Embed Size (px)

Citation preview

1

BHUTAN COUNTRY SNAPSHOT

The World Bank Group October 2014

Bhutan Country Snapshot

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

2

BHUTAN COUNTRY SNAPSHOT

COUNTRY SNAPSHOT

Recent Economic and Sector Developments

The economy is estimated to have grown at six percent in 2013-14, still constrained by various

administrative restrictions in place on credit, foreign exchange and imports limiting the expansion of

aggregate demand and lower than expected hydropower generation. For the first half of 2014, hydropower

(annualized) generation has declined by two percent due to lesser rainfall compared to 2013 (hydropower

projects are run-off-the river, so electricity generation depends on the amount of rainfall). Meanwhile,

tourism recorded a marked expansion following the introduction of new measures aimed at boosting tourism

during the low season months of June to August.1 Tourist arrivals more than doubled in June-July and grew by

12 percent year-on-year as of July 2014.

In 2012, corrective administrative measures to stop the rupee shortage led to a sudden halt in construction

and service growth in 2012 that, combined with a poor record in agriculture, contracted growth to 4.6

percent – the lowest level since 2008. Construction in hydropower has been sustained, with four projects

being built at an average annual investment cost of 28 percent of GDP. Domestic sales of cement, a good proxy

for construction-sector activities, slowed markedly in the first half of 2014, despite the Nu10.9 billion (about

$180 million) Dungsam Cement mega-project starting production.

In spite of the uncertainty and volatility in the external sector, economic growth is projected to be 6.8

percent in FY 2014-15. This growth will be driven by expansion in construction (including hydropower) and

a rebound of aggregate demand, boosted by the increase in public wages and allowances concomitant with

the lift of bans over housing/construction loans.

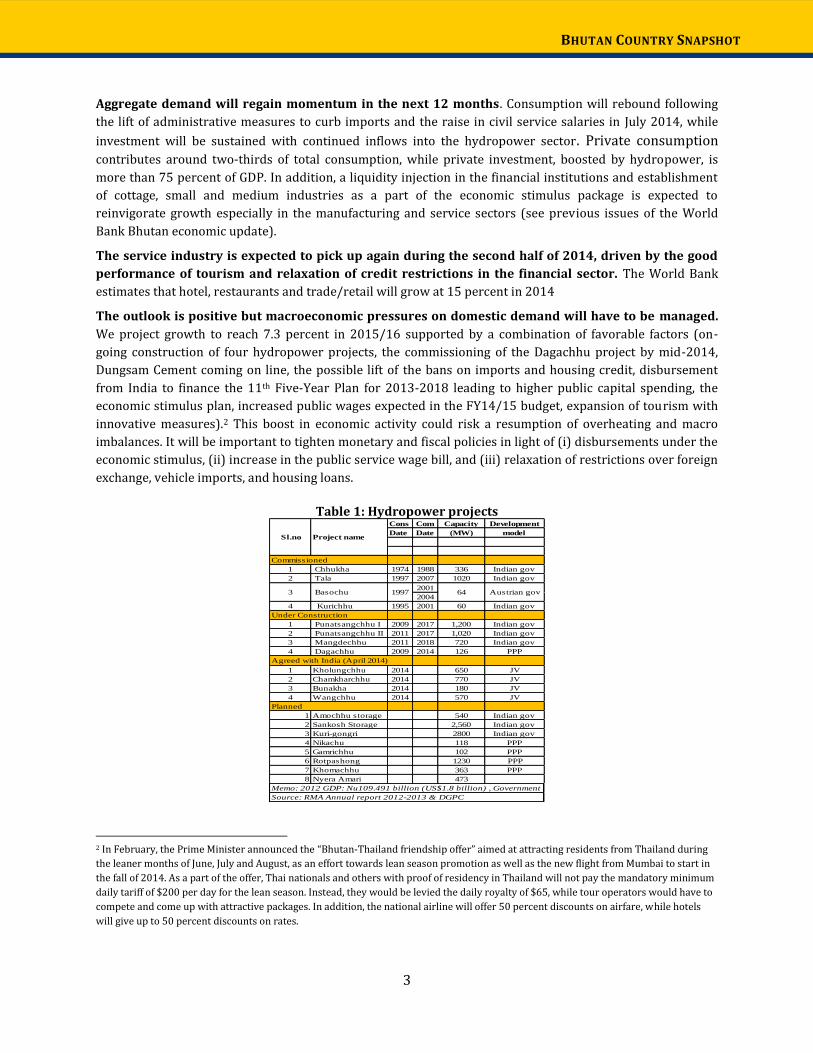

In 2014-15, the electricity sector is projected to contribute to growth with the commissioning of the

Dagachhu hydroelectric project by the end of September 2014. Hydropower construction will continue. Four

new projects have been agreed with the Government of India, under a Joint Venture mode, in April 2014 (see

Table 1). In June 2014, the 600MW Joint-Venture Kholongchu Hydro-electric project was inaugurated by

Indian Prime Minister Modi during his visit to Bhutan.

Figure 1: Economic Growth

Sources: National Statistical Bureau and Macroeconomic Framework Coordination Committee (MFCC)

1 Under the Bhutan-Thailand friendship initiative, Thai residents were offered a special package during the low season, including a 50 percent discount in airfare and hotel, and did not have to pay the mandatory minimum daily tariff of $200 a day for the lean season. Instead, they would be only levied the daily royalty of USD 65.

3

BHUTAN COUNTRY SNAPSHOT

Aggregate demand will regain momentum in the next 12 months. Consumption will rebound following

the lift of administrative measures to curb imports and the raise in civil service salaries in July 2014, while

investment will be sustained with continued inflows into the hydropower sector. Private consumption contributes around two-thirds of total consumption, while private investment, boosted by hydropower, is

more than 75 percent of GDP. In addition, a liquidity injection in the financial institutions and establishment

of cottage, small and medium industries as a part of the economic stimulus package is expected to

reinvigorate growth especially in the manufacturing and service sectors (see previous issues of the World

Bank Bhutan economic update).

The service industry is expected to pick up again during the second half of 2014, driven by the good

performance of tourism and relaxation of credit restrictions in the financial sector. The World Bank

estimates that hotel, restaurants and trade/retail will grow at 15 percent in 2014

The outlook is positive but macroeconomic pressures on domestic demand will have to be managed.

We project growth to reach 7.3 percent in 2015/16 supported by a combination of favorable factors (on-

going construction of four hydropower projects, the commissioning of the Dagachhu project by mid-2014,

Dungsam Cement coming on line, the possible lift of the bans on imports and housing credit, disbursement

from India to finance the 11th Five-Year Plan for 2013-2018 leading to higher public capital spending, the

economic stimulus plan, increased public wages expected in the FY14/15 budget, expansion of tourism with

innovative measures).2 This boost in economic activity could risk a resumption of overheating and macro

imbalances. It will be important to tighten monetary and fiscal policies in light of (i) disbursements under the

economic stimulus, (ii) increase in the public service wage bill, and (iii) relaxation of restrictions over foreign

exchange, vehicle imports, and housing loans.

Table 1: Hydropower projects

2 In February, the Prime Minister announced the “Bhutan-Thailand friendship offer” aimed at attracting residents from Thailand during

the leaner months of June, July and August, as an effort towards lean season promotion as well as the new flight from Mumbai to start in

the fall of 2014. As a part of the offer, Thai nationals and others with proof of residency in Thailand will not pay the mandatory minimum

daily tariff of $200 per day for the lean season. Instead, they would be levied the daily royalty of $65, while tour operators would have to

compete and come up with attractive packages. In addition, the national airline will offer 50 percent discounts on airfare, while hotels

will give up to 50 percent discounts on rates.

Cons Com Capacity Development

Date Date (MW) model

1 Chhukha 1974 1988 336 Indian gov

2 Tala 1997 2007 1020 Indian gov

2001

2004

4 Kurichhu 1995 2001 60 Indian gov

1 Punatsangchhu I 2009 2017 1,200 Indian gov

2 Punatsangchhu II 2011 2017 1,020 Indian gov

3 Mangdechhu 2011 2018 720 Indian gov

4 Dagachhu 2009 2014 126 PPP

1 Kholungchhu 2014 650 JV

2 Chamkharchhu 2014 770 JV

3 Bunakha 2014 180 JV

4 Wangchhu 2014 570 JV

1 Amochhu storage 540 Indian gov

2 Sankosh Storage 2,560 Indian gov

3 Kuri-gongri 2800 Indian gov

4 Nikachu 118 PPP

5 Gamrichhu 102 PPP

6 Rotpashong 1230 PPP

7 Khomachhu 363 PPP

8 Nyera Amari 473

Sl.no Project name

Commissioned

Agreed with India (April 2014)

64 Austrian gov

Under Construction

Memo: 2012 GDP: Nu109.491 billion (US$1.8 billion) , Government

Source: RMA Annual report 2012-2013 & DGPC

3 Basochu 1997

Planned

4

BHUTAN COUNTRY SNAPSHOT

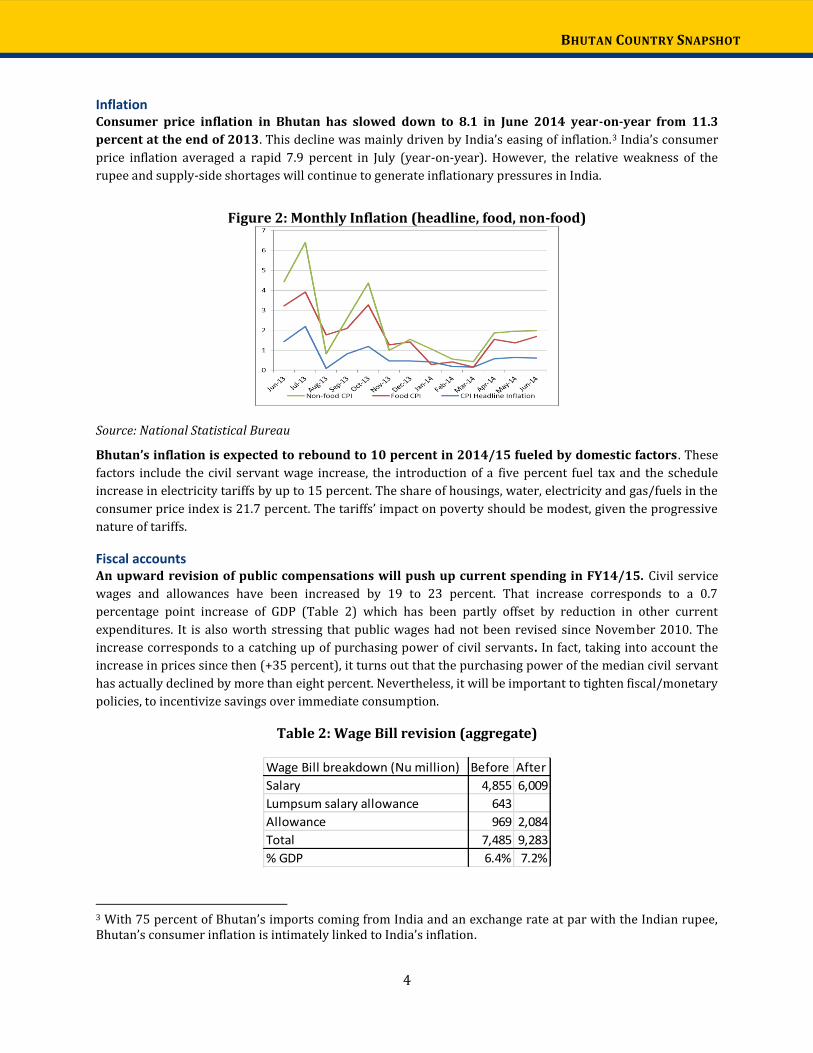

Inflation Consumer price inflation in Bhutan has slowed down to 8.1 in June 2014 year-on-year from 11.3

