Embed Size (px)

Citation preview

©2004 Burrill & Company. Confidential & Proprietary.

11

Biotech 2006Life Sciences: A Changing Prescription

NY Pharma

October 19th, 2006

G. Steven Burrill, CEOBurrill & Company

©2004 Burrill & Company. Confidential & Proprietary.

22

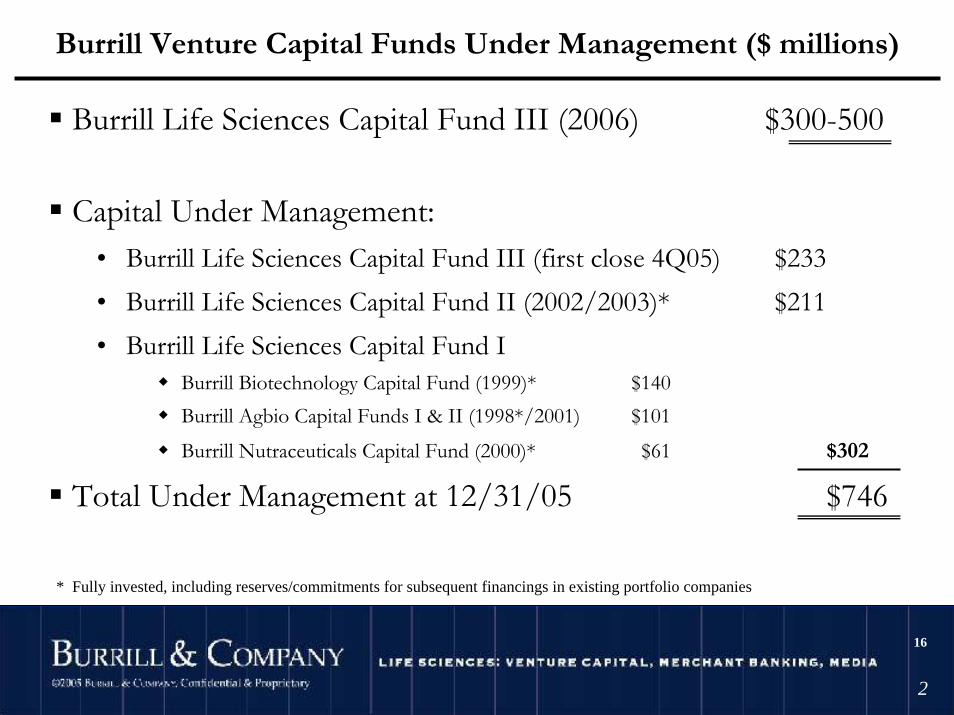

Burrill Venture Capital Funds Under Management ($ millions)

Burrill Life Sciences Capital Fund III (2006) $300-500

Capital Under Management:• Burrill Life Sciences Capital Fund III (first close 4Q05) $233• Burrill Life Sciences Capital Fund II (2002/2003)* $211• Burrill Life Sciences Capital Fund I

Burrill Biotechnology Capital Fund (1999)* $140Burrill Agbio Capital Funds I & II (1998*/2001) $101

Burrill Nutraceuticals Capital Fund (2000)* $61 $302

Total Under Management at 12/31/05 $746

* Fully invested, including reserves/commitments for subsequent financings in existing portfolio companies

16

©2004 Burrill & Company. Confidential & Proprietary.

33

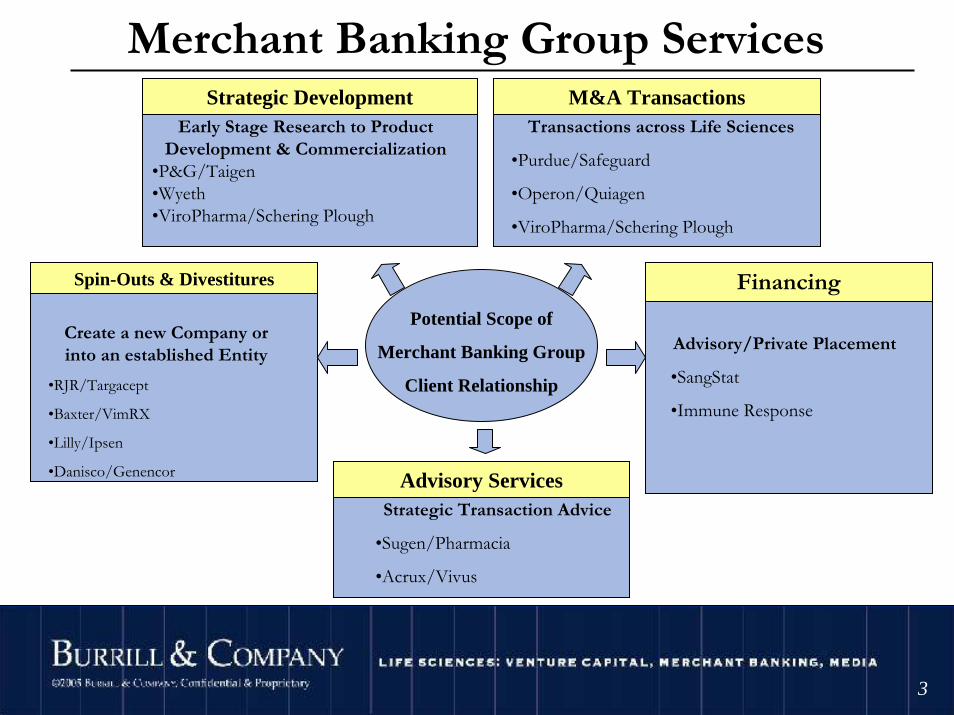

Merchant Banking Group ServicesStrategic Development

Early Stage Research to Product Development & Commercialization

•P&G/Taigen•Wyeth•ViroPharma/Schering Plough

M&A TransactionsTransactions across Life Sciences

•Purdue/Safeguard

•Operon/Quiagen

•ViroPharma/Schering Plough

Spin-Outs & Divestitures

Create a new Company or into an established Entity

•RJR/Targacept

•Baxter/VimRX

•Lilly/Ipsen

•Danisco/Genencor Advisory ServicesStrategic Transaction Advice

•Sugen/Pharmacia

•Acrux/Vivus

Financing

Advisory/Private Placement

•SangStat

•Immune Response

Potential Scope of

Merchant Banking Group

Client Relationship

©2004 Burrill & Company. Confidential & Proprietary.

44

Burrill Created/Hosted Industry Events

For inquires, contact Thea Schwartz at (415) 591-5477 or [email protected]

©2004 Burrill & Company. Confidential & Proprietary.

55

PublishingThe 2006 Biotech Industry Book

Life Science Indices (monthly)

Personalized Medicine

Stem Cells

Monthly & Quarterly Newsletters – China, India, Canada, Strategic Partnering/M&A

Burrill Website – Online resource for keeping up-to-date information about the biotech industry

Burrill & Company is the “go to” firm for industry insight

©2004 Burrill & Company. Confidential & Proprietary.

66

Industry ReportsThe seminal industry report for the last 20 years

To order most recent book visit www.burrillandco.com

©2004 Burrill & Company. Confidential & Proprietary.

77

This presentation is available

for download from our website

www.burrillandco.com

©2004 Burrill & Company. Confidential & Proprietary.

8

So what’s happened in these 20 years?(By the way…Biotech started over 10-15 years earlier…late ’60s/early ’70s…

so it’s a 35 year old industry now!)

©2004 Burrill & Company. Confidential & Proprietary.

99

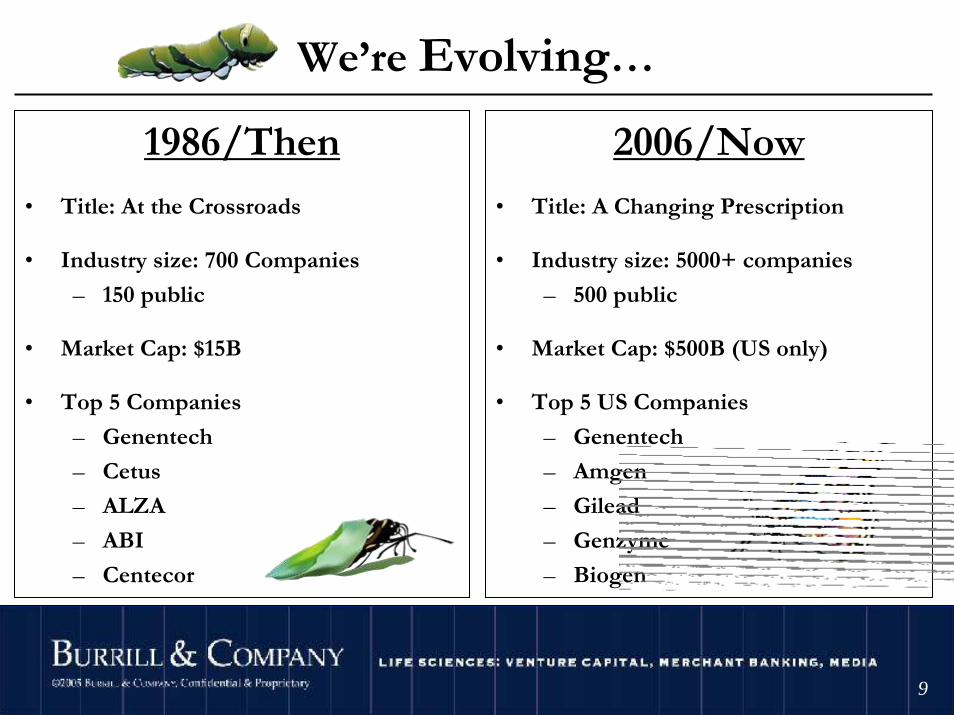

1986/Then

• Title: At the Crossroads

• Industry size: 700 Companies

– 150 public

• Market Cap: $15B

• Top 5 Companies

– Genentech

– Cetus

– ALZA

– ABI

– Centecor

We’re Evolving…

2006/Now

• Title: A Changing Prescription

• Industry size: 5000+ companies

– 500 public

• Market Cap: $500B (US only)

• Top 5 US Companies

– Genentech

– Amgen

– Gilead

– Genzyme

– Biogen

©2004 Burrill & Company. Confidential & Proprietary.

1010

Themes in ’86 book

…At The Crossroads• Science being converted to business• Products coming to market place• Are product liability, regulatory reform, patent court

behavior insurmountable barriers?• Partner or vertically integrate?• Acquisitions by pharma desirable?• How will the industry evolve?

©2004 Burrill & Company. Confidential & Proprietary.

1111

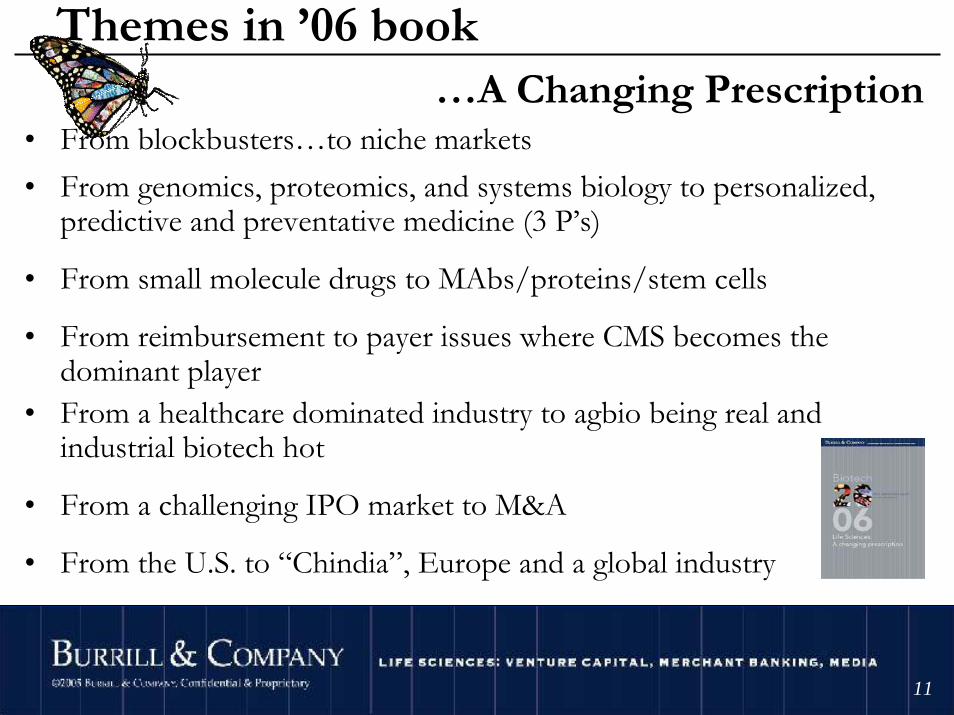

Themes in ’06 book…A Changing Prescription

• From blockbusters…to niche markets• From genomics, proteomics, and systems biology to personalized,

predictive and preventative medicine (3 P’s)

• From small molecule drugs to MAbs/proteins/stem cells

• From reimbursement to payer issues where CMS becomes the dominant player

• From a healthcare dominated industry to agbio being real and industrial biotech hot

• From a challenging IPO market to M&A

• From the U.S. to “Chindia”, Europe and a global industry

©2004 Burrill & Company. Confidential & Proprietary.

1212

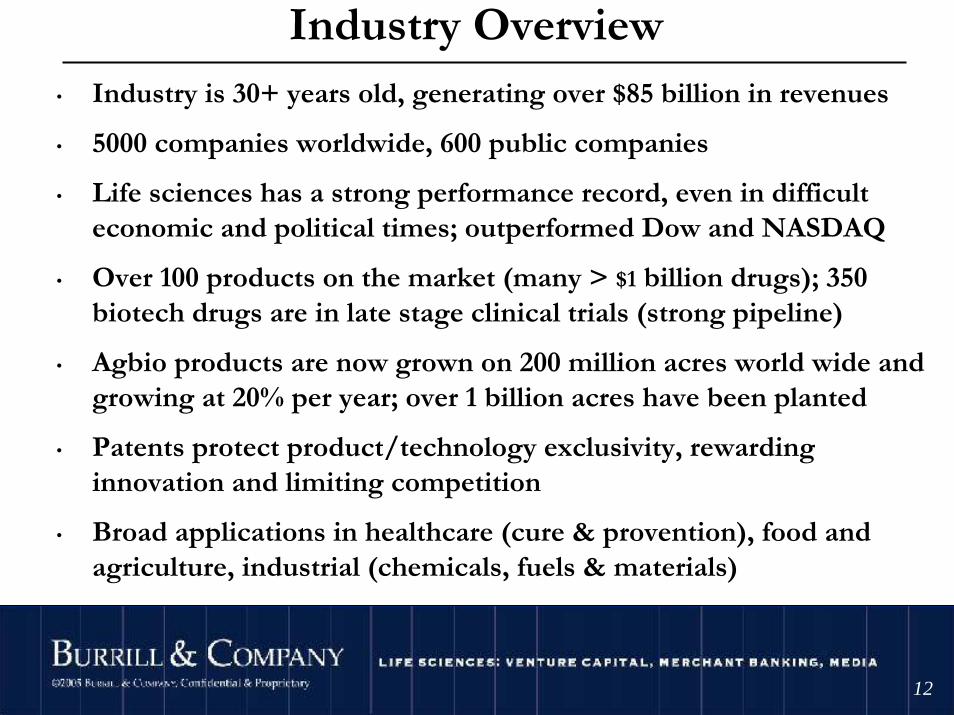

Industry Overview• Industry is 30+ years old, generating over $85 billion in revenues

• 5000 companies worldwide, 600 public companies

• Life sciences has a strong performance record, even in difficulteconomic and political times; outperformed Dow and NASDAQ

• Over 100 products on the market (many > $1 billion drugs); 350 biotech drugs are in late stage clinical trials (strong pipeline)

• Agbio products are now grown on 200 million acres world wide and growing at 20% per year; over 1 billion acres have been planted

• Patents protect product/technology exclusivity, rewarding innovation and limiting competition

• Broad applications in healthcare (cure & provention), food and agriculture, industrial (chemicals, fuels & materials)

©2004 Burrill & Company. Confidential & Proprietary.

1313

Biotech’s Globalness Begins Day OneScience/technologyIntellectual property/patents/FTOPeopleCommunicationsCompetitionCapitalMarkets—diseases know no borders

Even the smallest biotech is a global player from Day One

©2004 Burrill & Company. Confidential & Proprietary.

1414

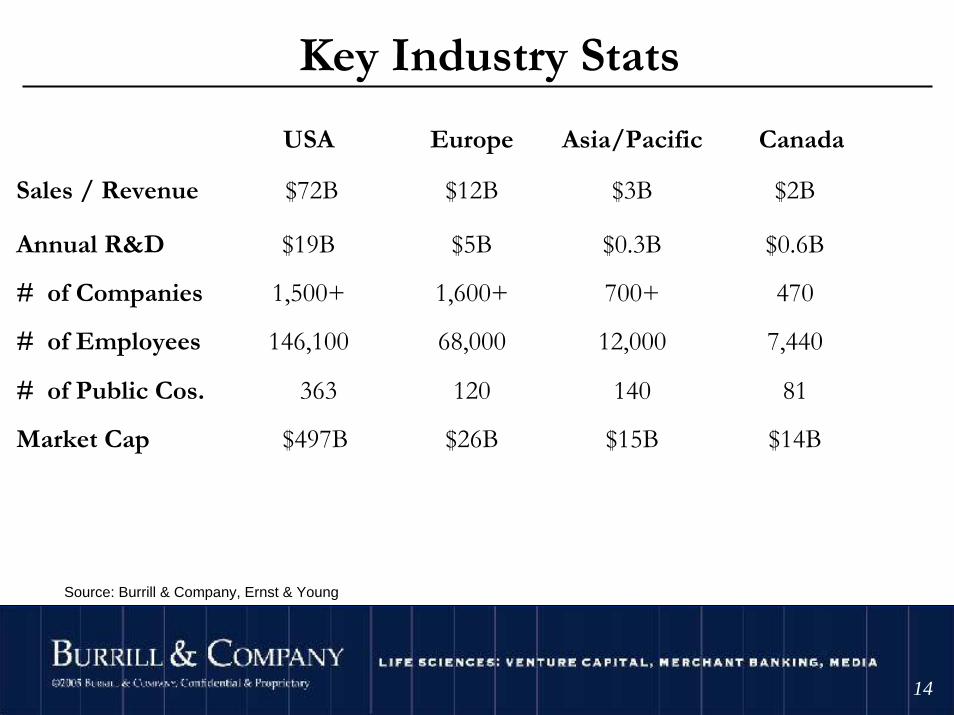

Key Industry Stats

$15B

140

12,000

700+

$0.3B

$3B

Asia/Pacific

$14B

81

7,440

470

$0.6B

$2B

Canada

$26B$497B Market Cap

120 363# of Public Cos.

68,000146,100# of Employees

1,600+1,500+# of Companies

$5B$19BAnnual R&D

$12B$72BSales / Revenue

EuropeUSA

Source: Burrill & Company, Ernst & Young

Total

$89B

$25B

4300+

233,600

700+

$552B

©2004 Burrill & Company. Confidential & Proprietary.

1515

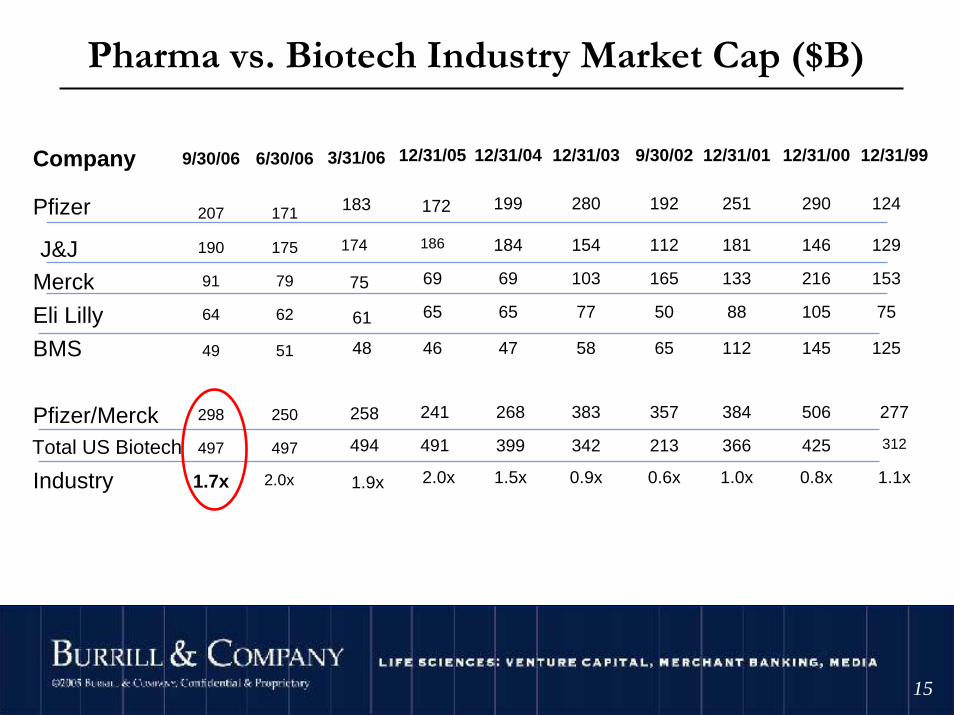

Pharma vs. Biotech Industry Market Cap ($B)

186

2.0x

491

241

46

65

69

172

12/31/05

1.5x

399

268

47

65

69

184

199

12/31/04

Merck

BMS

103

58

0.9x

342

383

77

154

280

12/31/03

165

65

0.6x

213

357

50

112

192

9/30/02Company

312

153

125

12/31/99

1.1x

277

75

129

124

Industry

Total US Biotech

Pfizer/Merck

Eli Lilly

J&J216

145

12/31/00

0.8x

425

506

105

146

290

133

112

12/31/01

1.0x

366

384

88

181

251Pfizer

3/31/06

183

174

75

61

48

258

494

1.9x

91

49

1.7x

497

298

64

190

207

9/30/06

2.0x

497

250

51

62

79

175

171

6/30/06

©2004 Burrill & Company. Confidential & Proprietary.

