Embed Size (px)

Citation preview

1

Bombardier Aerospace: The CSeries Dilemma Case written by Ali Taleb and Louis Hébert “Bombardier Aerospace announced today the name of its new commercial aircraft family and revealed the aircraft’s distinctive black and white livery. The CSeries, for Competitive, Continental, Connector, would target airlines operating aircraft in the lower end of the 100- to 150-passenger market, a large segment that is not well served by any aircraft in production today…”

Bombardier press release, 19 July 2004 “On March 15, 2005, Bombardier's Board of Directors granted Bombardier Aerospace authority to offer the new CSeries family of aircraft to customers. The authority to offer is an important step in the process that could lead to the aircraft program launch. Prior to launch, Bombardier will continue to seek firm commitments from potential customers and suppliers…”

Bombardier press release, 13 May 2005 “Bombardier announced today that present market conditions do not justify the launch of the CSeries program at this time. The Corporation will now reorient CSeries project efforts, team and resources to regional jet and turboprop aircraft opportunities to address regional airlines’ future needs in the 80- to 100-seat aircraft market...”

Bombardier press release, 31 January 2006

In March 2005, the Board of Directors of Bombardier Inc. (BI) authorized its Aeronautics division, Bombardier Aerospace, to offer a new generation of aircraft named CSeries to its clients. Since then, the company has postponed the actual launch of the project several times, which made investors and analysts wonder what the long-term strategy of the company was. As the date of the company’s annual meeting scheduled for May 29, 2007 was imminent, investors and industry analysts were expecting Pierre Beaudoin, president of Bombardier Aerospace, to clarify the company’s plans for CSeries during this meeting1.

Aerospace: A core business of Bombardier

Bombardier Inc., the parent company of Bombardier Aerospace, was headquartered in Montreal (Canada) since its inception by Joseph-Armand Bombardier in 1942. As its original name (Auto-Neige Bombardier Ltd.a) implied, the company specialized initially in developing and trading snowmobiles in its home province of Quebec. In May 2007, Bombardier’s activities were structured into two relatively independent divisions: Bombardier Aerospace (BA) which was the global leader in business and regional aircraft manufacturing; and Bombardier Transportation (BT) which was also a world leader in rail equipment.

a Auto-Neige stands for snowmobile in French.

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 2

Indeed, the strategic objective of Bombardier had always been to make both divisions global leaders in their respective markets. For instance, while BA was already the leading manufacturer of regional aircraft in 2001, Bombardier acquired the German DaimlerChrysler Rail Systems GmbH (ADtranz) and thus made BT the largest manufacturer of integrated rail equipment in the world2. However, Bombardier Inc. faced though times afterward essentially due to the crisis in the airline industry that followed the attacks on the World Trade Center. This led the company to rationalize its operations, lay off employees, and divest its recreational line of business including snowmobile and jetski products. The sale of this division – which represented the original business of the company – to a group of investors that included members of the Bombardier family in 2003, helped reduce the debt of the company. Subsequent to this restructuring, the performance of Bombardier Inc. has improved. In April 2007, the company’s overall revenues reached $4 billion and its gross margin around 15% (Exhibit 4). BA’s contribution represented 57% of revenues ($2.26 billion) and 57.6% of the gross margin ($344 million). From an organizational perspective, each of the divisions had its own president – Pierre Beaudoin for the aerospace division and André Navarri for the transportation division. The structure of group was highly decentralized in order to provide the divisions with a level of autonomy that is in line with their accountability in terms of growth and profitability3. The Head Office was only involved is providing shared services such as strategic planning, human resources management, organizational development, public relations, finance and budgeting, and legal affairs to the two divisions. In addition to their divisional responsibilities, the two divisional presidents became Executive Vice Presidents (EVP) of Bombardier Inc. in December 2004 and consequently formed the “Office of the President” along with the corporate president and CEO, Laurent Beaudoin. Several analysts interpreted this nomination of Pierre Beaudoin as EVP of Bombardier Inc. as a heads up on his future appointment as the head of the company in replacement of his soon-to-retire father, Laurent Beaudoin. Finally, Bombardier has essentially been a family-run business since its inception. The Bombardier and Beaudoin families have been leading the company for 58 years which provided leadership stability and strategic coherence during the company’s successful diversification era between 1975 and 1999. After this period, the company has been less stable as it changed its leadership regularly (Exhibit 5). In fact, industry analysts suggested that frequent changes in leadership led the company to blurred vision and strategic uncertainty which may explain why Bombardier has been lagging behind its competition – especially Embraer – in the regional aircraft market since then.

Aerospace industry: Temporary turbulences or permanent restructuring?

The first powered flight in history took place in December 17, 1903 when the Wright brothers flew briefly from the Kitty Hawk village (NC) in the United-States. The aircraft they engineered themselves is most generally referred to as Wright Flyer or the Kitty Hawk4. Since then, air travel has become an integral part of people’s everyday lives as trade globalized and individuals traveled more often thanks to decreasing airfares and increasing spare-time available to workers.

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 3

Fundamentally, the evolution of the aircraft industry followed this trend and competition among rivals intensified as the number of travelers increased and their behaviour evolved.

Market players

Airline companies

The direct-customers of aircraft manufacturers are essentially businesses for private jets and airline companies for commercial aircraft. However, the end-customers are passengers who put considerable bargaining pressure on airline carriers as they became increasingly price-sensitive. The expectations of an average traveler have changed significantly with the democratization of air travel and their needs and preferences guided – in a decisive way – the buying decisions of airline companies when they acquire new aircraft. In the mid 1990s, the deregulation of the industry started in the United States, spread quickly around the world, and put pressure on airline companies to seek new means of reducing their costs and passing on some of their savings to their clients. The most critical needs and preferences of travelers have shifted from comfort in the 1980s and 1990s to low price subsequently. That trend led to the proliferation of LCCb companies and to a significant decline in ticket prices. While the aircraft used to carry passengers must be comfortable and economical, those used in cargo transportationc require additional modularity and flexibility in order to accommodate the varying needs of customers.

Financing companies and leasing brokers

From the mid-1990s, the aircraft industry witnessed a significant change in the way new aircraft are being acquired and financed. Airline companies have moved from the traditional model that involved bank loans to acquire airplanes to more flexible modes of ownership and financial arrangements. To adapt to changing technical requirements and fluctuating demand, these companies use a variety of financial mechanisms among which two are the most common: Lease financing allowed airline companies to own aircraft which were financed by manufacturers rather than banks. Indeed, financial solutions became critical to successful sales negotiations. For instance, Boeing Capital Corporation (BCC) is a division of Boeing whose mandate was to devise financial solutions for potential acquirers of Boeing aircraft. From Boeing perspective, BCC’s mission was to facilitate sales and support business development teams during the negotiation process of new deals. Equipment leasing was different in that leasing companies owned and maintained the aircraft they lent to airline companies. This model allowed for flexibility and dynamic adaptation of airliners’ fleets to fluctuating demand both in terms of frequency and configuration of aircraft.

b LCC is an acronym for Low Cost Carriers, also known as Discount Carriers c Cargo is about the transportation of goods as opposed to the transportation of passengers

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 4

Furthermore, rental companies were able to negotiate better deals with manufacturers thanks to the high volume of aircraft they acquired as brokers.

Outsourcing to suppliers and co-development with partners

The design and manufacturing of reliable and economical aircraft required high expertise in numerous areas. Consequently, aircraft manufacturers tended to leverage the know-how of external partners and subcontractors that master very specific technologies and processes. Similar to its competitors – such as Airbus, Boeing and Embraer, – Bombardier was primarily an integrator of components and technologies that are developed by hand-picked strategic partners in compliance with the company’s specifications and requirements. In 2007, an airplane was made up of an average of 55,000 parts most of which are subcontracted to external partners. During the same year, Bombardier paid nearly $6 billion in outsourcing costs to subcontractors which are of three categories5. The first one included manufacturers of major structural components such as wings, engines, and landing gears (e.g., Allied Signals, Boeing Canada, GE Engines, McDonnel Douglas, Pratt & Whitney, Rolls-Royce Motors…). The second type included suppliers of less complex but important parts (e.g., Parker Hannifin, Rockwell Collins, Honeywell, Goodrich, Hamilton Sundstrand…). The third and last category consisted of repair and routine maintenance companies (e.g., Rolls-Royce, Field Aviation, CAE Aviation, Conair, Standard Aero…). Aircraft manufacturers sought strategic partnerships in order to access external expertise and competences they lack internally either by choice or by constraint. In terms of quality, the components provided by outside partners were expected to meet the highest standards set by industry regulators and thus fulfill the promises made by manufacturers to prospect customers, especially in terms of performance and operating costs. Strategic partnerships were also used by some manufacturers to achieve economies of scale while focusing on their core competencies and to reduce time-to-market while developing and marketing new products. This was often achieved by joining research efforts and achieving synergies between human and financial resources. In addition, partnerships allowed for the sharing of industrial and commercial risks which were inherent to any high-tech and research-intensive business such as aeronautics.

