Embed Size (px)

Citation preview

Annual Report 2011

Beyond Banking

Licensed as an Islamic Retail Bank by the Central Bank of Bahrain

Al Baraka Islamic Bank B.S.C (c)

CONTENTSOur Vision and Mission02

03 Branches

Bank’s Profile

Board of Directors

List of Committees for Year 2011 and Sharia’a Supervisary Board

Board of Directors’ Report

Executive Management

Chief Executive Officers’ Report

Corporate Governence

Corporate Social Responsibility

Sharia’a Supervisory Board Report

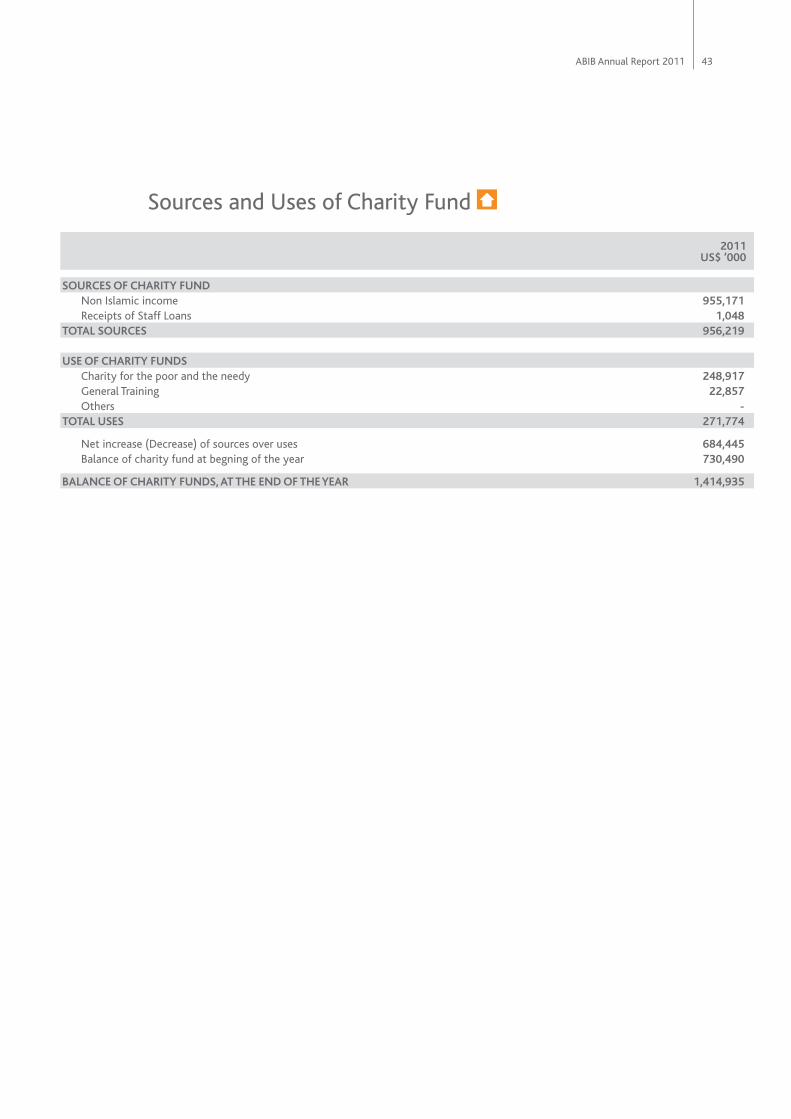

Sources and Users of Charity Fund

05

06

09

27

11

41

14

42

19

43

Independent Auditors’ Report

Financial Highlights

Consolidated Financial Statement

Basel II, Pillar III Disclosures

47

91

44

45

His Royal Highness PrinceKhalifa bin Salman Al Khalifa

The Prime Minister of theKingdom of Bahrain

His Majesty KingHamad bin Isa Al Khalifa

King of the Kingdom of Bahrain

His Royal Highness PrinceSalman bin Hamad Al Khalifa

The Crown Princeof the Kingdom of Bahrain andDeputy Supreme Commander

VISION

MISSION

BEYOND BANKING

‘We believe society needs a fair and equitable financial system: one which rewords

effort and contributes to the development of the community.’

‘To meet the financial needs of communities across the world by conducting business

ethically in accordance with our beliefs, practicing the highest professional standards and

sharing the natural benefits with the customers, staff and shareholders who participate

in our business success.'

We believe that banking has, or ought to have, a crucial role to play in society, one in which as bankers we have an incredible responsibility of stewardship for the resources placed in our hands. To meet this responsibility and use the resources wisely, we rely on Sharia'a principles to guide us as we participate in our customers' successes, sharing in the social development of families, businesses and society at large.

By 'partnership', therefore, be mean that our success and that of each of our customers are as intertwined as our jointly held beliefs. Taking part in the joint effort is therefore our reward. We see money as a means to Capitalise on opportunities and create a better society for all of us. Money becomes the conduit by which we enter into new opportunities together and take part in common effort for mutual reward; as steward of the resources entrusted to us, our efforts contribute to building the community, at home and in the wider world.

We call this concept: ‘Beyond Banking’

Al Baraka Islamic Bank B.S.C (c) 2

Head Office Subsidiary

Branches

CEO & Board Member

Mr. Mohammed Al Mutaweh

Al Baraka Tower

Diplomatic Area

P.O. Box 1882

Manama, Kingdom of Bahrain

Main Branch (Diplomatic Area)

Tel: +97317 535 300

Fax: +97317 533 993

Isa Town Branch

Tel: +973 17 788 388

Fax: +973 17 687 838

Muharraq Branch

Tel: +973 17 461 999

Fax: +973 17 324 888

Riffa Branch

Tel: +973 17 768 600

Fax: +973 17 490 003

Arad Branch

Tel: +973 17 358 885

Fax: +973 17 676 361

Ramil Mall Branch, A’ali

Tel: +973 17 646 677

Fax: +973 17 646 676

Email: [email protected]

Web: www.barakaonline.com

Al Baraka Bank Pakistan (Limited)

Shafqaat Ahmed

Chief executive Officer & Board Member

Plot No. 162, Bangalore Town

Block 7 & 8, Shahrah-e-Faisal

Karachi, Pakistan

Tel: +9221 34 315 851 / +9221 34 307 000

Fax: +9221 34 323 761 / +9221 34 546 465

Email: [email protected]

Web: www.albaraka.com.pk

ABIB Annual Report 2011 3

Throughout its history of over 25 years, since it’s establishment in 1984, the bank has played a prominent role in building the infrastructure of the Islamic finance industry.

Al Baraka Islamic Bank B.S.C (c) 4

Al Baraka Islamic Bank is one of Bahrain’s leading financial institutions in the Islamic banking sector. Throughout its history of over 25 years, since it’s establishment in 1984, the bank has played a prominent role in building the infrastructure of the Islamic finance industry, as represented by its taking part in the establishment of institutions responsible for providing the Islamic finance industry with professional and Sharia standards, provision of information, management of capital markets and management of liquidity. The bank also played a significant role in promoting the Islamic finance industry and publicizing its merits. The bank enjoys a good reputation and high standing with the community in Bahrain in particular, and in the Gulf, Arab and Islamic worlds in general. Al Baraka Islamic Bank offers innovative financial products, particularly in the areas of Islamic investment, international trade, management of short-term liquidity to all individual investors and consumer financing that the bank has lunched under (Taqseet product).... etc., which are all based on Islamic financing modes that conform to Sharia’a standards set by the Sharia’a Board of the Accounting and Auditing Organization for Islamic Financial Institutions. Such financing modes include Murabaha, Diminishing Musharaka, Mudaraba, and Ijarah Muntahia Bittamleek.

The Bank had achieved excellent results in its banking operations, thanks to its vast wealth of knowledge in the area of the Fiqh (jurisprudence) of Islamic finance, the diverse experience of its senior management team in different fields of Islamic banking and the strength and depth that the parent company, Al Baraka Banking Group, with its strong financial position and standing provides to the bank. Since its inception, Al Baraka Islamic Bank has managed more than US$ 7 billion in funds on behalf of many large financial institutions and high net worth clients who sought rewarding long-term financial returns by deploying Sharia’a-compliant financial instruments.

During the year 2010, AِIB completed the merger of its branches in Pakistan, which their operations dates back to 1991, with the branches of Emirates Global Islamic Bank (Pakistan), to establish Al Baraka Bank Pakistan Limited as a subsidiary by a majority of shares of AIB. The Head office is located in Karachi. ABPL have assets in excess of Rs. 50billion,

a workforce of more than 1400 professionals and a network of 89 branches in 36 cities and towns across the country. ABPL has commenced operations on 29th of October 2010 and consequently, all branches of AIBP and Emirates Global Islamic Bank is re-branded as ABPL.

As for its future strategic plans, the bank intends to maintain the pace of its growth in its business operations with particular focus on commissions and fee – based earnings. The bank also proposes to expand its investment portfolio, continue to develop its infrastructure, particularly with regard to modern information technologies (IT) and related services, improve customer service, provide training and coaching to employees and maintain our special relationship with our customers as their “Partners in Achievement” .

Al Baraka Islamic Bank is a banking institution registered with the Ministry of Industry and Commerce in Bahrain under Commercial Registration No. 14400 and has a Retail Banking license issued by the Central Bank of Bahrain. The bank has an authorized capital of US$ 600 million and issued and paid-up capital of US$122 million. Al Baraka Islamic Bank - Bahrain is one of the banking units of Al Baraka Banking Group, which is a Bahrain Joint Stock Company listed in Bahrain stock exchange and Nasdaq Dubai. Al Baraka Banking Group is a leading international Islamic banking group with Standard and Poor’s rating of investment grade BBB-/Stable/A-3 credit rating.. The Group offers retail, corporate and investment banking and treasury services, strictly in accordance with the principles of the Islamic Sharia’a. The authorized capital of Al Baraka Banking Group is US$1.5 billion, while total equity amounts to around US$1.5 billion. The Group has a wide geographical presence in the form of subsidiary banking units and representative offices in twelve countries, which in turn provide their Sharia’a-compliant banking products and services through around 400 branches. These banking Units are Jordan Islamic Bank, Jordan; Al Baraka Islamic Bank, Bahrain; Al Baraka Pakistan Limited , Pakistan; Al Baraka Bank Algeria; Al Baraka Bank Sudan; Al Baraka Bank Ltd, South Africa; Al Baraka Bank Lebanon; Al Baraka Bank Tunis; Al Baraka Bank Egypt; Al Baraka Turk Participation Bank, Turkey; Al Baraka Bank Syria and a representative office in Indonesia and a representative office in Libya.

