Embed Size (px)

Citation preview

bhfs.com

409A In Operation: Recent Guidance on

Correcting Errors, Wage Reporting & Withholding

and Calculating Includable Income

Presented by Nancy A. StrelauFebruary 10, 2009

410 Seventeenth St. Suite 2200Denver, CO 80202

Brownstein Hyatt Farber Schreck, LLP

2

409A In Operation

• Correcting Operational Errors IRS Notice 2008-113

http://www.irs.gov/pub/irs-drop/n-08-113.pdf

• Wage Reporting and Withholding Requirements IRS Notice 2008-115

http://www.irs.gov/pub/irs-drop/n-08-115.pdf

• Calculating Amounts Includable in Income for 409A Noncompliance

Proposed Treasury Regulations

http://www.irs.gov/irb/2008-51_IRB/ar14.html

Obama directive to delay

3

Correcting Operational Errors

4

Correcting Operational Failures

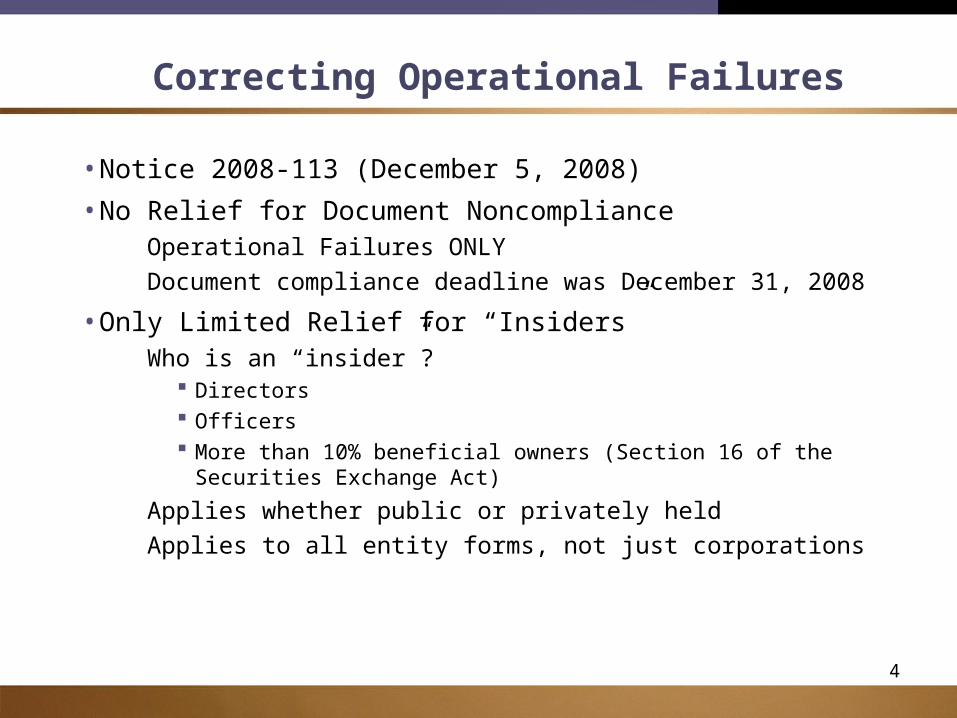

• Notice 2008-113 (December 5, 2008)

• No Relief for Document Noncompliance Operational Failures ONLY

Document compliance deadline was December 31, 2008

• Only Limited Relief for “Insiders” Who is an “insider”?

