Upload

pham-thao

View

41

Download

1

Tags:

Embed Size (px)

DESCRIPTION

BMI Vietnam auto report

Citation preview

Q2 2014www.businessmonitor.com

VIETNAMAUTOS REPORTINCLUDES 5-YEAR FORECASTS TO 2018

ISSN 1749-0286Published by:Business Monitor International

Vietnam Autos Report Q2 2014INCLUDES 5-YEAR FORECASTS TO 2018

Part of BMIs Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: January 2014

Business Monitor InternationalSenator House85 Queen Victoria StreetLondonEC4V 4ABUnited KingdomTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.businessmonitor.com

2014 Business Monitor InternationalAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind asto the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View ............................................................................................................... 7

SWOT .................................................................................................................................... 9SWOT ..................................................................................................................................................... 9Political ................................................................................................................................................. 10Economic ............................................................................................................................................... 11Business Environment .............................................................................................................................. 12

Industry Forecast .............................................................................................................. 13Table: Vietnam Autos Production, 2011-2018 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Table: Vietnam Autos Sales, 2011-2018 (VAMA Members) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Table: Vietnam Autos Trade, 2011-2018 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Table: Vietnam - 2014 Import Tax Regime . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Industry Forecast Passenger Cars ............................................................................................................ 23Industry Forecast Commercial Vehicles .................................................................................................... 24

Table: Top Five Companies By CV Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Industry Forecast Suppliers .................................................................................................................... 24

Macroeconomic Forecasts ............................................................................................... 30Table: Vietnam - Economic Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Industry Risk Reward Ratings .......................................................................................... 34Asia-Pacific Risk/Reward Ratings ............................................................................................................ 34

Table: Asia-Pacific Autos Risk/Reward Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Company Profile ................................................................................................................ 38Company Monitor .................................................................................................................................... 38GM Vietnam ........................................................................................................................................... 41Mercedes-Benz Vietnam ............................................................................................................................ 42Automotive Asia Ltd ................................................................................................................................. 44

Regional Overview ............................................................................................................ 45Table: Vehicle Sales 2013 (CBUS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Global Industry Overview .................................................................................................. 50Table: Passenger Car Sales November 2013 (CBUs) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Europe On Road To Recovery .................................................................................................................. 50Tax Hike Skews Japan's Outlook; US Hits Sweet 16 ...................................................................................... 52China Is BRIC Bright Spot ....................................................................................................................... 54

Demographic Forecast ..................................................................................................... 57Demographic Outlook .............................................................................................................................. 57

Table: Vietnam's Population By Age Group, 1990-2020 ('000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Vietnam Autos Report Q2 2014

Business Monitor International Page 4

Table: Vietnam's Population By Age Group, 1990-2020 (% of total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59Table: Vietnam's Key Population Ratios, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Table: Vietnam's Rural And Urban Population, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Methodology ...................................................................................................................... 61Industry Forecasts .................................................................................................................................. 61Sector-Specific Methodology .................................................................................................................... 62Sources ................................................................................................................................................ 62Risk/Reward Ratings Methodology ............................................................................................................ 63

Table: Automotive Risk/Reward Ratings Indicators And Weighting Of Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Vietnam Autos Report Q2 2014

Business Monitor International Page 5

BMI Industry View

According to the Vietnam Automobile Manufacturers Association (VAMA), vehicle sales of its membersgrew 20.0% in 2013, to 96,688 units. The strong showing in 2013 was largely attributed to the rebound in

the automotive sector, which was ravaged by the recession that hit the country in 2012.

We remain bullish on the Vietnamese auto market, however, and forecast vehicle sales to grow 10.0% in

2014. While this is below 2013's growth rate, it is because vehicle sales have normalised and the higher

base effects of 2013 will make it harder for them to continue growing at such a rapid clip.

Our bullish outlook on the sector chimes with our Country Risk team's optimistic view on Vietnam's

economy. As the government takes steps to privatise the country's state-owned enterprises (SOEs), we see itas a harbinger for more free market reforms in the coming years, which will undoubtedly provide a boost to

economic growth (see 'Privatisation Of SOEs Highly Positive For The Economy', January 8). BMI forecastsVietnam's GDP to grow 5.9% in 2014 and 6.4% in 2015.

Besides the ongoing privatisation drive, another factor supporting auto sales is our outlook for stable

interest rates in 2014. Our Country Risk team forecasts the State Bank of Vietnam's benchmark refinancing

rate to remain on hold at 7.00% throughout 2014 (see 'New Credit Growth Target Suggests Monetary PolicyTo Be Kept On', December 30 2013). The resultant stability in consumer financing rates will continue tomake it attractive for buyers to take on financing for their vehicle purchases.

We expect the outperformance of passenger car sales to continue in 2014, aided by the availability of

affordable car loans. That said, we forecast commercial vehicle (CV) sales, which were impacted by weakdemand from businesses in 2013, to grow 8.0% in 2014, as Vietnam's ongoing banking sector reforms and

SOE restructuring begin to bear fruit.

We have also upgraded our 2015 vehicle sales growth forecast from 7.2% to 8.6% due to the gradual

abolishment of import tariffs on vehicles imported from other ASEAN countries as part of the region's

Trade in Goods Agreement. As duties are slowly reduced, imported cars, which were previously priced out

of the local market due to high taxes, will now become more affordable for the average Vietnamese

consumer. This will then result in sustained sales growth for the imported car segment.

Despite our more optimistic outlook for vehicle production in the coming years, we warn that a lot needs to

be done in terms of policy changes to make Vietnam an attractive market for autos-related investment in the

Vietnam Autos Report Q2 2014

Business Monitor International Page 7

Asia-Pacific region. Although the government has tried to increase domestic production in the industry, in

particular by raising import tariffs on vehicles, there has been little in the way of rewards for companies

which have chosen to invest. This is reflected in the 'rewards' section of BMI's industry Risk/Reward

ratings for the autos sector in Asia, where Vietnam scores far below its neighbours in terms of the industry

rewards on offer.

Vietnam Autos Report Q2 2014

Business Monitor International Page 8

SWOT

SWOT

Vietnam Autos Industry SWOT

Strengths Low rates of vehicle ownership, together with Vietnam's large population, provide an

opportunity for strong vehicle sales growth over the long term.

Low manufacturing and labour costs.

Stable interest rates will continue to make it attractive for consumers to utilise credit

to purchase cars.

The cut in car registration fees is likely to see sustained growth in passenger car

sales.

Weaknesses Lack of production incentives mean that the automotive sector lags other sectors in

attracting FDI.

Domestic supplier industry is not well-developed, which results in automakers having

to pay high import tariffs on imported parts.

The still underdeveloped road network in the country means that two-wheelers remain

a more sensible option for consumers.

Opportunities The market shows diversity, with long-term growth likely for both the premium and

small car segments.

The annual reduction of tariffs on CBU imports from other ASEAN nations in the next

few years will give existing automakers as well as new entrants a chance to increase

their domestic sales through imports.

Threats The eventual elimination of import tariffs in the Vietnamese auto market by 2018 could

prevent the development of a vibrant local vehicle industry.

Vietnam Autos Report Q2 2014

Business Monitor International Page 9

Political

SWOT Analysis

Strengths The Communist Party of Vietnam remains committed to market-oriented reforms and

we do not expect major shifts in policy direction over the next five years. The one-

party system is generally conducive to short-term political stability.

Relations with the US have witnessed a marked improvement, and Washington sees

Hanoi as a potential geopolitical ally in South East Asia.

Weaknesses Corruption among government officials poses a major threat to the legitimacy of the

ruling Communist Party.

There is increasing (albeit still limited) public dissatisfaction with the leadership's tight

control over political dissent.