Bank’s Profile

ABIB Annual Report 2011 5

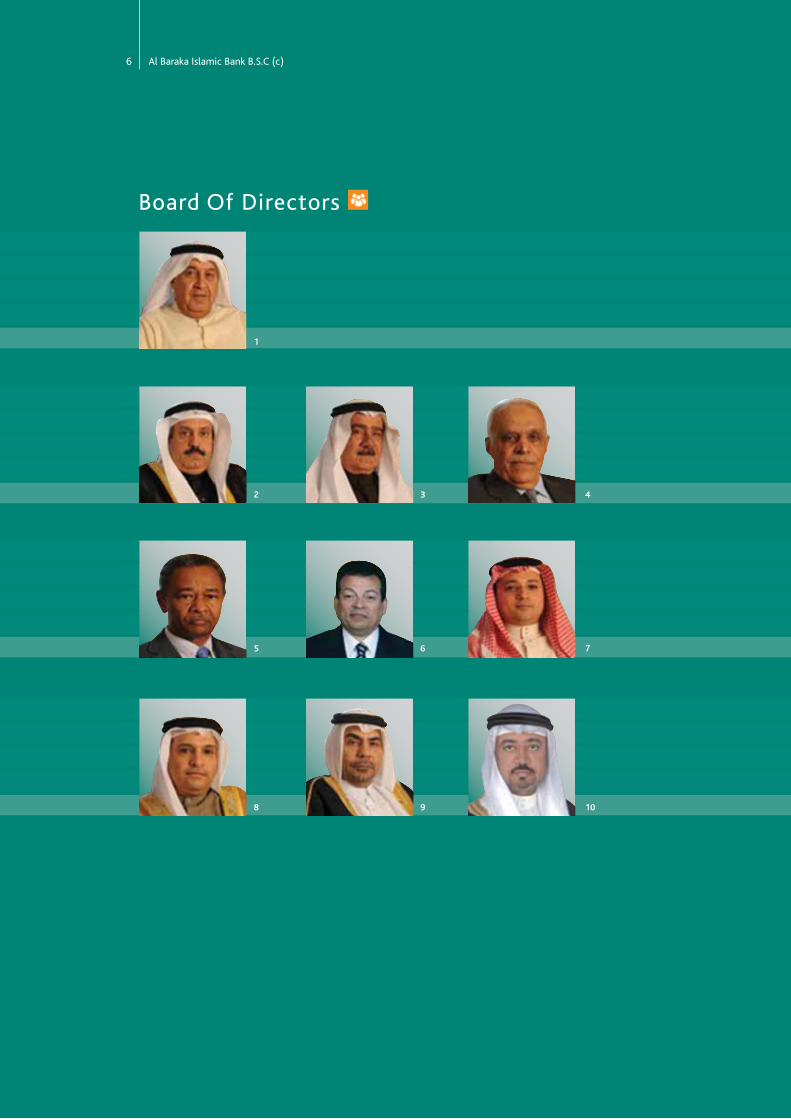

1

2

5

8

3

6

9

4

7

10

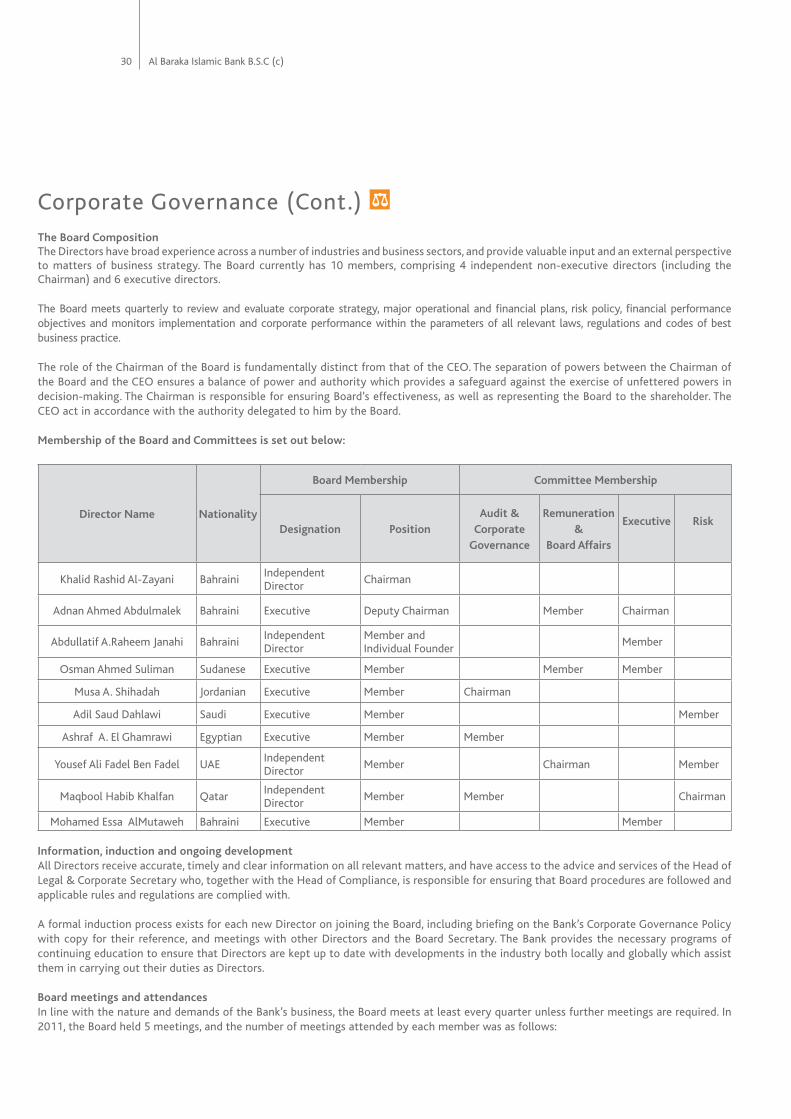

Board Of Directors

Al Baraka Islamic Bank B.S.C (c) 6

1) Mr. Khalid Rashid Al Zayani Chairman Experience: 42 years Mr. Khalid Rashid Al-Zayani is a

prominent businessman at the local, Arab and international levels and holds many leading positions in the areas of banking, investment and trade. He holds a bachelor degree in Business Administration from the University of London, United Kingdom. In addition to his position as chairman of the boards of directors of many companies affiliated to Al Zayani Group, such as Zayani Investments and Euro Motors, he is a member of the Board of Directors and Executive Committee member of Investcorp as well as being a member of the boards of a number of local and international associations and chambers of commerce.

2) Mr. Adnan Ahmed Yousif Vice Chairman Experience: 39 years Mr. Adnan Ahmed Yousif is a leading Arab

banker who held many senior positions at local and regional levels and in May 2007 became the first Gulf national to become the Chairman of the Union of Arab Banks. He serves as President & Chief Executive and member of the Board of Directors of Al Baraka Banking Group since August 2004 until the present time. Furthermore, Mr. Adnan Yousif is the Chairman of Banque Al Baraka D’Algerie, Algeria, Al Baraka Bank Ltd., South Africa, Jordan Islamic Bank, Al Baraka Bank Egypt, Al Baraka Turk Participation Bank, Al Baraka Bank (Pakistan) Limited and Al Baraka Lebanon. He is also a member of the Board of Directors of Al Baraka Bank Sudan and Al Baraka Bank Tunisia. Mr. Adnan Yousif received the Banker of the Year Award in 2004 from by the World Islamic Banking Conference.

3) Mr. Abdul Latif Abdul Rahim Janahi Board Member Experience: over 40 years Mr. Abdul Latif Abdul Rahim Janahi is one

of the early pioneers in Islamic economy, Islamic banking and Islamic insurance. He authored a number of books on these topics and prepared more than 60 studies and work papers presented at

numerous events, conferences, seminars and, universities. He worked hard to promote the idea of Islamic banking, insurance and re-insurance in Bahrain and was behind the establishment of a number of banks, financial institutions and insurance and reinsurance companies in Bahrain and outside Bahrain. He has practical experience of more than 40 years in the areas of banking, insurance and reinsurance. He holds a diploma in insurance and is a recognized expert in conventional insurance, Takaful (Islamic insurance), Islamic banking and Islamic economics. Mr. Janahi is the founder and Chief Executive Officer of the Safwa International, Bahrain (consultancy), and board member of many Islamic banking and investment institutions such as the Islamic Bank of Bangladesh - Dhaka, Khaleej Finance and Investment (being the Chairman of the Board of Directors) and the Islamic Arab Bank and Islamic Insurance and Reinsurance Company.

4) Mr. Moosa Abdul Aziz Shehadah Board Member Experience: 51 years Mr. Moosa Abdul Aziz Shehadah is a

prominent Arab banker who holds a Bachelor degree in Commerce from Beirut Arab University and an MBA degree from the University of San Francisco, United States of America. He is currently the General Manager and Deputy Chairman of the Board of Directors of Jordan Islamic Bank, as well as the Deputy Chairman of the Banks Association in Jordan. He is the chairman and board member of directors of several banks and companies such as Alaqsa Islamic Bank - Palestine, the Islamic Insurance Company, Al Amin investment Company, Arab Steel Pipes Company and Saudi Fransi Bank of Egypt - Cairo. He is also a member of the Board of Trustees and Board of Directors of the Petra University, the Hashemite Kingdom of Jordan, Lebanon Reconstruction Fund and Waqf Investment Funds as well as being the Chairman of the Investment Committee and member of Board of the Shariah Faculty at Jordan University, the Hashemite Kingdom of Jordan.

