Commissioner Kenneth Hayne the day after the media release and press conference announcing the inquiry, with Hayne and his commission team required to report back to the government by February 2019.

The terms of reference require the Royal Commission to produce a report that looks at the full extent of the behaviour of banks and other institutions, and provide recommendations. These can include recommendations for legislative change as well as any instances of further investigation that might be required.

The terms of reference acknowledge, however, that Australia’s financial system is robust and the inquiry was to investigate a broad range of misconduct.

CBA UNDER FIREThe commission has heard evidence from customers about the provision of inappropriate advice related to the provision of financial products, including credit cards.

Counsel assisting the commission, Rowena Orr QC, told the commissioner that Harris’s CBA experience was one example of the provision of an inappropriate product to an individual that had warned the bank of a personal problem.

“Mr Harris had a gambling problem of which CBA was aware, at least when credit limit increases were offered, and perhaps ought to have been aware earlier,” Orr told the commissioner.

“Nevertheless, Mr Harris was offered a credit limit increase only days after telling the Commonwealth Bank of his problem.”

GAMBLING ON CREDITHarris’s written statement contains further details of his dealings with the CBA, which had given him a series of increases in credit despite being aware he had a serious gambling problem.

He told the commission that he had applied for a credit card with a A$10,000 ($7,600) limit in 2014 in preparation for a trip overseas. Harris was planning a trip to visit the UK, as well as stopping over in Thailand for dental surgery.

While he says he repaid the credit balance soon after returning to Australia, Harris began to gamble using his credit card.

“I had gambled previously, but not to that degree, and I had previously only used my own money to gamble. I began using the First CSA Credit Card to pay for my gambling

cba highlights dangers of poor credit decisioningThe Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry in Australia has attracted worldwide publicity for all the wrong reasons. As Tom Ravlic reports, the cards sector is not immune

CI June 2018 556.indd 14 15/06/2018 14:33:44

www.cardsinternational.com | 15

expenses,” Harris explained in his written statement to commission.

“Initially, I was transferring cash from the First CSA Credit Card to another one of my CSA accounts using the cash advance function before using it to gamble.”

Harris developed a habit for “maxing out” his first CBA credit card on gambling. He admitted that he applied for a second credit card for gambling purposes that had a A$7,000 credit limit.

Harris also managed to get a third credit card with an A$8,000 credit limit. The CBA also offered Harris a credit increase on his first card, which meant the available credit across his three credit cards was A$27,100.

The problem gambler told the commission that he continued his habit of reaching maximum credit on one card and then trying to pay it off with the other cards. This had serious consequences for Harris’s work and social life.

“I was only able to continue paying off the credit card because I was working for extended periods. In the first half of 2016, I worked for 62 days in a row before taking one day off. I then worked another 40 days in a row,” Harris admitted.

“I did this because the debt hanging over my head was overwhelming. I was struggling with depression and anxiety. My social life had been destroyed and I wanted to get the debt paid off so that I could close the card.”

He continued to receive offers from the bank stating he was eligible for an increase in credit, which he accepted. At one point his credit limit was increased to A$35,100. This kept fuelling Harris’s gambling addiction.

“By way of example, from Friday 9 June 2017 to Sunday 11 June, I charged at least A$18,850 to the Consolidated CBA Credit Card in order to gamble,” Harris noted.

COMPLAINTSHarris made two complaints about his situation, and ended up receiving assistance from the bank to make arrangements allowing him to repay the debt owing on the cards.

He told the commission in his written submission dated 18 March 2018 that he still owed A$23,400 to the CBA, while also admitting that he had “gambled hundreds of thousands of dollars”.

The CBA appeared after Harris and the bank’s executive, Clive van Horen, told the commission that Harris should never have received increases in credit given his gambling addiction. Bank procedures related to assessing

customers for credit purposes had changed over the past 12 months.

“[We’ve] acknowledged we should not have provided that final credit limit offer. The basis for saying that is, having had the conversation with one of our staff members in a contact centre and declaring that Mr Harris had a gambling problem – to use the simple description of it – without in any way trying to minimise the challenge that presented, that information was not in any way passed through to credit-decisioning systems,” Van Horen told the commission.

“That’s a failing, and we acknowledge that and we’ve got to find ways to address that. So,

to that extent, having declared it to somebody working in the Commonwealth Bank, we did not use that information for the subsequent credit offer.”

Changes in the CBA’s internal processes had begun over the past 12 months in order to ensure that any signs of gambling by a bank customer with a credit card could result in them being banned from getting a credit increase.