Opportunities The government recognises the threat corruption poses to its legitimacy, and has

acted to clamp down on graft among party officials.

Vietnam has allowed legislators to become more vocal in criticising government

policies. This is opening up opportunities for more checks and balances within the

one-party system.

Threats Macroeconomic instabilities continue to weigh on public acceptance of the one-party

system, and street demonstrations to protest economic conditions could develop into

a full-on challenge of undemocractic rule.

Although strong domestic control will ensure little change to Vietnam's political scene

in the next few years, over the longer term, the one-party-state will probably be

unsustainable.

Relations with China have deteriorated over recent years due to Beijing's more

assertive stance over disputed islands in the South China Sea and domestic criticism

of a large Chinese investment into a bauxite mining project in the central highlands,

which could potentially cause wide-scale environmental damage.

Vietnam Autos Report Q2 2014

Business Monitor International Page 10

Economic

SWOT Analysis

Strengths Vietnam has been one of the fastest-growing economies in Asia in recent years, with

GDP growth averaging 7.1% annually between 2000 and 2012.

The economic boom has lifted many Vietnamese out of poverty, with the official

poverty rate in the country falling from 58% in 1993 to 20.7% in 2012.

Weaknesses Vietnam still suffers from substantial trade and fiscal deficits, leaving the economy

vulnerable to global economic uncertainties. The fiscal deficit is dominated by

substantial spending on social subsidies that could be difficult to withdraw.

The heavily-managed and weak currency reduces incentives to improve quality of

exports, and also keeps import costs high, contributing to inflationary pressures.

Opportunities WTO membership and the upcoming ASEAN AEC in 2015 should give Vietnam

greater access to both foreign markets and capital, while making Vietnamese

enterprises stronger through increased competition.

The government will in spite of the current macroeconomic woes, continue to move

forward with market reforms, including privatisation of state-owned enterprises, and

liberalising the banking sector.

Urbanisation will continue to be a long-term growth driver. The UN forecasts the

urban population rising from 29% of the population to more than 50% by the early

2040s.

Threats Inflation and deficit concerns have caused some investors to re-assess their hitherto

upbeat view of Vietnam. If the government focuses too much on stimulating growth

and fails to root out inflationary pressure, it risks prolonging macroeconomic

instability, which could lead to a potential crisis.

Prolonged macroeconomic instability could prompt the authorities to put reforms on

hold as they struggle to stabilise the economy.

Vietnam Autos Report Q2 2014

Business Monitor International Page 11

Business Environment

SWOT Analysis

Strengths Vietnam has a large, skilled and low-cost workforce, which has made the country

attractive to foreign investors.

Vietnam's location - its proximity to China and South East Asia, and its good sea links

- makes it a good base for foreign companies to export to the rest of Asia, and

beyond.

Weaknesses Vietnam's infrastructure is still weak. Roads, railways and ports are inadequate to

cope with the country's economic growth and links with the outside world.

Vietnam remains one of the world's most corrupt countries. According to

Transparency International's 2012 Corruption Perceptions Index, Vietnam ranks 123

out of 176 countries.

Opportunities Vietnam is increasingly attracting investment from key Asian economies, such as

Japan, South Korea and Taiwan. This offers the possibility of the transfer of high-tech

skills and know-how.

Vietnam is pressing ahead with the privatisation of state-owned enterprises and the

liberalisation of the banking sector. This should offer foreign investors new entry

points.

Threats Ongoing trade disputes with the US, and the general threat of American

protectionism, which will remain a concern.

Labour unrest remains a lingering threat. A failure by the authorities to boost skills

levels could leave Vietnam a second-rate economy for an indefinite period.

Vietnam Autos Report Q2 2014

Business Monitor International Page 12

Industry Forecast

Production

Vietnam's autos industry is still in its infancy as producers typically import completely knocked-down kits

(CKDs), which are assembled and sold domestically. The domestic parts sector is small at present, althoughthe government is making it a priority. Given rapid economic growth in the region, there is significant

development potential for the industry, especially as less than 4% of the population owns a car.

Table: Vietnam Autos Production, 2011-2018

2011 2012 2013e 2014f 2015f 2016f 2017f 2018f

Total Production 31,181 40,470 42,898 46,808 51,498 55,351 59,691 64,584

Passenger Car Production 29,904 38,900 41,234 45,028 49,575 53,293 57,468 62,161

Commercial Vehicle Production 1,277 1,570 1,664 1,781 1,923 2,058 2,222 2,422

e/f= BMI estimate/forecast. Source: BMI, OICA

Production Will Grow But Importing Still More Attractive

According to Gaikindo, auto production in Vietnam rose 27.4% y-o-y in November 2013 (latest available),to 10,003 units, bringing output for the first 11 months of 2013 to 83,656 units, an increase of 24.5% y-o-y.

This was the first time since November 2010 that monthly production crossed the 10,000 units mark.

However, auto production has been in a downtrend since late 2010. While the contraction in vehicle

production mirrors the fall in domestic sales since 2011, caused by the economic recession in that period,

there are also broader structural issues which have prevented an expansion in domestic auto production. The

lack of a coherent auto policy, weak government incentives, and, poor supplier presence, have all combined

to make local manufacturing an unattractive proposition for automakers (see 'Sales Soar, But ProductionStill Underperforming, September 23 2013).

Vietnam Autos Report Q2 2014

Business Monitor International Page 13

Rising, But Not Up To The Mark

Vietnam - Domestic Auto Production, Units (LHS); % Chg y-o-y (RHS)

Source: BMI, Gaikindo

That said, the uptick in monthly production in the past few months does indicate to us that output would

pick up in 2014. As previously highlighted, we believe the strong momentum in domestic sales will

continue in 2014 on the back of the resurgence in the Vietnamese economy, as the government moves to

privatise the country's state-owned enterprises and embark on a series of free market reforms in the coming

years (see 'Sales To Build On Solid 2013', January 16). This, will then, result in local carmakers raisingtheir output to meet higher demand. Against this backdrop, we have upgraded our 2014 and 2015

production growth forecast to 9.1% and 10.0% respectively.

However, due to a lack of attractive incentives to produce locally, we only see automakers with a strong

presence in the domestic market, such as Toyota Motor and Ford Motor, increasing their output. In our

opinion, it is unlikely that new entrants will set up production bases in the country to tap rising car demand,

which still remains low in absolute numbers.

We also see the gradual abolishment of import tariffs on vehicles imported from other ASEAN countries as

a key threat to the Vietnamese auto sector (see 'Will Abolishing Import Duties Decimate Local

Vietnam Autos Report Q2 2014

Business Monitor International Page 14

Manufacturing', January 9). As tariffs are lowered, potential entrants will likely prefer to import completelybuilt units into the country instead of establishing greenfield production facilities. Indeed, our trade balance

forecast shows net imports rising from 2014 to 2018 as sales growth of imported vehicles accelerates.

In order to prevent the worst case scenario of the decimation of local manufacturing as import tariffs are

eventually abolished, the Vietnamese government needs to put in place a strong and coherent auto sector

policy, and ensure greater domestic supplier presence, which will then incentivise more automakers to

invest in local production.

Supplier Segment Shares The Blame

An underdeveloped supplier segment has been an underlying problem in attracting vehicle production

investment for many years. According to the CCI's report, the parts produced locally are very simple and

the industry's technology as a whole is restricted to welding, assembly, painting and testing.

This means that while local content requirements have previously been set in order to necessitate

investment, they have rarely been met. For vehicles with less than nine seats, the average rate of local

content is just 15%, and for vehicles with 10 seats or more the level is 30-40%, vis-a-vis the 60% target.

