Embed Size (px)

Citation preview

Taxation of securities

Presentation by

Yogesh Thar July 11, 2018

Bombay Chartered Accountants Society

1. Business Income v. Capital Gains

Relevant Judicial Pronouncements and Legislations

Tests laid down in:

Instruction No. 1827 dated August 31, 1989

Circular no. 4/2007 dated June 15, 2007

Circular no. 6/2016 dated February 29, 2016

CBDT Letter F. No. 225/12/2016 of May 2016

2

YOGESH THAR

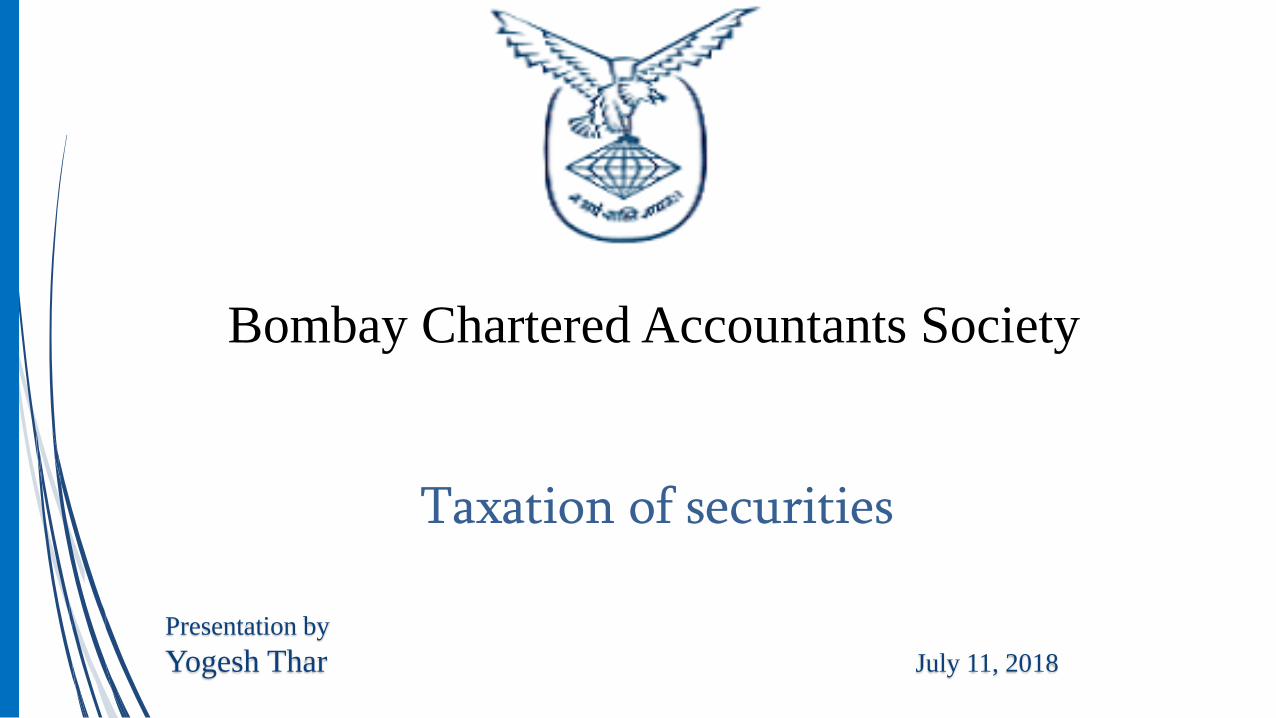

Tests summarised

Considering the judicial pronouncements, instructions and circulars above, the tests are

summarised as under…:

Past Assessment Records

Treatment in the books of account (i.e. whether shown as investment or as stock-in-trade)

Method of valuation

Nature and Quantum of purchase and sale

Ratio between purchase and sales

Period of Holding

YOGESH THAR

3

Tests summarised (contd…)

…Considering the judicial pronouncements, instructions and circulars above, the tests

are summarised as under:

Frequency, continuity and regularity of transactions

Motive or intention behind acquisition / sale of securities

Source of Acquisition – Whether from owned or borrowed funds

It is possible to have two portfolios - one for investment and the other for stock-in-trade

Any act subsequent to the purchase thereby making it more readily resalable

Any act prior to purchase making showing a design or purpose

4

YOGESH THAR

Chart demonstrating the facts in various case laws numerically and the judgement thereof

Sr.

no.

Criteria Nailesh

Dalal

Pargro

Investment

Pvt Ltd

S.K.

Finance

Dhiraj

Kenia

Bharat

Kenia

Kunverji

Kenia

Hriday

Nailesh

Dalal

Naishadh v.

Vachharajani

1

Period of

holding

over 6

months (avg) 1 to 9 months 106 days 107 days 116 days 124 days over 6 months 2 to 5 months

2

No. of scripts

purchased 41 79 51 129 142 213 25 2,00,066 shares

traded

3

No. of scripts

sold 49 79 49 105 168 173 25

4

Value of

purchases (Amt

in lakh) 250.38 368.24 79.16 153.70 272.94 2008.45 21.38 104.33

5

Value of sales

(Amt in lacs) 432.72 487.94 79.35 131.47 369.83 1059.95 23.90 117.81

6

No. of purchase

days 49 56 315 261 236 177 222 transactions

7 No. of sale days 68 45 312 240 202 162

Case Laws Summary

5

YOGESH THAR

Case Laws Summary (contd…)

Case laws referred to in the Chart:

Nailesh Dalal (ITA No. 3337/M/2009)

M/s Pargro Investments Pvt. Ltd. v. ITO (ITA No. 829/M/2010,ITA No.637/M/2010)

M/s S.K. Finance v. Dy. CIT (ITA No.6190/M/2008)

Bharat Kunverji Kenia v. ACIT (130 TTJ 86)

Kunverji Nanji Kenia v. ACIT (43 SOT 87)

ITO v. Hriday Nailesh Dalal (ITA No. 3469/M/2009)

ACIT v. Naishadh V. Vachharajani (ITA No.6429/M/2009)

