Embed Size (px)

Citation preview

Managing Liquidity : Be Prepared for the New Reality

September 2014

Not FDIC insured. May lose value. No bank guarantee.

Not NCUA or NCUSIF insured. May lose value. No

credit union guarantee.

For Institutional Investor Use Only

1

1. Overview of Regulatory Changes

2. Investment Implications & Potential Solutions

3. Investment Policy Implications

4. Path to Higher Interest Rates

Information provided is as of the date listed and may be subject to change. Fidelity is not responsible for any direct on incidental

loss resulting from any investment decision based upon information provided herein. Moreover, Fidelity is not engaged in

rendering any legal, tax, accounting or investment advice, nor should any of the information be construed as an recommendation

or solicitation to buy, sell or hold any investment product.

Agenda

For Institutional Investor Use Only

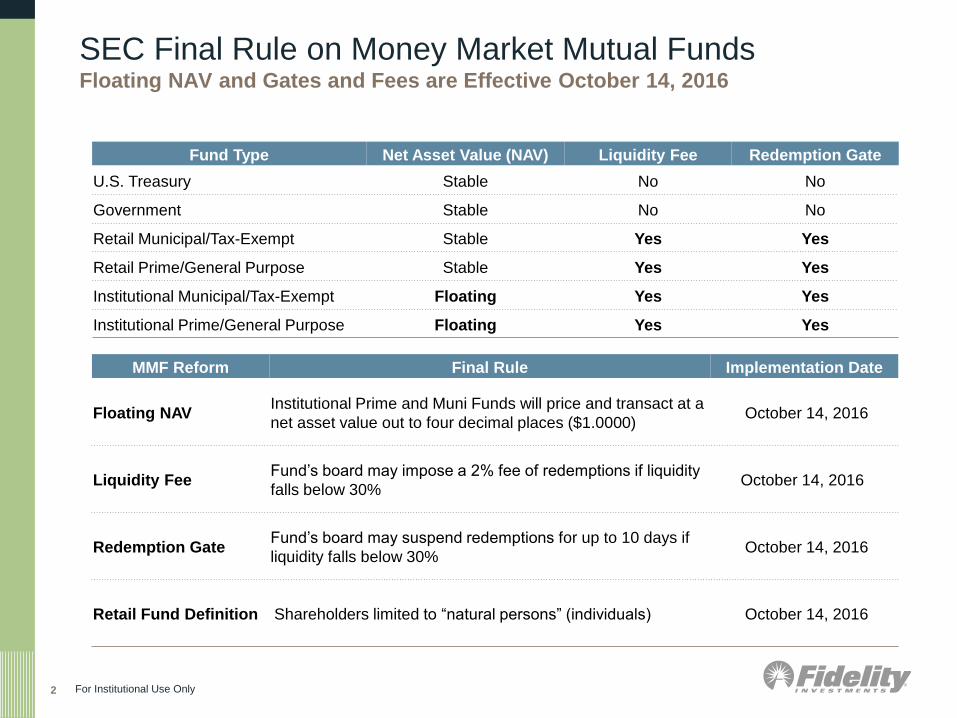

SEC Final Rule on Money Market Mutual Funds Floating NAV and Gates and Fees are Effective October 14, 2016

Fund Type Net Asset Value (NAV) Liquidity Fee Redemption Gate

U.S. Treasury Stable No No

Government Stable No No

Retail Municipal/Tax-Exempt Stable Yes Yes

Retail Prime/General Purpose Stable Yes Yes

Institutional Municipal/Tax-Exempt Floating Yes Yes

Institutional Prime/General Purpose Floating Yes Yes

MMF Reform Final Rule Implementation Date

Floating NAV Institutional Prime and Muni Funds will price and transact at a

net asset value out to four decimal places ($1.0000) October 14, 2016

Liquidity Fee Fund’s board may impose a 2% fee of redemptions if liquidity

falls below 30% October 14, 2016

Redemption Gate Fund’s board may suspend redemptions for up to 10 days if

liquidity falls below 30% October 14, 2016

Retail Fund Definition Shareholders limited to “natural persons” (individuals) October 14, 2016

For Institutional Use Only 2

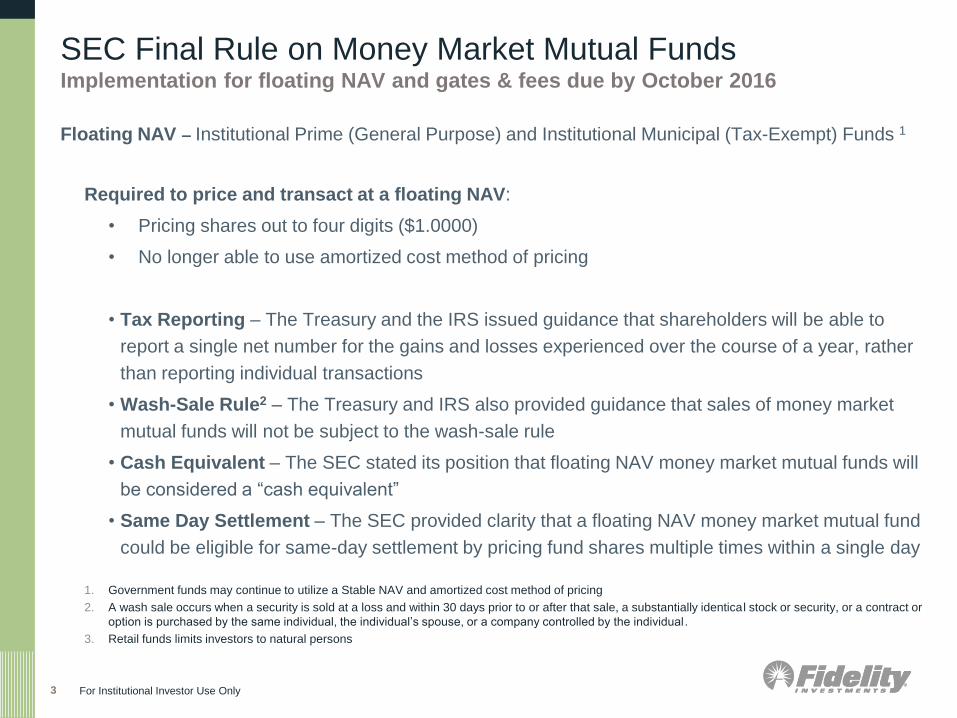

SEC Final Rule on Money Market Mutual Funds Implementation for floating NAV and gates & fees due by October 2016

Floating NAV – Institutional Prime (General Purpose) and Institutional Municipal (Tax-Exempt) Funds 1

Required to price and transact at a floating NAV:

• Pricing shares out to four digits ($1.0000)

• No longer able to use amortized cost method of pricing

• Tax Reporting – The Treasury and the IRS issued guidance that shareholders will be able to

report a single net number for the gains and losses experienced over the course of a year, rather

than reporting individual transactions

• Wash-Sale Rule2 – The Treasury and IRS also provided guidance that sales of money market

mutual funds will not be subject to the wash-sale rule

• Cash Equivalent – The SEC stated its position that floating NAV money market mutual funds will

be considered a “cash equivalent”

• Same Day Settlement – The SEC provided clarity that a floating NAV money market mutual fund

could be eligible for same-day settlement by pricing fund shares multiple times within a single day

1. Government funds may continue to utilize a Stable NAV and amortized cost method of pricing

2. A wash sale occurs when a security is sold at a loss and within 30 days prior to or after that sale, a substantially identical stock or security, or a contract or

option is purchased by the same individual, the individual’s spouse, or a company controlled by the individual .

