Embed Size (px)

Citation preview

MANAGER:BIMB INVESTMENT MANAGEMENT BERHAD (276246-X)

BIMB DANA AL-MUNSIFANNUAL REPORT FOR THE YEAR ENDED

31 AUGUST 2017

LAPORAN TAHUNAN BAGI TAHUN BERAKHIR 31 OGOS 2017

2

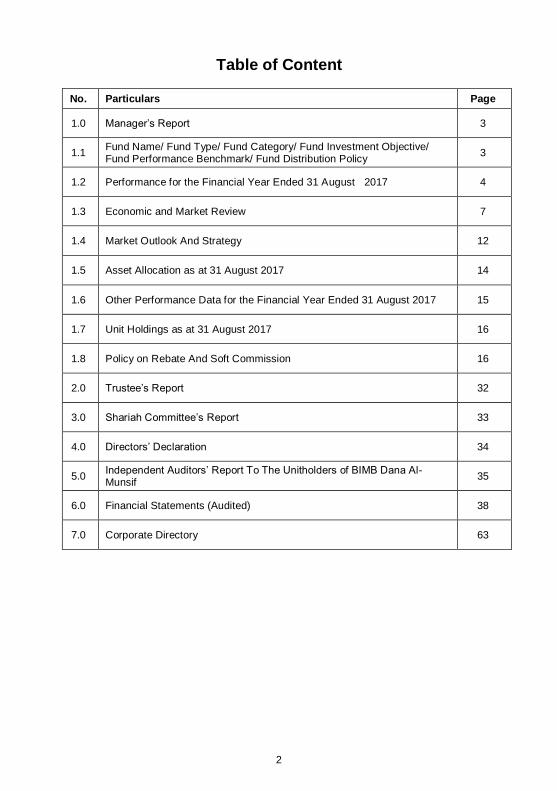

Table of Content

No. Particulars Page

1.0 Manager‟s Report 3

1.1 Fund Name/ Fund Type/ Fund Category/ Fund Investment Objective/ Fund Performance Benchmark/ Fund Distribution Policy

3

1.2 Performance for the Financial Year Ended 31 August 2017 4

1.3 Economic and Market Review 7

1.4 Market Outlook And Strategy 12

1.5 Asset Allocation as at 31 August 2017 14

1.6 Other Performance Data for the Financial Year Ended 31 August 2017 15

1.7 Unit Holdings as at 31 August 2017 16

1.8 Policy on Rebate And Soft Commission 16

2.0 Trustee‟s Report 32

3.0 Shariah Committee‟s Report 33

4.0 Directors‟ Declaration 34

5.0 Independent Auditors‟ Report To The Unitholders of BIMB Dana Al-Munsif

35

6.0 Financial Statements (Audited) 38

7.0 Corporate Directory 63

3

1.0 Manager’s Report

Dear Unit Holders,

We are pleased to present the Manager‟s report of BIMB Dana Al-Munsif for the

financial year ended 31 August 2017.

1.1 Fund Name/ Fund Type/ Fund Category/ Fund Investment Objective/ Fund

Performance Benchmark/ Fund Distribution Policy

Fund Name BIMB Dana Al-Munsif

Fund Type Income and growth

Fund Category Balanced

Fund Investment Objective

The principal investment objective of the Fund is to provide a steady and consistent income and capital appreciation of the units over the medium to long term period. Accordingly, returns shall be

in the form of long term capital growth and regular income distribution to the unit holders.

Note: Any material change to the investment objective of the Fund would require unit holders’ approval.

Fund Performance Benchmark

60:40 ratio of the FBM Emas Shariah Index and 12-month Term Deposit-i Tawarruq (TDT-i) rate of Bank Islam Malaysia Berhad

Fund Distribution

Policy

The Fund intends to pay out annual income distribution to Unit

Holders if sufficient investment income has been accumulated during the year.

Payment Mode for

Income Distribution

Payment into Unit Holders‟ bank account or reinvestment.

4

1.2 Performance for the financial year ended 31 August 2017

1.2.1 Performance review for BIMB Dana Al-Munsif

For the financial year under review, BIMB Dana Al-Munsif (Fund) registered a return of

12.42%, as compared to its benchmark‟s return of 2.92%.

From its commencement on 27 December 2001 to 31 August 2017, the Fund has

registered a total return of 108.76% as compared to its benchmark‟s return of

111.43%.

The selected performance benchmark for the Fund is based on 60:40 ratio of the FBM

Emas Shariah Index and 12-month Term Deposit-i Tawarruq (TDT-i) rate of Bank

Islam Malaysia Berhad.

The Fund‟s strategy has remained to focus on well-established companies that could

potentially pay sustainable dividends and have good prospects for earnings growth.

During its financial year ended 31 August 2017, the Fund was not able to acquire

adequate trading gains to declare income distribution for the year as a result of

unexpected volatility in the markets. Notwithstanding the above, the Manager has

improved the Fund‟s performance via cutting exposure on non-performing stocks and

reinvesting into companies and sectors that offer brighter prospects and potential

growth, resulting in better performance of its Net Asset Value (NAV).

As at 31 August 2017, the Fund has 58.75% exposure in equities, 22.4% in Islamic

debt securities and 18.85% in short term investments, cash and cash equivalents. In

terms of total NAV, the Fund size as at 31 August 2017 was at RM17.96 million, as

compared to RM31.31 million as at 31 August 2016. The NAV per unit of the Fund

has increased to RM0.4861 as at 31 August 2017 from RM0.4324 as at 31 August

2016.

Equity allocation of the Fund had been maintained at around 60% to capitalize more on

share price upside movement for the Fund. Moving forward, the Manager will resume

investing in companies with good earnings visibility, strong balance sheet, and high

dividend yield with good valuation prospects given the suitable opportunity arises.

For the financial year ended 31 August 2017, there were no significant changes to the

state of affairs of the Fund and no circumstances that materially affect the interest of

Unit Holders that have taken place up to the date of this Manager‟s Report.

5

1.2.2 Total return and average total return for the respective financial year ended 31

August 2017

BIMB Dana Al-Munsif Benchmark

Total

Return

(%)

Average

Total Return

(%)

Total

Return

(%)

Average

Total Return

(%)

1-Year Period 12.42 12.42 2.92 2.92

3-Year Period -2.23 -0.74 2.13 0.71

5-Year Period 6.39 1.28 14.74 2.95

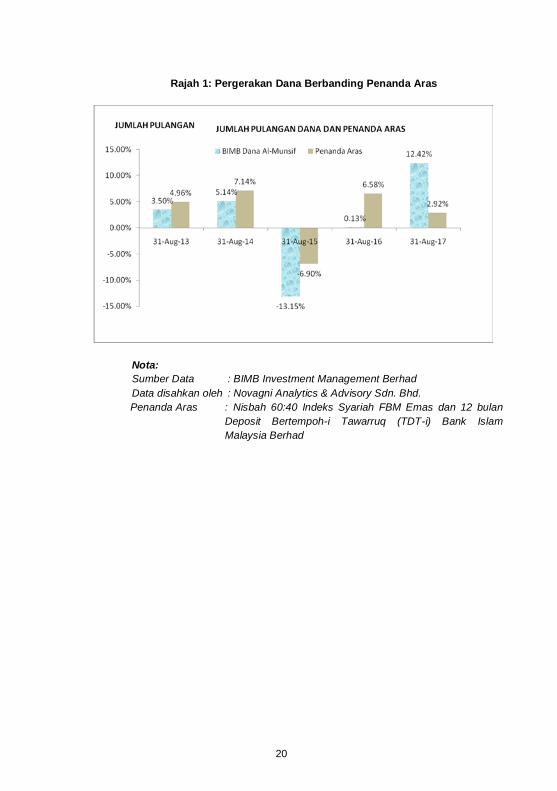

1.2.3 Total return for the last 5 financial years

Financial Years

Total Return

BIMB Dana Al-Munsif

(%)

Benchmark

(%)

31 August 2017 12.42 2.92

31 August 2016 0.13 6.58

31 August 2015 -13.15 -6.90

31 August 2014 5.14 7.14

31 August 2013 3.50 4.96

6

Figure 1: Movement of the Fund versus the Benchmark

Note:

Data Source : BIMB Investment Management Berhad

Data verified by :Novagni Analytics & Advisory Sdn. Bhd.

Benchmark :60:40 ratio of the FBM Emas Shariah Index and 12-

month Term Deposit-i Tawarruq (TDT-i) rate of Bank

Islam Malaysia Berhad.

7

1.3 Economic and Market Review

1.3.1 Economy

Global

The United States („US‟) Gross Domestic Product (GDP) grew at a rate of 2.6% in

the second quarter of 2017 as compared to 1.2% growth in the first quarter of 2017

and 1.8% in the fourth quarter of 2016. The acceleration in GDP for the second

quarter of 2017 was reflected in the upturns in federal government spending and

private inventory investment despite of deceleration in exports.

US headline inflation rate was up 1.9% in August 2017 compared to 1.5% in

September 2016 due to rising lodging and gasoline cost as Hurricane Harvey shut

down refineries in the Gulf coast.

US unemployment rate fell to 4.4% in August 2017 from 5.0% in September 2016 on

the back of rising income, consumer spending and economic growth.

The Euro zone economy grew 0.6% in the second quarter of 2017 as compared to

0.5% in the first quarter 2017 and 0.6% in the fourth quarter of 2016. The Euro zone

economic recovery has gained momentum while unemployment has fallen against a

backdrop of ultra-low interest rates which are among measures implemented by the

European Central Bank (ECB) to boost economic activity.

Euro zone‟s annual inflation increased to 1.5% in August 2017 from 0.4% in

September 2016, driven by better GDP growth in the Euro zone area.

