Embed Size (px)

Citation preview

1

FINANCIAL STATEMENTS 2013

BUILDING THE BIGGER PICTURE

2

CONTENTS

FINANCIAL STATEMENTS 2013

Report of the Board of Directors 3 Consolidated income statement and consolidated statement of comprehensive income (IFRS) 8Consolidated balance sheet (IFRS) 9Consolidated cash flow statement (IFRS) 10Consolidated statement of changes in equity 11 1. Accounting principles 12 2. Business operations sold 20 3. Revenue 20 4. Long-term projects 20 5. Material and services 20 6. Other operating income and expenses 20 7. Depreciations 20 8. Impairments 20 9. Employee benefits 21 10. Research and development expenses 21 11. Financial income and expenses 21 12. Income taxes 21 13. Discontinued operations 22 14. Earning per share 22 15. Tangible assets 23 16. Goodwill 23 17. Impairment tests 24 18. Other intaglible assets 25 19. Available receivables and other receivables 25 20. Inventories 26 21. Account receivables and other receivables 26 22. Cash and cash equivalents 26 23. Deferred tax assets and liabilities 27 24. Equity 28 25. Financial liabilities 29 26. Account payable and other liabilities 30 27. Pension obligations 30 28. Provisions 31 29. Financial risk management 32 30. Other lease agreement 35 31. Conditional liabilities and assets 35 32. Insiders 35 33. Events after the end of the reporting

period 35

Group´s key figures 36Parent company income statement (FAS) 37Parent company balance sheet (FAS) 38Parent company cash flow statement (FAS) 40Notes to financial statements, Parent company Destia Ltd. (FAS) 41Notes to income statement, Parent company Destia Ltd. (FAS) 41Board of Director’s proposal on the use of distributable assets 47Auditor’s report 48Consolidated income statement, quarterly figures 49Consolidated balance sheet, quarterly figures 50Consolidated cash flow statement, quarterly figures 51

3

REPORT OF TH E BOARD OF D I R E CTO R S

Operating environment

Uncertainty in the economy continued during 2013, which had a negative effect on the economic operating environment in infrastructure construction and on the availability of financing for projects. A slight decline in the infrastructure construction market during the year under review was due to a slowdown in house-building construction. Public infrastructure investments remained stable, while private infrastructure investments de-creased. Numerous new road development projects were put out to tender in 2013. In the next few years too, public sector project programmes will offer major projects, which will generate a base level of demand for the infrastructure construction sector, despite a decline in the market as a whole. The slowdown of the entire construction market can especially be seen in a lower demand for aggregates. The rather low amount of work currently available in infrastructure planning is cause for longer term concern.

According to a joint economic forecast made by the Tampere University of Applied Sciences and VTT Technical Research Centre of Finland, infrastructure construction and maintenance shrank 3.5 per cent in 2013. The municipal market was sluggish in the year ended, even though there were signs of life in growth municipalities, especially in the Greater Helsinki area. Competi-tion for projects increased.

The economic conditions of the civil engineering sector were affected by the general economic development, the public sector financial deficit, the level of costs that has remained high, and the decline in house-building construction.

According to an economic report by the Finnish Ministry of Finance, civil engineering production is contracting in 2013 for the fifth consecutive year, but more gently than before. Last year the decline was 6.8 per cent and this year it is expected to be 3.2 per cent.

Civil engineering sector costs rose 0.8 per cent from December 2012 to December 2013. According to Statistics Finland, the annual change in costs varied by sub- index, from -2.1 per cent in surfacings to 2.8 per cent in rock structures.

IFRS financial statements

Since 2011, the consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS). The 2013 interim reports with reference data have been prepared in accordance with IFRS regulations. Prior to this, the Group's financial reporting was based on the Finnish Accounting Standards (FAS). The Group adopted the IFRS on 1 January 2010.

The effect of the closure of business operations in Norway is presented under Discontinued operations.

Business development

In the 1 January–31 December 2013 accounting period, the op-erations of the Destia Group (hereinafter Destia) consisted of four regional and two operational business units. The regional business units providing infrastructure construction and maintenance servic-es are Southern Finland, Western Finland, Eastern Finland and Northern Finland. Their business includes the construction and maintenance of traffic routes, industrial and traffic environments and the complete living environment, as well as the services of the winter maintenance management centre, Kelikeskus. The Special

Construction business unit is responsible for railway construction and railway infrastructure maintenance, rock and mining construc-tion, aggregates services as well as the Group's own fleet service. Destia's other operational business unit, Consulting Services, takes care of design, surveying and international consultation.

During the accounting period, Destia's revenue from continuing operations amounted to EUR 489.7 million (EUR 507.3, 2012) and EUR 143.3 million (134.6) in the fourth quarter. The im-proved fourth quarter revenue over the previous year was due to favourable weather conditions. The annual revenue for continuing operations fell 3.5 per cent from the previous year. This drop in revenue was due not only to an overall slowdown in the market, but also a failure to win tenders for several major projects.

Key orders received during the year, and the order book

Destia's order book at year-end, EUR 593.0 million (600.8), was 1.3 per cent less than the previous year. In a tightened market sit-uation, the company's tendering activities had a negative impact on order book development.

In the fourth quarter of 2013, Destia won a significant track con-tract, which supports the company’s objectives of growing on the track maintenance and construction markets. The Maintenance Area 5 track and safety equipment maintenance contract put out to tender by the Finnish Transport Agency covers the period 2014−2019 plus two optional years. The maintenance area includes track sections from Haapamäki to Orivesi, Jyväskylä, Vaasa and Kaskinen, as well as from Jyväskylä to Äänekoski.

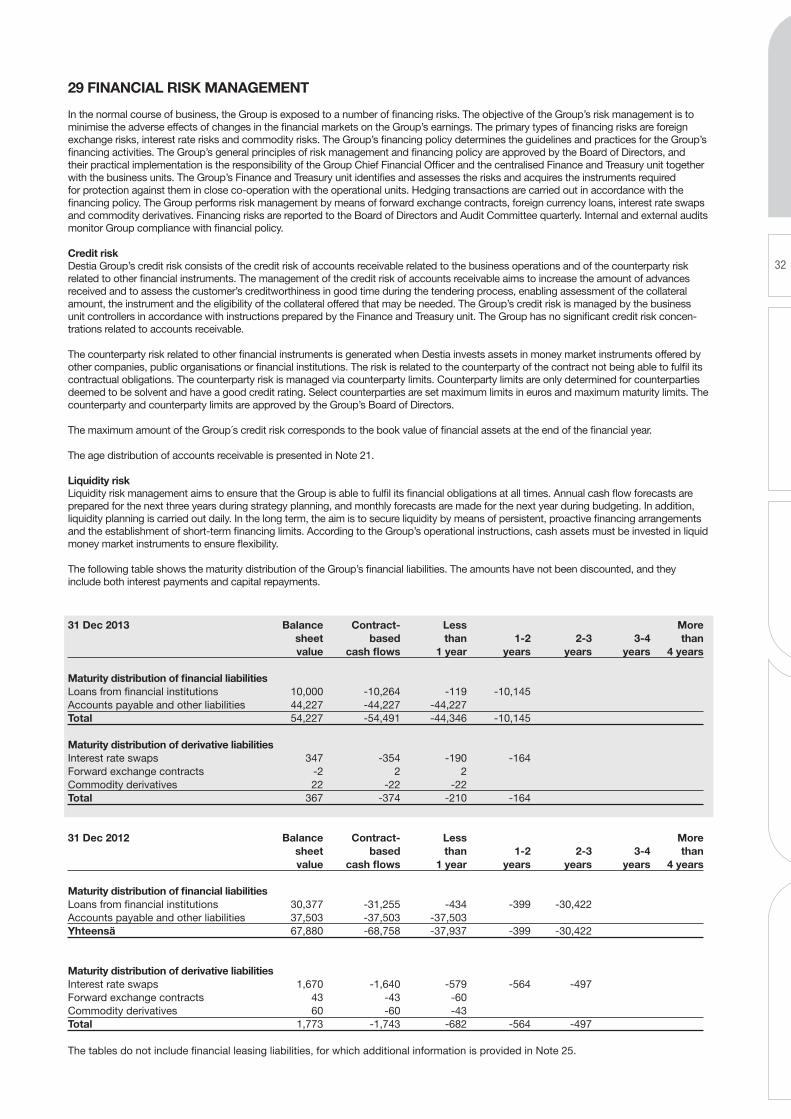

In the fourth quarter, Destia signed agreements with the munic-ipality of Kempele for the 2014 delivery of aggregates, with the City of Pori for renovation of the Pori Bridge, and with the Finnish Transport Agency for project management of the 2014 InfraTee-ma project.

During the accounting period, Destia won the construction contract put out to tender by Länsimetro for the tunnel section between Keilaniemi and Lauttasaari. The contract includes construction and structural engineering work of the metro tunnel over a 4 km distance between Keilaniemi and Lauttasaari. Work on the contract began in early March 2013 and is expected to be completed in September 2014.

Destia won the contract put out to tender by the Finnish Transport Agency for the construction of a double track in the Riippa−Eskola track section. The contract entails the renovation of old track and the construction of new track over a 30-km distance. The contract also includes the construction of new linesides, bridges, service and private roads as well as the conversion of the track’s elec-trification system to conform to double-track requirements. The contract is expected to be completed in November 2016.

In 2013, Destia won and carried out the maintenance contract for bridges put out to tender by the Uusimaa Centre for Economic De-velopment, Transport and the Environment (ELY Centre). The contract included the repair of 21 bridges, primarily in the Greater Helsinki area. The contracted work will be completed by the end of the year.

Destia implements the contract for the first stage of the construction of streets, municipal engineering and blocks in the Lakari industrial and logistics area to be built in Rauma. The contract started in Feb-ruary 2013, and is expected to be completed in spring 2014.

In public tendering for regional main road maintenance contracts in 2013, Destia won seven out of 12. The Huittinen, Jämsä, Pu-

4

dasjärvi−Taivalkoski, Vaasa, Suomussalmi and Paimio contracts won are five years in duration, and the Nurmes contract is seven years. All in all, Destia maintained its good market position in the regional maintenance of main roads.

Destia signed contracts with the Centres for Economic Develop-ment, Transport and the Environment in Northern Ostrobothnia, Lapland and North Savo to transfer the Kuusamo, Ivalo and Pieksämäki regional main road maintenance contracts to Destia’s responsibility in the middle of the maintenance period. All three regional contracts are one year in duration.

Destia signed a contract with the City of Joensuu for Joensuu’s southern regional contract. This contract will last until the end of September 2016.

Destia won the contract put out to tender by the Central Finland Centre for Economic Development, Transport and the Environment for the upgrading of National Road 56 between Jämsä and Mänttä. The planned completion of the contract is in December 2014.

Destia’s Consulting Services is involved in a consortium that won the project put out to tender by the Finnish Transport Agency that includes ground surveys of Pisararata.

Destia signed a contract with the Finnish Transport Agency for the service level measurements of surfaced roads during 2014−2019.

Destia also won the Technopark II parking project in Lappeenran-ta, which is scheduled for completion in June 2014.

Destia signed a contract for the first stage of the Kivikontie interchange put out to tender by the City of Helsinki, which will be completed in September 2014. A contract was also signed for track renewal between Myllymäki and Tuuri put out to tender by the Finnish Transport Agency, which will be completed in July 2014.

Contracts put out to tender by the Port of Oulu, for the second phase of its West Quay construction project, which started at the end of August and will be completed at the end of 2014, and by the Northern Ostrobothnia ELY Centre, for light traffic arrange-ments on National Road 27 in Ylivieska, were also signed. The planned completion of the contract is in September 2014.

The E18 Koskenkylä−Kotka life-cycle project, which was ongoing in 2013, has proceeded according to plan. The Main Road 51 Kiven-lahti–Kirkkonummi improvement project was completed in October 2013. The project will continue with the maintenance of surfacings, road structures and bridge structures for a period of 15 years.

