Embed Size (px)

Citation preview

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 Page 1

BEST PRACTICE MANUAL For ATM BUSINESS EFFICIENCY

(Introducing TALOS, the Total ATM Lifecycle

Operational Solution for ATMs)

International recommendations & guidelines

Produced by G. Mckay ATMIA

© 2006 ATM Industry Association. All rights reserved.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 Page 2

Contents Page

1. Foreword 3

2. Chapter 1 – Definition of ATM Lifecycle Operational Solution 4

3. Chapter 2 – Key Cost Drivers and Profit Drivers 8

4. Chapter 3 – Cost saving Strategies 10

5. Chapter 4 – Cash Cycle and Cash Management 11

6. Chapter 5 – Technical service monitoring Efficiencies 15

7. Chapter 6 – Adding Revenue through Marketing Media 19

8. Chapter 7 - ATM Outsourcing Business Model 29

9. Chapter 8- ISO/IAD Business Model 41

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 Page 3

Foreword

Today’s installed ATM base is in excess of 1.5 million ATM’s. Research has shown that each ATM will cost between $7.5k - $25k per annum to operate. If we assume an average of $15k/ATM then approximately $22.5billion is spent each year supporting the ATM operations, and assuming a ten year ATM life cycle, this leads to a staggering $225billion spent during the ATM Operational life cycle. This document sets out to review the factors impacting life cycle costs, and areas which may be addressed in order to improve business efficiency and cost saving for the overall benefit of the ATM Industry. Initially 5 areas will be provided for analysis, but it is anticipated that the complete life cycle analysis will be subject to continuous update as both technology, and service support management systems, are introduced. The five areas to be addressed are :-

1. Key Cost Drivers and Profit Drivers 2. Cash Cycle and Cash Management 3. Technical Service Monitoring Efficiencies 4. ATM Outsourcing Business Model 5. The ISO Business Model

The document takes advantage of current knowledge of “ATM Cost Efficiency” systems, technologies, and business processes. It is anticipated that the document will be subject to review change as further industry inputs are obtained. www.atmia.com Graham McKay Executive Director ATMIA Europe February 2006

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 Page 4

Chapter 1

Definition of the Total ATM Lifecycle Operational Solution (TALOS)

1.1 ATM Lifecycle

The full life cycle for an ATM commences with Research & Development, leading to Design & Manufacture. The ATM then enters the Operational phase of the lifecycle, normally extending to 10 years of use, before being subject to an equipment renewal phase which either leads to the ATM being disposed of, or refurbished for third world use. The figure below provides an end to end assessment of the overall ATM lifecycle, which identifies the key factors of “feedback” in order to ensure that the manufacturing research and development budgets are used to best effect in providing product that the customer requires. The customer “Business Unit Group” provides the essential elements of future self service strategy and functionality requirements, together with the IT unit who should provide input for the future development direction of the technology platform. Finally the Operations Group should provide input on the service operability and interfaces in order to maximise CIT efficiencies.

It is critical to obtain constructive customer and operational feedback for research & development in order to create both cost and business efficiencies, particularly in terms of :-

• Design for reliability of main components • Design for ease of Manufacture and cost reduction • Design for simplicity of Service • Design for functionality flexibility

The above can only be of value as input to the next generation Self Service equipment as it is introduced into operational service, and therefore cannot impact the current installed base, except for potential module upgrades. Therefore for the initial document, focus will be maintained on the current and recently installed ATM base in order to assess potential savings in the immediate future.

ATM

IA -

TALO

S T

otal

ATM

Life

cycle

Ope

ratio

nal S

olut

ions

1st I

ssue

20th

Feb

200

6

Page

6

Star

t Ope

ratio

nal L

ife

Cyc

le

Sale

s &

Pu

rcha

se

Cyc

le

MA

NU

FAC

TUR

E2n

dLi

ne S

ervi

ce

OPE

RA

TIO

NA

L M

AN

AG

EMEN

T C

YCLE

DES

IGN

1stLi

ne S

ervi

ceH

/W &

S/W

Man

agem

ent

EQU

IPM

ENT

R

ENEW

AL

–Mar

ket r

esea

rch

&

cust

omer

feed

back

–Ide

ntifi

catio

n of

cr

itica

l are

as–D

efin

e se

rvic

e st

rate

gy

–Def

ine

desi

gn

stra

tegy

–Bac

kwar

d co

mpa

tibili

ty–I

nter

face

st

anda

rdis

atio

n–M

odul

ar

upgr

adab

ility

–Des

ign

in re

liabi

lity

–Fie

ld fe

edba

ck o

n m

odul

e re

liabi

lity

–Rev

iew

com

pone

nt

supp

lier r

elia

bilit

y pr

oces

s–D

esig

n fo

r m

anuf

actu

re–F

unct

iona

lity

rese

arch

–Man

ual v

sm

echa

nise

d as

sem

bly

–Low

pric

e lo

catio

n vs

setu

p &

trai

ning

cos

ts–S

tand

ardi

satio

n of

m

odul

es–D

efin

e Se

rvic

e po

licy

and

acc

essa

bilit

y–D

efin

e so

ftwar

e pr

edic

tive

mai

nten

ance

Se

rvic

es–D

efin

e Pa

rtner

s–C

ompl

ianc

e w

ith k

ey

test

stan

dard

s &

com

plia

nces

–Mod

ular

Opt

ions

–Ris

k A

naly

sis

–Pric

ing

Rev

iew

–Com

mer

cial

Rev

iew

–Shi

ppin

g C

osts

–Cus

tom

s & T

ax–C

ost o

f Sal

es &

M

arke

ting

–Tec

hnol

ogy

eval

uatio

n u

nits

–Ins

talla

tion

Cos

ts–C

ost o

f upg

rade

s–L

ife c

ycle

cos

t–P

rice

Neg

otia

tion

–SLA

Neg

otia

tion

–Par

ts su

ppor

t co

sts (

1st &

2nd

line)