The unemployment rate in the Euro zone area fell to 9.1 % in July 2017 compared to

10.0% in September 2016 that remained at its lowest level since July 2011.

The Chinese economy maintained a growth rate of 6.9% for the second quarter of

2017, maintaining comparable economic growth rate to the first quarter of 2017 as

industrial output and private consumption improved, aided by a robust property

market and recovery on the exports sector.

(Source: Bloomberg and RHB Research Institute Sdn Bhd)

Local

The Malaysian economy grew faster at 5.8% in the second quarter of 2017 as

compared to 5.6% in the first quarter 2017 and 4.5% in the fourth quarter 2016. The

stronger GDP result for the period was due to improvements in private consumption

and exports.

Malaysia‟s headline inflation in August 2017 increased to 3.7% from 1.5% in

September 2016 due to higher cost of food & non-alcoholic beverages, transportation

and housing, in tandem with higher oil prices and stronger GDP growth performance.

8

Bank Negara Malaysia‟s Monetary Policy Committee (MPC) maintained the

Overnight Policy Rate (OPR) at 3.00% during its July meeting to accommodate

growth prospects for the country.

Bank Negara‟s international reserve stood at USD 100.5 billion as at 30 August 2017

as compared to USD 97.7 billion in September 2016 with improvement of capital

inflow from foreign institutional investors into Malaysia.

(Source: Bloomberg, Bank Negara Malaysia and RHB Research Institute Sdn Bhd)

1.3.2 Market Review

Equity

FTSE Bursa Malaysia EMAS Shariah Index (“FBM Shariah”) commenced the year

under review at 12,430.50 points before it declined to the lowest point of 11,845.46 on

30 November 2016. Subsequently, the FBM Shariah gained and peaked at the highest

point of 13,126.04 on 16 May 2017 before ending the financial year at 12,749.09

points on 30 August 2017. For the year under review, the FBM Shariah gained 318.59

points or 2.56% whereas the FBM KLCI gained 65.32 points or 4.05% respectively.

Among the key factors that contributed to the movement of the index are highlighted

below:

The US Federal Reserve declined to raise interest rates in September 2016 ahead of

the US presidential election in November 2016 and reckoned that the US economy

still have room to improve before it run the risk of overheating.

Malaysia‟s Prime Minister unveiled the country‟s budget for 2017 on 21 October 2016

with the aim of capping the federal budget deficit at 3.0% versus 3.1% for 2016 with a

GDP growth target of 4% to 5% for 2017. An average crude oil price of USD45 per

barrel was benchmarked for Federal government‟s 2017 budget.

In November 2016, Donald Trump‟s victory in the U.S. presidential election caught

the general markets off-guard as investors flock to safe heaven assets like gold,

bond and the Japanese yen, perceiving Trump‟s administration would bring

uncertainty to the markets. The Asian markets reacted with a sharp selldown,

however global investors rebalanced their portfolio to take advantage of the

perceived stronger US growth and higher US bond yields.

In December 2016, the Federal Reserve raised the widely anticipated interest rate

hike by 0.25% to 0.75% in light of the healthy expansion pace of the US economy

while counteracting the President elect‟s goal to further stimulate a recovering

economy. During the month, OPEC members agreed to cut oil production to reduce

the global oil supply glut which caused oil prices to rise to a 16-month high above

USD55 per barrel on 5 December 2016.

9

In January 2017, Mr. Donald Trump‟s inauguration as the new president for United

States of America had brought more policy uncertainty to the world with regards to

US-Mexico cross border trade and potential new restriction on immigration and

travelling into US. Nonetheless, the Dow Jones Index and global financial markets

remained steady during the month.

The global equities market welcomed another surprise 25bps rate hike from US

Federal Reserve on the back of stronger than expected US economic data and a pro-

growth stance by the new administration, bringing the Fed fund rates to 1.00% post

rate hike on 15 March 2017.

In April 2017, historic meeting between Donald Trump and China‟s leader Xi Jin P ing

signaled more understanding between the two countries after a summit held in

Florida, USA that could potentially defuse a trade war between the world‟s two

largest economies.

For the second time in 2017, the Federal Reserve raised interest rates in June,

bringing the Fed fund rate to 1.25%. The Federal Reserve‟s second rate hike

approval was in light of a higher GDP growth expectation of 2.2% and lower

unemployment rate 4.3% for 2017. Notwithstanding the above, the move for the

second hike came in amid expectations of a lower inflation rate compared to the

central bank's target.

In August 2017, the North Korea-US dispute escalated to new heights post of North

Korea‟s missile testing exercise that had prompted President Trump to issue a

retaliation warning with catastrophic effects. As such, the risk-averse sentiment had

weighed down Asian markets.

(Source: Bank Negara Malaysia, Bloomberg and RHB Research Institute Sdn. Bhd.)

10

Bond Market and Money Market

a) Global

In November 2016, US Treasury (UST) yields started a surge amid expectation

of the newly-elected President Donald Trump to embark on further fiscal

expansion. Before the election, the UST yields was already pressured upward as

the Federal Reserve policymakers had signaled additional monetary tightening in

the near term while economists had already projected an upbeat US growth in

2017.

The surge in the 2-year US Treasury yield to above 1.3% at the end of June

2017 was well within expectation given the two US Federal Reserve rate hikes to

date. However, US Treasuries strengthened in August 2017 on the back of safe

haven demand from a series of geopolitical tensions arise when North Korea

threatened to attack Guam and launched a missile testing exercise that flew over

Japan.

Notwithstanding the above, during the financial period under review, the UST

yield increased as compared to the yield as at 31 August 2016.

Figure 2: US Treasury Yields

Source: US Treasury Department, 31 August 2017

11

b) Local

The sovereign bonds dominated the local bond market activities when Malaysian

Government Securities (MGS) and Government Investment Issues (GII) recorded

secondary market traded volume of RM835.5 billion for the financial year under

review. Both the government bond yields and corporate bonds yields increased

across the yield curve after the increase of the Fed Fund rate in June 2017 along

with the market expectation that the US Federal Reserve will increase the Fed

Fund Rate in the second half of 2017.

Table 1: Sukuk/ Islamic Bond Yields

Tenure/Date 31 August 2017

(%)

31 August 2016

(%)

Change

* (bps)

3-Year Bonds

GII 3.54 2.85 69.0

AAA Corporate 4.16 3.84 32.0

5-Year Bonds

GII 3.76 3.27 49.0

AAA Corporate 4.29 4.04 25.0

7-Year Bonds

GII 3.98 3.52 46.0

AAA Corporate 4.44 4.16 28.0

10-Year Bonds

GII 4.06 3.64 42.0

AAA Corporate 4.63 4.33 30.0

Source: Bond Pricing Agency Malaysia (BPAM), 31 August 2017

12

Figure 3: Overnight Policy Rate (OPR)

Source: Bank Negara Malaysia (BNM), 31 August 2017

1.4 Market Outlook and Strategy

a) Equity

The equity market outlook for 2017 is expected to be another volatile year.

External factors may likely influence the domestic market sentiment, which

includes the OPEC and Non-OPEC commitment to stabilize the oil glut,

President Trump‟s stance on North Korea‟s nuclear ambition and potential

military strike, ramifications of US interest rate hikes and currency movement,

political sentiment in the Euro zone, China‟s economic position and monetary

policies employed by Central Banks. With potential interest on selective

sector to support the domestic market, the local bourse should be able to

withstand external shocks given the ample domestic liquidity and buying

interest of foreign and local institutional investors.

While the global economy continues to expand at a moderate pace, there has

been increasing divergence in the growth momentum among the major

economies. For most of Asia, growth is supported by the continued

expansion of domestic demand. Looking ahead, the global economy is

expected to continue on a moderate recovery path.

13

For Malaysia, the resilience of domestic consumption remains the support for

growth. With higher spending on infrastructure projects underway, higher

public sector wages adjustments, improve outlook for CPO production

volume and a rebound in Government consumption and expenditure will help

to improve corporate earnings and consumer spending for the year. Going

forward, domestic demand will still remain as the key driver of growth but the

equities market is likely to be influence by key market risk such as outbreak

of war between North Korea and US and also more outflows from emerging

market as the US Federal Reserve expedite its quantitative tightening

measures in 2018 and 2019.

b) Sukuk Market and Money Market

Moving forward, it is viewed that MGS and corporate bonds will trend higher

compared to their average levels in 2H2016, albeit at a moderate pace. This

is despite of bond yields drifting lower in 1H2017 as it is expected that some

upticks in yield movements on the prospect of a third Fed rate hike as the US

economy continues to recover. Malaysia‟s improving economic fundamentals

should provide some cushion against any sharp yield upticks. It is also

expected that yield movements to become relatively less sharp going forward

as investors come to terms with the Trump presidency and central banks

become more transparent when expressing their desired policy direction.

Bank Negara Malaysia‟s (BNM) Monetary Policy Committee (MPC) kept the

overnight policy rate (OPR) unchanged at 3.00% for its sixth straight meeting

on 13 Jul 2017. Looking forward, it is expected that BNM to maintain OPR at

3.00% for the rest of 2017. It is believed that the monetary policy would

unlikely be tightened for the remaining part of this year, as inflation would

likely normalize moving forward, as the economy has just picked up with

Malaysian Ringgit seeing some stabilisation. On the other hand, stronger

domestic economic growth in the country, coupled with more aggressive rate

hikes and plans to reduce the Fed‟s balance sheet in the US, would likely

limit the scope for BNM to cut interest rates.