6

YOGESH THAR

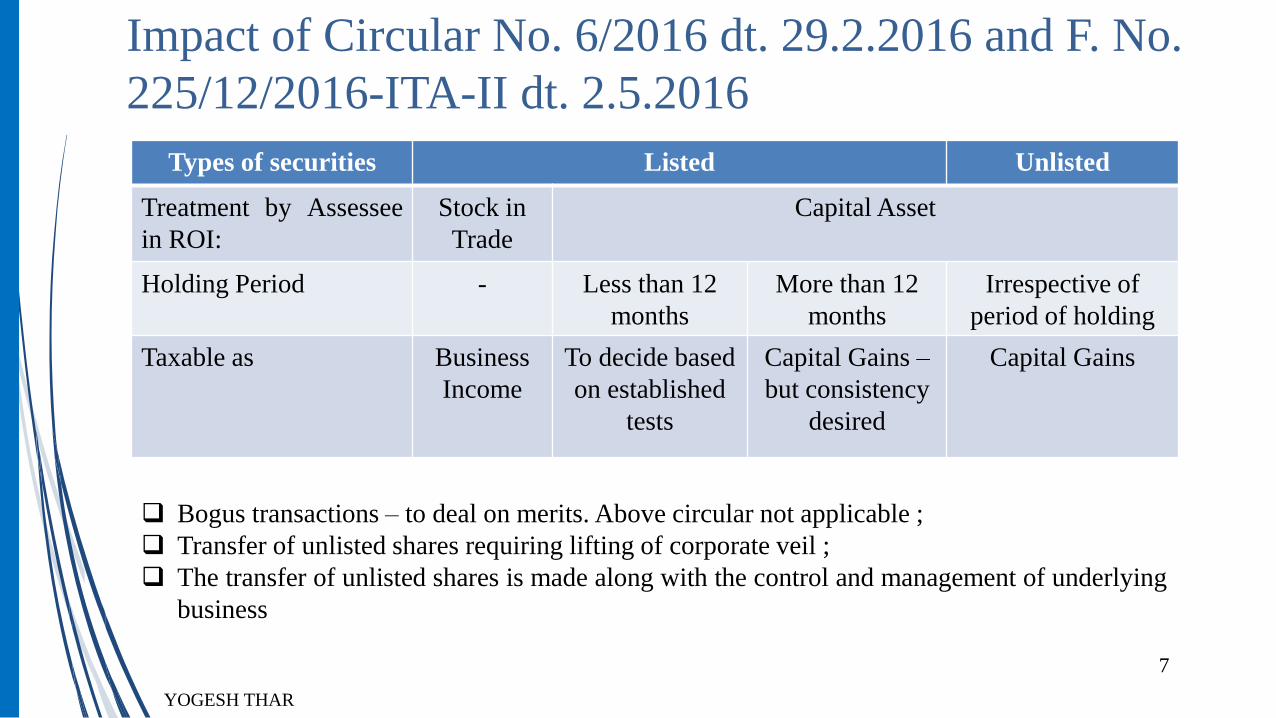

Impact of Circular No. 6/2016 dt. 29.2.2016 and F. No.

225/12/2016-ITA-II dt. 2.5.2016

7

Types of securities Listed Unlisted

Treatment by Assessee

in ROI:

Stock in

Trade

Capital Asset

Holding Period - Less than 12

months

More than 12

months

Irrespective of

period of holding

Taxable as Business

Income

To decide based

on established

tests

Capital Gains –

but consistency

desired

Capital Gains

Bogus transactions – to deal on merits. Above circular not applicable ;

Transfer of unlisted shares requiring lifting of corporate veil ;

The transfer of unlisted shares is made along with the control and management of underlying

business

YOGESH THAR

Transfer of “Control and Management” alongwith the

shares

Ramnarain Sons (P.) Ltd. v. CIT (41 ITR 534) (SC)

If the shares were acquired for obtaining control over the managing agency of the Mills, the

fact that the acquisition of the shares was integrated with the acquisition of the managing

agency did not affect the character of the acquisition of the shares

Shares acquired formed a capital asset

The loss suffered by sale of some of those shares in the year of account is a capital loss

8

YOGESH THAR

Bonus Stripping

Dividend stripping is covered under specific s. 94(7). However, Bonus stripping not

covered

Intention at the time of acquisition – A vital factor in determining the nature of

investment – Whether capital asset or stock-in-trade

Acquisition of shares with a view to sell them post issue of bonus – To claim STCL

Bonus shares sold after 12 months amounts to LTCG (earlier exempt - Now subject to

10% tax)

Overall – Commercial gain

Can the Department treat the transaction of acquisition as “business” on the ground

that the intention at the time of purchase is to sell?

9

Can GAAR provisions be invoked ?

YOGESH THAR

Finance Act, 2018 – ICDS VIII

ICDS VIII - Securities held as stock-in-trade to be valued at lower of cost or NRV - To

determine category-wise (For other than Banks)

Held - Contrary to Accounting Standards

Pre-amended s. 145A - non-obstante clause

Delhi HC - Held ICDS ultra vires

S. 145A substituted by FA 2018

10

YOGESH THAR

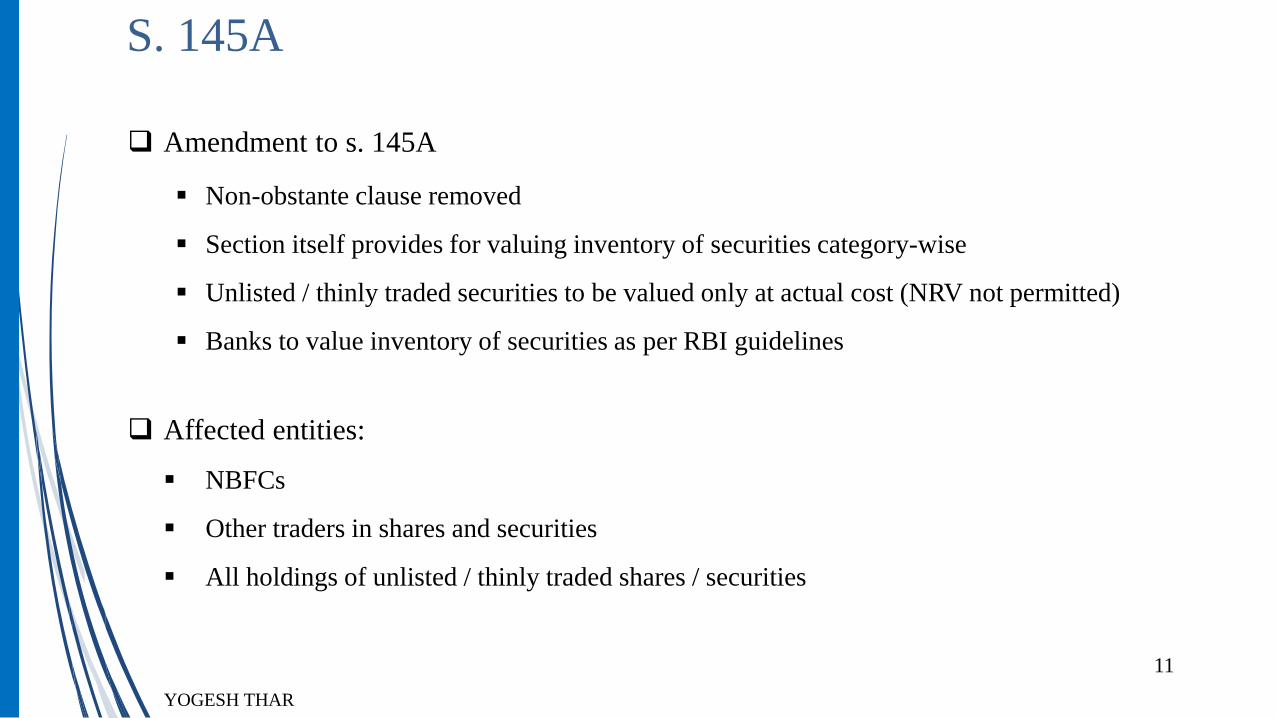

S. 145A

Amendment to s. 145A

Non-obstante clause removed

Section itself provides for valuing inventory of securities category-wise

Unlisted / thinly traded securities to be valued only at actual cost (NRV not permitted)

Banks to value inventory of securities as per RBI guidelines

Affected entities:

NBFCs

Other traders in shares and securities

All holdings of unlisted / thinly traded shares / securities

11

YOGESH THAR

S. 145A (contd…)

Units of mutual funds held as S-I-T

Securities “not listed on BSE”

Hence, covered under the mischief of this amendment

12

YOGESH THAR

S. 145A (contd…)

13

Individual Security Cost NRV Lower

Company P 150 20 20

Company Q 150 45 45

Company R 150 15 15

Company S 150 300 150

600 380 230

Valuation (A.S.) 230

Valuation (under 145A) 380

Illustration of impact: NRV has to be done category wise not individual asset wise.