percent at the end of 2013. This decline was mainly driven by India’s easing of inflation.3 India’s consumer

price inflation averaged a rapid 7.9 percent in July (year-on-year). However, the relative weakness of the

rupee and supply-side shortages will continue to generate inflationary pressures in India.

Figure 2: Monthly Inflation (headline, food, non-food)

Source: National Statistical Bureau

Bhutan’s inflation is expected to rebound to 10 percent in 2014/15 fueled by domestic factors . These

factors include the civil servant wage increase, the introduction of a five percent fuel tax and the schedule

increase in electricity tariffs by up to 15 percent. The share of housings, water, electricity and gas/fuels in the

consumer price index is 21.7 percent. The tariffs’ impact on poverty should be modest, given the progressive

nature of tariffs.

Fiscal accounts An upward revision of public compensations will push up current spending in FY14/15. Civil service

wages and allowances have been increased by 19 to 23 percent. That increase corresponds to a 0.7

percentage point increase of GDP (Table 2) which has been partly offset by reduction in other current

expenditures. It is also worth stressing that public wages had not been revised since November 2010. The

increase corresponds to a catching up of purchasing power of civil servants. In fact, taking into account the

increase in prices since then (+35 percent), it turns out that the purchasing power of the median civil servant

has actually declined by more than eight percent. Nevertheless, it will be important to tighten fiscal/monetary

policies, to incentivize savings over immediate consumption.

Table 2: Wage Bill revision (aggregate)

3 With 75 percent of Bhutan’s imports coming from India and an exchange rate at par with the Indian rupee, Bhutan’s consumer inflation is intimately linked to India’s inflation.

Wage Bill breakdown (Nu million) Before After

Salary 4,855 6,009

Lumpsum salary allowance 643

Allowance 969 2,084

Total 7,485 9,283

% GDP 6.4% 7.2%

5

BHUTAN COUNTRY SNAPSHOT

Table 3: Pay scale revision (by level)

Source: Ministry of Finance and Royal Civil Service Commission

The government relies heavily on foreign grants to finance capital expenditure. That said, only

confirmed donor-funding is actually factored in the budget at the start of the Fiscal Year. It usually leads, as it

does this fiscal year, to an under-estimated capital spending budget, which will be revised as more donor

resources come in. The drop of the capital budget from 17.5 to 11.7 percent of GDP does not reflect the actual

projections of capital spending, but provide merely a very conservative estimate of secured donor resources

for the year.

Grants financed about 27 percent of total spending, or nine percent of GDP, in FY13/14, 70 percent of it from

the government of India. Given the persistent shortage of rupees, the government has tightened expenditures

to bring them in line with available resources. Another reason for the spending dip is the slow start of the

budget year because of the elections in the summer, change of leadership, and delays in foreign grant

disbursements. Grants are expected to more than halve, from 15 percent in FY12/13 to about 6.6 percent of

GDP, due to slow initiation of the 11th Five-Year Plan (FYP-11).

Domestic revenues coverage of current spending has been shrinking consistently over the last four

fiscal years. The coverage is expected to be 112 percent of FY14/15 current spending, compared to 122

percent three years before. By constitution, domestic revenues should cover at minimum current spending

and FYP-11’s targets coverage of 85 percent of total expenditures by 2018. Domestic revenues as a share of

GDP have been declining over the last three years, from 22 percent to an estimate of 18.9 percent in FY14/15.

This calls for an effort to broaden the tax base, improve tax administration and rationalization, in particular

reducing tax holidays and exemptions to the extent they do not have the intended impact.

To replace the bans on vehicle imports lifted on July 19, new taxation measures on vehicles were

introduced. That includes a fuel tax of 5 percent, a tax on vehicle imports (other than from India) from 100 to

180 percent and a sale tax on Indian vehicle of 55 percent.

These tax measures are however weakened by the persistence of a civil service quota for vehicle

import. The quota allows civil servant (at or above grade P3A, or 7189 civil servants, 28 percent of total civil

Min Max Min Max

Cabinet

Secretary63,000 69,300 75,160 82,685 19%

Government

Secretary50,445 55,545 65,930 72,530 31%

EX/ES-1 45,860 59,585 54,575 70,925 19% 30

EX/ES-2 38,475 50,025 45,785 59,510 19% 50

EX/ES-3 32,520 42,270 38,700 50,325 19% 156

P1 25,610 33,260 30,990 40,290 21% 420

P2 22,620 29,370 27,370 35,545 21% 988

P3 19,830 25,755 23,995 31,195 21% 1,894

P4 17,660 22,985 21,370 27,745 21% 3,646

P5 14,460 18,810 17,495 22,745 21% 5,771

S1 13,305 17,280 16,365 21,240 23% 2,154

S2 12,055 15,655 14,830 19,255 23% 2,383

S3 11,015 14,315 13,550 17,600 23% 1,659

S4 9,775 12,700 12,025 15,625 23% 1,798

S5 9,045 11,745 11,125 14,500 23% 2,099

O1 8,580 11,130 10,725 13,950 25% 725

O2 8,060 10,460 10,075 13,075 25% 475

O3 7,325 9,500 9,155 11,930 25% 349

O4 6,805 8,830 8,505 11,055 25% 704

PositionExisting pay scale Pay scale after

Increase# Civil

servants

6

BHUTAN COUNTRY SNAPSHOT

service) to import every 7 years a vehicle duty free up to Nu800,000 (or $13,333). Efforts to replace the quota

by a financial allowance proved unsuccessful during the last Parliament session.

The deficit in FY14/15 is expected to ease to 2.7 percent of GDP, as more revenues will kick in with

commissioning of the Dungsam cement project, the Dagacchu hydro electricity scheme, and the Chhukha

power plant’s electricity export tariffs revision.

Table 4: Government Budget

2011/12 2012/13 2013/14 2014/15

Actual Actual Revised Budget

Revenue & Grants

35.2 29.3 28.5 24.6

Domestic Revenue

22.0 20.2 18.8 18.9

Tax 15.8 14.7 13.2 13.6

Non-tax 6.1 5.5 5.6 5.4

Grants 13.5 9.2 9.6 5.7

Project-tied 11.6 6.6 7.9 4.4

Program 1.9 2.5 1.7 1.3

Other receipts -0.2 0.0 0.1 0.0

Outlay 36.3 33.4 32.5 27.3

Total 37.6 35.0 34.1 28.6

Current 18.0 17.3 16.6 16.9

Capital 19.6 17.6 17.5 11.7

Net lending -1.1 -0.7 -1.6 -1.3

Fiscal Balance -1.1 -4.1 -4.0 -2.7

Source: Ministry of Finance

The Ministry of Finance was the last ministry to sign a performance agreement with the prime minister

on September 3. Key targets include (i) maintaining the fiscal deficit below three percent, maintaining the

non-hydro debt at 35 percent of GDP, and raising revenue above 20 percent of GDP.

Public debt Bhutan’s public and publicly guaranteed external debt stood at 93.2 percent of GDP by end-FY13/14.

The rise in the external public debt is primarily due to disbursement of on-going hydro projects (59.1 percent

of GDP). Hydropower projects are financed primarily by India with a mix of loans (70 percent) and grants (30

percent). External debt is largely denominated in Indian rupees (and related to hydropower sector debt),

which accounts for 64.4 percent of total external debt, with convertible currency debt accounting for only

35.6 percent of GDP. Domestic debt is due entirely to a loan to purchase aircraft for national carrier Druk Air

in FY9/10.

Bhutan’s rapid hydropower development is projected to lead to a substantial buildup of external debt

in the medium-term, with debt ratios breaching most of the country-specific indicative thresholds. Bhutan’s

debt situation is expected to improve over the long run, reflecting significantly higher electricity exports

when hydropower projects come on stream.

7

BHUTAN COUNTRY SNAPSHOT

Bhutan’s risk of external debt distress continues to be moderate.4 This is based on the commercial

viability of the hydropower projects, the risk-sharing agreement with India for hydropower loans, Bhutan’s

strong track record of project implementation, rapid growth in energy demand from India, committed donor

support, and Bhutan’s high level of international reserves. Bhutan’s concentrated export base, rupee-

reserves mismatch with external debt and the trade structure of the country leave it vulnerable to exports

and any shortfalls in aid inflows. Additional risks stem from bulky hydro-related debt service payments

requiring provisioning of rupee reserves.5

These projects also bring strong economic dividends in the long term, boosting average real GDP growth

and exports. Moreover, despite the large increase in the stock of debt, the addition of the new hydropower

projects does not create substantial vulnerabilities in debt servicing over the long term. Bhutan’s strong track

record of project implementation, the commercial viability of the new hydropower projects and the close

economic and political ties that Bhutan has with India are all factors that mitigate the commercial risks of

these projects. India has been both the main provider of financing for hydropower projects and the main

consumer of the projects’ output.

