Embed Size (px)

Citation preview

Biosurgery: Core Products Provide Foundation for Growth

Ann Merrifield, President

May 7, 2008 Analyst Day

2

Biosurgery Today

Sepra® Family Epicel®

Marketed Products and Services

Carticel® / MACI®*Synvisc®

Osteoarthritis OrthopaedicBiologics

AdhesionPrevention

Severe Burn

*Marketed in Europe and Australia

3

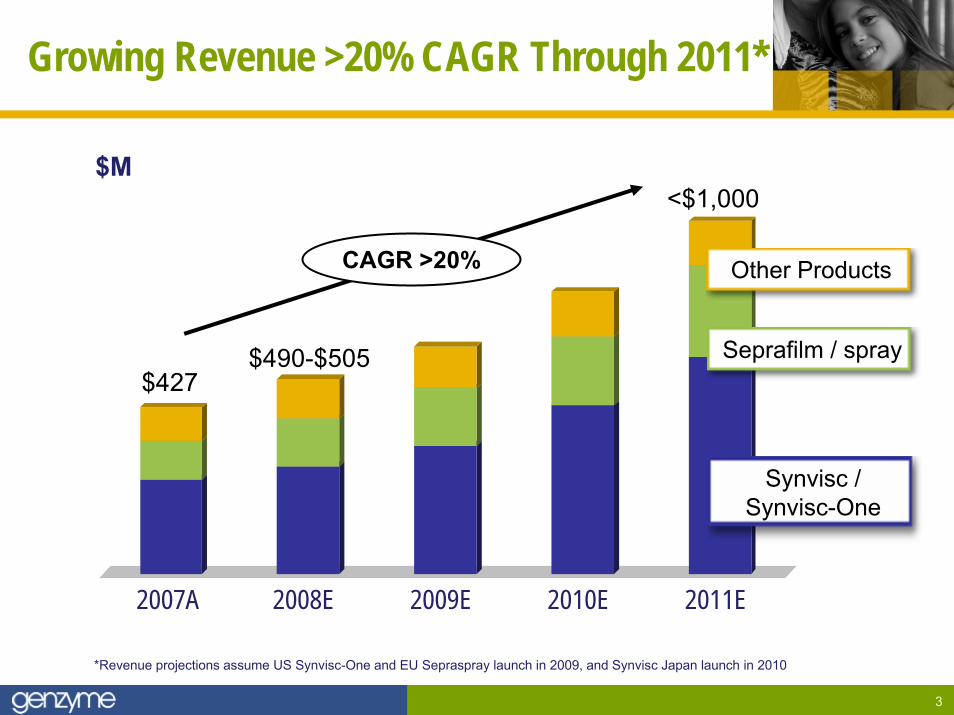

Growing Revenue >20% CAGR Through 2011*

2007A 2008E 2009E 2010E 2011E

$427

<$1,000

$490-$505

Synvisc / Synvisc-One

Seprafilm / spray

Other Products

$M

*Revenue projections assume US Synvisc-One and EU Sepraspray launch in 2009, and Synvisc Japan launch in 2010

CAGR >20%

4

Agenda

► Sepra family

► Synvisc and Synvisc-One

► Growth opportunities beyond 2011

5

Sepra Growth Drivers

►Seprafilm: diversification to adjacent procedures– Colorectal trauma– Gynecology ob-gyn

►Sepraspray: 2-3x film opportunity

►Ex-US “relaunch” with combined film / spray portfolio

Growth

6

Global Seprafilm Revenue Growth

2003 2004 2005 2006 2007

$46

$99

$59$64

$79

$M

7

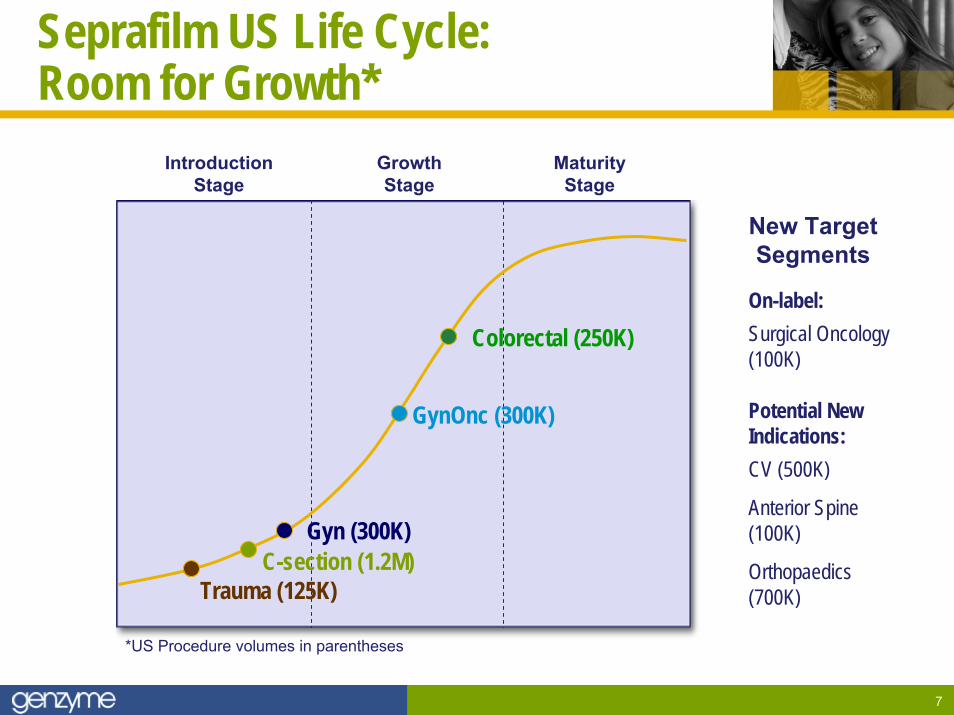

Seprafilm US Life Cycle: Room for Growth*

*US Procedure volumes in parentheses

On-label:Surgical Oncology (100K)

Potential New Indications:CV (500K)

Anterior Spine (100K)

Orthopaedics(700K)

New TargetSegments

Introduction Stage

GrowthStage

MaturityStage

C-section (1.2M)

GynOnc (300K)

Colorectal (250K)

Gyn (300K)

Trauma (125K)

8

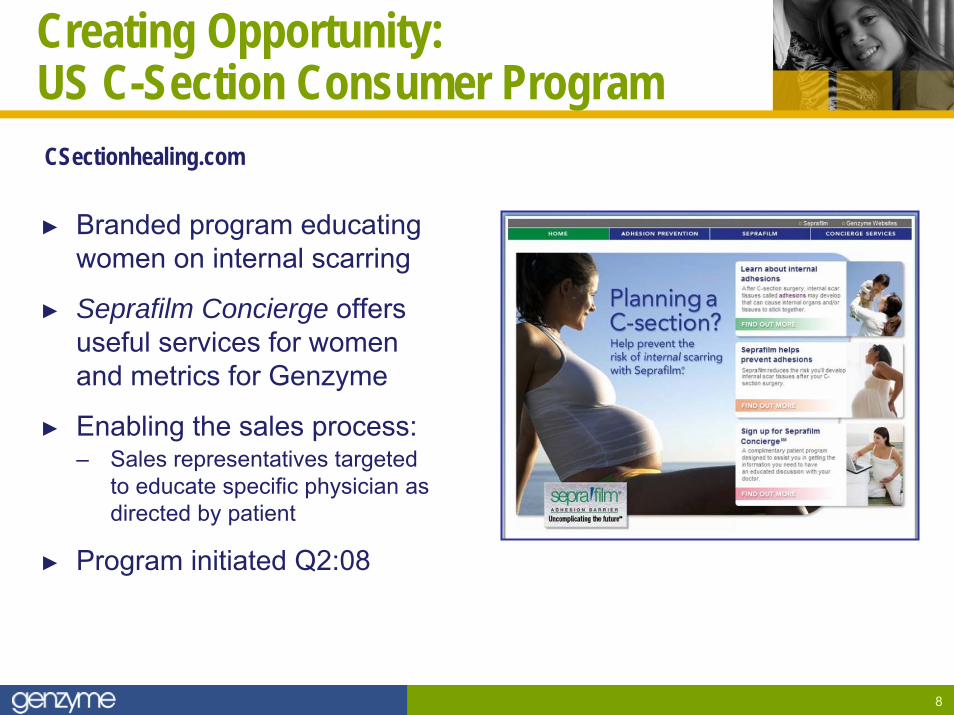

Creating Opportunity: US C-Section Consumer Program

► Branded program educating women on internal scarring

► Seprafilm Concierge offers useful services for women and metrics for Genzyme

► Enabling the sales process: – Sales representatives targeted

to educate specific physician as directed by patient

► Program initiated Q2:08

CSectionhealing.com

9

Sepraspray Progress

► Clinical program underway– EU abdominal trial – US pelvic pilot

► Preparing for commercial launch– 2009E: EU, selected Asian markets– 2010E: Canada, Australia– ‘12-’13E: US– ’13-’14E: Japan

10

Seprafilm Global Markets: Early Stagesof Geographic Penetration

Major Markets

11

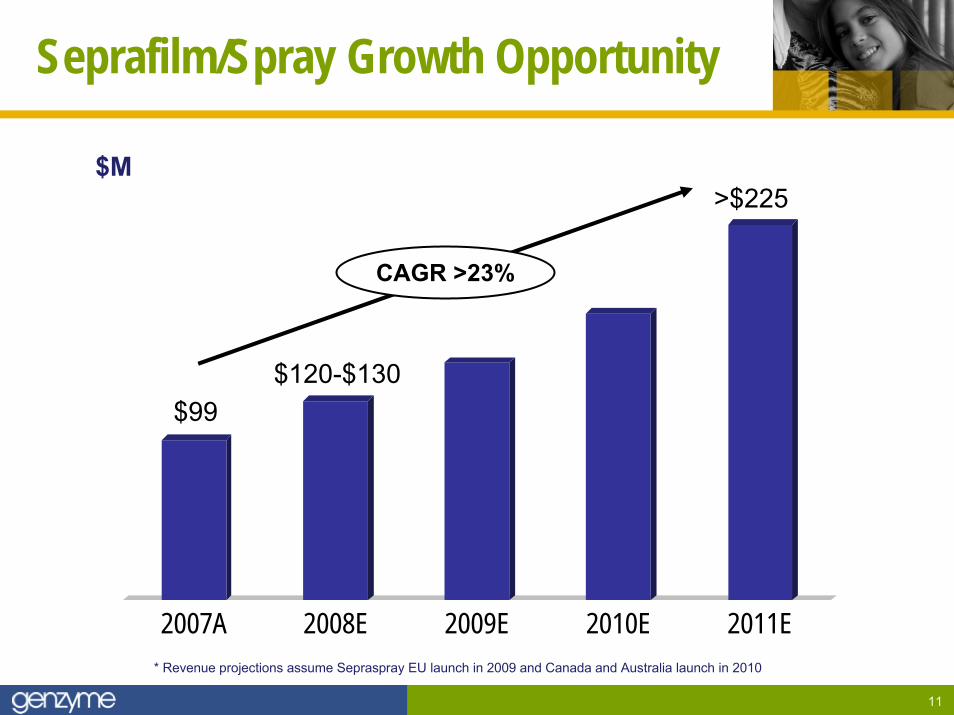

Seprafilm/Spray Growth Opportunity

2007A 2008E 2009E 2010E 2011E

$99$120-$130

>$225

CAGR >23%

* Revenue projections assume Sepraspray EU launch in 2009 and Canada and Australia launch in 2010