Van Horen told the commission that, while the law did not appear to require the additional monitoring of how customers used credit, he believed it was reasonable for banks to look more closely at how customers with credit limits spend those funds.

“In April last year we changed our credit-decisioning rules such that if we observed high levels of gambling spend in a customer’s credit card, we would not offer them any further credit limit increases,” Van Horen observed.

“That was a change that happened in April last year, which in isolation should have meant we wouldn’t offer significant [credit lending increases] to customers who exhibited high gambling spend on their credit card.”

SLIPPERY SLOPEThe bank, however, admitted to a challenge. Gambling is legal, Van Horen noted, and at what point should a bank decide to intervene?

“You can quickly see the slippery slope that puts us on if we say you can’t spend on gambling: what about other addictive

spending – on shopping, or on alcohol, or any other causes?” he said. “This is what we’ve grappled with. Absent any clear legal or regulatory guideline, how do we determine when we intervene and impose limits?”

One of the other challenges faced by the CBA is that its internal systems failed to provide information to people selling the idea of credit increases to someone like Harris that there were financial or other problems that had come to the bank’s attention. Put simply, the right hand at the CBA did not necessarily know what the left hand was doing.

“We need to build a flag. There are complexities around all that, but we need to

find a way to make sure that if somebody – and you will appreciate there’s a lot of people out there – has a conversation that flags a customer could be in difficulty, in the way of other flags for domestic violence, where we then trigger domestic violence support programs,” van Horen explained.

“We don’t have something that triggers a proactive action around a self-disclosed matter like this. It’s something we want to do something about; we’ve got to work out how we can do that, because it’s clearly not a simple thing to execute.”

Van Horen told the commission that details of Harris’s personal circumstances collected by a person on the bank’s customer hotline should have been recorded in some form so anyone dealing with him was able to see personal information that would them stop people from sending out letters of offer to increase their credit limit.

“We absolutely acknowledge we shouldn’t have [sent out other offers to increase the credit limit] – in a perfect world we would have used this information from the telephone call to find its way back into our credit models.”

The credit card calamities faced by Harris are not the only problems faced by the CBA at the Royal Commission or with other regulators. A recent inquiry by the Australian Prudential Regulation Authority found that the CBA’s board of directors had failed to do its job properly in overseeing the conduct of management in multiple areas. <

regulation | australia

There would be very few Australians who are not a customer or shareholder of the banks. Many of us are both