YOGESH THAR

2. Ind-AS – Impact on taxation of transaction in

securities

Investment in Units of Equity Mutual Fund

AS 13: Value long term investments at cost - Long term diminution to be recorded at

NRV

Ind AS 109:

Financial Assets measured at Amortised Cost:

• Hold FA to collect contractual cash flows

• Contractual cash flows = Principal + Return

Financial Asset measured at FVTOCI

• Hold FA to collect contractual cash flows + Sale

• Contractual cash flows = Principal + Return

Other Financial Assets – Measured at FVTPL (Exception: Equity instruments – Option to

FVTOCI)

EAC Opinion: Equity Mutual Fund Units are NOT Equity instruments. Hence, FVTPL

is mandatory

15

YOGESH THAR

Purpose of MAT

Hon’ble Finance Minister’s speech explaining the rationale for introducing s.

80VVA in the year 1983, vide Finance Act, 1983 -

“Hon’ble Members must be aware of the phenomenon of companies which are flourishing,

but are paying no tax at all, or only nominal tax. This is largely due to these companies

availing of the tax incentives and concessions available under the provisions of the Income-

tax Act. It has been a matter of concern to us that our tax system several highly profitable

companies are able to reduce their tax liability to zero even though they continue to pay high

dividends. It seems reasonable that profitable and prosperous companies should contribute

at least a small portion of their profits to the national exchequer at a time when other and

less better off sections of society are bearing burden. I, therefore, propose to provide that

fiscal incentives and concessions shall not absorb more than 70 per cent of the profits. This

would secure that companies pay a minimum tax, on at least 30 per cent of their profits.”

16

YOGESH THAR

Purpose of MAT (contd…)

Para 83 of the Explanatory Memorandum to the Finance Bill, 1983

“With a view to securing that the various deductions in respect of tax concessions admissible

under the Income-tax Act do not result in reducing the taxable income of companies to the

extent that no tax or only negligible tax is paid by profit-making companies, it is proposed to

make a provision in the Income-tax Act to the effect that where in the case of companies the

aggregate amount of deductions admissible under certain specified provisions of the Income-

tax Act exceeds 70 per cent of the amount of total income computed before making such

deductions, the amount to be deducted under those provisions will be restricted to 70 per

cent of the total income as computed before making such deductions…”

17

YOGESH THAR

Purpose of MAT (contd…)

Rationale of s. 115J - Surana Steel Pvt Ltd. v. CIT (104 Taxman 188)

“Section 115J was introduced in the assessment year 1988-89 to take care of the

phenomenon of prosperous zero tax companies which had continued in spite of the

enactment of section 80VVA. There were companies which were paying no income-tax

though they had profits and were declaring dividends. A minimum corporate tax was sought

to be ensured on prosperous companies.”

Proviso to s. 123(1)(a) of the Companies Act, 2013 –

“Provided that in computing profits any amount representing unrealised gains, notional gains or

revaluation of assets and any change in carrying amount of an asset or of a liability on measurement of

the asset or the liability at fair value shall be excluded, or”

18

YOGESH THAR

Purpose of MAT (contd…)

1st Report of the MAT-Ind AS Committee (under the convenorship of M P Lohia)

dated March 18, 2016 :

“2. The provisions of section 115JB of the Act provide for levy of MAT on the basis of "book

profit" i.e. the net profit disclosed in the profit and loss account prepared in accordance with

the provisions of the Companies Act. For determining the book profit, section 115JB of the

Act provides for certain adjustments mainly for items relating to income-tax, appropriation

of profit, adjustment for brought forward loss/unabsorbed depreciation, revaluation of

assets, distribution of dividend, etc. The adjustment for brought forward loss/unabsorbed

depreciation is provided on the basis of the provisions contained in section 205 of the

Companies Act, 1956 which provides computation machinery for determining the amount

available for distribution of dividend. The adjustments indicate that the provisions of section

115JB of the Act seek to compute the realised profit before tax which is available for

appropriation/distribution. Hence, there appears to be an implicit relation between the

distributable profits which is available for payment of dividend under the Companies Act

and the tax base for levying MAT under section 115JB of the Act.”

19

YOGESH THAR

One-time Settlement Agreement

Co. A (facing financial difficulties) has a loan liability of Rs. 100 currently repayable

Bank B agreed to convert the loan liability to 0.01% preference shares (face value of

Rs. 100) which will be redeemed at par after 10 years

On the date of conversion, the fair value of preference shares amounts to Rs. 40

Accordingly, Co. A to pass the following entry:

No dividend can be declared on Rs. 60 ;

If MAT levied on such amount, it will be against the objective of helping companies

which are facing financial difficulty

20YOGESH THAR

Entry

Loan Liability Dr. 100

To 0.01% Preference Shares 40

To Profit or Loss 60

Can Para 19 of Ind AS 1 be invoked?

YOGESH THAR

Accounting Policies and Changes

Deviation from Ind AS is permitted in extremely rare circumstances – Para 19 of

Ind AS 1 – “Presentation of Financial Statements”

“In the extremely rare circumstances in which management concludes that compliance with

a requirement in an Ind AS would be so misleading that it would conflict with the objective

of financial statements set out in the Framework, the entity shall depart from that

requirement in the manner set out in paragraph 20 if the relevant regulatory framework

requires, or otherwise does not prohibit, such a departure.”

Objectives of Financial Statements – Framework for the Preparation and

Presentation of Financial Statements in accordance with Ind AS (“Framework”)

To provide information about financial position, performance and cash flows

To provide information that users may need to make economic decisions

21

YOGESH THAR

Demergers

Resulting Company (Not under common control):

Required to record the assets and liabilities at fair values

Contrary to s. 2(19AA)

Can Scheme provide for recording at Book Values? Auditors’ certificate?

Way out?

• Two stage accounting treatment

• 1st stage: Record at Book Values

• 2nd stage: Bring it in line with Ind AS

22

YOGESH THAR

Debentures (Profit or Loss)

Assume Co. A invested Rs. 150 in debentures (maturity = 5 years) of Co. B on April 1,

2015

Under AS, Co. A had recorded Rs. 150 as long-term investments (as per AS 13)

Under Ind AS 32 / 109, Co. A elected to measure the investment at fair value through

profit or loss

The fair value of such investments is as under:

Co. A to pass the following entry on April 1, 2017 (transition date)

23

Dates Fair Value

April 1, 2017 120

March 31, 2018 110

Retained Earnings 30

To Investment in Debentures (Rs. 150 – Rs. 120) 30

YOGESH THAR

Debentures (Profit or Loss) (contd…)

On March 31, 2018, Co. A to pass the following entry:

Under AS, if the amount of Rs. 40 were to be debited to the Statement of Profit or Loss

as provision for diminution in the value of asset, it would have to be added back as per

clause (i) of Explanation 1 to s. 115JB

Would the above position change u/s. 115JB for Ind AS compliant companies or would

Rs. 40 be deducted from the book profits?

Yes - The amount of Rs. 40 would be considered as transition amount and be deducted from

book profits over 5 years – Q. 1 r.w. Q. 6 of the CBDT Circular 24/2017 dated July 25, 2017

24

Profit or Loss 10

To Investment in Debentures (Rs. 120 – Rs. 110) 10

YOGESH THAR

2. Re-introduction of long term capital gains tax

Exemption of LTCG arising on transfer of Equity shares; unit of equity oriented fund, unit of business

trust on transfer happening on or after October 1, 2004, subject to payment of STT

No exemption for MAT

PROVISIONS FOR & UPTO A.Y. 2017-18

Exemption from LTCG arising on sale of equity shares which were acquired on or after October1, 2004 only if:

a) STT is paid on acquisition; or

b) The transaction is notified as exempt

PROVISIONS for A.Y. 2018-19

Provisions prior to introduction of s. 112A

26

YOGESH THAR

• Chargeable under thehead capital gains

Income

• An equity share in acompany or

• Unit of an equityoriented fund or

• Unit of a businesstrust

Asset transferred

• Acquisition andtransfer, in case ofLTCA being anequity share

STT has been paid

Tax Computation = Long term capital gains would be taxed @ 10% in excess of Rs. 1 lakh

S. 112A – Applicability (from AY 2019-20)

27

YOGESH THAR

Analysis

Indexation benefit and benefit of exchange fluctuation as provided in the 1st and 2nd

proviso to s. 48 not to be applicable to LTCG as computed u/s. 112A (3rd proviso to s.

