Embed Size (px)

DESCRIPTION

project on Paint industry

Citation preview

www.hemonline.com

BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY

Company Report

Berger Paints India Ltd 18th

June, 2012

For Private Circulation Only 1 Hem Research

CMP Rs.144.05

Target Price Rs.190.00

BSE Code 509480

NSE Code BERGEPAINT

Market Cap (Rs. Cr.) 4986.34

52 Week High/Low 153.30/78.15

Industry Paints

Face Value Rs.2.00

Shares O/S 346153264

EPS 5.20

Book Value 22.87

P/E 27.70

P/B 6.30

Shareholding Pattern

Research Analyst: Vineeta Mahnot [email protected]

� Berger Paints India Ltd. (BPIL) is one of the India’s foremost

paint companies, currently ranked as second largest on the basis

of consolidated sales turnover in Indian paint industry. It enjoys

about 19 percent share of the over Rs.21,000 crore of the Indian

paint industry.

� The company has registered smart numbers for the quarter

ending March 2012. Revenues from operations stood at Rs. 746.50

crore as against Rs.592.50 crore in the corresponding quarter of

the last year representing an increase of about 26%. Improved

sales performance by subsidiaries and joint ventures boosted

revenue for the quarter together with strong domestic

performance. Operating profit too surged 29.45% in Q4FY12 at

Rs.73.40 crore from Rs.56.70 crore in the like quarter last year. A

comparatively sharp net profit growth of about 32% to Rs.44.60

crores was clocked for the Q4FY12 compared to Rs.33.90 crore of

same quarter previous year. The increase in net profit is due to

improved performance in the emulsion business and growing

presence in the western part of the country. EPS stood at Rs.1.29

compared to Rs.0.98 in the same quarter last year.

� Material cost to sales(%) jumped at 64.3% in quarter ended March

2012 as compared to 62.2% in the corresponding quarter last year.

This increase is attributable to consistent rise in raw material

prices and impact of depreciating rupee on imported raw

materials. Further, there is sustained increase in advertisement

and sales promotion spends in decorative business.

Valuation

With stronger market share, wide distribution network, huge

capacity expansion on stream, better product mix and higher A&SP

spends; Berger Paints India Ltd. growth prospects look promising.

We believe BPIL is trading at an attractive valuation at 22.9x and

19.79x of FY13EPS of Rs.6.29 and FY14EPS of Rs.7.28. We initiate a

‘BUY’ on the stock with a target price of Rs.190 (appreciation of about

32%) with the medium to long term investment horizon.

www.hemonline.com

For Private Circulation Only 2 Hem Research

Business Details

Established in 17th December, 1923, the company then known as Hadfiled's (India) Limited; was a small paint

company based in Kolkata having its only manufacturing facility at Howrah, West Bengal to produce ready mixed

stiff paints, varnishes and distempers. Post independence, towards the end of 1947, British Paints (Holdings) Limited,

U.K acquired Hadfield's (India) Limited and thus British Paints (India) Limited was incorporated. From a production

capacity of 150 tonnes and sales turnover of around Rs. 25 lakhs in 1947, the company has come a long way to become

at one point of time; a part of the worldwide BERGER group in 1983 and thereby acquiring its present name Berger

Paints India Limited to having subsequently gone through further ups & downs as well as ownership changes to gain

its present status wherein the majority stake is with Delhi based Dhingra brothers and business revenue more than Rs

2400 crs.

Today Berger Paints India Limited, having

solely used and developed the name and

trademark BERGER and all its variants in India,

is a household name in paint. It is the third

largest paint manufacturer and second largest

manufacturer in decorative paints. With Head

Office in Kolkata the company manufactures

and markets a range of decorative & industrial

paint products under various product brands

and has it operations spread throughout the

length & breath of the country; with seven

manufacturing facilities in India and more than

85 depots, several regional & area offices,

besides four facilities overseas. It has a

workforce of over 2500 employees and a countrywide distribution network of 15000 plus dealers. The company's

manufacturing facilities are located in West Bengal, Uttar Pradesh, Pondicherry, Goa, and Jammu and Kashmir. The

company has its presence mainly in the Tier II and Tier III cities.

