Embed Size (px)

Citation preview

SwissPLG Winter Conference 2013

Flims, 28 January 2013

Beyond the Spin:

Paths to Value Creation as a Spinoff

Eric de La Fortelle, CEO

• Sizeable capital requirement Avg apitalized cost of discovering/developing an asset from idea

to main value inflexion point is between $250 and $700 Mio;

avg time is 9.5 years*

Invest in an asset that has been partially de-risked in

Academia or can be ‘extracted’ from a for-profit organization

Introduction: Context

* Adapted from Paul. S.M. et al, Nature Reviews Drug Discovery 9, 203-214 (March 2010)

• Sizeable capital requirement Avg apitalized cost of discovering/developing an asset from idea

to main value inflexion point is between $250 and $700 Mio;

avg time is 9.5 years*

Invest in an asset that has been partially de-risked in

Academia or can be ‘extracted’ from a for-profit organization

• VCs under huge pressure makes funding difficult LPs (VC’s own investors) and reconsidering the asset class as a

whole**, and life sciences in particular (few IPOs, long timelines)***

Venture capital investment is very sensitive to risk and timelines

Introduction: Context

* Adapted from Paul. S.M. et al, Nature Reviews Drug Discovery 9, 203-214 (March 2010)

** http://www.kauffman.org/uploadedfiles/vc-enemy-is-us-report.pdf

*** http://www.pwc.com/us/en/press-releases/2012/12q2-life-sciences-moneytree-release.jhtml

• Sizeable capital requirement Avg apitalized cost of discovering/developing an asset from idea

to main value inflexion point is between $250 and $700 Mio;

avg time is 9.5 years*

Invest in an asset that has been partially de-risked in

Academia or can be ‘extracted’ from a for-profit organization

• VCs under huge pressure makes funding difficult LPs (VC’s own investors) and reconsidering the asset class as a

whole**, and life sciences in particular (few IPOs, long timelines)***

Venture capital investment is very sensitive to risk and timelines

• Driver for investment: Pharma’s ‘pull’ Biotech exits are driven by Pharma’s needs for differentiated

drug candidates with a strong hint of efficacy in patients

An ‘investible’ Biotech needs to get there as fast as possible

Introduction: Context

* Adapted from Paul. S.M. et al, Nature Reviews Drug Discovery 9, 203-214 (March 2010)

** http://www.kauffman.org/uploadedfiles/vc-enemy-is-us-report.pdf

*** http://www.pwc.com/us/en/press-releases/2012/12q2-life-sciences-moneytree-release.jhtml

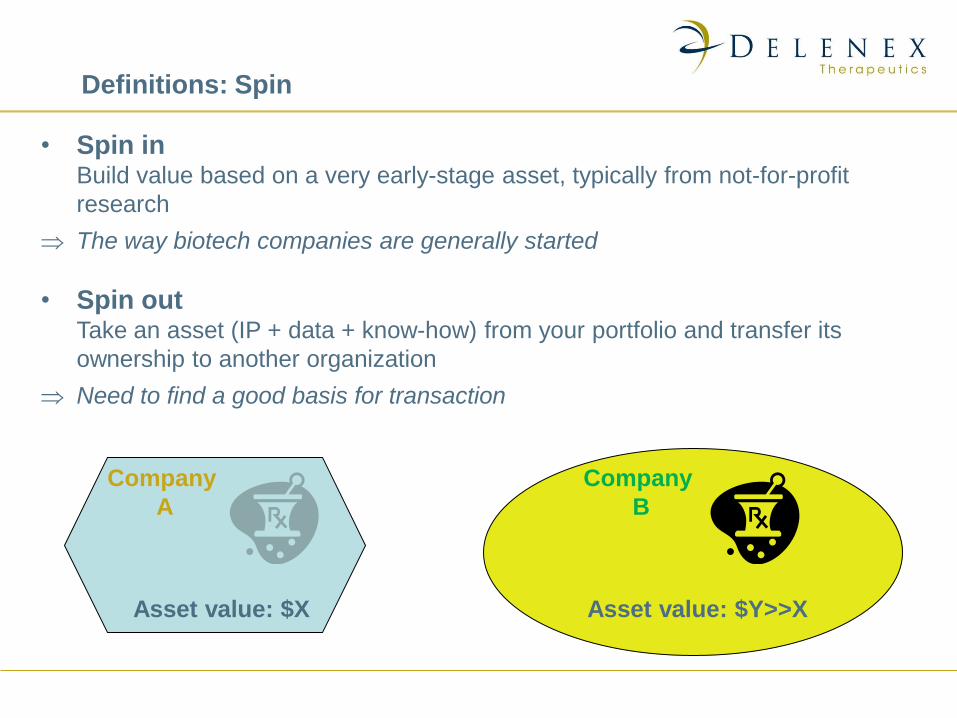

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

Definitions: Spin

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

• Spin out Take an asset (IP + data + know-how) from your portfolio and transfer its