Although the government has tried to increase domestic production in the industry before, particularly by

raising import tariffs on vehicles, there has been little in the way of rewards for companies which have

chosen to invest. This is reflected in the 'rewards' section of BMI's industry Risk/Reward Ratings for the

autos sector in Asia, where Vietnam scores far below its neighbours in terms of the industry rewards on

offer.

The industry's shortcomings will also have a financial impact. The autos trade deficit has been a concern for

a number of years, prompting increases in import tariffs and regulations to weed out smaller unauthorised

importers. However, tariffs will need to be lowered again in accordance with ASEAN trade obligations and

with the sector not yet in a position to compete with its more productive neighbours, the CCI report expects

Vietnam to be spending US$12bn per year on vehicle imports until 2025.

What Does The Government Need To Do?

To spur domestic production, we believe the government needs to do the following:

Vietnam Autos Report Q2 2014

Business Monitor International Page 15

Simplifying Tax Policies: There are currently nine different taxes on vehicles, with taxes accounting for

some 60% of the value of a new car in Vietnam. These range from registration fees to an environmental

protection tax imposed on imported cars in Vietnam. BMI has previously highlighted that increased import

taxes are making imported cars unaffordable (see our online service, August 9 2012, 'Increased ChargesDampen Demand'). We believe that the number of taxes needs to be reduced so as to make the purchase of acar more affordable and less confusing for businesses and consumers.

The recent measures to cut taxes, is a step in the right direction for the government's 2020 auto development

plan.

Investment In Infrastructure: While the Ministry of Industry and Trade (MOIT) has been making effortsto develop the automobile industry, the Ministry of Transport (MOT) and the Ministry of Finance (MOF)are concerned about road congestion and have therefore imposed tariffs on imported cars. Our Infrastructure

team believes that Vietnam needs greater investment in roads as currently many of its roads are just wideenough for two-wheelers.

Although the government needs to make a concerted effort to improve Vietnam's road infrastructure to allay

the concerns of MOT and MOF and therefore enable all three ministries to work harmoniously to develop

Vietnam's automobile sector, we believe it would be a challenge in the short term due to the lack of credit as

well as the banking sector's woes. However, it would be easier in the long term with the reforms the

banking sector is currently undergoing, as well as the possibility of getting financing from abroad.

Attractive Investment Policies: We believe that the Vietnamese government needs to offer incentives such

as tax breaks to attract more foreign direct investment (FDI) into the country. With investments from globalautomakers in the country, there can be knowledge-sharing as well as a transfer of technology with the local

players. Currently, most of the auto production in the country is just assembly of cars and that is insufficientfor Vietnam to develop a competency in this sector. With FDI, Vietnam would have the chance to move up

the value chain of production.

While the fledging auto manufacturing industry takes time to gain traction, we believe the component

industry could see more investments in the sector. Vietnam has one of the lowest labour costs in the region,

making it attractive for component manufacturers to base their production facilities in. While they may be

unable to sell many of their products locally due to the lack of auto production, exporting these components

from Vietnam is a viable alternative.

Vietnam Autos Report Q2 2014

Business Monitor International Page 16

South Korean manufacturer Hyundai Motor has already committed to an agreement with local company

Truong Hai Automobile, which will act as the company's exclusive distributor in the country. Hyundai

will also set up an engine production plant with an annual production capacity of 10,000 engines for the

domestic market in the initial phase, followed by an expansion to 50,000 to accommodate exports to China,

after 2015. Fellow Korean manufacturer Kia Motors is also reportedly in negotiations with the economic

zone's management regarding a project to produce 100,000 cars per year from 2015.

Sales

Table: Vietnam Autos Sales, 2011-2018 (VAMA Members)

2011 2012 2013e 2014f 2015f 2016f 2017f 2018f

Total sales 110,938 78,558 93,093 102,358 111,160 119,610 129,425 140,845

Total sales (%chg y-o-y) -1.1 -29.2 18.5 10.0 8.6 7.6 8.2

8.8

Passenger carsales 64,620 43,030 55,078 61,302 66,819 72,165 78,660

86,526

Passenger carsales (% chg y-o-y) 11.8 -33.4 28.0 11.3 9.0 8.0 9.0

10.0

CommercialVehicle sales 46,318 35,528 38,015 41,056 44,341 47,444 50,766

54,319

CommercialVehicle sales (%chg y-o-y) -14.9 -23.3 7.0 8.0 8.0 7.0 7.0 7.0

Figures exclude Mercedes-Benz's sales. e/f = BMI estimate/forecast. Source: BMI, VAMA

Sales To Build On Solid 2013

According to the VAMA, vehicle sales of its members grew 20.0% in 2013, to 96,688 units. The strong

showing in 2013 was largely attributed to the rebound in the automotive sector, which was ravaged by the

recession that hit the country in 2012.

Vietnam Autos Report Q2 2014

Business Monitor International Page 17

Surging In Line With Our Bullish Outlook

Vietnam - Domestic Auto Sales, Units (LHS); % Chg y-o-y (RHS)

Sales include Mercedes-Benz's figures. Source: BMI, VAMA

We remain bullish on the Vietnamese auto market, however, and forecast vehicle sales to grow 10.0% in

2014 (this excludes sales of Mercedes-Benz, which reports its figures separately). While this is below2013's growth rate, it is because vehicle sales have normalised and the higher base effects of 2013 will

make it harder for them to continue growing at such a rapid clip.

Our bullish outlook on the sector chimes with our Country Risk team's optimistic view on Vietnam's

economy. As the government takes steps to privatise the country's state-owned enterprises (SOEs), we see itas a harbinger for more free market reforms in the coming years, which will undoubtedly provide a boost to

economic growth (see 'Privatisation Of SOEs Highly Positive For The Economy', January 8). BMI forecastsVietnam's GDP to grow 5.9% in 2014 and 6.4% in 2015.

Besides the ongoing privatisation drive, another factor supporting auto sales is our outlook for stable

interest rates in 2014. Our Country Risk team forecasts the State Bank of Vietnam's benchmark refinancing

rate to remain on hold at 7.00% throughout 2014 (see 'New Credit Growth Target Suggests Monetary Policy

Vietnam Autos Report Q2 2014

Business Monitor International Page 18

To Be Kept On', December 30 2013). The resultant stability in consumer financing rates will continue tomake it attractive for buyers to take on financing for their vehicle purchases.

While the breakdown between 2013 passenger car and commercial vehicle sales is still unavailable, car

sales growth handily outperformed CV sales growth. We expect this outperformance in passenger car sales

to continue in 2014, aided by the availability of affordable car loans. That said, we forecast CV sales, which

were impacted by weak demand from businesses in 2013, to grow 8.0% in 2014, as Vietnam's ongoing

banking sector reforms and SOE restructuring begin to bear fruit.

We have also upgraded our 2015 vehicle sales growth forecast from 7.2% to 8.6% due to the gradual

abolishment of import tariffs on vehicles imported from other ASEAN countries as part of the region's

Trade in Goods Agreement. As duties are slowly reduced, imported cars, which were previously priced out

of the local market due to high taxes, will now become more affordable for the average Vietnamese

consumer. This will then result in sustained sales growth for the imported car segment.

Looking further forward, BMI forecasts The Vietnamese American Medical Association (VAMA)members' domestic auto sales to enjoy average annual growth of 8.6% over the 2014-2018 period, to hit141,000 units by 2018. This is due to the following two reasons:

Formation of ASEAN Economic Community (AEC) By 2015: The AEC is expected to provide a hugeboost to Vietnam's economy. Being an export-oriented economy, Vietnam is going to benefit from the free

movement of goods under this accord. A rise in exports will boost the incomes of the rising middle class in

the country. This increase in disposable incomes will translate in higher sales for consumer durables like

cars. Furthermore being part of the AEC would mean that Vietnam would have to reduce or abolish its high

automotive taxes, further providing a boost to vehicle sales.