CI June 2018 556.indd 15 15/06/2018 14:33:45

16 | June 2018 | Cards International

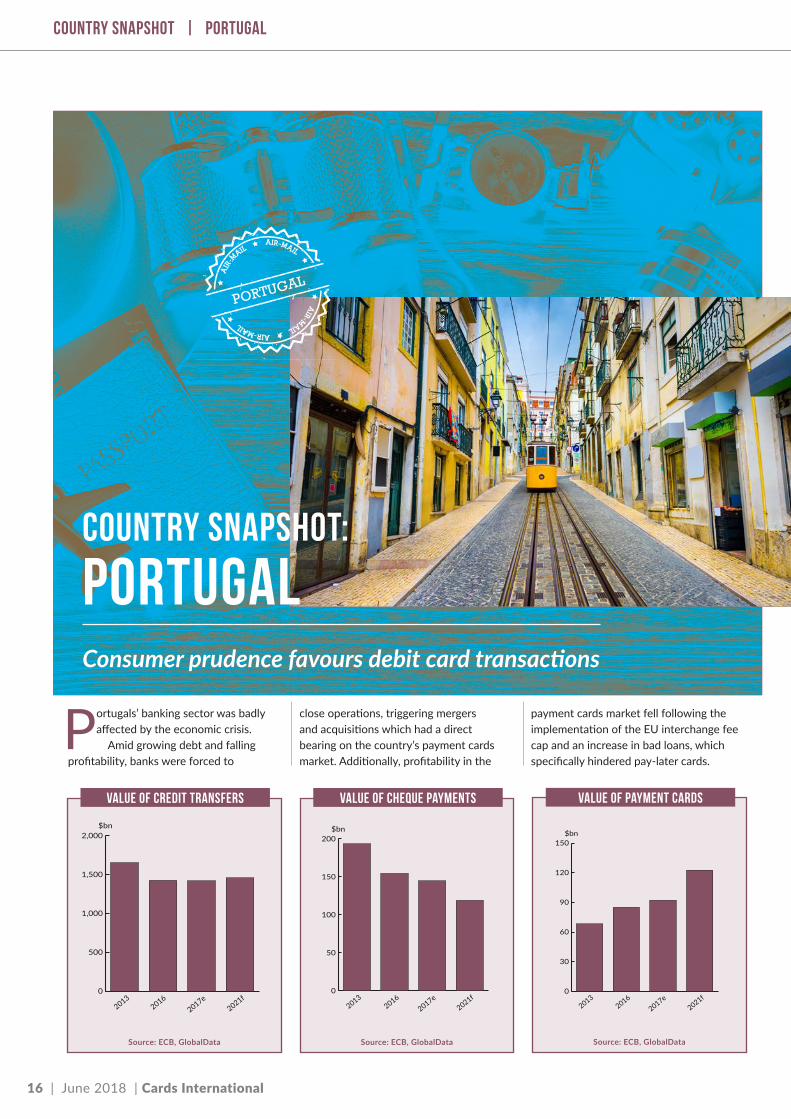

country snapshot | portugal

PORTUGAL

country snapshot: portugal

Portugals’ banking sector was badly affected by the economic crisis.

Amid growing debt and falling profitability, banks were forced to

close operations, triggering mergers and acquisitions which had a direct bearing on the country’s payment cards market. Additionally, profitability in the

payment cards market fell following the implementation of the EU interchange fee cap and an increase in bad loans, which specifically hindered pay-later cards.

0

500

1,000

1,500

2,000

20132016

2021f2017e

$bn

value of credit tRanSfers

Source: ECB, GlobalData

0

50

100

150

200$bn

20132016

2021f2017e

value of cheque payments

Source: ECB, GlobalData

Consumer prudence favours debit card transactions

0

30

60

90

120

150$bn

20132016

2021f2017e

value of payment cards

Source: ECB, GlobalData

CI June 2018 556.indd 16 15/06/2018 14:33:55

www.cardsinternational.com | 17

country snapshot | portugal

However, amid this turmoil, consumer preference for debt-free payments and prudent spending resulted in growing debit card transaction volumes and values. Consumers in Portugal made over 1.5 billion purchases with debit cards at the POS in 2017.

Contactless card numbers and usage have also seen strong growth in recent years, with the vast majority of contactless users in Portugal seeing the cards as helpful. In addition, with various government and bank initiatives, payment cards will grow steadily over the next five years and gradually become more accepted.

HIGH BANK PENETRATIONDebit card penetration in Portugal is high, supported by the large banked population.

The central bank has pushed banks to offer basic accounts with minimal charges to all citizens, offering services including a debit card and the ability to make credit transfers and direct debits. According to the central bank, the number of basic bank accounts rose from 9,646 in 2013 to 34,953 in 2016.

The government is also using digital channels to increase banking penetration. In July 2017, the central bank issued regulations enabling institutions with headquarters or branches in Portugal to allow customers to open accounts exclusively through digital channels. Consequently, banks such as Novo Banco, Millennium bcp and Santander Totta enable consumers to open bank accounts through digital channels.

E-COMMERCEE-commerce is acting as a key driver of payment card market growth. According to a 2016 SIBS Market Report, more than a third of Portuguese consumers prefer payment cards for online purchases.

Many banks offer customised payment cards for online shoppers. For instance, Millennium bcp offers a Visa-branded web card for an annual fee of €10 ($12). Emerging solutions such as PayPal, Masterpass and Seqr are also being used for online transactions.

Consumers most value security when choosing a mode of online payment, with 44% citing this feature. The growing number of online apps such as MB Way and Masterpass is expected to drive

e-commerce in Portugal to record a CAGR of 11% over the next five years.

CONTACTLESS GAINSContactless payments are expected to gain prominence in Portugal, with Caixa Geral de Depósitos, Novo Banco and Banco BPI now offering contactless cards.

Merchants have also started to provide the necessary infrastructure for contactless payments, and overall the number of contactless cards rose from three million in 2013 to 11.6 million in 2017.

Prepaid cards are gradually gaining acceptance among Portuguese consumers, primarily due to prudent consumer spending as a result of subdued economic growth. The number of prepaid cards grew significantly from 1.1 million in 2013 to 2.6 million in 2017.

Banks in Portugal offer prepaid cards for consumer segments such as children, shoppers and travellers. Caixa Geral de

Depósitos, for example, offers Mastercard-branded prepaid cards for children aged over 10 years. The LOL Junior Card can be loaded with funds from $6 to $600 through online banking, at ATMs and branches, or by direct debit.

