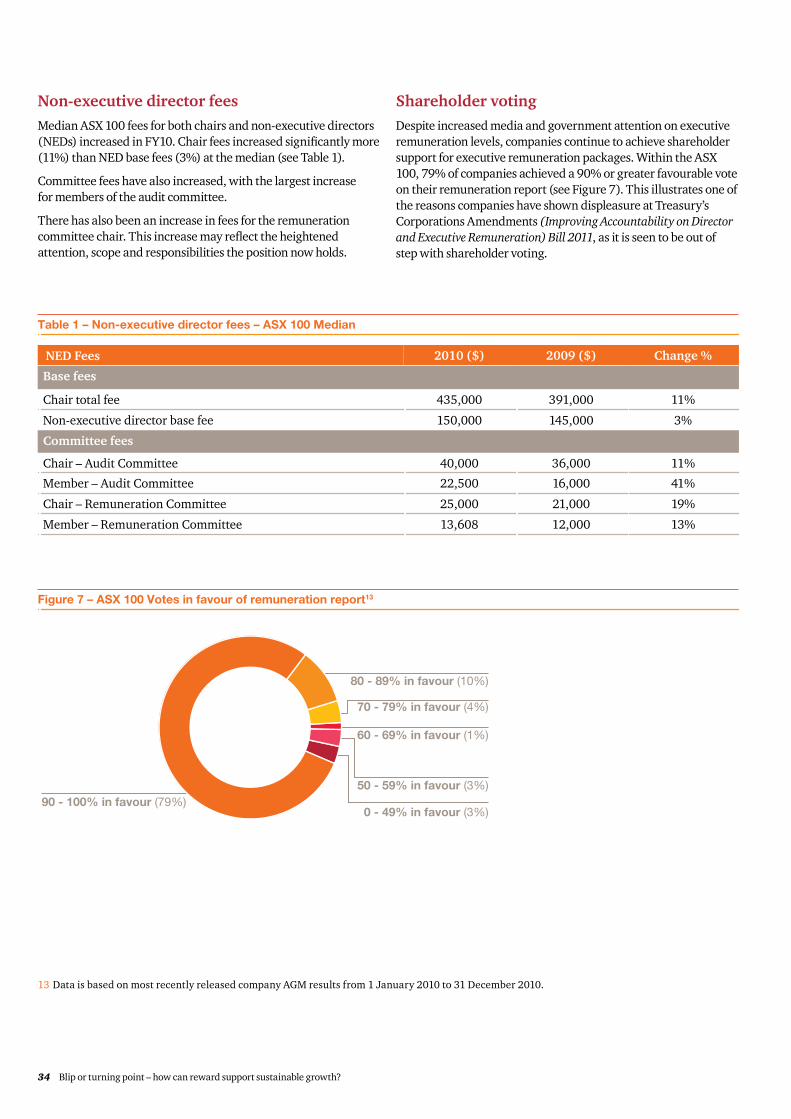

Embed Size (px)

Citation preview

Blip or turning point –How can reward support sustainable growth?

pwc.com.au

March 2011

Consulting

What would you like to grow?

Executive RemunerationFifth edition

Contents

Introduction03

Executive summary

04Breaking the mould – making it work in the real world

06

The impact of APRA regulation within and outside financial services

26How can we make remuneration changes stick?

19Can remuneration frameworks be sustainable in times of change?

13

ASX 100 remuneration in FY10

30Methodology35

Changes to remuneration regulations in 2010

36

PwC | Blip or turning pointHow can reward support sustainable growth?Fifth edition – March 2011

Debra Eckersley Partner

+61 (2) 8266 9034 [email protected]

Della Conroy Partner

+61 (3) 8603 2999 [email protected]

2010 was again a year of intense scrutiny for executive remuneration. Legislative and regulatory changes that aim to rein in executive remuneration were proposed in response to community and media concerns. Australian boards are now focused on planning for the impact of the new duties and obligations.

While these legislative and regulatory changes will likely bring a new set of challenges, companies that adopt a best practice approach to remuneration will be in the greatest possible position to deliver sustainable value for their shareholders, and will also find themselves in compliance.

We strongly believe remuneration structures must be designed to suit the needs of individual businesses. However, some elements are common to all robust and effective remuneration structures – alignment with business strategy, a strong link between performance and remuneration and proactive shareholder engagement.

This year, our publication provides a perspective on sustainable remuneration models in times of change, as we look beyond regulation and remain focused on the right structure for each business. The challenge over the coming years will be to embed remuneration models that endure and adapt to changing economic, market and regulatory pressures.

Welcome to PwC’s fifth annual Executive Remuneration Report

Executive summary

How can reward support sustainable growth?

Our view

Find the remuneration framework that supports your core business strategy.

Last year, we shared our ideas on new remuneration models. You told us ‘simplicity’ and the ability to address ‘long-standing performance measurement issues’ were of greatest interest. In the move from the theoretical to the real world, we suggest companies do the following: • Consider theoretical versus practical issues: does the need for simplicity of a design override

the tricky practical issues faced?• Treat any fundamental change to your remuneration model as a business

transformation change.• Be clear about the benefits of change and be transparent with shareholders, participants and

governance bodies.

Proactively develop a remuneration framework that will stand the test of time. Periodically assess ongoing relevance.

Incorporate key elements: • Affirm a remuneration strategy that speaks to the heart of your business goals. • Agree remuneration principles to allow enhancements to be applied consistently over time.• Ensure incentive awards correlate with corporate performance.• Align performance measures with actual executive or employee focus.• Conduct scenario modelling to highlight individual and organisational impacts in various

performance scenarios.• Communicate proactively and openly with shareholders.

Be confident your remuneration framework can adapt with market shifts and management changes.

Change is a certainty. A remuneration framework that is aligned with performance through good and bad outcomes will appropriately reward executive talent. We suggest you: • Understand the external trends that may challenge your remuneration framework. • Ensure all stakeholders have a good understanding of your remuneration framework

through clear and constant communication.

4 Blip or turning point – how can reward support sustainable growth?

How can reward support sustainable growth?

Our view

Make remuneration changes stick. Be disciplined in applying key success factors throughout the change process.

Remuneration can be a powerful tool for reinforcing a company’s strategy and should be used to its full potential. We believe there are 10 key factors underpinning successful and enduring remuneration change: Best-fit change approach

1. Design the best-fit change approach – don’t just tailor an earlier approach.Benefits

2. Keep business benefits at the heart of the change.3. Challenge the data and its interpretation.4. Agree the measures of success and how to monitor them.5. Focus on actions that make a difference fast.Involvement

6. Through involvement, build a vision and hunger for success.7. Engage the front line before, during and after.8. Communicate with a purpose.Sustainability

9. Give leaders the skills – and the heart – to lead.10. Make sure systems, processes and culture reinforce the change.

Use a response to regulation as an opportunity to enhance the effectiveness of your remuneration arrangements.

Recent responses to the Australian Prudential Regulation Authority’s (APRA) revised regulation have resulted in positive changes to remuneration structures. We expect that companies outside of APRA regulation will also begin to incorporate these learnings. Some of the changes we have seen to date are:• an increase in the use of deferral or greater levels of deferral of STI• recognition of the importance of behaviour as well as outcomes in variable pay plans;

‘how’ the company achieves its objectives, not just ‘what’ it achieves• greater interaction between the remuneration committee and management in determining

reward structures• greater board accountability, leading to boards seeking their own external remuneration advice.

Understand how changes to the remuneration framework can impact your ability to attract and retain talent.

• Changes in STI deferral, for example, as a result of APRA regulation, can be seen as ‘tweaking around the edges’, as opposed to a fundamental change. However, they can have a very real impact on attraction and retention, as key talent will not necessarily stay within the (regulated) financial services sector if deferral arrangements become too far out of line with non-regulated sectors.

Reinforce desired behaviour through incentive awards that reflect performance.