Huge Domestic Market Of 90 Million People: Vietnam has the largest population in the Association of

South East Asian Economies (ASEAN) of 90mn. BMI considers this to be a huge market with untappedpotential. As investment enters the country and its economy grows, more jobs will be created and we canexpect the share of middle class consumers to rise. This would increase discretionary spending for items

like cars. BMI forecasts the average annual growth rate for Vietnam's economy to be 7.0% for the next 10

years.

Vietnam Autos Report Q2 2014

Business Monitor International Page 19

Trade

Table: Vietnam Autos Trade, 2011-2018

2011 2012 2013 2014f 2015f 2016f 2017f 2018f

Vehicle trade balance, units -79,757 -38,088 -50,195 -55,550 -59,662 -64,258 -69,735 -76,761

Vehicle trade balance, units, % chgy-o-y 5.0 -52.2 31.8 10.7 7.4 7.7 8.5 9.4

f= BMI forecast. Source: BMI, VAMA

At present, the number of local parts used in car assembly is very low, with Suzuki Motor having a

localisation ratio of 3% and Ford Motor 2%, according to VietNamNet Online. This is far below the current

targeted ratio of 50%. Moreover, foreign manufacturers are yet to make a significant investment in

transferring modern technologies to Vietnam.

The government wants local suppliers to provide 50-60% of all the necessary car parts for domestic

production by 2020. Whether this can be achieved in such a short time, especially given a still-uncertain

tariff backdrop, remains to be seen.

Industry Trends And Developments - Will Abolishing Import Duties Decimate Local Manufacturing?

BMI View: The gradual abolishment of import tariffs in the Vietnamese auto market will inevitably pose a

threat to local manufacturing, especially to smaller carmakers, that may not have sufficient volumes to

enjoy economies of scale. That said, we still see pockets of opportunity for domestic production as the AECapproaches in 2015.

As of January 1 2014, Vietnam has reduced its duties on vehicles imported from other ASEAN countries by

10-50% as part of the ASEAN Trade in Goods Agreement (ATIGA). Under the ATIGA, Vietnam willeventually eliminate all import duties on cars by 2018.

The table below highlights the new 2014 tax regime for vehicle imports from other ASEAN nations.

Vietnam Autos Report Q2 2014

Business Monitor International Page 20

Table: Vietnam - 2014 Import Tax Regime

Type Of Vehicle Import Tax

Emergency cars and prisoner transport vehicles 0-5%

4-seater to 9-seater cars 50% (Down from 60% in 2013)

Trucks and other vehicles 0-50%

Bicycle, motorcycle and electric vehicles Set to decrease but % not stated

Completely knocked down kits 0-50%

Source: BMI, ASEANBRIEFING

Local Manufacturers At A Disadvantage?

While lower import taxes are definitely a boon for consumers as they will now get to enjoy cheaper cars,local carmakers such as Toyota Motor and Ford Motor have warned that the gradual removal of import

tariffs will hurt domestic auto manufacturing as the industry will need to compete with cheaper imports

flooding the Vietnamese auto market.

We believe there is some merit to this argument. We have stated before that auto production is

underperforming and more needs to be done by putting the right policies in place to attract investment in the

sector (see 'Sales Soar, But Production Still Underperforming', September 23 2013). Automakers have alsobeen reluctant to commit to local assembly due to the still small domestic sales volumes and with import

tariffs set to come down in the coming years it would make sense for many of these potential entrants to

import cars into Vietnam through dealerships rather than set up local assembly operations.

Therefore, it is reasonable to assume that even if policymakers put in place attractive incentives now, it will

be difficult for the Vietnamese auto sector to be able to reach the scale of Thailand and Indonesia, two

thriving auto hubs in the region, in the space of a few years. It is only when domestic sales pick up to the

levels seen in some of the bigger ASEAN markets that more manufacturing plants could be justified.

Imports Will Remain Strong

We believe the growth in car imports is set to accelerate in the coming years. For the first 11 months of

2013, the total vehicle sales of Vietnam Automobile Manufacturers Association (VAMA) members(automakers who have local assembly operations) came in at 85,507 units, an increase of 18.2%. On theother hand, the Vietnam Customs Office said that passenger car imports from Thailand and Indonesia (two

Vietnam Autos Report Q2 2014

Business Monitor International Page 21

of the major car exporters to Vietnam) more than doubled in the first 11 months of 2013, to 8,826 units. Asimport taxes steadily decrease, imported car sales can only grow strongly from their existing low base.

Furthermore, it is our long-held view that the formation of the ASEAN Economic Community (AEC) in2015 will accelerate trade in the region, as tariffs are further reduced, and result in automakers

concentrating their investment in one or two production hubs in the region to reap economies of scale. On

this front, we remain the most bullish on Thailand and Indonesia's potential and see carmakers increasing

their output in these countries as they gear up to increase their exports to other ASEAN markets such as

Vietnam (see 'Shipping And Auto Export Hubs Throw Up Interesting Possibilities', March 26 2013).

Is The Vietnamese Auto Industry Doomed?

That said, it is unfair to dismiss the potential of the Vietnamese auto industry and there remain pockets of

opportunity, even as imported vehicles will pose greater competition in the future. Below we summarise the

impact of the reduction in import tariffs.

Suppliers Will Remain Crucial

The growing imports of both used and new cars will mean that more consumers will require after-sales

services as well as spare parts to keep their vehicles in a roadworthy condition. Additionally, automakers

such as Toyota have long lamented the lack of localisation in the sector, which has resulted in them having

to import certain components and paying high import taxes on them. In addition, Toyota enjoys a domesticmarket share of greater than 30% and is likely to continue its local manufacturing operations even as import

duties are reduced. This will mean ample opportunities for auto suppliers to step in to commence production

of parts which are currently unavailable locally.

Furthermore, under the AEC framework, ASEAN countries which want to export cars to the rest of the

region need to ensure at least 40% local content in the vehicle. Once again, a higher concentration of

suppliers will be necessary in the sector if some of the larger local automakers are keen to export some of

their models to other markets.

2-Wheeler Industry To Remain Attractive

Vietnam is one of the biggest two-wheeler markets in the ASEAN region. Motorbikes remain an affordable

mode of transportation and are a practical option in a country where many of the roads are not wide enough

to accommodate cars. The more than 38mn two-wheelers on Vietnam's roads attest to their popularity and

we believe both manufacturers and suppliers in this segment still have plenty of growth potential.

Vietnam Autos Report Q2 2014

Business Monitor International Page 22

Smaller Local Manufacturers Could Exit

Some of the smaller VAMA members may be forced to shutter their operations well before 2018 as car

imports become more competitive vis--vis local manufacturing. These automakers may find it more

feasible to produce in their existing production facilities in the rest of the region and export to the

Vietnamese market.

Industry Forecast Passenger Cars

We forecast passenger car sales to grow 11.3% in 2014, to 61,000 units. Toyota remained the sales leader in

2013, a title it has held on to since September 2012.

Industry News - Rolls-Royce Opens A Dealership In Hanoi

Rolls-Royce is set to open a new showroom in Hanoi in Q413. It has appointed Regal Motor JSC as itsofficial importer-dealer for Vietnam.

The importer will also help Rolls-Royce to sell its high-end models in the country.

According to JSC's Asian regional manager, Herfried Hasenehrl, customers have a good understanding of

the firm's products as well as its value proposition.

Vietnam Autos Report Q2 2014

Business Monitor International Page 23

Industry Forecast Commercial Vehicles

Commercial Vehicles

As Vietnam's banking sector stabilises and state-owned enterprizes restructuring efforts begins to bear fruit,

we expect demand commercial vehicle (CV) demand from businesses to pick up in 2014.