14

1.5 Asset allocation as at 31 August

BIMB Dana Al-Munsif 2017

(%)

2016

(%)

2015

(%)

Investment in Quoted Securities

Construction - 1.18 0.75

Consumer Products 1.52 1.74 0.37

Financial - 2.31 1.97

Industrial Products 20.08 14.77 4.77

Infrastructure - 2.84 -

Plantation - 3.70 2.41

Properties - 5.52 3.83

Technology 35.60 10.07 -

Trading and Services 1.55 18.07 9.93

58.75 60.20 24.03

INVESTMENT IN ISLAMIC DEBT

SECURITIES: 22.40 30.72 33.88

SHORT TERM INVESTMENTS: 18.85 9.08 42.09

100.00 100.00 100.00

15

1.6 Other Performance Data for the Financial Year Ended 31 August

BIMB Dana Al-Munsif 2017 2016 2015

Unit Prices (RM)

Highest NAV per unit for the year 0.4901 0.4654 0.5189

Lowest NAV per unit for the year 0.4219 0.4324 0.4407

Net Asset Value (NAV) and Units in

Circulation (UIC) as at the End of the Year

Total NAV (RM) 17,964,710 31,310,926 36,519,502

Units in Circulation (UIC) 36,956,669 72,404,772 82,037,110

NAV per unit (RM)* 0.4861 0.4324 0.4452

Return of Fund (%)(a) [page 17]

Capital Growth (%)(b)

12.42 -2.88 -13.15

Income Return (%)(c)

- 3.01 -

Return of Fund (%) 12.42 0.13 -13.15

Gross Distribution per Unit (Sen) - 1.34 -

Net Distribution per Unit (Sen) - 1.34 -

NAV per Unit before Distribution (RM) - 0.4458 -

NAV per Unit after Distribution (RM)* - 0.4324 -

Date of Distribution - 30 August

2016 -

Management Expense Ratio (MER) (%)(d)

1.86 1.79 1.71

Portfolio Turnover Ratio (PTR) (times)(e)

1.18 1.10 0.79

* The price and net asset value per unit are ex-distribution.

Note:

a) Return of the

Fund

= NAV per unit (end of year) - 1 NAV per unit (beginning of year)

b) Capital Growth = Total Return of the Fund – Income Return

c) Income Return = {Income Distribution per Unit / NAV per Unit on beginning of

year} x 100

d) Management

Expense Ratio

= The management expense ratio is the total management

expenses expressed as an annual percentage of the Fund‟s

average Net Asset Value.

e) Portfolio

Turnover Ratio

= It represents the average of the total acquisitions and disposals

of the investment in the Fund for the annual period over the

average Net Asset Value of the Fund calculated on a daily

basis.

16

1.7 Unit Holdings as at 31 August 2017

Size of Holdings

BIMB Dana Al-Munsif

No. of Unit Holders No. of Units Held

No. % Units %

5,000 and below 945 84.22 990,423.79 2.68

5,001 to 10,000 80 7.13 563,697.34 1.53

10,001 to 50,000 73 6.51 1,377,874.88 3.73

50,001 to 500,000 21 1.87 2,262,976.74 6.12

500,001 and above * 3 0.27 31,761,696.19 85.94

1,122 100.00 36,956,668.94 100.00

Unit Held by Manager 0 0.00 0.00 0.00

Grand Total for The Fund 1,122 100.00 36,956,668.94 100.00

* included under this category are nominee accounts

1.8 Policy on Rebate and Soft Commission

Any stock broking rebates received by the Manager will be directed to the account of

the Fund. Any soft commissions received from the brokers which are in the form of

research and advisory services that assist in the decision-making process relating to

the Fund‟s investment may be retained by the Manager.

The Manager received soft commission from brokers in the form of research and

advisory services during the year under review.

For and on behalf of

The Manager

BIMB INVESTMENT MANAGEMENT BERHAD

Date: 26 October 2017

17

1.0 Laporan Pengurus

Para Pemegang Unit yang Dihormati,

Kami dengan sukacitanya membentangkan Laporan Pengurus BIMB Dana Al-Munsif

bagi tahun kewangan berakhir pada 31 Ogos 2017.

1.1 Nama Dana/ Jenis Dana/ Kategori Dana/ Objektif Pelaburan Dana/ Penanda Aras

Dana/ Polisi Agihan Dana

Nama Dana BIMB Dana Al-Munsif

Jenis Dana Pendapatan dan pertumbuhan

Kategori Dana Seimbang

Objektif

Pelaburan Dana

Objektif utama pelaburan Dana adalah untuk menyediakan

pendapatan yang stabil serta konsisten dan peningkatan modal Unit dalam jangkamasa sederhana hingga jangkamasa panjang. Sehubungan dengan itu, pulangan adalah dalam bentuk pertumbuhan

modal jangkamasa panjang dan pengagihan pendapatan yang konsisten kepada pemegang unit.

Nota: Sebarang perubahan ketara kepada objektif pelaburan Dana memerlukan kelulusan daripada pemegang unit.

Penanda Aras Dana

Nisbah 60:40 daripada Indeks Syariah FBM Emas dan 12 bulan Deposit Bertempoh-i Tawarruq (TDT-i) Bank Islam Malaysia Berhad

Polisi Agihan Dana

Dana ini bertujuan untuk membayar agihan pendapatan tahunan kepada pemegang unit sekiranya pendapatan pelaburan sepanjang

tahun terkumpul adalah mencukupi. Kaedah Pembayaran

Agihan Pendapatan

Bayaran ke akaun bank pelabur atau pelaburan semula.

18

1.2 Pencapaian bagi tahun berakhir 31 Ogos 2017

1.2.1 Kajian Pencapaian BIMB Dana Al-Munsif

Bagi tahun kewangan dalam kajian, BIMB Dana Al-Munsif (Dana) telah mencatatkan

pulangan sebanyak 12.42% berbanding dengan pulangan penanda aras sebanyak

2.92%.

Sejak penubuhannya pada 27 Disember 2001 hingga 31 Ogos 2017, Dana

mencatatkan pulangan berjumlah 108.76% berbanding pulangan penanda aras

sebanyak 111.43%.

Penanda aras terpilih prestasi Dana adalah berdasarkan kepada nisbah 60:40 Indeks

Syariah Emas FBM dan kadar 12 bulan Deposit Bertempoh-i Tawarruq (TDT-i) Bank

Islam Malaysia Berhad.

Strategi Dana secara konsistennya adalah kekal memberikan tumpuan kepada

syarikat-syarikat yang kukuh dan berpotensi untuk membayar dividen secara

berkekalan dan mempunyai prospek pertumbuhan pendapatan.

Dalam tahun kewangan berakhir pada 31 Ogos 2017, Dana tidak mendapat

keuntungan urus niaga yang mencukupi untuk mengumumkan agihan pendapatan

bagi tahun berkenaan disebabkan oleh kemeruapan pasaran yang di luar jangkaan.

Meskipun begitu, Pengurus telah meningkatkan prestasi Dana dengan mengurangkan

pendedahan terhadap saham-saham yang tidak berprestasi dan melaburnya semula

dalam syarikat-syarikat dan sektor-sektor yang menawarkan prospek dan potensi

lebih cerah untuk memberikan prestasi pergerakan Nilai Aset Bersih (NAB) yang lebih

baik.

Sehingga pada 31 Ogos 2017, Dana mempunyai pendedahan sebanyak 58.75%

dalam ekuiti, 22.4% dalam sekuriti hutang Islam dan 18.85% dalam pelaburan jangka

pendek, tunai dan setara tunai. Dari segi jumlah NAB, saiz Dana sehingga pada 31

Ogos 2017 adalah RM17.96 juta, berbanding RM31.31 juta sehingga pada 31 Ogos

2016. NAB seunit Dana telah meningkat kepada RM0.4861 pada 31 Ogos 2017

daripada RM0.4324 pada 31 Ogos 2016.

Peruntukan ekuiti Dana yang dikekalkan sekitar 60% untuk dimanfaatkan bagi

meningkatkan pelaburan ketika berlaku pergerakan menaik harga saham. Melangkah

ke hadapan, Pengurus akan meneruskan pelaburan dalam syarikat-syarikat yang

dijangka menawarkan pendapatan yang baik, mempunyai lembaran imbangan yang

kukuh, dan hasil dividen yang tinggi dengan prospek penilaian yang baik apabila

adanya peluang-peluang yang sesuai.

Bagi tahun kewangan berakhir pada 31 Ogos 2017, tidak terdapat sebarang

perubahan ketara dalam hal ehwal pengurusan Dana dan tidak berlaku sebarang

keadaan yang boleh menjejaskan kepentingan para pemegang unit sehingga tarikh

Laporan Pengurus ini disediakan.

19

1.2.2 Jumlah pulangan dan purata jumlah pulangan bagi setiap tahun berakhir 31

Ogos 2017

BIMB Dana Al-Munsif Penanda Aras

Jumlah

Pulangan

(%)

Purata

Jumlah

Pulangan

(%)

Jumlah

Pulangan

(%)

Purata

Jumlah

Pulangan

(%)

Jangkamasa

1-Tahun 12.42 12.42 2.92 2.92

Jangkamasa

3-Tahun -2.23 -0.74 2.13 0.71

Jangkamasa

5-Tahun 6.39 1.28 14.74 2.95

1.2.3 Jumlah pulangan tahunan bagi 5 tahun kewangan yang lalu

Tahun Kewangan

Jumlah Pulangan

BIMB Dana Al-Munsif

(%)

Penanda Aras

(%)

31 Ogos 2017 12.42 2.92

31 Ogos 2016 0.13 6.58

31 Ogos 2015 -13.15 -6.90

31 Ogos 2014 5.14 7.14

31 Ogos 2013 3.50 4.96

20

Rajah 1: Pergerakan Dana Berbanding Penanda Aras

Nota:

Sumber Data : BIMB Investment Management Berhad

Data disahkan oleh : Novagni Analytics & Advisory Sdn. Bhd.