• STI payouts increased in FY10 to reflect an improvement in reported corporate performance. Approximately half of the ASX 100 companies that awarded STIs did so at or above target opportunity. The increase in STIs awarded also contributed to an increase in total remuneration levels compared to FY09.

• We expect shareholders to become more interested in the rationale behind STI plans and payouts. As a result, clear communication on the performance measures used in STI schemes will become increasingly important.

PwC 5

There are commonly expressed views in the market that incentives are too prescriptive, that they provide a tenuous link between remuneration and performance, and as a result they do not drive performance, change behaviour or retain executives.

Despite this strong and consistent perception that the model is broken, we are yet to see material changes across the market. What we are seeing, on the other hand, is a continual ‘tweaking around the edges’, rather than any fundamental shift in the structure of the remuneration model.

Proposed legislative changes aimed at reining in excessive executive remuneration pose a risk that executive pay will become a question of compliance and convergence of design and practice into a ‘one-size-fits-all remuneration structure’.

This is not where we want to be. As the Productivity Commission noted in its review of executive remuneration, “… the way forward is not to by-pass the central role of Boards in remuneration-setting through prescriptive regulatory measures…”

In trying to address and respond to the regulatory reforms, we risk taking our eye off the main game – how can reward align to our business strategy and support sustainable growth?

So, if you could start with a clean sheet of paper what would your remuneration model look like? Clearly designing and implementing incentive plans is not simple. Selecting metrics that are within an executive’s control, are acceptable to external stakeholders and support the business strategy is a balancing act. And even if the stars align and you manage to satisfy these criteria, markets might collapse, regulations could change, commodity prices soar – and your plan could end up rewarding when underlying performance is poor or not paying out despite great performance.

Given this conundrum, what types of plans would mitigate these issues? And how would they actually work in the real world?

Last year, we presented four alternate remuneration models. Two attracted the most interest from our clients – the Simplified framework (Model A) and the Multi-year incentive plan (Model D). The Simplified framework (Model A) won favour for its simplicity, while the Multi-year incentive plan (Model D) was seen to address long-standing issues on forecasting targets.

Figure 1 – Simplified framework (Model A)

Current year

+1 +2 +3 +4 +5

FixedCash

FixedShares

Performance measurement

FixedCash

LTI

STI

$3m

$0

Traditionalremuneration

Cur

rent

year

Ves

ting

Model A

Breaking the mould – making it work in the real worldA customised remuneration model could improve the alignment between executive motivation, reward and business performance.

Simplified framework – Model A

Key features1

• Two components – Fixed cash and fixed shares (restricted shares with no performance conditions).

• Increase in guaranteed pay (fixed cash and fixed shares) to account for reduced upside.

• Removal of annual cash bonus.• Share price acts as key performance measure.• Potentially less emphasis on performance management in

determining remuneration.• Restricted shares and strict shareholding guidelines encourage

strong alignment to company performance over the long term.

1 For the purposes of this example a five year vesting period has been used. The length of this period could vary depending on an organisation’s specific circumstances.

6 Blip or turning point – how can reward support sustainable growth?

So, given the interest in these new models, why are we not seeing companies rushing to break the mould? If we take the Simplified framework (Model A) as an example, many are attracted to its simplicity, yet may be put off by the considerable organisational change that would be required to implement it in practice. Some of the changes required to adopt the Simplified framework (Model A) are set out in Table 1.

Given these challenges, it is not surprising that, today, the appetite to move to the Simplified framework (Model A) is low.

2 For the purposes of this example a three year vesting period has been used. The length of this period could vary depending on an organisation’s specific circumstances.

Figure 2 – Multi-year incentive plan (Model D)

Current year

+1 +2 +3 +4 +5

FixedCash

VariableShares

VariableCash

Performance measurement

Fixed

Cu

rren

tye

ar

Cash

LTI

STI

Vesting & clawback

$3m

$0

Traditionalremuneration

Model D

Current remuneration element What will need to change to make the Simplified framework effective

Annual grant of LTIs • Acknowledge the impact the removal of an annual LTI grant may have on some individuals (eg associated with seniority/status) and address this in communications.

• Communicate that the lower leverage opportunity is a trade off for more certainty.

Annual STI opportunity • Develop new ways other than STI to communicate strategic priority areas to management each year, and how success will be measured.

• Consider new ways of ensuring performance outcomes are understood and the desired level of performance differentiation at the individual level is achieved.

Performance management system • Review performance management frameworks and processes to ensure individual performance and development needs are sufficiently reinforced through channels other than remuneration.

• Consider the impact on employees below the executive level who may have less influence on share price growth or organisational performance.

Consistency with other organisations

• Incorporate changes to the remuneration model into the ‘reward deal’ used to attract and retain employees. Consider the changes in the context of the wider employee value proposition.

• Persuade investors of the value of this new model over more traditional approaches.

Multi-year incentive plan (single plan) – Model D

Key features2

• One total incentive plan, replacing short and long-term plans.

• Annual assessment of performance against a balanced scorecard, looking back three years.

• Award is made partly in cash, and deferred shares to vest over years one, two and three.

• Increased transparency for executives.

• Balances performance across a number of measures.

• Six-year total performance measurement timeframe.

• Provides the opportunity for clawback in future years.

Table 1 – Challenges associated with the Simplified framework (Model A)

PwC 7

Phased payment mechanism subject to forfeiturePerformance measurement

Balanced scorecard of KPIs

• Group performance

(may include use of Total Shareholder

Return measures)

• People

• Safety

• Individual performance

• Cash and shares

• Cash paid immediately, shares vest over 1-3 years

• Shares subject to forfeiture if any of the

following occurs:

Multi-year IncentiveDetermination and Award

- 2 years - 1 year Current year + 1 year + 2 years + 3 years

Award

– employment ceases before relevant share vest date

– material misstatement of accounts

– major reputational event linked to issues which arose

during the performance measurement period

4 to 6 year total performance measurement timeframe

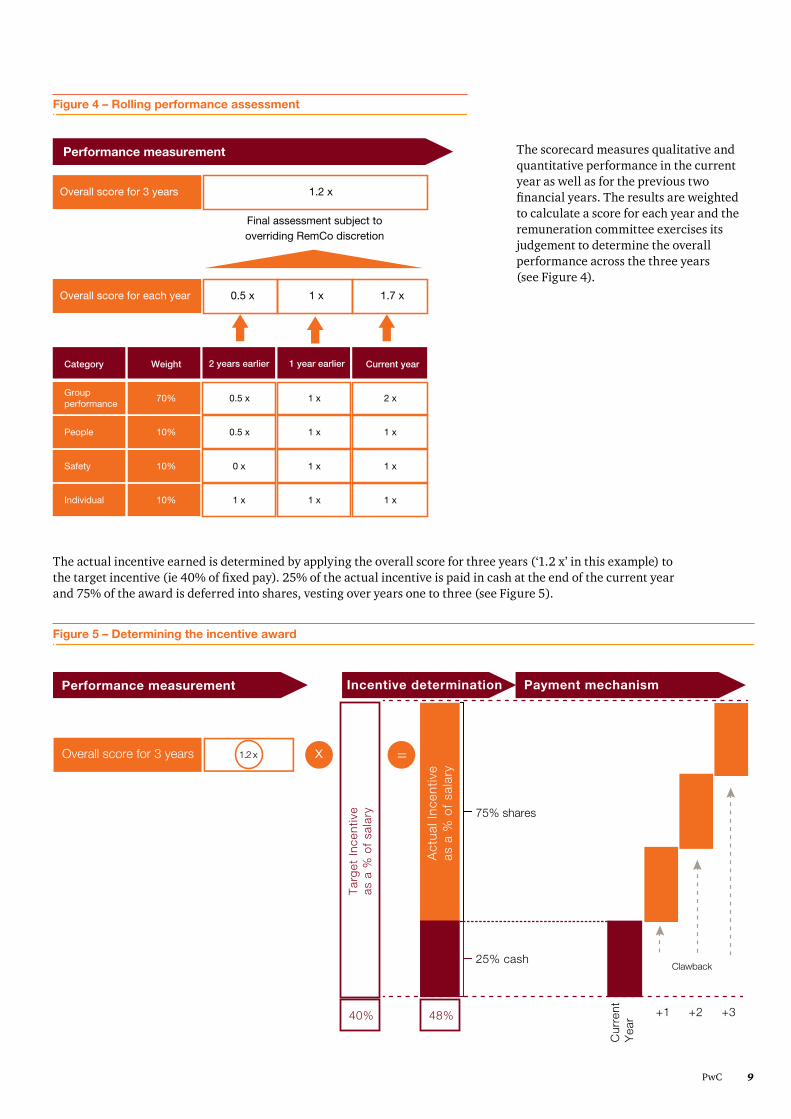

Figure 3 – How the Multi-year incentive plan works (Model D)

The Multi-year incentive plan combines STI and LTI awards into a single plan with a ‘look-back’ feature to encourage a focus on long-term sustainable performance.

