Embed Size (px)

Citation preview

Beneficial owners The new challenge in due diligence

Introducing:

Don Andrews Venable LLP

Steve Holm-Hansen Synchrony Financial Shelleyanne Rein Experian

©Experian 3

Regulatory enforcement is top of mind

4/13/2017

“The number of enforcement

actions rose 75% while

the total dollar amount of

penalties assessed was up

a dramatic 431% between

2011-2015 when compared

with the five-years prior.”

Experian Public Vision 2017

©Experian 4

It’s getting personal

4/13/2017 Experian Public Vision 2017

Source: blog.wsj.com, Jan 2016

©Experian 5

1. What is the Financial Crimes Enforcement Network (FinCen) ruling? How does it effect you?

2. Understanding the beneficial owner

3. How Synchrony is preparing for their customer due diligence

4. Verifying the beneficial owner

Contents

4/13/2017 Experian Public Vision 2017

©Experian 6

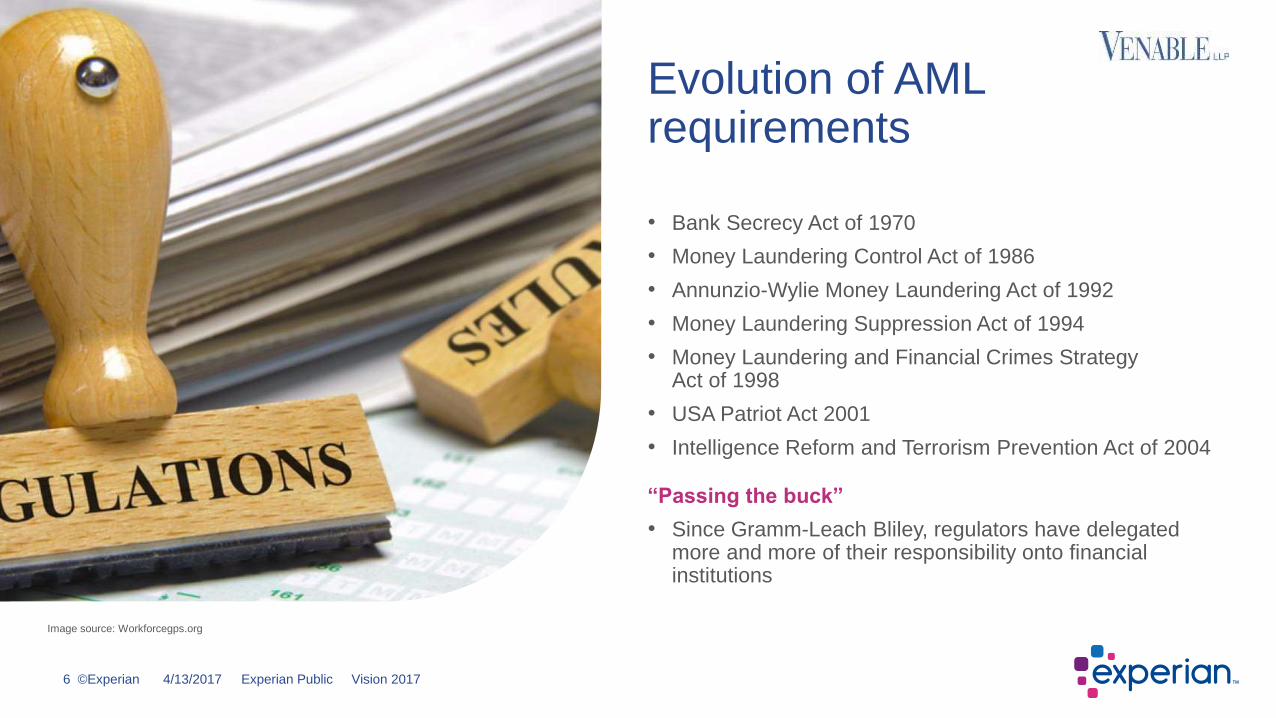

• Bank Secrecy Act of 1970

• Money Laundering Control Act of 1986

• Annunzio-Wylie Money Laundering Act of 1992

• Money Laundering Suppression Act of 1994

• Money Laundering and Financial Crimes Strategy Act of 1998

• USA Patriot Act 2001

• Intelligence Reform and Terrorism Prevention Act of 2004

“Passing the buck”

