Embed Size (px)

Citation preview

Binomial Option Pricing 1

Arbitrage Binomial trees are a no arbitrage model. S0 = $20 Call option strike = $21 Rf = 12% Stock price in 3 months will be either $22 or $18

Binomial Option Pricing 2

A Generalized Approach S0 = stock price at time 0 f0 = option price at time 0 u = size of up move d = size of down move Option can move up or down to S0u or down to S0d (u > 1; d < 1) Proportional increase: u – 1 Proportional decrease: 1 – d Payoff in an up move = fu Payoff in a down move = fd

Δ shares long in stock Short 1 option

Binomial Option Pricing 3

Previous Example: u = 1.1 d = 0.9 t = .25 = 3/12 Rf = 12% fu = $1 fd = $0

Binomial Option Pricing 4

Risk Neutral Valuation Risk neutral – Individuals are indifferent to risk, they require no compensation for risk, the only thing that matters is the expected return. In a risk neutral world, the return on all securities is the risk-free rate. What is the expected stock price at time T? Important option principle: It is valid to assume the world is risk neutral when valuing options. The option price in the “real world” is the same as the option price in a risk neutral world.

Binomial Option Pricing 5

Our example revisited So = $20 ST = $22 or $18 3 months step Rf = 12%

Binomial Option Pricing 6

Two Step Binomial Tree Call Option

S0 = $20 up or down 10% in each step Rf = 12% X = $21 step = 3 months u = 1.1 d = .9 T = .25 p = .6523

Binomial Option Pricing 7

European Put Option S0 = $50 up or down 20% in each step Expires in 2 years Rf = 5% X = $52 step = 1 year

Binomial Option Pricing 8

American Put Option – Notice that the inputs are the same S0 = $50 up or down 20% in each step Expires in 2 years Rf = 5% X = $52 step = 1 year u = 1.2 d = 0.8 Risk neutral probability = p =

. .. .

= .6282

Binomial Option Pricing 9

Delta

Binomial Option Pricing 10

u, d, Volatility and the “Real World” μ = Expected return of stock σ = Standard deviation of stock return p* = Probability of an up move in the real world p* =

∆ u = √∆ d = √∆ = 1/ u

Binomial Option Pricing 11

American Call

μ = 12% X = $50S0 = $55.00 Rf = 6%σ = 40%

Expires in 2 months, 1 month steps u = √∆ = e.40(1/12) = 1.1224 d = √∆ = 1/ u = 1/ 1.1224 = .8909

p* = ∆ =

. .. .

= .5146

Binomial Option Pricing 12

American Put E(R) = 12% S0 = $82 σ = 55% X = $80 Rf = 5% Expiration = 4 months Steps = 1 month

