Embed Size (px)

DESCRIPTION

Â

Citation preview

bne May 2008bne February 2015 Special report I 73

Special Report: Capital Markets Survey 2014

2014 in CEE/CIS proves rich in risk, relatively poor in rewardGuy Norton in Zagreb

2014 proved to be an extremely test-ing one for issuers, lead managers and investors in the Central and

Eastern Europe/Commonwealth of Inde-pendent States (CEE/CIS) region, domi-nated as it was by the political-economic fallout from the bitter standoff between the US and Europe on the one side and Russia on the other side over the bloody events in Ukraine. Add in one-off fears about the general health of the global economy, the plummeting price of oil, uncertainty over the continued use of quantitative easing and renewed concerns over the fate of the embattled Greek economy, and the capital markets environment in 2014 ultimately proved to be as challenging as when the credit crunch and associated global economic slowdown hit home in 2008-2009.

As such issuers, lead managers and investors in CEE/CIS had to have their

wits about them if they were to be suc-cessful. Arguably a crystal ball-like abil-ity to read which way the political winds were blowing and having nerves of steel proved to be every bit as important as

having a strong credit story to tell when it came to capital markets success.

EquityAccording to information supplied by Dealogic, nowhere was that more true than in the equity markets, where the decision to press ahead with a land-

mark initial public offering (IPO) at a time of rising chaos in Ukraine paid off for the selling shareholders in Russian supermarket chain Lenta, which yield-ed the largest equity market issue of

the year from the region. On the basis that fortune favours the brave, book-runners Credit Suisse, JPMorgan, VTB Capital, Deutsche Bank and UBS were arguably vindicated in their decision to proceed with a deal, which although it just failed to achieve the landmark issue volume of $1bn, did neverthe-

“2014 ultimately proved to be as challenging as when the credit crunch and associated global economic slowdown hit home in 2008-2009”

74 I Central Europe bne May 2008 bne May 2008bne February 2015 bne February 201574 I Special report Special report I 75

and Sberbank both raised over $2bn apiece in the first half of the year, the combination of the deterioration in investor sentiment towards Russia and the imposition of sanctions on banks from the country in the second half of the year meant that 2014 once again proved to be a disappointment from a Russian perspective.

That ultimately proved to be the principal leitmotif in the capital markets in CEE/CIS in 2014, and the multi-bil-lion-dollar question this year is whether that theme will be reversed or not. Only time will tell.

less actually make it to market, which a great number of mooted Russian issues singularly failed to do.

Although the share issue that valued the company at $4.3bn was priced at the lower end of the Lenta's indicative price range of $9.5-11.5 per global depository receipt, the deal nevertheless reaped a decent return for the selling sharehold-ers – private equity groups TPG Capital and VTB Capital, alongside the Europe-an Bank for Reconstruction and Develop-ment (EBRD).

And although for most of the year the issuance environment for Russian equi-ty issuers proved to be less than ideal, Russian stock market operator Micex and Qiwi, the operator of Russia’s larg-est instant payment system, both man-aged to launch sizeable additional share offerings in 2014 following on from the success of their IPOs in 2013.

Elsewhere, new issue activity was fairly limited. However, Georgia’s TBC Bank capitalised on the good reputation of the Georgian banking sector to join Bank of Georgia on the London Stock Exchange with a deal worth $256mn. And after a number of botched privati-sation sales, Romanian power company Electrica’s IPO on the London and Bucharest bourses proved a highlight from a country which also spawned

follow-on issues by real estate devel-oper New Europe Property Investments and energy company Romgaz. Finally, towards the end of the year insurer AvivaSa Emeklilik ve Hayat provided some welcome diversification with a relatively rare IPO from Turkey.

Overall, though, 2014 proved to be a disappointing year on the equity front, principally due to the cancellation of

a large number of potential deals from Russia, and the prime issue this year will be whether those offerings can be resurrected if sentiment towards Russia improves.

DebtSentiment in the syndicated loan mar-ket in 2014 remained relatively robust for entities from CEE/CIS, with a wide range of borrowers from the region able to secure jumbo-sized transactions. Although with the honourable excep-tion of mobile operator VimpelCom, sizeable syndicated loans from Rus-sia were notable by their absence, but borrowers from other countries tasted success.

Sovereigns Bulgaria and Turkmenistan took advantage of improving sentiment towards them to launch landmark deals, while well-known oil and gas companies from the region, including Hungary’s MOL alongside Poland’s PKN Orlen and PGNiG, also secured sizeable transac-tions with deals that ultimately proved well timed given plummeting commod-ity prices at the end of the year. As did Turkey’s Star Rafineri, which offered syndicated lenders a relatively rare opportunity to grab a large slice of Turk-ish corporate risk.