Governmental regulations and subsidies

The aircraft industry was often viewed as highly strategic by governments. Indeed, companies such as Bombardier were not only major job-creators but also symbols of pride and sovereignty due to the possible transfer of technology between the commercial and military streams of the industry6. As a result, governments tended to support their national manufacturers and spend billions of dollars in direct or indirect subsidies to support their research and development efforts, promote their products, and protect their markets from foreign competition.

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 5

In Canada, the provincial and federal governments initiated various programs to foster research and minimize investment risks for local players of the industry. Among the mechanisms they used, three programs are particularly illustrative: First, Export Development Canada (EDC) provided financial support and special warranty to all Canadian companies involved in the export of aerospace products; Second, Technology Partnerships Canada (TPC) aimed at facilitating the development and commercialization of aircraft products and services in Canada; Finally, Program productivity of the industry of the material of defense (PPIMD) provided generous credit lines to finance research and development projects that took place in Canada. More specifically, the government of Canada granted loans to local airline companies when they acquired Bombardier’s jets. While this program was clearly designed to favor Bombardier over Embraer – its main competitor – in the Canadian regional aircraft market, the government of Canada argued that this practice was common in the industry worldwide7. Nevertheless, whenever a government intervened to support its national aircraft industry, foreign governments and competitors reacted vigorously and engaged in legal battles to prevent them from enduring. They generally referred to the World Trade Organization’s (WTO) trade framework and anti-dumpingd policies which were ratified by these countries. A good illustration of this trade war can be provided by the WTO arbitration of several litigations between Canada and Brazil. In August 2000, WTO authorized Canada to apply countermeasures of up to $2.1 billion in response to the government of Brazil’s subsidies to Embraer through its PROEX program. Conversely, in December 2002, Canada lost a battle to Brazil as WTO decided that Brazil was entitled to impose countermeasures of up to $385 million (instead of the $5.2 billion initially claimed by Brazil) against Canada. This conflict originated from a financing offer – involving particularly low interest rates – made by the government of Canada to Air Wisconsin to support its acquisition of Bombardier’s jets. However, it is important to stress that while Brazil was able to apply countermeasures and increase its tariffs on Canadian products, the WTO ruling did not really prevent the transaction between Bombardier and Air Wisconsin from taking place. Another means of governments’ intervention in the industry was through environmental regulations. As global warming debates intensified, several governments created regulations and incentives to mitigate the negative effects of air transportation on the environment8. For instance, the European Union (EU) ruled the application of its Emissions Trading Scheme (ETS) to air transportation beginning 2011. All these trends resulted in a race for the development and acquisition of more environment-friendly aircraft, in an increase in demand for more fuel-efficient jets, and in earlier withdrawals of high fuel-consuming aircraft9. Consequently, the new

d Dumping means “The sale of goods of one nation in the markets of a second nation at less than the price charged within the first nation. Dumping can eliminate competitors by undercutting their prices.” in Dictionary.com – the American Heritage® New Dictionary of Cultural Literacy, 3rd Ed. Houghton Mifflin Company, 2005. http://dictionary.reference.com/browse/dumping (accessed: June 2, 2008).

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 6

generations of airplanes are expected to consume less energy, be more comfortable for passengers, and generate less noise and disturbance for the residential areas neighboring airports.

Evolution of aircraft market

The aircraft industry has experienced major transformations due to both unforeseeable events and cyclical phenomena. Regardless of their sources, most of these events had structuring and enduring effects on the industry as a whole.

Brief events with lasting effects

Overall, the market of commercial aircraft followed a growth trend since the 1970s in terms of both turnover and volume of sales. It must be noted nonetheless that the period between 2001 and 2003 was particularly difficult for the industry as a whole (Appendix 4). Before 2001, the dynamics of industry went through major transformations as reflected, for instance, by the increasing sensitivity of travelers to the ticket price (Appendix 10). A new category of airline companies – generally referred to as LCC or Low Cost Carriers – made their appearance first in the United States before the model was replicated in Europe and then globally. Furthermore, oil crises of the 1970s and 1990s triggered major psychological chocks in the industry but their economic impact was quickly mitigated by both airline companies and aircraft manufacturers. However, between 2001 and 2003, the industry was confronted with a major crisis due to several unforeseeable and almost simultaneous events. The attacks on the World Trade Center (WTC) in September 2001 had a devastating effect on many companies due essentially to the immediate collapse of the demand. As a result, many airline companies were pushed to defer or cancel the delivery of aircraft they previously ordered. As soon as the industry started to foresee its recovery from the effects of the WTC events, it was confronted with another challenge. An endemic respiratory disease, referred to as SARS or Severe Acute Respiratory Syndrome, started in Hong Kong and spread quickly throughout the world affecting 8,096 people among which 774 died between November 2002 and July 200310. The impact of the outbreak on most airline companies was as quick as critical. A large number of flights were cancelled putting airline companies yet again in a dire need for cash to survive. Several companies either sought hasty mergers with competitors or declared bankruptcy within the first few weeks following this second shock. Fortunately enough for the companies that survived these events, the activity in the industry picked up again in 2003 to reach the level of 2001 in terms sales (Appendix 11) by 2006. Subsequently, airline companies became profitable again11.

A cyclical industry in structural transformation

Aircraft industry is cyclical by nature and the replacement of aging airplanes is an important determinant of market dynamics. In fact, new airplanes are generally acquired either to respond

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 7

to increasing demand or to replace the aircraft that airliners deemed unfit for the transportation of passengers. Those retired airplanes were then recycled and reassigned to the transportation of goods. Starting in mid-1970s, airline carriers have started to reconfigure their routes into networks (hub-and-spoke) instead of the traditional point-to-point configurations. Hub-and-spokes consisted of rings of small routes (spokes) used by regional carriers to collect passengers and feed bigger regional airports (hubs) with larger volumes of passengers. This architecture led to a stunning development of regional carriers and subsequently to the commercial success of regional aircraft, which transformed the dynamics of the market in a profound way. In 2007, the long-term forecasts of major airline manufacturerse have predicted an even faster development of regional hubs in the horizon of 2025. The market implications for manufacturers are increasing demand for both regional aircraft (fewer than 140 seats) for regional traffic and larger aircraft (more than 250 seats) for intercontinental routes.

