Embed Size (px)

Citation preview

Brand OperationsCreating a Competitive Advantage

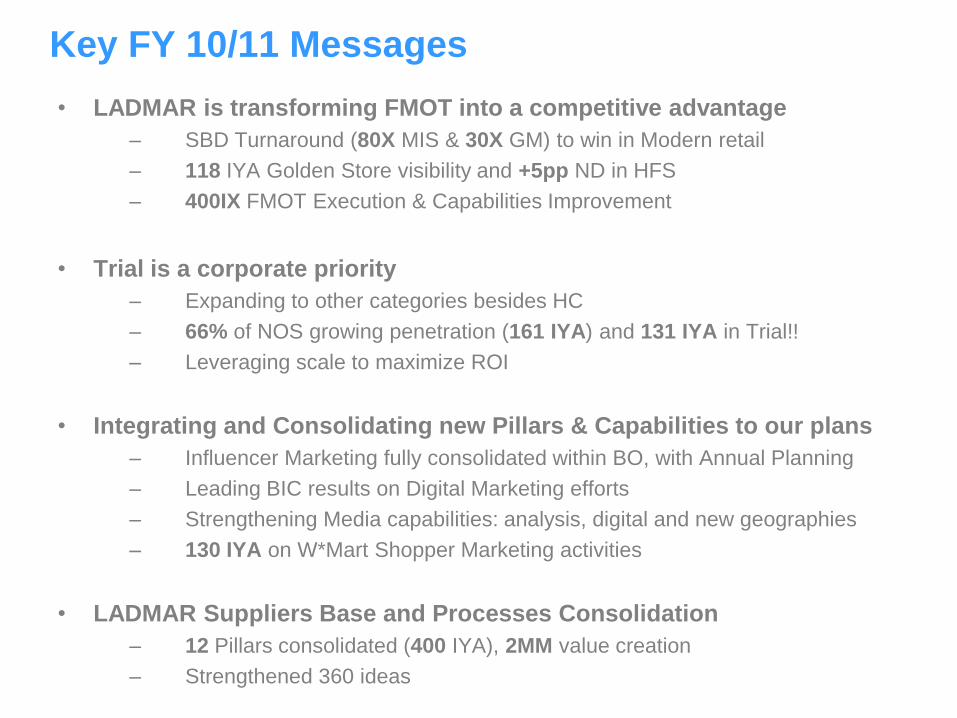

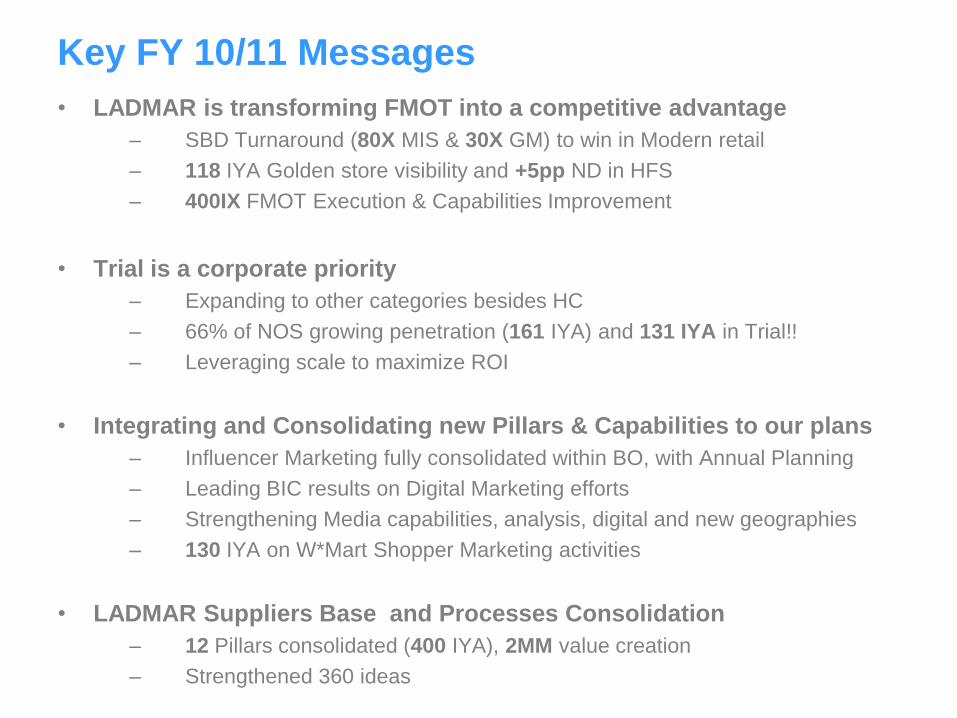

Key FY 10/11 Messages

• LADMAR is transforming FMOT into a competitive advantage

– SBD Turnaround (80X MIS & 30X GM) to win in Modern retail

– 118 IYA Golden Store visibility and +5pp ND in HFS

– 400IX FMOT Execution & Capabilities Improvement

• Trial is a corporate priority

– Expanding to other categories besides HC

– 66% of NOS growing penetration (161 IYA) and 131 IYA in Trial!!

– Leveraging scale to maximize ROI

• Integrating and Consolidating new Pillars & Capabilities to our plans

– Influencer Marketing fully consolidated within BO, with Annual Planning

– Leading BIC results on Digital Marketing efforts

– Strengthening Media capabilities: analysis, digital and new geographies

– 130 IYA on W*Mart Shopper Marketing activities

• LADMAR Suppliers Base and Processes Consolidation

– 12 Pillars consolidated (400 IYA), 2MM value creation

– Strengthened 360 ideas

FMOT

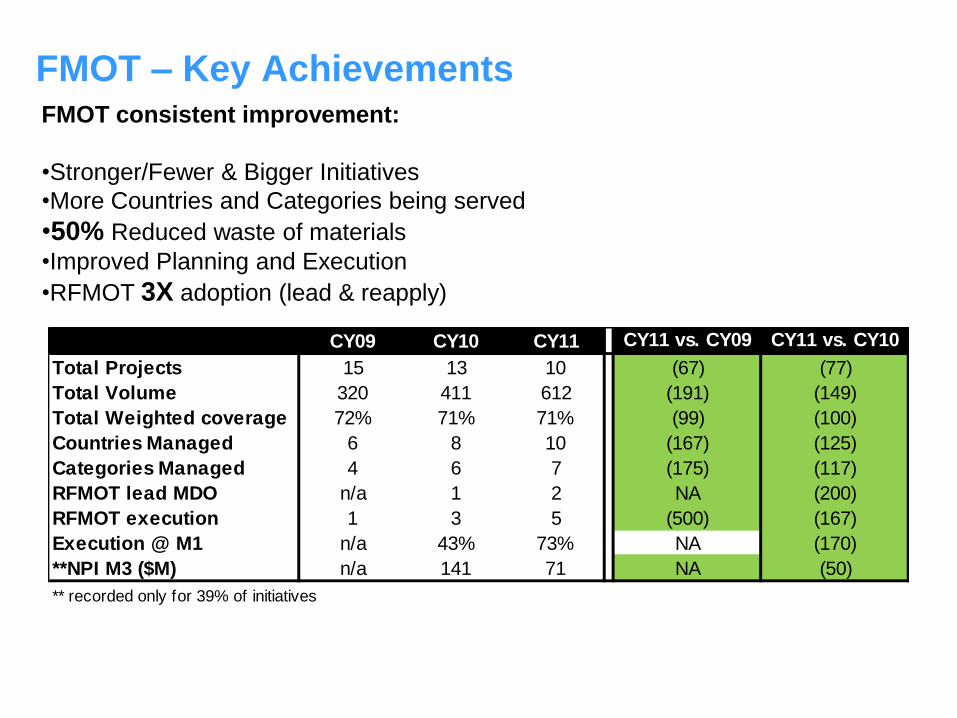

FMOT – Key AchievementsFMOT consistent improvement:

•Stronger/Fewer & Bigger Initiatives

•More Countries and Categories being served

•50% Reduced waste of materials

•Improved Planning and Execution

•RFMOT 3X adoption (lead & reapply)

CY09 CY10 CY11 CY11 vs. CY09 CY11 vs. CY10

Total Projects 15 13 10 (67) (77)

Total Volume 320 411 612 (191) (149)

Total Weighted coverage 72% 71% 71% (99) (100)

Countries Managed 6 8 10 (167) (125)

Categories Managed 4 6 7 (175) (117)

RFMOT lead MDO n/a 1 2 NA (200)

RFMOT execution 1 3 5 (500) (167)

Execution @ M1 n/a 43% 73% NA (170)

**NPI M3 ($M) n/a 141 71 NA (50)

** recorded only for 39% of initiatives

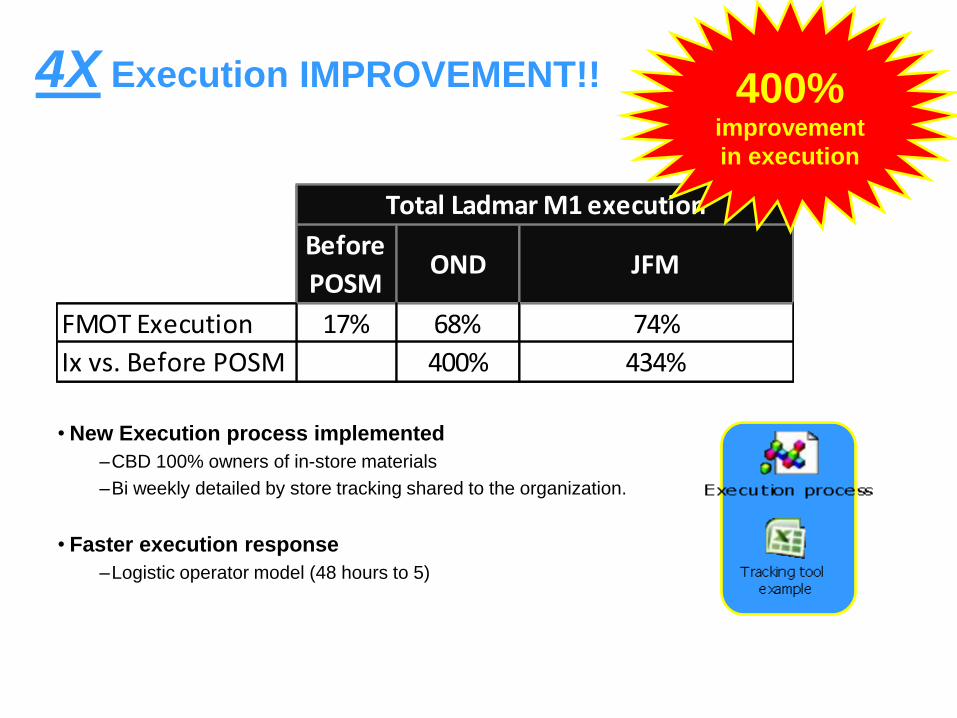

• New Execution process implemented

–CBD 100% owners of in-store materials

–Bi weekly detailed by store tracking shared to the organization.

• Faster execution response

–Logistic operator model (48 hours to 5)

4X Execution IMPROVEMENT!!

Before

POSMOND JFM

FMOT Execution 17% 68% 74%

Ix vs. Before POSM 400% 434%

Total Ladmar M1 execution

400% improvement

in execution

Key Messages

• FMOT Corporate annual Plan

– 6 categories with Annual FMOT spaces Mapped (per store)

– Leveraging Shopper Spectrum (premium materials on experiential consumer)

• LADMAR Leading LA D-Max implementation

– 4 D-Max executed initiatives (early win: savings stands @70% for Grooming)

• Capabilities Improvement at every FMOT stage– Design (briefing)

– Production (Prototyping pilot)

– Delivery (new process)

• Innovation at POS

– FuturAD Panama: TV End caps in HC (13% Incr. vol. & 8 ROI)

Awarded and recognized as a BIC

application of Shopper Spectrum

tool by the LA CMK team

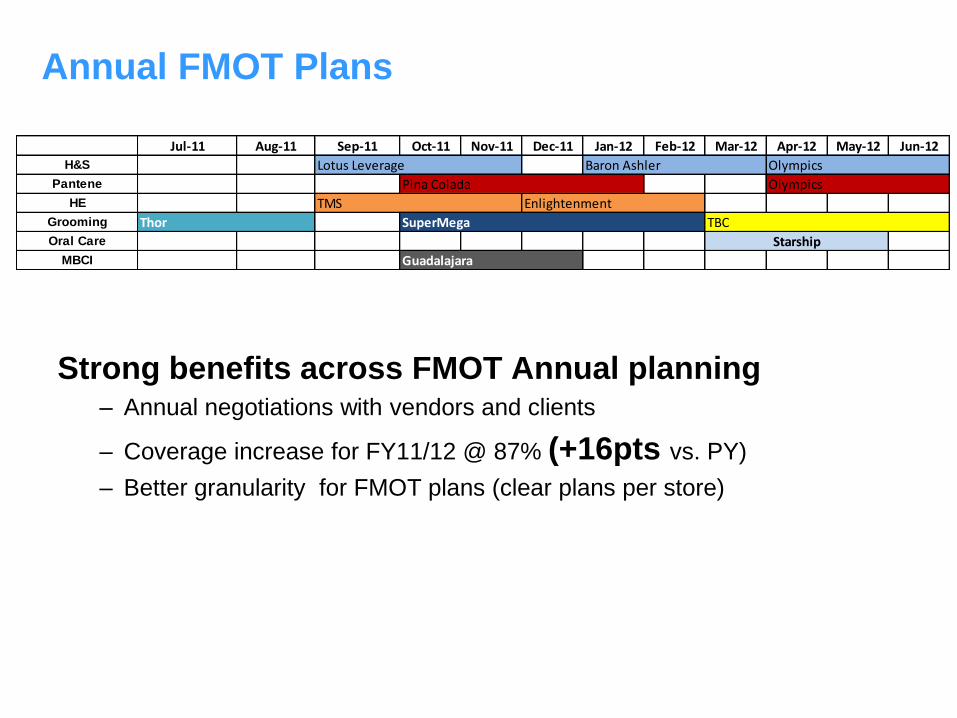

Annual FMOT Plans

Strong benefits across FMOT Annual planning– Annual negotiations with vendors and clients

– Coverage increase for FY11/12 @ 87% (+16pts vs. PY)

– Better granularity for FMOT plans (clear plans per store)

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

H&S

Pantene

HE

Grooming SuperMega TBC

Oral Care

MBCI Guadalajara

Starship

Olympics

Olympics

TMS Enlightenment

Thor

Baron AshlerLotus Leverage

Pina Colada

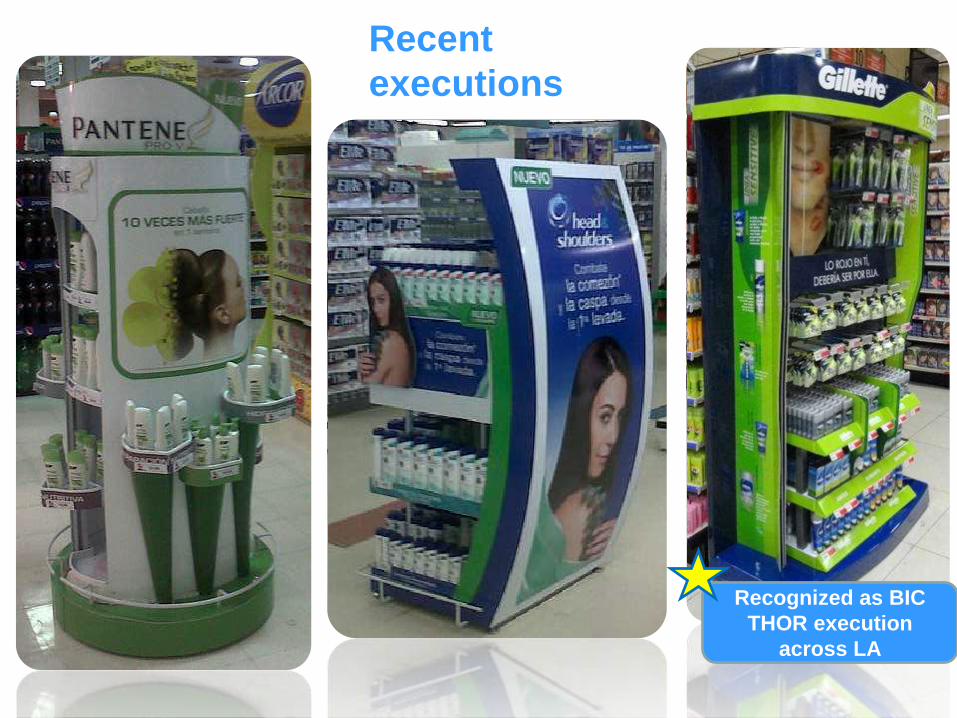

Recent

executions

Recognized as BIC

THOR execution

across LA

Recent

executions

Recognized as BIC

THOR execution

across LA

FutureAd

ISMT BIC results (ISMT):

•Stopping power: 255 Ix vs. average vehicle

•Holding power: 205 Ix vs. average vehicle

•Closing power: 507 Ix vs. control.