ownership to another organization

Need to find a good basis for transaction

Definitions: Spin

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

• Spin out Take an asset (IP + data + know-how) from your portfolio and transfer its

ownership to another organization

Need to find a good basis for transaction

Definitions: Spin

Company

A

Asset value: $X

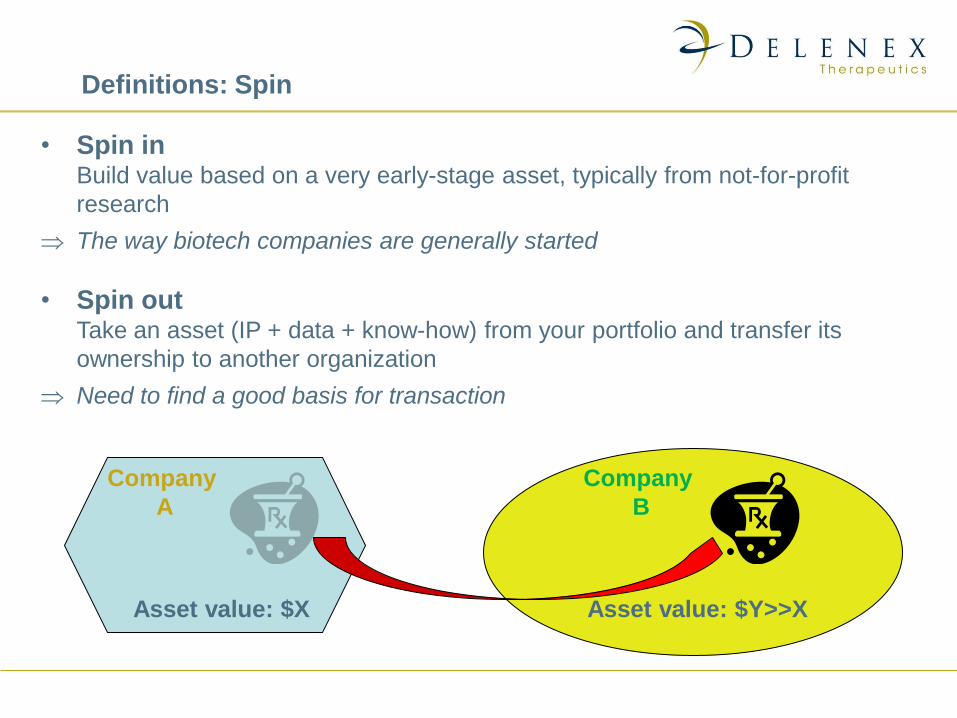

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

• Spin out Take an asset (IP + data + know-how) from your portfolio and transfer its

ownership to another organization

Need to find a good basis for transaction

Definitions: Spin

Company

A

Asset value: $X

Company

B

Asset value: $Y>>X

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

• Spin out Take an asset (IP + data + know-how) from your portfolio and transfer its