Bringing the Multi-year incentive plan (Model D) to lifeLet’s consider taking the best of both STI and LTI plans and morphing these into one incentive plan. Figures 3, 4 and 5 show what this would look like.

8 Blip or turning point – how can reward support sustainable growth?

Performance measurement

Overall score for 3 years

75% shares

25% cash

Cur

rent

Yea

r

Clawback

x =

Incentive determination

Tar

get

Ince

ntiv

eas

a %

of

sala

ry

Act

ual I

ncen

tive

as a

% o

f sa

lary

Payment mechanism

40% 48% +1 +2 +3

1.2 x

Figure 4 – Rolling performance assessment

Figure 5 – Determining the incentive award

Performance measurement

Category Weight 1 year earlier2 years earlier Current year

Groupperformance

70% 0.5 x 1 x 2 x

People 10% 0.5 x 1 x 1 x

Safety 10% 0 x 1 x 1 x

Individual 10% 1 x 1 x 1 x

Overall score for each year 0.5 x 1 x 1.7 x

Overall score for 3 years 1.2 x

Final assessment subject tooverriding RemCo discretion

The scorecard measures qualitative and quantitative performance in the current year as well as for the previous two financial years. The results are weighted to calculate a score for each year and the remuneration committee exercises its judgement to determine the overall performance across the three years (see Figure 4).

The actual incentive earned is determined by applying the overall score for three years (‘1.2 x’ in this example) to the target incentive (ie 40% of fixed pay). 25% of the actual incentive is paid in cash at the end of the current year and 75% of the award is deferred into shares, vesting over years one to three (see Figure 5).

PwC 9

Proxy adviser viewpoints on a Multi-year incentive plan (combining STI and LTI)We interviewed a number of the major proxy advisers in Australia to obtain views on the acceptability of a Multi-year incentive plan.

General comments

• Model is seen as viable if boards can increase trust with shareholders.

• Model is seen as an interesting alternative and workable provided there is clear disclosure of the discretion and transparency of performance and reward outcomes.

• Three-year look-back seen as a good idea and would help smooth out the boom or bust cycle.

Views on performance measures

• Transparency of the metrics being used in the balanced scorecard evaluations will be needed.

• The company will need to clearly provide the rationale for the selected scorecard metrics as a driver of long-term performance.

• A financial gateway may be required to prevent payments being made when profits are significantly down but non-financial hurdles have been achieved.

Views on disclosure

• Full explanation will be required in the remuneration report regarding the reasons for the change as well as the limits on the board’s discretion.

• Full disclosure of the performance metrics used and performance against those metrics will be needed.

The key challenges with this type of plan are its unconventional design (by ASX market practice standards), and the degree to which the remuneration committee will need to exercise judgement when assessing final awards.

Companies adopting this approach will also need to invest a considerable amount of time engaging with stakeholders to define the case for change and how the new plan will improve the link between pay and performance.

The remuneration committee will need to demonstrate that there is a robust framework in place, and ensure full and transparent disclosure of how performance/vesting has been determined and how judgement has been applied.

We believe the transition to a Multi-year incentive plan is entirely feasible for most companies with many of the required processes and procedures already in place (eg the use and measurement of corporate KPIs and the infrastructure for the delivery of equity-based incentives).

Case study – Tatts Group LtdTatts Group Ltd (Tatts) is an interesting example of a company that is on the path to significantly changing its remuneration model and implementing something different. Tatts have disclosed they are introducing one new ‘merged’ incentive plan that combines elements of short and long-term incentive plans, uses company specific KPIs and pays out in both cash

and equity. This is not dissimilar to our Multi-year incentive plan (Model D). Tatts have also begun to engage external and internal stakeholders, evidenced by early communication included in their 2010 annual report.

So, let’s examine how you might introduce a Multi-year incentive plan in practice.

10 Blip or turning point – how can reward support sustainable growth?

Key point 1 – It is absolutely critical that you articulate a clear case for change for the new model and share this with stakeholders. Your shareholders may be very sceptical (ie “You’re just making the change because the current arrangements do not pay out enough”).

Key point 2 – There needs to be transparency for both shareholders and participants as to how performance will be assessed, ie what metrics will be used and why they are considered appropriate as drivers of long-term value creation.

ExampleTatts devoted a considerable part of its 2010 remuneration report to explaining the context of the new arrangements proposed for 2011:

“Tatts Group retains its commitment to growth within the context of a responsible gambling business in a highly regulated industry. This makes the existing remuneration system of market wide benchmarks largely irrelevant as a measure of Group performance. The existing remuneration system has not been effective in achieving its fundamental intent to motivate employees for higher performance to improve business outcomes and therefore shareholder value. Similarly, government decisions have adversely impacted shareholders and employees alike, and have shown the remuneration structure to lack appropriate flexibility to adapt for such events, thereby reducing its effectiveness in driving business and employee outcomes to shareholder value creation.

To ensure the remuneration structure is more effective, the Board is realigning the operation of the remuneration approach to better reflect the specific nature of Tatts Group and its industry. The changes are designed to simplify and make more transparent the remuneration process so that Group wide, SBU/Division and individual targets are defined, understood, achievable and delivered with more clarity to employees and are more understandable to shareholders.”

ExampleTatts set out the new structure and basis for why the new performance metrics have been selected:

“The variable/risk incentive component of remuneration is being modified from the more generic existing STIP/LTIP structure to a more specifically focused bonus system that incorporates a combination of cash and restricted shares that will be delivered only in the event of achievement of pre-determined Key Performance Indicators (KPIs) approved by the Remuneration Committee annually…

…the basis upon which this variable/at risk remuneration may be awarded will be comprised of a number of market and performance related aspects of the overall Group effort. These are:

a) Company-wide Performance.

b) SBU/Divisional Performance.

c) Special Projects/Responsibilities.

d) Individual Performance…

…this first component of market based variable/at risk remuneration is available to all permanent staff but will only be paid if the Group as a whole, on its consolidated results, meets criteria associated with the annual financial performance against budget and previous year levels. These criteria will include consideration of:

• revenue and earnings per share outcomes;• profit growth;• maintenance/growth of the Group’s EBIT/revenue margin; and• maintenance/improvement of key expense groupings to revenue ratios, especially employee

costs and operating costs.

The funds available to be paid for this component, if any, will be primarily determined by the growth in earnings per share achieved by the Group, together with the revenue growth. However, at least two of the four criteria described above must be met. The key driver of profit growth in a licensed wide area networked gambling business is the revenue growth achieved annually, given the highly regulated variable deductions to determine the operating margin, and the fixed cost nature of the network based operational costs. Hence revenue growth, calibrated by EBIT margins to reflect cost control and EPS growth to take account of the capital management of the business, provides the key value driving components of the Group.”

PwC 11

Key point 3 – A key driver of the move to this type of incentive plan is its simplicity when compared to the current models, with shareholder alignment created through a strong focus on share ownership. The benefits of simplicity are at the forefront of why this model should be considered – remuneration reports will be easier to understand and the full amount of incentives will be transparent and not based on a theoretical future valuation model.