•Claim: 54DWB CO & 31DWB MX (higher

than Glade)

RFMOT Avalanche

Winner of POPAI to prize in

Brazil (Global association

for MKT at Retail)

Avalanche Colombia & Brazil

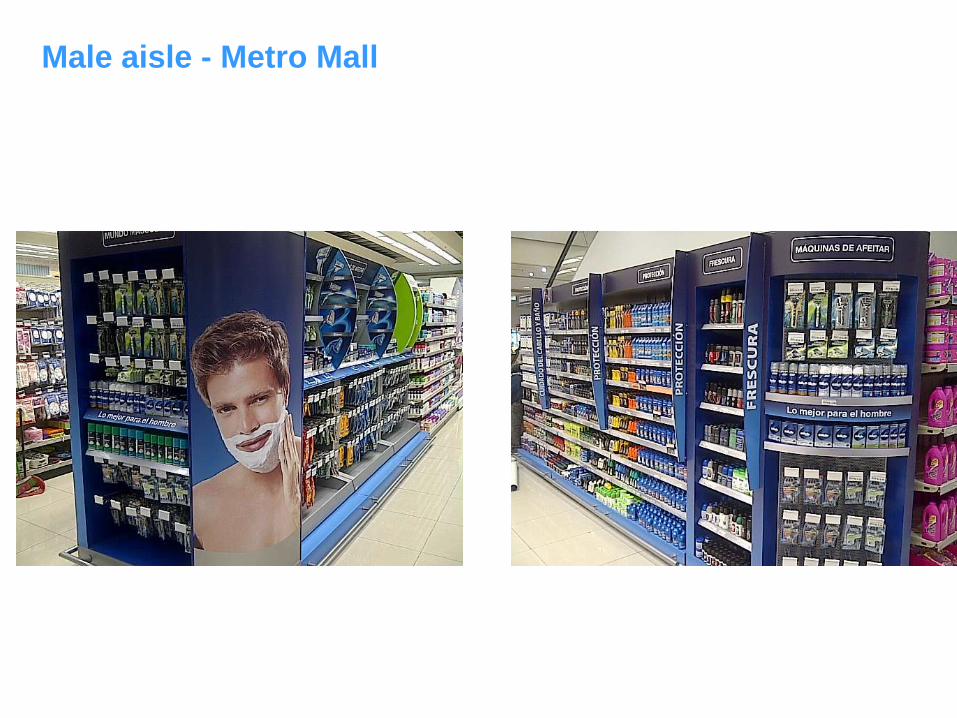

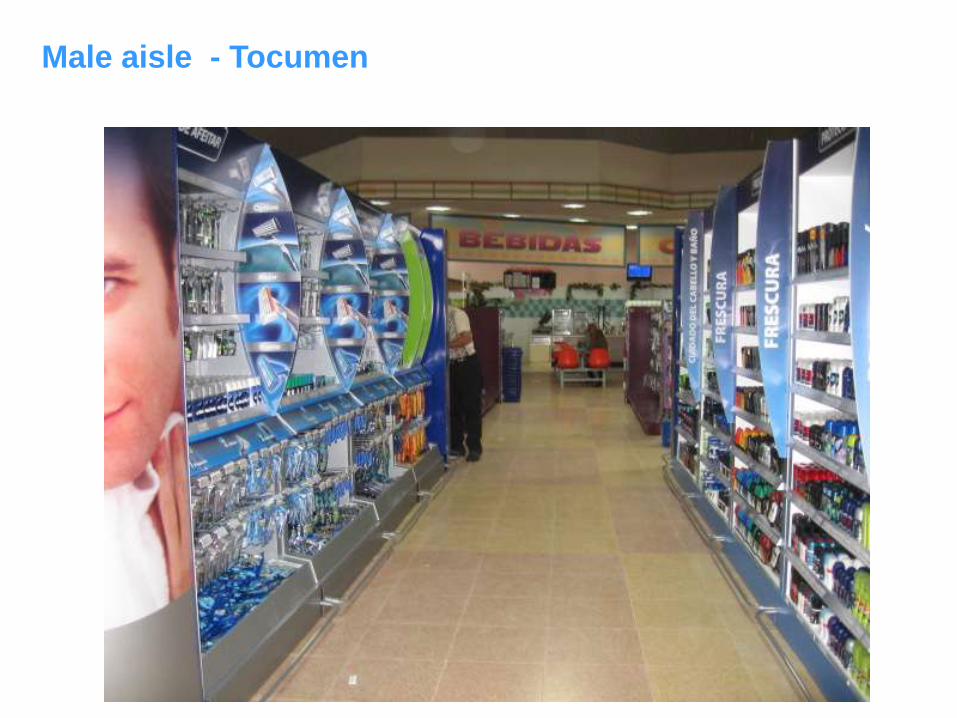

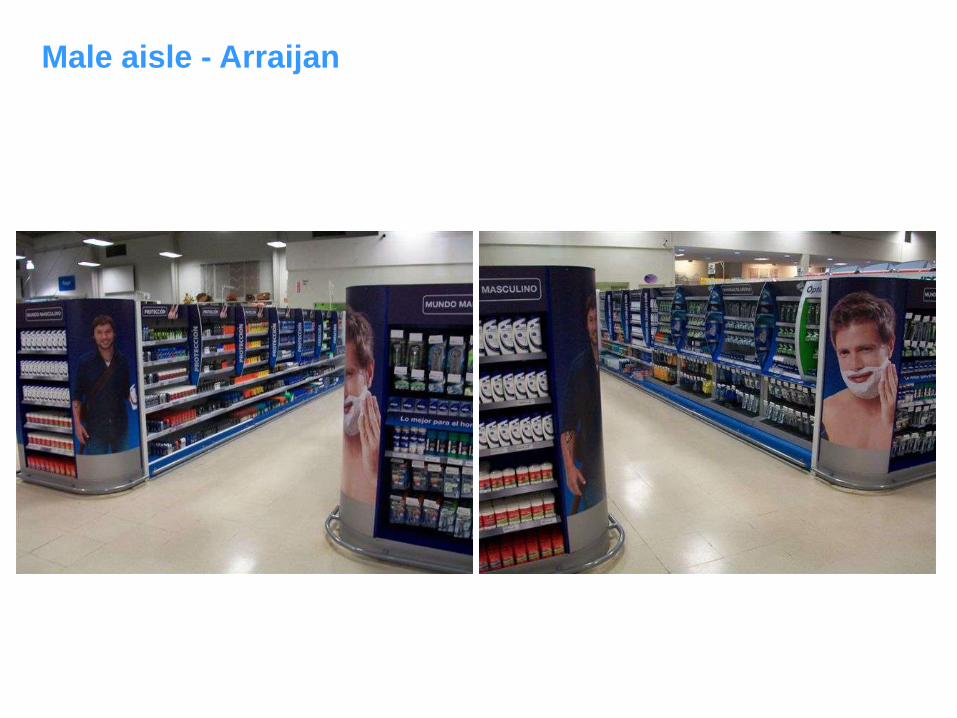

Male aisle - Metro Mall

Male aisle - Tocumen

Male aisle - Arraijan

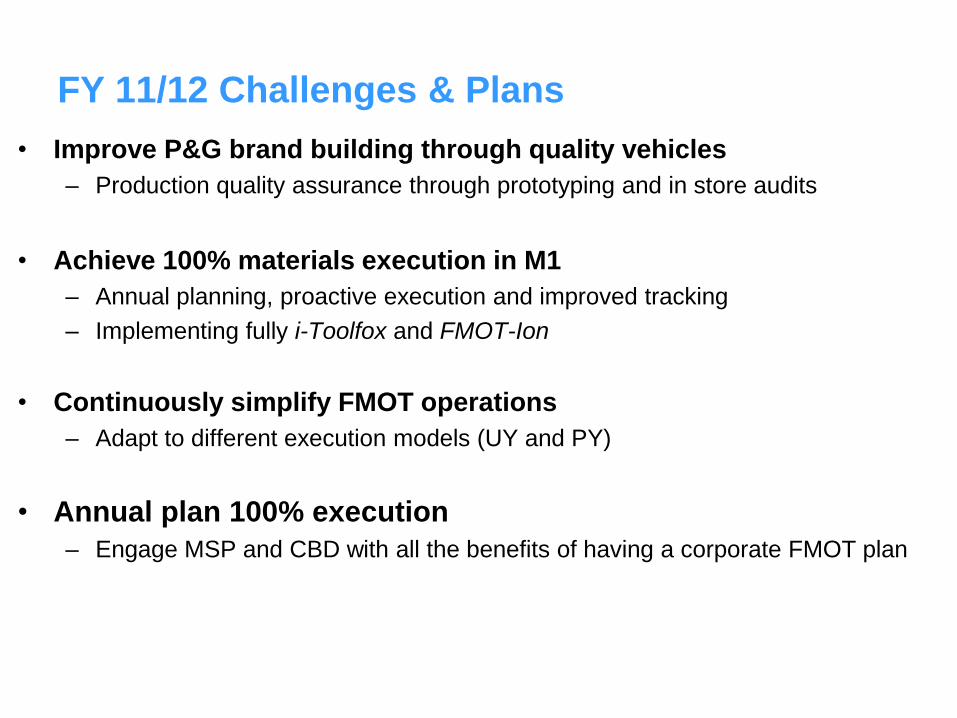

FY 11/12 Challenges & Plans

• Improve P&G brand building through quality vehicles

– Production quality assurance through prototyping and in store audits

• Achieve 100% materials execution in M1

– Annual planning, proactive execution and improved tracking

– Implementing fully i-Toolfox and FMOT-Ion

• Continuously simplify FMOT operations

– Adapt to different execution models (UY and PY)

• Annual plan 100% execution

– Engage MSP and CBD with all the benefits of having a corporate FMOT plan

SBD & CATMAN

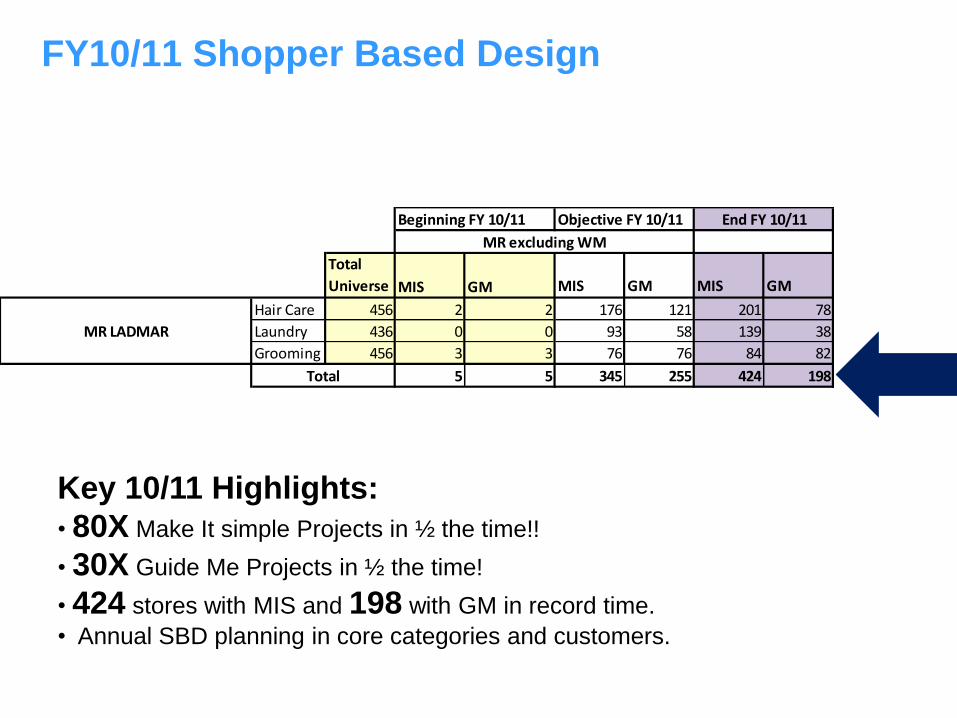

FY10/11 Shopper Based Design

Key 10/11 Highlights:

• 80X Make It simple Projects in ½ the time!!

• 30X Guide Me Projects in ½ the time!

• 424 stores with MIS and 198 with GM in record time.

• Annual SBD planning in core categories and customers.

Beginning FY 10/11 Objective FY 10/11

Total

Universe MIS GM MIS GM MIS GM

Hair Care 456 2 2 176 121 201 78

Laundry 436 0 0 93 58 139 38

Grooming 456 3 3 76 76 84 82

5 5 345 255 424 198

End FY 10/11

MR LADMAR

MR excluding WM

Total

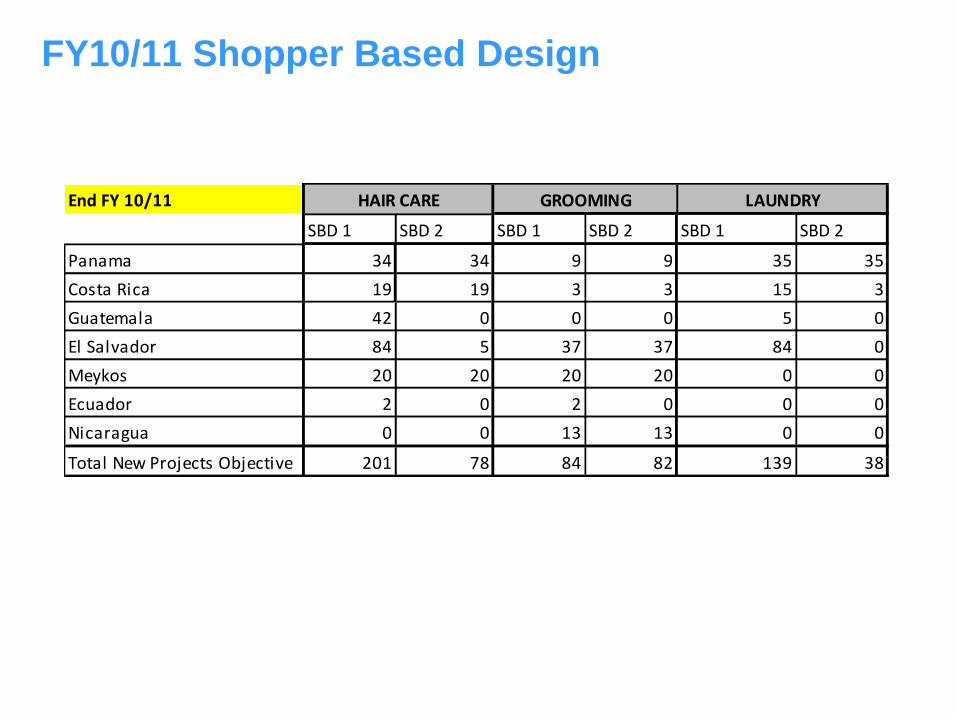

FY10/11 Shopper Based Design

End FY 10/11

SBD 1 SBD 2 SBD 1 SBD 2 SBD 1 SBD 2

Panama 34 34 9 9 35 35

Costa Rica 19 19 3 3 15 3

Guatemala 42 0 0 0 5 0

El Salvador 84 5 37 37 84 0

Meykos 20 20 20 20 0 0

Ecuador 2 0 2 0 0 0

Nicaragua 0 0 13 13 0 0

Total New Projects Objective 201 78 84 82 139 38

HAIR CARE GROOMING LAUNDRY

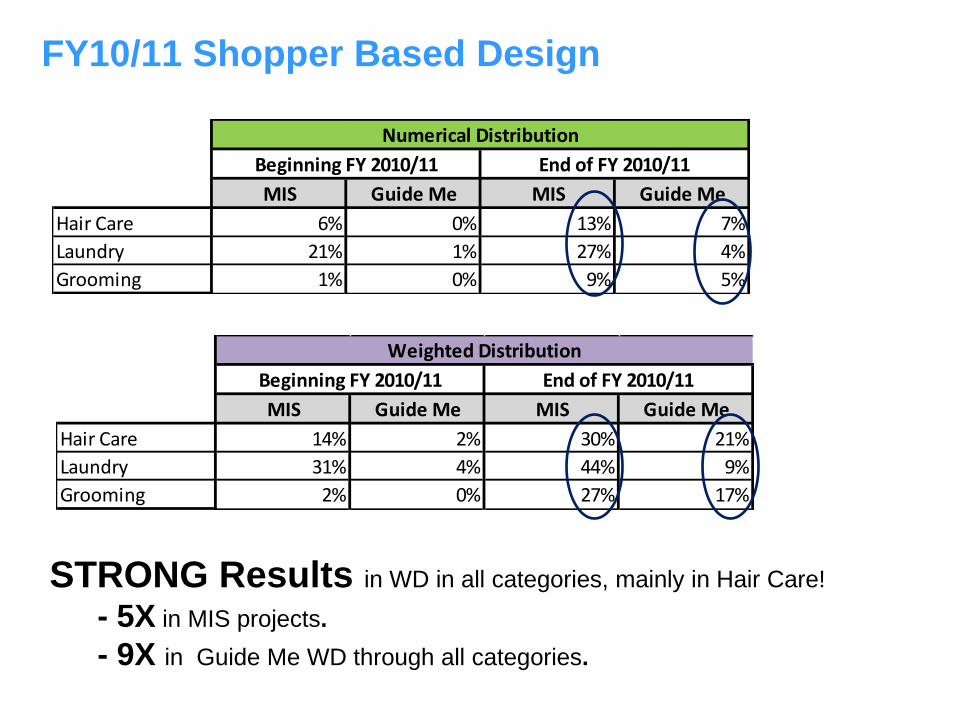

MIS Guide Me MIS Guide Me

Hair Care 6% 0% 13% 7%

Laundry 21% 1% 27% 4%

Grooming 1% 0% 9% 5%

Numerical Distribution

Beginning FY 2010/11 End of FY 2010/11

MIS Guide Me MIS Guide Me

Hair Care 14% 2% 30% 21%

Laundry 31% 4% 44% 9%

Grooming 2% 0% 27% 17%

Weighted Distribution

Beginning FY 2010/11 End of FY 2010/11

STRONG Results in WD in all categories, mainly in Hair Care!

- 5X in MIS projects.

- 9X in Guide Me WD through all categories.

