Embed Size (px)

Citation preview

1

G. Steven BurrillChief Executive OfficerBurrill & Company

Oracle Life Science ForumApril 15, 2009

But doth suffer a sea‐change, into something rich and strange…

—William Shakespeare, The Tempest

Biotech 2009: Life SciencesNavigating the Sea Change

22

Burrill & Company—Exclusively Focused on Life Sciences

• Human Healthcare (Rx, Dx, devices, services, informatics) from innovation to delivery

• Nutraceuticals/Wellness

• Agbio/food

• Industrial/energy

• Bio‐cleantech

• Enabling Technologies, including nanotechnology

33

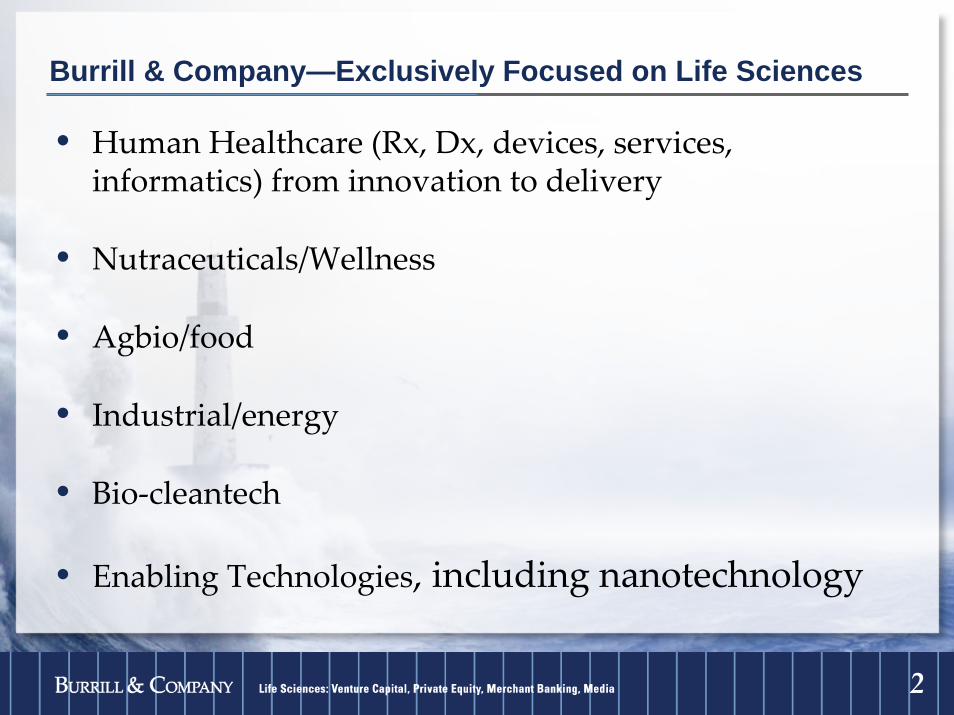

Burrill & Company

Headcount: 50+ professionals and staff

44

Burrill & Company U.S. & International Locations

Burrill & Company U.S.& International Locations

San Francisco (HQ)

PortlandIndianapolis

New York

London

Santiago, ChileRio de Janeiro, Brazil

Sao Paulo, Brazil

Buenos Aires, Argentina

Mumbai

Abu Dhabi/Dubai Shanghai

Seoul

Tokyo

Taipei

Kuala Lumpur

Burrill Operations

55

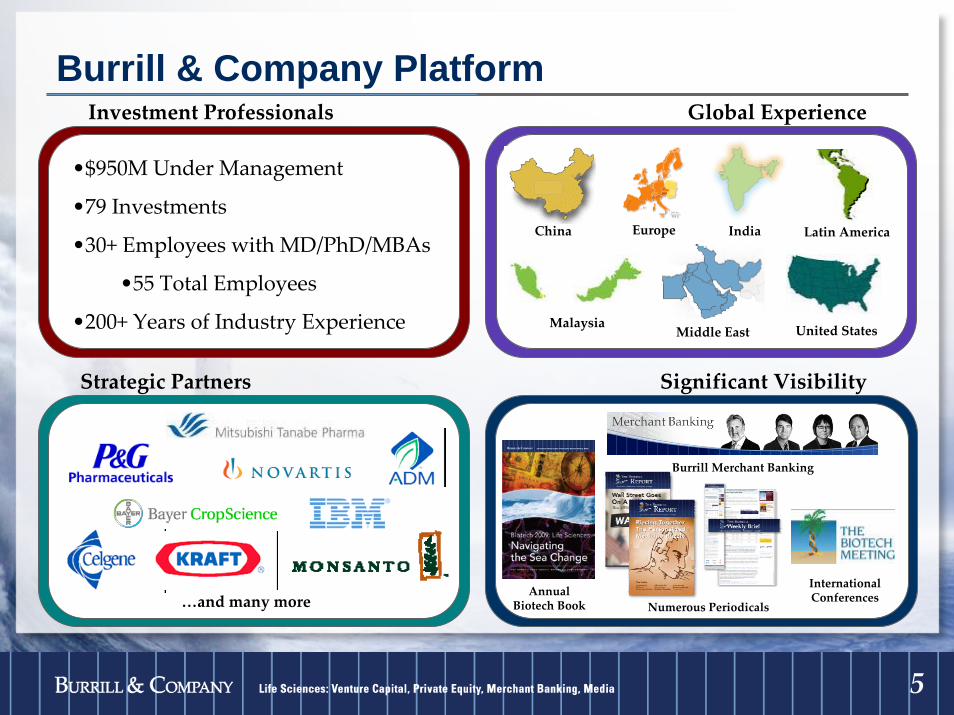

Strategic Partners

…and many more

Investment Professionals

•$950M Under Management

•79 Investments

•30+ Employees with MD/PhD/MBAs

•55 Total Employees

•200+ Years of Industry Experience

Burrill & Company PlatformGlobal Experience

Malaysia

IndiaChina

Middle East United States

Europe Latin America

Significant Visibility

Burrill Merchant Banking

International ConferencesAnnual

Biotech Book Numerous Periodicals

66

Order our 23rd annual book now!G. Steven Burrill’s Annual Book

For ordering information go to www.burrillandco.com

77

Burrill & Company Publications

Annually for 23 years 6x per year Weekly Daily

88

G. Steven Burrill’s State of the Industry

These slides are available for purchase.

For ordering information please visit www.burrillandco.com/slides.

99

Sea change

noun1. a striking change, as in appearance, often

for the better.2. any major transformation or alteration.3. a transformation brought about by the sea.

1010

What really happened in the last year?• World financial crisis – unprecedented (and not over yet)

“Wall Street” totally restructured

• Economic dislocation in the world (well beyond the US) will be pervasive and long term…Recession!

• Healthcare systems around the world reforming too expensive to treat everyone with all the new technologyan aging population dramatically increasing the demand

• Reimbursement/payment systems worldwide undergoing change

• Regulatory agencies increasingly risk‐averse

• Obama Administration in power in Washington

1111

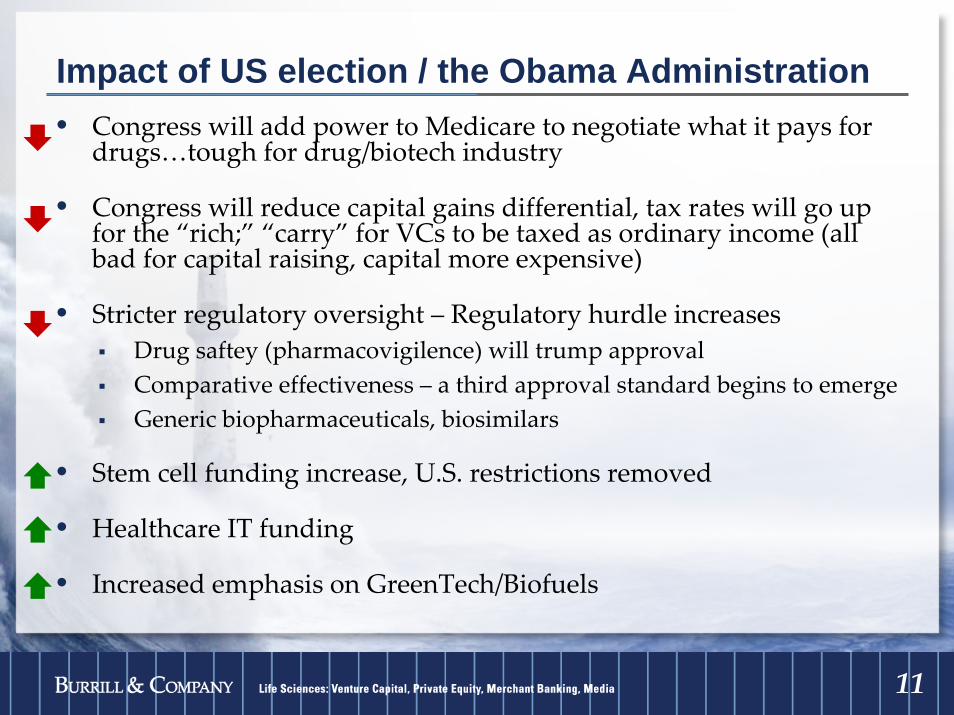

Impact of US election / the Obama Administration• Congress will add power to Medicare to negotiate what it pays for

drugs…tough for drug/biotech industry

• Congress will reduce capital gains differential, tax rates will go up for the “rich;” “carry” for VCs to be taxed as ordinary income (all bad for capital raising, capital more expensive)

• Stricter regulatory oversight – Regulatory hurdle increasesDrug saftey (pharmacovigilence) will trump approvalComparative effectiveness – a third approval standard begins to emergeGeneric biopharmaceuticals, biosimilars

• Stem cell funding increase, U.S. restrictions removed

• Healthcare IT funding

• Increased emphasis on GreenTech/Biofuels

1212

2008 vs. 2009

2008…A 20/20 Vision to 2020

2009…Navigating the Sea Change

1313

A 20/20 Vision to 2020 (just a decade away)

What will the healthcare delivery system look like in 2020?• In the U.S.?• In the world?

What will the “marketplace” include?• Products• Technology

Where is the “biotech revolution” taking us?

1414

A 20/20 Vision to 2020

So…..Where will we go for healthcare in 2020?

• Sickness?

• Wellness?

1515

A 20/20 Vision to 2020

1616

Healthcare will be… …on the sickness sideCentrally Delivered•

& other consumer distribution centers• Genetic Screening• Pharmacy Distribution• “Doc‐in‐the‐Box”, staffed with nurse practitioners

Specialized Delivery• Comprehensive cancer / cardiovascular centers• “Heart Transplants ‘R’ Us” (surgery centers)• Complex diseases

Home Diagnostics/Monitoring systems: • Drop blood onto your Blackberry or iPod, telecommunicated to central

labs, real‐time Dx/Px• Home monitoring

1717

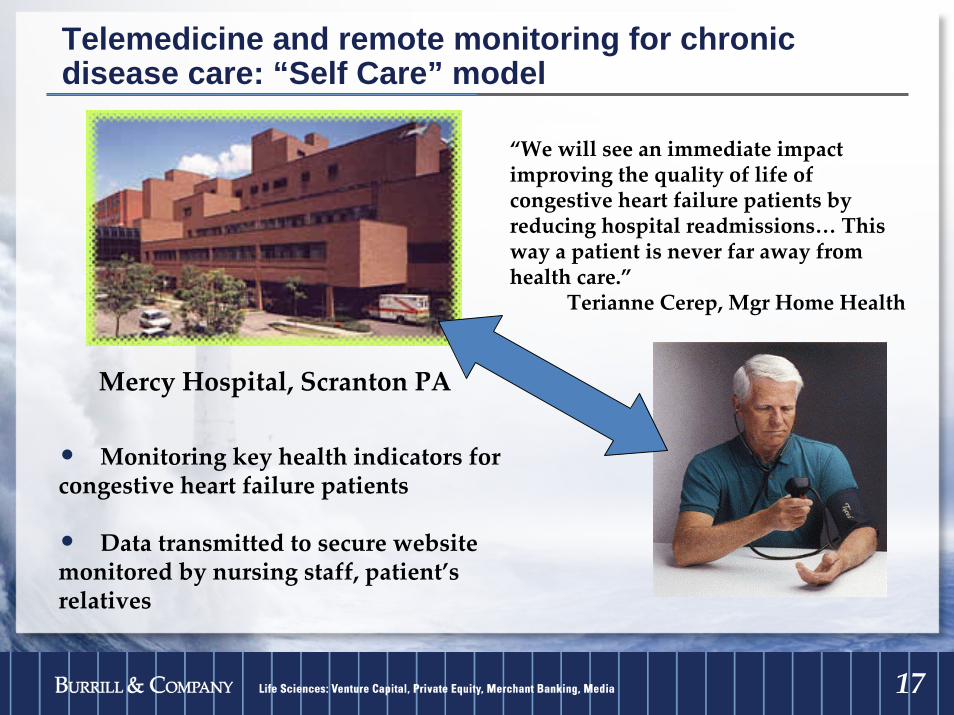

Telemedicine and remote monitoring for chronic disease care: “Self Care” model

Mercy Hospital, Scranton PA

“We will see an immediate impact improving the quality of life of congestive heart failure patients by reducing hospital readmissions… This way a patient is never far away from health care.”