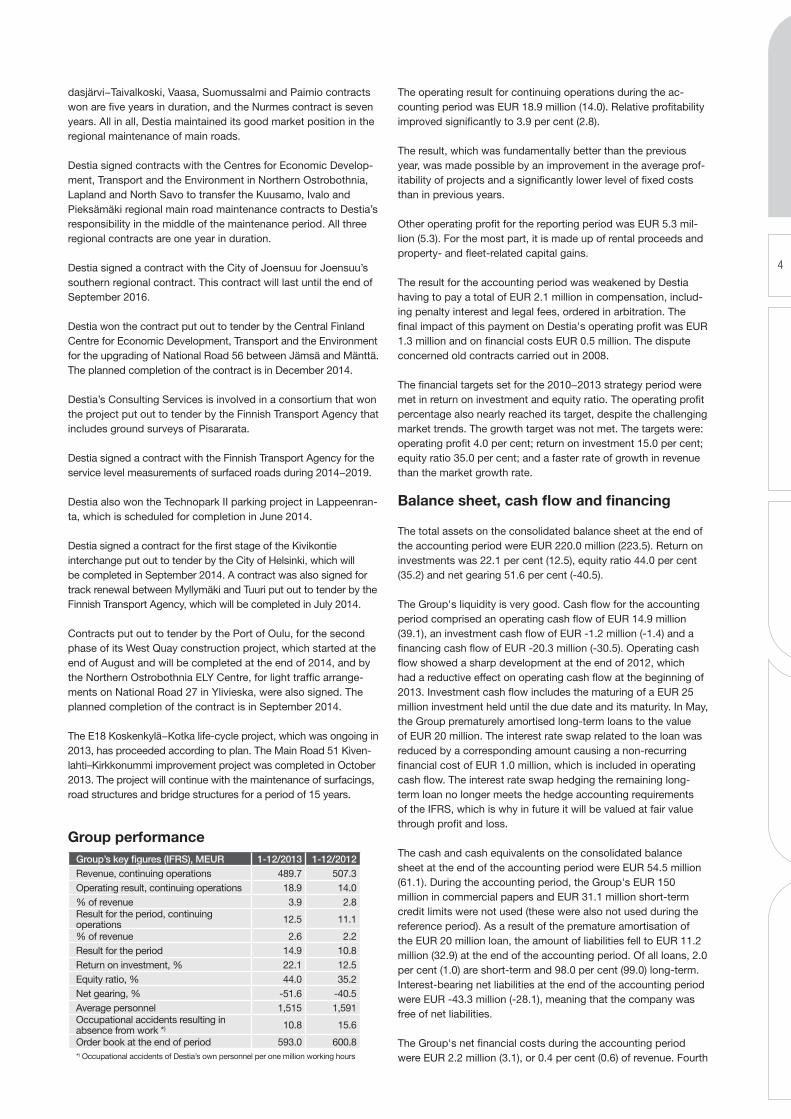

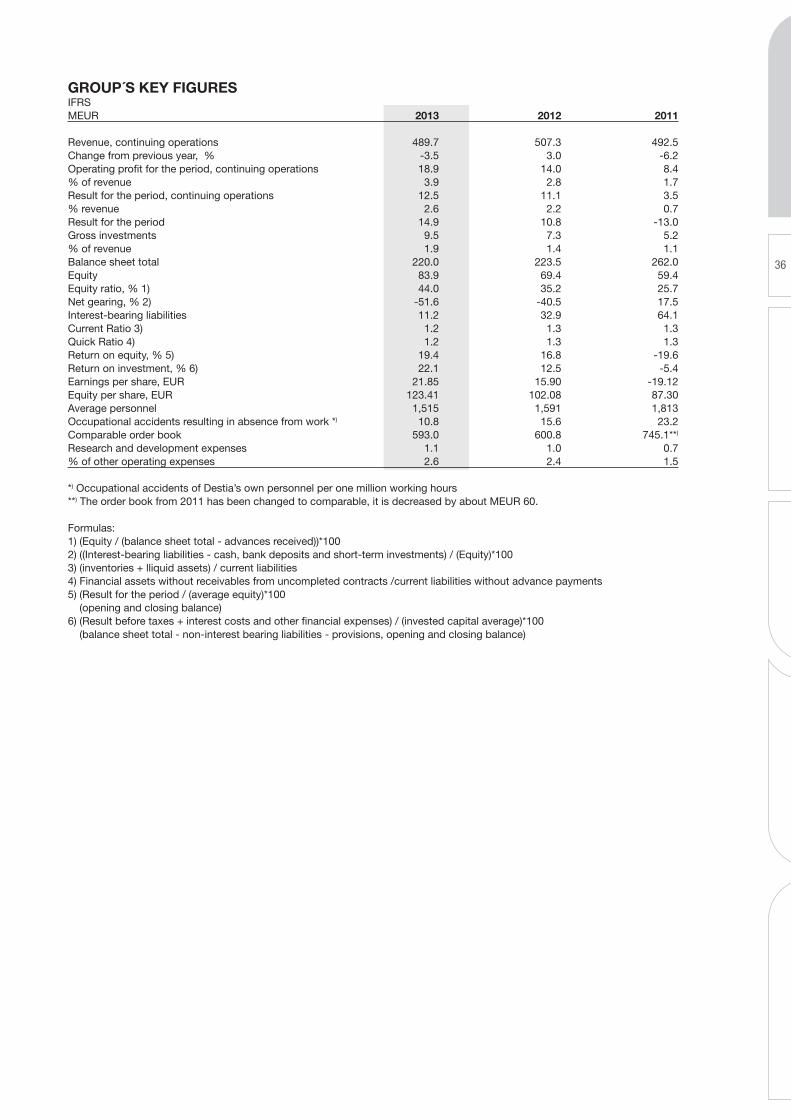

Group performanceGroup’s key figures (IFRS), MEUR 1-12/2013 1-12/2012Revenue, continuing operations 489.7 507.3Operating result, continuing operations 18.9 14.0% of revenue 3.9 2.8Result for the period, continuing operations 12.5 11.1

% of revenue 2.6 2.2Result for the period 14.9 10.8Return on investment, % 22.1 12.5Equity ratio, % 44.0 35.2Net gearing, % -51.6 -40.5Average personnel 1,515 1,591Occupational accidents resulting in absence from work *) 10.8 15.6

Order book at the end of period 593.0 600.8*) Occupational accidents of Destia’s own personnel per one million working hours

The operating result for continuing operations during the ac-counting period was EUR 18.9 million (14.0). Relative profitability improved significantly to 3.9 per cent (2.8).

The result, which was fundamentally better than the previous year, was made possible by an improvement in the average prof-itability of projects and a significantly lower level of fixed costs than in previous years.

Other operating profit for the reporting period was EUR 5.3 mil-lion (5.3). For the most part, it is made up of rental proceeds and property- and fleet-related capital gains.

The result for the accounting period was weakened by Destia having to pay a total of EUR 2.1 million in compensation, includ-ing penalty interest and legal fees, ordered in arbitration. The final impact of this payment on Destia's operating profit was EUR 1.3 million and on financial costs EUR 0.5 million. The dispute concerned old contracts carried out in 2008.

The financial targets set for the 2010−2013 strategy period were met in return on investment and equity ratio. The operating profit percentage also nearly reached its target, despite the challenging market trends. The growth target was not met. The targets were: operating profit 4.0 per cent; return on investment 15.0 per cent; equity ratio 35.0 per cent; and a faster rate of growth in revenue than the market growth rate.

Balance sheet, cash flow and financing

The total assets on the consolidated balance sheet at the end of the accounting period were EUR 220.0 million (223.5). Return on investments was 22.1 per cent (12.5), equity ratio 44.0 per cent (35.2) and net gearing 51.6 per cent (-40.5).

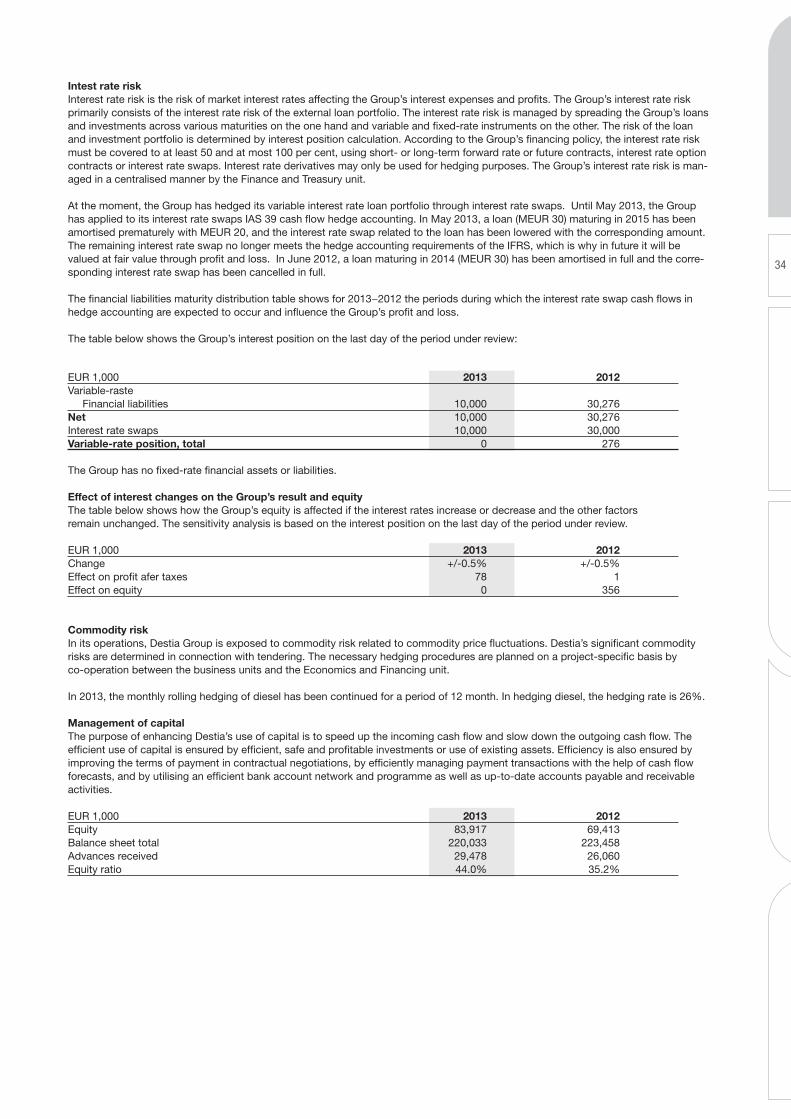

The Group's liquidity is very good. Cash flow for the accounting period comprised an operating cash flow of EUR 14.9 million (39.1), an investment cash flow of EUR -1.2 million (-1.4) and a financing cash flow of EUR -20.3 million (-30.5). Operating cash flow showed a sharp development at the end of 2012, which had a reductive effect on operating cash flow at the beginning of 2013. Investment cash flow includes the maturing of a EUR 25 million investment held until the due date and its maturity. In May, the Group prematurely amortised long-term loans to the value of EUR 20 million. The interest rate swap related to the loan was reduced by a corresponding amount causing a non-recurring financial cost of EUR 1.0 million, which is included in operating cash flow. The interest rate swap hedging the remaining long-term loan no longer meets the hedge accounting requirements of the IFRS, which is why in future it will be valued at fair value through profit and loss.

The cash and cash equivalents on the consolidated balance sheet at the end of the accounting period were EUR 54.5 million (61.1). During the accounting period, the Group's EUR 150 million in commercial papers and EUR 31.1 million short-term credit limits were not used (these were also not used during the reference period). As a result of the premature amortisation of the EUR 20 million loan, the amount of liabilities fell to EUR 11.2 million (32.9) at the end of the accounting period. Of all loans, 2.0 per cent (1.0) are short-term and 98.0 per cent (99.0) long-term. Interest-bearing net liabilities at the end of the accounting period were EUR -43.3 million (-28.1), meaning that the company was free of net liabilities.

The Group's net financial costs during the accounting period were EUR 2.2 million (3.1), or 0.4 per cent (0.6) of revenue. Fourth

5

quarter financial costs were increased by the EUR 0.5 million in penalty interest that Destia was ordered to pay in arbitration. A reduction in financial costs was primarily due to the low amount of interest-bearing net liabilities. Non-recurring items increased the net financial items by a total of EUR 1.5 million dur-ing the accounting period. Income taxes in the reporting period amounted to EUR 4.2 million (in the reference period, EUR 0.2 million negative).

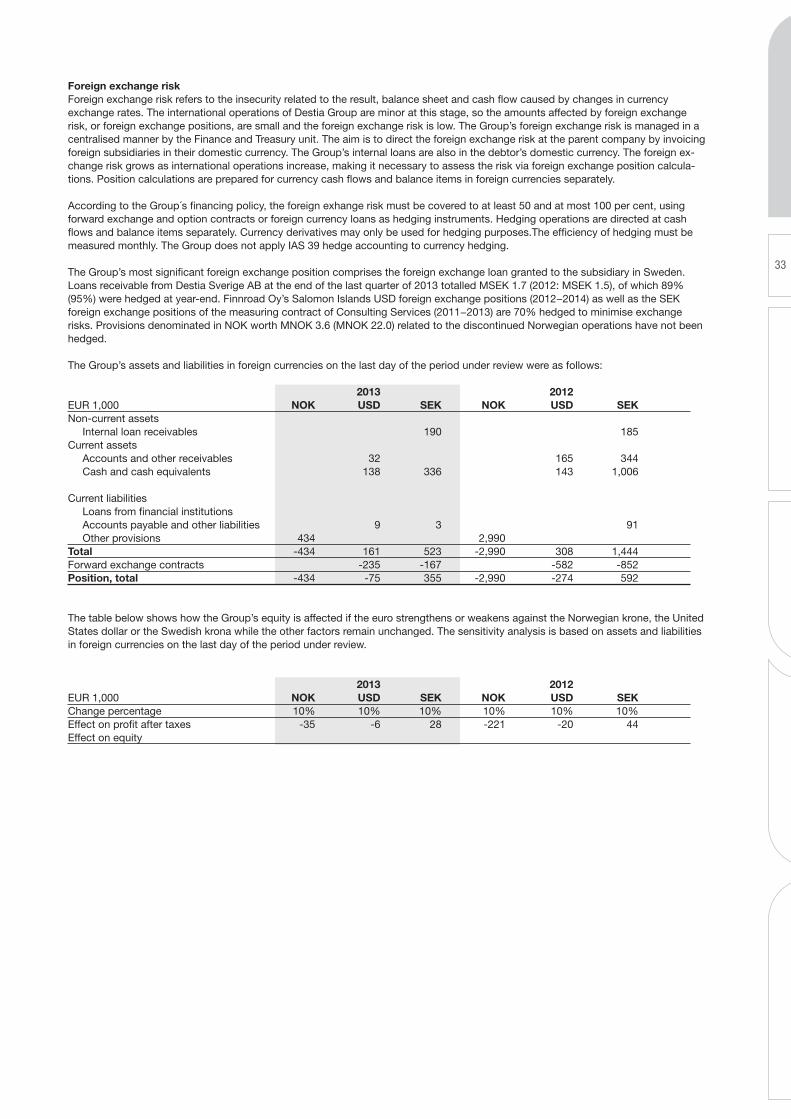

Protection against currency, commodity and interest risks has been organised in accordance with the Group’s treasury policy

Shares and share capital

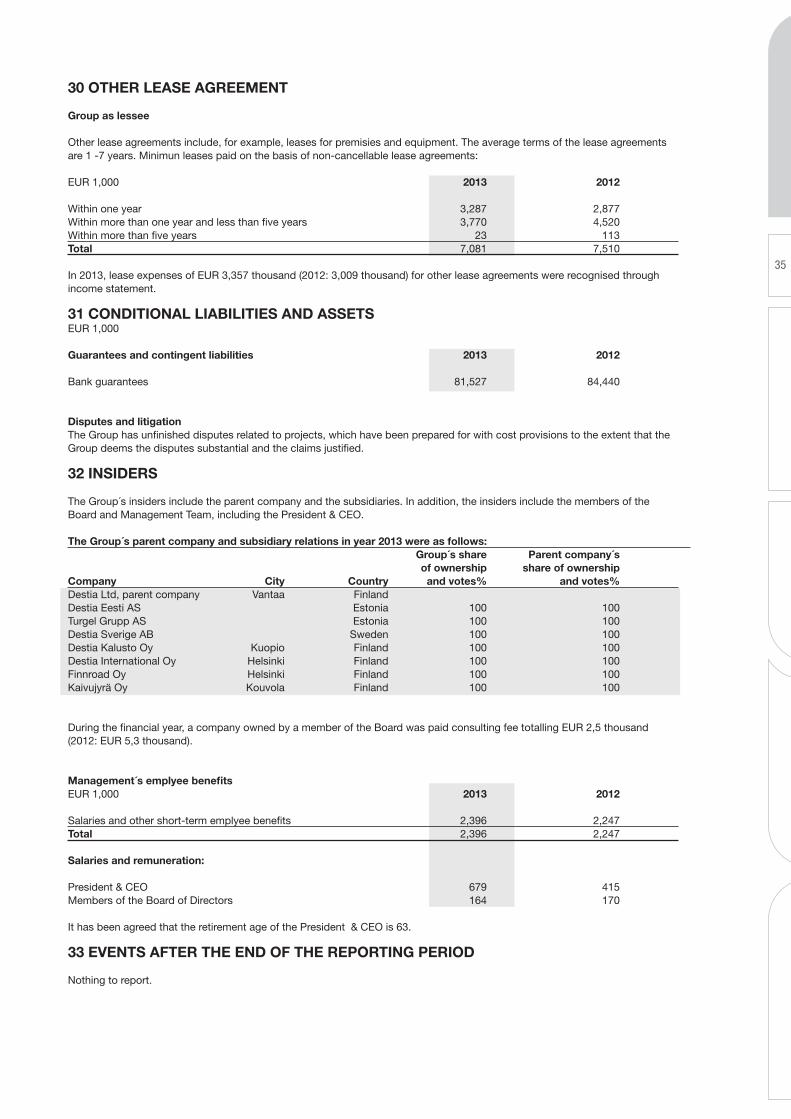

The registered share capital of Destia Ltd is EUR 17.0 million and its total number of shares is 680,000. The company is owned 100 per cent by the State of Finland.

