Embed Size (px)

DESCRIPTION

Behavioral Finance 6

Citation preview

Feedback Models

BEHAVIORAL ECONOMICS

Fischer Black on “Noise”

2

FE

ED

BA

CK

MO

DE

LS

Black is a strong believer in noise and noise traders in particular

• They lose money according to him (though they may make money for a short while)

• Prices are “efficient” if they are within a factor of 2 of “correct” value

• Actual prices should have higher volatility than values because of noise

FE

ED

BA

CK

MO

DE

LS

What is a short sale?

3

Example: Sell 100 shares of GOOG at 580• What happens?

• You enter an order to sell 100 shares at 580• Order is “executed” – you sold 100 shares to someone else

somewhere• Mechanically, how do you provide the 100 shares to the buyer?

• You borrow the 100 shares from an institutional holder• You provide collateral equal to the value of the stock ($58,000) and

perhaps a little more collateral in case the stock price goes up• You mark to market

• If stock goes to 585, you send $500 more in cash to lender• If stock goes to 575, lender sends you $500 in cash

• Where do you get the $58,000? • The buyer gives you $58,000 and you pass that through to the

stock lender• On some future date, you buy 100 shares at say 550, paying $ 55,000

which you receive back from the stock lender when you return the 100 shares to the lender

FE

ED

BA

CK

MO

DE

LS

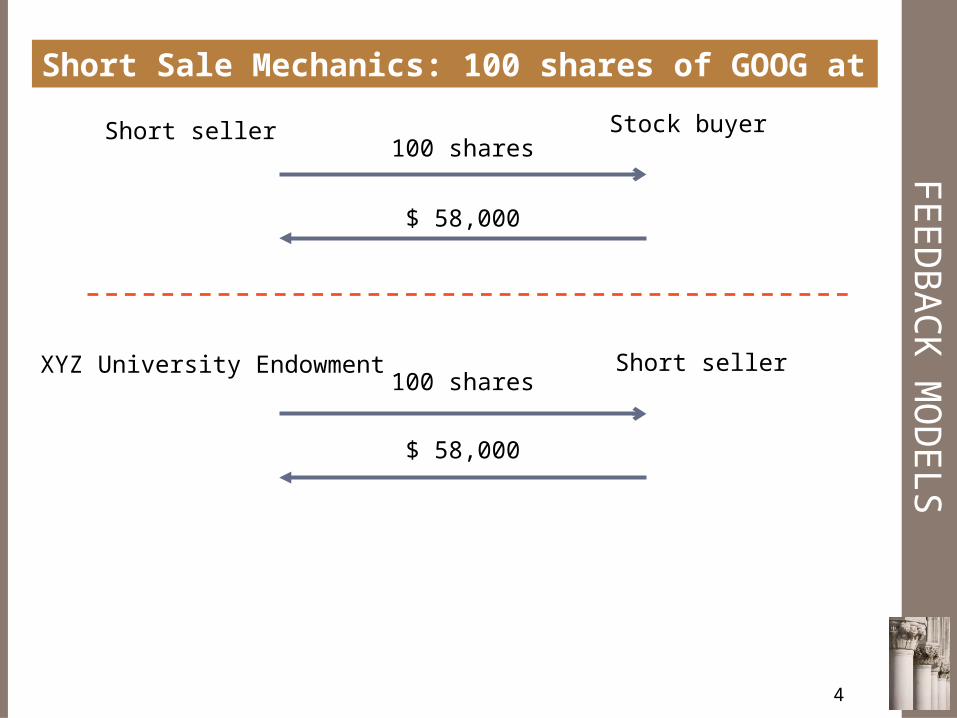

Short Sale Mechanics: 100 shares of GOOG at 580

4

Short seller Stock buyer100 shares

$ 58,000

XYZ University Endowment Short seller100 shares

$ 58,000

FE

ED

BA

CK

MO

DE

LS

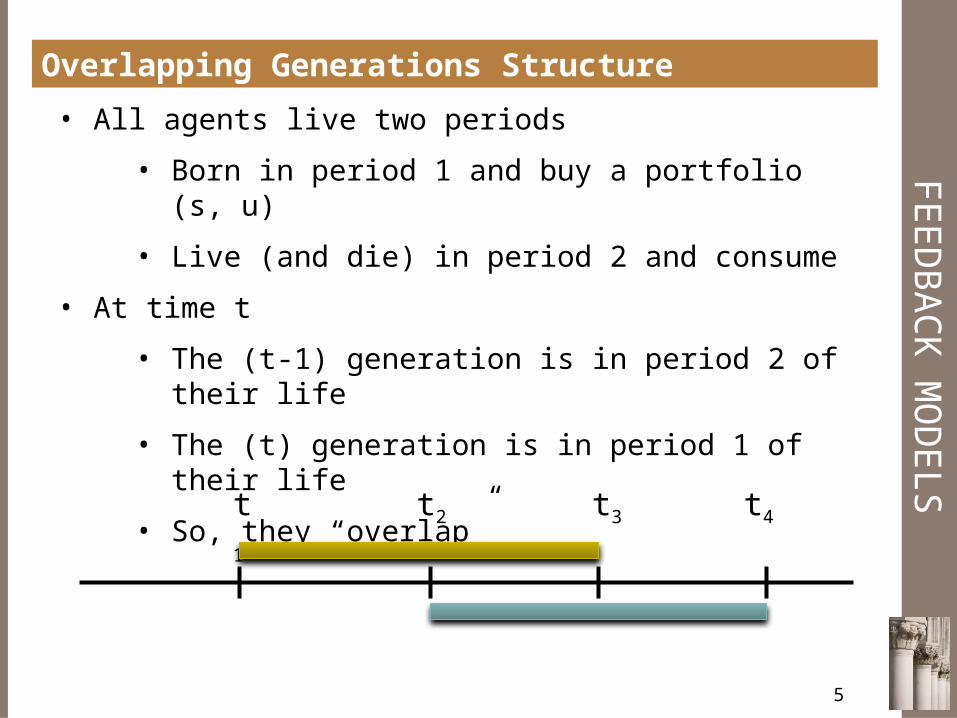

Overlapping Generations Structure

5

• All agents live two periods

• Born in period 1 and buy a portfolio (s, u)

• Live (and die) in period 2 and consume

• At time t

• The (t-1) generation is in period 2 of their life

• The (t) generation is in period 1 of their life

• So, they “overlap”

t1 t2 t3 t4

FE

ED

BA

CK

MO

DE

LS

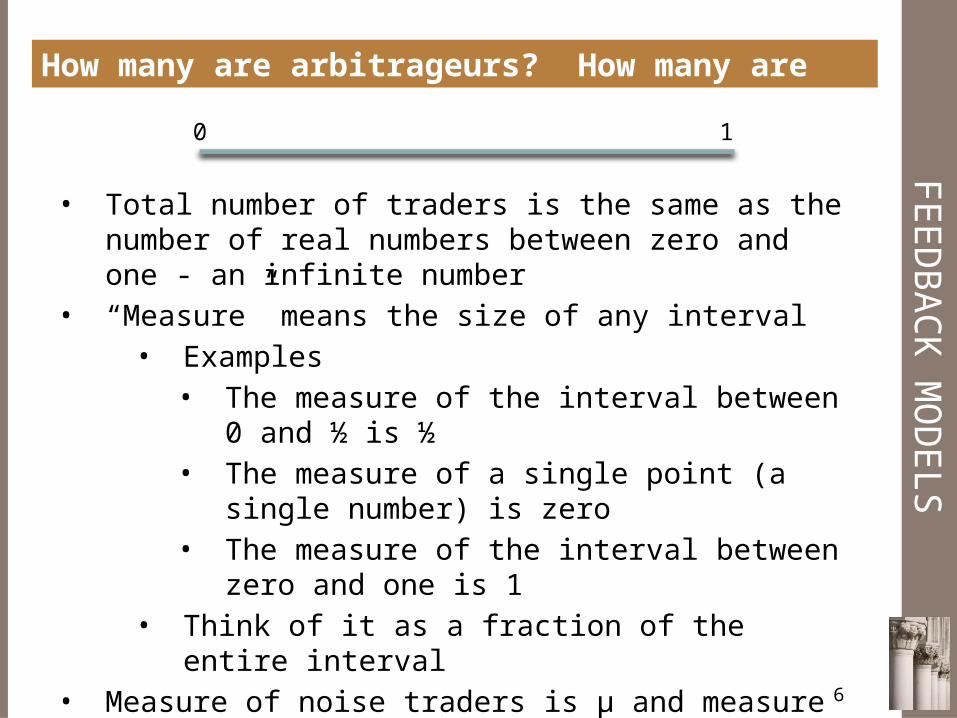

How many are arbitrageurs? How many are noise traders?