FY10/11 Shopper Based Design

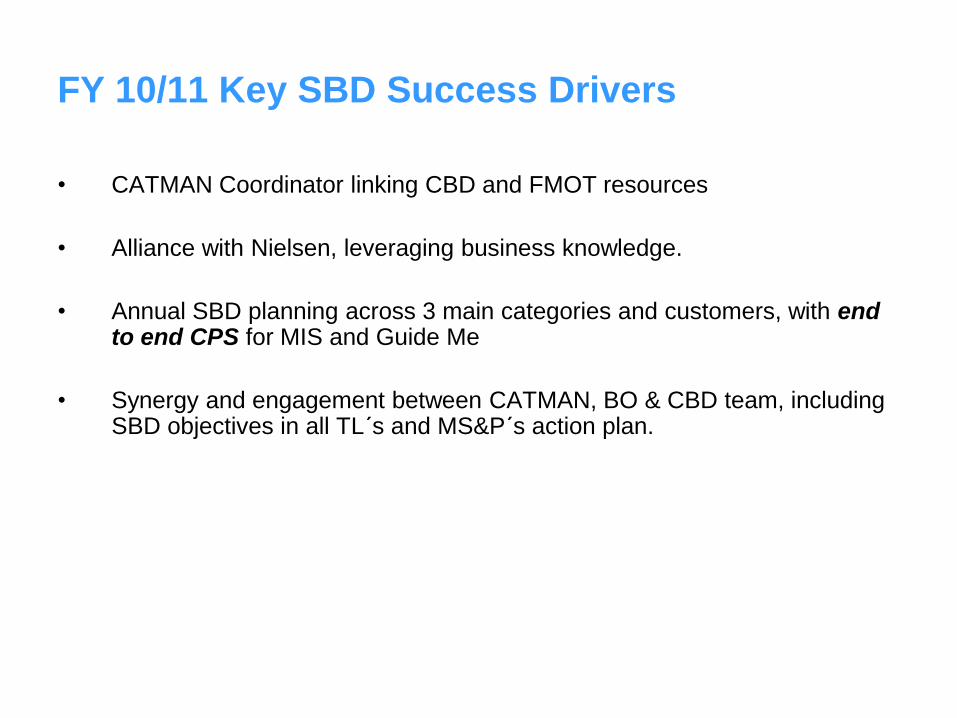

FY 10/11 Key SBD Success Drivers

• CATMAN Coordinator linking CBD and FMOT resources

• Alliance with Nielsen, leveraging business knowledge.

• Annual SBD planning across 3 main categories and customers, with end to end CPS for MIS and Guide Me

• Synergy and engagement between CATMAN, BO & CBD team, including SBD objectives in all TL´s and MS&P´s action plan.

FY 10/11 SBD Implementation Snapshots

Machetazo Male Aisle:

• 15% growth in P&G categories

• Superior shopping experience acknowledged by customers.

• Improved relationship with customer management.

• Extra visibility negotiated to improve ROI (BIC LA)

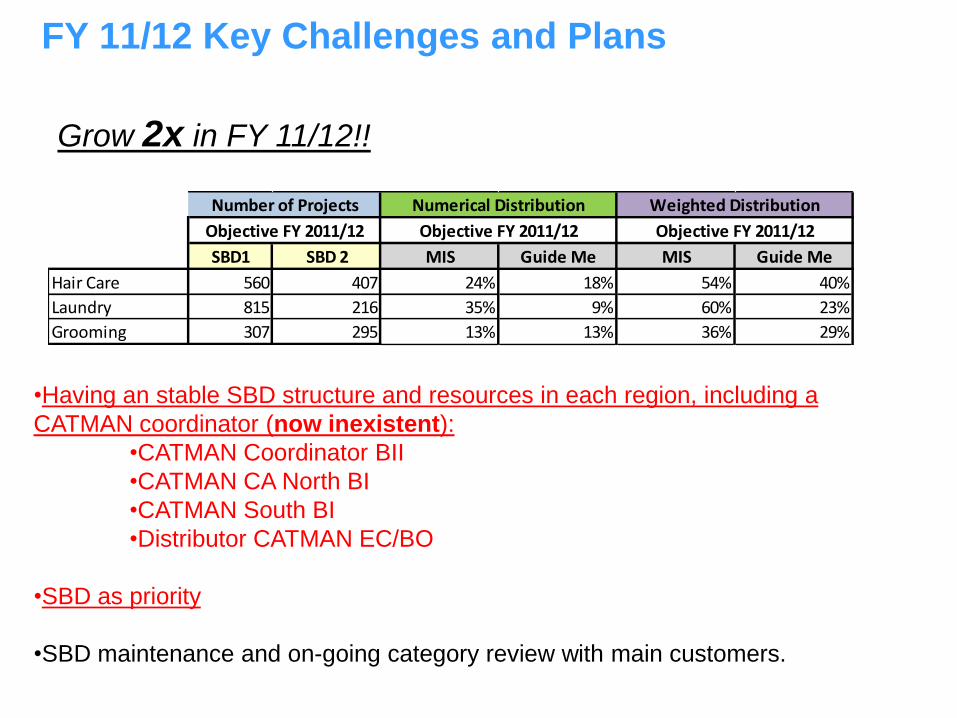

FY 11/12 Key Challenges and Plans

•Having an stable SBD structure and resources in each region, including a

CATMAN coordinator (now inexistent):

•CATMAN Coordinator BII

•CATMAN CA North BI

•CATMAN South BI

•Distributor CATMAN EC/BO

•SBD as priority

•SBD maintenance and on-going category review with main customers.

Grow 2x in FY 11/12!!

SBD1 SBD 2 MIS Guide Me MIS Guide Me

Hair Care 560 407 24% 18% 54% 40%

Laundry 815 216 35% 9% 60% 23%

Grooming 307 295 13% 13% 36% 29%

Weighted Distribution

Objective FY 2011/12

Numerical DistributionNumber of Projects

Objective FY 2011/12Objective FY 2011/12

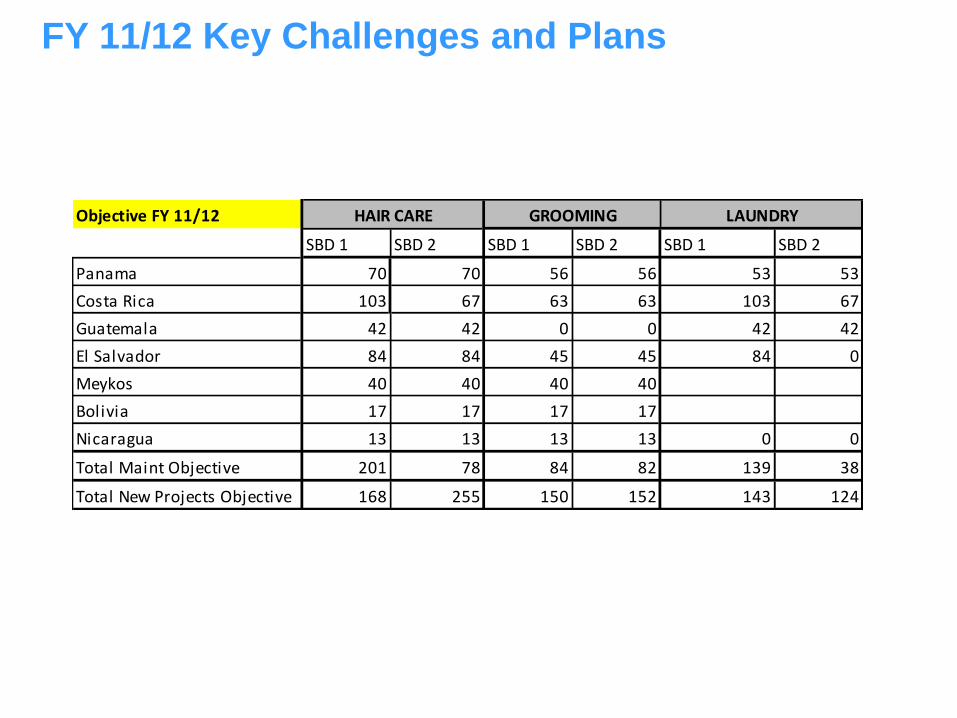

FY 11/12 Key Challenges and Plans

Objective FY 11/12

SBD 1 SBD 2 SBD 1 SBD 2 SBD 1 SBD 2

Panama 70 70 56 56 53 53

Costa Rica 103 67 63 63 103 67

Guatemala 42 42 0 0 42 42

El Salvador 84 84 45 45 84 0

Meykos 40 40 40 40

Bolivia 17 17 17 17

Nicaragua 13 13 13 13 0 0

Total Maint Objective 201 78 84 82 139 38

Total New Projects Objective 168 255 150 152 143 124

HAIR CARE GROOMING LAUNDRY

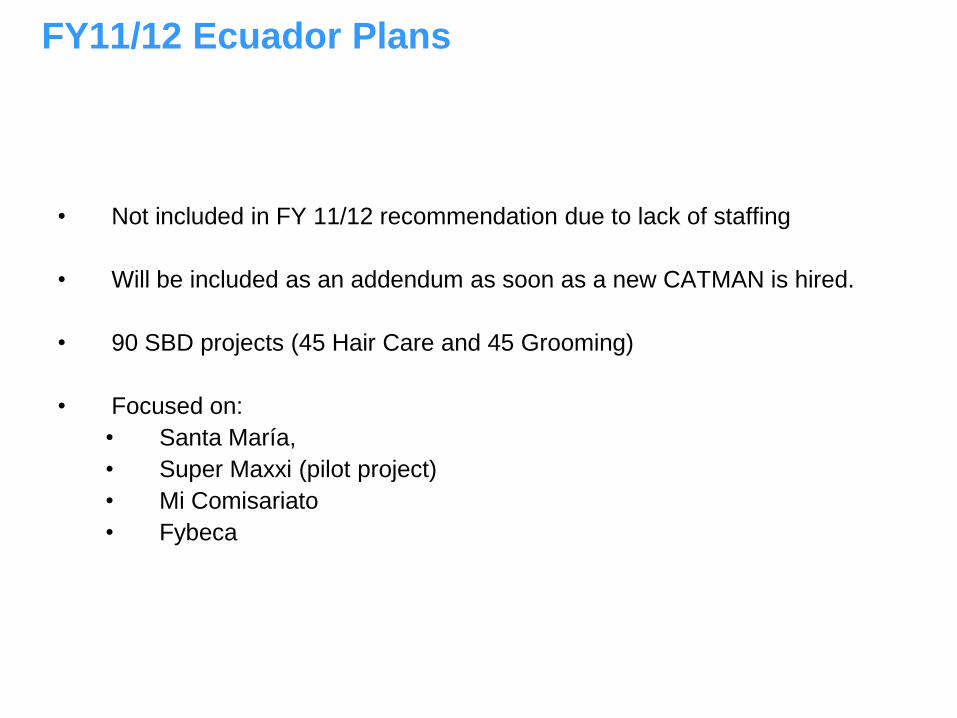

FY11/12 Ecuador Plans

• Not included in FY 11/12 recommendation due to lack of staffing

• Will be included as an addendum as soon as a new CATMAN is hired.

• 90 SBD projects (45 Hair Care and 45 Grooming)

• Focused on:

• Santa María,

• Super Maxxi (pilot project)

• Mi Comisariato

• Fybeca

Shopper Marketing HFS

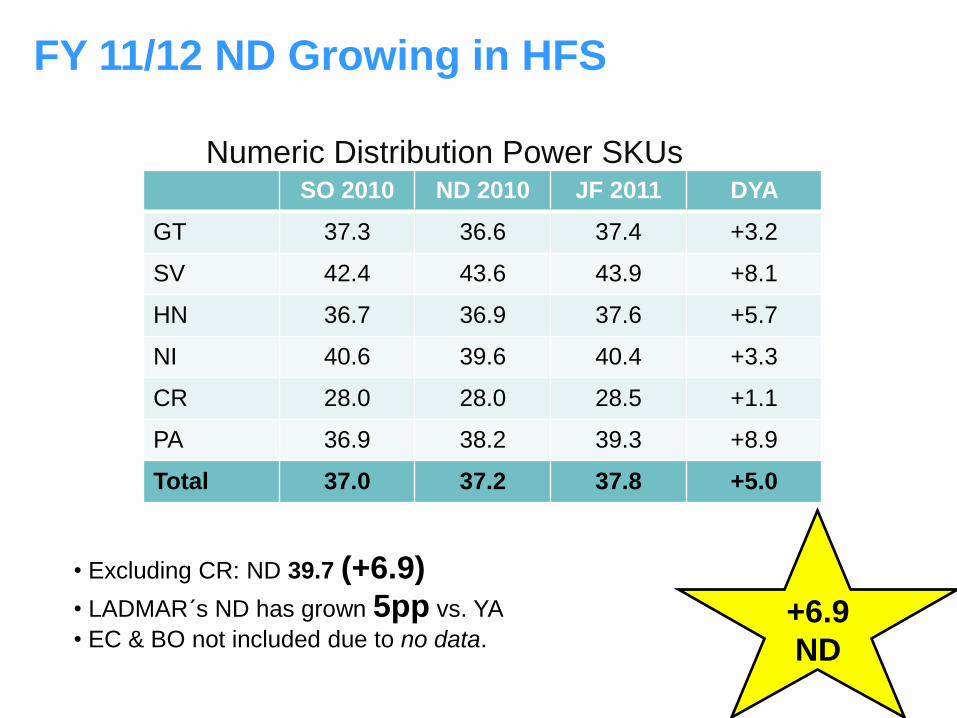

+6.9

ND

Numeric Distribution Power SKUsSO 2010 ND 2010 JF 2011 DYA

GT 37.3 36.6 37.4 +3.2

SV 42.4 43.6 43.9 +8.1

HN 36.7 36.9 37.6 +5.7

NI 40.6 39.6 40.4 +3.3

CR 28.0 28.0 28.5 +1.1

PA 36.9 38.2 39.3 +8.9

Total 37.0 37.2 37.8 +5.0

• Excluding CR: ND 39.7 (+6.9)

• LADMAR´s ND has grown 5pp vs. YA

• EC & BO not included due to no data.

FY 11/12 ND Growing in HFS

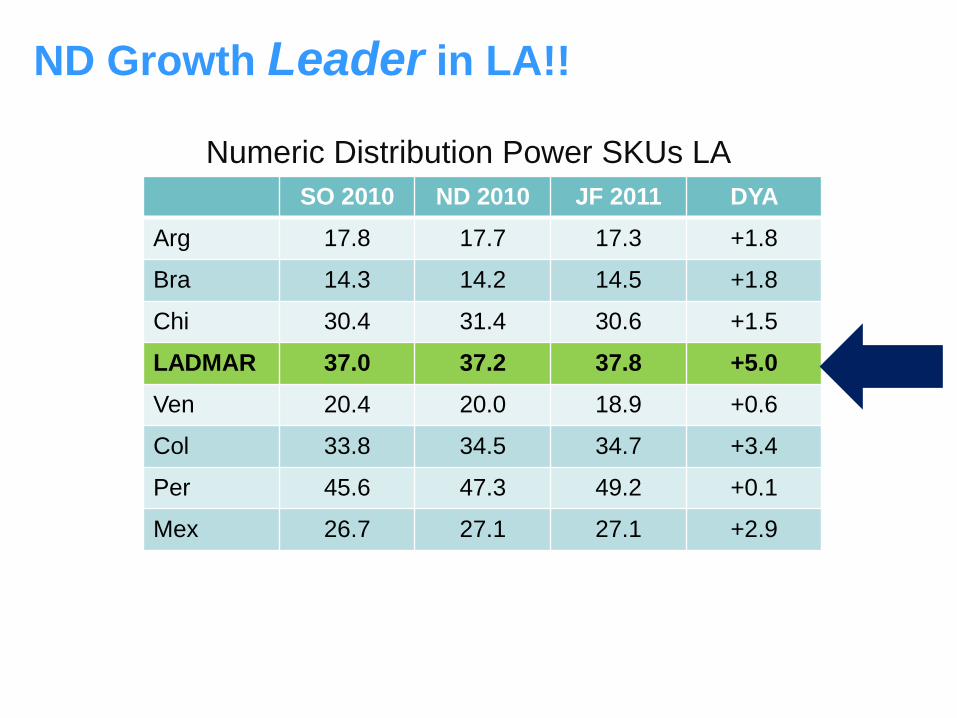

SO 2010 ND 2010 JF 2011 DYA

Arg 17.8 17.7 17.3 +1.8

Bra 14.3 14.2 14.5 +1.8

Chi 30.4 31.4 30.6 +1.5

LADMAR 37.0 37.2 37.8 +5.0

Ven 20.4 20.0 18.9 +0.6

Col 33.8 34.5 34.7 +3.4

Per 45.6 47.3 49.2 +0.1

Mex 26.7 27.1 27.1 +2.9

ND Growth Leader in LA!!