Investments and divestments

During the reporting period, gross investments made totalled EUR 9.5 million (7.3), or 1.9 per cent (1.4) of revenue. Investments were mainly targeted at the fleet, but also at data systems and holiday timeshares for the recreational use of personnel.

Annual General Meeting 2013 and administration

Destia Ltd’s Annual General Meeting held on 18 March 2013 confirmed the company’s financial statements for 2012 and discharged the members of the Board of Directors and the President & CEO from liability for the accounting period 1 Janu-ary–31 December 2012. The Annual General Meeting decided, as proposed by the Board of Directors, that no dividends be paid for the accounting period ending 31 December 2012.

The Annual General Meeting ratified the total number of members in the Board of Directors as five and reappointed Karri Kaitue as the Chairman of the Board of Directors. Kalevi Alestalo, Elina Engman, Matti Mantere and Solveig Törnroos-Huhtamäki were re-elected as members of the Board of Directors.

The Annual General Meeting elected Deloitte & Touche Ltd (Au-thorised Public Accountants) as Destia Oy’s auditor for the 2013 accounting period, with Aleksi Martamo (APA) as the auditor with principal responsibility.

At its organising meeting, the Board reappointed Matti Mantere as Vice Chairperson.

Two committees were appointed to support the work of the Board: a Nomination and Compensation Committee, and an Audit Committee. In accordance with Destia’s administration and management system, the Chairman of the Board, Karri Kaitue, will continue as the Chairperson of the Nomination and Com-pensation Committee. Kalevi Alestalo and Elina Engman were elected as the Committee's members. Matti Mantere was elected as the Chairperson of the Audit Committee, with Kalevi Alestalo and Solveig Törnroos-Huhtamäki as members.

The Annual General Meeting decided to keep the compensations of the Board members unchanged: monthly compensation for the Board’s Chairperson was EUR 3,300. The monthly compensation for the Vice Chairperson was EUR 1,800, and the other members of the Board each received EUR 1,500 as monthly compensa-tion. In addition to the monthly compensation, all members of

the Board were paid EUR 600 each as a participation fee for every Board and committee meeting. Travel costs are remitted in accordance with Destia’s travel regulations.

Management and personnel

At the beginning of 2013, Destia streamlined the work of its management team in order to enhance the control of customer work and to meet rapid changes in the market situation. The Group Management Team comprises President & CEO Hannu Leinonen, CFO Pirkko Salminen, and Executive Vice Presi-dents Minna Heinonen, Pasi Kailasalo, Jouni Karjalainen, Jukka Raudasoja, Marko Vasenius and Seppo Ylitapio, and personnel representative Kimmo Laaksola. In addition, Extended Manage-ment Team was established to prepare and guide development projects and strategy concerning the entire Group and to develop the management system. In addition to the persons mentioned above, the Extended Management Team also includes Senior Vice Presidents Laura Ahokas, Miia Apukka, Aki Markkola and Tom Schmidt.

The Group’s average number of personnel during the reporting period was 1,515 (1,591). At the end of December, the number of personnel was 1,465 (1,502), 1,375 (1,417) of which were perma-nent staff and 90 (85) temporary employees. Due to the season-ality of the business, the number of personnel varies during the year, peaking in the summer.

Collective labour agreements concerning infrastructure industry employees and salaried staff were signed on 17 November 2011. The contractual period for both agreements is 1 March 2012−31 March 2014.

On 24 June 2013, Destia Ltd concluded redundancy nego-tiations under the Act on Co-operation within Undertakings aimed at reducing the number of employees working in regional maintenance contracts, as a consequence of the results of the tendering of regional contracts. As a result of the negotiations, Destia Ltd made seven drivers redundant. The redundancies were implemented during 2013.

On 14 February 2013, Destia’s Board of Directors decided on a bonus scheme for 2013 covering all personnel. The bonus scheme forms a part of the overall personnel reward scheme. The bonus scheme brings a supportive, in-house co-operation and strategy enhancing control and reward element to compen-sation. The scheme will support and develop the company’s prof-itability and operating conditions. The target group for the new bonus scheme is comprised of three different personnel groups: 1) personnel working on Destia projects; 2) work supervisors; and 3) support function personnel and business unit support person-nel, including management.

On 14 February 2013, the Destia Board of Directors decided on the establishment and implementation of a long-term incentive scheme. The purpose of the scheme is to combine shareholder and management objectives in order to increase the value of the company as well as to get management to commit to the com-pany and offer them a competitive bonus scheme. The scheme features three separate three-year earnings periods, 2013–2015, 2014–2016 and 2015–2017. For each earnings period, the Board of Directors will decide on the earnings criteria, the targets set for them and the persons included in the scheme. The earnings criteria for earnings period 1 January 2013–31 December 2015 is the Group's cumulative 2013−2015 EBITDA adjusted with chang-es in net liabilities. At the Board meeting held on 19 December

6

2013, it was decided that the earnings criteria for earnings period 1 January 2014–31 December 2016 would be, correspondingly, the Group's cumulative 2014-2016 EBITDA adjusted with chang-es in net liabilities. Any bonuses earned during the earnings period 2014–2015 would be paid in money in the spring of 2020. The target group for earnings period 2014–2016 currently con-sists of 15 persons, including business unit and support function heads and the President and CEO. The Board of Directors is also authorised to review the remuneration paid, if needed.

The company’s remuneration schemes correspond to the opinion given on 13 August 2012 by the Cabinet Committee on Econom-ic Policy about compensation paid to company management and key personnel.

In 2013, the Group's staff costs remained on a par with the previous year at EUR 86.9 million (86.5), or 17.7 per cent (17.4) of revenue. Staff costs include the EUR 5.5 million (3.9) in perfor-mance and incentive bonuses for all personnel.

The improvement of safety is a key challenge for the construction field, since it substantially impacts productivity in the field and its attractiveness as an employer. Occupational health and safety are provided for in accordance with a separate occupational health and safety policy. The results of actions taken are meas-ured regularly. In 2013, Destia's personnel accident frequency, i.e. the number of workplace accidents leading to at least one day of absence per one million working hours, was 10.8 (15.6).

In 2013, Destia continued investments in human resources devel-opment. Some 600 Destia employees have taken part in the Tah-To training programme, which supports managerial work and per-formance management. All Destia employees have gone through the TahTo2 training programme. The TahTo2 training programme included the basic elements of performance management as well as occupational safety matters, analysis of the personnel survey results and addressing a discussion model.

Litigation and disputes

In January 2013, the environmental authority made a request to investigate Destia’s Harjula soil area at Mäntsälä. In summer 2012, on its own initiative Destia informed the environmental authority that soil had by mistake been taken from outside the extraction area covered by the valid permit, but from property owned by the company. Destia continues to investigate the mat-ter in co-operation with the environmental authority.

The Supreme Administrative Court rejected Destia’s right to appeal in spring 2013 concerning the excessive taking of soil in Hartola. Therefore, the decision on the matter given in 2011 by the Court of Appeal remains final. The Court of Appeal fined Destia’s two work supervisors for environmental offences and ordered Destia Ltd to pay compensation.

In a decision given by the District Court of Helsinki on 31 May 2013, Destia has won its civil case in which Telasteel Oy de-manded about EUR 1 million in compensation from Destia. The dispute concerned a contract in which Telasteel was a subcon-tractor for Destia. Telasteel has appealed the decision at the Court of Appeal. In Destia’s view, the demand is groundless.

The arbitration proceedings in a dispute between Destia and Rakennusliike Lehto Oy ended in November 2013 to the benefit of Rakennusliike Lehto Oy. The arbitration proceedings con-cerned a subcontracting contract for nine business properties in

2008. Destia was ordered to pay Rakennusliike Lehto Oy EUR 1.5 million in damages for contracts lost as well as legal expenses and penalty interest. Of the compensation, EUR 1.3 million had an impact on Destia’s 2013 operating result and EUR 0.5 million on financial costs. The decision of the arbitration proceedings cannot be appealed.

Short-term risks and uncertainties

In recent years, risk management has been developed at Destia in a variety of manners. The key risk-management guidelines and principles have been compiled in the company’s new risk man-agement policy ratified by the Board of Directors on 28 August 2013.

Destia’s risk management policy describes the main principles, responsibilities and modes of operation of risk management. To implement the policy, more detailed procedures for the various fields of the company's operations have been devised. The risk management policy is based on The Finnish Corporate Govern-ance Code and the international COSO ERM and SFS-ISO 31000 (”Risk management. Principles and Guidelines”) frameworks.

Destia divides risks into market and operating environment risks, operational risks, damage risks, and financial and financing risks.

The fluctuation in the economic operating environment and the uncertainty in the market situation are causing a significant risk for Destia’s business. Although the number of public infrastruc-ture projects has so far remained stable, all in all the amount of infrastructure construction is expected to decline. Public sector investments in infrastructure construction are declining and economic uncertainty has also reduced the willingness of the private sector to invest. The contracting market is reflected in the competitive situation in the sector and, in Destia’s core business areas, the competitive situation is expected to remain fierce. Suc-cess in tendering for regional main road maintenance contracts as well as major contracts is of paramount importance.

In the management of risks caused by the operating environ-ment, it is essential to focus on the selected business areas, and to ensure the operational cost-efficiency, solidity, as well as readiness to react in varying situations.

The most significant operational risks concern project manage-ment and profitability. Uncertainty in terms of project profitability is being created by the potential increase of input prices and the ability to manage project-related risks. The key factors in reaching project targets are active project management from tender calculation to implementation, cost monitoring, ensuring resources and developing project management expertise.

Destia has invested in the reliable financial reporting of essen-tial content, which is a requirement for the identification and assessment of financial risks. The reliability of financial reports is ensured through monitoring and by developing control methods. Risks concerning the financial reporting process are managed through uniform operating methods and by ensuring the reliability of reporting tools used.

Fluctuations in economic conditions may cause considerable changes on financial markets. Destia manages its financial risks in accordance with the company’s treasury policy and hedg-es fundamental risks by derivative contracts. The company’s freedom from net liabilities significantly reduces financial risks. Changes in the prices of oil-based commodities, in particular,

7

cause uncertainty for the profitability of the company. The risk is being prevented by monitoring and assessing the commodity price development, by ensuring key procurements economically from a project perspective, and by hedging the price risks using derivative instruments.

In Destia’s damage risk management, the key factors are proac-tive project management procedures, investments in occupation-al safety and ensuring adequate insurance cover.

Environmental issues

Destia holds the international combined ISO 9001 and 14001 quality and environmental certificate concerning all contracting services, or services for infrastructure construction, infrastructure maintenance consulting, aggregates, and railways. In the ac-counting period, Destia’s operations were conducted in accord-ance with the certification requirements. Operational focus was placed on eco-efficiency, use of natural resources and materials, consumption of fuels and energy, operational environmental safety, and consideration for the areas near locations where Destia operates. Destia’s environmental issues are reported more closely on the company's website.

Research and development

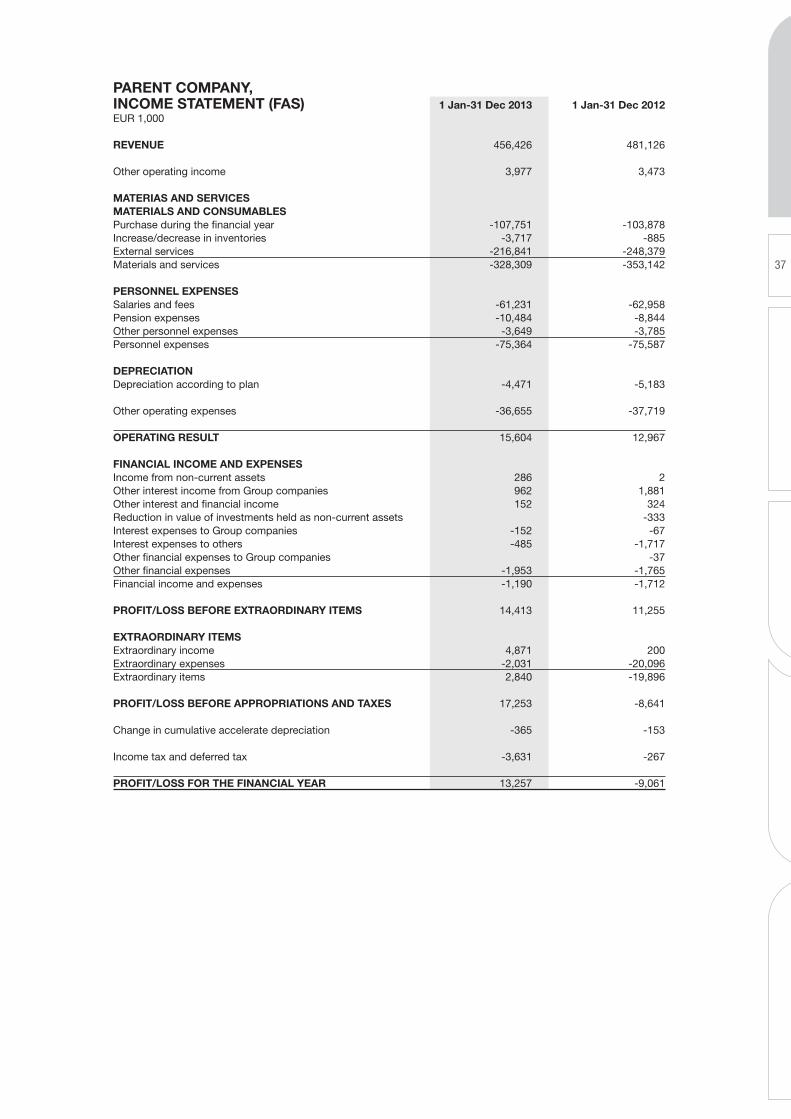

In the accounting period, the focal area in research and devel-opment was the information model-based method expanding around the utilisation of power tool automation, to which mobile data acquisition is also closely linked. A significant part of the development work is included in the field’s RYM Oy PRE research programme. Visibility in the field was especially gained by the model-based quality assurance method and the upgrad-ing of National Road 13, where an accurate initial data model was measured using mobile laser cutting to serve as the basis for model-based planning and implementation. The additional resources targeted at the development of engineering construc-tion have yielded results which can be made use of in service implementation. The renewal of the mobile data acquisition and reporting of infrastructure maintenance services progressed as planned, and the system has been introduced widely in produc-tion. Additionally, several results relating to method and fleet development improving productivity and safety were created. R&D costs totalled some MEUR 1.1 (1.0).

In addition, the company implemented an extensive TahTo train-ing, which supports managerial work and performance man-agement, and a number of significant ICT system development projects were ongoing. The development costs of these activities were MEUR 2.3 (1.9).

Corporate Governance Statement

Destia Ltd’s Corporate Governance Statement will be published separately from this interim report in the company’s 2013 Annual Report on Destia’s website at www.destia.fi.