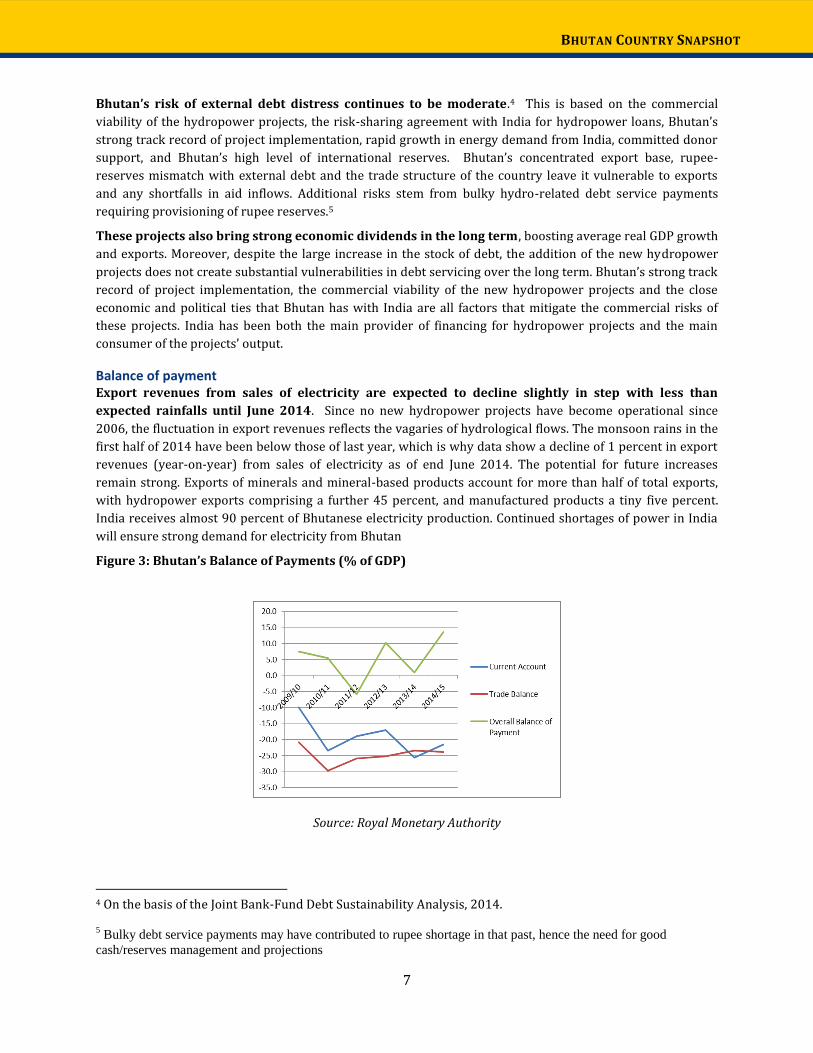

Balance of payment Export revenues from sales of electricity are expected to decline slightly in step with less than

expected rainfalls until June 2014. Since no new hydropower projects have become operational since

2006, the fluctuation in export revenues reflects the vagaries of hydrological flows. The monsoon rains in the

first half of 2014 have been below those of last year, which is why data show a decline of 1 percent in export

revenues (year-on-year) from sales of electricity as of end June 2014. The potential for future increases

remain strong. Exports of minerals and mineral-based products account for more than half of total exports,

with hydropower exports comprising a further 45 percent, and manufactured products a tiny five percent.

India receives almost 90 percent of Bhutanese electricity production. Continued shortages of power in India

will ensure strong demand for electricity from Bhutan

Figure 3: Bhutan’s Balance of Payments (% of GDP)

Source: Royal Monetary Authority

4 On the basis of the Joint Bank-Fund Debt Sustainability Analysis, 2014. 5 Bulky debt service payments may have contributed to rupee shortage in that past, hence the need for good

cash/reserves management and projections

8

BHUTAN COUNTRY SNAPSHOT

The tourism sector has turned into an important contributor of export revenues in recent years.

Tourism revenues are 20 percent of non-hydro exports. Tourist arrivals and revenues (from convertible

currency-paying tourists) expanded at an average of 15 percent per year in the five years to 2013. As of July

2014, 25,854 convertible currency tourists came to Bhutan, a jump of 12 percent year-on-year, earning the

country $67.5 million in convertible currency, a seven percent increase year-on-year compared to 2013. New

measures introduced towards Thai tourist have contributed. A similar number of tourists came overland,

mainly from India with light travel requirements but the statistics are not up-to-date for this segment.

Bhutan runs a large and growing current account deficit (estimated at about 25 percent in June 2014).

It is essentially financed by donor resources, of which India contributes the most through loans and grants to

finance hydropower development. Even when excluding self-financed hydropower construction imports of

goods and services (around a third of total good and services), the current account deficit would stand at 15

percent of GDP, illustrating a significant national dissaving, and the need for the country to borrow to finance

consumption. Foreign direct investment finances a low eight percent of the capital account (about $20m). The

recent amendment of the FDI policy should contribute to attract more foreign investment into the country. In

particular, foreign investors are now allowed to repatriate their profits in the currency of their choice.

Gross international reserves had built up to 17 months of goods and service imports . International

reserves amounted to $997.9 million by end-June 2014, 83 percent of which was in convertible currency,

with the rest in Indian rupees.6 There is, however, a continuing mismatch in the composition of Bhutan’s

reserves and the structure of its international transactions, as the country primarily needs Indian rupees for

trade settlement and debt service. To start addressing this issue, the RMA has implemented since August new

reserve policy measures allowing the conversion of convertible currency reserves into Indian Rupees above a

threshold of $700 million.

Monetary and financial sectors

The tight liquidity experienced by the banking system in 2012 has eased. Excess liquidity characterized

the financial system from 2008-mid 2011 due to large build-up of hydropower inflows and grants (and only

partial sterilization of these funds by the RMA). The tight liquidity conditions emerged in June 2011 as a

result of persistent growth in Indian rupee imports with an equivalent drain on local currency liquidity, a

reduction in the overall level of individual deposits, over-dependence on the more volatile and seasonal

corporate deposits as a source of funding; and bank-financing of the large, long-term public- and private-

sector investment projects (e.g., Dungsam cement project). Since March 2012, in order to address the tight

liquidity conditions, the RMA cut the cash reserve ratio (CRR) twice to five percent from 17 percent. As result,

the banking sector’s liquidity improved between Q2 2012 and Q2 2014.

Interest rates have shown little movement previously, despite the absence of explicit controls. Real

interest rates have been negative, introducing a strong bias towards investment in real estate. While the

reason for interest rate stickiness is unclear, higher and more flexible interest rates may better reflect market

conditions and be more aligned with those in India.

6 The Constitution requires that foreign exchange reserves should be maintained at 12 months of essential imports.

9

BHUTAN COUNTRY SNAPSHOT

Box 1: Royal Monetary Authority notice: introduction of housing & vehicle loans. This is to inform the general public that the RMA will lift the ban imposed on Housing and Vehicle loans with effect from 1st September 2014. The policy ban of March 2012, although unconventional in nature, was inevitable and had to be implemented by the RMA given the severe macroeconomic imbalances the country faced during the time. This policy normalization has been a yearlong process of extensive planning, preparation and consultation by the RMA, which was approved by the RMA Board during its 98th Board meeting. Further, along with the Housing and Vehicle loans guidelines, Consumer loans guidelines have also been issued as a pre-emptive measure by the RMA to mitigate systemic risk that could arise from potential build-up of risks particularly in these sectors. However, with the reintroduction of these Guidelines, we would strongly advise all FIs (Lenders) to lend responsively and all Borrowers to borrow responsibly.

http://www.rma.org.bt/what_newstp.jsp?newId=90

Monetary conditions need to remain sufficiently tight to ward off overheating and manage pressures on rupee reserves. Excess liquidity should be closely monitored and promptly adjusted to prevent credit growth from rebounding strongly. In future, along with the development of a domestic capital market, increased issuance of treasury bills could be used to mop up excess liquidity. Rupee inflows related to hydropower projects and grants should be sterilized in order to curtail excess liquidity in the banking system and dampen credit growth, without the need for administrative or macro-prudential measures.

Figure 4: Credit growth and reserves

Source: RMA Quarterly Bulletin

Since early 2013 to June 2014, private credit growth has slowed markedly to an average of 6-7 percent annually, as a result of the strict tightening of credit and foreign exchange availability following the shortage of Rupees. Since then, although it remains yet to be seen in the data, credit growth is expected to rebound with the lifting of credit restrictions and their replacement of market-friendly measures.

Strengthening supervision will be critical in the short-to-medium term financial sector because vulnerabilities have likely accumulated. While banks appear to be well capitalized, with the risk-weighted capital adequacy ratio rising to 19 percent, non-performing loans rose to 11.5 percent as of March 2014 (from 10.1 percent a year before) following the sudden halt of rapid credit growth. The financial sector remains adequately capitalized, with a capital adequacy ratio of 18.20 percent in March 2014, above the institutional requirement. Yet vulnerabilities arise from asset-liability mismatches, with a significant proportion of the deposit base being (short-term, seasonal and volatile) corporate deposits, whereas bank credit is concentrated in loans with longer time horizons to finance investment and projects (as in construction, particularly funding of large infrastructure projects). The concentration of lending in personal and real estate loans raises particular concerns; more than a quarter of the financial sector’s portfolio consists of building

10

BHUTAN COUNTRY SNAPSHOT

and construction loans, followed by personal loans that constitute around 16 percent of overall credit outstanding.

Efforts to deepen the financial sector in a sustainable manner are underway. A comprehensive Financial Sector Development Strategy is being prepared with a careful sequencing of reforms within a medium-term plan. It will emphasize the importance of balancing further deepening with maintaining financial stability, promoting alternatives to bank financing for the private sector, and improving information and market infrastructure by steps that included broadening coverage of the credit bureau.

Table 5: Macroeconomic indicators

Indicator 2011/12 2012/13 20013/14 20014/15 Gross domestic product (US$ million at current prices) 1,815 1,975 2,298 2,460

Consumer price index (% change) 13.5 5.5 8.0 10.0

Real annual growth rates (%, calculated at 2000 prices) Gross domestic product at market prices 8.1 5.6 6.0 6.8

Balance of Payments (US$ millions) 2011/12 2012/13 20013/14 20014/15

Exports (GNFS)a 706.5 709.9 789.3 n.a.