ABIB Annual Report 2011 7

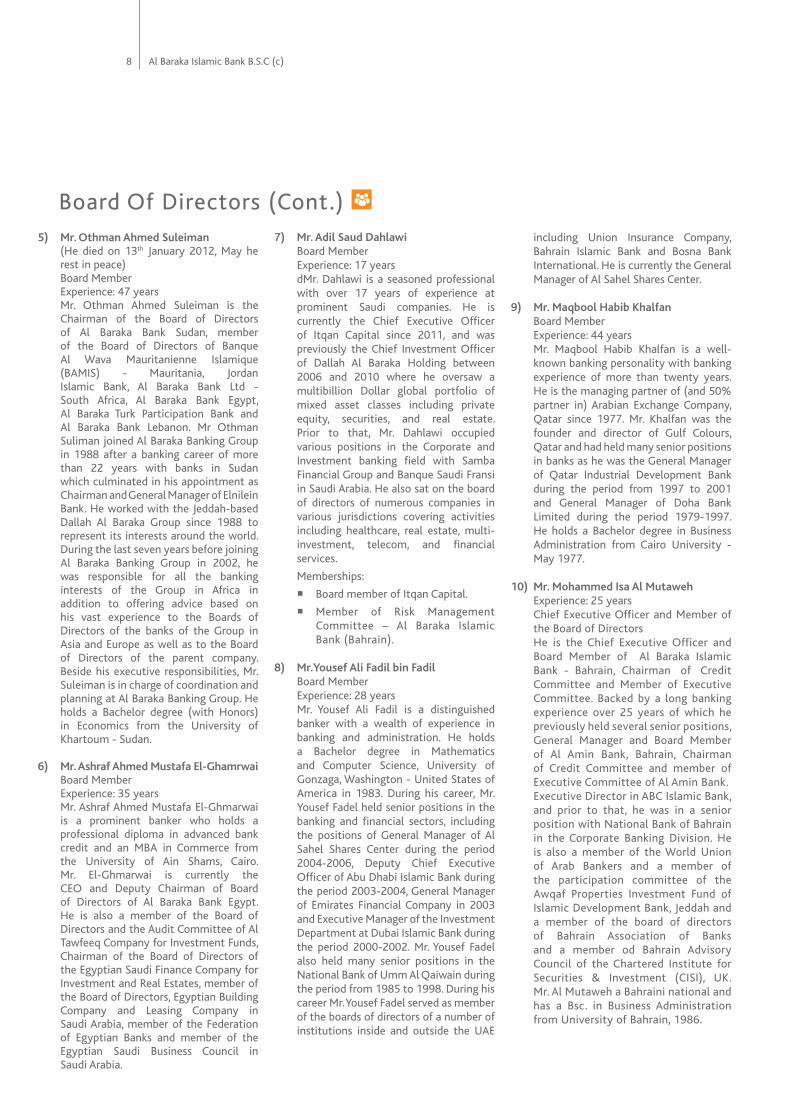

5) Mr. Othman Ahmed Suleiman (He died on 13th January 2012, May he

rest in peace) Board Member Experience: 47 years Mr. Othman Ahmed Suleiman is the

Chairman of the Board of Directors of Al Baraka Bank Sudan, member of the Board of Directors of Banque Al Wava Mauritanienne Islamique (BAMIS) - Mauritania, Jordan Islamic Bank, Al Baraka Bank Ltd - South Africa, Al Baraka Bank Egypt, Al Baraka Turk Participation Bank and Al Baraka Bank Lebanon. Mr Othman Suliman joined Al Baraka Banking Group in 1988 after a banking career of more than 22 years with banks in Sudan which culminated in his appointment as Chairman and General Manager of Elnilein Bank. He worked with the Jeddah-based Dallah Al Baraka Group since 1988 to represent its interests around the world. During the last seven years before joining Al Baraka Banking Group in 2002, he was responsible for all the banking interests of the Group in Africa in addition to offering advice based on his vast experience to the Boards of Directors of the banks of the Group in Asia and Europe as well as to the Board of Directors of the parent company. Beside his executive responsibilities, Mr. Suleiman is in charge of coordination and planning at Al Baraka Banking Group. He holds a Bachelor degree (with Honors) in Economics from the University of Khartoum - Sudan.

6) Mr. Ashraf Ahmed Mustafa El-Ghamrwai Board Member Experience: 35 years Mr. Ashraf Ahmed Mustafa El-Ghmarwai

is a prominent banker who holds a professional diploma in advanced bank credit and an MBA in Commerce from the University of Ain Shams, Cairo. Mr. El-Ghmarwai is currently the CEO and Deputy Chairman of Board of Directors of Al Baraka Bank Egypt. He is also a member of the Board of Directors and the Audit Committee of Al Tawfeeq Company for Investment Funds, Chairman of the Board of Directors of the Egyptian Saudi Finance Company for Investment and Real Estates, member of the Board of Directors, Egyptian Building Company and Leasing Company in Saudi Arabia, member of the Federation of Egyptian Banks and member of the Egyptian Saudi Business Council in Saudi Arabia.

7) Mr. Adil Saud Dahlawi Board Member Experience: 17 years dMr. Dahlawi is a seasoned professional

with over 17 years of experience at prominent Saudi companies. He is currently the Chief Executive Officer of Itqan Capital since 2011, and was previously the Chief Investment Officer of Dallah Al Baraka Holding between 2006 and 2010 where he oversaw a multibillion Dollar global portfolio of mixed asset classes including private equity, securities, and real estate. Prior to that, Mr. Dahlawi occupied various positions in the Corporate and Investment banking field with Samba Financial Group and Banque Saudi Fransi in Saudi Arabia. He also sat on the board of directors of numerous companies in various jurisdictions covering activities including healthcare, real estate, multi-investment, telecom, and financial services.

Memberships:

Board member of Itqan Capital.

Member of Risk Management Committee – Al Baraka Islamic Bank (Bahrain).

8) Mr.Yousef Ali Fadil bin Fadil Board Member Experience: 28 years Mr. Yousef Ali Fadil is a distinguished

banker with a wealth of experience in banking and administration. He holds a Bachelor degree in Mathematics and Computer Science, University of Gonzaga, Washington - United States of America in 1983. During his career, Mr. Yousef Fadel held senior positions in the banking and financial sectors, including the positions of General Manager of Al Sahel Shares Center during the period 2004-2006, Deputy Chief Executive Officer of Abu Dhabi Islamic Bank during the period 2003-2004, General Manager of Emirates Financial Company in 2003 and Executive Manager of the Investment Department at Dubai Islamic Bank during the period 2000-2002. Mr. Yousef Fadel also held many senior positions in the National Bank of Umm Al Qaiwain during the period from 1985 to 1998. During his career Mr. Yousef Fadel served as member of the boards of directors of a number of institutions inside and outside the UAE

including Union Insurance Company, Bahrain Islamic Bank and Bosna Bank International. He is currently the General Manager of Al Sahel Shares Center.

9) Mr. Maqbool Habib Khalfan Board Member Experience: 44 years Mr. Maqbool Habib Khalfan is a well-

known banking personality with banking experience of more than twenty years. He is the managing partner of (and 50% partner in) Arabian Exchange Company, Qatar since 1977. Mr. Khalfan was the founder and director of Gulf Colours, Qatar and had held many senior positions in banks as he was the General Manager of Qatar Industrial Development Bank during the period from 1997 to 2001 and General Manager of Doha Bank Limited during the period 1979-1997. He holds a Bachelor degree in Business Administration from Cairo University - May 1977.

10) Mr. Mohammed Isa Al Mutaweh Experience: 25 years Chief Executive Officer and Member of

the Board of Directors He is the Chief Executive Officer and

Board Member of Al Baraka Islamic Bank - Bahrain, Chairman of Credit Committee and Member of Executive Committee. Backed by a long banking experience over 25 years of which he previously held several senior positions, General Manager and Board Member of Al Amin Bank, Bahrain, Chairman of Credit Committee and member of Executive Committee of Al Amin Bank. Executive Director in ABC Islamic Bank, and prior to that, he was in a senior position with National Bank of Bahrain in the Corporate Banking Division. He is also a member of the World Union of Arab Bankers and a member of the participation committee of the Awqaf Properties Investment Fund of Islamic Development Bank, Jeddah and a member of the board of directors of Bahrain Association of Banks and a member od Bahrain Advisory Council of the Chartered Institute for Securities & Investment (CISI), UK. Mr. Al Mutaweh a Bahraini national and has a Bsc. in Business Administration from University of Bahrain, 1986.

Board Of Directors (Cont.)