ownership to another organization

Need to find a good basis for transaction

Definitions: Spin

Company

A

Asset value: $X

Company

B

Asset value: $Y>>X

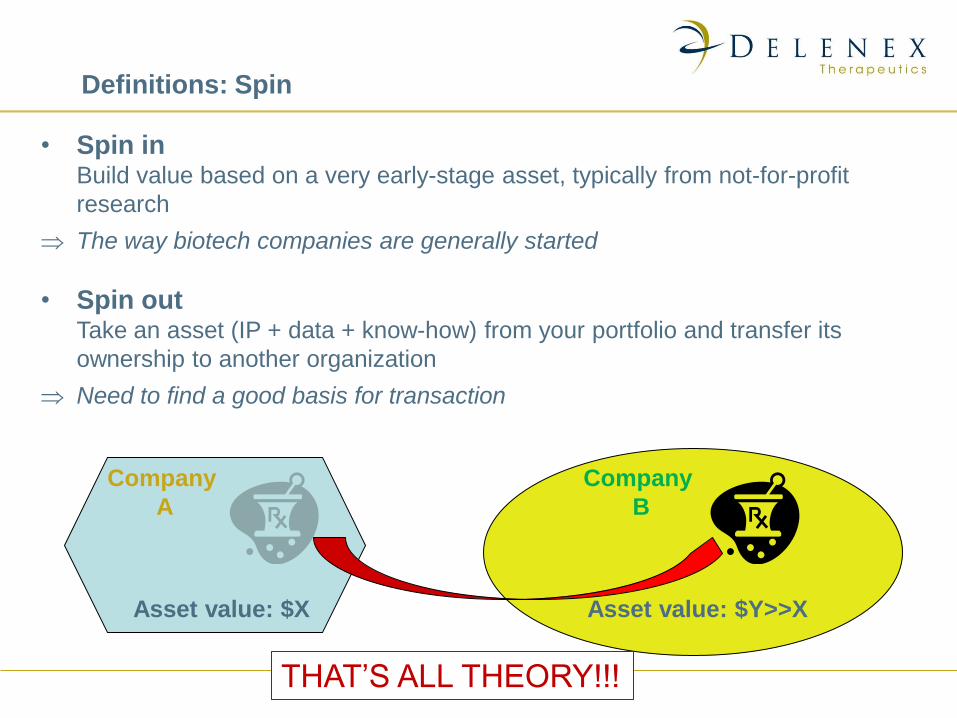

• Spin in Build value based on a very early-stage asset, typically from not-for-profit

research

The way biotech companies are generally started

• Spin out Take an asset (IP + data + know-how) from your portfolio and transfer its

ownership to another organization

Need to find a good basis for transaction

Definitions: Spin

Company

A

Asset value: $X

Company

B

Asset value: $Y>>X

THAT’S ALL THEORY!!!

• It happens by exception rather than by rule In a large organization, de-prioritized pre-PoC projects are

considered ‘dead’. Transacting them is generally not worth the effort

(limited partnering resources are better used hunting for assets to license in)

There is no systematic process of pre-PoC asset divestment

Spinning Out in Practice

• It happens by exception rather than by rule In a large organization, de-prioritized pre-PoC projects are

considered ‘dead’. Transacting them is generally not worth the effort

(limited partnering resources are better used hunting for assets to license in)

There is no systematic process of pre-PoC asset divestment

• Exceptions happen, under some typical scenarios 1. Inside track. The ‘buyer’ knows at least as much about the asset as the ‘seller’

(example: Actelion)

2. Strategic motive. The seller assigns little or no value to the asset and seizes the

opportunity to divest it for upfront cash, or avoidance of payment (example:

ESBATech/Alcon)