–Res

ourc

e id

entif

icat

ion

–Tra

nsiti

on

Plan

ning

–Con

tract

Sig

ned

–ATM

Ser

vice

M

onito

ring

–Pre

dict

ive

mai

nten

ance

–Res

pons

e M

anag

emen

t and

pa

rts lo

gist

ics

–Int

erna

l Con

tract

M

anag

emen

t –P

refe

rred

Par

tner

C

ontra

cts

–Sub

Con

tract

M

anag

emen

t–T

echn

olog

y R

efre

sh P

lan

–Tec

hnol

ogy

Upg

rade

–Sup

port

Syst

ems

Impl

emen

tatio

n–R

evie

w In

tern

al

proc

edur

es–R

evie

w E

xter

nal

–pro

cedu

res

–Cas

h O

ptim

isat

ion

–ATM

Ser

vice

M

onito

ring

–C

ontra

ct

Man

agem

ent

–Iim

prov

emen

tpr

oces

s–C

ontra

ct

Adm

inis

tratio

n an

d E

xecu

tion

–Con

tract

type

-Pe

r Cal

lout

-Ann

ual f

ixed

fe

e–O

utso

urci

ng–R

evie

w

Bus

ines

s Uni

t re

quire

men

ts–R

evie

w

Tech

nica

l re

quire

men

ts–R

evie

w

Cus

tom

er

rela

tions

hip

–Con

firm

co

ntra

ct st

atus

–R

evie

w a

reas

of

con

tract

ch

ange

–Rev

iew

ove

rall

RO

I–A

sses

s ch

ange

s re

quire

d–R

evie

w

Cus

tom

er

Stra

tegi

c di

rect

ion

–Ini

tiate

C

usto

mer

D

iscu

ssio

ns–C

onfir

m

revi

sed

pric

ing

and

Con

tract

co

nditi

ons

TALO

S -

Tota

l ATM

Life

-Cyc

le O

pera

tiona

l Sol

utio

ns

–ATM

Ser

vice

M

onito

ring

–Con

firm

de

liver

y v

s pl

an–R

evie

w S

LA

failu

re a

nd

qual

ity

perf

orm

ance

–Con

firm

su

ppor

t ef

fect

iven

ess

–Mon

itor s

ub-

cont

ract

s–E

stab

lish

Pe

nalti

es,

Proc

ess &

Pr

oced

ures

–Rev

iew

In

tern

al

proc

edur

es–R

evie

w

exte

rnal

pr

oced

ures

–Mul

ti-fu

nctio

n op

erat

iona

l so

ftwar

e–S

oftw

are

stan

dard

isat

ion

–Cas

h op

timis

atio

n–A

TM

perf

orm

ance

m

onito

ring

–Opt

imis

e pe

rfor

man

ce–C

onfir

m

Perf

orm

ance

vs

Req

uire

men

ts–R

evie

w a

ny

spec

ial c

ontra

ct

requ

irem

ents

–Ide

ntif

y eq

uipm

ent

flexi

bilit

y–R

evie

w o

vera

ll ef

ficie

ncy

and

prof

it m

argi

ns

End

Ope

ratio

nal

Life

Cyc

le

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 7

In order to provide positive impact of the existing installed base, the “Operational Lifecycle” is the area of prime interest, and will therefore be the defined “lifecycle” referenced in this document. In that context the figure below identifies those aspects which will be addressed in more detail in further chapters. A summary of items under key headings which, after investigation, can provide genuine cost savings are provided as support to the “Total ATM Lifecycle Operational Solution” (TALOS).

Start Operational Life Cycle

2nd Line Service

OPERATIONAL MANAGEMENT CYCLE

1st Line Service Hardware & Software

Management

–ATM Service Monitoring –Predictive maintenance –Response Management

and parts logistics –Internal Contract

Management –Preferred Partner

Contracts –Sub Contract Management –Technology Refresh Plan –Technology Upgrade –Support Systems

Implementation –Review Internal

procedures –Review External –procedures

–Cash Optimisation –ATM Service

Monitoring – Contract Management –Iimprovement process –Contract

Administration and Execution

–Contract type - Per Callout - Annual fixed fee –Outsourcing –Review Business Unit

requirements –Review Technical

requirements –Review Customer

relationship

–ATM Service Monitoring –Confirm delivery vs plan –Review SLA failure and

quality performance –Confirm support

effectiveness –Monitor sub- contracts –Establish Penalties,

Process & Procedures –Review Internal

procedures –Review external

procedures

–Multi-function operational

software –Software standardisation –Cash optimisation –ATM performance

monitoring –Optimise performance –Confirm Performance vs

Requirements –Review any special

contract requirements –Identify equipment

flexibility –Review overall efficiency

and profit margins

End Operational Life Cycle

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 8

Chapter 2

Key Cost Drivers and Profit Drivers

2.1 General The following “cost wheel” has been used to show the areas of annual expense related to an installed ATM. The percentages given are based upon generic research across USA, Europe, Africa and Asia. It is recognised that there will be variations from country to country, and between geographic regions due to differences in labour rates, tax & duty, local regulations, security, and management/contract efficiencies. This document will not set out to confirm values, but merely accept that they represent areas for cost reduction and business improvement.

Occupancy13%

Communications9%

Central Services15%

Depreciation11%Security

2%

User Maint10%

Consumable2%

H/W Maint9%

Cash Provision8%

Cost of Cash9%

Interest on Cash9%

Insurance3%

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 9

2.2 Cost Wheel Description of Elements For clarification each of the main cost elements defined are expanded below, and were appropriate costs include the internal administration, contract management, and personnel costs.

Table 1

1. INSURANCE For banks this is often internal self insurance, but of increasing cost for off premise ATM’s due to increased security risk.

2. INTEREST ON CASH The loss of interest which could be accumulated if the cash in the ATM was available for overnight investment

3. COST OF CASH The cost of purchasing cash from the National Bank, and holding for delivery direct to an ATM or via a Branch to an ATM

4. CASH PROVISION The cost and management of the CIT delivery of cash, emergency cash delivery, and collection/reconciliation of excess cash from the ATM

5. HARDWARE MAINTENANCE The cost and management of the ATM SLA hardware/software maintenance contract, the supply of parts and ATM upgrades.

6. CONSUMABLES The cost, management and supply of consumables for the ATM receipt, journal and statement printers

7. USER MAINTENANCE The cost of user 1st line servicing covering card retrieval, card jams, note jams and general area accessibility/cleanliness

8. SECURITY Cost of on-going security both in terms of CCTV monitoring/tape auditing, alarm contracts management, and regular visual inspections

9. DEPRECIATION The initial cost of the ATM, site inspection, site preparation, and installation cost, over a set period (typically 7 years)

10. CENTRAL SERVICES Includes all related costs for IT management, data security, network costs, central processing, and technology upgrades.

11. COMMUNICATION Cost of management and related telephone, virtual private network, and associated driver/routing equipment.

12. OCCUPANCY Apportioned rental cost for ATM installation area and service maintenance area. Additionally, in a banking or retail environment, the potential loss of “sales” area for other products.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 10

Chapter 3 Cost Saving Strategies

Based upon the ATM Annual Cost Wheel, and Table 1 above, items will be grouped for ease of review and assessment into the following areas :-

• Cash cycle cost saving – items 2,3 and 4 of Table 1 • Maintenance Cost saving – items 5,6 and 7 of Table 1 • ATM revenue generation – item 12 of Table 1 • Outsourcing of risk for Security, Depreciation, and Insurance – items 8, 9,

and 1 of Table 1 • Outsourcing of risk and technology – items 10, and 11 of Table 1

Five Elements of ATM Cost saving

Cost of Cash Cost of Delivery

& Loss of Interest

Hardware Maintenance Consumables

And User Maintenance

Security

Depreciation & Insurance

Central Services

and Communications

Occupancy and

Rental Costs and Income

Generation

Overall ATM Cost

Efficiency

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 11

Chapter 4 Cash Cycle and Cash Management

4.1 Introduction

Cash Optimisation can be used to minimize the cash in the both the Branch and ATM estate. This has the benefits of reducing the cost of cash and providing predictive information for the more effective and efficient delivery of cash. Additionally, if regulation allows, the accurate knowledge of cash in the ATM may allow this to be treated as “distributed vault” cash and therefore available to gain interest on overnight investment markets.

4.2 Predictive Cash Management:

This is a software solution which is now available offering sophisticated analysis of Cash in the complete Cash Cycle. Traditionally cash is addressed in three main areas, the Vault Cash, the Branch Cash and the ATM Cash. Within each area, there is duplication of inventory management by the Bank Cash Centre, the Bank Branch, and the ATM.

In a traditionally conservative environment, it is typical for each area to over order cash, which when amplified by the number of branches and the number of ATM’s, means that the Bank carries significant excess cash which is costing money.

It has been shown in the USA that cost savings at Branch level can be achieved up $3000 - $10,000 per year , and at ATM level of $2000 per year. For a typical bank of 1000 ATM’s and 200 Branches the implementation of a Cash Optimisation solution could realize around $3billion !

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 12

Cash management & optimisation …… improve your business & save you money

Cash Inventory

Transport

Service Providers/Vendors

Balance & Reconciliation

Technology

Communications

Product Strategy

Customer Interaction

Cash Inventory

Transport

Service Providers/Vendors

Balance & Reconciliation

Technology

Communications

Product Strategy

Customer Interaction

Cash InventoryTransport

Service Providers/Vendors

Balance & Reconciliation

Technology

Communications

Product Strategy

Customer Interaction

Branch ATM Vault

The potential savings available by integrating the management of branches, ATMs & vaults, has been under-exploited

The current approach

The end to end Cash cycle can be addressed from the point at which Cash is issued at the ATM, to the Branch were Cash is held, and then through to a central vault or Cash Centre. With the introduction of Cash deposit and cash recycling ATM’s the necessity to introduce cash flow predictions is of increasing importance to the overall efficiency of the cash cycle.

