Embed Size (px)

Citation preview

CBRE CAPITAL MARKETS

CBRE 2017 MULTIFAMILY CONFERENCE B E Y O N D T H E C Y C L E

M o d e r a t o r : C o l l e e n P e n t l a n d L a l l y, C B R E John German, Invesco

Stafford Lancaster, Delancey Konstant in Luet tger, CBRE Frankfur t

Tim MacMahon, CBRE Dubl in

WORLD TOUR OF EMERGING MULTIFAMILY MARKETS

3

THANK YOU TO OUR SPONSOR!

DIFFERENTIATED MARKETS AND OPPORTUNITIES UK residential investment market Immature but developing quickly Demand from domestic and institutional

investors Transparent legal framework with low

levels of regulation

Spanish residential investment market Market in recovery from GFC shocks Culture of ownership rather than renting Heterogeneous with a lack of transparency

German residential investment market Established and steady growth Recognised and dependable Transparent and tradable Stable

Ireland residential investment market Immature but developing quickly Demand from non-domestic

institutional investors Market in recovery from GFC shocks Transparent legal framework

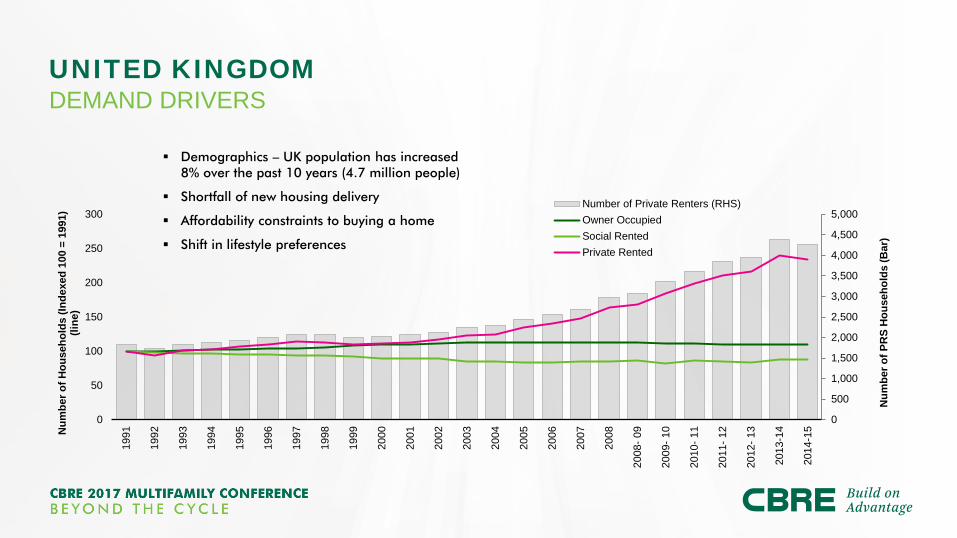

UNITED KINGDOM DEMAND DRIVERS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0

50

100

150

200

250

300

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2008

- 09

2009

- 10

2010

- 11

2011

- 12

2012

- 13

2013

-14

2014

-15

Num

ber o

f PR

S H

ouse

hold

s (B

ar)

Num

ber o

f Hou

seho

lds

(Inde

xed

100

= 19

91)

(line

)

Number of Private Renters (RHS)Owner OccupiedSocial RentedPrivate Rented

Demographics – UK population has increased 8% over the past 10 years (4.7 million people)