6

• Total number of traders is the same as the number of real numbers between zero and one - an infinite number

• “Measure” means the size of any interval• Examples

• The measure of the interval between 0 and ½ is ½

• The measure of a single point (a single number) is zero

• The measure of the interval between zero and one is 1

• Think of it as a fraction of the entire interval• Measure of noise traders is µ and measure of

arbitrage traders is 1 - µ. That is, the fraction of noise traders is µ and everybody else is an arbitrage traders

0 1

FE

ED

BA

CK

MO

DE

LS

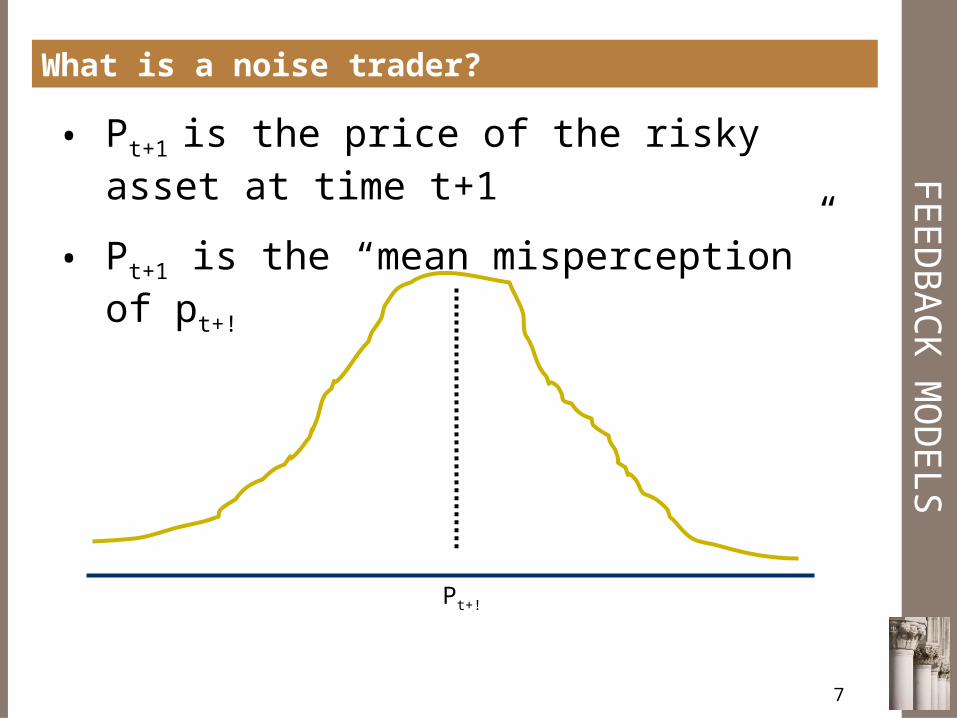

What is a noise trader?

7

• Pt+1 is the price of the risky asset at time t+1

• Ρt+1 is the “mean misperception” of pt+!

Ρt+!

FE

ED

BA

CK

MO

DE

LS

What is an arbitrage trader?

8

• Arbitrage traders “correctly” perceive the true distribution of pt+1

• There is “systematic” error in estimation of future price, pt+1

• But, arbitrageurs face risk unrelated to the “true” distribution of pt+1

• If there were no “noise traders,” then there would be no variance in the price of the risky asset…..but, there are noise traders, hence the risky asset is a risky asset

FE

ED

BA

CK

MO

DE

LS

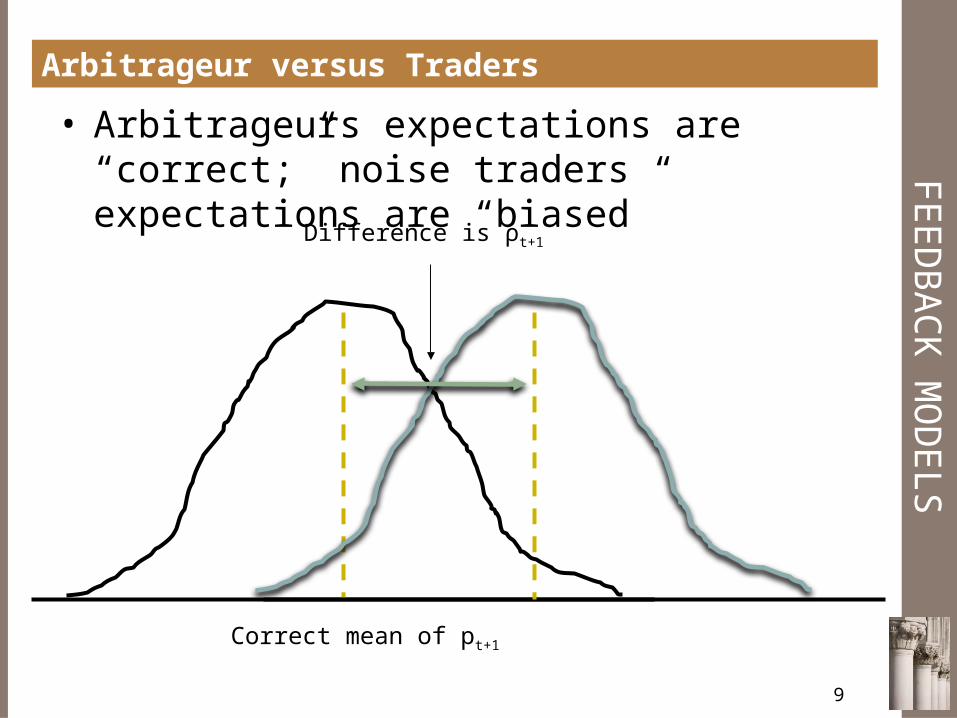

Arbitrageur versus Traders

9

• Arbitrageurs expectations are “correct;” noise traders expectations are “biased”