4.3 ATM Cash

Accurate statistical analysis of cash usage (transaction level), coupled with historical information relating to cash flow peaks, events, holiday periods, response times, will ensure that the statistical analysis can provide accurate information relating to both the overnight cash held at each ATM (distributed vault cash), and the anticipated refill amount and time.

If local regulations allow then a percentage of the cash held in ATM’s can be used as if it were part of the Bank vault cash for overnight investment and interest.

By forward predicting the refill amount & date, information can be provided in advance to CIT contractors to assist in improving the efficiency of route planning, and negate “cash out” situations. Both factors if integrated with the CIT contract, can be used to potentially reduce costs.

Were ATM’s are refilled on site by Bank staff, then the predictive elements of refill date and amount assist Branch staff in knowing the amount of cash to be held and when it will be required.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 13

The additional benefits include accuracy in reducing unused cash, which then requires reconciliation, and cash recycling. Systems can provide optimal order recommendations and should the anticipated demand for cash prior to the next scheduled delivery exceed the current balance, the system should issue a pre-emptive alert. Advance knowledge of a potential shortage provides the opportunity to handle the situation in a non-emergency fashion and outside of peak transaction periods. The systems offer ‘self learning’ logarithmic software which predicts demand for currency at each ATM or Teller position on an individual basis by applying sophisticated mathematical algorithms to historical, event and cost data.

The major advantages of the system ensure that an ATM ‘out of service’ due to lack of cash does not occur, the amount of cash held by the bank at cash points is accurately predicted (overnight short term loans), and the level of cash required to be held at the back office vault can be significantly reduced. Thereby enabling significant cost savings, and improvements in efficiency.

4.5 Branch Cash

It is typical that Branch managers never wish to be in a position of “low” cash, and therefore the trend has been shown to be one of “over” cash. This over cash situation has been shown in the US to cost typically $3000 per month per Branch in increased interest charge.

While any branch Manager should have the ability to override any Cash Predictions because of his local knowledge, and changing circumstances, it is important to provide the best technical tools available to assist his decision.

Most of the factors identified for ATM Cash flow cost savings apply also to the Branch with the additional input of “deposit” cash which is provided directly to the Branch office either via Teller or Cash Deposit ATM’s.

4.6 Cash Vault/Cash Centre

The cash vault/cash centre becomes the point at which Branch cash ordering is consolidated for purchase and delivery of cash. The ability to accurately predict cash usage, ensures that over-ordering or under-ordering are reduced and finally eliminated, therefore significantly reducing the “cost” of cash and delivery. The end to end cash management also provides information regarding Branches which are cash positive, cash neutral or cash negative. For cash positive branches, an improvement in collection and cash recycling reduces exposure and cost of cash

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 14

Functional components in detail …

ForecastingTime/Inventory monitoringPre-emptive alertingCost OptimizingRecommendation AutomationATM and Branch AnalyzingBranch Staff InterfacingCost DeterminationCost BalancingTransportation Cost TrackingOrder IssuingDenomination HandlingEmergency Order HandlingActual Delivery Tracking

History ComparingTrend DeterminationEvent ManagingSeason OverlayingData LoadingData Analysis and ExcludingCarrier ReportingVault ReportingGeneral ReportingWhat-If SimulationPerformance MeasurementExternal Database SynchronizationData Exporting toOther Applications

In summary a Cash Management solution should provides the following information: -

• Dynamic Forecasting

• Pre-emptive Cash out Prediction

• Availability Optimisation

• Cost Minimisation

• Cash in transit Scheduling/Interfacing

• Performance Measurement

• “What if” Simulation

• Extensive Reporting Facility

• Vault/Cash Centre, Branch and ATM/Teller Cash Management

• Secure Audit trail

• On line Cash balance analysis

• Multiple currency capability

• Secure Ordering on line & reports

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 15

Chapter 5 Technical Service Monitoring

Efficiencies 5.1 Introduction Most of the current generation of ATM’s, have sophisticated diagnostic capability, and in most cases this has intellectually proprietary protection for use with an authorized engineers “key” or access code. Much research and development funding is applied to this diagnostic ability in order to assist the manufacturer in providing additional service maintenance benefit. In many cases up to 2000 status event codes are generated, which provide detailed information on the component/module and cause of a fault condition. Additionally, latest generation ATM’s include information relating to “predictive” maintenance, providing advance warning to the service engineer of components/modules requiring maintenance prior to failure. The status event codes can either be available independently, or form part of the transaction message, transmitted to the host and are therefore available for interpretation to assist in call analysis and “first time fix”. When sent as part of the transaction message, all too often these codes are “stripped” out at the customers front end processor, as they are not relevant to the transaction. Occasionally the status information is passed to a Call management system for filtering, but due to the lack of sophistication the status is only diagnosed in simplistic categories, leaving diagnosis to a service engineer on call out. By introducing a system which extracted the full status event codes, and analyzing these using the manufacturer’s diagnostic software, then precise information can be supplied on the fault and component required to ensure a first time fix. • An Event Status System is an ATM monitoring system that automates the

identification, notification and corrective action of ATM abnormalities and supplies conditions

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 16

• The system should receive, analyse, and respond to event status messages sent by an ATM

• If implemented the system should assist customers to improve equipment

availability. • The system should have a flexible rules engine to define the proper

notification, escalation and corrective action for each status generated by the ATM

• Notification Techniques should Include:

– Pager with text capability/GSM – Fax – Interactive Voice Response – E-Mail – Electronic Dispatch

Comprehensive Management Reports in order to provide Performance and Uptime Statistics of the ATM Network and Service provider

FAXFAX

Direct CallDirect CallTo ServiceTo Service

Page/GSMPage/GSMTo ServiceTo Service

ElectronicElectronicDispatchDispatch

Device

Status

Device

Status

Messa

ge Gen

erated

Messa

ge Gen

erated

ATM NetworkATM Network

Call Acknowledged andEvent reportIs Updated

Problem Resolved and Event IsClosed

RULES ENGINERULES ENGINE

Analyzes situation andAnalyzes situation anddetermines actiondetermines action

Device Device Status Status MessageMessage

NotifyNotify

OnSite

Host ATMHost ATMProcessing SystemProcessing System

InterB oldi Series

InterB oldi Ser ies

InterB oldi Ser ies

Open or Log

Event

Central ATM Central ATM Event AnalysisEvent Analysis

ReportsReports

CommunicationsMonitoring

System

Using the above communications concept, Status messages are forwarded directly from the ATM and do NOT interrupt the transaction processing. An alternative using the existing network connection is given below, which has the advantage of No additional communications costs, but may require customer front end processor changes to ensure that all status messages are correctly made available.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 17

Network ConnectionWill Require IP Networking in Place

Authorization

InterB oldi Ser ies

InterB oldi Ser ies

InterB oldi Ser ies

ATM Network

Status messages are forwarded directly from Network

Status messages may be diluted/filtered at FEP

May require customer to make front end changes to their host system

Does Not interrupt transaction processing

TCP_IP

Event Management

Centre

Tran

sact

ion

and

Stat

us m

essa

ges

CSE Dispatched

for service

If the ATM has a “dial up” communication instead of a direct communication or VPN (virtual private network), then ATM’s can either, share same phone line as transaction processing line, or if not then it would require a second phone line. This will Not interrupt transaction processing, and will not require network re-certification. 5.2 Summary The addition of a Status Management System, capable of analyzing all the ATM status codes will provide business efficiency and cost-saving based on :-

• Improvement in ATM availability by immediate notification and quick resolution of ATM problems