INFRASTRUCTUREThe number of POS terminals recorded a moderate CAGR of 5.7%, rising from 259,428 in 2013 to 323,931 in 2017.

Retailers are also installing POS terminals that accept contactless payments, as a result of which the potential for card-based payments is also expected to grow.

Service providers are launching new products. In September 2017 the National Association of Road Transport Carriers collaborated with myPOS and the National Digital Taxis Center to equip taxi drivers in Lisbon with myPOS terminals that enable credit and debit card transactions and contactless payments. <

Novo Banco14.4%

Others47.8%

Millennium bcp16.0%

Caixa Geralde Depositos

21.8%

Debit card shares by issuer

Source: GlobalData

mBank21.7%

Others42.3%

BankPekao12.1%

Multibanco100%

Debit card shares by scheme

Source: GlobalData

WiZink13.6%

Novo Banco14.7%

Others58.4%

Millennium bcp 13.4%

pay later shares by issuer

Source: GlobalData

Mastercard29.8%

Others17.5%

Visa54.4%

pay later shares by scheme

Source: GlobalData

CI June 2018 556.indd 17 15/06/2018 14:33:57

18 | June 2018 | Cards International

country snapshot | finland

FINLAND

Finnish consumers are strong users of payment cards, with frequency of card use higher in Finland than in

other mature European markets such as

the UK and Germany. Improved banking infrastructure, new product developments, high awareness of electronic payments, and wide acceptance of payment cards at POS

terminals were the main growth drivers for payment cards in Finland.