Buying decision criteria

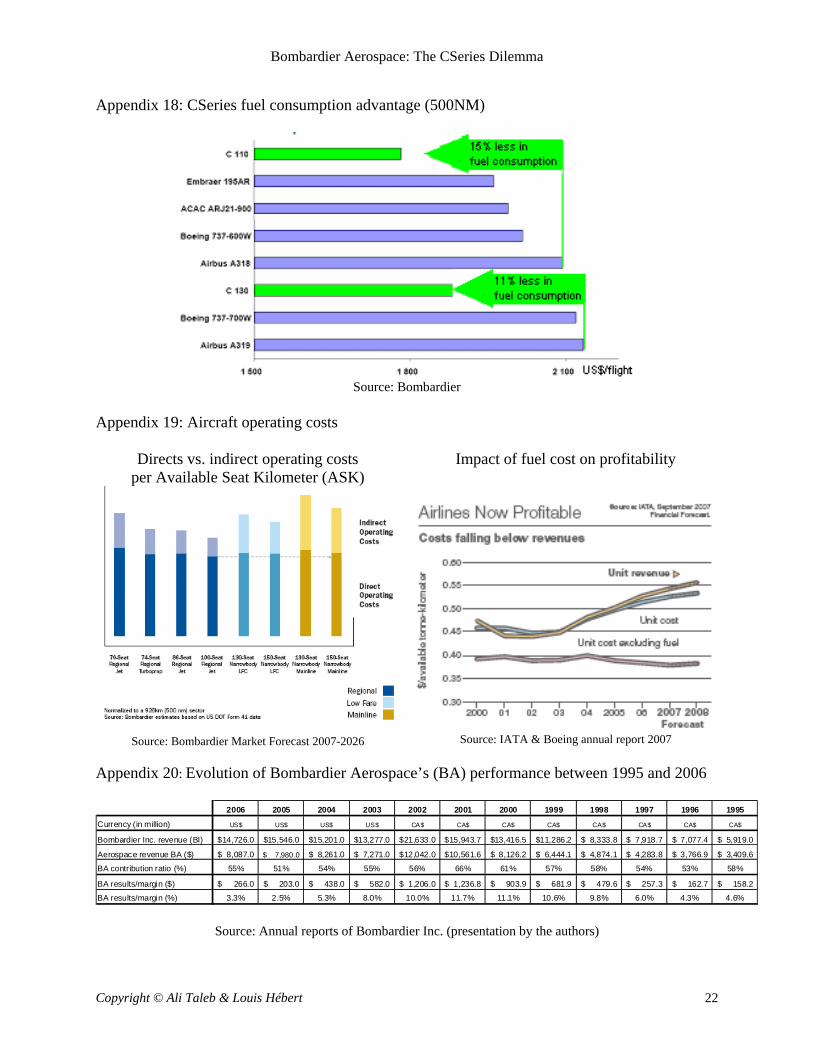

The configuration of a carrier’s network of routes was dependent on the level of demand on each route, the pricing strategy of the company, and the capacity of the fleet operated. As air transportation democratized, ticket price became the first buying criterion of travelers (Appendix 10) and airline companies were required to keep their operating costs under control and optimize their capacity utilization in order to offer low fares despite increasing fuel prices. In addition to the acquisition costs of aircraft, their exploitation costs were critical to the profitability and performance of airline companies. For instance, increasing fuel prices continued to impede the profitability of airliners notwithstanding the decrease of other operating costs as well as the increase of revenues of these companies. Therefore, the performance of airline companies was essentially dependent on the effective control of their operating costs. For example, regional aircraft of 70 to 100 seats were more cost-effective to operate than the larger aircraft that traditional carriers and some LCCs often used in long-hauls (Appendix 19). Fuel consumption was a major lever manufacturers tried to leverage to reduce their operating costs. As a result, the average consumption of commercial aircraft has dropped by 37% in just two decades. That is, modern aircraft consumed an average of 5% (or 5 liters per 100 RPKf) in 2005 compared to 8% in 198512. In addition, the technologies used in making engines played a major role in the level of performance of aircraft. In fact, every time manufacturers promised to improve the operating costs of a new aircraft, they often based their predictions on energy savings or lower maintenance requirements thanks to the use of new technologies. For instance, turboreactors were generally less expensive to maintain than turboprops (Appendix 19). Conversely, turboprops consumed less fuel, generated less pollution, and provided a better level of comfort for passengers than turboreactors. As a result, the number of turboprops acquired by regional carriers has increased significantly as fuel prices increased.

e Market forecasts of Airbus, Boeing, Bombardier and Embraer f RPK is an acronym for Revenue per Person-Kilometer

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 8

Future perspectives for the industry13

Supported by a positive business environment and a sustained economic growth, the aircraft market grew by about 30% between 2000 and 2005 despite sky-rocking fuel prices. This was made possible thanks to a combination of gains in productivity, increase in existing capacity, and entry of new companies to the market. According to Airbus, the number of passenger aircraft was expected to rise from 12,676 in 2005 to 27,307 in 2025, which represented an average annual growth of 4.8% over twenty years. The total number of aircraft of more than 30 seats – including cargo carriers – was expected to increase from 17,153 units in 2005 to 33,500 in 2025.