We forecast CV sales to grow 8.0% in 2014, to 42,000 units.

Table: Top Five Companies By CV Sales

Manufacturer 2012 CV Sales (CBUs) 8M13 CV Sales (CBUs)

Truong Hai (Thaco) 15,281 9,521

Suzuki 3,330 2,217

Vinaxuki 4,453 1,200

Vinamotor 2,555 1,157

VEAM 1,881 1,083

Source: BMI, VAMA

Industry Forecast Suppliers

Suppliers

The domestic spare parts and components sector in Vietnam is small at present, although the government is

making it a priority. Given rapid economic growth in the region, there is significant development potential

for the industry. The Ministry of Industry and Trade is looking to make the domestic industry more

competitive. BMI believes the parts segment needs to be better developed to attract vehicle producers to

invest in the country. We believe the Vietnamese industry is in danger of being trapped in a vicious cycle

where carmakers are reluctant to invest in production without a well-developed supplier base, yet suppliers

want to see growth potential in vehicle assembly before investing.

To that, one move to boost domestic part production is the imposition of higher import tariffs on parts that

can be made domestically. The government wants local suppliers to be providing 50-60% of all the

necessary car parts for domestic production by 2020.

Vietnam Autos Report Q2 2014

Business Monitor International Page 24

In October 2013, Bridgestone announced that it will invest will invest JPY41.6bn (US$424mn) to doublethe output of its passenger car radial tyre plant currently under construction in Haiphong. The plant's

capacity will be increased to 49,000 tyres per day from 25,000 tyres currently and will be ready for

operations in March 2014.

Bridgestone's move is part of a trend we are observing of more suppliers and manufacturers leveraging on

Vietnam's low-cost production base. Vietnam has an abundance of raw materials such as rubber and this

move is strategic for Bridgestone.

That said, we continue to emphasise the need for the Vietnamese government to do more to attract larger

investments in the sector. Some of the necessary policies include preferred tax incentives, reduced export

tariffs and better support infrastructure to connect production bases to the ports in the country.

Although Vietnam is not currently a major production base for the region, it has become Bosch's productionand research and development (R&D) hub for certain products in South East Asia and has now secureddouble the original investment intended, while a move into new product areas has resulted in the acquisition

of a Taiwanese supplier.

BMI also sees positive opportunities in the government's plans to create a national industry hub in the Chu

Lai Economic Zone. The aim of the project is to increase the scale of domestic production in order to makethe sector more competitive when import tariffs are eliminated under the ASEAN Free Trade Agreement in

2018.

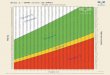

Global Trends: Suppliers In Driving Seat But Could Fortunes Turn?

BMI View: The global auto supplier and equipment index has outperformed the global auto manufacturersindex since the global financial crisis. We believe the possible reasons for this include the greater flexibilityof EU suppliers, the rise in the average age of US cars and trade protectionism. Two future developments,which may cause a reversal in fortunes in favour of original equipment manufacturers' are a pick up in theEuropean auto market and the upcoming AEC in 2015.

We recently highlighted original equipment manufacturers' (OEMs') greater bargaining power versus autosuppliers (see 'Illegal Cartels Highlight Low Supplier Power', October 1). However, we notice that thisdoes not always translate into automakers' share prices outperforming. Indeed, when we chart the

performance of the Bloomberg World Auto Manufacturers Index and Bloomberg World Auto Parts And

Vietnam Autos Report Q2 2014

Business Monitor International Page 25

Equipment Index over the past 10 years, we realise that both suppliers and automakers have their own

periods of outperformance.

It is important to realise that while suppliers' margins on the parts they sell are usually lower than the

margins which OEMs enjoy on their cars, there are other dynamics at play that determine the actualfinancial results of firms and ultimately their share price performance. The accompanying chart illustrates

the outperformance of suppliers versus carmakers since the global financial crisis in 2008-09. Below,

we outline our arguments to try and explain this phenomenon and give our thoughts on changing industry

trends, which may cause a reversal.

Vietnam Autos Report Q2 2014

Business Monitor International Page 26

Suppliers Outperforming Since Global Financial Crisis

BW Auto Manufacturers & Parts And Equipment Indices (Top); Spread (Bottom)

Indices are rebased to 100 from August 2003. *BW = Bloomberg World. Source: BMI, Bloomberg

EU Suppliers More Nimble Than Carmakers

Vehicle sales in the EU have been contracting since 2008 and sales declines in some markets intensified

when the eurozone crisis hit the region in 2010. This has led to heavy losses for European carmakers in the

past few years. Further compounding their problems is their inability to shed large proportions of their

Vietnam Autos Report Q2 2014

Business Monitor International Page 27

workforce, or expediently close underperforming factories, due to political pressure on some of these

national carmakers to retain workers.

European suppliers, on the other hand, are less in the political limelight due to their smaller size and have

therefore been able to rationalise their European operations faster. This has allowed them to be more nimble

and re-orientate their businesses to find new growth opportunities in emerging markets (EMs) in Asia,Eastern Europe and Latin America, which are increasingly making up a bigger share of their sales (see'Suppliers Continue To Shift Strategic Focus', June 24).

Therefore, it is no surprise that the share prices of European suppliers have recovered much faster and

stronger than their carmaker counterparts since the global financial crisis.

Ageing US Fleet Makes Market Attractive For Suppliers

To be sure, the American consumer has deleveraged significantly since the financial crisis. However, the

bumpy economic recovery has resulted in consumers holding on to their set of wheels longer and has also

given rise to strong used car sales. Therefore, while new vehicle sales have been growing at a strong clip

since 2009, the average age of the US vehicle fleet has recently climbed to an all-time high of 11.4 years.

In such an environment, suppliers would naturally perform better, as they are able to sell parts to OEMs for

the production of new cars as well as sell replacement parts directly to the end consumers. As the vehicles

on the road get older, it is reasonable to assume that spending on replacement parts has to rise to keep them

in a roadworthy condition.

Trade Protectionism Puts Vehicle Imports At A Disadvantage

In recent years, trade protectionism, especially in emerging markets (EMs), has been on the rise. Thesecountries have nascent auto industries, and in order to encourage automakers to produce domestically, they

usually impose high tariffs on auto imports. While both auto parts and vehicle imports are taxed, parts are

usually taxed at a lower rate. We believe this may be because governments realise that the lack of

localisation in their domestic auto industries would still require local manufacturers to import components

from overseas. A case in point is Vietnam, where the import tariff on completely built unit (CBU) importsfrom ASEAN will be 50% in 2014, but for car parts will only be 15-25%.

Vietnam Autos Report Q2 2014

Business Monitor International Page 28

The upshot of this, in our opinion, is that suppliers would find it easier to export their parts to early

emerging/frontier markets compared with automakers, whose exports may be priced out due to exorbitant

tariffs.

Can Suppliers Continue Outperforming?

While there may definitely be other reasons for suppliers' share prices outperforming manufacturers in the

past few years, the important question going forward is whether this trend will endure. We believe it is hard

to tell at this point. However, we highlight two developments in the future, which may cause a reversal in

fortunes.

Pick Up In The European Vehicle Market

Although BMI still maintains a bearish outlook on the European vehicle market, we expect the region to

recover in the coming years. As sales in individual car markets begin to slow their rate of contraction, and

eventually return to growth, on the back of pent-up demand, European carmakers' could begin to

outperform suppliers.