48)

Benefit of grandfathering u/s. 55(2)(ac) - Applicable for shares acquired on or before

February 1, 2018

CBDT vide notification dated April 24, 2018 - specifies the nature of acquisitions in

respect of which STT need not have been paid to avail the provision of S. 112A.

28

YOGESH THAR

Start

NN

YY

Was

acquisition

< 1.10.2004

Acquisition in

delisting periodWas STT

paid on

acquisition

Was STT paid on transfer

Not frequently

traded?

Was share

listed on date

of acquisition

Y

N

Y

N Preferential

issueAcqn

on

RSE

Permissi

ble

Mode B

(1 to 8)

Permiss

ible

Mode

B(9)

N

Y

Permissible Mode A

N N N

Y Y

Y

Y

Run Chart

Test For P.O.

Y Y

N

P.O. Result

112A N.A.

Apply S.112

Section 112A applies

COA- s. 55(2)(ac)

N

30

Sr. Exceptions to Clause (a) – Acquisition through a preferential issue - Shares not frequently traded

1. Acquisition which has been approved by SC, HC, NCLT, SEBI or RBI

2. Acquisition by any non-resident in accordance with FDI guidelines issued by the Government of India

3. Acquisition by a Category I or Category II Alternate Investment Fund (AIF) or a Venture Capital Fund (VCF) or a Qualified

Institutional Buyer (QIB)

4. Acquisition through a preferential issue to which provisions of Chapter VII of the ICDR Regulations, 2009 do not apply –

• Conversion of loan or option attached to convertible debt instruments in terms of s. 81(3) and 81(4) of the Companies

Act, 1956 or s. 62(3) and 62(4) of the Companies Act, 2013;

• Scheme approved by a HC (u/s. 391 to 394 of the Companies Act, 1956) or NCLT (u/s. 230 to 234 of the Companies

Act, 2013)

• Rehabilitation scheme approved by Board of Industrial and Financial Reconstruction under the Sick Industrial

Companies (Special Provisions) Act, 1985 or NCLT under the Insolvency and Bankruptcy Code, 2016; and

• Acquisition by secured lenders pursuant to conversion of their debt into equity shares under the strategic debt

restructuring scheme in accordance with the guidelines specified by the RBI

YOGESH THAR

Mode A

31

Sr. Exceptions to Clause (b) – Acquisition not through a RSE

1. Acquisition through an issue of share by a company other than preferential issue of non-frequently traded shares

2. Acquisition by scheduled banks, reconstruction or securitisation companies or public financial institutions during their

ordinary course of business

3. Acquisition which has been approved by the SC, HC, NCLT, SEBI or RBI in this behalf

4. Acquisition under employees stock option scheme or employee stock purchase scheme framed under the SEBI

(Employee Stock Option Scheme and Employee Stock Purchase Scheme) Guidelines, 1999

5. Acquisition by any non-resident in accordance with FDI guidelines of the Government of India

6. Acquisition of shares of company under SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011

7. Acquisition from the Government

8. Acquisition by a Category I or II AIF or a VCF or a QIB

9. Acquisition by mode of transfer referred to in s. 47 (transactions not regarded as “transfers”) or s. 50B (slump sale) of

the Act if the acquisition by the previous owner was not an Improper Acquisition

YOGESH THAR

Mode B

A long-term capital asset, referred in s. 112A, acquired before the 1st day of February,

2018 shall be:

Higher of : (i) Cost of Acquisition of the long term capital asset; or

(ii) Lower of : (i) - Fair market value of the long term capital asset or

(ii)- Full value of consideration received or accrued

Asset Transferred Determination

1) Listed on the RSE as on 31.1.18 Highest price quoted on that date

2) Not Listed on the RSE as on 31.1.18, but listed on date of transfer COA * CII of FY 17-18

CII of Year of acquisition or

2001 whichever is later3) Listed on date of transfer and which became the property of the assessee in

consideration of share which is not listed on such exchange as on the 31st day of

January, 2018 by way of transaction not regarded as transfer u/s. 47

Determination of Fair market value

Determination of Cost of Acquisition u/s. 55(2)(ac)

32

YOGESH THAR

Illustrations (1/3)

As per clause (b)(ix) of the Notification, if the previous owner has acquired the shares through

qualifying acquisitions, the assessee is covered by the said notification

Therefore, if the provisions of s. 112A were applicable to the previous owner, the provisions of s.

112A would apply to the donee

COA - Cost to previous owner, FMV as on 31.1.18, Grandfathering allowable

No indexation benefit

33

Particulars

Date of Transfer June 1, 2018

STT paid on acquisition No

Listed on date of transfer Yes

Date of acquisition April 2018

Mode of acquisition Gift

YOGESH THAR

Particulars

Date of Transfer July 2018 in Offer for Sale in IPO

STT paid on acquisition No

Listed on date of transfer No, but STT payable u/s 97(13) of FA

2004

Date of acquisition April 1996

Section 112A would apply. Therefore indexation not available.

Computing COA- Since, the shares not listed on the date of transfer, grandfathering u/s 55(2)(ac) not

available (Expln (a)(iii)(A) and (B) apply only to shares listed on date of transfer.

However, substitution of FMV as on 1.4.2001 available because 55(2)(ac) is “subject to” 55(2)(b)

34

Illustrations (2/3)

YOGESH THAR

Particulars Demerged Company Resulting Company

Date of Transfer 1 January 2019 1 January 2019

Listed or unlisted Unlisted Listed in December 2018

Listed on date of transfer No Yes

Date of acquisition Prior to 1.4.2001 Record date –November 2018

112A would apply No Yes

Indexation Yes, since covered by section 112 No

Grandfathering available NA No, since 55(2)(ac) applies for acquisition of

securities referred to in 112A, prior to 1.2.2018

FMV as on 1.4.2001 – whether

available

Yes. Bifurcation of COA as per s. 49(2C)

is done after substituting FMV as on

1.4.2001

Yes

Co A has demerged its Real estate Undertaking to Co B, with Appointed Date being 1.4.2018,

In consideration of the demerger, Co B has issued its shares to shareholders of Co. A.

A shareholder transfers shares of both the companies, COA to be as per s.49(2C)

35

Illustrations (3/3)

YOGESH THAR

4. Section 50CA& Section 56(2) & Valuation

Rules?