• Reduction in operational costs by automating the notification, follow-up and escalation of ATM problems

• Confidence to Operations Management that no problem will occur unnoticed or uncorrected within a defined set of parameters

• More Accurate Failure Analysis • Faster First Time Fix • Reduced Downtime • Increased ATM Revenue • Escalation Procedure Virtually Eliminates Lost/Ignored Fault or repeat

fault conditions • Historical Data and Management Reports Help Pinpoint Problem Areas • Enables the control centre to dispatch to the right person with the right

parts

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 18

By introducing effective and pro-active monitoring then clearly both the speed of repair (first time fix) is improved together with predictive maintenance, will improve ATM availability and provide greater uptime for increased transactions. The next thought phase of Hardware maintenance contracts, will be to use the integrated monitoring between Customer & Contractor in order to move towards a “call out” contract dictated by number of transactions/ATM and predictive maintenance, rather than the traditional fixed price per annum. This would follow the format of Cash in Transit contracts which in conjunction with the “cash optimization” software would lead to a more efficient “call out” contract based on ATM transactions (cash used) and predictive refill.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 19

Chapter 6 Adding Revenue through Marketing

Media

6.1 Introduction

Included in the annual cost of an ATM is an element of “Occupancy” cost based upon an apportioned rental cost for ATM installation area and service maintenance area. Additionally, in a banking, or retail environment, this would also include the potential loss of “sales” area for other products. Until recently the idea of including “positive marketing” at the ATM was not accepted due to interference on the network, (bandwidth limitations), and the ATM processor only having the ability to accept static screen downloads. To implement screen downloads was costly and time consuming as each ATM had to be taken out of service for a service engineer to download information using discs, re-programme, and reboot. As a result of the significant improvements in both ATM and Network technologies, processing capacity/speed and network bandwidth, the system has the capacity available for other functions, which enables remote downloads, and compressed video to be used on the ATM screens. These factors coupled with the desire of Network providers for increased revenue, and the internal and external advertisers desire to exploit new methods for market messaging, has led to increased interest in the ATM screen (and significantly effective pilot installations). The internet and mobile phone are prime targets, but the ATM gives a guaranteed time availability to a known audience who have spending power, earnings, and a requirement for potentially all other financial services (investment, insurance, mortgage etc). From an internal perspective, ATM screen advertising is one cornerstone of customer “Account Aggregation”, which may be coupled with CRM and supportive marketing messages.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 20

Independent research in UK on recent ATM screen advertising has indicated that:-

• 96% of customers are satisfied using an ATM running advertising • 44% of customers would like to see vouchers for the campaign on

their receipt • One in four customers are likely to buy the product being promoted

as a result of seeing the ATM advertising In addition for a bank, the use of screen advertising for internal marketing enables :-

• Bank to extend marketing reach and Branding • Cross sell products and Services • Generate revenue from the channel • Apply a multi-channel strategy

For external advertising channels the ATM represents :- • A unique customer one to one opportunity • Identifiable customer base • An ability to segment • A highly accountable marketing channel.

6.2 Implementation The introduction of marketing internal products using the ATM becomes an internal technology update coupled with a specialised agency, knowledgeable on the effectiveness and timing of “burst” screen material, the duration and refresh cycle, in order to gain maximum impact. Advertising of external agency products involves two critical additional factors.

- The first is based upon the products to be advertised - are they in keeping with bank policies, brand image, and ethics. How much control does the ATM owner wish to have over the adverts to be displayed, and how much does the advertiser wish to be constrained by the ATM owner’s approval mechanism?

- The second is based on the knowledge and ability of the ATM owner to find and interface with appropriate advertisers, and to understand the commercial rationale which will improve advertising revenue. Specialist organisations are now available that are capable of dealing with both issues

6.3 The Business of ATM Advertising One of the ways which both financial institutions and ISO’s have tried to add value and revenue to their ATM estates is through the process of selling advertising space on the ATM. This is not a new idea; it has been tried and implemented in pilot or restricted format in many countries around the world.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 21

Initially, many financial institutions have advertised their own products in an attempt to increase the market penetration of their products, however, more recently there has been a shift by major financial institutions towards 3rd Party advertising on the “off-site” ATMs they deploy. Independent analysts have tested the acceptability of the concept in the US with the following results:

1. 80% of users recalled seeing advertisements on the ATM screen 2. 81% of users felt their ATM experience was the same or better than

previous transactions. 3. The majority of users felt their ATM transaction took the same or less

time than usual

Until recently there have been a number of constraints facing the innovative deployers wishing to implement full motion ATM advertising. These constraints have been both technical and business related. It is an undisputed fact that until recently ATM’s were only capable of displaying static, single page adverts. While this proved useful in displaying product and service information to customers it is not a medium that is highly attractive to 3rd party advertisers. The main reason for this is that the recall of consumers to static advertising is greatly below that of full audio-visual adverts. Thus the technical requirement of an advertising partner is the ability to display digital audio-visual clips, such as MPEG, on the ATM screen. Beyond that the deployer must be able to deliver to the ATM on a regular basis, often weekly, new media clips or “shows” for playback in the ATM. Bandwidth limitations have been a barrier to the distribution of ATM adverts, however, there is a case for using the advertising revenue generation as one of the key factors in cost-justifying the upgrade and enhancement of the ATM network to support media distribution. Software now also exists to manage the distribution of that media to individual ATMs on the network.

The net result is that the technology barriers to full multi-media advertising on ATMs have rapidly fallen in the last 2 years. Infrastructure can now be put more cost effectively in place to support 3rd party ATM advertising. However, technology is only one of the barriers faced by deployers wishing to place adverts on their ATM estate. What the bank must deliver is an available network of ATMs, spread across

multiple sector types, located roughly in-line with the geographic spread of

the regional population but with the majority based at the most attractive

off-site and on-site locations close to the consumers “point of purchase”.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 22

