-

8/12/2019 Bhalani Diamond

1/24

1

ContentsSection I: Executive Summary

................................................................................................

2

Section II: Business Description

.............................................................................................

3

A. General description of the business

................................................................................................

3

B. Industry Background

......................................................................................................................

3

C. Goals and potential of the business and milestones

.......................................................................

5

D. Uniqueness of product or service

...................................................................................................

5

Section III: Marketing

.............................................................................................................

7

A. Research and analysis

....................................................................................................................

7

1. Target Market (customers) Identified

.........................................................................................

7

2. Market Size and Trends

...............................................................................................................

7

3. Competition

................................................................................................................................

8

4. Estimated Market Share

.............................................................................................................

8

5. Distribution

.................................................................................................................................

9

Section IV: Operations

..........................................................................................................

10

A. Identify Location

..........................................................................................................................

10

B. Proximity to supplies

....................................................................................................................

10

C. Access to transportation

...............................................................................................................

10

Section V: Management

........................................................................................................

11

A. Management team-key

personne...............................................................................................

11

B. Legal structure-stock agreements, employment agreements,

ownership .................................. 11

Section VI: Financial

.............................................................................................................

12

A. Financial forecast

.........................................................................................................................

12

1. Profit and Loss(Estimation)

.......................................................................................................

12

2. Break-even analysis (Estimation)

..............................................................................................

13

3. Cash flow (Estimation)

..............................................................................................................

14

2. Budgeting Plan

..........................................................................................................................

15

Section VII: Critical Risks

....................................................................................................

17

A. Potential problems

.....................................................................................................................

17B. Obstacles and risks

....................................................................................................................

21

Section VIII: Harvest Strategy

.............................................................................................

23

Marketing

Strategy........................................................................................................................

23

Section IX: Milestone Schedule

............................................................................................

24

-

8/12/2019 Bhalani Diamond

2/24

2

Section I: Executive Summary

A present situation of diamond industry is very strong. Shortage

of diamond is taken place in

future. Price of diamond is continuously growing it is strong

point of selecting diamond

industry. Availability of aircraft in Surat is creating a great

opportunity for diamond industry.

India has always been center stage in the dramatic history of

some of the worlds most

famous diamonds. India has been the earliest known source of

diamonds. Conversely, today

India is a pioneer in the gem industry and a world leader in the

manufacturing of cut and

polished diamonds. The diamonds used in jewelry worldwide, nine

out of every ten cut andpolished diamond come from India.

The Indian Diamond Industry is currently going through a

downturn phase. The total exports

of cut and polished diamonds during FY 2011-12 and 2012-13

(Apr-Dec) witnessed decline

of 17% and 36% respectively. USA is the major market for

diamonds as exports to the USA

are pegged at US 6.1 billion higher than that from Belgium and

Israel. Though the

diamond sales have bottomed out, the industry is expected to

witness positive growth in

festive months during October-December 2013. Our share in the

USA has started declining;

the industry strongly believes that the USA will continue to be

a strong global trading partner.

-

8/12/2019 Bhalani Diamond

3/24

3

Section II: Business Description

A. General description of the businessMANUFACTURING THE

DIAMOND

Cut is the only diamond characteristic under human control, and

considered by many to be

the most important. A good cut can offset a lower color or

clarity; however, even a D-color,

Internally Flawless stone will not look its best if the cut or

"make" is poor. A poor cut

actually reduces the brilliance, sparkle and scintillations of a

diamond.

The decision to cut a diamond in a particular shape is dictated

by the natural shape of the

rough stone. Some stones are naturally oblong and are destined

to become marquises, ovals

or pear shapes. Some rough diamonds occur in near perfect

crystal shapes and these will

more than likely be cut as princess cuts or some other square

cut.

B. Industry Background

Diamonds account for 54% of the total gem and the Jewellery

export basket of the industry

and India is the worlds leading exporterof Cut and Polished

Diamonds. A major contributor

to the creditable performance of the industry is the massive

diamond manufacturing sector,

which employs nearly one million people across the country. The

industry has grown from

its small origins in the 50s and has established itself as the

worlds largest manufacturing

center of cut and polished diamonds for the last many years,

contributing 60% of the worlds

supply in terms of value, 85% in terms of volume and 92% in

terms of pieces. Surat along

with Navsari, Bhavnagar, Amreli are known as the diamond

manufacturing/processing hub

whereas Mumbai is the diamond trading hub.

