Embed Size (px)

DESCRIPTION

Professional Home Buyer Guide by Ben Orozco

Citation preview

The Professional Home Buyer Guide

Your Real Estate Consultant

Ben Orozco ABR, Licensed Associate

RE/MAX Professionals 7111 West Bell Road, Suite 101 Glendale, Arizona 85308 NatesHomes.com 602-942-7000

A Few Words From Your Real Estate Consultant

Congratulations!

You are about to embark on the exciting and rewarding journey to homeownership! Whether it’s your first home, retirement, dream or an investment property, our Team of Professionals, will strive to make the experience one you will want to tell your friends and family about. As the real estate market becomes more advanced (and even more complex), we are continuing to improve our services and add to our marketing insight. Being informed of the current Real Estate Market allows us to custom design our services especially for your needs. We understand this is a big undertaking, no matter how many homes you may purchase in a lifetime. We believe that in order for you to feel comfortable during this process you will need to be well-equipped and armed with up-to-date information. This guide contains information about myself, our team, the home-buying process, as well as other valuable reading material to make your experience that much easier. With our Professional Home Buyer’s Guide you will know what to expect every step of the way. Also included are important phone numbers, time-lines and even a helpful moving checklist. You may also refer to the glossary of terms to familiarize yourself with terminology you may hear during the course of your home buying process. On behalf of the Nate Martinez Team, let me be the first one to congratulate you on your decision to purchase a home. We look forward to be your real estate guide on this exciting journey! Your Real Estate Consultant, Ben Orozco, ABR (602) 697-3360 direct [email protected]

“The journey of a thousand miles begins with one step”

RE/M

AX

Professionals

Why Choose The Nate Martinez Team?

“It’s Our Pleasure!”

Buying a home can be a complicated business. Mistakes could literally cost you thousands of dollars or the missed opportunity of owning the home of your dreams. As a buyer, you are always in competition with the other buyers who are also looking to buy their dream home. There is a vast difference in the level of expertise and quality of service provided by real estate agents. Give yourself the advantage of working with the Very Best ... work with Nate’s Team and get these value-added services that will make a lasting difference in your home buying experience.

1.) A Highly Trained Team of Specialists: Our team is set up to provide award-winning service from the very first phone call you make to our office. Each of our members work together as a “team” to make sure that all of the important details of your home purchase process are handled professionally, proficiently and with a personal touch. Our highly trained real estate consultants focus on nothing else but finding the perfect home for you, while our administrative team members are specialized by department to ensure support, organization and efficiency to you and your real consultant.

2.) Expert Negotiation Skills: Nate’s Team has helped over 3,000 families buy or sell a home in the Phoenix metro area over the last quarter of a century. This level of success is a testimonial to the expertise and negotiating skills that give any clients working with our team a major advantage over buyers working with other agents. Collectively, Nate’s team has close to 100 years of real estate experience - what does this mean for you? Well, simple, that if your real estate consultant doesn’t know the answer, someone on the team does!

3.) Reputation Talks: Over the years, Nate’s team has earned a reputation built on merit, achievement, reliability, honesty and integrity. We strive to provide an experience that our clients will want to tell their friends and family about. Additionally, we work hard to maintain a good reputation with our fellow industry colleagues. Because we value the relationship with other Valley Realtors, this will ultimately help you during the negotiation process.

4.) The Largest Inventory of Homes For Sale: Our team carries a large inventory of bank owned homes, resale, short sale and land listings. We pride ourselves on featuring move-in ready properties, which are priced competitively. When shopping for a home, we can assist you not only with our available inventory but also all other properties for sale through the Multiple Listing Service (MLS), new construction and those listed For Sale By Owner.

Our Professional Pledge

“Exceeding all your expectations is our Mission!”

To help you find your home in the shortest time, at the best price and terms, with superior service, we pledge the following to you:

♦ Explain real estate agency relationship ♦ Maintain communication during the term of the agreement ♦ Analyze your property needs and desires ♦ Orient you to the current market conditions ♦ Provide helpful community data ♦ Explain local real estate practices and procedures ♦ Provide information on lenders and financing alternatives ♦ Search the local Multiple Listing Service (MLS) for properties that meet your criteria ♦ Coordinate appointments and show all properties of interest, whether or not the properties are listed by the Nate Martinez Team

♦ Provide relevant market data to determine fair market value of homes ♦ Explain the offer and negotiation process ♦ Deliver required Property Disclosure Forms when applicable ♦ Carefully explain and prepare all paperwork required to make an offer ♦ Arrange to present all offers to seller in a timely manner ♦ Strive to obtain the best possible price and terms for you ♦ Explain post-purchase activities and responsibilities ♦ Follow-up on all post-purchase activities ♦ Keep confidential any information you designate in writing as confidential ♦ Explain the Buyer Advisory and “For Your Protection Get A Home Inspection”

To make this pledge official, let's all sign on the dotted line!

______________________________________________________ __________________________________ (Please sign) (Date) ______________________________________________________ __________________________________ (Please sign) (Date) ______________________________________________________ __________________________________ (Your Real Estate Consultant) (Date)

Your Team Of Experts

The Nate Martinez Team has multiple departments which we have designed to provide the best real estate experience for not only our sellers but for our buyer clients as well. Our team of experts is a finely tuned, well oiled machine, ready to service ALL your real estate needs!

♦ Nate Martinez ~ Owner/Agent, ABR, CRS, GRI, CRP, CDPE, CLHMS, ePRO, SFR ♦ Licensed Associates ~ Your Real Estate Consultants: Ben Orozco, ABR Darren Burrup Brandi Martinez, CDPE Sarah Bliss, ABR, ePRO Nathan Martinez, JR Nicole Froats ♦ Administrative Departments: Buyer Closing Coordinator Listing Manager Short Sale Negotiator Full Service REO Department Field Inspectors ♦ Industry Affiliates:

Title/Escrow Company Loan Officer Home Inspection Company Home Warranty Company Termite Inspection Company Handyman Services

Your Home Wish List

For the Following Rank Importance: 3= Must Have 2= Desirable 1= Not Important

Community Services Child care services available 3 2 1 YMCA/park district facilities 3 2 1 Churches 3 2 1 High-quality healthcare 3 2 1

Convenience Close to present or future jobs 3 2 1 Near grocery and other stores 3 2 1 Parks/play areas 3 2 1 Easy freeway access 3 2 1

Neighbors Relatives/friends in the neighborhood 3 2 1 Children for your kids to play with 3 2 1 Active community groups 3 2 1

HOME REQUIREMENTS:3 Price range? $_______________to $_________________ Down Payment: $ ________________________ What home styles do you prefer? Single Family / Townhouse / Condo / Patio Home / Other Single Story / 2 Story / No preference Age of home or new construction? __________________

How many bedrooms? _________________ How many bathrooms? Square feet?_____________________ Specific Subdivision? _____________________________________ Pool? (yes / no) Community Pool? (yes / no) No preference on pool? (yes / no) Spa? (yes / no) Parking? _______________________________ Lot Size? ________________________________________ RV Parking? (yes / no) Fireplace (yes / no) Formal Living/Dining Rooms? (yes / no) Please list any other special features you consider important for your home purchase: ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________

Important Information You Need To Know

A personal consultation will help your real estate consultant find you the type of home that meets your needs. In most cases, you will need to meet with one of our loan officer affiliates in order to determine what price range that will be suitable based your personal financial situation. The following information will be important to share with your loan officer:

1.) How much of your savings you intend to use toward down payment and closing costs. 2.) Your annual gross income (before taxes). 3.) The length of time with your current employer and previous employers, for the past 2 years. 4.) Your monthly payments on long term debts (such as a car payment) and credit card balances. 5.) Child care expenses and/or alimony, if any. 6.) Whether or not there has been a bankruptcy or credit problems.

Pre-Qualifying and Lender Requirements:

Nate’s Team is familiar with the current lending requirements however we will still require that you actually meet with a lender before we begin the house-hunting. In today’s competitive market conditions, having your letter of loan approval ready, may be the determining factor in a winning or losing bid on a home of your dreams.

Financing Options:

Depending upon the price of the home and/or the amount of your down payment, there may be several options that fit your needs. They include VA (for military veterans only) which allows 100% financing of the purchase, FHA (Federal Housing Administration) which allows purchase with as little as 3.5% down payment and CONVENTIONAL, with down payment options that range from 10-20%. In addition to these traditional methods, there are a variety of other creative financing options including Owner Financing, Bond Money Down Payment Assistance or Lease Purchase Options.

If you have not yet been qualified and approved through a reputable lender, please let us help you by referring you to one of our preferred lenders. In today’s economic times, securing a loan through a solid mortgage company is not only the first step in the home buying process, it is one of the most important.

*The information which you provide will be held in strict confidence*

Our Professional Lending Team: RE/MAX Professionals is proud to offer a team of loan officers to assist all your financing needs. Even if you are already approved with another lending institute, you owe it to yourself to talk to one our home loan consultants. It is always a good idea to compare loans to make sure you are getting the best deal. Choosing a reputable lending company is an important part of your home purchase process. Our professional lending team is ready to get started with your loan approval today!