1616

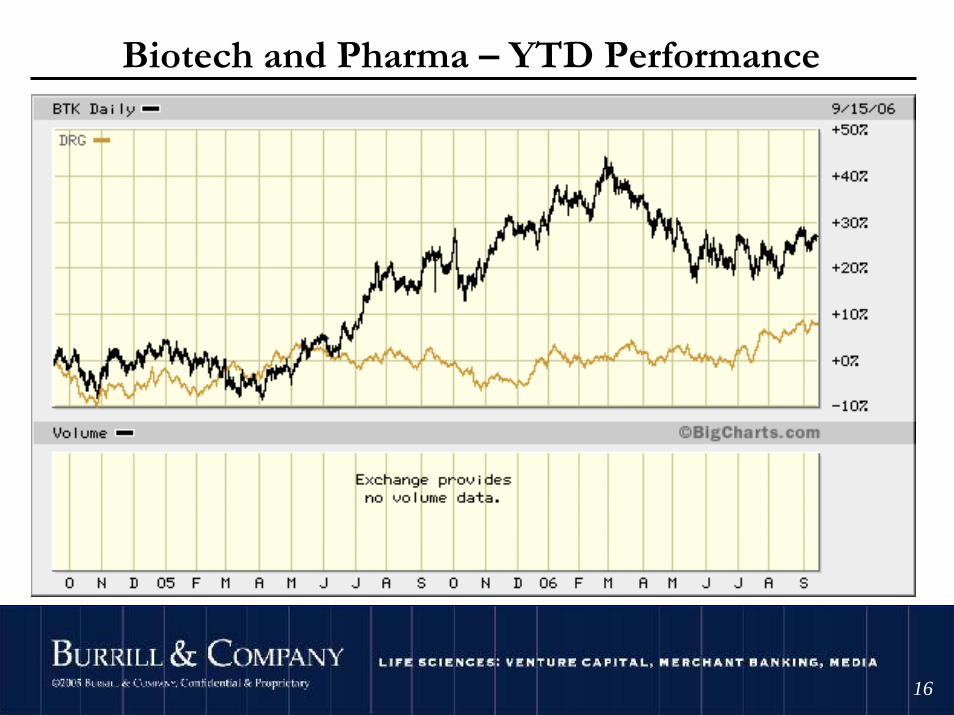

Biotech and Pharma – YTD Performance

©2004 Burrill & Company. Confidential & Proprietary.

1717

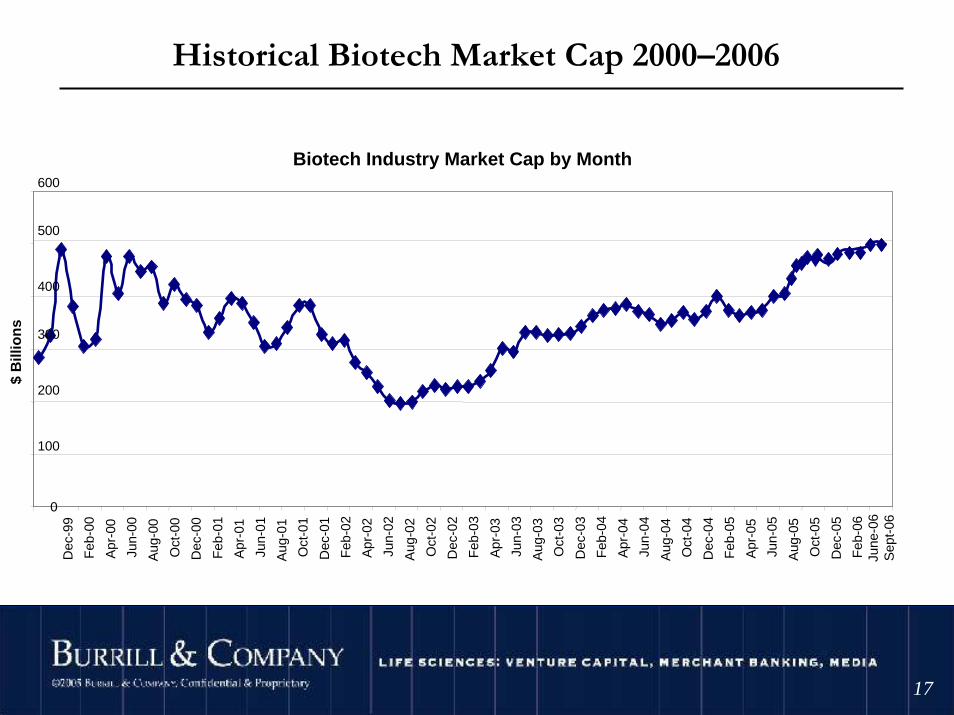

Historical Biotech Market Cap 2000–2006

Biotech Industry Market Cap by Month

0

100

200

300

400

500

600

Dec

-99

Feb

-00

Apr

-00

Jun-

00

Aug

-00

Oct

-00

Dec

-00

Feb

-01

Apr

-01

Jun-

01

Aug

-01

Oct

-01

Dec

-01

Feb

-02

Apr

-02

Jun-

02

Aug

-02

Oct

-02

Dec

-02

Feb

-03

Apr

-03

Jun-

03

Aug

-03

Oct

-03

Dec

-03

Feb

-04

Apr

-04

Jun-

04

Aug

-04

Oct

-04

Dec

-04

Feb

-05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb

-06

$ B

illio

ns

June

-06

Sep

t-06

©2004 Burrill & Company. Confidential & Proprietary.

1818

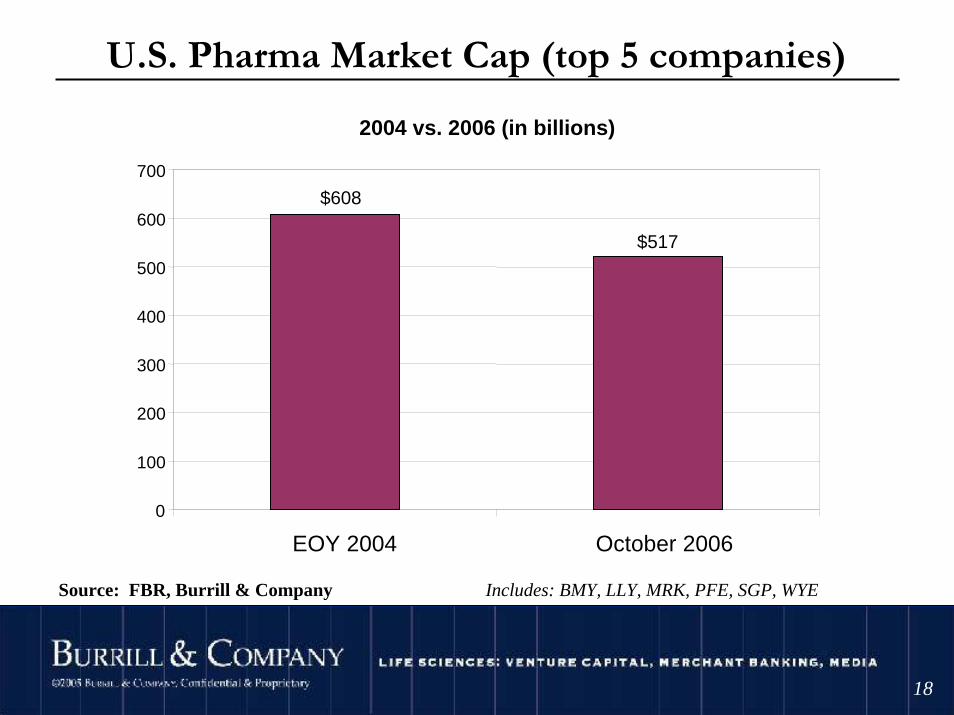

U.S. Pharma Market Cap (top 5 companies)

-25%

Source: FBR, Burrill & Company Includes: BMY, LLY, MRK, PFE, SGP, WYE

2004 vs. 2006 (in billions)

$608

$517

0

100

200

300

400

500

600

700

EOY 2004 October 2006

©2004 Burrill & Company. Confidential & Proprietary.

1919

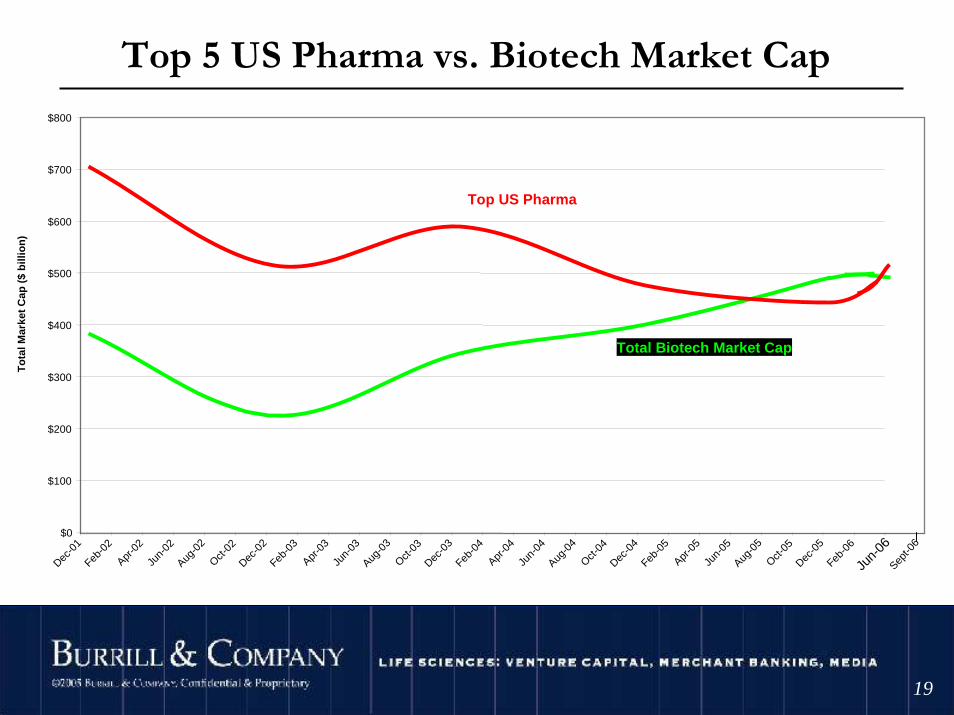

Top 5 US Pharma vs. Biotech Market Cap

$0

$100

$200

$300

$400

$500

$600

$700

$800

Dec-0

1Feb

-02

Apr-0

2Ju

n-02

Aug-0

2Oct-

02Dec

-02

Feb-0

3Apr

-03

Jun-

03Aug

-03

Oct-03

Dec-0

3Feb

-04

Apr-0

4Ju

n-04

Aug-0

4Oct-

04Dec

-04

Feb-0

5Apr

-05

Jun-

05Aug

-05

Oct-05

Dec-0

5Feb

-06

To

tal M

arke

t C

ap (

$ b

illio

n)

Top US Pharma

Total Biotech Market Cap

Sept-0

6

Jun-

06

©2004 Burrill & Company. Confidential & Proprietary.

2020

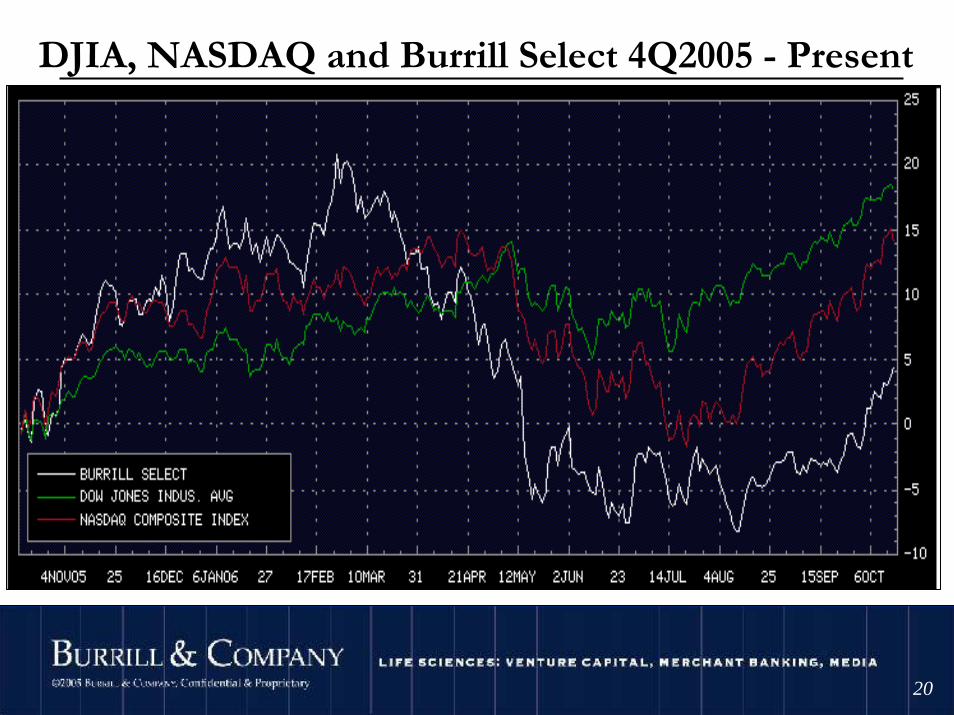

DJIA, NASDAQ and Burrill Select 4Q2005 - Present

©2004 Burrill & Company. Confidential & Proprietary.

21

…so that’s the baseline

Now, what’s really happening…

©2004 Burrill & Company. Confidential & Proprietary.

2222

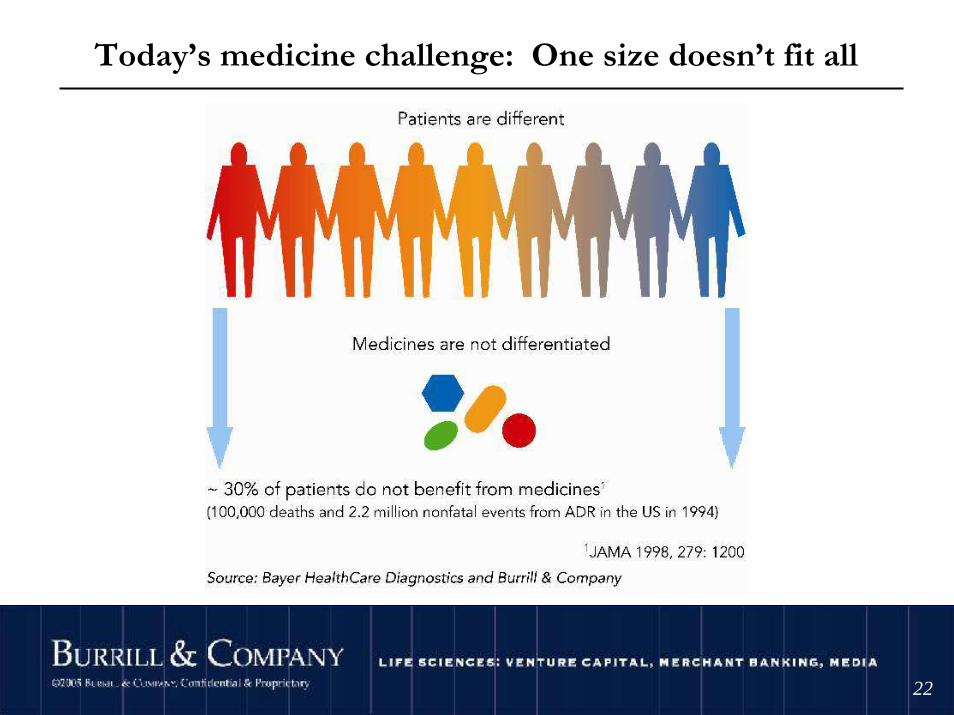

Today’s medicine challenge: One size doesn’t fit all

©2004 Burrill & Company. Confidential & Proprietary.

2323

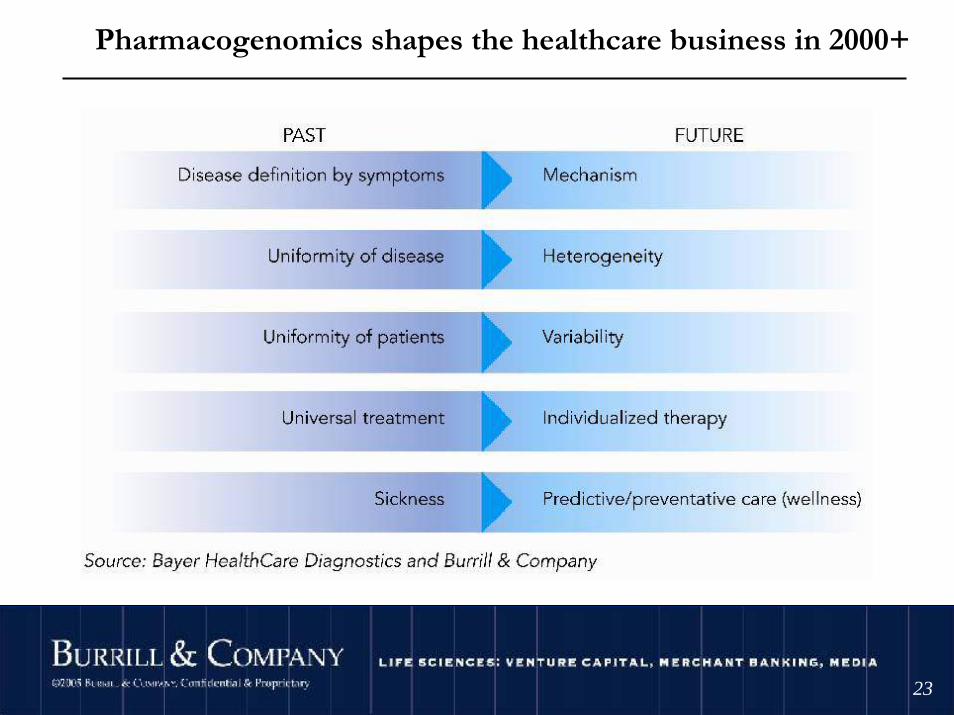

Pharmacogenomics shapes the healthcare business in 2000+

©2004 Burrill & Company. Confidential & Proprietary.

2424

140 Years of Drug Discovery Technology

©2004 Burrill & Company. Confidential & Proprietary.

2525

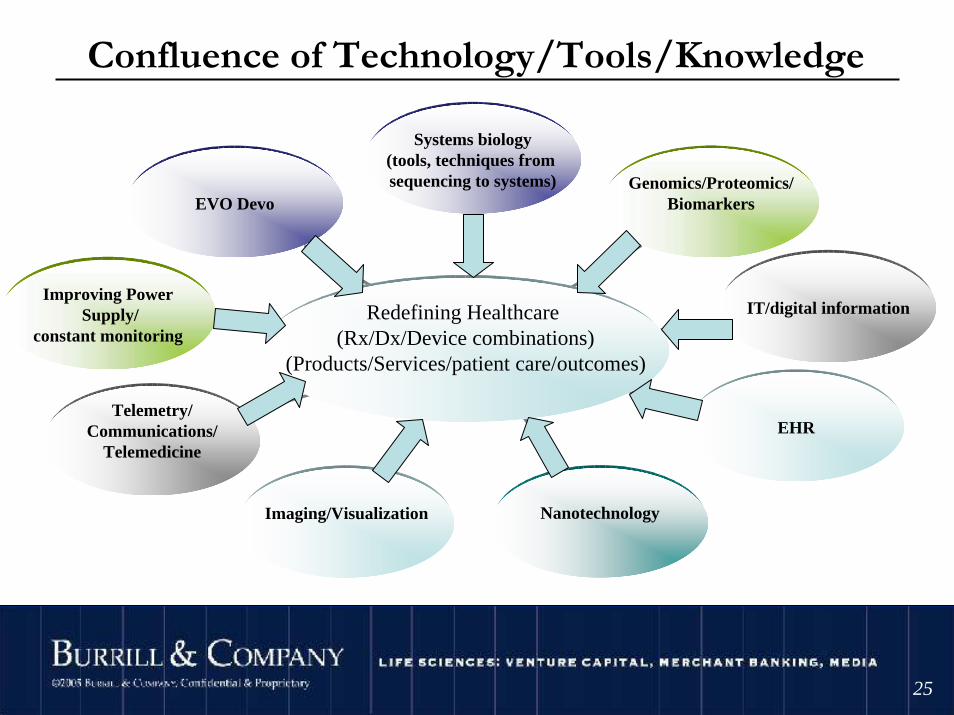

EVO Devo

Improving PowerSupply/

constant monitoring

Telemetry/Communications/

Telemedicine

Imaging/Visualization Nanotechnology

EHR

IT/digital information

Genomics/Proteomics/Biomarkers

Systems biology(tools, techniques from sequencing to systems)

Redefining Healthcare (Rx/Dx/Device combinations)

(Products/Services/patient care/outcomes)

Confluence of Technology/Tools/Knowledge

©2004 Burrill & Company. Confidential & Proprietary.

2626

Innovation Gap Getting Wider

©2004 Burrill & Company. Confidential & Proprietary.

2727

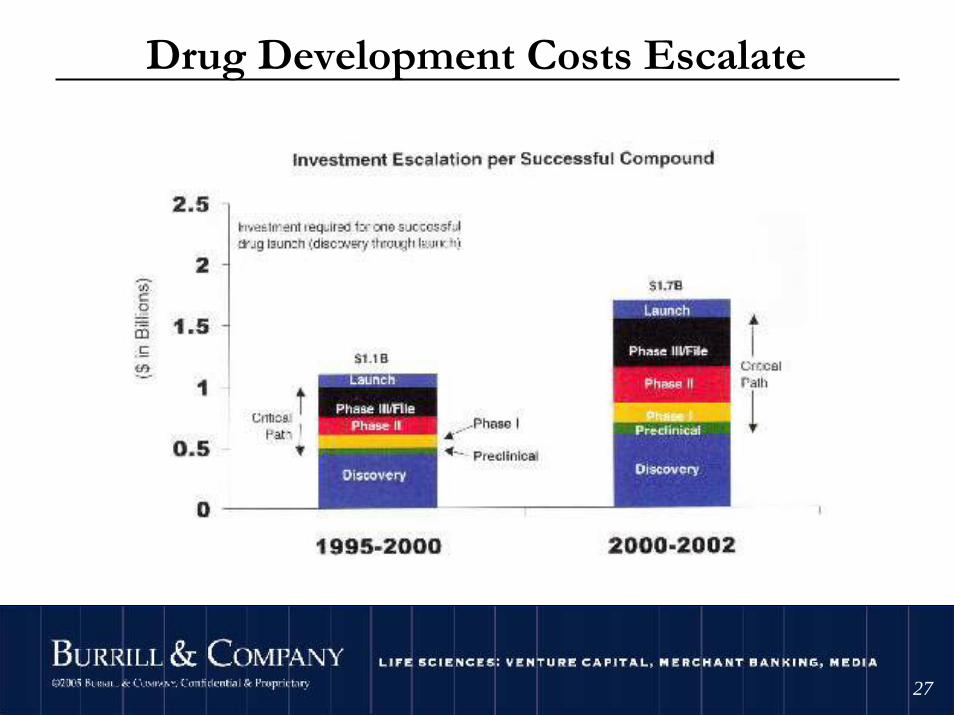

Drug Development Costs Escalate

Source: Windhover’s In Vivo. The Business & Medicine Report. Bain drug economics model, 2003

Costs are becoming prohibitive

©2004 Burrill & Company. Confidential & Proprietary.