Events following the reporting period

There have been no major exceptional events after the end of the accounting period.

Strategic direction

On 22 September 2013, the Destia Ltd’s Board of Directors rati-fied the new company strategy for 2014−2022 and the new finan-

cial targets for the 2014−2016 business planning period. The key focus of the strategy is to grow profitably on the infrastructure market through good customer work and by making good use of in-house expertise. Based on this, the Board set the following financial targets for the 2014−2016 business planning period: average growth in revenue of 5 per cent a year, operating profit of 5 per cent by the end of the period, return on investment of more than 15 per cent, and equity ratio of at least 40 per cent.

Destia’s core business are large road projects and infrastructure maintenance requiring special expertise. The focus areas of Destia’s strategic growth in the coming period are in the rock and railways businesses and in energy construction. Destia strongly invests in customer work and the improvement of occupation-al safety. The development of personnel is still the company’s strategic area of focus.

Outlook for 2014

The continuation of economic uncertainty and the tightening of the financial markets in the Eurozone influence the infrastructure market in 2014. With the public infrastructure market remain-ing relatively stable and the level of private sector investments decreasing, the infrastructure market is expected to contract further until 2015. Competition is fierce as the number of major projects decreases and as projects started during previous years are being completed.

Destia’s order book remains at the level of the turn of 2013/2014, with most of it extending till the current year and the next year. The lower than forecast level of the order book and, especially, the poor success in the tendering of major projects in 2013 set a challenge for revenue in 2014. However, the order book together with the measures taken to improve customer work and project management are a good foundation for keeping profitability and cash flow at a good level also in future.

Destia Group’s 2014 revenue and operating profit are expected to remain slightly below the previous year's level.

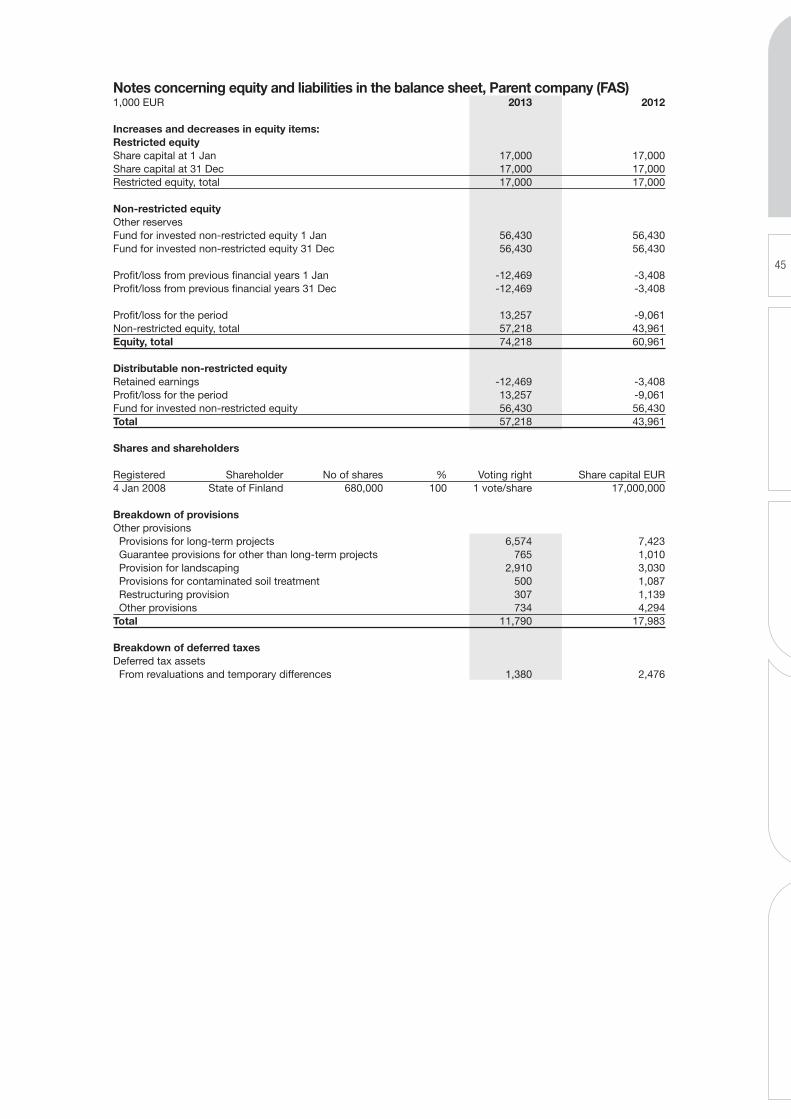

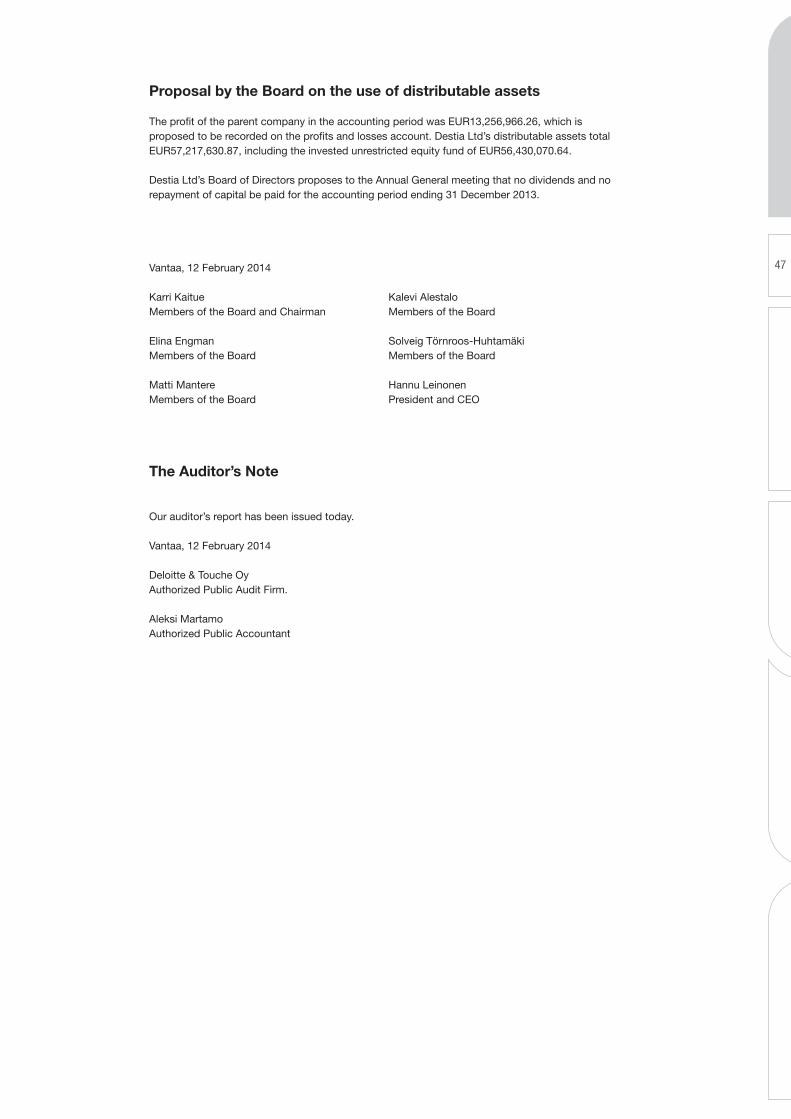

Proposal by the Board on the use of distributable assets

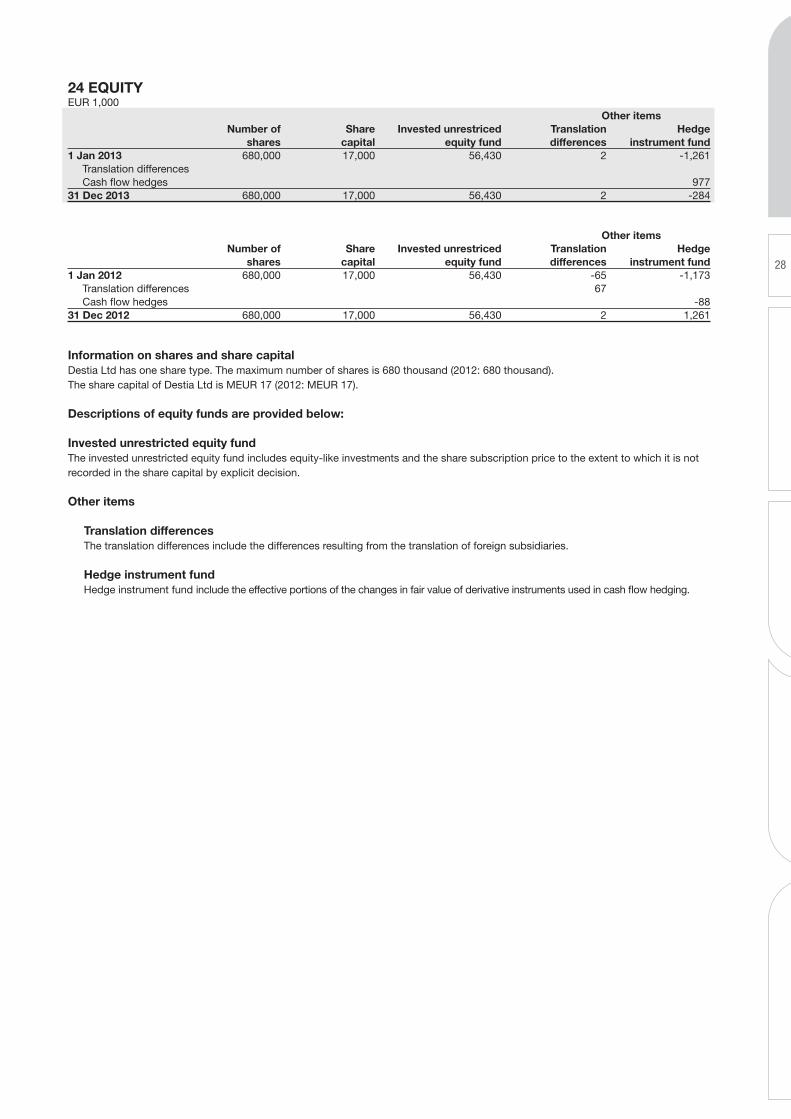

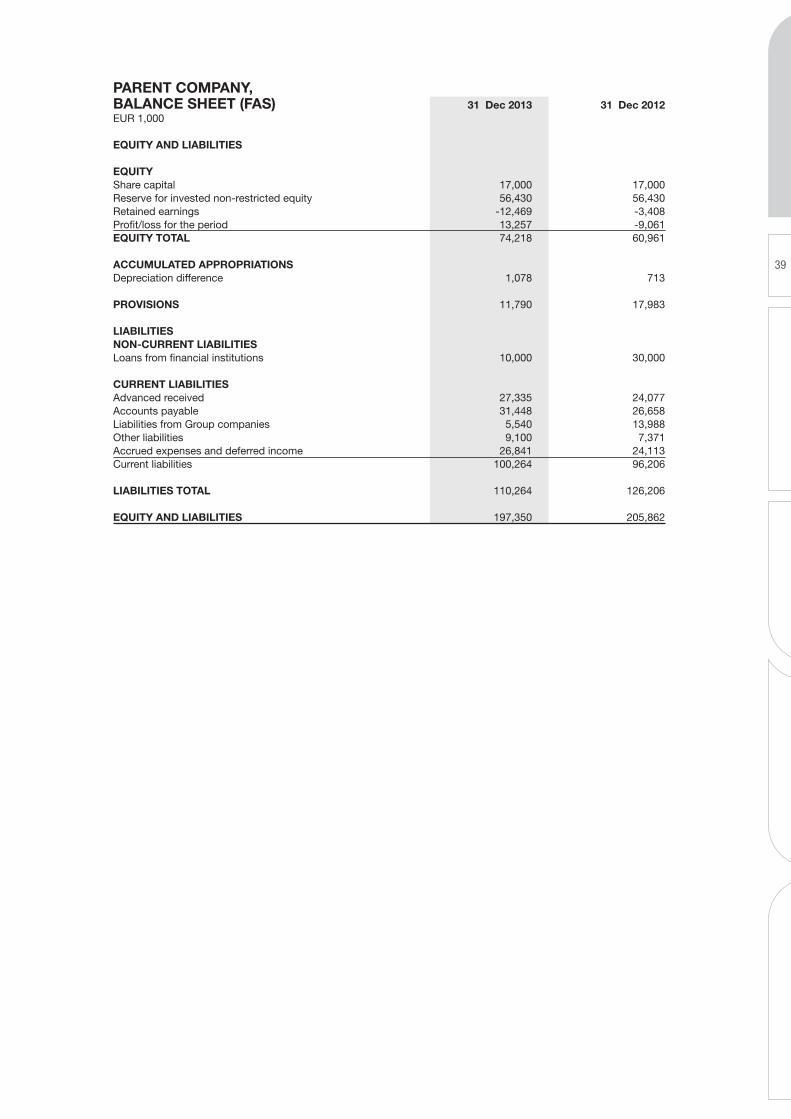

The profit of the parent company in the accounting period was EUR13,256,966.26, which is proposed to be recorded on the profits and losses account. Destia Ltd’s distributable assets total EUR57,217,630.87, including the invested unrestricted equity fund of EUR56,430,070.64.

Destia Ltd’s Board of Directors proposes to the Annual General meeting that no dividends and no repayment of capital be paid for the accounting period ending 31 December 2013.