Directors Officers More than 10% beneficial owners (Section 16 of the Securities

Exchange Act)

Applies whether public or privately held

Applies to all entity forms, not just corporations

5

Eligibility for Correction Program

• Operational failure must be inadvertent and unintentional

Failure to follow 409A(a) in practice

Failure to follow 409A-compliant plan terms

Failure cannot be related to listed transaction under Treas. Reg. section 1.6011-4(b)(2)

• Tax return of service provider (employee) must not be under IRS examination

Year in which operational failure occurred

6

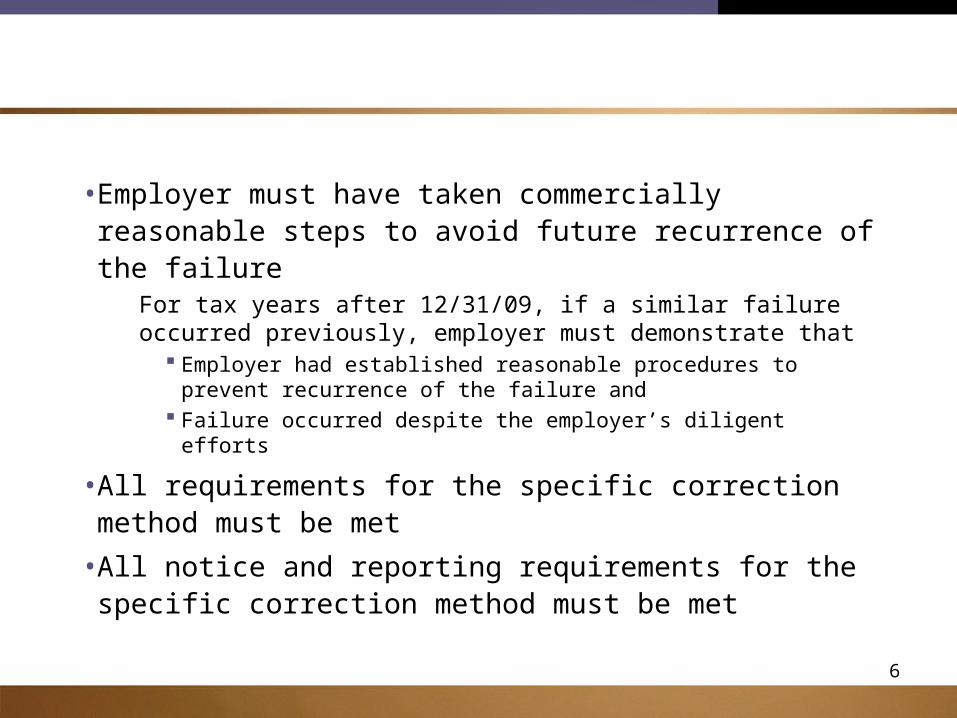

• Employer must have taken commercially reasonable steps to avoid future recurrence of the failure

For tax years after 12/31/09, if a similar failure occurred previously, employer must demonstrate that

Employer had established reasonable procedures to prevent recurrence of the failure and

Failure occurred despite the employer’s diligent efforts

• All requirements for the specific correction method must be met

• All notice and reporting requirements for the specific correction method must be met

7

• If error involves an erroneous payment, payment must not coincide with employer’s substantial financial downturn or other issues indicating a significant risk that the payment would not be paid when due

• The operational failure must be fully corrected

• There can be no “make-up” payments from employer to employee

8

General Categories of Operational Failures

• Payment of NQDC before the taxable year in which the amount was due to be paid under the terms of the plan

• Payment of NQDC more than 30 days before the date in the taxable year in which the amount was due to be paid under the terms of the plan

• Deferral of compensation less than or in excess of the amount that should have been deferred under the plan

• Payment of NQDC to a “specified employee” within 6 months of employment termination

• A stock right considered to provide for a deferral of compensation because exercise price is less than FMV on the date of the grant

9

Correction Made in Same Year as Failure

• Failure to defer amount or incorrect payment of an amount otherwise payable in a later year

• Early Payment Failures Employee repays the employer before year end of error

Employee may have to pay interest to employer

Examples: Payments resulting from failures to process deferral elections Payments made 30 days or more before payment date