Spinoffs usually have a mix of both elements

Spinning Out in Practice

Spinoff example

ESBATech/Alcon => Delenex

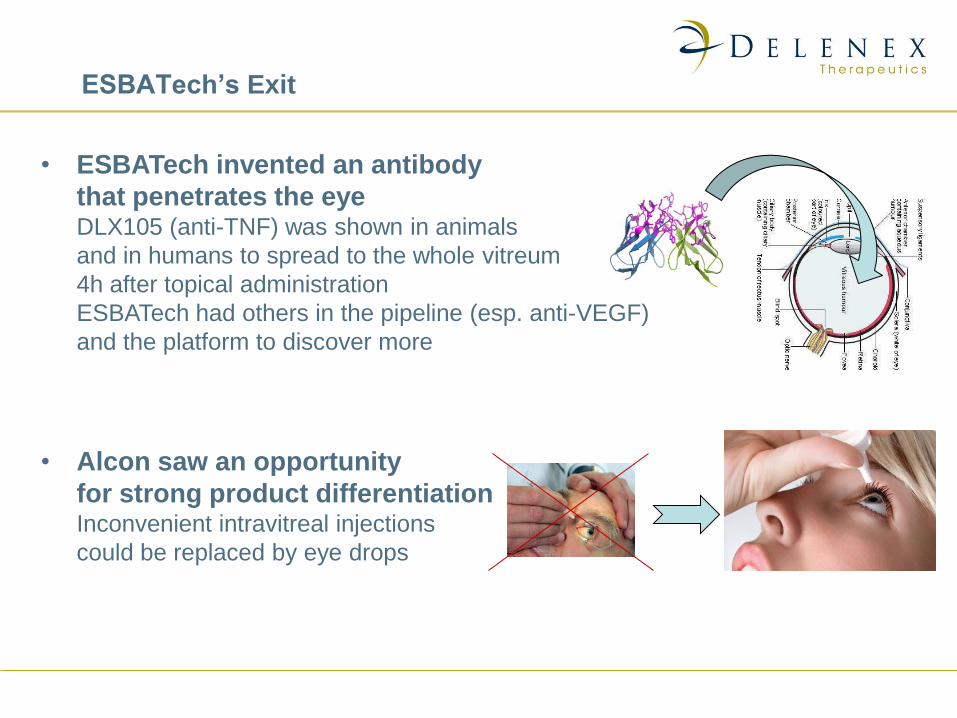

• ESBATech invented an antibody

that penetrates the eye DLX105 (anti-TNF) was shown in animals

and in humans to spread to the whole vitreum

4h after topical administration

ESBATech had others in the pipeline (esp. anti-VEGF)