On the sovereign Eurobond front, 2014 witnessed some notable successes, with

Slovenia taking advantage of improv-ing sentiment towards the country after it successfully averted a meltdown by securing close to $6bn in funding, while Poland, arguably the safe haven play of choice in the region, raised just under $7.5bn.

While other regular issuers such as Hun-gary, Turkey, Romania and Slovakia all tasted success, the return of Kazakhstan

to the international bond markets after more than a decade with a $2.5bn issue was undoubtedly one of the highlights of the year. The success of that offering was undoubtedly key to state oil and gas firm KazMunaiGas being able to issue the biggest corporate Eurobond of the year out of CEE/CIS, with the launch of a $1.5bn offering in the wake of the popular sovereign deal.

Although both Russian Railways with a brace of deals totalling over $1.4bn and Gazprom with a $1bn equivalent issue were able to access the interna-tional bond markets, Russian issuers as elsewhere in the capital markets were largely starved of market access in 2014. Whether that continues in 2015 – and with few signs of the Western sanctions being removed anytime soon, most likely it will – will have a major influence on corporate bond issuance volumes this year.

Other issues of note beyond a flurry of benchmark issues from Central Euro-

“The prime issue this year will be whether cancelled equity offerings can be resurrected if sentiment towards Russia improves”

"The return of Kazakhstan to the international bond markets after more than a decade with a $2.5bn issue was one of the highlights of the year"

And the winners are…

bne IntelliNews Best Bank for

M&A 2015

Goldman Sachs

bne IntelliNews Best Bank for Equity Capital Markets 2015

Deutsche Bank

bne IntelliNews Best Bank for

Debt Capital Markets (Sovereign/Local Authority) 2015

Citi

bne IntelliNews Best Bank for Debt

Capital Markets (Corporate) 2015

VTB Capital

bne IntelliNews Best Bank for

Debt Capital Markets (Financial Industrial

Group) 2015

Societe Generale Corporate & Investment Banking

pean energy companies from Poland, Slovakia and the Czech Republic included Turk Telekom offering up a rare opportunity for investors to access Turkish corporate Eurobond risk with a $1bn issue.

In terms of financial sector issuance, Turkish banks proved to be the pick of

a bunch, launching a series of well-received transactions from well-known and respected lenders such as Garanti Bankasi, which kicked off the bank funding party for the country’s lend-ers with a $750mn deal in April. While Russian banking titans Gazprombank

76 I Central Europe bne May 2008 bne May 2008bne February 2015 bne February 201576 I Special report Special report I 77

2013 v 2014 Central and Eastern Europe Syndicated All FIG DCM Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner Parents

SG Corporate & Investment Banking

Citi

Gazprombank

Bookrunner Parents

VTB Capital

JPMorgan

Gazprombank

Deal Value $

(Proceeds) (m)

2,167

1,611

1,577

Deal Value $

(Proceeds) (m)

4,729

2,153

1,956

No.

20

12

8

No.

32

19

10

%share

8.5

6.3

6.2

%share

15.4

7.0

6.4

2013 v 2014 Central and Eastern Europe Syndicated All Corporate DCM Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner Parents

VTB Capital

Citi

JPMorgan

Bookrunner Parents

Gazprombank

VTB Capital

Sberbank CIB

Deal Value $

(Proceeds) (m)

2,306

2,041

1,490

Deal Value $

(Proceeds) (m)

10,467

8,240

7,158

No.

11

14

9

No.

48

51

51

%share

11.2

10.0

7.3

%share

12.9

10.1

8.8

2013 v 2014 Central and Eastern Europe Syndicated All Sovereign and Local Authority DCM Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner Parents

Citi

JPMorgan

HSBC

Bookrunner Parents

Deutsche Bank

BNP Paribas

HSBC

Deal Value $

(Proceeds) (m)

6,801

6,595

4,699

Deal Value $

(Proceeds) (m)

8,478

4,617

4,015

No.

13

12

9

No.

16

9

8

%share

13.8

13.4

9.6

%share

17.2

9.3

8.1

2013 v 2014 Central and Eastern Europe Syndicated All Total DCM Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner Parents

Citi

JPMorgan

SG Corporate & Investment Banking

Bookrunner Parents

VTB Capital

Deutsche Bank

Gazprombank

Deal Value $

(Proceeds) (m)

10,552

9,432

6,499

Deal Value $

(Proceeds) (m)

17,661

15,317

14,252

No.

40

29

39

No.