• Since Gramm-Leach Bliley, regulators have delegated more and more of their responsibility onto financial institutions

Evolution of AML requirements

4/13/2017 Experian Public Vision 2017

Image source: Workforcegps.org

©Experian 7

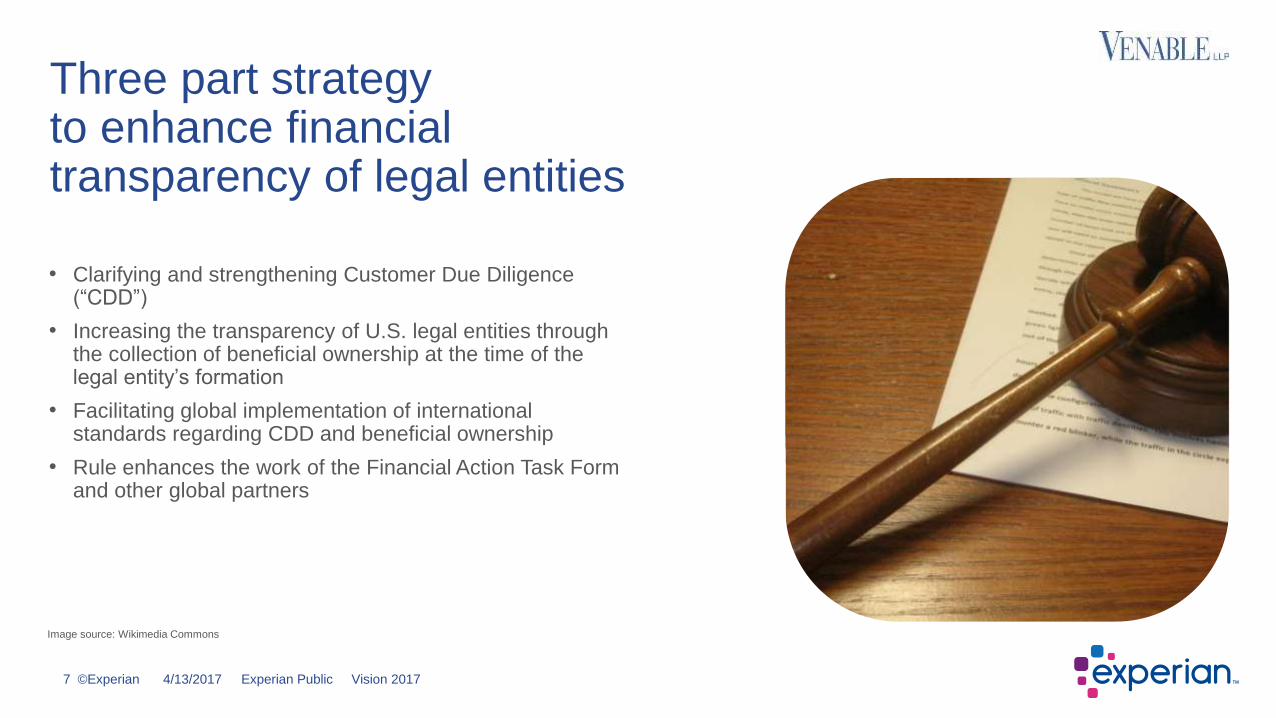

• Clarifying and strengthening Customer Due Diligence (“CDD”)

• Increasing the transparency of U.S. legal entities through the collection of beneficial ownership at the time of the legal entity’s formation

• Facilitating global implementation of international standards regarding CDD and beneficial ownership

• Rule enhances the work of the Financial Action Task Form and other global partners