Penanda Aras : Nisbah 60:40 Indeks Syariah FBM Emas dan 12 bulan

Deposit Bertempoh-i Tawarruq (TDT-i) Bank Islam

Malaysia Berhad

21

1.3 Ekonomi dan Kajian Pasaran

1.3.1 Ekonomi

Global

Keluaran Dalam Negara Kasar (KDNK) Amerika Syarikat ('AS') berkembang sebanyak

2.6% pada suku kedua 2017 berbanding pertumbuhan 1.2% pada suku pertama 2017

dan 1.8% pada suku keempat 2016. KDNK yang berkembang pantas pada suku kedua

2017 dapat dilihat daripada peningkatan perbelanjaan kerajaan persekutuan dan

pelaburan persediaan swasta walaupun diimbangi oleh penurunan dalam eksport.

Kadar inflasi utama AS meningkat sebanyak 1.9% pada bulan Ogos 2017 berbanding

1.5% pada bulan September 2016 disebabkan berlakunya peningkatan kos dan harga

gasolin apabila Taufan Harvey telah menyebabkan penutupan kilang penapis di pantai

Teluk.

Kadar pengangguran AS jatuh kepada 4.4% pada bulan Ogos 2017 daripada 5.0%

pada bulan September 2016, disokong oleh peningkatan pendapatan, perbelanjaan

pengguna dan pertumbuhan ekonomi.

Ekonomi zon Euro berkembang sebanyak 0.6% pada suku kedua 2017 berbanding

0.5% pada suku pertama 2017 dan 0.6% pada suku keempat 2016. Pemulihan

ekonomi zon Euro menyaksikan berlakunya peningkatan momentum manakala

pengangguran telah menurun di sebalik kejatuhan kadar faedah yang teramat rendah

diantara langkah-langkah lain yang dilaksanakan oleh Bank Pusat Eropah (ECB) untuk

meningkatkan aktiviti ekonomi.

Kadar inflasi tahunan zon Euro meningkat sebanyak 1.5% pada bulan Ogos 2017

daripada 0.4% pada bulan September 2016, didorong oleh prestasi pertumbuhan

KDNK yang lebih baik di kawasan zon Euro.

Kadar pengangguran di zon Euro jatuh kepada 9.1% pada bulan Julai 2017, merosot

daripada 10.0% pada bulan September 2016 dan kekal berada pada paras terendah

sejak bulan Julai 2011.

China mengekalkan kadar pertumbuhan ekonominya sebanyak 6.9% pada suku

kedua 2017, menyamai pertumbuhan pada suku pertama 2017 berikutan

peningkatan dalam pengeluaran perindustrian dan penggunaan swasta dengan

dibantu oleh pasaran hartanah yang kukuh dan pemulihan sektor eksport .

(Sumbe: Bloomberg dan RHB Research Institute Sdn Bhd)

22

Dalam Negara

Ekonomi Malaysia berkembang pantas sebanyak 5.8% pada suku kedua 2017

berbanding 5.6% pada suku pertama 2017 dan 4.5% pada suku keempat 2016. KDNK

yang lebih kukuh dalam tempoh berkenaan adalah hasil peningkatan dalam

penggunaan swasta dan eksport.

Kadar utama inflasi di Malaysia pada bulan Ogos 2017 meningkat kepada 3.7%

daripada 1.5% pada bulan September 2016, berikutan kos lebih tinggi bagi makanan

dan minuman bukan alkohol, pengangkutan dan perumahan, sejajar dengan kenaikan

lebih tinggi harga minyak mentah dan prestasi pertumbuhan KDNK yang lebih kukuh.

Jawatankuasa Dasar Monetari Bank Negara Malaysia (MPC) mengekalkan Kadar

Dasar Semalaman (OPR) pada paras 3.00% dalam mesyuaratnya yang diadakan pada

bulan Julai bersesuaian dengan prospek pertumbuhan negara.

Rizab antarabangsa Bank Negara berjumlah AS$100.5 bilion setakat pada 30 Ogos

2017 berbanding AS$97.7 bilion pada bulan September 2016 dengan terdapatnya

peningkatan aliran masuk modal daripada pelabur-pelabur institusi asing ke Malaysia.

(Sumber: Bloomberg, Bank Negara Malaysia dan RHB Research Institute Sdn Bhd)

1.3.2 Kajian Pasaran

Ekuiti

Indeks Syariah EMAS FTSE Bursa Malaysia (FBM Syariah) memasuki tahun dalam

kajian pada paras 12,430.50 mata sebelum jatuh ke paras terendah 11,845.46 pada

30 November 2016. FBM Syariah, kemudiannya meningkat ke paras tertinggi kepada

13,126.04 pada 16 Mei 2017 sebelum mengakhiri tahun kewangan di paras 12,749.09

mata pada 30 Ogos 2017. Bagi tahun dalam kajian, FBM Syariah meningkat 318.59

mata atau 2.56% manakala FBM KLCI mencatat kenaikan sebanyak 65.32 mata atau

4.05%. Antara faktor utama yang menyumbang kepada pergerakan indeks ini adalah

seperti berikut:

Rizab Persekutuan AS enggan menaikkan kadar faedah pada September 2016 iaitu

lebih awal daripada Pilihan Raya Presiden Amerika Syarikat yang diadakan pada

November 2016 kerana menganggap ekonomi AS masih mempunyai ruang untuk

meningkat sebelum berdepan dengan risiko mengalami pertumbuhan yang terlalu

tinggi.

Perdana Menteri Malaysia membentangkan Bajet 2017 pada 21 Oktober 2016 yang

bertujuan mengekang defisit bajet persekutuan pada paras 3.0% berbanding 3.1%

pada tahun 2016 dengan menyasarkan pertumbuhan KDNK antara 4% hingga 5% bagi

tahun 2017. Bajet 2017 itu disediakan berdasarkan harga purata minyak mentah pada

paras AS$45 setong.

23

Pada November 2016, kemenangan Donald Trump dalam Pilihan Raya Presiden AS

adalah di luar jangkaan dan mengejutkan pasaran amnya apabila para pelabur

berpusu-pusu mencari aset pelaburan yang selamat seperti emas, bon dan yen Jepun

kerana mempercayai bahawa pentadbiran Trump akan menyebabkan berlakunya

ketidaktentuan dalam pasaran. Pasaran Asia pula mengalami kegiatan jualan secara

besar-besaran sebelum para pelabur sejagat kemudiannya mengimbangi semula

portfolio mereka untuk mengambil faedah daripada pertumbuhan lebih kukuh dalam

ekonomi AS dan kadar hasil bon AS yang lebih tinggi.

Pada Disember 2016, Rizab Persekutuan menaikkan kadar faedah sebanyak 0.25%

kepada 0.75% seperti dijangkakan oleh banyak pihak berikutan berlakunya kadar

perkembangan yang menggalakkan dalam ekonomi AS sambil mengimbangi matlamat

Presiden yang baru dipilih untuk terus merangsang ekonomi negara itu. Pada bulan

tersebut, negara-negara anggota OPEC bersetuju mengurangkan pengeluaran minyak

mentah dalam usaha menangani lebihan komoditi berkenaan yang mengakibatkan

harga minyak mentah global meningkat ke paras tertinggi dalam tempoh 16 bulan iaitu

di atas paras AS$55 setong pada 5 Disember 2016.

Pada Januari 2017, Donald Trump secara rasminya menjadi presiden baharu Amerika

Syarikat namun beliau lebih banyak memperkenalkan dasar-dasar tidak jelas kepada

dunia berkaitan perdagangan melangkaui sempadan AS-Mexico dan potensi halangan

baharu imigresen dan perjalanan warga asing ke AS. Bagaimanapun, Indeks Dow

Jones dan pasaran kewangan global kekal stabil pada bulan itu.

Pasaran ekuiti global mengalu-alukan kenaikan mengejut kadar faedah AS sebanyak

25 mata asas oleh Rizab Persekutuan AS berikutan data ekonomi negara itu yang

lebih kukuh berbanding jangkaan dan juga pendirian pro-pertumbuhan oleh

pentadbiran baharu, menyebabkan kadar dana Persekutuan meningkat kepada 1.00%

selepas kenaikan kadar faedah pada 15 Mac 2017.

Pada April 2017, pertemuan bersejarah antara Donald Trump dan pemimpin China, Xi

Jin Ping telah meningkatkan persefahaman dalam hubungan antara kedua-dua negara

itu selepas sidang kemuncak diadakan di Florida, Amerika Syarikat yang mungkin

dapat menghapuskan potensi berlakunya perang perdagangan antara dua kuasa besar

ekonomi dunia.

Bagi kenaikan kali kedua dalam tahun 2017, Rizab Persekutuan AS telah menaikkan

kadar faedah pada bulan Jun dan menyaksikan kadar dana bank pusat itu berada

pada paras 1.25%. Kenaikan kali kedua itu diluluskan berdasarkan jangkaan

pertumbuhan KDNK lebih tinggi sebanyak 2.2% dan kadar pengangguran yang lebih

rendah sebanyak 4.3% bagi tahun 2017. Bagaimanapun, kenaikan kali kedua itu dibuat

di tengah-tengah jangkaan kadar inflasi yang lebih rendah berbanding sasaran bank

pusat.

Pada bulan Ogos 2017, pertikaian antara Korea Utara dengan AS semakin memuncak

menjadi lebih buruk selepas Korea Utara melakukan ujian peluru berpandu sehingga

mendorong Presiden Trump mengeluarkan amaran untuk bertindak balas dengan

kesan yang berat. Akibatnya, sentimen para pelabur mahu mengelak berdepan risiko

telah menjejaskan pasaran Asia.