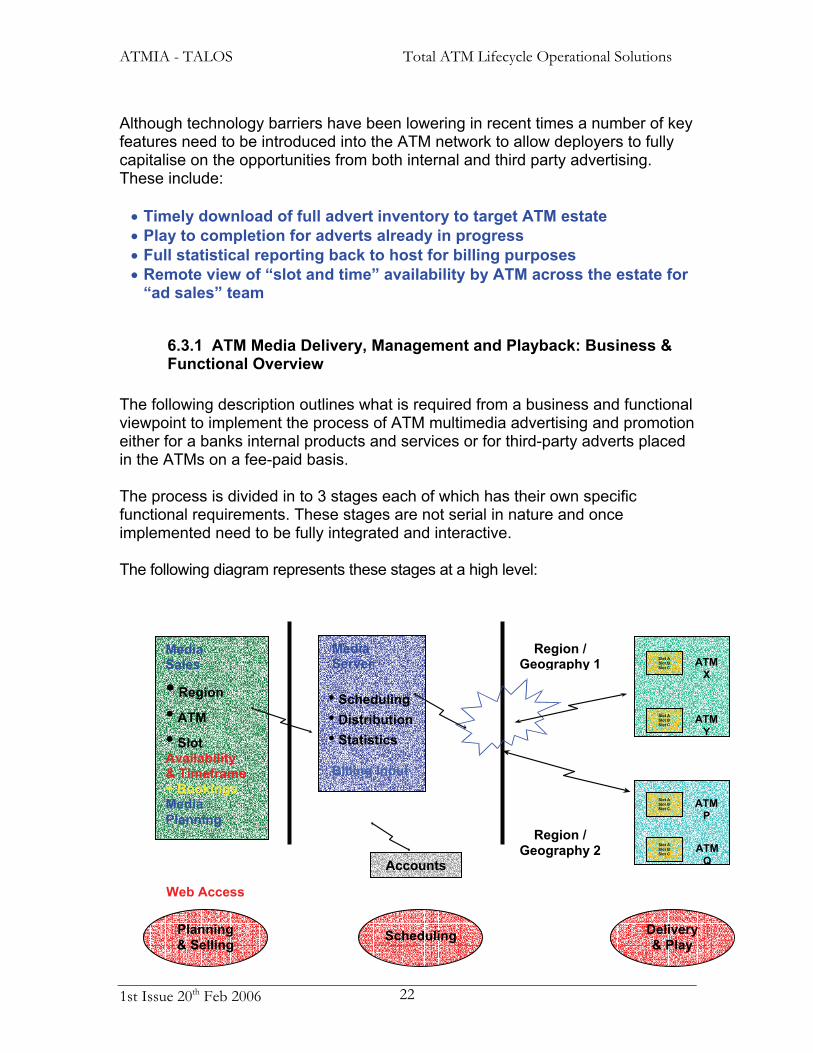

Although technology barriers have been lowering in recent times a number of key features need to be introduced into the ATM network to allow deployers to fully capitalise on the opportunities from both internal and third party advertising. These include: • Timely download of full advert inventory to target ATM estate • Play to completion for adverts already in progress • Full statistical reporting back to host for billing purposes • Remote view of “slot and time” availability by ATM across the estate for

“ad sales” team

6.3.1 ATM Media Delivery, Management and Playback: Business & Functional Overview

The following description outlines what is required from a business and functional viewpoint to implement the process of ATM multimedia advertising and promotion either for a banks internal products and services or for third-party adverts placed in the ATMs on a fee-paid basis. The process is divided in to 3 stages each of which has their own specific functional requirements. These stages are not serial in nature and once implemented need to be fully integrated and interactive. The following diagram represents these stages at a high level:

Media Sales

• Region

• ATM

• Slot Availability & Timeframe + Bookings Media Planning

ATM X

ATM Y

Region / Geography 1

ATM

P

ATM Q

Region / Geography 2

Media Server • Scheduling • Distribution• Statistics Billing Input

Accounts

Web Access

Planning & Selling Scheduling Delivery

& Play

Slot ASlot B Slot C

Slot ASlot B Slot C

Slot ASlot B Slot C

Slot ASlot B Slot C

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 23

Once the relevant media files are distributed to the ATM the following represents a possible advertising model that can be implemented. However, customer and country variations will need to be implemented.

6.3.2 The Role of the Media Server and what happens at the ATM Level

Assuming that the media files (MPEGs) that need to be played in the individual ATMs are produced and delivered to the “media server”, then these files need to be put together into appropriate “Media Campaigns” for distribution to the relevant ATMs. A campaign will consist of the actual MPEG media files plus the schedule file(s) associated with it. This process involves the creation of a range of distribution schedules that will list the ATMs due to receive the campaign (by geographic region perhaps) and for how long each campaign will last. The schedule will also identify which media “slot” in each ATM each advert will occupy.

Optional Deployer/Retailer Advertising Time,

Static or Multi Media 10 Seconds

...Media Advertising Time… 15 - 60 Seconds

“Enter Card at any Time to Begin ATM Transaction”…

No Sound

Attract Sequence

...Media Advertising Time… 10 - 20 seconds

“Please Press to Receive Printed Offer”…………..

Sound

“Offer” Sequence

Please Take Your Money

Media Adv. Time - THANK YOU

Receipt Print & make “Offer” if Req.d

No Sound

Transaction Sequence

Media Adv. Time

15 - 30 Seconds Replace Normal “Please Wait”

Choose Amount of cash to Withdraw

Choose Account etc as Normal

Choose Transaction

Type: “Withdraw Cash”

Enter Pin Number as Normal Transaction

Please Enter Card to Begin

Normal Deployer Welcome Screen

Sound

“Enter Card at any Time to Begin ATM Transaction”…

Back to Optional Retailer/

Media Adv. Time

- THANK YOU Receipt Print & make “Offer”

Return to “Attract” Sequence

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 24

Assuming that each ATM has 3 advertising slots available to run 5 second advertisements during the TRANSACTION sequence, then it will be required that the media server distributes flexible campaigns and/or updated campaigns on a regular basis to the whole ATM estate or to a sub-set based on the criteria as defined by the schedule laid down by the Media Sales & Planning process. The frequency of distribution will start at monthly or perhaps bi-weekly and as the business evolves then it is likely that campaign downloads and updates will be run on a weekly basis. Since a “campaign” will consist of media files of various types and sizes it is expected that each complete campaign will be up to 20Mb in size. Campaign updates that replace only one of the adverts in the three slots will naturally be smaller but at these file sizes, even allowing for the downloads to take place overnight, the distribution network will need to be high speed/bandwidth such as TCP/IP. Once the relevant Media files and their associated schedules have been downloaded to each relevant ATM, the schedule of media file plays needs to be addressed by the ATMs “transaction control software” (TCS) and/or application environment to ensure that the correct “advert” is played in the correct “slot” in each ATM and that each advert in each campaign is capable of running in a “play to completion” environment on each ATM. This therefore means that during the TRANSACTION SEQUENCE there must be the capability for the ATMs TCS to check when the host returns the requested verification and ensure that whatever advert is playing at the time on the ATM screen is allowed to complete its schedule. This may mean that the host message, and therefore transaction completion, is delayed for up to 4 seconds. Thus there is the potential to slightly increase the overall customer transaction time but due to the audio-visual nature of the interaction with the customer during the “Please Wait” time studies in the US have shown that the perception is that the total transaction time is shortened not lengthened. Initially, and possibly even for circumstances where the bank is only running its own adverts, it is expected that complete campaigns will all be changed at once. This means that all 3 slots in each ATM will be updated at the same time. This is not an ideal situation from a marketing viewpoint due to the previously discussed “wearout factor”, however it is simpler to administer from a deployers viewpoint. If 3rd party advertising is to be introduced then the estate owner or whoever is responsible for the campaign downloads will need to have more complete “inventory management” capabilities available at both the media server and ATM level.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 25

The infrastructure of the Media server, communications network and ATM terminal environment need to be able to provide in a timely manner the ability to:

• Download to the identified ATMs the required media files and the associated control file

• Obtain verification this has been done correctly • Update any media files and campaigns that require updating • Schedule the updated campaigns or new campaigns to be invoked as

required • Remove, under predetermined criteria, media files, control files

and/or complete campaigns no longer required • Provide statistical data back to the media server on previously run

campaigns This functionality ultimately needs to be deliverable to any individual ATM in the estate, for any individual campaign running in the ATM and for any specific media slot in that ATM.

6.3.3 Advertiser Billing Key Factors

• Advertisers see little value in the “IDLE LOOP” or “ATTRACT SEQUENCE” time

• Advertisers will only pay for completed plays of their advert during the TRANSACTION.

Generally the business model will be based on the advertisers being billed based on 2 criteria. First, a simple fee or “media charge” for having a presence or “slot” on the ATM(s) for any given week, 2-week or monthly period. The actual time scheduled will depend upon the advertisers campaign requirements, the length of time slots available in the required ATM estate sub-set and the overall sales campaign put together by the advertising sales force in conjunction with the advertisers agency. The second part of the fee will be based on a charge according to how many times the advert was run in the scheduled time period and how many coupons or “offers” were made/printed. To allow for this model to work a billing process must be implemented that gathers details on both elements of the charges and bases invoices on these criteria. This means that the media server must also pull from each estate and each individual ATM in the network statistical details on what advert is running in each slot during which timeframe and how many times it was played during this time with details of the number of coupons printed. This data will then need to be aggregated and fed into the financial and billings systems as appropriate.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 26

The Media Server should NOT become a billing system but should gather, perhaps from each ATMs audit log, the statistics required to provide the input to the billing and financial systems.