8

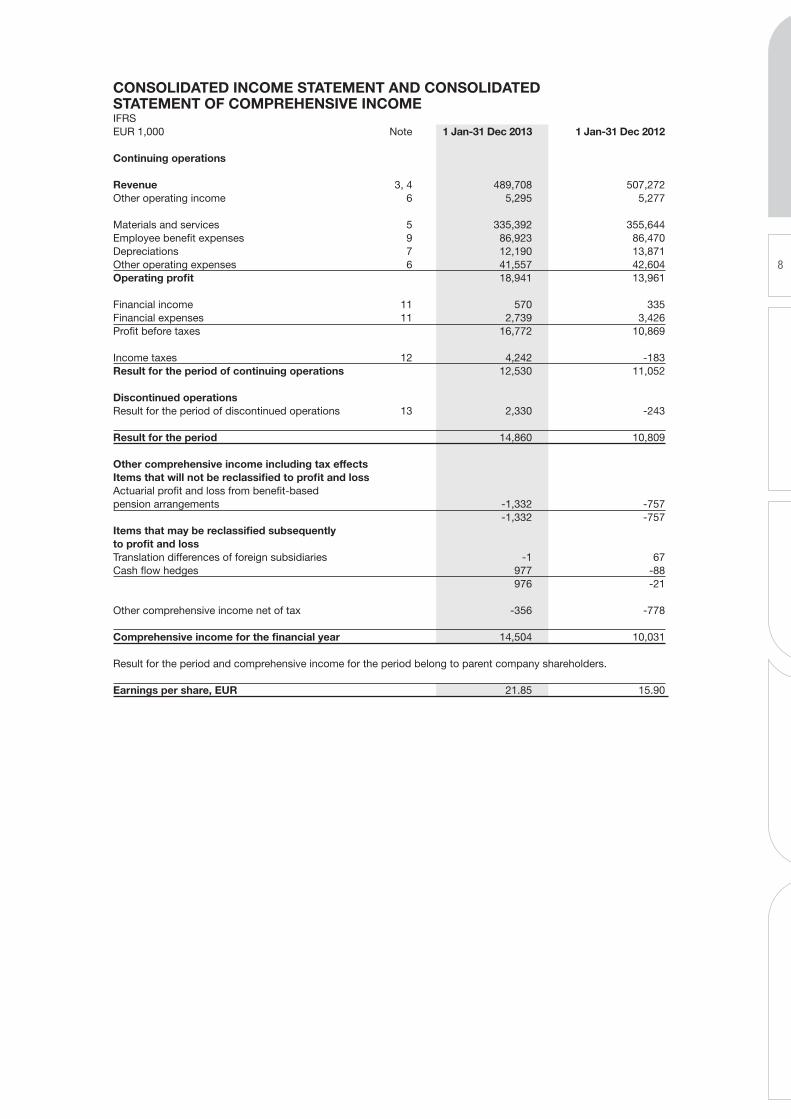

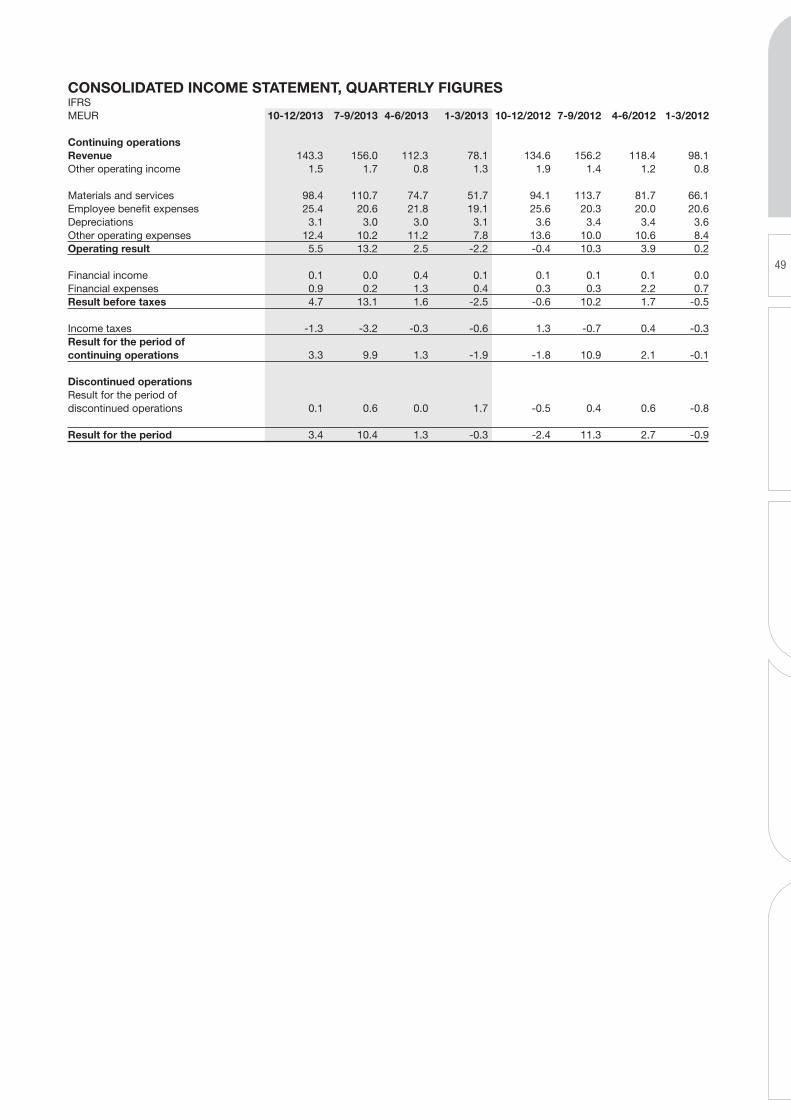

CONSOLIDATED INCOME STATEMENT AND CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME IFRS EUR 1,000 Note 1 Jan-31 Dec 2013 1 Jan-31 Dec 2012 Continuing operations Revenue 3, 4 489,708 507,272Other operating income 6 5,295 5,277 Materials and services 5 335,392 355,644Employee benefit expenses 9 86,923 86,470Depreciations 7 12,190 13,871Other operating expenses 6 41,557 42,604Operating profit 18,941 13,961 Financial income 11 570 335Financial expenses 11 2,739 3,426Profit before taxes 16,772 10,869 Income taxes 12 4,242 -183Result for the period of continuing operations 12,530 11,052 Discontinued operations Result for the period of discontinued operations 13 2,330 -243 Result for the period 14,860 10,809 Other comprehensive income including tax effects Items that will not be reclassified to profit and loss Actuarial profit and loss from benefit-based pension arrangements -1,332 -757 -1,332 -757Items that may be reclassified subsequently to profit and loss Translation differences of foreign subsidiaries -1 67Cash flow hedges 977 -88 976 -21 Other comprehensive income net of tax -356 -778 Comprehensive income for the financial year 14,504 10,031 Result for the period and comprehensive income for the period belong to parent company shareholders. Earnings per share, EUR 21.85 15.90