3. Retail funds limits investors to natural persons

For Institutional Investor Use Only 3

For Institutional Investor Use Only

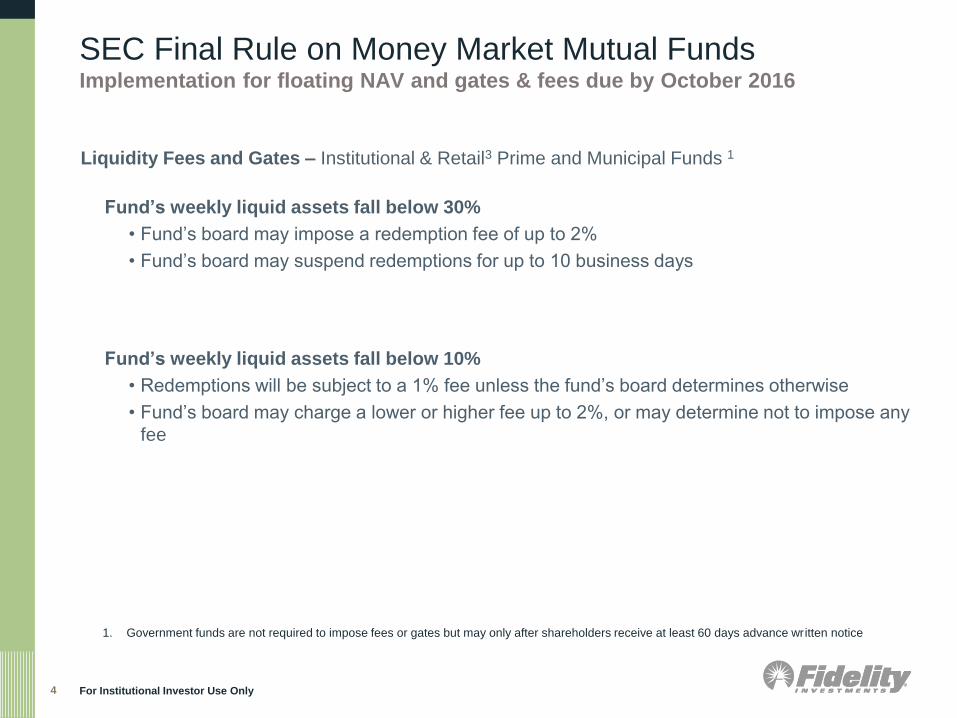

Liquidity Fees and Gates – Institutional & Retail3 Prime and Municipal Funds 1

Fund’s weekly liquid assets fall below 30%

• Fund’s board may impose a redemption fee of up to 2%

• Fund’s board may suspend redemptions for up to 10 business days

Fund’s weekly liquid assets fall below 10%

• Redemptions will be subject to a 1% fee unless the fund’s board determines otherwise

• Fund’s board may charge a lower or higher fee up to 2%, or may determine not to impose any

fee

4

SEC Final Rule on Money Market Mutual Funds Implementation for floating NAV and gates & fees due by October 2016

1. Government funds are not required to impose fees or gates but may only after shareholders receive at least 60 days advance written notice

SEC Final Rule on Money Market Mutual Funds Disclosures, diversification and stress testing due in 9-18 month

Fidelity Confidential Information

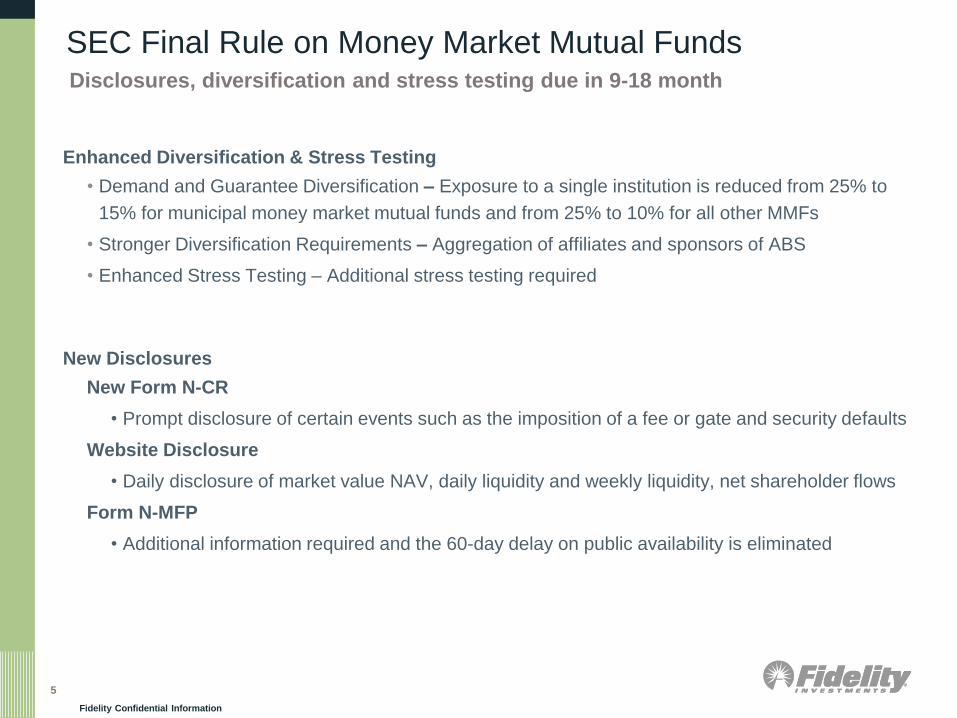

Enhanced Diversification & Stress Testing

• Demand and Guarantee Diversification – Exposure to a single institution is reduced from 25% to

15% for municipal money market mutual funds and from 25% to 10% for all other MMFs

• Stronger Diversification Requirements – Aggregation of affiliates and sponsors of ABS

• Enhanced Stress Testing – Additional stress testing required

New Disclosures

New Form N-CR

• Prompt disclosure of certain events such as the imposition of a fee or gate and security defaults

Website Disclosure

• Daily disclosure of market value NAV, daily liquidity and weekly liquidity, net shareholder flows

Form N-MFP

• Additional information required and the 60-day delay on public availability is eliminated

5

Additional Rule Proposals

For Institutional Investor Use Only

Proposes Changes to Credit Ratings

• A security would be eligible for purchase only if the fund’s board of directors determines that it

presents minimal credit risks

• Re-proposed amendments to Form N-MFP would require that a money market mutual fund

disclose any credit rating that the fund’s board considered in determining that a portfolio

security presents minimal credit risks

Proposes Changes to Issuer Diversification

• Proposed amendment to issuer diversification provisions to eliminate an exclusion from these

provisions that is currently available for securities subject to a guarantee issued by a non-

controlled person

Proposes Changes to Exemptive Relief

• Exempt broker-dealers from the written notification requirement under Rule 10b-10(a) of the

Exchange Act for transactions effected in shares of floating NAV money market mutual funds

6

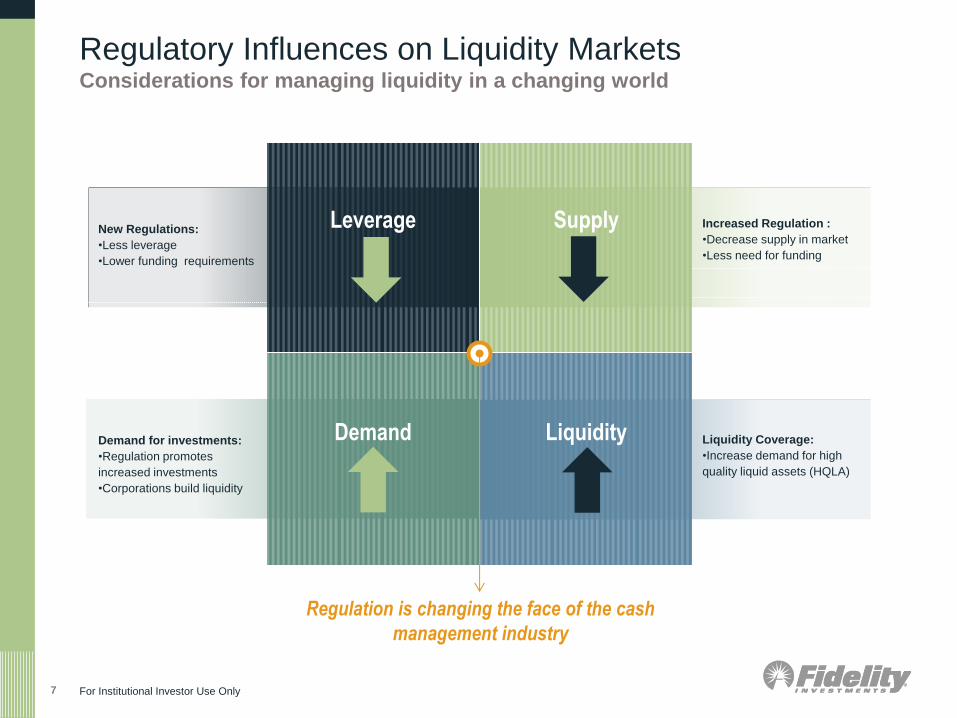

Regulatory Influences on Liquidity Markets Considerations for managing liquidity in a changing world