Numeric Distribution Power SKUs LA

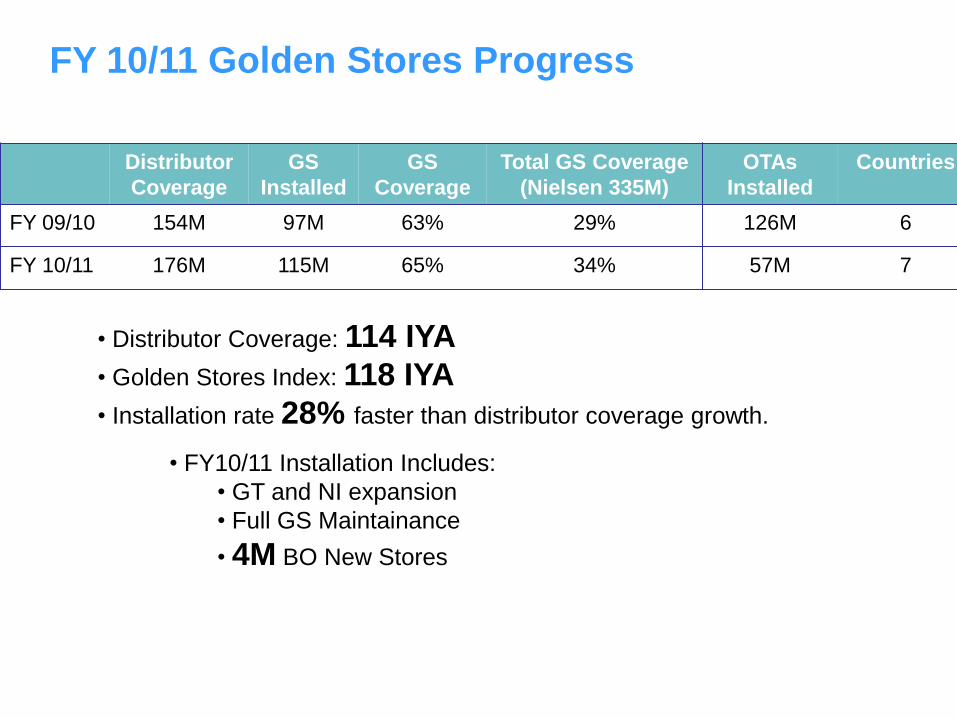

FY 10/11 Golden Stores Progress

Distributor

Coverage

GS

Installed

GS

Coverage

Total GS Coverage

(Nielsen 335M)

FY 09/10 154M 97M 63% 29%

FY 10/11 176M 115M 65% 34%

• Distributor Coverage: 114 IYA

• Golden Stores Index: 118 IYA

• Installation rate 28% faster than distributor coverage growth.

• FY10/11 Installation Includes:

• GT and NI expansion

• Full GS Maintainance

• 4M BO New Stores

OTAs

Installed

Countries

126M 6

57M 7

Key Messages

• Training Model/Module Improvement

• Video/Objection Management Exercises/ Exam and Presentation

• Distributor Involvement

• Installation Teams

• Ownership of Project

• Sales Incentive Pilot

• Reward installation

• Ensure complete installment in time frame

• Census & weekly tracking system

• Clear definition of stores

• Golden Stores Accountability

• Standardized tracking across executions

FY 11/12 Challenges

• Increase ND 20ppts in HFS Power SKU’s (4pp from GS/16pp Gana Gana)

•100% GS Installation on stores with direct distribution.

• Flawless Installation and maintainance

• Launch GANA GANA: Unified 3 Pillar Program to win in HFS:

-Storeowner

-Sales Force

-Consumers

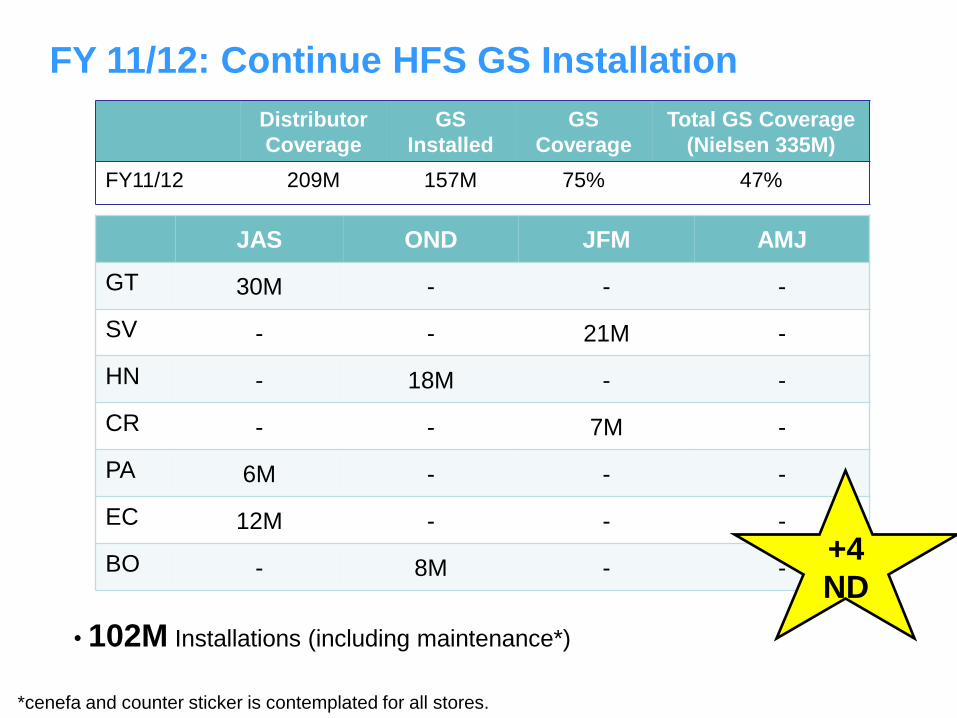

JAS OND JFM AMJ

GT 30M - - -

SV - - 21M -

HN - 18M - -

CR - - 7M -

PA 6M - - -

EC 12M - - -

BO - 8M - -

• 102M Installations (including maintenance*)

FY 11/12: Continue HFS GS Installation

Distributor

Coverage

GS

Installed

GS

Coverage

Total GS Coverage

(Nielsen 335M)

FY11/12 209M 157M 75% 47%

+4

ND

*cenefa and counter sticker is contemplated for all stores.

• Objective:

– Disproportionatelly grow P&G business in HFS.

– Win in Numerical Distribution, sales, Loyalty, and Trial.

• Reward each HFS key player for their

incremental support to PG brands.

– Consumer, Store Owner, & 2nd Sales Force

Gana Gana Corporate HFS Program

Store Owner

• Corporate Trade Plan to drive distribution of

low performance Power SKUs

• Bundle Packs defined by CMK Promo

Evolution

Sales Force

• Corporate Sales Incentive Program.

• 100% sales participation.

• Reward increase ND and sales.

Gana Gana Corporate HFS Program

• Objective:

– Disproportionatelly grow P&G business in HFS.

– Win in Numerical Distribution, sales, Loyalty, and Trial.

• Reward each HFS key player for their

incremental support to PG brands.

– Consumer, Store Owner, & 2nd Sales Force

Consumer

• Product Exchange

• Correlates with SO & SF Efforts

Gana Gana Corporate HFS Program

• Objective:

– Disproportionatelly grow P&G business in HFS.

– Win in Numerical Distribution, sales, Loyalty, and Trial.

• Reward each HFS key player for their

incremental support to PG brands.

– Consumer, Store Owner, & 2nd Sales Force

Shopper Marketing W*Mart

• Volume FYTD 117 IYA

• Shopper Marketing activities contributing to WM´s Sales Growth:

– 13 SMKT Activities (130 IYA):

– 6 Seasonal Promotions

– 3 SBD projects

– 2 MBCI´s – Themed Merchandising Events

– 2 Initiative Maximization Events

• W*M CTMM Integrated to BO Team!

FY 10/11 WM Team KEY Results

• Discount Checkouts (GT & CR)

– 100% Stores (240)

– 135 Ix vs SPYA!!

– Oral Care Big Winner!! but …W*M

removed after 6M.

• Isla del Hombre

– Offshelf exhibitions @ X-Mas

• 16 4Ways vs. 0 in Trade Plan

– 100% Hiper stores implemented (16)

– CR Hiper POS Data:

• Gillette 118 Ix vs SPYA

• H&S 110 Ix vs SPYA

• Old Spice 154 Ix vs SPYA

SBD Projects

• PAMPERS BABY GYM

– Boosting Pampers launch with Festival

Infantil via Baby Gym’s

– Extra Awareness & Trial

– Over 2000 contacts participating

– Shipments 110 Ix vs booklet.

• SEMANA NATURAL (CORA, LOTUS,

GENESIS)

– 30% Incr. Off-shelf visibility for 3 brands.

– In Store Demos w/ “BE Samples”

• 55M contacts with consumers

– POS Sales:

• CORA Pantene: 132 Ix!!

• Genesis: Pert 174 Ix!!

• Lotus H&S: 168 Ix!!

Initiative Maximization

• World Cup MBCI

– Todos ganan con los campeones (WC– WM

Exclusive)

• High visibility and support

• +15% Incr. free additional spaces at

Hiper Format

• High traffic in store.

• 114 POS Sales Ix vs SPYA.

• Wal-Mart Opening Event

– El Tornado Regalón

• May/June in 15 Stores

• Best Ever P&G Brand Visibility in High Traffic

Lobbies

• 21M Contacts!!!

• 9 P&G Brands!!!

• Target 120 off-shelf spaces!!! ~$120M

• 8 per store!!!

• 15 MSU (8% Incr.) - $244M NOS!!

Themed Merchandising Events

Themed Weeks

• Consiente a Papá

– Category innovation – Mach3

Sensitive

– Drive Trial (H&S for Men & Old Spice)

– Drive System usage (Male Grooming

= Head, Face, Body)

– +100M contacts

– 30 secondary locations @ Top 15

WM stores

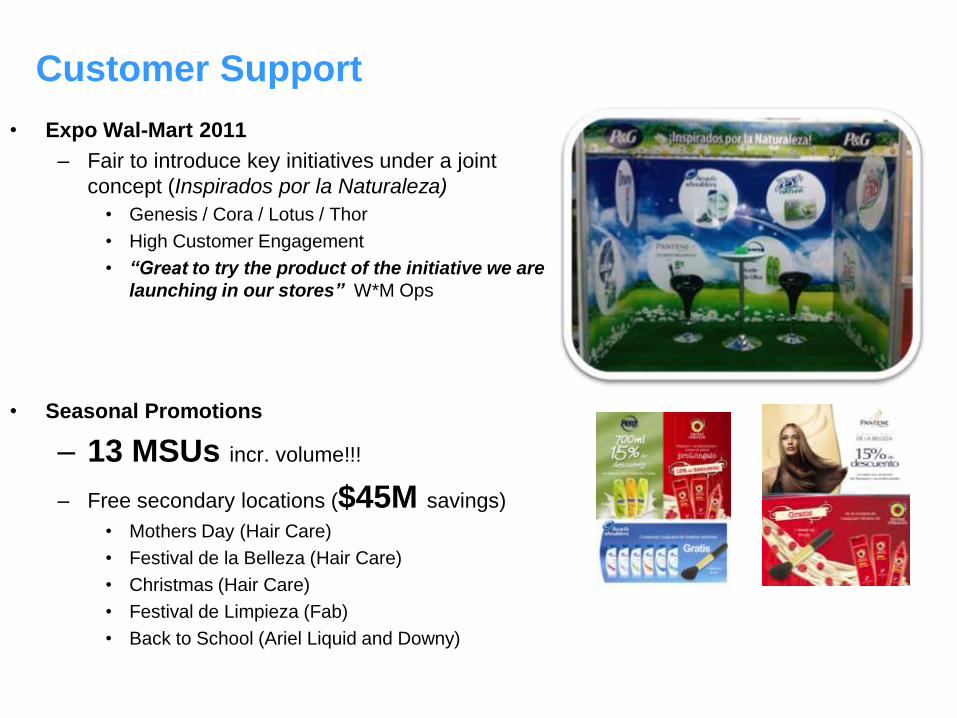

• Expo Wal-Mart 2011

– Fair to introduce key initiatives under a joint

concept (Inspirados por la Naturaleza)

• Genesis / Cora / Lotus / Thor

• High Customer Engagement

• “Great to try the product of the initiative we are

launching in our stores” W*M Ops

• Seasonal Promotions

– 13 MSUs incr. volume!!!

– Free secondary locations ($45M savings)

• Mothers Day (Hair Care)

• Festival de la Belleza (Hair Care)

• Christmas (Hair Care)

• Festival de Limpieza (Fab)

• Back to School (Ariel Liquid and Downy)

Customer Support

• Period impacted by WM´s internal transitions:

– Walmart Central America integration.

– Walmart Mexico & Central America merge and EDLP Model.

• Shopper Marketing strengthening commercial and strategic relationship

with WM

• Delivering solid business results in all core P&G categories. i.e. best in

class initiative executions by standardizing WM Mktg FMOT approval.

• Shopper Marketing became an integrated part of BO Pillars and MOTs

planning for Walmart.

FY 10/11 Messages:

• Overcome major changes in W*Mart

– P&G Brands visibility in Wal-Mart’s clean stores policy?

– Organization and Format re-structure (Mexico & Central America).

– Leverage category captaincies for SBD.

– Agile and flexible Bundles Solution.

• Leverage P&G scale via sustainable MBCI platform

– Develop Annual Plan focused on WM´s key seasons and format strategies

• Include top brands

• Focus on system/regime usage

• Strengthen analysis on business oportunities for core categories.

– Engage with MOTs on key initiatives from start up.

– Capitalize on Imports and WMs drive for these products.

– WM specific plans attacking specific shopper oportunities.

FY 11/12 Challenges & Focus Areas

Trial & Promotions

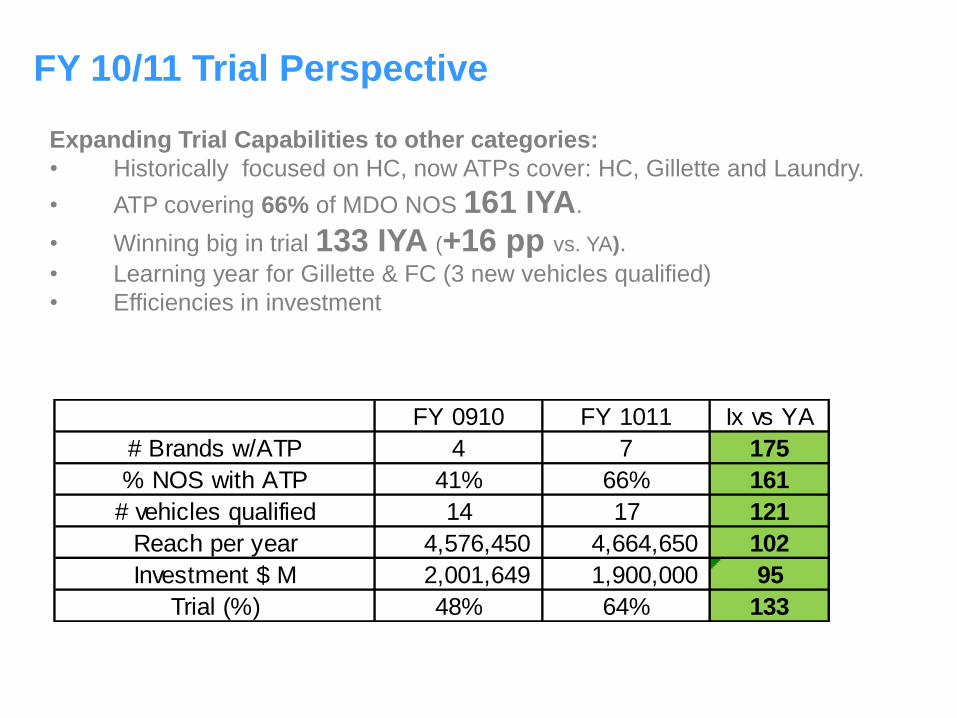

Expanding Trial Capabilities to other categories:

• Historically focused on HC, now ATPs cover: HC, Gillette and Laundry.

• ATP covering 66% of MDO NOS 161 IYA.

• Winning big in trial 133 IYA (+16 pp vs. YA).

• Learning year for Gillette & FC (3 new vehicles qualified)

• Efficiencies in investment

FY 10/11 Trial Perspective

FY 0910 FY 1011 Ix vs YA

# Brands w/ATP 4 7 175

% NOS with ATP 41% 66% 161

# vehicles qualified 14 17 121

Reach per year 4,576,450 4,664,650 102

Investment $ M 2,001,649 1,900,000 95

Trial (%) 48% 64% 133

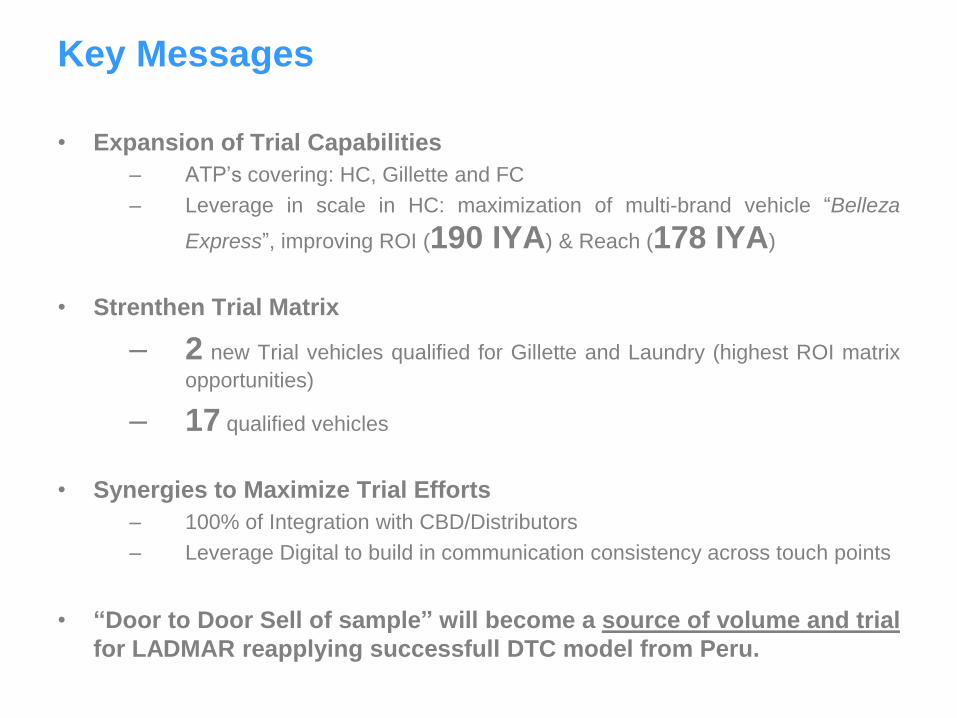

Key Messages

• Expansion of Trial Capabilities

– ATP’s covering: HC, Gillette and FC

– Leverage in scale in HC: maximization of multi-brand vehicle “Belleza

Express”, improving ROI (190 IYA) & Reach (178 IYA)

• Strenthen Trial Matrix

– 2 new Trial vehicles qualified for Gillette and Laundry (highest ROI matrix

opportunities)

– 17 qualified vehicles

• Synergies to Maximize Trial Efforts

– 100% of Integration with CBD/Distributors

– Leverage Digital to build in communication consistency across touch points

• “Door to Door Sell of sample” will become a source of volume and trial

for LADMAR reapplying successfull DTC model from Peru.