Market trends by geographical area

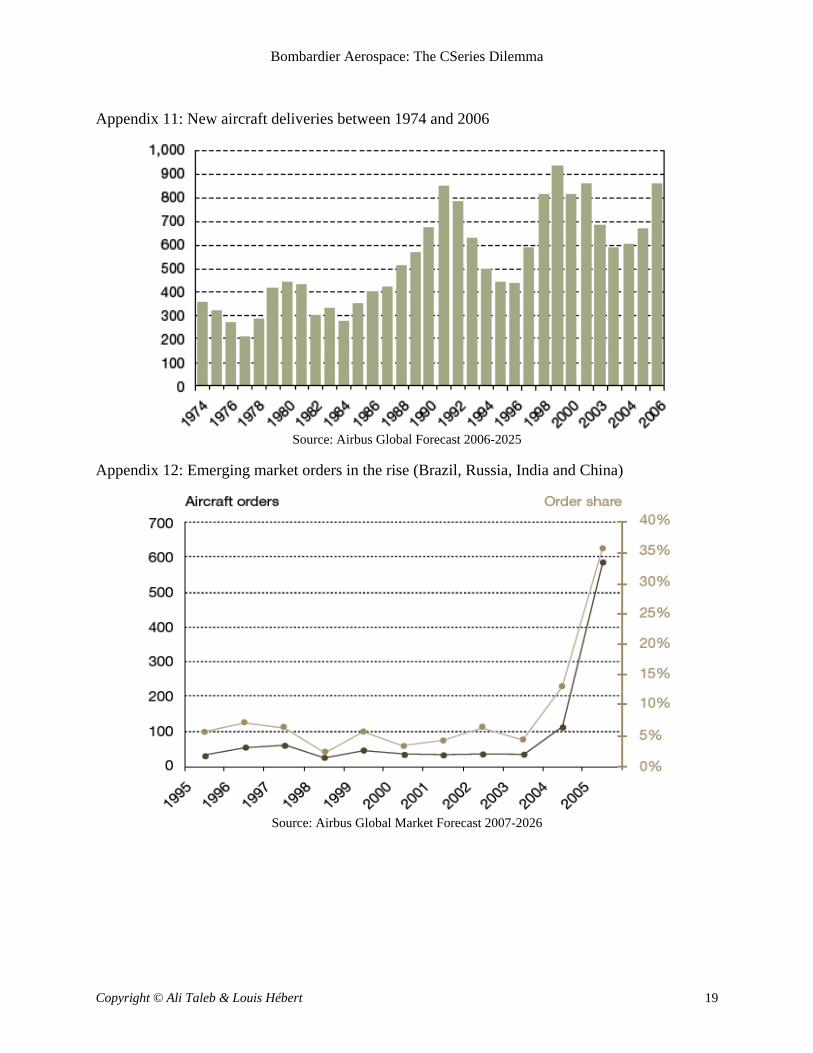

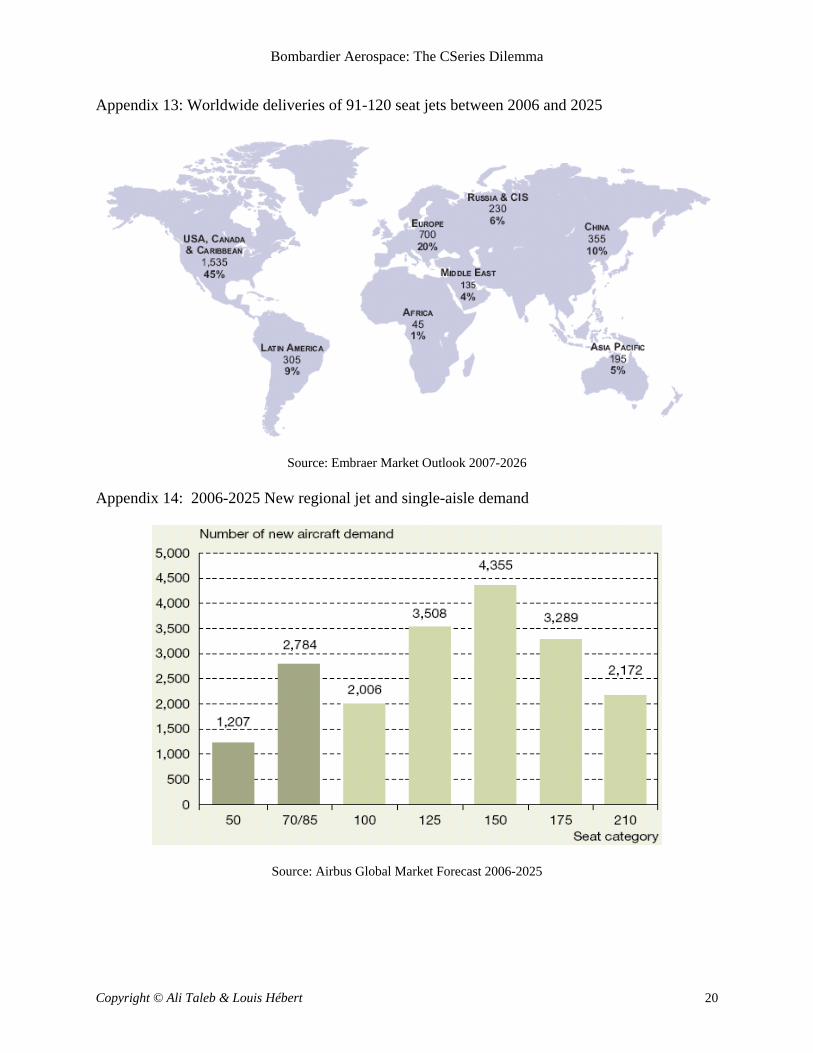

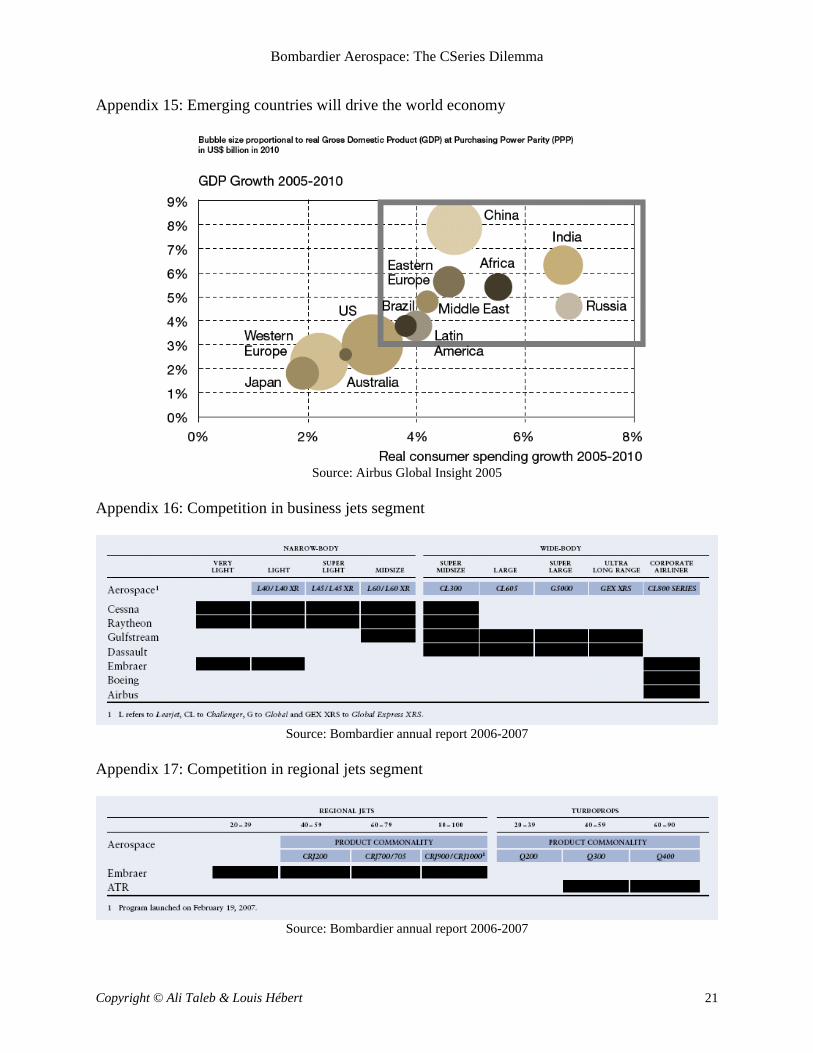

The business model of LCCs has been viable since early 1990s thanks to their tight control of operating costs especially if contrasted with those of traditional carriers. By the middle of the 1990s, regional carriers pushed the low-cost model even further by specializing in short- to med-range transportation while seeking synergies with traditional carriers that operated longer distance routes. Together, they offered a viable and flexible alternative to LCCs. This new model was expected to develop further as regional traffic grew especially in emergent countries which were expected to have enormous needs for this category of aircraft (Appendix 12). Indeed, large emergent countries such as Brazil, China, India and Russia span over wide geographic areas and their populations were growing quickly. Other smaller but fast growing countries in Eastern Europe, Asia, Africa, and Latin America were also expected to contribute to the steady development of the aircraft market in a significant way (Appendix 13)14. In fact, the orders of those small countries have already represented more than 35% of the global demand in 2005; a major rebound from less than 5% just a few years earlier (Appendix 12).

Market trends by categories of aircraft

In general, aircraft were categorized according to their capacity and their range of reach. Most analysts and manufacturers made a distinction between three categories or market segments. First, Commercial Aircraft were designed to carry more than 100 passengers. The European Airbus and American Boeing were the two main manufacturers of commercial jets. They were also the only manufacturers of jumbo jets carrying over 400 seats15. It was expected that, between 2006 and 2025, airline companies would acquire an average of 1,133 commercial airplanes every year. The new aircraft were meant to satisfy the constantly growing demand for transcontinental traffic as well as to replace retiring airplanes either because they were not fit anymore for the transportation of passengers or because the acquisition of new generation airplanes would be more cost-effective than operating the aging ones. The utilization of mid-size aircraft ranging from 100 to 140 seats has been increasing steadily in both domestic and regional transportation segments. For instance, in North America, this

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 9

category represented more than two-thirds of the aircraft sold between 2000 and 2006. In fact, their market share was expected to grow by 56% in twenty years, from 5,400 units in 2006 to 8,400 in 2026 (Appendix 14). Second, Regional Jets had a capacity of 20 to 100 seats. They were essentially used by regional airlines to respond to two types of needs: local point-to-point routes with high frequency; and interconnections between regional hubs used by long-haul carriers. Regional transporters often operated turboreactors or turboprops of fewer than 100 seats whereas large airline companies used higher capacity airplanes (more than 100 seats) on long-haul, continental, and international routes. According to GAMMA16, 245 regional aircraft of fewer than 100 seats have been delivered worldwide in 2006. Bombardier has also forecasted that the demand for regional jets of 20 to 100 seats was set to increase and reach 5,400 units by 202617. It was also clear that the demand was increasingly shifting towards regional jets with larger capacity – typically in the range of 100 to 150 seats (Appendix 15). Finally, Business Jets were designed to carry fewer than 20 passengers. These small planes were essentially intended for wealthy individuals or large organizations seeking flexibility in travel arrangements for their leadership teams.

Bombardier Aerospace: A leader in the regional jet market

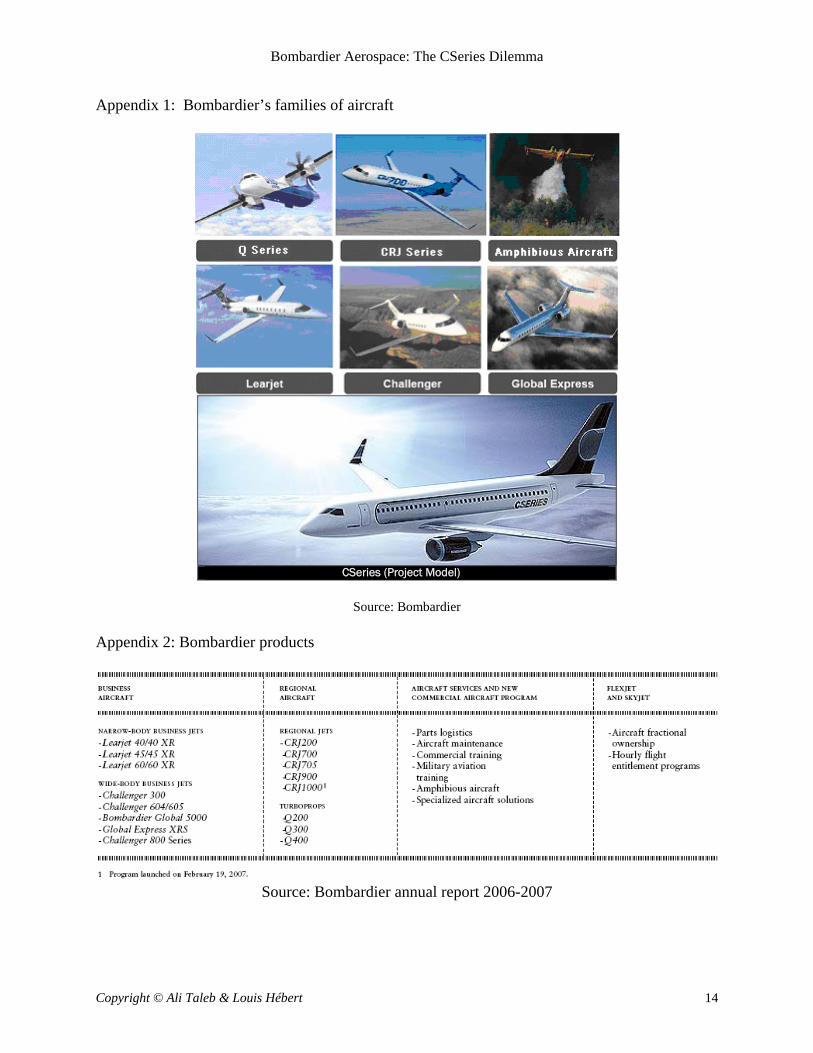

Bombardier specialized in the development and manufacturing of two types of passenger jets – business jets and regional aircraft – in addition to amphibious aircraft that were used in firefighting (Appendix 1). Besides, the company also sold spare parts, provided maintenance and training services, and offered multi-property Flexjet and Skyjet services (Appendix 2). In 2006, Bombardier has delivered 337 aircraft; including 197 business jets, 138 regional jets, and two amphibious aircraft.

Business jets segment

Bombardier had two categories of businesses jets: the Learjet family composed of narrow fuselage aircraft; and Challenger and Total Express families which include larger fuselage airplanes (Appendix 1). Compared to its competitors, Bombardier had a more diversified portfolio of products in this segment (Appendix 16). In 2006, Bombardier had 27% market share in this segment, which represented about 47% of the total sales of the company18. In terms of volume, Bombardier delivered 213 units out of the 798 business jets delivered by the industry during the same year.