Terianne Cerep, Mgr Home Health

• Monitoring key health indicators for congestive heart failure patients

• Data transmitted to secure website monitored by nursing staff, patient’s relatives

1818

Mobile and Home Health Monitoring• Chronic disease – diabetes, congestive

heart failure, etc. – accounts for 75% of medical costs in the US

• Disease management can substantially improve patient outcomes and lower cost

• Medical devices and telecommunications technologies are converging to develop monitoring and control systems for patients with chronic disease

• Aging, remote monitoring

1919

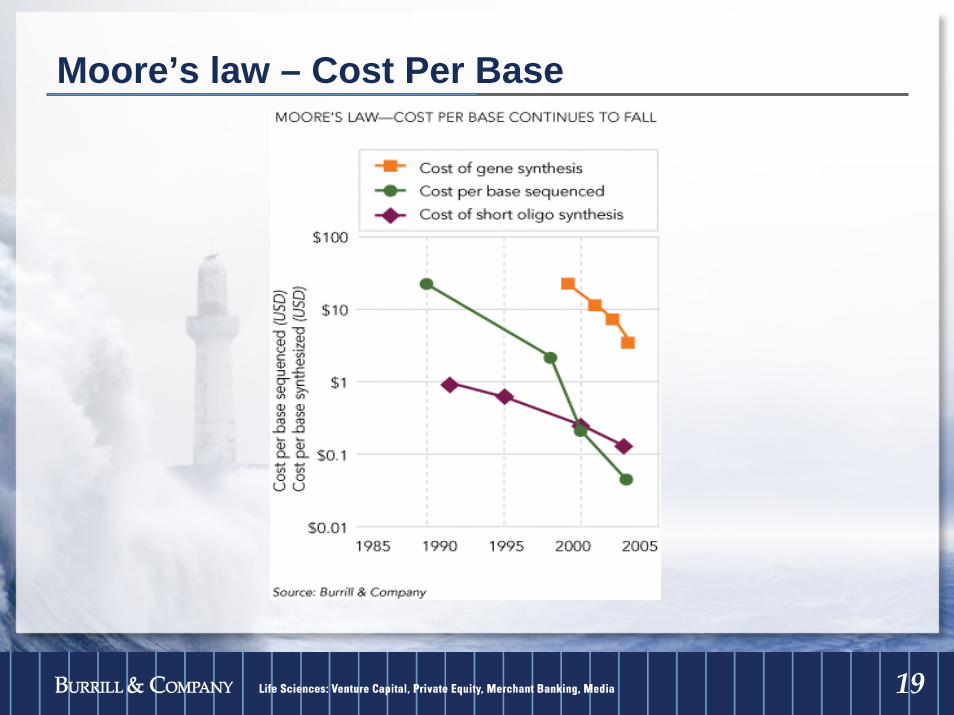

Moore’s law – Cost Per Base

2020

And where is technology taking us?Moore’s Law

• ID of genetic markers/links for most disease (algorithms of biomarkers)

Note: from a value standpoint‐ “Genes ‘R’ Us” model failed quickly; individual biomarker “valve” also likely to decline rapidly

• Genetic screening becomes normal

• Understanding of biochemical mechanisms of most diseases

Therefore: personalization (customization) of healthcare

2121

Longer Term Risk Assessment (prediction) Driving to Prevention:

• Genome wide association studies not just BRAC 1&2NavigenicsDeCode23andMe

• Shorter term, high accuracy risk assessment/clinical support tools

ProventysLabcorpQuestRocheGenomic HealthXDxCardioDx

2222

Healthcare will be…digitized• Smart cards with electronic health records & sequenced

DNA• Consumer driven personal health planning

PHR o Microsoft ‐HealthVault™o Google Healtho WebMDo Revolution Healtho WalMart/Dell

Europe / Asia may be faster, more integrated than US

2323

Tracking & Feedback• Nike/Apple –iPod Nano and online

workouts/equipment/fitness linked

• Tools to monitor medication regiments to drive compliance

• Tools to measureActivitySleepFood consumption

2424

Rapid Secure Communication with Doctors

• Relay health (McKesson)

• Minute clinic

• FitNet

2525

Nano/Bio/Regenerative MedicineNano devices in blood vessels “roaming under own power”

to diagnose and fix problems• Nanoparticles:

Removing bacteria from foodAdding nutrientsAids in packaging/retaining freshness

Artificial Organs/Regenerative Medicine:Heart, lungs, pancreas, liver, kidney, blood, eyes, ears, legs, hands, etc.

Advanced Prosthetics:Arms, legs, hands‐ all with biological/ technological / psychological interaction sensors

2626

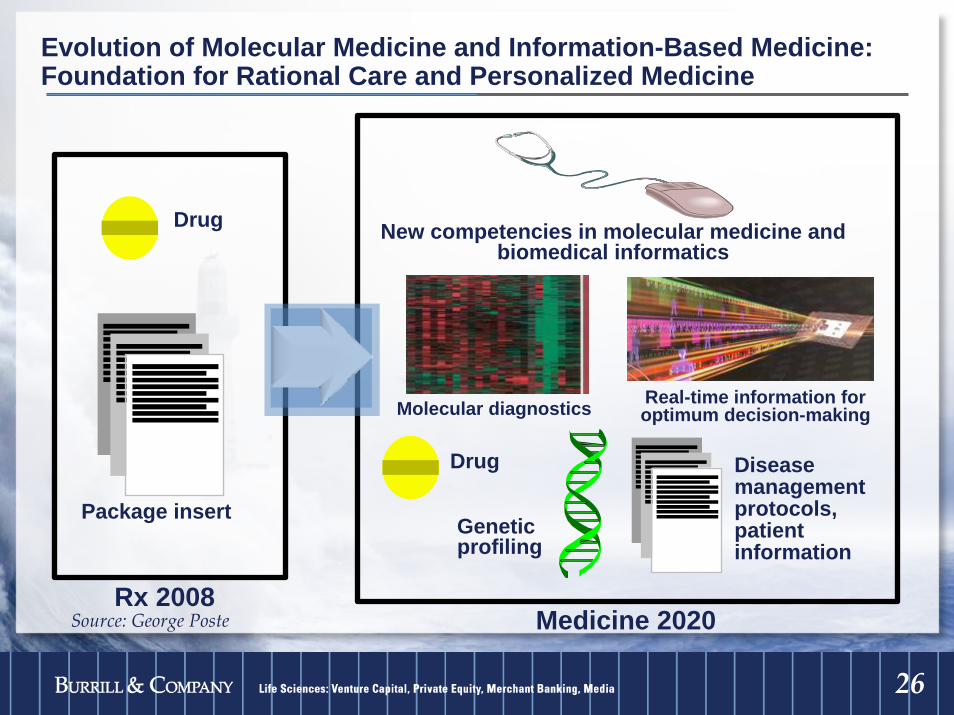

Medicine 2020Rx 2008

Drug

Geneticprofiling

Drug

Package insert

Diseasemanagementprotocols,patientinformation

New competencies in molecular medicine and biomedical informatics

Real-time information for optimum decision-makingMolecular diagnostics

Evolution of Molecular Medicine and Information-Based Medicine: Foundation for Rational Care and Personalized Medicine

Source: George Poste

2727

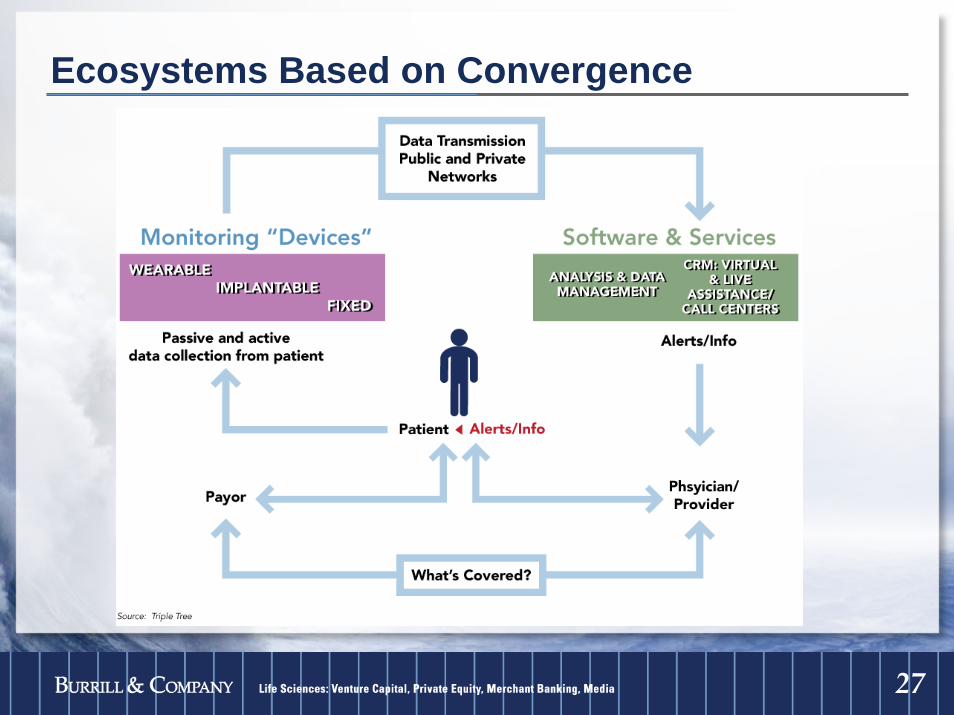

Ecosystems Based on Convergence

2828

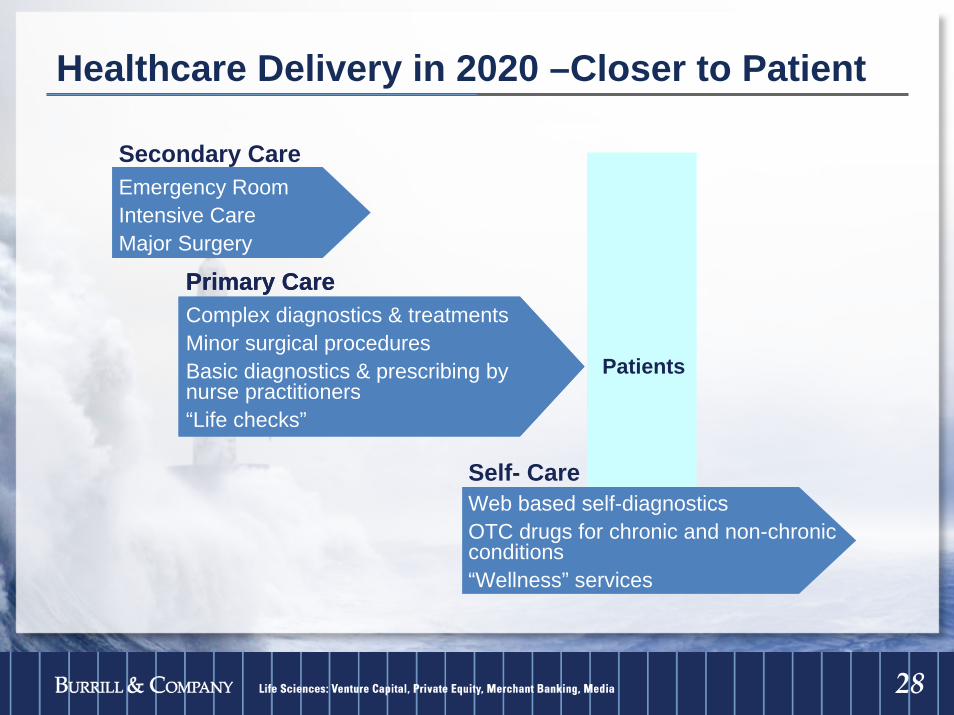

Primary CareComplex diagnostics & treatmentsMinor surgical proceduresBasic diagnostics & prescribing by nurse practitioners“Life checks”

Healthcare Delivery in 2020 –Closer to Patient

Patients

Secondary CareEmergency RoomIntensive CareMajor Surgery

Self- CareWeb based self-diagnosticsOTC drugs for chronic and non-chronic conditions“Wellness” services

Primary CareComplex diagnostics & treatmentsMinor surgical proceduresBasic diagnostics & prescribing by nurse practitioners“Life checks”