Correct mean of pt+1

Difference is ρt+1

FE

ED

BA

CK

MO

DE

LS

The Main Issue

10

• What happens in equilibrium

• Undetermined

• Some forces make pt > 1, some forces push pt < 1, result is indeterminant

• Who makes more profit, arbitrageurs or noise traders?

• Depends

• But, it is perfectly possible for arbitrageurs to make more!

• Survival?

FE

ED

BA

CK

MO

DE

LS

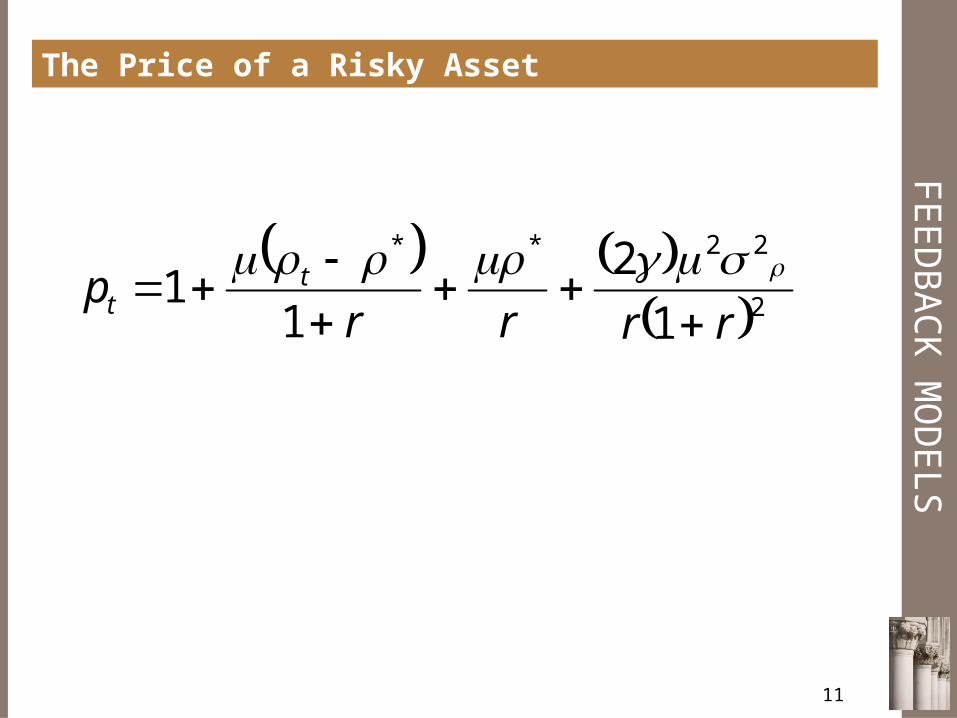

The Price of a Risky Asset

11

2

22**

1

2

11

rrrrp tt

FE

ED

BA

CK

MO

DE

LS

When Do Noise Traders Profit More Than Arbitrageurs?

12

• Noise traders can earn more than arbitrageurs when ρ* is positive

• Meaning when noise traders are systematically too optimistic

• Why?• Because they have relatively more of the

risky asset than the arbitrageurs• But, if ρ* is too large, noise traders will

not earn more than arbitrageurs• The more risk averse everyone is (higher

λ in the utility function), the wider the range of values of ρ for which noise traders do better than arbitrageurs

FE

ED

BA

CK

MO

DE

LS

What Does Shleifer Accomplish?

13

• Given two assets that are “fundamentally” identical, he shows a logic where the market fails to price them identically

• Assumes “systematic” noise trader activity

• Shows conditions that lead to noise traders actually profiting from their noise trading

• Shows why arbitrageurs could have trouble (even when there is no fundamental risk)

FEEDBACK MODELS

FE

ED

BA

CK

MO

DE

LS

Feedback Models

15

• Central idea is that a price higher than efficient price might have “real” effects. What are they?

• Hirshleifer et al. is one example of several attempts to show feedback effects

HIRSHLEIFER ET AL.