Merchandise FOB 594.3 582.6 642.0 n.a.

Imports (GNFS)a 1,301.5 1,258.9 1,288.9 n.a.

Merchandise FOB 1,184.7 1,126.5 1,125.2 n.a.

Trade balance -368.0 -358.0 -377.6 n.a.

Current account balance -418.1 -427.1 -499.6 n.a.

Net private foreign direct investment 22.2 20.0 n.a n.a.

Long-term loans (net) 289.8 292.0 n.a. n.a.

Official 279.8 316.6 n.a. n.a.

Change in reservesb 78.8 313.6 n.a. n.a.

Public finance (as % of GDP at market prices)c actual actual estimate (budget)

Current revenues (without grants) 22.0 20.0 18.8 18.9 Current expenditures 18.0 17.7 16.6 16.4 Current account surplus (+) or deficit (-) 3.9 2.3 2.2 2.5

Capital expenditure 19.6 19.7 17.5 11.7 Fiscal Balance -1.1 -4.1 -4.0 -2.7

Monetary indicators 2011/12 2012/13 20013/14 20014/15

M2/GDP 58.8 58.2 58 n.a

Growth of M2 (%) -1 18.6 6.6 n.a

Private sector credit growth / 30.1 7.1 8.2 n.a

Total credit growth (%) 51.3 12.8 0 n.a

Notes: a: GNFS=Good and Non-Factor Services; b: includes use of IMF resources; c: account is for consolidated general government. All statistical information follows Bhutan's fiscal year (from July to June), except Balance of payment data (calendar year)

11

BHUTAN COUNTRY SNAPSHOT

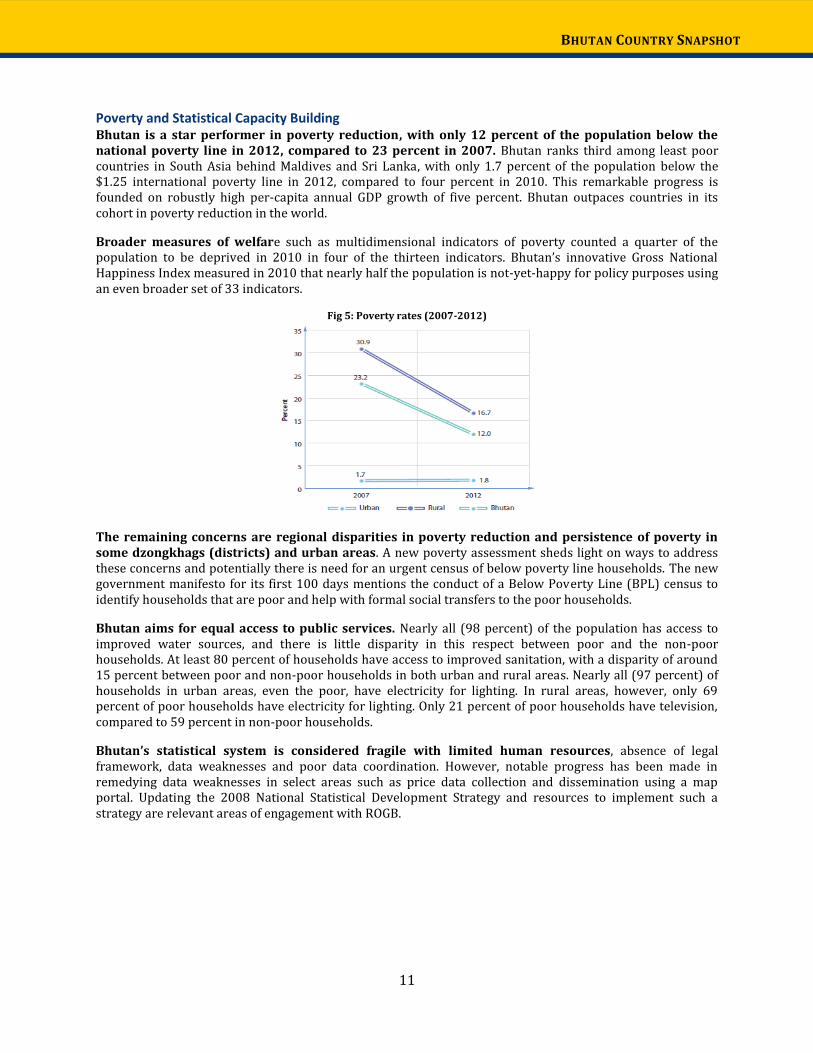

Poverty and Statistical Capacity Building Bhutan is a star performer in poverty reduction, with only 12 percent of the population below the national poverty line in 2012, compared to 23 percent in 2007. Bhutan ranks third among least poor countries in South Asia behind Maldives and Sri Lanka, with only 1.7 percent of the population below the $1.25 international poverty line in 2012, compared to four percent in 2010. This remarkable progress is founded on robustly high per-capita annual GDP growth of five percent. Bhutan outpaces countries in its cohort in poverty reduction in the world.

Broader measures of welfare such as multidimensional indicators of poverty counted a quarter of the population to be deprived in 2010 in four of the thirteen indicators. Bhutan’s innovative Gross National Happiness Index measured in 2010 that nearly half the population is not-yet-happy for policy purposes using an even broader set of 33 indicators.

Fig 5: Poverty rates (2007-2012)

The remaining concerns are regional disparities in poverty reduction and persistence of poverty in some dzongkhags (districts) and urban areas. A new poverty assessment sheds light on ways to address these concerns and potentially there is need for an urgent census of below poverty line households. The new government manifesto for its first 100 days mentions the conduct of a Below Poverty Line (BPL) census to identify households that are poor and help with formal social transfers to the poor households.

Bhutan aims for equal access to public services. Nearly all (98 percent) of the population has access to improved water sources, and there is little disparity in this respect between poor and the non-poor households. At least 80 percent of households have access to improved sanitation, with a disparity of around 15 percent between poor and non-poor households in both urban and rural areas. Nearly all (97 percent) of households in urban areas, even the poor, have electricity for lighting. In rural areas, however, only 69 percent of poor households have electricity for lighting. Only 21 percent of poor households have television, compared to 59 percent in non-poor households.

Bhutan’s statistical system is considered fragile with limited human resources, absence of legal framework, data weaknesses and poor data coordination. However, notable progress has been made in remedying data weaknesses in select areas such as price data collection and dissemination using a map portal. Updating the 2008 National Statistical Development Strategy and resources to implement such a strategy are relevant areas of engagement with ROGB.

12

BHUTAN COUNTRY SNAPSHOT

On September 11, 2014, the Honorable Prime Minister of Bhutan Launched the Bhutan Poverty Assessment report in Thimphu.

http://www.worldbank.org/content/dam/Worldbank/document/SAR/bhutan-poverty-assessment.pdf

Private Sector Bhutan's economy remains dominated by state-owned enterprises (SOEs), with private sector contributing a mere 8 percent of total national revenue. Advantages include a stable and low-corruption environment, reasonably good human development including wide-spread knowledge of English, access to low cost and reliable electricity, preferential access to the large Indian market and easy access to skilled and unskilled labor from India. Against these advantages, private sector development is limited by the absence of scale economies, unequal access to finance, mismatched skills of the labor force, and the lack of adequate infrastructure. To spur PSD, a number of policies and laws have been formulated. These include the Economic Development Policy (EDP) and the amended FDI policy and rules and regulations. Forthcoming policies include the industrial infrastructure development policy (governing economic zones), the licensing protocol, the mineral development policy, the renewable energy policy, the micro, small and medium enterprises (MSME) policy, the consumer protection bill and the enterprise registration act. With the support of the World Bank, Bhutan launched its first IT Park in 2012 as a Public Private Partnership (PPP) Despite reforms, Bhutan’s ranking in ease of doing business in 2013 remains in the last tier, having decreased to 148 (out of 185 economies) from 142 in 2012, suggesting that more needs to be done. The private sector remains small and, while 15-to-24 year olds represent a fifth of the Bhutanese population, unemployment among the youth remains high. To foster Private Public Partnerships (PPPs) a PPP policy has been drafted and submitted for Cabinet for approval. The Business Opportunity and Information Centre (BOIC) was established on December 19, 2013 as a time bound autonomous agency for implementation of the Revolving Fund created as part of the Economic Stimulus Program in order to foster growth of cottage and small manufacturing industries that contribute to employment creation, export enhancement/import substitution. The Centre was officially launched on August 27, 2014. Under the Nu. 5 billion worth of Economic Stimulus Plan (ESP), Nu. 1 billion is earmarked for the Special Support Scheme (SSS) activities, another Nu 1.5 billion will be pumped into the revolving fund I for cottage and small manufacturing industries. The revolving fund II, for non-formal rural activities, has a budget of Nu 0.40bn and the remaining Nu 2.1 billion has been allocated towards the Financial Institutes (FIs).

13

BHUTAN COUNTRY SNAPSHOT

Health Bhutan has sustained its investments in health over the last two decades and made remarkable progress. In 2010-11, public health expenditure stood at 4 percent of GDP and 9 percent of government spending, considerably higher than other South Asian countries. The expansion of the network of health facilities now ensures that 90 percent of the population live within three hours walk to a health facility; there are 25 traditional medicine units at Basic Health Units (BHUs), and there are more than two functioning ambulances at each district hospital.

Access to health services is satisfactory, with their utilization and quality requiring improvement. The Constitution (2008) provides that the state will provide basic public health services free of cost to all citizens. As of now, all health services (barring a handful of dental, cosmetic and other services) continue to be provided by the government for free. Nevertheless, some outreach centers (ORCs) are very remote and require health workers, the unsung heroes of the country’s public health system, to endure long walking hours (or even days) prior to reaching the remote facilities.

The most significant health problem is the high rates of malnutrition. Though there has been improvement in recent years, it is nevertheless still estimated that some 35 percent of Bhutanese preschool children are stunted. The Royal Government of Bhutan finalized the draft of the National Food and Nutrition Security policy during 2012. Although the burden of non-communicable diseases (NCDs) is growing, the health services continue to spend most of their resources at district level on the traditional infectious diseases such as common cold, diarrhea, skin diseases and conjunctivitis. In addition, alcoholism remains a significant health challenge.