• Late Payment Failures Employer must repay the employee

Employer may have to adjust for earnings or losses

Examples: Excess or improper deferral

10

• Non-Insider Payment Relief If service provider would incur an immediate and heavy

financial need if repayment made in the same year as error

Then repayment period may be extended for up to 24 months following the due date of employee’s tax return for the year in which the failure occurred

• Relief obtained No inclusion of income on vesting

No 20% penalty tax

No premium interest rate

No additional reporting and withholding

11

Correction Made After Year of Failure

• Available to non-insiders only

• May only correct in the year immediately following the year in which failure occurred

• Failure to defer or incorrect payment

• Early Payment Failures Employee must repay the employer - 24 month rule may apply Employee may have to pay interest to employer

• Late Payment Failures Employer must repay the employee Employer may have to adjust for earnings or losses

• Relief Obtained No 20% penalty tax No premium interest rate No additional reporting and withholding

12

Correction of Failures Involving Limited Amounts

• Failure must involve amounts less than annual elective deferral limit under IRC section 402(g)(1)(B)

$16,500 for 2009

• Limited relief to correct failures to defer small amount or erroneous early payment of small amount

• 409A income inclusion applies but limited to amount erroneously paid or made available

• Employee required to pay 20% tax Not required to pay the premium interest tax

13

Correcting Discounted Stock Options

• Background Nonstatutory stock options and SARS granted at no less than

100% FMV on date of grant are exempt from 409A

NQSOs and SARS granted at less than 100% FMV are subject to 409A

Standard stock option can’t comply with 409A

• Correction - Employers can reset exercise price of stock option and SAR to 100% FMV on original date of grant

14

• Correction must be made Before the stock right is exercised

For insiders – By December 31st of the year in which the stock right was granted

For non-insiders – By December 31st of the year following the year in which the stock right was granted

• Documentation must indicate the adjusted exercise price is to be at least 100% of FMV

• Relief applicable only to unexercised portion of the stock right

15

• Employer’s Federal tax return for tax year of correction Must be timely filed

Must include statement - “Section 409A Relief under Section V of Notice 2008-113”

Name and TIN of affected employee Identifying information about the plan under which the grant was

made A description of the circumstances surrounding the

misstatement of the exercise price The steps taken for correction and the date(s) taken A statement that the mispricing is eligible for correction and that

all required actions have been taken

16

• Notice to employee Contents similar to disclosure made with employer’s federal

income tax return

For corrections in same year, notice is discretionary

For corrections in following year, notice is required Employee must be informed that he has to attach this notice to

his personal tax return

Notice must be provided by Form W-2 distribution deadline for year in which correction made

17

Correcting Payments to Specified Employees

• Background – NQDC payments upon termination of employment to a “specified employee” of publicly traded company cannot be made for six months

• Eligibility Documentation providing for the payment must incorporate a

6 month delay provision

• Specified Employee = key employee under IRC 416(i) Limited to 50 officers with compensation in excess of IRC

401(a)(17) limit ($160,000 for 2009)

18

• Correction In Same Year as Mispayment By end of employee’s tax year, employee must repay the

gross value (including amount withheld for taxes) The repaid amount is not returned to the employee until

If repayment before the original correct payment date (the “6-month date”), new payment date is the 6-month date plus the number of days passed from the mispayment date through repayment date

If repayment after the 6-month date, new payment date is delayed for a number of days equal to the number of days from the mispayment date to the 6-month date

Adjustment for timing of withholding under IRC 6143 No adjustment for earning from mispayment date to

repayment date

19

• Correction in Year After Year of Mispayment Not available to specified employees who are insiders

By December 31 of year following year of mispayment, employee must pay gross value of the amount that should have been paid on the 6-month date

Repaid amount is not returned to employee until the number of days after the repayment date as the number of day that passed from the mispayment date through the 6-month date

Mispayment is reported as income on Form W-2 for year of mispayment

Reduction permitted if payment crosses years

20

• Employer’s Federal tax return for tax year of mispayment / year in which mispayment discovered

