Embed Size (px)

Citation preview

BENEFITS &COMPENSATION

INTERNATIONALT O TA L R E M U N E R AT I O N A N D

P E N S I O N I N V E S T M E N T

1

There are very few restrictions and/ordeterrents in terms of funding vehiclechoices available for employer medicalplans.

As it is such a fluid and sophisticated market, there aremany valuable lessons that can be learned from theemployers’ experience over time in trying to managewhat seems to be an insidious and irreversibleescalation of medical plan costs.

In this article, I aim to present:

– some important lessons that can be learned from theUS experience;

– the problems faced by multinational companies inmanaging their medical plan costs and liabilityexposure around the world;

– the limitations of the typical solutions that havebeen, and are being, applied;

– a brief summary of the trends and fundamentalfactors that will shape the 21st century landscape ofmedical plans; and

– suggestions for multinational companies in facingthe challenges ahead.

All these areas should be considered when managingmedical plan costs globally.

THE GLOBAL MEDICAL COST CONTROL CHALLENGEDespite the existence of robust social health careprograms in many countries, multinational employerssponsor supplementary medical plans in most locationswhere they operate. The cost of these programs hasbeen subject to alarmingly high medical unit costincreases over the last decade in virtually all countries,averaging more than five percentage points per annumin excess of retail domestic inflation levels.

My firm’s 2013/14 medical trend rate survey discloses acontinuation, if not an acceleration, of unit cost increases,as can be seen in TABLE 1 overleaf. Some small and mid-size US multinationals find that medical costs outside the

Managing Medical Plan CostsAround the World in the 21st Century

Wil J. Gaitán

Wil Gaitán is Senior Vice President and a Global Consulting Actuary at Aon Hewitt, where he isGlobal Benefits Practice Leader for the Midwest region. He previously spent 12 years with Buck Consultants as Global Consulting Actuary and Director for Latin America and Director of International Consulting operations in New York. He also worked with Watson Wyatt in the USA, the Far East and Europe in various senior roles for 17 years. Mr Gaitán has a BSc in Mathematics and a Master’s in Actuarial Science from Roosevelt University. A Fellow of the Conference of Consulting Actuaries, he is an Associate of the Society of Actuaries,an Enrolled Actuary and a Certified Compensation Professional with WorldatWork.

During the summer months many European benefitsmanagers can be found, along with the rest of Europe,soaking up the sun on Mediterranean shores.Meanwhile, their counterparts in the United States areexposed to a different form of heat.

For the past three decades, US benefits managers havebeen engaging in a different, less pleasant, annual ritualas they tackle high medical trend rates year after year.Their summer months have been consumed in anintense exercise of medical plan redesign and carriernegotiations. Executive management demands of “nostones unturned” efforts to mitigate escalating medicalcosts have become permanent annual fixtures.

The almost obsessive intensity of this annual planningprocess is understandable. The results are scrutinized bythe executive levels of every organization that sponsorsa medical plan, especially those with over 1,000participants. Basically, most of these medical plans areself-insured, and thus these companies are,fundamentally, part-time financial intermediaries ofhealth care services, in that they assume the attendantcost and liability risks implicit in their medical programs.

The occupational medical plan market in the USA isunique in comparison with other countries in thefollowing ways:

The USA is the only large economy in the world thatdoes not offer its citizens universal access to medicalcare. Cost shifting from the uninsured and theindigent, who only get partial subsidies from thegovernment, is a heavy burden being carried byprivate medical plans.

Medical benefit service pricing has not been subjectto legal ceilings or regulated pricing controls.

There is a significant layer of cost caused byinordinate malpractice insurance premiums.

Labor law is flexible relative to that of most othercountries. The employer is generally able tounilaterally adjust plan provisions in order to reducebenefits or require employees to share a higherproportion of the annual cost.

2

USA are still low relative to the alarming levels within theUSA, and thus have so far elected not to devote valuablemanagement time to an activity likely to yield low short-term financial gain. However, enlightened multinationalcompanies have recognized that the issue of employeehealth affects not just medical premiums, but disabilityand accident related costs as well as productivity costsdriven by turnover, absence and disengagement.

Recognizing the broader challenge, the majority ofmature multinationals have worked hard navigatingthrough a number of approaches targeting control ofrising health benefit costs. In a way, multinationalemployers are undergoing the same experiences in regardto the financial strategies that have been adopted in theUSA in that they have failed to produce long-term successin a consistent manner when measured on a global scale.