Key point 4 – The ultimate success of a move to this new model is very dependent on the organisation treating it as any other fundamental business transformation project, with appropriate planning, timing and resources dedicated to achieving the desired outcomes.

ExampleTatts described the more transparent disclosure that would result from the move to a restricted shares award:

“Shares issued under this program would be priced at the VWAP of the ten days prior to the day the Remuneration Committee decides to award them. This approach puts shares in the hands of executives at current values reflecting current performance, but the ultimate value of which will be dependent upon their performance in driving the business for capital and income growth for Tatts Group, entirely aligned to the interests of Tatts Group shareholders. These restricted shares may be subject to forfeiture if a participant leaves the employment of the Group before a pre-determined timeframe, or commits any act of fraud, defalcation or gross misconduct in relation to the Group.

This approach also provides a much more transparent disclosure regime of the Group’s remuneration to shareholders in that:

• it utilises a very clear and publicly verifiable pricing structure for equity-based remuneration of the 10-day VWAP, compared to the opaqueness of option-based pricing models under the previous approach;

• flowing from this, the annual remuneration tables in this Report will reflect the amounts actually paid in respect of the financial year, not an amortised cost amount for equity-based awards; and

• shareholders can more readily understand the levels of equity exposure of employees which is not readily the case with options and rights with their differing vesting and exercising criteria and inherent leverage attaching thereto.”

ExampleTatts outlines the transition implications:

“The transition to this new remuneration structure…may need to be managed over a number of years. This arises due to the need to ensure that existing employment contracts are transitioned to this new remuneration structure progressively and with no disadvantage to any employees.”

Which way should you go?The two models presented in this article have varying degrees of simplification when compared to traditional remuneration models. They offer greater transparency, reduce the risks associated with long-term forecasting, and present alternative value propositions to executives and shareholders.

Adopting a remuneration model similar to our Simplified framework (Model A) would certainly ‘break the mould’ but would also present implementation challenges. That said, a more nimble start-up company or a greenfield investment that is not bound to traditional structures is likely to find the Simplified framework more appealing.

On the other hand, our Multi-year incentive plan (Model D) retains performance as a determinant of reward and offers a single incentive opportunity, doing away with the delineation

between STI and LTI. The look-back feature helps avoid the calibration problem, while the balanced scorecard allows for customised measures. Although the Multi-year incentive plan is not a cure-all, we believe it addresses a number of issues with more traditional models and expect more companies to follow the lead of Tatts in coming years.

Whether you’re sticking with the status quo, or designing a new remuneration model matched to your business needs, shareholders will need to recognise that remuneration policy is a strategically important dynamic for a company, and that individual design (rather than strict adherence to compliance and common practice principles) can have a significant impact on how the remuneration plan supports sustainable value creation.

12 Blip or turning point – how can reward support sustainable growth?

Figure 1 – The ASX 100 index (2001 to 2010)

S&P/ASX 100

Ind

ex p

erfo

rman

ce

30 Nov, 20106,0005,500

5,000

4,500

4,000

3,500

3,000

2,500

2,0002002 2004 2006 2008 2010

Can remuneration frameworks be sustainable in times of change?

2010 proved that Australia emerged from the financial crisis as one of the strongest economies in the developed world. Despite this underlying strength, the crisis did lead to a softening of pressure on executive pay increases. As markets and confidence recover (see Figure 1), boards are facing the challenge of appropriately rewarding their executive talent – because as business performance improves, the demand for talent will increase, as well as the pay expectations of executives.

As Australia now enters a phase of potential market growth, remuneration committees will have some immediate tactical remuneration issues to address (for example, fixed pay rises for FY12, STI outcomes for FY11, retention considerations).

More importantly, we believe this is the time to be assessing the broader, macro consideration – whether your current remuneration framework can be managed in a more sustainable way, in order to avoid the need for changes

in the foreseeable future. A sustainable remuneration framework must be beneficial to both internal and external stakeholders. Shareholders are often sceptical of frequent change, but a framework that is consistently explained over time will help both management and shareholders understand both how it operates and when it delivers value.

It is therefore time to examine some pertinent questions:

• What are the immediate tactical remuneration challenges following the financial crisis and how can boards balance the demands of different stakeholders?

• Is your current remuneration framework sustainable, and if not, how can it be improved for the long term?

A remuneration framework that is aligned with performance through good and bad outcomes will appropriately reward executive talent.

Source: au.finance.yahoo.com

PwC 13

Figure 2 – The board’s balancing act

BoardRemCo

Management

Shareholders

Government

Proxy advisers/ Governance

bodies

What tactical issues need addressing right now? During the financial crisis, remuneration decisions were relatively straightforward. Executive pay went into a period of ‘lock-down’ where fixed pay was frozen, bonus payments were challenged, and in some mainly non-Australian cases, LTI award levels were reduced where share prices had decreased.

Retention of key executives seemed less difficult – many were happy to have a job, let alone consider looking for a new role with higher remuneration. With shareholders at their most vocal, many boards made few changes to their remuneration frameworks unless absolutely required (eg by new regulations).

However, as markets improve, and the demand for talent increases, the remuneration committee will find it has to manage a complex balancing act to account for four main stakeholders’ interests (see Figure 2).

• Management – if company performance is strong, management is likely to expect a return to times of healthy bonuses and substantial annual pay rises. If long-term incentive awards are unlikely to vest, there may be retention pressures in the form of calls for tailored arrangements or changes to existing arrangements. And where there is a new management team, these pressures for change will increase.

• Shareholders – though they are still feeling the real effects of the financial crisis, if company and share price performance has returned, or a management change seen as positive has occurred, shareholders may demonstrate short memories and be more accepting of remuneration uplifts/change.

• Proxy advisers and governance bodies – will be keen to ensure that the lessons learnt in terms of pay moderation during the financial crisis are kept at the front of stakeholders’ minds, in particular shareholders and company boards.

• Government – like the proxy advisers, will be keen to ensure lessons are learnt from the failures seen in the downturn, and will try to enable this through new legislation and regulation.

This leaves boards with a juggling act, trying to satisfy all stakeholders – ensuring talent is rewarded for performance, but not excessively rewarded.

14 Blip or turning point – how can reward support sustainable growth?

Previous upturn (circa 2003/04) Today

• In 2001 the dot-com ‘bubble’ burst, there were terrorist attacks in New York, and the likes of Enron and WorldCom collapsed. Global stock markets fell and a short downturn in executive remuneration levels was seen world-wide.

• From 2003/2004, however, healthy pay rises had returned (and would soon go back to double digit annual increases). Bonuses returned to above-target levels as profits entered positive territory again, and an upward spiral of executive pay returned as many companies increased the ‘at risk’ component of pay.

• At the same time, we need to understand that remuneration reports were not a requirement in Australia and shareholders did not yet have an (advisory) vote on remuneration. In addition, many bonus plans were linked largely to profit and many LTI plans would either have had no performance measures before vesting, or TSR or EPS ‘gates’ (ie an all-or-nothing payout).

• Essentially, when looking at the board’s balancing act (Figure 2), during the previous upturn, pressure from the proxy advisers and governance bodies did not exist to the same extent, and although shareholders could clearly have a say, their ability to understand pay levels and to vote on them was minimal.

• The credit crisis and the collapse of organisations such as Lehman Brothers have had lasting effects that include high rates of US unemployment, billion dollar government bail-out packages and struggling eurozone countries.

• Remuneration reports are a requirement, with increased disclosure continually sought.

• Shareholders have a vote on remuneration, and are certainly using it where they are unhappy. And with the ‘Two Strikes’ legislation on the horizon, the remuneration vote may soon have more ‘teeth’, and continued dissatisfaction may lead to potential board replacement.

• Many bonus plans are based on scorecards, with measures acknowledging the risks taken, and deferrals of STI awarded into equity are increasingly common (with the risk of clawback a newer addition).