Al Baraka Islamic Bank B.S.C (c) 8

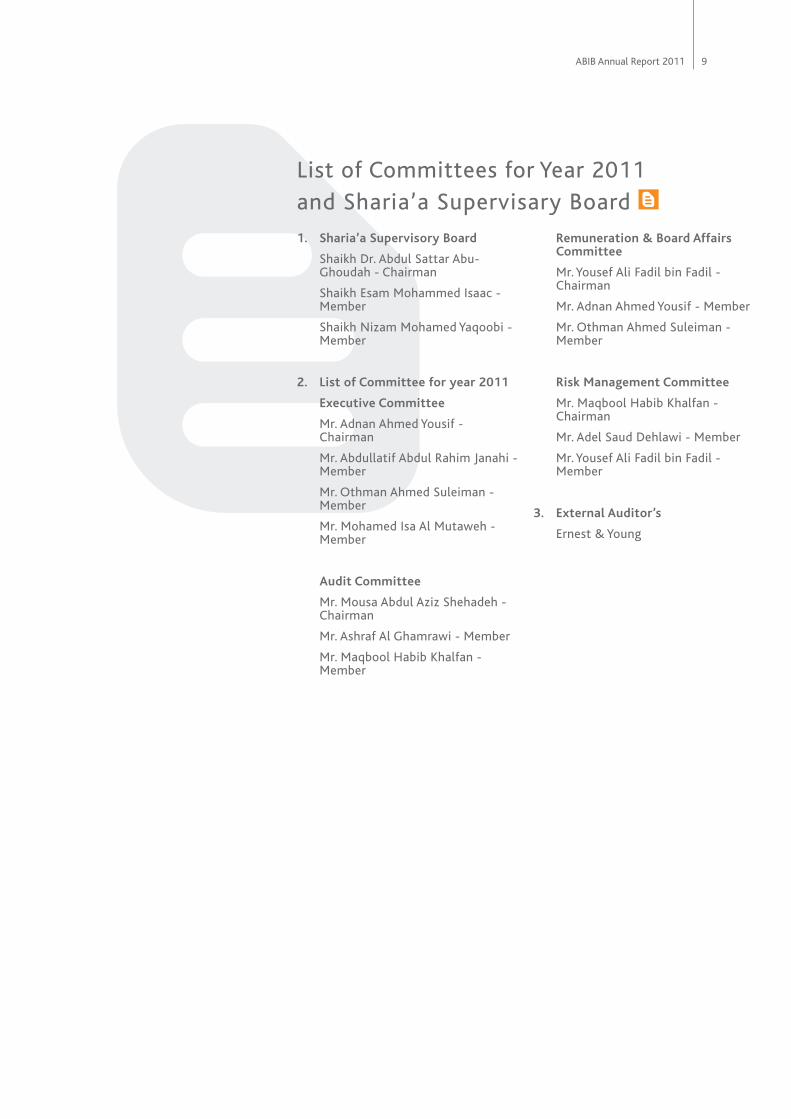

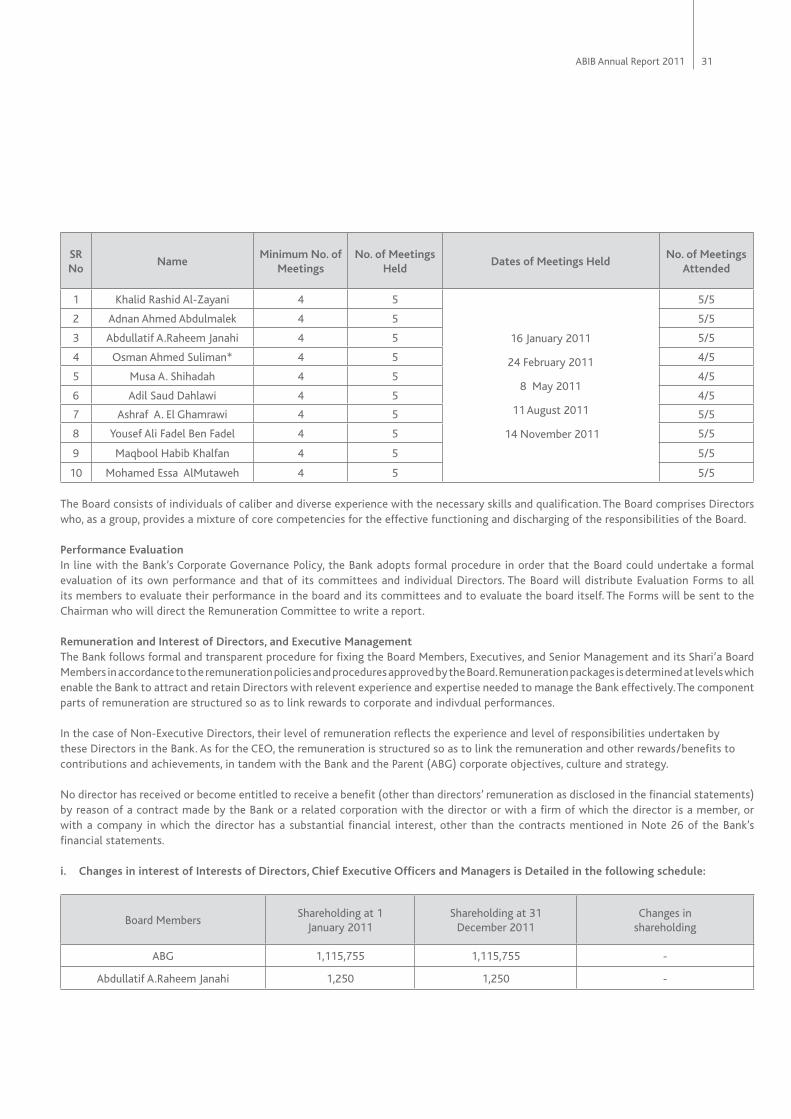

1. Sharia’a Supervisory Board

Shaikh Dr. Abdul Sattar Abu-Ghoudah - Chairman

Shaikh Esam Mohammed Isaac - Member

Shaikh Nizam Mohamed Yaqoobi - Member

2. List of Committee for year 2011

Executive Committee

Mr. Adnan Ahmed Yousif - Chairman

Mr. Abdullatif Abdul Rahim Janahi - Member

Mr. Othman Ahmed Suleiman - Member

Mr. Mohamed Isa Al Mutaweh - Member

Audit Committee

Mr. Mousa Abdul Aziz Shehadeh - Chairman

Mr. Ashraf Al Ghamrawi - Member

Mr. Maqbool Habib Khalfan - Member

Remuneration & Board Affairs Committee

Mr. Yousef Ali Fadil bin Fadil - Chairman

Mr. Adnan Ahmed Yousif - Member

Mr. Othman Ahmed Suleiman - Member

Risk Management Committee

Mr. Maqbool Habib Khalfan - Chairman

Mr. Adel Saud Dehlawi - Member

Mr. Yousef Ali Fadil bin Fadil - Member

3. External Auditor’s

Ernest & Young

List of Committees for Year 2011and Sharia’a Supervisary Board

ABIB Annual Report 2011 9

In spite of the difficult operating environment the Bank has been able to achieve a net profit of US$ 2.595 million in the year 2011.

Al Baraka Islamic Bank B.S.C (c) 10

Board Of Directors’ Report Dear Shareholders,On behalf of the Board of Directors, I am pleased to present our report covering an overview of the Bank’s business for the financial year ended 31 December 2011.

The year 2011 witnessed a more promising outlook and some economic activities started but the upside was constrained by major economic events globally led by, for instance, the USA facing difficulties in repaying significantly its debt which resulted in a downgrade of its rating. This key event was followed by downgrades of ratings of some other developed countries. Some major financial institutions also faced difficulties in repaying their financial obligations. The equity markets worldwide fell drastically. This series of events highlights the difficult operating environment worldwide.

However, by the grace of Allah, I am pleased to report that in spite of the difficult operating environment the Bank has been able to achieve a net profit of US$ 2.595 million in the year 2011, as compared to profit of US$ 4.652 million last year. After adjustment of a one-off gain related to the merger of the Pakistan Branches, amounting to US$ 9.833 million in 2010, the profit for the year 2011 is considerably higher as compared with the last year. The profit has been made despite setting aside general provisions and a substantial increase in the investment risk reserve. The total assets of the Bank showed healthy growth and increased to US$ 1.598 billion as compared to US$ 1.346 billion last year reflecting an increase of 18.72%. The on balance sheet equity of investment account holders also showed growth from US$ 0.958 billion in the year 2010 to US$ 1.056 billion in the year 2011, an increase of 10.20%.

The Bank is continuously increasing its infrastructure, product portfolio and client base. It is now among the key players in the Islamic banking industry in Bahrain and Pakistan. The size of the Bank is continuously increasing which is necessary to compete in the market. In line with its strategy of growth, the network has grown to 95 branches (including Pakistan). The Bank is currently benefiting from implementing a new Strategic Plan approved by the Board of Directors. Financial results have improved, the retail portfolio has increased and non performing financing is also showing a

declining trend. The Bank is in the process of completing the acquisition of the majority shares of Itqan Capital (Saudi Arabia) in line with the policy of its parent company, AlBaraka Banking Group, to enter into key regional markets. Last year the shareholders of the Bank approved the merger of the Pakistan Branches of the Bank with those of the Emirates Global Islamic Bank Limited. The name of the merged entity was changed to AlBaraka Islamic Bank Pakistan Limited (AIBPL). The Bank’s shareholding comprises 64.64% in AIBPL. The macro economic situation in Pakistan remained sluggish during the year under review. The State Bank of Pakistan (SBP) slashed the discount policy rate by a cumulative 200 bps during July-December 2011, which currently stands at 12%. The Ministry of Finance had also displayed resolve towards solving the massive issue of circular debt. These cohesive actions were aimed towards facilitating private sector credit on one hand and addressing the issue of energy shortages on the other in order to free up the productive capacity and re-ignite economic growth. However, recent monitory policy statements issued by the SBP cast significant uncertainties, as to how effective these measures will prove in achieving the desired objectives.

By the grace of Allah, despite the depressed economic scenario that prevailed in Pakistan throughout the year under review, our subsidiary in Pakistan has displayed a robust performance not only in terms of growth in deposits and asset base but also in terms of a significant turnaround which transformed the Subsidiary into a profitable operating unit. The Bank has made significant achievements in realizing cost and revenue synergies generated from the successful merger, as the integration agenda remained a top priority during the year 2011. The operating expenses have decreased despite of inflationary pressures in the country. Most of the integration work has been completed and Integration of core banking systems is expected to be completed during 2012.

Capital Intelligence has maintained its long term and short term foreign currency ratings of the bank at BB+ and A3 respectively with a stable outlook based on the financial statements for the year 2010.

ABIB Annual Report 2011 11

Board Of Directors’ Report (Cont.) AlBaraka Islamic has been a regular contributor to the societies and communities within which it operates. We sponsored many diverse and worthy programs to promote Islamic Banking and also helped various charitable organizations.

The Bank enjoys strong ownership and continued support through the AlBaraka Banking Group. The Group is a well established and reputable banking entity, which provides us with confidence, support and diversity. With a robust network of banking operations through numerous branches across 13 countries and a strong source of marketing, financial and technical capabilities, the Group provides the Bank with a highly diverse and extended horizon for development and growth. The Bank has successfully launched a number of initiatives in the field of trade finance and correspondent banking leveraging Group synergies. These initiatives have helped the Bank to increase its fee based income.

Although the economic and operating environment in both markets in which we operate, Bahrain and Pakistan, is challenging we look towards 2012 with great optimism as all indicators are positive for recovery and continued growth in the GCC countries. The Bank is well positioned to take advantage of the market opportunities and synergies offered through the merger of the Pakistan Branches. We will continue to invest for profitable growth as opportunities will continue to present themselves and we believe that the future is brighter inshallah.

Finally, I would like to take this opportunity to thank on behalf of the Board His Majesty King Hamad bin Isa Al Khalifa, HRH Prince Khalifa bin Salman Al Khalifa, the Prime Minister and HRH Prince Salman bin Hamad Al Khalifa, the Crown Prince and Deputy Supreme Commander of the Bahrain Defense

Force for their ongoing guidance which contributed to establishing a successful and distinguished Islamic bank in the Kingdom. Our thanks also extended to the Ministry of Industry and Trade, the Central Bank of Bahrain and the State Bank of Pakistan for their unwavering support to our business and for their guidance to promote various programs.

We would also like to extend our gratitude and appreciation to Al Baraka Banking Group, our parent company, to the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) for their support and valuable guidance, to our loyal clients and investors whose trust and support enabled us to achieve our goals, and of course we thank all of our employees who are the cornerstone of our success.

Regards,

Khalid Rashid AlZayaniChairman

Manama,Kingdom of Bahrain19 February 2012

Al Baraka Islamic Bank B.S.C (c) 12

Equity of investment account holders also showed growth from US$ 0.958 billion in the year 2010 to US$ 1.056 billion in the year 2011, an increaseof 10.20%.

ABIB Annual Report 2011 13

1

2

5

8

3

6

9

4

7

10

Executive Management

11 12

Al Baraka Islamic Bank B.S.C (c) 14

1) Mr. Mohammed Isa Al Mutaweh Experience: 25 years Chief Executive Officer and Member of

the Board of Directors He is the Chief Executive Officer and

Board Member of Al Baraka Islamic Bank - Bahrain, Chairman of Credit Committee and Member of Executive Committee. Backed by a long banking experience over 25 years of which he previously held several senior positions, General Manager and Board Member of Al Amin Bank, Bahrain, Chairman of Credit Committee and member of Executive Committee of Al Amin Bank. Executive Director in ABC Islamic Bank, and prior to that, he was in a senior position with National Bank of Bahrain in the Corporate Banking Division. He is also a member of the World Union of Arab Bankers and a member of the participation committee of the Awqaf Properties Investment Fund of Islamic Development Bank, Jeddah and a member of the board of directors of Bahrain Association of Banks and a member od Bahrain Advisory Council of the Chartered Institute for Securities & Investment (CISI), UK. Mr. Al Mutaweh a Bahraini national and has a Bsc. in Business Administration from University of Bahrain, 1986.

2) Mr. Tariq Mahmood Kazim Experience: 28 years Deputy General Manager - Support

Services and Overseas Branches (Pakistan).