2828

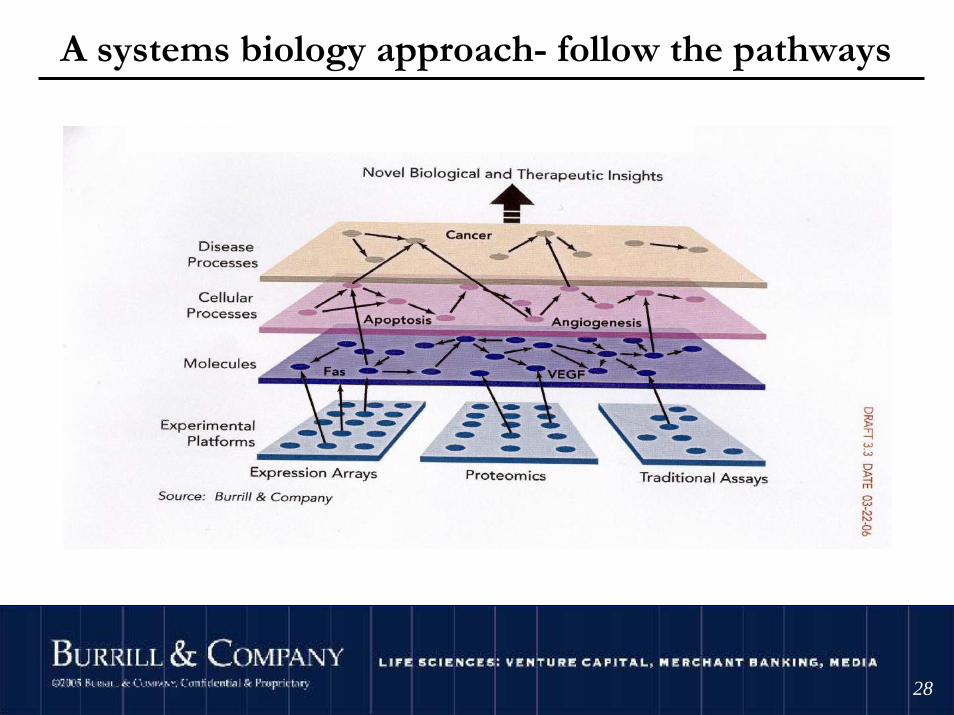

A systems biology approach- follow the pathways

©2004 Burrill & Company. Confidential & Proprietary.

2929

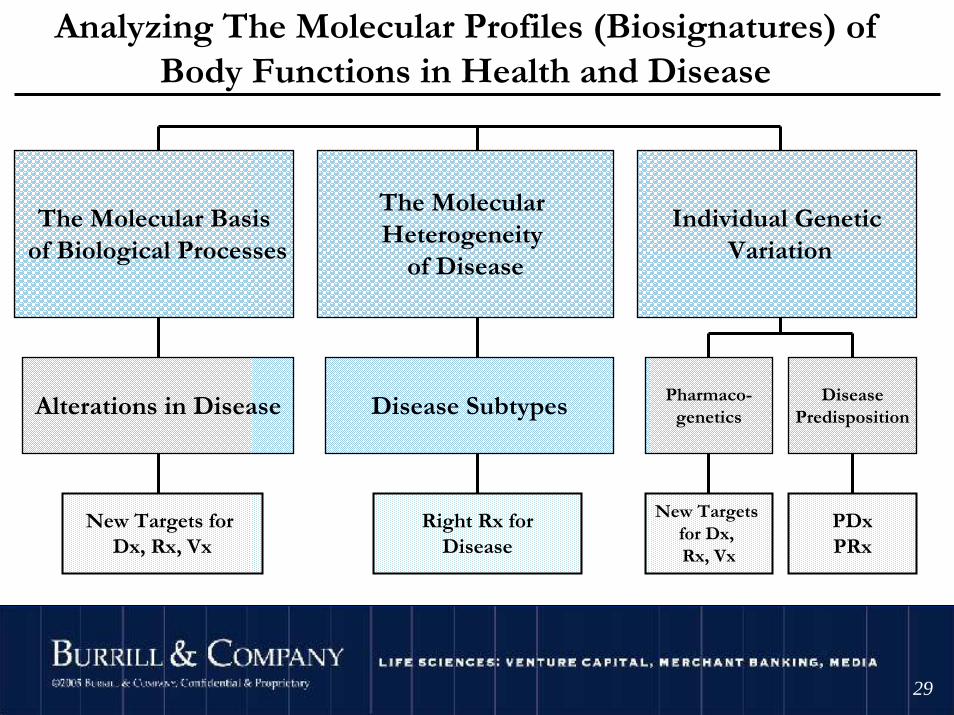

The Molecular Basisof Biological Processes

The Molecular Heterogeneity

of Disease

Individual GeneticVariation

Alterations in Disease Disease Subtypes Pharmaco-genetics

New Targets for Dx, Rx, Vx

Right Rx forDisease

New Targets for Dx, Rx, Vx

DiseasePredisposition

PDxPRx

Analyzing The Molecular Profiles (Biosignatures) of Body Functions in Health and Disease

©2004 Burrill & Company. Confidential & Proprietary.

3030

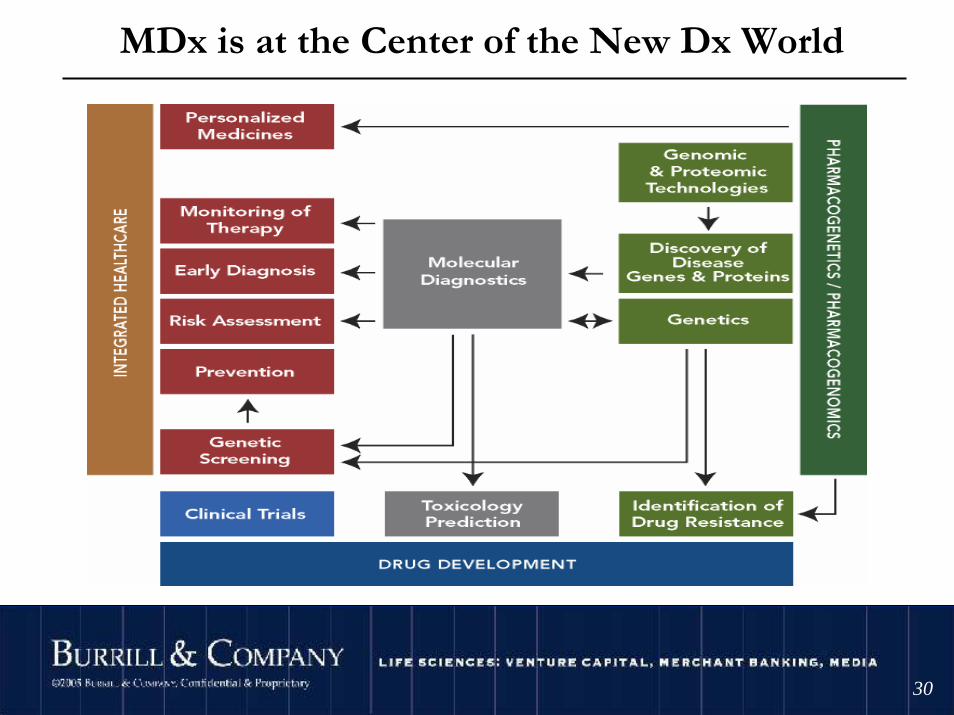

MDx is at the Center of the New Dx World

©2004 Burrill & Company. Confidential & Proprietary.

3131

Selected Targeted TreatmentsPersonalized cancer vaccines

Favrille – FavId for non-Hodgkin's lymphoma

Genitope – MyVax for non-Hodgkin's lymphoma

Gleevec (Novartis) - pH+ CML kinase inhibitor

Iressa (AstraZeneca) – EGFR tyrosine kinase inhibitor

Tarceva (Genentech/OSI) – HER1/EGFR inhibitor

Erbitux (ImClone/BMS) – HER1/EGFR inhibitor

Avastin (Genentech) – VEGF/VEGFR inhibitor

Herceptin (Genentech) – HER2 inhibitor

BilDil (NitroMed) - heart failure in African American patients

Other “Semi Targeted” Treatments (approved or late stage trials)

Nexavar (Bayer/Onyx) – multikinase inhibitor

Tykerb (GSK) - ErbB-2/EGFR inhibitor

Enzastaurin (Lilly) - PKC-Beta, AKT/P13 inhibitor

©2004 Burrill & Company. Confidential & Proprietary.

3232

Obesity Related Diseases• Diabetes – Costs $98 billion

– 90% of Type II diabetics are obese– 70% of those at risk are obese

• Heart Disease – Costs $8.8 billion

• Stroke

• Hypertension - $4.1 billion– Doubles incidence of hypertension

• Gall bladder disease – $3.4 Billion

• Osteoarthritis - $21 billion

• Sleep apnea – more prevalent then diabetes !

• Some forms of cancer

©2004 Burrill & Company. Confidential & Proprietary.

3333

Aging . . . Is it a disease?

About 1.4 million Americans are in their 90s, and another 64,000 are 100 years old or older

Baby boomers represent 30% of the total US population

Per person, seniors consume about five times the drugs of their working-age counterparts

By 2030, 20% of US population will be over 65 years of age

©2004 Burrill & Company. Confidential & Proprietary.

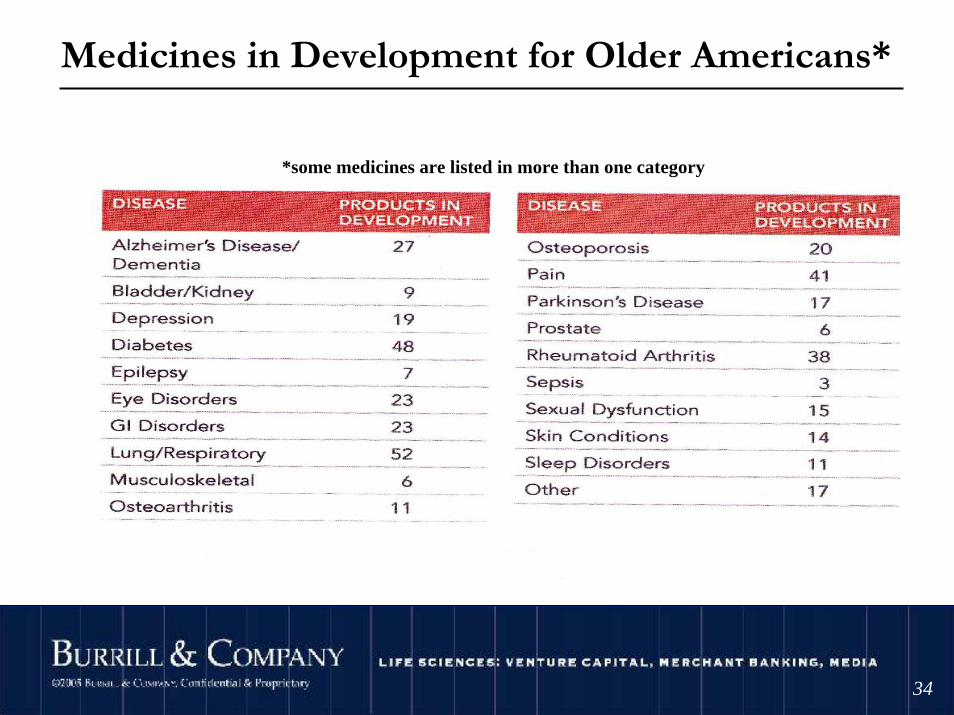

3434

Medicines in Development for Older Americans*

*some medicines are listed in more than one category

©2004 Burrill & Company. Confidential & Proprietary.

3535

Chronic Disease

125 million Americans have 1 or more chronic conditions (e.g. congestive heart failure, diabetes)

Chronic diseases account for 75% of all health care expenditures

Current costs for chronic diseases is approaching $1 trillion

These expenditures are not delivering what is possible

©2004 Burrill & Company. Confidential & Proprietary.

3636

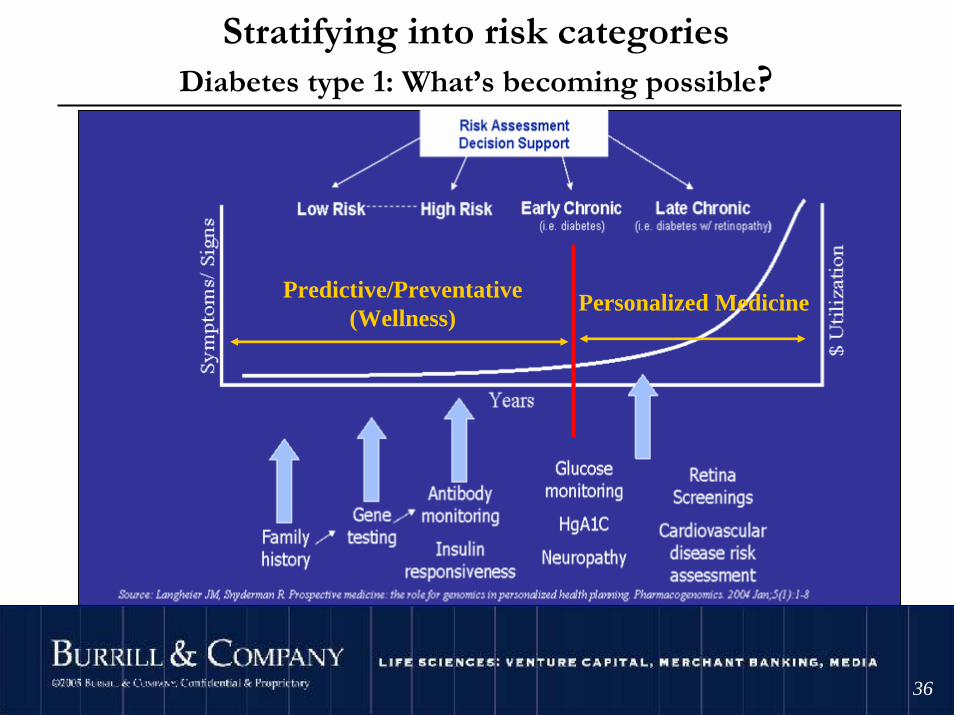

Stratifying into risk categoriesDiabetes type 1: What’s becoming possible?

Predictive/Preventative(Wellness)

Personalized Medicine

©2004 Burrill & Company. Confidential & Proprietary.

3737

What is Driving Personalized Medicine?

Convergence in technology…scientific advances and new technology

Patient care and rising consumerism

Payors (of all types) have economic incentiveGovernment health policy an global spending (e.g.: CMS)

©2004 Burrill & Company. Confidential & Proprietary.

3838

This Confluence of Healthcare Technology is bringing us…

• Targeted therapies (mutation specific), personalized medicine

• Drug/device combinations (drug eluding stents)

• Molecular diagnostics/Algorithm based diagnostics

• Non-invasiveness

• Non-hospital based with constant monitoring…• Increased predictions and prevention

©2004 Burrill & Company. Confidential & Proprietary.

3939

…that’s changing the healthcare economy

• Better outcomes/patients living longer

• Costs going up/more patients treatable…

• …But, US system leaves 25-45m uninsured/underinsured

• Consumer healthcare is here to stay (copays ), individuals empowered and informed

©2004 Burrill & Company. Confidential & Proprietary.

4040

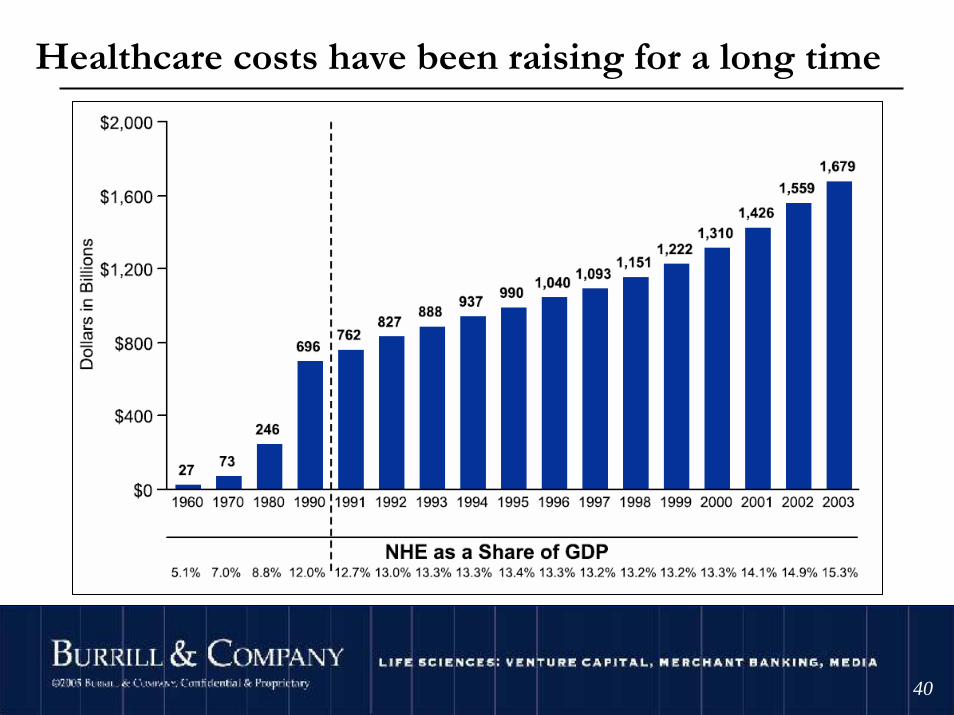

Healthcare costs have been raising for a long time

©2004 Burrill & Company. Confidential & Proprietary.

4141

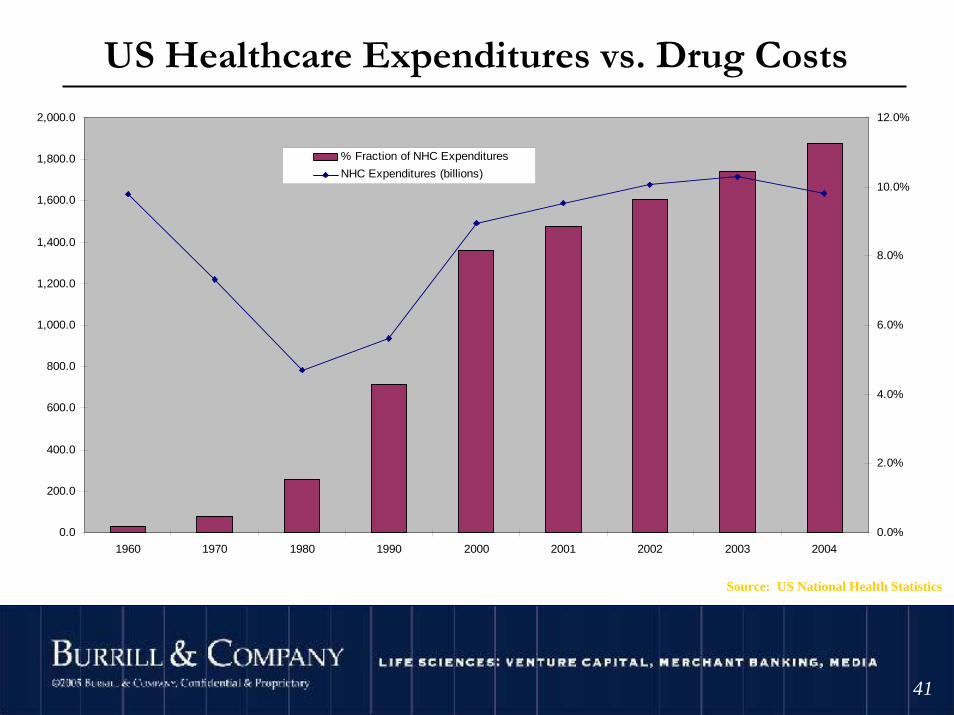

US Healthcare Expenditures vs. Drug Costs

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

1960 1970 1980 1990 2000 2001 2002 2003 2004

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

% Fraction of NHC Expenditures

NHC Expenditures (billions)

Source: US National Health Statistics

©2004 Burrill & Company. Confidential & Proprietary.

4242

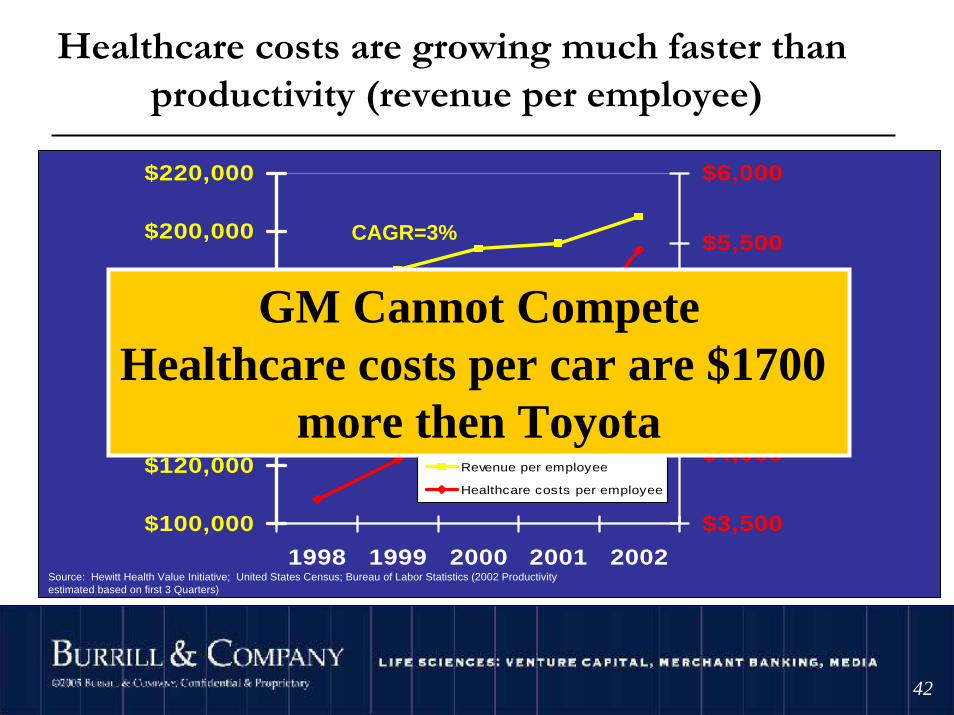

Healthcare costs are growing much faster than productivity (revenue per employee)

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

$220,000

1998 1999 2000 2001 2002

$3,500

$4,000

$4,500

$5,000

$5,500

$6,000

Revenue per employee

Healthcare costs per employee

Source: Hewitt Health Value Initiative; United States Census; Bureau of Labor Statistics (2002 Productivity estimated based on first 3 Quarters)

CAGR=3%

CAGR=10%

GM Cannot CompeteHealthcare costs per car are $1700

more then Toyota

©2004 Burrill & Company. Confidential & Proprietary.