Multibrand LIC Central Location Sampling

Trial – Hair Care

Improving ROI (190 IYA) & Reach (178 IYA)

OBJECTIVE: Zero logistic cost vehicles to improve ROI.

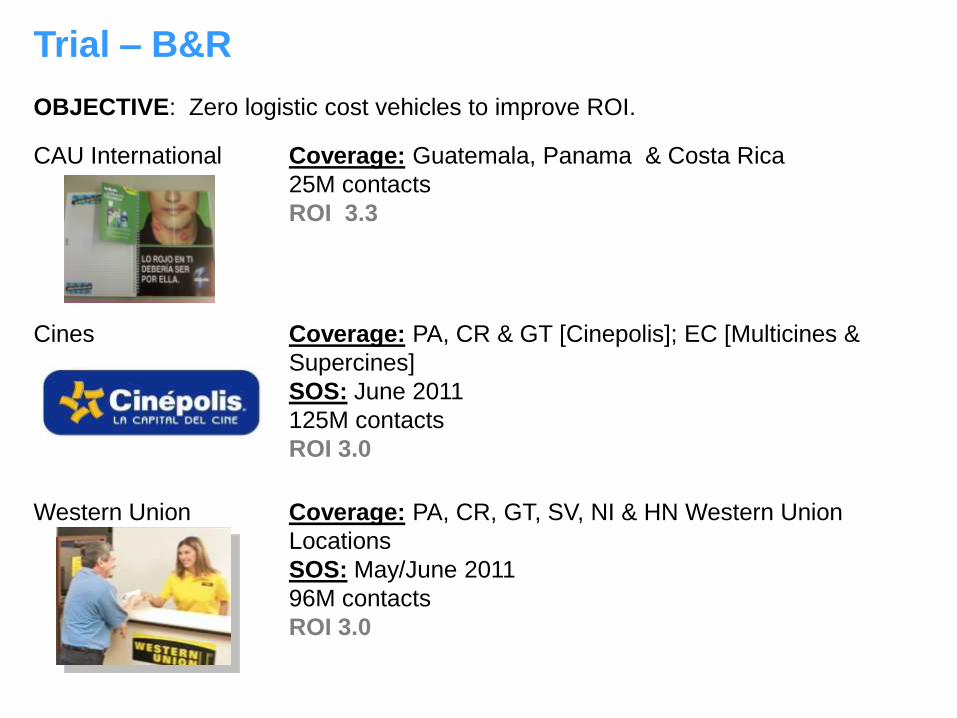

Trial – B&R

CAU International Coverage: Guatemala, Panama & Costa Rica

25M contacts

ROI 3.3

Cines Coverage: PA, CR & GT [Cinepolis]; EC [Multicines &

Supercines]

SOS: June 2011

125M contacts

ROI 3.0

Western Union Coverage: PA, CR, GT, SV, NI & HN Western Union

Locations

SOS: May/June 2011

96M contacts

ROI 3.0

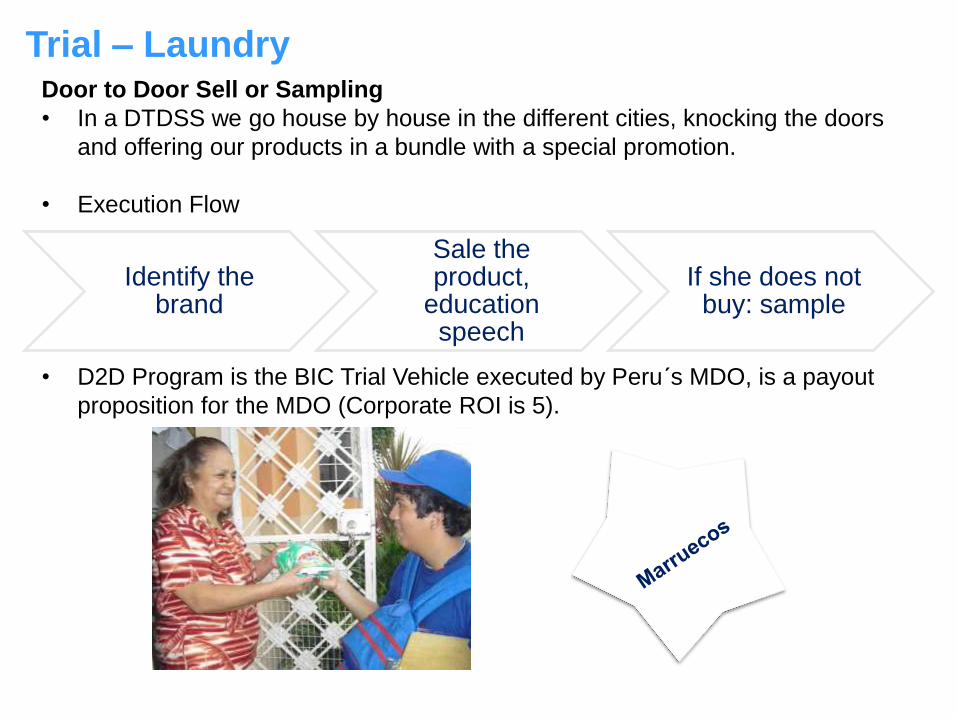

Door to Door Sell or Sampling

• In a DTDSS we go house by house in the different cities, knocking the doors

and offering our products in a bundle with a special promotion.

• Execution Flow

• D2D Program is the BIC Trial Vehicle executed by Peru´s MDO, is a payout

proposition for the MDO (Corporate ROI is 5).

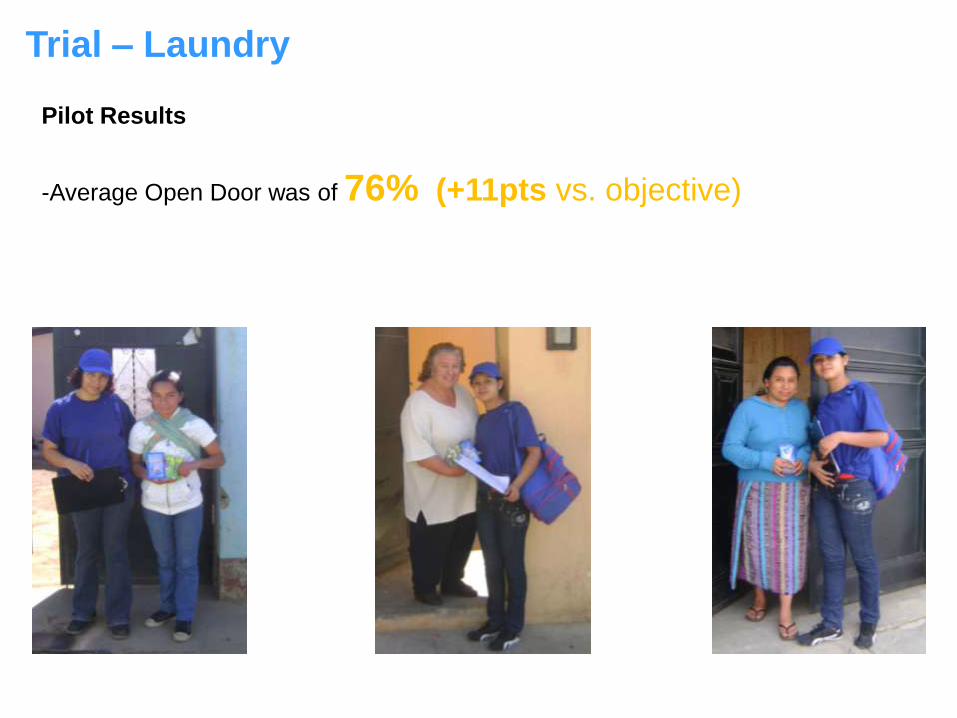

Trial – Laundry

Identify the brand

Sale the product,

education speech

If she does not buy: sample

Trial – Laundry

Pilot Results

-Average Open Door was of 76% (+11pts vs. objective)

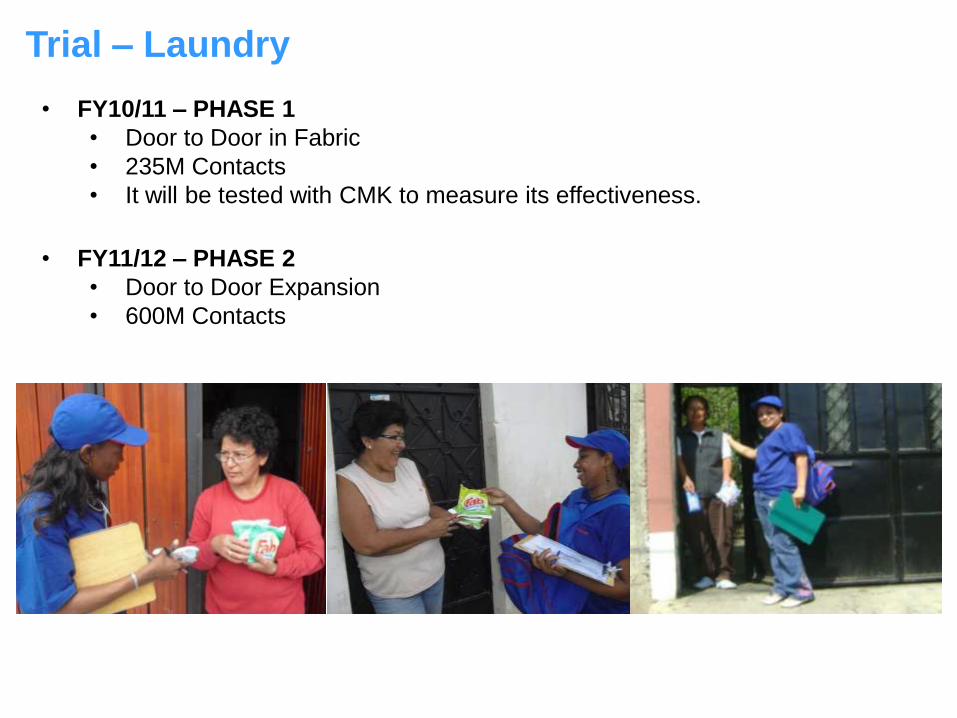

• FY10/11 – PHASE 1

• Door to Door in Fabric

• 235M Contacts

• It will be tested with CMK to measure its effectiveness.

Trial – Laundry

• FY11/12 – PHASE 2

• Door to Door Expansion

• 600M Contacts

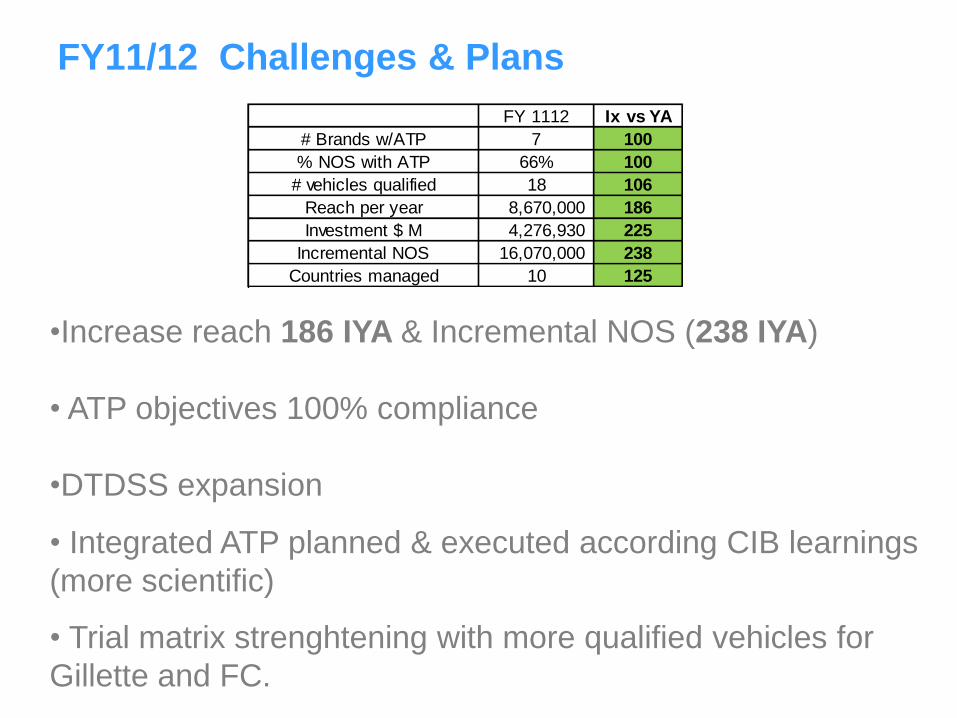

FY11/12 Challenges & Plans

•Increase reach 186 IYA & Incremental NOS (238 IYA)

• ATP objectives 100% compliance

•DTDSS expansion

• Integrated ATP planned & executed according CIB learnings

(more scientific)

• Trial matrix strenghtening with more qualified vehicles for

Gillette and FC.