Bachelor Degree in Systems Engineering and Analysis (University of Petroleum and Minerals Dhahran/Saudi Arabia) 28 years of experience in providing, managing and implementing Banking, Telecommunication and e-Commerce Solutions. Past careers include two years with Arabian Networks as General Manager and 16 years with NCR as a Business Unit Leader. Joined AlBaraka Islamic Bank in April 2002. He is also a Board Member in Al Baraka Bank Syria and Al Baraka Bank Pakistan Limited

3) Mr. Moosa Abdul Latif Mohammed Experience: 29 years Assistant General Manager - Operations Banking Studies (Diploma) 5 years

Banking experience with National Bank of Bahrain, and 27 years banking

experience with AlBaraka Islamic Bank, Bahrain. Various managerial and banking courses inside and outside Bahrain.

4) Mr. Rashid Hassan Alalaiwi Experience: 30 years Assistant General Manager - Retail

Banking and Domestic Branches Mr. Rashid is Assistant General

Manager for Retail Banking & Domestic Branches.Mr. Rashid is a holder of MBA - University of Glamorgan, Wales, UK and Executive Management Diploma - University of Bahrain. He has worked at senior positions in retail banking, customer services, e-banking and retail operations. Mr. Rashid held several senior positions prior to joining Al Baraka Islamic Bank with Bahrain Islamic Bank, Shamil Bank of Bahrain and bank of Bahrain and Kuwait.

5) Mr. Nadeem Khan Experience: 25 years AGM and Chief Financial Officer Mr. Nadeem Amjad Khan is a Chartered

Accountant and is a Fellow of the Institute of Chartered Accountants of Pakistan. Prior to his appointment as CFO of Albaraka Islamic Bank, Bahrain he worked in Pakistan Branches. He joined Pakistan Branches as Assistant Vice President and rose to the position of Assistant General Manager. He has also worked in leading accounting firms at senior position in Assurance and Management consultancy. He has also been teaching ACCA students. He specializes in accounting and financial matters and has developed broad expertise in treasury and capital markets.

6) Mr. Fouad El Ouzani Experience: 10 years Assistant General Manager - Credit

Department Mr. EL Ouzani main responsibilities

includes the development and updating of policies and monitoring the process of limit establishments, transaction booking and to supervise at credit departments sub-units business processing. Fouad held several managerial positions prior to joining Al Baraka Islamic Bank in Gulf international Bank, The Arab Investment Co. and Arab

ABIB Annual Report 2011 15

Al Baraka’s highly qualified Executive Management team provide the highest level of service to employee’s and customers alike.

Al Baraka Islamic Bank B.S.C (c) 16

Banking Corporation (ABC) Bahrain. Fouad holds a B.S.C Degree Chemical Engineering from University of Bahrain.

7) Mrs. Maisoon Mohammed Shams Experience: 27 years Assistant General Manager - Risk

Management and Compliance; Marketing Mrs. Maisoon has a thorough

experience in developing risk management framework, corporate governance, policies & procedures, and Business continuity plan. She has over 27 years of practical experience in Financial Banking Operations, Credit Risks Management, Operational Risks Management, Audit and Controls, Strategic and Management. She also has a thorough understanding of banking regulations and regulatory reporting require Basel II principles. During her career, Mrs. Maisoon held several senior positions in Central Bank of Bahrain as well as Retail Banks. Mrs. Maisoon holds Masters of Business Administration from the University of Strathclyde - UK, B.Sc degree in Accounting from University of Bahrain, and Strategic leadership and Executive Management Program Certificate from Beyster Institute, California - USA.

8) Mr. Adnan Shareeda Habib Experience: 27 years Senior Manager - Local Branches, Retail

Banking Banking Studies (Advanced Diploma),

8 years Banking experience with NBB and 19 years with AUB (Corporate, Commercial and Retail Banking), position Senior Manager Commercial Branch.

9) Mr. Asrar Uddin Abdul Ghafoor Senior Manager - Information Technology Experience: 15 years Mr. Asrar Uddin has over 19 years

experience in playing an effective role in the IT department of Islamic Bank’s in the GCC region. He joined alBaraka IT team in 2002. He has vast knowledge of core banking project implementations, project rollouts, automation of business processes, managing systems migrations, managing day to day activities of IT operations. His major achivements in

alBaraka are many but to name some are; Implementation of Misys Equation Banking System, migration fron Midas to Equation, sucessful completion of EMV Project, increasing branches and ATM network, implementation of IT policy and procedures, supporting other alBaraka Banks in Pakistan, South Africa, Egypt, Syria and Lebanon.

10) Mr. Isa Al Obaidly Senior Manager - Human Resources

and Administration Experience: 24 years Mr. Al Obaidly has 24 years experience

in several HR & Admin fields including recruitment, Setting of procedures, payroll & payment processing. Earlier he occupied the post Management Analyst the Civil Service Bureau and Chief for the Government Payroll & Leaves, Director of Fund Collection from Bahrain centre for study and research and HR & Finance cosultance and Acting Director at the Ministry of Information,. Isa attend several professional courses including civil service Bureau conducted by Management Institute Services, UK-1992, a course on Leadership for Democratic Society at the Federal Executive Institution West - Virginia U.S.A-1997. Al Obaidly holds the professional Auditor for ISO 2009 Certificate. He is a holder of a B.S.C degree in Business Administration from Grand View College, USA. And Master degree in Management Technology from Arabic Gulf University Jan1999.

11) Mr. Adel Al-Manea Senior Manager - Commercial Banking

Department Experience: 22 years Mr. Al-Manea is Senior Manager for

Commercial Banking Department. Mr. Al-Manea is a holder of Associated Accounting Technician from the Board of AAT - United Kingdom and Banking Studies (Diploma) from University of Bahrain. He has over 23 years of banking experience in commercial and Offshore Banks with Local, International and Islamic Banks. 2 years banking experience with Bank of Bahrain and Kuwait, and 18 years

banking experience with Ithmaat Bank. Various managerial and banking courses inside and outside Bahrain. Joined AlBaraka Islamic Bank in August 2008.

12) Mr. Hussain H. Nattaie Senior Manager - Corporate Banking

and Syndications Experience: 8 years Mr. Al Nattaie is the Head of Corporate

Banking and Syndications Department with over eight years experience in local and offshore corporate banking. Hussain held several senior positions prior to joining Al Baraka Islamic Bank in National Bank of Bahrain, The Arab Investment Company and Standard Chartered Bank. Hussain holds a B.Sc. degree in Accounting and Finance from the University of Bahrain and currently is doing the CMA. Mr. Al Nattaie became a member of Al Baraka Bank begining of year 2008.

Executive Management (cont.)

ABIB Annual Report 2011 17

We have continued also building fruitful business relations with major industrial and commercial companies in Bahrain with a view to providing them with products and services that meet their banking and finance needs.

Al Baraka Islamic Bank B.S.C (c) 18

Chief Executive Officers’ Report IntroductionThe year 2011 was tough year locally, regionally and globally and was characterized by aggravation of economic problems internationally, especially in the Euro zone and US, which in turn created unfavorable environment for businesses and banks in the world. Despite this, we are delighted to see the good performance of Al Baraka Islamic Bank. These results were achieved firstly by the Grace of Allah, and then by the outstanding efforts made by the Bank management in expanding the Bank’s activities and business at all levels based on the flexible and diverse business strategy that it had launched for the years 2009 - 2013 and which included a number of initiatives in the area of product diversification, expansion of branch network, enhancement of foreign trade financing and other initiatives that have had good impact on the results of the Bank.

The Bank continued in 2011 implementing a series of initiatives that had clear positive effects on the Bank’s performance. The conversion of the Bank’s branches in Pakistan to an independent Islamic commercial bank following the merger with Emirates Global Islamic Bank in Pakistan and our hard work to activate these branches and turnaround them to profitability had an evident positive effect on the operations of the Bank, and its ability to continue expanding and growth, despite the prevailed conditions their, in view of its deep experience in this market, and the large support from the parent company Al Baraka Banking Group. We also continued our ambitious work in Bahrain to launch new services and products, open new branches, and enhance capital, technical and human resources of the Bank. All these factors had helped in achieving the good results of the Bank during 2011.

We have continued also building fruitful business relations with major industrial and commercial companies in Bahrain with a view to providing them with products and services that meet their banking and finance needs, as well as turning much of our attention to the development of the Bank’s human resources and the hiring of skilled recruits to help the Bank in the implementation of its new business strategies. Furthermore, we introduced new IT systems to enable the Bank provide the most advanced banking services to its customers and increase its operational efficiency Based on all these steps, we succeeded in arranging a number of major finance transactions in which banks inside and outside the region had participated. In this regard, the Bank has succeeded in signing memoranda of understanding with

three Indian banks to finance Indian exports to African countries, in implementation of its ambitious plan to finance trade between India and African countries.

As for our local branch network, we have in June 2011 celebrated the opening of the Bank’s sixth branch in the Kingdom of Bahrain in Al Ramly Mall, Aali. Furthermore, we also started working on a plan to open two more branches this year 2012, which highlights our determination to enhance our financing and deposit market share, considering that the Bank has a range of highly successful financial and deposit products designed for individuals and companies which include many attractive features that best meet the needs of customers in strict compliance with Islamic Sharia.

We also started working on implementing the Bank’s plan to launch e-banking services which include providing Internet banking and phone banking services. These services are expected to be available to customers by the end of this year.

We are delighted also by the reaffirmation of the credit ratings of the Bank by Capital Intelligence, thanks to our large capital, technical and human resources, and being one of the oldest Islamic banks in Bahrain and the region, owning long experience with customers and markets needs, as well as our belonging to leading and strong Islamic banking group. All these factors have contributed to our good results in 2011.

We are in a good position to make strong progress and to enhance our leading position in the Kingdom of Bahrain and the region, where financial and economic conditions move towards recovery, especially that the economies and the financial and banking systems in the region are sound and strong and that the governments in the region stressed that they would continue their spending on investments and infrastructure development and reaffirmed their support to the financial and banking systems.

As we see it, the current financial crisis will encourage the demand on Islamic banking products and services on a larger scale after the Islamic banks had proved their credibility by staying away from the mishaps of the conventional banking system and protected themselves by following a banking framework based on the Islamic Sharia’a which prohibits all forms of speculation and uncalculated risks.

We are aware that we will be facing many challenges during year 2012, but we are

ABIB Annual Report 2011 19

significant growth in the financing and investment operations, which in turn led to an increase of 18.7% in the Bank’s assets rising from US$ 1.35 billion as at the end of 2010 to about US$ 1.60 billion as at the end of 2011.