FE

ED

BA

CK

MO

DE

LS

Hirshleifer et al. on Feedback

17

• Three dates

• Eight kinds of investors

• Early and late

• Informed and uninformed

• Rational and irrational

• Mainly rational and irrational (noise) traders

• One firm with equity shares

• Trades at period 1 and period 2

• Payoff in period 3

FE

ED

BA

CK

MO

DE

LS

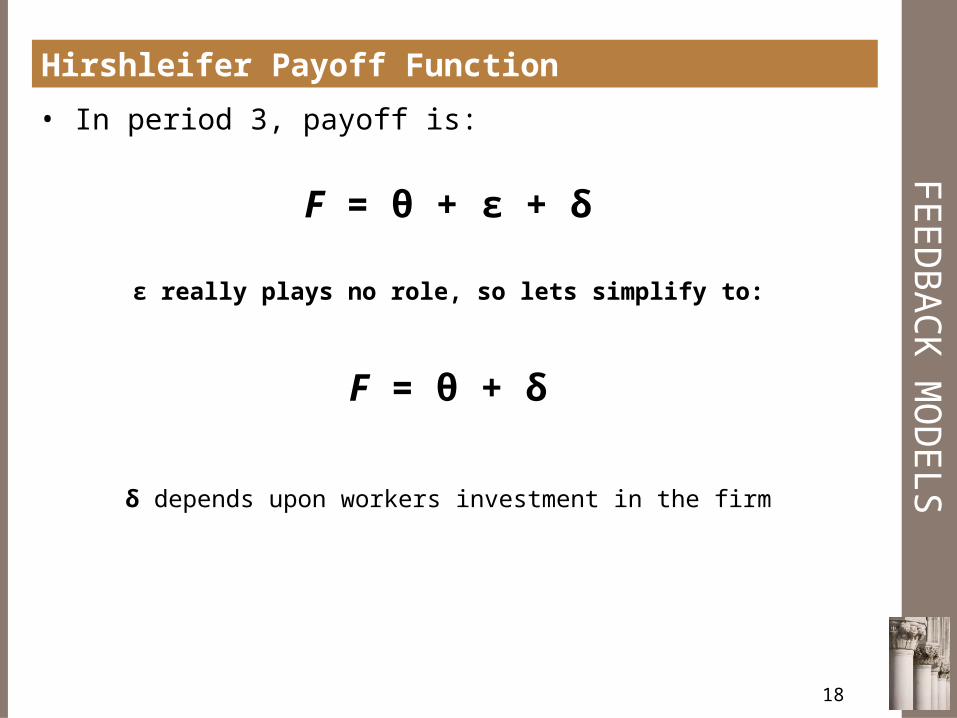

Hirshleifer Payoff Function

18

• In period 3, payoff is:

F = θ + ε + δ

ε really plays no role, so lets simplify to:

F = θ + δ

δ depends upon workers investment in the firm

FE

ED

BA

CK

MO

DE

LS

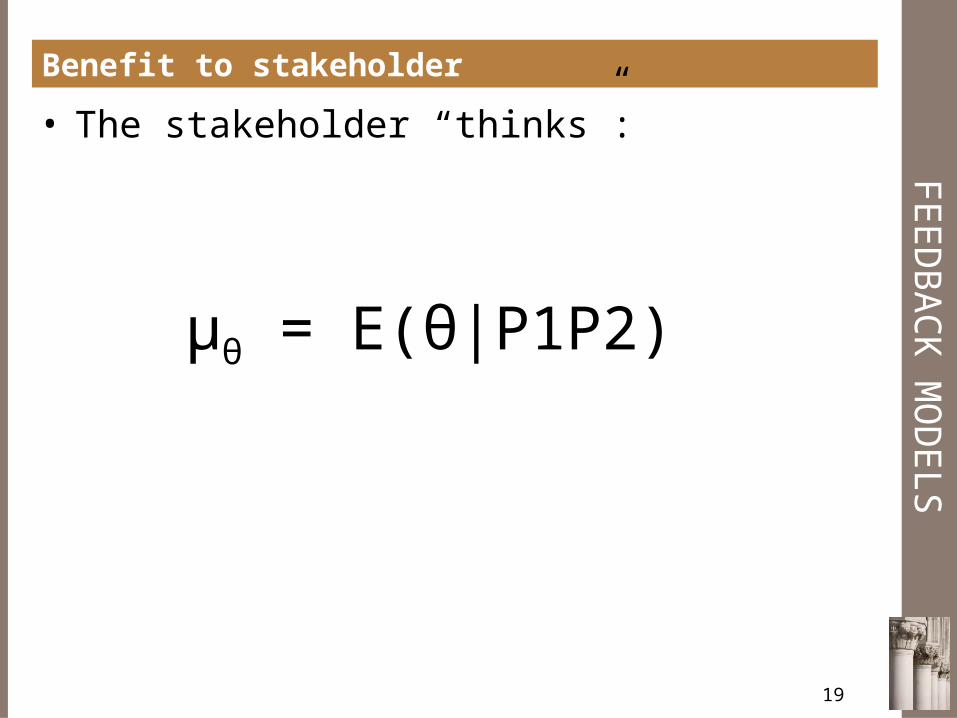

Benefit to stakeholder

19

• The stakeholder “thinks”:

μθ = E(θ|P1P2)

FE

ED

BA

CK

MO

DE

LS

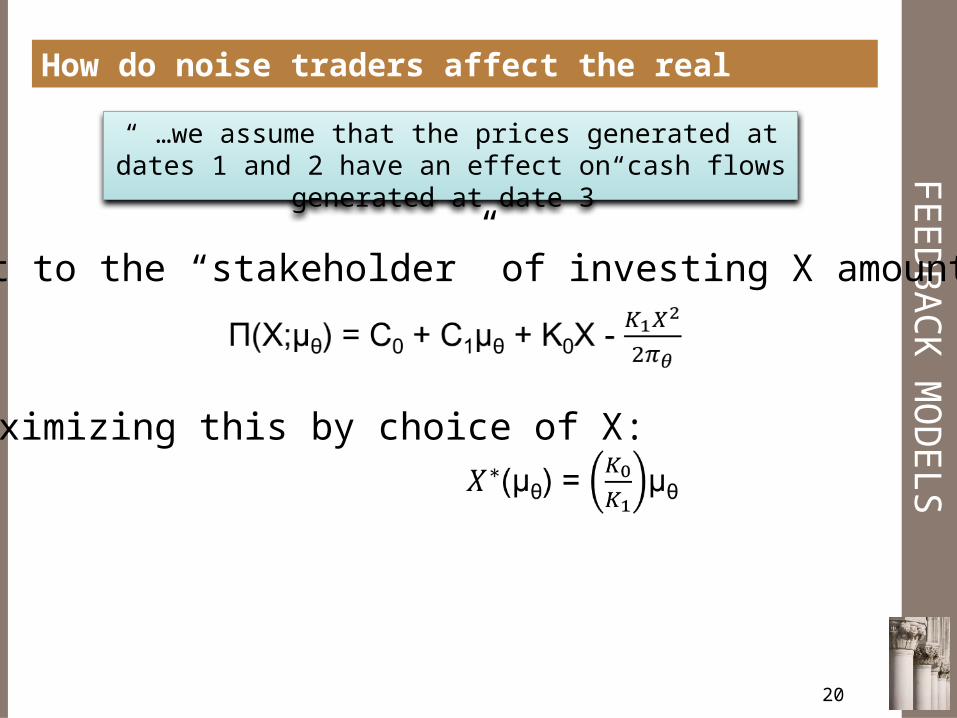

How do noise traders affect the real economy?

20

“ …we assume that the prices generated at dates 1 and 2 have an effect on cash flows generated at

date 3”

Profit to the “stakeholder” of investing X amount:

Maximizing this by choice of X:

FE

ED

BA

CK

MO

DE

LS

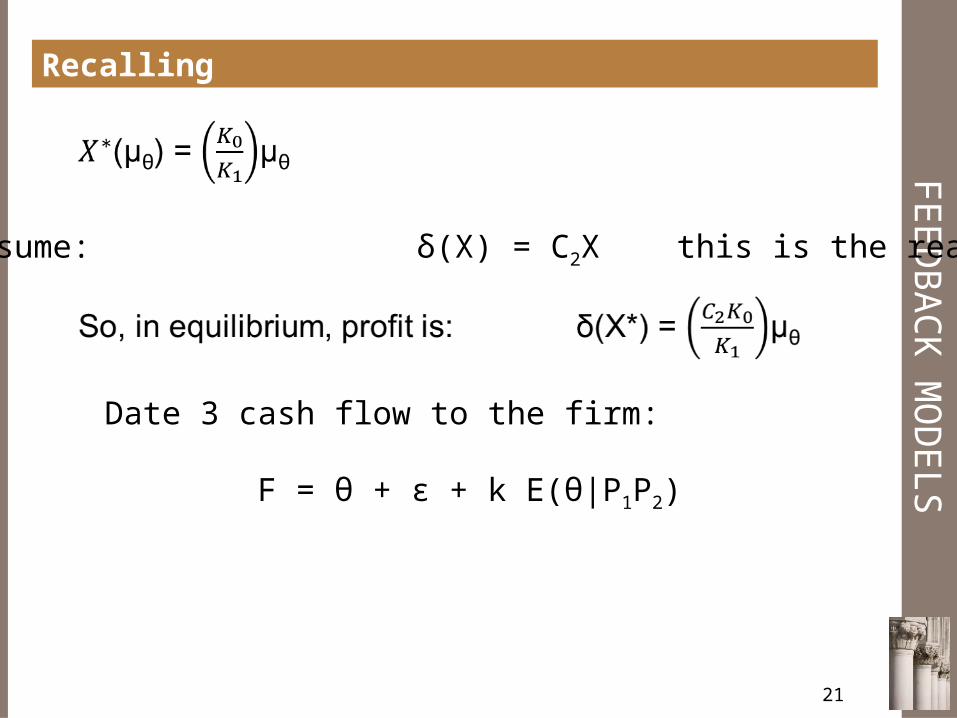

Recalling

21

Now assume: δ(X) = C2X this is the reality

Date 3 cash flow to the firm:

F = θ + ε + k E(θ|P1P2)

FE

ED

BA

CK

MO

DE

LS

Irrational Traders?

22

• They believe, irrationally, that the security pays off:

η + ε• Early informed irrational traders observe

the value of η at date 1• Late informed irrational traders observe

the value of η at date 2

FE

ED

BA

CK

MO

DE

LS

So what happens in Hirshleifer Etal

23

• Early irrational, but informed, traders benefit because later irrational traders buy and the early traders “know it”

• Sometimes, early informed traders benefit as well

• Late irrational traders get smashed

SUBRAHMANYAM & TITMAN (2001)

FE

ED

BA

CK

MO

DE

LS

Subrahmanyam & Titman (2001)

25

• Feedback into “Cascades”

• What is a cascade?

• Bandwagon effect

• Like a social network

• Could be an “operating system”

• The idea is that you benefit if others adopt

FE

ED

BA

CK

MO

DE

LS

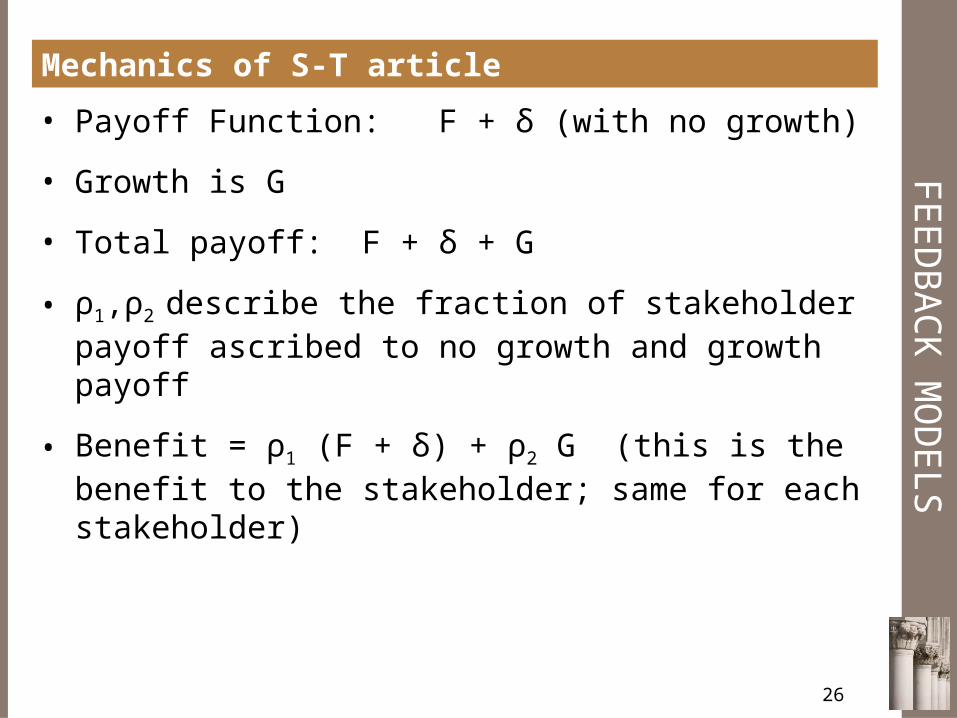

Mechanics of S-T article

26

• Payoff Function: F + δ (with no growth)

• Growth is G

• Total payoff: F + δ + G

• ρ1,ρ2 describe the fraction of stakeholder payoff ascribed to no growth and growth payoff

• Benefit = ρ1 (F + δ) + ρ2 G (this is the benefit to the stakeholder; same for each stakeholder)