-

8/12/2019 Bhalani Diamond

4/24

4

India is the world leader in diamonds both in quantity and value

terms. This pre- eminent

position has been achieved through progressive liberalization of

Government policies,

entrepreneurships and skilled labor. India has achieved global

leadership position, in thebusiness of cutting and polishing

diamonds also due to its price competitiveness and

willingness to work for low margins.

14 out of every 15 diamonds set in jewelry worldwide are

processed in India. India has

already established itself as International Diamond

Manufacturing Hub. Indian

diamantaires have gone on to create a marketing network

worldwide. Added to this is the

strong financial base of the industry and support of financial

institutions of the country.

Today, after creating a niche for itself in the diamond world

with small diamonds, India is

developing skills for cutting and polishing larger stones and

fancy cuts. Indian diamond

polishing factories are on par with the worlds best employing

cutting edge of technology

using laser machine, computerized yield planning machines,

advanced bruiting lathe,

diamond impregnated scarves etc.

-

8/12/2019 Bhalani Diamond

5/24

5

Growth rate of diamond industry

Retail diamond prices in the second half of 2008 experienced one

of the largest decreases in

decades and followed by relatively no price changes up or down

in 2009. However, rough

diamond prices in 2009 were up by about 15% and they have

increased that much already in

2010. As a result, there is significant pressure on polished

diamond prices to move upward.

C. Goals and potential of the business and milestones

Be the world largest diamond manufacturing organization with

high customer andemployee satisfaction.

D. Uniqueness of product or service

By finding the new cutting designing of diamond organization

provides new and innovative

to the customer. By finding new machinery for diamond cutting we

introduce new methods

of production and manufacturing.

Nimbark Gems main product is loose diamonds, from emerald-cut to

round-cut diamonds,

with brilliant color and V VS 1, meaning Very, Very Slightly

Included, or an excellent

quality diamond. All of NIMBARK GEMS's diamonds are GIA

certified (Gemological

Institute of America) with laser inscription inside. NIMBARK

GEMS was positioned as a

diamond wholesaler rather than a retailer in the past. NIMBARK

GEMS had been supplying

-

8/12/2019 Bhalani Diamond

6/24

6

local jewelers in the area for more than twenty years and

maintained very strong

relationships.

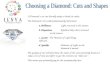

In the diamond business, we determine the price of a diamond

according to the "4C" criteria:

Clarity

The most expensive diamond is the one that is absolutely clear

in clarity, but many of them

have inclusions (scratches or trace minerals) that can detract

from the pure beauty of the

diamond. Clarity has several categories that affect the price of

a diamond: FL (Flawless, no

internal/external flaws), VVS1, VVS2 (Very, Very Slightly

Included, an excellent quality of

diamond), VS1, VS2 (Very Slightly Included, not visible to the

eye), S1, S2 (Slightly

Included, may be visible to the eye), I1, I2, I3 (Included, the

lowest grades of clarity).

NIMBARK GEMS does not carry the last two clarity grades in its

inventory.

Color

A diamond can divide light into a spectrum of colors, and

reflect light as more or less

colorful, depending on the color grade. The less color in a

diamond, the better the color

grade. Color grades are categorized into D (absolutely

colorless, the highest color grade), E

(colorless, only traces of color and only detected by

gemologists), F (colorless, slight color

detected, still a high quality diamond), G-H (near colorless,

color noticeable, but still an

excellent value), I-J (near colorless, color slightly

detectable), K-M (low grade color), N-Z

(low grade color). NIMBARK GEMS does not carry the last three

color grades in its

inventory to maintain a good selection of diamonds.

Cut

The roundness, depth, width and uniformity of the facets

determine a diamond's brilliance.

Cut is the most important characteristic of a diamond; even with

perfect color and clarity, a

poor cut will affect its brilliance.

