Embed Size (px)

Citation preview

Vol. 16 No. 5Copyright 2015 In Touch Today www.intouchtoday.com

What to Do After Paying Off Your Mortgage

Clients For Life

As the oldest millennials begin shopping for houses, many baby boomers are writing their final mortgage payment checks. Although homeowners are still responsible for property taxes and homeowners insurance, the lack of a mortgage payment provides a sudden positive cash flow. But you can’t forget the paperwork. Here are a few steps to take once that final check clears:

(1) Within a month after paying off your mortgage, your bank should send a satisfaction of mortgage statement. If it hasn’t arrived after three or four weeks, call your lender. A mortgage is a lien on the property that guarantees the loan, and the satisfaction of mortgage statement certifies the removal of the lien. This is the last step in the homeownership process.

(2) Ask your lender if they’ve filed the satisfaction of mortgage statement with the county deeds office—if not, you’ll need to do it yourself. (It’s more than likely that your lender will handle it.)

(3) If you paid into an escrow arrangement with your lender that included property taxes and homeowners insurance, you’ll now be taking over those payments yourself. Contact your insurance office

and the local tax authority to arrange for regular delivery of those statements. Additionally, your insurance agent might also be able to recommend a different level of coverage once your mortgage is paid.

(4) Those escrow plans often keep extra funds above and beyond your actual property tax owed. If this is the case, you’ll be receiving a check from your bank in the amount of the remainder. Again, if you haven’t received it within a month, call your bank to ask about it.

(5) Make a plan: Now that you’ve settled your biggest personal expenditure, it’s time to figure out what to do with your jump in disposable income. Talk to a financial planning professional about saving some of that money in a retirement savings vehicle or another investment plan. Two new expenditures for those with lender escrow arrangements are property taxes and homeowners insurance, so you should now calculate those expenses into your budget. It’s good to deposit a fixed amount monthly to prepare for those twice-yearly payments, but you’ve been paying a mortgage for 15 to 30 years—you’re used to allocating your income every month.

Vol. 16 No. 5

Clients For liFe

Orville OriginatorMortgage Officer

Street AddressCity, State 12345

Office: 123-123-1234Toll Free: 123-123-1234Email: [email protected] Originator

#1 Lender

Best way to reach you

Your name

Fax form to: 123-123-1234 Or mail to Company Name, Street Address, City, State 12345

Please send the following information: Current loan programs and available interest rates.

Information on purchasing investment property.

Home improvements that increase property value.

Information on debt consolidation loans.

Ten tips to prepare your home for sale.

Financial planning - strategies to restructure debt, increase equity, pay less interest & increase availability of investment funds.

If you or someone you know is thinking of buying or selling a home, give me a call.

Knowing my clients are informed, at ease and receive the very best service is my top priority.

Shed These Financial Burdens

Carl Sandburg, Pulitzer Prize winner and poet, once wrote, “Money is power, freedom, a cushion, the root of all evil, the sum of blessings.” His analysis was entirely correct, for while money can enable us to better ourselves and achieve our dreams, it’s also a topic many of us worry about relentlessly—regardless of how much or little of it we may have. If this

sounds like you, learning to better manage your finances may help. Consider these very common money-related burdens and the simple suggestions for shedding them.

You worry about paying down debts. Put aside your credit cards for a few months and make the minimum payments on each one as you adjust your budget to free up more cash. Then concentrate on paying off the debt on the card with the highest interest rate as you continue to pay the minimums on the others. When that’s done, move on to the next card.

You worry that your spending is out of control. Build better awareness of where your money goes by writing down every purchase for one month. Then take a look at your diary and identify your spending triggers. For example, maybe you tend to shop for clothes after you cash your paycheck or

spend more on meals when you dine out with friends. Find ways to stick to your budget that address these triggers, such as having your paycheck direct deposited or inviting friends over rather than going out to dinner.

You worry that you’re not saving enough for retirement. If you have not yet done so, open a Roth or traditional IRA. Then have a portion of each paycheck—even if it’s just a small portion—deposited directly into the account. You can also look for ways to make money doing the things you love—such as pet sitting, teaching yoga classes, or taking on freelance work. Put that extra cash into your retirement fund.