Three part strategy to enhance financial transparency of legal entities

4/13/2017 Experian Public Vision 2017

Image source: Wikimedia Commons

©Experian 8

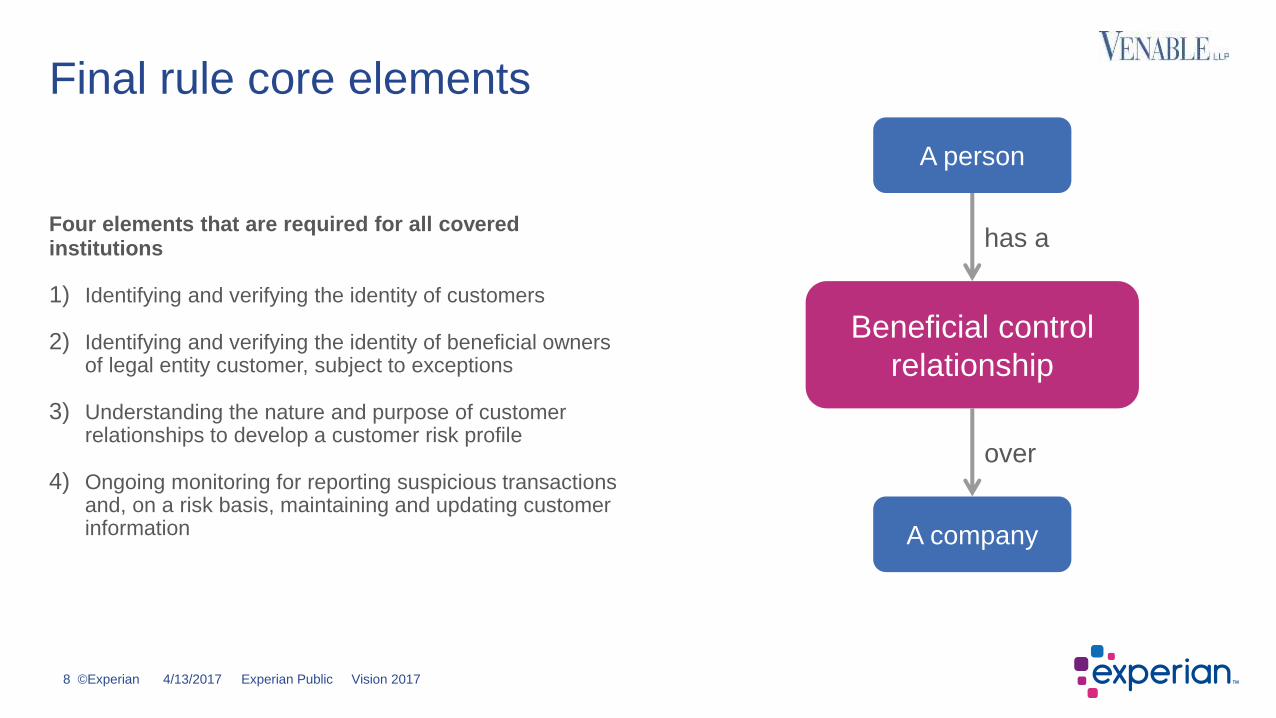

Four elements that are required for all covered institutions

1) Identifying and verifying the identity of customers

2) Identifying and verifying the identity of beneficial owners of legal entity customer, subject to exceptions

3) Understanding the nature and purpose of customer relationships to develop a customer risk profile

4) Ongoing monitoring for reporting suspicious transactions and, on a risk basis, maintaining and updating customer information

Final rule core elements

Experian Public Vision 2017 4/13/2017

A person

A company

Beneficial control

relationship

has a

over

©Experian 9

• Covered institutions must comply with the

Final rule by May 11, 2018

• On that date, covered institutions must

implement “written procedures that are

reasonably designed to identify and verify

the identities of beneficial owners of legal entity

customers at the time the new account is

opened, subject to exceptions

• Covered institutions are banks, U.S branches

of foreign banks, federally insured credit

unions, savings associations, Edge Act

corporations, broker – dealers, futures

commission merchants, introducing brokers

in commodities

Experian Public Vision 2017 4/13/2017

Image source: Stephen Melkisethian_Flickr

©Experian 10

• Currently required / not new

– Identify and verify the individual consumer

– Identify and verify the legal entity as a whole

• New component

– Identify and verify each individual with 25% or greater ownership in the legal entity

– Identify and verify ONE individual with significant responsibility for managing the legal entity

• Not new/were added (by FinCEN) for clarity

– Understand relationship risk of legal entity

– Understand relationship risk of individual consumer

• Not new/were added (by FinCEN) for clarity

– Ongoing monitoring of legal entity

– Ongoing monitoring of individual consumer

What is changing and why?

4/13/2017 Experian Public Vision 2017

Image source: Workforcegps.org

©Experian 11

Two-prong test

• Ownership prong: Are you an individual who owns, directly or indirectly 25% or more of the equity interests of a legal entity

• Control prong: Does your responsibility at the firm, corporation or entity amount to a form of control?