Its subsidiaries are Beepee Coatings, Berger Jenson & Nicholson (Nepal), Berger Paints (Cyprus) and Berger Paints

Overseas. It also acquired 100% stake of Motor and Industrial paints business of ICI India. The company has a joint

venture with Nippon Bee Chemical for manufacturing of coatings for plastic substrates used in automobiles and

mobile phones. It has wide range of colour bank with over 5000 shades. Lewis Berger ColorBank offers computerised

paint technology through its outlets which mixes different shades to create desired paint. It has a network of 2500 such

counters.

www.hemonline.com

For Private Circulation Only 3 Hem Research

Strong Industry growth

The industry size for paints is estimated at over Rs. 21,000 crores wherein the organized sector accounts for 70% while

the remaining is with the unorganized sector comprising of around two thousand small scale paint units. The paint

market is dominated by decorative paints, which accounts for nearly 70% of the total demand. The balance 30%

belongs to industrial paints - comprising automotive and industrial, protective, powder, coil and marine coatings. As

per the data published by the Central Statistical Organisation (CSO), paints production fell in four months and

remained subdued in six months for 2011-12. Paints industry’s aggregate production for 2011-12 rose by a mere 0.5 per

cent. However, the industry’s sales rose by a sharp 29.6 per cent during the year.

Paint production to remain healthy in 2012-14

Units 2008-09 2009-10 2010-11 2011-12(E) 2012-13(E) 2013-14(E)

Capacity Tonnes 12,72,151 14,14,607 15,46,459 17,15,014 23,67,014 27,38,514 Production Tonnes 10,07,606.1 11,85,195.6 13,52,465.8 15,11,275.3 17,12,274.9 19,69,116.1 Sales Tonnes 11,15,159.2 12,85,816.4 14,85,665.2 16,78,624.2 19,06,917.1 22,01,535.8 Export Rs.crore 147.6 216.0 223.5 251.2 291.4 312.1 Import Rs. crore 837.7 816.0 992.4 1,151.5 1,420.2 1,623.4 Realisation Rs./tonne 1,00,514.7 98,911.2 99,636.1 1,07,407.7 1,15,355.9 1,21,700.5 Sales Rs. crore 11,209.0 12,718.2 14,802.6 18,029.7 21,997.4 26,792.8 Domestic market value

Rs.crore 11,899.1 13,318.2 15,571.5 18,930.0 23,126.2 28,104.1

Source: CMIE

CMIE expects the production to grow by 13.3 per cent in 2012-13. The production is further expected to increase by 15

per cent in 2013-14 to around 19.6 lakh tonnes. Sales volumes are likely to remain higher than the production volumes

as some companies undertake trading alongwith manufacturing. The sales volumes are expected to grow by 14-15 per

cent per annum during 2012-14 period and are likely to cross 20 lakh tonnes by March 2014.

This healthy rise in volumes will be owing to an expected increase in the demand for both decorative and industrial

paints. Of the total demand for paints, 70 per cent comes from the decorative segment. Of this, demand for

refurbishment (repainting of existing houses) accounts for around 65 per cent. Taking into account the rising consumer

demand and diversified needs, the paint companies are coming out with new variants of paints. Also, the companies

are spending more on advertisement to tap these consumers. These initiatives are expected to increase the demand

from refurbishment.

www.hemonline.com

For Private Circulation Only 4 Hem Research

Additionally, the number of projects scheduled for completion in the real estate segment is increasing. Projects worth

around Rs.67,000 crore are expected to be completed in the real estate sector in 2012-14 as compared to Rs.31,500 crore

invested during 2010-12. This will lead to an increase in the demand for fresh painting as well.

Demand for industrial paints is derived mainly from the automobile sector. The demand remained subdued in the

previous year but the automobile production is expected to gain pace in the coming two years. Volumes for passenger

cars are likely to increase by 11-14 per cent during 2012-14. Commercial vehicles production is expected to grow by

around 8-13 per cent per annum during this period. This will increase the demand for industrial paints. Further, the

demand for protective coatings, high performance coatings and other industrial coatings from various user industries

is also expected to rise aiding the growth for industrial paints.

The paints industry is set for huge capacity expansion during

the year 2012-13. Around 6.5 lakh tonnes capacity is expected

to be added during the year. The overall cost for this

expansion is estimated to be Rs.1,700 crore spread over eight

projects. Further in 2013-14, five projects with investment of

Rs.1,253 crore are slated for completion. This will increase

the industry’s capacity by 3.7 lakh tonnes.

