Embed Size (px)

DESCRIPTION

Blominvest Bank - The Lebanon Brief - New Angel Investors for Tech Startups - The Lebanese Banks

Citation preview

Your Investment Reference

THE

LEBANON BRIEF

ISSUE 835

Week of 02 – 07 September, 2013

ECONOMIC RESEARCH DEPARTMENT

Rashid Karame Street, Verdun Area

P.O.Box 11-1540 Beirut, Lebanon

T (01) 747802 F (+961) 1 737414

www.blom.com.lb

S A L

The Lebanon Brief Table Of Contents Page 2 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

TABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTS

FINANCIAL MARKETSFINANCIAL MARKETSFINANCIAL MARKETSFINANCIAL MARKETS 3333

Equity Market 3

Foreign Exchange Market 5

Money & Treasury Bills Market 5

Eurobond Market 6

ECONOMIC AND FINANCIAL NEWSECONOMIC AND FINANCIAL NEWSECONOMIC AND FINANCIAL NEWSECONOMIC AND FINANCIAL NEWS 7777

Lebanon’s Fiscal Deficit Touches $1.62B by May 2013 7

Commercial Banks Consolidated Total Assets Grew to $157.81B in July 8

BMI: Lebanon’s Sovereign Risk Rating Score slips to 38/100 8

Trade Deficit Increases to $9.92B up to July 2013 9

Public Sector Wages Increased to $647.43M up to March 2013 10

CORPORATE DEVELOPMENTSCORPORATE DEVELOPMENTSCORPORATE DEVELOPMENTSCORPORATE DEVELOPMENTS 11111111

BLC Bank Lists New Preferred “C” shares 11

FOCUS IN BRIEFFOCUS IN BRIEFFOCUS IN BRIEFFOCUS IN BRIEF 12121212

New Angel Investors for Tech Startups: the Lebanese Banks 12

This report is published for information purposes only. The information herein has been compiled from, or based upon sources we believe to be

reliable, but we do not guarantee or accept responsibility for its completeness or accuracy. This document should not be construed as a

solicitation to take part in any investment, or as constituting any representation or warranty on our part. The consequences of any action taken

on the basis of information contained herein are solely the responsibility of the recipient.

The Lebanon Brief Page 3 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

FINANCIAL MARKETSFINANCIAL MARKETSFINANCIAL MARKETSFINANCIAL MARKETS

Equity Market

Stock Market

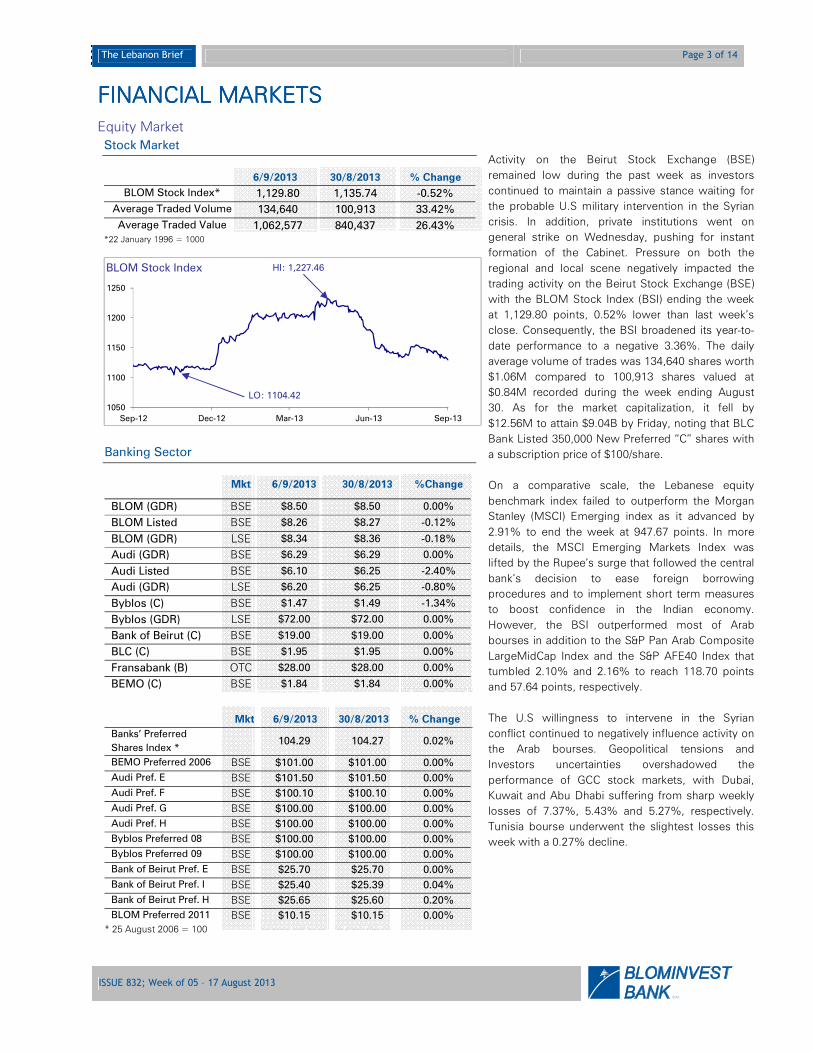

6/9/2013 30/8/2013 % Change

BLOM Stock Index* 1,129.80 1,135.74 -0.52%

Average Traded Volume 134,640 100,913 33.42%

Average Traded Value 1,062,577 840,437 26.43% *22 January 1996 = 1000

Activity on the Beirut Stock Exchange (BSE)

remained low during the past week as investors

continued to maintain a passive stance waiting for

the probable U.S military intervention in the Syrian

crisis. In addition, private institutions went on

general strike on Wednesday, pushing for instant

formation of the Cabinet. Pressure on both the

regional and local scene negatively impacted the

trading activity on the Beirut Stock Exchange (BSE)

with the BLOM Stock Index (BSI) ending the week

at 1,129.80 points, 0.52% lower than last week’s

close. Consequently, the BSI broadened its year-to-

date performance to a negative 3.36%. The daily

average volume of trades was 134,640 shares worth

$1.06M compared to 100,913 shares valued at

$0.84M recorded during the week ending August

30. As for the market capitalization, it fell by

$12.56M to attain $9.04B by Friday, noting that BLC

Bank Listed 350,000 New Preferred “C” shares with

a subscription price of $100/share.