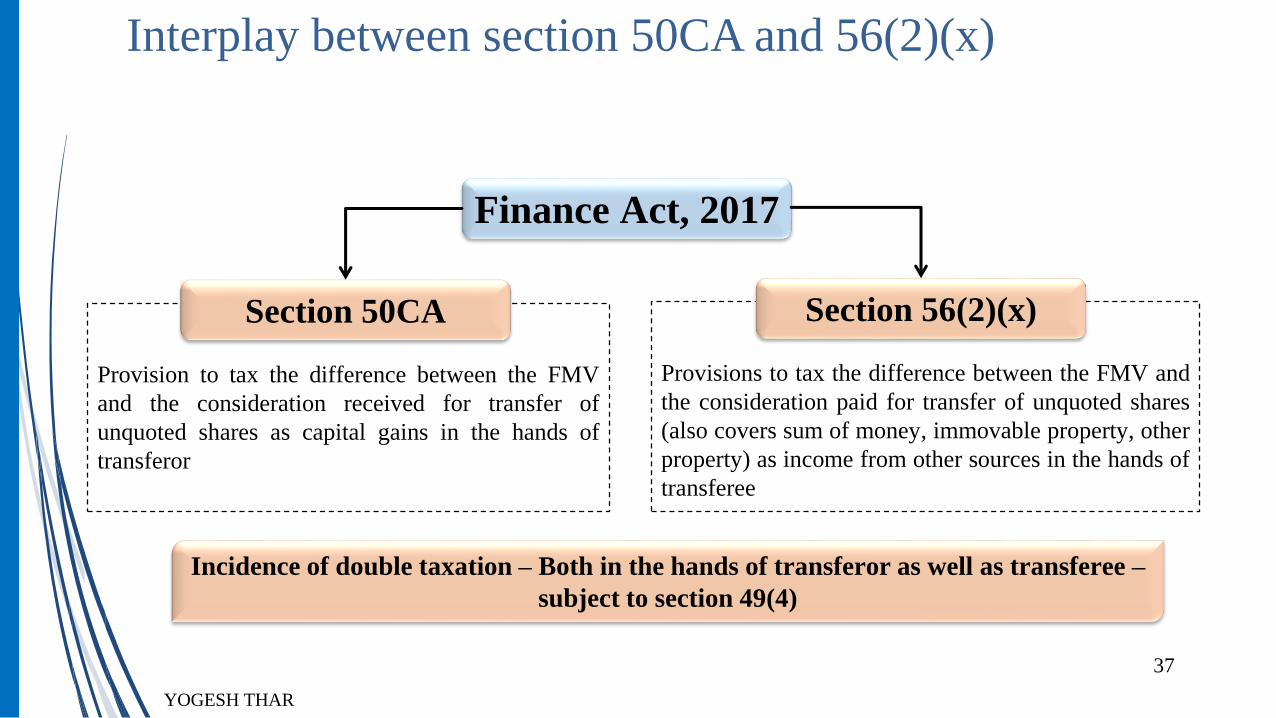

Interplay between section 50CA and 56(2)(x)

Provision to tax the difference between the FMV

and the consideration received for transfer of

unquoted shares as capital gains in the hands of

transferor

Section 50CA

Provisions to tax the difference between the FMV and

the consideration paid for transfer of unquoted shares

(also covers sum of money, immovable property, other

property) as income from other sources in the hands of

transferee

Section 56(2)(x)

Finance Act, 2017

YOGESH THAR

37

Incidence of double taxation – Both in the hands of transferor as well as transferee –

subject to section 49(4)

YOGESH THAR

Interplay between section 50CA and 56(2)(x) (contd…)

Transferee/Buyer : A Ltd.

Transferor/Seller : B Ltd.

A Ltd. purchased 100 shares of a private company from B Ltd. for a price of INR 600 per share;

total consideration = INR 60,000

B Ltd. had acquired such shares at INR 500 per share; gross amount paid = INR 50,000

Say, the FMV of said shares on transfer date is INR 700

Example

37

What would be the implications of provisions of section 50CA and 56(2)(x) under the

mentioned circumstances ?

YOGESH THAR

Interplay between section 50CA and 56(2)(x) (contd…)

Prior to amendment

Post amendment

FMV 70,000

Less: Cost of acquisition (50,000)

Capital gains 20,000

Impact of Sec. 50CA

Transferor – B Ltd.

FMV of shares 70,000

Less: Actual consideration (60,000)

IFOS 10,000

Impact of Sec. 56(2)(x)

Transferee – A Ltd.

Sale consideration 60,000

Less: Cost of acquisition (50,000)

Capital gains 10,000

Impact on Transferor – B Ltd.

No impact

Impact on Transferee – A Ltd.

39

YOGESH THAR

Interplay between section 50CA and 56(2)(x) (contd…)

Impact u/s 49(4) :-

When A Ltd sells the shares at (say) Rs.800 (which is also its FMV) ;

FMV of shares (when sold) 80,000

Less: FMV(when purchased) (70,000)

Capital gains 10,000

40

YOGESH THAR

50CA presupposes consideration

Applicability of the provisions in the absence of consideration

In case no consideration is received or accruing, section is not applicable :-• Transfer by a partner to the firm as capital consideration ;

In case of a gift (no consideration at all) ;• No capital gains, therefore section is not applicable

Transfer should be in relation to transfer of a “capital asset” only

41

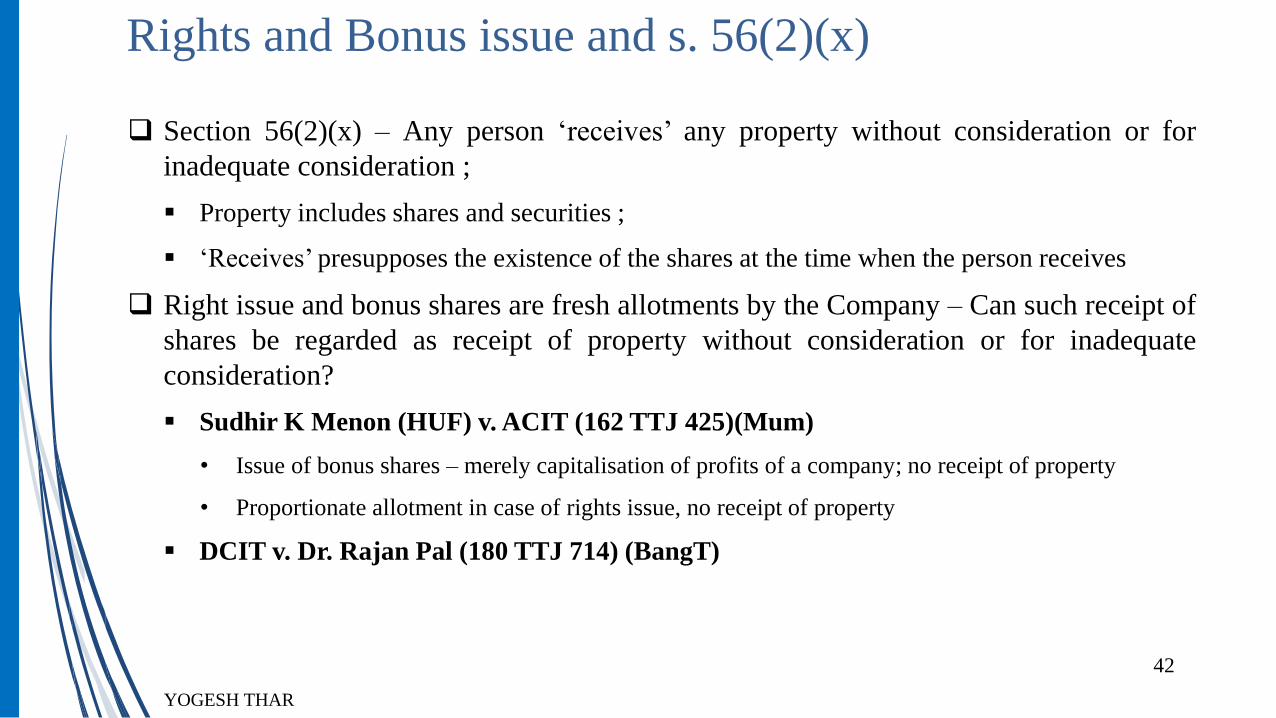

Rights and Bonus issue and s. 56(2)(x)

Section 56(2)(x) – Any person ‘receives’ any property without consideration or for

inadequate consideration ;

Property includes shares and securities ;

‘Receives’ presupposes the existence of the shares at the time when the person receives

Right issue and bonus shares are fresh allotments by the Company – Can such receipt of

shares be regarded as receipt of property without consideration or for inadequate

consideration?