The industry’s sales rose by a robust 29.6 per cent in the year

2011-12. This growth is a combination of higher volumes as

well as improved realisations. Raw material expense

remained on the higher side owing to the increase in the

prices of crude oil and titanium dioxide during the year. This faster 32 per cent rise in the raw material costs as

compared to sales resulted into an 150 basis points contraction in the operating profit from core operations. The

operating margin stood at 13.5 per cent. The PAT margin shrunk by 80 basis points to 9.6 per cent during the year.

CMIE expects the industry’s sales to grow by a healthy 22.1 per cent in the year 2012-13. This growth will be a result of

both higher volumes and improved realisations. Volumes are expected to increase by 14-15 per cent and the

realizations are likely to rise by around 6-7 per cent during the year. Realisations are expected to rise as the paint

companies have taken price hikes to pass on the rising input costs. Raw material-to-sales ratio is expected to expand

by 70 basis points. This will be on account of rising input prices and depreciation of rupee against the USD as around

25 per cent of the industry’s raw materials are imported. Thus, the industry’s profit margins are likely to contract by

30-40 basis points. The core operating profit margin is expected to be at 13.2 per cent and the net margin at 9.2 per cent

during the year.

www.hemonline.com

For Private Circulation Only 5 Hem Research

Strong Capacity expansion plans

BPIL has large capacity expansion plans and is well on track to

complete those projects. The 60000 MT Brownfield capacity

expansion in Decorative paints at Rishra, West Bengal is

progressing well, with first phase of 22000 MT already

completed. Its Tamil Nadu Paints project is scheduled for

completion in June 2012. The 60000 MT brown field expansions

at Goa is also progressing well, with first phase of 21600 MT

capacity already added. Greenfield project at Hindupur in AP

with an investment of Rs.200 crore would add new capacity of

320000 MT in decorative paints. All necessary approvals are in

place and the commercial production is expected to start in

FY13. The company plans to double the production capacity

from the present 2.5 million tonnes by 2013. The company

expects the Russian operations to breakeven in FY13 instead of

the projections of FY12 earlier. Company’s construction chemical

business is poised to grow well in coming years and is expected

to reach the sales target of Rs.100 crore in next three years time.

Excellent financial performance

On a consolidated basis, Berger Paints India has registered

excellent numbers for the year ended March 2012. Revenues

from operations shot up by 26% at Rs.2947.70 crore; helped by

price hikes and volume growth. In Decorative segment value

sales growth was witnessed due to five price increases during

the year. In Decorative business front, the company hiked the

prices by about 1.5% in March 2012 and by 2.5% in April 2012

and by about 3% on May 2012. Operating profit jumped about

21% from Rs.250.30 crore to Rs.303.50 crore. Margins are little

cooled on account of sharp increased in raw material prices like

solvents, rutile, vegetable oils and other petroleum-based

products. BPIL’s share in the emulsion business has improved

significantly and the company is hopeful that the trend will

continue in FY13 also. PAT improved by 20% to Rs.180 crore

from Rs.150 crore of last year. Operating profit margin stood at

10.30% and NPM at 6.11%. EPS for the financial year ended

March 2012 stood at Rs.5.20.