– If 25% of more is owned by a trust, the Trustee needs to be identified

So what is a beneficial owner?

Experian Public Vision 2017 4/13/2017

©Experian 12

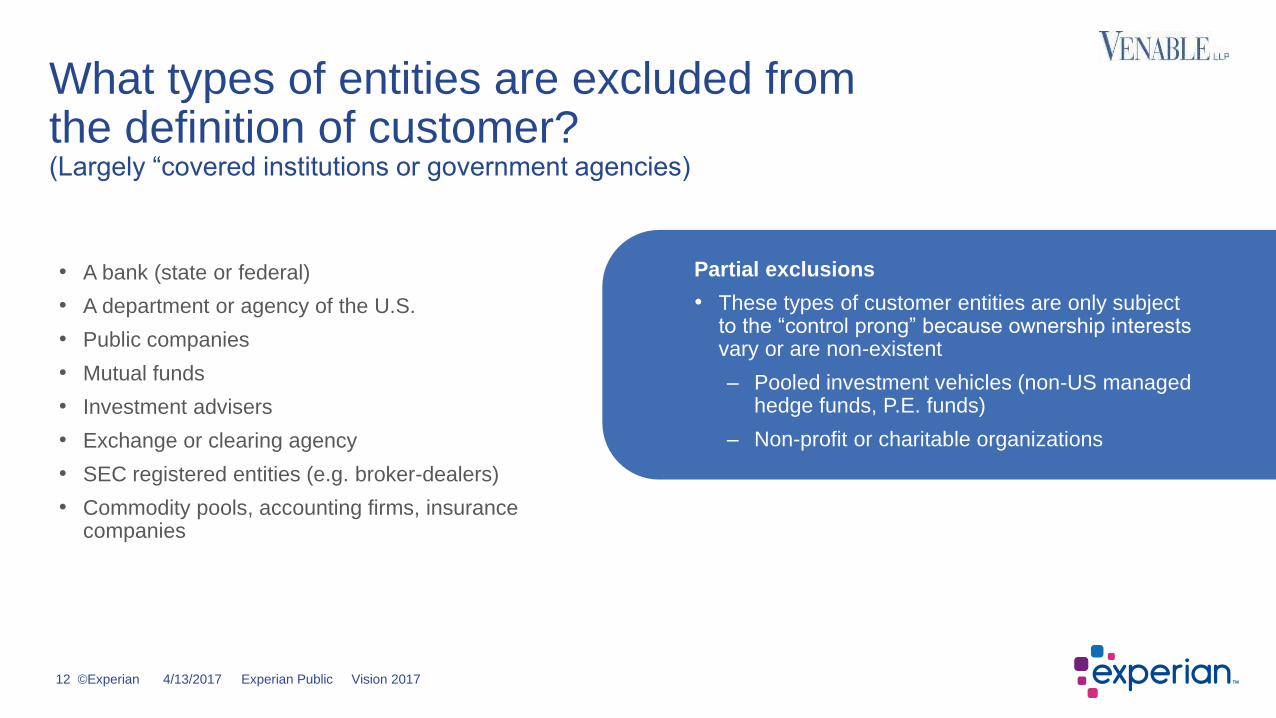

What types of entities are excluded from the definition of customer? (Largely “covered institutions or government agencies)

4/13/2017 Experian Public Vision 2017

• A bank (state or federal)

• A department or agency of the U.S.

• Public companies

• Mutual funds

• Investment advisers

• Exchange or clearing agency

• SEC registered entities (e.g. broker-dealers)

• Commodity pools, accounting firms, insurance companies

Partial exclusions

• These types of customer entities are only subject to the “control prong” because ownership interests vary or are non-existent

– Pooled investment vehicles (non-US managed hedge funds, P.E. funds)