121

53

73

%share

10.5

9.4

6.5

%share

10

8.7

8.1

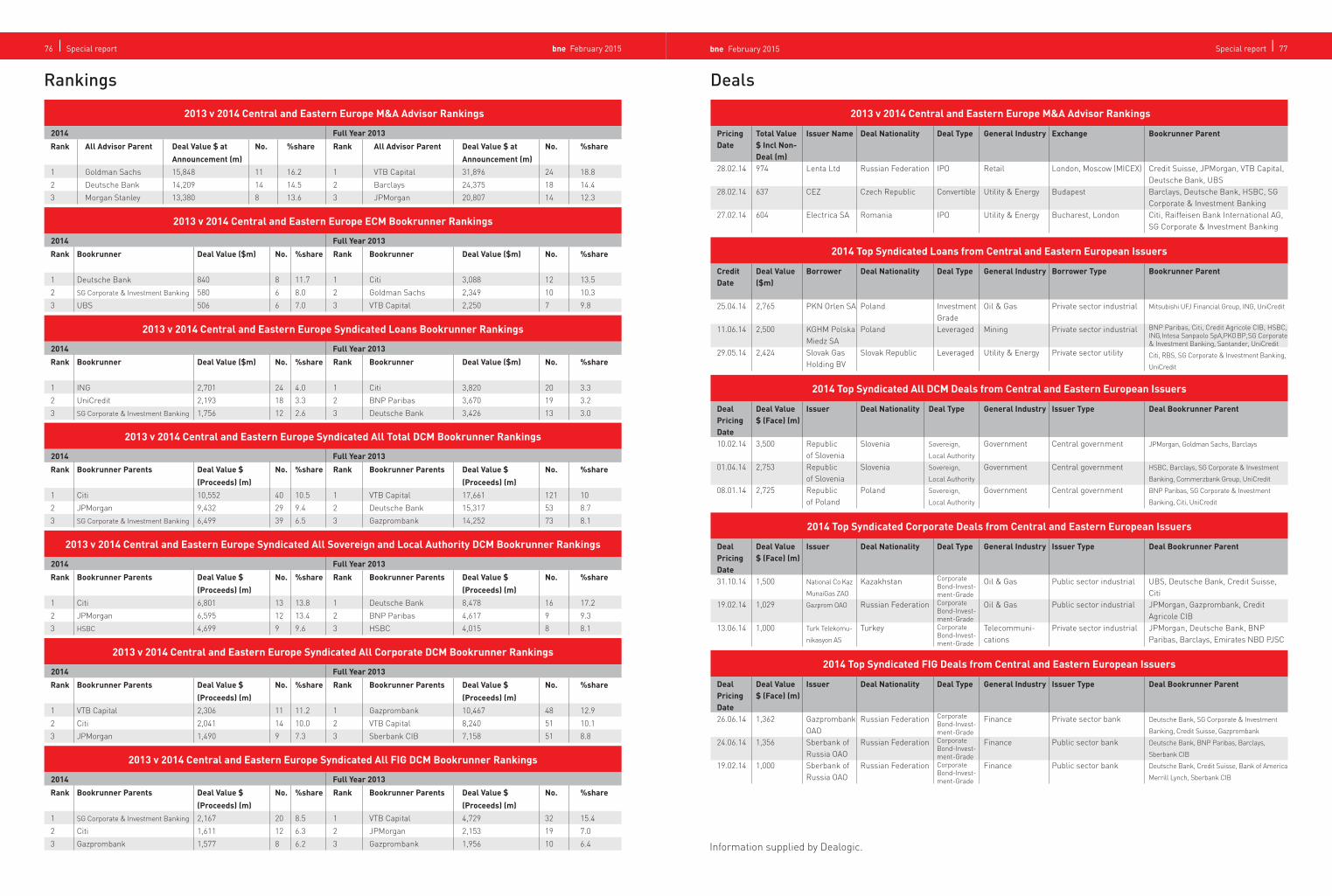

Rankings Deals

2013 v 2014 Central and Eastern Europe M&A Advisor Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

All Advisor Parent

Goldman Sachs

Deutsche Bank

Morgan Stanley

All Advisor Parent

VTB Capital

Barclays

JPMorgan

Deal Value $ at

Announcement (m)

15,848

14,209

13,380

Deal Value $ at

Announcement (m)

31,896

24,375

20,807

No.

11

14

8

No.

24

18

14

%share

16.2

14.5

13.6

%share

18.8

14.4

12.3

2013 v 2014 Central and Eastern Europe M&A Advisor Rankings

PricingDate

28.02.14

28.02.14

27.02.14

General Industry

Retail

Utility & Energy

Utility & Energy

Total Value $ Incl Non-Deal (m)974

637

604

Exchange

London, Moscow (MICEX)

Budapest

Bucharest, London

Issuer Name

Lenta Ltd

CEZ

Electrica SA

Bookrunner Parent

Credit Suisse, JPMorgan, VTB Capital, Deutsche Bank, UBSBarclays, Deutsche Bank, HSBC, SG Corporate & Investment BankingCiti, Raiffeisen Bank International AG, SG Corporate & Investment Banking