Some of the most popular measures that have beenadopted outside the USA include the following:

1. Tight local procurement of insurance. This avenue isgenerally the first recourse to most companies for haltinghigh premium increases. In some soft markets (caused bycarrier saturation, or due to many new carriers enteringthe market) such a technique has rendered some success.This approach eventually becomes relatively ineffective asmarkets stabilize and recurring adverse loss ratios mount.

2. Local self-insurance. This option has limitedapplicability in practice due to the lack of economies ofscale (as most multinationals only maintain a handful ofinternational locations with over 1,000 employees).Even when a company has the size and willingness toadopt this funding approach, actual execution isimpaired due to an often inadequate medical servicedelivery infrastructure at local level, or on account ofregulatory restrictions (except for a handful of countriesthat have a mature medical carrier market and enablinglegislation supporting self-insurance). Furthermore,many companies that have actually tried self-insurancehave in fact exacerbated the financial performance oftheir plans due to poor plan administration, especiallylax claim adjudication practices that emerge as the localsubsidiary management has more leeway for ad hocspecial cases.

3. Multinational pooling. According to my firm’s brokering experience data, pooling medical plans hasnot resulted in the up-front premium reductions that

would be expected from lower risk premium charges(which carriers assess in order to protect themselvesfrom adverse claim volatility). Furthermore, medicalplans are systematically being phased out ofmultinational pools, as nine out of every 10 medicalplans pooled in recent years have actually producednegative contributions to international dividends.

4. Captive reinsurance. Some companies elect to fundmedical benefits through a corporate captive. Most ofthese companies have other than pure cost control goals(tighter benefit governance, flexibility in planimplementation, corporate tax incentives on propertyand casualty reserves, etc.). Out of the companies thatfund benefits through a captive, most are very selectivein terms of including medical plans due to a number ofchallenges. First, there are few global carriers to frontthe risk locally with a robust medical service deliveryinfrastructure that competes with leading local players.Second, low potential for favorable underwritingexperience has to be tackled. Third, there can beexcessive transactional costs, as medical plans tend toexhibit frequent claims and insufficiently attractivefinancial upside from cash-flow improvements. Fourth,there are employee contribution considerations,including the respective fiduciary controls, andemployee consent requirements. Thus, using a captivein and of itself has not proven to be a viable long-termsolution for medical cost control.

5. Bulk purchasing across countries. This procurementtechnique for medical plans is often intrinsicallydiscouraged by local labor, tax and insurance laws thatrequire locally-admitted policies and adherence to localpricing norms, especially in light of employee cost-sharing features. Further barriers are a dearth of globalproviders with geographically widespread medical planofferings, and the multiplicity of plan designs acrosscountries which make pooled group pricing technicallychallenging or altogether impracticable.

It is instructive to note that none of the above measuresaddresses the demand challenge relating to healthclaims costs, nor the effectiveness of the care deliverysystem and instead companies try to minimize thefrictional costs caused by administration, insurance risktransfers, solvency and insurer profit.

Aside from the structural factors that are driving medicalcosts, there are exogenous factors that detract from an

TABLE 1

Region and country

GlobalNorth AmericaEuropeAsiaLatin America & CaribbeanMiddle East & Africa

2013 AnnualGeneral

Inflation Rate

%4.341.662.053.875.956.85

Nominal

%10.147.106.23

10.2012.8513.14

Real

%5.805.444.186.336.916.29

2014 AnnualGeneral

Inflation Rate

%4.231.762.044.215.855.93

Nominal

%10.348.505.94

10.1214.3512.28

Real

%6.116.743.905.918.506.35

Global Medical Trend Rates

2013 Annual Medical Trend Rates 2014 Annual Medical Trend Rates

Source: ‘2013/2014 Aon Hewitt Medical Trend Rate Survey’, 2013.

3

employer’s ability to manage medical costs downward,as follows:

1. Acquired rights. Acquired rights labor laws exist inmost international locations where multinationalsoperate. Essentially, these laws make it difficult orimpossible for a plan sponsor to amend existing plans inorder to introduce or harden cost-containment features,since these measures are seen as taking away benefitsalready earned by the employees. This effectivelyreduces the employer’s ability to fight the annualmedical trend through plan design changes.