6.4 Advertising Sales The above sections have addressed the functional and business requirements, at a high level, for the Media Server and ATM Delivery and Play stages in the ATM Media Network. Today, much of this functionality can be provided by products from the main ATM vendors. ATM vendors do not traditionally address the issue of meeting the requirements of the Media Sales and Media Planning parts of the business model. This is not historically an area where Banks or ATM vendors have a great deal of experience or expertise. Before discussing the requirements the following should be noted with regards to the Media side of the business. Many forms of advertising medium are sold in packages and ATM screen slots will be no different. Discounts to advertisers will be given according to spend, placement location, length of run time etc. When the medium is establishing itself greater discounts will have to be given especially when the network of available ATM screens is in its initial ramp up stage. It is expected that no ATM advertising network will be 100% full to capacity with adverts. It is the role of the Media Owner (partner) to offer special bundles and repeat runs to the advertisers so that the maximum advertising revenue is achieved but it will never yield 100% of its potential, just like any other advertising medium. While transaction volumes are important it is not necessarily the only factor in determining sites attractiveness to the advertisers. The media owner will rate each ATM site according to such factors as transaction levels plus the associated geo-demographic data available to them. Each side will therefore be rated as: HIGH, MEDIUM or LOW on an attractiveness matrix and then given an associated price for each advert slot on that basis. The media owner will therefore sell their “Media Bundle” of slots to fit in the advertisers criteria for population reach and their own desire to keep as many slots full for as much time as possible. An advertiser will not, generally, be able to buy just slots that rate HIGH but will have to take a spread across all 3 attractiveness types, unless they pay a large price premium. The IT infrastructure outlined in the diagram earlier will not be required to handle these aspects of the Media sales & Planning process although they must be understood if the correct functionality is to be provided from the ATM Network to the Media Sales & Planning personnel. By the nature of the job the media sales and planning people will work closely with the advertising agencies of the clients/advertisers. This means that they will be a mobile workforce and will need remote access to their support systems.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 27

Today this access is probably best provided via a secure website, utilising laptop PC’s. Each PC would also carry a database of information on each ATM on the Media network. This could alternatively also be provided through a remote link if appropriate. This would provide the basic data with which to negotiate and plan particular media “campaigns” with the agencies. However, before taking any firm orders the planners would need to ensure that sufficient slots of the correct attractiveness were available on the right number of ATMs in the targeted geographic locations. For this they would need to have access to the “Media Server”, via the secure website, where they would be able to get an exact picture of the slots, and location of ATMs which have advertising availability. These would then need to be able to be booked, and advertising slots reserved in a real time manner. In effect, constructing “campaigns” online or at least making the initial assignment of ATM slots. The Media Server would therefore need to keep track of the individual slot schedules for each ATM and provide that data to (possibly) a Media Sales web server that would allow the sales and planning personnel access and the capability to view the data in a graphical manner sorted by a range of different criteria such as: Available Slot types Available Geographic locations Available Bank/deployer slot and/or ATM types Available timescales by slot by ATM Etc Bookings, reservations and pricing data would then need to be entered into the system to provide input back to the “media Server” in the form of confirmed Advertising Campaigns, with associated Media and control files. It may be that within the media sales world that there are standard applications that can be utilised/adapted through suitable interfaces to/from the Media Server to meet these and other requirements. 6.5 General The effectiveness of current advertising & internal marketing campaigns has been confirmed in different geographies.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 28

A further use of the ATM “screen downloads” has been demonstrated, providing a social service. The screen is used to advertise “missing” children, thus bringing to all public areas immediate notification and child details. This alert programme brings a significant benefit and security service to a community, and raises the profile and brand image of the ATM deployer. ATM deployers should be aware of all aspects of using the ATM screen both during transaction, or during the idle mode (or more precisely “attract” mode) when it is still viewed by the public.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 29

Chapter 7 ATM Outsourcing Business Model

7.1 Introduction

« When an organisation produces internally, something that others can supply or producemore effectively or in better economical conditions, then that organisation sacrificesits competitive assets.

Re-orientate yourself on what gives a real competitive edge to your organisation, thenoutsource the rest. »

Harvard Business Review

Outsourcing is commonly used by most financial organisations for part of the annual cost, in particular for Cash delivery and Hardware Maintenance, however the concept of offering the complete ATM estate for an Outsourcing Contract, is still relatively new. Experience in outsourcing of other services such as Call Centre Management, Card Services, and IT functions has met with mixed reception (and in some cases failure). This document sets out to help understand the following :-

• Factors driving need to Outsource • Anticipated results from a Financial organisation perspective • Anticipated outcome from an Outsource Service Provider

perspective • Outsourcing Organisation Contract • Commercial Structure of an Outsource Contract • Legal Structure of an Outsource Contract • Make it work

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 30

7.2 Factors Driving Need to Outsource Based upon the annual costs identified against each of the key parameters given above, it is clear that these segments will be subject to increased pressure to reduce cost. Changes in the banking financial landscape, have seen banks increasingly subject to global pressure, mergers and acquisitions, and competition from non traditional bank sources. This has created a need to expand customer offerings, improve efficiencies, while increasing profits and expanding customer base. This has therefore led Financial Organisations to internally address

- Reduction of Operating costs - Recoup capital investment - Deploy a platform for Service Growth - Eliminate in-house solution costs - Leverage assets and Skills - Improve Customer Service - Improve speed to market of New Products & services - Reduce Risk profile - Focus on Strategic Issues - Create Additional future value

Occupancy13%

Communications9%

Central Services15%

Depreciation11%Security

2%User Maint

10%

Consumable2%

H/W Maint9%

Cash Provision8%

Cost of Cash9%

Interest on Cash9%

Insurance3%

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 31

The above has created a renewed interest in Outsourcing of some, or all parts of the current ATM annual costs. These may be categorised as “Managed Services” which add improved system management to an existing service (such as cash optimisation). 7.3 Anticipated Results from a Financial Organisation Perspective There is a myth that an Outsourcing Contract will almost instantly

- Increase availability - Reduce headcount - Lower cash inventory - Reduce fraud - Lower overall cost by 20%-40% - Provide immediate technology upgrade - Improve Security - Increase bank Product Marketing -

The reality of an Outsourcing contract needs to be fully understood before entering into an expensive process. It needs to be recognised that Outsourcing involves all key Customer Organisational Groups within the financial organisation, and each group must endorse, and be supportive of, the move to an Outsourcing Contract if it is to be successful. These internal customer organisational groups comprise

Customer Organizational Influence

Channel IT andTechnology

Legal &Commercial

HumanResourcesOperations

•Business Process•Availability•SLA’s•Hardware•Managed Services•Cash Process•Implementation•Project Mgt

•Strategy•Marketing•Consumer behavior•Business Direction•Channel Integration•New Services•Financial Options

•Software•Communications•Tech Risk•Tech Evaluations•Technology Futures

•Pricing and Contract•Partnerships•Mergers and Acquisitions•Commercial Conditions•Tax & legislation•Risk and Liability

•Staff & Training•Union Mgt•Employee Transition•Organizational behavior•Culture•Employee Fulfilment

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 32

From a business perspective, the prime objectives are based on the following factors :-

- Free up Capital & management resources - Increase focus on core business - Control and predictability of costs - Improve ratios (off balance sheet financing) - Improve quality - Manage reduction in risk - Leverage resources and skills - Improve branding & Share value