Deal Nationality

Russian Federation

Czech Republic

Romania

Deal Type

IPO

Convertible

IPO

2014 Top Syndicated Corporate Deals from Central and Eastern European Issuers

Deal Pricing Date31.10.14

19.02.14

13.06.14

General Industry

Oil & Gas

Oil & Gas

Telecommuni-cations

Deal Value $ (Face) (m)

1,500

1,029

1,000

Issuer Type

Public sector industrial

Public sector industrial

Private sector industrial

Issuer

National Co Kaz

MunaiGas ZAO

Gazprom OAO

Turk Telekomu-

nikasyon AS

Deal Bookrunner Parent

UBS, Deutsche Bank, Credit Suisse, CitiJPMorgan, Gazprombank, Credit Agricole CIBJPMorgan, Deutsche Bank, BNP Paribas, Barclays, Emirates NBD PJSC

Deal Nationality

Kazakhstan

Russian Federation

Turkey

Deal Type

Corporate Bond-Invest-ment-GradeCorporate Bond-Invest-ment-GradeCorporate Bond-Invest-ment-Grade

2014 Top Syndicated Loans from Central and Eastern European Issuers

Credit Date

25.04.14

11.06.14

29.05.14

General Industry

Oil & Gas

Mining

Utility & Energy

Deal Value ($m)

2,765

2,500

2,424

Borrower Type

Private sector industrial

Private sector industrial

Private sector utility

Borrower

PKN Orlen SA

KGHM Polska Miedz SASlovak Gas Holding BV

Bookrunner Parent

Mitsubishi UFJ Financial Group, ING, UniCredit

BNP Paribas, Citi, Credit Agricole CIB, HSBC, ING, Intesa Sanpaolo SpA, PKO BP, SG Corporate & Investment Banking, Santander, UniCredit

Citi, RBS, SG Corporate & Investment Banking,

UniCredit

Deal Nationality

Poland

Poland

Slovak Republic

Deal Type

Investment GradeLeveraged

Leveraged

2014 Top Syndicated FIG Deals from Central and Eastern European Issuers

Deal Pricing Date26.06.14

24.06.14

19.02.14

General Industry

Finance

Finance

Finance

Deal Value $ (Face) (m)

1,362

1,356

1,000

Issuer Type

Private sector bank

Public sector bank

Public sector bank

Issuer

Gazprombank OAOSberbank of Russia OAOSberbank of Russia OAO

Deal Bookrunner Parent

Deutsche Bank, SG Corporate & Investment

Banking, Credit Suisse, Gazprombank

Deutsche Bank, BNP Paribas, Barclays,

Sberbank CIB

Deutsche Bank, Credit Suisse, Bank of America

Merrill Lynch, Sberbank CIB

Deal Nationality

Russian Federation

Russian Federation

Russian Federation

Deal Type

Corporate Bond-Invest-ment-GradeCorporate Bond-Invest-ment-GradeCorporate Bond-Invest-ment-Grade

2014 Top Syndicated All DCM Deals from Central and Eastern European Issuers

Deal Pricing Date10.02.14

01.04.14

08.01.14

General Industry

Government

Government

Government

Deal Value $ (Face) (m)

3,500

2,753

2,725

Issuer Type

Central government

Central government

Central government

Issuer

Republic of SloveniaRepublic of SloveniaRepublic of Poland

Deal Bookrunner Parent

JPMorgan, Goldman Sachs, Barclays

HSBC, Barclays, SG Corporate & Investment

Banking, Commerzbank Group, UniCredit

BNP Paribas, SG Corporate & Investment

Banking, Citi, UniCredit

Deal Nationality

Slovenia

Slovenia

Poland

Deal Type

Sovereign,

Local Authority

Sovereign,

Local Authority

Sovereign,

Local Authority

2013 v 2014 Central and Eastern Europe ECM Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner

Deutsche Bank

SG Corporate & Investment Banking

UBS

Bookrunner

Citi

Goldman Sachs

VTB Capital

Deal Value ($m)

840

580

506

Deal Value ($m)

3,088

2,349

2,250

No.

8

6

6

No.

12

10

7

%share

11.7

8.0

7.0

%share

13.5

10.3

9.8

2013 v 2014 Central and Eastern Europe Syndicated Loans Bookrunner Rankings

2014 Full Year 2013

Rank

1

2

3

Rank

1

2

3

Bookrunner

ING

UniCredit

SG Corporate & Investment Banking

Bookrunner

Citi

BNP Paribas

Deutsche Bank

Deal Value ($m)

2,701

2,193

1,756

Deal Value ($m)

3,820

3,670

3,426

No.

24

18

12

No.

20

19

13

%share

4.0

3.3

2.6

%share

3.3

3.2

3.0

Information supplied by Dealogic.