2. Mounting regulatory requirements. Regulations toexplicitly or implicitly mandate employer sponsoredplans or to enhance medical plan coverage are rapidlyemerging. An example worth noting is Brazil, whereregulation has led to the following requirements. First,employers that offer medical plans must provide themto the entire workforce. Second, there is a “minimumplan” that has been dramatically expanded of late whichbans lifetime benefit maxima and eliminates exclusionsfor dreaded diseases (such as HIV). Third, certain specificexpensive medical procedures are mandated to becovered under the plan. Fourth, coverage is mandatoryfor same sex couples and domestic partners. Fifth, post-retirement benefit coverage is mandatory (albeit at theemployee’s full cost) for plans where the participant isrequired to share a portion of the premium.

As most multinationals know, the cornucopia ofregulations is by no means confined to Brazil. In fact,according to my firm’s 2012 global governance survey,health care and pension cost control and regulatorycompliance are top priorities for most multinationalemployers.

OCCUPATIONAL PLAN EXPERIENCE IN THE USAThe average annual employer cost of healthcare in 2012was approximately US$8,000 per employee – a 40% totalincrease in the last six years.

The corresponding annual average employee totalfinancial contribution to healthcare (out-of-pocket costsand payroll costs) was US$5,000 – a staggering 82%increase – over the same six-year period. The combinedcost has increased by a total of 52% and this is despite amyriad of strategies that have been implemented for thesake of cost-containment.

In order to appreciate these figures from the employee’sperspective, consider that the typical annual payincrease has averaged around 3%, compared with the10.5% annual average medical cost increase to theemployee over the past 10 years.

The increase in cost to employees has nearly erased theiraverage income gains over the same time period, whichmany consider a significant contributor to the wagestagnation over the past 10 years. In order to obtain abetter understanding of this unfortunate experience, abrief history of the evolution of occupational medicalplans in the USA is presented below.

Occupational medical plans in the USA began to emergeas a result of a 1942 law that limited wage increases butallowed employers to adopt employee benefit insuranceplans. These medical plans worked rather well until the

introduction in 1965 of the Medicare program forretired individuals. The Medicare program introduced:

– a fee-for-service reward structure for providers thatgenerated incentives for unnecessary volumes ofmedical procedures;

– adoption of “usual, customary and reasonable”rates, which essentially engendered uncontrolledwholesale price increases by providers; and

– a third-party payment system (the State) whichessentially removed the consumer’s ability to“bargain for best value.”