Copyright 2014 In Touch Today www.intouchtoday.com

Copyright 2015 In Touch Today www.intouchtoday.com

Many people in their 20s and 30s treat life more or less like a cafeteria, eating whatever’s nearby and

exercising whenever they have time. Life happens! But poor physical fitness is a risk factor for heart failure in aging adults, so if you’re now entering your 40s, or even your 50s, and beginning to think about healthy aging, a new study published in Circulation, the journal of the American Heart Association, has some very good news.

According to the researchers, middle-aged people have a 20-year window between the ages of 40 and 60 to improve their cardiac health. By exercising four to five days per week for two years within this two-decade age window, you can improve your blood vessel elasticity, which reduces your risk of heart disease.

The study included 53 adults between the ages of 45 and 64, who performed one of two exercise protocols over the course of the two-year study. One group consisting of adults with no history of regular exercise performed progressively intensifying aerobics; the second group did yoga and weight training. The aerobics group of previously sedentary adults showed an 18 percent improvement in their maximum oxygen intake, and a 25 percent increase in the elasticity of their blood vessels.

Based on the age ranges of the study participants, the researchers suggest that it doesn’t matter when you do those two years of regular exercise—as long as you do them within the two-year window between 40 and 60. After the age of 70, they note, it’s too late to make a difference in vessel elasticity, although exercise does still confer significant physical advantages at that age. They also note that further research is required owing to the size of the study group and its demographic makeup.

If you’re interested in starting an exercise program, consult your doctor and search for professionally licensed fitness trainers in your area.

First unveiled in October 2016, the Nintendo Switch became the fastest-selling video game console of the current generation. By last Christmas, Nintendo had sold 10 million units. There are a lot of reasons for the company’s home-run success, all of which are built into the core of Nintendo’s design philosophy. The Switch is a handheld-console hybrid that effectively marries two of Nintendo’s competencies. When inserted into a docking station connected to a TV, the Switch is a standard home console unit with two wireless controllers. Unlike any other console on the market, the Switch has an LCD touchscreen and can be removed from the dock for portable gaming. This capitalizes on Nintendo’s longtime dominance in the portable game console category.

The main unit is a battery-powered tablet with a 6.2-inch multi-touch screen and haptic feedback technology. The wireless controllers snap to the sides of the unit for gameplay in mobile configuration. Online services are provided via built-in wi-fi (though the company does not include a web browser). Classic games are available

for purchase and download directly through the Switch console.

The console’s debut was accompanied by the release of flagship game Zelda: Breath of the Wild, a game almost universally

praised for its emphasis on open-world gaming and its highly

polished design. Many critics have described it as one of the best games ever made.

Other hit games in the Switch launch window

included Mario Kart 8 Deluxe, Skyrim and Minecraft.

The console’s status was cemented last October with the release of the bestselling Super Mario Odyssey, another critically acclaimed monster hit that restored glory to a Nintendo bellwether that some critics had considered to be in decline. And the Switch, priced at $299, is the least expensive home console on the market.

Why the Nintendo Switch is the Fastest-Selling Gaming Console

The Mid-life Window for Heart Health

Did you know you have a 96 percent chance of surviving an actual plane crash? Those odds are pretty good, though you should probably still pay attention to the pre-flight safety announcements. Here are a few other facts about flying you might not have known:

● You lose about two cups of waterevery hour spent flying. This contributes to deep-vein thrombosis, an affliction associated with long-haul flights. It’s a good idea to hydrate before, during and after a flight.

● Thelifespansofairlinersaremeasuredby the number of cabin pressurizations. Pressurizing the cabin creates stress on the fuselage, and after about 75,000 pressurizations, planes are retired.

● In 1987, an American Airlinesexecutive saved the company $40,000 by suggesting that the company’s food services remove a single olive from each first-class salad.

● Similarly, when American Airlinesswitched its pilots’ paper manuals to iPads, it saved $1.2 million in fuel costs annually.

● Jet fuel is actually kerosene—eitherunleadedkerosene,knownasJetA-1,oranaptha-keroseneblend,calledJetB.

● TheemergencyradiocallMAYDAYisderived from the French “m’aidez,” which means “help me.”