Leverage

New Regulations:

•Less leverage

•Lower funding requirements

Demand

Demand for investments:

•Regulation promotes

increased investments

•Corporations build liquidity

Supply

Liquidity

Increased Regulation :

•Decrease supply in market

•Less need for funding

Liquidity Coverage:

•Increase demand for high

quality liquid assets (HQLA)

Regulation is changing the face of the cash

management industry

7 For Institutional Investor Use Only

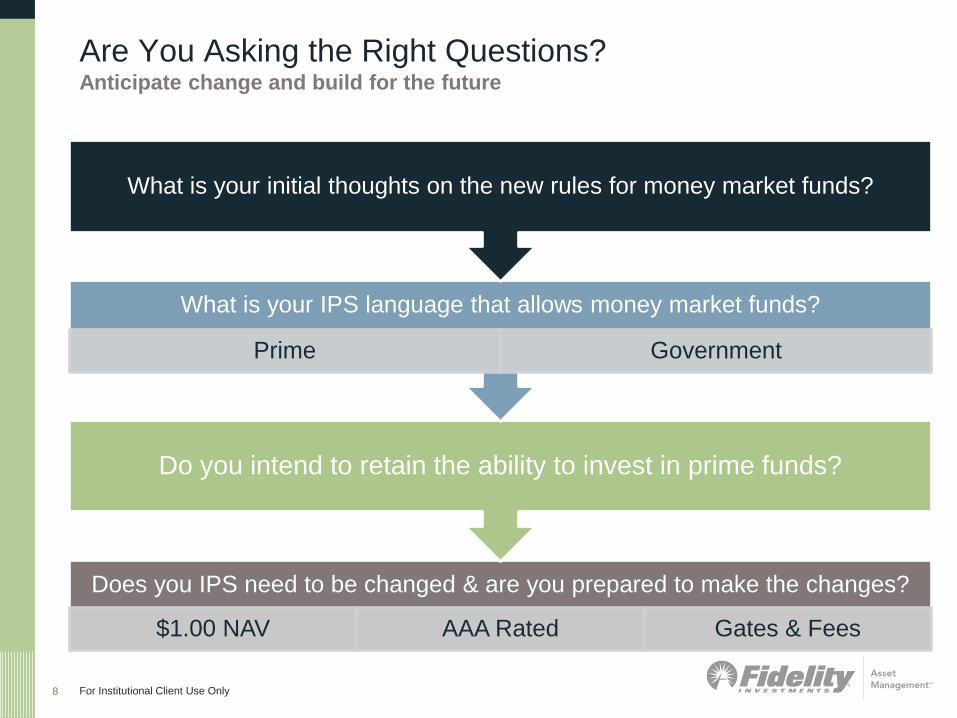

Are You Asking the Right Questions? Anticipate change and build for the future

Does you IPS need to be changed & are you prepared to make the changes?

$1.00 NAV AAA Rated Gates & Fees

Do you intend to retain the ability to invest in prime funds?

What is your IPS language that allows money market funds?

Prime Government

What is your initial thoughts on the new rules for money market funds?

8 For Institutional Client Use Only

Investment Implications : Potential Solutions

New Liquidity Rules – New Investment Considerations

For Institutional Use Only

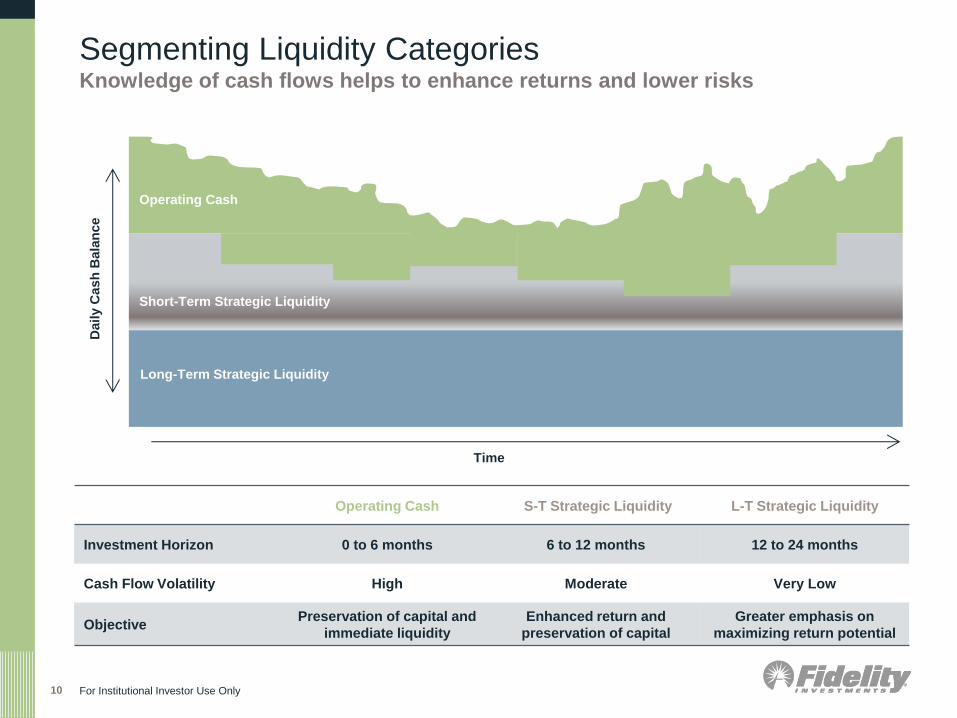

Segmenting Liquidity Categories Knowledge of cash flows helps to enhance returns and lower risks