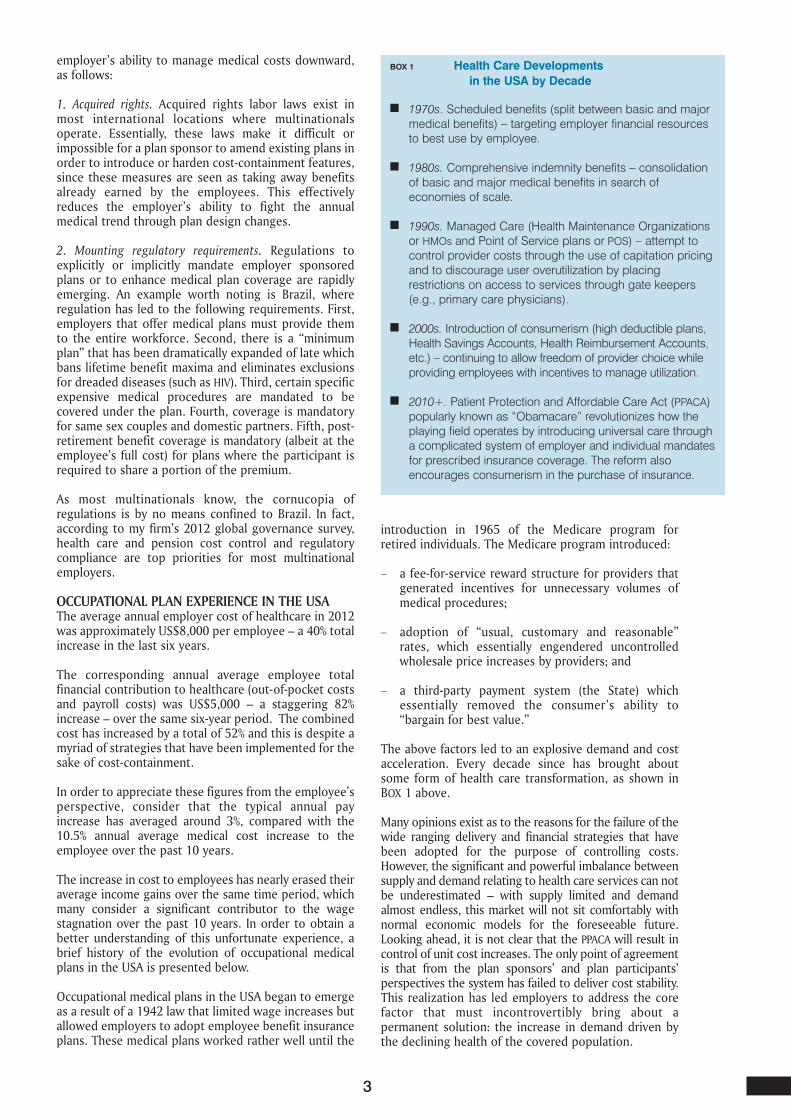

The above factors led to an explosive demand and costacceleration. Every decade since has brought aboutsome form of health care transformation, as shown inBOX 1 above.

Many opinions exist as to the reasons for the failure of thewide ranging delivery and financial strategies that havebeen adopted for the purpose of controlling costs.However, the significant and powerful imbalance betweensupply and demand relating to health care services can notbe underestimated – with supply limited and demandalmost endless, this market will not sit comfortably withnormal economic models for the foreseeable future.Looking ahead, it is not clear that the PPACA will result incontrol of unit cost increases. The only point of agreementis that from the plan sponsors’ and plan participants’perspectives the system has failed to deliver cost stability.This realization has led employers to address the corefactor that must incontrovertibly bring about apermanent solution: the increase in demand driven bythe declining health of the covered population.

BOX 1 Health Care Developmentsin the USA by Decade

1970s. Scheduled benefits (split between basic and majormedical benefits) – targeting employer financial resourcesto best use by employee.

1980s. Comprehensive indemnity benefits – consolidationof basic and major medical benefits in search ofeconomies of scale.

1990s. Managed Care (Health Maintenance Organizationsor HMOs and Point of Service plans or POS) – attempt tocontrol provider costs through the use of capitation pricingand to discourage user overutilization by placingrestrictions on access to services through gate keepers(e.g., primary care physicians).

2000s. Introduction of consumerism (high deductible plans,Health Savings Accounts, Health Reimbursement Accounts,etc.) – continuing to allow freedom of provider choice whileproviding employees with incentives to manage utilization.

2010+. Patient Protection and Affordable Care Act (PPACA)popularly known as “Obamacare” revolutionizes how theplaying field operates by introducing universal care througha complicated system of employer and individual mandatesfor prescribed insurance coverage. The reform alsoencourages consumerism in the purchase of insurance.

4

According to my firm’s 2012 health care survey and datafrom a 2010 World Economic Forum (WEF) study, the USAas a nation is becoming less healthy, but living longer onthe back of the advances in curative medicine.1 The maindrivers of worsening health are eight health risks andbehaviors (see FIGURE 1 above), including:

– poor diet, – physical inactivity, – smoking, – alcohol use, and – lack of health screening.

These risks drive the incidence and impact of the 15 most common chronic conditions, which in turn account for 80% of the total cost for all chronicillness worldwide. The impact of these 15 conditions onan employer’s medical spend typically exceeds 65% oftotal cost. By reducing the frequency and severity of themost costly medical conditions, employers can begin tocontrol health care costs, and improve employee healthand performance (see FIGURE 2 opposite).2 Employerswho can target and impact just three of the eight healthrisks can save as much as US$700 per employee per year.

FACTORS SHAPING THE MEDICAL PLAN LANDSCAPEIn my view, the following three factors will have a majorimpact on the cost structure of multinational companiesas related to medical plan expenditure and theopportunity cost of absenteeism on account of illness:

– transformation of the world economy with a powershift to emerging markets,

– aging of the world population, and

– growth of lifestyle risk factors around the world.

I will comment on each of these in turn.

Transformation of World EconomyMany studies have been published and much informationis available in the media regarding the economicdevelopment of China and India as well as Brazil andRussia. One of the most popular studies has beenproduced by Goldman Sachs, which first coined the term“BRIC” countries*. A later version of this study introduced11 other countries† which are projected to dominate theworld economy (see TABLE 2, also opposite). Multinationalcompanies are investing heavily in most of these countriesin order to penetrate their domestic markets – as opposedto merely exploiting cheap labor arbitraging opportunities.