and the platform to discover more

• Alcon saw an opportunity

for strong product differentiation Inconvenient intravitreal injections

could be replaced by eye drops

ESBATech’s Exit

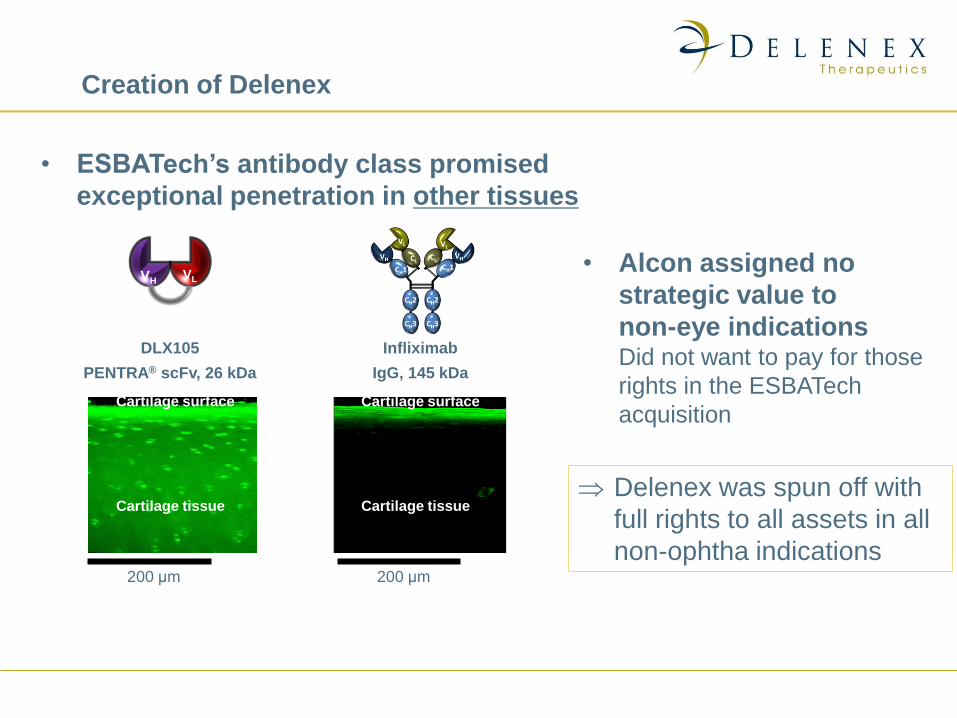

• ESBATech’s antibody class promised

exceptional penetration in other tissues

Creation of Delenex

DLX105

PENTRA® scFv, 26 kDa

Infliximab

IgG, 145 kDa

200 μm

VL VH

Cartilage surface

Cartilage tissue

Cartilage surface

Cartilage tissue

200 μm

• Alcon assigned no

strategic value to

non-eye indications Did not want to pay for those

rights in the ESBATech

acquisition

Delenex was spun off with

full rights to all assets in all

non-ophtha indications

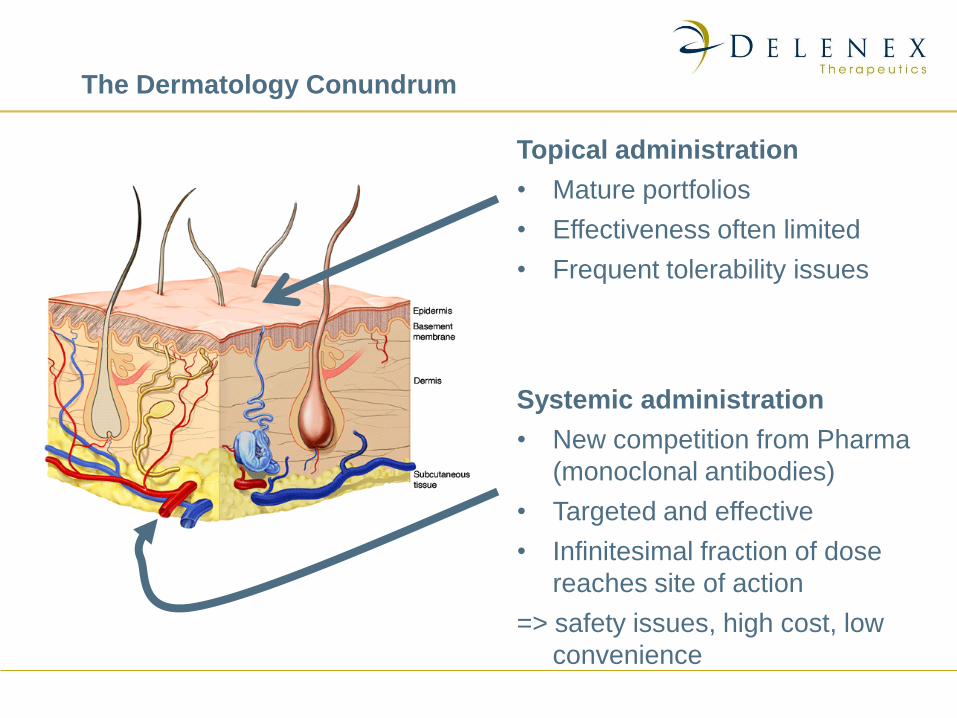

The Dermatology Conundrum

Topical administration

• Mature portfolios

• Effectiveness often limited

• Frequent tolerability issues

Systemic administration

• New competition from Pharma

(monoclonal antibodies)