Debit cards are the most popular card type in Finland, and are typically used

0

1,000

2,000

3,000

4,000

5,000$bn

20132016

2021f2017e

value of credit tRanSfers

Source: ECB, GlobalData

0

2

4

6

8

10$bn

20132016

2021f2017e

value of cheque payments

Source: ECB, GlobalData

0

10

20

30

40

50

60

70

80$bn

20132016

2021f2017e

value of payment cards

Source: ECB, GlobalData

country snapshot: finlandImproved infrastructure and awareness bolster card use

CI June 2018 556.indd 18 15/06/2018 14:34:06

www.cardsinternational.com | 19

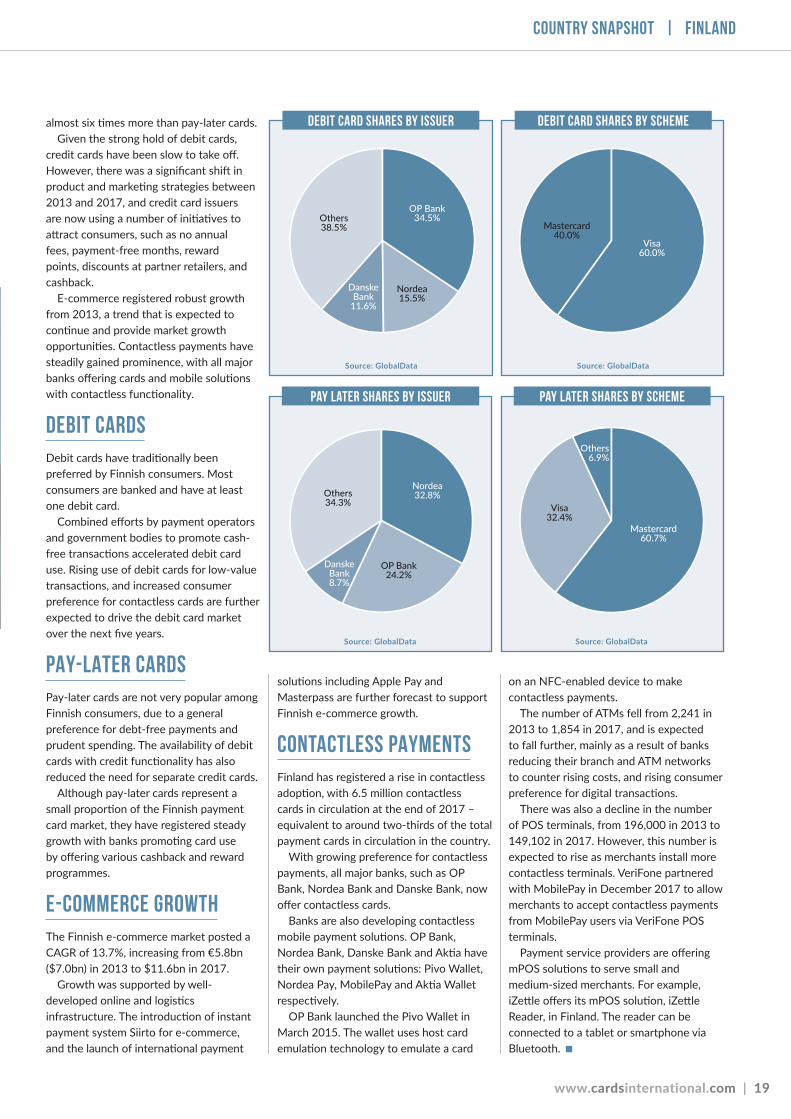

almost six times more than pay-later cards.Given the strong hold of debit cards,

credit cards have been slow to take off. However, there was a significant shift in product and marketing strategies between 2013 and 2017, and credit card issuers are now using a number of initiatives to attract consumers, such as no annual fees, payment-free months, reward points, discounts at partner retailers, and cashback.

E-commerce registered robust growth from 2013, a trend that is expected to continue and provide market growth opportunities. Contactless payments have steadily gained prominence, with all major banks offering cards and mobile solutions with contactless functionality.

DEBIT CARDSDebit cards have traditionally been preferred by Finnish consumers. Most consumers are banked and have at least one debit card.

Combined efforts by payment operators and government bodies to promote cash-free transactions accelerated debit card use. Rising use of debit cards for low-value transactions, and increased consumer preference for contactless cards are further expected to drive the debit card market over the next five years.

PAY-LATER CARDSPay-later cards are not very popular among Finnish consumers, due to a general preference for debt-free payments and prudent spending. The availability of debit cards with credit functionality has also reduced the need for separate credit cards.

Although pay-later cards represent a small proportion of the Finnish payment card market, they have registered steady growth with banks promoting card use by offering various cashback and reward programmes.

E-COMMERCE GROWTHThe Finnish e-commerce market posted a CAGR of 13.7%, increasing from €5.8bn ($7.0bn) in 2013 to $11.6bn in 2017.

Growth was supported by well-developed online and logistics infrastructure. The introduction of instant payment system Siirto for e-commerce, and the launch of international payment

solutions including Apple Pay and Masterpass are further forecast to support Finnish e-commerce growth.

CONTACTLESS PAYMENTSFinland has registered a rise in contactless adoption, with 6.5 million contactless cards in circulation at the end of 2017 – equivalent to around two-thirds of the total payment cards in circulation in the country.

With growing preference for contactless payments, all major banks, such as OP Bank, Nordea Bank and Danske Bank, now offer contactless cards.

Banks are also developing contactless mobile payment solutions. OP Bank, Nordea Bank, Danske Bank and Aktia have their own payment solutions: Pivo Wallet, Nordea Pay, MobilePay and Aktia Wallet respectively.

OP Bank launched the Pivo Wallet in March 2015. The wallet uses host card emulation technology to emulate a card

on an NFC-enabled device to make contactless payments.

The number of ATMs fell from 2,241 in 2013 to 1,854 in 2017, and is expected to fall further, mainly as a result of banks reducing their branch and ATM networks to counter rising costs, and rising consumer preference for digital transactions.

There was also a decline in the number of POS terminals, from 196,000 in 2013 to 149,102 in 2017. However, this number is expected to rise as merchants install more contactless terminals. VeriFone partnered with MobilePay in December 2017 to allow merchants to accept contactless payments from MobilePay users via VeriFone POS terminals.

Payment service providers are offering mPOS solutions to serve small and medium-sized merchants. For example, iZettle offers its mPOS solution, iZettle Reader, in Finland. The reader can be connected to a tablet or smartphone via Bluetooth. <

country snapshot | finland

OP Bank34.5%

Nordea15.5%

Others38.5%

DanskeBank

11.6%

Debit card shares by issuer

Source: GlobalData

Visa60.0%

Mastercard40.0%

Debit card shares by scheme

Source: GlobalData

Nordea32.8%

OP Bank24.2%

DanskeBank8.7%

Others34.3%

pay later shares by issuer

Source: GlobalData

Visa32.4%

Others6.9%

Mastercard60.7%

pay later shares by scheme

Source: GlobalData

CI June 2018 556.indd 19 15/06/2018 14:34:09

20 | June 2018 | Cards International

Country snapshot | kenya

Kenya’s payment card market is still very much in a developmental stage. The East African nation recorded

a penetration rate of 30 cards per 100

individuals in 2017, and 16.0 transactions per card per year – figures lower than Kenya’s peers in the continent, including South Africa, Morocco and Egypt.