Upcoming 2015 AEC Could Tilt The Scales In OEMs Favour

The upcoming ASEAN Economic Community (AEC) in 2015 will bring down trade tariffs within SouthEast Asia (SEA) and by 2018 most, if not all, countries in SEA will cut their import tariffs to zero. Thisdevelopment may end up being a game changer for automakers as they concentrate their production in one

or two hubs in the region and export their CBUs tariff-free to the rest of ASEAN.

Vietnam Autos Report Q2 2014

Business Monitor International Page 29

Macroeconomic Forecasts

BMI View: Although we expect the Vietnamese economy to record yet another quarter of sub-par growth inQ413, we are beginning to see potential for upside surprises to domestic demand over the coming quarters.Recent data on foreign direct investment inflows, remittances, passenger car sales, and property marketlaunches, suggests to us that domestic demand is on a nascent recovery, setting the stage for stronger 2014growth.

The general consensus is expecting the Vietnamese economy to suffer yet another quarter of sub-par growth

mainly due to subdued external demand and the lack of progress on banking sector reforms. This is closely

in line with our view that real GDP growth will come in at just 5.3% in 2013, a slight improvement from5.2% in 2012. Looking ahead to 2014, however, evidence of improving macroeconomic fundamentals in

Vietnam (especially with regards to the outlook for domestic demand) suggests to us the balance of risks toour growth forecast of 6.0% is gradually tilting towards the upside.

Robust Remittances Could Boost Domestic Demand

Vietnam - Unrequited Transfers, US$mn

Source: BMI, Asian Development Bank

Vietnam Autos Report Q2 2014

Business Monitor International Page 30

Remittances: According to estimates published by the World Bank, the Vietnamese economy is on track to

record a bumper year for remittance inflows. The country is expected to receive US$10.6bn in remittancesfrom Vietnamese citizens working abroad, a robust 6.5% increase from 2012. Crucially, we believe that

remittance inflows will remain strong over the coming quarters as macroeconomic conditions in Vietnam

continue to improve. Growing confidence in the stability of the Vietnamese dong should also help to

encourage Vietnamese workers abroad, to a certain extent, to remit a larger share of their earnings back

home. We believe that this will help to boost domestic demand while providing support for the currency.

Foreign Direct Investment: Total foreign direct investment (FDI) inflows are also set to surpass thegovernment's full-year target of US$13bn, after data released by the Ministry of Planning and Investmentshowed that inflows surged by 19.5% year-on-year (y-o-y) growth over the first eight months of the year.The strong reading chimes with our view that the country's solid long-term growth story should continue to

attract foreign investors over the coming years.

Automobile Sales: We are witnessing signs of a robust recovery in automobile sales, a sign that pent-up

domestic demand is beginning to rebound. According to the Vietnam Automobile Manufacturers

Association (VAMA), September vehicle sales of its members surged by 20.6% year-on-year (y-o-y),exceeding our already bullish forecast of 12.5% for the year (see 'Bullish On CV Sales In The Medium ToLong Term', October 14 2013).

Vietnam Autos Report Q2 2014

Business Monitor International Page 31

Developers Eyeing Property Market Rebound

Vietnam - Real Estate Index

Source: BMI, Blooomberg

Property Market: Meanwhile, we see increasing evidence that the Vietnamese property market may have

bottomed out (see 'Early Signs Of A Recovery, But No Property Market Boom In Sight', August 14 2013).According to a quarterly report published by real estate agency CBRE Vietnam, the number of new

launches surged by 12% y-o-y in Q313. Anecdotal evidence from the local media suggests to us thatdemand for real estate following the sharp decline in prices since 2011 may be recovering. To be sure, we

maintain our view that we are unlikely to see a property market boom given the healthy pipeline of new

units that will come online in 2014. Nonetheless, we acknowledge that consumer confidence is recovering

and we could potentially see some upside surprises to domestic demand in 2014.

Expenditure Breakdown

Private Consumption: We expect private consumption to grow at a relatively resilient pace of 5.0% in

2014. However, we note that the risk of further bankruptcies among SMEs could potentially lead to

widespread job losses, especially in export-driven sectors. Uncertainties over the outlook for employmentcould, in turn, prompt households to cut back on spending.

Vietnam Autos Report Q2 2014

Business Monitor International Page 32

Gross Fixed Capital Formation: We foresee a pickup in private sector investment growth in 2014, partly

led by increased foreign direct investment inflows. We believe lending rates will gradually ease over the

coming months as the effect of recent rate cuts by the SBV begins to kick in. We are also seeing evidence

that credit conditions are improving. Accordingly, we expect gross fixed capital formation growth to

accelerate slightly from 4.1% in 2013 to 4.8% in 2014.

Public Spending: We expect total public spending to remain relatively resilient in 2014, expanding at a

respectable pace of 6.1%. However, there is limited room for the government to increase spending further

owing to concerns over the need to finance a potential bailout of ailing state-owned commercial banks.

Net Exports: Net exports remain the biggest downside risk to our outlook for the Vietnamese economy,

although we expect external demand to pick up in 2014. Vietnam's trade account has fallen back into

deficits in recent months, but we see the case for a substantial pickup in external demand on the back of a

rebound in regional growth over the coming quarters. Accordingly, we still expect exports to expand at a

moderate pace of 5.9% in 2014.

Table: Vietnam - Economic Activity

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Nominal GDP,VNDbn 3 2,157,829 2,779,880 3,245,419 3,657,621 4,117,487 4,631,499 5,203,774 5,841,949

Nominal GDP,US$bn 3 112.9 134.6 155.5 175.0 200.2 227.8 257.4 291.4

Real GDP growth,% change y-o-y 3 6.4 6.2 5.2 5.3 6.0 6.9 7.0 7.0

GDP per capita,US$ 3 1,267 1,497 1,712 1,909 2,163 2,439 2,733 3,068

Population, mn 4 89.0 89.9 90.8 91.7 92.5 93.4 94.2 95.0

Industrialproduction index,% y-o-y, ave 1,5 14.1 10.9 7.0 7.6 8.7 9.6 9.9 9.8

Unemployment,% of labour force,eop 2,6 4.3 3.6 3.2 3.7 3.5 3.5 3.6 3.5

Notes: f BMI forecasts. 1 at 1994 prices; 2 Urban Area Only. Sources: 3 Asian Development Bank, General StatisticsOffice; 4 World Bank/UN/BMI; 5 General Statistics Office; 6 General Statistics Office/BMI.

Vietnam Autos Report Q2 2014

Business Monitor International Page 33

Industry Risk Reward Ratings

Asia-Pacific Risk/Reward Ratings

The aim of BMI's Risk/Reward Ratings for the automotive industry is to detail the rewards and the risks

that carmakers operating in a particular region - in this case Asia-Pacific - may face. The unique system

assesses crucial factors, such as sales and output growth, international trade, market size and location, and

the level of market competition, in addition to taking into account a country's economic and political

backdrop. The ratings system allows analysts to fully expound the potential advantages and disadvantages

of investing in Asian car markets, and offers an overall comparison of the key markets in the region.

Overall scores for most countries in this region have shifted downward on the back of relatively slower

growth in 2013. Government stimulus measures for the auto industry in countries such as Japan, Thailand

and China bolstered growth in the past few years. These are no longer present in 2013, and sales in these

markets have started to wane.

That said, despite China's overall score falling from 66 to 64.96, it has now surpassed South Korea and

Japan to take the first place in the ratings table. We remain bullish on the Chinese auto market despite our

view for a H213 slowdown, and expect vehicle sales growth to among the highest in the region. The sheer

size of the market offers plenty of long-term opportunities, especially to new entrants that are looking to

grab market share from well-established incumbents. Lastly, as the Chinese economy re-orientates itself to a

more consumption-driven one in the coming years, demand for passenger cars will continue to remain

robust.