10

Operating Cash S-T Strategic Liquidity L-T Strategic Liquidity

Investment Horizon 0 to 6 months 6 to 12 months 12 to 24 months

Cash Flow Volatility High Moderate Very Low

Objective Preservation of capital and

immediate liquidity

Enhanced return and

preservation of capital

Greater emphasis on

maximizing return potential

Daily C

ash

Bala

nce

Long-Term Strategic Liquidity

Short-Term Strategic Liquidity

Operating Cash

For Institutional Investor Use Only

Time

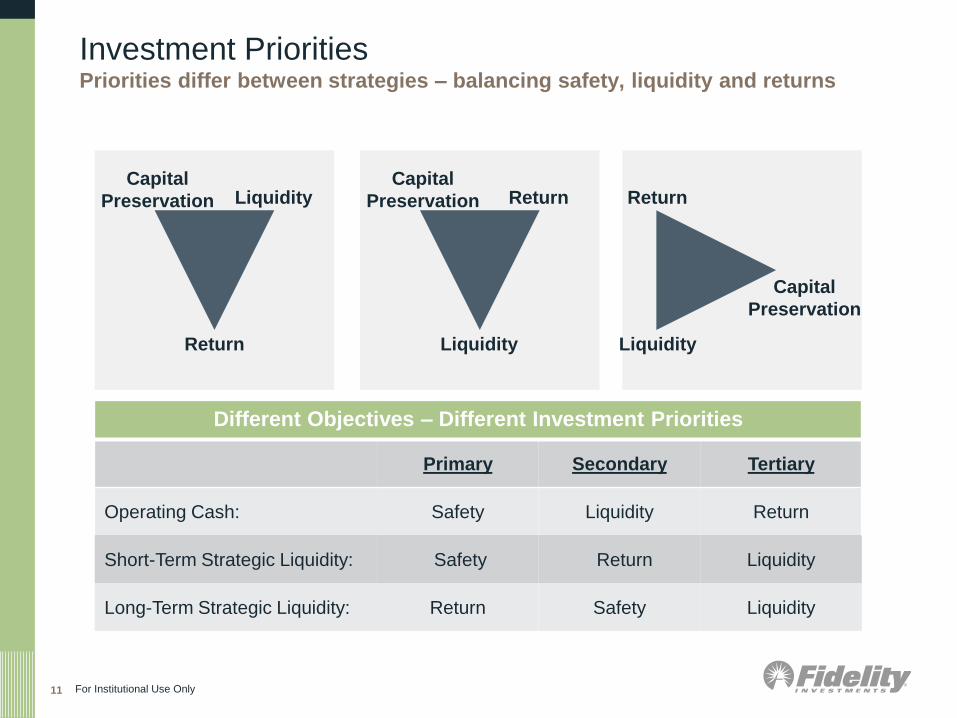

Investment Priorities Priorities differ between strategies – balancing safety, liquidity and returns

For Institutional Use Only 11

Capital

Preservation Liquidity

Return

Capital

Preservation Return

Liquidity

Capital

Preservation

Return

Liquidity

Different Objectives – Different Investment Priorities

Primary Secondary Tertiary

Operating Cash: Safety Liquidity Return

Short-Term Strategic Liquidity: Safety Return Liquidity

Long-Term Strategic Liquidity: Return Safety Liquidity

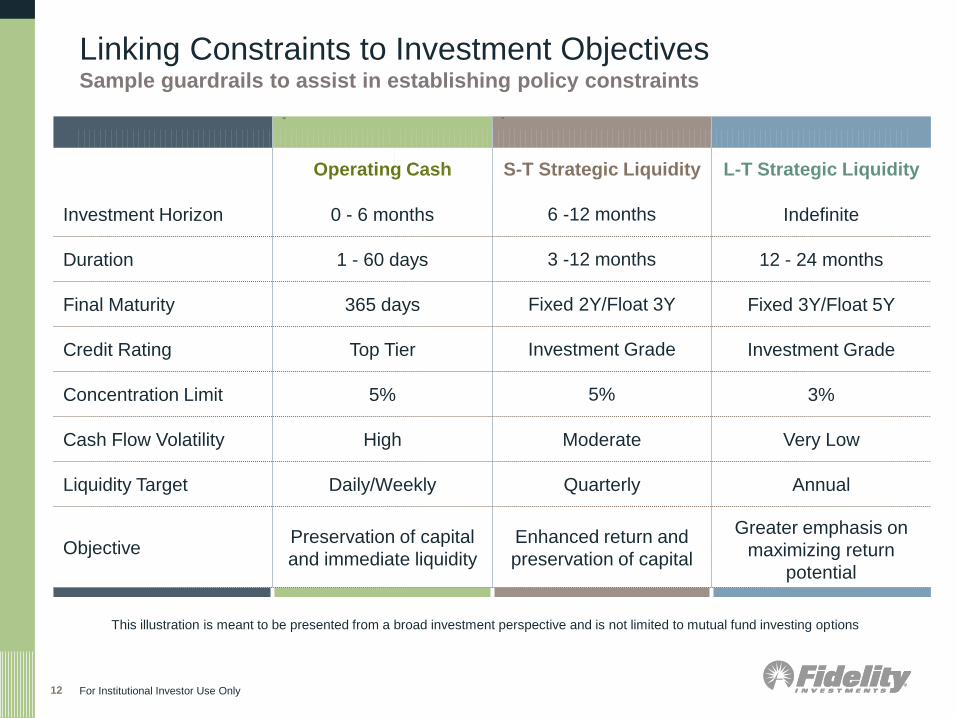

Linking Constraints to Investment Objectives Sample guardrails to assist in establishing policy constraints

For Institutional Investor Use Only 12

Op S

Operating Cash S-T Strategic Liquidity L-T Strategic Liquidity

Investment Horizon 0 - 6 months 6 -12 months Indefinite

Duration 1 - 60 days 3 -12 months 12 - 24 months

Final Maturity 365 days Fixed 2Y/Float 3Y Fixed 3Y/Float 5Y

Credit Rating Top Tier Investment Grade Investment Grade

Concentration Limit 5% 5% 3%

Cash Flow Volatility High Moderate Very Low

Liquidity Target Daily/Weekly Quarterly Annual

Objective Preservation of capital

and immediate liquidity

Enhanced return and

preservation of capital

Greater emphasis on

maximizing return

potential

add disclosure to

clarify that this

slide is speaking

from a broad

investment

perspective not

mutual fund. for

example of

possible wording "

This illustration is

meant to be

presented from a

broad investment

perspective and is

not limited to

mutual fund

investing options" This illustration is meant to be presented from a broad investment perspective and is not limited to mutual fund investing options