$M

12

Agenda

► Sepra family

► Synvisc and Synvisc-One

► Growth opportunities beyond 2011

13

Synvisc Growth Drivers

► Expanding patient types and repeat usage

► Robust competitive positioning

► Expanding consumer program

► Stabilizing US pricing and share– 3 – 4% ASP increase

effective April 1, 2008

► Synvisc Japan launch: 2010E

► Synvisc-One launches:– 2008E: EU, Canada, Australia– 2009E: US– 2012E: Japan

Growth

14

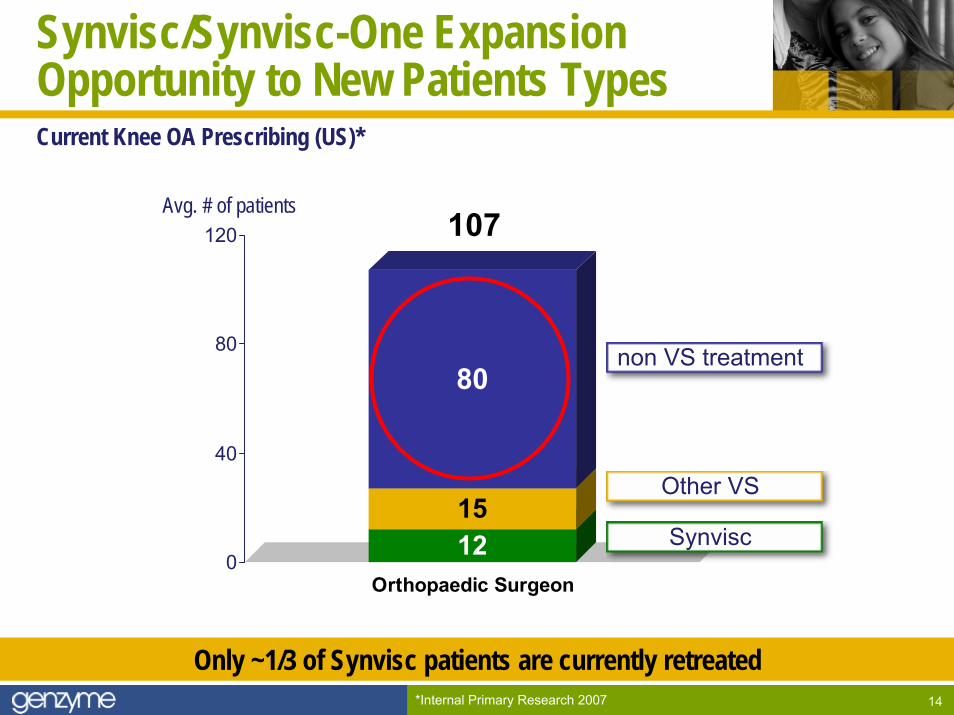

1215

80

0

40

80

120

Orthopaedic Surgeon

107

Synvisc

Other VS

non VS treatment

Avg. # of patients

Synvisc/Synvisc-One Expansion Opportunity to New Patients TypesCurrent Knee OA Prescribing (US)*

*Internal Primary Research 2007

Only ~1/3 of Synvisc patients are currently retreated

15

Competitive Positioning for the Physician

16

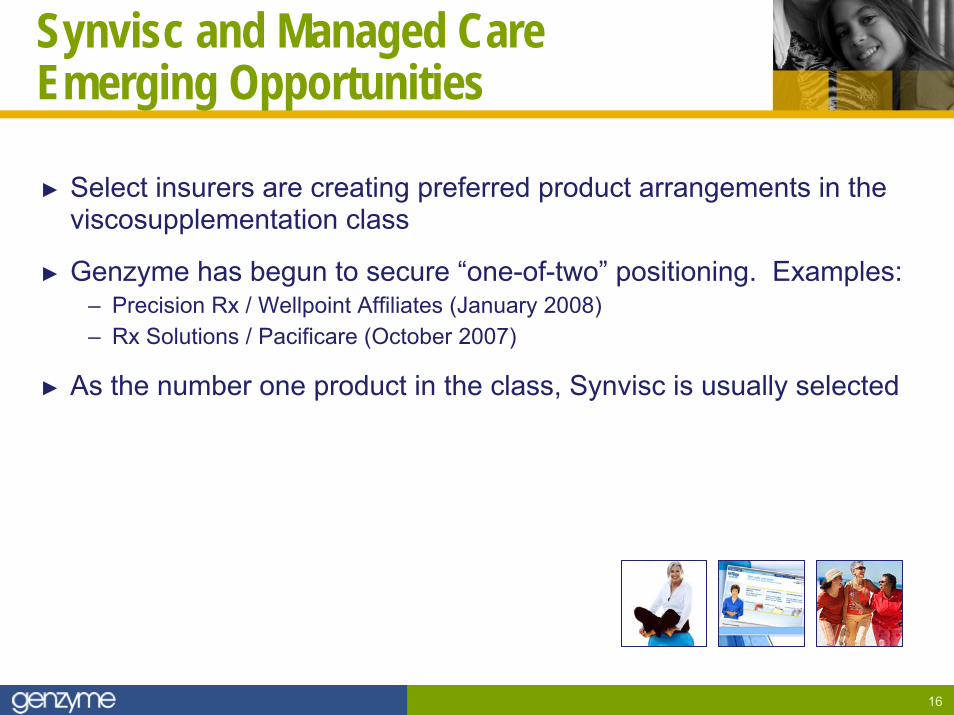

Synvisc and Managed CareEmerging Opportunities

► Select insurers are creating preferred product arrangements in the viscosupplementation class

► Genzyme has begun to secure “one-of-two” positioning. Examples: – Precision Rx / Wellpoint Affiliates (January 2008)– Rx Solutions / Pacificare (October 2007)

► As the number one product in the class, Synvisc is usually selected

17

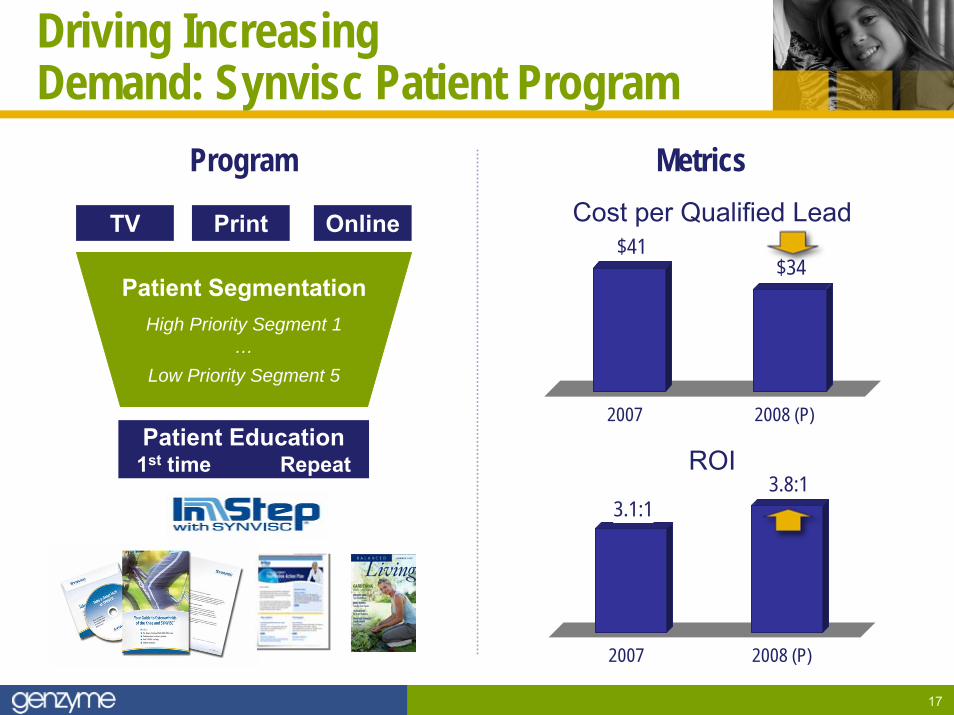

Driving Increasing Demand: Synvisc Patient Program

TV Print Online

Patient SegmentationHigh Priority Segment 1

…Low Priority Segment 5

Patient Education1st time Repeat

Cost per Qualified Lead

ROI

Program Metrics

$41$34

2007 2008 (P)

3.1:13.8:1

2007 2008 (P)