Carat

The weight of a diamond. In the engagement-ring market today,

usually the "dowry" is

around 1 carat and above.

-

8/12/2019 Bhalani Diamond

7/24

7

Section III: Marketing

A. Research and analysis

1. Target Market (customers) Identified

The main reason behind the selection of this target segment is

that the engagement ring

market has been the largest segment in diamond purchasing in the

U.S. for the last three

decades. In a patriarchal tradition, men offering their marriage

proposal usually accompany it

with a gift. The gift has to represent something that is

valuable to both families or parties.

The female target market segment had been showing a significant

growth in the last three

yeaThis trend has contributed to the NIMBARK GEMS diamond

expansion plan by adding

innovative cutting design into the sales strategy.

Here target market for NIMBARK GEMS Diamond will be

international as well as national

jewelry manufacture and investor.

2. Market Size and Trends

The US remains the worlds biggest consumer market for diamond

jewelry at around 40% of

global sales by value. Japan remained resiliently at around 8%

despite last Marchs

environmental catastrophe.

The emerging markets, led by China and India, continue to grow

strongly, despite a

slowdown in the levels of growth in 2012. Bain estimates Chinese

diamond jewelry demand

to have grown between 2005 and 2011 at 32% CAGR; and India at

22% CAGR. Chinese

consumption for diamond is still predicted to have grown by 10%

in 2012, and India at a

similar level. Indeed these two markets combined are anticipated

to exceed the size of the US

market by 2020.

-

8/12/2019 Bhalani Diamond

8/24

8

3. Competition

K. A. International Blue Nile Diamonds.com Mondera Sanjay

Brothers Srp & Sons Diamonds Pvt. Ltd. Hari Krishna Exports

Pvt. Ltd. Parul Diamond Bhumika Gems Khodal Star Mazal Diamond

Shashi Gems Siddhi Gems Anjali Diam Soham Overseas - India RS

Exports - India SANGHAVI JEWELLERY MFG . CO . PVT . LTD - India

CLASSIC DIAMONDS (I) LTD., - India Arihant Star - India Al Hussain

Fragrances & JewelsIndia JAGRUTI GEMS & JEWELLERYIndia

Jamuna Dass & Sons - India Dharmanandan DiamondsIndia Adani

Exports Ltd. - India

4. Estimated Market Share

34% in Indian Diamond Market 11% in International market

http://www.exportersindia.com/kainternational/http://www.exportersindia.com/sanjaybrothers/http://www.exportersindia.com/goti-diamonds/http://www.exportersindia.com/harikrishnaexports/http://www.exportersindia.com/parul-diamond/http://www.exportersindia.com/bhumikagems/http://www.exportersindia.com/khodal-star/http://www.exportersindia.com/mazal-diamond-shashi-gems/http://www.exportersindia.com/siddhigems/http://www.exportersindia.com/anjali-diam/http://www.exportersindia.com/anjali-diam/http://www.exportersindia.com/siddhigems/http://www.exportersindia.com/mazal-diamond-shashi-gems/http://www.exportersindia.com/khodal-star/http://www.exportersindia.com/bhumikagems/http://www.exportersindia.com/parul-diamond/http://www.exportersindia.com/harikrishnaexports/http://www.exportersindia.com/goti-diamonds/http://www.exportersindia.com/sanjaybrothers/http://www.exportersindia.com/kainternational/

-

8/12/2019 Bhalani Diamond

9/24

9

5. Distribution

The products (diamonds) move from diamond mines to diamond

cutters, then either directly

to large retailers, or to wholesalers, who further distribute

them to smaller retaile

In short, major jewelry stores could sell much cheaper diamonds

than the mom-and-pop

shops, as they purchase larger quantities than their local

counterparts. However, the mom-

and-pop jewelry shops do consignment sales with their diamond

suppliers to compete with

large jewelry chains.

Customers who already have a long-term relationship with their

local stores usually trust their

local jewelers more than the large brands. The consignment

business strategy had enabledmom-and-pop jewelry stores to compete

with large, middle-end diamond retailer giants such

as Zales Corporation.

