Embed Size (px)

Citation preview

Bookings, billing and revenue control

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• Bookings may be taken: by post by email by telephone via the internet (using online systems) from customers coming to the

establishment in person.

Taking bookings

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• Basic information is the same, regardless of how the bookings are taken. This includes: day and date name of the customer customer’s telephone number number of covers required time of arrival any special requirements signature of the person taking the booking in case of

queries.

Booking information

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Booking sheets• Most establishments use some form of booking

sheet, either manual or electronic.

Example of a booking sheet

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• The occasion of the meal may be to mark a special event, such as an anniversary or birthday.

• Customers may have preferences about the size, shape and/or location of a table.

• Any special requests, such as requirements for a celebration cake.

• Customers may have specific dietary requirements.

Other information

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Cancellations • When a cancellation is received, the details

should be confirmed by repeating the details back to the customer making the cancellation.

• It is good practice to ask if you can take a booking for any other occasion in place of the cancellation.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Larger party bookings • Larger party bookings may have different

procedures. For example: set meal and beverages price per head or for whole party requirement for a deposit seating plan deadline for confirmation of final numbers.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Purpose of a revenue control system

• Monitors areas where selling takes place, including: efficient control of all food and beverage items

issued reducing pilfering and keeping wastage to a

minimum ensuring bills are correct and proper payments

are made and accounted for providing management information.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• Order-taking methods

• Billing methods

• Sales summary sheets

• Performance measures

Main control methods

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Summary of food and beverage revenue control

Flow chart of food and beverage checking system, based on triplicate system

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Systems for revenue control• Manual systems

• Pre-checking systems

• Electronic cash registers

• Electronic point of sale (EPOS) control systems

• Computerised systems

• Satellite stations

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Radio-controlled electronic system

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Role of the cashier

• Each establishment will have its own procedure. Usually includes: checking the float ensuring the cash drawer is properly

organised ensuring enough till rolls, promotional items,

bill folders, stapler, paper clips and pens, etc. ensuring electronic systems are functioning.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Cashier’s duties• Issuing and recording

check books/ order systems.

• Maintaining cash floats.

• Preparing customer bills.

• Maintaining copies of food and wine orders.

• Counter-signing spoilt checks.

• Receiving payments.• Receiving back

unused checks back/order systems.

• Ensuring payments are balanced with manual or electronic sales summaries.

• Delivering the reports and payment to the control department.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Billing methods• Bill as check• Separate bill• Bill with order• Pre-paid• Voucher• No charge• Deferred (charged to account)

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Billing methods

Electronic point of sale billing and payment system

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Billing methods

Example of a bill

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Payment methods• Cash

• Cheque

• Credit cards/debit cards/charge cards

• Traveller’s cheques

• Vouchers and tokens

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Payments in restaurants• Two ways of taking payments:

Customer may be asked to come to the cash desk or workstation to complete the payment transaction: some customers prefer this.

Hand-held self-powered terminal is taken to the customer at their table.

Hand-held credit/debit card paymentterminal with printer

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• Additional considerations: Make sure all customers, including wheelchair

users, will be able to reach the payment point. Allow customer to pick up the PIN pad from

the cradle if appropriate. Offer assistance when needed. Exercise patience.

People with disabilities

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Dealing with payments • Do not allow anyone to interrupt you during a transaction.• Always double-check cash received and any change

before giving it out.• Check bank notes for forgeries.• Declined card transactions may require the card to be

retained.• If you make a mistake, always apologise.• Remain polite.• Ask for assistance from supervisor as required.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Till security• The security of the till can be ensured by:

using passwords/codes to access till using key or swipe cards to access till restricting access to certain staff assigning tills to specific servers signing in and out when using till locking and securing tills in the event of an

evacuation from premises.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Recording

mistakes

• Ensures proper record so that till balances with payments taken.

• Prevents cashier being suspected of theft.• Prevents taking longer to cash up.• Staff may be made accountable for

discrepancies.• Complies with procedures and avoids

disciplinary procedures.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Sales summary sheets

• Vary according to the establishment.

• Summary sheets allow: reconciliation of items with different gross

profits sales mix information records of popular/unpopular items records for stock control.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Sales sheet information• Name of food and

beverage outlet• Date• Period of service• Bill numbers• Table numbers• Number of covers

per table/ transaction

• Bill totals• Analysis of sales• Various

performance measures

• Cashier’s name

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

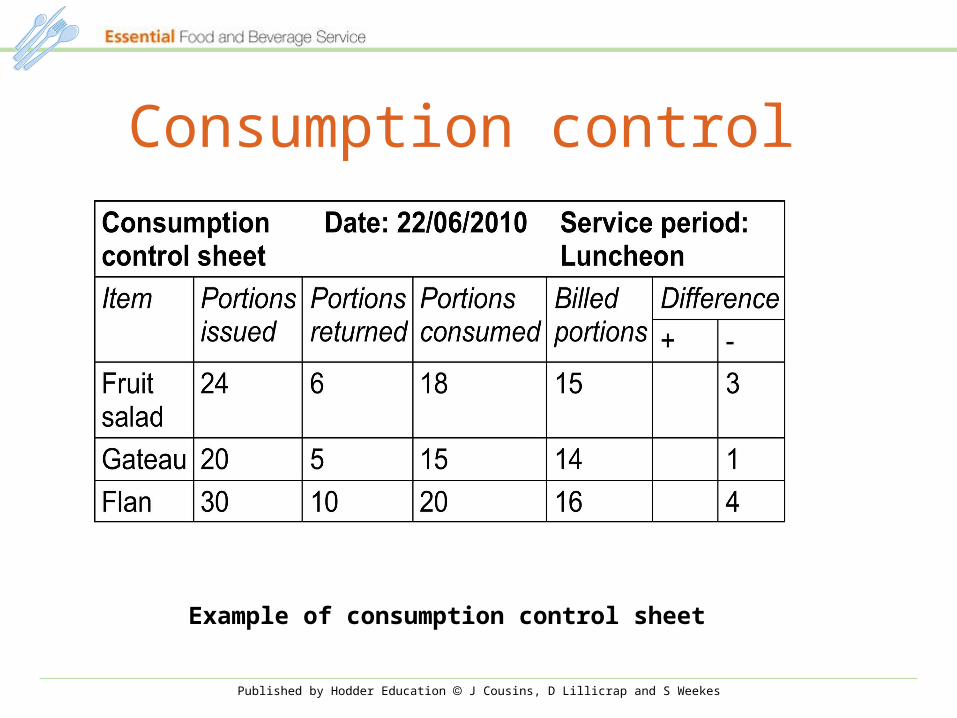

Consumption control• Used for:

cold tables buffets carving sweet cheese liqueur trolleys food and beverage counters.

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Consumption control

Example of consumption control sheet

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

• Range of information collected during the revenue control phase.

• Information often automatically on sales summaries and control sheets.

• Can include: sales mix, gross profit, cost percentages, seat turnover, sales per staff member, sales per seat and sales per area.

Performance measures

Published by Hodder Education J Cousins, D Lillicrap and S Weekes

Relationship between revenue, cost and profits

Note: In kitchen operations, gross profit is sometimes called kitchen percentage or kitchen profit.

Foods and beverage costs Cost of sales

Labour costs

Overhead costs Gross profit

Net profit

Total sales £ Revenue 100%