Understanding Closing Costs

Your Loan Application Checklist

When you decide to purchase a home, the following documentation will be required in order to complete the loan approval process. Save some time and gather everything you need before your

scheduled appointment with the lender. Employment:

• Addresses for two full years

• Gross monthly income

• W-2’s, if available

• Proof of pensions, retirement, disability or Social Security

• Proof of income from rentals, investments, etc.

• Year to date pay stub

• If self-employed: Two years 1040 Tax Returns Current year profit and loss statement Creditors:

• Each creditor’s name, address and type of account

• Account numbers

• Monthly payments and approximate balances Amount of child care expenses Banking:

• Names and addresses of saving institutions

• Account numbers for all accounts

• Type of accounts and present balances Miscellaneous:

• List of assets in stocks, bonds, land

• Life insurance cash value (documented if used as cash down payment)

• If applicant is selling a home, a copy of sales contracts

• Social Security numbers for all parties

• Veterans—Certificate of Eligibility & DD-214

• Cash or check to pay for application fee Real Estate Agents:

• Copy of sales agreement

• Copy of listing on property

• Instructions on how appraiser is to gain entrance

Why Hire a Real Estate Consultant?

Your Interests Are Professionally Represented: Enlisting the services of a professional real estate consultant is similar to using an accountant to help you with your taxes, a doctor to help you with your health care, or a mechanic to help you with your car. So the first advantage is pretty obvious. If you had the time to devote to learning all you need to know about accounting, medicine, and automotive mechanics, you could do these services yourself! But who has the time. You probably already have a full-time career to which you are committed. This is why you allow other professionals to help you in specific areas of expertise. It is always better to make an informed decision to buy something than it is to be sold something. When you hire a real estate consultant, your interests are professionally represented, and you have more control and peace of mind than if you are simply sold any home you find. Buying a home is a big decision. Let your real estate consultant act as your specialist, even if you happen to find the perfect home yourself. Finding the home is only one step in the home buying process.

Buyer Agency Agreement - Countless Advantages and NO Disadvantages: When you sign a Buyer Agency Agreement, you are simply agreeing to “hire” a personal consultant who, by law, must represent your best interests to the best of his/her ability. All of this personal service is available at absolutely NO COST TO YOU! When you work with the Nate Martinez Team you get an entire staff of real estate professionals devoted to protecting your needs and to helping you make one of the most important investment decisions of your life.

You will get a Great Home Quickly and Conveniently: It is nearly impossible to find a home that meets your needs, get a contract negotiated , and close the transaction without an experienced agent. Nate’s Team will ensure that you are only tour homes that meet your specific needs. You won’t need to spend endless evenings and weekends driving around looking for homes for sale. When you tour homes with your personal real estate consultant you will already know that the homes meet your criteria for bedrooms, bathrooms, garage space, square footage, neighborhood, etc.

You Get a Personal Specialist that Knows Your Needs: Just as your accountant, doctor and mechanic get to know your needs through a steady relationship; your real estate consultant also gets to know your real estate needs and concerns. This type of relationship is built by open communication at all times and by touring homes with your agent so they get a good idea of your feedback and concerns. If you try to jump from agent to agent, you will not receive the best real estate service available to you. About this time you are probably saying to yourself, “this sounds too good to be true! What’s the catch? The “catch” is that you are signing a legal document between you and the real estate consultant that will establish a legal relationship with duties and obligations for both parties. The commitment is simple: you agree to let your real estate consultant represent your home buying needs exclusively throughout the duration of the agreement or until you find a home which you successfully purchase. The duration is a variable you decide. This is to guarantee that the Buyer’s Agent receives compensation from the Seller’s Agent for the work she/he has been doing for you. Signing the Buyer Agency Agreement merely means that you agree that your real estate consultant should be compensated for the services they provide while guiding you professionally through the home buying process.

Why Choose RE/MAX Professionals?

Sales and Experience: • Nobody in the world sells more real estate than RE/MAX

• The average agent sells 6.8 transactions per year (according to National statistics)

• RE/MAX agents average 15.1

• RE/MAX Professionals agents average 26.19

• RE/MAX Professionals has been servicing the Valley of the Sun for 9 years!

• Nate’s Team has been helping Arizona families buy or sell a home for a 1/4 of a century!

• Nate’s Team continues to rank in the top 10 RE/MAX teams in Arizona in the past decade

• Nate’s Team ranked # 1 in Arizona for number of sales in 2009

Advertising and Branding: • Billions of dollars have been spent promoting the RE/MAX brand name, making it ONE of the most recognized real estate brands and logos around the world. • RE/MAX offices are located in over 80 countries world-wide, more than any of its competitors. • Millions of buyers and sellers visit REMAX.com every day for their real estate needs. • The RE/MAX Hot Air Balloon fleet is the largest in North America. • In 2009, RE/MAX claimed the top-spot in market share in 19 cities within the Phoenix metro area - 12.94% of all sales.

• RE/MAX leads the industry in professional designations.

Professional Designations - what does that mean for you? • Our Team of real estate professionals pride themselves on higher education. For every designation an agent receives, it is like another year in the bachelor degree. Ask anyone of our Team members what their designations represent and they’ll be happy to share how it helped them become a better steward of the real estate industry.

How We Give Back: • RE/MAX agents have donated funds directly from their personal accounts and have collectively arrived at an amazing milestone: $100 million dollars raised over the past 18 years for Children’s Miracle Network, which raises funds for more than 170 pediatric hospitals. RE/MAX is one of the top 3 donors of all times.

• When you buy or sell a home with our Team, a donation is made to the Phoenix Children’s Hospital in your name.

Our Technology Tool Box: • State-of-the-Art “Real Time” Multiple Listing Service (MLS) Auto-Search Service • Never miss a new listing opportunity with Voice Pad Curb-Side Availability • Online Transaction Manager Software - access your paperwork 24 hours a day, 7 days a week • Complementary Closing CD - all pertinent documentation saved in one convenient electronic location • NatesHomes.com, NatesLuxuryHomes.com and AzShortSaleResource.com • Daily Blogs and Podcasts • Large Inventory of Foreclosure Properties (REO homes) • Follow Us on Facebook, Twitter, LinkedIn, YouTube • 4 Valley office locations - Southwest Valley, Anthem, Sun City West, Central Corridor, Arrowhead Surprise and Glendale

Benefits of Purchasing a Home

“A house is a home when it shelters the body and comforts the soul.” Phillip Moffitt

Pride in Owning: Most people buy homes to have control over where they live. Although investment features are important, the psychological reasons for buying—the satisfaction of owning and freedom from paying rent—are the most important. In a survey done by the National Association of REALTORS® of 6,000 homeowners and 2,000 renters—perhaps the largest ever of attitudes toward home ownership—showed that 76% of owners and 66% of renters considered pride of ownership an—important reason for buying.

Dislike Paying Rent: Renting offers a lifestyle that’s nearly maintenance-free. That may appeal to you, but consider that renting offers you no equity, no tax benefit, and no protection against regular rent increases. Writing a rent check is just like watching your hard earned money sail away!

Settling Down: More than 6 in 10 renters said “settling down” was an important reason to buy.

Good Investment: 76% of owners and 69% of renters said the investment aspect of ownership was important.

Tax Advantages: Property taxes and qualified home interests are deductible on Schedule A, for itemized deduction.

Long-term Appreciation: People consider home ownership a good investment because they view it as a long-term venture. Historically, home prices have risen at relatively steady rates. Existing home prices rose at an average of 4% per year between 1980 and 1992. From 1999 to 2003, property values were reported to have increased in some areas as high as 7%.

Leverage Investment: People borrow a great deal to buy a home, yet they receive the full benefits of price appreciation. In the long run, investments in homes far outpace inflation.

Source of Savings: Home ownership always has and continues to comprise the single largest source of savings for American households. As Homeowners build equity, they continue to build long-term wealth.

Sacrifices Are Worth It: Almost 7 in 10 renters in the National Association of REALTORS® home ownership survey said they planned to buy a home in the future. More than three-quarters of these people said they were willing to sacrifice to do that.