On a comparative scale, the Lebanese equity

benchmark index failed to outperform the Morgan

Stanley (MSCI) Emerging index as it advanced by

2.91% to end the week at 947.67 points. In more

details, the MSCI Emerging Markets Index was

lifted by the Rupee’s surge that followed the central

bank’s decision to ease foreign borrowing

procedures and to implement short term measures

to boost confidence in the Indian economy.

However, the BSI outperformed most of Arab

bourses in addition to the S&P Pan Arab Composite

LargeMidCap Index and the S&P AFE40 Index that

tumbled 2.10% and 2.16% to reach 118.70 points

and 57.64 points, respectively.

The U.S willingness to intervene in the Syrian

conflict continued to negatively influence activity on

the Arab bourses. Geopolitical tensions and

Investors uncertainties overshadowed the

performance of GCC stock markets, with Dubai,

Kuwait and Abu Dhabi suffering from sharp weekly

losses of 7.37%, 5.43% and 5.27%, respectively.

Tunisia bourse underwent the slightest losses this

week with a 0.27% decline.

Banking Sector

Mkt 6/9/2013 30/8/2013 %Change

BLOM (GDR) BSE $8.50 $8.50 0.00%

BLOM Listed BSE $8.26 $8.27 -0.12%

BLOM (GDR) LSE $8.34 $8.36 -0.18%

Audi (GDR) BSE $6.29 $6.29 0.00%

Audi Listed BSE $6.10 $6.25 -2.40%

Audi (GDR) LSE $6.20 $6.25 -0.80%

Byblos (C) BSE $1.47 $1.49 -1.34%

Byblos (GDR) LSE $72.00 $72.00 0.00%

Bank of Beirut (C) BSE $19.00 $19.00 0.00%

BLC (C) BSE $1.95 $1.95 0.00%

Fransabank (B) OTC $28.00 $28.00 0.00%

BEMO (C) BSE $1.84 $1.84 0.00%

* 25 August 2006 = 100

Mkt 6/9/2013 30/8/2013 % Change

Banks’ Preferred

Shares Index *

104.29 104.27 0.02%

BEMO Preferred 2006 BSE $101.00 $101.00 0.00%

Audi Pref. E BSE $101.50 $101.50 0.00%

Audi Pref. F BSE $100.10 $100.10 0.00%

Audi Pref. G BSE $100.00 $100.00 0.00%

Audi Pref. H BSE $100.00 $100.00 0.00%

Byblos Preferred 08 BSE $100.00 $100.00 0.00%

Byblos Preferred 09 BSE $100.00 $100.00 0.00%

Bank of Beirut Pref. E BSE $25.70 $25.70 0.00%

Bank of Beirut Pref. I BSE $25.40 $25.39 0.04%

Bank of Beirut Pref. H BSE $25.65 $25.60 0.20%

BLOM Preferred 2011 BSE $10.15 $10.15 0.00%

1050

1100

1150

1200

1250

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

BLOM Stock Index HI: 1,227.46

LO: 1104.42

The Lebanon Brief Page 4 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

Real Estate

Mkt 6/9/2013 30/8/2013 % Change

Solidere (A) BSE $10.90 $11.01 -1.00%

Solidere (B) BSE $10.82 $10.62 1.88%

Solidere (GDR) LSE $10.31 $10.65 -3.19%

Once again, the banking sector spread its

dominance over the market this week, accounting

for 77.51% of total trades. The listed shares of

BLOM, Audi and Byblos declined by 0.12%,

2.40% and 1.34% to settle at $8.26, $6.10 and

$1.47, respectively.

Manufacturing Sector

Mkt 6/9/2013 30/8/2013 % Change

HOLCIM Liban BSE $15.68 $15.68 0.00%

Ciments Blancs (B) BSE $3.23 $3.23 0.00%

Ciments Blancs (N) BSE $3.24 $3.24 0.00%

On the London Stock Exchange, the GDRs of

Solidere, BLOM and Audi edged down by 3.19%,

0.18% and 0.80% to reach $10.31, $8.34 and

$6.20, respectively.

Funds

Mkt 6/9/2013 30/8/2013 % Change

BLOM Cedars Balanced

Fund Tranche “A” ----- $6,882.56 $6,898.26 -0.23%

BLOM Cedars Balanced

Fund Tranche “B” ----- $5,009.47 $5,024.81 -0.31%

BLOM Cedars Balanced

Fund Tranche “C” ----- $5,227.35 $5,239.28 -0.23%

BLOM Bond Fund ----- $9,621.91 $9,724.12 -1.05%

On the other hand, the BLOM preferred shares

index (BPSI) slightly edged up by 0.02% to reach

104.29 points boosted by Bank of Beirut preferred

shares increases. Accordingly, the class “I”

posted a 0.04% to $25.40, while the class “H”

edged 0.20% up to settle at $25.65. Worth

pointing out that BLC bank listed on the BSE

350,000 preferred shares class “C” that started

trading on Monday.

Retail Sector

Mkt 6/9/2013 30/8/2013 % Change

RYMCO BSE $3.50 $3.50 0.00%

ABC (New) OTC $33.00 $33.00 0.00%

Solidere stocks were seen traded on low volume

this week, representing 22.49% of total trades.

Solidere stock Class A fell 1.00% to end the week

at $10.90, while Solidere Class B increased by

1.88% to $10.82.

Looking ahead, if the cabinet formation dilemma

would be solved in the near future, it may pull up

the BSI from its losses. However, investors will

remain on the sidelines waiting the final decision

of the U.S concerning its military action in Syria.