Regional jets segment

Bombardier had also two families of regional aircraft – CRJ and Q-Series. Both families were built using technologies developed in the 1970s and fine-tuned over the years. The CRJ family

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 10

consisted of turboreactor jets whose capacity ranged from 40 to 100 seats. This family had the reputation of being energy-efficient compared to larger aircraft. In fact, it was considered the most popular regional airplane series in history19 with 1,409 units sold as of January 2007. The capacity of Q-Series ranged from 37 to 78 seats. This family was gaining in popularity because it required less maintenance than turboreactors. They had considerable economic advantages especially on short distance routes. For instance, they allowed for the reduction of 28% in fuel consumption, 83% in engine maintenance costs, and 14% in personnel and crew costs20. However, turboprops were less comfortable for passengers due to their narrow body and were much noisier especially during the takeoff and landing operations. In 2006, 245 regional aircraft of less than 100 seats were delivered by the industry worldwide compared to 288 in 2005. Among these, Bombardier delivered 126 units compared to 153 in 2005.

Competition in regional jets market

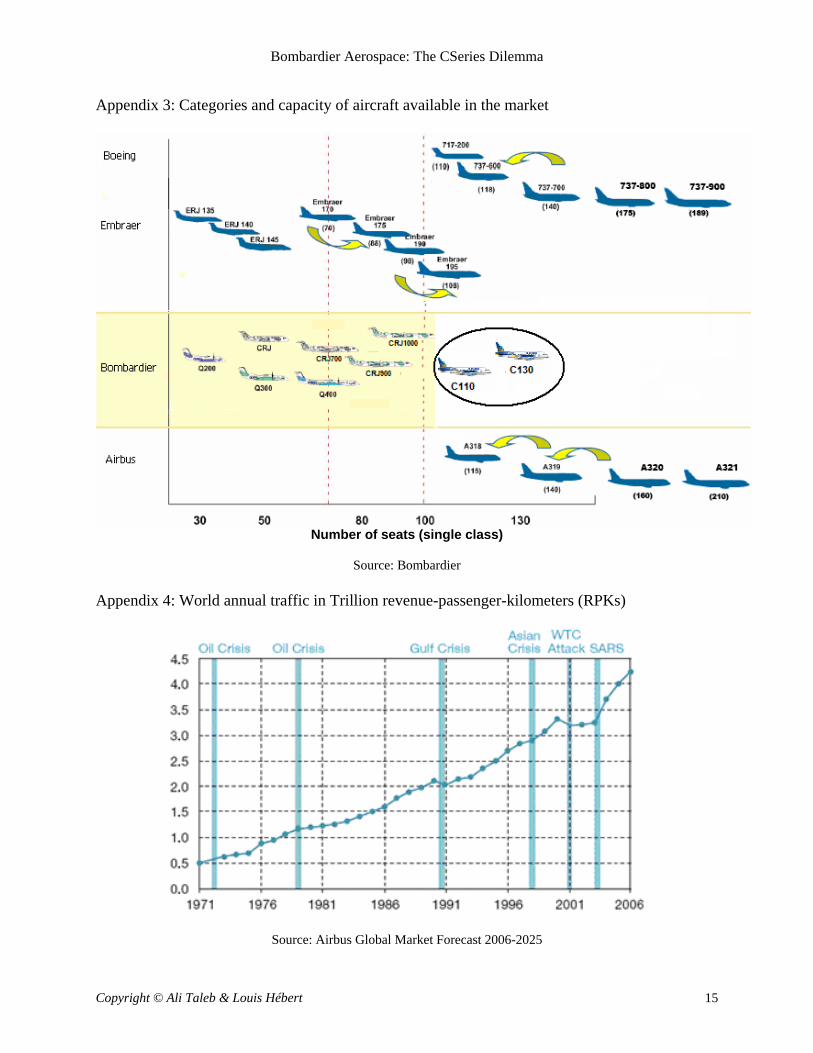

Bombardier had two main competitors in the regional aircraft market: Embraer in the segment of turboreactors whose capacity ranged from 40 to 100 seats; and ATR in the segment of turboprops whose capacity ranged between 40 and 90 seats (Appendix 17). In the segment of 90 to 149 seats, Embraer was the only real competitor of Bombardier. Embraer had two models (ERJ190 and ERJ195 with up to 120 seats in capacity) which were able to satisfy the requirements of regional airliners in terms of both capacity and efficiency (Appendix 3). On the other hand, Boeing and Airbus had several models (B717 and B737-600 for Boeing and A318-100 for Airbus) whose capacity was slightly above 100 seats but these aircraft were significantly more expensive to acquire and operate especially on regional routes. In 2007, Embraer and Bombardier were the leading manufacturers in the regional aircraft segment. However, several countries – driven by their national needs as well as by the attractive opportunity of entering a high potential segment – showed increasing interest in entering this market. For instance, the Chinese government vowed to build up a modern aircraft industry and the State owned AVIC-I (China Aviation Industry Corp.) already announced its ARJ21-900 model (105 seats) for 2011. It is also worth mentioning that AVIC-I was a supplier of some components Bombardier used in its Q Series. During the same year, the Japanese Mitsubishi Heavy Industries (MHI) is another supplier of Bombardier that announced the development of a new family of regional aircraft (MRJ) which included the MRJ-70 (70 passengers) and MRJ-90 (90 passengers) models21. Finally, the Russian Sukhoi also announced its intention to develop a similar family of products named the RRJ (Russian Regional Jet)22 – also known as Superjet 100 Regional Jet – and thus target the same market as Bombardier’s CSeries. As some analysts suggested, the Chinese and Russian aircraft would become serious threats to both Bombardier’s CRJ1000 model (launched February 19, 2007) and its CSeries project if these projects were implemented.

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 11

Bombardier Aerospace and the CSeries dilemma

The capacity of aircraft acquired by regional carriers tended to increase over time. Moreover, the commercial aircraft – especially those of Airbus and Boeing – which could be used in regional routes were oversized and more expensive to acquire and operate than regional jets (Appendix 19). Aware of this reality, Bombardier has decided in February 19, 2007 to extend its CRJ family and develop a new model (CRJ1000) that is scheduled to enter the market in 2010. In addition to its higher capacity ranging from 86 to 104 seats, this model was supposed to provide a better level of comfort and relatively lower operating costs compared to Bombardier’s own models as well as those of its competition in the range of 90 to 100 seats. The CRJ1000 program was launched with 38 conditional orders including 15 conversions from previous CRJ900 pipeline. According to some analysts, this decision was essentially tactical and short-lived because it only represented an extension of the CRJ family and did not solve the fundamental issue Bombardier was facing. That is, both Q-Series and CRJ aircraft used old technologies, had narrow bodies, and featured old designs. Other analysts argued that the only way Bombardier could address this strategic issue would be the development of a new generation of aircraft.

CSeries: Bombardier’s response to market transformation?

Since July 2004, Bombardier was contemplating the development of the CSeries, a new family of aircraft capable of carrying between 100 and 135 passengers depending on models. The airline carriers which were operating aircraft of this capacity at that time owned old generation airplanes such as DC9s, Fokker 100s, Boeing 737s, BAE-146s and MD80s. As these airplanes were getting older, airliners were replacing them with more comfortable and more efficient models. In 2007, all aircraft available in the market (Appendix 3) had to be either shortened (Airbus 318, Airbus 319, Boeing 737-200, Boeing 737-600) or prolonged (Embraer 190 and Embraer 195) from their original lengths to meet the optimal capacity and efficiency requirements of regional carriers. Conversely, the CSeries family offered a seat capacity ranging between 100 and 150 passengers depending on models and was specifically optimized to operate efficiently on regional routes. For instance, it was anticipated that the C110 would consume 17% less energy than the Airbus A318 and the C130 11% less than the Airbus A319 (Appendix 18). In terms of operating costs, both Airbus and Boeing aircraft were significantly more expensive to operate than CSeries (Appendix 19). For all these reasons, Bombardier maintained that the CSeries family would replace at least the existing Boeing 737 as they retire over time. In fact, it might even be suitable for airliners to get rid of their aging airplanes earlier than expected and achieve significant cost savings by simply operating CSeries aircraft on their regional routes. While Embraer’s 190 and 195 models could be considered direct competitors to Bombardier’s C110, the C130 model did not have any serious competitor in 2007. Nevertheless, Embraer could have also been working secretly on a similar initiative given the potential of this market segment as well as Embraer’s level of investment in research and development which reached $113 million in 2006 compared to $92 million in the previous year (Appendix 22). Therefore, the

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 12

window of opportunity for Bombardier’s CSeries seemed to narrow quickly as time passed and potential competitors loomed.