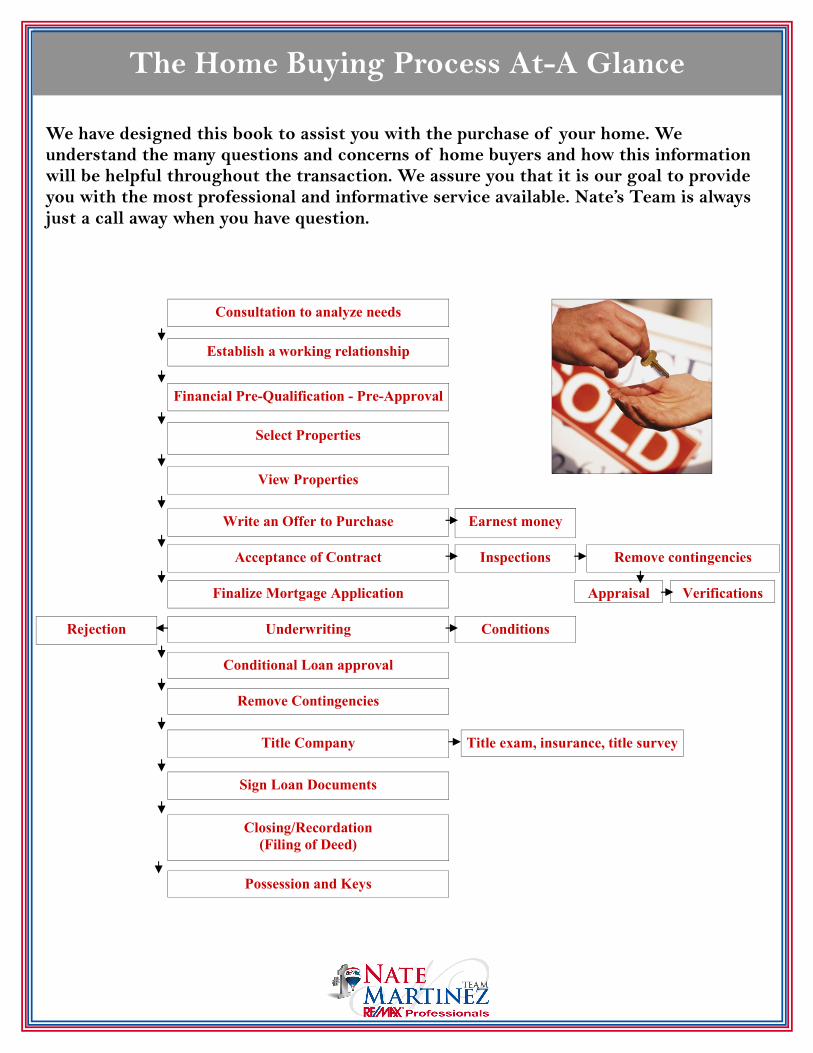

The Home Buying Process At-A Glance

We have designed this book to assist you with the purchase of your home. We understand the many questions and concerns of home buyers and how this information will be helpful throughout the transaction. We assure you that it is our goal to provide you with the most professional and informative service available. Nate’s Team is always just a call away when you have question.

Rejection

Inspections Remove contingencies

Establish a working relationship

Financial Pre-Qualification - Pre-Approval

Select Properties

View Properties

Write an Offer to Purchase Earnest money

Finalize Mortgage Application Appraisal Verifications

Underwriting Conditions

Conditional Loan approval

Consultation to analyze needs

Remove Contingencies

Title Company

Closing/Recordation

(Filing of Deed)

Title exam, insurance, title survey

Possession and Keys

Acceptance of Contract

Sign Loan Documents

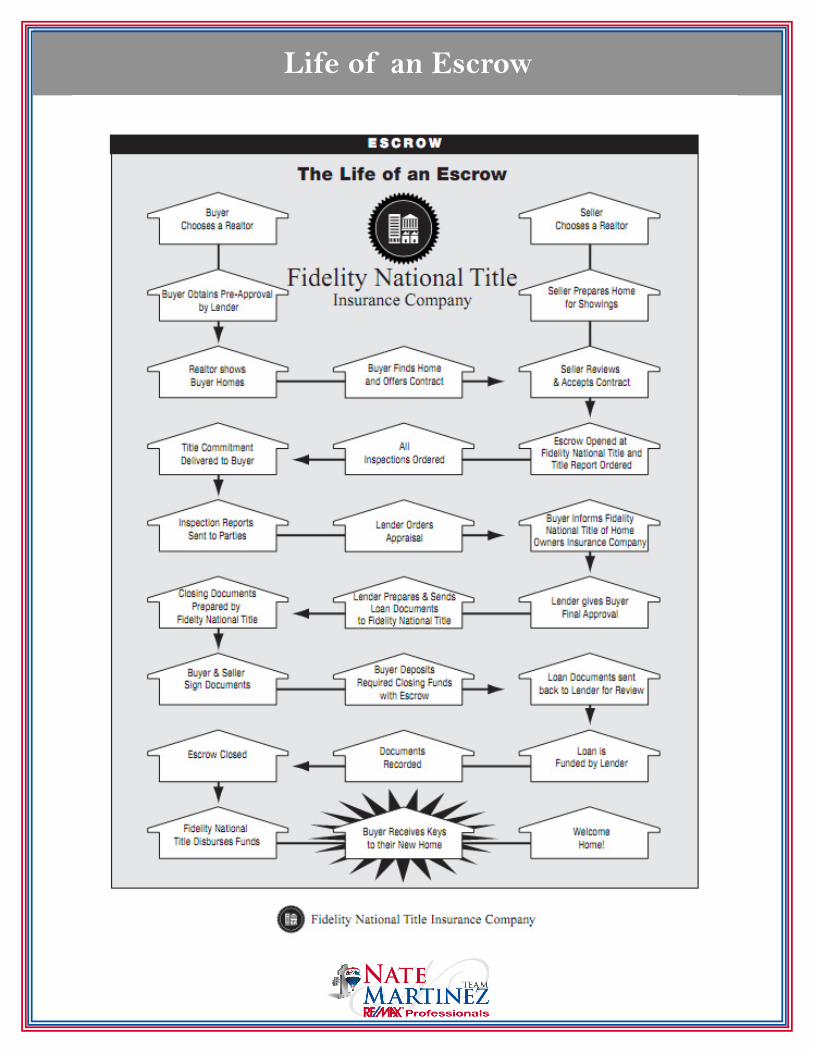

Understanding the Escrow Process

What is Escrow? As the escrow holder, the title company’s duty is to act as the neutral third party. They will hold all documents and all funds, pursuant to the purchase contract and escrow instructions., until all terms have been met and the property is in insurable condition. They do not work for the seller or for the buyer; rather, they are employed by ALL parties and act only upon MUTUAL WRITTEN INSTRUCTIONS.

Opening Escrow: “Opening Escrow” occurs when your real estate consultant brings a fully executed contract with your earnest money deposit to the title company. Your escrow officer reviews the contract, receipts in the earnest money, orders the commitment for title insurance, and prepares the documents required to close escrow. All of the documents are double checked by your escrow officer.

What is Title Insurance?

Definition: A contract where by the Insurer, for valuable consideration, aggress to indemnify the Insured for a specified amount against loss through defect of title to real estate where in the latter has an interest either as a purchaser or otherwise. Purpose: Title insurance services are designed to afford real property owners, lenders and others with interest in real estate, the maximum degree of protection from adverse title claims or risks. The financial assurance offered by a title insurance policy from the title company is, of course, the primary aspect of title protection. The policy affords protection both in satisfying valid claims against the title as insured and in defraying the expenses incurred in defending such claims. The Title Search: Title companies work to eliminate risks by performing as search of the public records or through the title company’s plant. The search consists of public records, laws and court decisions pertaining to the property to determine the current recorded ownership, any recorded liens, encumbrances or any other matters of record which could affect the title to the property. When a title search is completed, the title company issues a commitment for title insurance (pre-lim) detailing the current status of title.

Recordation: After the title company has received all funds needed and have ascertained that all loan conditions are met, original documentations are recorded. Once documents are recorded, the title company will notify all parties involved.

After the Closing: You will receive your loan coupon book or monthly statement before your first payment is due. If you do not receive any correspondence from your mortgage company, of if you have questions regarding your tax and insurance impounds, contact your mortgage company. The original recorded deed to your home will be mailed to you directly. Your title insurance policy will also be mailed to you from your title company.

Property Taxes: You may not receive a tax statement for the current year on the home you buy. However, it is your obligation to make sure the taxes are paid when due. Check with your mortgage company to find out if taxes are included with your payment. For more information on your Maricopa County property taxes, contact: • Maricopa County Tax Assessor: 602-506-3406 • Maricopa County Treasure: 602-506-8511

Life of an Escrow

Question & Answers

When I start visiting homes, what should I be looking for the first time through? The house you ultimately choose to call home will play a major role in your family’s life. A home can be an excellent investment, of course, but more importantly, it should fit the way you really live, with spaces and features that appeal to everyone in the family. At each home, pay close attention to these important considerations: 1.) Is there enough room for you now, and in the near future? 2.) Is the home’s floor plan right for your family? 3.) Is there enough storage space? 4.) Will you have to replace the appliances? 5.) Is the yard the size that you want? 6.) Are there enough bathrooms? 7.) Will your present furniture work in this home?

Is an older home as good a value as a new home? It’s a matter of personal preference. Both new and older homes offer distinct advantages, depending upon your unique taste and lifestyle. New homes generally have more space in the rooms where today’s families do their living, like a family room or activity area. They’re usually easier to maintain, too. However, many homes built years ago offer more total space for the money, as well as larger yards. Taxes on some older homes may also be lower. Some people are charmed by the elegance of an older home but shy away because they’re concerned about potential maintenance costs. Consider a home warranty to get the peace of mind you deserve. A good Home Warranty plan protects you against unexpected repairs on many home systems and appliances for a full year or more after you move in.

Do I need to bring anything along when I’m looking at homes? Bring your own notebook and pen for note taking and a flashlight for seeing enclosed areas. Be prepared to “snoop around” a little. After all, you want to know as much as possible about the home you buy. Sellers understand that because their home is on the market, it will be looked over pretty thoroughly. If you need to go back to a home for another look, Nate’s Team will be happy to schedule an appointment. Be sure to ask any questions you have about the home, even if you feel you’re being nosy. You have a right to know. It’s important to know that the seller will supply the buyer with a Residential Property Disclosure, which will disclose any defects known by the seller. A copy of this form is found towards the back of this book. And don’t forget to bring your checkbook!