Tourism Sector

Mkt 6/9/2013 30/8/2013 % Change

Casino Du Liban OTC $480.00 $480.00 0.00%

SGHL OTC $7.00 $7.00 0.00%

The Lebanon Brief Page 5 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

Foreign Exchange Market

Lebanese Forex Market

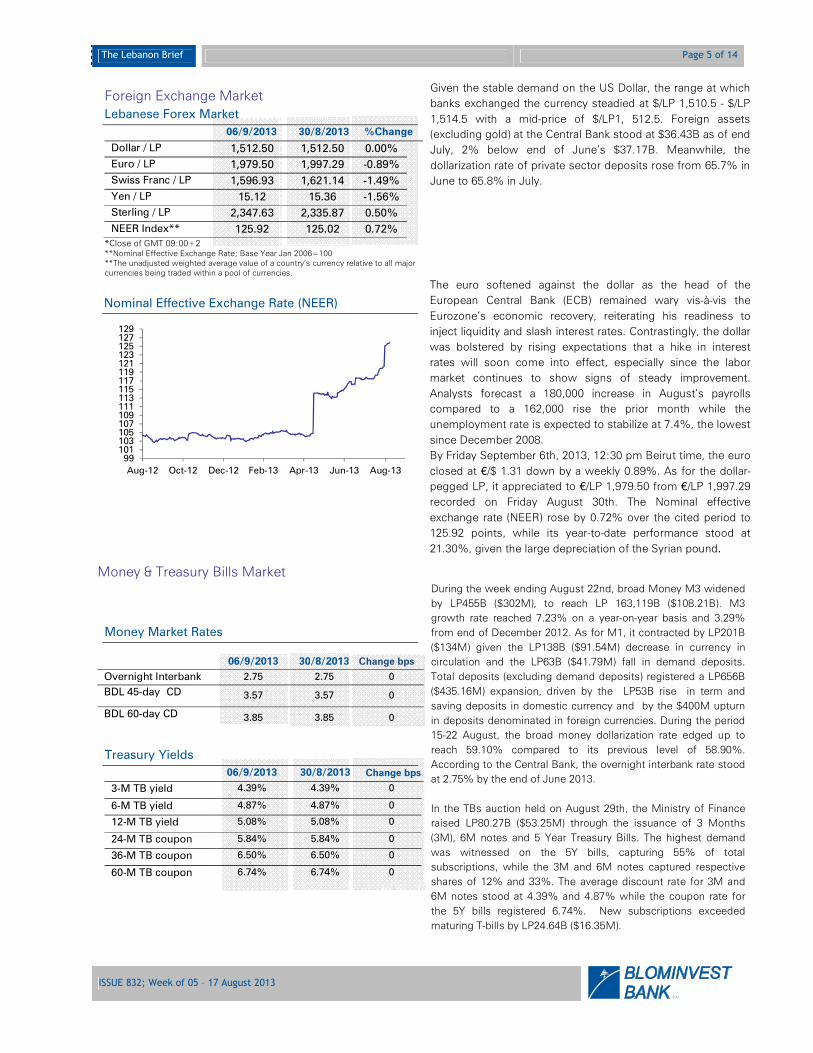

06/9/2013 30/8/2013 %Change

Dollar / LP 1,512.50 1,512.50 0.00%

Euro / LP 1,979.50 1,997.29 -0.89%

Swiss Franc / LP 1,596.93 1,621.14 -1.49%

Yen / LP 15.12 15.36 -1.56%

Sterling / LP 2,347.63 2,335.87 0.50%

NEER Index** 125.92 125.02 0.72% *Close of GMT 09:00+2 **Nominal Effective Exchange Rate; Base Year Jan 2006=100

**The unadjusted weighted average value of a country’s currency relative to all major

currencies being traded within a pool of currencies.

Given the stable demand on the US Dollar, the range at which

banks exchanged the currency steadied at $/LP 1,510.5 - $/LP

1,514.5 with a mid-price of $/LP1, 512.5. Foreign assets

(excluding gold) at the Central Bank stood at $36.43B as of end

July, 2% below end of June’s $37.17B. Meanwhile, the

dollarization rate of private sector deposits rose from 65.7% in

June to 65.8% in July.

Nominal Effective Exchange Rate (NEER)

The euro softened against the dollar as the head of the

European Central Bank (ECB) remained wary vis-à-vis the

Eurozone’s economic recovery, reiterating his readiness to

inject liquidity and slash interest rates. Contrastingly, the dollar

was bolstered by rising expectations that a hike in interest

rates will soon come into effect, especially since the labor

market continues to show signs of steady improvement.

Analysts forecast a 180,000 increase in August’s payrolls

compared to a 162,000 rise the prior month while the

unemployment rate is expected to stabilize at 7.4%, the lowest

since December 2008.

By Friday September 6th, 2013, 12:30 pm Beirut time, the euro

closed at €/$ 1.31 down by a weekly 0.89%. As for the dollar-

pegged LP, it appreciated to €/LP 1,979.50 from €/LP 1,997.29

recorded on Friday August 30th. The Nominal effective

exchange rate (NEER) rose by 0.72% over the cited period to

125.92 points, while its year-to-date performance stood at

21.30%, given the large depreciation of the Syrian pound.

Money & Treasury Bills Market

Money Market Rates

Treasury Yields

06/9/2013 30/8/2013 Change bps

3-M TB yield 4.39% 4.39% 0

6-M TB yield 4.87% 4.87% 0

12-M TB yield 5.08% 5.08% 0

24-M TB coupon 5.84% 5.84% 0

36-M TB coupon 6.50% 6.50% 0

60-M TB coupon 6.74% 6.74% 0

06/9/2013 30/8/2013 Change bps

Overnight Interbank 2.75 2.75 0

BDL 45-day CD 3.57 3.57 0

BDL 60-day CD 3.85 3.85 0

During the week ending August 22nd, broad Money M3 widened

by LP455B ($302M), to reach LP 163,119B ($108.21B). M3

growth rate reached 7.23% on a year-on-year basis and 3.29%

from end of December 2012. As for M1, it contracted by LP201B

($134M) given the LP138B ($91.54M) decrease in currency in

circulation and the LP63B ($41.79M) fall in demand deposits.

Total deposits (excluding demand deposits) registered a LP656B

($435.16M) expansion, driven by the LP53B rise in term and

saving deposits in domestic currency and by the $400M upturn

in deposits denominated in foreign currencies. During the period

15-22 August, the broad money dollarization rate edged up to

reach 59.10% compared to its previous level of 58.90%.

According to the Central Bank, the overnight interbank rate stood

at 2.75% by the end of June 2013.

In the TBs auction held on August 29th, the Ministry of Finance

raised LP80.27B ($53.25M) through the issuance of 3 Months

(3M), 6M notes and 5 Year Treasury Bills. The highest demand

was witnessed on the 5Y bills, capturing 55% of total

subscriptions, while the 3M and 6M notes captured respective

shares of 12% and 33%. The average discount rate for 3M and

6M notes stood at 4.39% and 4.87% while the coupon rate for

the 5Y bills registered 6.74%. New subscriptions exceeded

maturing T-bills by LP24.64B ($16.35M).