Local talent pools of the type being sought bymultinationals are very shallow. Consider that 30% ofIndia’s population and 10% of Brazil’s are illiterate. Theproblem of finding, and then retaining, the type ofqualified staff fit to work in multinational companies isat the top of business challenges for companies seekingto expand in emerging markets.

Aside from technical skills, English language capabilitiesand on-the-job experience, roles that require analysis,independent thinking and taking control of situations

FIGURE 1 The 8-15-80 Rationale

1 – Diabetes2 – Coronary artery disease

3 – Hypertension4 – Back pain5 – Obesity 6 – Cancer7 – Asthma8 – Arthritis

Drive 15 chronic conditions

Accounting for80%

of total for allillnesses

9 – Allergies10 – Sinusitis

11 – Depression12 – Congestive heart failure13 – Lung disease (COPD)

14 – Kidney disease15 – High cholesterol

Poor diet

Physical

inactivity

Smok

ing

Lack of

health

screenin

gPoor stress

management

Poor standard

of care

Insufficien

tslee

pExc

essive

alcohol

8risks and behaviors

Source: 2010 World Economic Forum Study

* For further information, please see ‘Report on the BRICCountries’, B&C International, January/February 2008.

† For further information, please see ‘Report on EmergingEconomies – the Next 11’, B&C International, July/August2008.

5

are often culturally foreign to individuals in collectivist,risk averse societies such as China. As a case in point,India, Brazil, China, Mexico, South Africa and Turkey areall rated by the World Economic Forum as having“severe” employability challenges.

What makes matters worse, anecdotal evidence aboundsthat indigenous employers, especially in BRIC countries,

are making a sport of poaching staff from multinationalcompanies with inducements such as higher economicupside, rapid career advancement opportunities, andbetter cultural fit.

At the same time, social systems have failed to keep pacewith the increasing demands of an expanding middle class.Inadequate facilities, waiting lines, red tape, and poor

FIGURE 2 Annual Total Costs per Covered Employee of Typical Medical Plans

0

Italy

US dollars

Country

NOTE: Representative costs in US dollars (as at 31 December 2012) of Aon Hewitt progressive multinational clients

500

1,000

1,500

2,000

2,5002,345

Canad

a

1,926

France

1,854

United

Kingdo

m

1,666

Spain

1,162

Turkey

931

Russia

726

Mexico

647

Brazil

529

Malay

sia

406

Ukrain

e

278

Belgiu

m

186

Thailan

d

167

India

153

China

131

TABLE 2

Country

ChinaIndiaIndonesiaBrazilPakistanBangladeshNigeriaRussiaMexicoPhilippinesVietnamEgyptIranTurkeyRep. of KoreaTotal BRIC + N11USAEU

2010population

m1,3401,210238191171159155143112949180757449

4,181309492

2010 labor force

m780.0478.3116.5103.655.873.948.375.647.038.946.226.125.724.724.6

1,965155228

Geographicarea

sq km m9.6 3.31.98.50.80.10.9

17.12.00.30.31.01.60.80.1

48.09.84.3

2012 GDP

US$bn8,2271,825878

2,396232123269

2,0221,177250138257549795

1,15620,29315,68016,360

Economicgrowth 2013*

%7.505.005.102.006.106.106.302.201.707.005.202.20

–1.903.202.804.841.60–0.50

ProjectedGDP in 2050

US$bn70,71037,6687,010

11,3662,0851,4664,6408,5809,3403,0103,6072,6022,6633,9434,083

172,77338,51433,084

The Next 11 and the BRIC Countries vs. the USA and the EU

* according to ‘Economic and financial indicators’, The Economist, 2013

Source: The World Factbook, Central Intelligence Agency; Wikipedia; and ‘Global Economics Paper No: 153 – The N-11: More Than anAcronym’, Goldman Sachs, 2007

References1 1 ‘2012 Health Care Survey’, Aon Hewitt, 2012, and Global Agenda Council Reports 2010, World Economic Forum, 2010.1 2 ‘2012 Corporate Governance of Global Benefits Survey’, Aon Hewitt, 2012.

overall service quality are common features of emergingmarket social health care systems.