Income - Generating AssetsThe total income- generating assets increased significantly by 19.4% from US$ 1.05 billion in 2010 to US$ 1.25 billion in 2011. Murabaha sale receivables continued to be the main component of the income- generating assets, rising by 12.8% from US$ 538.40 million in 2010 to US$ 607.36 million in 2011. These financing operations represent Murabaha financing agreements with financial institutions and corporations that the Bank provided to them primarily through syndicated financing arrangements.The Bank continued during year 2011 to focus on countries in which Al Baraka Banking Group has a presence such as Turkey, Jordan, Algeria, and Sudan with a view to enhancing the business between the subsidiary units of the Group and with major corporations and financial institutions in these countries to promote Islamic banking there. We have also took a number of initiatives particularly in the area of the development of treasury and trade finance business, especially the trade finance operations that enhance the Kingdom of Bahrain’s position as an intermediary between suppliers and exporters from different Arab countries and across the world. For this reason, the opening of documentary credits and guarantees by the Bank to facilitate import and export has continued in 2011.

Based on all these steps, we succeeded in arranging a number of major finance transactions in which banks inside and outside the region had participated. In this regard, the Bank has succeeded in signing memoranda of understanding with three Indian banks to finance Indian exports to African countries, in implementation of its ambitious plan to finance trade between India and African countries. The Bank is also working on arranging an Islamic financing deal of about US$ 40 million to finance the import of sugar to some Arab countries from a sugar- exporting country, and there are many more deals that will be arranged in the first quarter of 2012.

In the area of retail finance, the Retail Banking Department was launched in 2009 to implement an ambitious strategy to expand and increase the Bank’s market share in this sector. The financing products launched under the Taqseet (installment) scheme were

confident of our financial, technical and human resources capabilities and ability to achieve the ambitious goals set for the Bank to enable it to attain a leading position in the Kingdom of Bahrain.

Financial PerformanceIncomeThe continuation of the implementation of the Bank’s new strategy for the years 2009 - 2013 and the series of initiatives we have taken in accordance with this strategy, which we mentioned earlier, have had a positive and significant impact on the Bank’s business and activities.

As a result of the foregoing, the total income from the joint finance and investment accounts amounted to US$93.68 million in 2011, representing a remarkable growth of 101% from the previous year. This income includes the income from joint financing operations which has increased by 37.3% from US$ 33.81 million in 2010 to US$ 46.43 million in 2011 and income from other financings and investments which has increased significantly by 269.2% from US$ 12.80 million in 2010 to US$ 47.25 million in 2011. This latter income mainly includes income from Ijarah Muntahiya Bittamleek amounting to US$ 11.18 million dollars (US$ 7.12 million in 2010), income from investments amounting to US$ 33.32 million (US$ 5.97 million in 2010), income from Mudaraba finance amounting to US$ 1.25 million (US$ 1.05 million in 2010) and income from Musharaka financing amounting to US$ 6.15 million (US$ 1.95 million in 2010). It is clear from these figures that the there were significant improvements in all income items from other financing and investments, especially income from Ijarah, investments and Musharaka, as a result of the growth in the Bank’s business and activities and Merger pakistan.

In line with the growth in the total income from joint financing, the return on unrestricted investment accounts went up by 123.5% from US$ 30.61 million in 2010 to US$ 68.40 million in 2011, which represents the gross return on unrestricted investment amounting to US$ 86.98 million in 2011 (US$ 45.90 million in 2011) less the Bank’s share as a Mudarib of US$ 18.58 million in 2011 (USS 15.29 million in 2010).

After deducting the investors’ share from the revenue from the unrestricted investment accounts, the Bank’s total share of income (as a Mudarib and financier) amounted to US$ 25.28 million in 2011 compared with US$ 16.01 million in 2010, reflecting a significant increase of 57.90%.

The majority of the other sources of income also showed improvements in line with the expansion in financing and investment operations as at the end of the year. The Bank’s income from other financing and investments financed by the Bank increased by 107.5% from US$ 3.34 million in 2010 to US$ 6.94 million in 2011, while income from banking services increased by 42.23% from US$ 4.87 million in 2010 to US$ 6.93 million in 2011, which included primarily fees and commissions, letters of credit and acceptances fees and letters of guarantee fees. Other income, which mainly included gains from foreign exchange, also increased by 30.4% from US$ 2.87 million in 2010 to US$ 3.74 million in 2011.

As a result of these good results, the total operating income of the Bank has increased by a significant 51% from US$ 28.52 million in 2010 to US$ 43.06 million in 2011.

As a result of the Bank’s continuation to open new branches and install new ATMs which entailed an increase in the number of staff, and the installation of the Bank’s new core banking system, as well as the full consolidation, for the first time, of operating expenses of both Bahrain and Pakistan’s operations, the operating expenses showed a remarkable 60.7% growth from US$ 24.40 million in 2010 to US$ 39.20 million in 2011. The expenses mainly included staff costs, which went up by 47.2% from US$ 13.45 million in 2010 to US$ 19.80 million in 2011 and other operating expenses which increased by 87.8% from US$ 8.39 million in 2010 to US$ 15.75 million in 2011.

As mentioned earlier, the Bank, as part of its precautionary measures to address the repercussions of the financial crisis, has continued to set aside provisions to guard against any possible deterioration in the quality of the finance and investment portfolios. These provisions amounted to US$ 550 thousands in 2011 compared with US$ 8.52 million in 2011, reflecting the improved quality of the financing and investment portfolios of the Bank. The Bank’s efforts also focused on reducing the non- performing loan portfolio by active and successful follow-up to recover these loans and monitoring them closely.

As a result of the large increase in operating expenses and after deducting taxes, the Bank’s net income amounted to US$ 2.60 million in 2011 compared to US$ 4.65 million in 2010.

The Bank’s Financial PositionThe initiatives taken by the Bank during the year 2011 reflected in a positive and

Chief Executive Officers’ Report (Cont.)

Al Baraka Islamic Bank B.S.C (c) 20

well received by customers because they met all their financing needs in terms of the purchase of personal and consumer goods and real estate for own-use as residence or for investment purposes. During 2011, Al Baraka Islamic Bank launched a number of promotional offers offering customer finance on easy terms with competitive profit rates while at the same time maintaining prudent credit criteria. The Bank was successful in achieving its objectives for this year and its financing portfolio grew in spite of intense competition in the consumer and personal finance sector.

Al Baraka Islamic Bank has also added new benefits that Taqseet (installment) card offered which enhanced the Bank’s presence in new markets and attracted new customers. The Taqseet card is an innovative Islamic financing tool in the card market that has been developed on the basis of Murabaha Islamic financing mode. What makes the Taqseet Card so unique is that the customer can have several finance facilities running on just one card at the same time. The value of the purchase can be paid back on monthly Flexible Installments.Investments, which represented the second largest income generating assets, witnessed considerable growth during year 2011, going up by 34.5% to reach US$ 421.93 million compared with US$ 313.70 million in 2010. The investment portfolio consisted of Sukuks in an amount of US$ 341.59 million and investment funds, private equities, and real estate in an amount of US$ 85.93 million in 2011.

It is worth mentioning that the Bank decided in 2011 to acquire 60% of the issued shares of Al Tawfeek Financial Group, which its name was later changed to Itqan Capital. The procedures for consummating the acquisition are expected to complete during 2012. Al Tawfeek Financial Group Company is a closed joint stock company registered in the Kingdom of Saudi Arabia and licensed by the Capital Market Authority. The company engages in asset and portfolio management, and custody, research and advisory services. All products and services offered by the company are in strict compliance with the provisions of Islamic Sharia. The company’s paid-up capital is SAR 200 million and the authorized capital is SAR 360 million. This step represent the Bank and the parent company Al Baraka banking Group’s strategy to enter key regional markets, for Saudi Arabia is the largest Arab economy with strong fundamentals and a stable financial and investment environment, which presents us with significant business and investment opportunities.

The Treasury Department has been very active during year 2011 in the purchase investments in Islamic Sukuks, which are financial instruments approved by the Sharia’a, for the purpose of employing the surplus liquidity of the Bank. In this context, the Bank has expanded its portfolios in Salam Sukuks and the Sukuks issued by the Government of Bahrain, as well as that issued by other governments or state-owned companies in the region, considering the good returns that they yield compared to the level of risk they entail.

We also continued to closely monitor all of our investment portfolios. The Bank expanded its revenue- generating investments and disposed of the inactive investments, making appropriate provisions where necessary based on their actual market value. As for investment funds, we continually monitored their performance to ensure that they continued to yield satisfactory returns.

The income-generating assets also included Mudaraba finance, which increased by 2% from US$ 25.07 million in 2010 to US$ 25.56 million in 2011. These finance transactions are usually conducted with banks and financial institutions. The assets also included Ijarah Muntahiya Bittamleek which increased by 10% from US$ 93.20 million in 2010 to US$ 102.56 million in 2011. Similarly, Musharaka financing increased by 13.3% from US$ 55.59 million in 2010 to US$ 62.97 million in 2011. Ijarah financing also went up by 37.6% from US$ 18.50 million in 2010 to US$ 25.45 million in 2011, while the real estate investments portfolio had increased by 98.7% from US$ 1.48 million in 2010 to US$ 2.94 million in 2011.

The significant increases in the majority of the profit- generating assets reflect the success of the initiatives that the Bank took to expand its financing and investment activities and operations.

Geographical and Sectoral DistributionDuring 2011, the Bank continued to focus on its main business markets in Bahrain, GCC and MENA in order to benefit from the abundant opportunities available there. As a result, the share of the Asian markets represented 50% of the total assets of the Bank, followed by the Bank’s assets in the Gulf and the Middle East and North Africa region at 44%, then comes Europe at 4% while the remaining assets are divided between the other regions.

Of these assets, 40% represents transactions with banks and financial institutions, 19% with commercial and production businesses, 2% in construction and contracting and 39% in other sectors and activities.

Liquidity ManagementA key element of the Bank’s culture and policies is the maintenance of strong liquid assets to accord with its leading role as a commercial bank on the one hand, and its ability to seize upon good opportunities that may become available in the regional markets, as an investment bank on the other. After the outbreak of the financial crisis, we promptly re-emphasized this approach as part of our overall precautionary measures. Liquid assets (cash and balances with banks) amounted to US$ 253 million in 2011 compared to US$ 200 million in 2010, representing and increase of 26.5% and accounted for 19.7% of total customer deposits and unrestricted investment accounts. The distribution of assets in terms of maturity shows that 54% of the total assets has a maturity within a period not exceeding one year, compared to 84% on the liabilities and equity side, which reflects the strong liquidity position of the Bank.

Liabilities and Customer AccountsOn the liabilities side, the unrestricted investment accounts, deposits from financial institutions and current accounts represented the main source of funds for the business operations of the Bank. These accounts increased by a significant 13.1% in 2011 to reach US$ 1.28 billion up from US$ 1.14 billion in 2010 in spite of the liquidity squeeze caused by the global financial crisis, which confirms the customers’ confidence in the Bank. These accounts financed 80% of the total assets, which reflects the solid customer base of the Bank.