99101103105107109111113115117119121123125127129

Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Aug-13

The Lebanon Brief Page 6 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

Eurobond Market

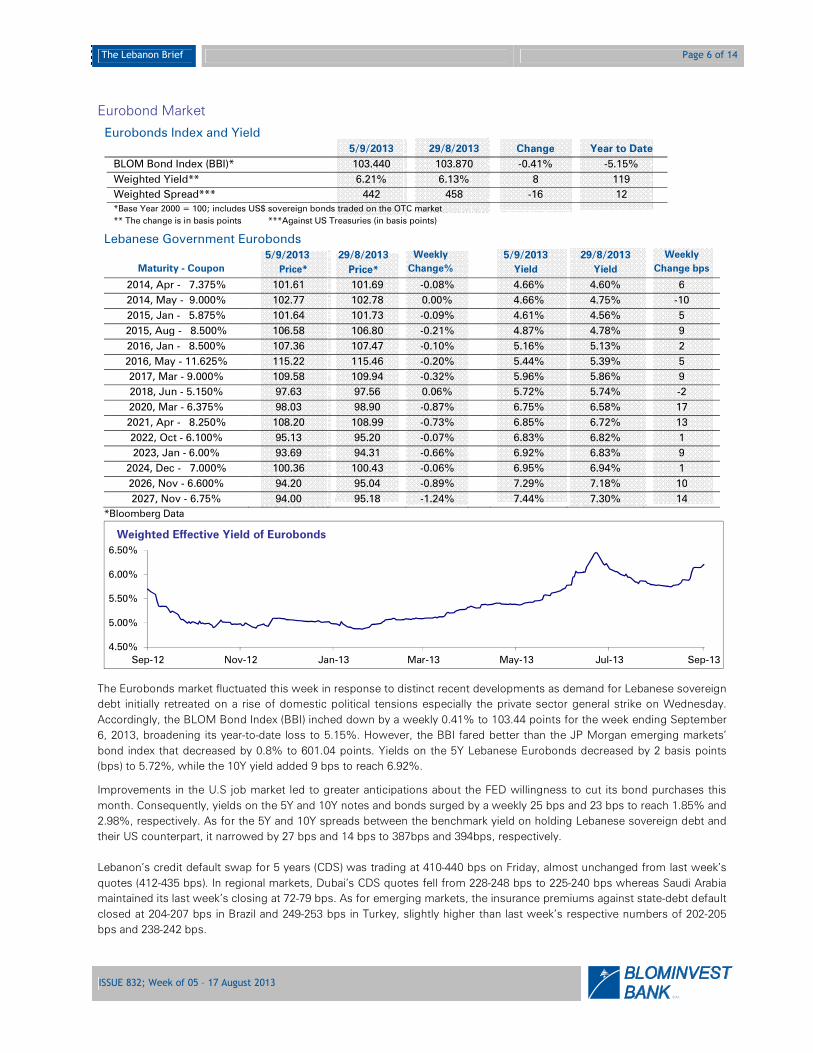

Eurobonds Index and Yield 5/9/2013 29/8/2013 Change Year to Date

BLOM Bond Index (BBI)* 103.440 103.870 -0.41% -5.15%

Weighted Yield** 6.21% 6.13% 8 119

Weighted Spread*** 442 458 -16 12

*Base Year 2000 = 100; includes US$ sovereign bonds traded on the OTC market

** The change is in basis points ***Against US Treasuries (in basis points)

Lebanese Government Eurobonds

Maturity - Coupon

5/9/2013

Price*

29/8/2013

Price*

Weekly

Change%

5/9/2013

Yield

29/8/2013

Yield

Weekly

Change bps

2014, Apr - 7.375% 101.61 101.69 -0.08% 4.66% 4.60% 6

2014, May - 9.000% 102.77 102.78 0.00% 4.66% 4.75% -10

2015, Jan - 5.875% 101.64 101.73 -0.09% 4.61% 4.56% 5

2015, Aug - 8.500% 106.58 106.80 -0.21% 4.87% 4.78% 9

2016, Jan - 8.500% 107.36 107.47 -0.10% 5.16% 5.13% 2

2016, May - 11.625% 115.22 115.46 -0.20% 5.44% 5.39% 5

2017, Mar - 9.000% 109.58 109.94 -0.32% 5.96% 5.86% 9

2018, Jun - 5.150% 97.63 97.56 0.06% 5.72% 5.74% -2

2020, Mar - 6.375% 98.03 98.90 -0.87% 6.75% 6.58% 17

2021, Apr - 8.250% 108.20 108.99 -0.73% 6.85% 6.72% 13

2022, Oct - 6.100% 95.13 95.20 -0.07% 6.83% 6.82% 1

2023, Jan - 6.00% 93.69 94.31 -0.66% 6.92% 6.83% 9

2024, Dec - 7.000% 100.36 100.43 -0.06% 6.95% 6.94% 1

2026, Nov - 6.600% 94.20 95.04 -0.89% 7.29% 7.18% 10

2027, Nov - 6.75% 94.00 95.18 -1.24% 7.44% 7.30% 14

*Bloomberg Data

The Eurobonds market fluctuated this week in response to distinct recent developments as demand for Lebanese sovereign

debt initially retreated on a rise of domestic political tensions especially the private sector general strike on Wednesday.

Accordingly, the BLOM Bond Index (BBI) inched down by a weekly 0.41% to 103.44 points for the week ending September

6, 2013, broadening its year-to-date loss to 5.15%. However, the BBI fared better than the JP Morgan emerging markets’

bond index that decreased by 0.8% to 601.04 points. Yields on the 5Y Lebanese Eurobonds decreased by 2 basis points

(bps) to 5.72%, while the 10Y yield added 9 bps to reach 6.92%.

Improvements in the U.S job market led to greater anticipations about the FED willingness to cut its bond purchases this

month. Consequently, yields on the 5Y and 10Y notes and bonds surged by a weekly 25 bps and 23 bps to reach 1.85% and

2.98%, respectively. As for the 5Y and 10Y spreads between the benchmark yield on holding Lebanese sovereign debt and

their US counterpart, it narrowed by 27 bps and 14 bps to 387bps and 394bps, respectively.