Sudhir K Menon (HUF) v. ACIT (162 TTJ 425)(Mum)

• Issue of bonus shares – merely capitalisation of profits of a company; no receipt of property

• Proportionate allotment in case of rights issue, no receipt of property

DCIT v. Dr. Rajan Pal (180 TTJ 714) (BangT)

YOGESH THAR

42

Convertible Instruments and s. 56(2)(x)

Receipt of equity shares is in ‘consideration’ of extinguishment of rights in bonds/preference

shares :-

Hence, not without consideration ;

Also not inadequate consideration – sacrifice = gain ;

Ratio of CIT v. Bai Shrinibai K. Kooka (46 ITR 86) (SC) and CIT v. Groz-Beckert Saboo

(116 ITR 125) (SC)

Taxing event arises when convertible instrument is issued. Upon conversion:

Mere working out of pre-exiting rights of the investor or mere discharging of pre-existing

obligation by the issuer

Ratio of CIT v Mohanbhai Pamabhai (165 ITR 393) and CIT v. R.M. Amin (106 ITR 368)

(SC)

YOGESH THAR

43

Other Issues

What would be the position in case of buy-back of shares?

M/s. Vora Financial Services P. Ltd v. ACIT (ITA No. 532/Mum/2018)

What happens in case of rights renunciation?

Receipt of shares on amalgamation of foreign company – by virtue of holding shares in

amalgamated company –

Whether s. 56(2) applicable ?

Whether capital gains payable ?

YOGESH THAR

44

Empirical studies show that market value of equity shares of an investment company does not capture the full market

value of its investments in other companies. The value leakages are on account of distance of time and control of

ownership, which, thereafter results in an inevitable discount especially because of the economic concept of liquidity

preference which requires converting a future inflow to its present value by using a rate of discount. Also, erosion on

account of tax leakages normally get factored in such valuation. The rule is unrealistic and would result in notional

taxation in cases where the transaction has happened at fair value considering the above aspects.

Valuation of equity shares of a company which carries on business as a going concern cannot be made based on present

market value of its immovable property. Market value of an immovable property may be considered only in case the

valuation is for the purpose of liquidation, or when the property is in surplus and is not actively used in business.

For immovable property “the value adopted or assessed” will never exist in case of sale/transfer of shares of a company.

It will always be “the value assessable”. Indeed, value assessable as per ready reckoner/circle rate does not always reflect

the fair market value. There have to be enough safeguards like in s. 50C if Stamp Duty value is to be considered even for

share valuation.

Rules – Whether fair

YOGESH THAR45

Valuation in cases of cross holdings is not addressed in the rules ;

As per the rules, equity shares of a foreign company would be “unquoted equity share” even if it is

listed on a foreign stock exchange.

The rules come into force from 1.4.2018 – i.e. AY 18-19

Rule Notified on 12 July 2017. For Transaction between 1 April 2017 and 12 July 2017- will Rules apply;

The rules shall apply irrespective of the valuation methodology agreed upon in Shareholder’s

Agreement/ J.V. Agreement;

Issues on Rules

YOGESH THAR

46

The rules may apply irrespective of lock-in-period under such Shareholder’s Agreement/ J.V.

Agreement where internal transfer to Affiliates is permitted ;

Leasehold rights in land whether to be considered for computing the value of shares for the purpose of

section 56(2)(x) / 50CA r.w. Rule 11UA

Acquisition of shares in tranches – what would be the date of valuation

As per Rule 11U of the Rules “valuation date" means the date on which the property or consideration, as the

case may be, is received by the assessee

Question : In case of receipt of staggered consideration on different dates- what would be the date of valuation

YOGESH THAR

Issues on Rules (contd…)

47

FC 1Section 56(2)(x)

Where any person receives in any previous year, from

any person

• Receipt of shares by FC 2/ FC 1

Section 5

Since change of name in IC’s Share Register - the

receipt is in India

Falls within the scope of total income

Therefore receipt taxable in India u/s 56(2)(x)

Even in Case of WOS, FC1 is not an Indian Company

hence 56(2)(x) applicable

IC

Gifts shares of ICFC 2

FC 1

FC 2

IC

WOS Gifts shares of IC

YOGESH THAR48

Applicability to transfer of Indian company shares

between foreign companies either by way of gift or sale

FC 1

Section 56(2)(x)

Where any person receives in any previous year, from

any person

• Receipt of shares by FC (3)

Section 5

Since, the receipt is not in India, it is outside the scope

of total income

Section 9(1)

Income accruing or arising directly or indirectly

through the transfer of a capital asset situated in India

Taxability u/s 56(2)(x) is triggered on “receipt” and not

on “transfer”

IC

FC 2

Gifts shares

of FC 2

FC (3)

YOGESH THAR49

Applicability to transfer of Indian company shares

between foreign companies either by way of gift or sale

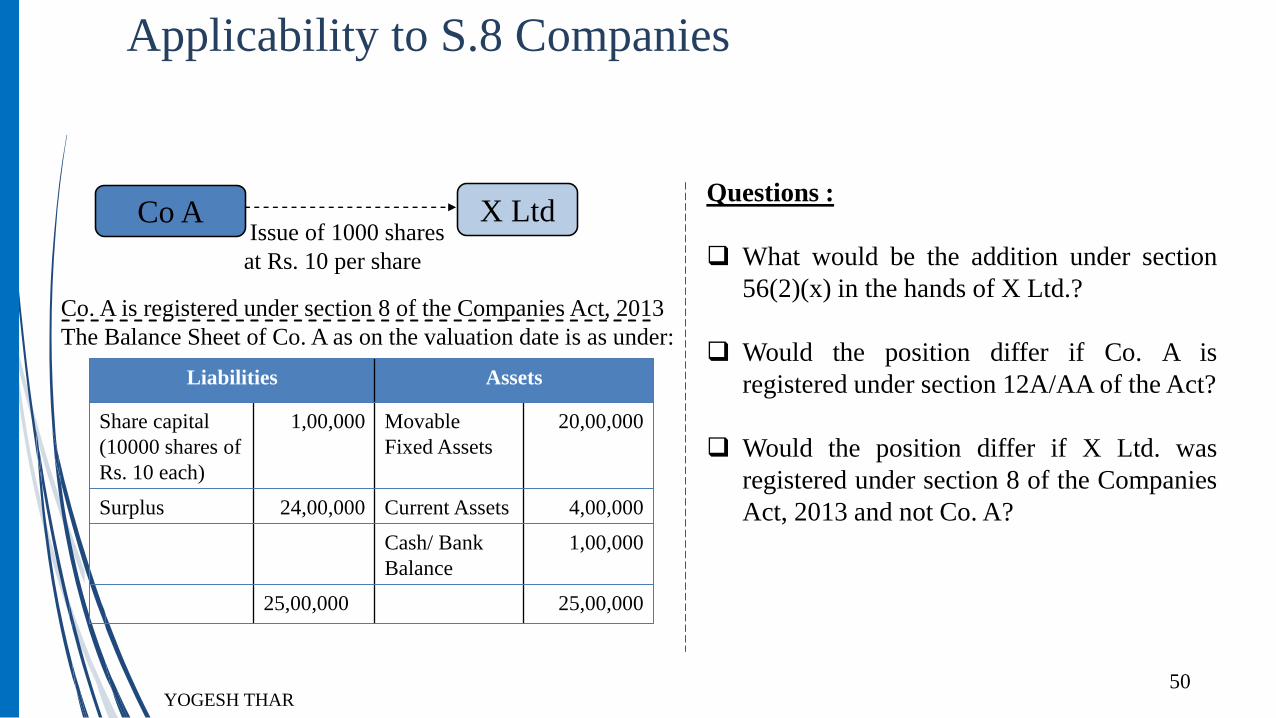

Co AQuestions :

What would be the addition under section

56(2)(x) in the hands of X Ltd.?