Individuals in the employable elite being keenly aware oftheir value do not hesitate to exercise their power todemand working conditions that best suit them, almostinvariably including supplementary medical benefits forthemselves and their dependents as part of their hiringpackages.

Population AgingIt is commonly known that the populations of the USA andEurope are aging rapidly as a result of the baby boomgeneration having been followed by decades of lowfertility. Even the rapid projected aging of China directlylinked to the one-child policy has been abundantlycovered in the press.

What is less commonly known is that population aging isa worldwide phenomenon with very few exceptions.

Two of the key impact areas for multinational employersare as follows:

Despite retirement ages increasing, net declines inworking-age population and shrinking labor supply areexpected.

There is increasing demand from employees foremployer sponsored medical and pension plans associal plans undergo severe financial stress and curtailtheir benefits.

In short, big projected increases in healthcare and long-term care can be expected.

Growth of Lifestyle Risk Factors Around the WorldLifestyle risk factors – sedentary lifestyle, poor diets, andhigher unmanaged stress levels – are growing globally.Alcohol and tobacco consumption are mature issues that,as people age, are becoming more of a problem andcontinue to be a challenge in many countries. These riskfactors lead to non-communicable diseases (cancer, andcardiovascular and respiratory conditions) or NCDs whichnow account for most deaths in the world. In short, theglobal burden of non-communicable diseases is alreadysignificantly greater than that of communicable diseases,and growing.

According to the WEF’s Annual Executive Opinion Survey,almost one half of all business leaders worry that at leastone non-communicable disease will hurt their company’sbottom line in the next five years. The largest concernscaused by NCDs are with cardiovascular disease and cancer.NCDs account for 63% of all deaths globally; and thus thesediseases are currently the world’s main killers.

The levels of concern are greatest among business leadersin low-income countries, in countries with poor qualityhealthcare and in those that offer low access to healthcare.

The problem goes far beyond the financials of medicalplans. The fact is that absenteeism and productivity losseson account of mortality and morbidity from NCDs areexpected to result in an estimated US$47 trillion in lostoutput in the next 20 years. This is equivalent to 5% of theworld’s GDP (in 2010 US dollars). Mental health andcardiovascular diseases account for over two-thirds of theprojected lost output.

The silver lining is that the magnitude of this expected losscan be significantly reduced through lifestylemodifications in the population in order to minimizeexposure to the above-mentioned risk factors. This silverlining extends to health-related benefits – reducing thehealth complications created by lifestyle risk is one optionthat does seem to address the fundamental issue ofexploding growth in demand for medical services.

CONCLUSIONSIn a world with a dwindling labor supply, lost productionfrom NCDs is not only an HR and Finance challenge but aserious strategic business issue.

Clearly, it will be crucial for employers to ensure thateffective health care benefits and health care education areavailable for all employees and their families, aimed at:

– preventing/reducing the future sickness experience,

– providing high quality health care treatment whenneeded;

– facilitating the management of chronic healthconditions;

– educating the global workforce on the benefits ofhealthcare and good health; and

– encouraging healthy behaviors.

As learned from the US experience, standard cost-management approaches will be insufficient to addressinganticipated future spiraling medical costs. The playingfield will become even more challenging and employerswill have to learn how to face projected lost productionfrom ill health and premature mortality resulting frompreventable conditions.

In conclusion, maintaining a healthy workforce will notonly be the way to solve the medical cost increaseconundrum, but, moreover, it will be a business imperativefor corporate success and survival. Ω

Copyright © Pension Publications Limited 2014.

Reproduced from Benefits & Compensation International, Volume 43, Number 6, January/February 2014.Published by Pension Publications Limited, London, England.

Tel: + 44 20 7222 0288. Fax: + 44 20 7799 2163. Website: www.benecompintl.comProduced by The PrintZone (www.theprintzone.co.uk).

![BENEFITS & COMPENSATION INTERNATIONAL1].pdf · United States who are US citizens, ... qualified deferred compensation plan”. ... Benefits & Compensation International• 2](https://img.pdfslide.us/doc/110x75/5b69676e7f8b9ab0128e2df1/benefits-compensation-1pdf-united-states-who-are-us-citizens-qualified.jpg)

![Compensation & Benefits[1]](https://img.pdfslide.us/doc/110x75/577d369f1a28ab3a6b938bc4/compensation-benefits1.jpg)