Education Bhutan’s education expenditures are equally strong. Public education expenditure stood at 7.3 percent of GDP and 16.7 percent of total government spending (MOF, 2012). These figures are among the highest in the South Asia region. The Constitution (2008) provides for the State to ensure free education up to Grade 10 for all children of school-going age, and to make technical and professional education generally available, and higher education equally accessible to all on the basis of merit. At the same time, this progress has led to a refocus by development partners on other priorities, which may make it difficult to sustain high education spending.

14

BHUTAN COUNTRY SNAPSHOT

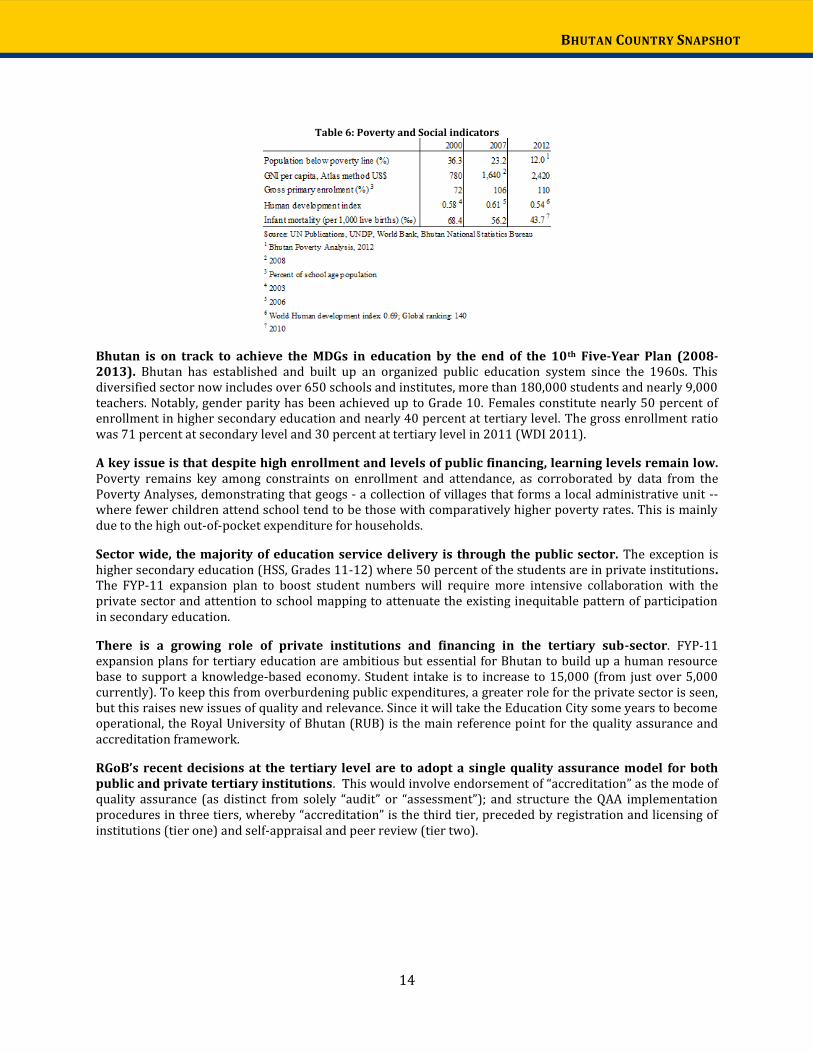

Table 6: Poverty and Social indicators

Bhutan is on track to achieve the MDGs in education by the end of the 10th Five-Year Plan (2008-2013). Bhutan has established and built up an organized public education system since the 1960s. This diversified sector now includes over 650 schools and institutes, more than 180,000 students and nearly 9,000 teachers. Notably, gender parity has been achieved up to Grade 10. Females constitute nearly 50 percent of enrollment in higher secondary education and nearly 40 percent at tertiary level. The gross enrollment ratio was 71 percent at secondary level and 30 percent at tertiary level in 2011 (WDI 2011).

A key issue is that despite high enrollment and levels of public financing, learning levels remain low. Poverty remains key among constraints on enrollment and attendance, as corroborated by data from the Poverty Analyses, demonstrating that geogs - a collection of villages that forms a local administrative unit -- where fewer children attend school tend to be those with comparatively higher poverty rates. This is mainly due to the high out-of-pocket expenditure for households.

Sector wide, the majority of education service delivery is through the public sector. The exception is higher secondary education (HSS, Grades 11-12) where 50 percent of the students are in private institutions. The FYP-11 expansion plan to boost student numbers will require more intensive collaboration with the private sector and attention to school mapping to attenuate the existing inequitable pattern of participation in secondary education.

There is a growing role of private institutions and financing in the tertiary sub-sector. FYP-11 expansion plans for tertiary education are ambitious but essential for Bhutan to build up a human resource base to support a knowledge-based economy. Student intake is to increase to 15,000 (from just over 5,000 currently). To keep this from overburdening public expenditures, a greater role for the private sector is seen, but this raises new issues of quality and relevance. Since it will take the Education City some years to become operational, the Royal University of Bhutan (RUB) is the main reference point for the quality assurance and accreditation framework.

RGoB’s recent decisions at the tertiary level are to adopt a single quality assurance model for both public and private tertiary institutions. This would involve endorsement of “accreditation” as the mode of quality assurance (as distinct from solely “audit” or “assessment”); and structure the QAA implementation procedures in three tiers, whereby “accreditation” is the third tier, preceded by registration and licensing of institutions (tier one) and self-appraisal and peer review (tier two).

15

BHUTAN COUNTRY SNAPSHOT

Social Protection There is no formal system of social protection in Bhutan. The lack of safety nets particularly for those outside of public sector jobs leaves the majority of the population vulnerable to shocks and risk. Employment opportunities for youth are limited, particularly at higher level managerial jobs (skills and job mismatch in market). The change in social structures and rapid urbanization is likely to leave many elderly rural poor without informal or social safety nets.

The coverage of Bhutan’s pension system is limited to civil servants and joint-sector companies. These groups encompass little under 7 percent of the population in 2012. In addition, the armed forces are covered under a separate scheme. The participation in National Pensions and Provident Fund (NPPF) extends across some part of the formal sector workforce beyond higher income groups and a similar proportion of the elderly are receiving some benefits from the system. This influences the decisions of the young people of Bhutan entering the labor market with a majority of youth focused on entering the limited opportunities in the public sector.

Employability of Bhutanese youth is a key priority. Employment opportunities for youth are limited. This includes particularly access to higher level managerial jobs due to a skills and job mismatch in the market. Similar imbalances and mismatches exist due to individuals’ preference for jobs in urban areas, jobs that are white-collar and jobs in the public sector. However, the number of these types of jobs is limited. In addition to these relatively well-documented issues, there are indications that a number of other, less obvious but nevertheless pressing challenges exist. In particular, informality and underemployment appear to be widespread, especially in rural areas. Besides, chronic or long-term unemployment might be a problem at least for certain parts of the Bhutanese labor force. The government target is to bring down the youth unemployment rate from 7.3 percent in 2012 to 5.0 percent or less by the end of the next plan period (2013-2018). Within this context, the Ministry of Labor and Human Resources (MOLHR) has decided to develop a social protection strategy to provide more equity of social protection to those who work across different sectors, and provide support to senior citizens outside of the formal sector.

There are some existing specialized grant programs such as scholarships, and welfare schemes distributed by His Majesty the King, or a few NGOS, but few are integrated into social assistance, social insurance or labor market program schemes. There is also little coordination across them. There is low coverage of target groups as most of the poorest 20 percent have no social protection coverage. Other support to the elderly only exists through family and social networks.

The World Bank is supporting the development of Social Protection and Labor Strategy, which includes assistance to expand and improve the Bhutan Labor Force Survey as well as a pilot Computer Assisted Personal Interviewing (CAPI).

Agriculture Bhutan is predominantly an “agriculture-based society”. The agriculture sector is dominated by smallholder subsistence farmers who occupy the majority of the arable land and produce most of the crop and livestock products. As per the Labor Force Survey Report of the MoLHR, 2011, the agriculture sector provides livelihood to 68.4 percent of the total population contributing to 14.3 percent of the total GDP.

While the contribution of the agriculture sector to GDP has been declining, it continues to be an important sector. It is particularly important as a source of employment and reducing poverty. However, the sector’s growth remained insufficient to adequately address poverty, and attain food security. Immigration from rural to urban areas, particularly by youth and men looking for a more modern life style, has resulted in the feminization of the agriculture sector particularly in the lagging areas.

A range of policies are needed to improve rural life and maintain rural population. Physical access to rural areas and between rural areas and markets needs to be improved, while dispersed and small scale

16

BHUTAN COUNTRY SNAPSHOT

production hinder adoption of good agriculture practices. Greater access to credit and technology is needed, and sustainable approaches to pest and wild life encroachment are needed. Other issues include loss of agriculture land for other development, lack of infrastructure such as irrigation, farm roads and post-harvest storage, labor shortage, and the scarcity of existing market traders and wholesalers.

The agriculture sector contributes to implementation of FYP-11. To achieve eradication of national poverty to less than 15 percent and rural poverty below 20 percent, the sector needs to grow at an annual rate of 4 percent. FYP-11 is expected to adopt a multi-dimensional approach to develop the lagging regions. To achieve this, the Ministry of Agriculture and Forestry has a mandate to improve food security and nutrition, improve rural livelihoods to overcome poverty, and sustainable management and utilization of natural resources.

FYP-11 has 16 programs with total budget outlay of Nu. 13.65 billion (more than $200 million). However, in FY 2013-14, the Ministry of Agriculture and Forest has an approved budget allocation of Nu. 2.96 billion (almost $50 million).

Environment and Cultural Heritage Environmental conservation is a cornerstone of Bhutan’s unique development approach. Bhutan remains endowed with dense and virtually untouched forests, abundant water resources and diverse wild species. The country’s vast endowment reflects its commitment to maximizing Gross National Happiness. Nevertheless, it confronts chronic pressures primarily related to land degradation and biodiversity loss due to development and population growth. Land degradation can stem from inappropriate agriculture production and mining practices, overgrazing, and excessive forest harvesting, as well as solid waste disposal in and around population centers. Threats to biodiversity include illicit forest harvesting, human-wildlife conflict, poaching, and habitat fragmentation arising from land development projects. A particularly important element is the need for integrated water management. Despite the positive outlook for water availability, incipient challenges relate to the sustainability of urban water supply systems and functionality of existing rural water supply schemes. Ongoing soil erosion and deforestation threaten watershed conditions and their functional integrity. Concerns on water quality stem from the rise in domestic and industrial waste generation along with improper disposal as well as run-offs from agricultural fields and urban centers.