Lebanon’s credit default swap for 5 years (CDS) was trading at 410-440 bps on Friday, almost unchanged from last week’s

quotes (412-435 bps). In regional markets, Dubai’s CDS quotes fell from 228-248 bps to 225-240 bps whereas Saudi Arabia

maintained its last week’s closing at 72-79 bps. As for emerging markets, the insurance premiums against state-debt default

closed at 204-207 bps in Brazil and 249-253 bps in Turkey, slightly higher than last week’s respective numbers of 202-205

bps and 238-242 bps.

4.50%

5.00%

5.50%

6.00%

6.50%

Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13

Weighted Effective Yield of Eurobonds

The Lebanon Brief Page 7 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

EEEECONOMIC AND FINANCIAL NEWS CONOMIC AND FINANCIAL NEWS CONOMIC AND FINANCIAL NEWS CONOMIC AND FINANCIAL NEWS

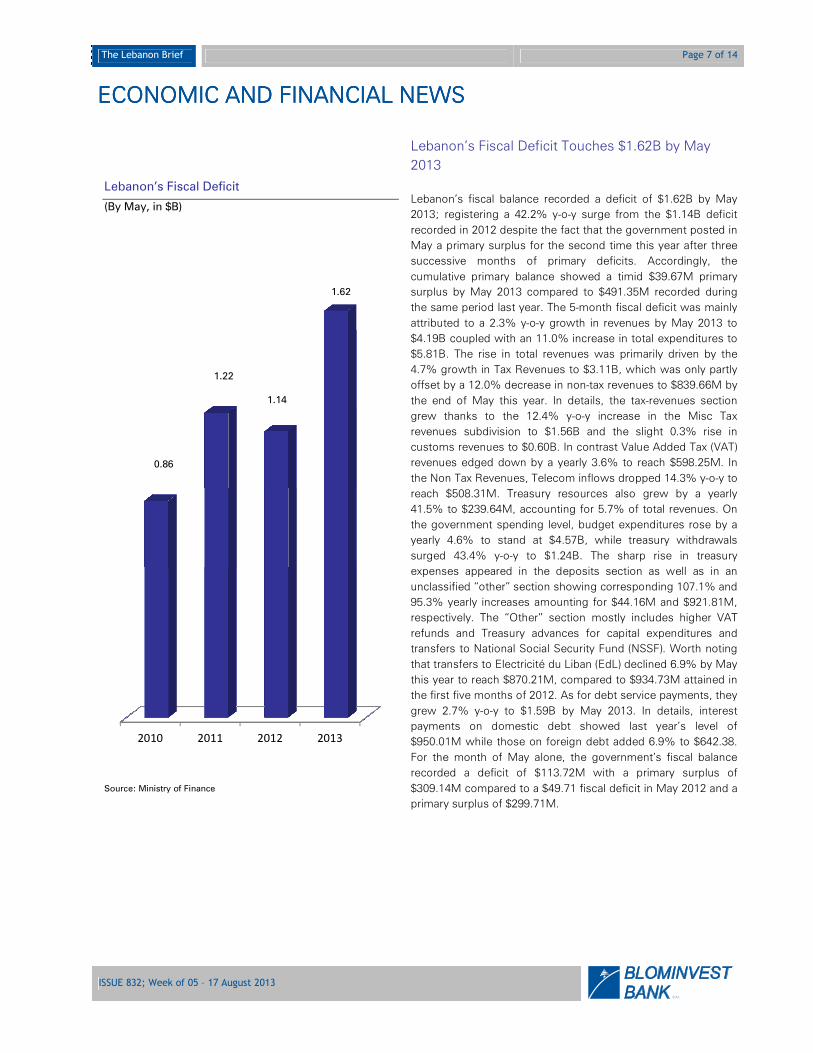

Lebanon’s Fiscal Deficit

(By May, in $B)

Source: Ministry of Finance

Lebanon’s Fiscal Deficit Touches $1.62B by May

2013

Lebanon’s fiscal balance recorded a deficit of $1.62B by May

2013; registering a 42.2% y-o-y surge from the $1.14B deficit

recorded in 2012 despite the fact that the government posted in

May a primary surplus for the second time this year after three

successive months of primary deficits. Accordingly, the

cumulative primary balance showed a timid $39.67M primary

surplus by May 2013 compared to $491.35M recorded during

the same period last year. The 5-month fiscal deficit was mainly

attributed to a 2.3% y-o-y growth in revenues by May 2013 to

$4.19B coupled with an 11.0% increase in total expenditures to

$5.81B. The rise in total revenues was primarily driven by the

4.7% growth in Tax Revenues to $3.11B, which was only partly

offset by a 12.0% decrease in non-tax revenues to $839.66M by

the end of May this year. In details, the tax-revenues section

grew thanks to the 12.4% y-o-y increase in the Misc Tax

revenues subdivision to $1.56B and the slight 0.3% rise in

customs revenues to $0.60B. In contrast Value Added Tax (VAT)

revenues edged down by a yearly 3.6% to reach $598.25M. In

the Non Tax Revenues, Telecom inflows dropped 14.3% y-o-y to

reach $508.31M. Treasury resources also grew by a yearly

41.5% to $239.64M, accounting for 5.7% of total revenues. On

the government spending level, budget expenditures rose by a

yearly 4.6% to stand at $4.57B, while treasury withdrawals

surged 43.4% y-o-y to $1.24B. The sharp rise in treasury

expenses appeared in the deposits section as well as in an

unclassified “other” section showing corresponding 107.1% and

95.3% yearly increases amounting for $44.16M and $921.81M,

respectively. The “Other” section mostly includes higher VAT

refunds and Treasury advances for capital expenditures and

transfers to National Social Security Fund (NSSF). Worth noting

that transfers to Electricité du Liban (EdL) declined 6.9% by May

this year to reach $870.21M, compared to $934.73M attained in

the first five months of 2012. As for debt service payments, they

grew 2.7% y-o-y to $1.59B by May 2013. In details, interest

payments on domestic debt showed last year’s level of

$950.01M while those on foreign debt added 6.9% to $642.38.

For the month of May alone, the government’s fiscal balance

recorded a deficit of $113.72M with a primary surplus of

$309.14M compared to a $49.71 fiscal deficit in May 2012 and a

primary surplus of $299.71M.