The genesis of the CSeries initiative

In July 2004, Bombardier announced its intention to develop a new family of regional aircraft, called CSeries, at the Farnborough Aerospace Fair (United Kingdom). The company anticipated that the demand for aircraft in the capacity range of 100 to 150 seats would represent 13% of the overall aircraft market by 2025. Therefore, that segment would represent about 6,000 units and $25 billion in sales. On March 15, 2005, the Board of Directors of Bombardier Inc. approved the concept and gave Bombardier Aerospace the permission to investigate the feasibility of the initiative further. On May 13, 2005, the government of Canada announced its commitment to provide Bombardier with financial assistance assuming the company was committed to developing the CSeries in Canada. The pledge consisted of an interest-free line of credit of $350 million which could be used to develop the new technologies needed to make CSeries. In 2005, the company conducted a feasibility study and released a mock-up of the aircraft at the Paris Le Bourget International Aeronautics & Space Show in France (Appendix 1). During the same period, the company also announced the selection of Bombardier’s Montreal-Mirabel (Canada) site as the preferred location for the final assembly of the CSeries as well as satisfactory progress in their negotiations with Pratt & Whitney Canada regarding the development of the CSeries engine. Indeed, the company needed to secure a partner to the new technology because, according to the spokesperson of Bombardier23, every time they talked to potential clients, they asked them: "Who is going to develop your engine? What kind of engine are you going to use?" Despite all these positive developments, Bombardier announced on January 31, 2006 they decided to put the project on hold because “market conditions (did) not justify the launch of the CSeries program at (that) time.” The project team was then reduced to about fifty people and the rest of the team was reassigned to other regional jets and turboprops aircraft within the range of 80 to 100 seats. During a January 31, 2007 press conference, Bombardier announced the company was still refining its plans and confirmed the new expected commercialization date by 2013 assuming the project’s effective launch in 2008. Two weeks later, on February 19, 2007 the company officially announced the launch of the CRJ1000 model targeting the 80-100 passengers range. This project was expected to proceed with the same resources initially transferred from the CSeries project back in January 2006. As of April 2007, the initial cost of the project reached $100 million, the ongoing monthly spend-rate was about $1 million US, and the total development cost was estimated at about $2 billion US24. To offset some of these costs, the governments of Canada, Quebec province, and

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 13

the United Kingdom (UK) were expected to finance about $700 million US. That is, Canada’s federal government pledged about $260 million US, Quebec provincial government about $90 million US, and the UK government about $350 million US (£180 million). The conditional release of these funds required Bombardier to carry out some R&D and production activities in Montreal-Mirabel (Canada) and Belfast (Northern Ireland).

The Dilemma

The annual meeting of shareholders was scheduled to take place on May 29, 2007. Industry analysts were expecting Pierre Beaudoin, president of Bombardier Aerospace, to clarify the long-term strategy of the company and more specifically the future of the CSeries.

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 14

Appendix 1: Bombardier’s families of aircraft

CSeries (Project Model)

Source: Bombardier

Appendix 2: Bombardier products

Source: Bombardier annual report 2006-2007

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 15

Appendix 3: Categories and capacity of aircraft available in the market

Number of seats (single class)

Source: Bombardier

Appendix 4: World annual traffic in Trillion revenue-passenger-kilometers (RPKs)

Source: Airbus Global Market Forecast 2006-2025

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 16

Appendix 5: Evolution of Bombardier’s leadership Year Events 1942 Jean-Armand Bombardier created Auto-Neige Bombardier Ltd. 1964 Jean-Armand Bombardier died. Laurent Beaudoin was appointed General Manager. 1966 Laurent Beaudoin became President of the company. 1969 Bombardier became a public company. 1975(a) Jean-Claude Hébert hired as chief executive with a mandate to diversify and grow the

company. Laurent Beaudoin became Director of Operations. 1978(a) Jean-Claude Hébert resigned. Laurent Beaudoin came back as chief executive of the

company. 1979(a) Laurent Beaudoin became Chairman and Chief Executive Officer (CEO) of Bombardier

Inc. 1990(a) Pierre (son of Laurent) Beaudoin was appointed Vice President of Product Development

for the Sea-Doo/Ski-Doo division of Bombardier Inc. 1992(a) Pierre Beaudoin became Executive Vice President of Sea-Doo/Ski-Doo.

1994(a) Pierre Beaudoin served as President of the Sea-Doo/Ski-Doo.

1996(a) Pierre Beaudoin was appointed President and Chief Operating Officer (COO) of Bombardier Recreational Products. Robert E. Brown was promoted President and Chief Operating Officer of Bombardier Aerospace.

1999(a) Laurent Beaudoin became Chairman of the Board and of the Executive Committee. Robert E. Brown was appointed President and CEO of Bombardier Inc.

2001 Pierre Beaudoin was appointed President of Bombardier Aerospace, Business Aircraft, in February. Then, President and COO in October.

2002(b) In December, Robert E. Brown resigned. Laurent Beaudoin became Chairman of the Board and of the Executive Committee of Bombardier Inc.

2003(b) In January, Paul Tellier was appointed President & CEO and director of Bombardier Inc.

2004(b) In December, Paul Tellier resigned. Laurent Beaudoin was appointed CEO. Pierre Beaudoin became Executive Vice President and a member of the Board of Directors of Bombardier Inc. in addition to his duties as President & COO of Bombardier Aerospace.

(a) period of diversification (b) period of restructuring

Source: Bombardier, compiled by the authors Appendix 6: Contribution of BA and BT to Bombardier Inc. performance

Revenue

($) Revenue

(%) Gross Margin

$ (%) Contribution

(%) Bombardier Inc. (Corporate) 3.969 100% 597 (15%) 100% Bombardier Aerospace (BA) 2.260 57% 344 (15.2%) 57.6% Bombardier Transportation (BT) 1.707 43% 253 (14.8%) 42.4% * All figures in billion $ as of end of April 2007

Source: Bombardier (presentation by the authors)

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 17

Appendix 7: Comparison of Bombardier and Embraer product activity

Year Bombardier’s product activity Embraer’s product activity 1991 Launch of Bombardier 415 1992 Delivery of CRJ100 1993 1994 Delivery of Bombardier 415 1995 Launch of Dash 8-200 Delivery of ERJ135 1996 Launch of CRJ200 1997 1998 1999 Launch of Q400

Inaugural flight of CRJ700 Launch of Embraer 170 Delivery of ERJ 135

2000 Delivery of Q400 Launch of CRJ900

Launch of Embraer 190

2001 Delivery of CRJ700 Inaugural flight of CRJ900

Delivery of ERJ140

2002 Launch of Embraer 175 Launch of Embraer 195

2003 Delivery of CRJ900 CSeries idea

Delivery of Embraer 170

2004 CSeries announced

Delivery of Embraer 175

2005 Delivery of CRJ705 Delivery of Embraer 190 2006 CSeries on hold Delivery of Embraer 195 2007 Launch of CRJ1000

Source: Bombardier and Embraer (presentation by the authors)

Appendix 8: Evolution of Bombardier and Embraer shares values (JUL2001-MAY2007)

Embraer (NYS:ERJ)

Bombardier (TSX:BBD.B)

Source: Google Finance

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 18

Appendix 9: Bombardier and Embraer sales during between 1997 and 2006 (units delivered) Bombardier model 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

CRJ100/200 64 77 81 103 136 140 152 100 44 36

CRJ 700 - - - 2 29 50 50 64 65 47

CRJ900 - - - - - 1 12 14 12 12

Q100/200 22 12 16 7 3 1 - 1 1 1

Q300 8 18 6 17 15 9 9 5 11 11

Q400 - - 1 28 23 19 9 16 16 16

Embraer model 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006EMB 120 10 13 7 - 2 - - - - -ERJ135 - - 16 45 27 3 14 - 2 -ERJ140 - - - - 22 36 16 - - -ERJ145 32 80 80 112 104 82 57 87 46 12EMBRAER 170 - - - - - - - 46 46 32EMBRAER 175 - - - - - - - - 14 11EMBRAER 190 - - - - - - - - 12 40EMBRAER 195 - - - - - - - - - 3

Source: Bombardier and Embraer annual reports, compiled by the authors from annual reports Appendix 10: Passenger’s ticket purchasing decision criteria

Source: Airbus Market Forecast 2006-2025

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 19

Appendix 11: New aircraft deliveries between 1974 and 2006

Source: Airbus Global Forecast 2006-2025

Appendix 12: Emerging market orders in the rise (Brazil, Russia, India and China)

Source: Airbus Global Market Forecast 2007-2026

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 20

Appendix 13: Worldwide deliveries of 91-120 seat jets between 2006 and 2025

Source: Embraer Market Outlook 2007-2026 Appendix 14: 2006-2025 New regional jet and single-aisle demand

Source: Airbus Global Market Forecast 2006-2025

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 21

Appendix 15: Emerging countries will drive the world economy

Source: Airbus Global Insight 2005

Appendix 16: Competition in business jets segment

Source: Bombardier annual report 2006-2007

Appendix 17: Competition in regional jets segment

Source: Bombardier annual report 2006-2007

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 22

Appendix 18: CSeries fuel consumption advantage (500NM)

Source: Bombardier

Appendix 19: Aircraft operating costs

Directs vs. indirect operating costs per Available Seat Kilometer (ASK)

Source: Bombardier Market Forecast 2007-2026

Impact of fuel cost on profitability

Source: IATA & Boeing annual report 2007

Appendix 20: Evolution of Bombardier Aerospace’s (BA) performance between 1995 and 2006

2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995

Currency (in million) US$ US$ US$ US$ CA$ CA$ CA$ CA$ CA$ CA$ CA$ CA$

Bombardier Inc. revenue (BI) 14,726.0$ 15,546.0$ 15,201.0$ 13,277.0$ 21,633.0$ 15,943.7$ 13,416.5$ 11,286.2$ 8,333.8$ 7,918.7$ 7,077.4$ 5,919.0$