7.4 Summary of the Overall Requirements of Outsourcing During the process of deriving an Outsourcing contract, there are a number of phases to complete. Phase 1 is a detailed internal analysis needs to be carried out which identifies both the precise elements to be outsourced, and the existing detailed costs, these then define the initial framework of the contract in terms of operations, products, business processes, personnel, and price boundaries. Phase 2 is to address the future strategy of the bank in terms of technology platform, customer service, functionality requirements, and the timescales required to move from the current operating model to the future operating model. Phase 3 is to review the above realistically, in order to produce technical Service Level Agreements, and Implementation Plans. Phase 4 the identification of an internal Customer Contract Team with responsibility for the production of the Outsourcing Tender documents (including technical to legal), Tender process, evaluation and selection and final negotiation with selected contractor Phase 5 is the implementation of the contract and final handover & acceptance sign off. Phase 6 monitoring of contract and transition from current operating model to the future operating model Phase 7 on-going monitoring and contract renewal or phase out

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 33

7.5 Anticipated Outcome from an Outsource Provider Perspective The key drivers from a range of Customer requirements are to :-

• Reduce Operating Costs and recoup capital investments while deploying a platform for volume and service growth

• Eliminate costs associated with in house solutions and leverage existing assets and skills

• Improve Customer service • Improve speed to market for new products and services • Improve risk profile • Enable management to refocus on strategic issues • Create additional future value

It is important to note that the above summarised Customer requirements require investment both in terms of financial and resources. Consequently the prime requirements from a Contractor perspective is a contract of sufficient duration to allow the investment value to be recouped. By having a short duration contract or one which can be readily terminated, there is no incentive to invest. Contractors do not have qualified personnel resources which can be switched on and off, and tend to offer efficiency by economy of scale and better utilisation of there resources. Some of the more obvious perceptions and facts are given below.

Outsourcing : perceptions and facts

• Vendors are efficient at lowering costs

• Negotiation ends when contract is signed

• Outsourcing is a partnership

• Vendors have a pool of specialized people

• The 3 benefits of outsourcing : less expensive, best quality, faster.

Vendors gross margin varies between 22 and 28% - inherent costs in the management of the client relation : between 3 and 7%The negotiation is ongoing after the signature as requirements evolveThe vendor becomes a real partner in gain/risk-sharing contract

Vendors are challenged by staff shortage

These 3 benefits are never gathered together at the same time

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 34

As stated above, Outsourcing is a Partnership but typically outsourcing contracts are drawn up as highly specialised purchase contracts. It is clear that outsourcing involves the transfer of some of the Customers business process, and this can only effectively be taken over through a planned migration period during which there will be a shared risk scenario. Most outsourcing contracts will cover the traditional “managed services”, together with the transfer of the ATM asset base. Areas to be addressed to ensure that the contractor fully understands the risks to be included are :

1. Who owns the cash, who purchases the cash 2. Changes in tax/VAT legislation by transferring liability 3. Control and reporting of balance and settlement activity 4. Duration and performance of existing contracts which are to be

transferred 5. The sub contract conditions and any price guarantees. 6. Decision ownership for replacement ATM’s (vendor/functionality)

Occasionally an Outsourcing contract will include the requirement for transaction processing, which includes the additional risks:

1. Firewalls between Customers 2. Meeting identity fraud regulatory issues 3. Customer controls for database examination 4. Meeting National & international regulatory controls for audit, and

customer cash processing (Basle II, cross border money transfer etc)

The overall areas to be considered by a contractor in an outsourcing contract are summarised below.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 35

Processing CenterServices

Direct Costs -Field Services

Back-OfficeServices

Processing Center Infrastructure- Monitoring Center- Disaster Recovery Center- Telecommunications Equipment &

Lines- Hardware, Software, Licenses- Set Up & Certifications of Services- Connections to Card Organizations &

Bank Host- Compliance with Card Organization &

Industry MandatesProcessing Services

- Transaction Acquiring, Switching,Authorization, Monitoring & Processing

- Maintenance of Connections- Daily Reporting- Screen, receipt, transaction flowimplementation, downloading, keysmanagement

SG&A Costs to Support All Above

ATM Purchase & DeploymentTelecommunicationsHardware DepreciationHardware Upgrades1st Line Maintenance2nd Line MaintenanceCash Supply & FillingConsumablesInsurance

Cash ForecastingCustomer Service/Help-DeskSubcontractor Management

- Coordination and dispatching of sub-contractors

Balancing & Reconciliation- ATM and Network Balancing,

reconciliation, report generationDisputed Transactions Handling-Exception handling, out of balance

items- Investigation, reporting, statistical

analysisChargeback ProcessingSG&A Costs to Support All Above

Value Added Services

- Top Up for Prepaid Mobile Airtime- Bill Payment- ATM Advertising

Additional SourcesOf Revenue

ATM Operations & Management Summary of Cost Components

ATM Operations & Management Summary of Cost Components

When reviewing the above, it is worth addressing the response to a Customers contract by considering core strengths which are internal, and the advantages of responding as a joint offer with a partner who compliments core strengths, or responding as a consortium, with the Customer having a management interest as part of the organisation 7.6 Outsourcing Contract Organisation The Commercial structure can be a single company response, or a joint venture with a key partner, or finally a vendor consortium which includes the Customer. This is graphically represented below, which demonstrates the evolving alternatives.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 36

Evolving AlternativesEvolving Alternatives

ATM UTILITYATM UTILITYATM Utility Co.ATM Utility Co.

RETAIN IN HOUSE RETAIN IN HOUSE Address inefficienciesAddress inefficiencies

JOINT VENTURE JOINT VENTURE SINGLE BANKSINGLE BANK

plus a Sector specialistplus a Sector specialist

JOINT VENTURE JOINT VENTURE MULTI BANKMULTI BANK

Several banks plus Several banks plus a sector specialista sector specialist

Degree of ChangeDegree of Change

OUTSOURCEOUTSOURCEOutsource to a strategic Outsource to a strategic

partnerpartner

Sector Specialists bring specific expertise & investment capabilSector Specialists bring specific expertise & investment capabilityity

••Ability to leverage scale economiesAbility to leverage scale economies••Supplier expertiseSupplier expertise••Shared / Avoided investmentShared / Avoided investment••Market Leading OpportunityMarket Leading Opportunity

••Bank confidence in Service Bank confidence in Service provisionprovision

••Reduced Bank focus on operational Reduced Bank focus on operational managementmanagement

7.7 Commercial Structure of an Outsource Contract The typical major headings to be expanded and included as part of the Commercial structure of an Outsourcing contract include definitions and expansion of the following:-

1. Contract Duration – Typically a minimum of at least 5 years in order to provide incentive, and take advantage of contractors investment

2. Client Strategy – Overview of potential future changes which may indirectly impact, or be incorporated in future amendments.

3. Organisation – The form of contract in terms of Single Vendor, Consortium or Joint Venture

4. Services to be Delivered – detailed breakdown of all Operations included, ATM estate value, replacement cycle, and personnel. Services to be delivered by Contractor to Customer, and from Customer to Contractor.

5. Escalation Procedures – Dispute resolution, timescales, and personnel involved, prior to contract breakdown and legal action

6. Service Level Agreements a. To achieve normal payment b. To receive bonus payment c. To receive penalty clause

7. Controls – Degree of Customer monitoring and Contractors limitations (relocation of ATM’s, branding, bank customers)

8. Reporting Matrix – List of reports required, frequency, and contact points

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 37

9. Tax System and Legislation – Confirmation of liabilities between the

Customer and Contractor for VAT, Tax, and National/Federal legislation changes)

10. Future Proofing – Technical upgrade and replacement cycle, maintaining estate book value

11. Pricing and Payments – Type and regularity of payment, which can be defined either as “fixed fee”, or “transaction” based fee, or “availability” fee. Based on section 6, the pricing and payment may be a combination of some or all of the above.

12. Committees – Regular Customer and Contractor meetings with a defined agenda to ensure that potential problems are identified and addressed at an early and regular stage.

13. Technical Evolution – Additional technology anticipated to be included in the Contract such as currency change, Chip and PIN, security improvements.