2929

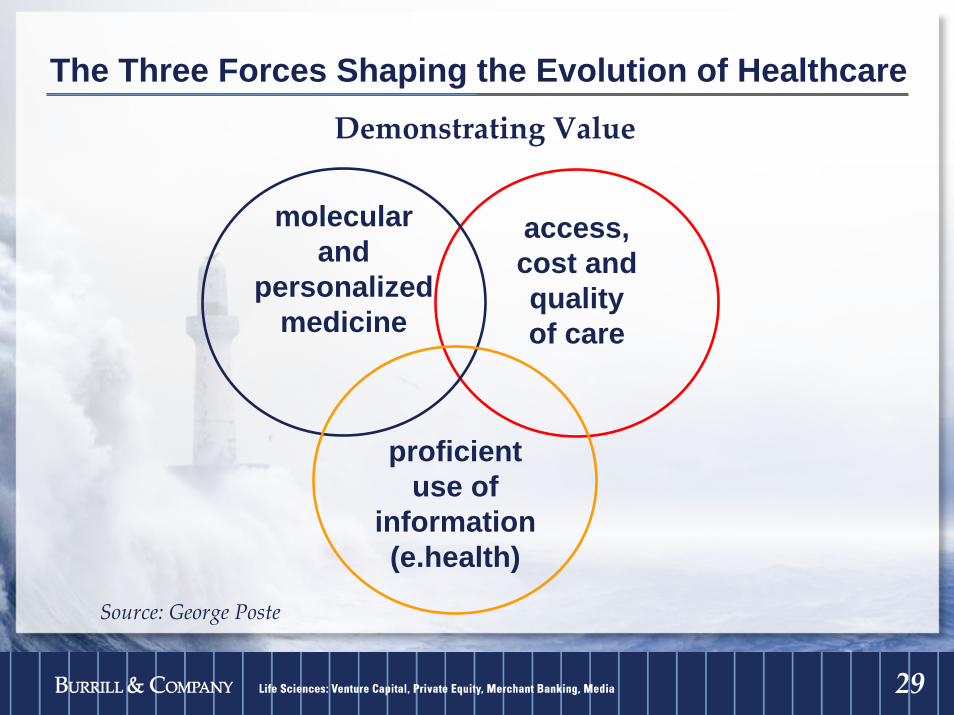

The Three Forces Shaping the Evolution of HealthcareDemonstrating Value

Source: George Poste

access,cost andqualityof care

molecularand

personalizedmedicine

proficientuse of

information(e.health)

3030

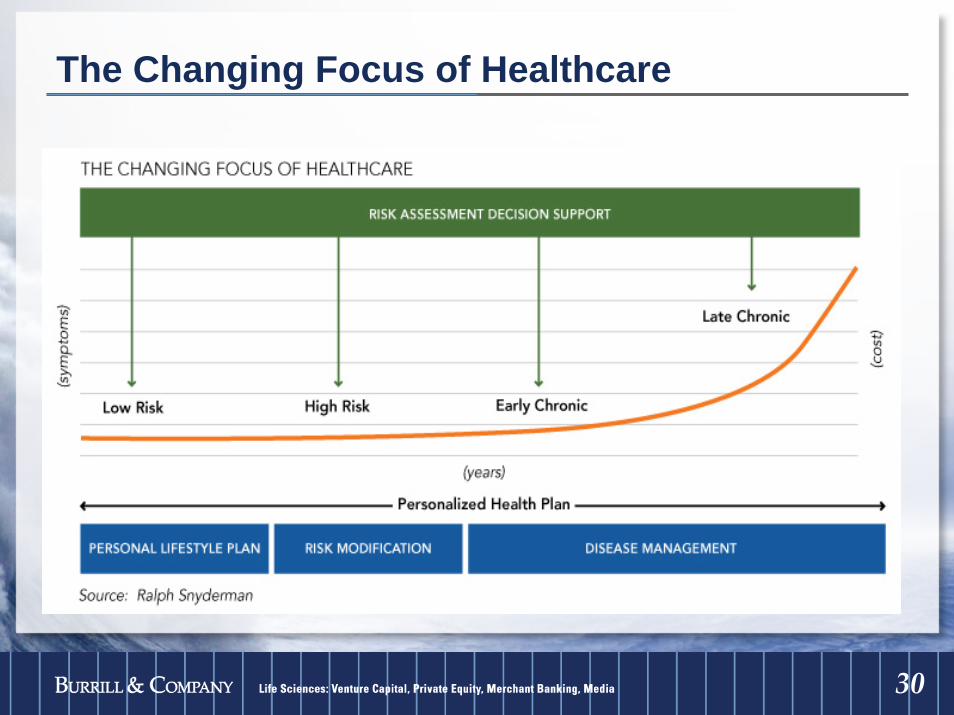

The Changing Focus of Healthcare

3131

Market Distortions and Perverse Incentives in Modern Healthcare Delivery

• Focus on late‐stage detection and interventionHigh costLow reversibility

• Multiple reimbursements for fragmented (siloed) care versus integrated management of patient needs

• Medical professionals paid for illness versus wellness• Inadequate social and economic incentives for wellness• Inadequate medical training/understanding of

genetics/genomics/proteomics

Source: George Poste / Burrill & Company

3232

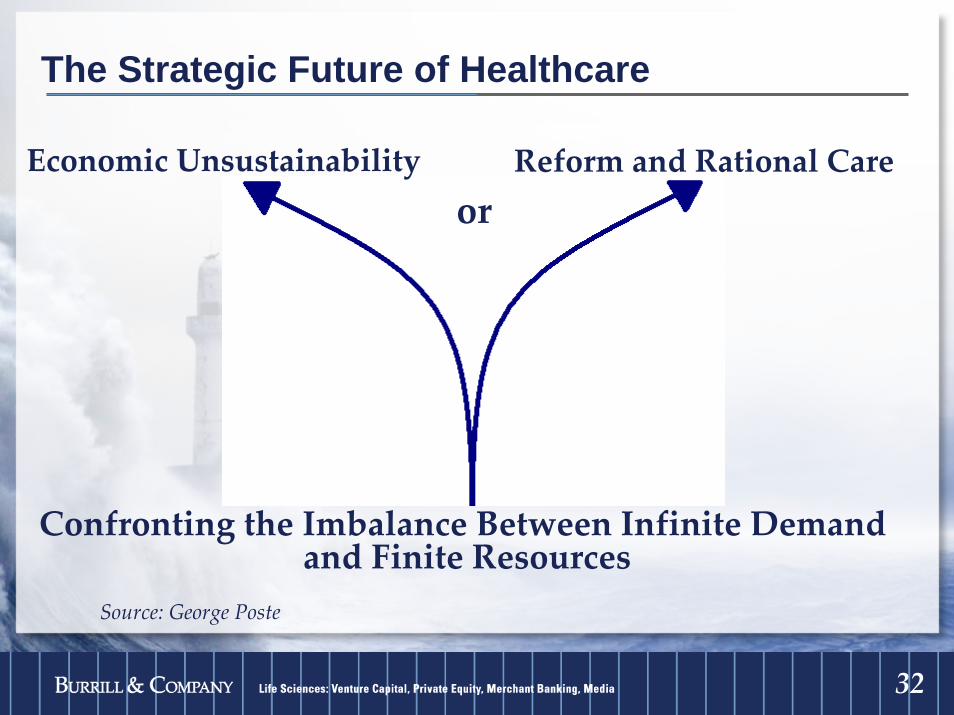

The Strategic Future of Healthcare

Economic Unsustainability Reform and Rational Care

Confronting the Imbalance Between Infinite Demand and Finite Resources

or

Source: George Poste

3333

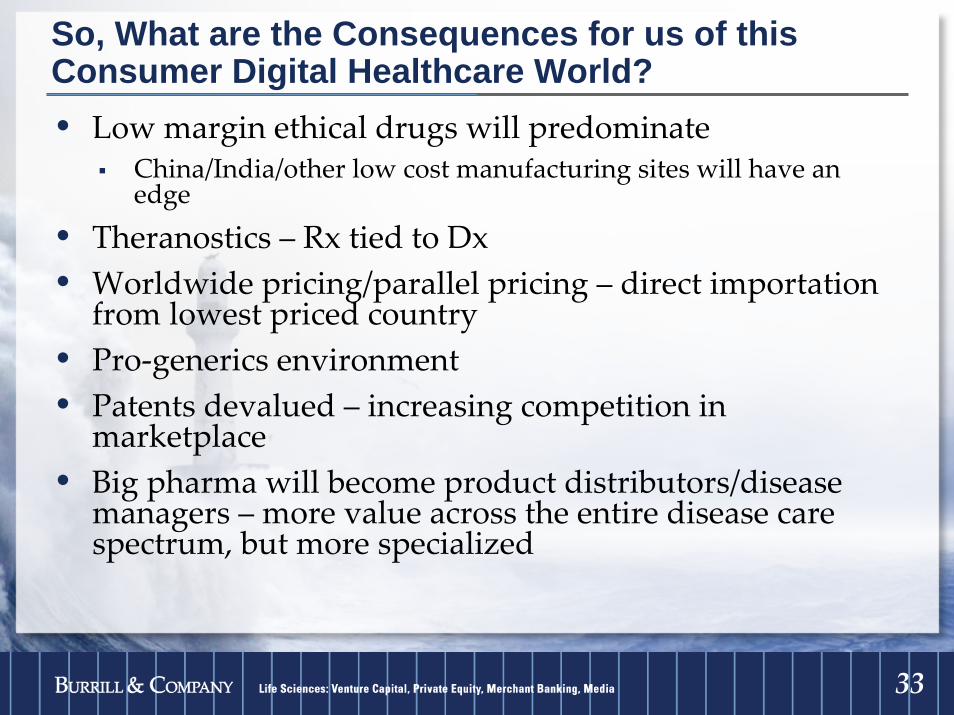

So, What are the Consequences for us of this Consumer Digital Healthcare World?• Low margin ethical drugs will predominate

China/India/other low cost manufacturing sites will have an edge

• Theranostics – Rx tied to Dx• Worldwide pricing/parallel pricing – direct importation

from lowest priced country• Pro‐generics environment• Patents devalued – increasing competition in

marketplace• Big pharma will become product distributors/disease

managers – more value across the entire disease care spectrum, but more specialized

3434

2020 –Globalization / Changing the environment too

• Markets ‐ demand increases in Asia & developing world

• R&D migrates to Asia

• Regulations – International agencies collaborate

• Information – healthcare payors share data on performance (clinical & financial)

• Diseases know no boundaries

• Every company is global from day one!

3535

Start-up’s Globalness Begins Day 1• Science/technology• Intellectual property/patents/FTO• People• Communications• Competition• Capital• Markets—diseases know no borders

Even the smallest company is a global player from Day One

3636

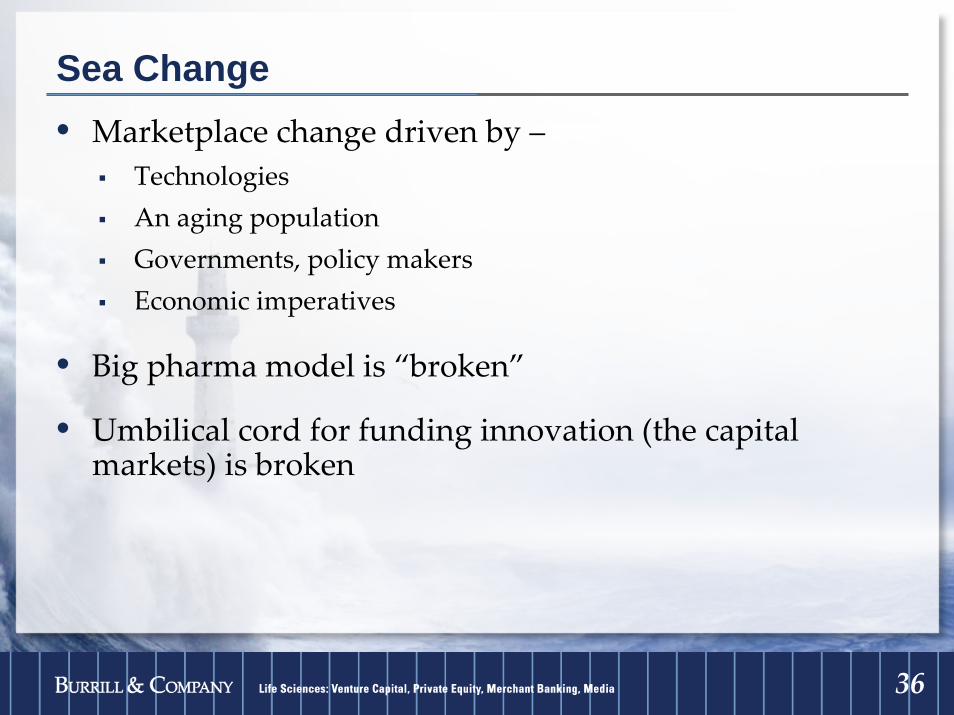

Sea Change• Marketplace change driven by –

TechnologiesAn aging populationGovernments, policy makersEconomic imperatives

• Big pharma model is “broken”

• Umbilical cord for funding innovation (the capital markets) is broken

3737

…and so, healthcare “reform” is on everyone’s agenda

• Politicians/Congress/White House/Gov’t Leaders

• Payors/Reimbursors/Insurers

• Physicians/Providers

• Patients/Consumers

…and patients are empowered, have economic cost, and really

want to stay well!