18

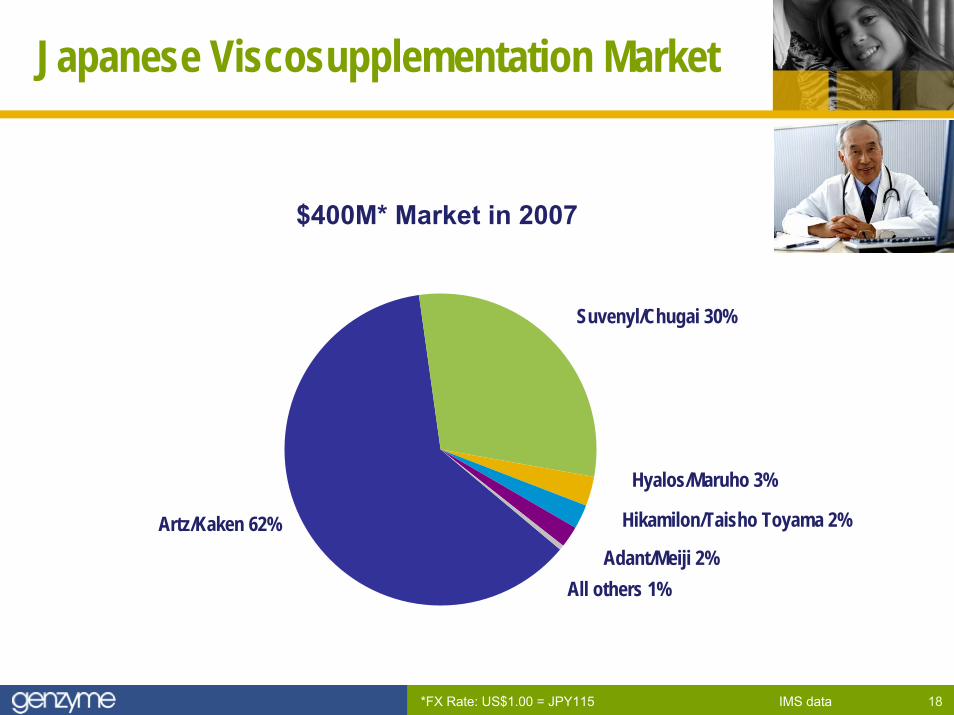

Japanese Viscosupplementation Market

$400M* Market in 2007

IMS data*FX Rate: US$1.00 = JPY115

Artz/Kaken 62%

All others 1%Adant/Meiji 2%

Hikamilon/Taisho Toyama 2%

Hyalos/Maruho 3%

Suvenyl/Chugai 30%

19

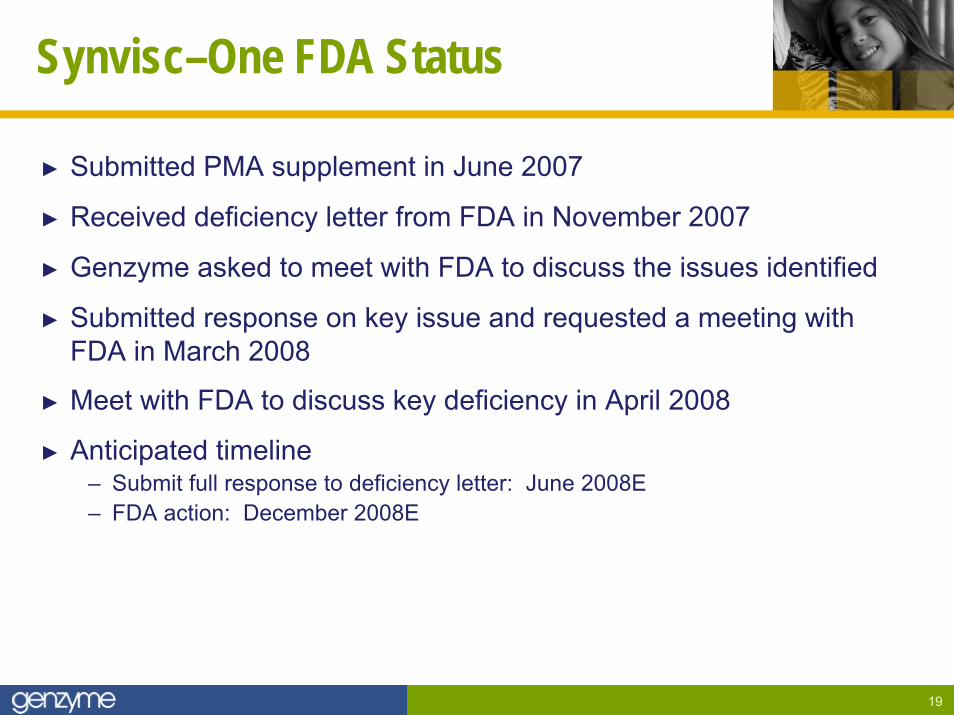

Synvisc–One FDA Status

► Submitted PMA supplement in June 2007

► Received deficiency letter from FDA in November 2007

► Genzyme asked to meet with FDA to discuss the issues identified

► Submitted response on key issue and requested a meeting with FDA in March 2008

► Meet with FDA to discuss key deficiency in April 2008

► Anticipated timeline – Submit full response to deficiency letter: June 2008E– FDA action: December 2008E

20

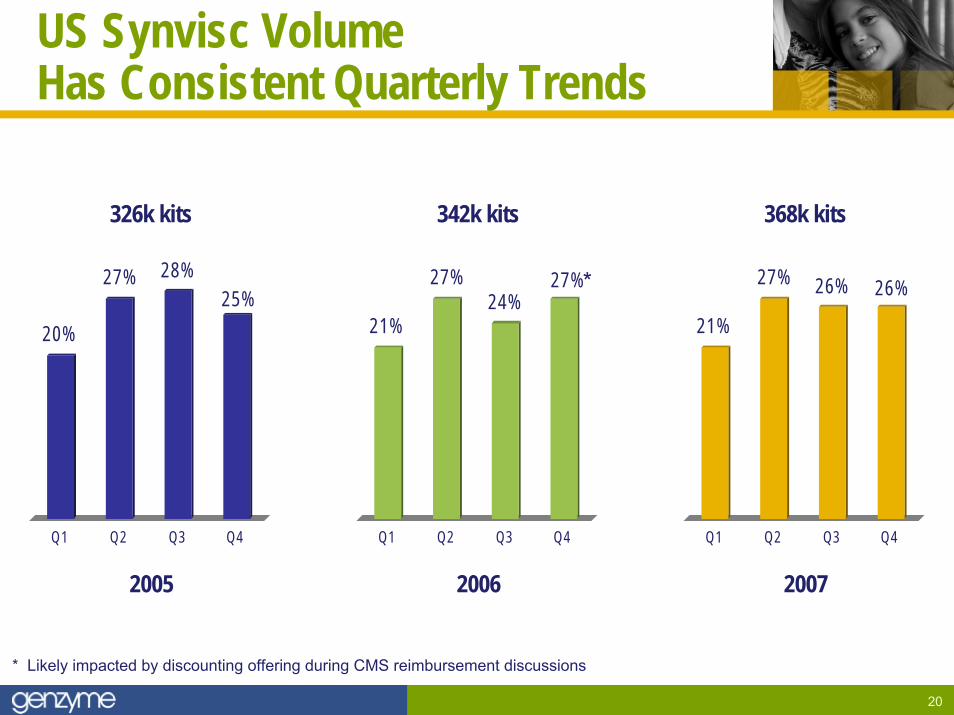

US Synvisc Volume Has Consistent Quarterly Trends

* Likely impacted by discounting offering during CMS reimbursement discussions

326k kits

20%

27% 28%25%

Q1 Q2 Q3 Q4

342k kits

21%

27%24%

27%

Q1 Q2 Q3 Q4

368k kits

21%

27% 26% 26%

Q1 Q2 Q3 Q4

20072005 2006

*

21

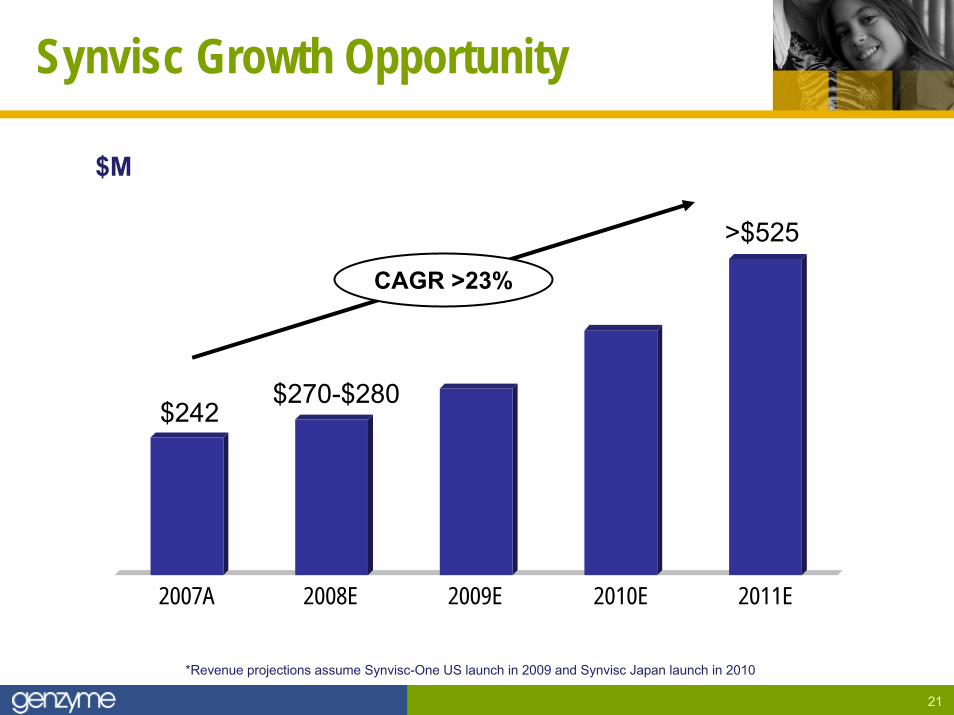

Synvisc Growth Opportunity

2007A 2008E 2009E 2010E 2011E

$242$270-$280

>$525

CAGR >23%

*Revenue projections assume Synvisc-One US launch in 2009 and Synvisc Japan launch in 2010

$M

22

Agenda

► Sepra family

► Synvisc and Synvisc-One

► Growth opportunities beyond 2011

23

Growth Drivers Beyond 2011

► Synvisc-One and Sepraspray

► Expanding Synvisc US label to other joint(s)

► OA combination products (drugs)– Gen-S for enhanced OA pain relief

(into clinic H1 ’09)– Further opportunities: pain and structure

► New adhesion prevention indications (ortho, spine, cardiac)

► MACI EU, US, China

► Business development

Growth

24

S U M M A R Y:

Strong Foundation for Growth

Sepra ► Procedure diversification

for film

► Sepraspray for laparoscopic

► Ex-US opportunities

► New indications beyond 2011

Synvisc / Synvisc-One► Expanding patient types

and repeat usage

► Synvisc-One

► Synvisc Japan

► Combination products beyond 2011

Growth Drivers

+

Alemtuzumab in MS: A Promising New Standard of CareTerry L. Murdock, Sr. Vice President

May 7, 2008 Analyst Day

26

Agenda

► Phase 2 data

► Phase 3 program

► Market research

27

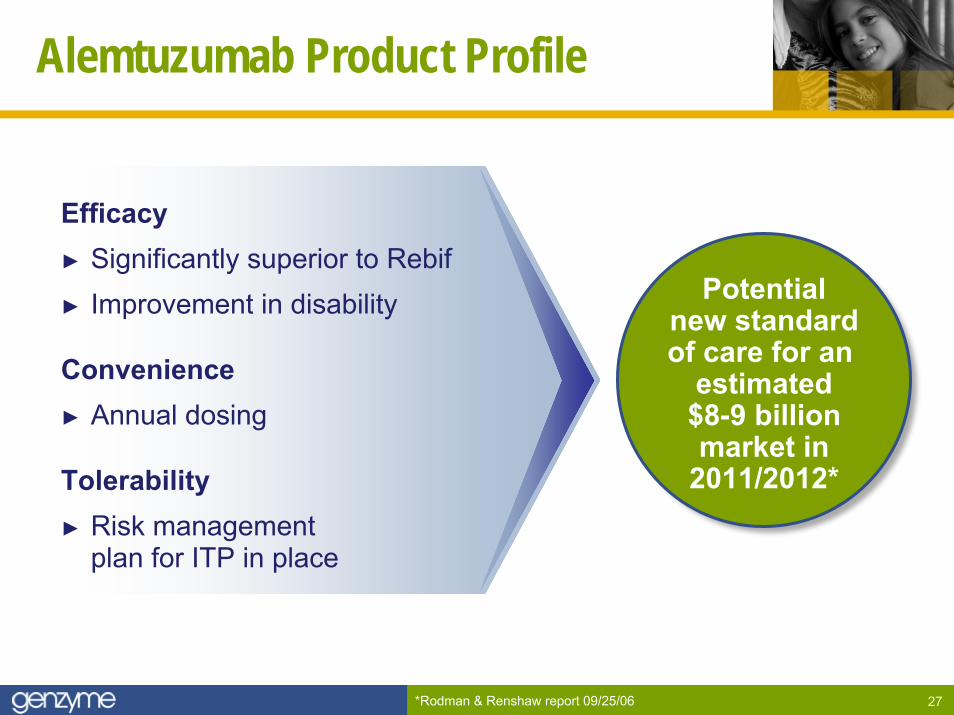

Alemtuzumab Product Profile

Potentialnew standardof care for an

estimated$8-9 billionmarket in

2011/2012*

Efficacy► Significantly superior to Rebif► Improvement in disability

Convenience► Annual dosing

Tolerability► Risk management

plan for ITP in place

*Rodman & Renshaw report 09/25/06

28

CAMMS223:Cumulative Number of Relapses

Annualized Relapse Rate (95% C.I.)