Must be timely filed

Must include a statement titled “Section 409A Relief under Section IV of Notice 2008-113”

Name and TIN of affected employee Identifying information about the plan under which the

mispayment was made A description of the circumstances surrounding the mispayment The steps taken for correction and the date(s) taken A statement that the mispayment is eligible for correction and

that all required actions have been taken

21

• Notice to employee Contents similar to disclosure made with employer’s federal

income tax return

Employee must be informed that he has to attach this notice to his personal tax return

Notice must be provided by Form W-2 distribution deadline for year in which correction made

22

What To Look Forward To

• Treasury Department and IRS considering a correction program for document failures

Seeking comments – due by March 6

• Possible extension of correction program for certain operational failures to allow service providers to repay an incorrect payment over an extended period

23

Wage Reporting and Withholding Requirements

24

Summary

• Notice 2008-115 (December 10, 2008)

• Extends guidance previously issued in Notice 2006-100 and Notice 2007-89

Continues to apply until further guidance issued

• Delays (again) the requirement for employers to report 409A compliant deferrals

• Explains how withholding and reporting requirements apply to includible amounts

• Explains how to calculate amounts includable in income for noncompliant NQDC plans

25

Employer Reporting and Wage Withholding

• 2008 Annual Deferrals For deferrals in 2008, suspends requirement to report on

Form W-2 (box 12, code Y) or Form 1099-MISc (box 15a)

• Reporting & Withholding on Amounts Includible in Gross Income

If NQDC plan fails to comply with 409A and amounts are includable in gross income for 2008, employer must treat such amount as “wages”

Employer must withhold federal income taxes at the applicable rate

Treated as “supplemental wages” to determine tax rate

Reported on Form 941 and Form W-2 (box 1 and 12, code Z)

26

• Calculation of amounts includible under 409A(a) for 2008

Amount includible in gross income for 2008 equals The portion of total amount deferred that is vested at 12/31/08

and not included in prior year income and Amounts paid in 2008

Exclude Grandfathered amounts (earned and vested before 1/1/05) Amounts reported on 2005, 2006 or 2007 Form W-2 or Form