FY 1112 Ix vs YA

# Brands w/ATP 7 100

% NOS with ATP 66% 100

# vehicles qualified 18 106

Reach per year 8,670,000 186

Investment $ M 4,276,930 225

Incremental NOS 16,070,000 238

Countries managed 10 125

MBCI

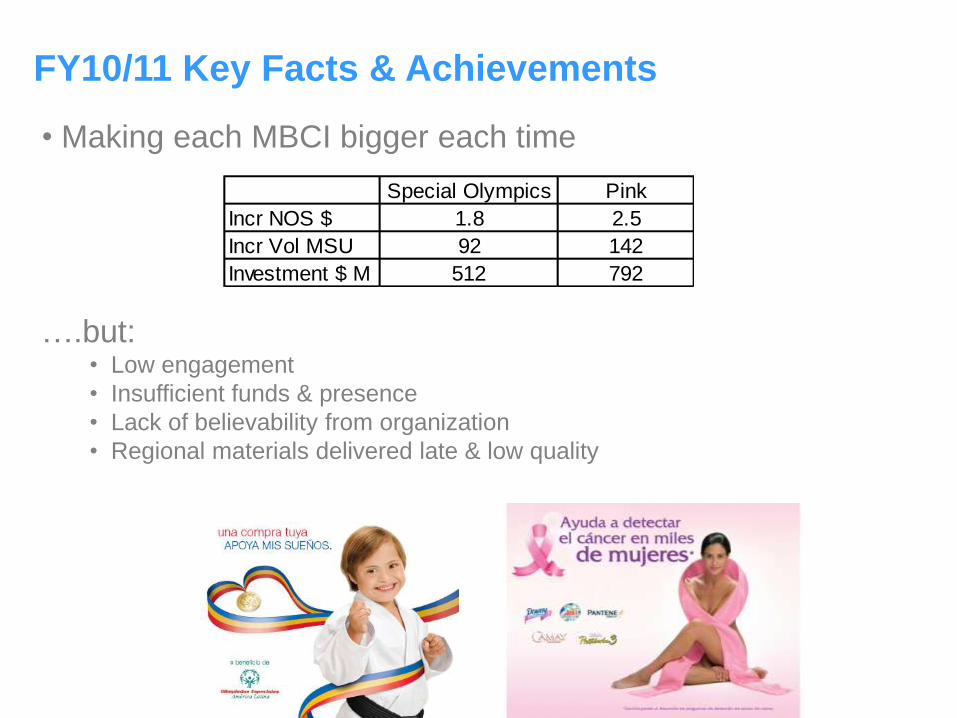

FY10/11 Key Facts & Achievements

• Making each MBCI bigger each time

….but:• Low engagement

• Insufficient funds & presence

• Lack of believability from organization

• Regional materials delivered late & low quality

Special Olympics Pink

Incr NOS $ 1.8 2.5

Incr Vol MSU 92 142

Investment $ M 512 792

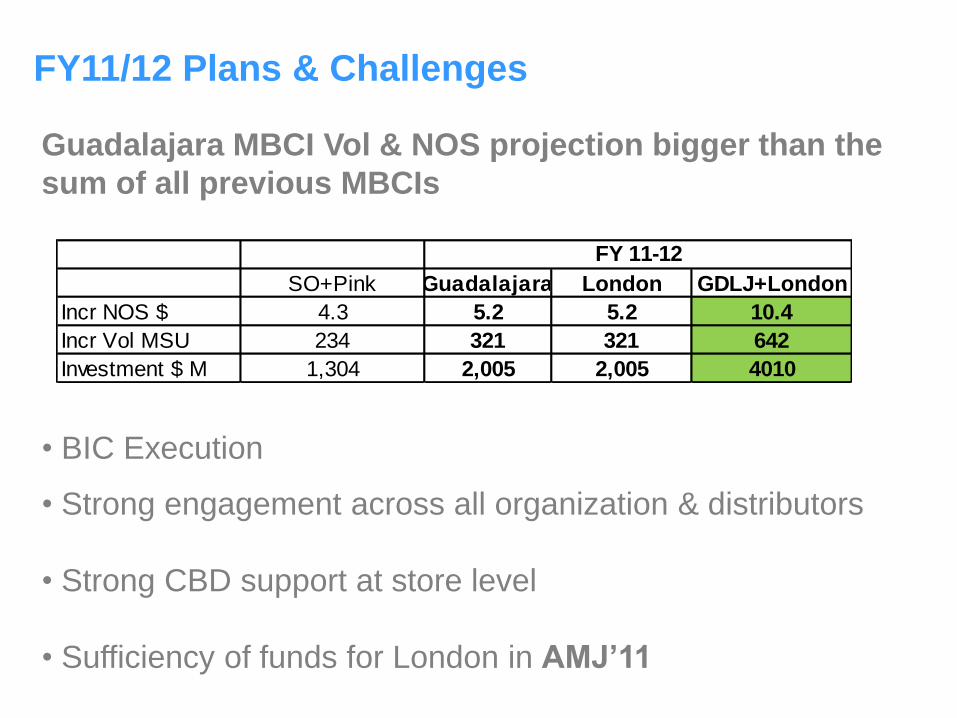

FY11/12 Plans & Challenges

Guadalajara MBCI Vol & NOS projection bigger than the

sum of all previous MBCIs

• BIC Execution

• Strong engagement across all organization & distributors

• Strong CBD support at store level

• Sufficiency of funds for London in AMJ’11

SO+Pink Guadalajara London GDLJ+London

Incr NOS $ 4.3 5.2 5.2 10.4

Incr Vol MSU 234 321 321 642

Investment $ M 1,304 2,005 2,005 4010

FY 11-12

Digital Marketing

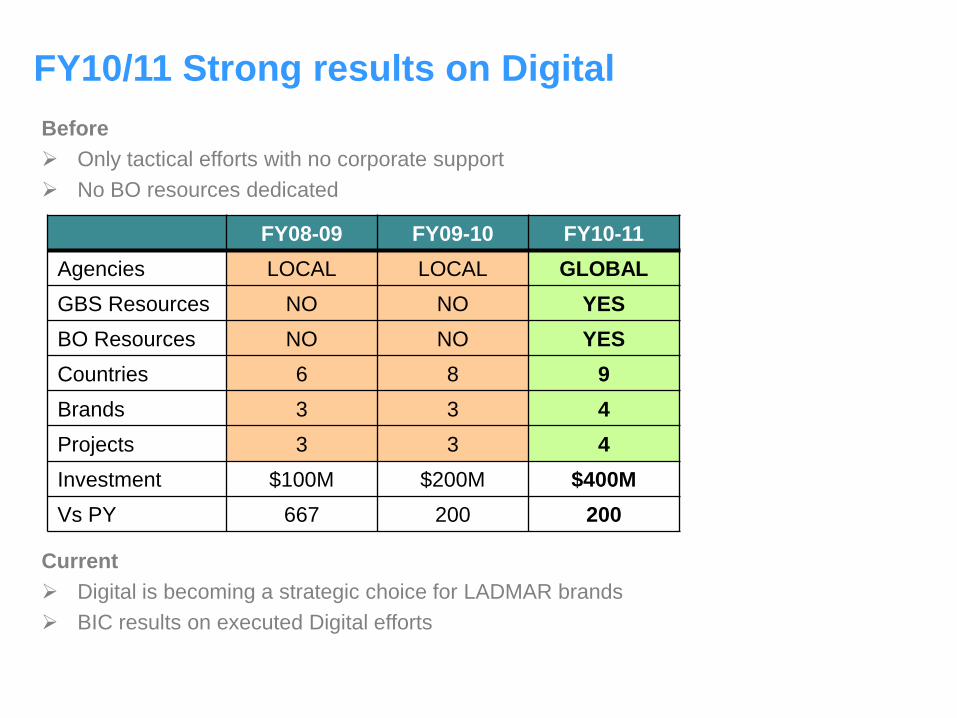

FY10/11 Strong results on Digital

FY08-09 FY09-10 FY10-11

Agencies LOCAL LOCAL GLOBAL

GBS Resources NO NO YES

BO Resources NO NO YES

Countries 6 8 9

Brands 3 3 4

Projects 3 3 4

Investment $100M $200M $400M

Vs PY 667 200 200

Current

Digital is becoming a strategic choice for LADMAR brands

BIC results on executed Digital efforts

Before

Only tactical efforts with no corporate support

No BO resources dedicated

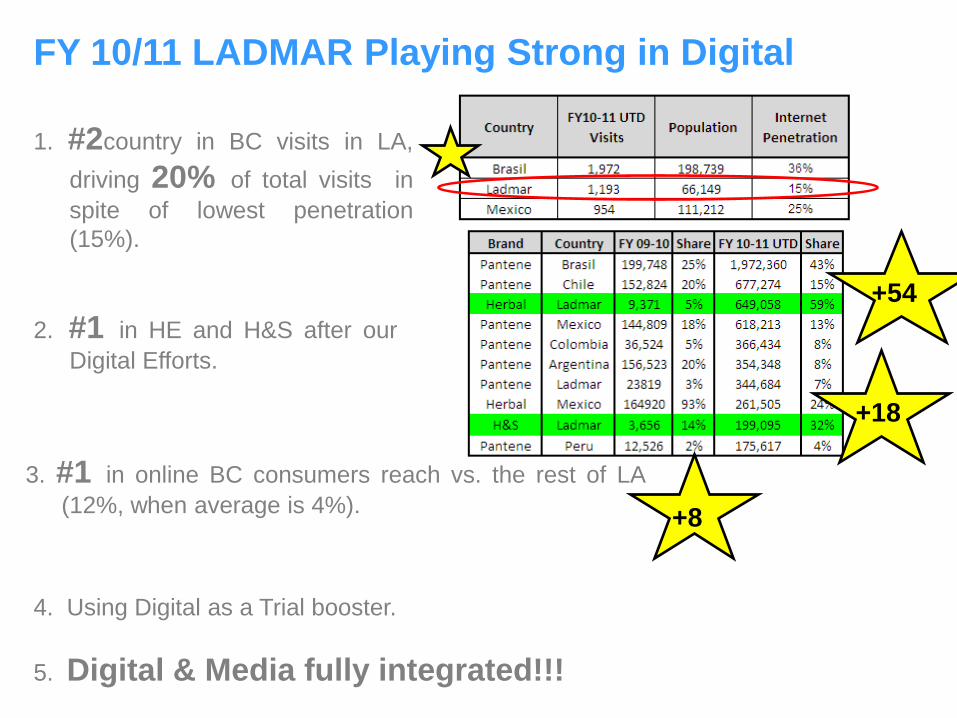

FY 10/11 LADMAR Playing Strong in Digital

4. Using Digital as a Trial booster.

5. Digital & Media fully integrated!!!

1. #2country in BC visits in LA,

driving 20% of total visits in

spite of lowest penetration

(15%).

2. #1 in HE and H&S after our

Digital Efforts.

+54

+18

+8

3. #1 in online BC consumers reach vs. the rest of LA

(12%, when average is 4%).

HERBAL ESSENCES “Look de Portada”

• #1 Site for HE in LA (representing 82% of LA visits!!.

• # 2 site in number of web visits for BC in LA (only below Brasil ).

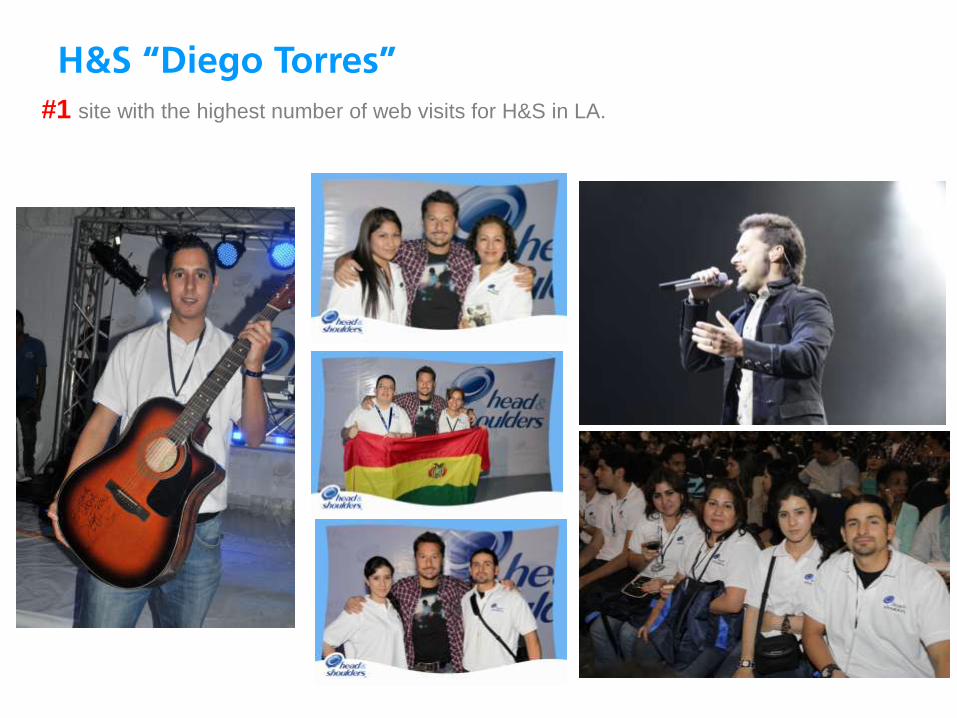

H&S “Diego Torres”

#1 site with the highest number of web visits for H&S in LA.

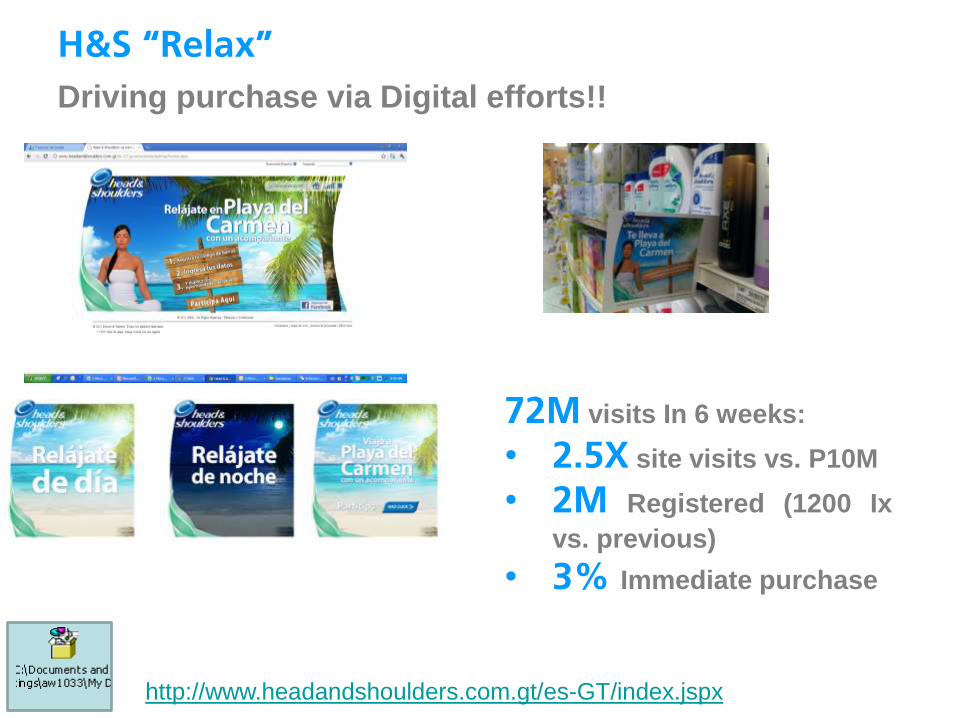

H&S “Relax”

Driving purchase via Digital efforts!!

http://www.headandshoulders.com.gt/es-GT/index.jspx

72M visits In 6 weeks:

• 2.5X site visits vs. P10M

• 2M Registered (1200 Ix

vs. previous)

• 3% Immediate purchase

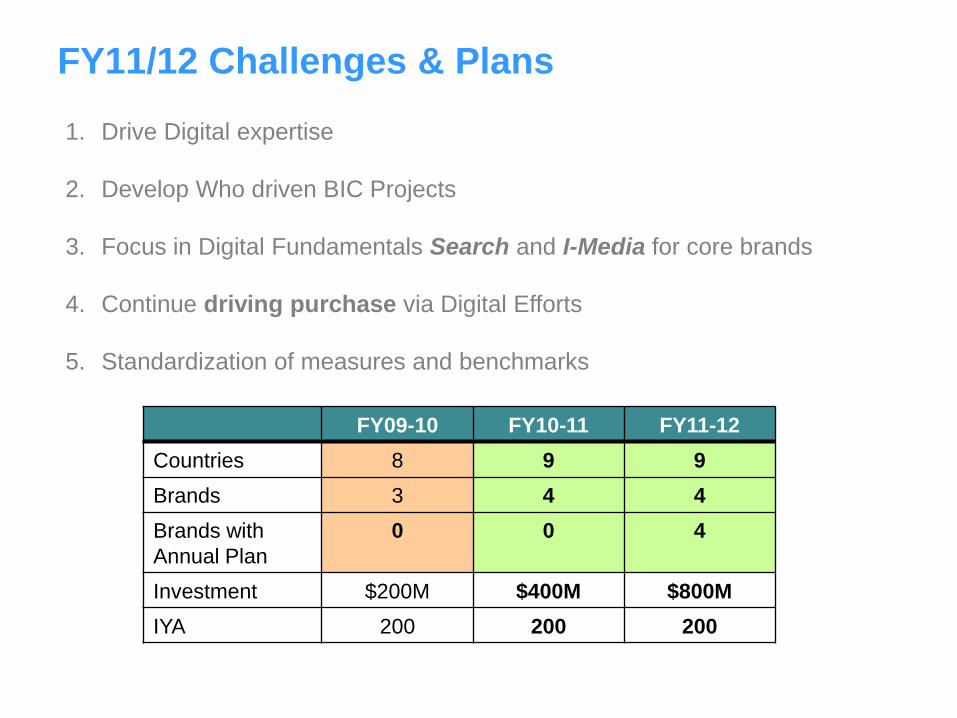

FY11/12 Challenges & Plans

1. Drive Digital expertise

2. Develop Who driven BIC Projects

3. Focus in Digital Fundamentals Search and I-Media for core brands

4. Continue driving purchase via Digital Efforts

5. Standardization of measures and benchmarks

FY09-10 FY10-11 FY11-12

Countries 8 9 9

Brands 3 4 4

Brands with

Annual Plan

0 0 4

Investment $200M $400M $800M

IYA 200 200 200

Media

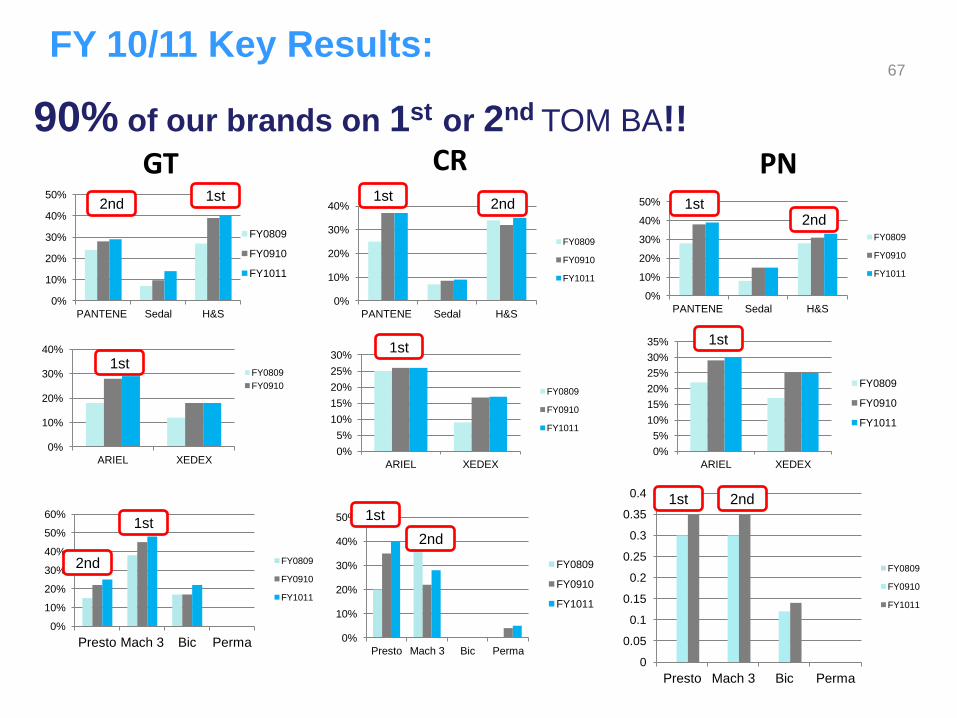

67

GT CR

0%

10%

20%

30%

40%

50%

PANTENE Sedal H&S

FY0809

FY0910

FY1011

0%

10%

20%

30%

40%

PANTENE Sedal H&S

FY0809

FY0910

FY1011

0%

10%

20%

30%

40%

50%

PANTENE Sedal H&S

FY0809

FY0910

FY1011

PN

0%

10%

20%

30%

40%

ARIEL XEDEX

FY0809

FY0910

0%

5%

10%

15%

20%

25%

30%

ARIEL XEDEX

FY0809

FY0910

FY1011

0%

5%

10%

15%

20%

25%

30%

35%

ARIEL XEDEX

FY0809

FY0910

FY1011

90% of our brands on 1st or 2nd TOM BA!!