Aerospace revenue BA ($) 8,087.0$ 7,980.0$ 8,261.0$ 7,271.0$ 12,042.0$ 10,561.6$ 8,126.2$ 6,444.1$ 4,874.1$ 4,283.8$ 3,766.9$ 3,409.6$

BA contribution ratio (%) 55% 51% 54% 55% 56% 66% 61% 57% 58% 54% 53% 58%

BA results/margin ($) 266.0$ 203.0$ 438.0$ 582.0$ 1,206.0$ 1,236.8$ 903.9$ 681.9$ 479.6$ 257.3$ 162.7$ 158.2$

BA results/margin (%) 3.3% 2.5% 5.3% 8.0% 10.0% 11.7% 11.1% 10.6% 9.8% 6.0% 4.3% 4.6%

Source: Annual reports of Bombardier Inc. (presentation by the authors)

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 23

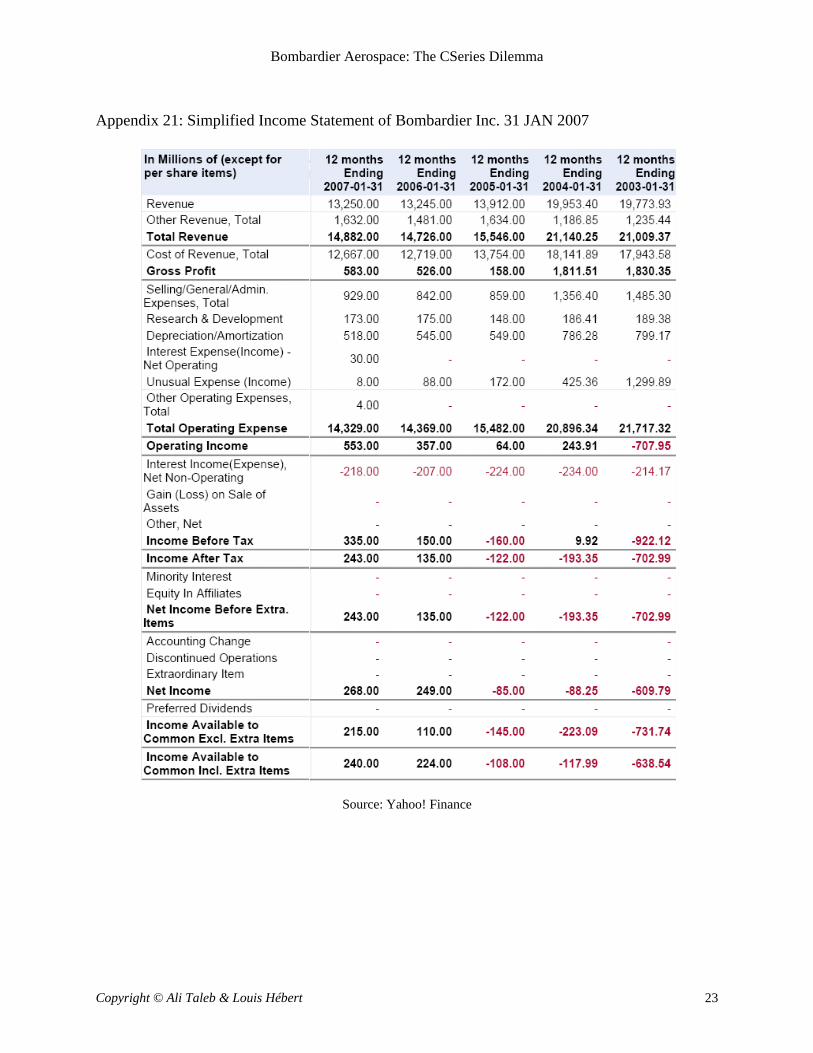

Appendix 21: Simplified Income Statement of Bombardier Inc. 31 JAN 2007

Source: Yahoo! Finance

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 24

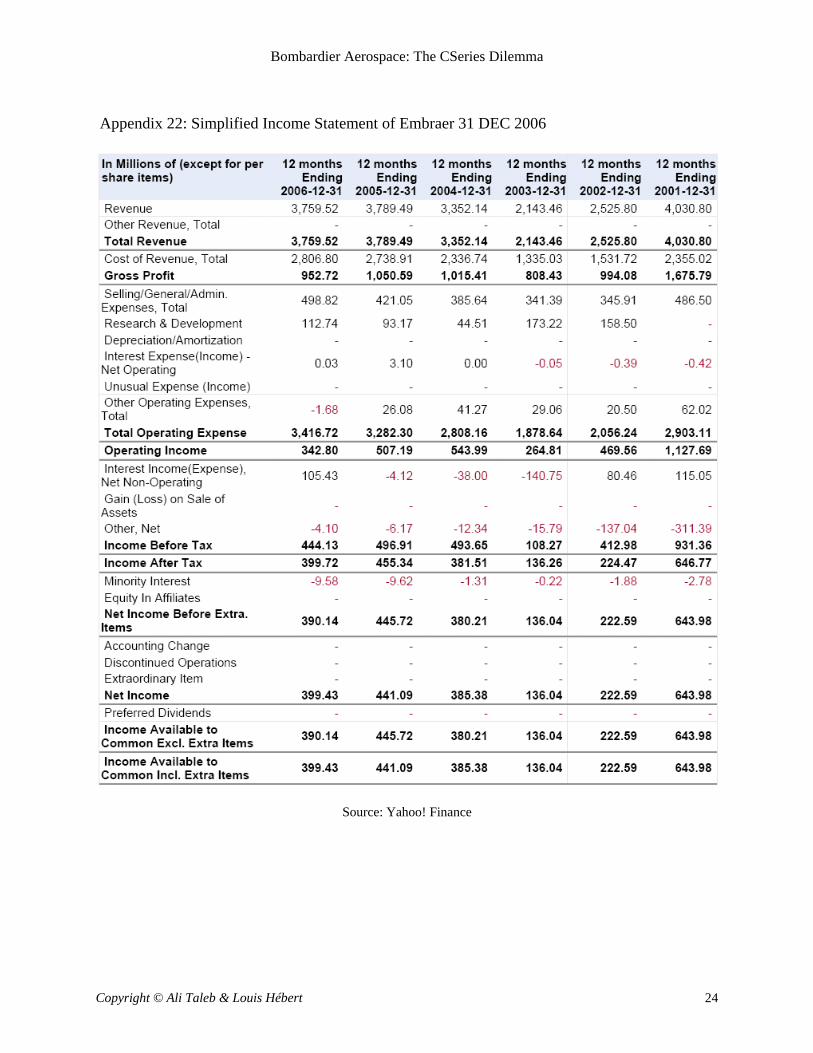

Appendix 22: Simplified Income Statement of Embraer 31 DEC 2006

Source: Yahoo! Finance

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 25

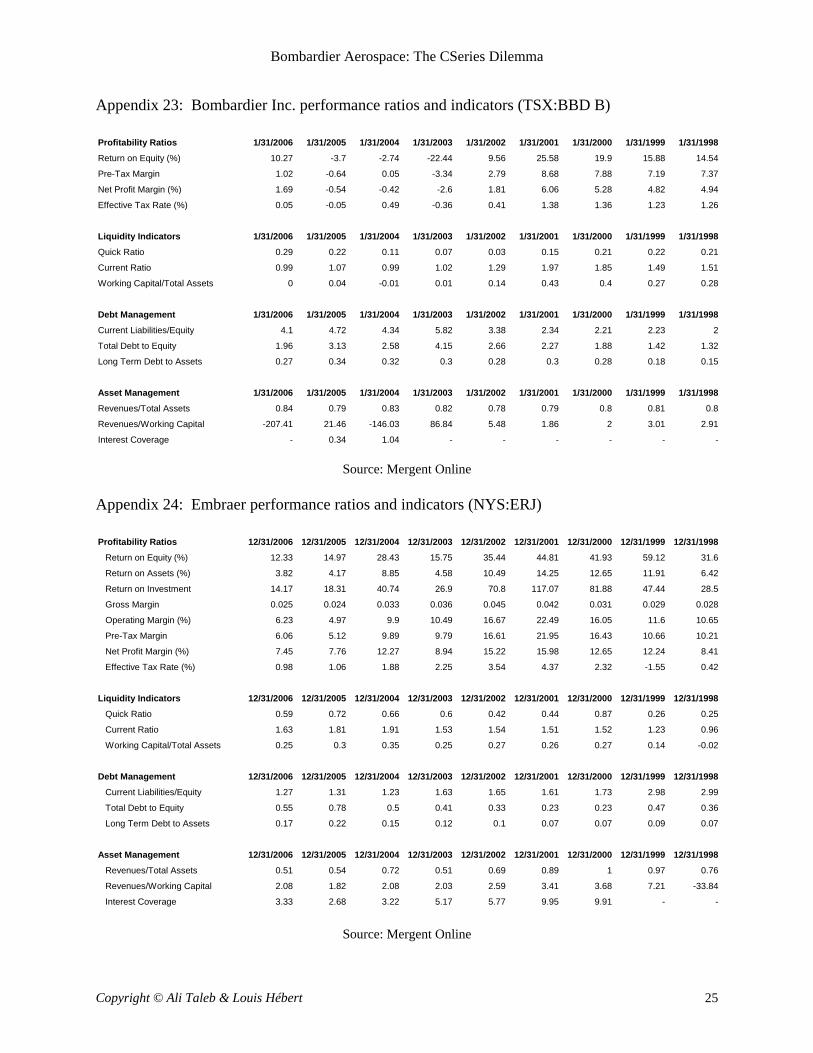

Appendix 23: Bombardier Inc. performance ratios and indicators (TSX:BBD B) Profitability Ratios 1/31/2006 1/31/2005 1/31/2004 1/31/2003 1/31/2002 1/31/2001 1/31/2000 1/31/1999 1/31/1998