The unrestricted investment accounts represent the main external source of funds for the Bank. These increased by a good 10.3% in 2011 to reach US$ 1.06 billion compared to US$ 957.95 million in 2010. The increase comes primarily from a rise in unrestricted investment accounts from financial and banking institutions.

While deposits from financial and banking institutions increased by 68.1% to US$ 98.81 million in 2011 compared to US$ 58.78 million in 2010. Current accounts increased by 9.1% from US$ 118.47 million in 2010 to US$ 129.26 million in 2011.

These achievements reflect the success of the many initiatives taken by the Bank

ABIB Annual Report 2011 21

children with autism or cerebral palsy along with the CARE Foundation, which provides education and rehabilitation to underprivileged children, in addition to partnering Afzal Memorial Thalassemia Foundation in its effort to rid the country of this debilitating blood disorder and sponsoring the rehabilitation of the disabled and contributing towards children’s education through The Citizen’s Foundation.

New Identity of the BankIn line with the strategy being implemented by Al Baraka Banking Group, BSC (ABG), regarding the unification of the new identity of the Group and its subsidiary banking units, Al Baraka Islamic Bank launched its new unified identity on 3rd June 2009. The main objective of the new identity is to ensure that all the banking units of the Group share unified goals and business strategies. For this reason, Al Baraka Islamic Bank views this step as a major achievement for the bank in its quest to attain a leading position in the Islamic banking industry.

The new identity requires us to adopt a set of policies and high ethical and professional standards with regard to the offering of innovative and highly efficient Sharia’a-compliant services and products. To achieve this, we put in place a number of programs and plans which are currently being implemented to embody the motto of the new identity of the Group in being a “Partner Bank” to our customers, investors, and all our stakeholders. These steps included the implementation of a number of programs at all levels at the Bank to promote the understanding and assimilation of the new corporate identity and the values and principles that it represents and, which in turn, require high skills and outstanding performance from all employees.

As we proceeded further with the launch of the unified corporate identity, the concept of Brand Guardianship had been introduced across all Al Baraka Banking Group units, to ensure the smooth assimilation of the brand in all markets. In line with international best practice, a high level branding committee at Group Head Office has been charged with the responsibility for “Brand Guardianship” across the Group. In this regard, several initiatives have been commissioned at the Group level through the Branding & Special Projects team and the Brand Guardians, amongst which are:

1. The issuance of Retail Products Guides and Manuals

2. The issuance of a detailed manual for the standardization of Al Baraka’s retail branches network.

in expanding its business with financial institutions and major companies in countries in the Gulf region, the Middle East and North Africa region and Asia, as well as developing innovative retail banking savings products and increasing the number of its branches.

Capital AdequacyTotal shareholders equity amounted to US$ 178.84 million in 2011 compared to US$ 183.96 million in 2010, representing a decrease of 2.8%. The capital adequacy ratio (in accordance with the instructions of the Central Bank of Bahrain “CBB” with respect to the implementation of the directives of Basel II) remained at a very satisfactory level of 17.5% in 2011 compared to 20.54% in 2010, which provides the Bank with a strong capital base for growth in the coming period.

Restricted Investment AccountsThe restricted investment accounts amounted to US$ 259.96 million in 2011 compared to US$ 182.90 million in 2010, reflecting an increase of 42.1%. These accounts are invested primarily in Mudaraba transactions with customers.

Al Baraka Bank (Pakistan) LimitedAs mentioned earlier in this report, the Bank’s branches in Pakistan have in 2010 been converted the to an independent Islamic commercial bank after the merger with Emirates Global Islamic Bank in Pakistan, which resulted in the emergence of Al Baraka Bank Pakistan as the second-largest Islamic bank in Pakistan with 89 branches covering all cities in Pakistan.

The Pakistan economy grew in 2011 by only around 2.4% compared with the stronger 3.8% growth exhibited the year before, as the country continued to try to deal with the aftermath of the devastating floods of 2010 and the power shortages that were the direct consequence of them. The acute energy crisis, which has led to riots in major cities by a frustrated populace and has particularly affected the manufacturing industries, reflects the failure of the government to achieve the rates of growth necessary to bring unemployment down. Although the key textiles industry, which accounts for 60% of the country’s exports, hit record revenues in the past fiscal year to June on the back of increased demand from OECD countries for cheaper garments, overall the future is uncertain. Inflation remains stubbornly high at an estimated 11.9% although it is an improvement over 2010’s 15.5%.

In an effort to stimulate the economy, the State Bank of Pakistan has steadily reduced

its discount rate over the last year, so that three-month rates now currently stand about 2% lower than at the end of 2010, although government 10-year bonds now pay 13.4% compared with 10.66% a year ago. The current account deficit has meanwhile risen to -1.3% of GDP from -0.9% at the close of 2010.

Al Baraka Pakistan’s assets grew in 2011 by 19% in Pakistan Rupee terms but by 13.4% in US dollar terms due to the change in exchange rates over the period. Total financings and investments increased by 22.16% to US$611 million primarily due to a substantial increase in the bank’s non-trading investments portfolio which expanded by 59.58% to US$298 million, while the Murabaha portfolio remained stable. This overall expansion was in turn funded by a 16% increase in customer deposits including IAH which itself rose by 15% to US$610 million.

Total operating income was 103.83% higher at US$26 million compared to 2010. The major contributors were the Murabaha, Musharaka, non-trading investments and Ijarah Muntahia Bittamleek portfolios. Operating expenses were 21.28% higher at $21 million, leaving a net operating income of $4 million. After provisions and taxation charge, the net profit for the year was $2 million.

The branch network at the end of the year was a total of 89 branches. Under its ambitious strategic plan, it plans to open a further 126 branches over the next 5 years, with 20 alone slated for 2012. The WAN (Wide Area Network) system connecting the branches to Head Office was restructured so that all branches are now synchronised on a single network. A detailed postmerger integration plan has meanwhile been completed and is due for implementation over 2012. Meanwhile, as the new bank focuses on updating and developing its range of Shari’a compliant products, it plans the launch of a new visa debit card for use at Point of Sale terminals and ATM machines globally, in addition to interbank funds transfer facilities permitting customers to transfer funds between banks of their choice around the country. These new products will be introduced as soon as migration to the new core banking system has been fully implemented.

Al Baraka Pakistan’s social contribution includes supporting the Rising Sun Institute, which provides education, speech therapy and vocational training to more than 400

Chief Executive Officers’ Report (Cont.)

Al Baraka Islamic Bank B.S.C (c) 22

3. Standardization of the marketing communication, especially in connection with customers touch points – both one to one as well as advertising messages.

At the subsidiary unit level, the Chief Executive Officer of each bank of the Group has been appointed Brand Guardian for his respective unit, assisted by senior executives, to ensure that all activities related to the brand conform to the unified policies. The launch of the Unified Identity resulted in attaining many achievements, which can be summarized as follows:

Customer interest levels have heightened, resulting in a good increase in the number of new customers.

Staff across the Group became highly motivated and fully engaged with the implementation of the Group Vision and the concept of partnership and participation was introduced at work.

As a result of this, there is now a strong customer oriented approach in all marketing activities. This approach is derived from the strategy outlined in the unified corporate identity and it has now been fully integrated into the policies, procedures and business methodologies.

We look forward in confidence to the challenges ahead and to the adoption of our newly articulated Group ethos, which we believe will truly reflect the essence of the promise we at Al Baraka Islamic Bank took upon ourselves.

BranchesAs for our local branch network, we have in June 2011 celebrated the opening of the Bank’s sixth branch in the Kingdom of Bahrain in Al Ramly Mall, Aali. Furthermore, we also started working on a plan to open two more branches this year 2012, which highlights our determination to enhance our financing and deposit market share, considering that the Bank has a range of highly successful financial and deposit products designed for individuals and companies which include many attractive features that best meet the needs of customers in strict compliance with Islamic Sharia.

As for the ATM network, work is in progress to add five more ATM machines during the current year 2012, to bring the total number of ATMs to 16. The focus will be on installing stand- alone ATMs that are not part of branches of the Bank, with particular emphasis on drive-by ATMs.

We also started working on implementing the Bank’s plan to launch e-banking services which include providing Internet banking and phone banking services. These services are expected to be available to customers during this year 2012.

Human Resources and TrainingAl Baraka Islamic Bank continued during 2011 to create a conducive work environment and enhance the values and principles of the Bank to promote the concept of working as one team that possesses the academic qualifications, expertise and capabilities needed for the Bank’s operations and satisfying the needs and expectations of our customers. The Bank also continued its efforts to fill senior positions and improve the performance and productivity of its staff to serve customers better. Furthermore, it organized specialized training courses and workshops, especially in the areas of anti-money laundering, risk management and compliance, human resources management, modern techniques in training and recruitment, banking relations, secretarial skills, investment banking and leadership skills. The training also included sending employees to obtain high or specialized academic qualifications and certificates.

The bank’s management also introduced, as part of its work in serving the community, a program called “Al Ruwad Program” to train university graduates. The program is designed to train university graduates to prepare them for filling leading and senior positions in the future, after arming them with the necessary knowledge and skills required for performing such functions. The management of the Bank, in partnership with Al Baraka Banking Group, has launched a training program for executive trainees in collaboration with Bahrain Institute of Banking and Finance (BIBF), which includes internal and external training on a number of areas in banking and bank departments operations in line with the requirements of the labor market.

The Bank’s management also focused on providing in-house training courses to help improve performance and increase awareness of key business and other essential skills, such as the first aid course, MS Office course and modern secretarial functions in Islamic banks.

Beginning of 2012 also saw the promotion of a large number of employees to enable them assume more senior positions, which will motivate them to continue their hard work and enhance their loyalty to the bank.

Also, some 17 employees who have served Al Baraka Islamic Bank for 30, 25, 20, 15, 10 or 5 years received recognition certificates and awards.

Information TechnologyIn view of the rapid advances in information technology at the global level and the changing developments in this area that this entails worldwide, Al Baraka Islamic Bank is very keen on modernizing the infrastructure of its computer network, increasing its capacity and introducing modern technologies with high-speed data transfer capabilities, which will lead to significant time-saving and reduction of effort on the part of the employees of the Bank.

After going life upon the successful implementation of the new “Equation” core-banking system, the Bank activated a number of programs to support the Bank’s operations relating to the operating and issuance of cards and reporting, as well as providing technology based services to customers such as sending withdrawal and deposit notifications by short text messages (SMS) and obtaining account balance on mobile phones. It also installed a number of internal IT applications such as credit rating of individuals and companies. Al Baraka Islamic Bank is the first amongst all the units of Al Baraka Banking Group to implement this system.

The Bank has also set up a call center equipped with the latest technologies and it is run by qualified staff to respond to customer calls in a professional manner. This is in addition to the development of a complaint system to handle customer complaints and suggestions with a view to improving the level of service offered by the Bank to its customers.