In second place is Japan, which has seen its score fall from 74 to 64.77, largely owing to its bleak domestic

sales outlook. While we forecast sales to contract in 2013, our long-term sales growth forecasts are also

nothing to cheer about, as the high level of vehicle ownership limits sales growth. Nonetheless, the country

scores well in terms of country risk, with low levels of corruption and a sound legal framework bumping up

the market's overall score. However, labour costs remain high owing to the rigidity of labour laws, which

adds to the cost of expanding production.

Malaysia has made an impressive climb to third position, from fifth previously. The country is a leader in

the Association of South East Asian Nations trade bloc, which has seen it attract regional production

activities in the autos sector, especially those which are higher value-added (see 'DRB-VW InvestmentDemonstrates Value-Added Production', May 3 2013). With the ruling Barisan Nasional party voted back in

Vietnam Autos Report Q2 2014

Business Monitor International Page 34

power in recent elections, we see greater stability in Malaysia's macro environment as well as auto sector

policies.

In South Korea, exports take up a much larger share of production compared with domestic sales, and the

country has dropped to fourth place with an overall store of 62.55 out of 100, down from 69. South Korea's

historically poor labour relations surfaced once more in 2013, with Hyundai Motor suffering a production

outage (see 'New Labour Dispute Adds To Hyundai's Woes', April 23 2013). Higher wage demands fromunions in the past few years have raised operating costs. This weighs on the country's overall score,

although long-term political and economic stability reduce the risks.

Singapore has made the biggest move upward, catapulting to fifth place from eighth previously, taking its

overall rating to 59.76. While the country does not have any domestic production facilities, its conducive

business environment and stable regulatory outlook gives it one of the highest risk ratings in the region.

While recent loan curbs will weigh on car demand slightly, demand for cars still outweighs supply, which is

regulated by the certificate of entitlement.

In sixth place is Australia, which has tumbled from its fourth position. The decision by Ford to terminate

domestic production by 2016 (see 'Ford Throws In The Towel', May 23 2013), highlights the intensity of thedetrimental impact on manufacturing brought about by a strong Australian dollar and high labour costs.

Although the Australian dollar has been weakening lately, our downbeat outlook on the economy limits the

auto market rewards to firms.

Dropping one place to seventh is Thailand. While we expect domestic vehicle sales to contract in 2013

following the end of the first car buyer scheme in 2012, the export outlook for the country remains bright.

Strong government support, together with excellent support infrastructure, continues to attract auto sector-

related investment from both suppliers and carmakers. BMI is bullish on Thailand's production growth

potential for the next five years.

Hong Kong slides down one place to eighth. While its regulatory scores have improved further owing to

government incentives to scrap old and polluting commercial vehicles (which will improve new vehiclesales), the country's lack of production facilities means that the market is unlikely to climb much further inthe ratings in the foreseeable future.

In ninth place is India, which has moved up one notch. However, its overall score has dropped drastically

from 55 to 50.91. The passenger car market is in its eight consecutive month of contraction, which has

prompted the industry to seek a revival package from the government. Given that we expect consumer

Vietnam Autos Report Q2 2014

Business Monitor International Page 35

confidence to remain low for some time, we have turned increasingly downbeat on the industry's prospects,

resulting in a lowering of our industry rewards score to 48.68.

Indonesia has dropped to 10th place, from ninth previously. While the country's long-term auto sector

growth potential is undoubtedly strong owing to the size and still underpenetrated nature of the domestic

market, its country risk rating acts as a hindrance, with low scores for corruption, bureaucracy and legal

framework. Furthermore, the recent hike in fuel prices will serve to heighten market risk in the short term.

Taiwan and Philippines have held their positions in 11th and 12th place respectively. Taiwan's strength is in

its low corruption and strong regulatory framework, which boosts its country risk scores. The Philippines,

on the other hand, benefits from a competitive landscape that is still underpenetrated by carmakers,

providing opportunities for new entrants despite the dominance of Japanese brands in the market.

Vietnam and Pakistan have traded places in 13th and 14th. While Pakistan continues to suffer from weak

demand in the auto sector, there are some measures introduced in the latest budget that are likely to boost

the long-term potential of the industry (see 'Budget Brings Short-Term Pain But Long-Term Gain', June 282013). Vietnam, on the other hand, continues to suffer from the lack of a coherent auto sector policy by thegovernment, which is hampering the production potential of the country.

Vietnam Autos Report Q2 2014

Business Monitor International Page 36

Table: Asia-Pacific Autos Risk/Reward Ratings

Rewards Risks

Autos

MarketCountry

StructureIndustryRewards

MarketRisks

CountryRisk Risks

AutosMarketRating Ranking

China 73.33 38.83 61.26 80.00 67.18 73.59 64.96 1

Japan 63.33 74.81 67.35 45.00 72.50 58.75 64.77 2

Malaysia 58.33 62.59 59.82 70.00 76.57 73.29 63.86 3

South Korea 55.00 77.50 62.88 50.00 73.60 61.80 62.55 4

Singapore 31.67 92.06 52.81 65.00 86.99 76.00 59.76 5

Australia 46.67 75.74 56.84 45.00 77.99 61.49 58.24 6

Thailand 46.67 49.26 47.58 85.00 69.73 77.37 56.51 7

Hong Kong 25.00 96.03 49.86 50.00 81.95 65.97 54.69 8

India 61.67 24.56 48.68 65.00 47.20 56.10 50.91 9

Indonesia 53.33 33.56 46.41 70.00 49.94 59.97 50.48 10

Taiwan 40.00 40.16 40.06 65.00 73.48 69.24 48.81 11

Philippines 31.67 39.59 34.44 80.00 57.24 68.62 44.69 12

Pakistan 45.00 18.00 35.70 70.00 42.00 56.00 42.00 13

Vietnam 28.33 38.60 31.93 65.00 49.50 57.25 39.52 14

Source: BMI

Vietnam Autos Report Q2 2014

Business Monitor International Page 37

Company Profile

Company Monitor

BMI View: Ford Motors' record 2013 sales in China have put the firm among the top five largestautomakers in the market. China remains an important Asian market for the carmaker as it embarks on astrategic plan to diversify away from its main profit centre in North America, and going forward, we see theAsia Pacific region increasing its profit contribution to Ford's operations as the automaker's expansionstrategy bears fruit.

Ford Motor had a phenomenal 2013 in China, where its sales reached a record of 935,813 vehicles, an

increase of 49%. An expanded line of products, a sustained inland push, as well as strong demand helped to

boost sales. The automaker introduced seven of its next generation global vehicles in the market in 2013,

including the Ford Ecosport, Ford Kuga, the new Fiesta and the latest Mondeo. However, its Ford Focus

remaining the best-selling model, with 2013 sales growing 36%, to 403,640 units.

No Longer An Underdog In China

We believe Ford can continue to build on its success in 2014. We highlighted the gain in sales of non-

Japanese brands at the expense of their Japanese counterparts back in October 2012, as the outbreak of the

Sino-Japanese dispute saw consumers boycotting Japanese marques (see 'Japan's Pain Is Korea's GainOnce More', October 2012). During that time, Ford's sales also experienced a positive tailwind from late2012 and early 2013.

However, for much of 2013, Ford's success could be attributed to the company's successful local strategy

and going forward, we see the firm's internal strengths driving its sales. The Ford brand is gaining traction

in the market and the automaker's expansion plans will be a positive growth factor for sales in 2014.

According to John Lawler, chairman and CEO of Ford Motor China, the firm plans to grow its domestic

capacity and expand its dealership network in 2014 so as to "continue bringing high quality, safe, and fuel

efficient vehicles to consumers."