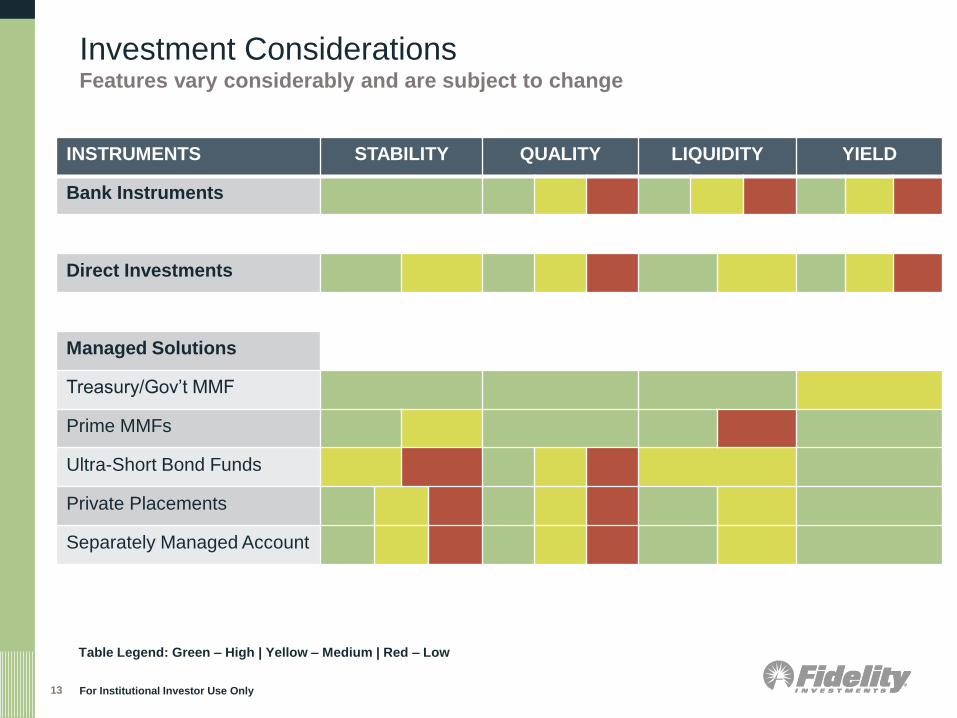

Investment Considerations Features vary considerably and are subject to change

For Institutional Investor Use Only 13

INSTRUMENTS STABILITY QUALITY LIQUIDITY YIELD

Bank Instruments

Direct Investments

Managed Solutions

Treasury/Gov’t MMF

Prime MMFs

Ultra-Short Bond Funds

Private Placements

Separately Managed Account

Table Legend: Green – High | Yellow – Medium | Red – Low

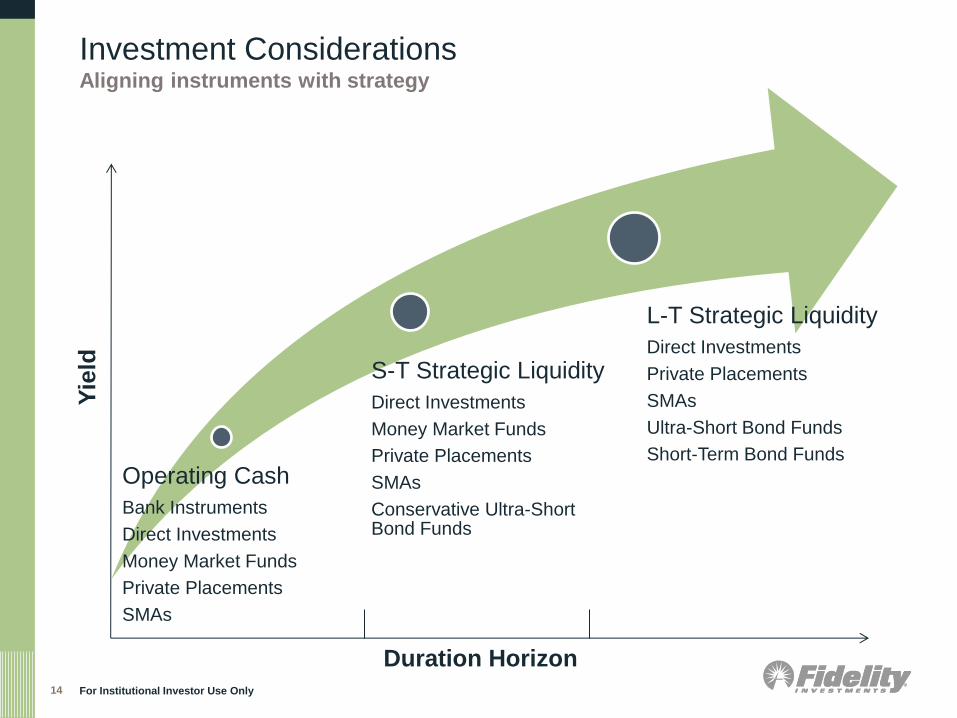

Investment Considerations Aligning instruments with strategy

For Institutional Investor Use Only 14

Operating Cash

Bank Instruments

Direct Investments

Money Market Funds

Private Placements

SMAs

S-T Strategic Liquidity

Direct Investments

Money Market Funds

Private Placements

SMAs

Conservative Ultra-Short Bond Funds

L-T Strategic Liquidity

Direct Investments

Private Placements

SMAs

Ultra-Short Bond Funds

Short-Term Bond Funds

Duration Horizon

Yie

ld

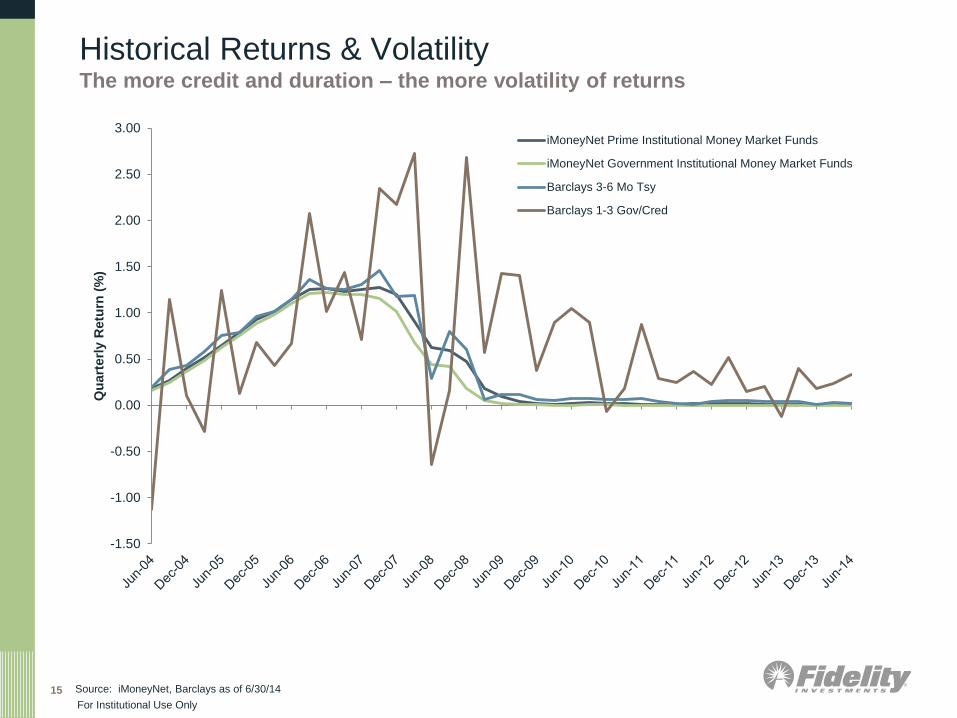

Historical Returns & Volatility The more credit and duration – the more volatility of returns

Source: iMoneyNet, Barclays as of 6/30/14 15

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Qu

art

erl

y R

etu

rn (

%)