3838

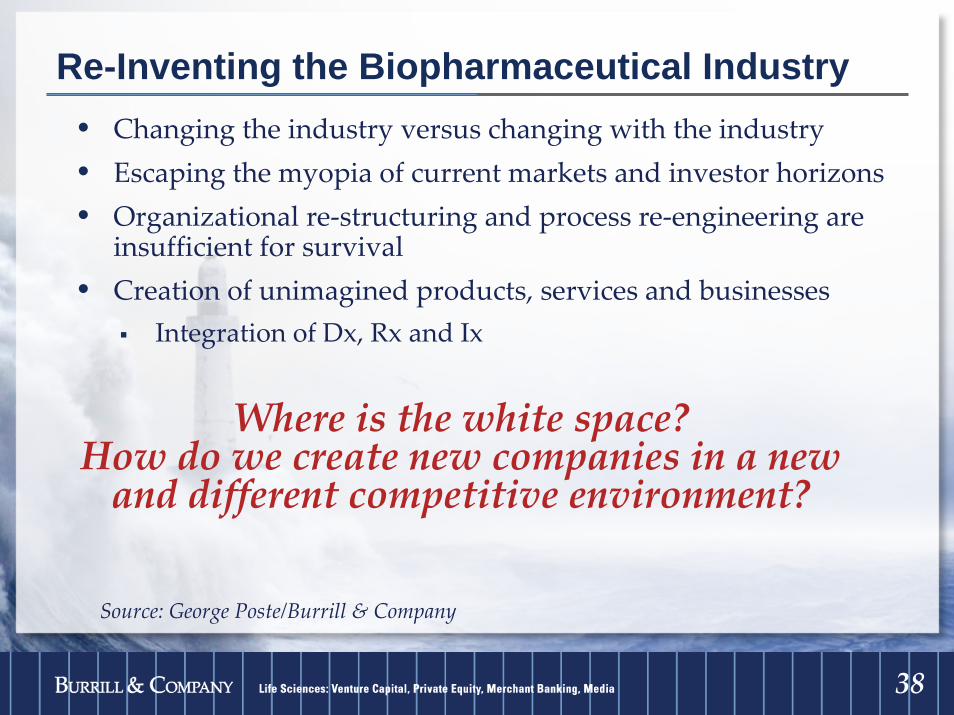

Re-Inventing the Biopharmaceutical Industry• Changing the industry versus changing with the industry• Escaping the myopia of current markets and investor horizons• Organizational re‐structuring and process re‐engineering are

insufficient for survival• Creation of unimagined products, services and businesses

Integration of Dx, Rx and Ix

Source: George Poste/Burrill & Company

Where is the white space? How do we create new companies in a new and different competitive environment?

3939

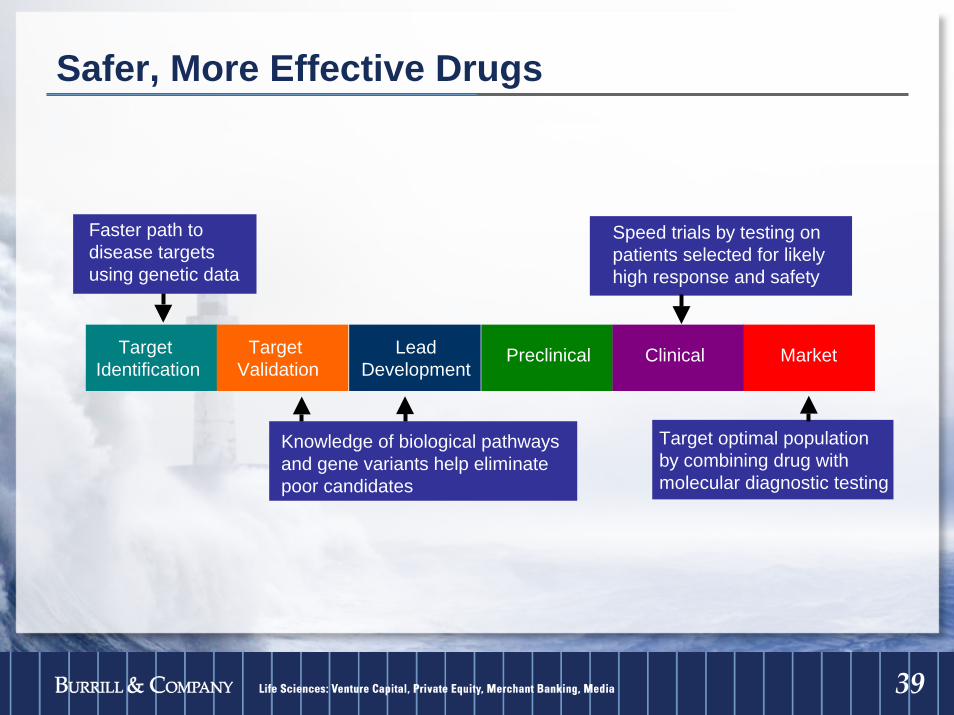

Safer, More Effective Drugs

Target Identification

Target Validation

LeadDevelopment

Preclinical Clinical Market

Faster path todisease targetsusing genetic data

Speed trials by testing onpatients selected for likelyhigh response and safety

Knowledge of biological pathwaysand gene variants help eliminatepoor candidates

Target optimal populationby combining drug withmolecular diagnostic testing

4040

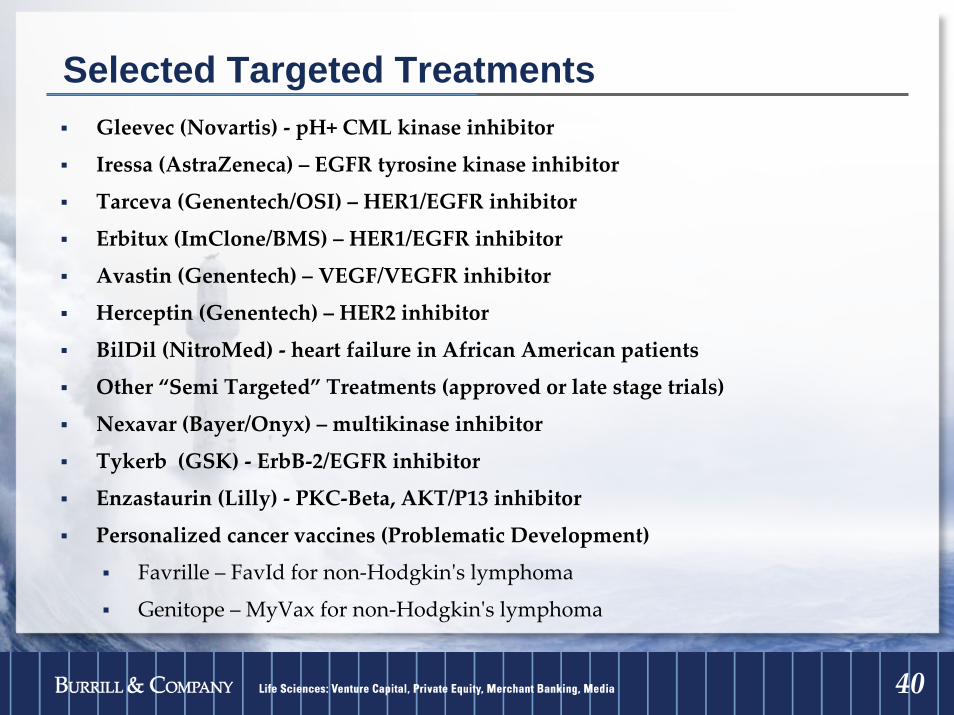

Selected Targeted TreatmentsGleevec (Novartis) ‐ pH+ CML kinase inhibitor

Iressa (AstraZeneca) – EGFR tyrosine kinase inhibitor

Tarceva (Genentech/OSI) – HER1/EGFR inhibitor

Erbitux (ImClone/BMS) – HER1/EGFR inhibitor

Avastin (Genentech) – VEGF/VEGFR inhibitor

Herceptin (Genentech) – HER2 inhibitor

BilDil (NitroMed) ‐ heart failure in African American patients

Other “Semi Targeted” Treatments (approved or late stage trials)

Nexavar (Bayer/Onyx) – multikinase inhibitor

Tykerb (GSK) ‐ ErbB‐2/EGFR inhibitor

Enzastaurin (Lilly) ‐ PKC‐Beta, AKT/P13 inhibitor

Personalized cancer vaccines (Problematic Development)

Favrille – FavId for non‐Hodgkinʹs lymphoma

Genitope – MyVax for non‐Hodgkinʹs lymphoma

4141

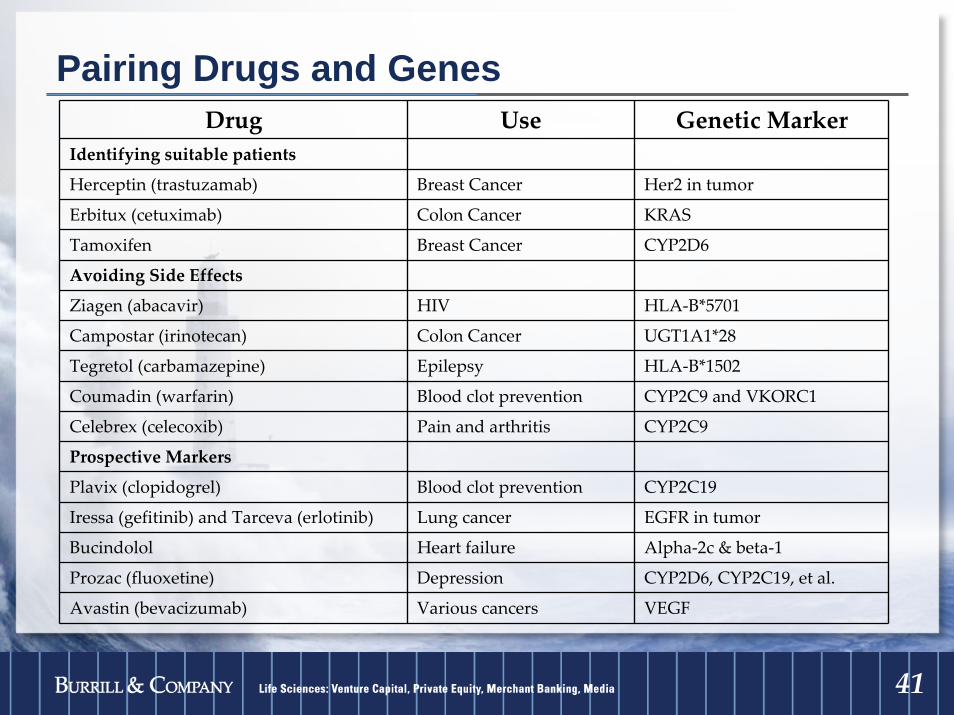

Pairing Drugs and GenesDrug Use Genetic Marker

Identifying suitable patients

Herceptin (trastuzamab) Breast Cancer Her2 in tumor

Erbitux (cetuximab) Colon Cancer KRAS

Tamoxifen Breast Cancer CYP2D6

Avoiding Side Effects

Ziagen (abacavir) HIV HLA‐B*5701

Campostar (irinotecan) Colon Cancer UGT1A1*28

Tegretol (carbamazepine) Epilepsy HLA‐B*1502

Coumadin (warfarin) Blood clot prevention CYP2C9 and VKORC1

Celebrex (celecoxib) Pain and arthritis CYP2C9

Prospective Markers

Plavix (clopidogrel) Blood clot prevention CYP2C19

Iressa (gefitinib) and Tarceva (erlotinib) Lung cancer EGFR in tumor

Bucindolol Heart failure Alpha‐2c & beta‐1

Prozac (fluoxetine) Depression CYP2D6, CYP2C19, et al.