Overall, cash accounted for 88.4% of the total payment transaction volume in 2017. The low uptake of payment cards is a result of society’s dependence on cash, and limited acceptance of payment cards at merchant locations.

Advanced security features such as EMV are being adopted to encourage consumer adoption of payment cards. In addition, scheme providers have launched campaigns to raise overall consumer awareness of the security issues and benefits related to EMV chip cards.

Visa ran a Security Week programme in May 2015, and also launched a chip and PIN campaign in September 2014 to promote the security benefits of cards for everyday payments.

Similarly, Mastercard partnered with card processor Paynet in July 2013 to launch the Great Migration to EMV Chip initiative, which aimed to encourage consumers

0

5

10

15

20

25

30$bn

20132016

2021f2017e

value of cheque payments

Source: Central Bank of Kenya, GlobalData

0.0

0.5

1.0

1.5

2.0$bn

20132016

2021f2017e

value of payment cards

country snapshot: kenyaConsumer attitudes and limited acceptance restrict card use

KENYA

Source: Central Bank of Kenya, GlobalData

CI June 2018 556.indd 20 15/06/2018 14:34:16

www.cardsinternational.com | 21

Country snapshot | kenya

to switch from magnetic stripe to EMV-compliant cards.

The wide popularity and acceptance of mobile payment solutions such as M-Pesa and Pesapal have been major obstacles for payment card growth, as the solutions offer convenience and cost-effectiveness. Unlike banks, mobile payment solution providers offer their services to small merchants and charge lower processing fees, making them attractive to consumers.

Overall, the Kenyan payment card transaction value at POS terminals recorded a subdued CAGR of 0.6% between 2013 and 2017.

The government has taken several initiatives to bring the unbanked population into the formal banking system, which in turn helps to promote card use. One initiative is the adoption of an agency banking model to provide financial access to individuals in remote areas.

In 2016, the government made it mandatory for all Kenyan individuals to complete a form if they deposit or withdraw more than KES1.0m ($10,000) in cash from a bank account. The aim of the move was to increase the traceability of bank transactions and boost electronic payments in the country,

M-PESA REMAINS POPULARCard-based payments have grown marginally in the last five years due to the convenience and cost-efficiency of mobile-based retail payment solutions.

As of March 2017, M-Pesa had 27 million registered users in Kenya, as well as more than 136,000 agents and over 260,000 active retail outlets.

Mobile payment solution providers typically charge lower processing fees than other payment operators; for example, Safaricom charges merchants a 0.5% transaction processing fee on its Lipa Na M-Pesa service – much cheaper than the average merchant service charge for bank card payments.

AGENCY BANKINGAll major banks in Kenya offer agency banking services, with an aim to improve financial inclusion in the country,

According to the Central Bank of Kenya, as of 30 June 2017, 60,102 agents from 18 commercial banks and five microfinance banks were active in the country.

Between June 2016 and June 2017, transactions undertaken by banking agents increased by 56.5% in value. Growth in Kenya’s banked population has led to a rise in overall debit card penetration in the country.

E-COMMERCE GROWTHKenya’s e-commerce market recorded a robust CAGR of 23.8% between 2013 and 2017, as a result of increased internet penetration and a growing middle class, as well as the presence of various mobile payment services. E-commerce growth has also been supported by the availability of solutions such as M-Pesa, PayPal, mVisa and JamboPay.

A number of companies have launched online payment solutions, with Chinese company Demart entering Kenya in May 2017 and I&M Bank’s Webpay platform enabling merchants to accept Visa and Mastercard for online purchases.

PREPAID CARD GROWTHBanks offer various customised prepaid cards to serve consumer segments such as students and salaried individuals.

In July 2016, Equity Bank launched a Mastercard-branded prepaid card for students at Maseno University. The card enables holders to receive loans from the Higher Education Loans Board, and to make fee payments, withdraw cash from ATMs, and make in-store payments. Card holders also have access to cash at ATMs, branches and Equity Bank agents.

In September 2015 Ecobank launched the Visa SalaryXpress prepaid card with chip-and-PIN technology. The card can be used to withdraw cash and make in-store and online payments.

Employers with arrangements with Ecobank can use the card to pay employees directly, allowing card holders to receive salaries through the card without holding an Ecobank account. <

Others37.4%

Equity Bank32.0%

Co-operativeBank of Kenya

19.7%KCB

10.9%

Debit card shares by issuer

Source: GlobalData

Visa55.1%

Mastercard44.9%