• Targeted and effective

• Infinitesimal fraction of dose

reaches site of action

=> safety issues, high cost, low

convenience

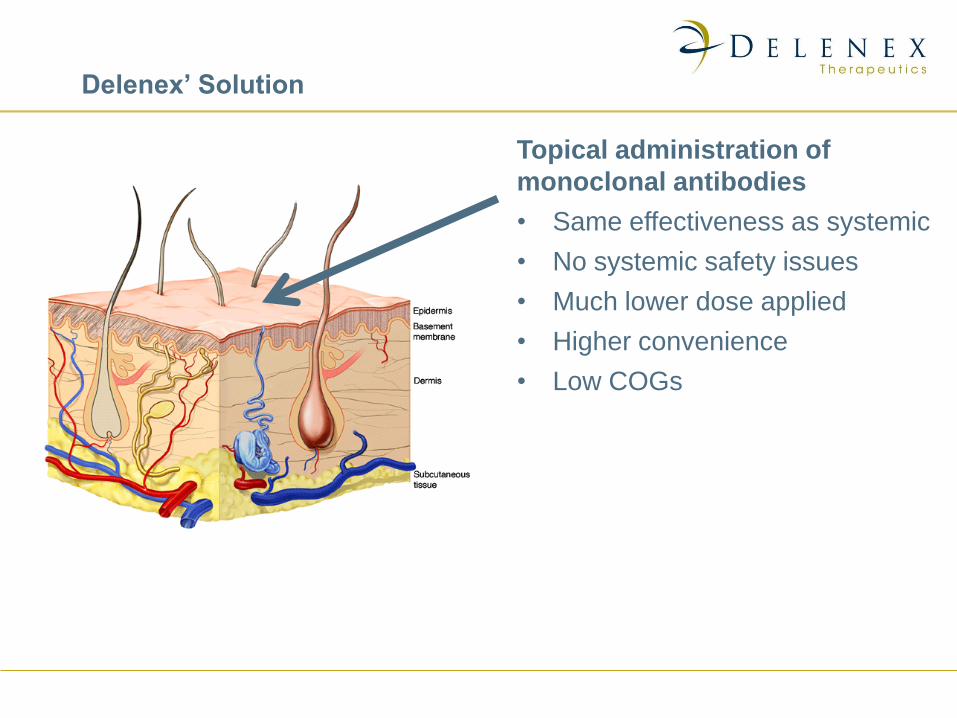

Delenex’ Solution

Topical administration of

monoclonal antibodies

• Same effectiveness as systemic

• No systemic safety issues

• Much lower dose applied

• Higher convenience

• Low COGs

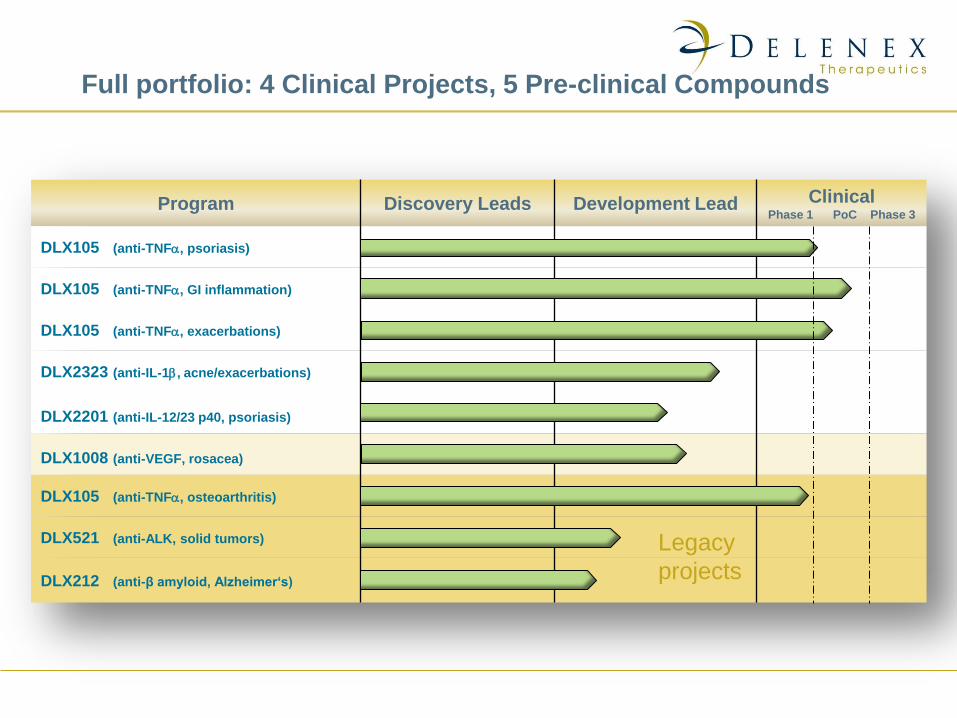

Full portfolio: 4 Clinical Projects, 5 Pre-clinical Compounds

Program Discovery Leads Development Lead Clinical Phase 1 PoC Phase 3

DLX105 (anti-TNFa, psoriasis)

DLX105 (anti-TNFa, GI inflammation)

DLX105 (anti-TNFa, exacerbations)

DLX2323 (anti-IL-1b, acne/exacerbations)

DLX2201 (anti-IL-12/23 p40, psoriasis)

DLX1008 (anti-VEGF, rosacea)

DLX105 (anti-TNFa, osteoarthritis)

DLX521 (anti-ALK, solid tumors)

DLX212 (anti-β amyloid, Alzheimer‘s)