iMoneyNet Prime Institutional Money Market Funds

iMoneyNet Government Institutional Money Market Funds

Barclays 3-6 Mo Tsy

Barclays 1-3 Gov/Cred

For Institutional Use Only

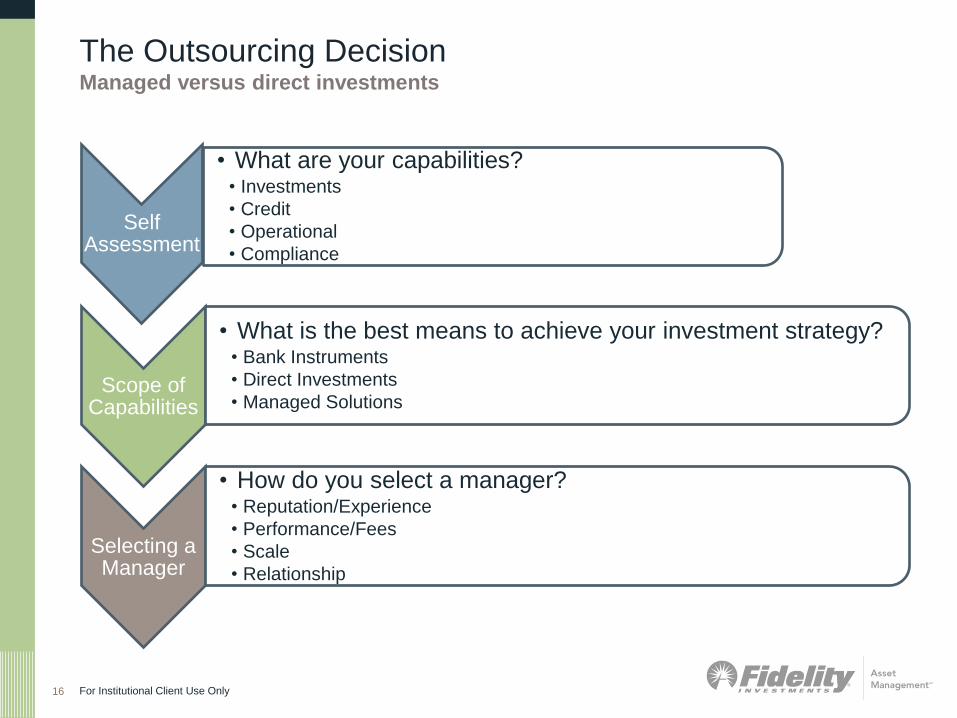

The Outsourcing Decision Managed versus direct investments

Self Assessment

• What are your capabilities? • Investments

• Credit

• Operational

• Compliance

Scope of Capabilities

• What is the best means to achieve your investment strategy? • Bank Instruments

• Direct Investments

• Managed Solutions

Selecting a Manager

• How do you select a manager? • Reputation/Experience

• Performance/Fees

• Scale

• Relationship

16 For Institutional Client Use Only

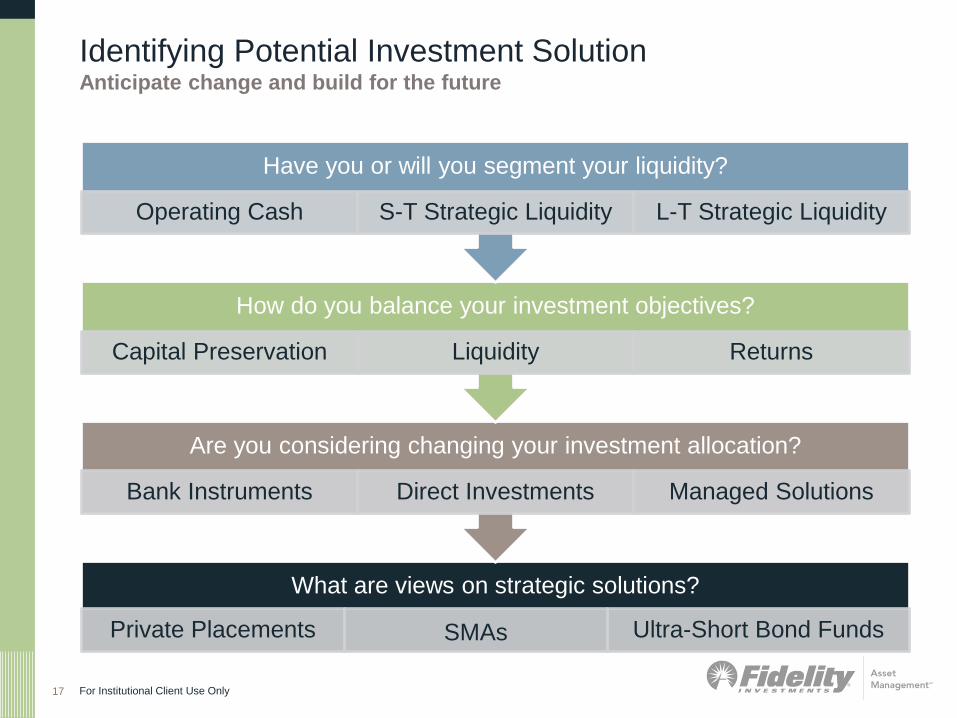

Identifying Potential Investment Solution Anticipate change and build for the future

What are views on strategic solutions?

Private Placements SMAs Ultra-Short Bond Funds

Are you considering changing your investment allocation?

Bank Instruments Direct Investments Managed Solutions

How do you balance your investment objectives?

Capital Preservation Liquidity Returns

Have you or will you segment your liquidity?

Operating Cash S-T Strategic Liquidity L-T Strategic Liquidity

17 For Institutional Client Use Only

Policy Implications : Potential Solutions

New Liquidity Rules – New Policy Considerations

For Institutional Use Only

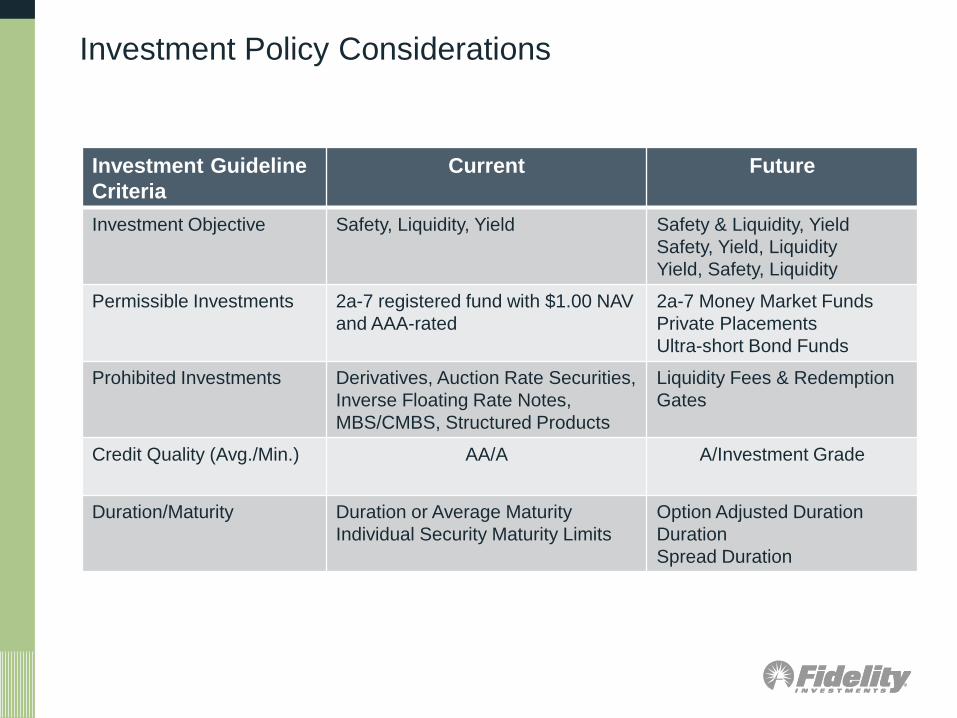

Investment Policy Considerations

Investment Guideline

Criteria

Current Future

Investment Objective Safety, Liquidity, Yield Safety & Liquidity, Yield

Safety, Yield, Liquidity

Yield, Safety, Liquidity

Permissible Investments 2a-7 registered fund with $1.00 NAV

and AAA-rated

2a-7 Money Market Funds

Private Placements

Ultra-short Bond Funds

Prohibited Investments

Derivatives, Auction Rate Securities,

Inverse Floating Rate Notes,

MBS/CMBS, Structured Products

Liquidity Fees & Redemption

Gates

Credit Quality (Avg./Min.) AA/A A/Investment Grade

Duration/Maturity Duration or Average Maturity

Individual Security Maturity Limits

Option Adjusted Duration

Duration

Spread Duration

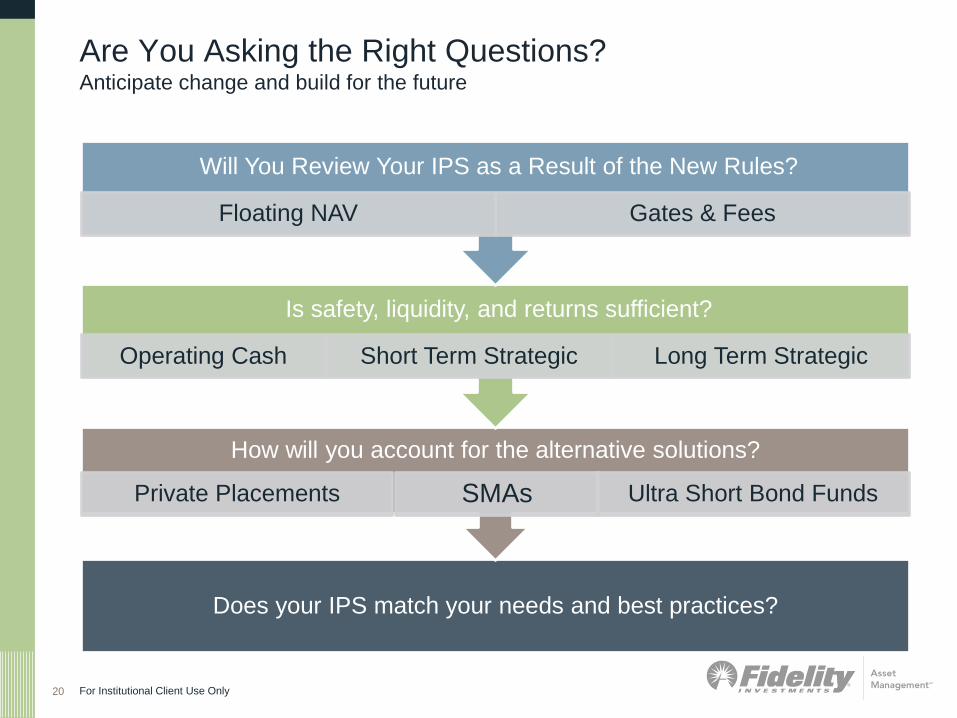

Are You Asking the Right Questions? Anticipate change and build for the future

Does your IPS match your needs and best practices?