Avastin (bevacizumab) Various cancers VEGF

4242

Healthcare Changes to Wellness (vs. sickness)• Healthcare moves from one size fits all to the three/four P’s:

PersonalizationPredictionPrevention / disease preemptionPatient Responsibility

• Increased life span (80s are new 60s; 100s are new 80s)Health maintenanceFitnessEat for life

4343

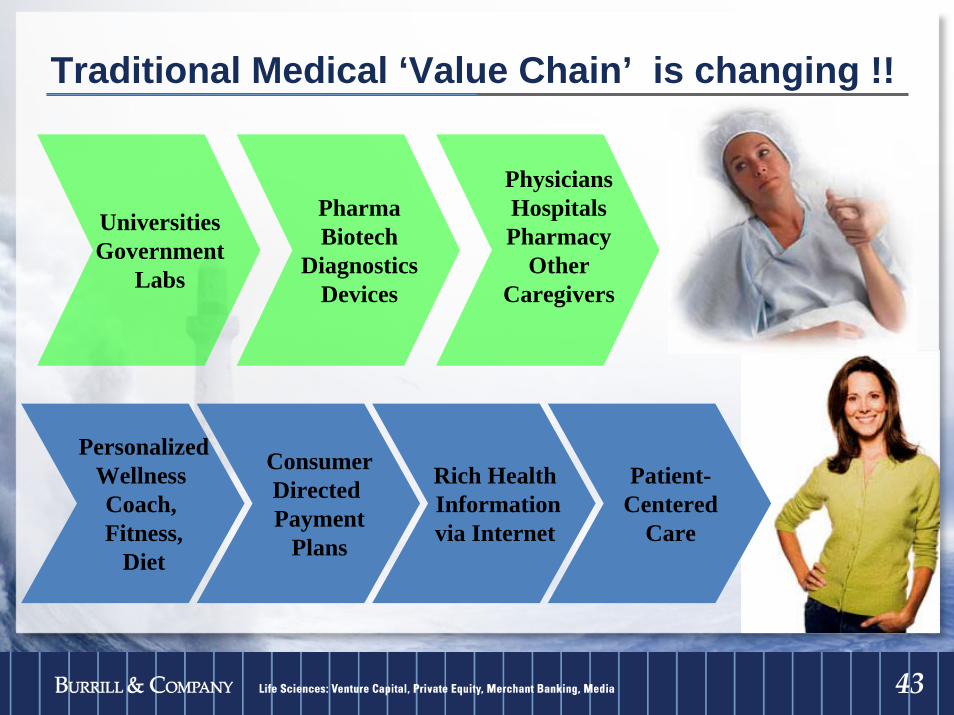

Traditional Medical ‘Value Chain’ is changing !!

UniversitiesGovernment

Labs

PharmaBiotech

DiagnosticsDevices

PhysiciansHospitalsPharmacy

OtherCaregivers

PersonalizedWellness Coach, Fitness,

Diet

ConsumerDirected Payment

Plans

Rich HealthInformation via Internet

Patient-Centered

Care

4444

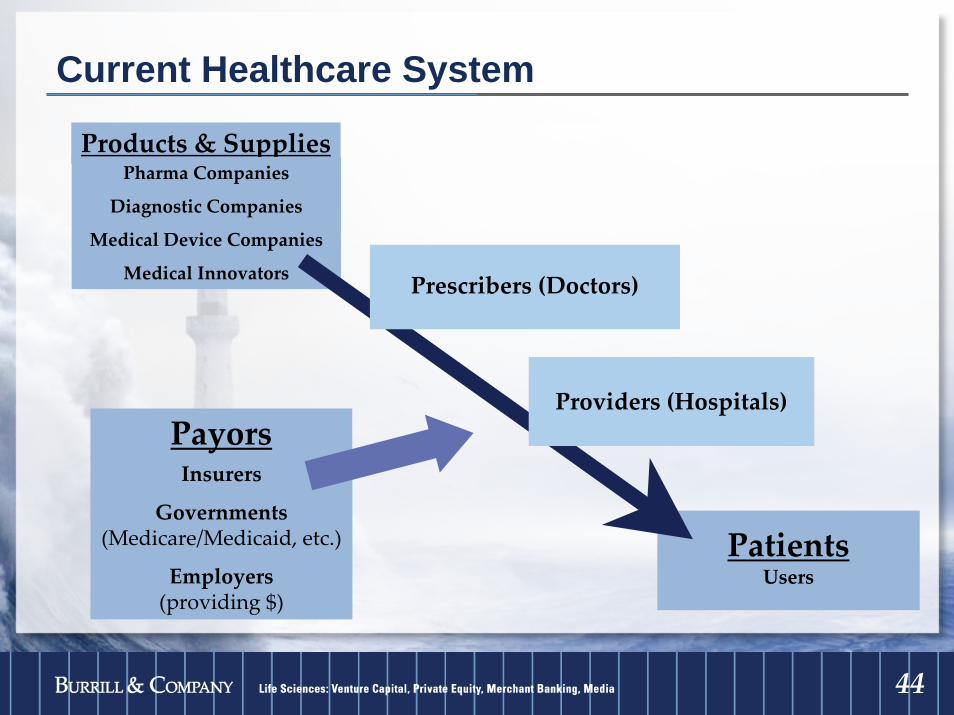

PatientsUsers

Current Healthcare System

PayorsInsurers

Governments (Medicare/Medicaid, etc.)

Employers (providing $)

Products & SuppliesPharma Companies

Diagnostic Companies

Medical Device Companies

Medical Innovators Prescribers (Doctors)

Providers (Hospitals)

4545

Reimbursement• Who is the payor?

Government?Employers?Patients?

• Studies in comparative effectiveness –who will pay for this?

• Evidentiary framework should not be left to payors(CMS/HHS/Kaiser/Aetna, etc.)

Pharmaco‐economic benefit tests?

4646

Efficacy

Drug is 30% effective

vs.

Drug effective for 30% of the market

4747

Big “New” Markets

• Alzheimerʹs/memory

• Obesity/diabetes/metabolic disease

• Anti‐aging

• Anti infectives (antibiotic resistance)

• Wellness (preventative/predictive cure)

4848

Generics –Why is it Booming?

• Major blockbusters coming off patent

• Scale/globalization is key

• Emerging markets growing

• Fewer NCE approvals

• Little growth in primary care markets

4949

Regulatory News – FDA Developments 2008/2009• LabCorpʹs OvaSure Dx ʹHigh Risk,ʹ Validation ʹInadequate’

• Draft Guidance on Regulating Genetically Engineered Animals

• Warning Letters to Ranbaxy Laboratories Ltd., and an Import Alert for Drugs from Two Ranbaxy Plants in India

• Revision of Process for Responding to Drug Applications; moves from “Approvable” and “Not‐Approvable” to “Complete Response” letters

• Attempts to harmonize pharmacogenomic definitions and sample coding guidance

• Establishing eight full time permanent FDA positions at U.S. diplomatic posts in China, pending authorization from the Chinese government

• Watch out for Sidney Wolfe – 4 year term on the FDA’s Drug Safety and Risk Management Committee

5050

On the Regulatory/Patent/Policy Front…Gov’ts are our Partners!• Patent reform (PTO proposals to restrict claims examined in a single application and

limit continuation applications)• FDA resources – PDUFA IV authorization

follow‐on biologics (biogenerics)drug safetytheranosticsfood safety (pet food)

• Biofuels – renewable and alternative energy sources through use of biotechnology• Medicare Prescription Drug Price Negotiation Act – Non‐interference (proposal to

require Medicare interference)• Sarbanes Oxley compliance – reducing the burden on small companies• SBIR eligibility• Agbio/ GMO’s• Stem cell research – federal funding• Passing of Genetic Information Non‐Discrimination Act (GINA)• Bailouts (US, UK)?

5151

Major Government Initiatives in Biotechnology

• Canada• EU: Scandinavia, Germany, UK, Spain, Italy, Switzerland• Eastern Europe• China• India• Japan• Korea• Malaysia• Singapore• UAE (Dubai/Abu Dhabi), Bahrain and Kuwait• Israel• Latin America (esp. Chile/Brazil/Argentina)• Australia/New Zealand

5252

Biotech and Healthcare are Global Businesses

ASEAN

MIDDLE EAST

ISRAEL

AUS/NZ

CANADA

INDIA

CHINA

USA

UK/EUROPE

JAPAN

LATIN AMERICA

5353

World Market for Health and Wellness is Expanding• China and India have large populations, growing wealth

and middle class and increased demand for high quality healthcare

Additional growth markets: Middle East, Latin America, South Africa, Russia, Eastern Europe

• Burden of disease is changing in developed and developing countries: chronic diseases (cardiovascular, diabetes, cancer, CNS et al.) on the rise everywhere

• Aging populations around the world• National healthcare and private payor/employer models

are converging and all facing issues of affordability, quality and equal access

Consumers becoming an important factor in the healthcare equation

5454

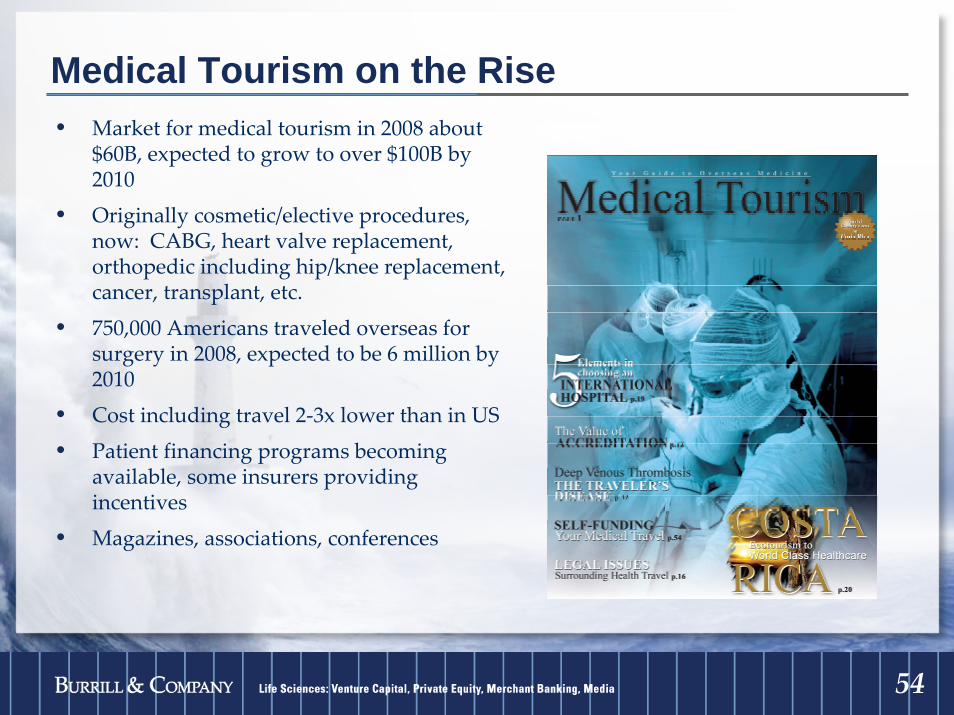

Medical Tourism on the Rise• Market for medical tourism in 2008 about

$60B, expected to grow to over $100B by 2010

• Originally cosmetic/elective procedures, now: CABG, heart valve replacement, orthopedic including hip/knee replacement, cancer, transplant, etc.

• 750,000 Americans traveled overseas for surgery in 2008, expected to be 6 million by 2010

• Cost including travel 2‐3x lower than in US

• Patient financing programs becoming available, some insurers providing incentives

• Magazines, associations, conferences

5555

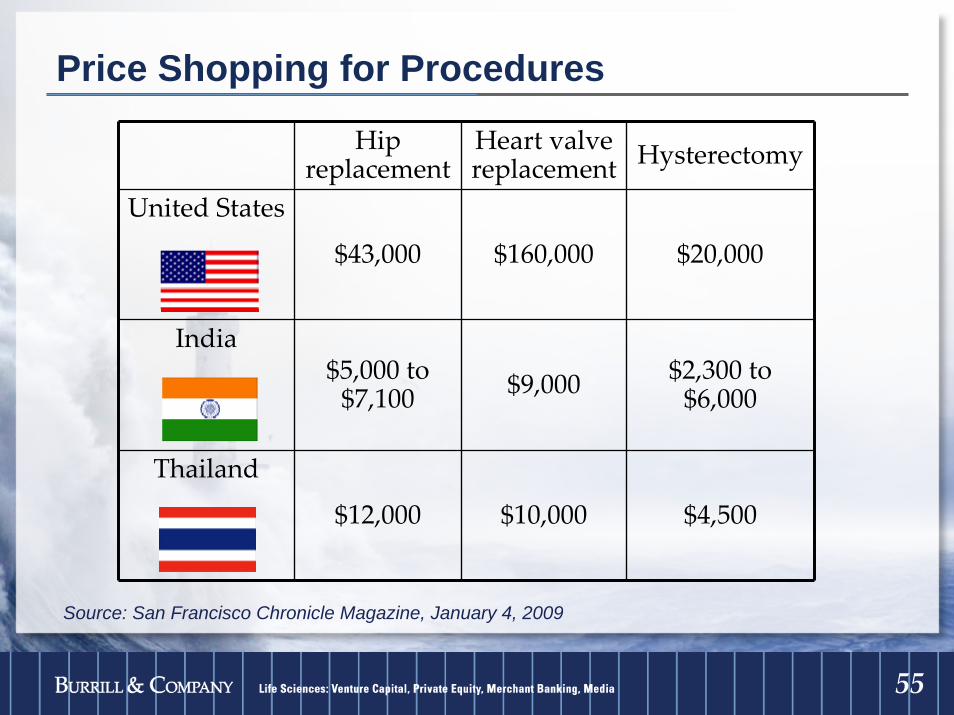

Price Shopping for Procedures

Hip replacement

Heart valve replacement Hysterectomy

United States

$43,000 $160,000 $20,000

India$5,000 to $7,100 $9,000 $2,300 to

$6,000

Thailand

$12,000 $10,000 $4,500

Source: San Francisco Chronicle Magazine, January 4, 2009

5656

Medical Tourism Growth Drivers• India

Gov’t investing $3.6 Billion in medical tourism infrastructure.McKinsey estimates Indian medical tourism at $2.3B by 2012.