The government has taken several important steps to preserve the environment. Bhutan’s environment policies include: (i) mandating a minimum forest cover of 60 percent of the country’s total land area in the Constitution; and (ii) increasing the proportion of land under protected area status to around 50 percent at present from 26 percent in 2000. The Bhutan Trust Fund for Environmental Conservation (BTFEC) is working towards the adoption of more modern governance and business practices. With grants made possible by BTFEC, conservation projects began to be implemented in the high altitude northern areas which form part of the fragile eastern Himalayan ecosystem. The wildlife crime unit within the Department of Forest and Park Services is in the process of upgrading the Bhutan Forest Enforcement Database into an online reporting system on wildlife offenses by field offices and expanding programs for raising public awareness and sensitivity to forest and wildlife crime. Environmental sustainability is at the core of Bhutan’s Five-Year Plans, including the 11th Plan currently under implementation. Bhutan has also taken steps to preserve its cultural heritage. Protection of its culture is one of the four pillars of Bhutan’s unique GNH vision. It is also a key economic driver through the tourism industry; as such conservation of heritage monuments need to be prioritized in synergy with the development of urban infrastructure and services.

The World Bank will assist the Royal Government of Bhutan to implement the Heritage Sites Bill with a focus on improving the living conditions and economic opportunities of the poorest communities in the country, which tend to live in traditional houses and villages across the country.

17

BHUTAN COUNTRY SNAPSHOT

Disaster Risk Management Bhutan is highly prone to disasters and climate related risks. Its rugged topography, geographic and climatic features make it prone to flooding, landslides, glacial lake outburst floods (GLOFs), drought and earthquakes. Over the past 40 years, several earthquakes above a magnitude of 6 on the Richter scale have occurred. According to the World Bank report on Natural Disaster Hotspots (2005), 31.3 percent of Bhutan is in risk areas, and 60.8 percent of population is at high mortality risk from multiple hazards.

The frequency and intensity of extreme weather events appears to be increasing. The country has become increasingly vulnerable to glacial lake outburst floods (GLOFs), other flooding, drought, forest fires and loss of vegetation/biodiversity. Heavy seasonal monsoon rains and glacial melt contribute to flooding and landslides. Of the 2,674 glacial lakes that exist in Bhutan, 25 have been identified as potentially dangerous. This poses not only a threat to the development of hydropower in the country but also a threat to food security.

The government adopted the Disaster Management Act in 2013 to strengthen the disaster management system. The Act decentralizes disaster management activities, empowers the nodal institutions with the legal status to implement disaster reduction strategies and emphasizes a consultative process at the village level. The Department of Disaster Management (DDM) under the Ministry of Home & Cultural Affairs - the national coordinating agency - is formulating a comprehensive National Disaster Risk Management Strategy for Bhutan. It is expected to result in the formation of a National Disaster Management Authority (NDMA) under the leadership of the Prime Minister. Key challenges include (i) strengthening preparedness and early warning systems: (ii) mainstreaming disaster risk management, including in construction and (iii) strengthening disaster response capacity.

An important aspect of disaster risk mitigation, climate adaptation and early warning systems is improved capacity for hydro meteorological monitoring and forecasting. Importance of hydromet services is well recognized in FYP-11. In Bhutan, the main agency responsible for these services and for weather, hydrological and flood forecasting is the Department of Hydromet Services (DHMS) under the Ministry of Economic Affairs. DHMS was established in 2011. It is a relatively new agency in significant need of capacity strengthening. At present, there is no legal or regulatory framework for delivering hydromet services or a national framework for climate services. Most of the existing observation network is manual with limited capacity for real time monitoring. Capacity for snow, permafrost and glacier monitoring within DHMS is only now beginning. Bhutan at present features only 24-hour weather forecasts, therefore, there is a need to improve the lead time to better prepare communities. Also, the current practice issues flood forecasts only when the water level is high. While DHMS’s activities are being supported by several development partners such as the U.N. Development Program and Japan International Cooperation Agency, there is substantial room for strengthening DHMS to support its transformation into a modern service delivery agency that can support disaster risk mitigation, and also provide climate services in various sectors such as agriculture, water resources and hydropower.

Urban Development Bhutan is undergoing a rapid transition from a rural economy to an urban society. The average annual urban population growth rate has been around 4 percent since 2007. The Bhutan National Urban Strategy (NUS, 2008) projects that by 2020, the country will be most likely 60 percent urbanized. As Bhutan evolves into a more urbanized society, RGOB recognized the country’s unique challenges in urban development – (i) the rapid rates of urbanization, and (ii) the limited availability of serviced land.

The urbanization rate across the country is skewed toward the Western region. Thimphu and Phuentsholing are the two most favored destinations for migrants. These cities, especially Thimphu, are experiencing urban sprawl and densification with consequent rise in demand for municipal services. Through the enactment of the Local Government Act (2009) and the approval of the Municipal Finance Policy (2012), the RGOB has established four autonomous cities (Thimphu, Phuentsholing, Gelephu and Samdrup-Jokhar). Under the proposed National Urban System, these urban centers would play an important role as future engines of growth.

18

BHUTAN COUNTRY SNAPSHOT

Bhutan is relatively well-positioned to meet the challenge of rapid urbanization, given its low population. Nevertheless, urban institutional and governance systems need to be strengthened. Spatial planning is also needed, as lack of affordable and housing for lower-income groups is becoming a critical issue. In this context, the Bank is supporting the RGoB through the Second Bhutan Urban Development Project and its Additional Financing, which provides resources for sites and services development in northern Thimphu and for municipal finance and management systems development in the four cities as well as for related capacity building. Another important issue related to the rapid urbanization is to provide jobs for an increasingly urban youth population.

Energy Hydropower development has underpinned the rapid growth of Bhutan’s economy. The total installed capacity of existing hydropower plants is 1,488 megawatts (MW). Of total annual power generated, 80 percent is exported to India after meeting domestic consumption. Power exports account for the largest source of national revenue in the form of taxes and dividends, generating more than 40 percent of government revenue. Power exports also contribute to 25 percent of gross domestic product (GDP), and hydropower infrastructure development contributes another 25 percent of GDP through the construction sector.

However, power generation can get disrupted during winter months. During wet seasons, existing hydropower plants can generate sufficient electricity to meet domestic demands and power exports. Since all the existing plants are run-of-the-river, the total generation capacity drastically drops to around 288 MW during winter dry seasons (December–March). This low capacity does not meet the system peak demand during winter. To deal with the seasonal power shortage, industrial loads have been curtailed during the winter months. Winter power shortages will likely remain until 2016 when the Punatsangchhu-I hydropower plant (1,200 MW) is expected to come online.

In 2008, Bhutan agreed to develop and export 10,000 MW of new capacity with India by 2020. Under the bilateral framework, one project at Punatsangchhu (stage 1, 1,200 MW) has started construction and contracts for two projects at Punatsangchhu (stage 2, 1,020 MW) and Mangdechhu (720 MW) have been awarded. Seven other large hydropower projects are at various development stages with the Indian government and its own enterprises.

In addition, small and medium sized hydropower operations are being developed as public–private partnerships (PPPs). In 2008, the Asian Development Bank (ADB) agreed to finance the Dagachhu hydropower project (126 MW) as the first PPP infrastructure in Bhutan. The project’s joint venture was established between DGPC and India’s Tata Power Company. The Department of Hydropower and Power Systems also intends to promote independent power producers (IPPs) as the next step after formulating rules and guidelines required for IPPs.

The hydropower development will require extensive investments in power transmission. While these transmission lines are expected to be developed and aligned with hydropower development, a holistic development approach will be crucial for the network expansion to maximize the investment benefits and minimize any adverse safeguard impacts on transmission corridors.

Bhutan has set an ambitious goal of providing electricity for all by 2015. Mountainous terrain and the resultant difficulties of grid extension have kept some of the rural population without access to clean energy. Traditional fuels, such as kerosene and fuel wood, cause indoor pollution and health burdens. To reduce poverty and stimulate inclusive economic development, the government has embarked on a large-scale rural electrification campaign. As of December 2012, 84 percent of households had access to electricity, supported by the ADB and JICA. In addition to grid extension to rural areas, households in remote villages may have access to electricity through standalone solar home systems.

Bhutan has also begun to develop renewable energy to diversify the energy supply base through wind, solar, biomass, and small and micro hydropower. Wind power projects have the potential to generate clean energy to supplement hydropower in winter dry seasons. Bhutan also has biogas development potential as an alternative energy source to replace fuel wood for cooking in rural areas. Rural households depend heavily on

19

BHUTAN COUNTRY SNAPSHOT

fuel wood, which emits indoor air pollutants and poses a health hazard. To promote renewable energy, a national policy must be established and financial and fiscal incentives provided to help overcome the entry and financial barriers for development.

Transportation Transportation is the biggest infrastructure problem encountered by firms in Bhutan according to Bhutan’s 2010 Investment Climate Assessment. In rural areas transport connectivity is also a key determinant of affordable access to basic social and economic services. The Bhutan Living Standards Survey (2012) reports that transportation services alone account for approximately 23 percent of the cost incurred where households sought health care to address sickness or injury. In the broader economic context, roughly 40 percent of all firms and 70 percent of large firms surveyed had experienced losses due to ground transportation difficulties.

Bhutan has achieved significant milestones in the transport sector. Investments under the 10th Five-Year Plan (FYP-10) have helped increase connectivity towards the official goal of having 85 percent of the population within half a day's walk from the nearest road. Parliament has also passed the Road Act in 2012 which empowers the Department of Roads to coordinate various institutions working in the roads sector. These accomplishments show a strong Government commitment to developing Bhutan’s transport sector and the institutions that will sustain it into the future. Recent achievements, supported by World Bank projects, include: (i) 67 km of new roads, (ii) 24 km of improved roads; and (iii) seven newly constructed motorable bridges. Project beneficiaries have experienced a 62 percent reduction in travel time to reach socio economic facilities (schools, clinics, etc.).