4343

…So, healthcare cost increases are on everyone’s agenda-

• Politicians/Congress/White House

• Payors/Reimbursors/Insurers

• Physicians/Providers

• Patients/Consumers

…and patients are empowered, have economic costs, and really want to stay well!

©2004 Burrill & Company. Confidential & Proprietary.

4444

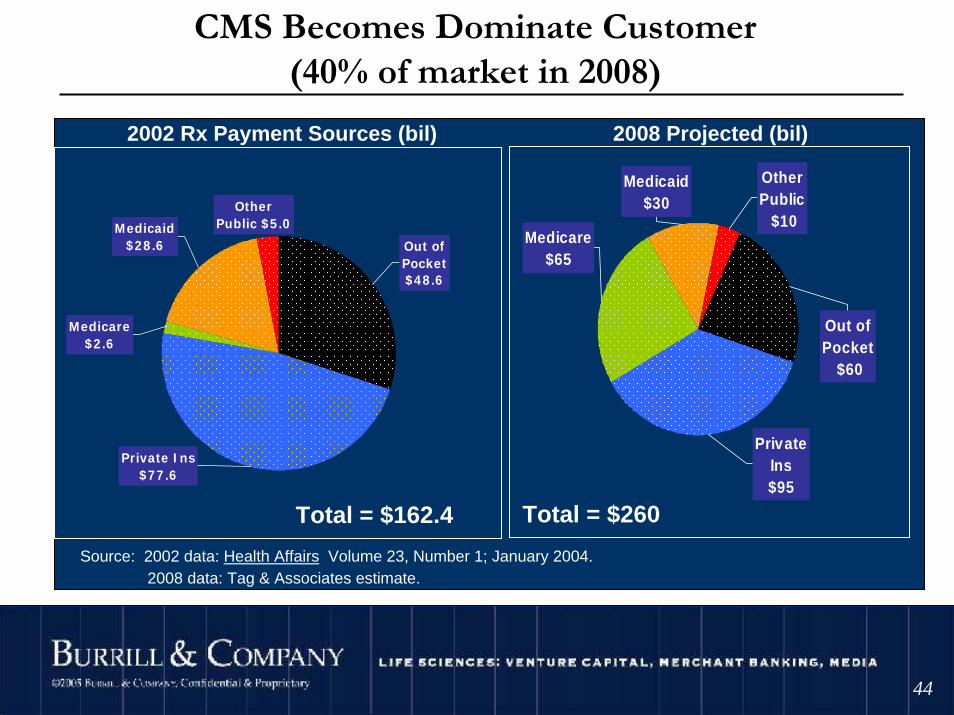

Medicaid$30

Out of Pocket

$60

Other Public $10

Medicare $65

Private Ins $95

2002 Rx Payment Sources (bil) 2008 Projected (bil)

Medicare $2.6

Out of Pocket $48.6

Medicaid $28.6

Private Ins $77.6

Other Public $5.0

Source: 2002 data: Health Affairs Volume 23, Number 1; January 2004. 2008 data: Tag & Associates estimate.

Total = $162.4 Total = $260

CMS Becomes Dominate Customer(40% of market in 2008)

©2004 Burrill & Company. Confidential & Proprietary.

4545

. . . and what’s happeningto big pharma?

Putting Biotech into Context

©2004 Burrill & Company. Confidential & Proprietary.

4646

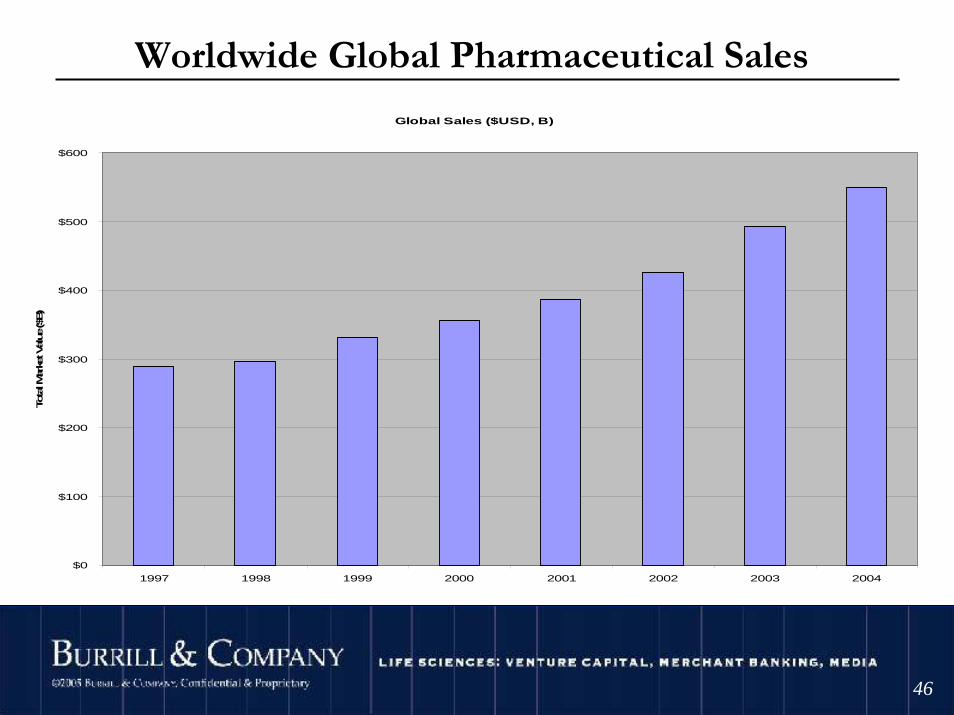

Worldwide Global Pharmaceutical Sales

Global Sales ($USD, B)

$0

$100

$200

$300

$400

$500

$600

1997 1998 1999 2000 2001 2002 2003 2004

Tota

l Mar

ket Value ($

B)

©2004 Burrill & Company. Confidential & Proprietary.

4747

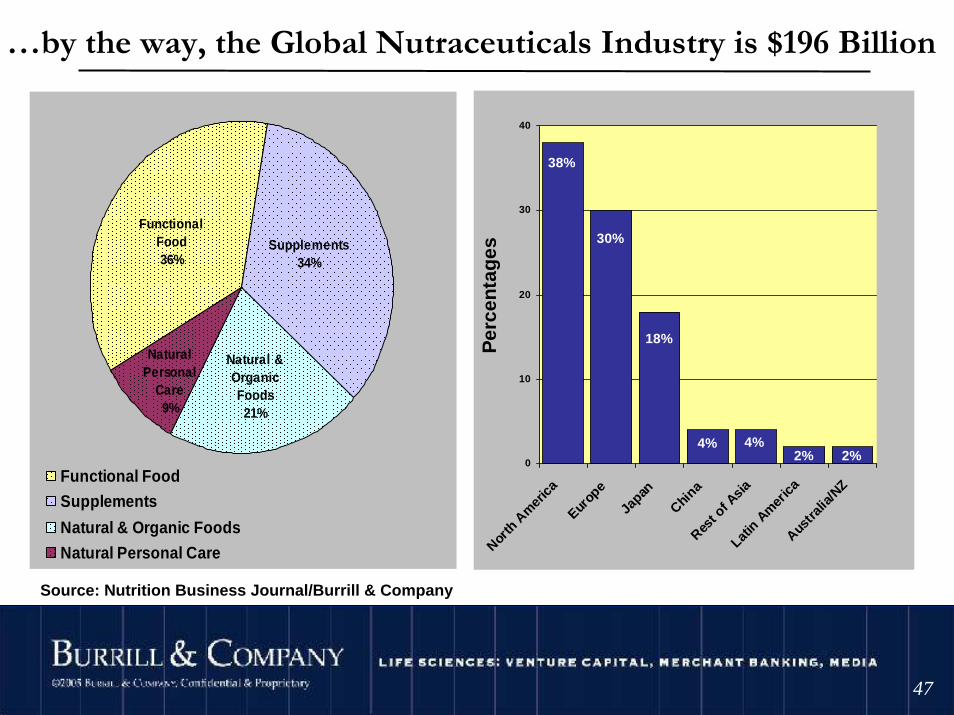

…by the way, the Global Nutraceuticals Industry is $196 Billion

Functional Food36%

Supplements34%

Natural & Organic Foods21%

Natural Personal

Care9%

Functional Food

Supplements

Natural & Organic Foods

Natural Personal Care

2%2%4%4%

18%

30%

38%

0

10

20

30

40

North

Am

erica

Europ

e

Japan

China

Rest o

f Asia

Latin

Am

erica

Austra

lia/N

Z

Per

cen

tag

es

Source: Nutrition Business Journal/Burrill & Company

©2004 Burrill & Company. Confidential & Proprietary.

4848

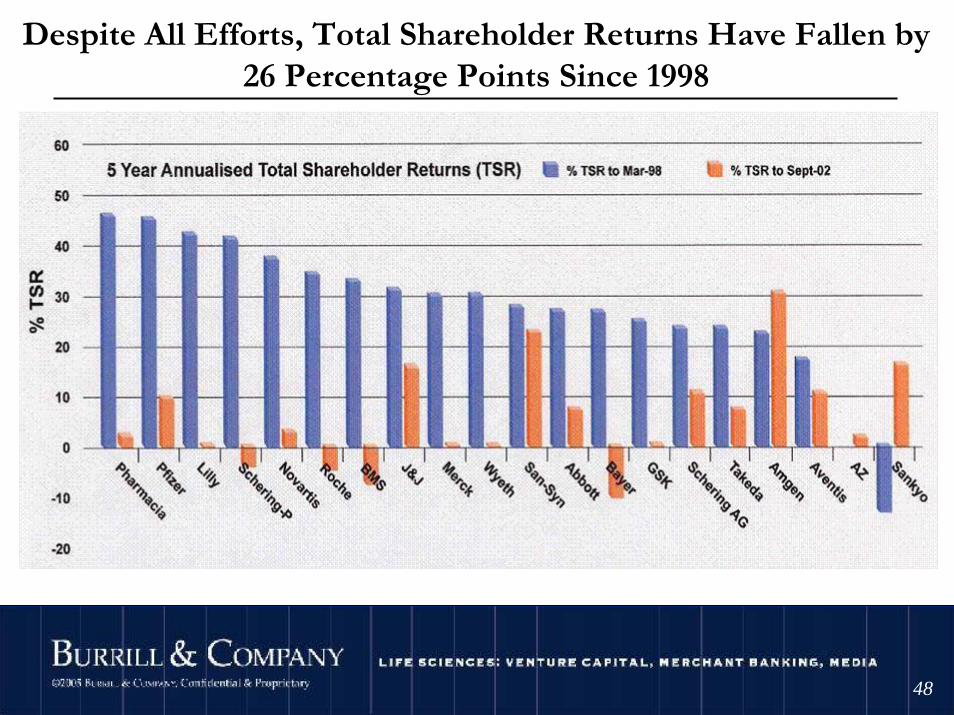

Despite All Efforts, Total Shareholder Returns Have Fallen by26 Percentage Points Since 1998

Source: IBM Life Sciences Solutions

©2004 Burrill & Company. Confidential & Proprietary.

4949

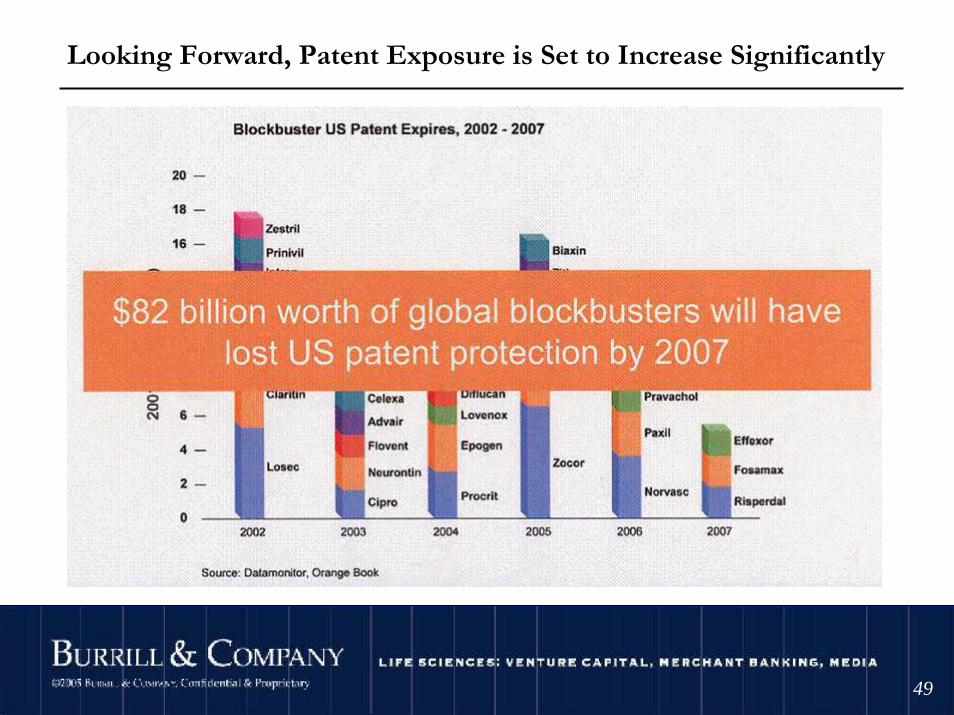

Looking Forward, Patent Exposure is Set to Increase Significantly

©2004 Burrill & Company. Confidential & Proprietary.

5050

Biogeneric Status of Biotech Drugs

©2004 Burrill & Company. Confidential & Proprietary.

5151

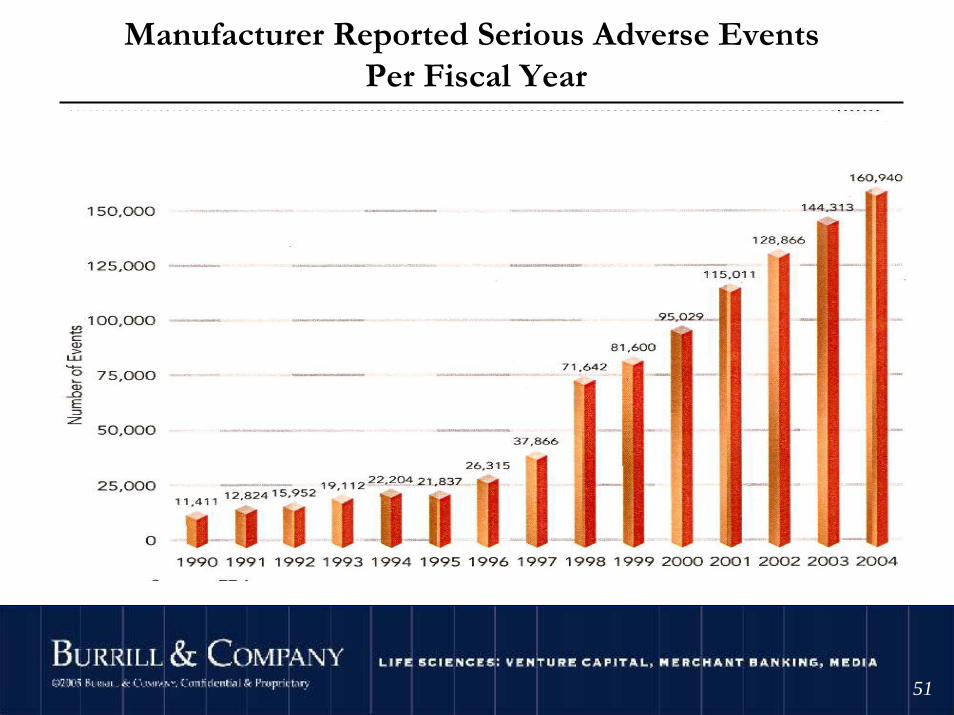

Manufacturer Reported Serious Adverse Events Per Fiscal Year

©2004 Burrill & Company. Confidential & Proprietary.

5252

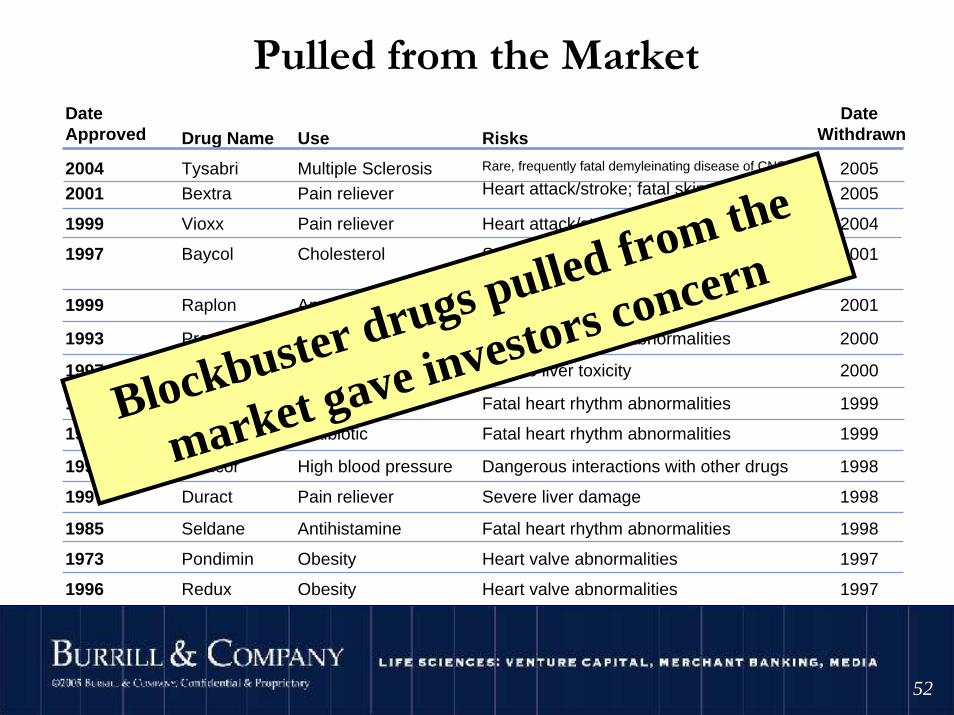

Pulled from the MarketDateApproved Drug Name Use Risks

DateWithdrawn

20042001

TysabriBextra

Multiple SclerosisPain reliever

Rare, frequently fatal demyleinating disease of CNS

Heart attack/stroke; fatal skin reactions

Heart attack/stroke

Severe damage to muscle, that is sometimes fatal

An inability to breathe normally

Fatal heart rhythm abnormalities

1997 Rezulin Type 2 diabetes Severe liver toxicity 2000

1997 Posicor High blood pressure Dangerous interactions with other drugs 1998

1973 Pondimin Obesity Heart valve abnormalities 1997

1997 Duract Pain reliever Severe liver damage 1998

1985 Seldane Antihistamine Fatal heart rhythm abnormalities 1998

1988 Hismanal Antihistamine Fatal heart rhythm abnormalities 1999

1997 Raxar Antibiotic Fatal heart rhythm abnormalities 1999

Heart valve abnormalities

1999 Vioxx Pain reliever

20052005

2004

2001

2001

2000

1997 Baycol Cholesterol

1999 Raplon Anesthesia

1993 Propulsid Heartburn

19971996 Redux Obesity

Blockbuster drugs pulled from the

market gave investors concern

©2004 Burrill & Company. Confidential & Proprietary.

5353

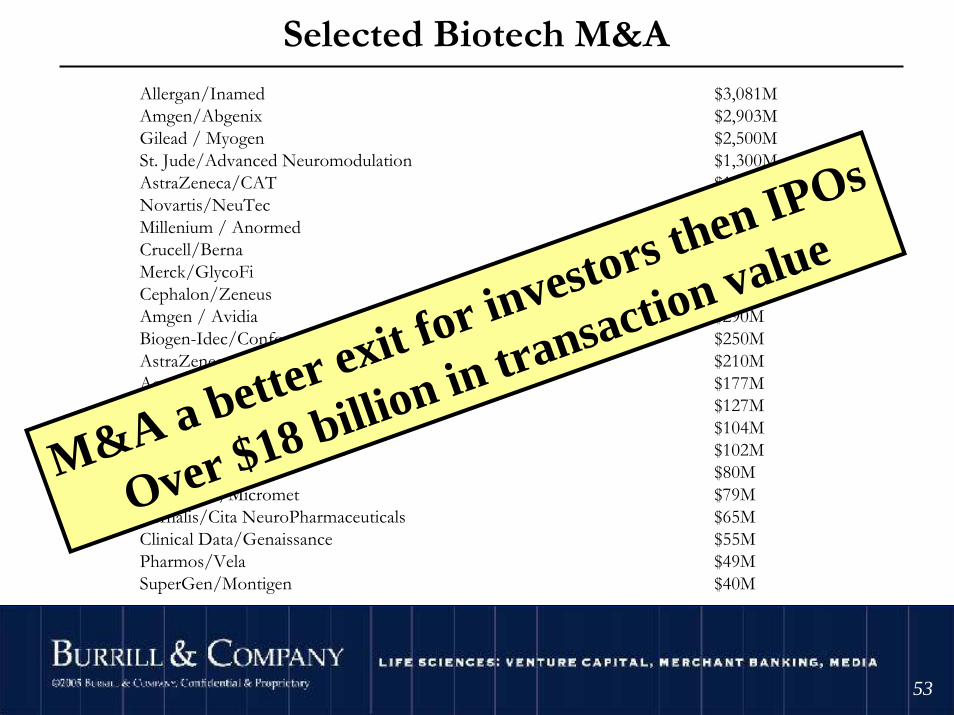

Selected Biotech M&AAllergan/Inamed $3,081MAmgen/Abgenix $2,903MGilead / Myogen $2,500MSt. Jude/Advanced Neuromodulation $1,300MAstraZeneca/CAT $1,071MNovartis/NeuTec $568MMillenium / Anormed $515MCrucell/Berna $451MMerck/GlycoFi $400MCephalon/Zeneus $360MAmgen / Avidia $290MBiogen-Idec/Conforma $250MAstraZeneca/KuDos $210MActavis/Sindan $177MEpix/Predix $127MPSividia/Control Delivery Systems $104MZentiva/Romanian Sicomed $102MMerck/Abmaxis $80MCancerVax/Micromet $79MVernalis/Cita NeuroPharmaceuticals $65MClinical Data/Genaissance $55MPharmos/Vela $49MSuperGen/Montigen $40M

M&A a better exit for investors then IPOs

Over $18 billion in transaction value

©2004 Burrill & Company. Confidential & Proprietary.