What should I ask Nate’s Team about each home that I look at? As a rule of thumb, ask any questions you have about specific rooms, features or functions. Pay particular attention to areas that you feel could become “problem” areas—additions, defects, areas that have been repaired. And above all, if you don’t feel your question has been answered, ask until you do understand and are satisfied. In most cases, Nate’s Team will be able to provide you with detailed in-formation.

How many homes should I look at before I buy? There is no set number of homes you should look at before you decide to make an offer on one. That’s why providing Nate’s Team with as many details as possible up front is so helpful. The perfect home may be waiting for you on your first visit. Even if it isn’t, the house-hunting process will help you get a feeling for the homes in the community and narrow your choices to a few homes that are worth a second look. If you’re looking in more than one community, try to make the most of each house-hunting trip. Ask Nate’s Team for welcome kits, maps, and information about schools, churches, and recreational facilities. Also, be sure to take along a camera and snap some pictures of all the homes you like. That’ll make it easier to remember.

What should I think about when I’m deciding which community I want to live in? Good city services, nice parks and playground facilities, convenient shopping and transportation, a track record of sound development and good planning—these are just a few considerations that are important to many people when they choose a community in which to live. Nate’s Team knows the people and the communities they service, and chances are, they can help you find a neighborhood that really fits your family’s needs.

Where can I get information about local schools? Nate’s Team can help you research local schools. There are also a multitude of website available online to help you find the information you need about school districts, including test scores, extracurricular activities, bus service and more.

Question & Answers

How can I find out what homes are selling for in a given neighborhood? Home sales are a matter of public record. The Recorder’s Office, a local residential appraiser, the planning department for the locality are all resources the buyer can call on. However, a better and easier way for you to get this information is to ask Nate’s Team. If you’re interested in a particular home, we can provide you with a list of comparables—sale prices of homes in your area that are roughly the same size and age as the home you’re considering. Although there will certainly be some differences between the homes—the house next door may have an extra bedroom, or the one down the block may be older than the one you’re looking at—it’s a good way to evaluate the seller’s asking price.

How do I determine the amount of my initial offer? There is really no rule to use in calculating a realistic offer. Naturally, the buyer wants the best value and the seller wants the best price, but negotiations can be influenced by many factors, such as a seller who may be changing jobs and wants to sell quickly, or a buyer who really wants a specific home. After you’ve looked at the home’s features, asked questions, checked comparables, and talked about it with your real estate consultant, you should have a good idea of what the home’s value is in the current market. Consider what you can afford and make an offer that you consider to be fair. Negotiations can vary from price to closing date to concessions paid by the seller. When all terms are completely agreed upon, the paperwork will be signed by each party involved in the transaction. At that point, your real estate consultant will assist you in the process of arranging for an inspection and completing the appraisal The home inspection – what does a home inspector do? For your own safety, and to make sure you are fully aware of what is in the home you choose, using a professional home inspector is highly recommended. A home inspector will check a home’s plumbing, heating and cooling, electrical systems, and look for structural problems which could lead to other more serious issues with the home. Before you sign any written offer, make sure that it includes an inspection clause or other language which says that your purchase obligation is contingent on the findings of a professional home inspector. Arizona Department of Real Estate Contracts automatically contains this important verbiage. Your home cannot “pass” or “fail” an inspection, and your inspector will not tell you whether he or she thinks the home is worth the money you are offering. The inspector’s job is to make you aware of repairs that are recommended or necessary. A seller may be willing to renegotiate a price to accommodate needed repairs, or you may decide that the home will take too much work and money. A professional inspection will help you make a clear-headed decision. In addition to the overall inspection, you may wish to have separate tests conducted to check for termites, or the presence of radon gas. Talk to Nate’s Team for information about these tests and companies in the area that perform them. In choosing a home inspector, consider one that has been certified as a qualified and experienced member by a trade association. Nate’s Team may refer you to several qualified inspectors.

Should I be present during the inspection? Yes. It’s not required, but it is very much to your advantage. You’ll be able to clearly understand the inspection report, and know exactly which areas need attention. Plus, you can get answers to many questions, tips for maintenance, and a lot of general information that will help you when you move into your new home. Most important, you’ll see the home through the eyes of an objective third party. *Remember, the purpose of a home inspection is to help you learn things about the home that are not easily discoverable during your home-buying tour. IT IS NOT INTENDED TO BE A “LAUNDRY LIST” OF MINOR REPAIRS FOR SELLERS TO COMPLETE.

Is there any way I can protect myself against emergency repair bills in my new home? Yes. Home warranties offer you protection against many potentially costly problems not covered by your homeowner’s insurance. They’ve become increasingly popular in recent years, and for good reason: the coverage can save you thousands in the event of a major mechanical breakdown, at a time when your cash reserves have been depleted by your down payment and moving expenses. Ask Nate’s Team whether a Home Warranty is offered when looking at homes. But remember, if it is not offered, feel free to ask for it when writing the offer to purchase. The Home Warranty will give you the peace of mind necessary to feel comfortable in your new home. In most cases, the warranty plan will cover appliances, hot water heater, air conditioning units, electrical systems, garage door openers, plumbing systems, heating systems, faucets, ceiling fans and water softeners. Check with Nate’s Team regarding the specifics of the Home Warranty plan!

Do I need to talk to my insurance agent? Yes, and the sooner, the better. Most insurance professionals have a lot of experience in working with homeowners and can offer useful tips about home ownership, particularly regarding home safety and keeping your premiums low. Once you’ve found a home, your insurance agent can help you with a homeowner’s policy that meets your individual insurance needs. You’ll need to supply a copy of your policy to your mortgage lender prior to closing.

Question & Answers

What are the different types of lenders? How do I choose the right one for me? Before someone lends you the money to purchase your home, they’ll want to know a lot about you. And you’re entitled to know as much as you can about them, too. It’s important because getting a mortgage is not just a one-time signing of documents, a handshake and a check. You will be depending on your lender to fund the loan as promised, on time, and over the life of the loan, to keep good payment records, pay your taxes and insurance (if included in your monthly payment) and many other continuing services. Look for a lender that has the authority to approve and process your loan locally. It’s easier to obtain information on the status of your loan and discuss conditions directly with the person who will approve your loan, rather than some far away loan committee. It’s important that your lender know home values and conditions in your local area. And while biggest doesn’t always mean best, financial stability, repu-tation, qualifying procedures, and unique programs benefits are what they offer home buyers.

Are there any mortgages especially designed for first-time buyers? Today, first-time buyers enjoy a number of mortgage options that make purchasing a home more affordable by minimizing down payments and keeping monthly payments as low as possible during the early years of the loan. Most ARM type loans feature an interest rate that is below market for the first year, and may rise gradually after that. VA and FHA-insured loans call for extremely low down payment (0-5% of the purchase price), and often offer a below market interest rate. Similarly favorable terms can also be arranged with the help of Private Mortgage Insurance or PMI. Finally, first-timers who can find a cooperative seller or third-party investor can look into such non-traditional financing methods as a lease/buy arrangement

How does a lender determine the maximum mortgage I can afford? The three primary areas lenders examine in determining the size of mortgage you can handle include your monthly income, non-housing expenses, and cash available for down payment, moving expenses and closing costs. There are a number of different ways lenders interpret these variables to estimate your mortgage capacity. The most popular method is detailed here. Most lenders feel a family should spend no more than 28% of its gross monthly income on housing costs, including the mortgage, insurance, and real estate taxes. Also, these housing costs plus your long-term debts (car loans, student loans, etc.) shouldn’t exceed 36% of your income. If your down payment is 10% or lower, most lenders will tighten these restrictions even further. Some lenders may also include home maintenance costs and utility payments in their calculations.

How much of a down payment will I need to buy a home? A down payment of 20% has been the benchmark for conventional financing, but today, many options are available, some requiring as little as 5% down. For buyers who qualify for conventional financing but can’t handle the high down payment requirements, lenders offer this financing with Private Mortgage Insurance (PMI). Designed to protect the lender against default by the borrower, PMI allows you to obtain traditional financing with a down payment significantly lower than the standard 20%. By using PMI, you may be able to get a fixed rate or adjustable rate mortgage by putting as little as 5%. As with an FHA-insured loan, you must pay premiums for PMI coverage, the amounts are determined by the lender. Moreover, PMI premiums are often lower than FHA insurance, and may be paid as part of your monthly mortgage payment, in annual installments, or in a lump sum at the time you obtain the loan. Your mortgage expert can help you determine which down payment option is right for you and your budget.

What is Earnest Money? How much do I need? When you sign an offer to purchase, Nate’s Team will ask you for earnest money—that is an upfront deposit made with the title company, which shows how serious your intent is to purchase the home. Usually, you will be asked to write a check for 1 to 5% of the sale price. This money will be held in a special, non-interest baring escrow account. Your earnest money will be included as part of your down payment. There are several ways your earnest money maybe forfeited during the escrow process. Make sure you contact your real estate consultant right away if you feel you may want to cancel your purchase agreement to ensure you do not loose your earnest deposit.