www.hemonline.com

For Private Circulation Only 6 Hem Research

Consolidated Profit & Loss Account Rs. Crore

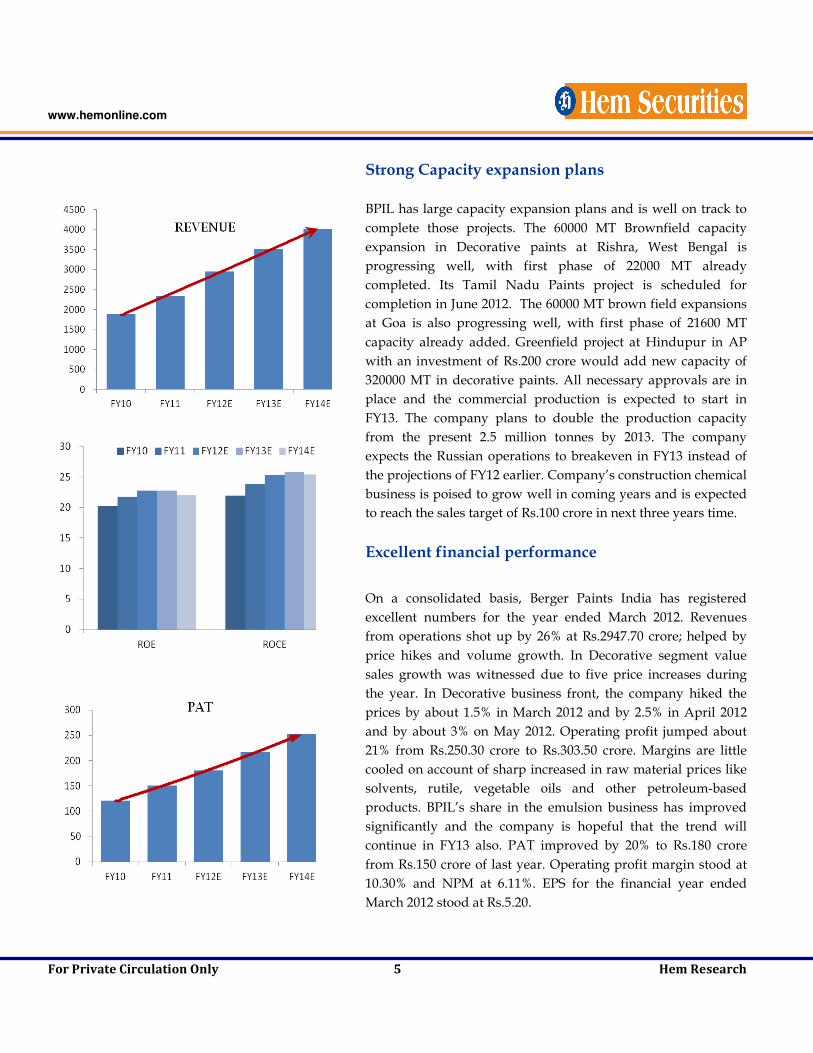

Particulars FY10 FY11 FY12 FY13E FY14E

Net sales 1891.30 2340.70 2947.70 3507.76 4016.39

Growth 23.76% 25.93% 19.00% 14.50%

Expenditure 1692.17 2090.40 2644.20 3139.45 3590.65

EBITDA 199.14 250.30 303.50 368.32 425.74

Growth 25.69% 21.25% 21.36% 15.59%

EBITDA margin 10.53% 10.69% 10.30% 10.50% 10.60%

Other income 25.89 30.20 30.50 34.38 38.16

Depreciation & Amortization 35.82 40.10 47.20 54.04 62.36

EBIT 189.21 240.40 286.80 348.65 401.53

EBIT margin 10.00% 10.27% 9.73% 9.94% 10.00%

Interest 17.20 24.30 32.30 37.87 41.47

PBT 172.01 216.10 254.50 310.78 360.06

Tax 51.62 66.00 74.40 93.23 108.02

PAT 120.39 150.10 180.10 217.55 252.04

Minority interest/Share of JV/Associates 0.00 0.00 0.00 0.00 0.00

Adjusted PAT 120.39 150.10 180.10 217.55 252.04

Growth 24.68 19.99 20.79 15.86

Net Profit margins 6.37 6.41 6.11 6.20 6.28

Extraordinary item 0.00 0.00 0.00 0.00 0.00

Reported PAT 120.39 150.10 180.10 217.55 252.04

Equity Capital 69.21 69.20 69.20 69.20 69.20

Res. & Surplus 527.25 620.30 722.30 887.94 1,077.69

Equity Shares 34.61 34.61 34.61 34.61 34.61

EPS 3.48 4.34 5.20 6.29 7.28

Ratios

Particulars FY10 FY11 FY12 FY13E FY14E

Return on Equity 20.18 21.77 22.75 22.73 21.98

Return on Capital employed 21.90 23.88 25.32 25.72 25.36

Debt/Equity 0.45 0.46 0.43 0.42 0.38

Current Ratio 1.84 2.05 1.92 1.97 2.08

Cash per share 1.19 3.62 5.27 6.44 8.30

Book value per share 17.24 19.92 22.87 27.66 33.14

www.hemonline.com

For Private Circulation Only 7 Hem Research

Balance Sheet

Rs. Crore

Particulars FY10 FY11 FY12 FY13E FY14E

Share Capital 69.21 69.20 69.20 69.20 69.20

Reserves & Surplus 527.25 620.30 722.30 887.94 1,077.69

Shareholders’ funds 596.47 689.50 791.50 957.14 1146.89

Borrowings 267.37 317.30 341.00 398.61 436.56

Foreign Currency Translation Diff acc 0.02 0.00 0.00 0.00 0.00