5454

M&A Highlights

With the 2006 IPO window remaining tight, M&A is an increasingly attractive “exit” mechanism

Large pharma acquisitions continue to drive the M&A market (Bayer/Schering, Abbott/Guidant, J&J/Pfizer consumer)

Momentum shifting to Europe

European mid-cap buying spree (UCB/Schwarz Pharma, Merck KGaA/Serono, Nycomed/Altana)

Big Pharma acquired for pipeline products (AZ/CAT) and strategic technologies (Merck/GlycoFi and Abmaxis)

Several smaller value biotech-biotech acquisitions*As of September 2006

©2004 Burrill & Company. Confidential & Proprietary.

5555

Selected Biotech PartneringAtheroGenics /AstraZeneca $1,000MFibroGen / Astellas $815M*Wyeth/Trubion $800MAlnylam / Novartis $700MRoche/Actelion $630MNastech/P&G $577MAffymax / Takeda $535MIdenix/Novartis $525MSGX/Novartis $515MProgenics/Wyeth $417MInfinity/Novartis $400MNuvelo/Bayer $385MKai/Daiichi Sankyo $340MNicOx/Merck $340MAmira/Roche $287MAstraZeneca/Pozen $200MAstraZeneca/Abraxis $200MEnzon/Santaris $200MAstex/Novartis $190MMethylGene/Pharmion $170M

Over $8.2 Billion in Deals

©2004 Burrill & Company. Confidential & Proprietary.

5656

Partnering Highlights

Partnering continues to play an important role in our industry – over $8.2 B in total transaction value

On track to meeting/exceeding partnering transaction values in 2005 (~$17B)

Novartis on a roll with 3 partnering deals signed worth $1.4B total in the last several months

Big Pharma continues to partner early to access key technologies, targets and products

©2004 Burrill & Company. Confidential & Proprietary.

5757

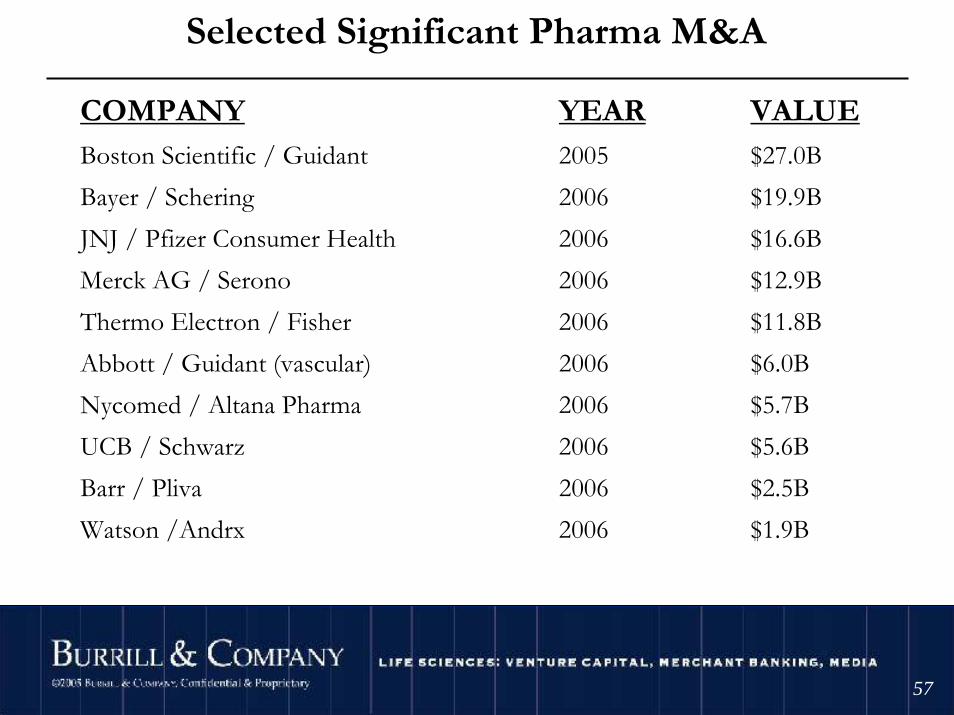

Selected Significant Pharma M&A

COMPANY YEAR VALUE Boston Scientific / Guidant 2005 $27.0BBayer / Schering 2006 $19.9BJNJ / Pfizer Consumer Health 2006 $16.6BMerck AG / Serono 2006 $12.9BThermo Electron / Fisher 2006 $11.8BAbbott / Guidant (vascular) 2006 $6.0BNycomed / Altana Pharma 2006 $5.7BUCB / Schwarz 2006 $5.6BBarr / Pliva 2006 $2.5BWatson /Andrx 2006 $1.9B

*As of September 2006

©2004 Burrill & Company. Confidential & Proprietary.

5858

So what does Big Pharma do better than anyone else?

• Discovery?

• Development?

• Manufacturing?

• Distribution?

• Disease Management?

Answer: ???

©2004 Burrill & Company. Confidential & Proprietary.

5959

Pharma/biotech alternative structures

• Technology licensing• R&D Agreement, Co-development• Manufacturing• Marketing and distribution agreement, co-promotion• Deals by molecule/biologic, therapeutic area, demographic, or

geography• Strategic partnership, including any or all combination of the

above• Minority or partial acquisition• M&A

©2004 Burrill & Company. Confidential & Proprietary.

6060

Benefits of Strategic PartneringStrategic Alliances between cash-starved Biotechs and research-poor Pharmas…

– Are less costly and less risky than outright acquisitions – Allow for acquisition of capabilities rather than growing them

internally– Enable Pharma to tap into Biotech companies’ cutting-edge

research and entrepreneurial energy– Reduce redundancies in product development, manufacturing,

marketing and sales

20,000 alliances formed since 1988 and growing by annual rate of 25%!

©2004 Burrill & Company. Confidential & Proprietary.

6161

Key Partnering Trends• Consolidation of mid/large European pharma

– Need to reach critical mass– Need to bolster R&D budgets– Reduction in “national” regulatory boarders– Geographic proximity

• Growth of Emerging Markets (China, India & Africa)– Foreign targets to enable international presence and access

• Matrix Laboratories, an Indian Pharmaceutical company, was acquired by Mylan Laboratories of Illinois

• “Buyers” are partnering at increasingly earlier stages– Fifty percent of partnering deals with significant terms involved preclinical assets

• Established biotech players are expanding their therapeutic focus to drive growth– Larger companies are seeking growth areas outside of their traditional niche markets and

diversifying their pipelines in order to reduce risk.• Gilead has made two recent large acquisitions involving Myogen with a lead compound for

Hypertension. • Cephalon built a pipeline and franchise in oncology through a series of acquisitions (Salmedix,

Trisenox, Zeneus)

©2004 Burrill & Company. Confidential & Proprietary.

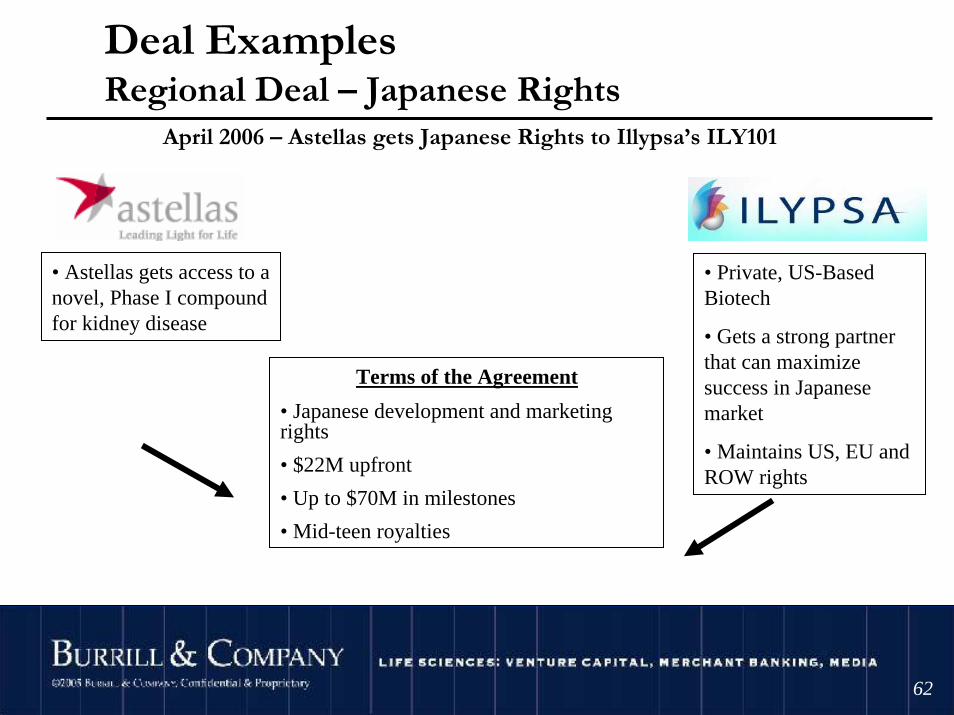

6262

Deal ExamplesRegional Deal – Japanese Rights

• Astellas gets access to a novel, Phase I compound for kidney disease

Terms of the Agreement

• Japanese development and marketing rights

• $22M upfront

• Up to $70M in milestones

• Mid-teen royalties

• Private, US-Based Biotech

• Gets a strong partner that can maximize success in Japanese market

• Maintains US, EU and ROW rights

April 2006 – Astellas gets Japanese Rights to Illypsa’s ILY101

©2004 Burrill & Company. Confidential & Proprietary.

6363

Deal ExamplesCo-Development

• Purdue shares developmental costs and risks

• Can advance multiple programs simultaneously

Terms of the Agreement

• Worldwide co-development and co-promotion deal

• 3 pain programs

• Shionogi funds research first 3 years

• Companies share development expenses

• Co-promote products worldwide

• Shionogi gets access to 3 early stage pain programs

January 2006 – Shionogi and Purdue Collaborate on Pain Therapeutics

©2004 Burrill & Company. Confidential & Proprietary.

6464

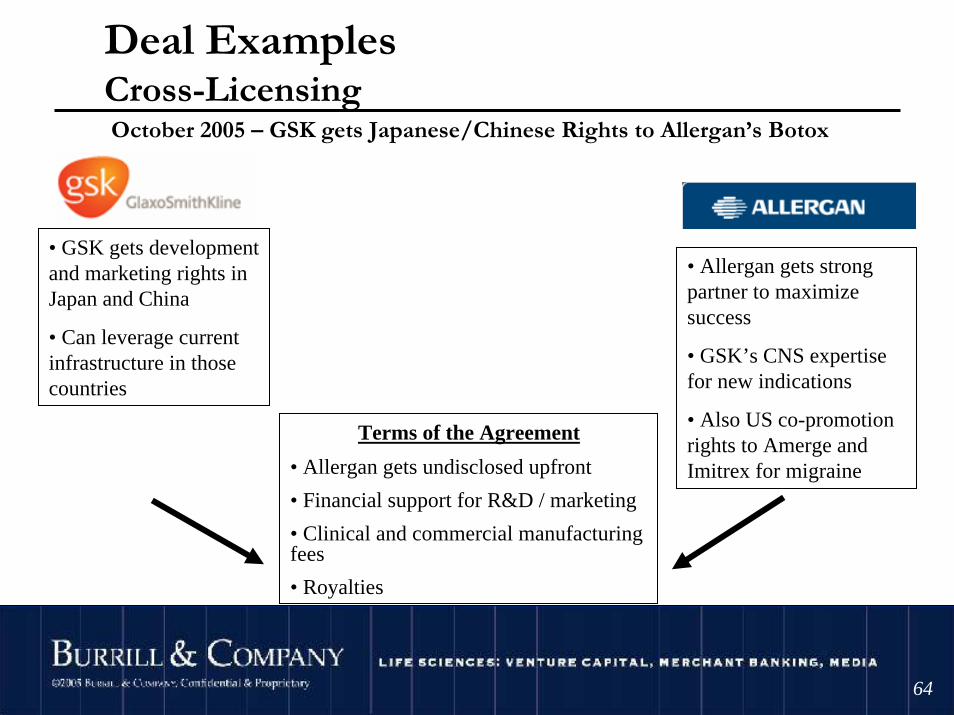

Deal ExamplesCross-Licensing

• Allergan gets strong partner to maximize success

• GSK’s CNS expertise for new indications

• Also US co-promotion rights to Amerge and Imitrex for migraine

Terms of the Agreement

• Allergan gets undisclosed upfront

• Financial support for R&D / marketing

• Clinical and commercial manufacturing fees

• Royalties

• GSK gets development and marketing rights in Japan and China

• Can leverage current infrastructure in those countries

October 2005 – GSK gets Japanese/Chinese Rights to Allergan’s Botox

©2004 Burrill & Company. Confidential & Proprietary.

6565

Wellness: Its time has come

• Rising healthcare costs are impacting individuals

• Rising incidence of chronic disease

• Recognition of the importance of genetic variation

• Scientific knowledge base for:– Personalization– Cost effective technologies

• Financial markets beginning to recognize opportunity

©2004 Burrill & Company. Confidential & Proprietary.

6666

Food and Lifestyle can Influence our Genes and How they Work

• Diet – Gene Interactions• Exercise – Gene Interactions

©2004 Burrill & Company. Confidential & Proprietary.

6767

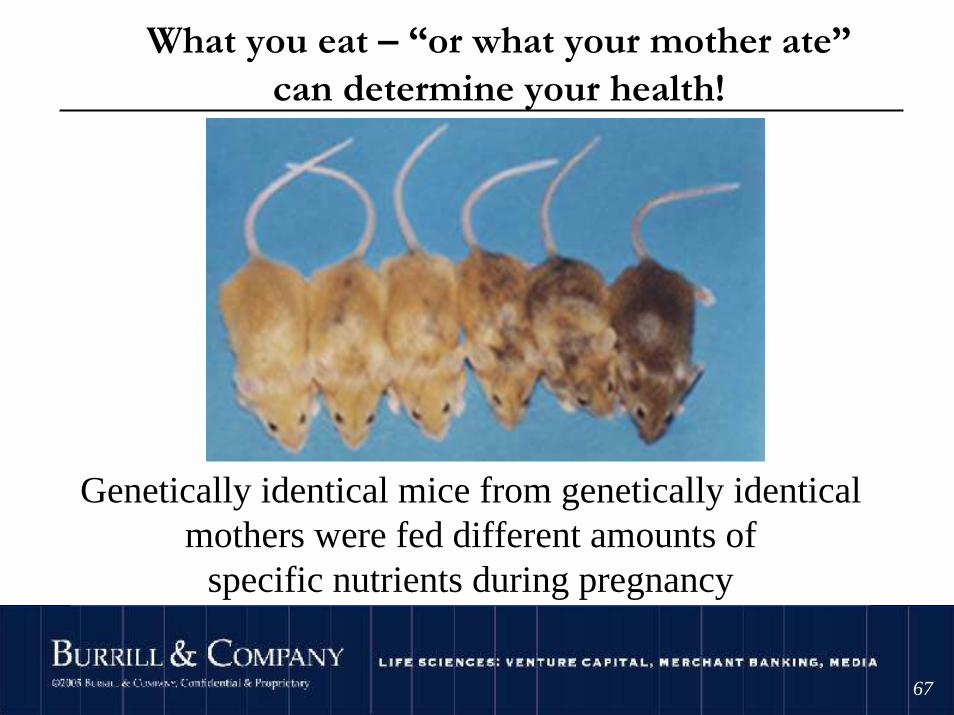

Genetically identical mice from genetically identicalmothers were fed different amounts of

specific nutrients during pregnancy

What you eat – “or what your mother ate”can determine your health!

©2004 Burrill & Company. Confidential & Proprietary.

6868

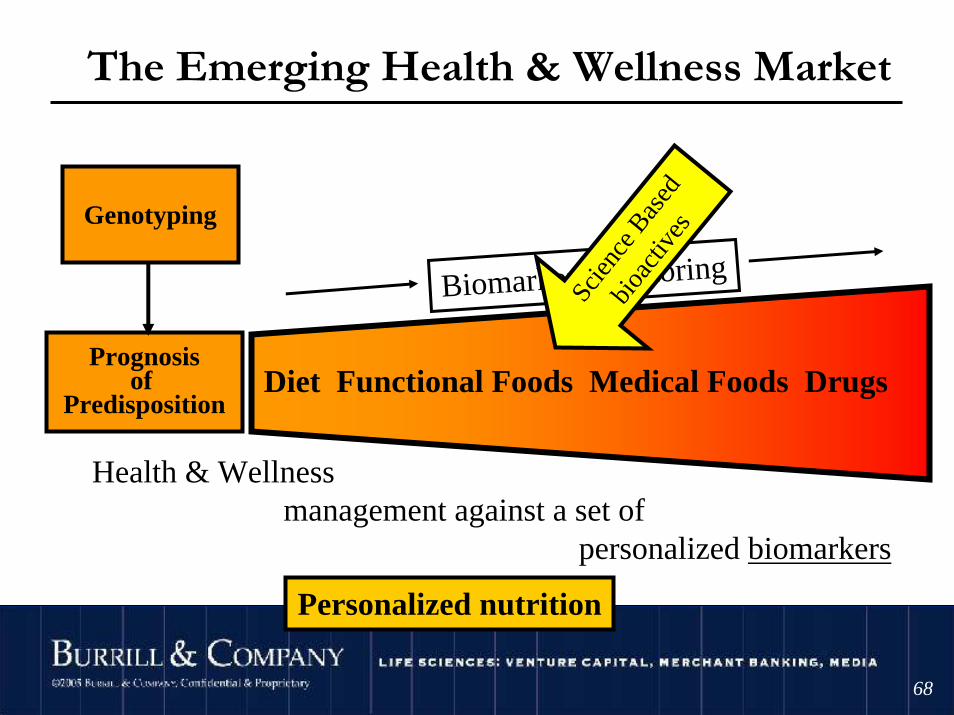

The Emerging Health & Wellness Market

Genotyping

Diet Functional Foods Medical Foods DrugsPrognosis

of Predisposition

Health & Wellness management against a set of

personalized biomarkers

Biomarker monitoring

Personalized nutritionSc

ienc

e Bas

ed

bioa

ctive

s

©2004 Burrill & Company. Confidential & Proprietary.

6969

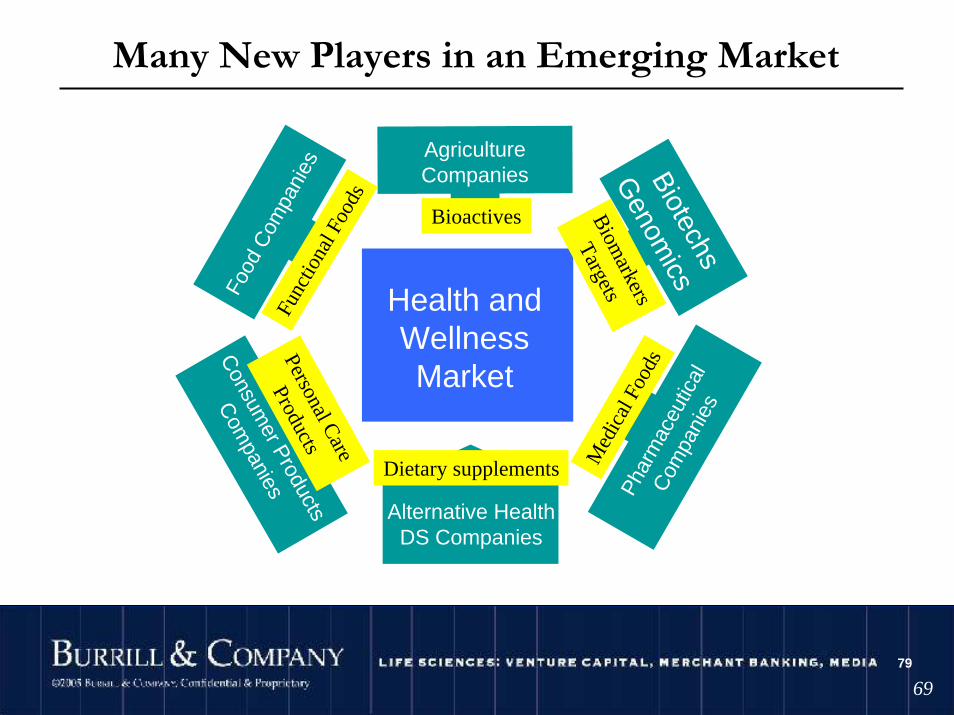

Many New Players in an Emerging Market

Health and WellnessMarket

Food

Com

pani

es

Consum

er Products

Com

panies Phar

mac

eutic

al

Com

pani

es

Biotechs

Genom

ics

AgricultureCompanies

Alternative HealthDS Companies

79

Dietary supplements Med

ical

Foo

ds

Biom

arkers

Targets

Bioactives

Func

tiona

l Foo

ds

Personal Care

Products

©2004 Burrill & Company. Confidential & Proprietary.

7070

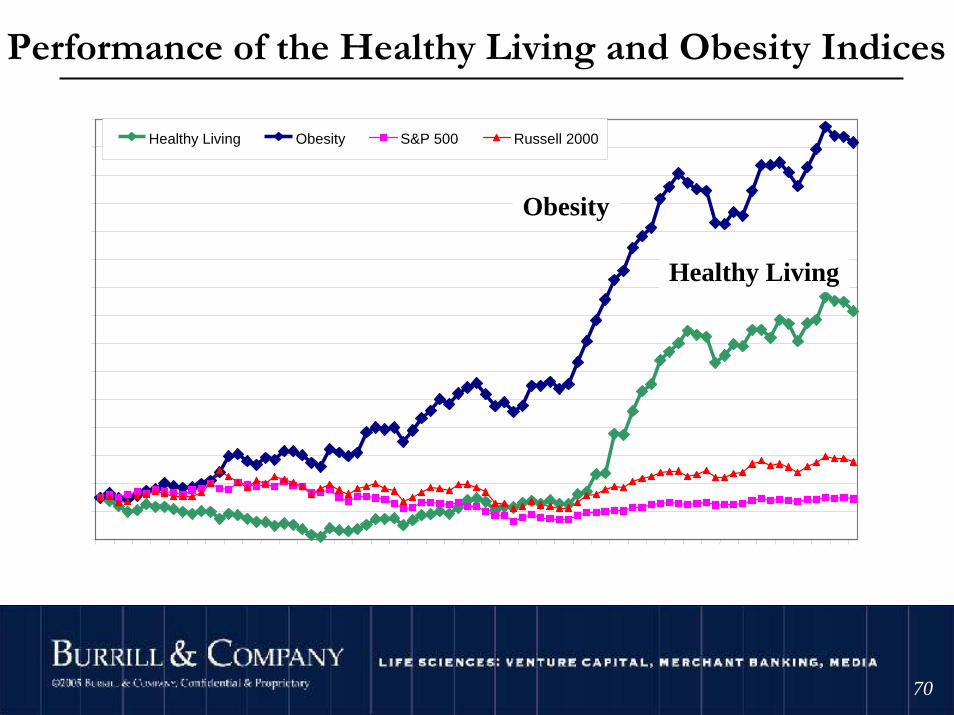

Performance of the Healthy Living and Obesity Indicesvs. the S&P 500 & Russell 2000

40

80

120

160

200

240

280

320

360

400

440

480

520

560

600

640D

ec-9

8F

eb-9

9A

pr-9

9Ju

n-99

Aug

-99

Oct

-99

Dec

-99

Feb

-00

Apr

-00

Jun-

00A

ug-0

0O

ct-0

0D

ec-0

0F

eb-0

1A

pr-0

1Ju

n-01

Aug

-01

Oct

-01

Dec

-01

Feb

-02

Apr

-02

Jun-

02A

ug-0

2O

ct-0

2D

ec-0

2F

eb-0

3A

pr-0

3Ju

n-03

Aug

-03

Oct

-03

Dec

-03

Feb

-04

Apr

-04

Jun-

04A

ug-0

4O

ct-0

4D

ec-0

4F

eb-0

5A

pr-0

5Ju

n-05

Aug

-05

Oct

-05

Healthy Living Obesity S&P 500 Russell 2000

Healthy Living

Obesity

©2004 Burrill & Company. Confidential & Proprietary.