Interferon-beta 1a0.37 (0.29, 0.47)

Alemtuzumab 12 mg/day

0.10 (0.07, 0.16)

Alemtuzumab 24 mg/day

0.05 (0.03, 0.09)

AlemtuzumabPooled

0.08 (0.05, 0.11)

333 314 303 288 277No. Ptsat Risk

P < 0.0001

RiskReduction

81%

29

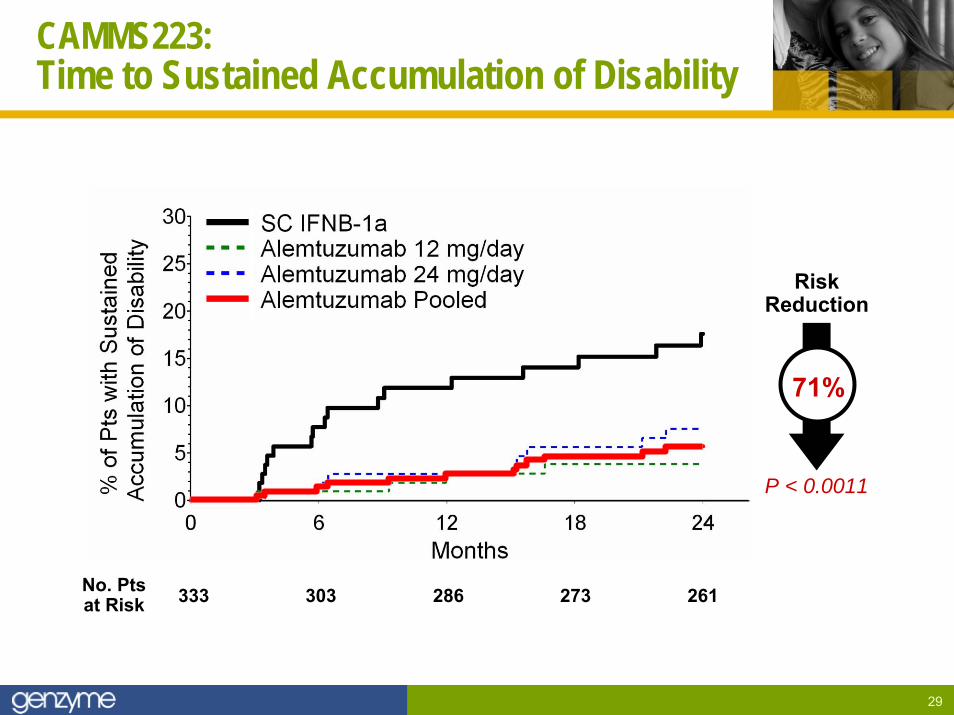

CAMMS223:Time to Sustained Accumulation of Disability

333 303 286 273 261No. Ptsat Risk

P < 0.0011

RiskReduction

71%

30

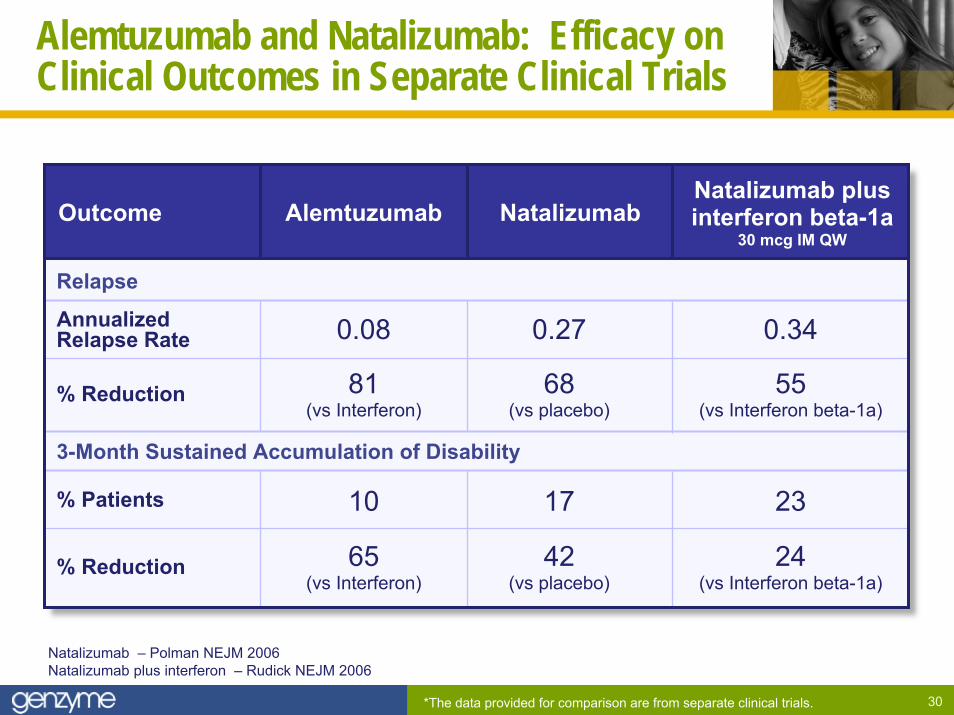

Alemtuzumab and Natalizumab: Efficacy onClinical Outcomes in Separate Clinical Trials

AlemtuzumabOutcome NatalizumabNatalizumab plusinterferon beta-1a

30 mcg IM QW

3-Month Sustained Accumulation of Disability

Relapse

% Reduction

% Patients

% Reduction

AnnualizedRelapse Rate

24(vs Interferon beta-1a)

42(vs placebo)

65(vs Interferon)

231710

55(vs Interferon beta-1a)

68(vs placebo)

81(vs Interferon)

0.340.270.08

Natalizumab – Polman NEJM 2006Natalizumab plus interferon – Rudick NEJM 2006

*The data provided for comparison are from separate clinical trials.

31

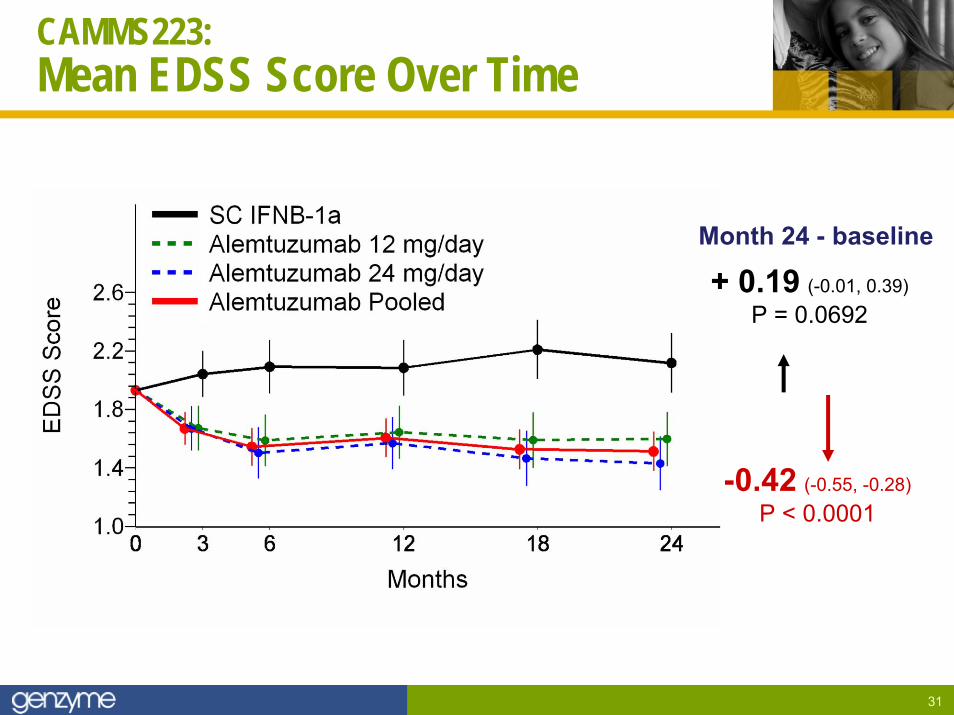

CAMMS223: Mean EDSS Score Over Time

+ 0.19 (-0.01, 0.39)P = 0.0692

Month 24 - baseline

-0.42 (-0.55, -0.28)P < 0.0001

32

Strong 3-Year Results

► Three-year results presented at AAN 2008 confirm and extend conclusions from the interim analyses at 1- and 2-years:

– Markedly reduced the risk of relapse versus IFNB-1a (statistically significant)– Markedly reduced the risk for SAD versus IFNB-1a (statistically significant)

► Significant improvements observed on MRI– Markedly reduced T2 lesion load (statistically significant)– Increase in brain volume v. atrophy with INFB-1a (statistically significant)

► No new cases of ITP since September of 2006

33

Agenda

► Phase 2 data

► Phase 3 program

► Market research

34

Phase 3 Program

Comparison of Alemtuzumab and Rebif Efficacy in Multiple Sclerosis

35

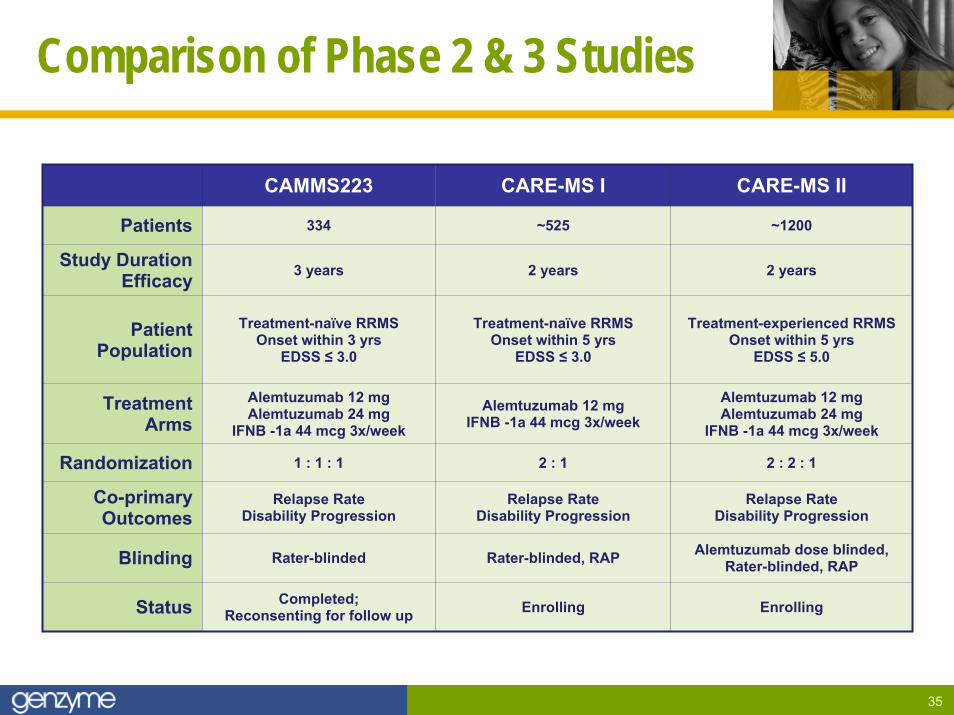

Comparison of Phase 2 & 3 Studies

CAMMS223 CARE-MS I CARE-MS II

Patients 334 ~525 ~1200

2 years 2 years

Treatment-naïve RRMSOnset within 5 yrs

EDSS ≤ 3.0

Treatment-experienced RRMSOnset within 5 yrs

EDSS ≤ 5.0

Alemtuzumab 12 mgIFNB -1a 44 mcg 3x/week

Alemtuzumab 12 mgAlemtuzumab 24 mg

IFNB -1a 44 mcg 3x/week

Randomization 1 : 1 : 1 2 : 1 2 : 2 : 1

Blinding Rater-blinded Rater-blinded, RAP Alemtuzumab dose blinded,Rater-blinded, RAP

Relapse RateDisability Progression

Relapse RateDisability Progression

Enrolling Enrolling

Study Duration Efficacy 3 years

Patient Population

Treatment-naïve RRMSOnset within 3 yrs

EDSS ≤ 3.0

TreatmentArms

Alemtuzumab 12 mgAlemtuzumab 24 mg

IFNB -1a 44 mcg 3x/week

Co-primary Outcomes

Relapse RateDisability Progression

Status Completed;Reconsenting for follow up

36

Safety Monitoring Plan

► Hematologic monitoring– Monthly (or more frequent) complete blood counts (CBCs) with platelets– Monthly phone calls from sites to patients