Would the position differ if Co. A is

registered under section 12A/AA of the Act?

Would the position differ if X Ltd. was

registered under section 8 of the Companies

Act, 2013 and not Co. A?

Issue of 1000 shares

at Rs. 10 per share

X Ltd

Co. A is registered under section 8 of the Companies Act, 2013

The Balance Sheet of Co. A as on the valuation date is as under:

Liabilities Assets

Share capital

(10000 shares of

Rs. 10 each)

1,00,000 Movable

Fixed Assets

20,00,000

Surplus 24,00,000 Current Assets 4,00,000

Cash/ Bank

Balance

1,00,000

25,00,000 25,00,000

YOGESH THAR50

Applicability to S.8 Companies

Questions :

Would Rule 11UA apply even in case of issue of

shares?

If yes, what would be the Rule 11UA value of the

shares issued to Mr. A? (Pre-issue: 600-10=590

for 5000 shares = 29,50,000

As against this, what would be the holding of Mr.

A in P Ltd. post acquisition of the shares?

Can addition under section 56(2)(x) exceed the

real benefit?

Liabilities Assets

Share capital

(5000 shares of

Rs. 10 each)

50,000 Plant &

Machinery

30,00,000

Loans 25,00,000 CAs 20,00,000

Surplus 29,50,000 Bank Balance 5,00,000

55,00,000 55,00,000

Balance Sheet of P Ltd. Pre issue

Net Worth of the company: A – L = Rs. 30,00,000

Value as per Rule 11UA: A – L = Rs. 600/share

No. of shares

Mr. A has been allotted 5000 shares of P Ltd. at face value on

preferential basis

YOGESH THAR51

Applicability of Rule- Pre or Post Issue

Liabilities Assets

Share capital

(10,000 shares of Rs. 10

each)

100,000 Plant & Machinery 30,00,000

Loans 25,00,000 CAs 20,00,000

Surplus 29,50,000 Bank Balance 5,50,000

55,50,000 55,50,000

Shareholding of Mr. A in P Ltd - 5000 shares

% shareholding of Mr. A in P Ltd. (5000/10000*100) 50%

Net worth of P Ltd. post issue of

shares

A-L : 55,50,000 – 25,00,000 Rs. 30,50,000

Value of shareholding of Mr. A based

on post – issue balance sheet

50% of 30,50,000 Rs. 15,25,000

Actual Benefit to Mr. A 15,25,000 – 50,000 Rs. 14,75,000

Addition u/s. 56(2)(x) based on pre-

issue balance sheet

30,00,000 – 50,000 Rs. 29,50,000

YOGESH THAR52

Applicability of Rule- Pre or Post Issue (contd…)

A Ltd Would Mr. Z be required to compute FMV of C Ltd.

while computing Rule 11UA value of A Ltd.?

If yes, as on which date?

Similarly, would he require to compute the fair

market value of B’s interest in P-LLP?

Would the position change if P-LLP held immovable

properties?

In case, A Ltd. holds leasehold rights in a plot of

land, would its fair market value be considered under

Rule 11UA?

C Ltd

B Ltd

P-LLP

Mr. Z is to purchase shares of A Ltd.

YOGESH THAR53

Multi layered shareholdings

5. TAXABILITY OF ESOPS

No income tax implication in the hands of the employee

Grant of Options

No income tax implication in the hands of the employee

Vesting of Options

Difference between fair market value and the exercise price - Taxed as perquisites

Determine FMV as per the Income-tax Rules, 1962

Tax deduction at source u/s. 192 of the Income-tax Act, 1961

Exercise of Options

55YOGESH THAR

Taxability of ESOPs

Capital gains tax liability - Difference between consideration received and cost of acquisition

Cost of acquisition = FMV taxed as perquisite

Determine period of holding from date of allotment / transfer

Sale of shares

ACIT v. Bharat V. Patel (Civil Appeal No. 4380 of 2018) (SC)

Amount received on redemption of SARs prior to amendment in s. 17(2) is not taxable as perquisite in

the absence of an express provision of retrospective effect

Further, the said amount is not taxable u/s. 28(iv) since s. 28 only deals with any business or

profession related transactions

Recent development in taxability of Stock

Appreciation Rights (SARS)

56YOGESH THAR

Taxability of ESOPs (contd…)

Issues under DTAA

Timing mismatch in taxing the ESOP benefit

Distinguishing employment income from Capital Gains

Difficulty in linking ESOP benefit to employment

Difficulty due to exercise of employment in multiple states

Multiple residence taxation

Compliance issue

YOGESH THAR57

Deductibility of ESOP expenses

Accounting treatment and SEBI guidelines permit amortisation

Allowability u/s. 37: Law getting settled in favour of allowability of the amount debited to

P&L…

Allow –

• CIT v. PVP Ventures Ltd. [TC (A) No. 1023 of 2005 (Mad HC)]

• CIT v. Lemon Tree Hotels Ltd. (ITA No. 107/2015) (Del HC)

• CIT v. People Interactive India P. Ltd. (ITA Nos. 6990, 6986, 4979/M/2015)

Quantum of deduction –

• Biocon Ltd. v. DCIT (ITA Nos 368/369/370/371/1206/Bang/2010)

YOGESH THAR58

Deductibility of ESOP expenses (contd…)

No cash payout by Indian company to foreign parent of discount amount incurred by

foreign parent – Whether deductible by Indian company?

Indian company issues shares to employees of foreign subsidiary at discount – Whether

deductible by Indian company?

Transfer Pricing implications?

YOGESH THAR60

Hold Co. grants 200 share options to each of 100 employees of Sub Co., conditional upon the

completion of 2 years’ service with Sub Co

The fair value of the share options on grant date is Rs. 30 each

At grant date, Sub Co. estimates that 80% of the employees will complete 2-year service period

At the end of the vesting period, 81 employees complete 2 years’ of service

Hold Co. does not require Sub Co. to pay for the shares needed to settle the grant of share

options

Sub Co. to pass the following entries as per Ind AS 102:

Year 1

Remuneration expense 2,40,000

To Other Equity (Deemed Capital Contribution) 2,40,000

(200 options x 100 employees x Rs. 30 x 0.8/2 years)

60

YOGESH THAR61

Ind AS – MAT implications

Hold Co. to pass the following entries as per Ind AS 102:

Sub Co.

Amount debited to profit or loss as remuneration expenses – Allowable under MAT

Amount credited to Other Equity – Taxable under MAT if suggestion of Ind AS Committee Report is

accepted - Therefore, net impact on book profits will be NIL

Hold Co.

No amount is debited / credited to profit or loss. Therefore, no question of MAT

However, amount credited to ESOP O/s. Account will form part of Other Equity – Will credit be

taxable under MAT if suggestion of Ind AS Committee Report is accepted ?

Year 1

Investment in Sub Co. 2,40,000

To ESOP O/s Account 2,40,000

(200 options x 100 employees x Rs. 30 x 0.8/2 years)

YOGESH THAR59

Ind AS – MAT implications (contd…)

6. GAAR applicability to transactions in securities - in

particular for FPIs?

Central Board of Direct Taxes (“CBDT”) has issued the said circular providing clarification on

implementation of GAAR

“Question no. 4: Will GAAR apply where the jurisdiction of FPI is based on non-tax

commercial consideration, and such foreign portfolio investor

(FPI) has issued P-notes referencing Indian securities? Will GAAR

apply to deny treaty benefits to a Special Purpose Vehicle (SPV) on

the ground that it is located in a tax friendly jurisdiction, or on the

ground that it does not have its own premises or employees?