Deferred tax Liability 26.42 26.30 31.20 31.20 31.20

Sources of funds 890.28 1033.10 1163.70 1386.95 1614.65

Gross block 675.66 721.59 818.13 948.04 1056.94

Accumulated Depreciation 246.19 286.29 333.49 387.53 449.89

Net block 429.47 435.30 484.64 560.51 607.05

Capital work in progress 32.60 81.80 98.16 122.22 145.86

Goodwill 0.00 0.00 0.00 0.00 0.00

Investments 128.16 55.80 9.90 18.01 33.05

Projects in progress 0.00 0.00 0.00 0.00 0.00

Inventories 329.86 443.80 554.40 627.13 718.19

Sundry debtors 242.32 272.80 358.60 418.09 446.88

Cash and bank balance 41.26 125.30 182.40 222.98 287.28

Other current assets 0.00 0.00 0.00 0.00 0.00

Loans and advances 43.23 55.30 98.70 125.43 143.64

Total current assets 656.67 897.20 1,194.10 1,393.62 1,595.99

Deferred tax asset 0.00 0.00 0.00 0.00 0.00

Current liabilities and provisions 356.61 437.00 623.10 707.42 767.30

Net current assets 300.05 460.20 571.00 686.20 828.69

Misc exp 0.00 0.00 0.00 0.00 0.00

Uses of funds 890.28 1,033.10 1,163.70 1,386.95 1,614.65

www.hemonline.com

For Private Circulation Only 8 Hem Research

Cash Flow Statement

Rs. Crore

Particulars FY11 FY12 FY13E FY14E

PAT 150.10 180.10 217.55 252.04

Depreciation 40.10 47.20 54.04 62.36

Interest 24.30 32.30 37.87 41.47

Direct Taxes Paid 66.00 74.40 93.23 108.02

Change in WC (76.11) (53.70) (74.62) (78.19)

Other Operating Activities 0.00 0.00 0.00 0.00

CF from Operations (a) 138.39 205.90 234.84 277.69

Capital expenditure (95.14) (112.90) (153.97) (132.54)

Chg in investments 72.36 45.90 (8.11) (15.04)

Other investing activities 0.00 0.00 0.00 0.00

CF from investing (b) (22.77) (67.00) (162.09) (147.58)

Free Cash flow (a+b) 115.62 138.90 72.75 130.11

Equity raised/(repaid) -0.01 0.00 0.00 0.00

Debt raised/(repaid) 49.79 28.60 57.61 37.95

Interest paid (24.30) (32.30) (37.87) (41.47)

Dividend(inctax) (44.99) (48.45) (51.91) (62.29)

other financing activities (12.06) (29.65) 0.00 (0.00)

CF from financing © (31.58) (81.80) (32.17) (65.81)