FE

ED

BA

CK

MO

DE

LS

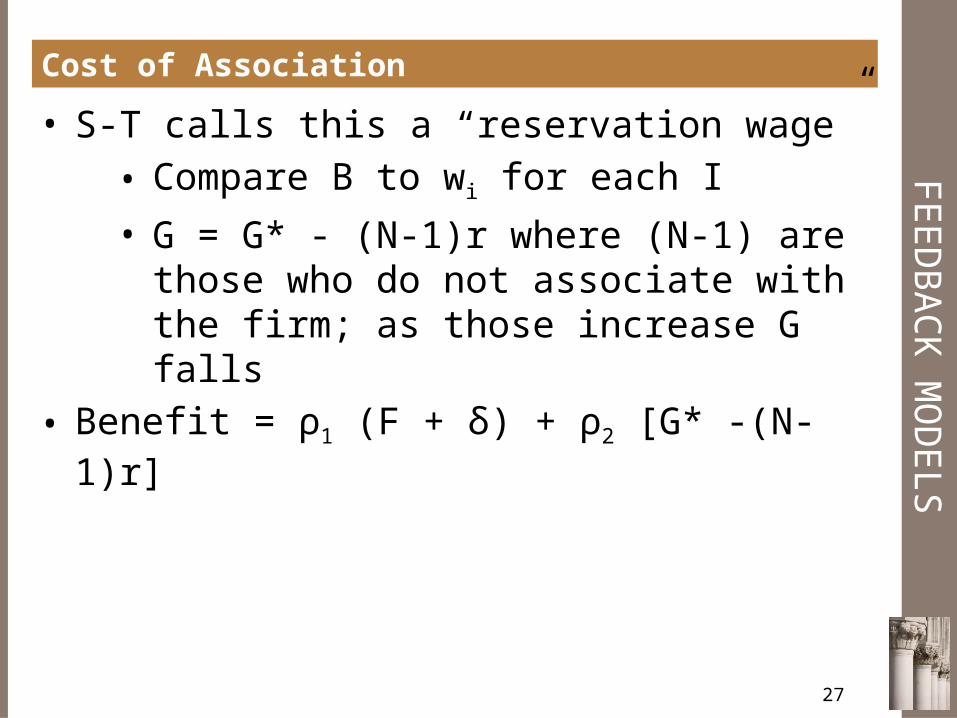

Cost of Association

27

• S-T calls this a “reservation wage”• Compare B to wi for each I

• G = G* - (N-1)r where (N-1) are those who do not associate with the firm; as those increase G falls

• Benefit = ρ1 (F + δ) + ρ2 [G* -(N-1)r]

![University of HawaiiTranslate this page of Hawaii System ... ÐÏ à¡± á> þÿ rŽ8 8 ‹8 8 8 8 8 8 8 8 8 8 8!8"8#8$8%8&8'8(8)8*8+8,8-8.8/808182838485868788898:8;88=8>8?8@8A8B8C8D8E8F8G8H8I8J8K8L8M8N8O8P8Q8R8S8T8U8V8W8X8Y8Z8[8\8]8^8_8](https://img.pdfslide.us/doc/110x75/5aabfa6d7f8b9a9c2e8c9b24/university-of-hawaiitranslate-this-of-hawaii-system-rz8-8-8-8-8-8-8-8-8.jpg)

![apdu.orgTranslate this pageapdu.org/wp-content/uploads/2011/12/2011-01-27_Research...ÐÏ à¡± á> þÿ r‘8 þÿÿÿ 8 8 8!8"8#8$8%8&8'8(8)8*8+8,8-8.8/808182838485868788898:8;88?8@8A8B8C8D8E8F8G8H8I8J8K8L8M8N8O8P8Q8R8S8T8U8V8W8X8Y8Z8[8\8]8^8_8`8a8b8c8d8e8f8g8h8i8j8k8l8m8n8o8p8q8r8s8t8u8v8w8x8y8z8{8|8](https://img.pdfslide.us/doc/110x75/5ae7f3457f8b9a87049010f1/apduorgtranslate-this-r8-8-8-8888888888888-888081828384858687888988888888a8b8c8d8e8f8g8h8i8j8k8l8m8n8o8p8q8r8s8t8u8v8w8x8y8z8888888a8b8c8d8e8f8g8h8i8j8k8l8m8n8o8p8q8r8s8t8u8v8w8x8y8z888.jpg)

![[XLS] · Web view8 6212.5 8 19478.2 8 8015 8 8597.35 8 4585 8 15861.9 8 4797.5 8 8597.35 8 15235 8 5153 8 8257.5 8 5592.2 8 19565.7 8 15861.9 8 7575 8 19947.5 8 10215 8 2970 8 15861.9](https://img.pdfslide.us/doc/110x75/5bc48cb809d3f274118c1b96/xls-web-view8-62125-8-194782-8-8015-8-859735-8-4585-8-158619-8-47975.jpg)