1099-MISC

27

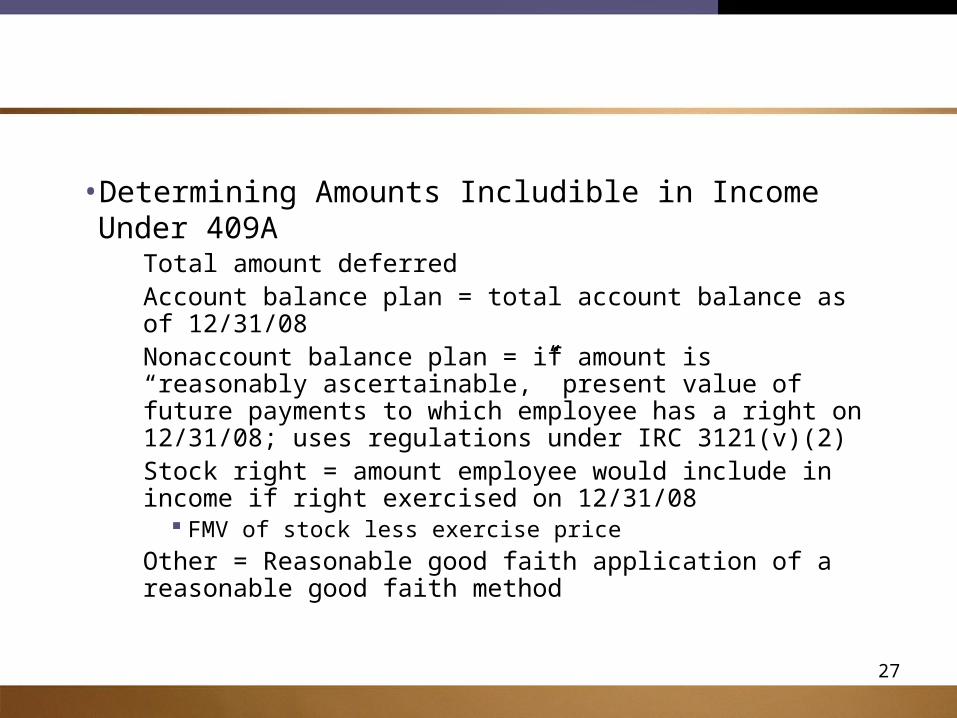

• Determining Amounts Includible in Income Under 409A Total amount deferred Account balance plan = total account balance as of 12/31/08 Nonaccount balance plan = if amount is “reasonably

ascertainable,” present value of future payments to which employee has a right on 12/31/08; uses regulations under IRC 3121(v)(2)

Stock right = amount employee would include in income if right exercised on 12/31/08

FMV of stock less exercise price

Other = Reasonable good faith application of a reasonable good faith method

28

• Wage Payment Date for 2008 Includable Amounts Wages = amounts actually or constructively received during

2008

Wages = amounts not actually or constructively received but are includible under 409A(a) treated as paid on 12/31/08

Employer can withhold required taxes before 2/1/09

Employer can pay the required withholding and treat the amount as additional wages to employee

29

Amounts Includible In Income under 409A(b)

• Amounts includible in gross income under 409A(b) Must be determined under a reasonable good faith

application of a reasonable, good faith method

Must be treated as wages for withholding and reporting

• Amounts subject to transition relief under Notice 2006-33 not includible income if NQDC plan became compliant with 409A(b) by 12/31/07

30

Protection from Future Additional Reporting and Withholding for 2008

• Employer that complies with Notice 2008-115 regarding computation of amounts includible in gross income will have no liability for additional income tax withholding or penalties resulting from future guidance

• Employer also will not be required to furnish corrected reporting as a result of future guidance

31

Service Provider Requirements

• Employee must report as income and pay taxes due on amounts includible in gross income by operation of 409A

• Calculate amounts per Notice 2008-115

• If fail to report and pay taxes on 2008 includible amounts may be subject to additional taxes and penalties

Interest on underpayments or taxes resulting from a failure

32

Impact on Transition Relief

• Notice 2007-86 extended the deadline for amending NQDC plans for 409A compliance to 12/31/08

• If comply with Notice 2007-86, and have operational compliance, amounts deferred under NQDC should not be includible income for 2008 or any subsequent year

33

Calculating Amounts Includable in Income for 409A

Noncompliance

34

• Proposed Regulations address: Calculation of amounts that must be included in taxable

income if NQDC doesn’t comply with 409A in form or operation

Calculation of the additional 20% penalty tax applicable to such income

Calculation of the premium interest tax on amounts that should have been included in taxable income in prior years (underpayments)

• Degree of reliance on proposed regulations to be determined in future guidance

• White House memo dated January 20, 2009

35

• General rule – If NQDC plan fails to comply with 409A in form or operation, service provider (employee) will recognize income equal to the compensation deferred to the extent vested

• Consequences Includible income subject to income tax at regular rate plus

20%

Includible income may be subject to an additional premium interest tax

36

Amounts Includible in Income

• In event of a 409A failure, the amount includible in income means the “total amount deferred” under the NQDC plan for the taxable year less the portion that is unvested or previously included in income

“Previously included in income” = Amounts actually income on an original or amended tax return or as a result of an IRS examination or court decision

37

Total Amount Deferred for a Taxable Year

• Total Amount Deferred for a Taxable Year Equals: Present value of the future payments to which the service

provider has a legally binding right on the last day of the taxable year PLUS

The payments of deferred that are made during the year Proposed regulations specify in detail how present value is

calculated – varies for different types of future payments – and the assumptions that can be used