7171

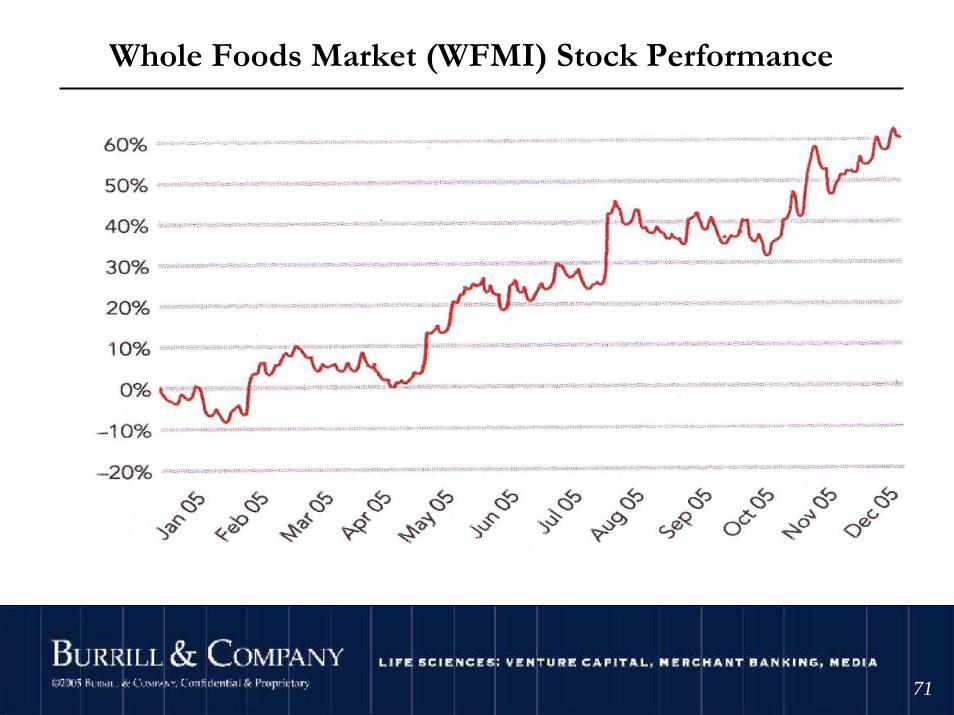

Whole Foods Market (WFMI) Stock Performance

©2004 Burrill & Company. Confidential & Proprietary.

7272

…And what about the regulators?

Leadership changes

Phase III/IV (Pharmacovigilance)

Drug Safety Review Board (Vioxx, Tysabri)

GMP—Chiron vaccine problems, others

Generics

Theranostics (Rx/Dx)…critical path initiative

©2004 Burrill & Company. Confidential & Proprietary.

7373

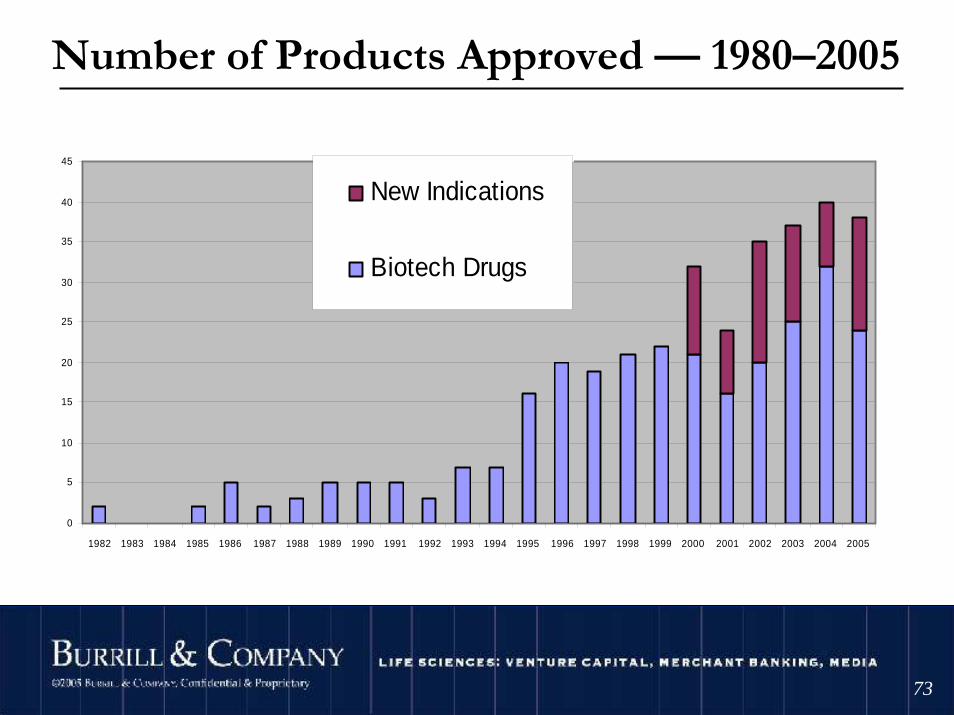

Number of Products Approved — 1980–2005

0

5

10

15

20

25

30

35

40

45

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

New Indications

Biotech Drugs

©2004 Burrill & Company. Confidential & Proprietary.

7474

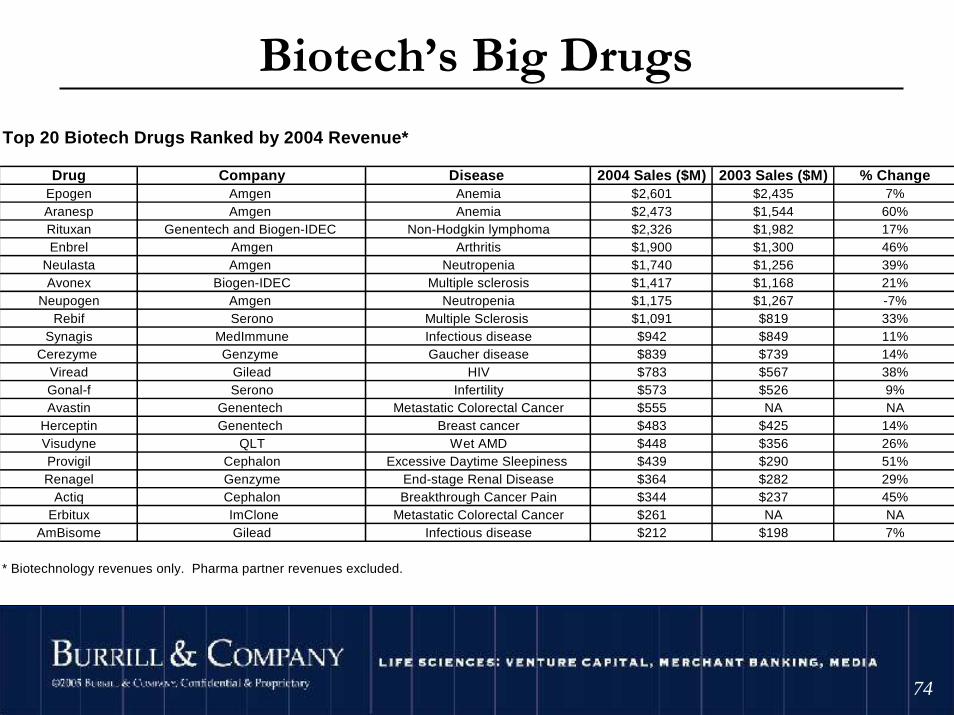

Biotech’s Big Drugs

Top 20 Biotech Drugs Ranked by 2004 Revenue*

Drug Company Disease 2004 Sales ($M) 2003 Sales ($M) % ChangeEpogen Amgen Anemia $2,601 $2,435 7%Aranesp Amgen Anemia $2,473 $1,544 60%Rituxan Genentech and Biogen-IDEC Non-Hodgkin lymphoma $2,326 $1,982 17%Enbrel Amgen Arthritis $1,900 $1,300 46%

Neulasta Amgen Neutropenia $1,740 $1,256 39%Avonex Biogen-IDEC Multiple sclerosis $1,417 $1,168 21%

Neupogen Amgen Neutropenia $1,175 $1,267 -7%Rebif Serono Multiple Sclerosis $1,091 $819 33%

Synagis MedImmune Infectious disease $942 $849 11%Cerezyme Genzyme Gaucher disease $839 $739 14%

Viread Gilead HIV $783 $567 38%Gonal-f Serono Infertility $573 $526 9%Avastin Genentech Metastatic Colorectal Cancer $555 NA NA

Herceptin Genentech Breast cancer $483 $425 14%Visudyne QLT Wet AMD $448 $356 26%Provigil Cephalon Excessive Daytime Sleepiness $439 $290 51%Renagel Genzyme End-stage Renal Disease $364 $282 29%

Actiq Cephalon Breakthrough Cancer Pain $344 $237 45%Erbitux ImClone Metastatic Colorectal Cancer $261 NA NA

AmBisome Gilead Infectious disease $212 $198 7%

* Biotechnology revenues only. Pharma partner revenues excluded.

©2004 Burrill & Company. Confidential & Proprietary.

7575

Biotechnology Drugs in Clinical Development

©2004 Burrill & Company. Confidential & Proprietary.

7676

. . . and the marketplaceis changing too

©2004 Burrill & Company. Confidential & Proprietary.

7777

Big “new” marketsObesity/diabetes/metabolic disease

Alzheimer's/memory

Anti-aging

Anti infectives (antibiotic resistance)

Wellness (preventative/predictive cure)

©2004 Burrill & Company. Confidential & Proprietary.

7878

Is the blockbuster Model Really Dead?

“From a strategic standpoint, of meeting the needs of our customers, the current blockbuster

model doesn’t work.”

Sidney Taurel, Chairman & CEO, Eli Lilly & Co.Drugs Get Smart, Business Week, September 5, 2005

©2004 Burrill & Company. Confidential & Proprietary.

7979

The Personalized Medicine ModelThe right drug for the right patient at the right time

• Utilizes pharmacogenomics, which benefits from the recent advances of genomics/proteomics technology

• Reduced development cost; shorter development time from discovery to launch

• Smaller clinical trials required to prove efficacy in target population

• Greater probability of clinical compounds reaching market

• Better safety profile

• Treat specific populations based on biomarkers or molecular diagnostics/imaging results

• Product focus: personalized medicines (nichebusters) that do not require blockbuster-sized sales to generate attractive returns

©2004 Burrill & Company. Confidential & Proprietary.

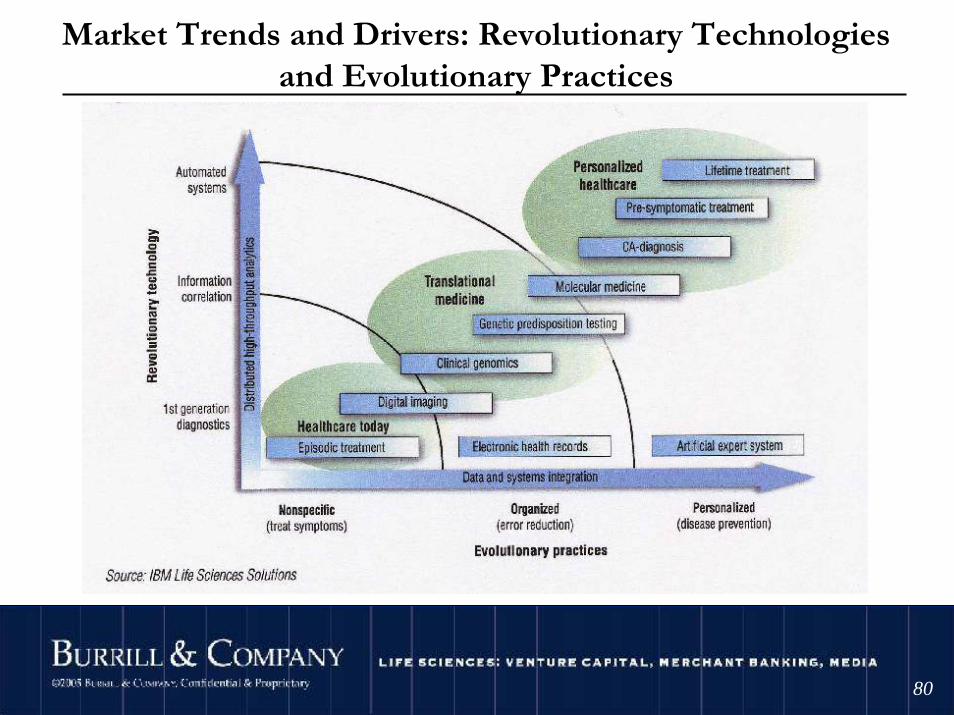

8080

Market Trends and Drivers: Revolutionary Technologiesand Evolutionary Practices

©2004 Burrill & Company. Confidential & Proprietary.

8181

(China/India)» What’s happening?

» Impact

©2004 Burrill & Company. Confidential & Proprietary.

8282

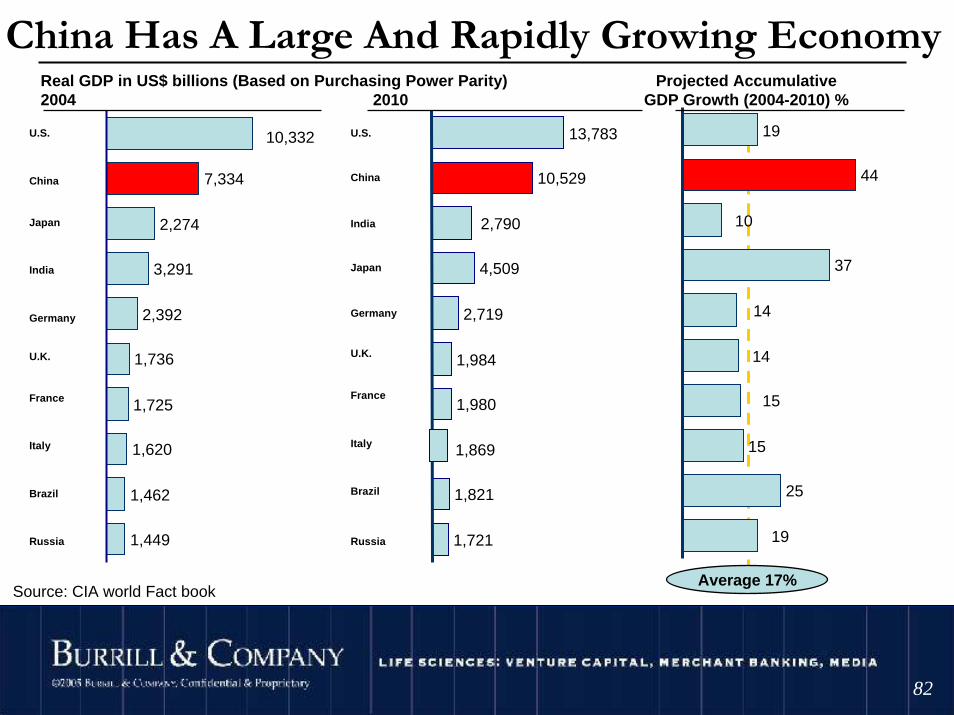

10,529

4,509

2,719

1,984

1,980

1,869

1,821

1,721

13,783

2,790

7,334

3,291

2,392

1,736

1,725

1,620

1,462

1,449

10,332

2,274

44

37

15

25

15

14

10

14

19

19

China Has A Large And Rapidly Growing EconomyProjected Accumulative

GDP Growth (2004-2010) %

Average 17%

Real GDP in US$ billions (Based on Purchasing Power Parity)2004

U.S.

Japan

Germany

France

China

Italy

U.K.

Brazil

Russia

India

2010

Source: CIA world Fact book

U.S.

Japan

Germany

France

U.K.

Italy

China

Brazil

India

Russia

©2004 Burrill & Company. Confidential & Proprietary.

8383

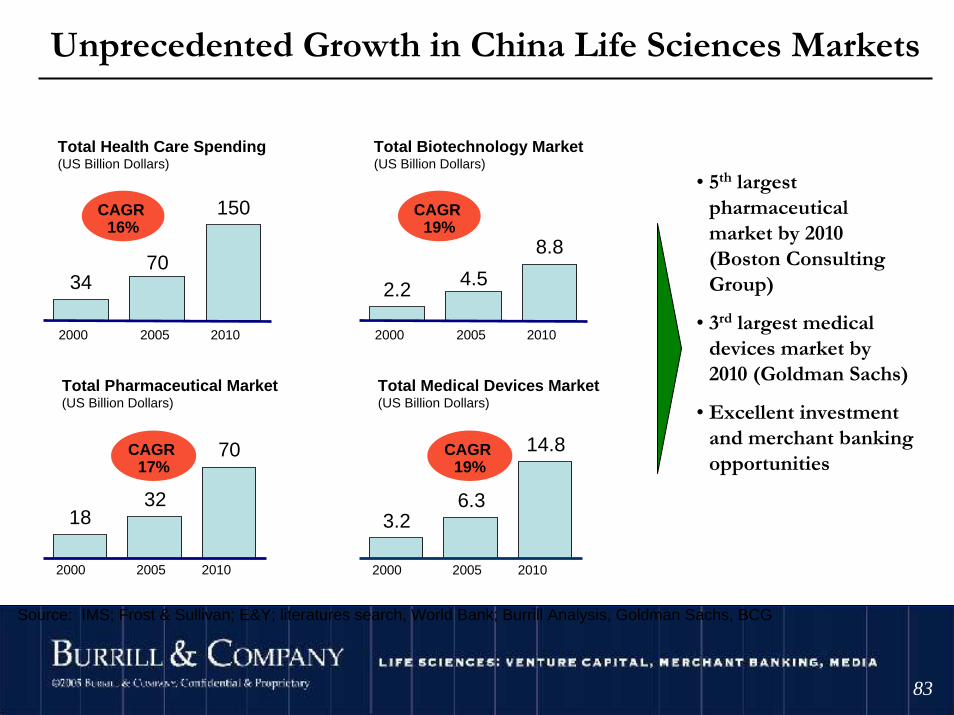

Unprecedented Growth in China Life Sciences Markets

2000 2005 2010

2000 2005 2010

Total Health Care Spending(US Billion Dollars)

Total Pharmaceutical Market(US Billion Dollars)

CAGR 16%

CAGR 17%

2000 2005 2010

2000 2005 2010

Total Biotechnology Market(US Billion Dollars)

Total Medical Devices Market(US Billion Dollars)

CAGR 19%

CAGR 19%

Source: IMS; Frost & Sullivan; E&Y; literatures search, World Bank; Burrill Analysis, Goldman Sachs, BCG

• 5th largest pharmaceutical market by 2010 (Boston Consulting Group)

• 3rd largest medical devices market by 2010 (Goldman Sachs)

• Excellent investment and merchant banking opportunities

34

150

70

1832

70

2.2

8.8

4.5

3.26.3

14.8

©2004 Burrill & Company. Confidential & Proprietary.

8484

China Life Sciences Strengths

Low costs in drug R&D and manufacturing

High growth potential in domestic market driven by aging population and improved personal income

Large researcher talent pool with technology and industry knowledge and skills

Strong central and local government support, with favorable tax policies and grants

Special strengths: Gene therapy, stem cell research, Traditional Chinese Medicine (TCM), chemistry services

Sources: *IMS Global Health

©2004 Burrill & Company. Confidential & Proprietary.

8585

China’s market size for ethical & OTC drugs in USD$Billion

346Total6China8Mexico8Canada9Spain

13Italy14UK19France20Germany53Japan

196USA2002 Top 10

447Total10Spain10Canada10Brazil14China15Italy16UK21France24Germany65Japan

262USA2005 Top 10

731Total15Brazil16Spain17Canada23Italy24UK24China28France37Germany81Japan

466USA2010 Top 10

Source: Boston Consulting Group

China’s Pharma Market To Become #5 World Wide by 2010

©2004 Burrill & Company. Confidential & Proprietary.

8686

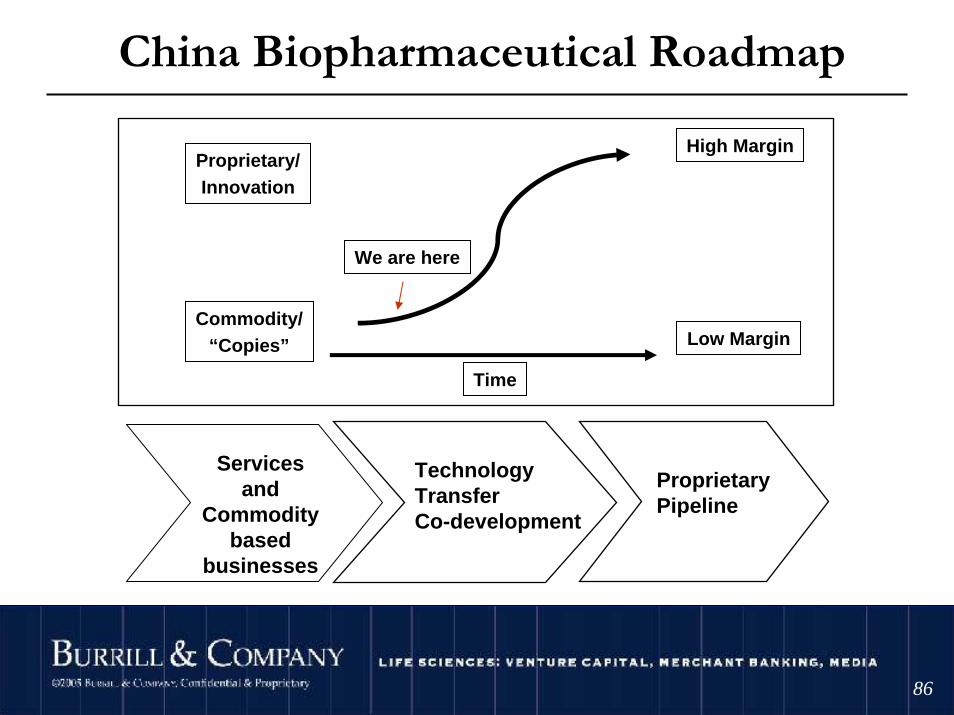

China Biopharmaceutical Roadmap

Time

Commodity/“Copies”

Proprietary/Innovation

Low Margin

High Margin

We are here

Technology TransferCo-development

Proprietary Pipeline

Services and

Commodity based

businesses

©2004 Burrill & Company. Confidential & Proprietary.