Can I get an FHA or VA mortgage? Just about anyone can apply for an FHA-insured mortgage through banks and other lending institutions. They are particularly well-suited for buyers of moderate income; the low down payment requirements (as low as 3% of the purchase price) are matched by a relatively low maximum mortgage amount. Similarly VA-guaranteed loans often require no down payment. These loans are reserved for either active military personnel or veterans, or spouses of veterans who died of service-related injuries. If there is a downside to these loans, it’s the qualifying process. Though you apply for government-insured financing through a lending institution, the Federal Housing Administration or the Department of Veterans Affairs must insure or guarantee the loan and may require specific documentation or procedures not necessarily required for conventional financing. That may take more time than is generally required for conventional mortgage approval. Additionally, FHA-required insurance must be added to your payment. Make sure the lender you select has approved authority by each of these agencies to ensure a quicker loan process.

Question & Answers

What are the steps involved in the loan process? The information your lender needs is not much different than what is needed when you apply for a major credit card: names and addresses of your employer and bank account numbers and balances. The lender will also need other financial information such as installment payments, auto loans, charge cards, and department store accounts. Your lender will verify this information with your present and past employers, order a routine credit report on your current and past accounts, and order a professional appraisal of the property you want to purchase. Allow yourself two to four weeks to complete the application process. Then once all the verifications have been completed, your lender will underwrite and approve the loan. Overall, the time from the date of application to the date of move-in is generally four to five weeks for conventional loans and five to seven weeks from the date of application for FHA and VA loans.

What are Points? In real estate, the term “point” refers to 1% of the total mortgage loan amount. Buyers often pay lenders this supplemental fee, calculated in points, to get a better interest rate on a particular mortgage. Many lenders will advise you to pay the points for the better rate if you can afford it, especially if you plan on keeping the home for more than a few years. Like interest, the money you pay for points may be tax-deductible, and the investment may pay for itself through savings generated by lower monthly payments. We suggest you call your tax preparer.

What is APR and how is it calculated? The Annual Percentage Rate (APR) is a calculated rate of interest for a loan over its projected life. This rate includes the interest, all points (which are considered prepaid interest), mortgage insurance, and other charges associated with making the loan that the lender collects from the borrower. The APR is calculated by a standard formula that all lenders use. This enables the borrower to comparison shop between lenders and/or loan products.

What is a good faith estimate? Your lender must provide you with a good-faith estimate within three days of your application. This is the information you need to make a fair and accurate judgment when shopping for a loan. Your estimate is a written document that shows all the costs that can be estimated in advance by the lender. You need this information so there are no surprises on the day you close your sale on the property to be purchased. You will be expected to pay closing costs. You should review all costs, know which are non-refundable in the event your loan is not approved, and be prepared to pay outstanding fees at closing. You may also want to compare these costs to those charged by other lenders when shopping for your home plan.

What does my monthly mortgage payment include? What does PI and PITI stand for? The bulk of your monthly mortgage payment goes toward paying off the principal and interest of your loan, (you may hear lenders refer to this as “PI” for Principal & Interest). In addition, most lenders require that you pay a sufficient amount to cover your local real estate tax, plus your homeowner’s or hazard insurance, (you may hear this “total” payment referred to as “PITI” or Principal, Interest, Taxes & Insurance.) This amount is placed in an escrow account, from which your lender then pays your tax and insurance bills as they come due. When shopping for a loan, it is important to ask the lender if the monthly payment you are being quoted is PI or PITI.

What are the respective advantages of 15-year and 30-year terms? The 30-year fixed rate mortgage remains the standard mortgage, with an array of valuable benefits designed especially for buyers who expect to stay in their homes for a long time. Because the borrower pays more interest than principal for the first 23 years, the tax de-duction is substantial. As you’d expect, a 15-year monthly mortgage means higher monthly payments than an equivalent 30-year loan ... but not as much higher as you may think. At the same rate of interest, payments on the 15-year mortgage are roughly 20-25 % higher than a loan that takes twice as long to pay off. And one of the benefits of choosing a 15-year mortgage is that you can generally get a lower interest rate for an otherwise similar loan. Another advantage is faster equity build-up because a larger portion of your early payments are going to pay off principal. This makes the 15-year mortgage an ideal alternative for couples approaching retirement or anyone else interested in owning their home free and clear as quickly as possible.

Do adjustable rate mortgages offer any protection against rising rates? Yes. ARMs and other variable rate or payment plans offer lower-than-market interest rates initially, but because they are tied to the interest rates of U.S. Treasury Bills or other indexes, interest rates later in the loan term may rise. However, many such loans offer built-in safeguards designed to minimize the effect of any rapid escalation in interest rates. A protective device included in some ARMs is the payment cap. Under this provision, your monthly payments may rise by only a set dollar amount. The potential disadvantage of this type of cap is that it can slow or even reverse your equity build-up. If rates rise dramatically, you could actually wind up owing more principal at the end of the year than you did at the beginning. Of course, ARM holders can also consider refinancing to a fixed rate loan after a few years. Some ARMs even include a provision for converting to a fixed rate after a set period of time.

Question & Answers

How can I find out what my property tax bill will be? Usually, the total amount of the previous year’s property taxes is included on the listing information sheet for the home you’re interested in. Remember, tax rates change from year to year, so the previous year’s bill should be considered simply as a “ballpark” figure of what you would pay. For a more precise projection, call the local assessor’s office for assistance, or ask your real estate consultant for a copy of the current tax record.

What can I do if I have a fixed rate loan and interest rates go down? When interest rates drop significantly, the homeowner should investigate the financial advantages of refinancing. Essentially, this means taking out a new loan to pay off your existing loan. Refinancing may require paying many of the same fees paid at the original closing, plus origination fees. Most mortgage experts agree that if you can get a rate 2% less than your existing loan and you plan on staying in your home for at least 18 months, refinancing is a good investment.

Can I pay off my loan early? If you can afford it and are interested in the considerable advantages of having more equity and/or owning your home free and clear at the earliest possible date, the answer in most cases is yes. The FHA, VA, and even some states do not allow lenders to charge penalties for paying mortgages early or refinancing. In fact, many lenders now include space on monthly statements for borrowers to itemize any additional principal payment they wish to include with their regular payment. If you are unsure about the rules governing pre-payment, review your mortgage agreement.

What is the difference between pre-qualifying and pre-approval? Pre-qualifying for a mortgage up to a certain amount is the first step for all home buyers. It’s a verbal exchange in which the lender tells you in advance approximately how much money the buyer is able to borrow, based upon the information you provide the lender on your debt and income. Pre-approval goes a step further than pre-qualifying. It is an actual commitment to lend, provided that, when the borrower is ready to buy, he or she still meets all the qualifying conditions that were met at the time of conditional approval. We strongly recommend it!

WANT TO PAY OFF YOUR LOAN EARLY? ⇒ Save extra every month. With the interest you earn on savings you may be able to make an extra payment at the end of the year.

⇒ Pay an extra twelfth of your P & I payment monthly. Or just send whatever extra you can every month. Whichever method you choose, be sure to clearly indicate that the excess payment is to be applied to principal.

“House Hunting Tips” When you find a home you may be interested in buying, make sure to asks your

real estate consultant to find out the following information:

• How much money do you pay for monthly utilities? • What features have you enjoyed most about living in this home? • Are there defects or problem areas that need to be fixed right away? • How old is the furnace and central air conditioning system? • How old is the roof ? Have you experienced any leaking?

Understanding Closing Costs

Application Fee: Fee charged by lender to offset fixed costs related to mortgage loan processing such as appraisal, credit report and underwriting. Closing Fee: The fee charged by the closing agent who prepares the closing documents and closes the loan on behalf of the lender. Commitment Fee: This is often called an origination fee and is generally computed at 1% of the mortgage amount. Discount Points: Each point is equal to 1% of the mortgage amount. Points are used by the lender to adjust the yield on the mortgage when it is sold to an investor. By paying more points, the borrower can obtain a lower mortgage interest rate. Funding Fees: Normally applicable on VA loans only, equal to 1% of the loan amount. The fee is due at closing or may be added to the loan amount and financed. Homeowner’s Insurance: One year premium is due in advance at time of closing. Mortgage Insurance: Insurance required by the lender when the down payment is less than 20%. In the case of loan default, this insurance reduces the lender’s loss. Pre-payables: Adjustment to escrow accounts from the date of closing to the date of the first payment. Interest is paid through the end of the month of closing,, while taxes are paid through the end of the month of closing plus the following month. Two months of PMI (Principle Mortgage and Interest) are collected. Two months of homeowner’s insurance may be collected. A homeowner’s insurance policy must be provided along with a receipt showing that the first year’s premium is paid. Processing Fee: Fees charged by the escrow processor, either working for the escrow company, title company, or real estate company, for administrative escrow services performed from the point of contract through closing. Recording Fees: Fees charged by state or municipal entities for entering the closing documents into the public record. Survey Fee: Is usually required and is used by the lender to check for encroachments from within or from outside the subject property. Title Insurance: Provides protection for lenders and homeowners against financial loss resulting from legal defects in the title. Underwriting Fee: Usually included in the application fee. However, practices vary from lender to lender.