– Non-profit or charitable organizations

©Experian 13

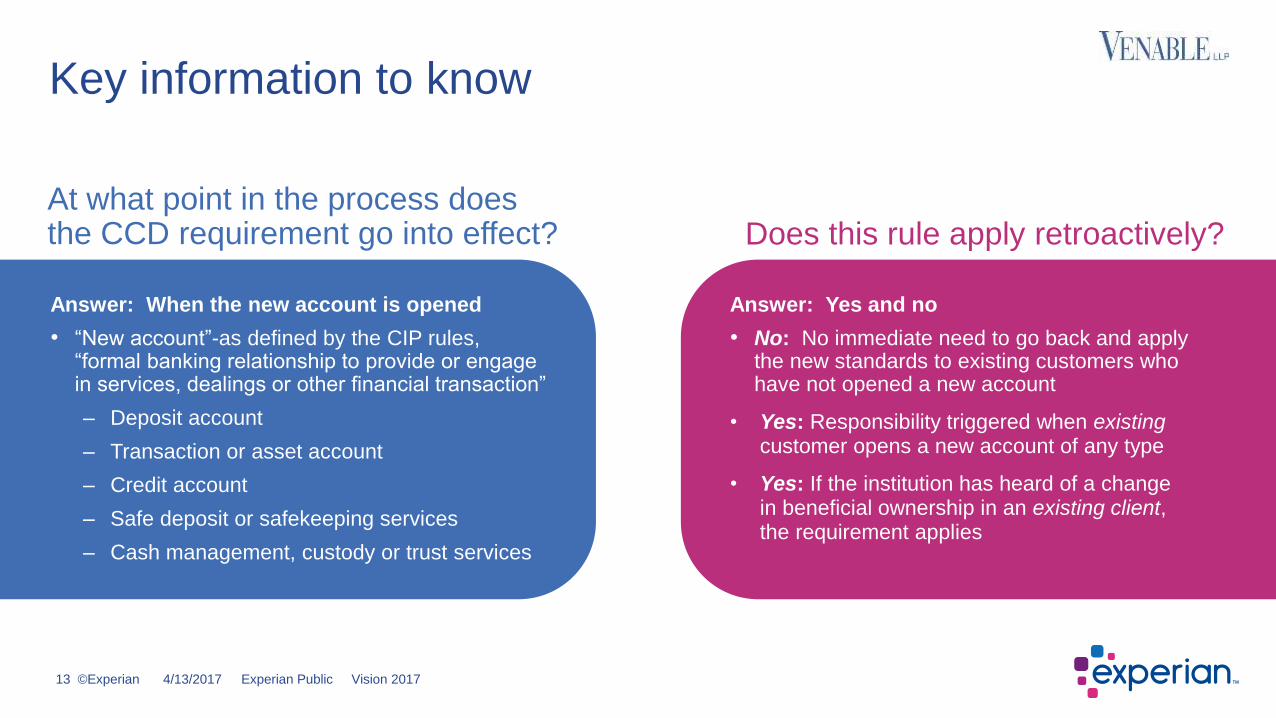

Key information to know

4/13/2017 Experian Public Vision 2017

Answer: When the new account is opened

• “New account”-as defined by the CIP rules, “formal banking relationship to provide or engage in services, dealings or other financial transaction”

– Deposit account

– Transaction or asset account

– Credit account

– Safe deposit or safekeeping services

– Cash management, custody or trust services

At what point in the process does the CCD requirement go into effect?

Answer: Yes and no

• No: No immediate need to go back and apply the new standards to existing customers who have not opened a new account

• Yes: Responsibility triggered when existing customer opens a new account of any type

• Yes: If the institution has heard of a change in beneficial ownership in an existing client, the requirement applies

Does this rule apply retroactively?

©Experian 14

Covered institution must be able identify the beneficial owners of each legal entity customer at the time the new account is opened by either certification or CIP

Two methods: Certification and traditional CIP

Certification consists of:

1) Obtaining a certification from the individual opening the account on behalf of the legal entity; or

2) Obtaining from the individual the information required on the certification by another means, provided that the individual certifies that the information is accurate;

3) CIP is the means of identifying beneficial owners by existing Customer Identification Program requirements already in place

CDD identification requirements

4/13/2017 Experian Public Vision 2017

©Experian 15

Customer information required: (risk – based approach)

• Name, date of birth (for individuals), address, identification number, or more information depending upon the nature of the client

• Bank must do enough verification to “form a reasonable basis” that it knows the identity of the customer

• For non-individual, principal place of business or physical location

• Bank’s procedures must describe the required documentation, non-documentary procedures or both

Traditional CIP requirements

4/13/2017 Experian Public Vision 2017

©Experian 16

Documentary verification

• Expectation that the institution will rely on an “unexpired” form of photo documentation