Answer: GAAR shall not be invoked merely on the ground that the entity is

located in a tax efficient jurisdiction. If the jurisdiction of the FPI

is finalised based on non-tax commercial considerations and the

main purpose of the arrangement is not to obtain tax benefit,

GAAR will not apply.

YOGESH THAR63

Circular no.7 of 2017 dated 27/01/2017

Draft guidelines for GAAR implementation under Direct Tax

Code Bill, 2010 (“DTC”)

A foreign investor has invested in India through a holding company situated in a low tax

jurisdiction “X”

The holding company is doing business in the country of incorporation, i.e. “X‟, has a Board

of Directors that meets in that country and carries out business with adequate manpower,

capital and infrastructure of its own and therefore, has substantial commercial substance in the

said country “X”

Would GAAR be invocable or would the arrangement be permissible ?

In view of the factual substantive commercial substance of the arrangement, Revenue would

not invoke the GAAR provisions.

YOGESH THAR64

As per section 97 of the Act :

An arrangement shall be deemed to lack commercial substance, if—

…….

a transaction which is conducted through one or more persons and disguises the value,

location, source, ownership or control of funds which is the subject matter of such

transaction

YOGESH THAR65

Under the Act

A Ltd.

Mechanics :

It is proposed to sell the shares of “C Ltd” to another

company “D Ltd”;

In case the shares of C Ltd are directly sold to D Ltd, B Ltd

would be liable to tax in India.

Plausible option :

B Ltd. is liquidated and A Ltd being the shareholder of B Ltd

would be liable to tax u/s 46(2) of the Act ; but A Ltd. can

avail the treaty benefit (assuming grandfathering) and such

liquidation proceeds would be taxable in country of residence

– Country A;

Subsequently, A Ltd. sells shares of C Ltd. to D Ltd.

There would be negligible capital gains on such transfer in

India, since COA of shares in C Ltd. would be the FMV on

the date of liquidation of B Ltd.

100%

C Ltd.

B Ltd.

49%

Country A

India

Transfer of shares not chargeable to tax in

Country A

YOGESH THAR66

Case Study

Can GAAR provisions be invoked

FACTS :

The India-F1 tax treaty provides for non-taxation of

capital gains in the source country and country F1

charges no capital gains tax in its domestic law.

A Ltd is also designated as “ permitted transferee”

of Y Ltd. “ Permitted transferee” means that though

shares are held by A Ltd, all rights of voting,

management, right to sell etc., are vested in Y Ltd.

As per the joint venture agreement, 49% of X Ltd’s

equity is allotted to A Ltd and 51% is allotted to Z

Ltd.

Thereafter, the shares of X Ltd held by A Ltd are

sold to C Ltd., a company connected to Z Ltd.

group.

As per the tax treaty with country F1, capital gain

arising to A Ltd are not taxable in India.

Country- C1

India

Country- FI- LTJ

Y Ltd

51%

100%

DebtZ Ltd

A Ltd

X Ltd

49%

Y Ltd is a company incorporated in country C1 and is a

non-resident in India.

Z Ltd is a company resident in India.

A Ltd. is a company incorporated in country F1 and it is a

100% subsidiary of Y Ltd.

A Ltd and Z Ltd form a joint venture company X Ltd in

India after the date of commencement of GAAR

provisions. There is no other activity in A Ltd;

Can GAAR provisions be invoked

YOGESH THAR67

Example-10- Final Report on GAAR in the Act

The arrangement of routing investment through country F1 results into a tax benefit. Since there is no

business purpose in incorporating company A Ltd. in country F1 which is a LTJ, it can be said that the

main purpose of the arrangement is to obtain tax benefit. The alternate course available in this case is

direct investment in X Ltd. joint venture by Y Ltd. The tax benefit would be the difference in tax

liabilities between the two alternate courses.

The next question is, does the arrangement have any tainted element? It is evident that there is no

commercial substance in incorporating A Ltd. as it does not have any effect on the business risk of Y

Ltd. or cash flow of Y Ltd. As the twin condition of main purpose being tax benefit and existence of a

tainted element are satisfied, GAAR may be invoked.

Additionally, as all rights of shareholders of X Ltd are being exercised by Y Ltd instead of A Ltd. it

again shows that A Ltd. lacks commercial substance. Hence, GAAR may be invoked.

68YOGESH THAR

Analysis

7. Penny stocks

Total income of an assessee :

includes any income referred to in section 68, section 69, section 69A, section 69B, section 69C or section

69D and reflected in the return of income furnished under section 139; or

determined by the Assessing Officer includes any income referred to in section 68, section 69, section

69A, section 69B, section 69C or section 69D, if such income is not covered under clause (a)

No deduction in respect of any expenditure or allowance or set off of any loss allowed in computing

the income u/s 115BBE

S.271AAC provides for a penalty of 10% of the tax payable under section 115BBE, in case an addition

has been made by the AO. No penalty would be leviable if assessee suomotu makes an addition in the

return of income;

Taxability u/s.115BBE

YOGESH THAR

Tax Computation = on the income computed above @ 60%

Thus effective tax Computation = tax @ 60%+ penalty @10%= effective tax rate =66%

70

The shares are traded on the Stock Exchange

The payments and receipts are routed through the bank

There is no evidence to indicate it is a closely held company

The trading on the Stock Exchange was not manipulated

Safeguards against transactions being treated as fictitious

Lack of adverse material produced by the Department

71YOGESH THAR

Contract notes for sale and purchase

Bank statements of broker

Demat account showing transfer in and out

Abstract of transactions furnished by stock exchange

Audited Balance sheet of previous years

Documents required to prove genuineness

72YOGESH THAR

Judicial Analysis

In favour of the assessee:

Pr CIT vs. Prem Pal Gandhi (P&H High Court)(ITA-95-2017)

Shyam R Pawar v CIT (229 Taxman 256 (Bom HC)

CIT v Jamna Dev Agarwal (328 ITR 656) (Bom HC)

CIT v Vivek Mehta (204 Taxmann 177) (P&H HC)

CIT v Mahesh Chandra G. Vakil (220 Taxmann 166) (Guj HC)

Smt. Anjli Pandit v ACIT (188 TTJ 645) (Mumbai - Trib.)

ITO v Arvind Kumar Jain HUF (ITA No. 4862/Mum/2014)

In favour of the revenue:

Sanjay Bimalchand Jain v PCIT (89 taxmann.com 196) (Bom HC)

ITO v Shamim M Bharwani (170 TTJ 238)(MumT)

73

YOGESH THAR

8. Transfer Pricing

Transfer Pricing

Inbound Investments

Whether subscription to shares of Indian Subsidiary by Foreign Co. considered as

‘international transaction’

Vodafone India Services (P.) Ltd v. UOI (368 ITR 1) (BOM)

• TP provisions only apply if there is chargeable income resulting from the transaction

• Capital investments, which do not create chargeable income, cannot therefore be brought within

the scope of transfer pricing provisions

75YOGESH THAR

Transfer Pricing (contd…)

Outbound Investments

Whether subscription to shares of Foreign Subsidiary by Indian Holding Company

considered as ‘international transaction’

M/s PMP Auto Components v DCIT (ITA 7724/Mum/2014)

• Investments in share capital outside India were in the nature of capital investments, and such

transactions are not in the nature of "international transactions" within the meaning of s. 92B

Whether Rule 11UA value is a proper benchmark for transfer pricing ?

FEMA requires internationally accepted valuation methodology ;

Whether transfer pricing provisions would apply for buy-back taxable u/s 115-QA

76YOGESH THAR

Thank You