24

Pasaran Bon dan Pasaran Wang

a) Global

Pada bulan November 2016, hasil Perbendaharaan AS mula melonjak dengan

jangkaan Presiden Donald Trump akan memulakan pengembangan fiskal.

Sebelum pilihan raya, hasil bon perbendaharaan AS (UST) telah berdepan tekanan

untuk mencatat peningkatan di mana penggubal dasar Rizab Persekutuan telah

memberi isyarat akan pelaksanaan dasar kewangan yang lebih ketat dalam masa

terdekat manakala pakar-pakar ekonomi telah membuat unjuran akan peningkatan

pertumbuhan AS pada tahun 2017.

Peningkatan dalam hasil 2 tahun UST untuk berada di atas paras 1.3% pada akhir

bulan Jun 2017 adalah dalam jangkaan memandangkan setakat ini terdapat dua

kenaikan kadar Rizab Persekutuan AS. Akan tetapi, bon perbendaharaan AS

mengukuh pada bulan Ogos 2017 dengan wujudnya permintaan terhadap

pelaburan lebih selamat berikutan terdapat satu siri ketegangan geopolitik di mana

Korea Utara mengancam untuk menyerang Guam dan melancarkan peluru

berpandu balistik melintasi ruang udara Jepun.

Walau bagaimanapun, dalam tempoh kewangan yang dikaji, hasil UST meningkat

berbanding hasil pada 31 Ogos 2016.

25

Rajah 2: Kadar Pulangan Perbendaharaan AS

Sumber : Jabatan Perbendaharaan AS, 31 Ogos 2017

26

b) Dalam Negara

Bon kedaulatan menguasai aktiviti pasaran bon tempatan apabila Sekuriti Kerajaan

Malaysia (MGS) dan Terbitan Pelaburan Kerajaan (GII) mencatatkan jumlah

dagangan pasaran sekunder sebanyak RM835.5 bilion bagi tahun kewangan

dalam kajian. Hasil bon kerajaan dan bon korporat meningkat di keseluruhan

keluk hasil selepas peningkatan kadar Dana Rizab Persekutuan AS pada bulan

Jun 2017 dan pasaran menjangkakan Rizab Persekutuan AS akan meningkatkan

Kadar Dana bank pusat itu pada separuh kedua tahun 2017.

Jadual 1: Kadar Pulangan Sukuk/ Bon Islam

Tempoh/ Tarikh 31 Ogos 2017

(%)

31 Ogos 2016

(%)

Perubahan

* (bps)

Bon 3 Tahun

GII 3.54 2.85 69.0

Korporat AAA 4.16 3.84 32.0

Bon 5 Tahun

GII 3.76 3.27 49.0

Korporat AAA 4.29 4.04 25.0

Bon 7 Tahun

GII 3.98 3.52 46.0

Korporat AAA 4.44 4.16 28.0

Bon 10 Tahun

GII 4.06 3.64 42.0

Korporat AAA 4.63 4.33 30.0

Sumber: Agensi Penetapan Harga Bon Malaysia (BPAM), 31 Ogos 2017

27

Rajah 3: Kadar Polisi Semalaman (OPR)

Sumber: Bank Negara Malaysia (BNM), 31 Ogos 2017

1.4 Tinjauan Pasaran dan Strategi

a) Ekuiti

Tinjauan pasaran ekuiti bagi tahun 2017 menunjukkan ia akan terus berada

dalam keadaan tidak menentu. Faktor luaran berkemungkinan mempengaruhi

sentimen pasaran domestik termasuklah komitmen negara-negara anggota Opec

dan bukan Opec untuk menstabilkan pasaran minyak yang mengalami lebihan

pengeluaran, pendirian Presiden Trump terhadap cita-cita nuklear Korea Utara

dan opsyen tindakan ketenteraan, kesan kenaikan kadar faedah AS dan

pergerakan mata wang, sentimen politik di zon Euro, pelarasan ekonomi China

dan dasar kewangan yang diterima pakai oleh Bank-bank Pusat. Dengan potensi

minat terhadap sektor terpilih untuk menyokong pasaran domestik, bursa

tempatan harus berupaya menahan kejutan luaran memandangkan terdapat

mudah tunai yang besar dalam negara dan minat belian daripada para

pelabur institusi asing dan tempatan.

Ketika ekonomi global terus berkembang pada kadar yang sederhana,

pencapahan didapati meningkat dalam momentum pertumbuhan didapati dalam

kalangan negara maju yang utama. Bagi sebahagian besar Asia,

pertumbuhannya disokong oleh pengembangan permintaan domestik yang

berterusan. Dalam melangkah ke hadapan, ekonomi global dijangka terus berada

pada landasan pemulihan yang sederhana.

28

Di Malaysia, ketahanan penggunaan domestik kekal menjadi penyokong kepada

pertumbuhannya. Dengan jumlah perbelanjaan lebih besar diperuntukkan kepada

projek-projek infrastruktur yang sedang dijalankan, upah sektor awam yang lebih

tinggi, tinjauan jumlah pengeluaran MSM (CPO) yang bertambah baik dan

terdapat lonjakan dalam penggunaan dan perbelanjaan Kerajaan akan

membantu menambah baik pendapatan korporat dan perbelanjaan pengguna

pada tahun ini. Dalam melangkah ke hadapan, permintaan dalam negeri kekal

menjadi pemacu utama pertumbuhan tetapi pasaran ekuiti mungkin akan

dipengaruhi oleh risiko pasaran utama seperti meletusnya perang antara Korea

Utara dan Amerika Syarikat dan juga pengaliran keluar dana daripada pasaran

baru muncul memandangkan Rizab Persekutuan AS mempercepatkan langkah

pengetatan kuantitatif pada tahun 2018 dan 2019.

b) Pasaran Sukuk dan Pasaran Wang

Bergerak ke hadapan, MGS dan bon korporat dilihat akan berada dalam aliran

menaik yang lebih tinggi berbanding paras puratanya pada setengah kedua

tahun 2016 walaupun pada tahap sederhana. Keadaan ini berlaku di sebalik hasil

bon berada di paras rendah dalam setengah pertama tahun 2017 kerana

terdapat jangkaan berlaku beberapa kenaikan dalam pergerakan hasil berikutan

prospek kenaikan kadar Rizab Persekutuan yang ketiga apabila AS terus

mencatat pemulihan ekonomi. Asas-asas ekonomi Malaysia yang semakin baik

akan menjadi penampan kepada sebarang kenaikan hasil yang mendadak.

Pergerakan hasil dijangka meningkat secara tidak mendadak dalam masa yang

mendatang apabila para pelabur lebih maklum tentang pendirian Trump dan

bank-bank pusat menjadi lebih telus apabila menyatakan arah dasar yang

dikehendaki.

Jawatankuasa Dasar Monetari Bank Negara Malaysia (MPC) mengekalkan kadar

dasar semalaman (OPR) pada paras 3.00% bagi mesyuarat yang ke-6 secara

berturut-turut pada 13 Julai 2017. Memandang ke hadapan, BNM dijangka

mengekalkan OPR pada kadar 3.00% untuk tempoh yang seterusnya dalam

tahun 2017. Dasar monetari ini dipercayai tidak akan diketatkan lagi dalam

bulan-bulan berikutnya pada tahun ini kerana kadar inflasi dijangka kembali

normal selepas ini memandangkan pertumbuhan ekonomi baru sahaja meningkat

dengan Ringgit Malaysia memperlihatkan kestabilannya. Sebaliknya,

pertumbuhan ekonomi domestik yang lebih kukuh ditambah pula dengan

kenaikan kadar faedah yang lebih agresif dan pelan untuk mengurangkan

lembaran imbangan Rizab Persekutuan di AS, berkemungkinan akan

mengehadkan skop bagi BNM mengurangkan kadar faedah dalam negara.

29

1.5 Peruntukan Aset Pada 31 Ogos

BIMB Dana Al-Munsif 2017

(%) 2016

(%) 2015

(%)

Pelaburan Sekuriti Tersiarharga:

Pembinaan - 1.18 0.75

Barangan Pengguna 1.52 1.74 0.37

Kewangan - 2.31 1.97

Barangan Industri 20.08 14.77 4.77

Infrastruktur - 2.84 -

Perladangan - 3.70 2.41

Hartanah - 5.52 3.83

Teknologi 35.60 10.07 -

Perdagangan dan Perkhidmatan 1.55 18.07 9.93

58.75 60.20 24.03

PELABURAN DALAM SEKURITI

HUTANG SECARA ISLAM: 22.40 30.72 33.88

PELABURAN JANGKA PENDEK: 18.85 9.08 42.09

100.00 100.00 100.00

30

1.6 Lain-Lain Data Prestasi Bagi Tahun Berakhir 31 Ogos

BIMB Dana Al-Munsif 2017 2016 2015

Harga Unit (RM)

NAB tertinggi seunit dalam setahun 0.4901 0.4654 0.5189

NAB terendah seunit dalam setahun 0.4219 0.4324 0.4407

Nilai asset Bersih (NAB) dan Unit Dalam Edaran (UDE) pada Akhir Tahun

Jumlah NAB (RM) 17,964,710 31,310,926 36,519,502

Unit Dalam Edaran (UDE) 36,956,669 72,404,772 82,037,110

NAB seunit (RM)* 0.4861 0.4324 0.4452

Jumlah Pulangan Dana (%)(a)

Pertumbuhan Modal (%)(b)

12.42 -2.88 -13.15

Pulangan Pendapatan (%)(c)

- 3.01 -

Jumlah Pulangan Dana (%) 12.42 0.13 -13.15

Agihan Kasar seunit (Sen) - 1.34 -

Agihan Bersih seunit (Sen) - 1.34 -

Nilai Aset Bersih sebelum Pengagihan (RM) - 0.4458 -

Nilai Aset Bersih selepas Pengagihan (RM)* - 0.4324 -

Tarikh Pengagihan - 30 Ogos

2016 -

Nisbah Perbelanjaan Pengurusan (NPP)

(%)(d) 1.86 1.79 1.71

Nisbah Pusing Ganti Portfolio (Kali)(e)

1.18 1.10 0.79

* Harga NAB selepas pengagihan pendapatan.