• MexicoStarMedica hospital groups built 7 hospitals in last 5 years;AmeriMed opening 10 new hospitals by 2012; Grupo Angeles (largest private hospital group in Mexico) spending $700 million to build 15 hospitals in the next 3 years

• SingaporeMore internationally accredited facilities than any other country.

• ThailandOne Bangkok hospital (Bumrungrad) served over 500,000 health travelers last year.

• Costa RicaOne in five visitors is a medical tourist Source: Health Travel Guides

5757

Wall Street’s Implosion…What does it mean to us?It’s a sea change, not a temporary blip

• We’ve had ≈ 30‐40 years of relatively easy access to relatively cheap capital

That game is OVER! Capital markets permanently restructured

• Access to capitalMore difficult to find (IB resources for micro‐cap stocks decreased)More expensiveBuyside interest/resources reduced (Hedge funds gone)VC/private investors (deep pockets/short arms) business is challenging – no IPOs for exits

• Big Pharma – not as eager (things will be cheaper if they wait)

5858

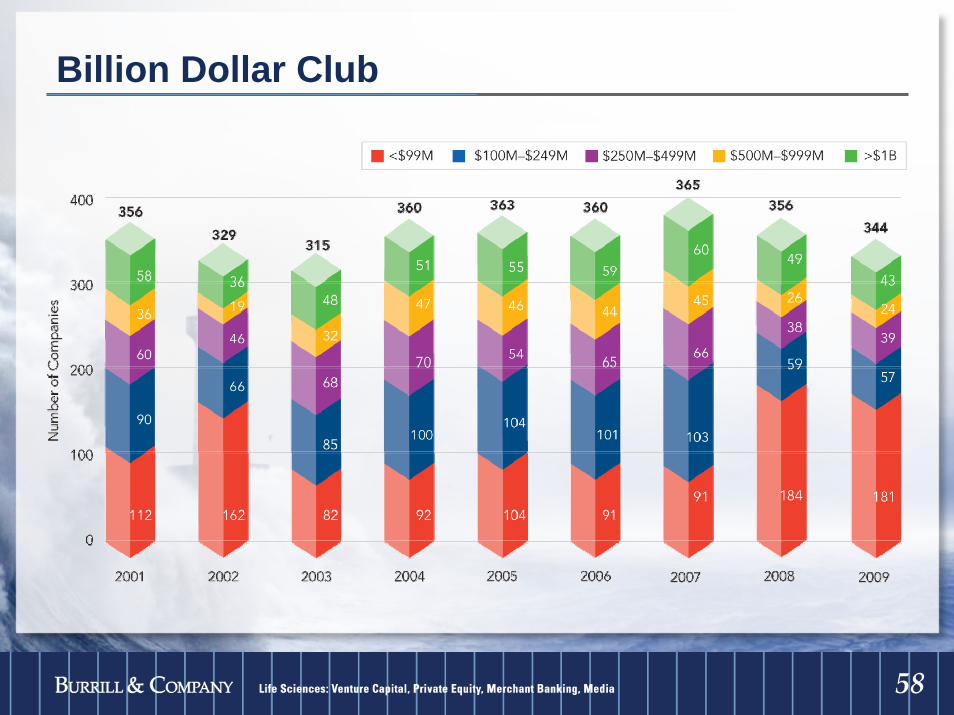

Billion Dollar Club

5959

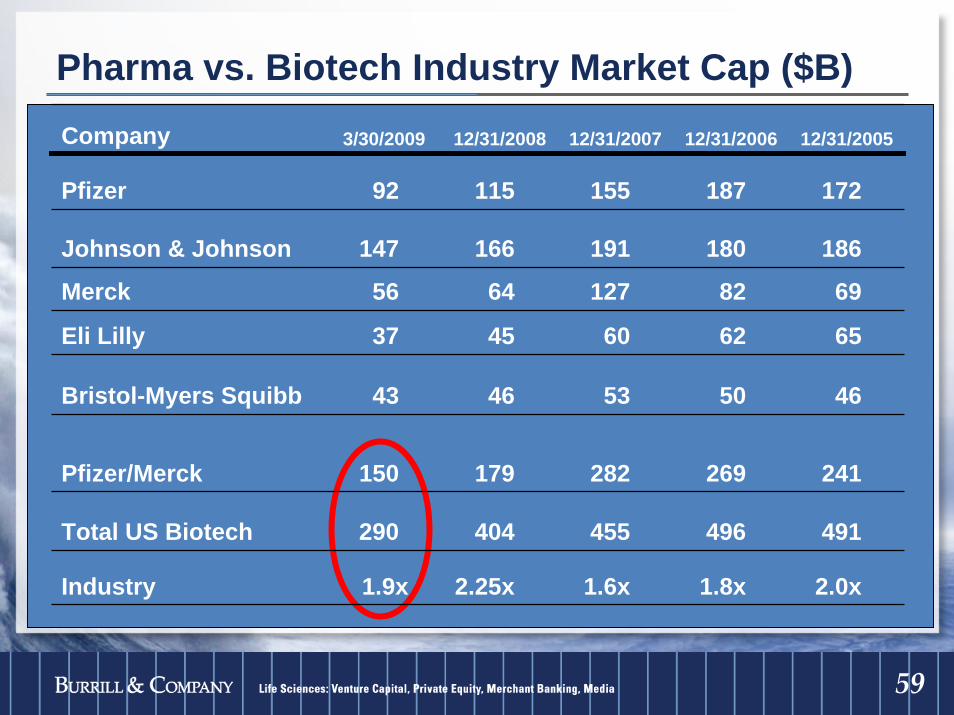

Pharma vs. Biotech Industry Market Cap ($B)Company 3/30/2009 12/31/2008 12/31/2007 12/31/2006 12/31/2005

Pfizer 92 115 155 187 172

Johnson & Johnson 147 166 191 180 186

Merck 56 64 127 82 69

Eli Lilly 37 45 60 62 65

Bristol-Myers Squibb 43 46 53 50 46

Pfizer/Merck 150 179 282 269 241

Total US Biotech 290 404 455 496 491

Industry 1.9x 2.25x 1.6x 1.8x 2.0x

6060

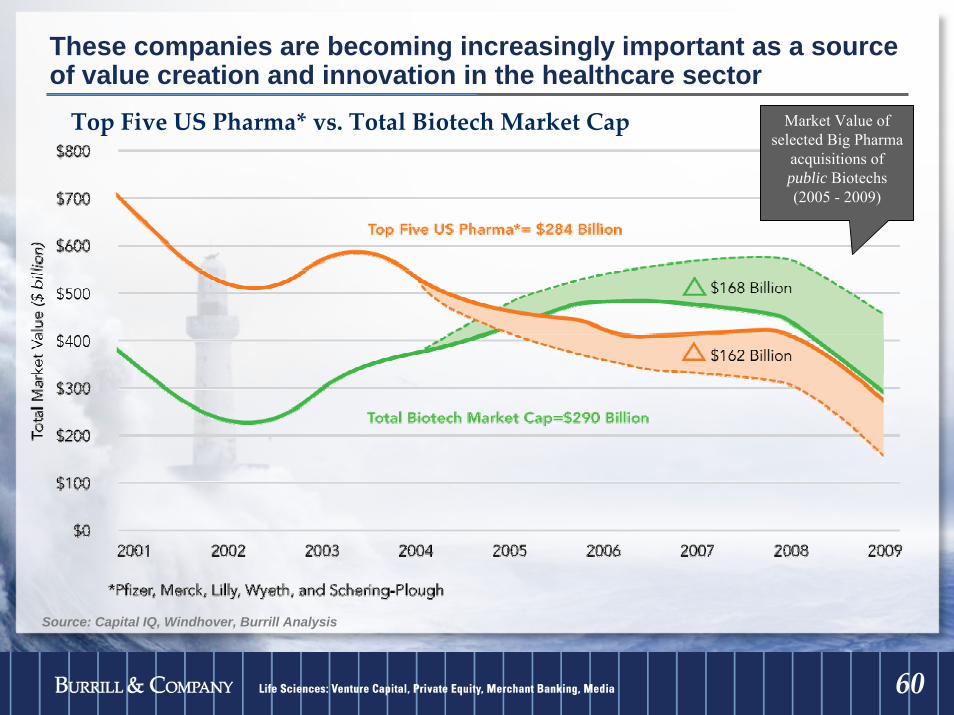

These companies are becoming increasingly important as a source of value creation and innovation in the healthcare sector

Source: Capital IQ, Windhover, Burrill Analysis

Top Five US Pharma* vs. Total Biotech Market Cap Market Value of selected Big Pharma

acquisitions of public Biotechs(2005 - 2009)