• Offset from CBCs by 2 weeks– At least 3 years of follow-up after last alemtuzumab treatment

► Patient and physician education about ITP

► Monitoring for thyroid disorders

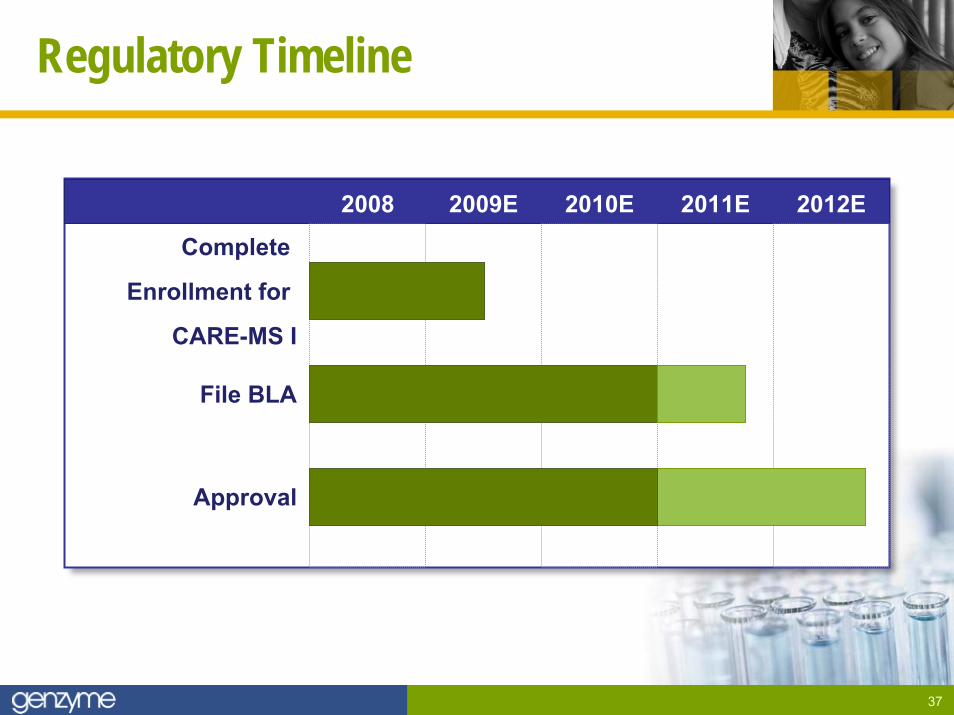

37

Regulatory Timeline

2008 2009E 2010E 2011E 2012E

Complete

Enrollment for

CARE-MS I

File BLA

Approval

38

Agenda

► Phase 2 data

► Phase 3 program

► Market research

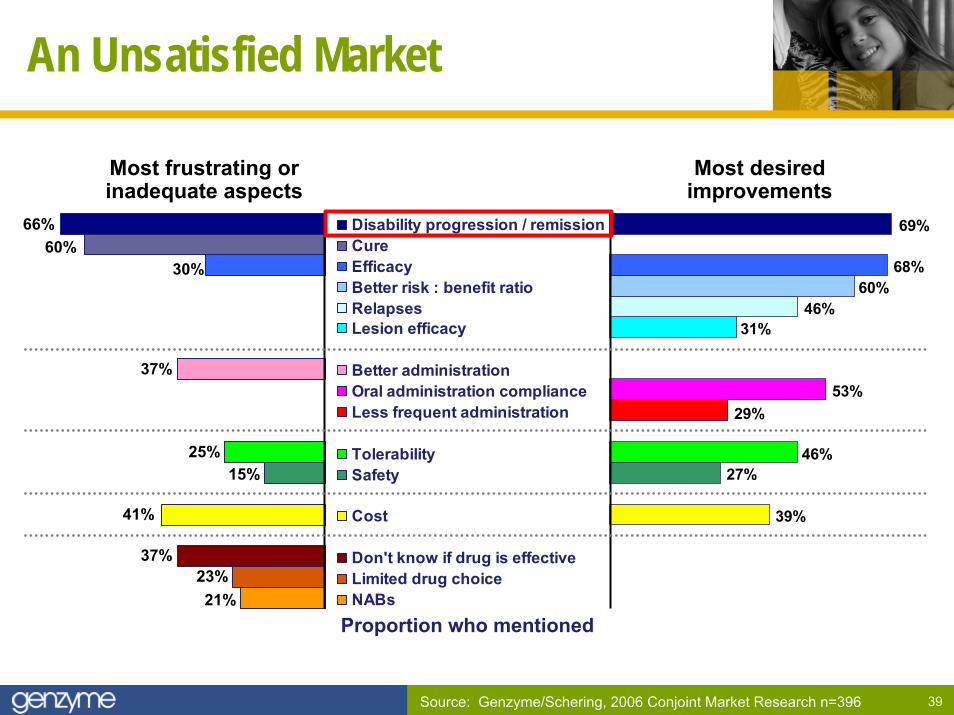

39

An Unsatisfied Market

Most frustrating orinadequate aspects

Most desiredimprovements

Source: Genzyme/Schering, 2006 Conjoint Market Research n=396

Disability progression / remissionCureEfficacyBetter risk : benefit ratioRelapsesLesion efficacyBar 13Better administrationOral administration complianceLess frequent administrationBar 9TolerabilitySafetyBar 6CostBar 4Don't know if drug is effectiveLimited drug choiceNABs

39%

27%46%

29%53%

31%46%

60%68%

69%66%60%

30%

37%

25%15%

41%

37%23%21%

Proportion who mentioned

40

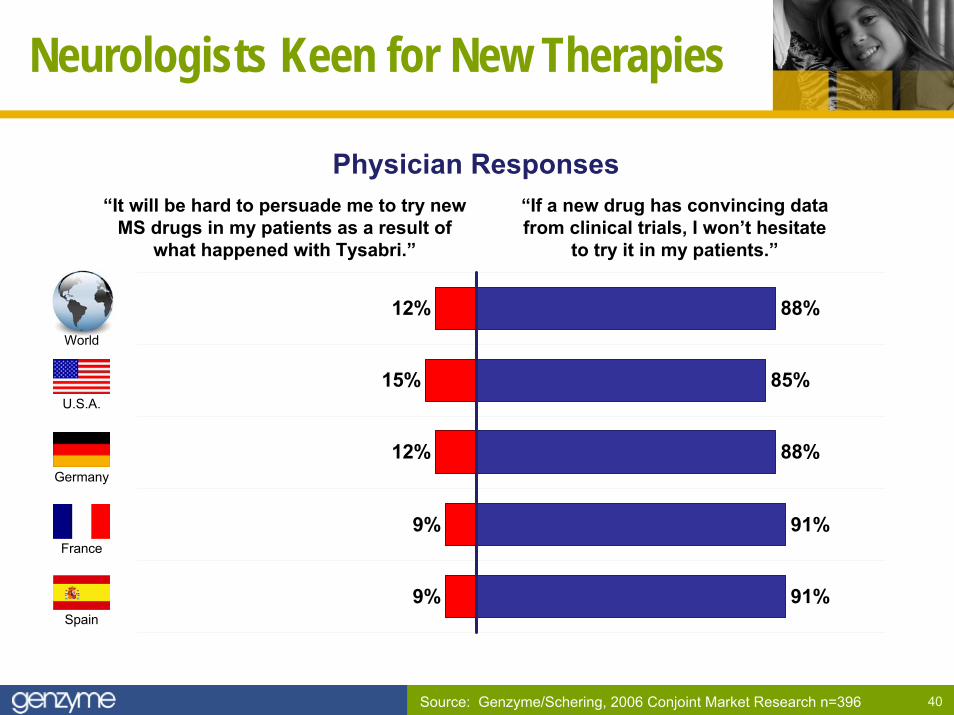

Neurologists Keen for New Therapies

91%

91%

88%

85%

88%

9%

9%

12%

15%

12%

“If a new drug has convincing data from clinical trials, I won’t hesitate

to try it in my patients.”

“It will be hard to persuade me to try new MS drugs in my patients as a result of

what happened with Tysabri.”

Physician Responses

Source: Genzyme/Schering, 2006 Conjoint Market Research n=396

World

U.S.A.

Germany

France

Spain

41

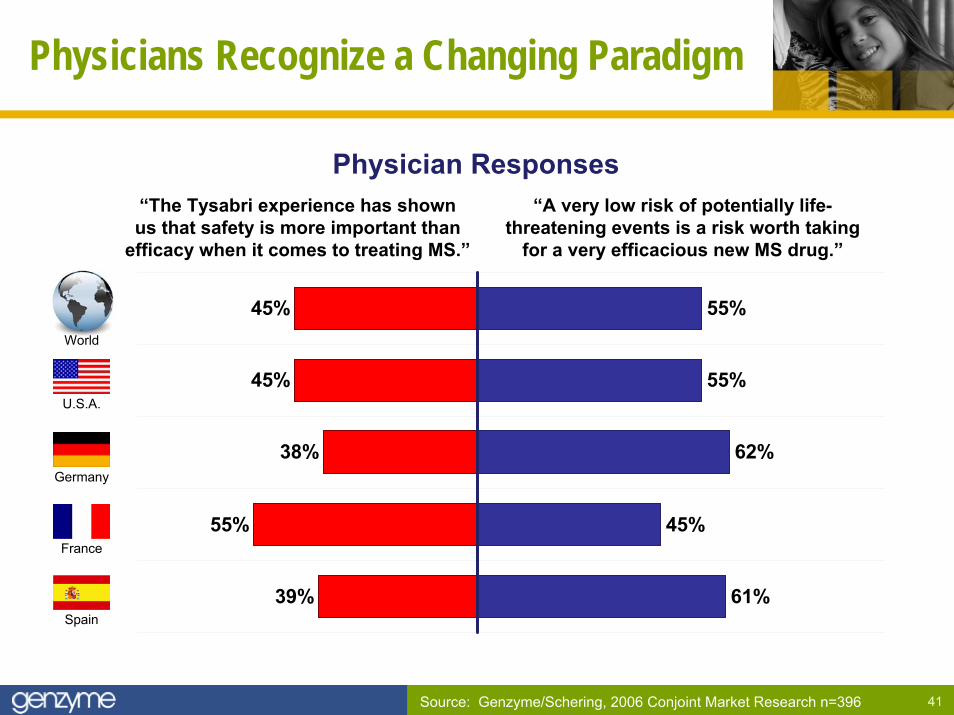

Physicians Recognize a Changing Paradigm

61%

45%

62%

55%

55%

39%

55%

38%

45%

45%

“A very low risk of potentially life-threatening events is a risk worth taking

for a very efficacious new MS drug.”

“The Tysabri experience has shownus that safety is more important than

efficacy when it comes to treating MS.”

Physician Responses

Source: Genzyme/Schering, 2006 Conjoint Market Research n=396

World

U.S.A.