8787

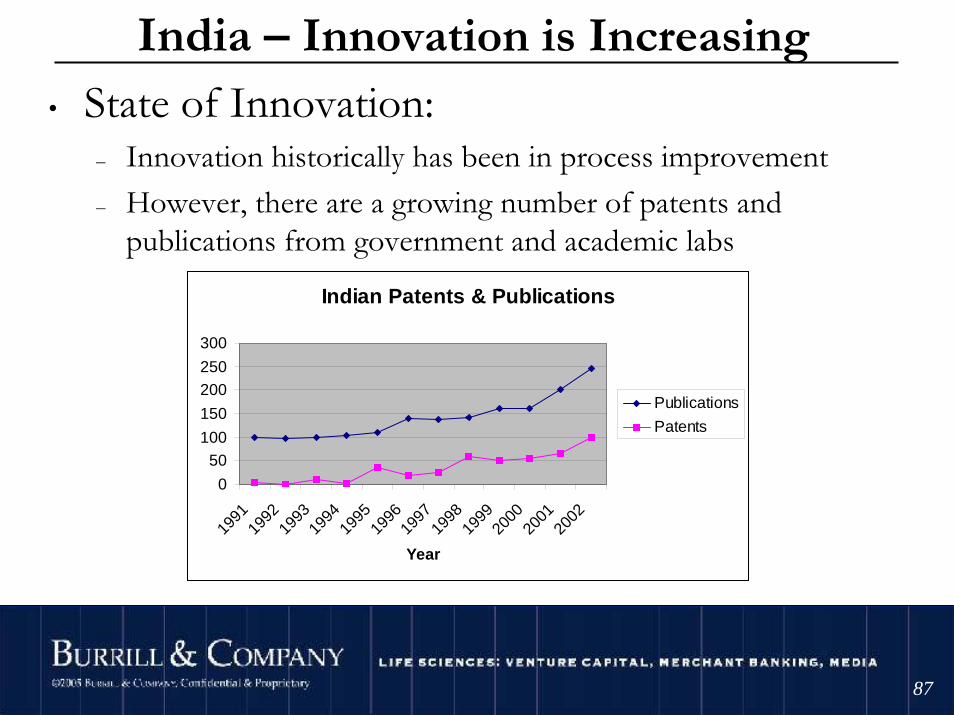

• State of Innovation:– Innovation historically has been in process improvement – However, there are a growing number of patents and

publications from government and academic labs

India – Innovation is Increasing

Indian Patents & Publications

0

50100

150

200250

300

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Year

Publications

Patents

-Nature Magazine

©2004 Burrill & Company. Confidential & Proprietary.

8888

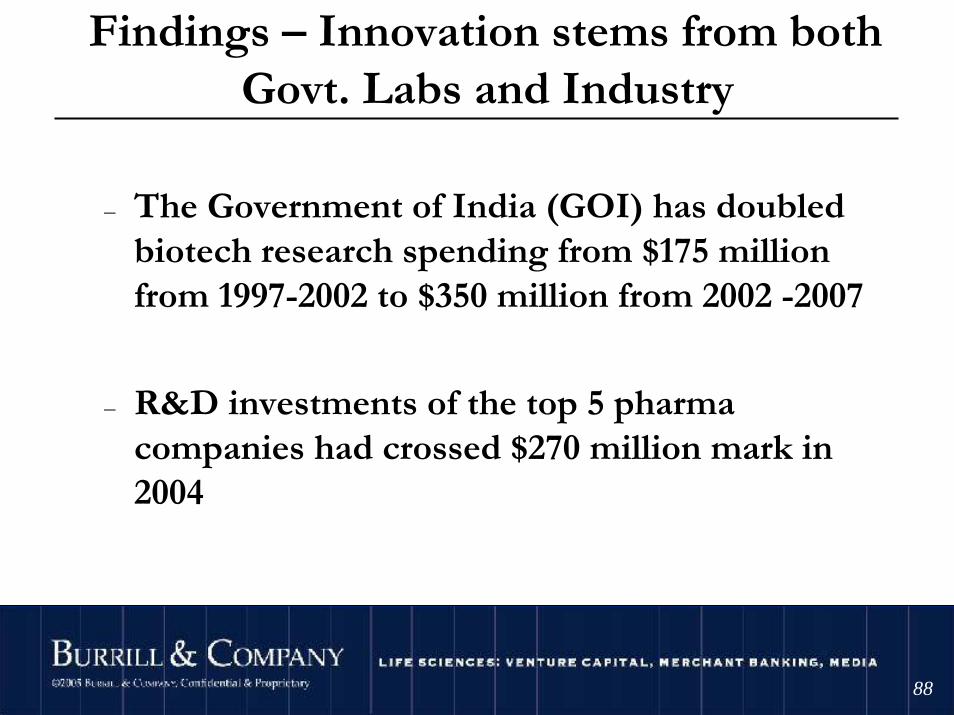

Findings – Innovation stems from bothGovt. Labs and Industry

– The Government of India (GOI) has doubled biotech research spending from $175 million from 1997-2002 to $350 million from 2002 -2007

– R&D investments of the top 5 pharma companies had crossed $270 million mark in 2004

©2004 Burrill & Company. Confidential & Proprietary.

8989

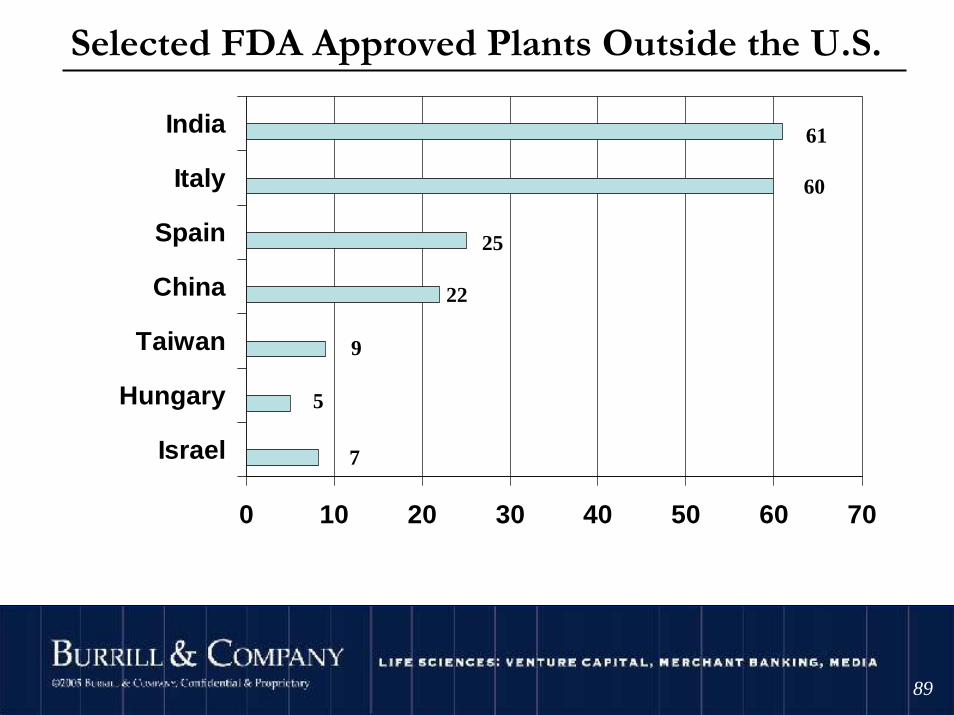

0 10 20 30 40 50 60 70

Israel

Hungary

Taiwan

China

Spain

Italy

India 61

60

25

22

9

5

7

Selected FDA Approved Plants Outside the U.S.

Source: Businessworld Number of Plants

©2004 Burrill & Company. Confidential & Proprietary.

90

Capital Markets

©2004 Burrill & Company. Confidential & Proprietary.

9191

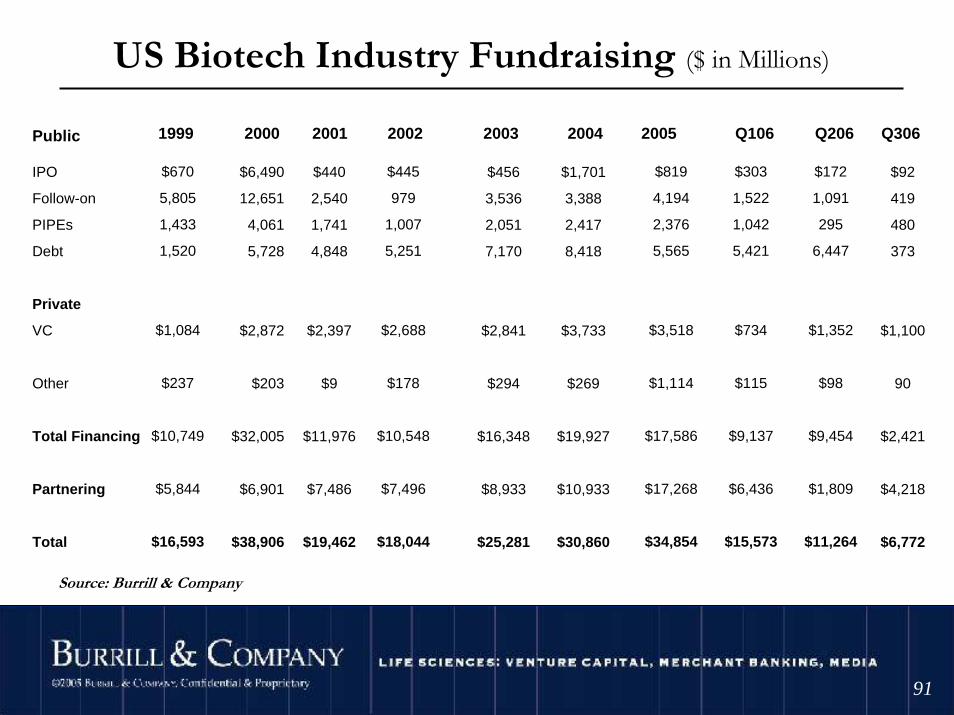

US Biotech Industry Fundraising ($ in Millions)

IPO

Follow-on

PIPEs

Debt

Private

VC

Other

Total Financing

Partnering

Total

$670

5,805

1,433

1,520

$1,084

$237

$10,749

$5,844

$16,593

$6,490

12,651

4,061

5,728

$2,872

$203

$32,005

$6,901

$38,906

$440

2,540

1,741

4,848

$2,397

$9

$11,976

$7,486

$19,462

$445

979

1,007

5,251

$2,688

$178

$10,548

$7,496

$18,044

$456

3,536

2,051

7,170

$2,841

$294

$16,348

$8,933

$25,281

$1,701

3,388

2,417

8,418

$3,733

$269

$19,927

$10,933

$30,860

Public 1999 2000 2001 2002 2003 2004

$819

4,194

2,376

5,565

$3,518

$1,114

$17,586

$17,268

$34,854

2005

Source: Burrill & Company

$303

1,522

1,042

5,421

$734

$115

$9,137

$6,436

$15,573

Q106

$172

1,091

295

6,447

$1,352

$98

$9,454

$1,809

$11,264

$92

419

480

373

$1,100

90

$2,421

$4,218

$6,772

Q206 Q306

©2004 Burrill & Company. Confidential & Proprietary.

9292

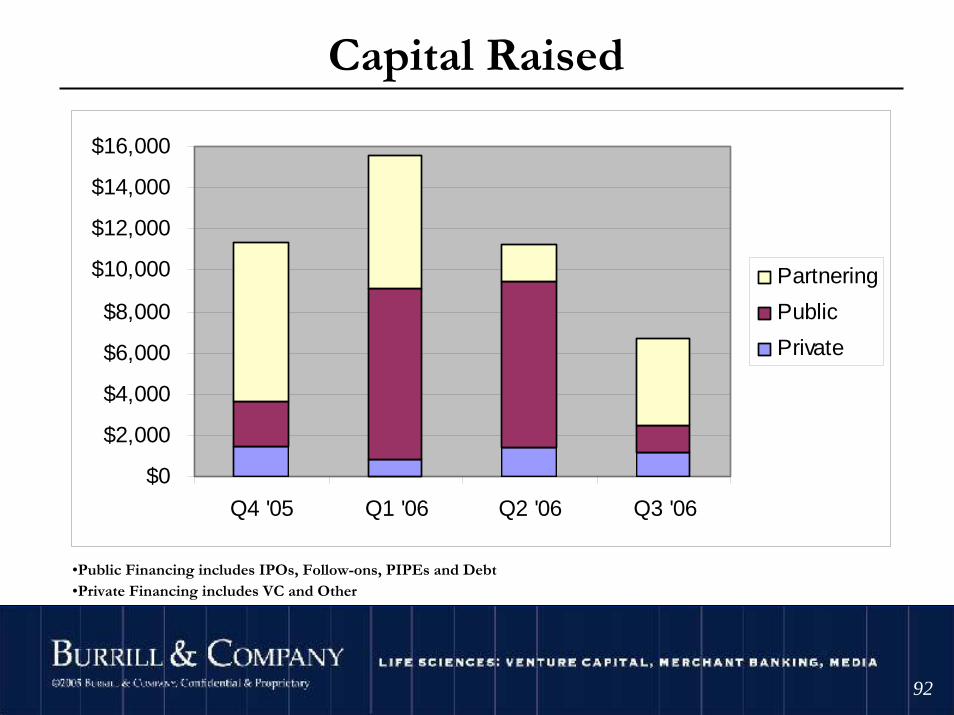

Capital Raised

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

Q4 '05 Q1 '06 Q2 '06 Q3 '06

Partnering

Public

Private

•Public Financing includes IPOs, Follow-ons, PIPEs and Debt•Private Financing includes VC and Other

©2004 Burrill & Company. Confidential & Proprietary.

9393

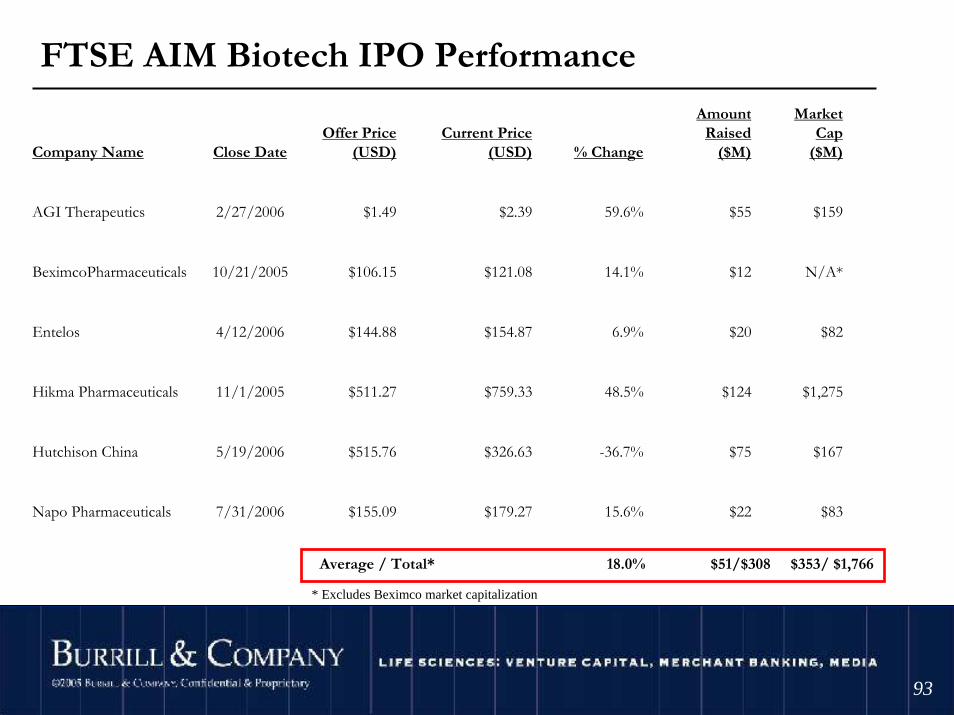

FTSE AIM Biotech IPO Performance

Company Name Close DateOffer Price

(USD)Current Price

(USD) % Change

Amount Raised

($M)

Market Cap

($M)

AGI Therapeutics 2/27/2006 $1.49 $2.39 59.6% $55 $159

BeximcoPharmaceuticals 10/21/2005 $106.15 $121.08 14.1% $12 N/A*

Entelos 4/12/2006 $144.88 $154.87 6.9% $20 $82

Hikma Pharmaceuticals 11/1/2005 $511.27 $759.33 48.5% $124 $1,275

Hutchison China 5/19/2006 $515.76 $326.63 -36.7% $75 $167

Napo Pharmaceuticals 7/31/2006 $155.09 $179.27 15.6% $22 $83

Average / Total* 18.0% $51/$308 $353/ $1,766

* Excludes Beximco market capitalization

©2004 Burrill & Company. Confidential & Proprietary.

9494

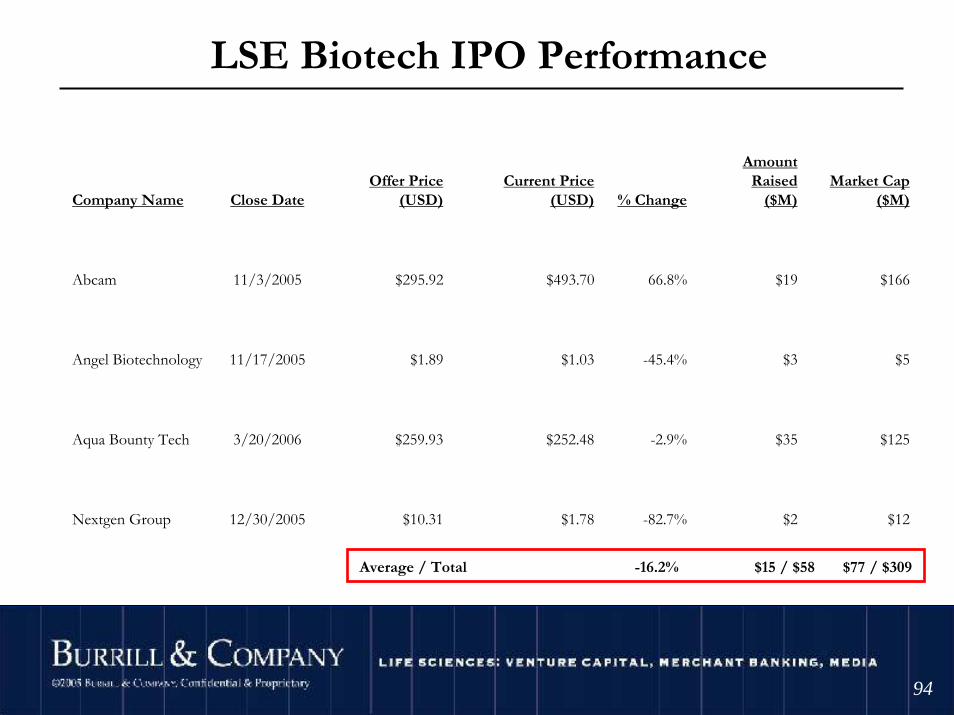

LSE Biotech IPO Performance

Company Name Close DateOffer Price

(USD)Current Price

(USD) % Change

Amount Raised

($M)Market Cap

($M)

Abcam 11/3/2005 $295.92 $493.70 66.8% $19 $166

Angel Biotechnology 11/17/2005 $1.89 $1.03 -45.4% $3 $5

Aqua Bounty Tech 3/20/2006 $259.93 $252.48 -2.9% $35 $125

Nextgen Group 12/30/2005 $10.31 $1.78 -82.7% $2 $12

Average / Total -16.2% $15 / $58 $77 / $309

©2004 Burrill & Company. Confidential & Proprietary.

9595

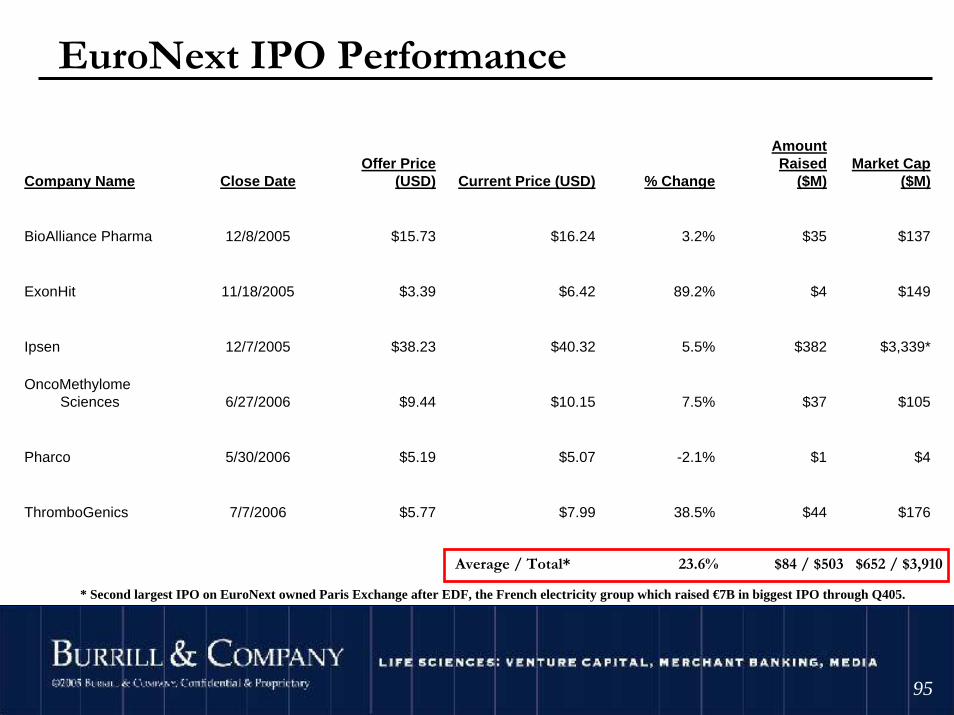

EuroNext IPO Performance

Company Name Close DateOffer Price

(USD) Current Price (USD) % Change

Amount Raised

($M)Market Cap

($M)

BioAlliance Pharma 12/8/2005 $15.73 $16.24 3.2% $35 $137

ExonHit 11/18/2005 $3.39 $6.42 89.2% $4 $149

Ipsen 12/7/2005 $38.23 $40.32 5.5% $382 $3,339*

OncoMethylomeSciences 6/27/2006 $9.44 $10.15 7.5% $37 $105

Pharco 5/30/2006 $5.19 $5.07 -2.1% $1 $4

ThromboGenics 7/7/2006 $5.77 $7.99 38.5% $44 $176

Average / Total* 23.6% $84 / $503 $652 / $3,910

* Second largest IPO on EuroNext owned Paris Exchange after EDF, the French electricity group which raised €7B in biggest IPO through Q405.