Furthermore, the Bank has undertaken several other initiatives to upgrade the level of customer service including the implementation of a modern banking system based on advanced technology that helps provide superior banking services and that can accommodate the launch of new innovative products. We also launched an ATM card incorporating the embedded EMV chip, which makes it a highly secured and acceptable method of payment in all parts of the world. Many enhancements and improvements were introduced to maximize the benefits of the Core Banking Systems.

As for the anti-money laundering unit, a Suspicious Activities Monitoring system and Watch List Customers (WLC) system

ABIB Annual Report 2011 23

For the third year in a row, the five-year strategy of the Bank for the years 2009 - 2013 proves success, and comes to fruition, as we achieved satisfactory results.

Al Baraka Islamic Bank B.S.C (c) 24

were installed to improve the daily monitoring of Bank activities in combating money laundering.

Corporate GovernanceThe Bank strictly abides by the laws and regulations of the authorities in the countries in which it operates, and it adheres to the guidelines and rules issued by the regulatory authorities such as the Central Bank of Bahrain (CBB) and the Commercial Companies Law.

FinallyAt the end of our presentation of the performance of Al Baraka Islamic Bank in 2011, and in light of the positive financial results that we have made, particularly in terms of enhancing revenues from core operating sources of the Bank, which cover our both main markets Bahrain and Pakistan, we can emphasize our confidence in the future, where the Bank has great capital, human and technical resources and high liquidity that place him in a strong position to take advantage of the regional and global economies once they are recovering from the repercussions of the current crisis, especially as the crisis has proved the merits of the Islamic banking system, its success, and ability to reduce the effects of the crisis on it.

For the third year in a row, the five-year strategy of the Bank for the years 2009 - 2013 proves success, and comes to fruition, as we achieved satisfactory results, and our financing and investments grew significantly, which will be reflected more on the revenue stream during the year 2012. The new five-year strategy of the Bank include the development of the current business of the Bank, as well as new areas of business and expanding the network of relationships with clients from individuals, companies and financial institutions in Bahrain and the rest of the region’s markets.

We recognize the continuing economic difficulties at regional and global levels through 2012, but we believe that the economic fundamentals of the Kingdom of Bahrain and other GCC countries are strong, and are supported by active official and civil efforts to maintain the satisfactory growth rates and to continue implementing economic and social development programs.The efforts made by the Bank in addition to the initiatives carried out at all levels will advance the status and profitability of the Bank through the future, and will achieve for it the leadership in Islamic banking industry with the help of God.

Mohammed Isa Al-MutawehMember of the Board of Directors and Chief Executive Office

Chief Executive Officers’ Report (Cont.)

ABIB Annual Report 2011 25

The Bank aspires to the highest standards of ethical conduct by delivering our promise to clients, reporting our financial results accurately and transparently.

Al Baraka Islamic Bank B.S.C (c) 26

Corporate Governance Governance and CompliancePhilosophy, Strategy and objectives

We are committed to safeguarding the interests of our stakeholders and recognize the importance of good corporate governance. The Bank aspires to the highest standards of ethical conduct by delivering our promise to clients, reporting our financial results accurately and transparently and maintaining full compliance with all laws, rules and regulations governing the Bank’s business.

The Bank’s governance and compliance strategies, objectives and structures have been designed to ensure that the Bank complies with legislation and the myriad of codes, while at the same time moving beyond accountability and assurance issues to value creation and resource utilization issues. Internally the function has expanded in five complementary directions, namely:

enterprise-wide corporate governance;

business governance;

corporate accountability and ethics;

sustainability management and reporting; and

Compliance.

The Bank Compliance Unit works closely with Legal, Company Secretary, Risk, and Internal Audit in promoting a culture of good governance and compliance within the Bank. The Bank has taken the necessary steps to continuously enhance its corporate governance to ensure conformity and seeking best practices.

The board adopted written Corporate Governance Policy covering the matters stated in Module HC and other corporate governance matters related to the Board. This policy refers to the principles and rules of Central Bank of Bahrain (CBB) on Corporate Governance for Islamic retail Licensed Institutions - Module HC. The Bank conducts annual detailed self-assessments to ensure compliance with the new requirements and has set specific milestone for implementation of any shortfalls. Continuous review and upgrades to strong corporate governance practices included the Bank’s subsidiary in Pakistan. The Bank’s shareholders, Board of Directors and executive and senior management have been fully apprised of the amendments to

the requirements and the milestones set. Starting from 2011, Corporate Governance was an item on the agenda of the annual shareholder meeting for information and any questions from shareholders regarding the Islamic Bank’s governance.

In November 2011, CBB clarified the definition of independent directors and Executive Directors. The Bank complies substantially with the code. The only areas of non-compliance with the code, which the board is satisfied does not impair the governance integrity or perceptions of it, are indicated below:

1. The majority of the members of the Audit Committee and the Remuneration and Board Affairs Committee are non independents.

2. The Chairman of the Audit Committee is not an independent member.

The Bank plan to fulfill the aforesaid requirements of the Code during the year 2012.

These disclosures should be read in conjunction with the Bank’s consolidated financial statements for the year ended 31 December 2011. To avoid any duplication, information required under CBB Rulebook PD module but already disclosed in other sections of the annual report has not been reproduced in these disclosures.

Governance FrameworkOwnership Structure

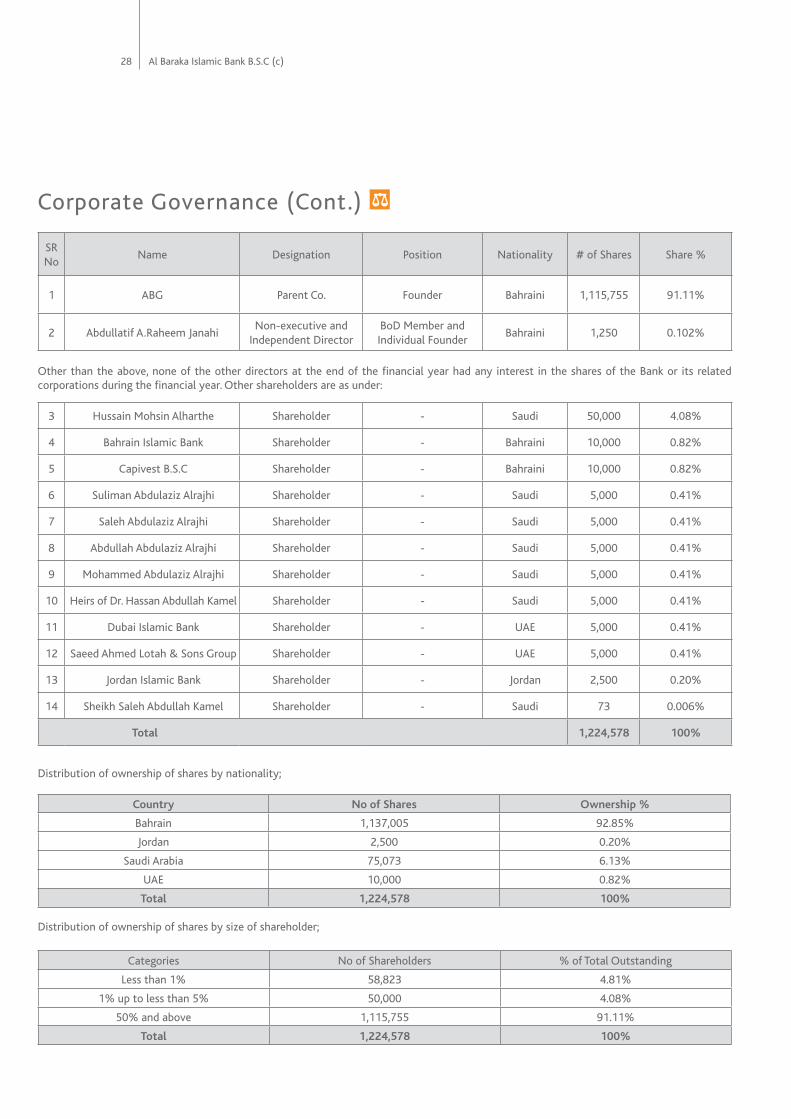

Al Baraka Islamic Bank B.S.C. is a Bahrain-based licensed Islamic retail Bank and operates as a subsidiary of Al Baraka Banking Group. Al Baraka Banking Group (ABG) is the dominating shareholder. The shareholding structure is transparent and the existing share structure consists entirely of Ordinary Shares and there are no different classes of Ordinary Shares. AIB can also confirm that the minority shareholders of the Bank are well represented on the Board of Directors, either directly or through the independent directors.

As at 31st December 2011, distribution schedule of shares, setting out the number and percentage of holders were as the following categories:

ABIB Annual Report 2011 27

SR No

Name Designation Position Nationality # of Shares Share %

1 ABG Parent Co. Founder Bahraini 1,115,755 91.11%

2 Abdullatif A.Raheem Janahi Non-executive and

Independent DirectorBoD Member and Individual Founder

Bahraini 1,250 0.102%

Other than the above, none of the other directors at the end of the financial year had any interest in the shares of the Bank or its related corporations during the financial year. Other shareholders are as under:

3 Hussain Mohsin Alharthe Shareholder - Saudi 50,000 4.08%

4 Bahrain Islamic Bank Shareholder - Bahraini 10,000 0.82%

5 Capivest B.S.C Shareholder - Bahraini 10,000 0.82%

6 Suliman Abdulaziz Alrajhi Shareholder - Saudi 5,000 0.41%

7 Saleh Abdulaziz Alrajhi Shareholder - Saudi 5,000 0.41%

8 Abdullah Abdulaziz Alrajhi Shareholder - Saudi 5,000 0.41%

9 Mohammed Abdulaziz Alrajhi Shareholder - Saudi 5,000 0.41%

10 Heirs of Dr. Hassan Abdullah Kamel Shareholder - Saudi 5,000 0.41%

11 Dubai Islamic Bank Shareholder - UAE 5,000 0.41%

12 Saeed Ahmed Lotah & Sons Group Shareholder - UAE 5,000 0.41%

13 Jordan Islamic Bank Shareholder - Jordan 2,500 0.20%

14 Sheikh Saleh Abdullah Kamel Shareholder - Saudi 73 0.006%

Total 1,224,578 100%

Distribution of ownership of shares by nationality;

Country No of Shares Ownership %

Bahrain 1,137,005 92.85%

Jordan 2,500 0.20%

Saudi Arabia 75,073 6.13%

UAE 10,000 0.82%

Total 1,224,578 100%

Distribution of ownership of shares by size of shareholder;

Categories No of Shareholders % of Total Outstanding

Less than 1% 58,823 4.81%

1% up to less than 5% 50,000 4.08%

50% and above 1,115,755 91.11%

Total 1,224,578 100%

Corporate Governance (Cont.)