Little-Known Facts About Air Travel

Be sure to schedule regular eye appointments with your optometrist. Even if you aren’t experiencing any problems with your vision, a comprehensive eye exam can detect even the smallest changes in your eye health, and even other health related issues such as glaucoma and diabetes, before there are any other symptoms. Protect your eyes. When outside, protect your eyes with sunglasses with 100% AVA and AVB protection. Wear protective eyewear when playing sports and working with hazardous or airborne materials at work or home. Maintain a balanced diet. By incorporating foods that are rich in protective nutrients and antioxidants, you can help maintain good eye health. Eat a healthy diet that includes leafy greens, dark pigmented fruits such as blueberries and cherries, salmon, eggs, nuts, beans and other non meat protein sources. Stop Smoking. Smoking can contribute to a higher chance of developing cataracts, macular degeneration, and optic nerve damage. If you have tried to quit before, keep trying. The more times you try to quit, the more likely you are to succeed. Take a break to help eye strain. If you use computers or other digital devices for extended periods of time on a regular basis, you could experience dry eyes, blurry vision, and headaches. Every 20 minutes, rest your eyes by looking 20 feet away for 20 seconds.

Our eyes provide us with one of our most treasured senses. Follow these easy tips to ensure you are taking care of your eyes properly.

Sure, you might have chairs or even outdoor couches on your porch, but have you considered a hanging chair? There are tons of options available, to meet your space and size needs. Don’t forget to add comfy pillows. If you have the space, think about setting up a projector to watch films on a wall and host an outdoor movie night. Colorful throws and pillows can make your space inviting and comfortable. Have a craving for s’mores? Set aside an afternoon and DIY a firepit with curved paving stones that don’t require any mortar and you’ll be toasting marshmallows in no time. Having a large deck or patio means you can set up zones for dining and for lounging. Use a water resistant outdoor rug to help keep your spaces defined while adding some texture. Breezy white, sheer curtain panels attached to the ceiling of your porch can create a shady spot to spend some time. You can pull them closed to create some privacy or tie them back to create an open, but still polished area. Keep a wheeled cart stocked with drink essentials, such as straws, napkins, and cups, and you’ll be ready to host an impromptu happy hour.

l

l

l

l

l

l

With summer right around the corner, these ideas will help you create the best outdoor space to enjoy.

Porch and Patio Ideas

Vol. 16 No.5

1. Preheat oven to 400°. In a large skillet, bring 1 in. of water to a boil; add asparagus. Cook, covered, until crisp-tender, 3-5 minutes. Drain and pat dry.

2. Onalightlyflouredsurface,rollpastrysheetintoa16x12-in.rectangle. Transfer to a parchment paper-lined large baking sheet. Bake until golden brown, about 10 minutes.

3. Sprinkle 1-1/2 cups cheese over pastry to within 1/2-in. of edges. Placeasparagusovertop;sprinklewithremainingcheese.Mixremainingingredients; drizzle over top. Bake until cheese is melted, 10-15 minutes. Serve warm.

Directions

Prep Time: 15 minutesBake Time: 20 minutesServings:16 1 pound fresh asparagus, trimmed

1 sheet frozen puff pastry, thawed 2 cups shredded fontina cheese1 teaspoon grated lemon zest

2 tablespoons lemon juice1 tablespoon olive oil¼ teaspoon salt ¼ teaspoon pepper

Fontina Asparagus Tart

Ingredients

Copyright 2015 In Touch Today www.intouchtoday.com

INTOUCHTODAYCORPORATIONANDITS LICENSORS.Allrightsreserved.Reproductionsinanyform,inpartorinwhole,areprohibitedwithoutpermission.Thisnewsletterisforinformationpurposesonly.Theinformationcontainedherein may not be wholly or at all applicable to every situation or jurisdiction. We strongly urge you to consult your professional advisor prior to acting upon information contained herein. Links to websites within this newsletter can not be guaranteed to be active. This newsletter is not an attempt to solicit other brokers’ or originators’ clients. Please disregard this information if you currently have a professional affiliation.

PLEASE RECYCLE Printed on recycled paper.