• Performance measures are the norm for LTI plan vesting, and while TSR and EPS are still the most prevalent measures, they are normally sliding-scale vesting schedules.

• With the additional changes required by APRA (for regulated financial services companies), the termination benefits legislation, independence requirements for remuneration committees, the expected legislative changes to the Corporations Act and the anticipated guidance from Corporations and Markets Advisory Committee (CAMAC) on improving remuneration report disclosure, the environment is markedly different to that of 2003/2004.

Can we learn any lessons from past upturns, or has the world changed?

How can boards manage these present-day pressures?

Table 2 – Some current tactical remuneration considerations

Table 1 – Lessons from past upturns

Issue Points for the board to consider

Fixed pay rises for FY12 • With most executive fixed pay rises in FY11 expected to be moderate (around 4% – 5%) as the pay freezes of FY10 are removed, high-performing executives’ expectations for FY12 will likely be higher again.

• The level of fixed pay rises among the broader employee population will also need to be taken into account, as shareholders and proxy advisers are expected to use this as a barometer to assess whether the gap between employees and executives is increasing again.

• As remuneration budgets may still be under constraint, ‘healthy’ rises should be targeted at individuals/groups where high performance or potential has been demonstrated – particularly as these may be the most immediate retention threats moving into an upturn.

Most remuneration committees will be debating some specific needs as we move away from the remuneration ‘freeze’ environment common during the financial crisis. Table 2 sets out some of the tactical remuneration issues that are likely to be on the board’s agenda at this time. We have listed some points for consideration when addressing these tactical issues.

PwC 15

Issue Points for the board to consider

STI outcomes for FY11 • With markets and company performance moving into the black, shareholders and proxy advisers should be expecting that bonus payments will rise into FY11.

• Transparent and forthright communication will be key to obtaining shareholder support of the remuneration report. If shareholders understand the measures that determine bonuses and company performance is evident and visible, this will minimise pushback.

• In support of the transparency debate, and corporate governance best practice, the specific performance targets and the outcomes of assessment against these should be disclosed in the remuneration report. Generally, this is no longer sensitive information, but is disclosure that shareholders will view positively.

• If not already in place, mandatory deferrals of bonuses above a certain threshold into equity should also be considered outside the regulated FS sector (where they are now required).

Need for retention payments awards

• In assessing whether targeted retention awards are required, consider both the current unvested equity holdings of the executive (and their associated vesting/release dates) as well as any formal talent assessment and succession plans.

• Proxy advisers and shareholders will be quick to question executive retention awards, and as such the rationale (based on the above) will be crucial. Clear upfront communication is recommended (eg why awards are required on top of the normal incentive arrangements).

• Awards should be targeted to individuals identified as both high risk and critical to organisational success, because broad-brush awards to large employee groups will call into question the existing incentive plans’ applicability/success.

• Awards should, where possible, be in the form of equity with vesting over the long term (ie longer than two years).

16 Blip or turning point – how can reward support sustainable growth?

Is your current remuneration framework sustainable, and if not, how can this be improved?The external environment is dynamic, and there will inevitably be ups and downs. However, one thing is certain: when there is change, be it a market downturn or upturn, a new management team, or new rules or regulations, we nearly always see accompanying changes in the remuneration framework.

And change is not always a good thing, for example, if we look at our three main stakeholders in Figure 2 in the context of remuneration change:

• Management – will ‘switch off’ when change is too frequent, as they are likely to have little understanding of what they need to do year on year to earn their incentives. They risk seeing the framework as a fancy ‘lottery’ which cannot benefit anyone, and for which they will be criticised if it pays out.

• Shareholders & proxy advisers – become sceptical of regular change, perhaps suggesting it is occurring simply because previous arrangements were not paying out. The complexity that can result from change, eg the need to report on historical remuneration arrangements that differ from today’s, may add to the frustration. Commonly, the questions asked are “Why are you changing now?” and “Is it purely to benefit executives?”

Some of these suspicions may in fact be true, but in many cases change happens because of a number of interrelated drivers:

• The performance measures for vesting to occur may be poorly aligned to the drivers of a new business strategy.

• The framework is simply not flexible enough to cope with a change in (for example) market conditions, and the remuneration committee has not fully understood how the plan or plans would perform under various performance scenarios.

• The plans are poorly communicated internally and externally, and if they fail to pay out, management may be puzzled; alternatively, if they pay out handsomely, external commentators may be critical if their view of company performance does not warrant the payouts.

Our view therefore is that if constant changes in the remuneration framework is an imperfect position, surely the goal should be a reward strategy and framework that can endure, that will stand the test of changes in both personnel and market conditions.

Market practice When considering an enduring remuneration model, Macquarie Group (Macquarie) provides a good example:

• A remuneration strategy/philosophy that has broadly been in place since the inception of the company, with its objectives and principles clearly communicated to shareholders and with a demonstrable link to shareholder value.

• A remuneration framework that is underpinned by a set of principles that have barely changed in recent years – one of the most notable being: “Using broadly consistent arrangements over time to ensure staff are confident that efforts over multiple years will be rewarded.”3

• A remuneration philosophy that has changed little over time, when compared to most other ASX-listed entities – this despite the recent volatility of markets and the wealth of changes that were required by APRA.

There are certainly many reasons why the Macquarie model has endured, but by remaining clear and consistent in its messaging over the years, it has ensured that both management and shareholders understand how the framework works, and in what scenarios it will pay out or not.

While this example may be in an industry that is very different to your own, nevertheless it is worth asking what individual boards can do to determine whether their remuneration frameworks will endure, or whether they are susceptible to the next market or management change.

Macquarie’s remuneration framework is underpinned by a set of

principles that have barely changed in recent years – one of the most notable being: “Using

broadly consistent arrangements over time to ensure staff

are confident that efforts over multiple years will

be rewarded.”

(Source: Macquarie’s

2010 Remuneration

Report)

3 Source: Macquarie’s 2010 Remuneration Report

PwC 17

Table 3 sets out some of the considerations the remuneration committee may wish to debate in the context of achieving an enduring framework.

Table 3 – Considerations that may support the achievement of a sustainable remuneration framework

Action What to consider

Affirm a remuneration strategy that speaks to the heart of your business goals

• Review your remuneration strategy: – It should be a short statement that plays to the heart of what you want to focus your

people on delivering, rather than a ‘blue sky’ statement that means little to the executives or the board.

– Most companies state their strategy at the start of their remuneration report, but many look the same.

Agree and articulate a set of remuneration principles

• These may be externally communicated or not, but should be the basis on which the board evaluates any decisions for change to the framework.

• They will allow the board to ensure that decisions made over time will continue to focus on similar considerations (even where board members may change). They will also allow the current model to be ‘scored’ against a potential change (again consistently over time).

Ensure incentive awards correlate with corporate performance

• Can the components of the corporate strategy be traced to both the scorecards that individuals’ performance are assessed against, and to the measures through which incentive awards vest?

• A common headline during the financial crisis was ‘payment for failure’; this does not always refer to termination payments, but also to remuneration quantum appearing to lack correlation to corporate performance.

Conduct scenario modelling on incentive awards

• Has the board evaluated how reward outcomes would look under different performance scenarios? Do incentive awards appropriately reflect these different scenarios and sufficiently differentiate between them?

Seek management input • Does management understand the current framework – that is, how their actions affect their remuneration outcomes?

• Ensuring that management buy in to any redesign ‘journey’ with the board will heighten the likelihood that a framework is understood, valued and accepted.

Communicate proactively and openly with shareholders

• Frameworks that are successful may not always align to market practice, but by ensuring that both the detail of change and the underlying rationale are discussed openly with shareholder/proxy adviser groups before implementation, boards significantly reduce the chance of subsequent pushback.

• External suspicion/critique often stems from opaque communications, so consult early and regularly (especially with any key bodies you know to have had issues in the past).