0%

10%

20%

30%

40%

50%

60%

Presto Mach 3 Bic Perma

FY0809

FY0910

FY1011

0%

10%

20%

30%

40%

50%

Presto Mach 3 Bic Perma

FY0809

FY0910

FY1011

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Presto Mach 3 Bic Perma

FY0809

FY0910

FY1011

1st

1st1st

1st1st

1st

1st

1st

2nd

2nd

2nd2nd2nd

2nd

FY 10/11 Key Results:

1st

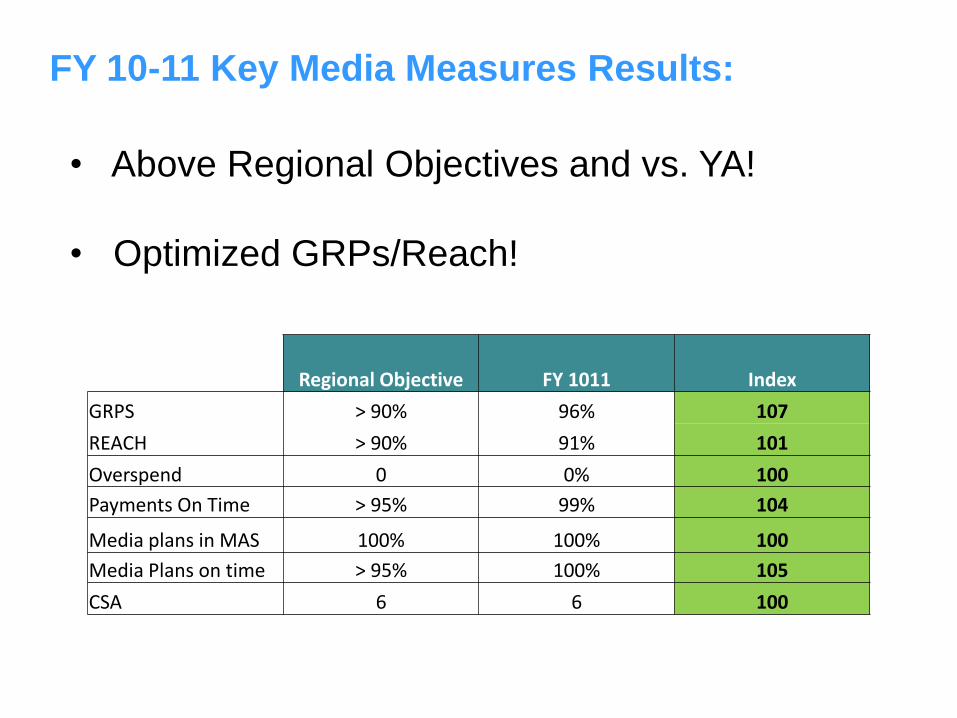

FY 10-11 Key Media Measures Results:

• Above Regional Objectives and vs. YA!

• Optimized GRPs/Reach!

Regional Objective FY 1011 Index

GRPS > 90% 96% 107

REACH > 90% 91% 101

Overspend 0 0% 100

Payments On Time > 95% 99% 104

Media plans in MAS 100% 100% 100

Media Plans on time > 95% 100% 105

CSA 6 6 100

69

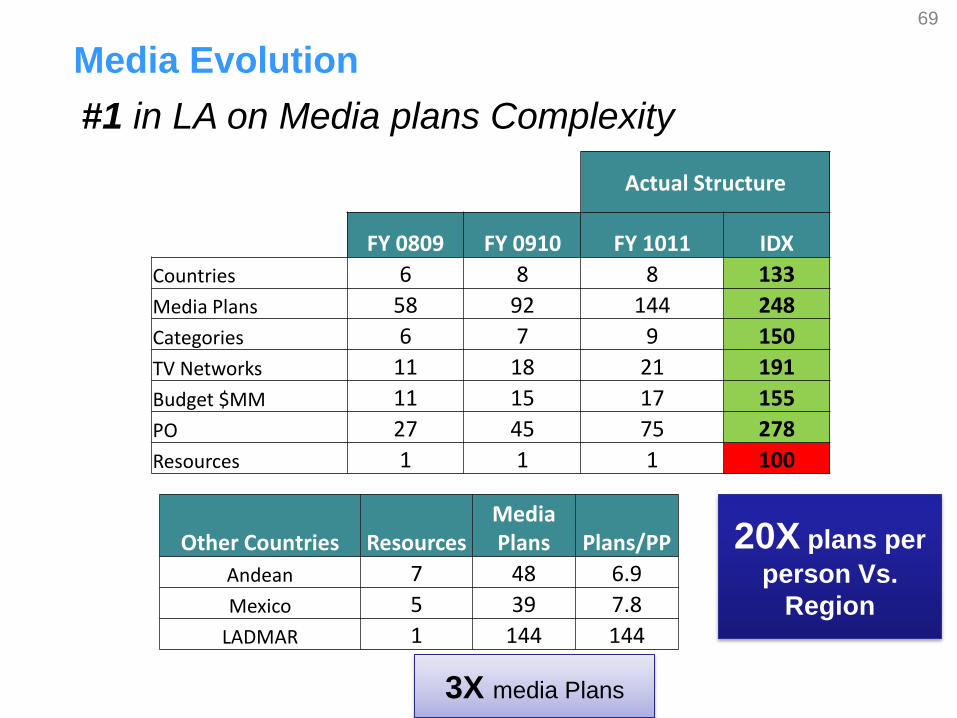

Media Evolution

#1 in LA on Media plans Complexity

Other Countries ResourcesMedia Plans Plans/PP

Andean 7 48 6.9

Mexico 5 39 7.8

LADMAR 1 144 144

Actual Structure

FY 0809 FY 0910 FY 1011 IDX

Countries 6 8 8 133

Media Plans 58 92 144 248

Categories 6 7 9 150

TV Networks 11 18 21 191

Budget $MM 11 15 17 155

PO 27 45 75 278

Resources 1 1 1 100

3X media Plans

20X plans per

person Vs.

Region

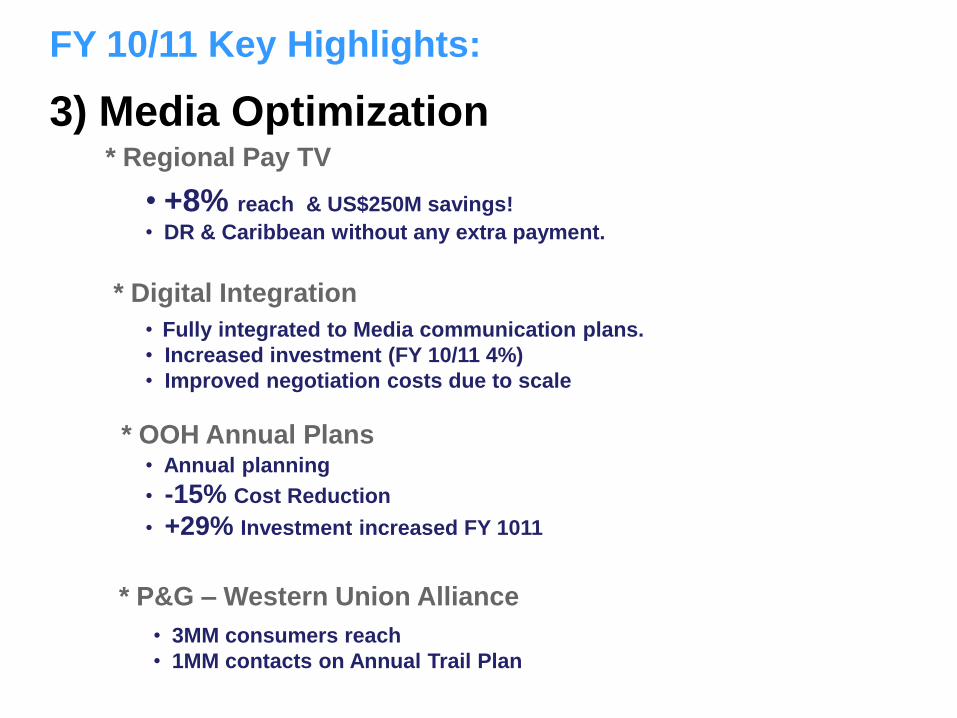

FY 10/11 Key Highlights:

1) Media Analysis capability to strengthen media plans:

• Media Reviews (Semestral/Annual)

• CIB Analysis (Quartely)

• Score Card (Bi-monthly)

2) LADMAR HU media model being reapplied across LA

next FY 11/12 (8w vs. 12W)!!

FY 10/11 Key Highlights:

3) Media Optimization* Regional Pay TV

• +8% reach & US$250M savings!

• DR & Caribbean without any extra payment.

* Digital Integration

* OOH Annual Plans• Annual planning

• -15% Cost Reduction

• +29% Investment increased FY 1011

* P&G – Western Union Alliance

• 3MM consumers reach

• 1MM contacts on Annual Trail Plan

• Fully integrated to Media communication plans.

• Increased investment (FY 10/11 4%)

• Improved negotiation costs due to scale

72

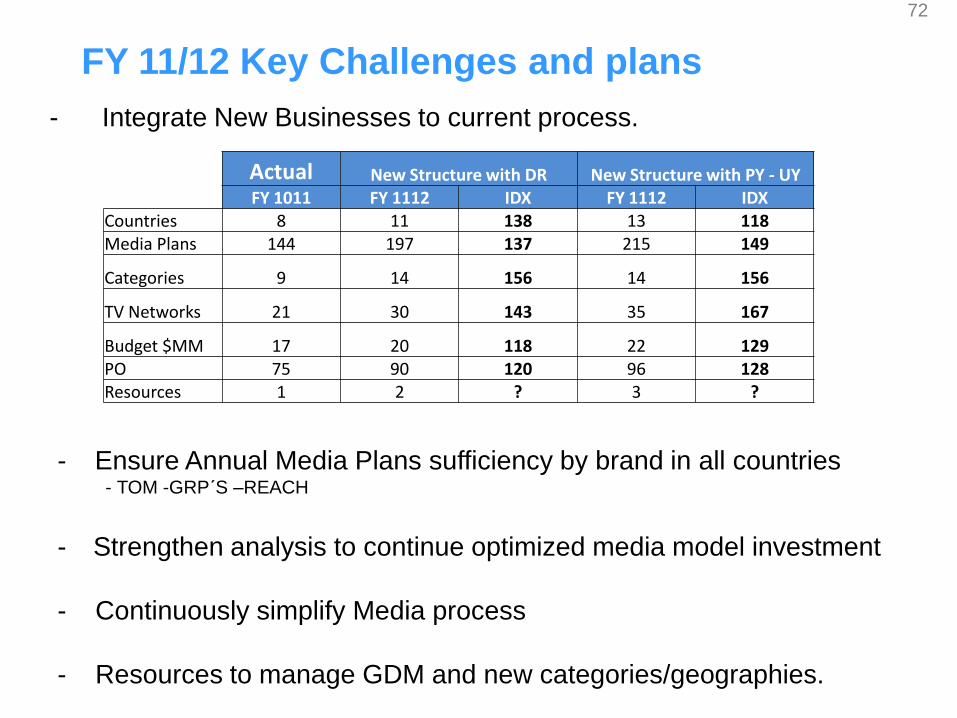

FY 11/12 Key Challenges and plans

- Integrate New Businesses to current process.

- Ensure Annual Media Plans sufficiency by brand in all countries- TOM -GRP´S –REACH

- Strengthen analysis to continue optimized media model investment

- Continuously simplify Media process

- Resources to manage GDM and new categories/geographies.

Actual New Structure with DR New Structure with PY - UYFY 1011 FY 1112 IDX FY 1112 IDX

Countries 8 11 138 13 118Media Plans 144 197 137 215 149

Categories 9 14 156 14 156

TV Networks 21 30 143 35 167

Budget $MM 17 20 118 22 129PO 75 90 120 96 128Resources 1 2 ? 3 ?

Influencer Marketing

74

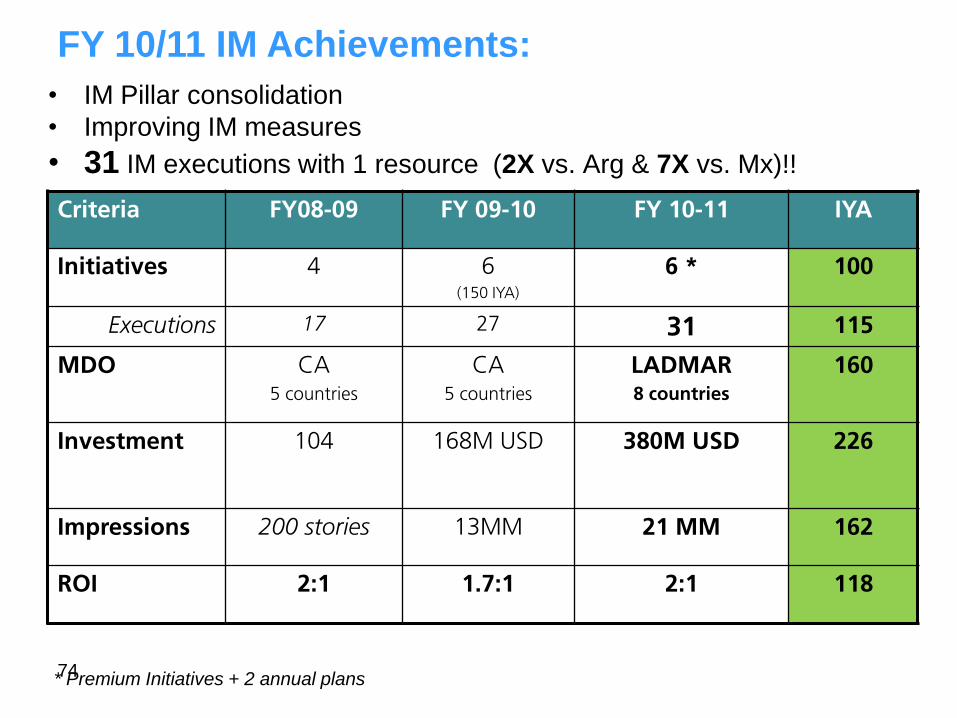

Criteria FY08-09 FY 09-10 FY 10-11 IYA

Initiatives 4 6

(150 IYA)

6 * 100

Executions 17 27 31 115

MDO CA

5 countries

CA

5 countries

LADMAR

8 countries

160

Investment 104 168M USD 380M USD 226

Impressions 200 stories 13MM 21 MM 162

ROI 2:1 1.7:1 2:1 118

* Premium Initiatives + 2 annual plans

• IM Pillar consolidation

• Improving IM measures

• 31 IM executions with 1 resource (2X vs. Arg & 7X vs. Mx)!!

FY 10/11 IM Achievements:

IM pillar consolidation as part of BO, consistently

improving our support!!!

• Shifting from tactical executions to strategic communication

planning:

- 2 annual plans for core brands (Pantene and H&S)

- Focus to win ESOV among key editors.

- Monitoring agency for CA to start tracking.

- Improving execution alignment with initiative launches.

• Strengthening relations with key media influencers.

- 1:1 Contacts with top local magazines for core countries

- Becoming a source of information for Hair Care

FY 10/11 Highlights

• FY 10/11 Pantene’s IM Annual Plan

• 95 PR stories (146 IYA)

41 prints, 16 radios spots, 13 TV mentions and 25 web articles

• 4MM printed impressions (141 IYA)

• US$137.5M of free publicity for 4.2:1 ROI (210 IX vs. objective / 2:1 target)

• FY 10/11 H&S IM Annual Plan

– 115 PR stories (107 IYA)

49 print, 21 radios spots, 14 TV mentions and 31 web articles

– 6.1MM impressions (221IX vs. obj. and 120 IYA)

– US$140M of free publicity (83% vs. obj / 1.7:1 in glide path to reach target 2:1)

FY 10/11 Annual Plans

* Results by Apr’11

Pantene’s Examples

H&S Examples

Leverage on Scale

(Beauty Care)

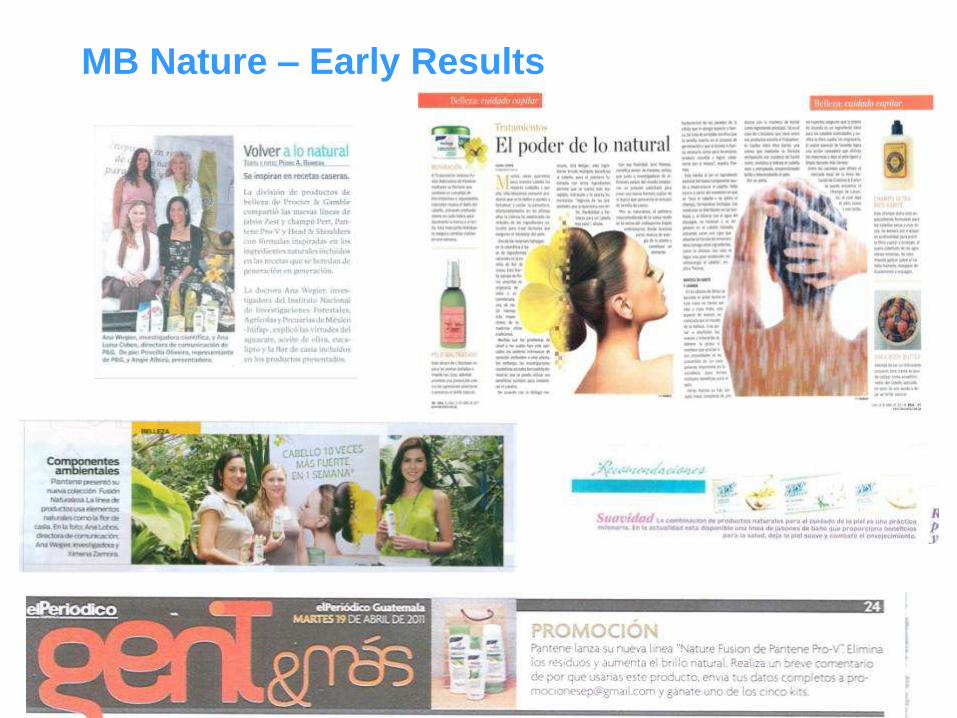

MB Nature – Early Results

• Continue developing capabilities in agencies for BIC

execution:

– Improve agencies structure to expand IM capacity due to lack

of internal resources.