6161

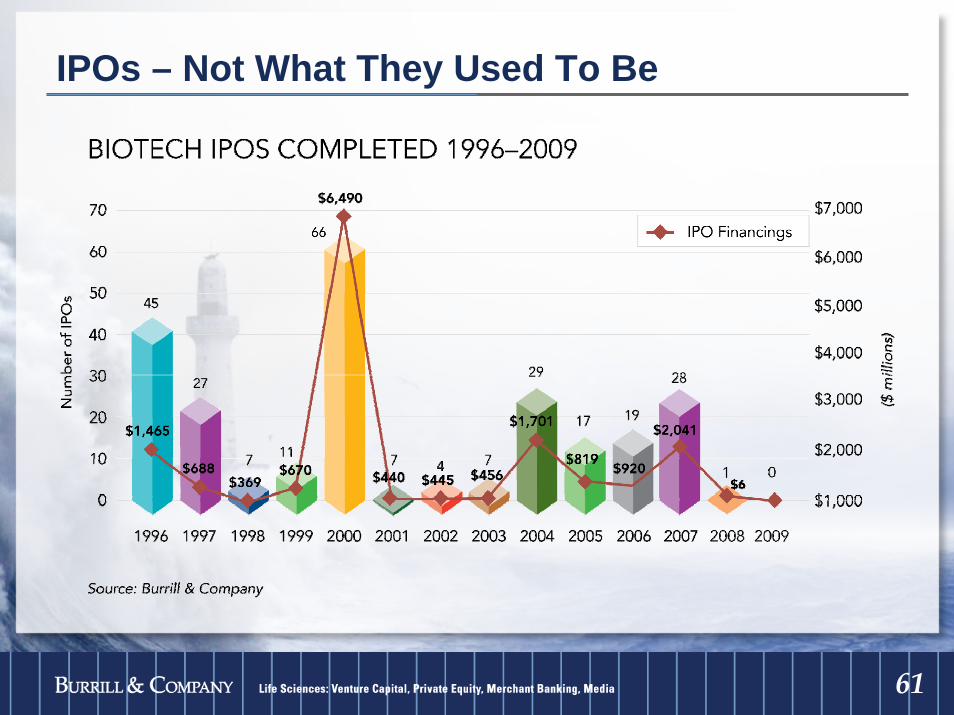

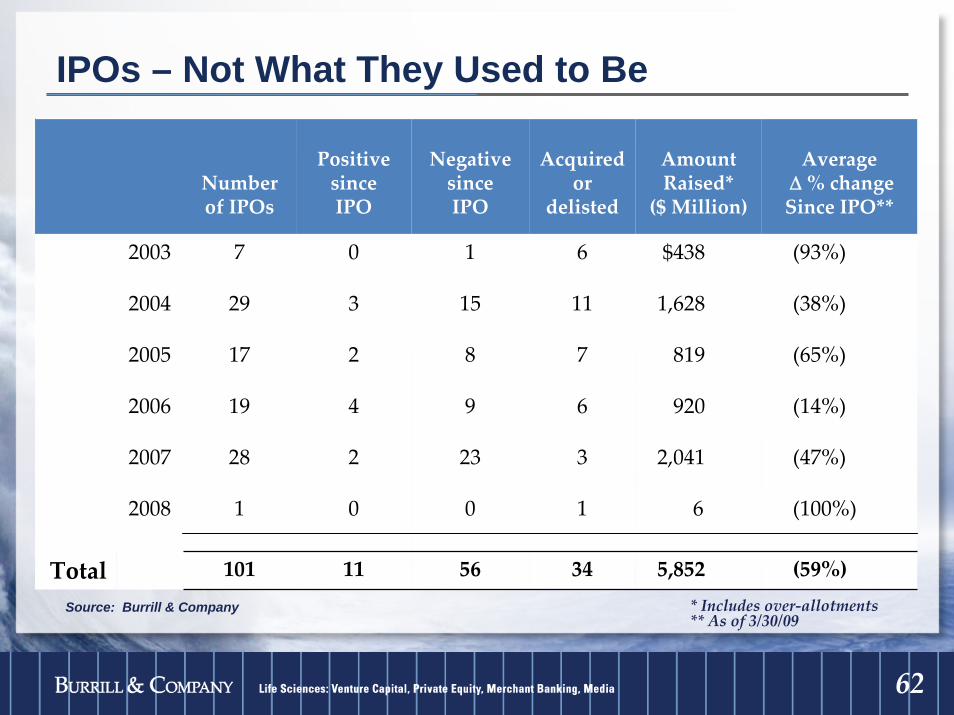

IPOs – Not What They Used To Be

6262

IPOs – Not What They Used to Be

Number of IPOs

Positive sinceIPO

NegativesinceIPO

Acquired or

delisted

Amount Raised*($ Million)

AverageΔ% changeSince IPO**

2003 7 0 1 6 $438 (93%)

2004 29 3 15 11 1,628 (38%)

2005 17 2 8 7 819 (65%)

2006 19 4 9 6 920 (14%)

2007

2008

28

1

2

0

23

0

3

1

2,041

6

(47%)

(100%)

Total 101 11 56 34 5,852 (59%)* Includes over‐allotments ** As of 3/30/09

Source: Burrill & Company

6363

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

12/3

1/20

071/

14/2

008

1/28

/200

82/

11/2

008

2/25

/200

83/

10/2

008

3/24

/200

84/

7/20

084/

21/2

008

5/5/

2008

5/19

/200

86/

2/20

086/

16/2

008

6/30

/200

87/

14/2

008

7/28

/200

88/

11/2

008

8/25

/200

89/

8/20

089/

22/2

008

10/6

/200

810

/20/

2008

11/3

/200

811

/17/

2008

12/1

/200

812

/15/

2008

12/2

9/20

081/

12/2

009

1/26

/200

92/

9/20

092/

23/2

009

3/9/

2009

3/23

/200

9

DJIANASDAQBurrill Select

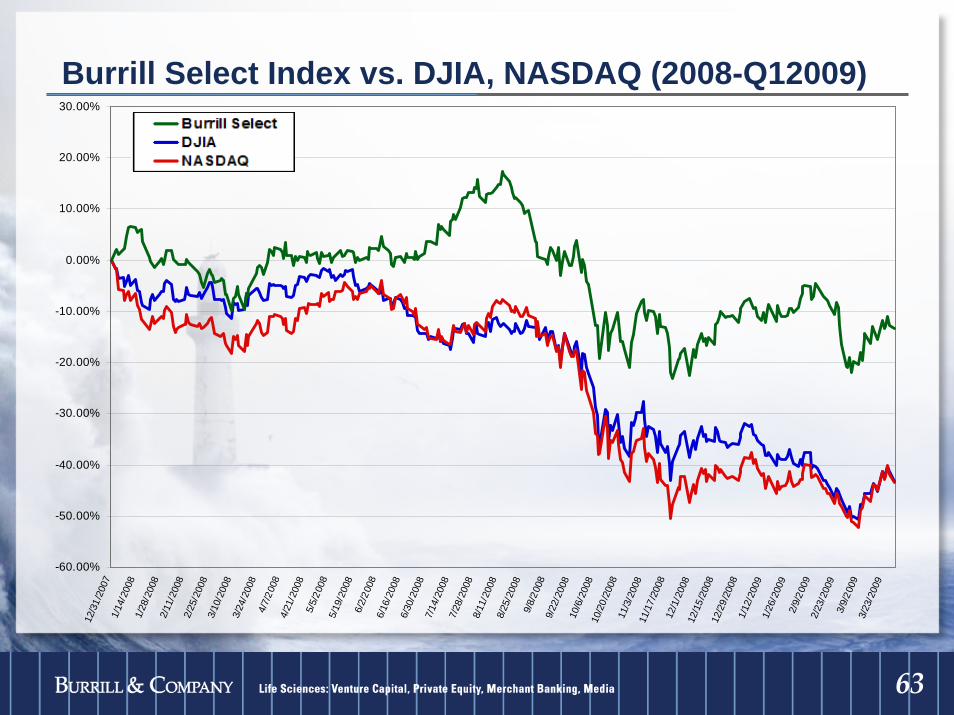

Burrill Select Index vs. DJIA, NASDAQ (2008-Q12009)

6464

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09

MidCapSmallCapLargeCap

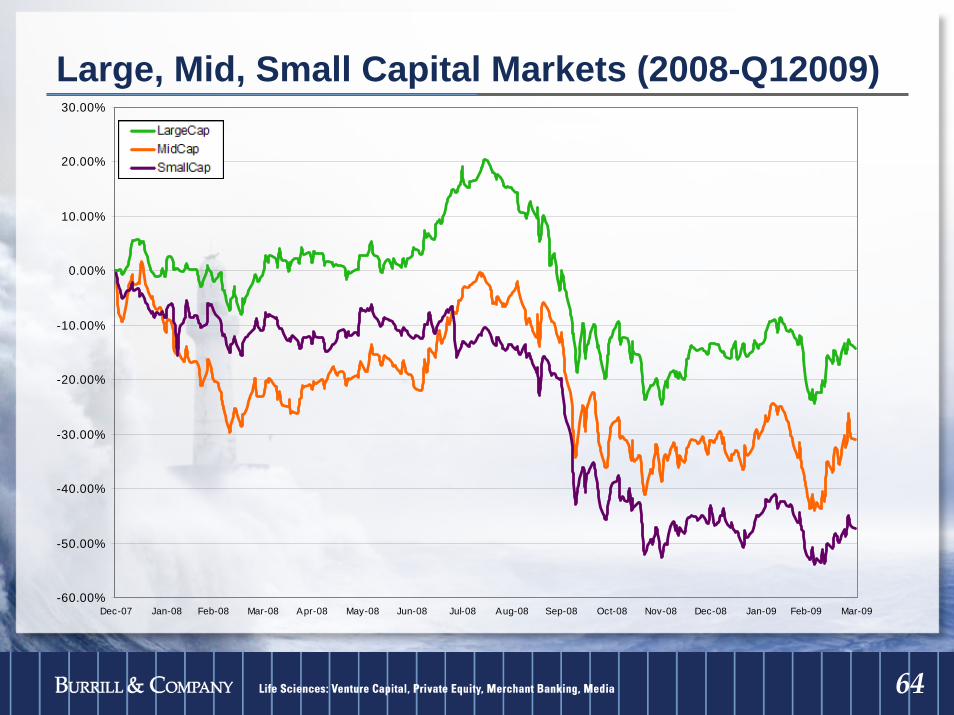

Large, Mid, Small Capital Markets (2008-Q12009)

6565

Large, Mid, Small Capital Markets (2003 – Q12009)