Legacy

projects

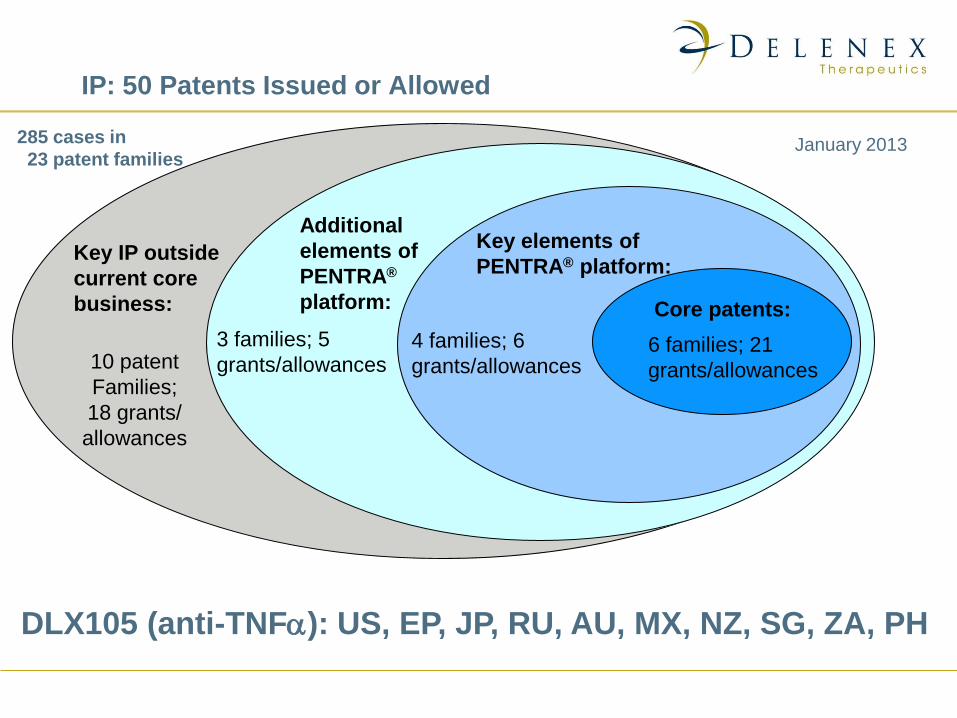

DLX105 (anti-TNFa): US, EP, JP, RU, AU, MX, NZ, SG, ZA, PH

285 cases in

23 patent families

Key elements of

PENTRA® platform:

Additional

elements of

PENTRA®

platform:

Key IP outside

current core

business:

6 families; 21

grants/allowances

4 families; 6

grants/allowances 10 patent

Families;

18 grants/

allowances

Core patents:

3 families; 5

grants/allowances

IP: 50 Patents Issued or Allowed

January 2013

Management and Key Investors

Jakob Schlapbach, lic. rer. pol., MBA

• 18 years experience as CFO of public and

private companies (Ascom, Cytos

Biotechnology)

• Previous position, CFO of Cytos

Biotechnology

Eric de La Fortelle, PhD, MBA • 10 years research in protein structure

determination (Paris XI, BMC Sweden,

MRC UK)

• 12 years leading pharma/biotech deal

teams (SGX Pharmaceuticals, Roche)

• Previous position: global head, external

research and technologies, Roche

Titus Kretzschmar, PhD • 20 years experience in novel antibody

discovery, protein evolution and

leadership of scientific organizations

(Ciba-Geigy, Novo Nordisk, MorphoSys,

Lonza/ex-amaxa)

• Previous position, CSO and head of the

Lonza Initiative for Future Technologies

HBM Partners (Chandra Leo)

Novo A/S (Thomas Dyrberg)

SV Life Sciences (Hamish Cameron)

Key investors

BioMedInvest (Gerhard Ries)

VI Partners (Arnd Kaltofen)

CEO CFO

CMO CSO

Thomas Jung, MD • Board-certified dermatologist

• 10 years immunology research

experience (DNAX, U. Göttingen,

Novartis Research Institute, Vienna)

• 9 years development experience

(Novartis, Basel)

• Previous position: head translational

medicine EU, Novartis

• The Delenex spinoff extends ESBATech’s value proposition It worked in the eye …

But it took quite some faith to believe it could work in skin, gut or exacerbations

Seeing value beyond reasonable expectations is essential

Conclusion

• The Delenex spinoff extends ESBATech’s value proposition It worked in the eye …

But it took quite some faith to believe it could work in skin, gut or exacerbations

Seeing value beyond reasonable expectations is essential

• Clinical PoC studies are key Potential buyers will only recognize value when shown efficacy data in humans

PoC studies need not be large, if well designed for statistical significance

We had the chance to build a clinical infrastructure and culture early on

Conclusion

• The Delenex spinoff extends ESBATech’s value proposition It worked in the eye …

But it took quite some faith to believe it could work in skin, gut or exacerbations

Seeing value beyond reasonable expectations is essential

• Clinical PoC studies are key Potential buyers will only recognize value when shown efficacy data in humans

PoC studies need not be large, if well designed for statistical significance

We had the chance to build a clinical infrastructure and culture early on

• Opportunity and risk The Delenex circumstances are unique, and may not apply to other situations

A rapidly-reorganizing Pharma/Biotech sector creates many interesting

opportunities

Good timing and scientific/medical savvy are required

Conclusion

Delenex Therapeutics AG

Wagistrasse 27

CH-8952 Schlieren-Zürich

Switzerland

Phone +41(0)44-7305 180

www.delenex.com

Changing the Game in Immuno-Inflammation