How will you account for the alternative solutions?

Private Placements SMAs Ultra Short Bond Funds

Is safety, liquidity, and returns sufficient?

Operating Cash Short Term Strategic Long Term Strategic

Will You Review Your IPS as a Result of the New Rules?

Floating NAV Gates & Fees

20 For Institutional Client Use Only

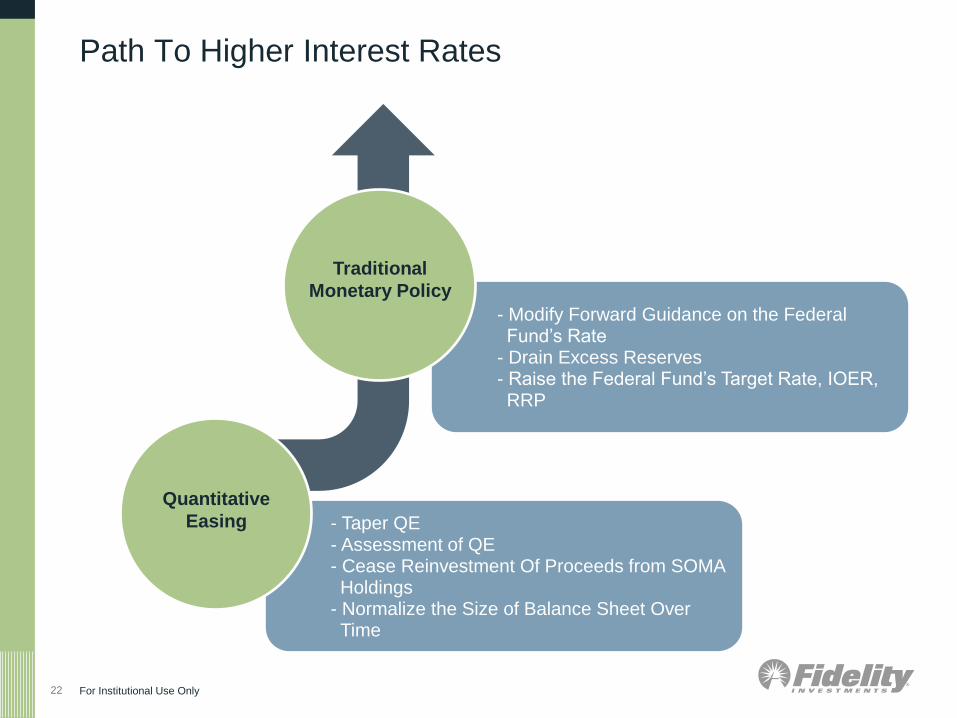

The Path to Higher Interest Rates

For Institutional Use Only

- Taper QE - Assessment of QE - Cease Reinvestment Of Proceeds from SOMA Holdings

- Normalize the Size of Balance Sheet Over Time

- Modify Forward Guidance on the Federal Fund’s Rate

- Drain Excess Reserves - Raise the Federal Fund’s Target Rate, IOER, RRP

Path To Higher Interest Rates

For Institutional Use Only 22

Traditional

Monetary Policy

Quantitative

Easing

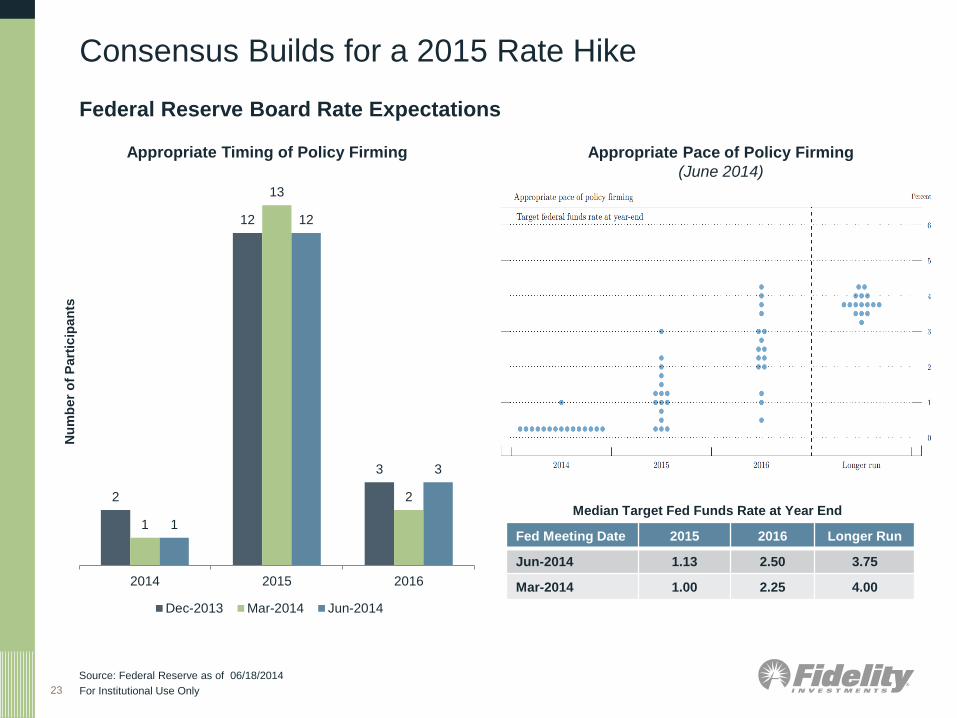

Consensus Builds for a 2015 Rate Hike

23

Source: Federal Reserve as of 06/18/2014

Federal Reserve Board Rate Expectations

Appropriate Pace of Policy Firming

(June 2014)