Net chg in cash (a+b+c) 84.04 57.10 40.58 64.30

www.hemonline.com

For Private Circulation Only 9 Hem Research

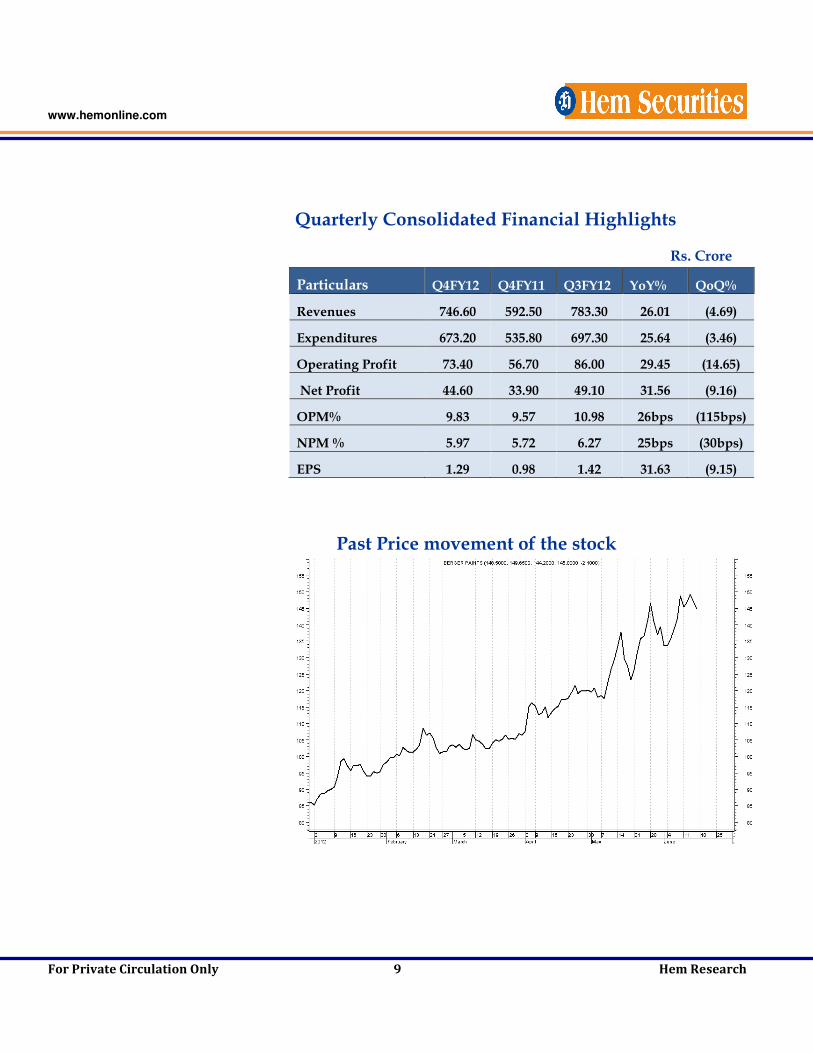

Quarterly Consolidated Financial Highlights

Rs. Crore

Particulars Q4FY12 Q4FY11 Q3FY12 YoY% QoQ%

Revenues 746.60 592.50 783.30 26.01 (4.69)

Expenditures 673.20 535.80 697.30 25.64 (3.46)

Operating Profit 73.40 56.70 86.00 29.45 (14.65)

Net Profit 44.60 33.90 49.10 31.56 (9.16)

OPM% 9.83 9.57 10.98 26bps (115bps)

NPM % 5.97 5.72 6.27 25bps (30bps)

EPS 1.29 0.98 1.42 31.63 (9.15)

Past Price movement of the stock

www.hemonline.com

For Private Circulation Only 10 Hem Research

www.hemonline.com

HEM SECURITIES LIMITED

MEMBER-BSE,CDSL, SEBI REGISTERED CATEGORY I MERCHANT BANKER

MUMBAI OFFICE: 14/15, KHATAU BLDG., IST FLOOR, 40, BANK STREET, FORT, MUMBAI-400001

PHONE- 0091 22 2267 1000 FAX- 0091 22 2262 5991

JAIPUR OFFICE: 203-204, JAIPUR TOWERS, M I ROAD, JAIPUR-302001

PHONE- 0091 141 405 1000 FAX- 0091 141 510 1757

GROUP COMPANIES

HEM FINLEASE PRIVATE LIMITED MEMBER-NSE

HEM MULTI COMMODITIES PRIVATE LIMITED MEMBER-NCDEX, MCX

HEM FINANCIAL SERVICES LIMITED

NBFC REGISTERED WITH RBI

www.hemonline.com

For Private Circulation Only 11 Hem Research

Disclaimer & Disclosure: This document is prepared for our clients only, on the basis of publicly available information

and other sources believed to be reliable. Whilst we are not soliciting any action based on this information, all care

has been taken to ensure that the facts are accurate, fair and reasonable. This information is not intended as an offer

or solicitation for the purchase or sell of any financial instrument and at any point should not be considered as an

investment advise. Reader is requested to rely on his own decision and may take independent professional advise

before investing. Hem Securities Limited, Hem Finlease Private Limited, Hem Multi Commodities Pvt. Limited,

Directors and any of its employees shall not be responsible for the content. The person accessing this information

specifically agrees to exempt Hem Securities Limited, Hem Finlease Private Limited, Hem Multi Commodities Pvt.

Limited or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and

further agrees to hold Hem Securities Limited, Hem Finlease Private Limited, Hem Multi Commodities Pvt. Limited or

any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by

the person accessing this information due to any errors and delays. The companies and its affiliates, officers, directors,

and employees, including persons involved in the preparation or issuance of this material may from time to time, have

long or short positions in, and buy or sell the securities there of, company (ies) mentioned here in and the same have

acted upon or used the information prior to, or immediately following the publication.

Analyst Certification

The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject

securities or issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly

related to the specific recommendations and views expressed by research analyst(s) in this report.

Disclosure of Interest Statement Company Name

1. Analyst Ownership of the Stock No

2. Hem & its Group Company Ownership of the Stock No

3. Hem & its Group Companies’ Director Ownership of the Stock No

4. Broking relationship with company covered No