The Home Inspection

It’s easy to make sure the home you’ve chosen is a smart buy. By having a home inspection, the home’s vital systems are checked. A home inspection allows you to purchase your home with confidence. Our team of professionals also includes a list of highly recommended home inspectors. Your real estate consultant will assist you arranging for a home inspection after your offer has been fully executed. The Nate Martinez Team recommends the following minimum standards when choosing an inspector: 1. Membership in ASHI (American Society of Home Inspectors) and adherence to its Standards of Practice and Code of Ethics. 2. Written report at the time of inspection. Items on your inspection report will include:

FOUNDATIONS, BASEMENTS, AND STRUCTURES: Basement floor and walls, proper drainage and ventilation, evidence of water seepage. EXTERIOR SIDING, WINDOWS, DOORS: Exterior walls, windows, and doors; porches, decks and balconies; garage. ROOF: Roof type and material, condition of gutters and downspouts. INTERIOR PLUMBING SYSTEM: Hot and cold water system; the waste system and sewage disposal; water pressure and flow; and hot water equipment. ELECTRICAL SYSTEM: Type of service, the number of circuits, type of protection, outlet grounding and the load balance. CENTRAL HEATING SYSTEM: Energy source, type of cooling equipment, capacity and distribution. INTERIOR WALLS, CEILINGS, FLOORS, WINDOWS AND DOORS: Walls, floors, ceilings, stairways, cabinets and countertops. ATTIC: Structural, insulation and ventilation information. FIREPLACE: Notes about the chimney, damper and masonry. GARAGE: Doors, walls, floor, opener. APPLIANCES: Includes a wide range of built-in and other home appliances, smoke detectors and television/cable hookups. LOT AND LANDSCAPING: Ground slope away from foundation, condition of walks, steps and driveway. *This list does not constitute the complete make-up of any one inspections or inspector’s practice. Upon completion of any home inspections, you should receive a copy of the written report*

Why Choose a Home Warranty?

If the seller does not provide a home warranty policy, the buyer may purchase one at the time the contract is accepted. Nate’s Team can facilitate your purchase of a home warranty. The typical cost of a home warranty can range from $330-$600 and can be paid for at the close of escrow. However, keep in mind a home warranty can be purchased at any point the homeowner wishes. Why a home warranty is so important to your peace of mind: If you’re buying a home, your expenses are only just beginning at closing. Most people have lots of renovations to make, or furniture to buy, or landscaping to install. So the last thing you want to have happen is additional expenses due to unexpected mechanical failures of major components in your home. Benefits when you’re the buyer: Your home is one of the biggest investments of your life. Why take chances? Be covered against the expense of an unexpected repair or replacement for a full year after closing, less standard deductible. Think about it. No matter how closely you inspect a home before you buy, you just can’t predict everything. Like breakdowns from normal wear and tear, or the possibility of mechanical failure during the first year of ownership. Things like internal plumbing, electrical wiring, or vital parts of the air conditioning and heating systems. Only a good home warranty program can give you the protection you need. Coverage by one of the largest providers of home protection plans: When the major systems and appliances in your home are protected by a home warranty, both buyer and seller can relax. Because your home warranty protection is solid and reliable; the kind you can count on for the peace of mind you want in your home. Toll-free, 24-hour claim service: What could be easier when something goes wrong than making a single, toll-free phone call? Well, when your home is protected by a home warranty, that’s how easy it is—24 hours a day, seven days a week. As soon as the home warranty company receives your call, the claim is entered into their state-of-the-art computer system. They’ll notify a contractor in your area who contacts you for an appointment. When the contractor arrives at your home, he/she will verify the claim, prepare a repair or replacement estimate and call their claims department. He/she is then authorized to complete the necessary repairs or replacement on covered items. Who do I choose for a warranty company? Your real estate consultant can assist you in selecting a reputable home warranty company. There are several factors you want to considering when reviewing different companies. Make sure you compare apples-to-apples in coverage. Some companies may appear to be less expensive, but when you read the fine print, they do not offer the same comprehensive policies that other companies do. You also want to make sure you are fully aware of what the home warranty company considers to be “pre-existing” conditions. These are things that maybe wrong with the house at the time you close, or may fail within 30 days of owning the home, that would not be covered 100% by your home warranty. Make sure you go over your home inspection and warranty with your real estate consultant.

Your Moving Checklist

□ Decide what to move and what not to move. Possibly plan a garage sale (extra cash & less to move).

□ Getting estimates from several moving companies or truck rental companies, depending on how you plan to make

the move. Arrange any special movers for items of value like a piano or pool table.

□ If you plan to move yourself with a moving truck, make sure you ask for a hand-truck (appliance dolly).

□ Create a floor plan of where your furniture should be placed to avoid confusion for you or your movers.

□ Planning your travel itinerary and making transportation and lodging reservations in advance (make sure you

leave a copy with a friend or relative.)

□ Obtain your children’s school records to make for an easier transfer. Arrange the transfer of children’s school

records (if applicable).

□ Transfer your bank accounts (if applicable). They will be happy to open your accounts by mail.

□ Contact your local credit bureau to find out if they are on the same system your new home town subscribes to;

if not, they will be able to transfer your credit file.

□ Request records from doctors and dentists, including eye glass prescriptions, dental x-rays and vaccinations.

□ Pay existing bills and closing out local charge accounts. Get refunds from your present utility and phone

companies and arrange for service at your new home.

□ Recording expenses incurred during your house-hunting trips. You will also want to save your moving expense

receipts (if the move is employment-related) for tax deductions.

□ Cancel or transfer deliveries, newspaper, garbage collection, etc. Coordinate the transfer of gas, electric, water to avoid a lapses in service and extra re-start expenses.

□ Check on personal items that might be at the photo shop, bank safe deposit box, a neighbor’s house, on lay-away or in the repair shop (i.e., shoe repair, jewelry store, small appliance repair or dressmaker).

□ Make arrangements for transporting your plants and pets.

□ Save the phone book from your former city residence for tying up loose ends or for future correspondence.

□ Transfer insurance policies or arrange for new policies.

□ Gather all valuables, jewelry, important papers (birth certificates, deeds, documents) to take with you personally. Appraise valuable items, such as antiques, art pieces, etc.

□ Have the car serviced for the trip.

□ Pack an arrival kit of necessities just in case you arrive before the mover.

□ Purchase moving insurance. Your mover’s liability for lost or damaged goods will not equal their replacement cost (if applicable).

□ Check with your attorney about your will if crossing state lines.

□ Ask for professional referrals if available (i.e. doctor, accountant, etc.)

□ Change these addresses: Post Office, charge accounts, subscriptions (at least four weeks in advance), relatives and friends, national and alumni organizations, church, mail order clubs (books, tapes, catalogues), firms with which you have time payments, past employer in order to receive your W-2 form.

□ Save your old address labels to speed up your change of address forms.

Moving Checklist:

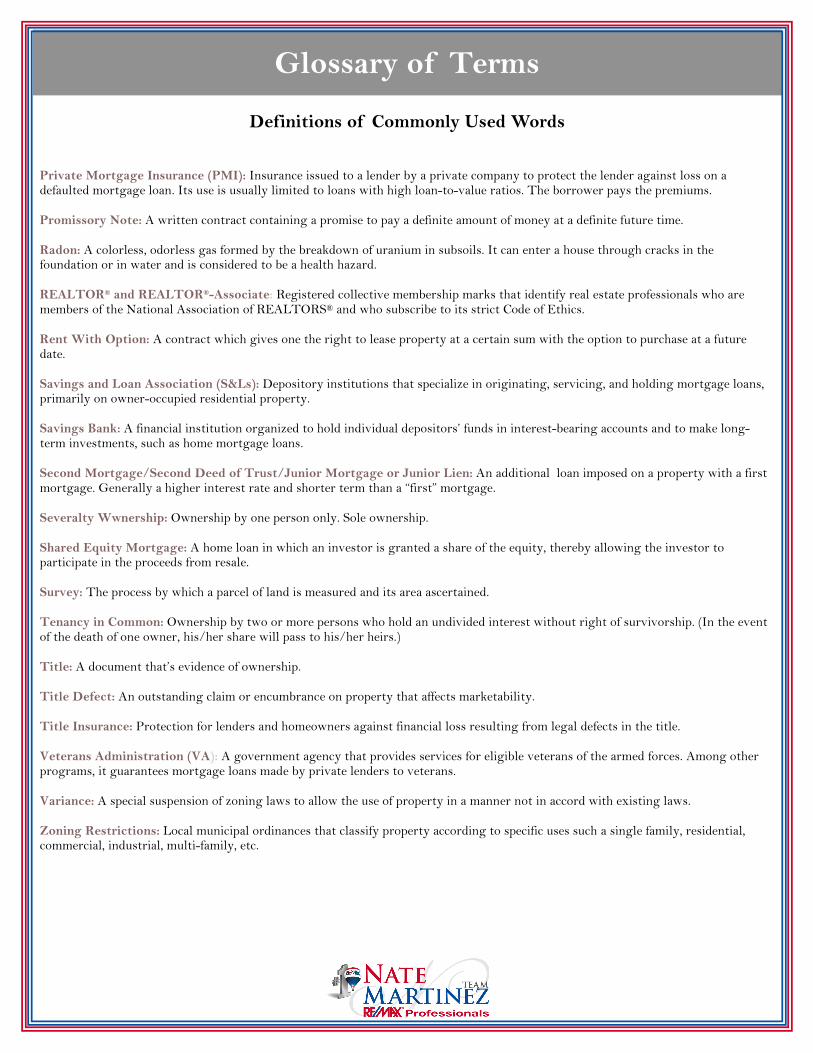

Glossary of Terms

Definitions of Commonly Used Words

Abstract of Title: A summary of the public records relating to the ownership of a particular piece of land. It represents a short legal history of an individual piece of property, and traces the ownership of that property from the time of the first recorded transfer to present. Acceptance: Consent to an offer to enter into contract. Adjustable Rate Mortgage (ARM): A mortgage that allows the interest rate to be changed periodically. Agency: A legal relationship in which an owner-principal engages a broker-agent in the sale of property or a buyer-principal engages a broker-agent in the purchase of property. American Society of Home Inspectors (ASHI): A professional trade association that provides training and education in home inspections. Members must meet qualification requirements to join. Amortization: The gradual repayment of a mortgage by periodic installments. Annual Percentage Rate (APR): The total finance charge (interest, loan fees, points) expressed as a percentage of the mortgage amount. Appraisal: An evaluation of a piece of property to determine its value. Appreciation: Increase in value due to any cause. Asbestos: A mineral fiber used in some building materials such as flooring, siding, insulation and roofing. It is presently banned for most uses in real property. Assessed Value: The valuation placed on property by a public tax assessor as the basis of property taxes. Assumption of Mortgage: An agreement whereby the buyer assumes responsibility for a mortgage owed by the seller. Balloon Mortgage: A mortgage where the amount financed is not fully amortized over the period of the loan. When the loan becomes due, a large sum or “balloon” payment is required to satisfy the mortgage. Bridge Loan: A short-term mortgage made until a longer-term loan can be made; it’s sometimes used when a person needs money to build or purchase a home before the present one has been sold. Broker: A person licensed by a state real estate commission to act independently in conducting a real estate brokerage business. Although requirements vary from state to state, an individual must usually have at least one year of experience in the industry and pass an examination to earn a broker’s license. Building Codes: State and local laws that regulate the construction of new property and the rehabilitation of existing property. Cap: The maximum amount an interest rate or monthly payment can change, either at adjustment time or over the life of the mortgage. Closing: The final step in the sale and transfer of ownership of a property. The title is transferred from the seller to the buyer; the buyer signs the mortgage and pays costs of settlement; any money due the seller and purchaser are paid. Closing Costs: Fees and expenses, not including the price of the home, payable by the seller and the buyer at the closing (e.g., brokerage commissions, title insurance premiums, and inspection, appraisal, recording, and attorney’s fees). Closing Statement: A financial statement rendered to the buyer and seller at the time of transfer of ownership, giving an account of all funds received or expended.

Glossary of Terms

Cloud on the Title: Any condition which affects the clear title to real property.

Commercial bank: A financial institution authorized to provide a variety of financial services, including consumer and business loans

(generally short-term), checking services, credit cards, and savings accounts.

Comparables: Properties similar in size and character to the one being bought or sold.

Condominium: Ownership of a unit only, rather than of the entire building with the land.

Consideration: Anything of value to induce another to enter into a contract (i.e. money, services, a promise).

Contingency: A condition that must be satisfied before a contract is binding.

Contract: An agreement to do or not to do a certain thing.

Conventional mortgage: A fixed rate, fixed-term mortgage not insured by the federal government.

Deed: A legal document conveying title to a property.

Deed (quit claim): A deed that transfers only that title or right to a property that the holder of that title has at the time of the transfer. It

does not warrant or guarantee a clear title.

Department of Housing and Urban Development (HUD): A U.S. Government agency established to implement certain federal hous-

ing and community development programs.

Disclosure Laws: State and federal regulations which require sellers to disclose such conditions as whether a house is located in a flood plain or whether there are known defects in or affecting the property.

Earnest Money: A portion of a down payment given to the seller by a potential buyer indicating the buyer’s intent to complete the pur-

chase of the property.

Easement: A right to use the land of another.

Encroachment: A condition that limits the interest in a title to property such as a mortgage, deed restrictions, easements, unpaid taxes,

etc.

Equity: The value of real estate over and above the liens against it. It is obtained by subtracting the total liens from the value.

Equity Mortgage: A mortgage based on the borrowers’ equity in their home rather than on their credit worthiness.

Escrow: The placement of money or documents with a third party for safekeeping pending the fulfillment or performance of a specified

act or condition.

Federal Housing Administration (FHA): An agency within the Department of Housing and Urban Development (HUD) that adminis-

ters loan guarantee programs and loan insurance programs to make more housing available.

Fannie Mae: Nickname for Federal National Mortgage Corp. (FNMA), a tax paying corporation created by Congress to support the secondary mortgages insured by FHA or guaranteed by VA, as well as conventional home mortgages. FHA Insured Mortgage: A mortgage under which the Federal Housing Administration insures loans made, according to its regulation, by approved lenders.

Definitions of Commonly Used Words

Glossary of Terms

Definitions of Commonly Used Words

Fixed rate Mortgage: A loan that fixes the interst rate at a prescribed rate for the duration of the loan. Foreclosure: Procedure whereby property pledged as security for a debt is sold to pay the debt in the event of default. Freddie Mac: Nickname for Federal Home Loan Mortgage Corp. (FHLMC), a federally controlled and operated corporation to support the secondary mortgage market. It purchases and sells residential conventional home mortgages. Graduated-Payment Mortgage: A mortgage that starts with low monthly payments and increases at a predetermined rate. Growing-Equity Mortgage: A mortgage loan in which the monthly payments increase by a specific amount each year, with the “Overpayments” applied to the principal. Installment Debts: Long-term debts that usually extend for more than one month. Investor: The holder of a mortgage or the permanent lender for whom the mortgage maker services the loan. Any person or institution that invests in mortgages. Joint & Survivorship Deed: (Also known as “Warranty deed creating tenants in common with right of survivorship”) Upon death of one of the owners, title to the interest transfers “by contract” to survivors. Lease Purchase Agreement: Buyer makes a deposit for the future purchase of a property with the right to lease the property in the interim. Lien: A legal claim against a property that must be paid when the property is sold. Loan-to-value Ratio: The relationship between the amount of a home mortgage and the total value of the property. Lenders may limit their maximum mortgage to 80-95 percent of value. Lock-in-Rate: A commitment made by lenders on a mortgage loan to “lock in” a civilian rate pending mortgage approval. Lock-in periods vary. Market Value: The highest price a buyer will pay for a property and the lowest price the seller will accept. Mortgage: One type of document used to make property the security for the payment of a loan. Mortgage Broker: An individual or company that obtains mortgages for others by finding lending institutions, insurance companies, or private sources to lend the money; may also make collections and handle disbursements. Mortgagee: The lender of money or the receiver of the mortgage. Mortgagor: The borrower of money of the giver of the mortgage document. Negative Amortization: An increase in the outstanding balance of a mortgage resulting from the failure of periodic debt service payments to cover required interest charges on the loan. Note: A written promise to pay a certain amount of money. Origination Fee: A fee or charge for work involved in the evaluation, preparation and submission of a proposed mortgage loan. Pre-payment penalty: A fee paid to the mortgagee for paying the mortgage before it becomes due. Also known as pre-payment fee or reinvestment fee.

Glossary of Terms

Definitions of Commonly Used Words

Private Mortgage Insurance (PMI): Insurance issued to a lender by a private company to protect the lender against loss on a defaulted mortgage loan. Its use is usually limited to loans with high loan-to-value ratios. The borrower pays the premiums. Promissory Note: A written contract containing a promise to pay a definite amount of money at a definite future time. Radon: A colorless, odorless gas formed by the breakdown of uranium in subsoils. It can enter a house through cracks in the foundation or in water and is considered to be a health hazard. REALTOR® and REALTOR®-Associate: Registered collective membership marks that identify real estate professionals who are members of the National Association of REALTORS® and who subscribe to its strict Code of Ethics. Rent With Option: A contract which gives one the right to lease property at a certain sum with the option to purchase at a future date. Savings and Loan Association (S&Ls): Depository institutions that specialize in originating, servicing, and holding mortgage loans, primarily on owner-occupied residential property. Savings Bank: A financial institution organized to hold individual depositors’ funds in interest-bearing accounts and to make long-term investments, such as home mortgage loans. Second Mortgage/Second Deed of Trust/Junior Mortgage or Junior Lien: An additional loan imposed on a property with a first mortgage. Generally a higher interest rate and shorter term than a “first” mortgage. Severalty Wwnership: Ownership by one person only. Sole ownership. Shared Equity Mortgage: A home loan in which an investor is granted a share of the equity, thereby allowing the investor to participate in the proceeds from resale. Survey: The process by which a parcel of land is measured and its area ascertained. Tenancy in Common: Ownership by two or more persons who hold an undivided interest without right of survivorship. (In the event of the death of one owner, his/her share will pass to his/her heirs.) Title: A document that’s evidence of ownership. Title Defect: An outstanding claim or encumbrance on property that affects marketability. Title Insurance: Protection for lenders and homeowners against financial loss resulting from legal defects in the title. Veterans Administration (VA): A government agency that provides services for eligible veterans of the armed forces. Among other programs, it guarantees mortgage loans made by private lenders to veterans. Variance: A special suspension of zoning laws to allow the use of property in a manner not in accord with existing laws. Zoning Restrictions: Local municipal ordinances that classify property according to specific uses such a single family, residential, commercial, industrial, multi-family, etc.