Binomial Option Pricing 13

Binomial Option Pricing 14

Known Dollar Dividend

Binomial Option Pricing 15

Known Dividend Alternate Procedure

Find and use S* → S* = S0 – (Dividend)e–Rt

European Put

E(R) = 12% S0 = $52.00 s = 40%

X = $50.00 Rf = 5% D = $2.06

D due in 3.5 months Expiration 4 months Steps 1 month

Binomial Option Pricing 16

Binomial Option Pricing 17

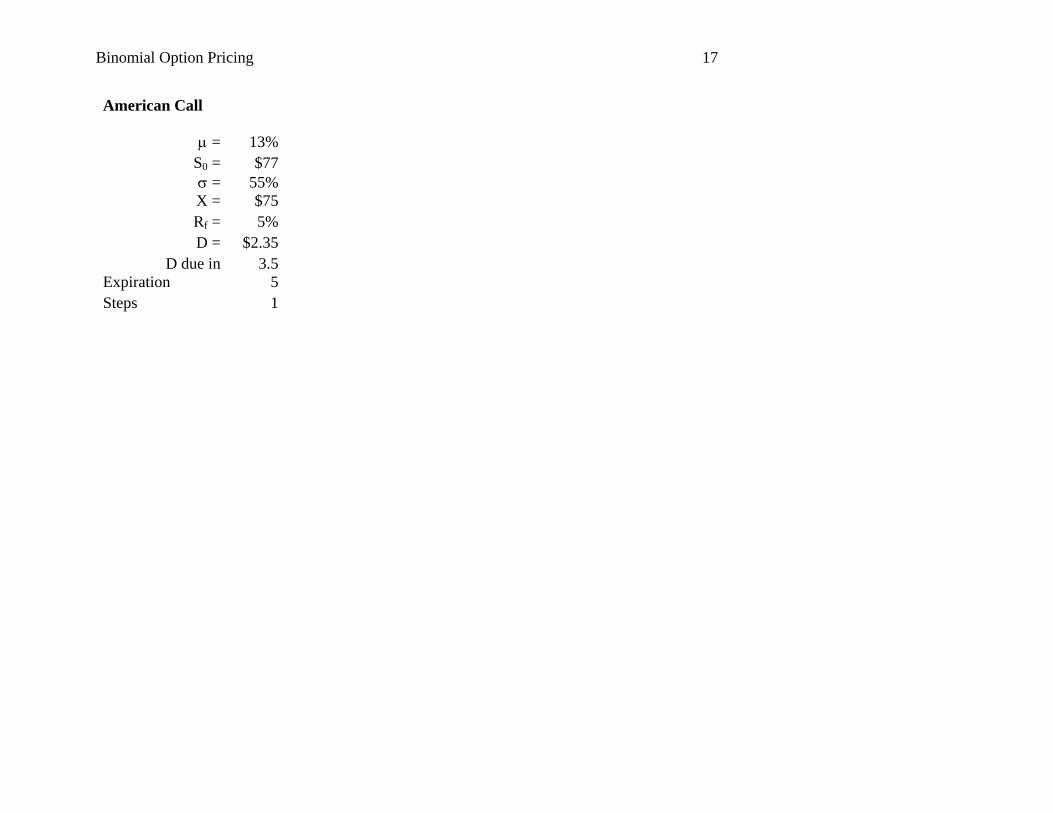

American Call

μ = 13% S0 = $77 σ = 55% X = $75 Rf = 5% D = $2.35

D due in 3.5 Expiration 5 Steps 1

Binomial Option Pricing 18

SP*= SK*u = 165.19 SP = SP*-PV(D) = 165.19

fP = 90.19 SK* = 140.94

SK = 140.94 fK = 67.20

SG* = 120.25 SQ* = 120.25 SG = 122.60 SQ = 120.25 fG = 47.60 fQ = 45.25

SD*= 102.60 SL* = 102.60 SD = 104.93 SL = 102.60 fD = 32.09 fL = 28.60

SB* 87.53 SH* = 87.53 SR* = 87.53 SB = 89.86 SH = 89.88 SR = 87.53 fB = 20.84 fH = 17.19 fR = 12.53

S0* 74.7 SE* = 74.68 SM* = 74.68 S0 = 77.00 SE = 77.02 SM = 74.68 fA = 13.12 fE = 10.00 fM = 6.17

SC* 63.72 SI* = 63.72 SS* = 63.72 SC = 66.05 SI = 66.06 SS = 63.72 fC = 5.68 fI = 3.04 fS = 0.00

SF* = 54.37 SN* 54.37 SF = 56.70 SN = 54.37 fF = 1.50 fN = 0.00

SJ* = 46.38 SV* = 46.38 SJ = 48.73 SV = 46.38 fJ = 0.00 fV = 0.00

SO* = 39.57 SO = 39.57 fO = 0.00

SW* = 33.76 SW = 33.76 fW = 0.00

Binomial Option Pricing 19

Known Dividend Yield (δ)

Binomial Option Pricing 20

Continuous Dividend Yield (δ)

p =

∆

u = √∆ d = √∆ = 1/ u

6-month European call on the S&P 500, 3 month steps X = 800 S = 810 Rf = 5% σ = 20% q = 2%

Binomial Option Pricing 21

Options on Futures In a risk neutral world, futures should have a growth rate of zero. So:

u = √∆ d = √∆ = 1/ u

p = 9 month American put, 3 month steps F0 = 31 X = 30 σ = 30% Rf = 5%

![A Skewness-Adjusted Binomial Model for Pricing …file.scirp.org/pdf/JMF20120100011_82298793.pdf · Black-Scholes (B-S) [2] model and the binomial option pricing model (BOPM) with](https://img.pdfslide.us/doc/110x75/5b6b45f97f8b9a422e8d3f09/a-skewness-adjusted-binomial-model-for-pricing-filescirporgpdfjmf20120100011.jpg)