2010 2011 2012 2013

0.86

1.22

1.14

1.62

The Lebanon Brief Page 8 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

Total Consolidated Assets of Commercial Banks

(By July, in $B)

Source: Banque du Liban

MENA Sovereign Risk Rating Scores- Q3 2013

Country Total Score

Oman 88

Qatar 86

UAE 85

Israel 76

Algeria 69

Bahrain 65

Iraq 65

Morocco 50

Jordan 46

Lebanon 38

Tunisia 38

Egypt 36

Commercial Banks Consolidated Total Assets Grew

to $157.81B in July

Commercial banks’ total consolidated assets amounted to

$157.81B by July, equivalent to an 8.5% y-o-y growth. On a year-

to-date basis, total assets grew by 3.9%, slightly faster than

3.5% recorded in the same period last year. The upturn in total

assets is accredited to the respective 5% and 6% y-t-d growths

of claims on the resident private sector and the public sector to

$39.77B and $32.88B. By July, commercial banks’ holdings of

LBP denominated treasury bills (T-bills) stood at $17.16B, higher

than $15.62B for foreign-currency denominated T-bills.

However, the latter grew by 19.4% since year-start compared to

a 4.6% slip in the former, showing banks’ preference towards

holding Eurobonds in their lending portfolio. Meanwhile, foreign

assets continued their downward trend, slipping by 2.9% to

$25.41B by July. In detail, claims on the non-resident private

and financial sectors were scaled down by 3.7% and 4.9% to

$5.40B and $13.69B, respectively. In fact, lower non-resident

lending is linked to further instability in several MENA countries.

On the liabilities side, resident private sector deposits edged up

by 3% since year start to $104.1B, as deposits in foreign

currencies rose by 4% to $62.53B and as those in local currency

inched up by 2% to $41.58B. As for non-resident private sector

deposits, they continue to grow significantly, advancing by 12%

y-t-d to $27.08B, especially as heightened security tensions in

neighboring countries generates hefty capital outflows. The

dollarization rate of private sector deposits went from 65.7% in

June to 65.8% in July.

BMI: Lebanon’s Sovereign Risk Rating Score slips to

38/100

Business Monitor International (BMI)’s average Sovereign Risk

Rating (SRR) score for 12 MENA countries (excluding Syria)

steadied at 62/100 in Q3 2013. However, the report warns that

this broad figure fails to portray the widening gap between

gas/oil rich countries of the Gulf and net oil importers in North

Africa and the Levant region. In this light, and compared to the

previous quarter, the average SRR for the four rated Gulf States

rose by one point to 81 in parallel to a frail 47 for the six-rated oil

importers, a 2 points drop. In details, Lebanon’s SRR lost 2

points to 38 in Q3 2013 as BMI forecasts that no major policy

initiatives will see the light of day amidst the Syrian-imported

violence. Moreover, with public debt being one of the highest in

the world and with the primary budget sliding into deficit for the

first time in six years, future external shocks are likely to weigh

on Lebanon’s external position. On a comparative note,

Lebanon, Tunisia and Egypt were the bottom three with

respective scores of 38, 38 and 36. Contrastingly, Oman, Qatar

and UAE were the top rankers, with respective scores of 88, 86

and 85.

105.39

124.05

136.88

145.51

157.81

2009 2010 2011 2012 2013

The Lebanon Brief Page 9 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

Source: Ministry of Tourism

Lebanon’s trade deficit

(Up to July, in $B)

Source: Jones Lang LaSalle

Trade Deficit Increases to $9.92B up to July 2013

The Lebanese trade deficit widened by 6.3% up to July 2013 to

reach $9.92B compared to $9.33B in the same period last year.

When annualized, the trade deficit to GDP ratio amplified from

37.9% in 2012 to 39.4% in 2013. This increase in deficit is due

to a 5.87% upturn in imports to $12.51B which outpaced the

4.26% rise in exports to $2.59B. The rise in imports does not

indicate a boost in domestic demand but is rather linked to the

heavy influx of Syrian refugees into the country. Mineral

products represented 24.5% of total imports as Machinery and

Electrical Instruments followed suit with a share of 12.37%. The

latter increased by 27% to $1.55B while the former rose by 4%

to $3.05B. China holds 9% of overall imports followed by 8% for

Italy and the USA and 7% for France. As for exports, Pearls,

Precious stones and metals, the largest with a share of 22% of

the total, plummeted by 40% year-on-year to reach $578.76M.

Exports of mineral products and base metals came in second

with the same share of 13%. Exports of mineral products

surged from $31.45M up to July 2012 to $325.445M up to July

2013 while those of base metals increased by 41% to

$347.28M. Syria still holds the largest portion of Lebanese

exports with 16% of total exports, followed by South Africa with

12%. Transit revenues rose by 36% to reach $266.45M up to

July compared to $196.318M for the same period in 2012. In

July alone, the trade deficit reached $1.44B given the 4.97%

monthly rise in imports to $1.72B and the 19.5% slump in

exports to $279.98M.