The carmaker has certainly made great strides in the Chinese market where it was a late entrant compared

with the first movers Volkswagen AG (VW) and General Motors Company (GM). It has steadilyincreased its market share over the years and 2013 was the first year since 2001 that its sales surpassed that

of Toyota Motor. Toyota increased its sales by 9%, to 917,500 units, as the Japanese automaker recovered

Vietnam Autos Report Q2 2014

Business Monitor International Page 38

from its 2012 slump in sales. In fact, Ford's 2013 domestic auto sales now make it the fifth largest carmaker

in China.

Force In Its Own Right

China - 2013 Vehicle Sales Of Top Carmakers

Source: BMI

China A Crucial Pillar For Asian Strategy

North America remains the main profit centre for Ford and the region contributed US$7.08bn in operatingincome to the firm's business for the first nine months of 2013. However, the automaker has stated in its

global 'ONE FORD' plan that it aims to diversify its profit sources by increasing its presence in some of the

largest and fastest growing markets in the world. China is one such market where Ford is aggressively

increasing its investment, as it makes up for lost time due to its rather delayed entry into the country.

The firm's Asian division has yet to post large profits as the carmaker is still in the stage of ramping up

investment in the region (which is a cost to the company). Besides China, Ford is investing over US$1bn inIndia to build its Sanand manufacturing facility and double the number of dealerships in the country to 300

by 2015 (see 'Ford's India Strategy Finally In Right Gear', December 6 2012). While estimates suggest that

Vietnam Autos Report Q2 2014

Business Monitor International Page 39

regional expansion plans could cost the company over US$5bn, we believe it will reap dividends for Ford inthe long run.

Asia To Be Next Profit Centre

Ford - Operating Income By Geography (Outside North America), US$mn

Source: BMI, Company Financials

The Asia Pacific and Africa region bounced back from an operating loss of -US$116mn in 9M12 to anoperating profit of US$309mn in 9M13. We see this region increasing its profit share in the coming years asinvestments in capacity and dealerships begin to pay off.

Vietnam Autos Report Q2 2014

Business Monitor International Page 40

GM Vietnam

SWOT Analysis

Strengths Good use of Chevrolet brand.

Third in terms of market share.

Weaknesses Market share of 5% still trails Toyota's 35%.

Opportunities Could increase sales in commercial vehicle segment by introducing more models.

Mass market positioning could benefit sales with Vietnam's steady GDP growth.

Threats Strong competition from Ford and other brands which have similar market share.

Company Overview GM Vietnam Motor Company was established in 1993 by the former Daewoo Motor

Corporation. In 2011, GM Vietnam decided to align its operations to make Chevrolet its

retail brand and sells its cars under that brand in the country. However, it continues to

provide after-sales care and spare parts for owners of Daewoo cars.

In 2012, GM Vietnam sold a total of 5,613 units of vehicles, a 45.8% y-o-y decrease.

From that, 1,202 units were commercial vehicles and 4,411 units were passenger cars.

For the first eight months of 2013, GM Vietnam sold 3,090 vehicles.

Strategy GM Vietnam launched the new Chevrolet Colorado pickup truck imported from Thailand

in March 2013.

It says the Colorado LTZ is equipped with a turbo-diesel engine that provides a

combination of performance and fuel efficiency, as well as better performance on

Vietnam's roads.

The pickup is distributed as a CBU vehicle imported from Thailand in GM Vietnam's

dealer network nationwide at a price of VND729mn (US$34,570), including VAT.

Company Data Number of employees: 600

Vietnam Autos Report Q2 2014

Business Monitor International Page 41

Mercedes-Benz Vietnam

SWOT Analysis

Strengths Strong global brand name

Sales leader among VAMA members in the luxury market

Weaknesses Idle capacity at the plant could eat into profits

Opportunities Expansion into Vietnamese cities with growing affluence

Threats Competition from luxury brands not in VAMA, such as Audi

Volatile Vietnamese dong might require hedging, to protect profits

Company Overview Mercedes-Benz Vietnam (MBV) is a joint venture between Daimler (70%) and Saigon

Automobile Mechanical Corporation (30%). MBV is introducing passenger cars and

commercial vehicles (CVs) to the Vietnamese market under the brand and standards of

Mercedes-Benz. The company is the 2012 sales leader among Vietnam Automobile

Manufacturers Association (VAMA) members in the luxury vehicle market (includes both

its passenger cars and CVs).

MBV's factory is located in Go Vap District, Ho Chi Minh City. The factory covers

105,000 square meters and has a production capacity of about 3,500 vehicles per year.

The factory includes a Training Centre, which carries out sales, marketing and technical

training courses to ensure a high level of employee competence.

MBV's total vehicle sales for 2012 were up 110% y-o-y to 1,929 units. While its

passenger car sales contracted y-o-y, its commercial vehicle sales helped the company

post a y-o-y increase in total vehicle sales. The company's 2012 market share in the

vehicle market among VAMA members was 2.4%.

For the first eight months of 2013, Mercedes sold 974 vehicles.

Strategy During the period 2010-2012, Mercedes-Benz invested more than US$10mn in the

assembly line of its factory and another US$10mn to expand its network nationwide.

Company Data Year established: 1995

General Director: Michael Behrens

Vietnam Autos Report Q2 2014

Business Monitor International Page 42

No. of employees: 500-600

Vietnam Autos Report Q2 2014

Business Monitor International Page 43

Automotive Asia Ltd

SWOT Analysis

Strengths Selling more than one luxury brand gives the company diversification.

An increase in Audi's imports shows the luxury car market is performing better than

the mass market.

Weaknesses Lack of domestic production could make imported cars expensive.

Opportunities New showroom in Hanoi would give company more exposure.

Expansion opportunities in Vietnamese cities with growing affluence.

Threats Competition from Mercedes, which has domestic production.

Company Overview Automotive Asia sells both Audi and BMW brands in Vietnam through its dealerships.

While sales in the passenger car premium market among Vietnam Automobile

Manufacturers' Association (VAMA) members declined about 44% y-o-y, sales in the

imported passenger car premium market (which Automotive Asia is in), declined just

29%. Furthermore, according to industry sources, Audi's 2012 imports increased y-o-y.

Automotive Asia, the official Audi Importer in Vietnam, is a joint venture between

CFAO - the majority shareholder - and Openasia. Registered in December 2007,

Automotive Asia launched Audi in Vietnam in October 2008.

Lien-A International JSC is the official distributor for Audi cars in Vietnam. To ensure

Audi customers optimal operation of their cars in Vietnam, Lien-A International JSC

operates its own branches in HCMC and Hanoi. Audi Ho Chi Minh City, the second Audi

Terminal launched in South East Asia, was inaugurated in October 2008.

Strategy Automotive Asia is set to open a new 3,000 square foot terminal in Hanoi, which will

serve as a showroom as well as a workshop, where painting and tooling services will be

provided.

Operational Data General Director: Laurent Genet

Vietnam Autos Report Q2 2014

Business Monitor International Page 44

Regional Overview

In this quarterly regional round-up, we examine the trends in Asian auto markets, which we believe will be

dominant in 2014. We specifically focus on the Chinese, Indian, Indonesian and Japanese auto markets as

we believe that important developments in the first half of 2014 will be crucial in determining the sales

trajectory in these markets.

Table: Vehicle Sales 2013 (CBUS)

Last Month Monthly Sales % Chg y-o-y YTD Sales%

GrowthBMI End-2013

Sales

BMI Full-yearGrowth

Forecast(2013, % Chg

y-o-y)

China December 2,100,000 16.0 21,980,000 13.8 21,635,298 12.1

India November 245,250 -14.2 2,063,446 -8.2 3,240,621 -6.7

Japan December 423,000 25.0 5,375,515 0.1 5,492,000 2.3