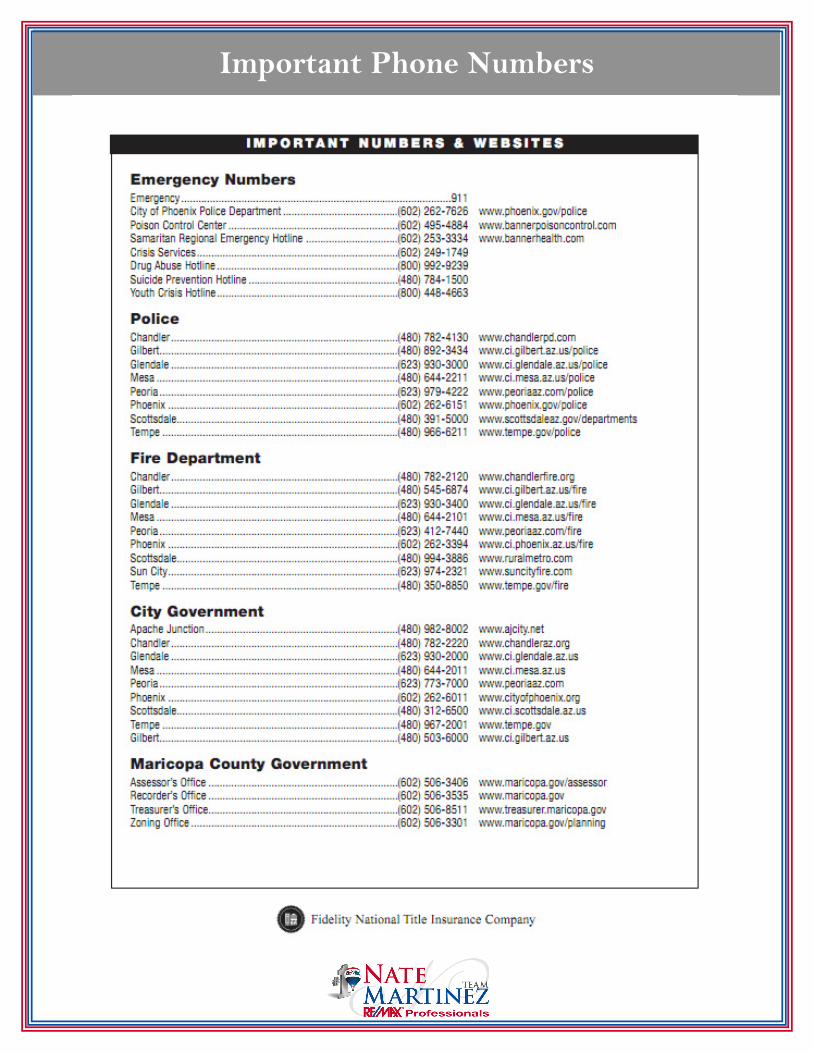

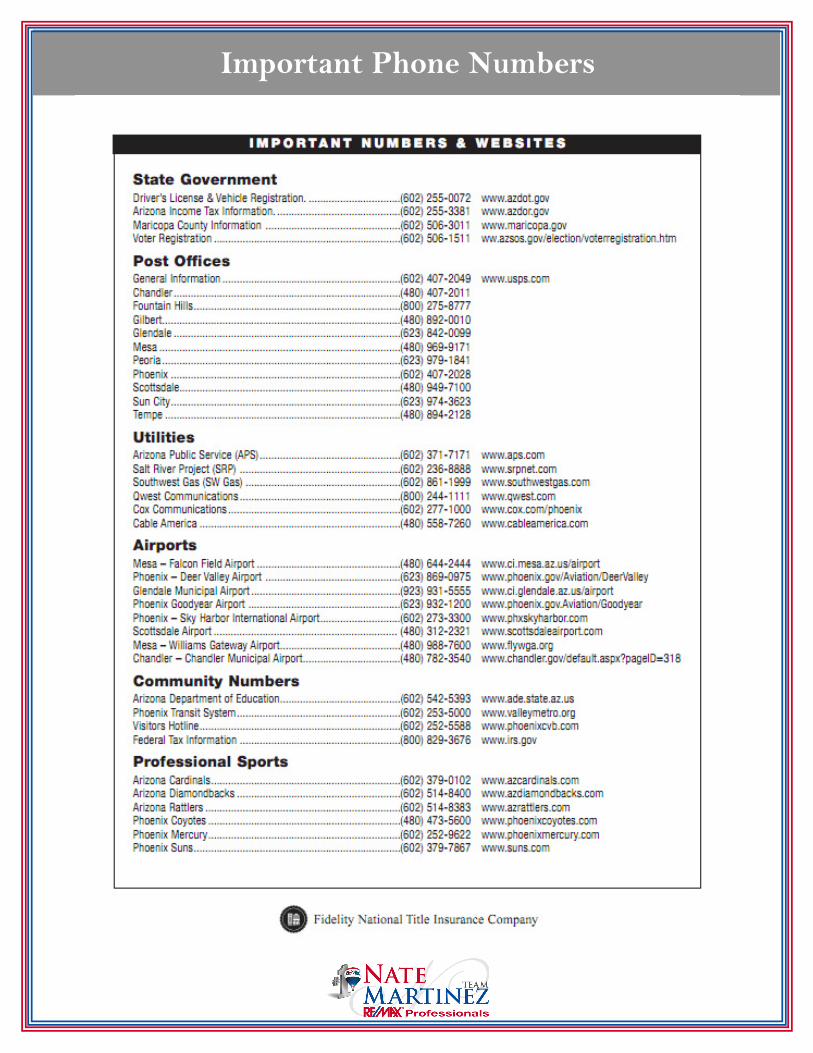

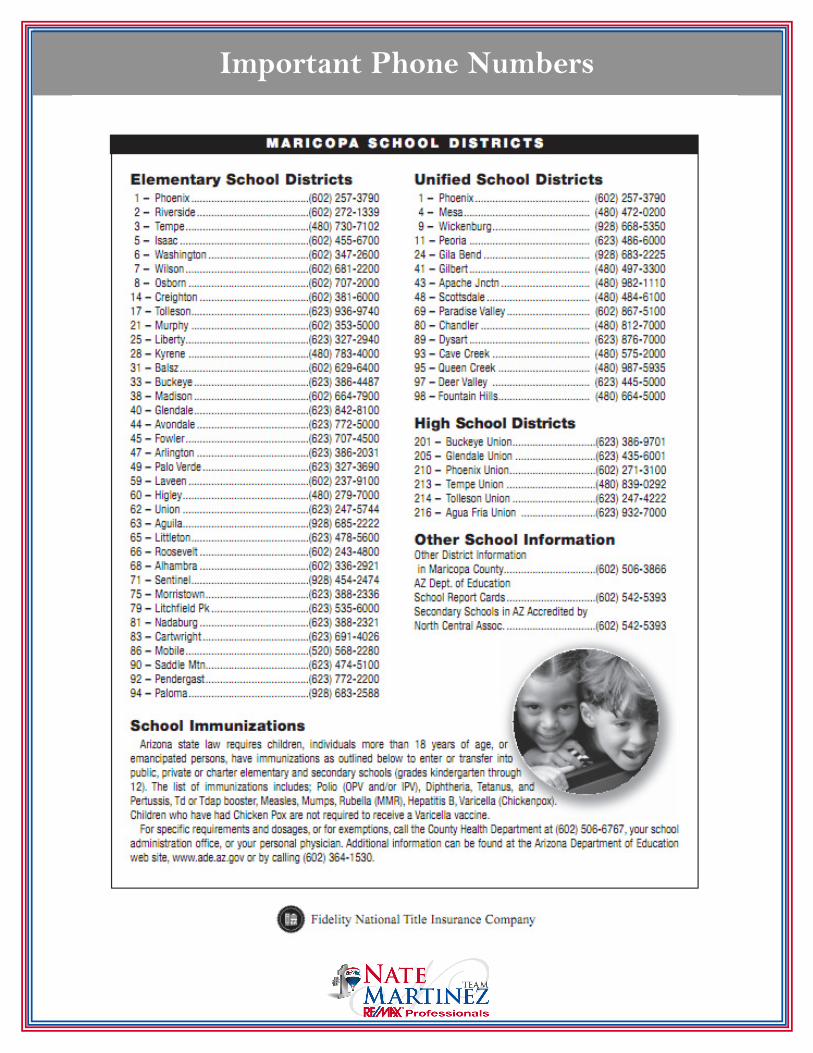

Important Phone Numbers

Important Phone Numbers

Important Phone Numbers