©2004 Burrill & Company. Confidential & Proprietary.

9696

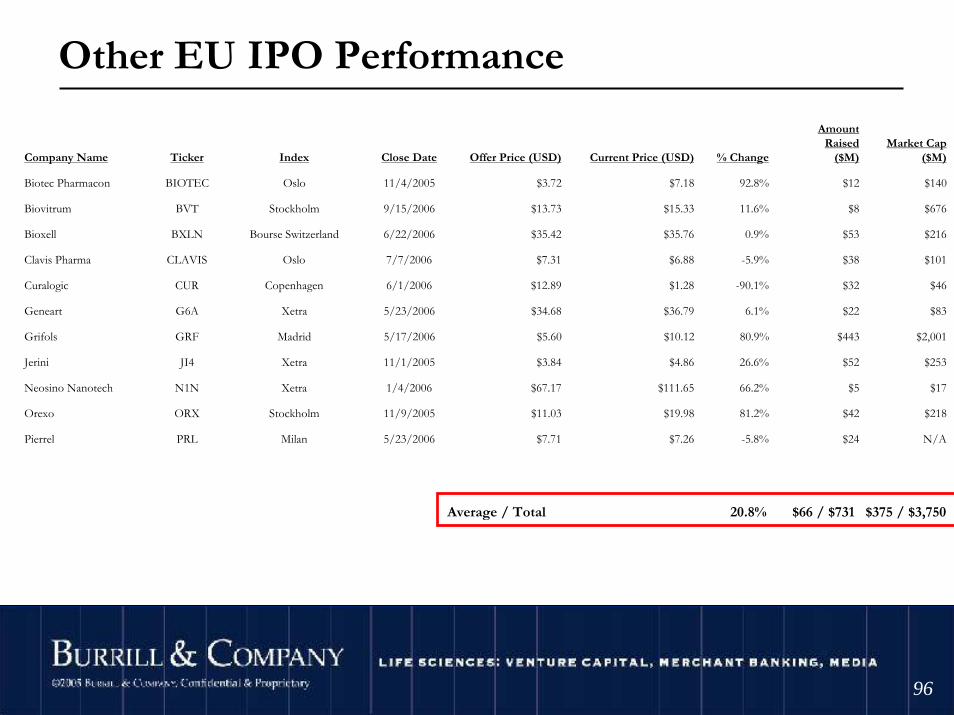

Other EU IPO Performance

Company Name Ticker Index Close Date Offer Price (USD) Current Price (USD) % Change

Amount Raised

($M)Market Cap

($M)

Biotec Pharmacon BIOTEC Oslo 11/4/2005 $3.72 $7.18 92.8% $12 $140

Biovitrum BVT Stockholm 9/15/2006 $13.73 $15.33 11.6% $8 $676

Bioxell BXLN Bourse Switzerland 6/22/2006 $35.42 $35.76 0.9% $53 $216

Clavis Pharma CLAVIS Oslo 7/7/2006 $7.31 $6.88 -5.9% $38 $101

Curalogic CUR Copenhagen 6/1/2006 $12.89 $1.28 -90.1% $32 $46

Geneart G6A Xetra 5/23/2006 $34.68 $36.79 6.1% $22 $83

Grifols GRF Madrid 5/17/2006 $5.60 $10.12 80.9% $443 $2,001

Jerini JI4 Xetra 11/1/2005 $3.84 $4.86 26.6% $52 $253

Neosino Nanotech N1N Xetra 1/4/2006 $67.17 $111.65 66.2% $5 $17

Orexo ORX Stockholm 11/9/2005 $11.03 $19.98 81.2% $42 $218

Pierrel PRL Milan 5/23/2006 $7.71 $7.26 -5.8% $24 N/A

Average / Total 20.8% $66 / $731 $375 / $3,750

©2004 Burrill & Company. Confidential & Proprietary.

9797

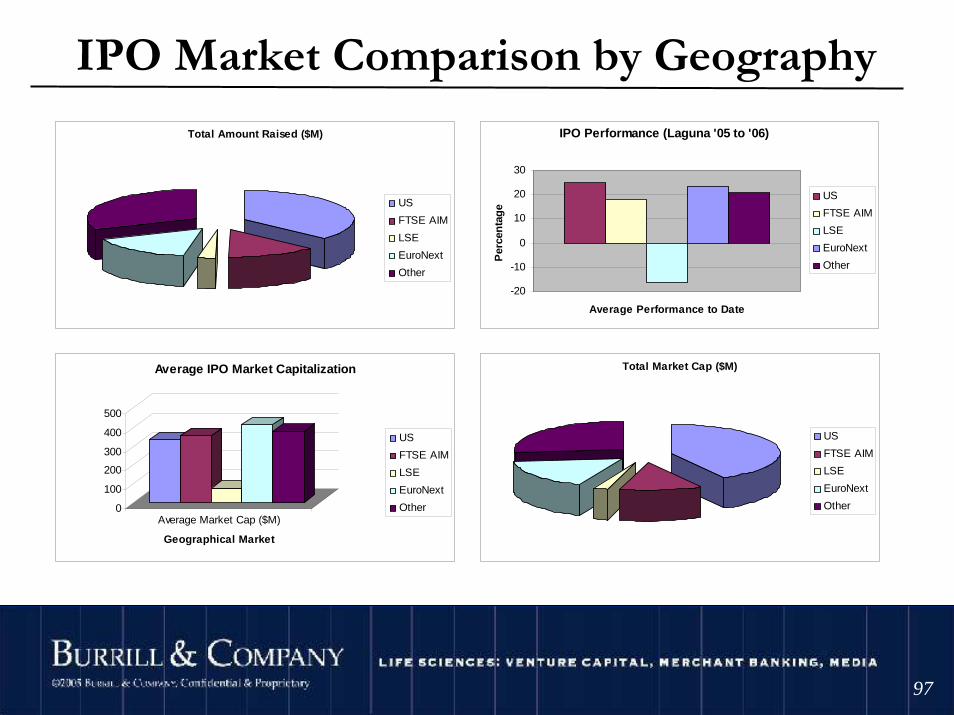

IPO Market Comparison by Geography

Total Amount Raised ($M)

US

FTSE AIM

LSE

EuroNext

Other

IPO Performance (Laguna '05 to '06)

-20

-10

0

10

20

30

Average Performance to Date

Per

cen

tag

e

US

FTSE AIM

LSE

EuroNext

Other

0

100

200

300

400

500

Average Market Cap ($M)

Geographical Market

Average IPO Market Capitalization

US

FTSE AIM

LSE

EuroNext

Other

Total Market Cap ($M)

US

FTSE AIM

LSE

EuroNext

Other

©2004 Burrill & Company. Confidential & Proprietary.

9898

Current Price

Amount Raised

Market Cap

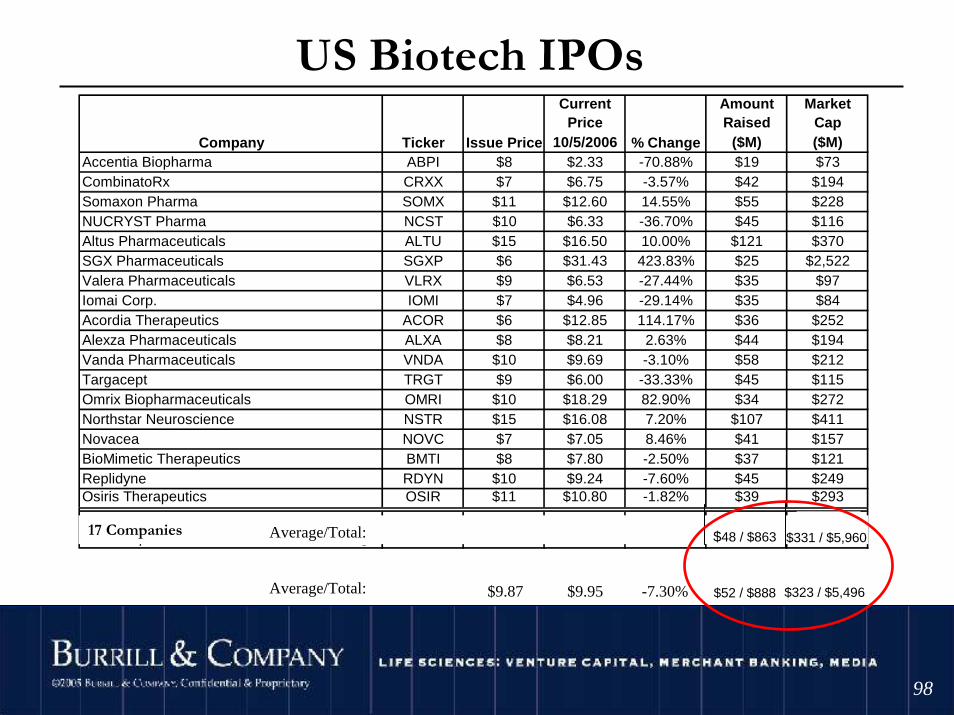

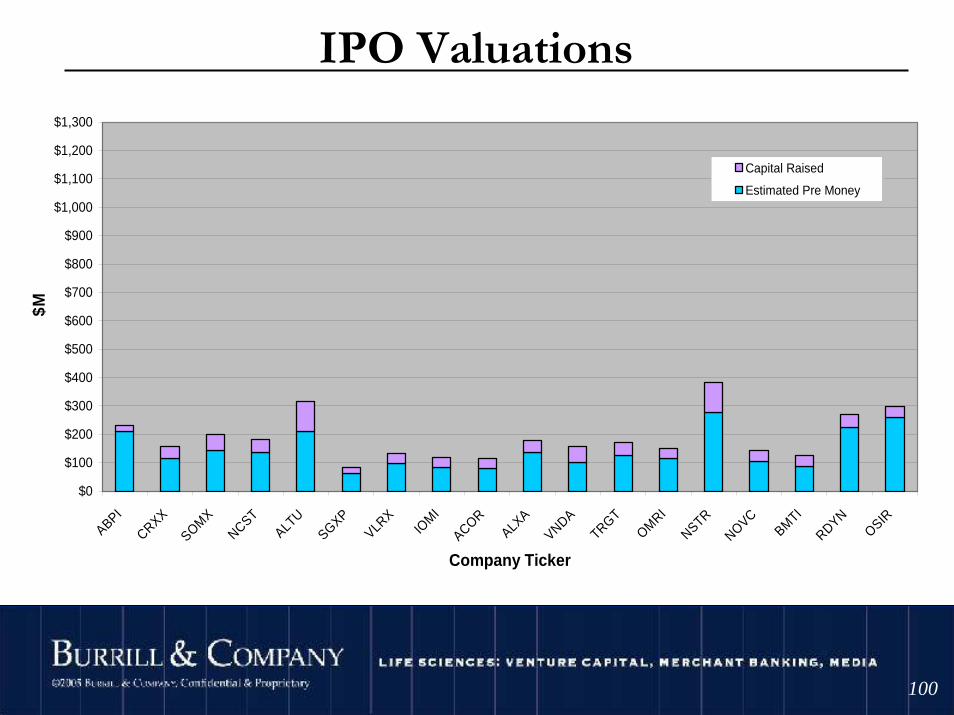

10/5/2006 ($M) ($M)Accentia Biopharma ABPI $8 $2.33 -70.88% $19 $73 CombinatoRx CRXX $7 $6.75 -3.57% $42 $194 Somaxon Pharma SOMX $11 $12.60 14.55% $55 $228 NUCRYST Pharma NCST $10 $6.33 -36.70% $45 $116 Altus Pharmaceuticals ALTU $15 $16.50 10.00% $121 $370 SGX Pharmaceuticals SGXP $6 $31.43 423.83% $25 $2,522 Valera Pharmaceuticals VLRX $9 $6.53 -27.44% $35 $97 Iomai Corp. IOMI $7 $4.96 -29.14% $35 $84 Acordia Therapeutics ACOR $6 $12.85 114.17% $36 $252 Alexza Pharmaceuticals ALXA $8 $8.21 2.63% $44 $194 Vanda Pharmaceuticals VNDA $10 $9.69 -3.10% $58 $212 Targacept TRGT $9 $6.00 -33.33% $45 $115 Omrix Biopharmaceuticals OMRI $10 $18.29 82.90% $34 $272 Northstar Neuroscience NSTR $15 $16.08 7.20% $107 $411 Novacea NOVC $7 $7.05 8.46% $41 $157 BioMimetic Therapeutics BMTI $8 $7.80 -2.50% $37 $121 Replidyne RDYN $10 $9.24 -7.60% $45 $249 Osiris Therapeutics OSIR $11 $10.80 -1.82% $39 $293

18 Companies Average: $9.25 $10.75 24.87% $48 $331

Company Ticker Issue Price % Change

US Biotech IPOs

17 Companies Average/Total:

-7.30% $52 / $888 $323 / $5,496$9.95$9.87

$48 / $863

Average/Total:

$5,960 $331 / $5,960

©2004 Burrill & Company. Confidential & Proprietary.

9999

# of IPOs Amount Raised * Perf. since IPO Ups / Downs

2003 7 $438 M -6% 2 / 5

2004 29 $1,628 M +30% 14 / 14/ 1acq.

2005 17 $819 M +21% 10 / 7

2006 6 $303 M +18% 4 / 2

TOTAL 60 $2,892 M +16% 30 / 29 / 1acq.

IPO Window Summary 2003-2006 (as of 3/31/06)

* Includes over-allotments

©2004 Burrill & Company. Confidential & Proprietary.

100100

IPO Valuations

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

ABPI

CRXX

SOMX

NCST

ALTU

SGXP

VLRX

IOMI

ACOR

ALXA

VNDA

TRGT

OMRI

NSTR

NOVC

BMTI

RDYN

OSIR

Company Ticker

$M

Capital Raised

Estimated Pre Money

©2004 Burrill & Company. Confidential & Proprietary.

101101

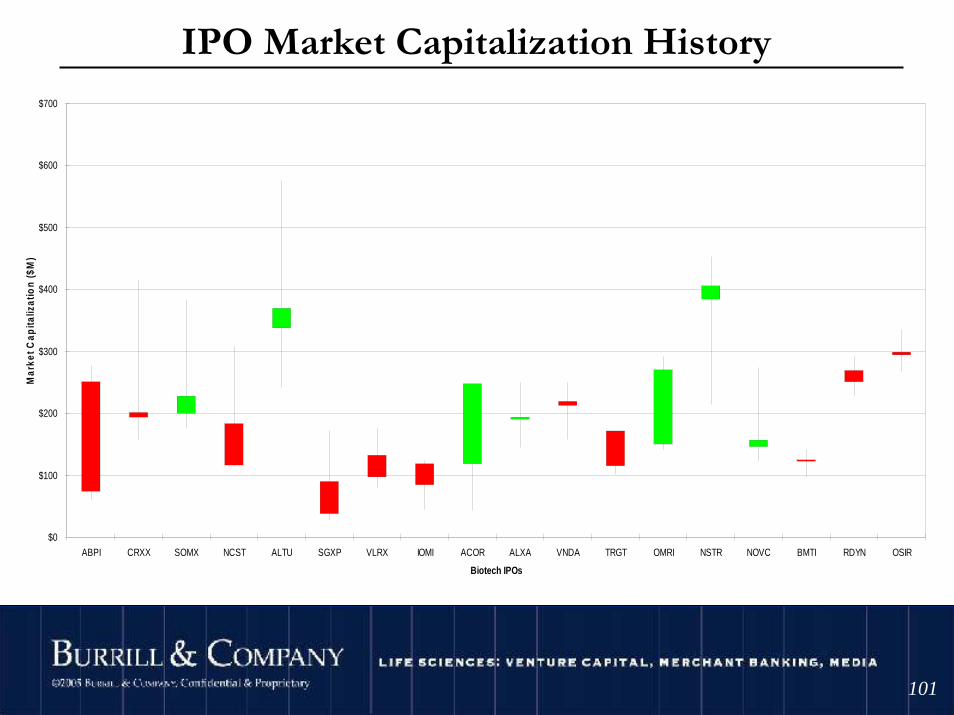

IPO Market Capitalization History

$0

$100

$200

$300

$400

$500

$600

$700

ABPI CRXX SOMX NCST ALTU SGXP VLRX IOMI ACOR ALXA VNDA TRGT OMRI NSTR NOVC BMTI RDYN OSIR

Biotech IPOs

Mar

ket C

apita

lizat

ion

($M

)

©2004 Burrill & Company. Confidential & Proprietary.

102102

• Surge in M&A for US and European biotechs/pharma, changing tactics

• US saw first attempt at hostile takeover (AnorMed rebuffs GENZ, courted by MLNM)

– European M&A competition even higher, survival for mid-sized players

• Expiring patents, encroaching generics, pipeline shortages– Includes enabling tech, not just pipelines

• More global access to capital– More companies choosing to IPO on AIM (~250 companies listed),

and other non-US markets– Interest in biotech from hedge funds– US IPOs slow pace, number of PIPEs continues climb

Financing Events

©2004 Burrill & Company. Confidential & Proprietary.

103103

• Innovation and development rewarded but kept in check by safety issues

– RNAi work wins Nobel in Medicine (Fire, Stanford / Mello – U Mass), products progress through clinical development (Alnylam, SIRNA, Nucleonics)

– Kornberg (Stanford) wins Nobel in Chemistry for work on eukaryotic transcription

– However, drug development risks still very real (Parexel/TeGenero - multiple deaths in phase I)

• Intricacies of “evolution” top list as the scientific breakthrough of 2005-2006

– Widely published study showing a mere 4% difference between human and chimp DNA

– Runner’s up - advances in system biology, genetics of brain disease, flu studies

What’s happening in Science?

©2004 Burrill & Company. Confidential & Proprietary.

104104

• Stem Cells linger in scientific & business cloudy environment– Advanced Cell Therapeutics creates embryonic stem cells without destroying embryo

– US political football with limited federal funding• Alternative development strategies, some research moves off-shore (Asia, UK)

– Increased State funding initiatives• CIRM gets State of California support for bond anticipation notes

• Other state initiatives- Missouri/Maryland/Wisconsin/NY/Mass all make progress

• Innovation transfer slows as federal basic research funding shrinks– Gap from academic medical centers to private sector, new models tried (UPMC,

MIT)

• Europe/Japan/ROW increasing investment in basic research

What’s happening in Science?

©2004 Burrill & Company. Confidential & Proprietary.

105105

• Complexity of product approvals, market re-entry– FDA approval of 1st Follow-On-Biologic lagged behind EMEA

approval (Omnitrope, Sandoz) but precedent now set (BioSimilars/BioGenerics)

– In-Vitro Diagnostic Multivariate Index Assays (IVDMIAs) may require FDA approval vs. CLIA certification

– Theragnostics– how to find responsive population for best outcomes– Drug safety and pharmacovigilence

• Tysabri re-enters but Bayer hides Trasylol data – IOM report on drug safety- tougher challenges for industry– Off label promotion strenuously challenged– CMS/FDA comparative studies

Regulatory Events

©2004 Burrill & Company. Confidential & Proprietary.

106106

• Hostile US regulatory environment for small companies continues– Sarbanes-Oxley’s excessive burden (section 404)– SBIR grants challenged– SEC disclosure / corporate governance requirements– Costs for listing in U.K. are lower than the U.S.

• Challenges of Part B (prescription drug benefit for seniors)• Medicare Modernization Act incentives for companies seeking to

address costs for expanding aging market• Leadership changes at CMS (McClellan announced departure)• Leadership approval pending at FDA (Andy von Eschenbach)

– Top Women’s Health official Susan Wood quits over Plan B which year later gets approved

• FDA’s New Drug Safety & Critical Path Initiatives- will the approval rate freeze?

Regulatory Events

©2004 Burrill & Company. Confidential & Proprietary.

107107

• US taxpayers unwilling to support innovation by paying higher prices, potential price ceiling emerges

– Big pharma challenged on “country by country” pricing– AMGN prices Vectibix at 20% discount to IMCL’s Erbitux– Re-importation of drugs across border continues as political issue

• Big US Pharma squeezed for profits and risk empty pipelines– Leadership changes (McKinnell/PFE, Gilmartin/MRK,

Dolan/BMY)• Developing world diseases - big opportunity

– TB, Malaria, AIDS, Avian Flu, pandemic diseases– New funders (Gates Foundation, VCs, KPCB $200m pandemic

disease fund)• Worldwide interest in BioFuels, global economic incentives

Marketplace Events

©2004 Burrill & Company. Confidential & Proprietary.

108108

• The time is now for life sciences• Confluence of technologies is changing biotech and the healthcare world• Personalized, predictive and preventative medicine is changing healthcare• Payor/reimbursement world is changing with Medicare’s power• Market opportunities are different today (pandemic diseases, memory,

obesity, aging, and wellness)• Wellness is a huge growth market• AgBio is back, animal genomics is ready• Industrial biotech’s time has arrived• Capital markets worldwide are robust, but expensive

Biotech 2006

Biotech is a global businessBe aggressive, be bold…the competition is

©2004 Burrill & Company. Confidential & Proprietary.

109

the next 12 months will be interesting!

Biotech’s on a roll…

©2004 Burrill & Company. Confidential & Proprietary.

110110

Biotech 2006Life Sciences: A Changing Prescription

NY Pharma

October 19th, 2006

G. Steven Burrill, CEOBurrill & Company

![First part: Deep Learning for Speech recognition · 2017. 4. 4. · a guy on a skate board on the side of a ramp [bear (0.71)] (elephant (0.99jl [brown (0.6B)) [baby [laying (0.61))](https://img.pdfslide.us/doc/110x75/60368da64232a67aab24f1b4/first-part-deep-learning-for-speech-recognition-2017-4-4-a-guy-on-a-skate.jpg)