• Evidence of customer’s nationality or residence

• Bank encouraged to have more than one form of identification given possibility of fraudulent documents

• For corporations: certified articles of incorporation, unexpired business license, partnership or trust agreement

Two forms of verification

4/13/2017 Experian Public Vision 2017

Non-documentary evidence

• Methods include contacting a customer, information obtained from a consumer reporting agency, or public database

• Checking references, obtaining a financial statement

• Must address special circumstances, such as individual not appearing in person, no unexpired identification

• Controls must address issues on a risk-adjusted basis

• Procedures must also address instances where bank cannot verify identity and thus will not open an account

©Experian 17

Answer: To be utilized in the same manner as current account owner information

• OFAC requirements

• Currency transaction reporting requirements

• Recordkeeping requirements (5 years)

• Now the “five pillars” as opposed to the “four pillars”

– Establishment of internal policies and procedures, controls reasonably designed…

– Designation of a CCO to monitor compliance

– Independent testing

– Training

What is the point of obtaining “beneficial owner” information?

4/13/2017 Experian Public Vision 2017

©Experian 18

• Establishment of internal policies and procedures

• Designation of a CCO to monitor compliance

• Independent testing

• Training

From four to five pillars…

4/13/2017 Experian Public Vision 2017

The “fifth pillar” • Risk assessment now codified

• Risk-based procedures to for conducting ongoing CDD

– Understanding the nature and purpose of customer relationships

– Conducting ongoing monitoring to identify and report suspicious transactions and to update customer information (including beneficial ownership)

©Experian 19

The rules are already in effect:

• FinCEN has made it clear that it believes that the CDD obligations for legal entities are de facto already in effect

• Closely linked to a bank’s existing monitoring AML obligations.

• FinCEN has indicated that the federal banking regulators are authorized to impose more stringent requirements on regulated banks

• Banks should implement as soon as possible

Operational challenges It’s already the law!

4/13/2017 Experian Public Vision 2017

Image source: Workforcegps.org

©Experian 20

• Third party institutions may wish to perform enhanced DD before providing certifications causing delay in establishing accounts

• Contractual obligations of third parties should conform to current legal requirements

• CDD requirements for lending banks will be affected and result in need for significant enhancements: contract and disclosure documents require update

• Differing requirements for IRS beneficial ownership vs. CDD beneficial ownership per bank regulators

Third party certifications Severe civil and criminal penalties could lead to chilling effect

4/13/2017 Experian Public Vision 2017

©Experian 21

• Lending banks will need to re-consider degree of CDD for beneficial ownership

• Underwriting may require stronger controls and greater transparency

• 10% or 25%? Bank regulators normally consider 10% ownership a presumption of control

• New contractual standards in loan documents for CDD

• Amend documentation as soon as possible given the regulatory view that the rules are “already in place”

Lending issues

Experian Public Vision 2017 4/13/2017

©Experian 22

• Reputation: AML fines have skyrocketed from the landmark case of $24 million into the billions

• Standard has moved from “scienter” to negligence or “should have known”

• Under new rule: False certifications involve fine of $1,000,000 or “imprisoned not more than 30 years or both..”

• Senior managers now responsible for AML / BSA

• Period of adjustment to the new reality

• Attorneys will need to adjust documentation to affect the new reality

• Client acceptance procedures will require greater transparency and documentation

• Greater need for investigative services to understand structure of corporate entities and individual backgrounds

What’s at stake?

Experian Public Vision 2017 4/13/2017

©Experian 23

• Review all legal paperwork and conform to the new standards

• Initiate a new client acceptance process that includes senior management

• Document clients that were rejected as well as accepted

• Prepare for possibility that regulators will impose a stricter standard of “control”

Immediate steps to consider

4/13/2017 Experian Public Vision 2017

©Experian 24

FinCen Ruling from a client perspective How Synchrony Financial is preparing for the ruling