The commercial structure should reflect a partnership rather than procurement approach, with both penalties and performance improvement payments being possible. The incentive for an Outsourcing Contractor to invest in the Customers business must be reflected in the ability to benefit from improved performances. The Contract should therefore include flexibility of payment as business improvements are achieved. This may be achieved by introducing a bonus or penalty percentage payment, based on a reference to ATM availability, or transaction levels. It should be recognised that Outsourcing contracts have failed due to lack of planning, internal rejection (people & politics) as well as Contractors failings to meet contract expectations. The core components of an outsourcing contract engagement are more about :

- customer relationships - governance structures - business processes - human resources - establishing SLA’s - project management - system integration - business process change - Governance

It should not be seen as a matter of hardware and software management, and product selection.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 38

Outsourcing is about providing the most effective “business solution”, and therefore one of the keys to success is to ensure that the evaluation process of the tender includes detailed analysis of Contractors capability, and is not based on the lowest price All too often the Outsourcing contract becomes a legal Purchase Contract with penalties – a stick without the carrot ! 7.8 Legal Aspects of an Outsource Contract The final legal tender outsourcing contract, should ensure that the customer technical requirements are correctly interpreted in a legal framework, and which should ensure that the following are included and readily understood.

• Commercial structure (see above) • Contracts and compliance • Current scenario and Transition Management • Projected Final Operating Scenario • Self Service Channel Development • Human Resource Management • Project Implementation & Change Management • Contingency & risk Management • Pricing • Phase out & Contract Termination

The typical key headings for a legal document defining an Outsourcing Contract would include the following. No attempt is made to provide detail as this will be subject to local legal specialists.

Outsourcing Contract Framework

a) Interpretation of Terms b) Subject Matter of the Contract c) ATM Asset Price Evaluation d) ATM Asset Conditions & Upgrade programme e) Replacement of existing ATM’s and Acquisition of new

ATM’s f) Services to be provided by Contractor g) Services to be provided by Customer h) Report requirements and Monitoring Structure i) Personnel transfer and obligations j) Business Process transfer k) License agreements l) Purchase and transfer of ATM’s m) Form of Fee

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 39

n) Duration of Contract o) Cessation of Rights and Takeover obligations p) Assurance of Contracting parties q) Contractors Duties and obligations r) Customer Duties and obligations s) Preliminary payments and Settlement of Damage t) Confidential Information u) Common and Final Provisions v) Interpretation of Terms

7.9 Making It Work

CONTRACTORS RESPONSE DOCUMENT Based on a form of legal contract given above, the Contractors response document must clearly respond to all conditions. In general, the response document is dictated largely by the Customers form of Tender document, which leaves little room to modify the form of response. Quality of response is dictated by three things, the time to respond, the commitment to respond, and the experience of the response team. When a tender document is received, an internal analysis will be required to assess if the potential contract is either within the capability of the contractor, or will not lead to over exposure. Once a decision to proceed has been agreed, a contractors bid response team should be assigned in order to assess and prepare the response. At key points in the bid preparation, a management overview should be provided in order to address any key points or direction changes. The final stage is the pricing, risk assessment and the final legal framework of the response.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 40

For guidance only, as response is governed by both the Customer tender documents, the following typical headings can be used to ensure a composite response which should include but not be limited to the following:-

- Executive Summary - Corporate and Contract Structure - Partners/joint venture Corporate and contract support structure - Contract & Compliance statements - Specific Information Request - Channel development - Specific Information Request - HR policy - Project Implementation - Compliance and Risk management - Pricing and Payment - Confidentiality statement

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 41

Chapter 8 ISO/IAD Business Model

8.1 Introduction For clarification both ISO and IAD1 terms are both used, in conjunction with the “non financial institution” deployer. Throughout the remainder of this text only reference will be made to ISO. The ISO business model is a financial calculation based upon income and expenditure in order to provide a profit/loss statement. Unlike a bank, the ISO cannot offset ATM costs against other business operations in order to establish the cost efficiency of an ATM. The ISO therefore relies solely upon the income (transaction fee x number of transactions) to offset all front end expenditure and on-going costs. ISO Business Models follow a number of different formats

1. ISO has full responsibility for provision of installed hardware, site location, and support of ATM, and ISO takes full transaction fee

2. As above less site location, retailer provides site location and shares fee 3. As above but less cash which is merchant fill, and retailer shares fee 4. Retailer pays ISO a lease fee for Hardware & Support, retailer takes

transaction fee. 8.2 Business Strategy In order to assess if you wish to become or remain an ISO, the following Business strategy considerations need to be addressed. These will form the core elements of an ISO “Business Plan”, which will provide a risk free analysis of the business case. The key element of the strategy being the site analysis which will provide indications of the potential number of transactions, and therefore max/min range of income.

• Market analysis/Competition • Funding • Site Analysis • Form of Contract • Network/Host Processor Provider • Provision of Cash • Security/Risk • Fee and Contract Structure

1 ISO – independent Service Operator; IAD – Independent ATM Deployer

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 42

As part of the analysis the following items need to be taken into consideration. Depending upon the form of contract adopted by the ISO, all or some of the following will be applicable: EXPENDITURE INCOME Set up Charges

- Hardware Cost - Site Preparation - Warranty - Import duties & taxes - Delivery to Site - Sales Support

Note: Above normally amortised over 3 years to obtain monthly lease cost of Hardware

) ) } Hardware Only Lease Contract ) )

Monthly Expenditure - Hardware Lease (see above) - Hardware maintenance - Communication fees - Network Membership Fee - Software License fees - Cost of Cash (or Retail Fill) - Delivery of cash (as above) - Retailer % of transaction Fee - Finance costs

(payments/receipts) - Insurance (to include damage,

robbery, vandalism, and bad debt)

- Site Rental (based on trade loss for ATM site area)

- Customer maintenance (ATM fill, print paper, jams, training)

- Contract Monitoring - Tax

) ) ) ) ) ) ) } May be Shared with Retailer ) ) ) ) ) ) )

Contingency Funding - Technical Upgrades (EMV ,

3DES) - Additional Security (Ram raids,

skimming) - Legislation Changes

(Liabilities) - Fee Structure Changes (Visa,

EPC) - Competition (Banks, ISO’s

Technology) - Business disruption (Virus,

refurbishment, downsizing, M&A)

- Legal Fees (litigation) - Branding (defend territory)

Potential Income - Transaction Fee (x

number of transactions) - Interchange Fee x

number of transactions) - Media revenue - Additional services

(Phone Top up) - Call Out charges (non

contractual) - Vandalism Parts

Total Expenditure + contingency Minus Income = Profit/Loss

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 43

The above table represents a composite of factors which influence the profit/loss of the business. However by far the most critical factor remains the number of transactions which the ATM attracts, and the factors which may influence these both positively (increased transaction functions such as phone top up, increased market segment capture, expanded customer acceptance), and negatively (Competition, Changes in Fee structure, and Security issues). A number of ISOs have failed or found difficulty because of lack of contingency planning. Factors outside of the ISO control such as the recent EU regulations concerning the general move for Cash Recycling via ATM’s to be only with “fit” notes which have been checked for quality and counterfeit, and the new EPC (European Payments Commission). The European commission is completing a full review of interchange fees across Europe between selected banks. The complete list will be the subject of review and a report by mid 2006, and subsequently European regulation. The prime objective being to unify the European Payments Industry to ensure its integrity, security and it is more efficient to the benefit of the European Union. The details of regulation are important to the IAD/ISO who may utilise “Interchange Fee” as the charge per transaction, as potential changes could significantly impact the business financial balance. It has been noted that some Financial Institutions are either already initiating an ISO model, or are monitoring their effectiveness for potential acquisition or duplication. This recent move by Financial Institutions may add new pressures, and motivation, for existing ISOs to ensure that their Business Model is profitable.

ATMIA - TALOS Total ATM Lifecycle Operational Solutions

1st Issue 20th Feb 2006 44