Return on Equity (%) 10.27 -3.7 -2.74 -22.44 9.56 25.58 19.9 15.88 14.54

Pre-Tax Margin 1.02 -0.64 0.05 -3.34 2.79 8.68 7.88 7.19 7.37

Net Profit Margin (%) 1.69 -0.54 -0.42 -2.6 1.81 6.06 5.28 4.82 4.94

Effective Tax Rate (%) 0.05 -0.05 0.49 -0.36 0.41 1.38 1.36 1.23 1.26

Liquidity Indicators 1/31/2006 1/31/2005 1/31/2004 1/31/2003 1/31/2002 1/31/2001 1/31/2000 1/31/1999 1/31/1998

Quick Ratio 0.29 0.22 0.11 0.07 0.03 0.15 0.21 0.22 0.21

Current Ratio 0.99 1.07 0.99 1.02 1.29 1.97 1.85 1.49 1.51

Working Capital/Total Assets 0 0.04 -0.01 0.01 0.14 0.43 0.4 0.27 0.28

Debt Management 1/31/2006 1/31/2005 1/31/2004 1/31/2003 1/31/2002 1/31/2001 1/31/2000 1/31/1999 1/31/1998

Current Liabilities/Equity 4.1 4.72 4.34 5.82 3.38 2.34 2.21 2.23 2

Total Debt to Equity 1.96 3.13 2.58 4.15 2.66 2.27 1.88 1.42 1.32

Long Term Debt to Assets 0.27 0.34 0.32 0.3 0.28 0.3 0.28 0.18 0.15

Asset Management 1/31/2006 1/31/2005 1/31/2004 1/31/2003 1/31/2002 1/31/2001 1/31/2000 1/31/1999 1/31/1998

Revenues/Total Assets 0.84 0.79 0.83 0.82 0.78 0.79 0.8 0.81 0.8

Revenues/Working Capital -207.41 21.46 -146.03 86.84 5.48 1.86 2 3.01 2.91

Interest Coverage - 0.34 1.04 - - - - - -

Source: Mergent Online Appendix 24: Embraer performance ratios and indicators (NYS:ERJ) Profitability Ratios 12/31/2006 12/31/2005 12/31/2004 12/31/2003 12/31/2002 12/31/2001 12/31/2000 12/31/1999 12/31/1998

Return on Equity (%) 12.33 14.97 28.43 15.75 35.44 44.81 41.93 59.12 31.6

Return on Assets (%) 3.82 4.17 8.85 4.58 10.49 14.25 12.65 11.91 6.42

Return on Investment 14.17 18.31 40.74 26.9 70.8 117.07 81.88 47.44 28.5

Gross Margin 0.025 0.024 0.033 0.036 0.045 0.042 0.031 0.029 0.028

Operating Margin (%) 6.23 4.97 9.9 10.49 16.67 22.49 16.05 11.6 10.65

Pre-Tax Margin 6.06 5.12 9.89 9.79 16.61 21.95 16.43 10.66 10.21

Net Profit Margin (%) 7.45 7.76 12.27 8.94 15.22 15.98 12.65 12.24 8.41

Effective Tax Rate (%) 0.98 1.06 1.88 2.25 3.54 4.37 2.32 -1.55 0.42

Liquidity Indicators 12/31/2006 12/31/2005 12/31/2004 12/31/2003 12/31/2002 12/31/2001 12/31/2000 12/31/1999 12/31/1998

Quick Ratio 0.59 0.72 0.66 0.6 0.42 0.44 0.87 0.26 0.25

Current Ratio 1.63 1.81 1.91 1.53 1.54 1.51 1.52 1.23 0.96

Working Capital/Total Assets 0.25 0.3 0.35 0.25 0.27 0.26 0.27 0.14 -0.02

Debt Management 12/31/2006 12/31/2005 12/31/2004 12/31/2003 12/31/2002 12/31/2001 12/31/2000 12/31/1999 12/31/1998

Current Liabilities/Equity 1.27 1.31 1.23 1.63 1.65 1.61 1.73 2.98 2.99

Total Debt to Equity 0.55 0.78 0.5 0.41 0.33 0.23 0.23 0.47 0.36

Long Term Debt to Assets 0.17 0.22 0.15 0.12 0.1 0.07 0.07 0.09 0.07

Asset Management 12/31/2006 12/31/2005 12/31/2004 12/31/2003 12/31/2002 12/31/2001 12/31/2000 12/31/1999 12/31/1998

Revenues/Total Assets 0.51 0.54 0.72 0.51 0.69 0.89 1 0.97 0.76

Revenues/Working Capital 2.08 1.82 2.08 2.03 2.59 3.41 3.68 7.21 -33.84

Interest Coverage 3.33 2.68 3.22 5.17 5.77 9.95 9.91 - -

Source: Mergent Online

Bombardier Aerospace: The CSeries Dilemma

Copyright © Ali Taleb & Louis Hébert 26

References

1 Aero Morning http://www.aeromorning.com/en/chroniques.php?ch_id=178 (30 March 2007) 2 European Community:

http://europa.eu/rapid/pressReleasesAction.do?reference=IP/01/501&format=HTML&aged=1&language=en&guiLanguage=en

3 Canadian Business Resource: http://www.cbr.ca/CompanyProfile.aspx?format=printable&CompanyID=2559&Language=en

4 International Aerospace Federation : http://www.fai.org/news_archives/fai/000295.asp 5 Quebec Aeronautical Industry Development Strategy:

http://www.mdeie.gouv.qc.ca/fileadmin/sites/internet/documents/publications/pdf/ministere/aeronautical_strategy2006.pdf

6 Industry Canada: http://www.ic.gc.ca/epic/site/ad-ad.nsf/en/ad01212e.html 7 Industry Canada:

http://www.ic.gc.ca/cmb/welcomeic.nsf/261ce500dfcd7259852564820068dc6d/85256a5d006b972085256f3b0072305c!OpenDocument

8 Bombardier Aerospace – Commercial Aircraft Market Forecast 2007-2026 (published in 2007):

http://www.bombardier.com/en/0_0/0_0_1_7/0_0_1_7_8/pdf/20080507_Market_Forecast_Pre-Farnb_FNL.pdf

9 International Civil Aviation Organization Air Transport Bureau: http://www.icao.int/env/EmissionsTrading.htm 10 World Health Organization (21 April 2004) 11 Airline Monitor, January-February 2007 12 Airbus Global Market Forecast 2006-2025: http://www.airbus.com/en/corporate/gmf/ 13 Also see Bombardier Aerospace’s Commercial Aircraft Market Forecast 2007-2026, Airbus’s Global Market

Forecast 2006-2025, Embraer’s Market Outlook – 4th Edition, Boeing’s Current Market Outlook 2007. 14 Airbus Global Market Forecast 2006-2025: http://www.airbus.com/en/corporate/gmf/ 15 Aircraft Industry Report by National Defense University, Washington:

http://www.ndu.edu/icaf/industry/reports/2007/pdf/2007_AIRCRAFT.pdf 16 General Aviation Manufacturers Association: www.gama.aero 17 Bombardier Annual Report 2006 (31 January 2007) 18 General Aviation Manufacturers Association report (9 February 2007): www.gama.aero 19 Bombardier annual report 2007 (31 January 2008):

http://bombardier.com/en/0_0/0_0_1_7/0_0_1_7_4/pdf/annual_report_2007.pdf 20 Bombardier & Speed News public presentation (6 November 2006) 21 Aviation Week : http://www.aviationweek.biz/aw/generic/story_generic.jsp?channel=awst&id=news/

aw061807p3.xml&headline=Mitsubishi%20Spec%20To%20Rival%20Embraer,%20Bombardier%20RJs 22 Aviation-Imaginova Corp.: http://www.aviation.com/technology/ap-070926-superjet-100-rollout.html 23 CompanyNewsGroup : http://news.fraggo.com/2045_-bombardier-devoile-la-maquette-du-cseries-au-salon-

de.htm