-

8/12/2019 Bhalani Diamond

10/24

10

Section IV: Operations

A. Identify Location

1. Advantages

The diamond cutting Factory is rural and village area of

Gujarat, because this businessrequired more manpower and also woman

labor.

Office of assorting in city areas like Surat, Bhavnagar, and

Mumbai because businessrequired facility like Exporting, banking,

and Insurance.

2. Zoning

Factory In rural zone Office at urban zone No need manufacturing

in to GIDC and Special Industrial Zone3. Taxes

Diamond Cutting Business is Art work business so that there are

no required for specialtaxes saving and Cutting

Business has to pay the Taxes of Export and Import.

B. Proximity to supplies

For the diamond polish and cutting business the raw material i.e

rough Diamond are to

require from the urban country such as Africa, USA.

The main supplier for diamond manufacturing is those who have

license for importing

rough diamond.

We can collect rough diamond from Surat market, Mumbai market

and at Bhavnagar Market.

C. Access to transportation

For the Transportation of rough Diamond we use Angadiya service

because diamond

required safety and security.

-

8/12/2019 Bhalani Diamond

11/24

11

Section V: Management

A.Management team-key personnel Mr.Nagjibhai Bhalani(Founder)

Mr.Pradip Bhalani (Partner) Mr.Manoj Bhalani (Partner)

B.Legal structure-stock agreements, employment agreements,

ownership The NIMBARK GEMS GEMS be the Partnership firm. NAME OF

PARTNERS Mr.Nagjibhai Bhalani Mr.Pradip Bhalani Mr.Manoj

Bhalani

-

8/12/2019 Bhalani Diamond

12/24

12

Section VI: Financial

A. Financial forecast

1. Profit and Loss(Estimation)

2014 2015 2016

Sales 5,360,000 6,432,000 7,716,900

Direct Cost of Sales 3,752,000 4,502,800 5,400,400

Other Costs of Sales 138,600 166,400 199,600

Total Cost of Sales 3,890,600 4,669,200 5,600,000

Gross Margin 1,469,400 1,762,800 2,116,900

Gross Margin % 27.41% 27.41% 27.43%

Expenses

Payroll 546,799 546,800 546,800

Marketing/Promotion 48,000 48,000 48,000

Depreciation 0 0 0

Rent @ Brannan Street 36,000 36,000 36,000

Utilities @ Brannan Street 4,200 4,200 4,200

Warehouse Utilities 7,200 7,200 7,200

Payroll Taxes 0 0 0

-

8/12/2019 Bhalani Diamond

13/24

13

Warehouse Rent 72,000 72,000 72,000

Web Hosting 480 480 480

Database Maintenance 100 100 100

Shipping 30,000 30,000 30,000

Total Operating Expenses 744,779 744,780 744,780

Profit Before Interest and Taxes 724,621 1,018,020 1,372,120

EBITDA 724,621 1,018,020 1,372,120

Interest Expense 0 0 0

Taxes Incurred 217,386 305,406 411,636

Net Profit 507,234 712,614 960,484

Net Profit/Sales 9.46% 11.08% 12.45%

2. Break-even analysis(Estimation)

With monthly fixed costs and variable costs, the table and chart

below show what we need to

sell in diamonds each month to break even. We are well past the

break-even point, even with

these lower margins.

Monthly Revenue Break-even 206,883

Assumptions:

Average Percent Variable Cost 70%

Estimated Monthly Fixed Cost 62,065

-

8/12/2019 Bhalani Diamond

14/24

14

3. Cash flow(Estimation)

2014 2015 2016

Cash Received

Cash from Operations

Cash Sales 5,360,000 6,432,000 7,716,900

Subtotal Cash from Operations 5,360,000 6,432,000 7,716,900

Additional Cash Received

Sales Tax, VAT, HST/GST Received 0 0 0

New Current Borrowing 0 0 0

New Other Liabilities (interest-free) 0 0 0

New Long-term Liabilities 0 0 0

Sales of Other Current Assets 0 0 0

Sales of Long-term Assets 0 0 0

New Investment Received 0 0 0

Subtotal Cash Received 5,360,000 6,432,000 7,716,900

Expenditures 2006 2007 2008

Expenditures from Operations

Cash Spending 546,799 546,800 546,800

Bill Payments 3,791,764 5,151,736 6,198,175

-

8/12/2019 Bhalani Diamond

15/24

15

Subtotal Spent on Operations 4,338,563 5,698,536 6,744,975

Additional Cash Spent

Sales Tax, VAT, HST/GST Paid Out 0 0 0

Principal Repayment of Current Borrowing 0 0 0

Other Liabilities Principal Repayment 0 0 0

Long-term Liabilities Principal Repayment 0 0 0

Purchase Other Current Assets 0 0 0

Purchase Long-term Assets 0 0 0

Dividends 0 0 0

Subtotal Cash Spent 4,338,563 5,698,536 6,744,975

Net Cash Flow 1,021,437 733,464 971,925

Cash Balance 3,308,437 4,041,902 5,013,827

3. Budgeting Plan

Future Performance(Estimation)

2014 2015 2016

Sales 3,300,000 3,630,000 3,993,000

Gross Margin 1,320,000 1,452,000 1,597,200

Gross Margin % 40.00% 40.00% 40.00%

Operating Expenses 900,000 900,000 900,000

Inventory Turnover 0.00 0.00 7.99

Balance Sheet

2014 2015 2016

Current Assets

-

8/12/2019 Bhalani Diamond

16/24

16

Cash 3,080,000 2,752,000 2,287,000

Inventory 0 0 600,000

Other Current Assets 600,000 200,000 30,000

Total Current Assets 3,680,000 2,952,000 2,917,000

Total Assets 3,680,000 2,952,000 2,917,000

Current Liabilities

Accounts Payable 260,000 200,000 120,000

Current Borrowing 0 0 0

Other Current Liabilities (interest

free) 0 0 0

Total Current Liabilities 260,000 200,000 120,000

Long-term Liabilities 0 0 0

Total Liabilities 260,000 200,000 120,000

Paid-in Capital 3,000,000 2,200,000 1,500,000

Retained Earnings 420,000 552,000 1,297,000

Earnings 0 0 0

Total Capital 3,420,000 2,752,000 2,797,000

Total Capital and Liabilities 3,680,000 2,952,000 2,917,000

Other Inputs

Payment Days 30 30 30

-

8/12/2019 Bhalani Diamond

17/24

17

Section VII: Critical Risks

A.Potential problemsThe PESTEL Analysis

The macro environment includes all relevant focus outside a

companys boundaries relevant

in the sense that they are important enough to have brought on

the decision. An industry

ultimately makes about its business model and strategy.

Why many forces in the micro environment are beyond a companys

sphere of influence?

Companys strategy may be needed for answer it. Micro environment

includes all general

force that do not directly touch on the short run activities of

the organization but that

can and often does, indulgence itsalso ran decisions.

1.Political Factors

The Government of India (GOI) has been working to develop the

Diamond industry in

India through several initiatives but under the purview of

Diamond industry. The main

political factors are as follows.

Excise duty: In the budget of year 2008-09 government reduce

excise duty from 10%to 5% on cut and polished diamond units.

Marketing and control orders: Import of rough diamonds

controlled by the Jewelryexport Promotion Councils.The Council

provides market information to its members

regarding foreign trade inquiries, trade and tariff regulations,

rates of import duties,

and information about Diamond fairs and exhibitions. FDI

approval: India is now the third most favored destination for

Foreign Direct

Investment (FDI), Government of India may permits 49% of FDI in

the Diamond

industry. FDI of 2 billion are invested in terms of working

capital in the industry.

-

8/12/2019 Bhalani Diamond

18/24

18

Trade Policy for Diamond

Replenishment Licenses:

The exporters of gem and Diamond products are entitled for REP

license as per rates

indicated in the Handbook of Procedures. Such licenses are

transferable.

Diamond Impress License:

Diamond Impress Licenses are issued in advance for import of

rough diamonds and for

export of cut and polished diamonds. These licenses or the

materials imported against them

may be freely transferred after the export obligation has been

fulfilled.