• As critical as it is to ensure that shareholders have sufficient information to make decisions, it is equally important that shareholders feel they have a voice and the company is listening. Offering a variety of avenues for shareholders to communicate their thoughts and concerns to the board is essential. Some examples of innovative ways to communicate with shareholders include:

– an executive remuneration interactive website – the provision of an email address for the chair of the remuneration committee – an open question in proxy cards soliciting feedback.

The items in Table 3 are by no means a comprehensive list of matters to be considered, nor a foolproof way to ensure your remuneration framework can endure the test of time. However, if robustly applied, the points can be considered as tools to make the

board’s balancing act easier and one where all parties feel involved and empowered. And with legislation such as the ‘Two Strikes’ rule on the horizon, this is something that boards will be keen to achieve if they have not already done so.

18 Blip or turning point – how can reward support sustainable growth?

How can we make remuneration changes stick?

Remuneration can be a powerful tool to reinforce your strategy, so it is important that any remuneration changes be sustainable and produce the desired outcomes.

To examine what this might mean in practice, we explore a performance alignment case study and apply it to PwC’s Making Change Stick framework, identifying questions your company should be asking and common pitfalls in the design and implementation of a new remuneration approach.

Making Change Stick Truly embedding and then sustaining remuneration changes that produce the desired business outcomes is a challenge many companies continue to face. Testing economic conditions, strategic game changes and organisational culture shifts are common drivers for a change in remuneration arrangements. Yet even with a valid business case, most companies face lack of buy-in to the change initiative.

So we believe it’s important to ask the question: “How do you know if your approach to remuneration change is the one with the greatest chance of success (ie will the change stick)?”

Our global experience shows there are 10 key factors underpinning successful and enduring change. They are incorporated within the four components of the Making Change Stick framework: Change approach; Benefits; Involvement; and Sustainability (see Figure 1).

We have used the following case study to illustrate the practical application of these key success factors.

There is no one-size-fits-all change framework; organisations need to design an approach specifically tailored for their own situation.

Case study: The company challengeAn ASX-listed company has just finalised its five-year transformation strategy. The CEO believes that aligning the executive remuneration arrangements to this new corporate strategy is an immediate priority, but is yet to communicate this belief broadly. It has been three years since the leadership team’s remuneration arrangements were last revised and they have fallen out of line with market practice, attracted negative scrutiny from shareholders, and resulted in a ‘silo’ culture. Additionally, the company is facing challenging times in the market and employee morale is low.

Figure 1 – Key success factors for Making Change Stick

Involvement

Best-

fit c

hang

e ap

proa

ch Benefits

Sustainability

Makingchange

stick

10 key success factors…Change approach 1. Design the best-fit change approach.

Benefits 2. Keep business benefits at the heart

of change. 3. Challenge the data and its

interpretation. 4. Agree the measures of success and

how to monitor them. 5. Focus on the actions that make a

difference fast.

Involvement 6. Through involvement build a vision

and hunger for success. 7. Engage the front line before, during

and after.8. Communicate with a purpose.

Sustainability 9. Give leaders the skills – and the

heart – to lead. 10. Make sure systems, processes and

culture reinforce change.

PwC 19

1. Design the best-fit change approachThere is no one-size-fits-all change framework; simply using a change approach previously tailored to another situation is not necessarily the right way to proceed. To ensure you have the best-fit approach, you need to consider all of the following elements during the design phase: the business drivers, intended benefits, speed and urgency of the change, extent of behavioural change required, existing culture and values, leadership capability, and the company’s readiness for change.

The human aspect of decision-making can influence how the approach is designed. The greater the impact on high profile individuals, as is common with remuneration changes, the higher the risk the change will be either incrementally introduced or delayed. But despite the difficulties involved in making changes, remuneration can be a powerful tool for the reinforcement of a company’s strategy and should be utilised to its full potential.

When deciding the best-fit change approach we recommend that you ask yourself the following questions:

• Have you developed, documented and shared your draft approach to change with all the right people?

• Have you engaged the right people, for example, the remuneration committee, board, executives, shareholders, to assess whether the approach to change is appropriate?

• Have you considered both internal and external environmental demands? For example, market practice and regulatory requirements.

• Is the approach tailored specifically to your project and do you have plans in place to review and refine it regularly?

• Have changes of this nature been attempted in the past? If so, who holds relevant experience?

• Who are the key stakeholders that must support this change if it is to be successful? For example, board members, executives, proxy advisers and shareholders.

• What are the other things that success will depend on? For example, if there is a new corporate strategy, will your people recognise the need for a change in the remuneration strategy to deliver on that strategy?

The approach to involving and engaging key stakeholders plays a pivotal part of the design in a best-fit change approach.

Case study: Key learning

The change approach was devised at a high level, but should also have been discussed with the key stakeholders from the beginning to ensure that it remained suitable for the new situation.

Change approachCase study continued:The CEO engaged with proxy advisers to obtain their view of the current executive remuneration arrangements, and is now working with the HR Director to devise the next steps. However, given the urgency for this change, the HR Director has come up with a high-level approach based on previous approaches – that is, design the structure first, and then engage the executives and the board.

20 Blip or turning point – how can reward support sustainable growth?

2. Keep business benefits at the heart of the change

Formal agreement to the benefits and the approach to realising them is the first step in supporting an organisation’s effort to change. But while business benefits need to be clearly articulated, it is also important to tailor those benefits to your people’s needs. People want to know “How will I be affected?” and “What does this mean for me?” Personalising the benefits for each stakeholder group helps gain greater buy-in for the change. Where some of the individual benefits (or other impacts) are not yet known, then be clear that the answer is not known and give people the process and timing of when more will be known.

Benefits realisation is a process that determines how to realise objectives and derive the desired outcomes of the change. It does this by:

• breaking down high-level benefits into manageable components

• measuring benefits before, during and after a change• using techniques to ensure that the potential and planned

benefits of transformation initiatives are obtained• helping to focus attention on the core benefits.

Generally, the core benefit for a significant remuneration change is positively affecting the company’s ability to deliver on its corporate strategy by attracting and retaining top talent. The challenge is to ensure that all of these activities are carried out effectively and that they are aligned with any broader concurrent projects.

3. Challenge the data and its interpretationIn cases where data and its interpretation are being relied on to inform key decisions, consider whether:

• the data captured is fit for purpose and agreed on by key stakeholders

• the data has been presented in the most appropriate format• all data sources have been considered, both financial and

non-financial (including attitudes and opinions), and are relevant

• scenario modelling is robust enough to highlight individual and organisational impacts in various performance scenarios, and accurately measures return on investment.

4. Agree the measures of success and how to monitor them

Agreeing the measures used to define what success looks like is essential. Any plan should include how the benefits will be measured and when.

Continuing to measure the benefits post-implementation will also support ongoing success.

Some examples of measures of success for remuneration projects are:

• level of performance improvement• employee retention • employee engagement scores• the percentage of profit paid out as variable pay compared to

market norms• the percentage of votes in support of the remuneration report• talent attraction.

BenefitsCase study continued:

The following month at an executive briefing, the CEO explains that the executive remuneration arrangements will change for the following performance year. During the conversation, the CEO consciously focuses on the benefits, including:

• alignment to the new corporate strategy • simplified remuneration arrangements• consequent ability to attract and retain the right talent.

The CEO also outlines the next steps, including that the executives will be expected to help with stakeholder management. However, the executives viewed the benefits as too high-level, and were also given no indication that they would be involved in the design or decision process. Executives were left wondering what these changes meant for them.

Organisations often lose sight of the real success factors: Is the change effective? Have business outcomes improved as a result?

Case study: Key learning

Although the business benefits have been well articulated, they were too high-level and have not been further translated into benefits that are meaningful for each stakeholder.

PwC 21

5. Focus on actions that make a difference fastNever underestimate the power of early wins to generate confidence that change is possible and to galvanise stakeholders. An early win can be achieved from something as simple as discussing with some of the key stakeholders the reason for the change and initial thoughts on the design of the new remuneration arrangements. This will allow them to feel involved and reassure them that the change is moving on the right track.