Nota:-

a) Pulangan ke

atas Dan

= Harga seunit (pada akhir tahun) - 1

Harga seunit (pada awal tahun)

b) Penambahan

Modal

= Pulangan Ke atas Dana – Pulangan Pendapatan

c) Pulangan

Pendapatan

= {Pengagihan Pendapatan Se Unit / NAB se unit pada awal tahun}

x 100

d) Nisbah

Perbelanjaan

Pengurusan

= Ia dikira dengan mengambil jumlah perbelanjaan pengurusan

sepertimana yang dinyatakan sebagai peratusan tahunan daripada

jumlah purata Nilai Aset Bersih Dana.

e) Nisbah Pusing

Ganti Portfolio

= Ia dikira dengan mengambil purata jumlah perolehan dan pelupusan

pelaburan dalam Dana bagi tempoh tahunan dibahagi dengan

purata Nilai Aset Bersih Dana yang dikira pada asas harian

31

1.7 Pecahan Pegangan Unit pada 31 Ogos 2017

Saiz Dipegang

BIMB Dana Al-Munsif

Bilangan Pemegang Unit Bilangan Unit Pegangan

Bilangan % Bilangan %

Kurang daripada 5,000 945 84.22 990,423.79 2.68

5,001 hingga 10,000 80 7.13 563,697.34 1.53

10,001 hingga 50,000 73 6.51 1,377,874.88 3.73

50,001 hingga 500,000 21 1.87 2,262,976.74 6.12

500,001 dan ke atas * 3 0.27 31,761,696.19 85.94

1,122 100.00 36,956,668.94 100.00

Unit yang dipegang oleh Pengurus

0 0.00 0.00 0.00

Jumlah Keseluruhan Dana

1,122 100.00 36,956,668.94 100.00

*Akaun penama juga termasuk di bawah kategori ini

1.8 Polisi Rebat dan Komisyen Bukan Tunai

Sebarang rebat broker saham yang diterima oleh Pengurus akan dimasukkan ke

dalam akaun Dana. Mana-mana komisen ringan (bukan tunai) yang diterima daripada

broker dalam bentuk perkhidmatan penyelidikan dan khidmat nasihat bertujuan

membantu proses membuat keputusan berkaitan dengan pelaburan Dana boleh

disimpan oleh Pengurus.

Pengurus menerima komisen bukan tunai daripada broker dalam bentuk perkhidmatan

penyelidikan dan khidmat nasihat bagi tahun dalam kajian.

Bagi dan bagi pihak

Pengurus

BIMB INVESTMENT MANAGEMENT BERHAD

Tarikh: 26 Oktober 2017

Nota:

Laporan ini telah diterjemahkan daripada laporan asal (dalam Bahasa Inggeris). Jika

terdapat perbezaan, sila rujuk kepada laporan Bahasa Inggeris

32

2.0 Trustee’s Report

AFFIN HWANG TRUSTEE BERHAD

ANNUAL REPORT FOR THE YEAR ENDED 31 AUGUST 2017

To the Unit Holders of

BIMB Dana Al-Munsif

We have acted as Trustee of BIMB Dana Al-Munsif (“the Fund”) for the year ended 31

August 2017. To the best of our knowledge, BIMB Investment Management Berhad

(“the Manager” or “the Management Company”) has managed the Funds in accordance

with the following:

1. The limitations imposed on the investment powers of the Management Company and

the Trustee under the Deeds, the Securities Commission‟s Guidelines on Unit Trust

Funds, the Capital Markets and Services Act 2007 and other applicable laws;

2. The valuation or pricing of the Funds is carried out in accordance with the Deeds and

any regulatory requirement;

3. The creation and cancellation of units of the Funds are carried out in accordance

with the Deeds and any regulatory requirement; and

For Affin Hwang Trustee Berhad

…………………..…………

Tan Ping Ying

Authorised Signatory

………………………

Wong Chiew Leng

Authorised Signatory

Date: 26 October 2017

33

3.0 Shariah Committee’s Report

ANNUAL REPORT FOR THE YEAR ENDED 31 AUGUST 2017

حيم ن ٱلر ـ حم بسم ٱهلل ٱلر To the Unit Holders of

BIMB Dana Al-Munsif

We have acted as the Shariah Committee of BIMB Dana Al-Munsif.

Our responsibilities are to ensure that the procedures and processes employed by BIMB

Investment Management Berhad and that the provisions of the Deed dated 6 December

2001 are in accordance with Shariah principles.

In our opinion, BIMB Investment Management Berhad has managed BIMB Dana Al-

Munsif in accordance with Shariah principles and complied with applicable guidelines,

rulings or decisions issued by the Securities Commission pertaining to Shariah matters

for the year ended 31 August 2017.

In addition, we also confirm that the investment portfolio of BIMB Dana Al-Munsif

comprises securities which have been classified as Shariah-compliant by the Shariah

Advisory Council (SAC) of the Securities Commission, as the case may be and that all

deposits and money market instruments placed by the Funds are Shariah-compliant.

أعلم وهللا

For and on behalf of the Shariah Committee ………………………………………………..

USTAZ DR. AHMAD SHAHBARI@SOBRI SALAMON (Chairman)

……………………………………………….. USTAZ DR. YUSOF RAMLI (Committee Member)

……………………………………………….. USTAZAH DR. ASMAK AB. RAHMAN

(Committee Member) Date: 26 October 2017

34

4.0 Directors’ Declaration

ANNUAL REPORT FOR THE YEAR ENDED 31 AUGUST 2017

To the Unit Holders of

BIMB Dana Al-Munsif

We, Dato‟ Ghazali Bin Awang and Najmuddin Bin Mohd Lutfi, being two of the directors

of the Manager, BIMB Investment Management Berhad, for BIMB Dana Al-Munsif, do

hereby state that in our opinion, the accompanying Statement of Financial Position,

Statement of Profit or Loss and other Comprehensive Income, Statement of Changes in

Net Asset Value and Statement of Cash Flows are drawn up so as to give true and fair

view of the Statement of Financial Position of the Fund as at 31 August 2017 and

Statement of Profit or Loss and other Comprehensive Income, Statement of Changes in

Net Asset Value and Statement of Cash Flows for the year ended on that date.

For and on behalf of the Board of Directors,

…………………………………

DATO’ GHAZALI BIN AWANG

(Non Executive Independent Director)

…………………………………

NAJMUDDIN BIN MOHD LUTFI

(Chief Executive Officer)

Date: 26 October 2017

35

5.0 Independent Auditor’s Report

Independent Auditors’ Report to the Unitholders of BIMB Dana Al-Munsif

(Established in Malaysia)

Report on the Financial Statements

We have audited the financial statements of BIMB Dana Al-Munsif (“the Fund”), which

comprise the statement of financial position as at 31 August 2017, and the statement of profit

or loss and other comprehensive income, statement of changes in net asset value and cash

flows for the year then ended, and notes to the financial statements, including a summary of

significant accounting policies, as set out on pages 38 to 62.

In our opinion, the accompanying financial statements give a true and fair view of the financial

position of the Fund as at 31 August 2017, and of its financial performance and its cash flows

for the year then ended in accordance with Malaysian Financial Reporting Standards,

International Financial Reporting Standards and Securities Commission‟s Guidelines on Unit

Trust Funds in Malaysia.

Basis for Opinion

We conducted our audit in accordance with approved standards on auditing in Malaysia and

International Standards on Auditing. Our responsibilities under those standards are further

described in the Auditors’ Responsibilities for the Audit of the Financial Statements section of

our report. We believe that the audit evidence we have obtained is sufficient and appropriate

to provide a basis for our opinion.

Independence and Other Ethical Responsibilities

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics,

Conduct and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the

International Ethics Standards Board for Accountants‟ Code of Ethics for Professional

Accountants (“IESBA Code”), and we have fulfilled our other ethical responsibilities in

accordance with the By-Laws and the IESBA Code.

Information Other than the Financial Statements and Auditors’ Report Thereon

The Manager of the Fund is responsible for the other information. The other information

comprises the information included in the annual report, but does not include the financial

statements of the Fund and our auditors‟ report thereon.

Our opinion on the financial statements of the Fund does not cover the annual report and we

do not express any form of assurance conclusion thereon.

36

Auditors’ Responsibilities for the Audit of the Financial Statements (continued)

Information Other than the Financial Statements and Auditors’ Report Thereon

(continued)

In connection with our audit of the financial statements of the Fund, our responsibility is to

read the annual report and, in doing so, consider whether annual report is materially

inconsistent with the financial statements of the Fund or our knowledge obtained in the audit

or otherwise appears to be materially misstated.

If, based on the work we have performed, we conclude that there is a material misstatement

of the annual report, we are required to report that fact. We have nothing to report in this

regard.

Responsibilities of the Manager and Trustee for the Financial Statements

The Manager of the Fund is responsible for the preparation of financial statements of the

Fund that give a true and fair view in accordance with Malaysian Financial Reporting

Standards, International Financial Reporting Standards and Securities Commission‟s

Guidelines on Unit Trust Funds in Malaysia. The Manager is also responsible for such internal

control as the Manager determine is necessary to enable the preparation of financial

statements of the Fund that are free from material misstatement, whether due to fraud or

error.