– Build integrated communications to strengthen annual plans

and MBCI

• Expand long term relations with influencers

• Continue maximizing synergy between BO pillars to

make BIC ideas leveraging IM.

– Align RBU deliveries of toolkits to better meet SIMPL timings

FY 11/12 Key Challenges

• ANNUAL PLANS

Strengthen annual plans to improve share of voice among

key media:

- Hair Care: Pantene; Head & Shoulders (DR launch)

- Baby Care: Pampers

• Premium Initiatives

Oral-B Starship

• MBCI

Touch more consumer lives. Brand and corporate reputation

- OLYMPICS : GUADALAJARA, LONDON

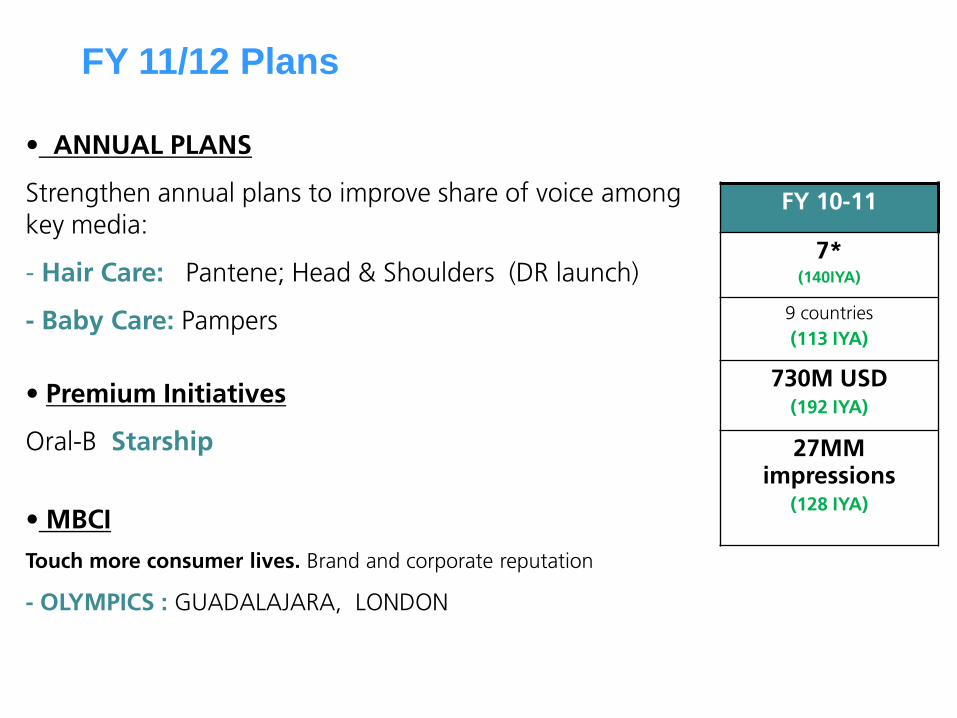

FY 10-11

7*

(140IYA)

9 countries

(113 IYA)

730M USD

(192 IYA)

27MM

impressions

(128 IYA)

FY 11/12 Plans

Suppliers Base Consolidation

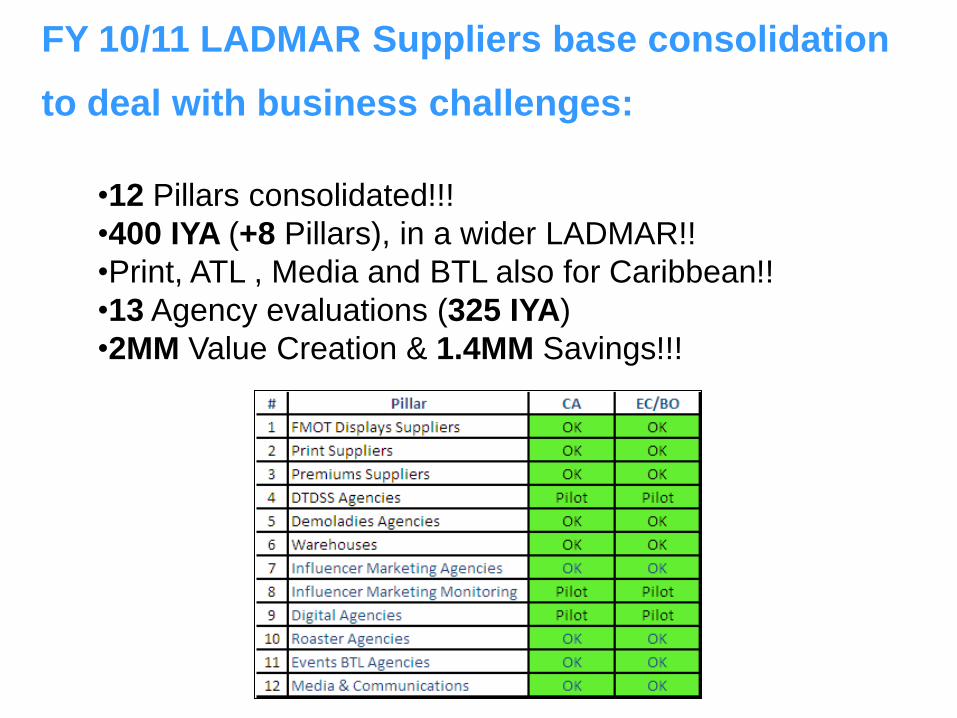

FY 10/11 LADMAR Suppliers base consolidation

to deal with business challenges:

•12 Pillars consolidated!!!

•400 IYA (+8 Pillars), in a wider LADMAR!!

•Print, ATL , Media and BTL also for Caribbean!!

•13 Agency evaluations (325 IYA)

•2MM Value Creation & 1.4MM Savings!!!

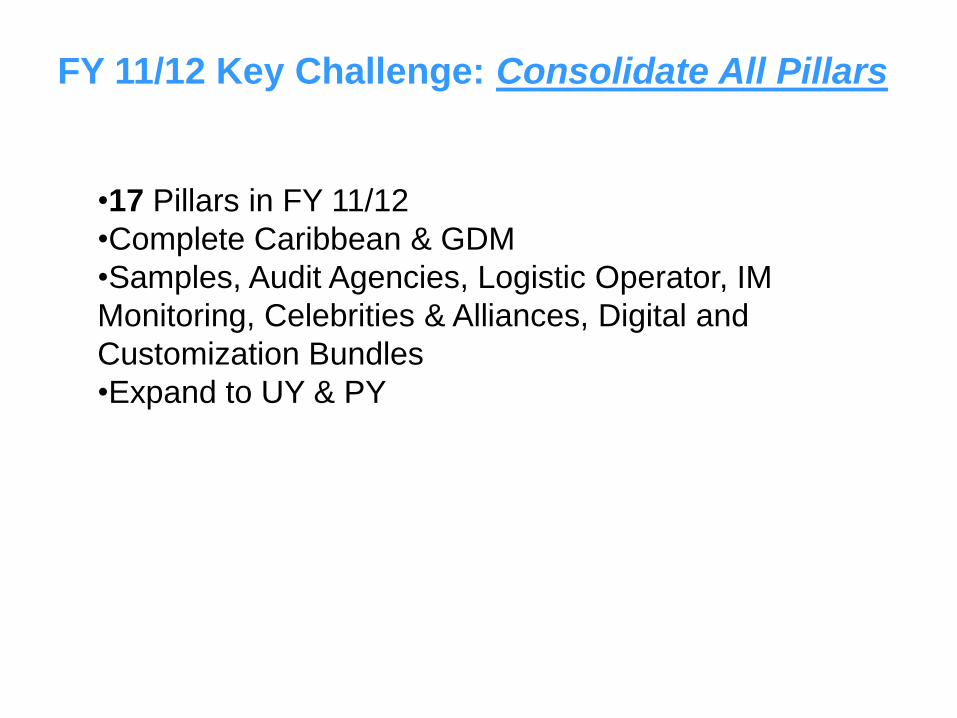

FY 11/12 Key Challenge: Consolidate All Pillars

•17 Pillars in FY 11/12

•Complete Caribbean & GDM

•Samples, Audit Agencies, Logistic Operator, IM

Monitoring, Celebrities & Alliances, Digital and

Customization Bundles

•Expand to UY & PY

BO Organization

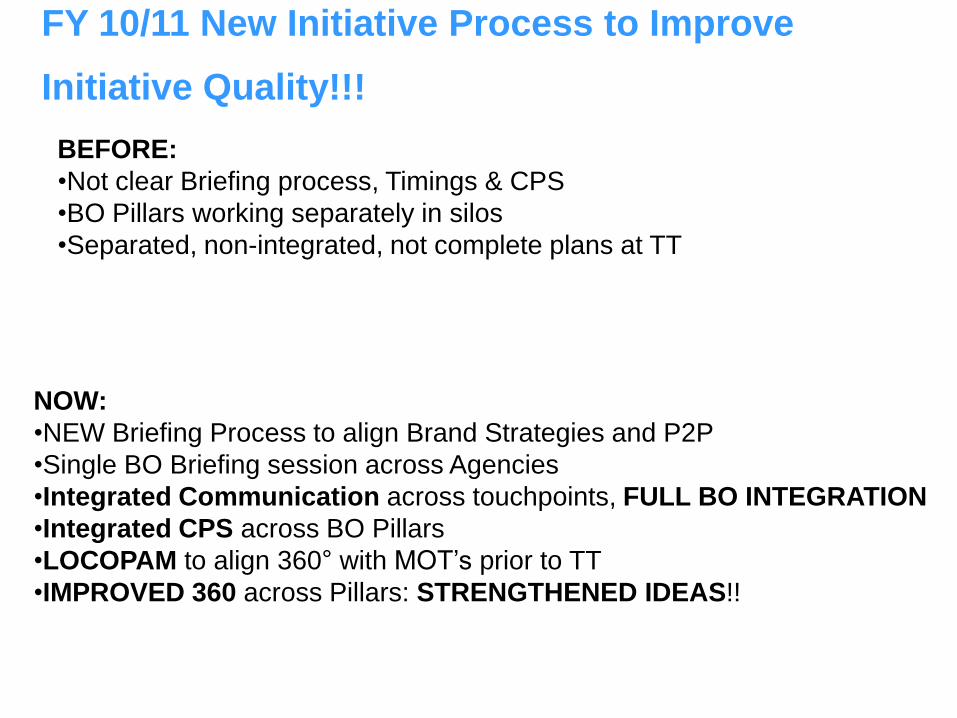

FY 10/11 New Initiative Process to Improve

Initiative Quality!!!

NOW:

•NEW Briefing Process to align Brand Strategies and P2P

•Single BO Briefing session across Agencies

•Integrated Communication across touchpoints, FULL BO INTEGRATION

•Integrated CPS across BO Pillars

•LOCOPAM to align 360° with MOT’s prior to TT

•IMPROVED 360 across Pillars: STRENGTHENED IDEAS!!

BEFORE:

•Not clear Briefing process, Timings & CPS

•BO Pillars working separately in silos

•Separated, non-integrated, not complete plans at TT

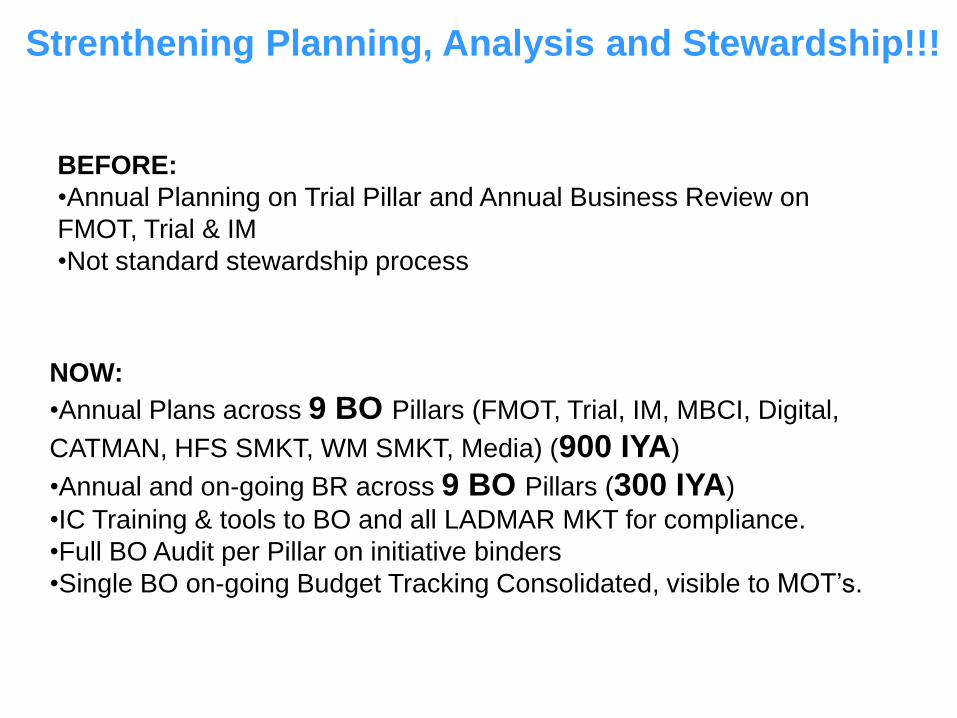

Strenthening Planning, Analysis and Stewardship!!!

NOW:

•Annual Plans across 9 BO Pillars (FMOT, Trial, IM, MBCI, Digital,

CATMAN, HFS SMKT, WM SMKT, Media) (900 IYA)

•Annual and on-going BR across 9 BO Pillars (300 IYA)

•IC Training & tools to BO and all LADMAR MKT for compliance.

•Full BO Audit per Pillar on initiative binders

•Single BO on-going Budget Tracking Consolidated, visible to MOT’s.

BEFORE:

•Annual Planning on Trial Pillar and Annual Business Review on

FMOT, Trial & IM

•Not standard stewardship process

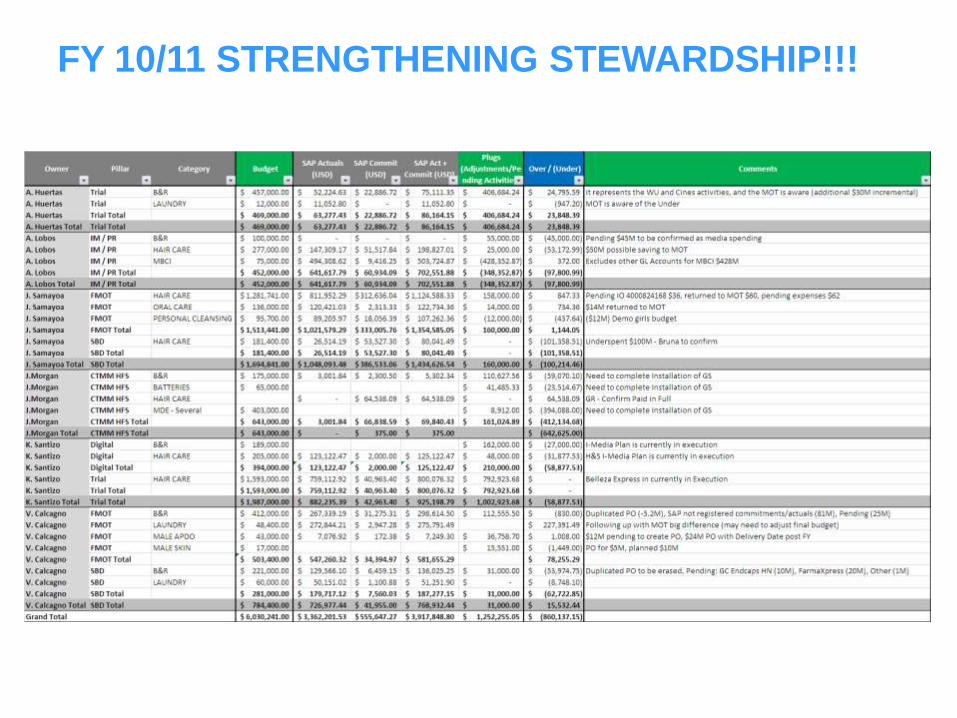

FY 10/11 STRENGTHENING STEWARDSHIP!!!

Key FY 10/11 Messages

• LADMAR is transforming FMOT into a competitive advantage

– SBD Turnaround (80X MIS & 30X GM) to win in Modern retail

– 118 IYA Golden store visibility and +5pp ND in HFS

– 400IX FMOT Execution & Capabilities Improvement

• Trial is a corporate priority

– Expanding to other categories besides HC

– 66% of NOS growing penetration (161 IYA) and 131 IYA in Trial!!

– Leveraging scale to maximize ROI

• Integrating and Consolidating new Pillars & Capabilities to our plans

– Influencer Marketing fully consolidated within BO, with Annual Planning

– Leading BIC results on Digital Marketing efforts

– Strengthening Media capabilities, analysis, digital and new geographies

– 130 IYA on W*Mart Shopper Marketing activities

• LADMAR Suppliers Base and Processes Consolidation

– 12 Pillars consolidated (400 IYA), 2MM value creation

– Strengthened 360 ideas

Brand OperationsCreating a Competitive Advantage