8.028.37

9.339.92

10.4310.91

11.8212.51

2.41 2.53 2.49 2.59

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2010 2011 2012 2013

Trade Deficit Imports Exports

The Lebanon Brief Page 10 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

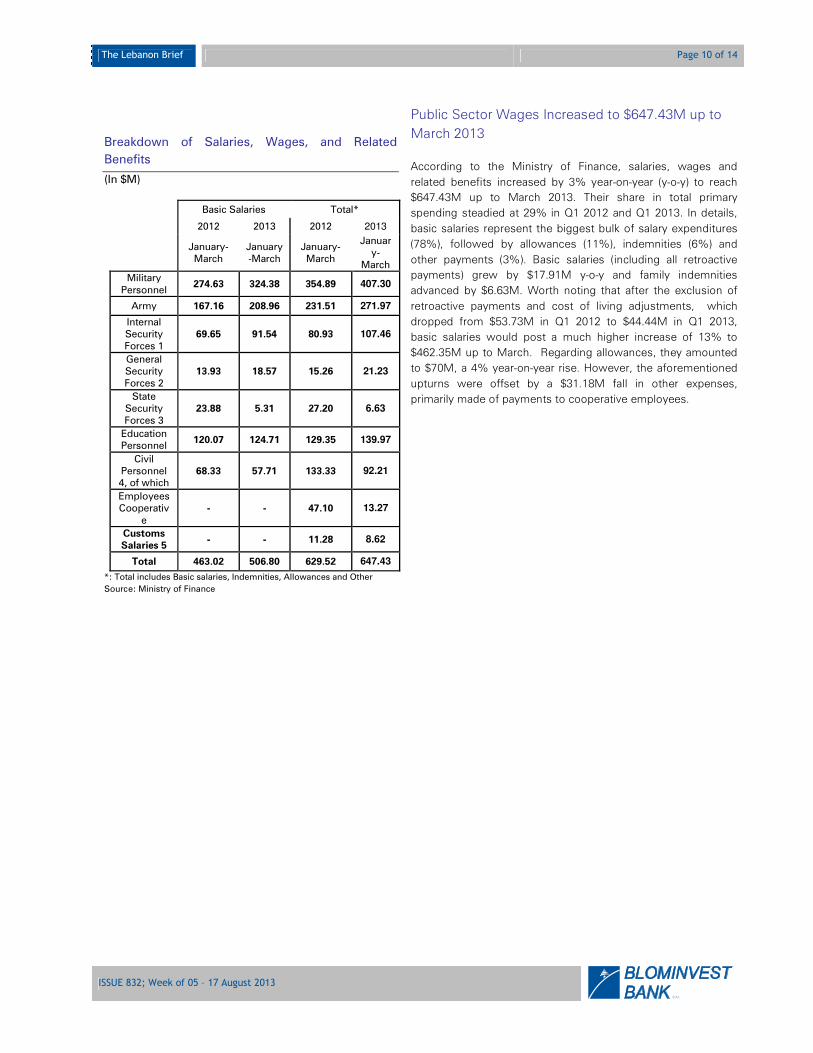

Breakdown of Salaries, Wages, and Related

Benefits

(In $M)

Basic Salaries Total*

2012 2013 2012 2013

January-March

January-March

January-March

January-

March

Military Personnel

274.63 324.38 354.89 407.30

Army 167.16 208.96 231.51 271.97

Internal Security Forces 1

69.65 91.54 80.93 107.46

General Security Forces 2

13.93 18.57 15.26 21.23

State Security Forces 3

23.88 5.31 27.20 6.63

Education Personnel

120.07 124.71 129.35 139.97

Civil Personnel 4, of which

68.33 57.71 133.33 92.21

Employees Cooperativ

e - - 47.10 13.27

Customs

Salaries 5 - - 11.28 8.62

Total 463.02 506.80 629.52 647.43

*: Total includes Basic salaries, Indemnities, Allowances and Other

Source: Ministry of Finance

Public Sector Wages Increased to $647.43M up to

March 2013

According to the Ministry of Finance, salaries, wages and

related benefits increased by 3% year-on-year (y-o-y) to reach

$647.43M up to March 2013. Their share in total primary

spending steadied at 29% in Q1 2012 and Q1 2013. In details,

basic salaries represent the biggest bulk of salary expenditures

(78%), followed by allowances (11%), indemnities (6%) and

other payments (3%). Basic salaries (including all retroactive

payments) grew by $17.91M y-o-y and family indemnities

advanced by $6.63M. Worth noting that after the exclusion of

retroactive payments and cost of living adjustments, which

dropped from $53.73M in Q1 2012 to $44.44M in Q1 2013,

basic salaries would post a much higher increase of 13% to

$462.35M up to March. Regarding allowances, they amounted

to $70M, a 4% year-on-year rise. However, the aforementioned

upturns were offset by a $31.18M fall in other expenses,

primarily made of payments to cooperative employees.

The Lebanon Brief Page 11 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

CCCCORPORATEORPORATEORPORATEORPORATE DEVELOPMENTSDEVELOPMENTSDEVELOPMENTSDEVELOPMENTS

Performance of BLC’s Listed Shares

SOURCE: Beirut Stock Exchange, BlomInvest

BLC Bank Lists New Preferred “C” shares

BLC Bank, part of Fransabank Group, recently announced a

capital increase of $35M through the listing of 350,000 BLC

Preferred C shares on the Beirut Stock Exchange (BSE), with a

subscription price of $100/share. Each Preferred C share

generates dividends worth 6.75% of 2013’s profits and shall be

disbursed in 2014. The newly listed shares started trading as of

Monday 2 September. Prior to the new addition, BLC had two

classes of listed preferred shares: A and B. The number of A

shares totaled 400,000 while that of B shares stood at 550,000.

BLC has over 51M listed shares and above 100M non-listed

shares.

$1.70

$1.75

$1.80

$1.85

$1.90

$1.95

$2.00

The Lebanon Brief Page 12 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

FFFFOCUS IN BRIEFOCUS IN BRIEFOCUS IN BRIEFOCUS IN BRIEF

New Angel Investors for Tech Startups: the Lebanese Banks

Value Added of Information &Technology to GDP, 2012

Source: world Bank data

Main Challenges for Private Equity Investments

Source: Survey by Zawya focusing on General Partners in the MENA

region, during Q1 of 2013

Amidst tighter economic conditions, an innovative financial service consented by the BdL introduced a new financing option

to the Lebanese startups. A new Circular (#331, available on BdL’s website) licensed the stepping in of banks to finance

startups, venture capital firms, incubators and accelerators working in the knowledge economy, not through the usual debt,

but this time through equity.

In essence, the move complements past initiatives to subsidize companies working in various economic sectors, and aims

at boosting the economic cycle through domestic lending and job creation. Meanwhile the unconventional part allowing

equity investment in startups builds on further market characteristics.

Tech startup firms are especially appreciated for their job creation benefits and resilience to the economic downturns when

fixed jobs are less available and entrepreneurship becomes more tempting. Yet, they are the ones facing most difficulties

when it comes to financing. Their current options were limited to private equity and some products of Islamic banking,

while the commercial banks were only involved through debt offering, provided that it is guaranteed by Kafalat and only for

a ceiling of $400k per company.

The BdL’s move thus reshuffled some of the financing options for both banks and startups. Building on the continuous

growth of bank deposits which advanced at an annual pace of 10% by July, much faster than the economy’s growth,

Lebanese banks preserved the best position to provide capital for the private sector, as the BdL governor puts it. On the

other hand, their lending portfolio to the private sector reached around $39.7 billion, almost 94% of the country’s GDP,

representing a high leverage ratio for companies and limiting the growth of debt-driven investments capabilities, hence the

benefits of switching to equity.