Germany

France

Spain

42

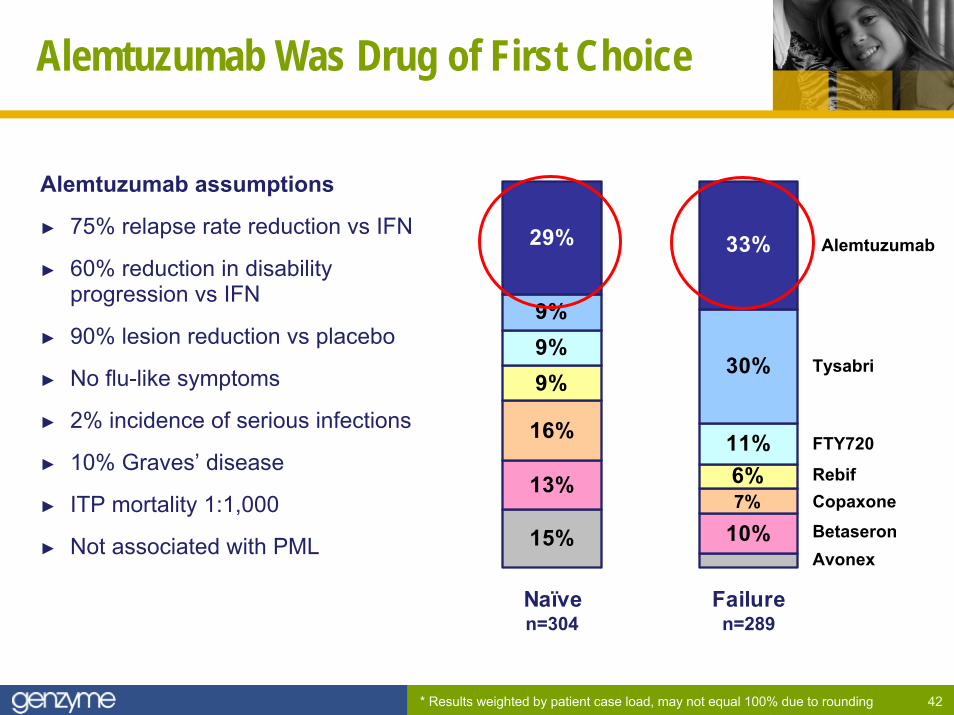

Alemtuzumab Was Drug of First Choice

Alemtuzumab assumptions

► 75% relapse rate reduction vs IFN

► 60% reduction in disability progression vs IFN

► 90% lesion reduction vs placebo

► No flu-like symptoms

► 2% incidence of serious infections

► 10% Graves’ disease

► ITP mortality 1:1,000

► Not associated with PML

* Results weighted by patient case load, may not equal 100% due to rounding

n=289n=304

13%

10%

16%

9%

6%

9%

11%

30%

29% 33%

15%7%

9%

Naïve Failure

Alemtuzumab

Tysabri

FTY720

RebifCopaxoneBetaseronAvonex

43

Research Confirmed and Extended

► 20 in-depth interviews with community-based neurologists

► Board certified in neurology

► See at least 30 MS patients monthly

► Physicians provided alemtuzumab interim Phase 2 data and Phase 3 MS trial designs to review prior to the interview

44

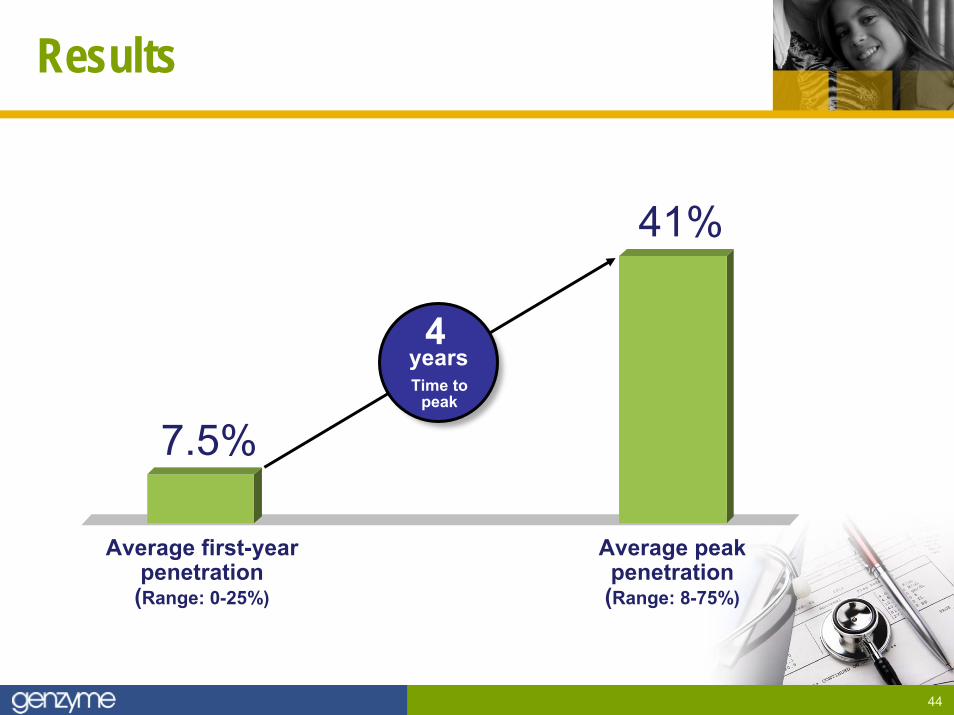

Results

Average first-yearpenetration(Range: 0-25%)

Average peakpenetration(Range: 8-75%)

7.5%

41%

4yearsTime to

peak

45

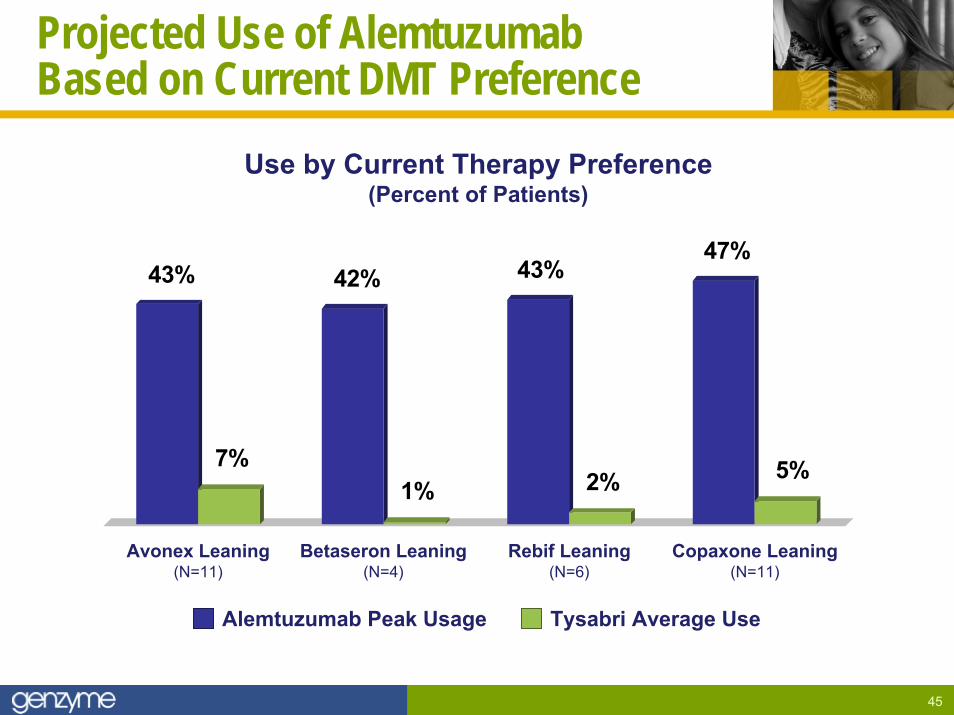

Projected Use of Alemtuzumab Based on Current DMT Preference

Use by Current Therapy Preference(Percent of Patients)

43%

7%

42%

1%

43%

2%

47%

5%

Avonex Leaning(N=11)

Betaseron Leaning(N=4)

Rebif Leaning(N=6)

Copaxone Leaning(N=11)

Alemtuzumab Peak Usage Tysabri Average Use

46

S U M M A R Y:

A Promising New Standard of Care

► Significant efficacy and manageable safety profile in comparison to Rebif

► Pivotal trials are on-track for BLA filing in 2011E

► Potential revenue beginning in 2011/2012

Mipomersen: An Attractive New OpportunityJames A. Geraghty, Senior Vice President

May 7, 2008 Analyst Day

48

Agenda

► Hypercholesterolemia: unmet needs

► Introduction to Mipomersen

► Responses to investor questions

Cholesterol

49

Profile of Homozygous FH Patients (HoFH)