In preparing the financial statements of the Fund, the Manager is responsible for assessing

the ability of the Fund to continue as a going concern, disclosing, as applicable, matters

related to going concern and using the going concern basis of accounting unless the Manager

either intend to liquidate the Fund or to cease operations, or have no realistic alternative but

to do so.

The Trustee is responsible for ensuring that the Manager maintains proper accounting and

other records as necessary to enable true and fair presentations of these financial statement.

Auditors’ Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements of

the Fund as a whole are free from material misstatement, whether due to fraud or error, and

to issue an auditors‟ report that includes our opinion. Reasonable assurance is a high level of

assurance, but is not a guarantee that an audit conducted in accordance with approved

standards on auditing in Malaysia and International Standards on Auditing will always detect a

material misstatement when it exists. Misstatements can arise from fraud or error and are

considered material if, individually or in the aggregate, they could reasonably be expected to

influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit conducted in accordance with approved standards on auditing in Malaysia

and International Standards on Auditing, we exercise professional judgement and maintain

professional scepticism throughout the audit. We also:

37

Auditors’ Responsibilities for the Audit of the Financial Statements (continued)

Identify and assess the risk of material misstatement of the financial statements of the

Fund, whether due to fraud or error, design and perform audit procedures responsive to

those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis

for our opinion. The risk of not detecting a material misstatement resulting from fraud is

higher than for one resulting from error, as fraud may involve collusion, forgery,

intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of

expressing an opinion on the effectiveness of the Fund‟s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of

accounting estimates and related disclosures made by the Manager.

Conclude on the appropriateness of the Manager‟s use of the going concern basis of

accounting and, based on the audit evidence obtained, whether a material uncertainty

exists related to events or conditions that may cast significant doubt on the ability of the

Fund to continue as a going concern. If we conclude that a material uncertainty exists,

we are required to draw attention in our auditors‟ report to the related disclosures in the

financial statements of the Fund or, if such disclosures are inadequate, to modify our

opinion. Our conclusions are based on the audit evidence obtained up to the date of our

auditors‟ report. However, future events or conditions may cause the Fund to cease to

continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements of the

Fund, including the disclosures, and whether the financial statements of the Fund

represents the underlying transactions and events in a manner that gives a true and fair

view.

We communicate with the Manager regarding, among other matters, the planned scope and

timing of the audit and significant audit findings, including any significant deficiencies in

internal control that we identify during our audit.

Other matter

This report is made solely to the unitholders of the Fund, as a body, in accordance with

Securities Commission‟s Guidelines on Unit Trust Funds in Malaysia and for no other

purpose. We do not assume responsibility to any other person for the content of this report.

KPMG Desa Megat PLT

(LLP0010082-LCA & AF 0759)

Chartered Accountant

Adrian Lee Lye Wang

Approval Number: 2679/11/17(J)

Chartered Accountants

Petaling Jaya, Selangor

Date: 26 October 2017

38

6.0 Financial Statements (Audited) BIMB Dana Al-Munsif

6.1 Statement of Financial Position as at 31 August 2017

Note 2017 2016

RM RM

Assets

Quoted securities 4 10,554,000 18,849,727

Islamic debt securities 5 4,024,920 9,618,745

Amount due from Manager 1,306 1,691

Other receivables 35,234 127,662

Current tax assets - 5,991

Cash and cash equivalents 6 3,414,603 2,944,389

Total assets 18,030,063 31,548,205

Liabilities

Amount due to Manager 9,813 135,119

Other payables 55,540 84,192

Distribution payable - 17,968

Total liabilities 65,353 237,279

Net asset value 17,964,710 31,310,926

Unitholders’ fund

Unitholders‟ capital 7 22,358,416 37,892,073

Accumulated losses (4,393,706) (6,581,147)

Net asset value attributable to unitholders 17,964,710 31,310,926

Number of units in circulation 7 36,956,669 72,404,772

Net asset value per unit

-Ex distribution (sen)

48.61

43.24

The notes on pages 42 to 62 are an integral part of these financial statements.

39

BIMB Dana Al-Munsif

6.2 Statement of Profit or Loss and Other Comprehensive Income for the financial

year ended 31 August 2017

Note 2017 2016

RM RM

Income

(Loss)/Gain on sale of quoted shares (4,921,211) 739,411

Gain on sale of Islamic debt securities 4,096 -

Gross dividends from shares quoted in

Malaysia 315,490 455,912

Income from Islamic debt securities 286,327 524,274

Income from short term investments 99,471 148,865

Hibah from Al-Wadiah account 600 514

Net unrealised gain/(loss) from financial

instruments at fair value through profit or

loss

6,844,217

(1,096,795)

2,628,990 772,181

Less: Amortisation of premium (14,696) (38,139)

Gross income 2,614,294 734,042

Expenses

Manager‟s fee 8 347,740 517,031

Trustee‟s fee 9 18,546 27,575

Audit fee 13,000 11,000

Tax agent‟s fee 2,000 2,000

Administrative expenses 50,146 57,700

431,432 615,306

Net income before taxation 2,182,862 118,736

Taxation 10 4,579 -

Net income after taxation 2,187,441 118,736

Other comprehensive income for the year - -

Total comprehensive income for the year 2,187,441 118,736

Total comprehensive income for the year

consist of:

Realised amount (4,656,776) 1,215,531

Unrealised amount 6,844,217 (1,096,795)

2,187,441 118,736

The notes on pages 42 to 62 are an integral part of these financial statements.

40

BIMB Dana Al-Munsif

6.3 Statement of Changes in Net Asset Value for the financial year ended 31 August

2017

Unitholders’

capital

Accumulated

losses Total

RM RM RM

As at 1 September 2015 42,277,784 (5,758,282) 36,519,502

Creation of units via cash 174,465 - 174,465

Reinvestment of distributions 923,633 - 923,633

Cancellation of units (5,483,809) - (5,483,809)

Distributions - (941,601) (941,601)

Total attributable to unitholders (4,385,711) (941,601) (5,327,312)

Total comprehensive income for

the year - 118,736 118,736

As at 31 August 2016/

1 September 2016

37,892,073

(6,581,147)

31,310,926

Creation of units via cash 344,706 - 344,706

Cancellation of units (15,878,363) - (15,878,363)

Distributions - - -

Total attributable to unitholders (15,533,657) - (15,533,657)

Total comprehensive income for

the year - 2,187,441 2,187,441

As at 31 August 2017 22,358,416 (4,393,706) 17,964,710

The notes on pages 42 to 62 are an integral part of these financial statements.

41

BIMB Dana Al-Munsif

6.4 Statement of Cash Flows for the financial year ended 31 August 2017

2017 2016

RM RM

Cash flows from operating activities

Proceeds from sale of quoted investments 29,753,658 29,412,328

Purchase of quoted investments (19,494,600) (40,100,735)

Purchase of Islamic debt securities - (1,527,900)

Maturity of Islamic debt securities 5,542,900 4,500,000

Dividend received 363,346 502,146

Income from Islamic debt securities and short

term investments

430,971

696,570

Management fee paid (366,360) (519,747)

Trustee fee paid (19,539) (27,712)

Audit fee paid (22,000) -

Tax agent fee paid (4,500) -

Payment for administrative expenses (47,686) (57,369)

Cash generated from/(used in) operations 16,136,190 (7,122,419)

Tax refund 10,570 -

Net cash generated from/(used in) operating

activities 16,146,760 (7,122,419)

Cash flows from financing activities

Cash receipt for creation of units 345,092 273,134

Cash payment for cancellation of units (16,003,670) (5,448,516)

Payment of distributions (17,968) -

Net cash used in financing activities (15,676,546) (5,175,382)

Net increase/(decrease) in cash and cash

equivalents 470,214 (12,297,801)

Cash and cash equivalents at 1 September 2,944,389 15,242,190

Cash and cash equivalents at 31 August 3,414,603 2,944,389

Cash and cash equivalents comprise:

Cash at bank 324,465 297,797

Short term placements 3,090,138 2,646,592

3,414,603 2,944,389

The notes on pages 42 to 62 are an integral part of these financial statements.

42

BIMB Dana Al-Munsif

6.5 Notes to the Financial Statements

1. Information on the Fund

BIMB Dana Al-Munsif (hereinafter referred to as “the Fund”) was constituted pursuant

to the execution of a Deed dated 6 December 2001 between the Manager - BIMB

Investment Management Berhad, the Trustee and the registered unitholders of the

Fund. Effective from 5 September 2017 the trustee has been changed from Affin

Hwang Trustee Berhad to SCBMB Trustee Berhad.

The principal activity of the Fund is to invest in authorised investments as defined in

the Deed, which include stocks and shares of companies quoted on Bursa Malaysia,

short term deposits and Islamic debt securities.

The Manager, BIMB Investment Management Berhad, a company incorporated in

Malaysia, is a subsidiary of Bank Islam Malaysia Berhad.

The financial statements were approved by the Board of Directors of the Manager on

26 October 2017.

2. Basis of preparation

(a) Statement of compliance

The financial statements of the Fund have been prepared in accordance with

Malaysian Financial Reporting Standards (“MFRS”), International Financial

Reporting Standards (“IFRS”), the Deed and Securities Commission‟s Guidelines

on Unit Trust Funds (“Guidelines”) in Malaysia.