The benefits realisation approach (referred to in Key success factor 2) should occur early in the process. It will help to:

• reduce program risk• ensure that each outcome has a directly attributable value (benefit) attached to it • identify and address obstacles to realising the benefits, since the method encourages

‘looking back’ to understand how the benefit was achieved • provide a basis for continuous improvement by reviewing the benefits regularly and

identifying risks to realising them.

So, when you are planning your change approach, think about how and when there are opportunities for “quick wins” rather than all the benefits coming as an avalanche at the end. Without the positive momentum generated by these quick wins, the risk of inertia means that this avalanche of benefits may never come.

Change needs to be leader driven, and not seen as an HR project. Equip leaders with the skills and desire to be role models and to effectively lead the change.

InvolvementCase study continued:

After an intense three-month review of existing arrangements, the board endorses the following changes:

• introduction of a balanced scorecard to determine individual performance ratings for annual bonuses

• limiting LTI in the form of share rights to top-tier executives and replacing LTI with deferred shares (based on a percentage of STI) for all other LTI participants.

Feedback on the changes is not positive and internal stakeholders raise a range of concerns. These concerns are logged but the outcome is not communicated to these stakeholders. As a result, these stakeholders become disengaged and feel that their concerns have not been considered.

Case study: Key learning

Engaging key executives to discuss the proposed changes was an important step. However, particularly given that the change would have a high personal effect on these stakeholders, earlier communication would have helped to manage their expectations. Also, responding to stakeholder concerns is just as important as logging them.

22 Blip or turning point – how can reward support sustainable growth?

6. Through involvement, build a vision and hunger for success

Stakeholder engagement is often a rushed exercise at the end of the project. However, real stakeholder engagement requires earlier involvement in, for example, the design phase. This increases the likelihood that stakeholders are excited by and committed to the change. Achieving this is a disciplined and complex process that requires planning and attention right from the start. This is particularly true when it comes to sensitive topics such as remuneration, where the impact of any change will vary depending on the stakeholder.

7. Engage the front line before, during and after

Understanding your stakeholders and their needs is essential for achieving buy-in and a common understanding of what successful change will look like. But how and when stakeholders become engaged can be tricky, given the inherent self-interest associated with sensitive changes such as those involving remuneration. It is therefore important to understand all stakeholder needs and perspectives upfront, so that you can know at which stage you need to involve them.

For example, how much involvement does the board believe that executive participants should have in the design of their own remuneration arrangements?

From the board’s perspective, are there “non-negotiables” which are set? If so, let people know this and get their input to the aspects that can be influenced.

8. Communicate with a purposeSimply applying one communication method to a wide group of stakeholders will not result in the desired buy-in. An effective communication plan not only tailors key messages to the specific needs of each group, but also provides answers to their concerns and the reasons for accepting or discarding their feedback.

Consider what you want your stakeholders to know, think, feel and do as a result of your communications. By approaching it from this angle, you will be able to tailor your communication materials and implementation support as appropriate.

Questions to ask when building involvement:

• Does everyone share the vision? How can you bring it to life?• Have you allowed time to understand what your stakeholders

really think?• Is the whole team clear about what you want people to know,

think, feel and do?• Have you included in your project plan activities to generate

enthusiasm and engagement?• How are you going to keep on track while maintaining

engagement and taking new ideas and differing views on board?

• Have you tailored your communications to the various stakeholder groups? Are you communicating in a language they understand and through channels they know and use? Are they communicating back?

The higher up the power and influence scale, the more time and energy you will need to invest in the stakeholder (see Figure 2). These are the people or organisations that could make or break your initiative (your ‘partners’). Examples include the board, remuneration committee, executives, participants and proxy advisers. Those stakeholders with low influence and low power will need to be kept informed, but do not need the same levels of time and energy (see Figure 3).

Influence

Pow

er

High

HighLow

Influence Partners

InvolveInform

Figure 2 – Stakeholder mapping (high power, high influence)

Influence

Pow

er

High

HighLow

Influence Partners

InvolveInform

Figure 3 – Stakeholder mapping (low power, low influence)

PwC 23

Case study: Key learning

The CEO was right to respond to the signals and amend the approach to move to a step-by-step implementation plan. Regularly reviewing the change approach means it can be tweaked where necessary and still achieve the desired outcomes.

SustainabilityCase study continued:

The CEO was confident that the proposed changes were clearly aligned to the corporate strategy and the desired culture and company values. The CEO also believed that the new remuneration strategy would achieve all its desired objectives.

However, the initial rounds of the stakeholder engagement process showed that the communication phase needed to be extended and that there were a large number of interdependencies relating to the vision, systems, people management and process changes.

The CEO now decides that it would be best to approach the changes in steps, first working on the other dependencies and the balanced scorecard for the STI plan, and deferring the remaining changes until the next performance year.

9. Give leaders the skills and the heart to leadChanging a remuneration strategy is only one tool for changing behaviour. To effect real change in behaviour, it is also important to have people in the company who can lead by example, set the tone for change, show by their actions and behaviour what success looks like in practice, and encourage others to follow.

Questions to ask when enabling your leaders to lead:

• Challenge yourself – are you leading by example?• Are you coaching leaders to adapt their management styles to support the change?• Are you satisfied that leaders are bringing their people with them?

In remuneration changes, it is important that your leaders have all the relevant information to be able to answer the “big” questions. Also, they need to actually believe (in their heart) that the changes are the right ones for the organisation.

Ensure that interdependent systems and processes are ready to support the change.

24 Blip or turning point – how can reward support sustainable growth?

10. Make sure systems, processes and culture reinforce the change

Make sure that the new remuneration arrangements are reinforced by policies, processes and supporting systems. A recent multi-year study4 tracking the day-to-day activities, emotions and motivation levels of hundreds of knowledge workers in a wide variety of settings has found that the top motivator of performance is progress. On days when employees believe they are making headway, their emotions are most positive and they have a strong drive to succeed. On days when they feel they are hitting a brick wall or encountering roadblocks, their moods and motivation are lowest. The role of managers should be to ensure that roadblocks are removed wherever possible and that processes and systems are not impeding progress.

So, what does this mean for a remuneration change project? Remember, generally the benefit we are trying to achieve with remuneration changes is to have a positive impact on the attraction, motivation and retention of our talent to successfully deliver on our organisational strategy. A change to remuneration arrangements in isolation will not deliver on this. Therefore, think through the interdependencies which affect the contribution of talent and how you will ensure that they reinforce the changes and are not a road block.

Questions to ask when considering the sustainability of the change:

• Is your team equipped with the information and skills they need to work in a new way?

• Are systems and processes reinforcing the behaviours needed both now, and in the longer term? A major dependency for remuneration changes is “performance management”. Importantly, this is often less about the system and more about the quality of performance conversations.

• Will benefits still be achieved once the project team has been disbanded?

Summing upRemuneration arrangements will remain a hot agenda item, particularly given the continued regulation, external scrutiny and expectations concerning pay for performance. However, to ensure that any changes stick and are not just reactive, we suggest that applying the Making Change Stick framework will help make them sustainable and relevant within the context of the company’s broader strategy and culture.

As with all organisational change, there will be unintended consequences. What is more important is the leaders’ and change team’s response, not just the consequence itself. The key to making change stick is ensuring that issues are effectively dealt with by the leaders and that the change approach continually evolves to enable the successful delivery of the desired changes.

4 T Amabile and S Kramer, ‘What really motivates workers – understanding the power of progress’, Harvard Business Review, January – February 2010, page 44.

PwC 25

The impact of APRA regulation within and outside financial services

In its first round of reviews since the revised APRA Prudential Standard (APS/LPS/GPS 510) came into effect on 1 April 2010, APRA found that remuneration (and governance) arrangements have changed.5

The APRA regulations that were initially perceived to be onerous have resulted in many positive developments in remuneration structures and governance processes in APRA-regulated companies.