► Extremely high LDL levels

► Unable to be controlled on optimal current therapy

► Coronary events common in childhood/adolescence

► Regular apheresis recommended

The need for a new therapy is clear

50

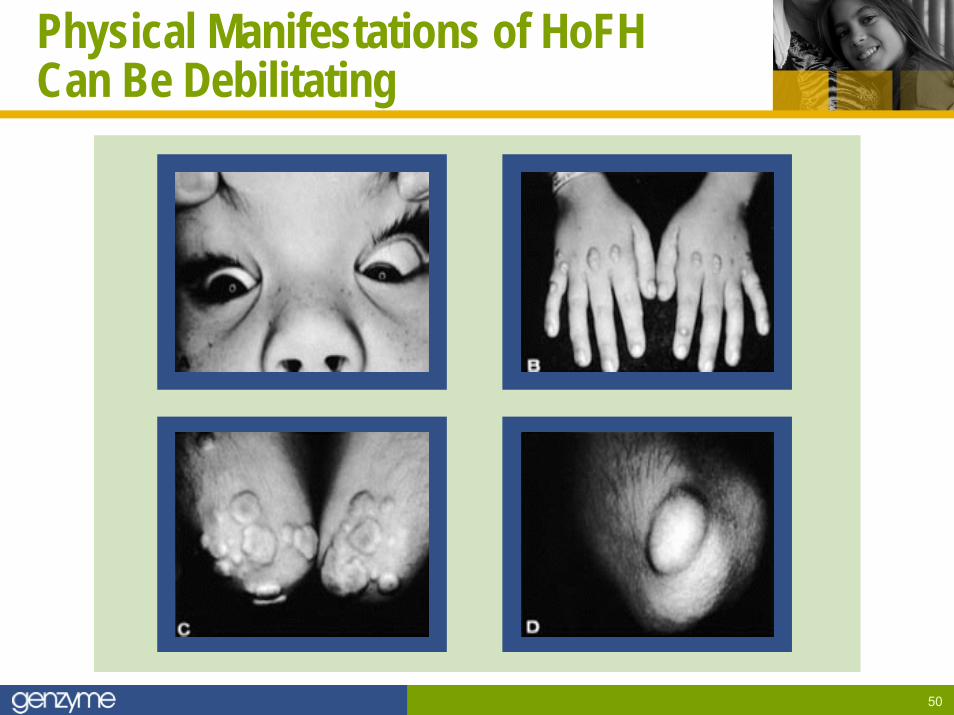

Physical Manifestations of HoFHCan Be Debilitating

51

Other High-Risk Patients:Achieving LDL Goals is Key to Avoiding Events

► High risk patients have >20% 10 year CVD risk

► Some are highly statinintolerant/resistant

► Highest risk groups have up to 30% >5 year CVD risk

Many cannot get to goal on optimal current therapy

52

Agenda

► Hypercholesterolemia: unmet needs

► Introduction to Mipomersen

► Responses to investor questions

Cholesterol

53

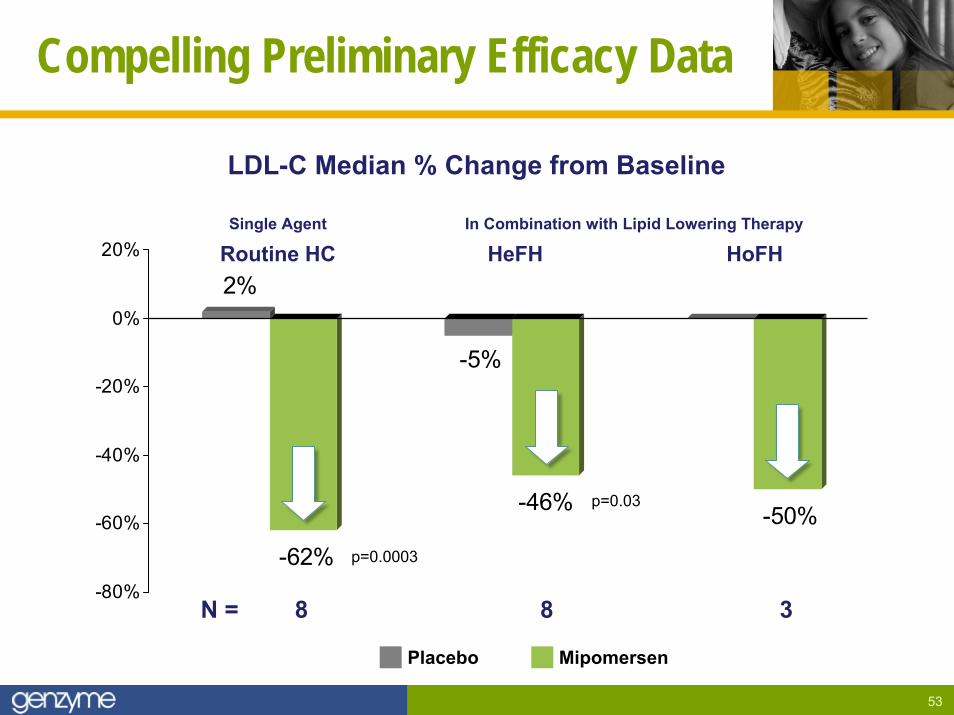

Compelling Preliminary Efficacy Data

LDL-C Median % Change from Baseline

2%

-62%

-5%

-46% -50%

-80%

-60%

-40%

-20%

0%

20%

p=0.0003

p=0.03

N = 8 8 3

Single Agent

Routine HCIn Combination with Lipid Lowering Therapy

HeFH HoFH

Placebo Mipomersen

54

Limited Adverse Events Reported

► Injection site reaction– Most frequently reported adverse event– Reported painless, spontaneously resolve– No worsening with long-term dosing

► Hepatic effects– ALT elevations: consistent with pharmacologic effects– Tend to decrease with continued dosing– No elevated bilirubin or Hy’s Law cases

Ensuring safety will be our highest concern

55

Clinicians Very Positive on Mipomersen

► Novel, first-in-class product

► Every physician interviewed was very excited about the product

► Lipid specialists see clear need in high risk populations

► All see value in FH and high risk patients not at goal

► Potential benefit for apheresis eligible patients extremely high

Positivephysicianresponse

56

Agenda

► Hypercholesterolemia: unmet needs

► Introduction to Mipomersen

► Responses to investor questions

Cholesterol

57

Investor Questions

1. How do you define each patient population?

2. What are the development plans for the HoFH population?

3. What are the plans for the apheresis eligible population?

4. What would be the design of the clinical outcome study?

5. What is the timing for the expected filings?

58

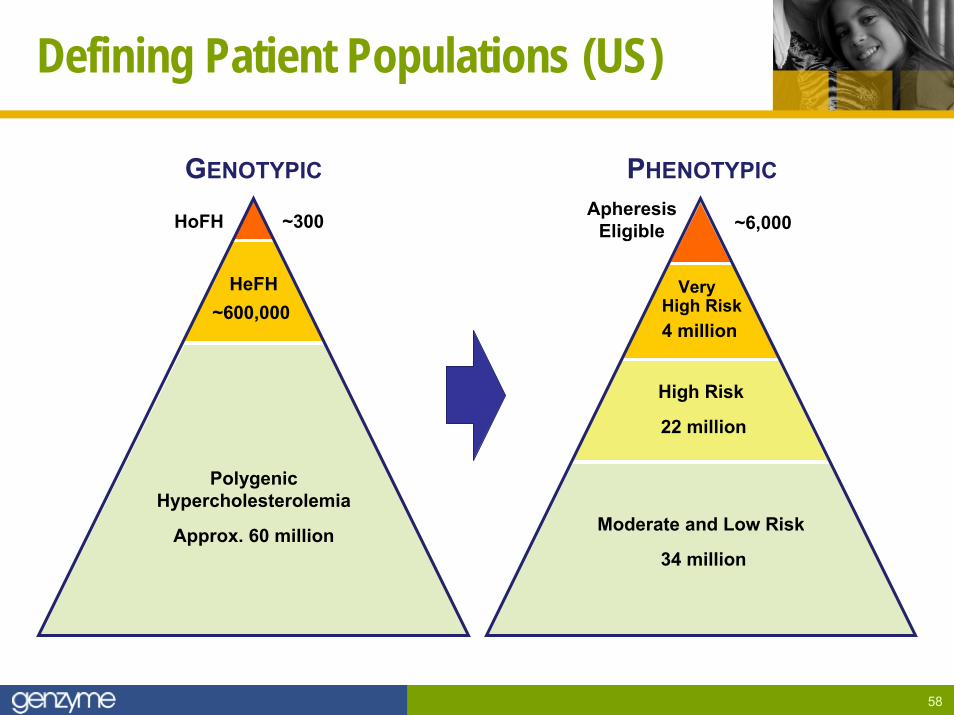

Defining Patient Populations (US)

HoFH

PolygenicHypercholesterolemia

Approx. 60 million

HeFH~600,000

GENOTYPIC

~300 ApheresisEligible

High Risk

22 million

Moderate and Low Risk

34 million

Very High Risk4 million

PHENOTYPIC

~6,000

59

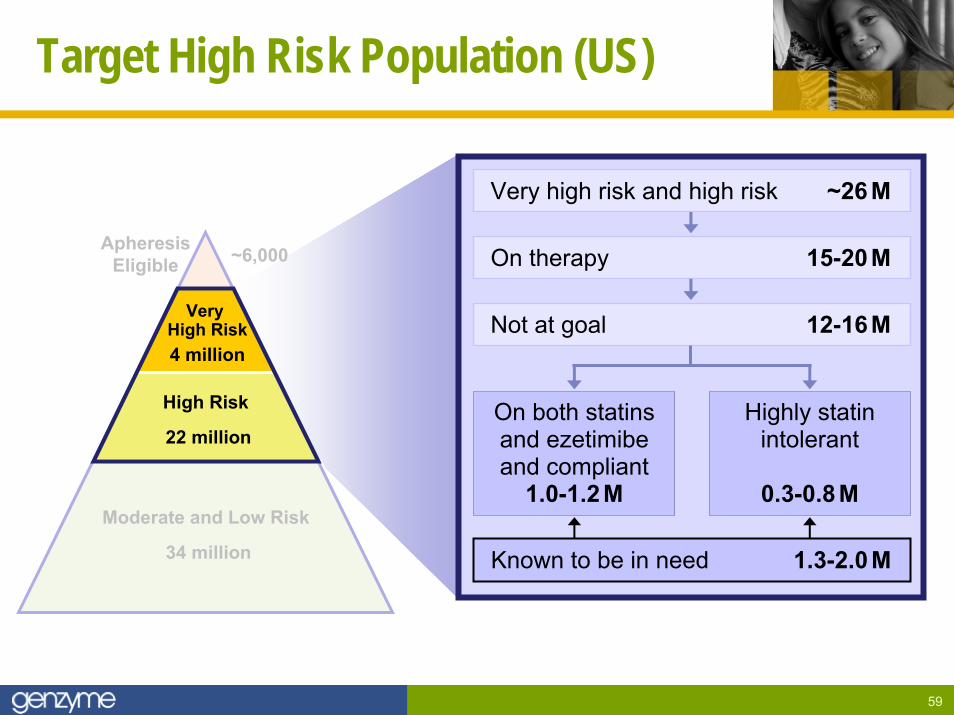

Target High Risk Population (US)