But does the circular offer enough incentives for banks to make use of it? A review of its clauses and conditions reveal

interesting opportunities, and quite some challenges.

The circular allows investments up to 7 years in startup companies, incubators, accelerators and venture capital firms

working in the knowledge economy field, as long as they are a Lebanese joint stock company and not working offshore.

36%

30%

30%

29%

20%

20%

Egypt

Tunisia

Morocco

Jordan

Lebanon

UnitedStates

21%

14%

14%

10%

9%

8%

8%

7%

7%

2%

Quality of deal flow

Corporate governance

High valuations

Human capital

Acceptance of PE funds as…

Market Regulations

Growth prospects

Lack of control over deals

Lack of bank financing

Lack of intermediary

The Lebanon Brief Page 13 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

The returns are tempting. The circular stipulates that BdL will finance 75% of the bank’s investment in these firms. Banks

would receive zero-interest loans from BdL, and invest them in treasury bills. The invested loans will be calculated in a way

to generate interest equivalent to 75% of the bank’s participation in the firm, therefore limiting the banks’ exposure to 25%.

Total investable amounts in these firms are also limited. Only 3% of the bank’s capital can be used, out of which a

maximum of 10% is allowed in a single company. To put this into perspective, the largest banks such as BLOM and Audi

can individually invest up to $50 million and $66 million in the field, respectively, and given the offered hedge from BdL, the

direct exposure won’t exceed $12.5 million for BLOM and $16 million for Audi. Investments in a single company would also

be limited to $5million from BLOM and $6.6 million from Audi. Whilst this is minimal on a large bank’s balance sheets, it is

very advantageous for firms, as most current investments are concentrated below the $2 million bar.

For reference, Lebanese Business Angels and Cedrus Ventures offer to finance companies with a budget going from $50k

to $500k. Venture capital funds like Berytech’s and Middle East Venture Fund invest up to $2 million, and only the

International Finance Corporation (IFC) and Riyada Enterprise Development (RED) participate with more than $2 million.

Now, and as a result of the new circular, the Lebanese banks would make around $385 million available to fund startups in

the knowledge economy.

The 10% rule also highlights the need for diversification and entails investment in 10 different companies. The reason is that

despite their unlimited upside potential, startup companies have a low survivorship rate of around 20% during the first 3

years. In this area, incubators and accelerators play a significant role as they increase the chances of hosting successful

companies. For instance, Seeqnce reported that 10 of 22 of their graduated tenants are fully active.

The offered hedge by BdL against the banks’ investments therefore looks appealing. Some aspects remain to be cleared

though. One is the method that will be used to calculate the interests to be received by banks, or more accurately whether

the bank’s initial investment would be matched by interests based on its present or future value. Another question for banks

would be the risk-weighted assets required for such investments. Basel II stipulates a risk weighted allocation of 100% for

exposures to equity investments, while Basel III can go up to 400% for exposures to not publicly traded equity investments

and 600% for certain investment funds.

But aside from the risks and returns, many challenges await the implementation of this circular.

Certainly, the regular channels of commercial banks’ credit are not best suited to advise on equity financing opportunities,

but most of the Lebanese banks have an investment arm and are not short of skilled investment teams. Many banks are

also already indirectly engaged in the private equity world. Blominvest bank, alongside 5 other banks1, holds a share in the

Building Block Equity Fund which has a capital of $7.3 million and is managed by Middle East Venture Partners (MEVP). The

fund had made successful investments in 3 companies (shahiya.com, shawarmanji and cedar books). Audi Saradar

investment bank is also a partner in Berytech. The question remains whether banks’ participations in these funds and firms

would benefit from BdL’s facilities, given that the majority are not limited to tech companies and many have the legal form

of a limited partnership or registered offshore.

The circular also notes an active role for banks in the development of the firm’s business, which might be of concern to

both banks and startups. The screening and selection of successful startups is an enormous effort and the continuous

counseling and follow up require a mobilization of dedicated teams. To note the difficulty of having companies in the

pipeline, it suffices to see that many of the funds’ available capital are still not allocated. Incubators and accelerators remain

the first place where investment funds look as they have developed considerable experience in screening companies and

fostering their development. Berytech, the pioneer incubator in Lebanon graduated over 60 tenants during the past decade.

In this context, banks might opt for investments in funds at the expense of direct investing in companies if they represent

less of a hassle.

In all cases, the potential remains huge, especially for technology and information startups. Software and online products

and solutions can reach a huge consumer base and need not be capital intensive. The MENA region alone has a population

of over 350 million people, a third of which are under the age of 15, eager for connectivity and smart devices. Some of the

1 Fransabank, Bank Audi, BankMed, BLF, Crédit Libanais

The Lebanon Brief Page 14 of 14

ISSUE 832; Week of 05 – 17 August 2013

S A L

MENA countries also rank well on the list of highest GDP/Capita in the world. In Lebanon, around 1 million are subscribed to

3G services and around 2.6 million use internet through their fixed lines. The penetration rate for mobiles is also projected

to exceed the current 93% as Lebanon remains one of the few countries with a less than 100% rate.

Private equity remains subdued in the MENA region, with total investments representing 0.05% of its GDP in 2012, well

below the US’ 0.86% and the UK’s 1.05%. However information and technology gained special focus earning it the largest

share of 40% of the total investment volume made in the MENA region (excluding Israel) during 2012. This is one sector

where a small population is not an impediment. The 7million+ population of Israel recorded around 3,500 startups solely

focused on tech during 2012. Its dubbed “Silicon Wadi” is the second largest concentration of high tech industries after US’

“Silicon Valley”.

With low liquidity needs, high expected returns and a hedged risk, funding the tech startups though equity represents a

worthy opportunity. The legendary entrepreneurial spirit of the Lebanese might find more reasons to hold on to the country

and help pull the economy out of stagnation and debt. Certainly, the accompanying infrastructure and mechanics need to

follow, but it is still a milestone that was achieved by the Central bank and to be followed by the financial sector, hoping it

will encourage talent to uncover and multiply.

The Lebanon Brief

Page 15 of 14

Your Investment Reference

S A L

Research Department:

Riwa Daou [email protected]

Mirna Chami [email protected]

Maya Mantach [email protected]

Marwan Mikhael [email protected]