Copyright 2015 In Touch Today www.intouchtoday.com

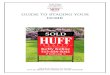

Um… Should We Be Saving More Like Millennials?The pundit class likes to flog millennials for their supposed narcissism, smartphone addiction and their lack of financial savvy. This smacks of unfair stereotyping, and according to a recent survey from Bank of America, at least one of those assumptions is actually dead wrong—millennials are fantastic at saving money. In fact, the survey says that one in six millennials has at least $100,000 in savings. Compare this to the 57 percent of people nationally who have less than $1,000 saved.

Half of the survey participants were millennials between the ages of 23 to 37. One in six of the millennial participants reported that their total savings including bank accounts, investment accounts and retirement plans was $100,000 or greater.

Over the five years that Bank of America has conducted the survey, the number of millennials reporting $15,000 in savings made a big jump. One expert believes that the savings habits of this demographic have been strongly shaped by factors including the financial collapse in 2007, underemployment and the burden of high student loan payments. As a result, they’re approaching their finances with much more discipline than their parents.

So yes, we should all definitely be saving more like millennials.

But there are a few caveats: According to the survey, a lack of trust in the markets compels millennials to stow money in savings vehicles instead of investments. They are far more likely than Gen-Xers to have savings accounts instead of 401Ks. And other surveys have found much lower rates of saving among this demographic. But the Bank of America survey is revised annually, so future installments might yield more clarity.

IN TOUCH TODAY CORPORATION AND ITS LICENSORS. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without permission. This newsletter is for information purposes only. The information contained herein may not be wholly or at all applicable to every situation or jurisdiction. We strongly urge you to consult your professional advisor prior to acting upon information contained herein. Links to websites within this newsletter can not be guaranteed to be active. This newsletter is not an attempt to solicit other brokers’ or originators’ clients. Please disregard this information if you currently have a professional affiliation.

PLEASE RECYCLE Printed on recycled paper.

Clients For liFe

Orville OriginatorMortgage Officer

Street AddressCity, State 12345

Office: 123-123-1234Toll Free: 123-123-1234Email: [email protected] Originator

#1 Lender

Best way to reach you

Your name

Fax form to: 123-123-1234 Or mail to Company Name, Street Address, City, State 12345

Please send the following information: Current loan programs and available interest rates.

Information on purchasing investment property.

Home improvements that increase property value.

Information on debt consolidation loans.

Ten tips to prepare your home for sale.

Financial planning - strategies to restructure debt, increase equity, pay less interest & increase availability of investment funds.

If you or someone you know is thinking of buying or selling a home, give me a call.

Knowing my clients are informed, at ease and receive the very best service is my top priority.

Copyright 2014 In Touch Today www.intouchtoday.com

Don't Forget the Garage When Selling Your Home

It’s common knowledge that selling a home for the best price possible requires careful preparation. The inside must appear clean and inviting, and the landscaping and exterior

must be equally appealing. What many homeowners forget, however, is the need to ensure the garage looks fantastic as well. Some buyers consider it an important amenity when choosing a new home, so investing the time necessary to make sure your garage shines can be well worth the effort.

Remove as much ‘stuff’ as possible. When you gather items you no longer need from the rest of your home, tackle discards in the garage as well. Donate them to charity or hold a yard sale. Then take things you won’t be using while your home is on the market (your lawn mower and bicycles in winter or your snow blower and shovels in summer, for example) and put them in storage to open up space.

Get everything up off the floor. If your garage does not already have them, add hooks and shelves. Heavy-duty hooks are perfect for large items like bicycles and sawhorses. Smaller hooks easily hold gardening and maintenance tools. And shelves

are essential for the neat and tidy storage of other items.

Give the interior a thorough cleaning. Dust the walls and corners to eliminate all spider webs. Vacuum the floor to remove loose dirt and debris. If you have oil stains on the concrete, try removing them with paint thinner or liquid bleach.

Paint the garage door. If it’s in good shape, a quick cleaning with soap and water may be all that’s needed to spruce it up. If it’s worn or scratched, a fresh coat of paint will make a big difference in its appearance.

![[PPT]What is t,n,m staging and summary staging? Staging for... · Web viewWhat are we discussing? What is AJCC Staging Purpose of staging General rules for clinical and pathological](https://img.pdfslide.us/doc/110x75/5b1cc7cc7f8b9a8c5a8ba42e/pptwhat-is-tnm-staging-and-summary-staging-staging-for-web-viewwhat.jpg)