Shortfall of new housing delivery

Affordability constraints to buying a home

Shift in lifestyle preferences

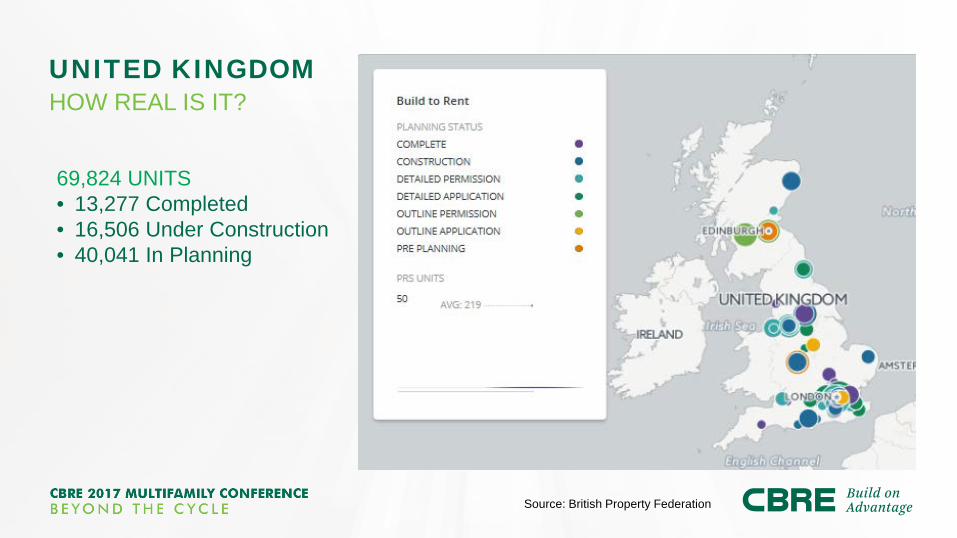

Source: British Property Federation

69,824 UNITS • 13,277 Completed • 16,506 Under Construction • 40,041 In Planning

UNITED KINGDOM HOW REAL IS IT?

DUBLIN DEMAND DRIVERS

WHY DUBLIN

?

Sentiment Swing from

Buyer market to Rental Market

Multi-National Employer base

Transient Population

Growth in Population

6.7% unemployment

Lack of private, affordable and social housing

Largest proportion of

25-40 year olds in Europe

Rising Rents & Low Capital

Values

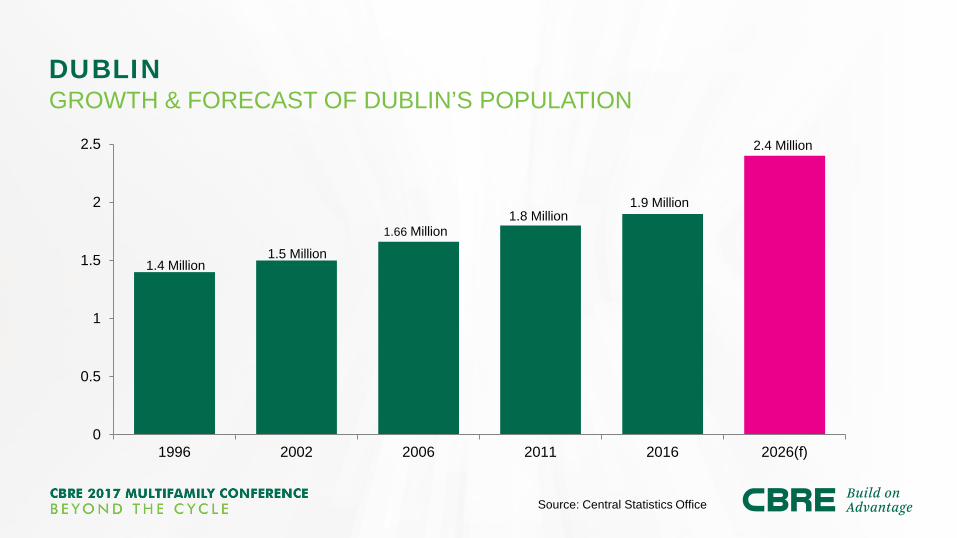

DUBLIN GROWTH & FORECAST OF DUBLIN’S POPULATION

0

0.5

1

1.5

2

2.5

1996 2002 2006 2011 2016 2026(f)

1.4 Million 1.5 Million

1.66 Million 1.8 Million

1.9 Million

2.4 Million

Source: Central Statistics Office

EAST VILLAGE, LONDON THE UK’S FIRST PRS NEIGHBOURHOOD

EAST VILLAGE, LONDON THE UK’S FIRST PRS NEIGHBOURHOOD • 67 acre Freehold District in Zone 2/3

• Move-ins from 2013

• More than 6,000 residents now living in 2,818 homes:

– 1,439 homes for market rent – managed by Get Living

– 1,379 ‘affordable’ homes

• Further 1,850 consented homes

• 51% Estate Management Company

• 1,800 pupil ‘Outstanding’ academy school

• Health & Wellbeing Centre

• Unrivalled transport connections

• 1.9m sqft Westfield Stratford City shopping centre

• On doorstep of Queen Elizabeth Olympic Park - 500 acre parkland and sporting venues

GLOBAL RESPONSE INVESCO EU RESIDENTIAL INVESTORS

14

7

3

1 1

1 1

Germany

UK

Denmark

Canada

Netherlands

Australia

US

EUROPEAN RESIDENTIAL EXPERIENCE

Currently committed: - US$540 million - 15 investments (1,766 units) - Forward funding developments - Investments in Germany, UK and Spain

U.S. $540 million; 15 investments

ASIAN RESIDENTIAL EXPERIENCE

Currently manage: - US$472 million - 2 investments (2,607 units) Sold: - US$851 million - 10 Investments (1,380 units)

U.S. $1,323 million; 12 investments

U.S. RESIDENTIAL EXPERIENCE

Currently manage: - US$9.0 billion - 107 investments (36,278 units) Sold: - US$7.6 billion - 262 investments (75,447 units)

U.S. $16.6 billion; 369 investments

SOURCE: INVESCO REAL ESTATE AS OF 31 DECEMBER 2016. FOR ILLUSTRATIVE PURPOSE ONLY. PHOTOGRAPHS SHOWN ABOVE REPRESENT ACQUIRED ASSETS. IMAGES ARE ONLY RENDERINGS. IRE HAS PERMISSION TO USE PHOTOGRAPHS.

GLOBAL EXPERTISE, LOCAL IMPLEMENTATION INVESCO GLOBAL RESIDENTIAL

GERMANY • 41M residential units (17.5M owner-occupied; 23.5

rental apartments) • Vacancy rate decreased from 3.6% (2010) to 3.0

(2015) • Top 7 market vacancy rates under 1.5%; Munich

just 0.2% • Berlin most liquid residential market with an overall

residential volume of approx. €4bn – Berlin current annual population growth:

+50,000 – Vacancy rate 2015: 1.2% – Average market rent 2016: EUR 9.00 (+6%

compared to 2015 and +55% compared to 2009)

– Average condominium price 2016: €3,300 (+10% compared to 2015 and +105% compared to 2009)

GERMANY INVESTMENT ACTIVITY

0

50

100

150

200

250

300

350

400

02468

1012141618202224

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q12016

Q12017

Cou

nt re

side

ntia

l uni

ts (x

1,00

0)

Tran

sact

ion

volu

me

(€ b

illion

)

Transaction volume (€) Average transaction volume 1999-2016

Number of residential units Average number of residential units 1999-2016

Portfolio transaction volume and number of residential units

RESIDENTIAL ACROSS THE RISK SPECTRUM

Germany

UK

Spain

5

6

7

8

9

10

11

12

13

14

15

Total return expectations (%)

Core/stabilized (5-8%)

Ret

urn

Core+ (8-12%)

Value added/enhanced (12-15%)

Risk

IRR FROM RESIDENTIAL INVESTMENTS

SOURCE: IPD MULTINATIONAL INDEX AS OF 31 DECEMBER 2015.

10.1

0%

11.1

0%

13.2

0%

8.30

% 9.80

%

9.00

%

9.30

% 11

.60%

11.4

0%

8.40

%

8.60

%

11.0

0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

USA Japan Switzerland Netherlands France Germany Sweden UK Canada Finland

1 year 3 year 5 year

Residential real estate total returns over 1, 3 and 5 years to end 2015

FIRST MOVERS U.S PLAYERS IN GLOBAL MARKETS

IRELAND • AIG • Ares • Hines • BlackRock Capital • CapREIT • CBRE Global Investors • Heitman • Kennedy Wilson • Lone Star • Marathon Asset

Management

GERMANY • Angelo Gordon • GI Partners • Greystar • Heitman • Hines • Invesco • Lincoln Equities • PGIM • Tristan

UNITED KINGDOM • AIG • Akelius • Apollo • Atlas Residential • Blackstone • Brookfield • Deutsche Asset

Management

• Goldman Sachs • Greystar • Invesco • LaSalle Investment

Management • Lone Star • Related • TH Real Estate

THANK YOU!