Bulk Licenses for Rough Diamonds

Bulk licenses for rough diamonds are allowed to any exporter

whose annual average f.o.b.

value of exports of cut and polished diamonds during the

preceding three licensing years was

not less than 75 crores and iv) any overseas Company with its

branch office in India whose

annual turnover in diamond during the preceding three licensing

years is not less than 150

crores.

Import of raw material (rough diamonds) is highly affected by

war and global marketconditions.

Fund contribution: As per current scenario to ease the liquidity

problem in diamondindustry the task force constituted by RBI.

Task Force may propose asking banks to finance diamond

manufacturers especially

small and medium ones against their stock of polished

diamonds.

2. Economic factors

Per capita consumption: Per capita consumption power of

customers may highly affect

diamond jewelry purchase. India`s per capita income is likely to

grow more than double over

the last seven years, to Rs 38,084 in the current fiscal,

reflecting improvement in the living

standards of the average Indian.

Per capita income, according to the advance estimates for

national income is expectedto grow by 14% during the current

fiscal.

However, after discounting for inflation, per capita income is

expected to rise to Rs25,661 representing an increase of 5.6%.

-

8/12/2019 Bhalani Diamond

19/24

19

3. Social factors

The main social factors of the organization, which are deals as

the business organization

are as follows.

Emergence of retail org. makes people aware about diamond as a

luxury product or aninvestment option.

Emergence of substitute: Diamond Diamond is preferred by

consumers with increasein the price gold.

Changing consumer preferences: with the increase in standard of

living consumerpreference change from gold Diamond to diamond

Diamond, its also considered for

status symbol.

4. Technological factors

The main technological are as follows.

As diamond industry try to moving up in to the value chain they

are focusing more onthey use high end equipments.

Technology solutions are also available for production control,

supply chain andinventory management in the Diamond industry.

The Special Economic Zones and Diamond Parks developed in

various states offer

technology-enabled environments that are conductive to growth

and quality production.

5. Environment Factors

This section draws on literature relating to the general

environmental impacts associated with

ASM and related processing activities, and where

availablespecific information relating

to the production of gemstones. In relation to environmental

impacts of ASM and gemstone

ASM in particular, the situation in each country varies

according to the type of gemstones

being exploited, the social and natural environment of the area

and cultural and

organizational aspects of the mining operation itself.

-

8/12/2019 Bhalani Diamond

20/24

20

Exploration Underground Extraction Surface Extraction River

Dredging

Due to the unique geological nature of gemstone deposits,

whereby mineralization is

localized in small pockets, processing of mined gemstones

differs from one gem to another.

Generally, however, the processing of gemstones that occur as

distinct crystals consists of

hand sorting with the aid of the visual characteristics of the

gems (fluorescence, shine, color).

Typically, no equipment is used in this process. Normally, such

pieces recovered during

hand-sorting in the pits and trenches still need

-

8/12/2019 Bhalani Diamond

21/24

21

6. Legal Factors

Trade Facilitator: The Council undertakes direct promotional

activities likeorganising joint participation in international

Diamond shows, sending and hosting

trade delegations.

Advisory Role: A crucial area of activity of the Council has

also been aiding betterinteraction and understanding between the

trade and the government.

Nodal Agency for Kimberly Process Certification Scheme: GJEPC

has beenappointed as the Nodal Agency in India under the Kimberly

Process CertificationScheme.

Training and Research: The Gems & Diamond Export Promotion

Council runs anumber of institutions that provide regular and

part-time training in all aspects of

manufacture and design in Mumbai, Delhi, Surat and Jaipur.

Boosting Exports: Among the promotional activities GJEPC

undertakes for thesector is the organising of joint participation

of member - exporters in some importantinternational exhibitions

and puts up promotional stalls in othe

B. Obstacles and risksThreats from close substitute:

As entrance of Synthetic diamond which is close substitute of

real diamond leads to

threats for Indian diamond industry.

China, Sri Lanka and Thailands entry in small diamond segment

Infrastructural bottlenecks, frequent changes in ex-im policies,

irregular supply of

gold.

Over dependence on single-channel supply chain. Decisions of De

Beers and Argylesterms for renewing their supply contract.