9

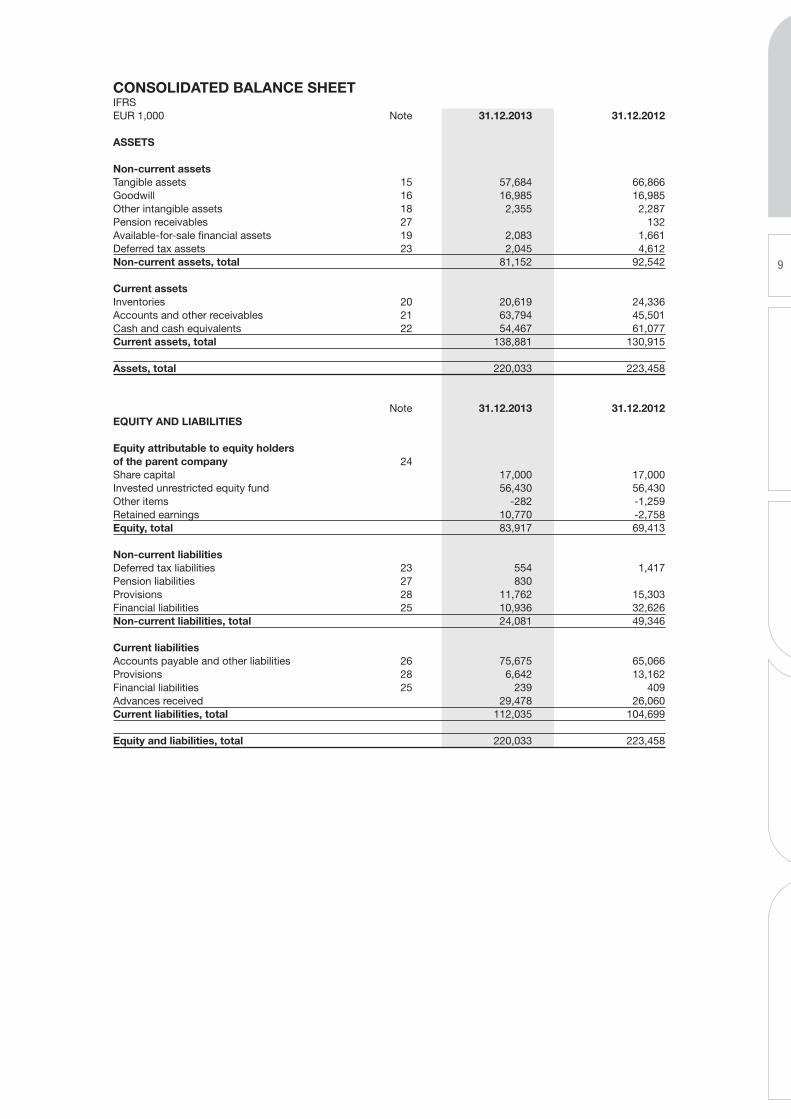

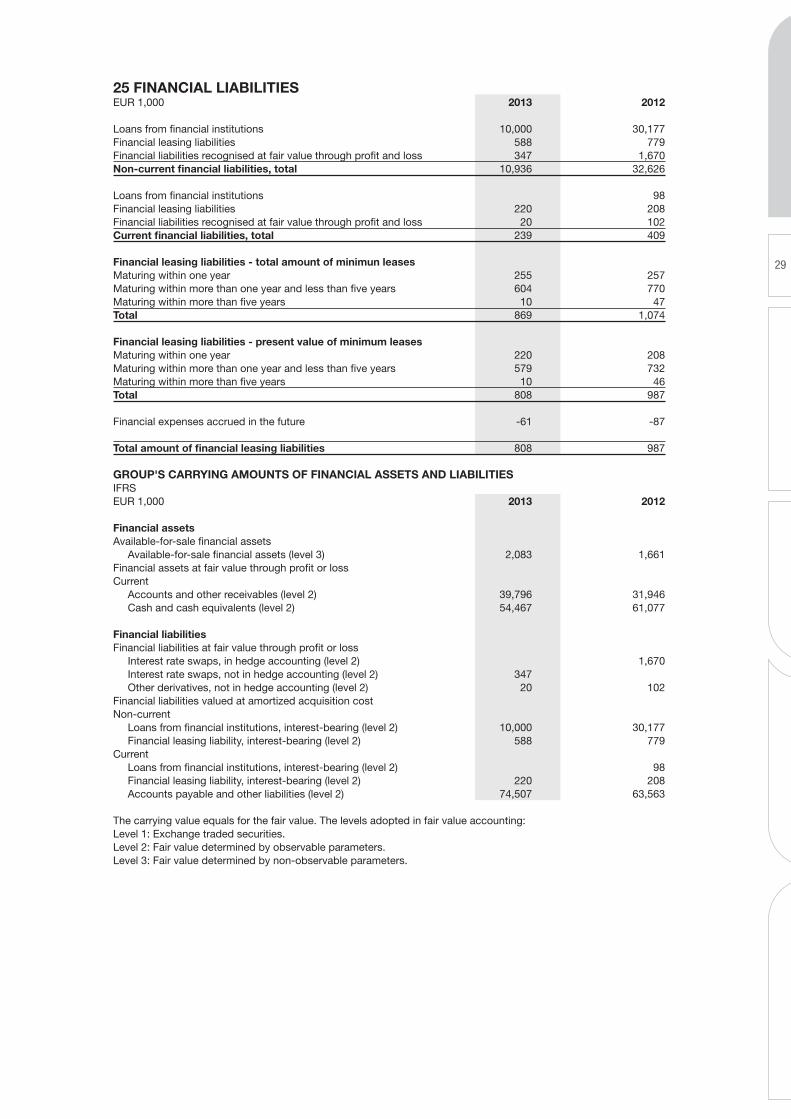

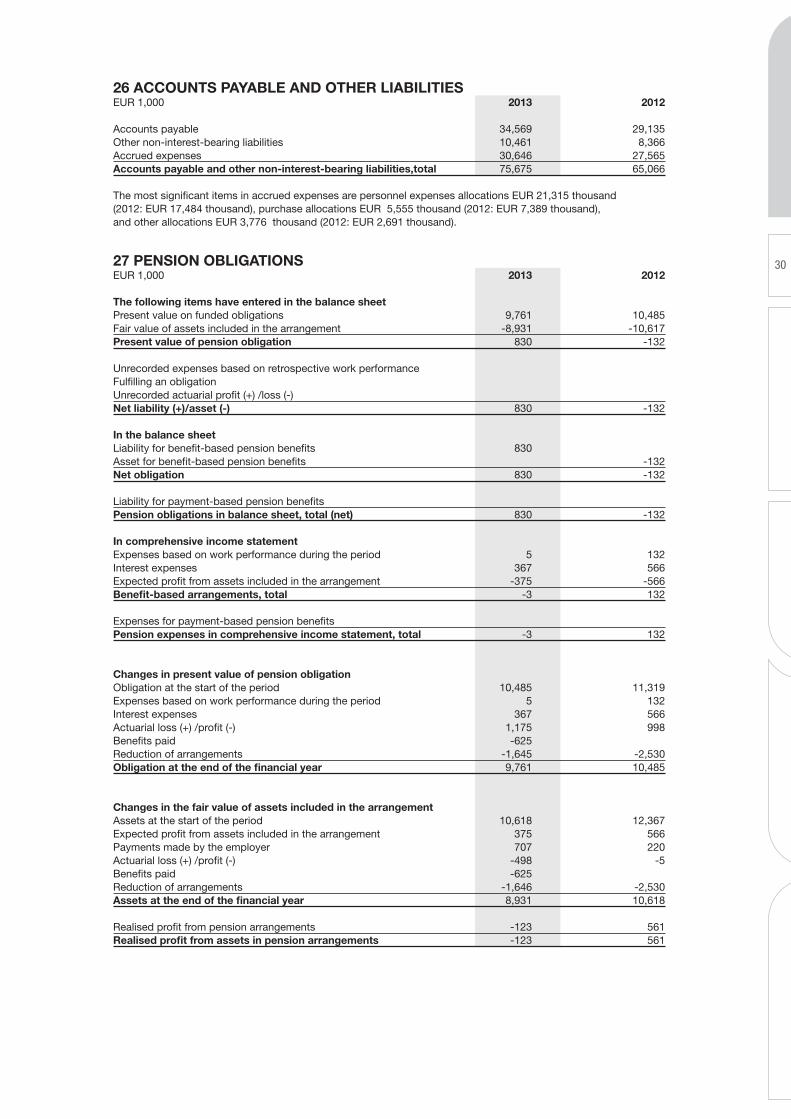

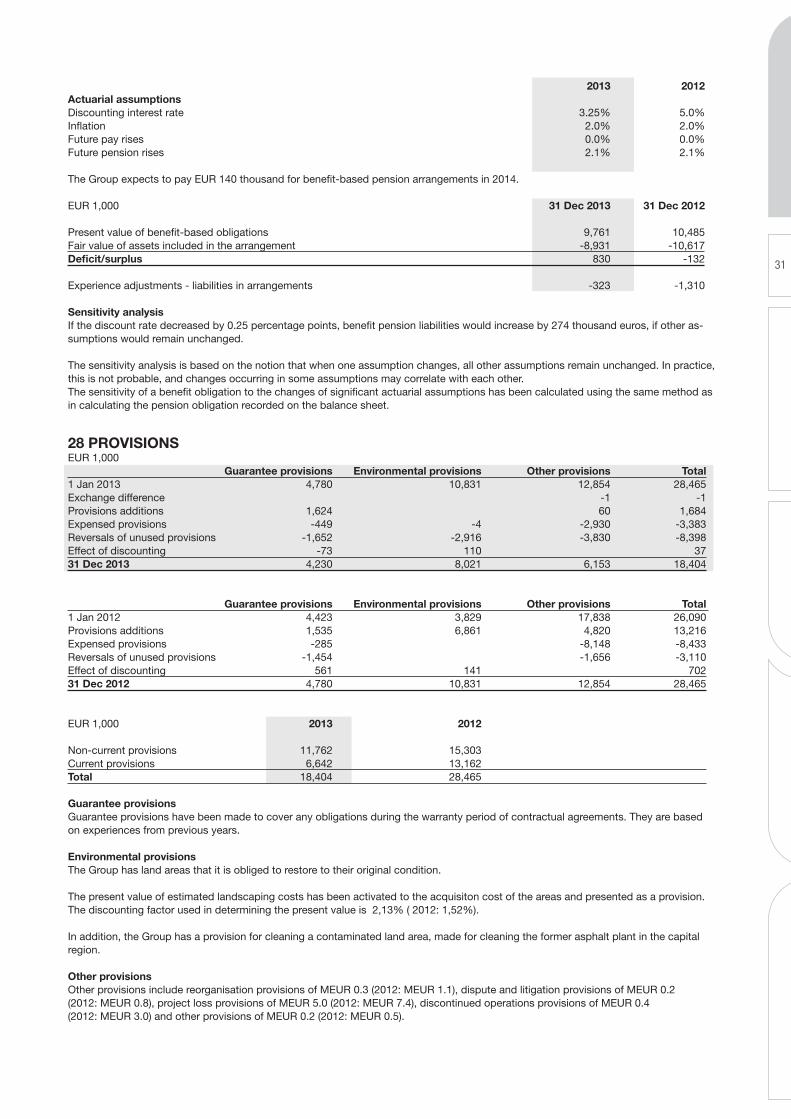

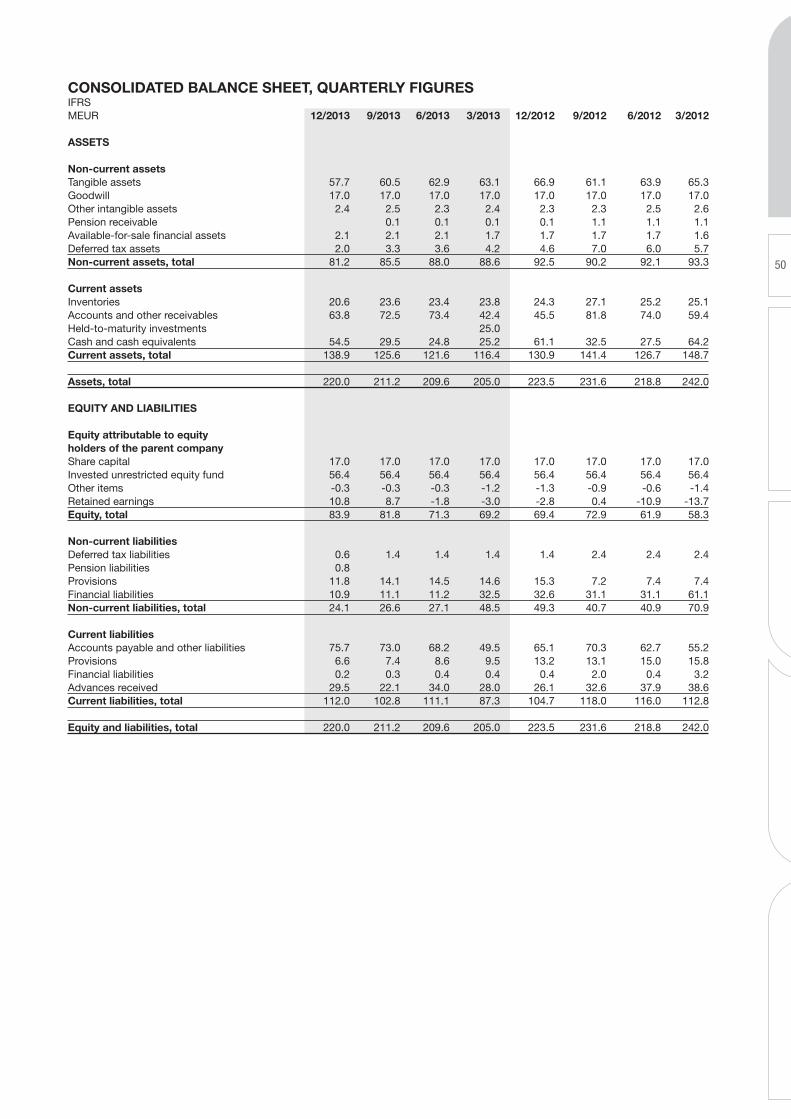

CONSOLIDATED BALANCE SHEET IFRS EUR 1,000 Note 31.12.2013 31.12.2012 ASSETS Non-current assets Tangible assets 15 57,684 66,866Goodwill 16 16,985 16,985Other intangible assets 18 2,355 2,287Pension receivables 27 132Available-for-sale financial assets 19 2,083 1,661Deferred tax assets 23 2,045 4,612Non-current assets, total 81,152 92,542 Current assets Inventories 20 20,619 24,336Accounts and other receivables 21 63,794 45,501Cash and cash equivalents 22 54,467 61,077Current assets, total 138,881 130,915 Assets, total 220,033 223,458 Note 31.12.2013 31.12.2012EQUITY AND LIABILITIES Equity attributable to equity holders of the parent company 24 Share capital 17,000 17,000Invested unrestricted equity fund 56,430 56,430Other items -282 -1,259Retained earnings 10,770 -2,758Equity, total 83,917 69,413 Non-current liabilities Deferred tax liabilities 23 554 1,417Pension liabilities 27 830 Provisions 28 11,762 15,303Financial liabilities 25 10,936 32,626Non-current liabilities, total 24,081 49,346 Current liabilities Accounts payable and other liabilities 26 75,675 65,066Provisions 28 6,642 13,162Financial liabilities 25 239 409Advances received 29,478 26,060Current liabilities, total 112,035 104,699 Equity and liabilities, total 220,033 223,458

10

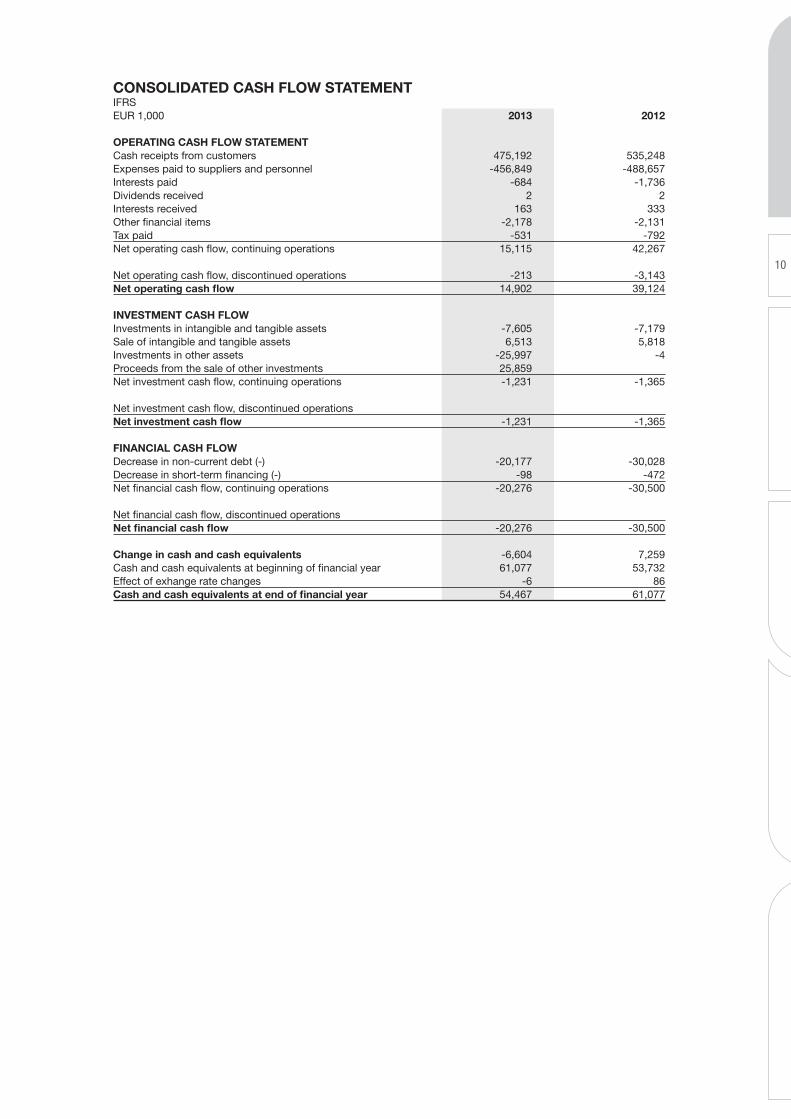

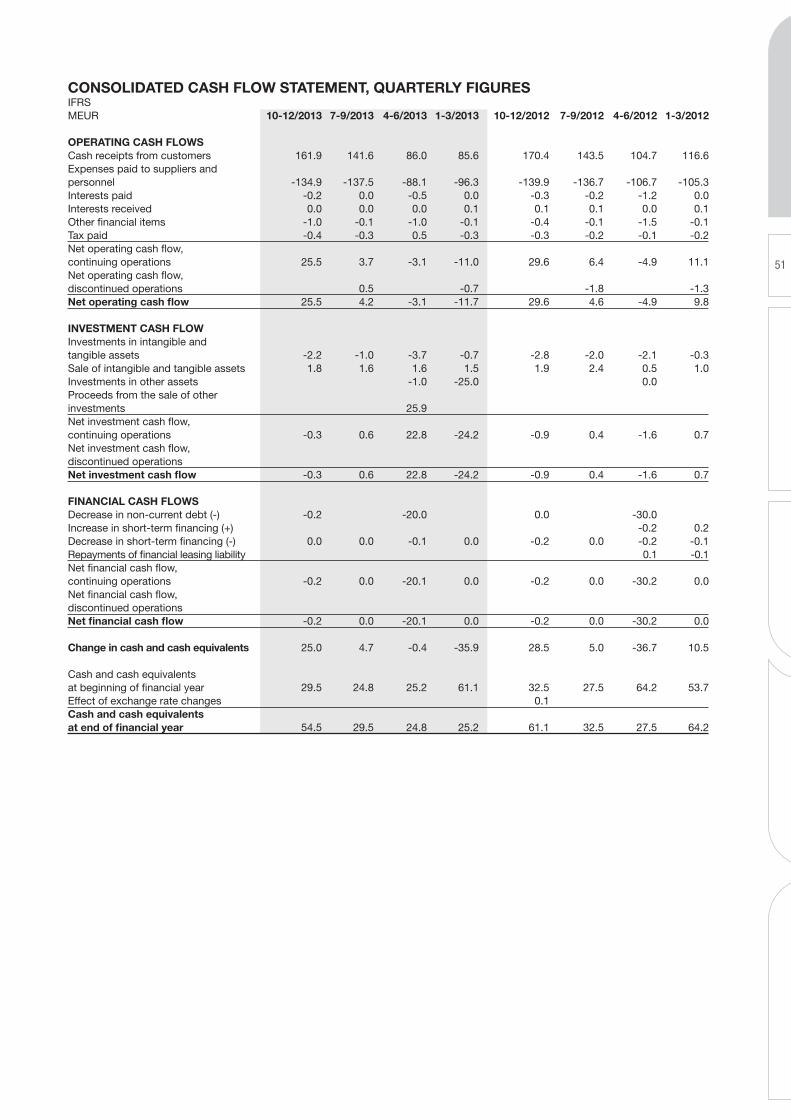

CONSOLIDATED CASH FLOW STATEMENT IFRS EUR 1,000 2013 2012 OPERATING CASH FLOW STATEMENT Cash receipts from customers 475,192 535,248Expenses paid to suppliers and personnel -456,849 -488,657Interests paid -684 -1,736Dividends received 2 2Interests received 163 333Other financial items -2,178 -2,131Tax paid -531 -792Net operating cash flow, continuing operations 15,115 42,267 Net operating cash flow, discontinued operations -213 -3,143Net operating cash flow 14,902 39,124 INVESTMENT CASH FLOW Investments in intangible and tangible assets -7,605 -7,179Sale of intangible and tangible assets 6,513 5,818Investments in other assets -25,997 -4Proceeds from the sale of other investments 25,859 Net investment cash flow, continuing operations -1,231 -1,365 Net investment cash flow, discontinued operations Net investment cash flow -1,231 -1,365 FINANCIAL CASH FLOW Decrease in non-current debt (-) -20,177 -30,028Decrease in short-term financing (-) -98 -472Net financial cash flow, continuing operations -20,276 -30,500 Net financial cash flow, discontinued operations Net financial cash flow -20,276 -30,500 Change in cash and cash equivalents -6,604 7,259Cash and cash equivalents at beginning of financial year 61,077 53,732Effect of exhange rate changes -6 86Cash and cash equivalents at end of financial year 54,467 61,077

11

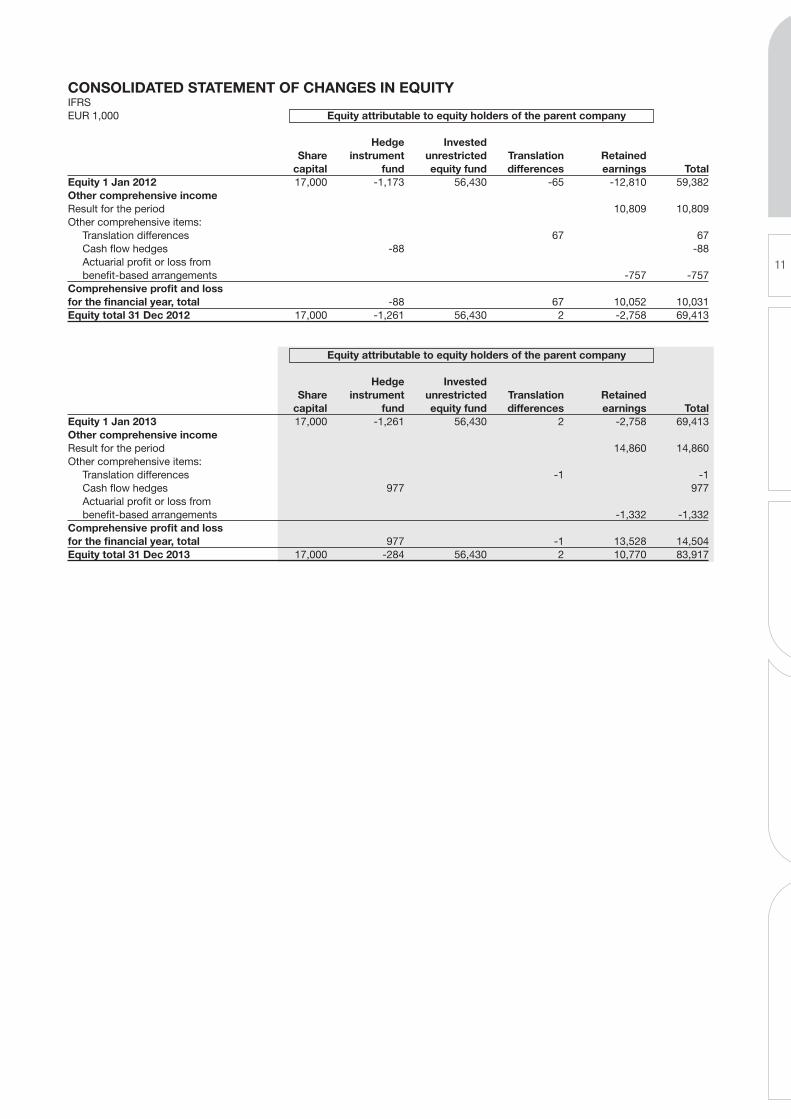

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY IFRS EUR 1,000 Equity attributable to equity holders of the parent company Hedge Invested Share instrument unrestricted Translation Retained capital fund equity fund differences earnings TotalEquity 1 Jan 2012 17,000 -1,173 56,430 -65 -12,810 59,382Other comprehensive income Result for the period 10,809 10,809Other comprehensive items: Translation differences 67 67 Cash flow hedges -88 -88 Actuarial profit or loss from benefit-based arrangements -757 -757Comprehensive profit and loss for the financial year, total -88 67 10,052 10,031Equity total 31 Dec 2012 17,000 -1,261 56,430 2 -2,758 69,413