Looking forward, Bhutan Transport 2040 envisages meeting increased demand for rural transport with a dzongkhag road network that is 3.5 times its current length with connections to every geog. Achieving such targets will require approximately 2,500km new roads. Bhutan Transport 2040 also targets major investments such as (i) widening of the existing East–West Highway (and other key routes) to two lanes; (ii) improving access routes between industrial centers and major border crossings; and (iii) improving various existing alignments along the national highways network to improve safety and travel times.

Improving urban transport services is also a priority. The number of Bhutanese living in urban areas nearly tripled between 1990 and 2010. Increasing rates of motor vehicle ownership and use have accompanied this trend, bringing unprecedented impacts on the urban environment (many negative, including emissions, congestion, noise, etc.). Bhutan’s urban transport systems are still developing to meet increasing demand for urban mobility. Nevertheless, less than one third of urban households in Bhutan report using public transport in a given month.

The Royal Government of Bhutan (RGoB) is pursuing a green transport and electric vehicles initiative to promote improved urban mobility and reduced reliance on fossil fuels. The World Bank has been requested to provide technical advice and analytical work to inform decisions taken to develop this initiative. There are four components to this work as follows:

(i) Technical advice on electronic vehicles initiative options, infrastructure, planning, as well as fiscal and trade impacts;

(ii) Technical advice on enhancing the Thimphu city public transportation system; (iii) Knowledge sharing and partnerships to bring international experiences of electric vehicle and public

transport programs to Bhutan; and (iv) A household survey on travel behavior, needs, and vehicle preferences in Thimphu.

Under the activity to improve the resilience and affordability of roads and bridges, a grant from the Global Facility for Disaster Reduction and Recovery (GFDRR) has been applied to support Bhutan’s Department of Roads with:

20

BHUTAN COUNTRY SNAPSHOT

(i) Developing and asset management system to track the condition and vulnerability of roads and bridges. This information would provide the basis for directing investments to strengthen resilience and optimize the lifecycle cost of road and bridge infrastructure; and

(ii) Improving DOR’s capabilities on specific technical design topics through a knowledge exchange with Japan.

South-South Knowledge Exchange on urban public transport. This activity has also been seeking a grant from the South-South Knowledge Exchange Trust Fund to bring knowledge of urban public transport initiatives from Colombia, Ecuador, and China to Bhutan and Nepal. There are two key aims that this activity would seek to achieve: (i) informing government stakeholders within non-technical institutions about what is possible through improving urban public transport services and the institutions that provide them; and (ii) increasing the operational knowledge and capacity of City Bus Company staff. The international knowledge exchange would be particularly useful in this regard, given Latin America’s relatively extensive experience of transformational bus initiatives.

Governance, Public Financial Management and Procurement Bhutan outperforms its neighbors on Transparency International’s Corruption Perception Index. In 2012, Bhutan moved further up the index, from 38th to 33rd, in recognition of additional steps it has taken to strengthen its anti-corruption legal framework, including passage of the 2011 Anti-Corruption Act, the establishment of an Anti-Corruption Commission (ACC), and further strengthening of rules governing asset declaration by public servants in 2012. In 2013, Bhutan has moved further up to be ranked 31. A key element for improving governance has been an ambitious government-to-citizen program to provide services electronically through community centers, which is particularly important in light of geographical barriers. Similarly, with support from the IFC, the government has developed a government-to-business e-portal to provide a comprehensive inventory of licenses and other information on business processes.

Public financial management (PFM) reforms are part of national priorities. Bhutan over the years has been making progress in the area of accounting, budget execution oversight, control and reporting. Parliamentarians increasingly pay attention to the budget approval process and also in reviewing the audit observations through public accounts committee. The government continues to take steps to strengthen PFM in the country. The public at large has also become more demanding in terms of transparent and efficient government. Nevertheless, further improvement is needed on oversight of public sector entities, predictability in funds available for expenditures, the quality and timeliness of budget reports and financial statements, implementing the standards on auditing and accounting, PFM information systems, availability of professionally qualified staff and effectiveness of internal audits. The Bank has provided an IDF Grant to help the government in strengthening PFM in the public and private sectors in Bhutan by strengthening internal audit in the public sector, assisting in the implementation of Bhutanese Accounting standards (BAS), strengthening public accounting functions of RGoB, and supporting the RGoB in establishment of Bhutanese Institute of Chartered Accountants.

Significant progress has been achieved on public procurement reforms. Among the outcomes are: (i) the introduction of the procurement rules and regulations and standard Bidding Documents for Goods, Works and Services in April 2009; (ii) the establishment of the Public Procurement Policy Division in August 2008; (iii) the career path and recruitment tools put in place for a procurement profession; (iv) the generally well-functioning procurement market; (v) a strong framework for control and audit, spearheaded by the Royal

Audit Authority and the Anti-Corruption Commission; (vi) set up of the Government Procurement and Property Management Division to conduct centralized procurement of common items; and (vii) an independent review body to handle procurement grievances has been constituted. Because of this progress, the World Bank is moving towards use of country systems for all procurements up to the International Competitive Bidding Thresholds in Bhutan from end FY 2014-15.The Alternative Dispute Resolution Act of Bhutan, 2013 has come into being and formal arbitration expertise needs to be built in the country. In its endeavor to professionalize the procurement function, Bhutan has enrolled more than 300 government staff in the World Bank’s Certificate Program in Public Procurement.

21

BHUTAN COUNTRY SNAPSHOT

The World Bank Program in Bhutan The World Bank provides around $15-20 million of new IDA resources per year. There are four ongoing specific investment operations for a net commitment of $82 million of IDA resources. These include three country specific IDA operations – Decentralized Rural Development, Urban Development II, Remote Rural Communities Development – and one regional IDA project – Regional Cooperation on Wildlife Protection – as well as one GEF grant operation – Sustainable Financing for Biodiversity Conservation. In addition, the Bank manages several small grants for Bhutan on Disaster Management, Corporate Governance, Public Financial Management, Urban Budget Processes, and improving the resilience to Seismic Risk.

The World Bank has also extended three development policy operations over the last six years. The most recent, Development Policy Credit-2 (DPC-2), was approved by the World Bank’s Board of Executive Directors in November 2012 for a total of $36 million. This operation has focused on (i) Promoting government efficiency and effectiveness through sound fiscal and public financial management and procurement, and strong public administration; (ii) Fostering private-sector development by improving the policy environment and facilitating productive employment opportunities; and (iii) Expanding access to infrastructure in a sustainable manner.

The World Bank also provides support on knowledge. Recent analytic work includes an HD Public Expenditure Review, a review of higher education, and an Investment Climate Assessment which served to underpin the most recent budget support operation (DPC-2) to improve the policy framework governing private sector development. A poverty assessment, Financial Sector Assessment and a green growth study are underway.

The overarching goal of the new CPS (FY15-19) is to support Bhutan’s aspirations to achieve sustainable and inclusive growth. The proposed CPS will be aligned with the government’s 11th Five-Year Plan and will organize its activities under three results areas: (i) improving fiscal and spending efficiency, (ii) increasing private sector growth and competitiveness, and (iii) supporting green development.

However, it is anticipated that many of the themes of the current CPS will continue to resonate. The bulk of IDA financing is expected to continue in the form of development policy lending, supplemented by a limited number of specific investments in key areas, particularly infrastructure, and a robust analytic program.

International Finance Corporation (IFC) The IFC has a total committed investment portfolio in Bhutan of about $31 million. The portfolio consists predominantly of IFC’s equity participation in Bhutan National Bank. The advisory portfolio includes advice in structuring Public Private Partnerships (PPPs), improving Bhutan’s investment climate and enhancing access to financial services.

The IFC successfully completed a PPP transaction advisory for the multi-level car park project with the Thimphu Municipality. The project involves the development of two Multi-Level Car Parks (MLCPs) in order to address the parking requirements in the core city area.

IFC is providing assistance to the development of the power sector in the country by particularly assisting the Ministry of Economic Affairs and Druk Holding and Investments consider setting up a Power Trading Company in India.

IFC continues to explore areas of assistance in hydropower, tourism, manufacturing, agribusiness, health and education sectors among others. IFC’s advisory support on investment climate reforms, PPP development and the financial sector is expected to continue.

Multilateral Investment Guarantee Agency (MIGA) Bhutan has taken the first step to becoming a member of MIGA by signing the MIGA Convention in January 2013, which will be ratified by parliament in September 2013. In light of the newness of membership there has been no guarantee to date.

22

BHUTAN COUNTRY SNAPSHOT

BHUTAN: Decentralized Rural Development Project (DRDP) Additional Financing Key Dates: Approved: March 21, 2011 Effective: April 26, 2011 Closing: December 31, 2014 Financing in million USDollars*: Financier Financing

MDTF 5.00

Total Project Cost 5.00

Financier Total Disbursed Undisbursed

MDTF 5.00 5.0 0.0

*As of Sept 2014

Project Background: The Decentralized Rural Development Project (DRDP) was approved on March 1, 2005 for a credit of $7 million. Effective March 21, 2011 under the Global Food Crisis Response Program (GFRP) Multi-Donor Trust Fund, a grant for $5 million was allocated to Bhutan as additional financing for the DRDP. The additional DRDP grant funds were to help finance the costs associated with scaled-up activities and to address the impact of the continuing high prices associated with essential food commodities. Due to significant exchange rate savings/gains the project was restructured and the closing date extended to December 31, 2014.

Project Development Objective and brief component description: The project development objective is to improve market access and increase agricultural output for rural communities in selected areas of Bhutan. The project supports improvements/rehabilitation of rural infrastructure (rural roads and irrigation) and promotes extension activities particularly for rice, maize and potato crops to address disease outbreaks and low productivity. The DRDP Additional Financing supports three components. The first component focuses on the rehabilitation and construction of irrigation canals and on the improvement of selected roads that support rice, potato and maize production areas. The second component helps farmers improve production of rice and maize through demonstration, knowledge sharing, improved technologies and capacity building. Finally, the third component focuses on institutional strengthening activities such as capacity-building at the local-level administration, for planning aspects, and for the physical reporting of project implementation performance, to ensure the appropriate transfer of funds to the local level. In addition, capacity building activities for pest surveillance, financial management, environmental and social screening will be supported.

Results:

The project is on course to achieving its targets in improving rural infrastructure (irrigation canals and farm roads) and food crop production (rice, maize and potato). To date the project has benefitted over 8,272 households (target 6,700 households) from improved infrastructure and over 8,703 households (target 8,500 households) through improved extension services.