High domestic interest rates compared to elsewhere:The overall

lending rate in Indian financial market is too high with comparison

to

-

8/12/2019 Bhalani Diamond

22/24

22

financial Market of other countries so it affects the overall

investment of country along

with the investment in diamond.

Small firms lacking technological/ export information

expertise:

As small firm not have so much capital fund to invest in

technology and research and

development because of this they havent get benefit of

technological advancement.

Low productivity compared to labor in china, Thailand and Sri

lanka:

The labours of Indian diamond industry are less productive than

the labour of China,

Thailand, and Srilanka.

High carring cost:

As the major raw material requirements need to be imported,

companies normally stock

huge quantities of inventory resulting high inventory carrying

costs.

-

8/12/2019 Bhalani Diamond

23/24

23

Section VIII: Harvest Strategy

The growth strategy of NIMBARK GEMS will require an expansion of

the current divisions

inside the organization, a restructuring of the company. Without

the benefits of the

restructuring, it is likely that the NIMBARK GEMS business will

stagnate. The process of

restructuring, however, is not without any risk, as the current

business practices that had been

the foundation of the company will have to be slightly adjusted

in response to today's retail

environment.

There will be two phases of restructuring the company. First,

changes will be made in the

current NIMBARK GEMS location. Second, we must revamp the

NIMBARK GEMS brandto build and strengthen customers' "emotional"

attachment to it.

The revised brand messaging will suggest the companys

seriousness in increasing its value

in serving the customers. Some of the characteristics of the new

brand will reflect the sense

of:

Sophistication Exclusivity Globalization Professionalism Respect

Fashionable/Contemporary Youthful Mysticism

Marketing Strategy

The concept of e-marketing is similar to a traditional

marketing, which is the process of

planning and executing conception, pricing, promotion, and

distribution of ideas, goods, and

services to create exchanges that satisfy the company's

objectives. Marketing does not

necessarily mean forms of advertising of products, but fully

utilizing all of the company's

resources into getting the customers to buy our products. In

this case study, we will explore

the three marketing strategies for NIMBARK GEMS that are

involved in e-commerce

marketing, including posting and positioning, and traditional

marketing, including advertising

and the combination of all.

-

8/12/2019 Bhalani Diamond

24/24

Section IX: Milestone Schedule

The milestones program shows the detailed implementation

schedule for NIMBARK

GEMS's expansion in its product portfolio and distribution

strategy. Partner himself will lead

the project in finding potential upscale jewelry stores in the

area, and control the budget in

several strategic areas.

Deadlines and Milestones

Milestone Start Date End Date Budget Department

Website Redesign 20/11/2014 12/2/2015 500 IT

Annual Marketing Program 16/11/2014 2/1/2015 48,000

Marketing

Finding Potential Jeweler

Partner 28/10/2014 6/6/2015 1,200 Business Dvpmnt

Establish Alliance With

Internet Vendors 15/12/20014 10/2/2015 1,200 Business Dvpmnt

Establish RelationshipWith Outsourcing

Workshops 2/12/2014 12/2/2015 1,200 Business Dvpmnt

Revamp Logo Design 20/11/2014 6/6/2015 800 Business Dvpmnt

Establish Relationship

With Banks For Co

Branding 22/11/2014 17/1/2015 1,200 Business Dvpmnt

Upgrade Existing

Warehouse 2/12/2014 20/3/2015 12,000 Operation

Update List of New Local

Jeweler Partners 5/1/2015 1/9/2015 0 IT

![[XLS] · Web viewSANGHVI 38, PRARTHNA VIHAR, OPP.,MANEKBAUG, P.O.AHMEDABAD,, 380015 FOLIOB000193 BHALANI 167 PARASKUNJ SOC NO 3,,ISRO ROAD,AHMEDABAD,, FOLIOM000002 PUSHKAR BAGGA H.NO](https://img.pdfslide.us/doc/110x75/5abb9d917f8b9ad1768ce91e/xls-viewsanghvi-38-prarthna-vihar-oppmanekbaug-poahmedabad-380015-foliob000193.jpg)