Equity attributable to equity holders of the parent company Hedge Invested Share instrument unrestricted Translation Retained capital fund equity fund differences earnings TotalEquity 1 Jan 2013 17,000 -1,261 56,430 2 -2,758 69,413Other comprehensive income Result for the period 14,860 14,860Other comprehensive items: Translation differences -1 -1 Cash flow hedges 977 977 Actuarial profit or loss from benefit-based arrangements -1,332 -1,332Comprehensive profit and loss for the financial year, total 977 -1 13,528 14,504Equity total 31 Dec 2013 17,000 -284 56,430 2 10,770 83,917

12

NOTES OF TH E CO N SOl I DATE D F INANC IA l STATE m E N T

Basic information about the Group

Destia is a Finnish infrastructure and construction service company, which plans, builds and maintains traffic routes and industrial and traffic environments as well as complete living environments. Our services cover the whole spectrum, from overground operations to subterranean construction. The Group mainly operates in Finland.

The Group’s parent company is Destia Oy, registered in Vantaa. Its registered address is Heidehofintie 2, 01300 Vantaa, Finland.

A copy of the Consolidated Financial Statements is available at www.destia.fi or from the parent company’s head office at Heide-hofintie 2, 01300 Vantaa.

On 12 February 2014, the Destia Oy’s Board of Directors ap-proved these financial statements for publication in their entirety. Under the Finnish Limited Liability Companies Act, shareholders may approve or reject the financial statements at the General Meeting held following their publication. The General Meeting may also take the decision to amend the financial statements.

1. Accounting principles

Basic principles

The consolidated financial statements were prepared in compli-ance with the International Financial Reporting Standards (IFRS), and the preparation abided by the International Accounting Standard (IAS) and International Financial Reporting Standards (IFRS) as well as the interpretations by the Standing Interpre-tations Committee (SIC) and International Financial Reporting Interpretations Committee (IFRIC) in force as at 31 December 2013. The International Financial Reporting Standards refer to the standards approved in the Finnish Accounting Act and provisions issued by virtue of it to be adopted in the EU in accordance with the procedure regulated by the EU regulation (EC) no 1606/2002 and the subsequent interpretations. The notes to the consolidat-ed financial statements are also in line with the requirements of the Finnish accounting and Community legislation supplementing the IFRS regulations.

At the end of 2011, the Group switched to IFRS practices, at the same time applying IFRS 1 First-time Adoption of International Financial Reporting Standards, the switchover date being 1 January 2010.

The Consolidated Financial Standards were prepared with refer-ence to original acquisition costs, with the exception of tradable financial assets, financial assets and liabilities recognised at fair value through profit or loss, and fair value hedges, which are valued at the current rate. The figures are in thousands of euros.

Preparing the statements in accordance with the IFRS stand-ards requires management to make certain estimates and have information relating to considered decisions the management has taken. This information relating to considered decisions, used in the application of the Group’s accounting policies, and which mostly affect the figures in the financial statements, is given in the section entitled ‘Accounting policies requiring discretion on the part of the management and the main factors of uncertainty connected with the estimates made’.

Accounting policies governing the Consolidated Financial Statements

Subsidiaries

Subsidiaries are companies over which the Group exercises con-trol. This is when the Group holds more than 50% of the votes, or has control of the company in another way. Furthermore, the existence of a potential voting right is taken into account when the conditions for control of the company are being assessed, when the instruments giving entitlement to a potential voting right can be realised at the time of examination. Control means the right to decide the company’s principles underlying finances and business in order to achieve benefit from its operations.

Intra-Group shareholdings are eliminated using the acquisition cost method. The consideration transferred, the acquired com-pany’s identifiable assets and liabilities assumed are measured at their acquisition-date fair values. The expenditure incurred through an acquisition is recognised as a cost. The consideration transferred does not include transactions treated separately from the acquisition. Their effect is accounted for through profit or loss at the time of the acquisition. Any contingent consideration is measured at its acquisition-date fair value, and is classed either as a liability or equity. Contingent consideration classed as a liability is measured at fair value on the last day of each reporting period, and the ensuing profit or loss is recognised through profit or loss or in other comprehensive income. Contingent considera-tion classified as equity is not remeasured. Acquired subsidiaries are consolidated from the time the Group has acquired control, and transferred subsidiaries until that control ceases. All the Group’s internal commercial transactions, receivables, liabilities, unrealised gains and internal profit distribution are eliminated when the Consolidated Financial Statements are being prepared. Unrealised losses are not eliminated if the loss is due to impair-ment. Changes to the parent company’s share of ownership in subsidiaries that do not lead to loss of control are treated as equity-related transactions.

Under the exemption allowed in the IFRS 1 standard, any company acquisitions prior to the IFRS switchover date are not adjusted to comply with IFRS principles, but remain at their value according to former Finnish accounting practices.

In March 2012, Destia’s Norwegian subsidiary Alpha Veg AS filed for bankruptcy. The effect on the result of the Norwegian busi-ness is shown in ‘Discontinuing operations’. The discontinued operation is presented in the notes to the accounts.

Changes to items denominated in foreign exchange

Figures showing the results and financial position of the units in the Group are denominated in the currency which is that for each unit’s main operating environment (‘functional currency’). The figures in the Consolidated Financial Statements are in euros, which is the functional and reporting currency of the Group’s parent company.

Commercial transactions denominated in foreign exchange

Commercial transactions denominated in a foreign currency are denominated in the functional currency at the rate on the date of the transaction. In practice, rates are often used that approximate to the rate on the date in question. Monetary items denominated in a foreign currency are converted to the functional currency

13

using the rate of exchange on the last day of the reporting peri-od. Non-monetary items denominated in a foreign currency, and which are measured at fair value, are converted to the function-al currency using the exchange rates on the date fair value is determined. Otherwise, non-monetary items are measured at the exchange rate on the date of the transaction.

Gains and losses from commercial transactions denominated in a foreign currency and changes to monetary items are treated through profit or loss. Exchange rate gains and losses from the business operation are included in equivalent items above oper-ating profit. Exchange rate gains and losses from foreign curren-cy loans are included in finance income and expenses, except for exchange rate differences on loans which are to protect net investments in foreign units, and which are effective there. These exchange rate differences are recognised in other comprehensive income, and accumulated exchange rate differences are shown separately under equity, until the foreign unit is partially or wholly disposed of.

Conversion of the financial statements of foreign companies in the Group

The items for income and costs in the statements of comprehen-sive income and separate income statements of foreign compa-nies in the Group are converted to euros at the exchange rates on the dates on which the commercial transactions take place, and the figures in the balance sheets are converted using the ex-change rates on the date on which the reporting period ends. The translation of the profit and loss and comprehensive profit and loss for the financial period using different exchange rates, in the income statement and comprehensive income statement, causes a translation difference in equity on the balance sheet, which is entered in ‘Other comprehensive profit a loss items’. Translation differences arising from the elimination of the acquisition cost of foreign subsidiaries and the conversion of equity items accumu-lating after an acquisition are recognised in other comprehensive income. If a subsidiary is sold wholly or partially, the accumulated translation differences are reclassified to profit or loss as part of the profit or loss from sales.

Under the exemption allowed in the IFRS 1 standard, transla-tion differences arising prior to 1 January 2010, which was the date on which the Group switched to compliance with IFRS standards, are to be recognised in accumulated profit funds in connection with the switch, and will not be recognised through profit or loss when a subsidiary is sold at a later date. From the switchover date, translation differences arising when the Consol-idated Financial Statements are being prepared will be presented as a separate item under equity. From 1 January 2010, goodwill generated from the acquisition of foreign units and fair value adjustments made to the book values of the assets and liabilities of foreign units when they are acquired are to be treated as the assets and liabilities of these foreign units. They are converted to euros at the exchange rate on the last day of the reporting period. Goodwill from acquisitions prior to 1 January 2010 is recognised in euros.

Tangible fixed assets (Property, plant and equipment)

Tangible fixed assets are measured at acquisition cost less accu-mulated depreciation and impairment losses.

An acquisition cost includes the expenditure incurred directly from acquiring a tangible fixed asset, including the costs of

dismantling or moving the asset based on the original value, and of restoring the location to its original state, if the organisation has such an obligation. The acquisition costs of an asset that has been produced by the company itself includes the costs of materials, the direct costs of employee benefits and the other di-rect costs of preparing the asset for its intended purpose. When preparation of an asset for its intended purpose or sale requires a good deal of time, the direct borrowing costs of its acquisition, construction or production are capitalised as part of its acquisi-tion costs.

If an asset consists of more than one part, whose lifetimes vary in length, each part is treated as a separate commodity. In such cases, expenditure for the replacement of the part is capitalised and any book value remaining when that replacement takes place is derecognised. Expenditure incurred at a later date is only included in the book value of a tangible fixed asset if the Group is likely to benefit financially from the commodity in the future and the acquisition cost of the commodity can be reliably determined. Other repair and maintenance costs are recognised as incurred.

Assets are depreciated during their estimated useful life on a straight-line basis. The exception is areas of soil, depreciation on which is calculated according to use. No depreciation is calculat-ed for land. Estimated useful lives are as follows:

• Buildings: 10–40 years• Machinery and equipment: 3–20 years• Other tangible assets: according to use

An asset’s residual value and its useful life are revised at the end of each financial year, at the very least, and, where necessary, adjusted to reflect the changes that have taken place with regard to the expectations of its financial benefit. When a tangible fixed asset is classified as held for sale in accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, the depreciation process ends. The gains and losses from the sale of decommissioned tangible fixed assets or their disposal are recognised in profit and loss.

Government subsidies

Government/public subsidies are entered in the profit and loss statement when it is reasonably certain that they will be obtained. Subsidies that have been received as payments against already realised costs are recognised through profit or loss in the period in which the subsidy is realised. Subsidies are presented in other operating income.

Intangible assets

Goodwill

Goodwill is recognised at the amount by which the transferred consideration exceeds the Group’s share of identifiable fair value net assets for an acquired company on the date it is acquired. Goodwill arising from the merger of business oper-ations prior to 2010 is equivalent to the book value according to the earlier norms for the financial statements, which is used as the default acquisition cost under IFRS 1. No deprecation is recognised for goodwill (or any other unlimited-life intangible assets), but it is tested annually for potential impairment. For this purpose, goodwill is allocated to units producing money flow. Goodwill is measured at the original acquisition price less impairment.

14

Research and development expenditure

Research expenditure is recognised through profit or loss. Devel-opment expenditure incurred from the planning of new or more advanced procedures and concepts is capitalised as intangible assets in the balance sheet from the time when they are technical-ly feasible, can be commercially exploited and can be expected to produce future economic benefit. Capitalised development costs include the material, labour and testing costs which are directly incurred when preparing the commodity for its intended purpose. Previously amortised development costs are no longer recognised at a later date. Amortisation begins when the asset is ready to be used. Incomplete assets are tested annually for impairment. After initial recognition, capitalised development costs are valued at the original acquisition cost less amortisation and impairment.

Other intangible assets

An intangible asset is entered in the balance sheet at the original acquisition cost, where it can be determined reliably and where the Group is likely to expect to benefit financially from the asset in the future.

Intangible assets with a restricted useful life are amortised on a straight-line basis through profit or loss within their known or estimated useful life.

The depreciation periods for other intangible assets are:

• Computer software: 5 years• Other intangible rights: 5 years

Inventories

Inventories are measured at the acquisition cost or net realisation value, whichever is the lower. The acquisition cost is determined using the average weighted share price method. The acquisition cost of finished good and intermediate inventories consists of the raw materials, the expenses incurred from direct work, other direct expenses, an appropriate share of the variable general costs of manufacture and fixed general costs at a normal level of activity. The net realisable value is the estimated selling price in the ordinary course of business less the estimated necessary costs of completion of the inventories and the estimated costs necessary to realise yield.

Rental agreements

The Group as lessee

Rental agreements relating to fixed tangible assets, which expose the Group to significant risks and rewards inherent in holding such assets, are classified as finance lease agreements.

An asset acquired through a finance lease agreement is entered in the balance sheet at the inception of the lease at the fair value of the leased commodity or the present value of the minimum lease payments, whichever is lower.

An asset acquired through a finance lease agreement is depre-ciated over its useful life or within the lease term, whichever is shorter. Lease payments are apportioned between the finance charge and the reduction of the outstanding liability so that the finance charge is allocated to each period during the lease term to produce a constant periodic rate of interest on the remaining balance of the liability. Rental obligations are included in financial liabilities. Leases where a significant portion of the risks and

rewards of ownership are retained by the lessor are classified as other rental agreements. Payments made under operating leases expenses are charged to the income statement on a straight-line basis over the period of the lease.

The Group as lessor

Assets let by the Group are included in tangible fixed assets in the balance sheet. They are depreciated during their useful life in the same way as equivalent tangible fixed assets in the Group’s use. Revenue from rental agreements is charged to the income statement on a straight-line basis over the period of the lease.

Impairment of tangible and intangible assets

At each date the reporting period ends, the Group assesses whether there are suggestions that an asset is impaired. If there are such signs, an estimate is made of the amount that is recov-erable on the asset in question. In addition, an estimate is made each year of the following: goodwill, unlimited-life intangible assets and intangible assets in progress.

The need to record impairment is examined at the level of units producing money flow, i.e. at the lowest unit level, which is mainly independent of the other units and whose money flows can be distinguished from the money flows of equivalent units and are virtually independent of them. The recoverable amount is the fair value of the asset less expenditure incurred from its sale or its utility value, whichever is the greater. The utility value is the present value of future net money flows expected to be derived from an asset or cash-generating unit. The discounting has been performed in accordance with IAS 36.