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

12/31

/2003

2/29/2

0044/3

0/2004

6/30/2

0048/3

1/2004

10/31

/2004

12/31

/2004

2/28/2

0054/3

0/2005

6/30/2

0058/3

1/2005

10/31

/2005

12/31

/2005

2/28/2

0064/3

0/2006

6/30/2

0068/3

1/2006

10/31

/2006

12/31

/2006

2/28/2

0074/3

0/2007

6/30/2

0078/3

1/2007

10/31

/2007

12/31

/2007

2/29/2

0084/3

0/2008

6/30/2

0088/3

1/2008

10/31

/2008

12/31

/2008

2/28/2

009

Large CapMidCapSmallCap

6666

Significant Mergers and Acquisitions 2008-2009

Pharma/SpecialtyPharma/Specialty

Pharma/BiotechPharma/Biotech

Shionogi/Sciele$ 11 billion

Novartis/Alcon$ 10.4 billion

Roche/Genentech$ 46 billion

King/Alpharma$ 1.6 billion

Pfizer/Wyeth$ 68 billion

Biotech/BiotechBiotech/Biotech

DiagnosticsDiagnostics

MedtechMedtech

Invitrogen/Applied Biosystems$ 6.7 billion

Gilead/CV Therapeutics$ 1.4 billion

Roche/Ventana$ 3.4 billion

Kinetic Concepts/LifeCell

$ 1.7 billion

Fresenius/APP Pharma

$ 3.7 billion

Hologic/Third Wave$580 million

CSL/Talecris$ 3.1 billion

Takeda/Millennium$ 8.2 billion

Eli Lilly/ImClone$ 6.2 billion

Celgene/Pharmion$ 2.7 billion

Inverness/BBI$ 100 million

Boehringer/Actimis$ 515 million

ViroPharma/Lev Pharma

$ 618 million

Johnson & Johnson/Mentor

$ 1.07 billion

Eisai/MGI Pharma$ 3.5 billion

Inverness/Paradigm$ 230 million

Pharma/PharmaPharma/PharmaMerck/Schering

Plough$ 41.1 billion

6767

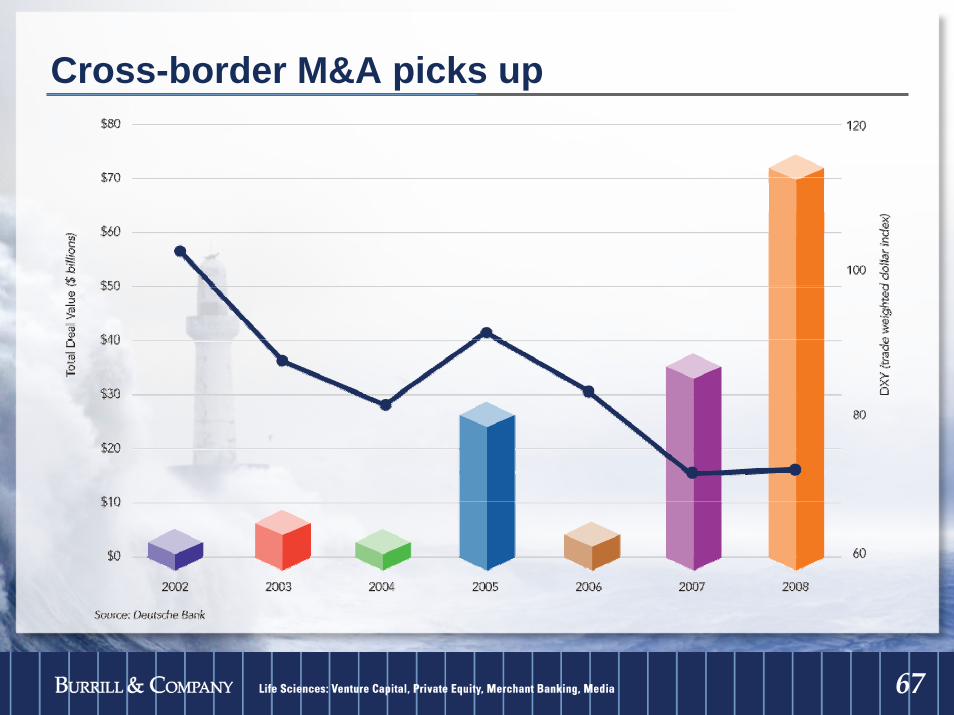

Cross-border M&A picks up

6868

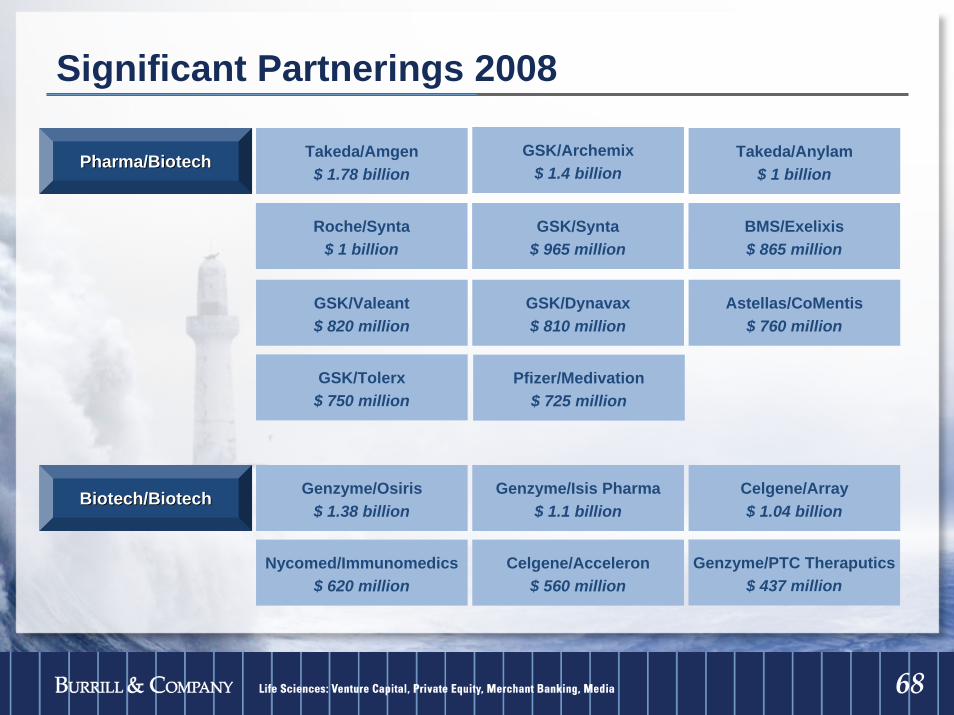

Significant Partnerings 2008

Pharma/BiotechPharma/Biotech Takeda/Amgen$ 1.78 billion

GSK/Archemix$ 1.4 billion

GSK/Valeant$ 820 million

Takeda/Anylam$ 1 billion

GSK/Dynavax$ 810 million

Astellas/CoMentis$ 760 million

GSK/Tolerx$ 750 million

Biotech/BiotechBiotech/Biotech Genzyme/Osiris$ 1.38 billion

Genzyme/Isis Pharma$ 1.1 billion

Nycomed/Immunomedics$ 620 million

Celgene/Array$ 1.04 billion

Celgene/Acceleron$ 560 million

Roche/Synta$ 1 billion

GSK/Synta$ 965 million

BMS/Exelixis$ 865 million

Pfizer/Medivation$ 725 million

Genzyme/PTC Theraputics$ 437 million

6969

How Does All This Impact Entrepreneurial Start-ups in 2009?• VC & Angels are hesitant to invest

Business models are changingMore financing of projects

• Higher bar for regulatory approval

• Reimbursement compression

• Globality essential

• Capital efficiency required

BUT…

• Rate of start‐ups around the world are increasing(go figure…)

7070

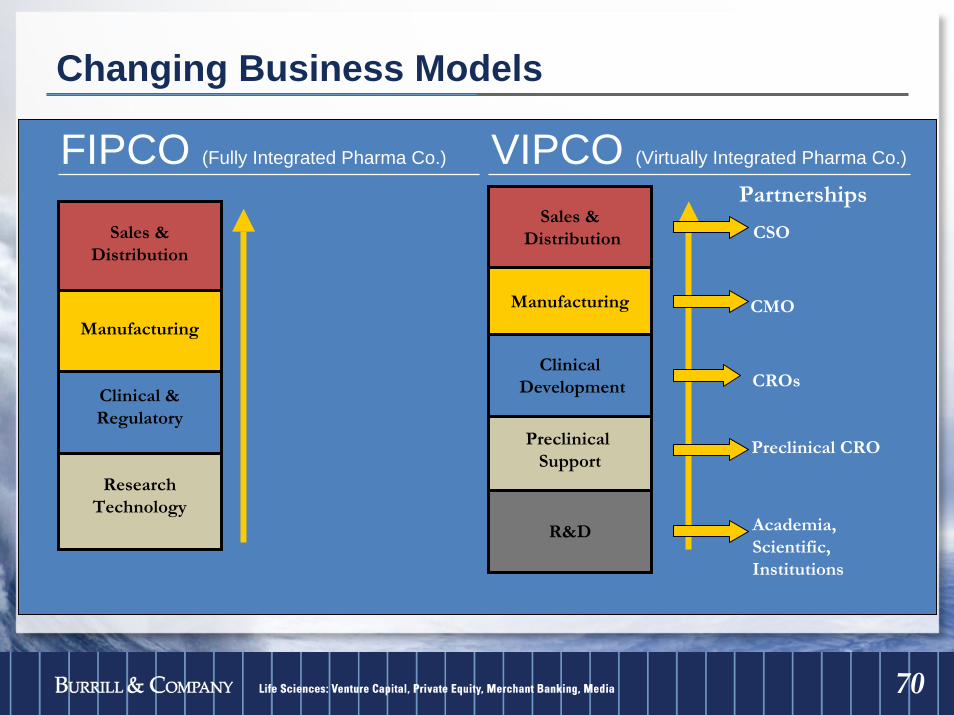

FIPCO (Fully Integrated Pharma Co.)

ResearchTechnology

Manufacturing

Clinical &Regulatory

Sales &Distribution

CSO

CMO

CROs

Partnerships

Academia, Scientific, Institutions

R&D

Preclinical Support

ClinicalDevelopment

Manufacturing

Sales &Distribution

Preclinical CRO

VIPCO (Virtually Integrated Pharma Co.)

Changing Business Models

7171

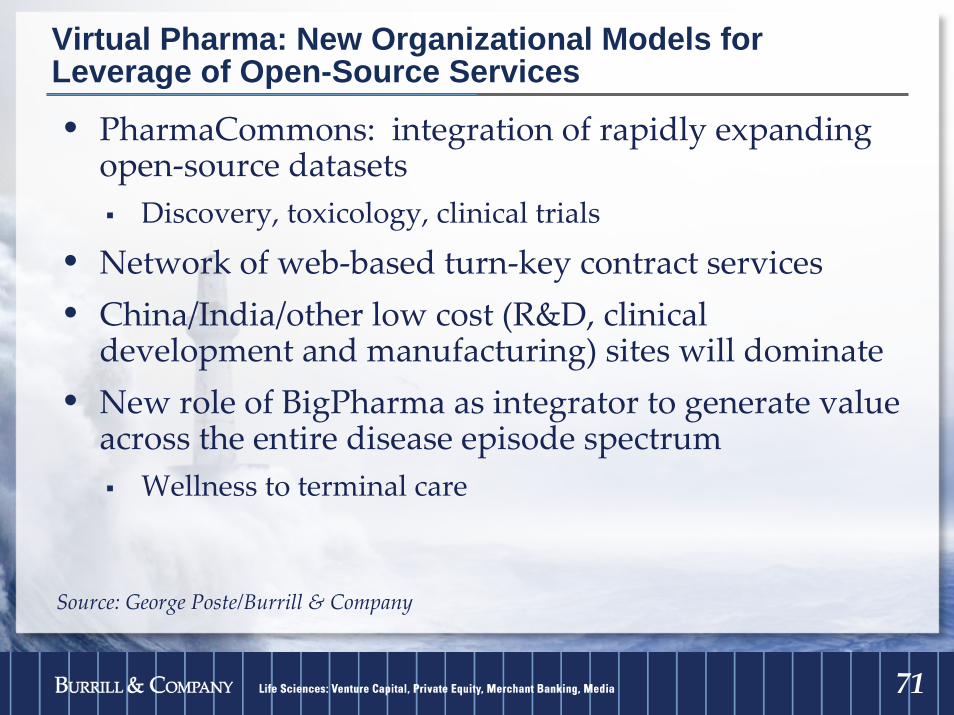

Virtual Pharma: New Organizational Models for Leverage of Open-Source Services

• PharmaCommons: integration of rapidly expanding open‐source datasets

Discovery, toxicology, clinical trials

• Network of web‐based turn‐key contract services• China/India/other low cost (R&D, clinical

development and manufacturing) sites will dominate• New role of BigPharma as integrator to generate value

across the entire disease episode spectrumWellness to terminal care

Source: George Poste/Burrill & Company

7272

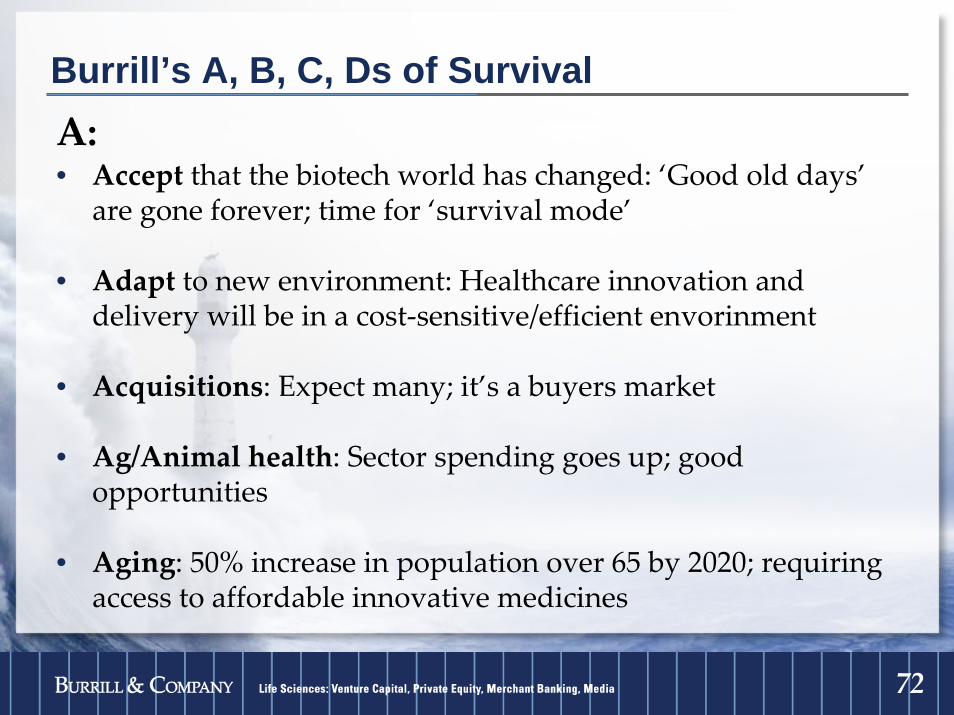

Burrill’s A, B, C, Ds of SurvivalA: • Accept that the biotech world has changed: ‘Good old days’

are gone forever; time for ‘survival mode’

• Adapt to new environment: Healthcare innovation and delivery will be in a cost‐sensitive/efficient envorinment

• Acquisitions: Expect many; it’s a buyers market

• Ag/Animal health: Sector spending goes up; good opportunities

• Aging: 50% increase in population over 65 by 2020; requiring access to affordable innovative medicines

7373

Burrill’s A, B, C, Ds of Survival (continued)

B:• Bailout: Don’t expect one; though US stimulus trickle down will

create pockets of opportunity• BioGreenTech: The revolution is here; be a part of it• Big Pharma: Be creative in your dealings with them; they have the

cash for M&A• Biomarkers are booming globally; where the action will be in all

stages of drug development• Biosimilars are set to offer lucrative returns; significant opportunity• Business models: Virtual companies and networks are being

formed• Buying opportunities: This will be the best year ever• Bankruptcies: Some companies will disappear

7474

Burrill’s A, B, C, Ds of Survival (continued)

C:• Chronic diseases: More than 75% of healthcare is spent on them; a fundamental

shift is needed from treating sickness to promoting wellness

• Conserve cash: Work on the programs that will yield the most value, put the rest on ice

• Creative: Finance the valubale parts of your company; individual components may have greater value than as part of the whole

• Climate change: VC investment in clean tech is hot; big opportunities for job and wealth creation

• Comparative effectiveness: Dialogue is essential for this critical issue of effectiveness vs. cost

• Convergence of technologies: Emphasis on translational research in biomedicine, and cross‐fertilization of biotech, nanotech, and information technology; promise of innovative solutions provide fabulous business opportunities

7575

Burrill’s A, B, C, Ds of Survival (continued)

D:• Dilution: Remove this word from your vocab; cash will be

expensive, but you’ll need it

• Drug prices: More transparency, competition and generics; perceived and proven value for patients and payors will be critical

• Different but better: We will come through these turbulent times and be better for it!

7676

So…

When the going gets tough, the tough get going –

77

G. Steven BurrillChief Executive OfficerBurrill & Company

Oracle Life Science ForumApril 15, 2009

But doth suffer a sea‐change, into something rich and strange…

—William Shakespeare, The Tempest

Biotech 2009: Life SciencesNavigating the Sea Change