How significant have the changes been?There’s no doubt some changes are just ‘tweaking around the edges’ but there are also signs of more fundamental changes taking place. Changes in STI deferral could be described as tweaking around the edges, despite the very real impact on attraction and retention, yet the incorporation of a more rigorous risk component into the remuneration framework and the increased emphasis on behaviour is a more significant change (see Table 1).

Key change New practice

Variable pay pools increasingly based on risk-adjusted metrics

• Economic Profit (EP) and Profit After Capital Charge (PACC) are examples of how financial services companies determine their variable pay pools. Where variable pay pools are not influenced directly by a risk-adjusted metric, there is often a provision for the board to use discretion to adjust variable pay pools based on the company’s management of risk throughout the performance period. We expect that the use of risk-adjusted metrics will increase over time.

Key Performance Indicators (KPIs) now more risk-focused or risk-aware

• KPIs at the group level now often include specific risk management and capital management metrics, and business unit and individual KPIs are generally more risk-aware. It is also common for risk to now constitute a minimum weighting on an employee’s scorecard.

• Compliance and assessment of values and behaviour are part of the incentive determination, either through gateways or a distinct behaviour assessment component.

Typically 40-50% of actual STI is now being deferred

• This is a more meaningful percentage compared to past practice of 25-33%, but will increasing the deferral percentage really change behaviour to focus employees on sustainable performance?

• Where the deferral applies to the entire STI amount, or there is a low threshold in place for deferral, we believe this level of deferral is sufficient. Any deferral above 50% is likely to put pressure on companies to increase STI opportunities.

Table 1 – Changes to remuneration frameworks

5 APRA regulation only applies to APRA-regulated entities within the financial services sector.

A response to regulation can be an opportunity to enhance the effectiveness of your remuneration arrangements.

26 Blip or turning point – how can reward support sustainable growth?

Key change New practice

Tranche-vesting is now common for STI deferral, either 50% over 1-2 years or 33% over 1-3 years

• Tranche-vesting has become common as a result of:– increased deferral percentages– deferral periods needing to be set over a long enough period to determine

whether the basis of the original STI payment was warranted– companies not wanting to risk losing key talent by having deferral periods

too far out of line with non-regulated companies– companies wanting consistent deferral periods for simplicity and to aid

agility even though risks are likely to be realised over different periods depending on the various business activities.

Greater board discretion to adjust STI and LTI payments downwards, if necessary

• Greater board discretion is a positive development as it leads to greater board accountability over remuneration outcomes.

• To date, boards have focused adjustments more on extreme circumstances; for example, to protect the financial soundness of the company or to respond to significant unexpected or unintended consequences.

• This raises the question whether there should be greater board discretion over both STI and LTI outcomes. It is clear that APRA and other foreign regulators are heading this way, although there are a number of challenges associated with increasing discretion and hindsight performance reviews (see commentary on ex-post adjustments in Table 3).

Changes in the structure of remuneration for risk and financial control (R&FC) personnel

• The remuneration arrangements of R&FC personnel are considered separately to maintain their independence. Such arrangements generally include:– KPIs for R&FC personnel based on company, function and/or individual

performance (not business unit financial performance)– hard-line reporting structures to risk and finance personnel, not business unit

personnel (or, at a minimum, Finance and/or Risk sign-off on variable pay payments above a certain threshold)

– a more conservative remuneration mix compared to revenue-generating staff.

Multi-disciplinary management remuneration committees established

• Some companies have established multi-disciplinary management remuneration committees consisting of representatives from HR, Risk, Finance, Legal and key business units to ensure that remuneration plans are examined from multiple angles before being presented to the remuneration committee and the board for approval.

PwC 27

It will take time for companies to determine what are appropriate ex-post adjustments and how best to implement them without taking an overly punitive approach. As a first step, we believe that inserting a review point before vesting is needed to ensure that boards are checking that incentive awards are still warranted in the context of broader performance.

We recommend that companies take into account line of sight, agility and acting within predefined parameters when considering whether incentive payments are still warranted (see Table 3).

What impact has APRA regulation had on non-regulated companies?Companies that are not governed by APRA regulation have also made changes, or are considering making changes, to their remuneration structure and governance processes.

Some of the changes we have seen to date are:

• increased use of deferral or greater levels of deferral

• recognition of the importance of behaviour as well as outcomes in variable pay plans

• greater interaction between the remuneration committee and management in relation to determining reward structures

• an increased number of boards seeking their own external remuneration advice.

Whilst not a regulatory requirement for these companies, we expect that more companies will begin to further incorporate their own key risks into incentive plan structures to promote sustainable performance.

What is APRA likely to focus on going forward?APRA has indicated that in the immediate future it will focus on:

• understanding how the definition of risk and financial control personnel and material risk takers is applied in practice

• performance measures and how these align to risk

• the role of the remuneration committee

• policies and procedures concerning third party contracts and how these fit into the broader risk management framework

• ex-ante and ex-post risk adjustments (as defined in Table 2).

Ex-ante and ex-post risk adjustments The issue that may challenge companies the most is ex-ante and ex-post adjustments. Since the APRA regulations came into effect, companies have made significant changes to remuneration structures to incorporate ex-ante adjustments, although less progress has been made on ex-post adjustments.

Ex-post adjustments have generally been in extreme circumstances (eg gross misconduct or fraud) or have been ‘implicit’. Implicit ex-post risk adjustments are where the ultimate reward outcome depends on the value of the equity instrument at the vesting date (ie the reward value fluctuates in line with the company’s share price).

Regulators believe these adjustments are insufficient in isolation because share prices may move for reasons unrelated to employee actions. Accordingly, APRA is advocating ‘explicit’ ex-post risk adjustments, which require a formal decision (or process) to reduce the deferred amount based on observed risk and performance outcomes.

Ex-ante adjustments

• Adjustments that occur at the time the remuneration entitlement is determined.

Ex-post adjustments

• Adjustments to remuneration that has already been accrued and awarded in light of observed risk and performance outcomes.

• Can be in the form of a clawback (where the employee agrees to return previously paid or vested remuneration) or a malus (where the company can reduce, or not pay at all, unvested deferred remuneration).

Table 2 – Definition of ex-ante and ex-post adjustments6

6 Source: The Basel Committee on Banking Supervision, Range of Methodologies for Risk and Performance Alignment of Remuneration, October 2010. APRA participated in the drafting of this paper.

The level of rigour that APRA is likely to expect in relation to ex-post adjustments is still unclear. Figure 1 sets out the possible range of treatments.

Adjustments usedonly in exceptional

circumstances

Formal reviewpoint by the board

prior to vesting

Range of possible treatments for ex-post adjustments

Rigorous hindsight performance assessment

process

Figure 1 – Treatments of ex-post adjustments

28 Blip or turning point – how can reward support sustainable growth?

Line of sightAdjustments should only be made where the reason for the adjustment is within the employee’s line of sight. Employees should not be penalised for underperformance resulting from the macroeconomic environment.

AgilityThe practice of role rotation poses challenges when boards are determining whether an STI payment is warranted because different people may have been responsible for performance at different times.

Acting within pre-defined parametersWhere employees have acted within pre-defined parameters (eg a mortgage broker writes new loans in accordance with policy), we believe they should not be unduly penalised if bad debts subsequently turn out to be higher than envisaged.

Table 3 – Key issues to consider in the context of ex-post adjustments

Ex-post adjustments: can these go up as well as down?A follow-up question is whether ex-post adjustments should only work to scale down variable pay or whether there should also be the potential for upside. The Basel Committee on Banking Supervision expressed the view that “deferral is more effective when deferred remuneration can only be adjusted downward”.7 This is because “methodologies that allow increases of deferred remuneration, to reflect for instance a lower level of risk observed than expected, may undo some or all of the effect on incentives for risk adjustment”.7

There is a possibility that ex-post adjustments will force deferred remuneration upwards because the more ‘unknowns’ there are in remuneration outcomes, the less valuable deferred remuneration is to employees.