It has improved 43.95 km of farm roads, exceeding the end of project target of 15 km. Similarly, 256 km of irrigation canals have

been rehabilitated, exceeding the target of 200 km.

In the last cropping season Jan-Feb 2013, 111 tons of basic seeds of potatoes were produced. With the increase in number of contract farmers for seed production and also with the increase in National Seed Center (NSC) area for cultivation, the total basic seed production is expected to exceed the 700 metric ton target by the project closing date. . The adaptation rate for improved rice varieties is 45 percent against a project target of 25 percent. On the other hand, 27 metric tons of Green Leaf Spot (GLS) disease tolerant maize seeds were produced by community based seed production (CBSP) groups, resulting in 60 percent of GLS affected maize seeds being replaced. The target replacement rate for the project is 80 percent.

Key Partners: Ministry of Agriculture and Forests

23

BHUTAN COUNTRY SNAPSHOT

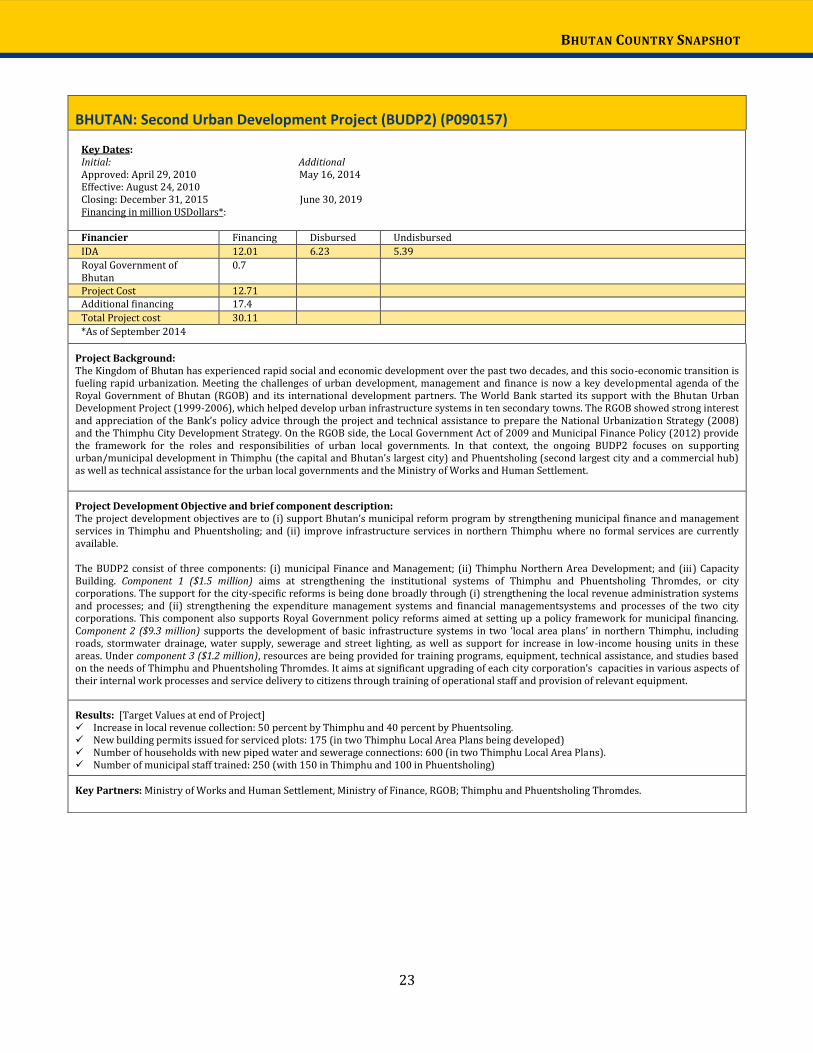

BHUTAN: Second Urban Development Project (BUDP2) (P090157) Key Dates: Initial: Additional Approved: April 29, 2010 May 16, 2014 Effective: August 24, 2010 Closing: December 31, 2015 June 30, 2019 Financing in million USDollars*: Financier Financing Disbursed Undisbursed

IDA 12.01 6.23 5.39

Royal Government of Bhutan

0.7

Project Cost 12.71 Additional financing 17.4

Total Project cost 30.11

*As of September 2014

Project Background: The Kingdom of Bhutan has experienced rapid social and economic development over the past two decades, and this socio-economic transition is fueling rapid urbanization. Meeting the challenges of urban development, management and finance is now a key developmental agenda of the Royal Government of Bhutan (RGOB) and its international development partners. The World Bank started its support with the Bhutan Urban Development Project (1999-2006), which helped develop urban infrastructure systems in ten secondary towns. The RGOB showed strong interest and appreciation of the Bank’s policy advice through the project and technical assistance to prepare the National Urbanization Strategy (2008) and the Thimphu City Development Strategy. On the RGOB side, the Local Government Act of 2009 and Municipal Finance Policy (2012) provide the framework for the roles and responsibilities of urban local governments. In that context, the ongoing BUDP2 focuses on supporting urban/municipal development in Thimphu (the capital and Bhutan’s largest city) and Phuentsholing (second largest city and a commercial hub) as well as technical assistance for the urban local governments and the Ministry of Works and Human Settlement.

Project Development Objective and brief component description: The project development objectives are to (i) support Bhutan’s municipal reform program by strengthening municipal finance and management services in Thimphu and Phuentsholing; and (ii) improve infrastructure services in northern Thimphu where no formal services are currently available. The BUDP2 consist of three components: (i) municipal Finance and Management; (ii) Thimphu Northern Area Development; and (iii) Capacity Building. Component 1 ($1.5 million) aims at strengthening the institutional systems of Thimphu and Phuentsholing Thromdes, or city corporations. The support for the city-specific reforms is being done broadly through (i) strengthening the local revenue administration systems and processes; and (ii) strengthening the expenditure management systems and financial managementsystems and processes of the two city corporations. This component also supports Royal Government policy reforms aimed at setting up a policy framework for municipal financing. Component 2 ($9.3 million) supports the development of basic infrastructure systems in two ‘local area plans’ in northern Thimphu, including roads, stormwater drainage, water supply, sewerage and street lighting, as well as support for increase in low-income housing units in these areas. Under component 3 ($1.2 million), resources are being provided for training programs, equipment, technical assistance, and studies based on the needs of Thimphu and Phuentsholing Thromdes. It aims at significant upgrading of each city corporation’s capacities in various aspects of their internal work processes and service delivery to citizens through training of operational staff and provision of relevant equipment.

Results: [Target Values at end of Project] Increase in local revenue collection: 50 percent by Thimphu and 40 percent by Phuentsoling. New building permits issued for serviced plots: 175 (in two Thimphu Local Area Plans being developed) Number of households with new piped water and sewerage connections: 600 (in two Thimphu Local Area Plans). Number of municipal staff trained: 250 (with 150 in Thimphu and 100 in Phuentsholing)

Key Partners: Ministry of Works and Human Settlement, Ministry of Finance, RGOB; Thimphu and Phuentsholing Thromdes.

24

BHUTAN COUNTRY SNAPSHOT

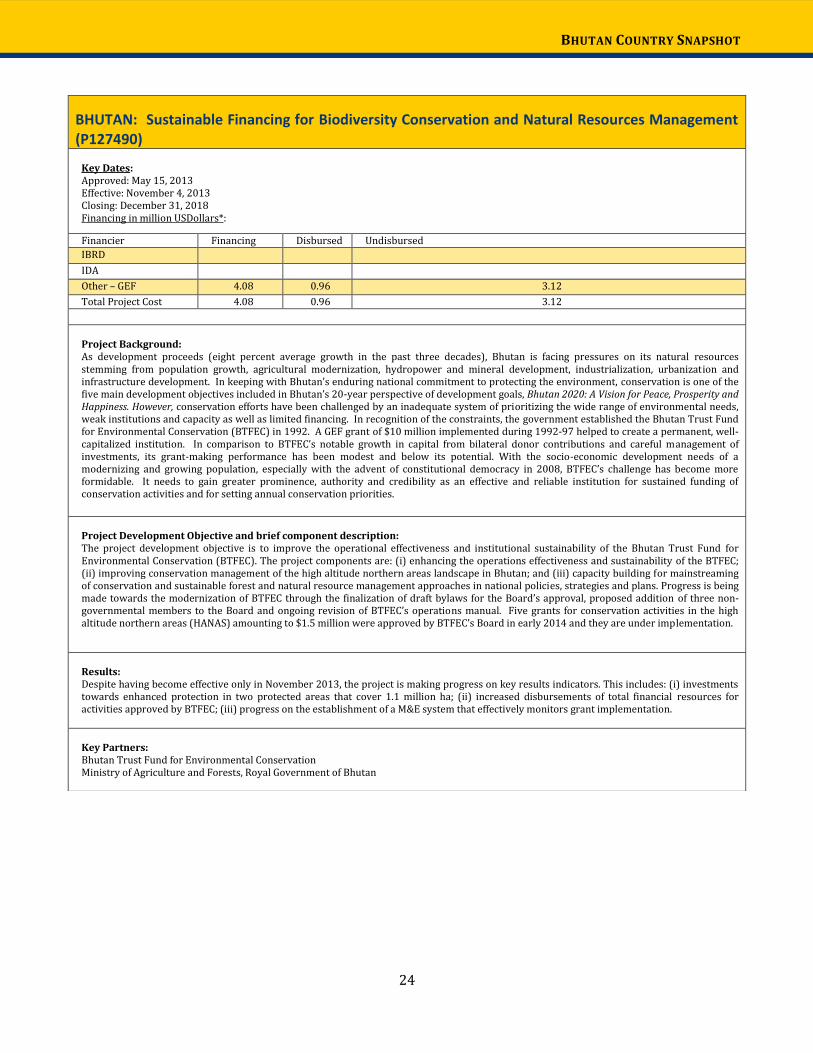

BHUTAN: Sustainable Financing for Biodiversity Conservation and Natural Resources Management (P127490)

Key Dates: Approved: May 15, 2013 Effective: November 4, 2013 Closing: December 31, 2018 Financing in million USDollars*:

Financier Financing Disbursed Undisbursed

IBRD

IDA

Other – GEF 4.08 0.96 3.12

Total Project Cost 4.08 0.96 3.12