38

• Account balance plan Total of the account balances

• Nonaccount balance plan Present value of future payments

Disregard potential additional service credits

Disregard compensation increases after year end

• Unexercised stock option or SAR The spread value on the last day of the taxable year

The cash and FMV of the stock to be received on exercise, less the exercise price

39

Application of Additional 20% Tax

• This tax is subject to the rules governing the assessment, collection and payment of income taxes

40

Premium Interest Tax

• This is an additional tax to account for underpayment of taxes in prior years

• Amount of premium interest tax The interest at the applicable underpayment rate plus 1% that

would have been owed on the tax underpayment that would have occurred if the deferred amount had been included in income for the prior taxable years in which it was first deferred or became vested

• This tax is subject to the rules governing the assessment, collection and payment of income taxes

41

• Proposed regulations contain detailed methodology for calculating the premium interest tax

• Allocates the amount includible in income under 409A(a) to the prior taxable years in which the amount or portion thereof was first deferred or became vested

• Then determines the hypothetical tax underpayment for each prior taxable year

Allocated amount is treated as additional cash compensation paid to the service provider during the prior taxable year

42

• Hypothetical tax underpayment is calculated based on Deemed payment of additional cash compensation (above)

Service provider’s taxable income, credits, filing status and other tax information for the prior taxable year

Availability of deductions Use of carryovers

• Hypothetical tax underpayment calculation in subsequent years must consider changes in previous taxable year

As a result of the additional compensation income treated as paid in such previous year

43

Allocation to Subsequent Payouts

• Any amount included in income under 409A is not required to be included under any other provisions of the Code at any later time

• Proposed regulation describe the process for determining when amounts paid from an NQDC plan are treated as previously included in income

Deemed basis in the deferred compensation payments is recovered first

The first payments are treated as amounts already included in income until the deemed basis is recovered

After basis is recovered, payments will be includible in income

44

Deduction for Forfeited Amounts

• Proposed regulations provide for the treatment of deferred compensation that was included in income, but was never received due to permanent forfeiture

• Taxpayer can take a deduction for the taxable year in which the forfeiture occurs

As long as no amounts remain deferred under the plan

• Deduction equal to the forfeited amount previously included in income, less any portion allocated to subsequent payments under the deemed basis recovery procedure (described above)

45

Correcting Future Compliance Failures

• Failure in one taxable year may not cause a continuing or permanent failure

Failure to comply with 409A(a) during a taxable year would not result in the taxation of amounts deferred under the plan for subsequent taxable years if the plan complies during those subsequent years

• The deferred compensation amount includible in income under 409A for any taxable year is determined on a year-by-year basis

Determined as of the last day of the year Excludes amounts subject to a substantial risk of forfeiture

(vesting)

46

• Significance If NQDC plan is noncompliant at some point during a year and

If, as of the last day of the year, all of the employee’s deferred compensation is not vested

Then 409A penalties won’t apply for that year to compensation deferred by the employee under the NQDC plan

• Also If prior to the year in which deferred compensation becomes vested,

the NQDC plan is amended and operates in compliance with 409A

Then 409A penalties won’t apply in the vesting year or subsequent years

• Don’t rely on as a planning tool, though!! Treasury Department and IRS authority to prevent abuse of this rule

47

CONCLUSION / RECOMMENDATONS

• IRS gearing up for enforcement?

• Correction program rewards early detection and correction

Less tax

Easier procedures

• Don’t be an ostrich Address discovered issues immediately

Implement measures to prevent occurrence / recurrence of failures

48

CONCLUSION / RECOMMENDATONS

• Action steps: Conduct internal audit

Correct identified operational failures

Create an oversight committee

Develop written procedures

Train personnel

Counsel / notify participants

Timely report income and excise taxes

49

Questions?

Nancy A. StrelauBrownstein Hyatt Farber Schreck, LLP

410 Seventeenth Street, Suite 2200Denver, CO 80202

(303) [email protected]