ApheresisEligible

High Risk

22 million

Moderate and Low Risk

34 million

Very High Risk4 million

~6,000

On both statinsand ezetimibeand compliant

1.0-1.2M

Highly statinintolerant

0.3-0.8M

Very high risk and high risk ~26 M

On therapy 15-20M

Known to be in need 1.3-2.0M

Not at goal 12-16M

60

Investor Questions

1. How do you define each patient population?

2. What are the development plans for the HoFH population?

3. What are the plans for the apheresis eligible population?

4. What would be the design of the clinical outcome study?

5. What is the timing for the expected filings?

61

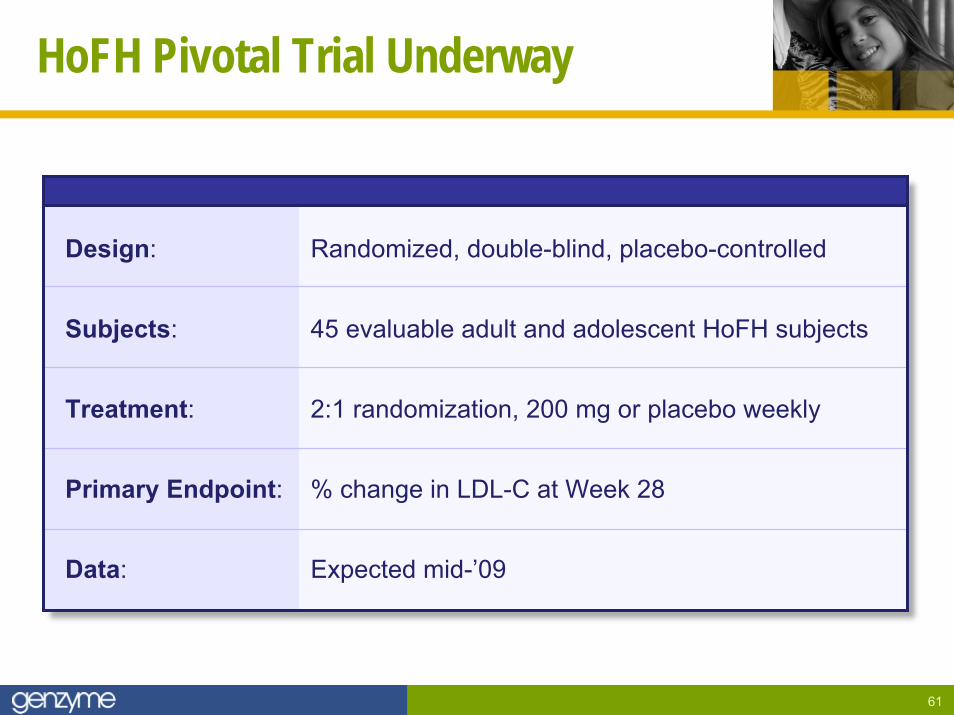

HoFH Pivotal Trial Underway

Design: Randomized, double-blind, placebo-controlled

Subjects: 45 evaluable adult and adolescent HoFH subjects

Treatment: 2:1 randomization, 200 mg or placebo weekly

Primary Endpoint: % change in LDL-C at Week 28

Data: Expected mid-’09

62

Investor Questions

1. How do you define each patient population?

2. What are the development plans for the HoFH population?

3. What are the plans for the apheresis eligible population?

4. What would be the design of the clinical outcome study?

5. What is the timing for the expected filings?

63

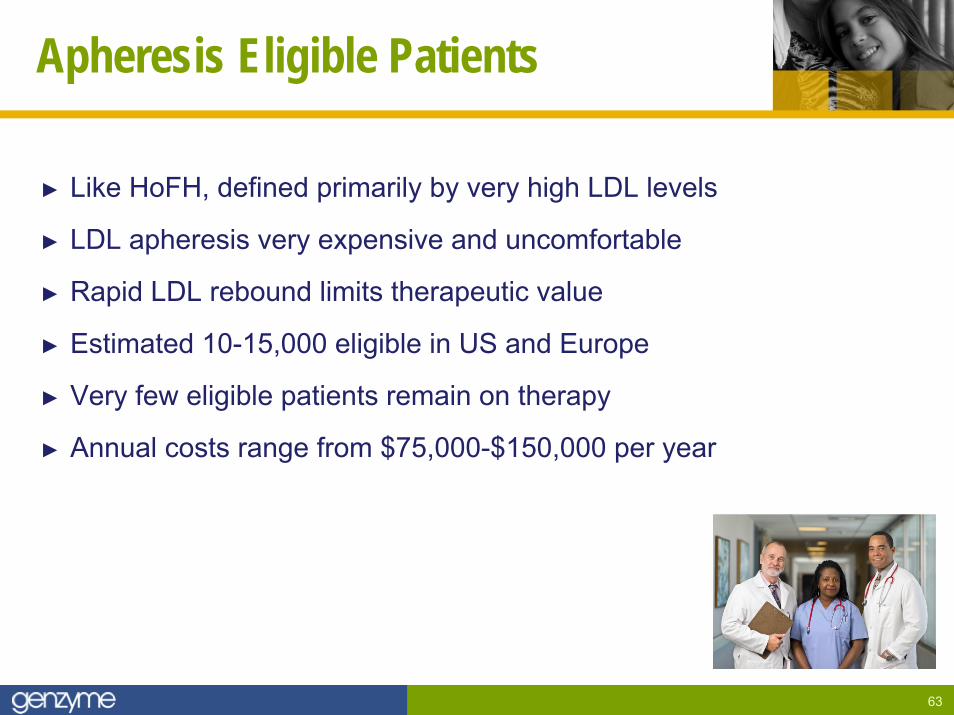

Apheresis Eligible Patients

► Like HoFH, defined primarily by very high LDL levels

► LDL apheresis very expensive and uncomfortable

► Rapid LDL rebound limits therapeutic value

► Estimated 10-15,000 eligible in US and Europe

► Very few eligible patients remain on therapy

► Annual costs range from $75,000-$150,000 per year

64

Preliminary Apheresis Trial Plans

► Eligible patients not currently on apheresis

► All patients kept on optimal current therapy

► Randomized 2:1 mipomersen to placebo

► Approximately 60 patients with 6 months of treatment

► Goal is to have data at time of the HoFH filing

65

Investor Questions

1. How do you define each patient population?

2. What are the development plans for the HoFH population?

3. What are the plans for the apheresis eligible population?

4. What would be the design of the clinical outcome study?

5. What is the timing for the expected filings?

66

Emerging Clinical Outcome Study Plans

► Goal is to start and finish as soon as possible

► Focus on highest risk, highest event rate groups

► Includes patients with CVD, diabetes, very high LDL levels

► Assumptions being drawn from many prior large LDL reduction studies

► Working target is to begin enrollment in H1:09E

► Details to be finalized in coming months

67

Investor Questions

1. How do you define each patient population?

2. What are the development plans for the HoFH population?

3. What are the plans for the apheresis eligible population?

4. What would be the design of the clinical outcome study?

5. What is the timing for the expected filings?

68

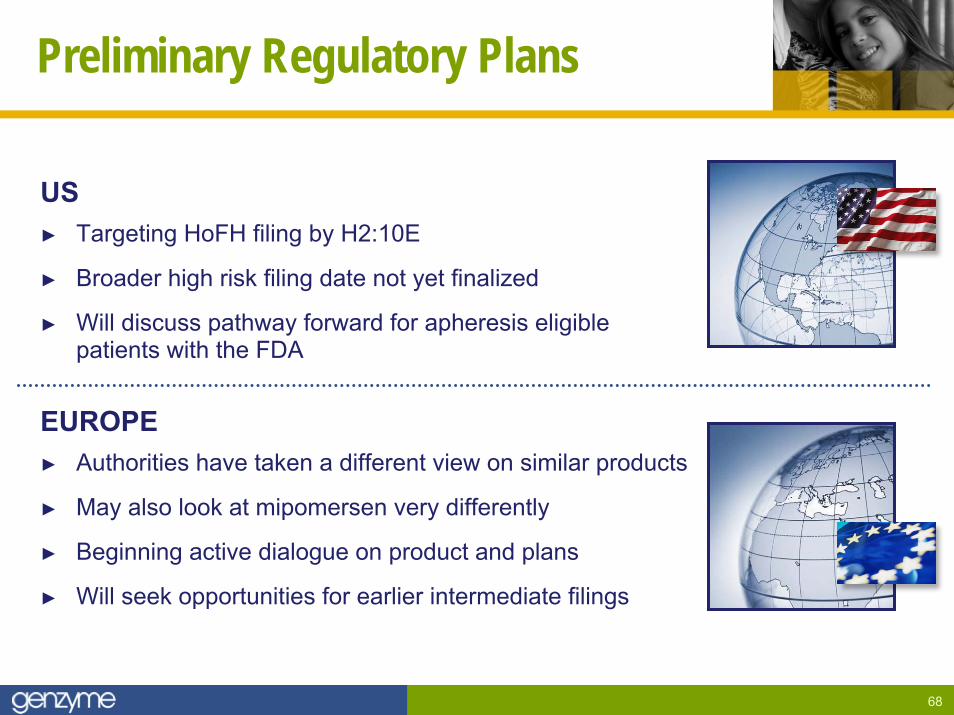

Preliminary Regulatory Plans

US► Targeting HoFH filing by H2:10E

► Broader high risk filing date not yet finalized

► Will discuss pathway forward for apheresis eligible patients with the FDA

EUROPE► Authorities have taken a different view on similar products

► May also look at mipomersen very differently

► Beginning active dialogue on product and plans

► Will seek opportunities for earlier intermediate filings

69

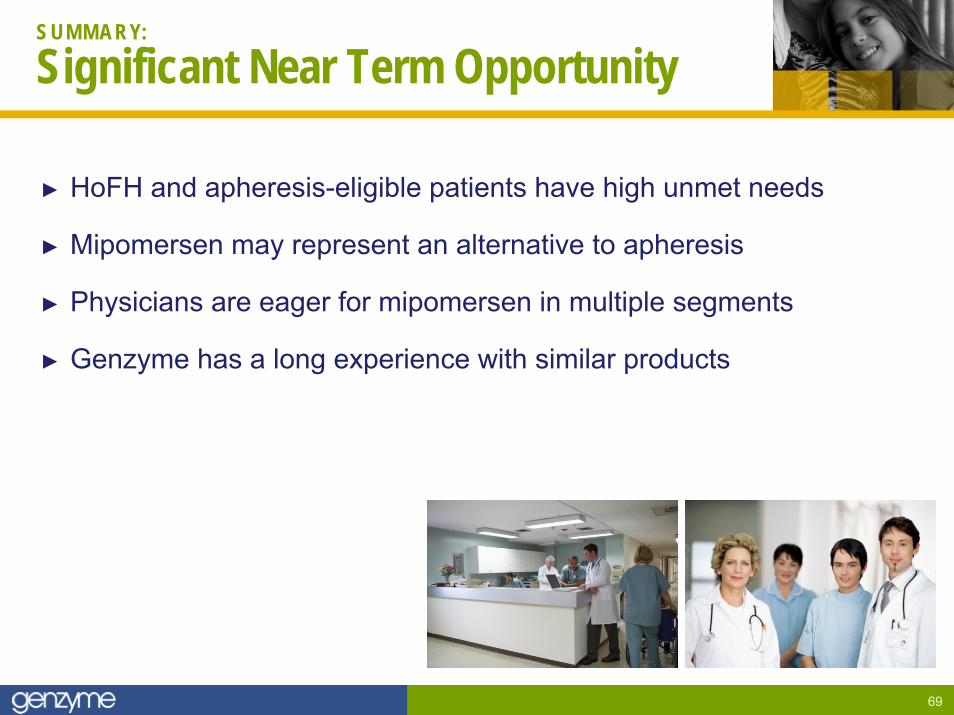

S U M M A R Y:

Significant Near Term Opportunity

► HoFH and apheresis-eligible patients have high unmet needs

► Mipomersen may represent an alternative to apheresis

► Physicians are eager for mipomersen in multiple segments

► Genzyme has a long experience with similar products

70

Question and Answer

Moderator:

► Duke Collier, Esquire, Executive Vice President

Panel:

► Joe Lobacki, Sr. Vice President and General Manager, Transplant

► Terry Murdock, Sr. Vice President and General Manger, Campath

► Jim Geraghty, Sr. Vice President

► Michael Wyzga, Executive Vice President, Chief Financial and Accounting Officer

Concluding Comments

Henri Termeer, Chairman, CEO, President

May 7, 2008 Analyst Day

72

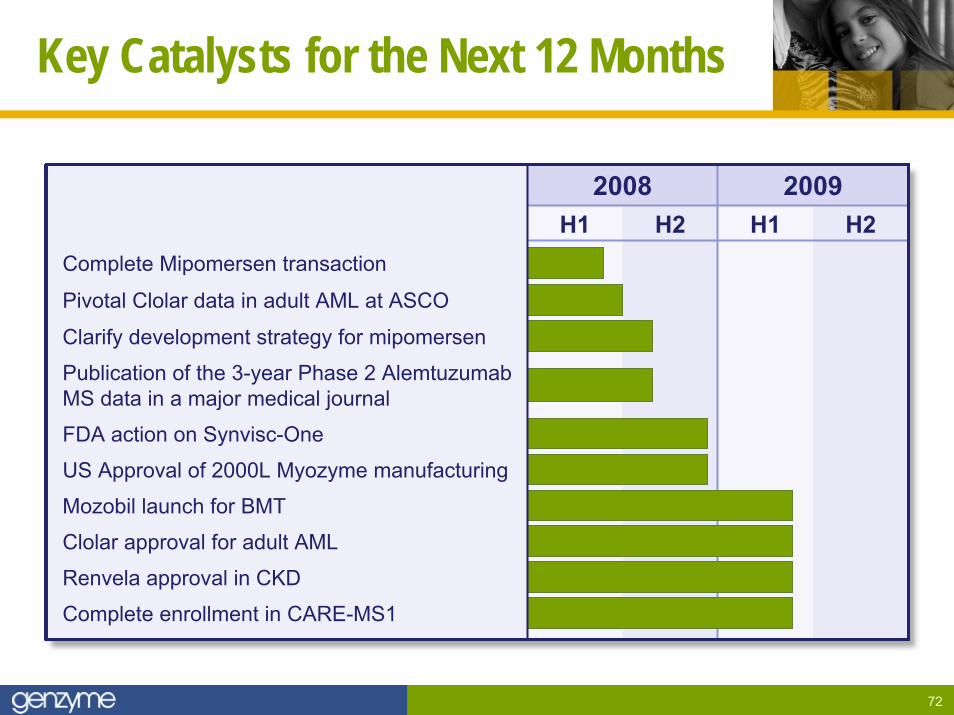

Key Catalysts for the Next 12 Months

H1 H2 H1 H22008 2009

Complete Mipomersen transaction

Pivotal Clolar data in adult AML at ASCO

Clarify development strategy for mipomersen

Publication of the 3-year Phase 2 AlemtuzumabMS data in a major medical journal

FDA action on Synvisc-One

US Approval of 2000L Myozyme manufacturing

Mozobil launch for BMT

Clolar approval for adult AML

Renvela approval in CKD

Complete enrollment in CARE-MS1