Embed Size (px)

Citation preview

BenchmarkingTechniques & Application

Benchmarking

• Used to identify standards that are critical to a company’s success

• Used to compare:– Actual Performance– Determination of gaps

in performance– Implementation of

improvements

• External benchmarks are typically best practice

External Benchmarking

Productivity Measures• Productivity- ratio of outputs achieved to inputs into

production

• Objectives of Productivity Measures:– Were all inputs used needed to produce the actual

output?– Was the best mix of inputs used?

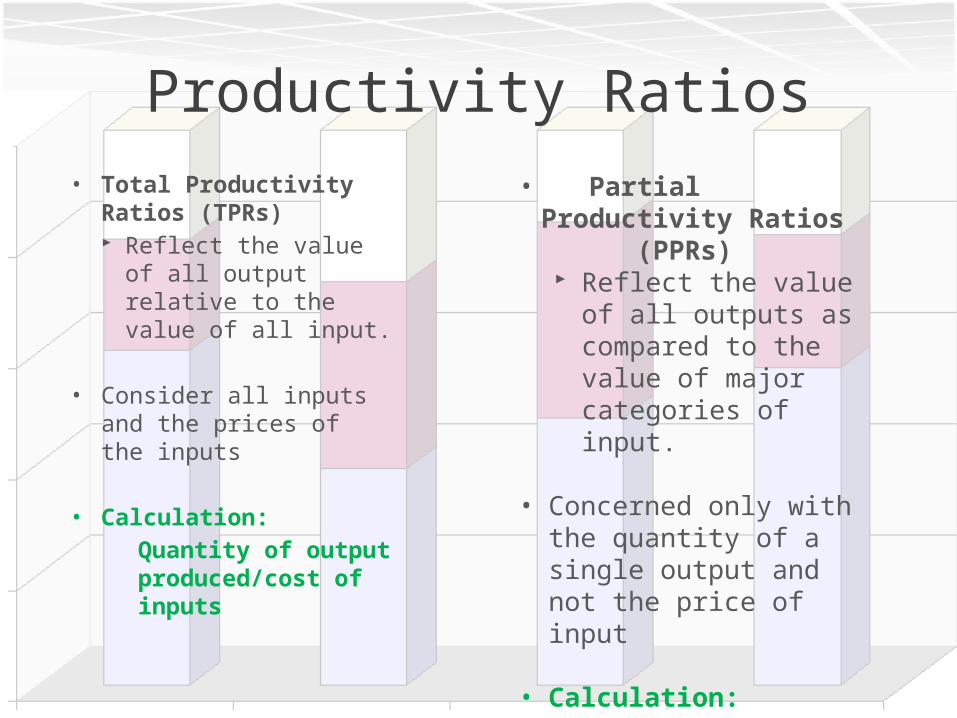

Productivity Ratios• Total Productivity Ratios

(TPRs) Reflect the value of all

output relative to the value of all input.

• Consider all inputs and the prices of the inputs

• Calculation: Quantity of output produced/cost of inputs

• Partial Productivity Ratios (PPRs)

Reflect the value of all outputs as compared to the value of major categories of input.

• Concerned only with the quantity of a single output and not the price of input

• Calculation:Quantity of output produced/quantity of the single input used

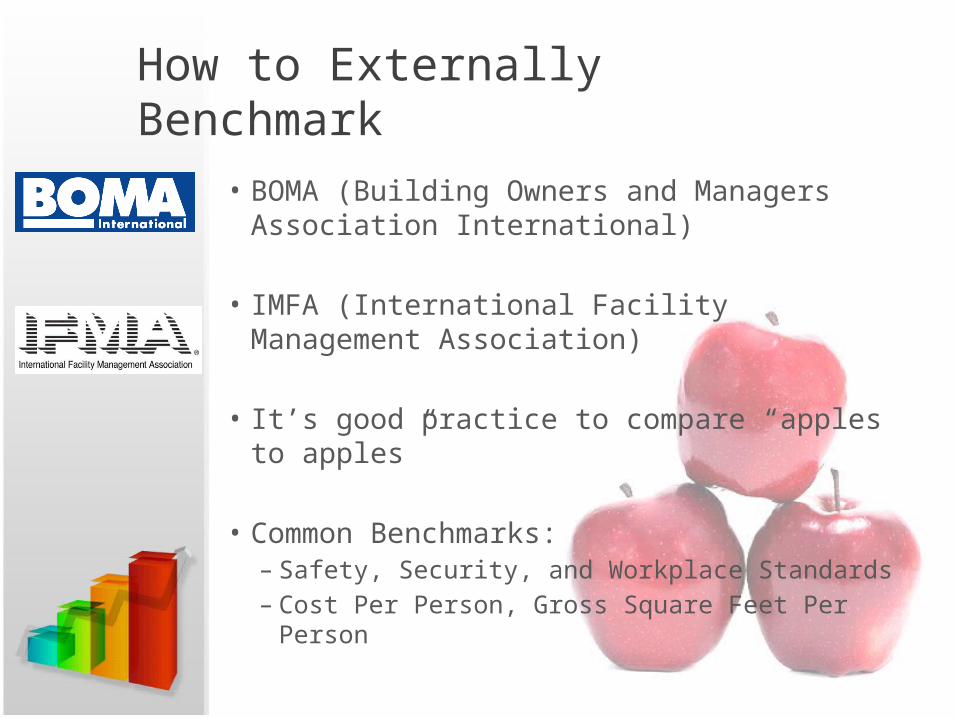

How to Externally Benchmark

• BOMA (Building Owners and Managers Association International)

• IMFA (International Facility Management Association)

• It’s good practice to compare “apples to apples”

• Common Benchmarks:– Safety, Security, and Workplace Standards– Cost Per Person, Gross Square Feet Per Person

Internal Benchmarking

Monitoring & Investigative Techniques:

1. Control Charts

2. Pareto Diagrams

3. Cause & Effect (Fishbone) Diagram

Internal Benchmarking

1. Control Chartsa. 3 Basic Componentsb. Common Cause, “noise”c. Special Cause, “signal”

Internal Benchmarking

2. Pareto Diagramsa. Useb. Interpretation

Internal Benchmarking3. Cause and Effect Diagram• “Fishbone Diagram”

1. Machinery2. Method3. Materials4. Manpower5. Measurements6. Environment

Process Improvements & Activity-Based Management

1. Activity Based Costing

a. Allocating Costs

b. Identifying Necessary Activities

c. Process

d. Determining Driving Costs

e. Companies with Multiple Products

f. Pricing and Outsourcing Decisions

Process Improvements & Activity-Based Management

2. Activity Based Management

Using ABC to determine…

a. Where are Overhead Costs Allocated?

b. Should we Outsource Processes?

c. Should Prices Change?

Process Improvements & Activity-Based Management

3. Cost Identification

a. Value Adding vs. Non-Value Adding Activities

b. Exact Costs of Each Unit

c. Cost Data by Activity

Title

Title

![CorrespondenceUsing caching and optimization techniques to ... · Apache benchmarking The Apache webserver comes with a benchmarking pro-gram, ab [7], which can be used to analyze](https://img.pdfslide.us/doc/110x75/5ee08cffad6a402d666bb764/correspondenceusing-caching-and-optimization-techniques-to-apache-benchmarking.jpg)