4/13/2017 Experian Public Vision 2017

©Experian 25

• Identify the types of accounts falling under the rule

• Understand exemptions to the rule

• Understand the applicant / customer impact

• Understand the business impacts

• Understand impact and gaps to credit systems and processes

Key considerations of the Beneficial Owner Rule

4/13/2017 Experian Public Vision 2017

Ensure you have all the right teams in place

to successfully implement

©Experian 26

The complexities

of finding and maintaining

the beneficial owner

in a sea of regulations

4/13/2017 Experian Public Vision 2017

©Experian 27

Common client problems Regulatory compliance and fraud detection

4/13/2017 Experian Public Vision 2017

Client problems

Regulatory

KYC violations carry billions

of dollars in criminal and civil

fines, possible jail time and

negative company press

Conducting KYC

on businesses and

beneficial owners to

as well as identifying shell

companies, shelf companies

and commercial identity theft

can be costly and both in

dollars and resources

Manual review and requests

for additional documentation

to meet regulatory

requirements may create

significant friction at the

point of sale

Need to use analytics,

automation and workflow

efficiencies to reduce

customer acquisition

costs and enhance

customer experience

while mitigating risk

Economic Customer Technology

©Experian 28

Beneficial owner matching

Challenges:

Identification and verification of potentially multiple beneficial owners to meet FinCEN final rule

• Up to 5 identities may need to be verified for a single legal entity

– 47% of AML shops plan to verify beneficial ownership to 25%

– 26% of AML shops plan to verify beneficial owners to 10%

What is needed for customer due diligence?

4/13/2017 Experian Public Vision 2017

*Source: Dow Jones and ACAMS Global Anti-Money Laundering Survey 2016

©Experian 29

• Business identities

• Complex

• Identifiers more challenging

– Tax IDs – Federal and State (the government doesn’t make FEINs readily available)

– Name – Legal and trade

– Address – Headquarters/branch, parent / subsidiary

• Different business structures (i.e. corporations vs. sole proprietors)

• Names may include special characters (e.g. @, &, etc.) impacting matching

Complexities in authenticating business vs. consumer identities

4/13/2017 Experian Public Vision 2017

©Experian 30

• Identity verification (Are they who they say they are?)

• Business age and activity level

• Registration and business structure

• High risk address conditions

• Presence on watch lists (OFAC, EPLS)

• Multiple entities associated to business phone or address

• Business affiliations

• Indicators of financial stability

Finding Waldo Identifying the beneficial owner

4/13/2017 Experian Public Vision 2017

*Source: U.S. Census

©Experian 31

• Understand the nature and purpose of customer relationships to develop a customer risk profile – For both consumer and business

• Ongoing monitoring for reporting suspicious transactions and, on a risk basis, maintaining and updating customer information

– For both consumer and business

Beneficial owner and not a straw man

4/13/2017 Experian Public Vision 2017

©Experian 32

Business activity

• Inquiry activity

• Public record updates

• Trade activity

• Disputes

• Financial instability

Business structure

• LLCs

• Sole Props

• Nonprofits

Additional business activity and structure risk indicators

4/13/2017 Experian Public Vision 2017

©Experian 33

1. Collect detailed information on businesses and beneficial owners

2. Utilize confidence scores and decision strategies

3. Match codes that identify quality of match in addition to other attributes

4. Probabilistic match score that provides proximity between the input data and data on file

5. Set appropriate match thresholds to ensure accuracy and minimize manual review

Key elements to successful compliance

4/13/2017 Experian Public Vision 2017

©Experian 34

1. Understand the requirements and how they pertain to your company

2. Balance customer experience with securing the right data to optimize your verification process

3. Work with your compliance department to set responsible match cut-offs

4. Adopt a risk-based strategy, applying additional fraud checks to keep fraudsters out of your portfolio

There is no silver bullet Regulatory compliance and fraud prevention require a balanced approach

4/13/2017 Experian Public Vision 2017

©Experian 35

Experian contact:

Shelleyanne Rein [email protected]

Questions and answers

4/13/2017 Experian Public Vision 2017

©Experian 36

Share your thoughts about Vision 2017!

4/13/2017 Experian Public Vision 2017

Please take the time now to give us your feedback about this session.

You can complete the survey at the kiosk outside.

How would you rate both the Speaker and Content?

![Definitions · Web viewShared ownership agreement residential property Dated:[date] [Names of all Owners] Contents Definitions Interpretation Terms of beneficial interest Relationship](https://img.pdfslide.us/doc/110x75/5abfef9c7f8b9ab02d8ec153/definitions-viewshared-ownership-agreement-residential-property-dateddate-names.jpg)