An impairment loss is recognised when the book value of an asset is greater than its recoverable amount. An impairment loss is recognised directly through profit or loss. If the impairment loss is allocated to a unit producing a money stream, it is first applied to reduce the goodwill for that unit, and then to reduce the value of other assets of the unit uniformly. When an impairment loss is being entered, the useful life of the asset being depreciated is re-assessed. An impairment loss for an asset other than goodwill is reversed if there has been a change in the values used to de-termine the recoverable amount on the asset. However, impair-ment losses cannot be reversed to exceed the asset’s book value as it would be, had no impairment loss been recognised. In no circumstances can impairment losses recognised for goodwill be reversed.

Employee benefits

Pension obligations

Pension schemes are classified as defined benefit or defined contribution plans. With the latter, the Group pays fixed premi-ums into a separate unit. The Group has no legal or constructive obligation to increase premiums if the organisation in receipt of the premiums is unable to pay the relevant pension benefits. All schemes that do not fulfil these conditions are defined bene-fit plans. Payments made into defined contribution plans are recognised through profit or loss in the financial year in which the obligation arises.

The Group’s obligations regarding defined benefit plans are calculated separately for each scheme, using the projected unit credit method.

15

Pension expenditure is recognised as costs on the basis of au-thorised actuarial calculations for the length of service of person-nel. When the current value of a pension obligation is being cal-culated, the discount rate used is the yield on high-quality bonds issued by companies, and if that is not available, the interest on state debentures. Owing to the non-recurring payment of pension contributions, the pay rise percentage used in the calculations is 0. The maturity of bonds and debentures corresponds essentially to the maturity of the pension obligation being calculated. From the current value of a pension obligation in a balance sheet is subtracted the assets included in the pension scheme meas-ured at fair value on the last day of the reporting period and the unvested past service costs.

All actuarial gains and losses that accumulated by 1 January 2010, the date of the switchover to IFRS standards, were recog-nised under equity in the opening IFRS balance sheet, in accord-ance with IFRS 1 standard. Actuarial gains and losses thereafter are recognised in other comprehensive income in the period in which they are made.

Past service costs are recognised on the straight-line basis through profit or loss for the period in which they are vested. If the benefits are vested directly, they are recognised as direct costs.

Provisions and contingent liabilities

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events, it is proba-ble that an outflow of resources will be required to settle the obligation, and a reliable estimate of the amount can be made. Provisions are stated at the present value of the obligation. The discount rate is determined to reflect current market assess-ments of the time value of money and the risks specific to the obligation. If the Group expects a provision to be reimbursed, for example, by a third party, the reimbursement is recognised as a separate asset if the reimbursement is virtually certain.

A quality reservation (provision) is recognised when a project covered under a guarantee clause is delivered. The amount of the quality reservation (provision) is based on the experience-based estimate of the guarantee costs to be incurred.

The Group recognises a provision for onerous contracts when the expected benefits to be derived from a contract are less than the unavoidable costs of meeting obligations.

A reorganisation provision is recognised when the Group has drawn up a detailed reorganisation plan, begun on its execution and reported the matter.

A provision associated with environmental obligations is recog-nised when the Group has an obligation based on environmental legislation and the Group’s principles of environmental respon-sibility and which relates to the decommissioning of a produc-tion plant, landscaping responsibilities, repairing environmental damage or moving equipment from one place to another.

A contingent liability is a potential obligation arising as a result of past events, whose existence is only confirmed when an uncertain event takes place which is beyond the Group’s control. Contingent liabilities may also be regarded as existing obligations that are unlikely to require fulfilment of a payment obligation, or a reliable estimate of the amount cannot be made. A contingent liability is presented in the Notes to the Financial Statements.

Taxes based on taxable income for the period and deferred taxes

Tax expenses comprise tax based on taxable income for the pe-riod and deferred tax. Income tax is recognised through profit or loss, except for taxes related to items recognised directly to the shareholders’ equity or the comprehensive income statement. With these, tax is recognised in the relevant items. Tax based on taxable income for the period is calculated using the corporate income tax rate effective in each country. Deferred taxes are calculated on all temporary differences between the book value and taxable value. However, no deferred tax liability is recognised if it is due to the initial recognition of an asset or liability where there is no matter of a merger or the commercial transaction at the time does not affect the business results or taxable income.

Deferred taxation is recognised for investments in subsidiaries, except where the Group is able to specify a date on which the temporary difference dissolves and the temporary difference will probably not dissolve in the foreseeable future.

The largest temporary differences arise from the depreciation of tangible fixed assets, the valuation of derivative contracts at fair value, defined benefit pension plans and unused taxable losses.

Deferred taxes are calculated using the statutory tax rates by the last day of the reporting period or the tax rates which have been approved in practice by the closing date. Deferred tax assets are recognised to the extent that it is probable that taxable income, against which the temporary difference can be applied, will mate-rialise in the future.

Revenue recognition

Sales (Turnover) are/is presented in such a way that the revenue from the sales of goods and services at fair value are recognised and adjusted to allow for indirect taxes, discounts and exchange rate differences for sales in foreign currencies.

Long-term projects

The revenue and costs of long-term projects are recognised as such with reference to the stage of completion, when the final financial result for the project can be estimated reliably enough. The stage of completion is determined for each project as the share of the costs incurred from the work carried out by the review date compared with the total costs estimated for the project.

Expenditure that relates to a project still not entered as income is recognised as long-term projects in progress under inventories. If the expenditure incurred and recognised gains exceed the amount invoiced for the project, the difference is shown under trade and other receivables in the balance sheet. If the expendi-ture incurred and recognised gains are less than what is invoiced for the project, the difference is shown under trade payables and other debt. When the end financial result of a long-term project cannot be reliably assessed, the project expenditure is recog-nised in the same period in which it is incurred, and the revenue from the project is only recognised up to the amount where a sum of money equivalent to the expenditure incurred is available. If it is probable that the overall expenditure incurred in complet-ing the project will exceed total income from it, the expected loss is entered as a direct cost.

16

Sold goods and services

Revenue from the sale of goods is recognised when the signif-icant risks, rewards and effective control associated with the ownership of the goods have transferred to the purchaser. As a general rule, this is when delivery under the terms of the contract relating to the products takes place. Revenue from services is entered as income in the financial year in which the service is delivered.

Interest and dividends

Interest received is recognised using the effective interest rate method, and dividend income when entitlement to a dividend arises.

Non-current assets held for sale and discontinued operations

Non-current assets (or a disposal group) and assets and liabilities relating to discontinued operations are classified as held for sale, if their book value will be recovered principally through the sale of the assets rather than through continuing use. For this to be the case, the sale must be highly probable, the asset (or disposal group) must be available for immediate sale in its present con-dition, subject only to terms that are usual and customary, the management must be committed to selling and the sale should go ahead within one year from the date of classification.

Immediately prior to classification, the assets held as for sale or assets and liabilities of a disposable group are measured in accordance with the IFRS standards to be applied. From the time of the classification, assets held for sale (or a disposable group) are measured at book value or at fair value less the expenditure incurred from their sale, whichever is the lower. Depreciation of these assets ends at the time of classification.

Assets included in a disposable group - and not included in the scope of the IFRS 5 valuation rules - and liabilities (in a dispos-able group) are measured in accordance with the IFRS standards even after the classification date.

A discontinued operation is a part of the Group which has been disposed of or which has been classified as held for sale, and which meets the following conditions: it is a significant sepa-rate business unit or unit representing a geographical area, part of one coordinated plan relating to disposal of a separate key business area or geographical territory, or a subsidiary that was acquired exclusively for the purpose of selling it on. The financial result for discontinued operations is recognised as its own item in the Group’s comprehensive income statement. Assets held for sale, disposable groups, items recognised in other compre-hensive income relating to assets held for sale, and liabilities in-cluded in a disposable group are presented in the balance sheet separately from other items.

Financial assets and liabilities

Financial assets

The Group classifies financial assets in the following categories: financial assets at fair value through profit or loss, investments held till maturity, loans and other receivables and availa-ble-for-sale financial assets. The classification depends on the purpose of the acquisition of the financial assets, and they are classified when they are originally purchased.

Transaction costs are included in the original book value for financial assets, where it concerns an item that is not measured at fair value through profit or loss. All purchases and sales of fi-nancial assets are recognised on the date of trading, which is the date on which the Group undertakes to buy or sell the financial instrument. The balance sheet depreciation of financial assets takes place when the Group has lost its agreed entitlement to money flows, or when it has transferred risks and revenue out-side the Group to a significant extent.

Included in financial assets at fair value through profit or loss are items included in financial assets acquired to be held for trading, or which are classified at fair value at initial recognition through profit or loss (use of the fair value option). The classification may only be altered in rare circumstances. The latter group includes financial assets that are managed based on fair value or an item included in financial assets associated with one or more embedded derivatives that changes contractual money flows substantially, where the entire compound instrument is measured at fair value. Financial assets held for trading are mainly acquired to control changes in short-term market prices. Derivatives that are not contracts of guarantee or do not meet the conditions of hedge accounting are classified as held for trading. Derivatives that are held for trading and financial assets maturing within 12 months are included in current assets.

Group items are measured at fair value, based on the quoted market price on the last day of the reporting period. The fair values of interest rate swaps are determined as the current value of future money flows and foreign exchange forwards are measured at the rates in force for them on the last day of the reporting period. When measuring derivatives and other financial instruments that are not to be traded, the Group usually uses approved valuation methods and discounted values for future money streams. Both unrealised and realised gains and losses from changes in fair value are recognised through profit or loss in the financial year in which they are made.

Loans and other receivables are non-derivative assets with fixed or measurable payments. They are not quoted in active markets and the Group does not hold them for trading or classify them as available-for-sale at initial recognition. They are valued at amortised cost using the effective interest rate method. Loans and other receivables are presented as current or non-current fi-nancial assets depending on their nature, the latter if they mature after 12 months have passed.

Available-for-sale financial assets are non-derivative assets specifically included in this classification or not included in any other. They are included in non-current assets, except if they are to be held for under 12 months from the last day of the reporting period, in which case they are included in current assets.

Available-for-sale financial assets may consist of shares and interest-bearing investments. They are measured at fair value or, when fair value cannot be reliably determined, at acquisition cost. The fair value of an investment is determined with reference to its buying rate. If there are no quoted rates for available-for-sale financial assets, the Group applies various valuation methods to value them. They include, for example, references to recent trades between independent bodies, discounted money flows or valuations for other similar instruments. For this, information obtained from the markets is generally used as opposed to contributing factors that the Group has itself decided, which are used as little as possible.

17

Changes to the fair value of available-for-sale financial assets are recognised in other comprehensive income, and are presented in the fair value fund, with consideration being given to their implications for tax. Accumulated fair value adjustments are transferred from equity through profit or loss when an investment is sold or its value is impaired so that an impairment loss on the investment should be recognised. Interest on available-for-sale debt instruments is recognised in finance income using the effec-tive interest rate method.

Cash and cash equivalents

Cash and cash equivalents comprise cash balances, call depos-its and other short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. The items classified as cash and cash equivalents have a maturity of no more than twelve months from the time of acquisition.

Impairment of financial assets

The Group assesses on the last day of each reporting period whether there is any objective evidence that a financial as-set or group of financial assets is impaired. If the fair value of investments has fallen significantly below the acquisition cost and period determined by the Group, this is an indication of an impairment of available-for-sale share. If any such evidence exists, the amount recognised in the shareholders’ fair value reserve is unrecognised and recognised in the income statement. Impairment loss on available-for-sale financial assets categorised as equity instruments are not reversed through profit or loss. A later reversal of impairment loss on interest rate instruments is, however, recognised through profit or loss.

The Group recognises an impairment loss on trade receivables, when there is objective evidence that a receivable is not fully col-lectible. The borrower’s significant financial difficulties, probability of a bankruptcy or non-payment exceeding 90 days are evidence of impairment loss on a trade receivable.

Financial liabilities

Financial liabilities are initially recognised in accounting at fair value. Transaction costs are included in the initial book value of the financial liabilities measured at acquisition cost. Later, financial liabilities, except for derivatives that are liabilities, are measured at amortised acquisition cost using the effective inter-est rate method. Financial liabilities are included in non-current and current liabilities, being classed as current unless the Group has an unconditional right to defer payment of the debt within at least 12 months from the last day of the reporting period.

Expenses under liabilities are recognised as costs in the period in which they are incurred. Commissions associated with loan commitments are recognised as transaction costs to the extent that it is probable that the entire loan commitment or part of it will be taken up. In such a case, the commission is entered in the balance sheet until the loan is taken up. When it is, the commis-sion associated with loan commitments is recognised as part of the transaction costs. If the loan commitment is unlikely to be taken up, the commission is recognised as an advance payment for a liquidity service and is amortised as a cost for the period of the loan commitment.

Derivative financial instruments and hedge accounting

Derivatives are initially recognised at fair value on the date the derivative contract is entered into and are subsequently remeasured at their fair value. Gains and losses resulting from measurement at fair value are treated in the accounts in the way specified for the purpose of use of the derivative instrument. The profit and loss effects of the changes to the values of derivative instruments where hedge accounting is applied, and which are effective hedging instruments, are presented uniformly with the hedged item. When entered into, derivative financial instruments are treated as fair value hedges of receivables, liabilities or fixed commitments, or, in the case of currency exchange risk, as mon-ey flow hedges, money flow hedges for an anticipated and highly likely commercial transaction, as hedges of net investments in a foreign unit, or as derivative financial instruments that do not meet the hedge accounting criteria.

When a hedging arrangement is entered into, the relationship between the item being hedged and the hedging instrument, as well as the objectives of the Group’s risk management and the hedging strategy are documented. When starting out, and at least every time the financial accounts are being prepared, the Group documents the effectiveness of qualifying derivatives by examining their ability to offset changes to the fair value of the hedged item or money streams.

Money flow hedging

The change in the fair value of the effective portion of derivative instruments qualifying for hedge cash flow is recognised in other comprehensive income and presented in the hedge fund under equity (in Other funds). The gains and losses accumulated in equity from hedging instruments are transferred to the statement of income when the hedged item impacts on profit or loss. Gains and losses from derivatives hedging an anticipated sale in a for-eign currency are recognised as sales adjustments when the sale goes ahead. The ineffective portion of a derivative instrument is recognised in other operating income and expenses. If a hedged, anticipated commercial transaction leads to the recognition of an asset not included in financial assets, such as a tangible fixed asset, the gains and losses accumulated in equity are reclassified as an adjustment to the acquisition cost of that asset. When a derivative financial instrument acquired for money flow hedging matures or is sold, or when the conditions of hedge accounting are no longer met, the gain or loss from the derivative instrument remains under equity until such time as the anticipated commer-cial transaction takes place. However, if that is no longer expect-ed to happen, the gain or loss under equity is directly recognised through profit or loss.

Other hedging instruments where hedge accounting does not apply