Fed Meeting Date 2015 2016 Longer Run

Jun-2014 1.13 2.50 3.75

Mar-2014 1.00 2.25 4.00

Median Target Fed Funds Rate at Year End 2

12

3

1

13

2

1

12

3

2014 2015 2016

Nu

mb

er

of

Part

icip

an

ts

Appropriate Timing of Policy Firming

Dec-2013 Mar-2014 Jun-2014

For Institutional Use Only

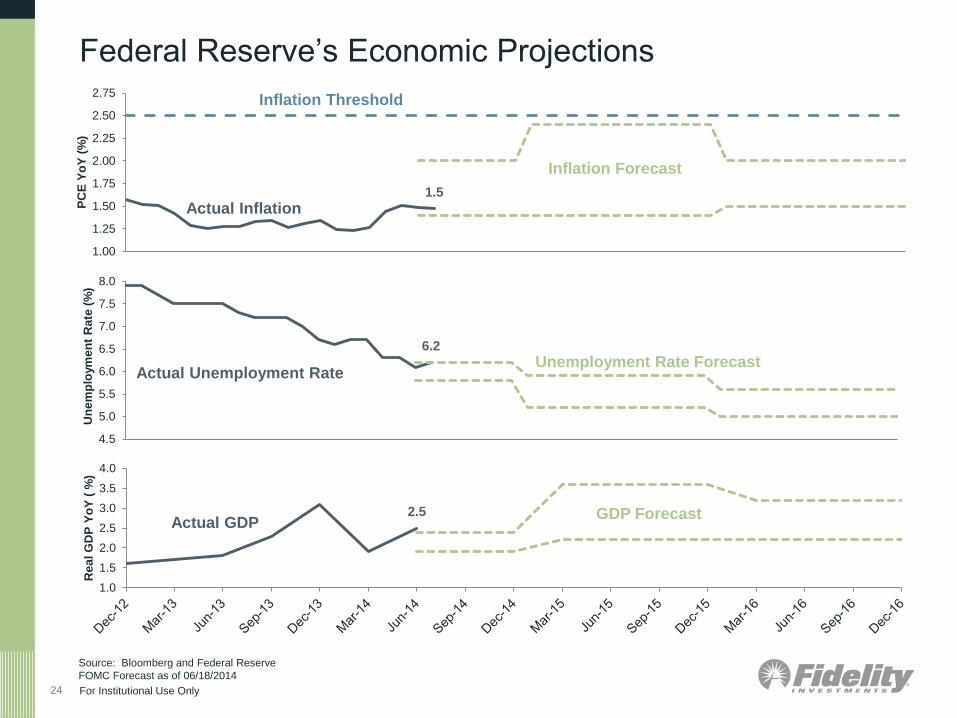

Federal Reserve’s Economic Projections

Source: Bloomberg and Federal Reserve

FOMC Forecast as of 06/18/2014

6.2

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Un

em

plo

ym

en

t R

ate

(%

)

1.5

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75P

CE

Yo

Y (

%)

2.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Rea

l G

DP

Yo

Y (

%)

Actual Inflation

Inflation Forecast

Unemployment Rate Forecast Actual Unemployment Rate

Actual GDP GDP Forecast

Inflation Threshold

24 For Institutional Use Only

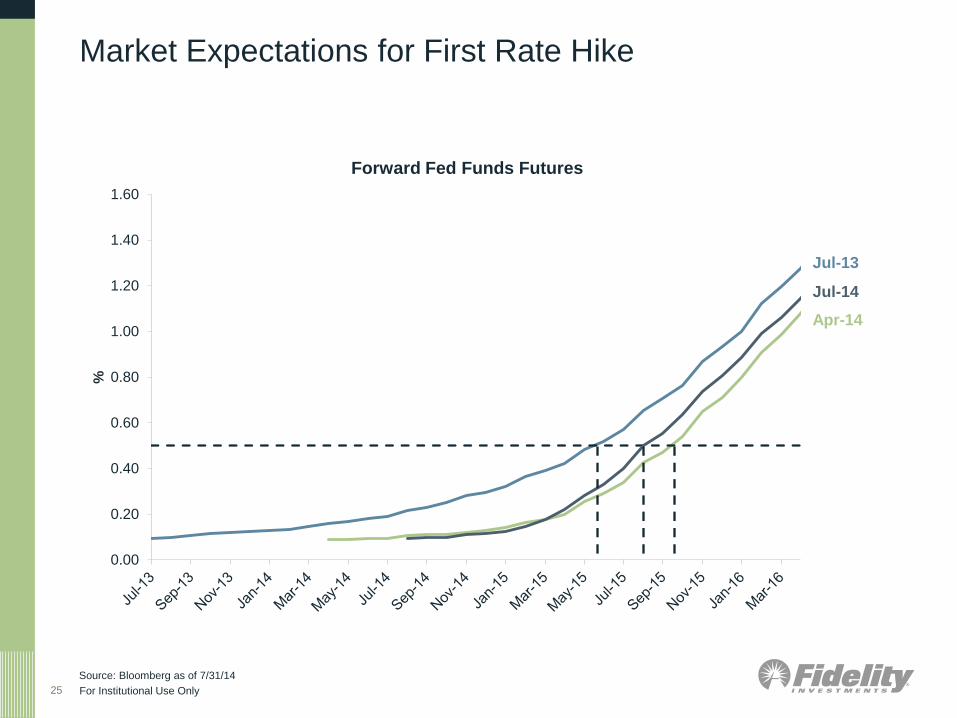

Market Expectations for First Rate Hike

25

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

%

Forward Fed Funds Futures

Source: Bloomberg as of 7/31/14

Apr-14

Jul-13

For Institutional Use Only

Jul-14

For Institutional Use Only

Important Information

Read this important information carefully before making any investment. Speak with your relationship manager if you have any

questions.

Risks

Hypothetical returns have many inherent limitations. Unlike actual performance, it does not represent actual trading. Since trades have not

actually been executed, results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of

liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process.

Hypothetical performance also is developed with the benefit of hindsight. Actual performance may differ substantially from the hypothetical

performance presented. There can be no assurance that this strategy will achieve profits or avoid incurring substantial losses.

Past performance is no guarantee of future results. An investment may be risky and may not be suitable for an investor's goals, objectives

and risk tolerance. Investors should be aware that an investment's value may be volatile and any investment involves the risk that you may

lose money. Performance results for individual accounts will differ from performance results for composites and representative accounts

due to factors such as portfolio size, account objectives and restrictions, and factors specific to a particular investment structure.

The value of a strategy's investments will vary day to day in response to many factors, including in response to adverse issuer, political,

regulatory, market or economic developments. The value of an individual security or a particular type of security can be more volatile than

the market as a whole and can perform differently from the value of the market as a whole.

The performance of fixed income strategies will change daily based on changes in interest rates and market conditions and in response to

other economic, political or financial developments. Debt securities are sensitive to changes in interest rates depending on their maturity,

and may involve the risk that their prices may decline if interest rates rise or, conversely, if interest rates decline, their prices may increase.

Debt securities carry the risk of default, prepayment risk and inflation risk. Changes specific to an issuer, which may involve its financial

condition or economic environment, can affect the credit quality or value of an issuer's securities. Lower-quality debt securities (those of

less than investment grade quality, also referred to as high yield debt securities) and certain types of other securities are more volatile and

are often considered to be speculative and involve greater risk due to increased sensitivity to adverse issuer, political, regulatory and

market developments, especially in periods of general economic difficulty. The value of mortgage securities may change due to shifts in

the market's perception of issuers and changes in interest rates, regulatory or tax changes.

Derivatives may be volatile and involve significant risk, such as credit risk, currency risk, leverage risk, counterparty risk and liquidity risk.

Using derivatives can disproportionately increase losses and reduce opportunities for gains in certain circumstances. Investments in

derivatives may have limited liquidity and may be harder to value, especially in declining markets. Derivatives involve leverage because

they can provide investment exposure in an amount exceeding the initial investment. Leverage can magnify investment risks and cause

losses to be realized more quickly. A small change in the underlying asset, instrument, or index can lead to a significant loss. Assets

segregated to cover these transactions may decline in value and are not available to meet redemptions. Government legislation or

regulation could affect the use of these transactions and could limit the ability to pursue such investment strategies.

26

Important Information

Not NCUA or NCUSIF insured. May lose value. No credit union guarantee.

Lipper Analytical Services, Inc., is a nationally recognized organization that ranks the performance of mutual funds.

The views expressed in this statement reflect those of the portfolio manager only through the end of the period of the report as stated on the

cover and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to

change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may

not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be

relied on as an indication of trading intent on behalf of any Fidelity fund.

Past performance is no guarantee of future results. Investment return will fluctuate, therefore you may have a gain or loss when you sell

shares.

Diversification does not ensure a profit or guarantee against a loss.

An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance

Corporation or any other government agency. Although the fund seeks to preserve the value of your

investment at $1.00 per share, it is possible to lose money by investing in the fund. Interest rate increases

can cause the price of money market securities to decrease.

Before investing, have your client consider the funds’ investment objectives, risks, charges, and expenses.

Contact Fidelity for a prospectus or, if available, a summary prospectus containing this information. Have

your client read it carefully.

Fidelity Investments & Pyramid Design is a registered service mark of FMR LLC.

Fidelity Investments Institutional Services Company, Inc., 500 Salem Street, Smithfield, RI 02917

27

Not FDIC insured. May lose value. No bank guarantee.

For Institutional Use Only

698632.1.0