The following are accounting standards, amendments and interpretations that

have been issued by the Malaysian Accounting Standards Board (“MASB”) but

have not been adopted by the Fund:

MFRSs, Interpretations and amendments effective for annual periods

beginning on or after 1 January 2017

Amendments to MFRS 12, Disclosure of Interests in Other Entities (Annual

Improvements to MFRS Standards 2014-2016 Cycle)

Amendments to MFRS 107, Statement of Cash Flows – Disclosure Initiative

Amendments to MFRS 112, Income Taxes – Recognition of Deferred Tax

Assets for Unrealised Losses

43

2. Basis of preparation (continued)

(a) Statement of compliance (continued)

MFRSs, Interpretations and amendments effective for annual periods

beginning on or after 1 January 2018

MFRS 9, Financial Instruments (2014)

MFRS 15, Revenue from Contracts with Customers

Clarifications to MFRS 15, Revenue from Contracts with Customers

IC Interpretation 22, Foreign Currency Transactions and Advance

Consideration

Amendments to MFRS 1, First-time Adoption of Malaysian Financial Reporting

Standards (Annual Improvements to MFRS Standards 2014-2016 Cycle)

Amendments to MFRS 2, Share-based Payment – Classification and

Measurement of Share-based Payment Transactions

Amendments to MFRS 4, Insurance Contracts – Applying MFRS 9 Financial

Instruments with MFRS 4 Insurance Contracts

Amendments to MFRS 128, Investments in Associates and Joint Ventures

(Annual Improvements to MFRS Standards 2014-2016 Cycle)

Amendments to MFRS 140, Investment Property – Transfers of Investment

Property

MFRSs, Interpretations and amendments effective for annual periods

beginning on or after 1 January 2019

MFRS 16, Leases

IC Interpretation 23, Uncertainty over Income Tax Treatments

MFRSs, Interpretations and amendments effective for annual periods

beginning on or after 1 January 2021

MFRS 17, Insurance Contracts

MFRSs, Interpretations and amendments effective for a date yet to be

confirmed

Amendments to MFRS 10, Consolidated Financial Statements and MFRS 128,

Investments in Associates and Joint Ventures – Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture

The Fund plans to apply the abovementioned accounting standards,

amendments and interpretations, where applicable:

from the annual period beginning on 1 September 2017 for those amendments

that are effective for annual periods beginning on or after 1 January 2017;

from the annual period beginning on 1 September 2018 for those accounting

standards, amendments and interpretation that are effective for annual periods

beginning on or after 1 January 2018;

44

2. Basis of preparation (continued)

(a) Statement of compliance (continued)

from the annual period beginning on 1 September 2019 for the accounting

standard that is effective for annual periods beginning on or after 1 January

2019.

from the annual period beginning on 1 September 2021 for the accounting

standard that is effective for annual periods beginning on or after 1 January

2021.

The initial application of the accounting standards, amendments or

interpretations are not expected to have any material financial impacts to the

current year and prior year financial statements of the Fund, except as

mentioned below:

(i) MFRS 9, Financial Instruments

MFRS 9 replaces the guidance in MFRS 139, Financial Instruments:

Recognition and Measurement on the classification and measurement of

financial assets and financial liabilities, and on hedge accounting.The Fund

is currently assessing the financial impact that may arise from the adoption

of MFRS 9.

(b) Basis of measurement

The financial statements are prepared on the historical cost basis except as

disclosed in Note 3(a)(ii).

(c) Functional and presentation currency

These financial statements are presented in Ringgit Malaysia (“RM”), which is the

Fund‟s functional currency.

(d) Use of estimates and judgements

The preparation of financial statements in conformity with MFRSs requires

management to make judgements, estimates and assumptions that affect the

application of accounting policies and the reported amounts of assets, liabilities,

income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis.

Revisions to accounting estimates are recognised in the period in which the

estimate is revised and in any future years affected.

There are no significant areas of estimation uncertainty and critical judgements in

applying accounting policies that have significant effect on the amounts

recognised in the financial statements.

45

3. Significant accounting policies

The accounting policies set out below have been applied consistently to the periods

presented in these financial statements, unless otherwise stated.

(a) Financial instruments

(i) Initial recognition and measurement

A financial instrument is recognised in the statement of financial position

when, and only when, the Fund becomes a party to the contractual

provisions of the instrument.

A financial instrument is recognised initially, at its fair value plus, in the case

of a financial instrument not at fair value through profit or loss, transaction

costs that are directly attributable to the acquisition or issue of the financial

instrument.

(ii) Financial instrument categories and subsequent measurement

The Fund categorises financial instruments as follows:

Financial assets

(a) Financial assets at fair value through profit or loss

Fair value through profit or loss category comprises financial assets

that are held for trading, or financial assets that are specifically

designated into this category upon initial recognition. These include

Islamic debt securities.

Financial assets categorised as fair value through profit or loss are

subsequently measured at their fair values with the gain or loss

recognised in the statement of profit or loss.

(b) Financing and receivables

Financing and receivables category are debt instruments that are

not quoted in an active market and these comprises amount due

from Managers, other receivables, cash and cash equivalents and

short term investments.

Financial assets categorised as financing and receivables are

subsequently measured at amortised cost using the effective profit

method.

All financial assets except for those measured at fair value through profit or

loss, are subject to review for impairment, see Note 3(e).

46

3. Significant accounting policies (continued)

(a) Financial instruments (continued)

(ii) Financial instrument categories and subsequent measurement

(continued)

Financial liabilities

All financial liabilities are subsequently measured at amortised cost.

Financial liabilities measured at amortised cost comprises amount due to

Manager and other payables.

(iii) Derecognition

A financial asset or part of it is derecognised when, and only when the

contractual rights to the cash flows from the financial asset expire or the

financial asset is transferred to another party without retaining control or

substantially all risks and rewards of the asset. On derecognition of a

financial asset, the difference between the carrying amount and the sum of

the consideration received (including any new asset obtained less any new

liability assumed) and any cumulative gain or loss that had been recognised

in equity is recognised in profit or loss.

A financial liability or a part of it is derecognised when, and only when, the

obligation specified in the contract is discharged or cancelled or expires. On

derecognition of a financial liability, the difference between the carrying

amount of the financial liability extinguished or transferred to another party

and the consideration paid, including any non-cash assets transferred or

liabilities assumed, is recognised in profit or loss.

(b) Income recognition

(i) Dividend income

Dividend income is recognised in profit or loss on the date that the Fund‟s

right to receive payment is established, which in the case of quoted shares

is the entitlement date.

(ii) Income from short term investments and Islamic debt securities

Income from short term investments and Islamic debt securities are

recognised as it accrues, using the effective profit method in profit or loss.

47

3. Significant accounting policies (continued)

(b) Income recognition

(iii) Gain on sale of investments

The realised gain on sale of investments is measured as the difference

between the net disposal proceeds and the carrying amount of the

investments. The carrying amount for determining the realised gain on sale

of investments is based on the weighted average cost method and where

applicable adjusted for accretion for discount and amortisation of premium.

(c) Islamic debt securities

Islamic debt securities are investments in sukuk which are held for trading. It is

categorised as fair value through profit or loss and subsequently measured at

their fair values with the gain or loss recognised in profit or loss.

(d) Cash and cash equivalents

Cash and cash equivalents consist of cash at bank and short term placement

with licensed financial institutions which have insignificant risk of changes in fair

value with original maturities of less than 30 days, and are used by the Fund in

the management of its short term commitments.

Cash and cash equivalents are categorised and measured as financing and

receivables in accordance with policy Note 3(a)(ii)(b).

(e) Impairment

Financial assets

All financial assets (except for financial assets categorised as fair value through

profit or loss) are assessed at each reporting date whether there is any objective

evidence of impairment as a result of one or more events having an impact on

the estimated future cash flows of the asset. Losses expected as a result of

future events, no matter how likely, are not recognised.

An impairment loss in respect of financing and receivables is recognised in profit

or loss and is measured as the difference between the asset‟s carrying amount

and the present value of estimated future cash flows discounted at the asset‟s

original effective profit rate. The carrying amount of the asset is reduced through

the use of an allowance account.

48

3. Significant accounting policies (continued)

(f) Income tax

Income tax expense comprises current tax. Current tax is recognised in profit or

loss except to the extent that it relates to items recognised directly in equity or

other comprehensive income.

Current tax is the expected tax payable or receivable on the taxable income for

the year, using tax rates enacted or substantively enacted at the statement of

financial position date, and any adjustment to tax payable in respect of previous

years.

(g) Unitholders’ capital

The Fund issues cancellable units, which are cancelled at the unitholder‟s option

and are classified as equity. Cancellable units can be put back to the Fund at any

time for cash equal to a proportionate share of the Fund‟s net asset value. The

outstanding units is carried at the redemption amount that is payable at the

financial position date if the holder exercises the right to put the unit back to the

Fund.

Units are created and cancelled at the unitholders‟ option at prices based on the

Fund‟s net asset value per unit at the time of creation or cancellation. The Fund‟s

net asset value per unit is calculated by dividing the net asset attributable to

unitholders with the total number of outstanding units. In accordance with the

Securities Commission‟s Guidelines on Unit Trust Funds in Malaysia, investment

positions are valued based on the last traded market price for the purpose of

determining the net asset value per unit for creations and cancellations.

The units in the Fund are puttable instruments, classified as equity, which entitle

the unitholders to a pro-rata share of the net asset of the Fund. The units are

subordinated and have identical features. There is no contractual obligation to

deliver cash or another financial assets other than the obligation on the Fund to

repurchase the units. The total expected cash flows from the units are based on

the change in the net asset of the Fund.

(h) Distribution

Distribution is at the discretion of the Fund. A distribution to the Fund‟s

unitholders is accounted for as a deduction from realised reserves. A proposed

distribution is recognised as a liability or equity in the year in which they are

declared.

49